Industry Effects of Monetary Policy in Spain

11

This article was downloaded by: [USM University of Southern Mississippi] On: 12 September 2014, At: 17:48 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK Regional Studies Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/cres20 Industry Effects of Monetary Policy in Spain Carlos J. Rodríguez-Fuentes a & David Padrón-Marrero a a Department of Applied Economics , University of La Laguna , Campus de Guajara, S/C de Tenerife, E-38071 , Spain E-mail: Published online: 08 Apr 2008. To cite this article: Carlos J. Rodríguez-Fuentes & David Padrón-Marrero (2008) Industry Effects of Monetary Policy in Spain, Regional Studies, 42:3, 375-384, DOI: 10.1080/00343400701291583 To link to this article: http://dx.doi.org/10.1080/00343400701291583 PLEASE SCROLL DOWN FOR ARTICLE Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) contained in the publications on our platform. However, Taylor & Francis, our agents, and our licensors make no representations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of the Content. Any opinions and views expressed in this publication are the opinions and views of the authors, and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon and should be independently verified with primary sources of information. Taylor and Francis shall not be liable for any losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoever or howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use of the Content. This article may be used for research, teaching, and private study purposes. Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http:// www.tandfonline.com/page/terms-and-conditions

Transcript of Industry Effects of Monetary Policy in Spain

This article was downloaded by: [USM University of Southern Mississippi]On: 12 September 2014, At: 17:48Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: MortimerHouse, 37-41 Mortimer Street, London W1T 3JH, UK

Regional StudiesPublication details, including instructions for authors and subscription information:http://www.tandfonline.com/loi/cres20

Industry Effects of Monetary Policy in SpainCarlos J. Rodríguez-Fuentes a & David Padrón-Marrero aa Department of Applied Economics , University of La Laguna , Campus de Guajara, S/Cde Tenerife, E-38071 , Spain E-mail:Published online: 08 Apr 2008.

To cite this article: Carlos J. Rodríguez-Fuentes & David Padrón-Marrero (2008) Industry Effects of Monetary Policy inSpain, Regional Studies, 42:3, 375-384, DOI: 10.1080/00343400701291583

To link to this article: http://dx.doi.org/10.1080/00343400701291583

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) containedin the publications on our platform. However, Taylor & Francis, our agents, and our licensors make norepresentations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose ofthe Content. Any opinions and views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be reliedupon and should be independently verified with primary sources of information. Taylor and Francis shallnot be liable for any losses, actions, claims, proceedings, demands, costs, expenses, damages, and otherliabilities whatsoever or howsoever caused arising directly or indirectly in connection with, in relation to orarising out of the use of the Content.

This article may be used for research, teaching, and private study purposes. Any substantial or systematicreproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Industry Effects of Monetary Policy in Spain

CARLOS J. RODRIGUEZ-FUENTES and DAVID PADRON-MARRERODepartment of Applied Economics, University of La Laguna, Campus de Guajara, S/C de Tenerife E-38071, Spain.

Emails: [email protected] and [email protected]

(Received May 2006: in revised form December 2006)

RODRIGUEZ-FUENTES C. J. and PADRON-MARRERO D. Industry effects of monetary policy in Spain, Regional Studies. The aim

of this paper is to analyse the presence of sectoral asymmetries in monetary policy transmission in Spain in the period before the

introduction of the single monetary policy in Europe (1988–98). Monetary policy shocks are identified through both a standard

vector auto-regression model (VAR-shock) and the specification of a reaction function (RF-shock) for the monetary authority in

Spain. The responses of the different industrial branches with regard to the estimated monetary shocks are then analysed at national

accounting sector and subsector levels. The results confirm the presence of significant differences in the sectoral responses with

respect to national monetary shocks in Spain. In addition, the sectoral asymmetries found in the present study show a strong cor-

relation with regard to the regional asymmetries found in a previous study.

Monetary policy Industry effects Monetary shocks Spain

RODRIGUEZ-FUENTES C. J. et PADRON-MARRERO D. Les effects de la politique monetaire sur le secteur industriel en Espagne,

Regional Studies. Cet article cherche a analyser la presence des asymetries sectorielles dans la transmission de la politique monetaire en

Espagne pendant la periode qui a precede l’etablissement du systeme monetaire europeen (de 1988 a 1998). On identifie les chocs de

la politique monetaire a la fois par moyen d’un modele d’auto-regressionvectorielle type (choc-VAR) et de la specification d’une fonction

de reaction (RF-choc) pour les instances monetaires espagnoles. Dans le cadre des comptes de la nation et sur le plan sectoriel, il s’ensuit

une analyse des reponses des divers secteurs industriels quant aux chocs monetaires approximatifs. Les resultats confirment d’importantes

differences des reponses sectorielles quant aux chocs monetaires nationaux en Espagne. En outre, les asymetries sectorielles qui se

presentent, sont en correlation etroites avec les asymetries regionales qui se presentaient dans une etude anterieure.

Politique monetaire Effets industriels Chocs monetaires Espagne

RODRIGUEZ-FUENTES C. J. und PADRON-MARRERO D. Branchenspezifische Auswirkungen der Wahrungspolitik in Spanien,

Regional Studies. In diesem Beitrag wird die Prasenz sektoraler Asymmetrien in der Ubertragung der Wahrungspolitik in Spanien

im Zeitraum vor der Einfuhrung der einheitlichen Wahrungs-politik in Europa (1988–98) untersucht. Die Schocks in der Wah-

rungspolitik werden mit Hilfe eines Standardvektor-Autoregressionsmodells (VAR-Schock) sowie durch Spezifizierung einer

Reaktionsfunktion (RF-Schock) fur die spanische Wahrungsbehorde identifiziert. Anschließend werden die Reaktionen der

verschiedenen Industriebranchen hinsichtlich der geschatzten Wahrungsschocks auf den Ebenen des nationalen Buchhaltungssek-

tors und der Untersektoren analysiert. Unsere Ergebnisse bestatigen die Prasenz signifikanter Unterschiede hinsichtlich der sek-

toralen Reaktionen im Zusammenhang mit den nationalen Wahrungsschocks in Spanien. Daruber hinaus wiesen die in unserer

Studie festgestellten sektoralen Asymmetrien eine starke Korrelation mit den in einer fruheren Studie festgestellten regionalen

Asymmetrien auf.

Wahrungspolitik Branchenspezifische Auswirkungen Wahrungsschocks Spanien

RODRIGUEZ-FUENTES C. J. y PADRON-MARRERO D. Los efectos de la polıtica monetaria sobre la industria en Espana, Regional

Studies. El objetivo de este artıculo es analizar la presencia de las asimetrıas sectoriales en la transmision de la polıtica monetaria en

Espana durante el periodo antes de la introduccion en Europa de la polıtica monetaria unica (1988–98). Identificamos los choques

de la polıtica monetaria a traves de un modelo estandar vector de autorregresion (choque VAR) y la especificacion de una funcion

Regional Studies, Vol. 42.3, pp. 375–384, April 2008

0034-3404 print/1360-0591 online/08/030375-10 # 2008 Regional Studies Association DOI: 10.1080/00343400701291583http://www.regional-studies-assoc.ac.uk

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14

de reaccion (choque RF) para la autoridad monetaria en Espana. Analizamos luego las respuestas de las diferentes ramas industriales

con respecto a los choques monetarios estimados en el sector de contabilidad nacional y los niveles de subsectores. Nuestros resul-

tados confirman la presencia de diferencias significativas en las respuestas sectoriales con respecto a los choques monetarios nacio-

nales en Espana. Asimismo las asimetrıas sectoriales de nuestro estudio muestran una fuerte correlacion con las asimetrıas regionales

de un estudio previo.

Polıtica monetaria Efectos en la industria Choques monetarios Espana

JEL classifications: E52, L60

INTRODUCTION

The study of the transmission mechanism of monetarypolicy has traditionally focused on the aggregate levelof the economy, specifically on the impact of monetarypolicy decisions on production and price levels. Never-theless, the last decade has seen an increasing amount ofresearch that concentrates on the study of asymmetrieswhich can arise in the transmission of national monetaryshocks, either in specific regions which make up thenational economy (regional asymmetries), or amongtheir respective productive sectors (sectoral asymme-tries). Undoubtedly, a significant portion of thisliterature is motivated by the loss of monetary sover-eignty which some European Union (EU) countrieshave experienced as a result of their conversion intoregions within the euro zone. These countries have allirreversibly lost their prior ‘national monetary identi-ties’ and as such have begun to be concerned aboutthe regional repercussions of the European CentralBank’s monetary policy (RODRIGUEZ FUENTES,2005, pp. 5–7).

The growing interest in the study of sectoral asym-metries in the transmission of monetary policy hasalso been stimulated by the forecast that the establish-ment of a single currency in the EU would convert sec-toral shocks in truly regional shocks (KRUGMAN andVENABLES, 1996), which in turn would lead to regionaltensions in the process of European integration.1 Thisforecast has also been reinforced by some empirical evi-dence in studies that emphasize the importance of thedifferences in the regional productive structure in theexplanation of the different regional responses withregard to national monetary policy shocks (e.g.CARLINO and DEFINA, 1996, 1998a, b, 1999; GUISO

et al., 1999; ARNOLD, 2001).The present paper analyses sectoral asymmetries in

the transmission of national monetary shocks in Spainand also explores the possible relationships among esti-mated sector shocks with the estimated regional shocksfrom an earlier paper (RODRIGUEZ FUENTES et al.,2004).

The paper is divided into an introduction, four mainsections, and conclusions. The body of the paper beginswith a brief review of the empirical literature concern-ing sectoral asymmetries in monetary policy trans-mission. The responses of the different branches thatmake up the industrial sector in Spain are then studied

in the next two sections. The third section introducesthe estimates of monetary policy shocks in Spain forthe period 1988–98. It is well known that the estimationof monetary shocks is a critical step in any study thatattempts to analyse the effects of monetary policy, andthat the observed correlations between interest rates,output and prices can be due to an inverse causationprocess. Consequently, the exogenous component(monetary shocks) must be isolated from its endogenousresponse. A vector autoregressive (VAR) model is usedto identify these shocks. Most of the empirical literatureemploys the VAR model when studying the monetarytransmission mechanism. However, the present studydoes not end with just the VAR model. In addition, areaction function for the Bank of Spain is estimated inorder to compare the robustness of the results obtainedfrom the VAR model. This new approach can be used,in the authors’ opinion, as a complement to thetraditional VAR literature. The fourth section studiesthe response of industrial production (by sector andsubsector) with regard to the estimated monetarypolicy shocks from the previous section.2 The resultsconfirm the presence of important differences in the sec-toral responses with respect to national monetary shocksin Spain and are consistent with the available empiricalevidence of other countries. In addition, the sectoralasymmetries presented in this section show somesimilarities with the regional asymmetries found inprevious work (RODRIGUEZ FUENTES et al., 2004)since the classification of the Spanish regions accordingto their implicit sectoral sensitiveness reflect a strongcorrelation with the ordering which is obtained byusing their sensitivity when taking into account nationalmonetary shocks (regional asymmetries).

SECTORAL ASYMMETRIES IN

THE TRANSMISSION OF MONETARY

POLICY: AN OVERVIEWOF THE

EMPIRICAL LITERATURE

A review of the literature on the sectoral effects of mon-etary policy based on empirical evidence leads to threeimportant conclusions. Firstly, the choice of the VARmodel as the econometric technique to identify monet-ary shocks. Secondly, that the strategy followed to valuethe measure of heterogeneity in the sectoral responseconsists in estimating a VAR model for each of the

376 Carlos J. Rodrıguez-Fuentes and David Padron-Marrero

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14

sectors studied. This strategy leads to an estimation of asmany reaction functions as sectors that are considered inthe study and, consequently, obtaining a series of differ-ent monetary shocks3 for each of the studied sectors(which hinders the validity of intersectoral compari-sons). The third conclusion is that most studies tendto incorporate among the endogenous variables bothnational and sectoral variables (production and pricelevels). In this case it is more common that nationalaggregates are placed ahead of the monetary policy vari-able, while sectoral variables appear after that variable(GANLEY and SALMON, 1997; DEDOLA and LIPPI,2000, 2005). This consideration and the use of recursiveidentification methods (the Cholesky decompositionmethod) lead to the inclusion of the implicit assumptionthat monetary shocks do not have a contemporaneousimpact on national aggregates but do have an instan-taneous effect on sectoral variables, which could beinterpreted as an inconsistency in the model.4

This analysis is found in the work of GANLEY andSALMON (1997), which studies the responses of differentproduction sectors with respect to monetary policyshocks in the UK. This study estimates 24 VARmodels (one for each of the sectors under study) thatincorporate, as endogenous variables, short-term interestrate, the real gross national product (GNP) of the UK andits implicit deflactor, and, lastly, the production index ofeach sector. The Cholesky decomposition method isused with the variables ordered according to their pre-viously mentioned description. Results from the studyindicate that monetary policy measures implementedby the Bank of England have had varying impacts accord-ing to sectors. Examples can be found in the constructionsector and, to a lesser extent, in manufacturing, whereboth sectors are subject to stronger and more rapidresponses to national monetary shocks. In addition, theauthors confirm large variability in the response toeach of the branches that make up the manufacturingsector. For instance, there are cases where some branchesoffer a very weak response (industries linked to non-durables consumer expenditures, as producers of food,drink and tobacco, textiles and footwear), while otherindustries (industries supplying construction, as glass,tiles, concrete and bricks, and wood products; or indus-tries linked to durables consumer expenditures, as vehiclemanufacture) react in a very clear manner.

Results obtained by HAYO and UHLENBROCK

(1999/2000) also suggest the presence of important sec-toral differences in their responses to national monetaryshocks in West Germany. Their findings show thatapproximately half of the analysed branches show adifferent response than the average one for the sector.

DEDOLA and LIPPI (2000, 2005) focus on theresponses of industrial production in five countriesbelonging to the Organization for Economic Co-operation and Development (OECD). They studiedthe production sector response of 21 industrialbranches in Germany, France, the USA, Italy, and the

UK by using a common specification in the estimatedVAR models. The results from these papers indicatethat the differences among sectoral responses withrespect to monetary shocks are much greater thanthose found in other countries. The authors also inves-tigated if the observed sector heterogeneity in theresponse to national monetary shocks was due toindustry-specific factors or country-specific factors.They concluded that sectoral responses were similaramong all the different countries studied. Theirresults also show that the impact of monetary shocksis greater in production industries including durablegoods, which place greater demands on workingcapital and smaller borrowing capacity (DEDOLA andLIPPI, 2005, p. 1565).

As noted above, most of the empirical studies thatanalyse sectoral effects of monetary policy tend toemploy a VAR model to estimate each sector’s response.This decision also assumes that national variables are notinstantaneously affected by monetary shocks whereas thesectoral variables are affected, which could be interpretedas an inconsistency in the model. Various alternativeshave been proposed to address this inconsistency. Oneis seen in the work of RADDATZ and RIGOBON

(2003), which suggests estimating a single nationalVAR model where national production is substitutedby the production levels in each sector under consider-ation. These authors also introduce a non-recursiveidentification method that allows them to sort theobstacle, namely that monetary shocks do not have acontemporaneous effect on national variables but dohave an instantaneous effect on sectoral variables. Evenso, the results obtained by Raddatz and Rigobon alsosuggest the presence of important sectoral asymmetriesin the responses from different industrial branches inthe US economy with respect to national monetarypolicy, where durable goods and property investmentare the two sectors that show the strongest response.Nevertheless, the approach of Raddatz and Rigobon isnot free of problems. For instance, the complete identi-fication of all structural parameters of the model requiresseveral assumptions. In addition, the large number ofestimated parameters creates an important reduction inthe degrees of freedom, which is a sensitive issue whenworking with short time series.

PEERSMAN and SMETS (2002) propose a two-stepstrategy to value sectoral asymmetries in monetarypolicy transmission in the euro zone. The first stage iscarried out by extracting monetary shocks from the esti-mates derived from a VAR model for the nationaleconomy. The estimated national monetary shocksfrom the first stage are then used in the second stageto explain the behaviour of the sectoral productionbased upon its past behaviour and estimated nationalmonetary shocks from the prior stage. These estimatednational monetary shocks will be equal for each of thestudied sectors since they have been extracted fromthe national VAR model.

Industry Effects of Monetary Policy in Spain 377

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14

The present paper begins by incorporating the strat-egy used by Peersman and Smets, but it will also estimatenational monetary shocks by using the specification of areaction function for the Bank of Spain.

IDENTIFICATION OF MONETARY SHOCKS:

VECTOR AUTOREGRESSIVE (VAR)

MODELS AND REACTION FUNCTIONS

Following the current orthodox empirical literature onmonetary policy (CHRISTIANO et al., 1999), the presentauthors have identified the exogenous monetary shocksby means of a VAR model and a reaction function of thecentral bank.5 This second approach is, in the authors’opinion, a novel contribution in the context of theempirical literature regarding sectoral asymmetries inthe transmission of monetary policy. Details of the spe-cification of the VAR model as well as the reactionfunction follow.

Vector autoregressive (VAR) model

The general equation of the VAR model that has beenchosen to identify the monetary policy shocks Spain isof the form:

Xt

Yt

� �¼

A(L) B(L)

C(L) D(L)

� �Xt�1

Yt�1

� �þ

a b

c d

� �

�eXteYt

� �(1)

where Yt is the vector containing the endogenous vari-ables of the system, all of which refer to the set repre-senting the national economy. This set is made up ofthese variables in the following order: national industrialproduction index (IPI); the consumer price index(CPI); the German inter-bank interest rate (iAL); theM3 monetary aggregate; the interest rate for three-month non-transferable deposits (iESP); and the realeffective exchange rate for the peseta (REER):6

Yt ¼ ½ IPIt CPIt iAL M3 iESP REER �0 (2)

An exogenous variable vector has also been introducedthat includes a constant (const), a tendency (trend), anda world commodity price index (WCPI) to controlpossible external shocks:

Xt ¼ ½ const trend WCPIt �0 (3)

The VAR model has been estimated in levels, whichallows one to control the possible existence of co-integration. Almost all variables are expressed in logar-ithmic form, the exception being interest rates. Datahave been taken from the Monthly Statistical Bulletin ofthe Bank of Spain; and the sample covers the period

from January 1988 to December 1998.7 The lag struc-ture used in the model is two months; and the monetarypolicy shock that has been identified is a result of theCholesky decomposition method, with the variablesdefined and ordered according to the above comments.8

Fig. 1 depicts the impulse–response function ofthe most important variables, namely production andprices. It indicates that prices remain unaltered afteran unexpected monetary policy shock, which couldbe justified by the high levels of price (and nominalwages) rigidity that have been traditionally seen in theSpanish economy. The case of production, however, isconsistent with other studies where monetary policyreaches its maximum impact on production on theseventh month after the unexpected monetary shocktook place.

Reaction function

The VAR methodology has played an important rolein the empirical analysis concerning the impact of mon-etary policy actions on economy. Even so it has beenquestioned not only in its method for retrieving

Fig. 1. Function of impulse–response of industrial production(IPI) and prices (CPI) with respect to a monetary shock (one

standard deviation)Note: Estimates were carried out using Eviews

378 Carlos J. Rodrıguez-Fuentes and David Padron-Marrero

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14

monetary shocks, but also with the problems associatedwith capturing the forward-looking behaviour whichmodern monetary policy theory attributes to centralbanks (CLARIDA et al., 1999; SVENSSON, 1999). Underthis scenario, the monetary authority considers theexpected evolution of the relevant economic aggregatesin the near future while making decisions in the present.This approach has grown in favour among a number ofauthors when evaluating the actions of central banks,and can be adapted to its inclusion in the specificationof a reaction function for the monetary authority.

For this reason it was also decided to estimate a reac-tion function for the Bank of Spain where the unex-pected monetary shock is identified with theunexplained observed interest rates by deriving ratesbased on the estimated reaction function.

The reaction function that was estimated has the fol-lowing form:

ii ¼ rit�1 þ (1 þ r)baþ bptþk þ gxtþp þ lZtc

þ 1t (4)

where p is the inter-annual inflation rate; x is theoutput-gap; and Z is a set of variables which canaffect interest rate decisions, independently of its expla-natory power on inflationary trends and the output-gap,which include the exchange rate and a foreign interestrate. The model specification includes the peseta/mark nominal exchange rate and the German three-month interest rate.

The proposed reaction function is a simple combi-nation of a Taylor Rule-type reaction function(TAYLOR, 1993) and a first-order partial autoregressionrule. The Taylor Rule reaction function incorporatesthe forward-looking behaviour assumption for themonetary authority (under the assumption of rationalexpectations). The autoregression rule captures

demonstrated tendencies by central banks to smoothinterest rate changes.

The resultant reaction function was estimated by thegeneralized method of moments (GMM) by takingadvantage of the following set of orthogonal conditions:

E½1t=Vt� ¼ Ebit � rit�1 � (1 � r)caþ bptþk

þ gxtþp þ lZtb=Vtc

¼ 0 (5)

Possible problems of heteroskedasticity and autocorrela-tion led the authors to use the Newey and West methodwhen calculating standard errors. The Hansen J-statisticwas also calculated to control possible over identifi-cation. Table 1 shows that the best results were obtainedby the forecast horizon k ¼ 6 > p ¼ 3. In addition, itwas decided to omit the peseta/mark nominal exchangerate since changes in the variable were not statisticallysignificant in any of the tested specifications.

Fig. 2 compares the accumulated monetary shocksobtained from VAR models with those derived fromthe reaction function. The resultant time profiles indi-cate that both series are quite similar, leading to aninterpretation of favourable evidence regarding therobustness of the results. Also worth mentioning is thepresence of a strong relationship between the shownpath from the accumulated shocks and the short-terminterest rate. Consequently, in the periods where theshort-term interest rate increases, contracting shocksare seen, as in the opposite case for falling rates. Never-theless, from 1996 to 1997 this relationship seems tostray from this trend. If this is the case, these actionscould be interpreted as deliberate actions by the Bankof Spain to tighten monetary policy and thus exercise

Table 1. Results from estimating the reaction function for the Bank of Spain

k ¼ 3

p ¼ 3

k ¼ 6

p ¼ 6

k ¼ 12

p ¼ 12

k ¼ 6

p ¼ 3

k ¼ 12

p ¼ 3

k ¼ 12

p ¼ 6

k ¼ 3

p ¼ 3

Z ¼ iAL

k ¼ 6

p ¼ 3

Z ¼ iAL

r 0.905�� 0.949�� 0.973�� 0.924�� 1.006�� 1.002�� 0.898�� 0.897��

a 20.485 22.015 20.249 21.943� 33.049 81.290 20.414 21.204

b 2.054�� 2.556�� 1.532�� 2.252�� 20.700 24.583 1.895�� 1.523��

g 0.223�� 0.088 20.337� 0.423�� 22.662 23.986 0.205�� 0.226��

l – – – – – – 0.122 0.561��

R2 0.986 0.985 0.982 0.983 0.982 0.982 0.986 0.985

SE 0.419 0.424 0.444 0.458 0.439 0.443 0.419 0.433

J-test 17.12

[0.998]

17.32

[0.998]

16.69

[0.998]

17.60

[0.997]

17.22

[0.998]

17.39

[0.997]

16.99

[0.997]

17.75

[0.995]

Notes: Estimates were carried out using Eviews.

A variable is significant at the �5% and ��1% level, respectively.

The following variables were used in the estimation: constant, it21, it22, it23, it24, it25, it26, it29, it212, pt21, pt22, pt23, pt24, pt25, pt26,

pt29, pt212, xt21, xt22, xt23, xt24, xt25, xt26, xt29, xt212, qt21, qt22, qt23, qt24, qt25, qt26, qt29, qt212, mt21, mt22, mt23, mt24, mt25, mt26,

mt29, and mt212, where q is the change in the nominal peseta2mark exchange rate; and m is the rate of growth in the M3 monetary aggregate.

Also shown is the J-statistic and the probability of accepting the null hypothesis.

Industry Effects of Monetary Policy in Spain 379

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14

stricter control on the inflation rate and satisfy theMaastricht criteria.

SECTORAL ASYMMETRIES IN

THE TRANSMISSION OF

MONETARY SHOCKS

Following PEERSMAN and SMETS (2002), the industryeffects of monetary policy shock in Spain9 are studiedherein by using the following expression which relatesthe trends from the production activity from each indus-trial branch with its past behaviour and the estimatedaccumulated monetary shock from the prior section:

ipii,t ¼ ai þX12

j¼1

bi � ipii,t�j þ gi � shockt�1 þ hi, t (6)

where ipii,t is monthly growth rate of the industrial pro-duction index (IPI) of branch i; shockt – 1 is the accumu-lated monetary policy shock estimated previously(VAR- and RF-shock); and hi,t is an error term.Given the possibility of instantaneous correlationbetween the different Spanish industrial branches,expression (6) has been estimated using the SeeminglyUnrelated Regressions (SUR) method.

Table 2 summarizes the estimated values from theresponse of the different industrial sections in Spainwith respect to a monetary shock (gi). Table 2 indicatesthat the production response with respect to an unex-pected monetary shock is generally negative. Anotheraspect which deserves attention is the presence ofclear similarities among the obtained results for bothVAR- and RF-shocks. These results suggest that thecontraction in production is greater among miningindustries (section C), while section E (electricity, gasand water supply) is found at the opposite extreme.However, the low statistical significance of the estimatesfor this disaggregated level (sections) should be high-lighted since only the estimated response for themining industries from the RF-shock were seen to bestatistically significant.

The lack of statistical significance from the obtainedresults at the section level of industrial activity could beattributed to the presence of distinct behaviour amongthe activity branches (subsections) which make up thedifferent industrial sections. Therefore, the paper willnow analyse the sectoral responses at the subsectionlevel, with the results shown in Table 3.

The estimated parameters are generally characterizedby an expected negative sign, indicating the (unex-pected) tightening of monetary policy resulting in acontraction of the different industrial branches under

Table 2. Response from different industrial branches with respect to a monetary shock (gi)

RF-shock VAR-shock

Section Coefficient t-statistic Section Coefficient t-statistic

C 21.260707 22.648278 C 20.665141 21.641380

D 20.490532 21.509285 D 20.229419 20.973417

E 20.025145 20.103596 E 0.221215 0.869998

Note: C (mining and quarrying), D (manufacturing), and E (electricity, gas a water supply).

Fig. 2. Monetary shocks and short-term interest rates in Spain

380 Carlos J. Rodrıguez-Fuentes and David Padron-Marrero

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14

study. The results also indicate once again that estimatedparameters from the RF-shock are greater (in absolutevalue) than those obtained from using the VAR-shock, in addition to having greater statistical signifi-cance. Although there is a greater level of disaggregationin these estimates, the comparison between theobtained sectoral responses from both VAR- andRF-shocks allow one to offer some conclusions. First,that subsection EA (electricity, gas and water supply)once again is seen as one of the branches least sensitiveto monetary shocks, as in the case at the section level.Other branches also appear, such as the manufactureof food products, beverages and tobacco (subsectionDA), as well as the manufacture of leather and leatherproducts (subsection DC), the paper industry (subsec-tion DE), and the manufacture of coke, refinedpetroleum products and nuclear fuels (subsection DF).Another observation is that the greater sensitivity tonational monetary shocks would take place in machin-ery and mechanical equipment (subsection DK), themining and quarrying of energy producing material(subsection CA), and the mining and quarrying ofother minerals (subsection CB).

Some important differences need to be mentionedwhen comparing the results from the obtained estimatesfrom the reaction function (RF-shock) and the VARmodel (VAR-shock). The first difference concerns theDM (manufacture of transport equipment) and DJ(manufacture of basic metals and fabricated metal pro-ducts) subsections. While high sensitivity is observedwith respect to estimated monetary shocks based onthe reaction function (RF-shock) of these subsections,the VAR-shock produces much lower sensitivity. Asecond difference occurs in the different manufacturingindustries (subsection DN), where slight sensitivity withrespect to estimated monetary shocks based on the VARmodel are noted (VAR-shock). Nevertheless, the esti-mated response for the reaction function (RF-shock)ranks this section in an intermediate position amongall sectors.

The presence of sectoral asymmetries in thetransmission of monetary policy has obvious directimplications at the regional level. Indeed, given thatSpanish regions show important differences in industrialspecialization, the presence of different sectoralresponses with respect to monetary policy impulses in

Table 3. Response by industrial subsections with respect to monetary shock (gi)

FR-shock VAR-shock

Subsection Coefficient t-statistic Subsection Coefficient t-statistic

DA 0.107995 0.367364 EA 0.245455 0.968357

DC 20.032593 20.082099 DN 0.208370 0.460732

EA 20.051506 20.213997 DF 0.070817 0.185372

DE 20.081628 20.342259 DE 20.033691 20.139498

DF 20.224908 20.668028 DA 20.090756 20.293388

DG 20.292967 20.733748 DC 20.095969 20.228702

DI 20.412020 21.659494 DH 20.276524 20.644695

DN 20.537933 21.236804 DI 20.314554 21.506139

DL 20.823875 21.465081 DJ 20.339709 21.129706

DD 20.861333 21.646532 DM 20.391174 20.435383

DB 20.948324 22.477780 DL 20.515330 20.896411

DH 21.088006 22.424762 DG 20.535510 21.533995

DJ 21.090333 22.990396 DB 20.551075 21.706137

CB 21.126873 21.988770 DD 20.630545 21.298233

CA 21.560122 23.520476 CA 20.715491 21.580320

DK 21.925580 23.067467 CB 20.819522 21.629274

DM 22.002185 22.523202 DK 21.111361 22.136371

Wald test

x2 (probability) x2 (probability)

Total sample 34.60183 (0.0045) Total sample 20.32358 (0.2060)

7þ and 5– 29.93248 (0.0016) 7þ and 5– 17.41318 (0.0962)

3þ and 3– 24.76408 (0.0002) 3þ and 3– 12.56997 (0.0278)

Note: CA, mining and quarrying of energy producing materials; CB, mining and quarrying, except of energy-producing materials; DA,

manufacture of food products, beverages and tobacco; DB, manufacture of textiles and textile products; DC, manufacture of leather and

leather products; DD, manufacture of wood and wood products; DE, manufacture of pulp, paper and paper products; publishing and print-

ing; DF, manufacture of coke, refined petroleum products and nuclear fuel; DG, manufacture of chemicals, chemical products and man-

made fibres; DH, manufacture of rubber and plastic products; DI, manufacture of other non-metallic mineral products; DJ, manufacture

of basic metals and fabricated metal products; DK, manufacture of machinery and equipment not elsewhere classified (n.e.c.); DL, manu-

facture of electrical and optical equipment; DM, manufacture of transport equipment; DN, manufacturing n.e.c.; EA, electricity, gas and

water supply.

Industry Effects of Monetary Policy in Spain 381

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14

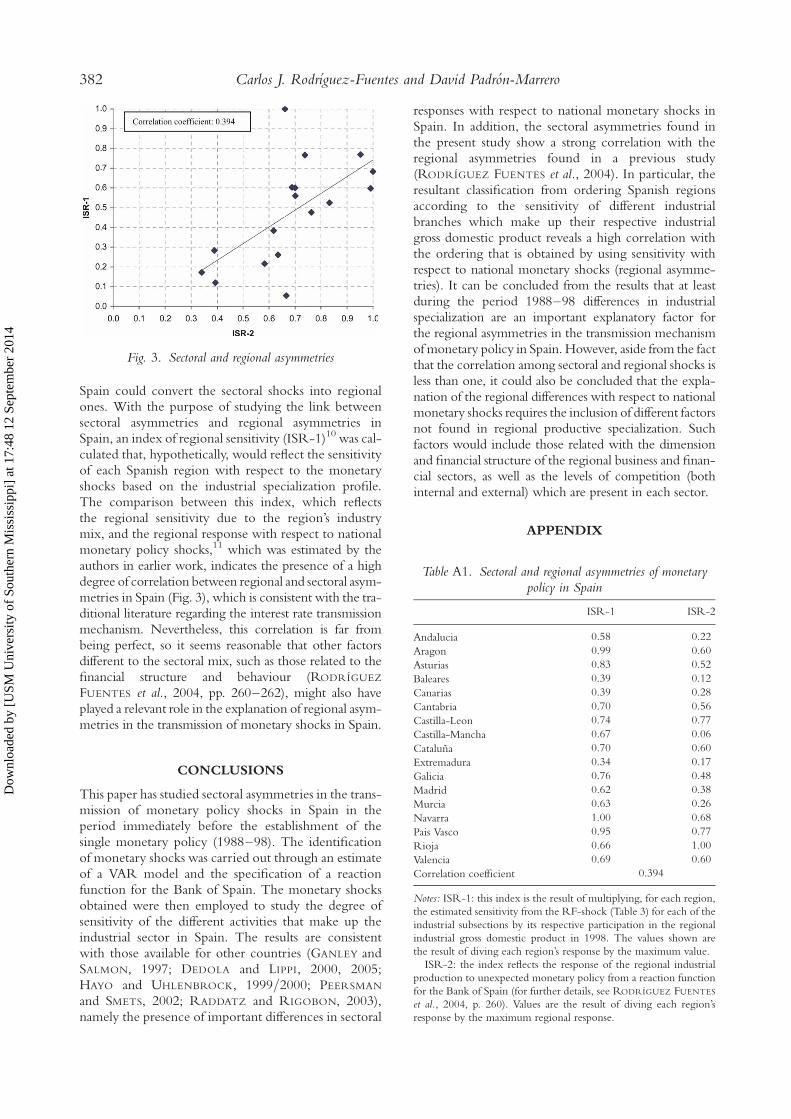

Spain could convert the sectoral shocks into regionalones. With the purpose of studying the link betweensectoral asymmetries and regional asymmetries inSpain, an index of regional sensitivity (ISR-1)10 was cal-culated that, hypothetically, would reflect the sensitivityof each Spanish region with respect to the monetaryshocks based on the industrial specialization profile.The comparison between this index, which reflectsthe regional sensitivity due to the region’s industrymix, and the regional response with respect to nationalmonetary policy shocks,11 which was estimated by theauthors in earlier work, indicates the presence of a highdegree of correlation between regional and sectoral asym-metries in Spain (Fig. 3), which is consistent with the tra-ditional literature regarding the interest rate transmissionmechanism. Nevertheless, this correlation is far frombeing perfect, so it seems reasonable that other factorsdifferent to the sectoral mix, such as those related to thefinancial structure and behaviour (RODRIGUEZ

FUENTES et al., 2004, pp. 260–262), might also haveplayed a relevant role in the explanation of regional asym-metries in the transmission of monetary shocks in Spain.

CONCLUSIONS

This paper has studied sectoral asymmetries in the trans-mission of monetary policy shocks in Spain in theperiod immediately before the establishment of thesingle monetary policy (1988–98). The identificationof monetary shocks was carried out through an estimateof a VAR model and the specification of a reactionfunction for the Bank of Spain. The monetary shocksobtained were then employed to study the degree ofsensitivity of the different activities that make up theindustrial sector in Spain. The results are consistentwith those available for other countries (GANLEY andSALMON, 1997; DEDOLA and LIPPI, 2000, 2005;HAYO and UHLENBROCK, 1999/2000; PEERSMAN

and SMETS, 2002; RADDATZ and RIGOBON, 2003),namely the presence of important differences in sectoral

responses with respect to national monetary shocks inSpain. In addition, the sectoral asymmetries found inthe present study show a strong correlation with theregional asymmetries found in a previous study(RODRIGUEZ FUENTES et al., 2004). In particular, theresultant classification from ordering Spanish regionsaccording to the sensitivity of different industrialbranches which make up their respective industrialgross domestic product reveals a high correlation withthe ordering that is obtained by using sensitivity withrespect to national monetary shocks (regional asymme-tries). It can be concluded from the results that at leastduring the period 1988–98 differences in industrialspecialization are an important explanatory factor forthe regional asymmetries in the transmission mechanismof monetary policy in Spain. However, aside from the factthat the correlation among sectoral and regional shocks isless than one, it could also be concluded that the expla-nation of the regional differences with respect to nationalmonetary shocks requires the inclusion of different factorsnot found in regional productive specialization. Suchfactors would include those related with the dimensionand financial structure of the regional business and finan-cial sectors, as well as the levels of competition (bothinternal and external) which are present in each sector.

APPENDIX

Fig. 3. Sectoral and regional asymmetries

Table A1. Sectoral and regional asymmetries of monetarypolicy in Spain

ISR-1 ISR-2

Andalucia 0.58 0.22

Aragon 0.99 0.60

Asturias 0.83 0.52

Baleares 0.39 0.12

Canarias 0.39 0.28

Cantabria 0.70 0.56

Castilla-Leon 0.74 0.77

Castilla-Mancha 0.67 0.06

Cataluna 0.70 0.60

Extremadura 0.34 0.17

Galicia 0.76 0.48

Madrid 0.62 0.38

Murcia 0.63 0.26

Navarra 1.00 0.68

Pais Vasco 0.95 0.77

Rioja 0.66 1.00

Valencia 0.69 0.60

Correlation coefficient 0.394

Notes: ISR-1: this index is the result of multiplying, for each region,

the estimated sensitivity from the RF-shock (Table 3) for each of the

industrial subsections by its respective participation in the regional

industrial gross domestic product in 1998. The values shown are

the result of diving each region’s response by the maximum value.

ISR-2: the index reflects the response of the regional industrial

production to unexpected monetary policy from a reaction function

for the Bank of Spain (for further details, see RODRIGUEZ FUENTES

et al., 2004, p. 260). Values are the result of diving each region’s

response by the maximum regional response.

382 Carlos J. Rodrıguez-Fuentes and David Padron-Marrero

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14

NOTES

1. Nevertheless, this hypothesis has been questioned by

other authors, who point out that the shape of a monetary

union also reinforces bilateral trade among its members.

This effect would result in higher levels of correlation

in their respective cycles and a lower probability of

experiencing asymmetric shocks (FRANKEL and ROSE,

1998).

2. The authors have not been able to include the services in

their analysis due to a lack of statistics in Spain in this

regard.

3. This result is unconvincing since Central Bank decisions

will always cause a single (and common) monetary shock,

which undoubtedly might produce different effects on

certain sectors; but it is the response that might differ

across sectors not the shock itself.

4. Nevertheless, DEDOLA and LIPPI (2005, p. 1551) point

out that the estimated parameter associated with the

instantaneous response of the production sector monet-

ary shock is not far from zero, and such an inconsistency

would not be relevant in their model.

5. It is important to note that the present study is only con-

sidering the unanticipated monetary policy, that is, the

monetary policy ‘surprises’ or exogenous shocks, which

is common practice in the current empirical literature

on sectoral effects of monetary policy (GANLEY and

SALMON, 1997; HAYO and UHLENBROCK, 1999/2000;

PEERSMAN and SMETS, 2002; DEDOLA and LIPPI,

2005). However, the present authors are aware that the

monetary policy decisions also have a systematic com-

ponent which is at least as important as the ‘monetary

surprises’ (MCCALLUM, 2001, p. 38), but its identifi-

cation usually requires the estimation of structural

models which are highly demanding in terms of data

(not available to the authors).

6. The reasoning behind the inclusion of the German inter-

est rate is to acknowledge Spain’s membership in the

European Monetary System (EMS) and the ‘anchoring’

role performed by the German economy within the

EMS. The authors also considered the insertion of the

M3 due to the importance attributed by the Bank of

Spain to monetary aggregates (in its monetary strategy)

during most of the period under study (BANK OF

SPAIN, 1997, pp. 89–119).

7. The reasoning for using this period is to avoid the period

of monetary instability present during the 1970s and early

1980s where monetary policy of the Bank of Spain

focused on the strict control of monetary aggregates.

Starting with the mid-1980s the growing financial

opening of the Spanish economy, with its membership

in the EMS, and especially the liberalization process of

the Spanish financial system created important changes

in the strategy followed by the Bank of Spain, resulting

in the growing importance of interest rates in the

execution of monetary policy. The year 1988 was

chosen as the beginning date for this second period,

thus avoiding the important variability experienced in

interest rates during 1987 (for further details, see BANK

OF SPAIN, 1997, esp. pp. 89–119).

8. By acting this way, the authors assumed that unexpected

monetary policy actions do not have an instantaneous

impact on output (IPI) and prices (CPI).

9. Data restrictions limit the estimates for the industrial

activity branches to the period 1991–98.

10. This parameter was calculated as the result of multiplying,

for each region, the estimated sensitivity from the

RF-shock (Table 3) for each of the industrial subsections

by its respective participation in the regional industrial

gross domestic product in 1998.

11. The values of both parameters are shown Appendix

Table A1.

REFERENCES

ARNOLD I. J. M. (2001) The regional effects of monetary policy in Europe, Journal of Economic Integration 16, 399–420.

BANK OF SPAIN (1997) La polıtica monetaria y la inflacion en Espana. Alianza Editorial, Madrid.

CARLINO G. and DEFINA R. (1996) Does monetary policy have differential regional effects?, Federal Reserve Bank of Philadelphia,

Business Review March/April, 17–27.

CARLINO G. and DEFINA R. (1998a) The differential regional effects of monetary policy, Review of Economics and Statistics 80,

572–587.

CARLINO G. and DEFINA R. (1998b) Monetary Policy and the U.S. States and Regions: Some Implications for the European Monetary

Union. Working Paper No. 98–17. Federal Reserve Bank of Philadelphia, Philadelphia, PA; repr. in VON HAGEN J. and

WALLER C. J. (Eds) (2000) Regional Aspects of Monetary Policy in Europe, pp. 45–67. Kluwer, London.

CARLINO G. and DEFINA R. (1999) Do states respond differently to changes in monetary policy?, Federal Reserve Bank of

Philadelphia, Business Review July/August, 17–27.

CHRISTIANO L., EICHENBAUM M. and EVANS C. (1999) Monetary policy shocks: what have we learned and to what end?, in

TAYLOR J. and WOODFORD M. (Eds) Handbook of Macroeconomics. North Holland, Amsterdam.

CLARIDA R., GALI J. and GERTLER M. (1999) The science of monetary policy: a new Keynesian perspective, Journal of Economic

Literature 37, 1661–1707.

DEDOLA L. and LIPPI F. (2000) The Monetary Transmission Mechanism: Evidence from the Industries of Five OECD Countries. Discus-

sion Paper No. 2508, July. Centre for Economic Policy Research (CEPR), London.

DEDOLA L. and LIPPI F. (2005) The monetary transmission mechanism: evidence from the industries of five OECD countries,

European Economic Review 49, 1543–1569.

GANLEY J. and SALMON C. (1997) The Industrial Impact of Monetary Policy Shocks: Some Stylized Facts. Working Paper No. 68. Bank

of England, London.

GUISO L., KASHYAP A. K., PANETTA F. and TERLIZZESE D. (1999) Will a Common European Monetary Policy have asymmetric

effects?, Federal Reserve Bank of Chicago, Economic Perspectives fourth quarter, 56–75.

Industry Effects of Monetary Policy in Spain 383

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14

HAYO B. and UHLENBROCK B. (1999/2000) Industry Effects of Monetary Policy in Germany [1999]. Working Paper No. B14. Center

for European Integration Studies (ZEI); repr. in VON HAGEN J. and WALLER C. J. (Eds) (2000) Regional Aspects of Monetary

Policy in Europe. Kluwer, London.

KRUGMAN P. and VENABLES A. J. (1996) Integration, specialization and adjustment, European Economic Review 40, 959–967.

MCCALLUM B. T. (2001) Analysis of the monetary transmission mechanism: methodological issues, in DEUTSCHE BUNDESBANK

(Ed.) The Monetary Transmission Process. Recent Developments and Lessons for Europe, pp. 11–43. Palgrave Macmillan, New York, NY.

PEERSMAN G. and SMETS F. (2002) The Industry Effects of Monetary Policy in the Euro Area. Working Paper No. 165. European

Central Bank; also Economic Journal 115, 319–342.

RADDATZ C. and RIGOBON R. (2003) Monetary Policy and Sectoral Shocks: Did the FED React Properly to the High-Tech Crisis?

Mimeo.

RODRIGUEZ FUENTES C. J. (2005) Regional Monetary Policy. Routledge: London.

RODRIGUEZ FUENTES C. J., PADRON MARRERO D. and OLIVERA HERRERA A. (2004) Estructura financiera regional y polıtica

monetaria. Una aproximacion al caso espanol, Papeles de Economıa Espanola 101, 252–265.

SVENSSON L. (1999) Monetary Policy Issues for the Eurosystem. Seminar Paper No. 667. Institute for International Economic Studies.

TAYLOR J. B. (1993) Discretion versus policy rules in practice, Carnegie-Rochester Conference Series on Public Policy 39, 195–214.

384 Carlos J. Rodrıguez-Fuentes and David Padron-Marrero

Dow

nloa

ded

by [

USM

Uni

vers

ity o

f So

uthe

rn M

issi

ssip

pi]

at 1

7:48

12

Sept

embe

r 20

14