Industries Energy, Utilities & Mining

80

Industries Energy, Utilities & Mining *connectedthinking Utilities global survey 2009 A world beyond recession*

Transcript of Industries Energy, Utilities & Mining

IndustriesEnergy, Utilities & Mining

*connectedthinking

Utilities global survey 2009

A world beyond recession*

Utilities global survey 2009

A world beyond recession*

credit crisis financial crisis economic growth widespread recession

receding recession being ready to power the upturnworld insecurity future energy security

climate change debate sustainable cleaner power

In the space of the past 12 months, utility companies have found themselvesin a very different world with a series of momentous events – the collapse ofgiants of the banking system, the credit and wider financial crisis, the reversalin demand and price growth, and outright recession in many major markets.But the time horizons required for planning in the energy sector requirecompanies to plan and think a long way ahead. A world beyond recessionlooks at the impact of the events of the past year, through the views of seniorutility company executives, and ahead at the world that lies beyond thedownturn.

d recessiony to power the upturny securitye cleaner power

4 Global 26 The Americas2 Report highlights

Utilities global survey 2009

“We are experiencing atransformational economic crisis – one that is on course to fundamentally changeglobalization well beyond the domain of internationalfinance”Klaus Schwab, founder and executive chairman of the World Economic Forum

42 Europe 46 Asia Pacific 58 Middle East & Africa

1 Introduction

2 Report highlights

4 Inside the boardroom: Global4 Risk8 Growth

13 Regulation19 Operations22 People

26 The Americas26 United States34 Canada37 South America

42 Europe

46 Asia Pacific46 Asia50 Australia and New Zealand

58 Middle East and Africa58 Middle East63 Central, East and West Africa68 Southern Africa

70 Looking ahead

71 Contact us

73 Methodology

The AmericasArgentinaCanadaChileEcuadorMexicoPeruUnited StatesEurope AustriaCzech RepublicFranceGermanyHungaryPolandPortugalRussiaSpainSwedenUnited KingdomAsia PacificAustralia India Korea Malaysia New Zealand Philippines Singapore Thailand Middle East & AfricaBotswana Ghana Israel Jordan Kenya Mauritius Namibia Nigeria Qatar South Africa Tanzania United Arab Emirates Zambia

This year’s surveyinterviewed 69 seniorpower utility executivesfrom 65 utility companiesin 39 countries from 4major regions.

Manfred Wiegand

Global Utilities Leader

Introduction 1

Each year PricewaterhouseCoopers goes to the heartof boardroom thinking in power utility companies witha survey of senior executives across the globe. In2008, our World of difference report mapped theenormity of the changes witnessed in the last 10years and those lying ahead in future decades. Our2009 report, A world beyond recession, looks at theimpact of the economic downturn and financial crisison the sector but, also, beyond to the time horizonsthat are important for long-term energy planning.

We interviewed about 70 executives from leadingpower utility companies in major markets around theworld to gain their perspective on the implications ofthis very different world environment. We also includethe viewpoints of CEOs from a number of leadingutility companies in different parts of the world.

Power utility companies find themselves operating ina very different world from just a year before. It is aworld shell-shocked by the rapidity of the financialand economic collapse, where previous certaintieshave been replaced by uncertainty, where faith inmarkets and regulation has been shaken and whererecession has taken the place of growth.

For utility companies, however, the timescalesrequired for imperatives such as infrastructurerenewal, new generation and greener energy reachbeyond the recession. The very business of powerrequires them to stretch their horizons further. The investment required in the sector is considerable.Yet the financial crisis has tightened the availability ofcapital. Governments are debt-laden, clouding theoutlook for future subsidy for greener energy, and thedownturn has dampened demand, particularly frombig industrial consumers.

Companies face a delicate balancing act. They needto make the adjustments necessary to steer throughthe changed economic and financial environment butalso maintain a long-term horizon. Fewer investmentswill surely mean reduced reserve margins in thefuture with the danger of higher price spikes andgreater competition for limited supplies when theevolving global recession recedes.

Credit crunch clouds outlook forfuture targets

Utility companies have to judge the pace andlevel of investment programmes to respond toa complex mix of future demand, energysecurity and climate change drivers. Oneresult of the current market environment hasbeen to cast considerable doubt on whetherinvestment will come forward in a timelymanner to keep pace with future demand forpower and climate change targets. Two-thirds(67%) of our survey respondents report that ashortage of capital is having a high or veryhigh impact on their activities.

Investment barriers heighten

The development of new generation capacityand the renewal of existing generation plantsare priority areas for most companies; 83%are seeking to make medium to largeinvestment in new generation and three-quarters are seeking to do likewise intransmission and distribution. However, thesenior utility company executives in oursurvey are worried about the high costs andhigh levels of cost uncertainty associated withprojects. Two-thirds cite problems in securingfinance as a medium or high barrier to projectdevelopment. Skill shortages and access togood procurement capability also continue topose challenges for many companies.

Risk controls set to red alert

The current environment is heighteningenergy trading risk. Liquidity in the market is amajor concern. Eighty-six per cent ofrespondents indicated that reduced liquidityin energy trading markets was having animpact on their companies, with 60% of allrespondents rating this impact as high or veryhigh. Customer credit risk is also identified asan area of major concern and 90% ofrespondents reported a high or very highimpact of increased sales and retail creditrisk. Companies are mindful of the risks ofcustomers going into liquidation, defaultingon payments, bargaining over delivery orsimply shutting down plants and requiring less supply.

Maintaining a focus on climatechange

2009 will be a watershed year for climatechange regulation with world leaders seekingto agree a successor to the Kyoto Protocol.Utility companies in our survey emphasise theimportance of greater clarity of climatechange policy but express concern that theeconomic recession is undermining thechances of an effective response to climatechange. Asked if the economic recessionwould slow down responses to climatechange, 79% felt it would with two thirds ofthe 79% saying it would have a high or veryhigh slowdown impact. Many of thosesurveyed also thought that a return to highenergy prices would dilute commitment toenvironmentalism.

2

Economic incentives needed to boost renewables in the mix

Nearly three-fifths of respondents (59%) feelthat their renewable energy investmentprogrammes are being affected by the lack ofclarity from governments on renewable energytargets and financial support for renewableenergy. The importance of greater certainty onboth targets and economic mechanisms tosupport renewable energy is highlighted by thefact that, even coming off the back of a periodof record high power prices, only 28% ofrespondents believe that unsubsidisedrenewable power can compete commerciallyagainst fossil fuel generation.

Technology holds the key

Technology will be central to future growth andcompetitive advantage. The importance oftechnology for key developments, such asenergy efficiency and the expansion of nuclearpower, has led many survey respondents topinpoint power equipment and technologycompanies as a more significant competitivethreat than even direct competition in the retailmarket by other utility company home marketrivals. Technological innovation is seen ascentral to a range of key developments in thesector. In the coming decade, technologicalinnovation is seen as having most new impacton energy efficiency, solar power, combinedheat and power, distributed generation andcombustible renewable generation. Lookingfurther afield, carbon capture and storage willbe essential for the sector’s contribution to themitigation of climate change.

Report highlights 3

An estimated cumulative investment of US$13.6 trillion isneeded by the power industry in the period to 2030according the reference scenario model used by theInternational Energy Agency. Although this outlookpredated the intensification of the economic downturn inlate 2008 and early 2009, the timeframe for the modeland, indeed, the timescales required to develop newgeneration capacity, particularly in nuclear, take theindustry’s horizons beyond even a deep recession.Moreover, much of the projected electricity demandgrowth occurs outside of the OECD and this rebalancingof world demand is likely to remain a key trend evenduring recession.

4 Inside the boardroom: Global

The investment challenges for the sector flow from threeprincipal imperatives – renewal, diversification andgrowth. The need for renewal of ageing infrastructuremay be alleviated by falling demand but the underlyingrequirement to replace or upgrade plants and networkswill not go away. Similarly, the need for diversification,driven by the twin imperatives of greater energy securityand responding to climate change, remains in place.Energy security concerns have again been highlightedwith interruptions to Russian gas supply to Europe inearly 2009. On the climate change front, the latestscientific consensus on climate change indicates thatthe timetable for effective responses is more urgent thanever.

These concerns are reflected in the industry’sassessment of the most important developments in theirpower market in the coming decade (see Figure 1) andthe most pressing investment priorities (see Figure 2).The need to respond to the encouragement of renewableenergy and to reduce emissions is emphasised by themajority of survey respondents. Concerns over securityof supply also remain strong with over half ofrespondents stating that this would remain a key issue intheir market in the coming decade. The transmissioninfrastructure challenge is reflected in its reappearancein the top six chart in 2009 after dropping out in the pastfew years. Significant proportions of respondentshighlight the need for investment to respond to worriesabout transmission congestion, capacity margins andsecuring upstream gas supply.

RiskEconomic recession and the financial crisishave heightened the risks that utilitycompanies must manage. A major area of riskfor utility companies comes from balancingboth short-term and long-term supply anddemand. In turn, that means judging the paceof investment programmes to respond to acomplex mix of future demand, energysecurity and climate change drivers.

The current economic downturn has dampened energydemand, particularly from big industrial consumers, butthe long-term imperatives highlighted by respondentsremain in place. One result of the current marketenvironment has been to cast considerable doubt onwhether investment will come forward in a timely mannerto keep pace with future demand for power and climatechange targets. Two thirds (67%) of respondents reportthat a shortage of capital is having a high or very highimpact on their activities (see Figure 3).

Uniformly high responses were recorded to this questionacross all regions in the world and this is being reflectedin cutback announcements. In the US, for example,almost half of the top ten utilities have announcedreductions to planned 2009 capital expenditure. In sucha bearish climate, utilities are more than ever mindfulthat the cost and availability of capital is a key risk whendetermining a project’s financial viability.

Global 5

Figure 1: Top six ranking of the most important developments in your power market over the next 10 years?

Source: PricewaterhouseCoopers, Utilities global survey 2009

High or very high impact

Medium impact

Low or very low impact

71%

22%

7%

Encouragement of renewable energy

High or very high impact

Medium impact

Low or very low impact

66%

22%

12%

Regulation of emissions

High or very high impact

Medium impact

Low or very low impact

64%

32%

4%

Increasing efficiency

High or very high impact

Medium impact

Low or very low impact

56%

28%

15%

Increasing regulation and obligation

High or very high impact

Medium impact

Low or very low impact

55%

26%

19%

Increasing transmission capacity

High or very high impact

Medium impact

Low or very low impact

52%

26%

21%

Concerns over security of supply

Figure 2: The most pressing investment drivers

Source: PricewaterhouseCoopers, Utilities global survey 2009

Very pressing

Medium importance

Least pressing

61%

28%

12%

Renewable energy targets

Very pressing

Medium importance

Least pressing

58%

25%

17%

Meeting carbon emission targets

Very pressing

Medium importance

Least pressing

47%

33%

20%

Transmission congestion

Very pressing

Medium importance

Least pressing

46%

26%

28%

Smart metering regulation

Very pressing

Medium importance

Least pressing

45%

29%

26%

Securing gas supplies

Very pressing

Medium importance

Least pressing

35%

36%

29%

A low capacity margin

Figure 3: The impact of a shortage of capital for infrastructure projects

Source: PricewaterhouseCoopers, Utilities global survey 2009

High or very high impact

Medium impact

Small or very small impact

67%

20%

13%

Figure 5: Increased credit risk in the sales and retail business

Source: PricewaterhouseCoopers, Utilities global survey 2009

High / very high impact 55%

Small / very small impact 10%

Medium impact 35%

6

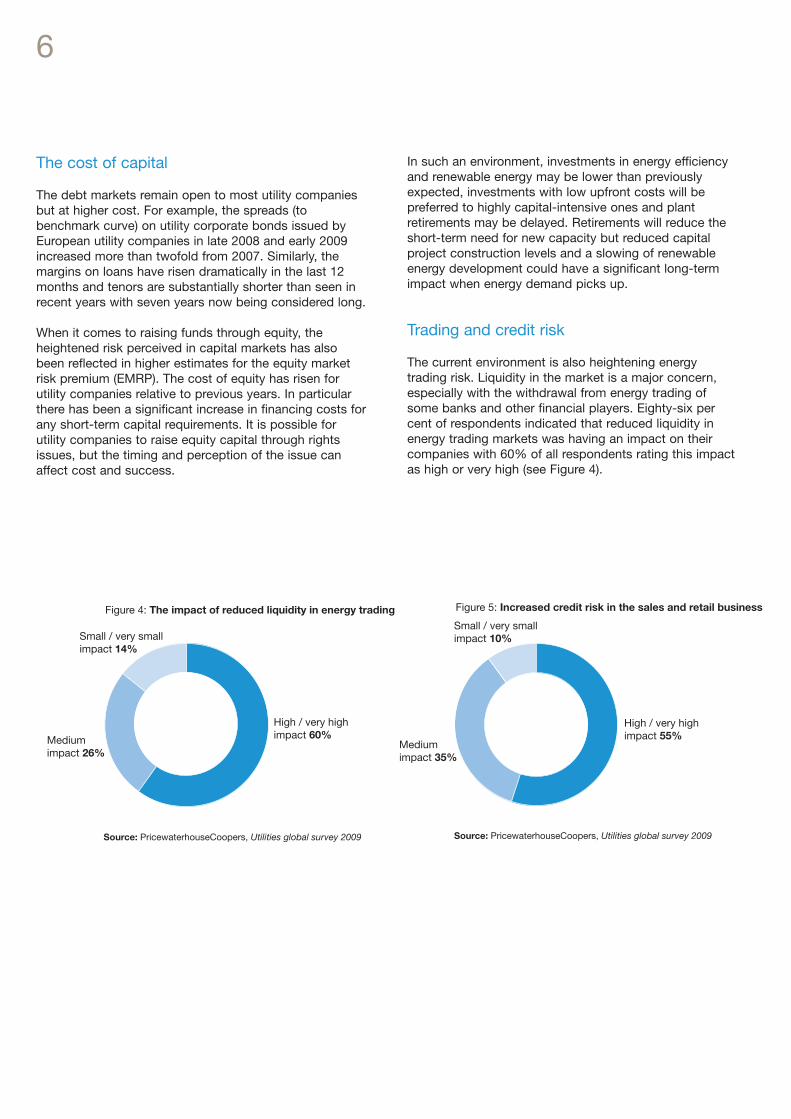

The cost of capital

The debt markets remain open to most utility companiesbut at higher cost. For example, the spreads (tobenchmark curve) on utility corporate bonds issued byEuropean utility companies in late 2008 and early 2009increased more than twofold from 2007. Similarly, themargins on loans have risen dramatically in the last 12months and tenors are substantially shorter than seen inrecent years with seven years now being considered long.

When it comes to raising funds through equity, theheightened risk perceived in capital markets has alsobeen reflected in higher estimates for the equity marketrisk premium (EMRP). The cost of equity has risen forutility companies relative to previous years. In particularthere has been a significant increase in financing costs forany short-term capital requirements. It is possible forutility companies to raise equity capital through rightsissues, but the timing and perception of the issue canaffect cost and success.

In such an environment, investments in energy efficiencyand renewable energy may be lower than previouslyexpected, investments with low upfront costs will bepreferred to highly capital-intensive ones and plantretirements may be delayed. Retirements will reduce theshort-term need for new capacity but reduced capitalproject construction levels and a slowing of renewableenergy development could have a significant long-termimpact when energy demand picks up.

Trading and credit risk

The current environment is also heightening energytrading risk. Liquidity in the market is a major concern,especially with the withdrawal from energy trading ofsome banks and other financial players. Eighty-six percent of respondents indicated that reduced liquidity inenergy trading markets was having an impact on theircompanies with 60% of all respondents rating this impactas high or very high (see Figure 4).

Figure 4: The impact of reduced liquidity in energy trading

Source: PricewaterhouseCoopers, Utilities global survey 2009

High / very high impact 60%

Small / very small impact 14%

Medium impact 26%

Global 7

Liquidity is especially critical because companies areincreasingly dealing on a cleared exchange basis. If theyare in the over-the-counter market, there are collaterals tobe made. Large amounts of funds need to be available forcollateral or as a variation margin. As a result, credit riskmanagement is a very important area for companies. Customer credit risk is also identified as an area of majorconcern and 90% of respondents reported a high or veryhigh impact of increased sales and retail credit risk (seeFigure 5). Companies are clearly mindful of the risks ofcustomers going into liquidation, defaulting on payments,bargaining over delivery or simply shutting down plantsand requiring less supply.

1 2 30

Figure 6: The impact of market volatility

4 5

Note: Rate where 4-5 = agree/strongly agree; 3 = neither agree or disagree; 1-2 = disagree/strongly disagreeSource: PricewaterhouseCoopers, Utilities global survey 2009

Tightened counterparty creditmonitoring in response to

market price volatility

Manage risk exposures throughthe use of a structural hedge as a

result of market price volatility

Reduced/deferred investments/capitalexpenditure in response to

market price volatility

Current trading activities pose anincreasing reputational risk

to the business

Market events have caused mycompany to be concerned about

the efficacy of the firm’s tradingrisk management and governance

control frameworks

Strongly agree/agree

Strongly disagree/disagree

Neither agree or disagree

74%

63%

45%

39%

33%

13%

16%

24%

31%

22%

13%

20%

30%

30%

45%

Agree orstrongly agree

disagree orstrongly disagree

neither agreeor disagree

Price volatility

Companies are having to manage the latest turn of eventsagainst a background of continuing energy price volatility.They are responding in a range of ways. A significantmajority of respondents have taken measures to offset theimpact of volatile energy prices through structural hedgingand tighter counterparty monitoring (see Figure 6).Uncertainty and instability in wholesale energy markets isalso having an effect in terms of reductions or delays incapital expenditure. Respondents are mindful of thepotential for trading activities to cause reputational risk totheir companies and, indeed, 39% see such potentialincreasing. However, only a third go so far as to expressconcern about the efficacy of their firm’s trading riskmanagement and governance control frameworks.

Inorganic growth

However, some players will be less constrained thanothers by the financial markets. Transformational largetransactions cannot be ruled out but the main activity islikely to be at lower value levels and with an emphasis onindividual assets as well as corporate assets. Certainly theunderlying drivers of consolidation, supply security andcapitalisation remain in place and will create increasingpent-up deal demand. M&A remains a key route foracquiring new customers, securing supply and demandbalance in power, the acquisition of new capabilities anddelivering scale (see Figure 7).

8

GrowthThe power utilities industry has come off theback of a series of record-breaking years formergers and acquisitions activity. Inorganicgrowth has been the order of the day for manycompanies, particularly in Europe, ascompanies sought to acquire scale andpresence across territories. Now, many of thebusiest M&A players are concentrating onbedding down their acquisitions and deliveringthe synergies they are seeking. The constrainedavailability of finance will also inhibit dealactivity and, until that situation is eased, thereis unlikely to be a revival in deal values.

Figure 7: Inorganic growth: what is the driver of M&A within your business?

Source: PricewaterhouseCoopers, Utilities global survey 2009

Strong or very strong driver

Medium driver

Weak or very weak driver

Acquisition of skills or knowledge

Strong or very strong driver

Medium driver

Weak or very weak driver

Geographic expansion outside home territory

Strong or very strong driver

Medium driver

Weak or very weak driver

Creating an inherent hedge in portfolio – supply & demand balance in power

47%

33%

20%

Strong or very strong driver

Medium driver

Weak or very weak driver

Regulatory pressure

49%

25%

26%

Strong or very strong driver

Medium driver

Weak or very weak driver

Acquiring new customers

55%

33%

12%

Strong or very strong driver

Medium driver

Weak or very weak driver

Broadening product portfolios to existing customer

34%

30%

36%

46%

35%

19%

Strong or very strong driver

Medium driver

Weak or very weak driver

Scale for competitive advantage

40%

33%

27%

26%

39%

35%

Global 9

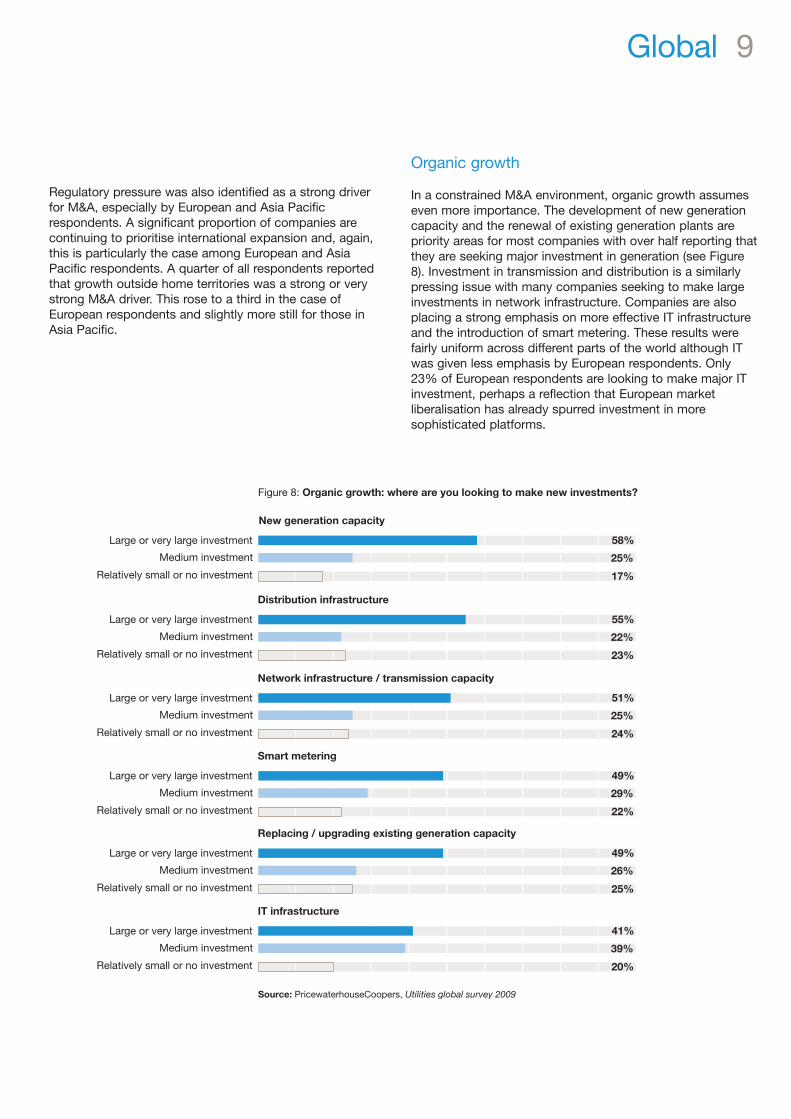

Organic growth

In a constrained M&A environment, organic growth assumeseven more importance. The development of new generationcapacity and the renewal of existing generation plants arepriority areas for most companies with over half reporting thatthey are seeking major investment in generation (see Figure8). Investment in transmission and distribution is a similarlypressing issue with many companies seeking to make largeinvestments in network infrastructure. Companies are alsoplacing a strong emphasis on more effective IT infrastructureand the introduction of smart metering. These results werefairly uniform across different parts of the world although ITwas given less emphasis by European respondents. Only23% of European respondents are looking to make major ITinvestment, perhaps a reflection that European marketliberalisation has already spurred investment in moresophisticated platforms.

Regulatory pressure was also identified as a strong driverfor M&A, especially by European and Asia Pacificrespondents. A significant proportion of companies arecontinuing to prioritise international expansion and, again,this is particularly the case among European and AsiaPacific respondents. A quarter of all respondents reportedthat growth outside home territories was a strong or verystrong M&A driver. This rose to a third in the case ofEuropean respondents and slightly more still for those inAsia Pacific.

Figure 8: Organic growth: where are you looking to make new investments?

Source: PricewaterhouseCoopers, Utilities global survey 2009

Large or very large investment

Medium investment

Relatively small or no investment

New generation capacity

Large or very large investment

Medium investment

Relatively small or no investment

Distribution infrastructure

Large or very large investment

Medium investment

Relatively small or no investment

Network infrastructure / transmission capacity

Large or very large investment

Medium investment

Relatively small or no investment

Smart metering

Large or very large investment

Medium investment

Relatively small or no investment

Replacing / upgrading existing generation capacity

Large or very large investment

Medium investment

Relatively small or no investment

IT infrastructure

58%

25%

17%

55%

22%

23%

51%

25%

24%

49%

29%

22%

49%

26%

25%

41%

39%

20%

The UK is an example of the trend to establish long-termcontracts from foreign sources to replace a declining NorthSea gas supply. UK utility companies have put in placelong-term contracts for gas – from Statoil in Norway(through the Langeled pipeline); from Gazprom in Russiapiped through Europe and the Bacton-Zeebruggeinterconnector; and for LNG shipments from sources suchas Qatar. The latter has necessitated considerableinvestment in LNG offload, regasification and pipelineinfrastructure. The BG Group has embarked on a majorinternational acquisition spree to gain access to Australiancoal methane gas for LNG shipping to internationalmarkets in Asia Pacific and further afield.

10

Upstream supply

Securing upstream supply, particularly of gas, remainsessential for most utility companies and our survey showsa progressive ramping-up over recent years ofprocurement strategies and moves to secure access toresources. More companies are placing long-termcontracts or sourcing supply from new regions in order tosecure their energy supply; 70% and 55% of respondentsrespectively cited these two moves compared with only49% and 26% just two years ago (see Figure 6). There isalso a notable increase in the proportion of respondentsreconsidering their fuel mix in both new and existingplants.

Source: PricewaterhouseCoopers, Utilities global survey 2009

Figure 9: How are you responding to upstream fuel challenges now and in the next 5 years?

2007 2008 2009

Improve your company procurement 39% 64% 77%

Secure current fuel mix by entering into long-term contracts 49% 54% 70%

Secure current fuel mix by sourcing fuel from new regions 26% 38% 55%

Change fuel mix in new & planned plants 29% 38% 55%

Upstream integration via direct investments 33% 51% 52%

Upstream integration via joint venture or alliance 27% 53% 46%

Change fuel mix in existing plants 27% 28% 39%

Upstream integration via acquisitions 16% 37% 35%

Global 11

Technology-driven competition and growth

Technology will be key to future growth and competitiveadvantage. The importance of technology for keydevelopments, such as energy efficiency and theexpansion of nuclear power, has led many surveyrespondents to pinpoint power equipment and technologycompanies as a more significant competitive threat thaneven direct competition in the retail market by other utilitycompany home market rivals. Only 14% of surveyrespondents viewed equipment and technologycompanies as no threat and 35% identified them as astrong or very strong threat.

1 2 30

Figure 10: Over the next 10 years, how would you rate the competitive threat posed to companies in your sector in your home territory by the following?

4 5

Note: Rate where 5 = greatest threat; 1 = no threatSource: PricewaterhouseCoopers, Utilities global survey 2009

Financial institutions and investment banks

New entrants from the power equipmentand technology sector

Utility companies based in your home territory

New entrants from energy-intensive users

New entrants from the construction sector

Companies from upstream oil & gas sector

‘New entrant’ technologies, being invested in bycompanies with strong balance sheets, are a threat tocompanies with older and less efficient coal and gasgeneration. Among the important technologies currentlybeing introduced, for example, are very efficient combinedcycle gas turbines (CCGTs) that have a thermal efficiencyof well over 50%. Super-critical coal technology uses highpressures and high temperatures to achieve thermalefficiency of above 40% (compared to mid-30s for mostexisting coal fired generation). These are cleaner, as wellas more efficient, power generation technologies. EarlyCCGTs sometimes had an efficiency of only 40% withlimits on their flexibility. Looking ahead, the potential forstand-alone or distributed local off-grid generation mayalso provide opportunities for power equipment andtechnology companies to play a more visible role with end-customers in the future power landscape.

The downturn may ease some of these constraints butfinance could continue to be a problem for many projects,particularly in the renewable energy field whereuncertainties about market competiveness are cloudingmany investments. Falling carbon prices have exacerbatedthe difficulties faced by renewable energy projects. Sector-wide, companies are expected to adjust their strategies byreducing costs and evaluating risks versus returns on newand existing projects. Postponement or cancellation,however, can increase costs and leave companiesexposed to market share losses in an upturn.

12

Barriers to growth

The importance of capital projects is reflected in thechallenges that companies identify in delivering theirgrowth strategy. Respondents are worried about the highcosts and high levels of cost uncertainty associated withprojects. Over a third cite problems in securing finance asa major barrier to growth. Skill shortages and access togood procurement capability also continue to posechallenges for many companies.

Figure 11: What difficulties/constraints do you anticipate in realising your growth strategy?

Source: PricewaterhouseCoopers, Utilities global survey 2009

Major or significant difficulty/constraint

Medium difficulty/constraint

Little or no difficulty/constraint

52%

33%

15%

Higher levels of project cost

Major or significant difficulty/constraint

Medium difficulty/constraint

Little or no difficulty/constraint

41%

36%

23%

Uncertainties in project cost

Major or significant difficulty/constraint

Medium difficulty/constraint

Little or no difficulty/constraint

36%

32%

32%

Difficulty in securing finance

Major or significant difficulty/constraint

Medium difficulty/constraint

Little or no difficulty/constraint

39%

25%

36%

Lack of skilled labour

Major or significant difficulty/constraint

Medium difficulty/constraint

Little or no difficulty/constraint

32%

32%

36%

Engineering procurement and construction (EPC) shortages

Major or significant difficulty/constraint

Medium difficulty/constraint

Little or no difficulty/constraint

31%

41%

29%

Uncertainty in ability to pass costs on down value-chain

Global 13

RegulationFrom market structure and rules, pricing andcompetition requirements through toemissions frameworks and theencouragement of renewable energy,regulation plays a vital role at the heart of theutilities sector. As we saw in Figure 1, 84% ofrespondents to our survey expect regulation toplay an increasing role in the next 10 yearsand two-thirds of the 84% say it will have alarge or very large impact on their market.

Market change

Regulation is already making itself more strongly felt. Forexample, structural change within energy markets is a keyregulatory challenge faced by major utilities today.Initiatives such as the Energy Third Package in Europehave been designed to facilitate a more transparent andcompetitive landscape. This is raising issues such as assetunbundling and cost reduction. In Europe, the past 12months have seen anti-trust investigations and courtrulings on power market competition and market access.The exact shape of European market reform will not beclear until summer 2009 and there are signs ofcompromise on network unbundling (see Europe section).In the UK, the energy regulator Ofgem is seeking newpowers to investigate and fine electricity companies formarket abuse amid concerns that generators are exploitingweaknesses in the system to push up prices.

In turn, we see utility companies stepping up theirresponses to regulatory change. Ninety three per cent ofsurvey respondents said their company was implementingoperational measures to respond to regulatory moves – upsharply from 76% of respondents two years ago (see Figure 12). A significant proportion of respondents arealso repositioning within the value chain (43%) or by country(41%) – again up from just two years ago. In some cases,such as E.ON’s earlier proposed sale of its networks,companies are seeking to be proactive in anticipation ofregulatory moves. Repositioning, while most evident inEurope with 83% of respondents saying their company isrepositioning by country and 50% within the value chain, isnot confined to that continent. Half of Asia Pacificrespondents and a third of American respondents reportthat their company is repositioning along the value chain inresponse to regulatory initiatives.

Attitudes towards the regulator

Despite the challenges that can come from regulation, mostsurvey respondents are appreciative of the regulatory roleand many more disagreed than agreed with a set ofstatements critical of regulation. Only 32%, for example, feltthat their market had an ‘unclear or non-transparentregulatory process’ and only 30% complained that theretended to be ‘frequent changes to regulatory decisions andoutcomes’. These minority criticisms were slightly more feltby respondents in countries in Asia Pacific, the Middle Eastand Africa.

The less mature evolution of regulation in some of thesecountries was also reflected in a greater lack of support forregulation and lack of personnel with experience ofregulation within utility companies. For example, 44% ofMiddle East and African respondents felt that they lacked anexperienced regulatory resource in their company comparedwith only 14% of American respondents. The stepping up ofregulatory initiatives in Europe also appeared to be causingconcern among European respondents about theircompanies’ regulatory capacity – as many (41%) felt theylacked resource as felt their internal set-up was adequate.

Source: PricewaterhouseCoopers, Utilities global survey 2009

Figure 12: How are you responding to regulatory challenges?

2007 2008 2009

Operational initiatives to respond to regulatory framework & execution (eg unbundling, cost cutting, performance improvement etc) 76% 81% 93%

Industry-wide initiatives, aiming to improve regulatory framework & execution 76% 75% 81%

Reposition in the value chain, ie reducing or increasing presence in individual countries, following regulatory terms & conditions 32% 28% 43%

Reposition by country, ie reducing or increasing presence in individual countries, following regulatory terms & conditions 31% 38% 41%

We also tested respondent views about the political willbehind climate change action by asking whether highenergy prices would deter governments from increasingutility company environmental obligations. Morerespondents (40%) felt that high energy prices would diluteenvironmentalism than disagreed with this view (30%). Theremainder were undecided. Respondents from AsiaPacific, Middle East and African countries were most likelyto see a direct trade-off between energy prices andenvironmentalism – 50% of Asia Pacific respondents and54% of Middle East and African respondents believe thathigher prices would soften policy requirements.

14

Climate change

2009 will be a watershed year for climate changeregulation. Falling energy and carbon prices are castingdoubt on the viability of some renewable energy schemesand the economic downturn is testing commitment toclimate change mitigation. Governments have a chance toset a more certain framework for the industry. The firstyear of the Obama presidency, the direction of travel in therun-up to the December 2009 UN Climate Summit inCopenhagen and the outcome of those talks will all have avital bearing on the outlook for the power utilities industry.The political will of heads of government for a new climatetreaty and the extent of their ambition for clean energy willset the context for the sector for many years.

Whether governments have the political will to drivethrough measures to combat climate change is in somedoubt in the minds of our survey respondents. Asked if theeconomic recession would slow down responses toclimate change, 51% felt that it would have a high or veryhigh impact on a likely slowing of responses and 28% feltthat it would have a medium impact (see Figure 13). Only21% thought it unlikely that the recession would slowclimate change responses.

Figure 13: Will the economic downturn slow down responses to climate change?

Source: PricewaterhouseCoopers, Utilities global survey 2009

High or very high impact

Medium impact

Small or very small impact

51%

28%

21%

A watershed year for climate change policy

Global 15

Call for clarity

The importance of governments delivering greater clarityand developing an effective framework for thedevelopment of cleaner energy is highlighted by surveyresponses to a series of statements about renewableenergy and cleaner energy investment decisions (seeFigure 14). Nearly three-fifths of respondents (59%) feelthat their renewable energy investment programmes arebeing affected by the lack of clarity from governments onrenewable energy targets and financial support forrenewable energy. There were, however, strong regionalvariations in responses with European respondents muchhappier with the renewables policy framework.

The EU has committed to a 20% target of renewableenergy by 2020. Negotiations are taking place to translatethat overall target into individual country targets. Suchnegotiations will prove the testing ground for how far theEU target can be realised.

The Obama administration in the US has placedconsiderable emphasis on building ‘clean energy’measures into its economic stimulus package. TheObama-Biden New Energy for America plan has pledgedUS$150bn over 10 years to such measures and aims toproduce 10 per cent of the country’s electricity fromrenewable sources by 2012, and 25 per cent by 2025. Theplan was announced in late January 2009, part-waythrough our survey interviews, and may go some waytowards assuaging the 60% of American surveyrespondents who felt that lack of clarity was affecting theirinvestment decisions.

The more patchy approach to renewables targets in AsiaPacific, the Middle East and Africa, is reflected in largermajorities of survey respondents in these regions statingthat lack of policy clarity is holding them back. However,even in Europe, there is a need for greater certainty giventhe long-term timescales for investment. For example,58% of European respondents report that uncertainty overthe shape of phase 3 of the EU emissions trading schemepost-2012 is hampering their investment decisions.

Figure 14: Do you agree with the need for environmental regulatory clarity?

Agree 59%

Note: *European respondents onlySource: PricewaterhouseCoopers, Utilities global survey 2009

58%Agree

47%Agree

28%Agree

Lack of clarity from government on targets for renewable energy and long term financial support is impacting my investment decisions

Unsubsidised renewable generation is now commercially competitive against fossil fuel generation in my market

Uncertainty around phase 3 of ETS is impacting on my investment decisions *

Government policy is giving appropriate support to energy efficiency measures

Disagree

Disagree

Neither agree/disagree

Neither agree/disagree

25%Disagree

17%Neither agree/disagree

Disagree

Neither agree/disagree

23%

17%

51%

20%

28%

25%

Impact of climate change regulation

Utility executives in our survey also highlight the need formore effective specific policy mechanisms to restrictgreenhouse gas emissions (GHG). Even in Europe, wherethe EU emissions trading scheme has been in operationsince 2005, a third of respondents felt that GHGregulations had had no impact on their capital projectinvestment decisions (see Figure 15), although the impactof emissions trading was more tangible in Europeanresponses to a separate question on the scheme (seeEurope section). Around half of the respondents from AsiaPacific, the Middle East and Africa reported that suchregulation had no impact on them. Everywhere, fewrespondents said that GHG regulation had caused thecancellation of projects.

16

The importance of greater certainty on both targets andeconomic mechanisms to support renewable energy ishighlighted by the fact that, even coming off the back of aperiod of record high power prices, only 28% ofrespondents believe that unsubsidised renewable powercan compete commercially against fossil fuel generation.American respondents are especially likely to seerenewable power as uncompetitive – only 11% felt it couldcurrently compete without subsidy.

Moreover, the current financial crisis and constraints oncapital investment are exerting significant pressure oninvestment in renewable energy. Investments in wind, solar,and other evolving technologies have been among the firstto be cut. Alone out of the regions, respondents in AsiaPacific were more optimistic about the ability of renewablepower to hold its own in the marketplace.

Figure 15: How have existing and proposed GHG regulations and the carbon price affected major capital project investment decisions to date?

No impact 38%

Americas

Europe

Asia Pacific

MEA

Global

6%

3%

23%Revised projectspecification

7%Delayed orpostponed project

23%Acceleratedthe project

Cancelled project

Relocated project

Source: PricewaterhouseCoopers, Utilities global survey 2009

20 40 600 80 100%

Global 17

Energy savings and efficiency

As the responses in Figure 14 show, utility companysurvey respondents are less critical of regulatory supportfor energy efficiency measures than on other regulatorymatters, with only 28% of all respondents disagreeing withthe proposition that government policy is givingappropriate support. Again there are strong regionaldifferences. European and American respondents aremuch more likely to feel that energy efficiency support hasnot been developed sufficiently.

Energy efficiency is a critically important element in theenergy equation. Energy saved through efficiency is theonly source of ‘free’ energy that is available. However, ifsignificant reductions in per capita energy use are to occur,huge technological advancements will be required. As wedevelop more and better technologies, these efficiencieswill enable us to maximise precious energy resources,meet long-term energy challenges, and revolutioniseenergy usage in transportation and in industry.

Figure 16: Who should take the lead in achieving energy savings and efficiency?

End-users 46%

Americas

Europe

Asia Pacific

MEA

Global

3%

19%Utility companies

7%Oil & gas companies

23%Governments

Others

Source: PricewaterhouseCoopers, Utilities global survey 2009

20 40 600 80 100%

But who is to take the lead? Despite continuing initiatives,there is the danger that energy saving is something thatfalls between different stools and, indeed, only reallycomes to the fore when prices are high. Our surveyindicates the danger that this will continue to be the case.There is an increasing belief among respondents that it isnot for governments to take the lead (see Figure 16). Incontrast to last year’s survey, when 59% of all respondentsfelt that governments should take the lead, only 23% wereof this viewpoint in 2009. Instead, 46% felt the leadneeded to come from the end-users who would benefitfrom efficiency savings. However, unless prices are high, ithas to be questioned just how effective such an approachwill be.

18

Nuclear power expansion

Nuclear power is undergoing a renaissance as moregovernments change their policy stance on new nuclearexpansion. In February 2009, for example, Swedenannounced it will allow the construction of nuclear powerstations, ending a ban imposed after a 1980 referendum.Italy looks set to follow suit and the UK has alreadyannounced a programme of growth in its nuclear plants.This revival of nuclear power is reflected in 59% ofrespondents worldwide anticipating that nuclear powerwould have a significant impact in their market (see Figure17). More than half of these felt that it will have a high orvery high impact. Indeed, some respondents go further andbelieve that nuclear power should be given preference overrenewable energy in reducing CO2 emissions although theirviews are nearly balanced by those who would prioritiserenewable over nuclear power.

Figure 17: Nuclear maintains momentum

Source: PricewaterhouseCoopers, Utilities global survey 2009

High impact

Medium impact

Low impact

34%

25%

41%

Renaissance of nuclear power

Agree

Neither agree or disagree

Disagree

40%

35%

25%

New nuclear should be given preference over renewable energy as a means of reducing CO2

Nuclear power set to make a significant impact

Global 19

OperationsOur survey focused on three critical operationalareas for utility companies – deliveringtechnological improvements, limiting the growthof greenhouse gases and achievingimprovements in operational and environmentalperformance. Effective responses on thesechallenges will be vital for many aspects ofindividual company success, requiringinnovation from power utility companies.

Source: PricewaterhouseCoopers, Utilities global survey 2009

A focus on technology

Where will technological developments have most impactin the coming years? As Figure 18 shows, with regard togeneration and supply, respondents see technology havinga high but steady impact in areas such as wind andnuclear power. However, growing scores for energyefficiency, solar power, combined heat and power,distributed generation and combustible renewable andwaste generation indicate that these are seen as the likelyareas where technology will have the most new impact. All these developments will increase the likelihood oftechnology-driven competition highlighted earlier in Figure 10.

Figure 18: In which areas of generation and supply do you expect technological developments to have the greatest impact over the next 10 years in your market?

2007 2008 2009

Energy savings and efficiency 62% 79% 81%

Wind power plants 66% 62% 68%

Gas-fired plants 45% 69% 67%

Solar power plants 29% 54% 62%

Combined heat and power (CHP) plants 33% 52% 61%

Distributed generation 38% 49% 59%

Coal-fired plants 45% 49% 57%

Nuclear power plants 56% 57% 54%

Combustible renewable 33% 47% 54%

Waste incineration and landfill gas 26% 41% 51%

Micro-generation - - 45%

Geothermal 24% 40% 39%

Hydro power plants 31% 36% 36%

Oil-fired plants 11% 20% 35%

20

The introduction of new energy efficient technology is seen as a key enabler to major improvements in energyefficiency (see Figure 19). Subsidy of energy efficiencyequipment is also seen as important. The Obama-BidenNew Energy for America plan includes a US$1bn perannum federal grant programme “to identify and supportlocal manufacturers with the most compelling plans formodernizing existing or closed manufacturing facilities toproduce new advanced clean technologies”. However,unless prioritised by governments as part of stimulusprogrammes, the potential for substantial subsidyschemes is likely to be restricted because of the pressureson the public spending in many countries as a result of thecost of the various bail out and stimulus measures.

Figure 19: What are the key enablers for major energy efficiency improvements in your market?

New energy efficienttechnology

70%AmericasEuropeAsia PacificMEA

Global

Subsidy of energyefficient equipment

51%

The roll out ofsmart metering

48%

Regulating the energyperformance of buildings

46%

Distributed generation/virtualpower plants

36%

Professionally managedenergy contracting

36%

No really strong enablers 16%

Source: PricewaterhouseCoopers, Utilities global survey 2009

20 40 600 80 100%

Smart metering, which helps individual users to bettermonitor and control the way they use energy, is viewed asplaying a key role by American and Asia Pacific respondentsalthough, in Europe, despite the EU mandating an 80% roll-out of smart metering by 2020, only a minority ofrespondents saw it as important. European utilities appearsceptical about the ability of smart metering to deliver majorimprovements in energy efficiency. Smart metering in Europeis mainly predicated on other gains such as firm monthly bills,back and front office cost savings and improvements inoutage management. In contrast, smart metering in NorthAmerica and many Asia Pacific countries offers greater‘demand response’ advantages due to the very high summerair conditioning loads. Other measures that were identified asplaying a role in delivering efficiency gains included regulationof the energy performance of buildings and distributedgeneration. By placing power generation close to the enduser, distributed generation could play a part in reducingenergy lost in transmission and distribution systems.

Global 21

Limiting the growth of greenhouse gases

Expansion of renewable power sources and nuclear energyremain the principal routes by which respondents to oursurvey anticipate that GHG growth will be contained infuture decades (see Figure 20). Despite its potentialimportance in the generation mix, carbon capture andstorage (CCS) of emissions from coal-fired generationcomes lower down the list of expected technologicalimpacts over the next ten years. In the short-term,respondents are right to be cautious as, although thetechnology is available, it is expensive and is yet to beapplied to large-scale power plants. Current pilotdemonstration projects are still a few years away.Reference scenarios modelled by the IEA assumecommercialisation will not come until around 2020 (WorldEnergy Outlook 2008, International Energy Agency).

Source: PricewaterhouseCoopers, Utilities global survey 2009

However, it is anticipated that CCS will have a significantlong-term impact. Even in its less ambitious 550ppm policyscenario of stabilising GHGs, the IEA assumes that CCS willfeature in 101GW of the 323GW of additional coalgeneration capacity coming onstream between 2021 and2030, including 70% of additional capacity in OECD+countries. Thus, survey respondents’ expectation that thecoal carbon capture and storage picture in 2050 will be littledifferent from 2018 seems pessimistic and, indeed, slightlyalarming given the continuing importance of coal in thegeneration mix. The IEA’s reference scenario projects coal-fired generation to grow at two percent per annum to 2030,maintaining a 47% share of the power generation fuel mix.In the 550ppm policy scenario there is a substantialreduction in the growth of coal-fired generation but, even inthis scenario, it would still play a major role and, indeed, isprojected to be 26% higher by 2030 compared to currentlevels.

Figure 20: In which areas of generation and supply do you expect technological developments to have the greatest impact over the next 10 years in your market?

Over the next 10 years By 2050

2007 2008 2009 2007 2008 2009

Renewable power generation 47% 50% 54% 43% 54% 54%

Nuclear 43% 53% 45% 59% 58% 54%

Energy efficiency improvements 42% 42% 48% 38% 35% 46%

Displacement of new and existing coal fired capacity with gas-fired generation – 18% 16% – 14% 7%

Coal-fired generation with carbon capture & long-term geologic storage – 25% 20% – 26% 26%

Gas-fired generation with carbon capture & long-term geologic storage – 13% 17% – 13% 13%

Carbon capture and storage 26% – – 26% – –

Coal gasification 19% – – 21% – –

Gas-fired generation 22% – – 14% – –

22

Operational and environmental performance

Reduced demand for power in the economic downturnreinforces the importance of utility companies maximisingtheir operational performance. Our survey identified a rangeof opportunities for performance improvement (see Figure21). Better management of the supply chain, utilisation ofassets, billing operations and the delivery of large capitalprojects were seen as areas where high or very highperformance improvement could be achieved. Indeed, atleast half of survey respondents thought the scope forimprovement was high or very high in these areas.Relatively few felt there was little scope for performancegains. Supply chain management stood out with 62%identifying a high or very high potential for performanceimprovement and only 10% seeing little potential.

A company’s environmental performance is becomingincreasingly important from an investment point of view,particularly where carbon trading or other regulatorymechanisms impact investment feasibility and marketperformance. The senior utility company executives weinterviewed reported that communicating theirenvironmental performance was aiding their investorrelations (see Figure 22). Seventy per cent reported apositive impact, up from 57% last year, with very fewreporting a negative impact.

Figure 21: The scope for operational improvements

Source: PricewaterhouseCoopers, Utilities global survey 2009

High potential

Medium potential

Small potential

62%

28%

10%

Supply chain and logistics

High potential

Medium potential

Small potential

59%

30%

10%

Asset management

High potential

Medium potential

Small potential

45%

35%

20%

Finance operations

High potential

Medium potential

Small potential

54%

23%

23%

Billing operations

High potential

Medium potential

Small potential

49%

28%

23%

Delivering large construction projects

PeopleHaving the right people skills in place andusing these flexibly is critical to sustainingbusiness strategy and responding to marketchanges, especially as companies facetougher market conditions. Utility companieshave diverse workforces, often workingremotely and geographically dispersed. Whilethe economic downturn has helped to pushthe people factor slightly lower down theboardroom agenda, the issue of a limitedsupply of candidates with the right skillsremains a major challenge. In the long-term,companies are worried about decliningenrolment in university courses for thesciences and technologies, and expectdifficulties in recruiting and integratingyounger employees.

Global 23

Our survey confirmed continuing skills shortage concernsamong utility companies, particularly in the field of capitalproject management and technical expertise in the growthareas of renewable power and nuclear energy (see Figure23). Concern about lack of capital project managementexpertise was particularly expressed by Americanrespondents, reflecting the relative lack of infrastructureinvestment in recent years and the need to ramp up suchinvestment in the period ahead. In Europe, in contrast,anxiety about nuclear expertise stood out, again reflectingthe need to expand nuclear generation after a period inwhich nuclear power was largely off the developmentagenda.

Companies are deploying a range of strategies to respondto these concerns. In order to meet immediate needs, 70%of respondents said their companies were outsourcingspecific operations to specialists. A minority (41%) werealso looking to the international labour market and importingtalent from abroad. Looking to the longer term, 77% ofrespondents reported that their companies are stepping upclose co-operation with universities and academicinstitutions on course content and 54% were developingand running their own academies. In-house academies wereparticularly favoured by Asia Pacific respondents with 69%saying that they are taking this route.

Figure 22: What has been the impact of your environmental strategy & performance on your investors?

Source: PricewaterhouseCoopers, Utilities global survey 2009

Positive

Negative

No impact

70%

7%

23%

Positive

Negative

No impact

57%

13%

31%

2009

2008

Figure 23: In which sectors do you have a skills shortage?

Capital project managers 62%

Source: PricewaterhouseCoopers, Utilities global survey 2009

20 40 600 80 100%

20%

33%

Renewable generation - technical skills

Nuclear generation - technical skills

Electrical engineers

Energy traders

Gas engineers

IT professionals

Thermal generation - technical skills

Sales professionals

Procurement professionals

Marketing and communication professionals

HR professionals

61%

19%

32%

52%

38%

38%

29%

26%

29%

24

With survey respondents putting so muchemphasis on the need to balance short-term reaction to the financial crisis andeconomic downturn with a long-term focuson a world beyond recession, we decidedto hear the viewpoint of chief executivesand top leaders from power utilitycompanies in North America, Europe andAsia.

Dr. Jürgen Großmann is president and CEO of RWE AG, oneof Europe’s leading energy companies. Reflecting on thechanges of the past year, he says: “No one could havesuspected that we were about to face the biggest financialcrisis in the post-war era. Its extent and consequences stillcannot be predicted entirely”. He points out that one impactof the events of the past year has been that many people“now question the entire (banking) system and are secondguessing the fundamental principles of the market economy.State intervention in the economy has become the order ofthe day. Could we have imagined this a year ago? Certainlynot”.

The need to look ahead decades not years

Among the short-term impacts Dr. Großmann observes that“industrial energy consumption is on the decline, andcustomers are experiencing difficulty in making payments.Financing costs are on the rise and politicians areincreasingly inclined to regulate functioning marketprocesses more intensely”. However, notwithstanding thesefactors, and the profound nature of the changes wrought bythe financial and economic crisis, RWE emphasises theimportance of maintaining a long term perspective: “Weshould think in terms of decades, not years. This is why, inaddition to the demands currently placed on us, we alwayskeep a watchful eye on the fundamental challenges facingthe energy industry that have lasting effects. Majorinvestments must be made in Europe’s energyinfrastructure, especially in new generation capacity,electricity and gas grids, and gas storage facilities”.

Sources: BC Hydro and CPI – PwC interview. RWE – Do It. The New RWE, Annual Report 2008. CPI quotes also published in Risk, Responsibility & Opportunity: The CEO’s guide to climate action, PwC in conjunction with the Copenhagen Climate Council

Bob Elton, president & CEO of Canada’s BC Hydro, thethird largest electric utility in Canada, emphasises thatpower utility companies are used to facing short-termsituations that are different from the long-term outlook. Theimportant thing is maintaining focus on the long-term whileoptimising, and indeed looking for opportunities, in theshort-term. “The key objective of any leader must be to beclear about where you intend to be when the recession isover. You do have to adjust the pace a bit but the importantthing is to make sure that you’re facing in the right directionwhen it is over and it doesn’t have an impact on your longterm course”, says Elton.

Like RWE, BC Hydro has experienced reductions in demandfor power. “There are pluses and minuses”, Bob Elton pointsout. “It can give you more time and reduce risks. Forexample, there are opportunities to step up maintenanceprogrammes and other capital asset improvements. It givesus a chance to drive down costs, particularly on the capitalside, to take advantage of the market being a bit softer”.Skills shortages and an ageing workforce are among thekey challenges facing power utility companies in NorthAmerica and in many regions around the world. Again Eltonhighlights advantages that flow from the downturn:“Responding to the talent shortage has probably been a biteasier this year because of reduced hiring in the generaleconomy. We’re continuing to hire more young people toaddress demographic imbalances in the workforce”.

Climate change policy

While utility companies are used to planning for the long-term, the stakeholder landscape is more complex and canbe more short-term. “Our customers are less interested inthe long-term trends and, in some jurisdictions, governmentpolicy has a tendency to change pretty quickly towardsshort-term measures”, observes Elton. “A good example isenvironmental rules or legislation on climate change. It istempting for governments to lose focus on that which Ipersonally think would be a big mistake. I have seen that insome parts of the world, although not in our home market.Some form of carbon pricing is very important”.

maintaining a focus on long-term sustainabilityCEO viewpoint: 25

The importance of maintaining a focus on climate change isreiterated by Li Xiaolin, vice president of China PowerInvestment Corporation (CPI) and Executive Director,President of China Power International Holding Ltd. CPI wasestablished from part of the constituent businesses of theformer State Power Corporation of China and, by 2008, hadcontrollable installed generation capacity of 51990MW andequity installed capacity of 40116MW. Li Xiaolin believesthat “dealing with climate change now … will hopefullysecure a happy and healthy future for our children” andstresses that climate change needs to be a priority CEOissue as it “benefits business operations — by becomingcleaner and more efficient, companies should secureincreased profits over the long term”.

In Europe, much of RWE’s focus is on seeking a morecertain long-term policy context. “Political decisions in thefield of energy policy have a significant impact on theoptions available to the RWE Group to reduce CO2

emissions sustainably”, says RWE. As a utility with asignificant proportion of coal-burning generation, RWE islikely to be a key player in the development of carboncapture and storage (CCS) technology but stresses thatCCS needs more support from government: “We welcomethe rules for the promotion of CCS power plants. However,the planned subsidy is unlikely to be sufficient to realize theten to twelve demonstration plants envisaged by the EU.This will require further subsidies from the member states”.

In China, CPI’s Li Xiaolin makes the point that: “Stepping upscientific innovation and international cooperation will becrucial. Achieving development goals with minimum GHGemissions is a must-go direction for the future, which canonly be made possible through technological innovation andinternational cooperation”. She stresses that “efforts mustbe made to perfect the market mechanisms under theUnited Nations Framework Convention on Climate Change,with a focus on facilitating technological development andtransfer, and to ensure that consensus is reached quickly inthe international community. If these technologies can betransferred and deployed to developing countries atrelatively low cost, it may well help reduce large amounts ofGHG emissions”.

RWE is seeking to more than triple generation from itsrenewable subsidiary, RWE Innogy, to 4.5 gigawatts by2012. However, renewable plant is not sufficiently certain tobe the mainstay for delivering base-load power. RWE observes that “the most effective and affordable wayto avoid emissions is to extend the lifetimes of nuclearpower plants. Nuclear power generation emits practically nocarbon dioxide, and if nuclear power stations are shutdown, they will have to be replaced by higher-emissionfossil fuel-fired power plants. This is because renewables-based facilities are not capable of generating the sameamounts of base-load power. We could prevent up to anadditional 15 million metric tons of CO2 emissions per yearmerely by extending the lifetimes of our two Biblis units”.This is a key focus of RWE’s discussions with the Germangovernment.

A different kind of power sector

Looking further ahead, BC Hydro’s Bob Elton foresees aworld where the traditional model of large grid supply isturned on its head. He points to two key trends that willforce change. “In developed countries, it is becomingincreasingly difficult to build large infrastructure projects,whether that is power plant or transmission lines. Each oneis getting more challenging and that will put a premium ondemand side management and distributed generation”.Urbanisation is another key trend influencing a future wheredistributed energy plays more of a role. Elton points out: “In1800 only 3% of the world’s population lived in urban areas,by 1950 it was 30% and by 2007 it was just short of 50%.By 2050 it is projected to be 67%. Cities will have tobecome increasingly self-sufficient”.

“Distributed power sources will mean the grid will be theback-up service and not the primary means of delivery inthe future” predicts Elton. Distributed generation and arevolution in demand side management will, in turn, demanddifferent approaches by utility companies. “If you are anintegrated company then you’ll need to decide early onwhat kind of role you want to take in this new energy world.It will require new relationships with customers. Individualcustomers and communities of customers will be muchmore involved in developing their own solutions andcompanies will need to be very good at partnering andfacilitating that”.

26 The Americas

United States

The drive to deliver shareholder value

Utility company managers are looking with renewedurgency at the best options to more effectively manageand maintain ‘utility plant in service’. In terms of plantmaintenance and operations, companies are increasingtraining, retaining skills, implementing more effectiveprocurement practices, deploying standardised supplychain processes and systems, embracing portfoliomaximisation modelling techniques and improving plantperformance information. Managers recognise theexponential impact of an extra percentage point ofcapacity and are exploring all options to consistentlydeliver at higher levels. When asked about their strategyto enhance shareholder value, 67% of the USrespondents to our survey cited ‘improving capacityfactors’ as receiving a high focus in their companies (see US Figure 1).

Utility managers are also focusing more on fuel diversitythan they did in the past. This is cited as an importantroute to more shareholder value. Fifty-seven per cent ofrespondents reported that this was being given a ‘high’ or‘very high’ focus. The importance of greater fuel diversityis partly driven by the need to secure supply and avoidoverdependence on a narrow range of fuel sources, but isalso influenced by climate change concerns.

Similarly, utility managers are seeking new ways toprovide better and more efficient customer service withhalf of respondents giving this a high or very high focusas a means of delivering shareholder value. Investmentsare being made in new and information-rich customerbilling systems.

The United States moved into the downturn ahead of other world economies andhas seen some of the most dramatic events of the financial crisis. Historic USfederal government intervention, designed to prevent a more severe economiccrisis, has come from both the outgoing Bush administration and the new Obamapresidency. In this environment, fundamental operational matters have played aprominent role in US utility company priorities. Companies continue to focus onplant capacity and maintenance, customer service, long-term capital projects,rate case preparedness, and environmental/climate change readiness rather thanon mergers and acquisitions or other strategic restructuring moves.

United States 27

1 2 30

United States Figure 1: What is the focus of your company’s strategy forenhancing shareholder value?

4 5

Note: Average response. Rate where: 5 = greatest focus; 1 = least focusSource: PricewaterhouseCoopers, Utilities global survey 2009

Improving capacity factors

Increasing fuel diversity

Focused customer service initiatives

Developing new products and services

Spinning off a portion of thecompany to become a pure play

Outsourcing backoffice functions

Advanced metering infrastructure (AMI) and other smartmeter/grid technology is being either explored orimplemented by nearly every large-scale utility. Improvedcustomer cost and service information is being capturedand acted upon. Utility managers also appear more awareof additional costs that are often driven by a minority of thecustomer base, and they are more cognizant of theregulatory and customer care issues (and costs) that canarise when service levels do not achieve desired targets.

The ability to drive shareholder value is further complicatedby the difficulties in accessing the capital markets. Highperformance in the areas of focus highlighted in Figure 1are an integral part of demonstrating the ability to be anoutstanding operator and thus not further limiting access tocapital markets. Survey respondents are focused onoptimising working capital and other cash managementpractices in order to respond to the increased tightening ofthe capital markets (see US Figure 2). In addition to theareas of focus above, working capital optimisationpractices include such strategies as expense control,collateral management, maintaining headroom on existingcredit facilities, and hedging interest rates and commodityprice risk.

1 2 30

United States Figure 2: How will your company respond to the increased difficulties to access the capital markets?

4 5

Note: Average response. Rate where: 5 = greater focus; 1 = least focusSource: PricewaterhouseCoopers, Utilities global survey 2009

Optimise working capital and other cashmanagement practices and related information

Reduce the size of the current establishedconstruction programme

More aggressively pursueconsolidation opportunities

Partner with utilities and others to reducethe size of your individual company’s

construction capital requirements

28

A focus on infrastructure and majorconstruction

Large-scale construction and other capital projects beganincreasing at a rapid pace from 2006 onward. This trendhas continued into 2009 with the announcement of manynew projects, including an unprecedented level of focus onnuclear generation. Investment in infrastructure andconstruction of new generation head the list of strategicgrowth priorities for survey respondents in the coming year(see US Figures 3 and 4). Transmission congestion, carbonand other government environmental initiatives, increaseddemand in certain markets and the need for greaterreliability are among the issues most often cited by utilitymanagers as drivers of this investment.

There is also new interest in nuclear construction asutilities, independent power producers, and other industryparticipants develop generation to meet the demand fornew capacity. The sizable costs of such an environmentallydriven investment, allied with the related construction risk,mean companies and regulators will need to collaboratethoughtfully to ensure shareholder and ratepayer interestsare equitably maintained. There may be significant hurdlesto obtaining financing for new construction. In addition,even if financing is available, the resurgence ofconstruction has created a long lead time and increasingprices. These issues may further delay development.

1 2 30

United States Figure 3: What are your company’s strategic growth opportunities?

4 5

Note: Average response. Rate where: 5 = most strategic; 1 = least strategicSource: PricewaterhouseCoopers, Utilities global survey 2009

Investment in infrastructure (wires)

Constructing new generation

Investment in renewables

Energy trading

Promoting new products

Investment in transmission

United States 29

1 2 30

United States Figure 4: Over the next year, what will your company’s focus be on?

4 5

Note: Average response. Rate where: 5 = most focus; 1 = least focus*Question not asked in 2008Source: PricewaterhouseCoopers, Utilities global survey 2009

Acquiring/constructing new generation

Rate cases

Acquiring/constructing distribution infrastructure

Acquiring/constructing new transmission

20082009

*Developing new products and services

Mergers/acquisitions

Rising costs and regulatory transitionhave elevated rate cases to the topfocus of US survey respondents

Consistent with expectations and the focus on marketrecovery, regulators are continuing to allow lower returnsand rates than requested. The average return on equityreceived in 2008 rate cases was 10.28% versus an averagerequested rate of return of 11.13% (SNL Interactive).Mergers and acquisitions (M&A) are beginning to trendupward as compared with the prior year's responses. M&Ais likely to be an important part of many companystrategies as they respond to deregulated marketopportunities and the capital market environment.

Regulation and government – the new administration

The beginning of 2009 ushered in a new politicaladministration focused on embracing economic recovery.Utilities continue to experience rising costs for power,materials, labour, and other costs to provide services. Inaddition, transition periods and rate freezes have ended orare ending in many states. Rate cases are now the numberone focus for utility companies in the coming 12 months.Many utilities are filing rate cases for the first time in yearsand are requesting significant rate increases to cover theserising costs and capital investment.

1 2 30

United States Figure 5: What will be the biggest change in the US utility industry over the next five years?

4 5

Note: Average response. Rate where: 5 = most change; 1 = least changeSource: PricewaterhouseCoopers, Utilities global survey 2009

More environmental regulationsregarding GHG emissions

Greater share of non-US ownership

More merged companies

More pure-play companies (eg, generation only,transmission & distribution only)

20082009

More regulation

GHG emissions – the big change issue

Looking ahead, US utility company senior executives areincreasingly aware that legislation limiting GHG emissionsis forthcoming with Congress seeking a cap-and-tradesystem and the administration supporting moreEnvironmental Protection Agency (EPA) regulations andoversight. The vast majority (91%) of survey respondentsexpect ‘big’ or ‘very big change’ with more carbonemission regulation and none gave a ‘low change’ ratingto this aspect of regulation (see US Figure 5). In thisenvironment, power companies that own coal plants arereluctant to make investments in their existing or newassets as new regulations may significantly impact theirdecisions.

30

Further, US utility company senior executives see moremergers on the horizon – exactly half see a ‘big’ or ‘verybig’ change with more merged companies and a further42% give ‘medium change’ rating to more M&A. Mergersmay be necessary to raise capital to fund improvementsand new construction. Support for critical infrastructureand renewable energy may lead to less complicatedregulatory M&A approval. There is also a significantexpectation of more foreign ownership coming into thesector – 84% gave this scenario a medium to highprobability and none gave it a ‘little or no change’ rating.

1 2 30

United States Figure 6: What is your company’s strategy for dealing with climate change, carbon credits and other environmental issues?

4 5

Note: Average response. Rate where: 5 = most important; 1 = least importantSource: PricewaterhouseCoopers, Utilities global survey 2009

Energy efficiency (AMI, smart grids)

Renewables investment

Advanced coal generation investment

Nuclear investment

Carbon capture and sequestration

Purchase credits

To manage environmental demands, utility managers planto make a range of technological and generationinvestments, headed by ‘energy efficiency’ technologiessuch as AMI (see US Figure 6), which 83% ofrespondents viewed as ‘very important’ or ‘mostimportant’ with the remainder rating it as ‘mediumimportance’. Renewables investment is also important. An increasing number of power deals have been forrenewable assets or technology with wind energy leadingthe trend. Growth in ‘renewables’ will be fuelled by taxincentives and public sentiment for clean energy.

United States 31

Nuclear license applications are on the riseand pro-nuclear sentiment is growing

The new administration has pledged to significantlyincrease the production of alternative energy in the nextfew years to create a clean energy economy. A third ofUS survey respondents were attaching a ‘mostimportant’ rating to renewable investment with a furtherthird rating of medium or high importance to theircompanies’ strategy for dealing with climate change.Significantly, half of survey respondents highlightednuclear investment as ‘most important’ or ‘veryimportant’ to their companies’ climate change response.

United States Figure 7: Is your utility company’s stock appropriately valued?

Source: PricewaterhouseCoopers, Utilities global survey 2009

Yes 25%

Too low 67%

2009

Yes 76%

Too low 24%

2008

Don’t know 8%

The impact of IFRS

Most of the world already talks to investors andstakeholders about corporate financial performance inthe language of International Financial ReportingStandards (IFRS). In addition, US investors buysecurities issued by foreign companies that report theirinformation using IFRS. The Securities and ExchangeCommission (SEC) continues to drive toward theadoption of IFRS to allow US companies to competefairly against foreign companies for capital, as theirfinancial information would be presented on aconsistent basis of accounting.

32