Industrialisation for job creation and shared prosperity · Uganda National Budget 2019/20 June...

27

Industrialisation for job creation and shared prosperity Uganda National Budget Bulletin 2019/20 June 2019

Transcript of Industrialisation for job creation and shared prosperity · Uganda National Budget 2019/20 June...

Industrialisation forjob creation and sharedprosperityUganda National BudgetBulletin 2019/20

June 2019

PwC

Uganda National Budget 2019/20 June 2019

2

In this bulletin…

1. Economy 3

2. Fiscal performance 8

3. Tax amendments 11

Corporate income tax 11

Value Added Tax 14

Excise duty 17

Customs duty 18

Stamp duty 20

Tax Procedures Code 21

4. East Africa highlights 22

PwC

Uganda National Budget 2019/20 June 2019

3

Global Economic Growth

According to the IMF’s April 2019 WorldEconomic Outlook (WEO), global growthmomentum slackened in 2018 to 3.6%from 3.8% in 2017, showing greater thanexpected weaker performance in someeconomies, notably Europe and Asia.

The global economy is projected to growat an even lower rate of 3.3% in 2019compared to previous years. Globalgrowth will start to level off in the secondhalf of 2019 to achieve 3.6% in 2020based on on-going build- up of policystimulus in China, recent improvement inglobal financial market and, stabilizationof conditions and declining pressures ongrowth in the Euro area and emerging

markets.

Beyond 2020, global growth is set tosettle at about 3.6%

According to the IMF, growth acrossemerging markets and developingeconomies is projected to stabilizeslightly below 5%.

For some regions, the outlook isconvoluted by a combination of structuralbottlenecks, slower advanced economygrowth and, in some cases, high debtand tighter financial conditions.

These factors, alongside subduedcommodity prices and civil strife orconflict in some cases, contribute tounresponsive medium-term prospects forLatin America; the Middle East, NorthAfrica, and Pakistan region; and parts ofSub-Saharan Africa

The EconomyGlobal

%3.6

2.2

4.5

3.3

1.8

4.4

3.6

1.7

4.8

0

1

2

3

4

5

6

Global Economy AdvancedEconomies

Emerging Marketsand Developing

Economies

2018 2019 2020

GDP for World Economies

Source: IMF 2019 World Economic Outlook

PwC

Uganda National Budget 2019/20 June 2019

4

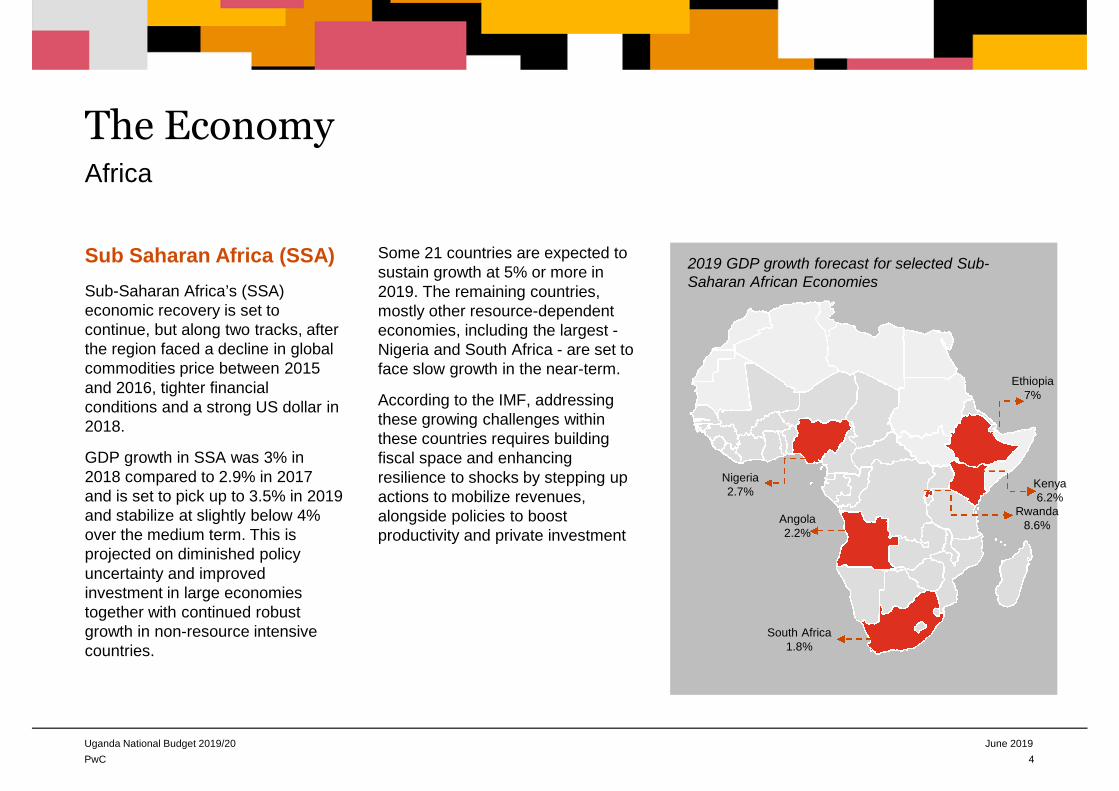

Sub Saharan Africa (SSA)

Sub-Saharan Africa’s (SSA)economic recovery is set tocontinue, but along two tracks, afterthe region faced a decline in globalcommodities price between 2015and 2016, tighter financialconditions and a strong US dollar in2018.

GDP growth in SSA was 3% in2018 compared to 2.9% in 2017and is set to pick up to 3.5% in 2019and stabilize at slightly below 4%over the medium term. This isprojected on diminished policyuncertainty and improvedinvestment in large economiestogether with continued robustgrowth in non-resource intensivecountries.

Some 21 countries are expected tosustain growth at 5% or more in2019. The remaining countries,mostly other resource-dependenteconomies, including the largest -Nigeria and South Africa - are set toface slow growth in the near-term.

According to the IMF, addressingthese growing challenges withinthese countries requires buildingfiscal space and enhancingresilience to shocks by stepping upactions to mobilize revenues,alongside policies to boostproductivity and private investment

The EconomyAfrica

Nigeria2.7%

Angola2.2%

Ethiopia7%

Kenya6.2%

South Africa1.8%

Rwanda8.6%

2019 GDP growth forecast for selected Sub-Saharan African Economies

PwC

Uganda National Budget 2019/20 June 2019

5

The EconomyEast African Community

According to the African DevelopmentBank’s 2019 African Economic Outlook,East Africa is the fastest growing regionof the continent with a robust GDPforecast of 5.9% from an estimated5.7% in 2018. However, the regionalaverage is disguised by substantialvariation across countries.

The countries with the highesteconomic growth are Rwanda,Tanzania and Kenya. The regionhowever continues to face variousdownside risks that could undermineeconomic growth and developmentprospects. Major risks are agriculture’ssusceptibility to the impulses of nature,heavy reliance on primary commodityexports, rising oil prices, persistentcurrent account deficits and relatedincreases in external indebtedness.

of exports and significantly higher thanthe continental average.

The Continental Free Trade Area(CFTA), launched in Kigali in March2018, is the latest regional integrationinitiative. The tripartite free trade areainvolving COMESA, EAC, and theSouthern African DevelopmentCommunity was an importantmotivation for the CFTA, especially inEast and Southern Africa.

These initiatives are believed to beadvancing regional integration in EastAfrica and will accelerate inter-regionaltrade.

0

1

2

3

4

5

6

7

2 0 1 7 2 0 1 8 2 0 1 9( E S T )

2 0 2 0( E S T )

Africa North Africa

West Africa Central Africa

East Africa Southern Africa

GDP growth by region 2017 to 2020

Source: Africa development bank- East AfricaEconomic Outlook

Whilst international trade within Africa remainslow averaging at about 14.5% and roughlyunchanged over the past five years, intra-EACtrade is the highest among all regionaleconomic communities in Africa - above 20%

PwC

Uganda National Budget 2019/20 June 2019

6

Ease of doing business score EAC countries have continued topush the frontiers of reforms morebroadly. The World Bank’s 2019Doing Business report showed theprogress made by sub-SaharanAfrica among reforming economies.

The 2019 report showed that theEAC has continued to excel,accounting for one-third of allbusiness regulatory reforms.Uganda performed slightly abovethe regional average while SouthSudan and Burundi weresignificantly below average.Rwanda continues to lead the way.

The EconomyEase of doing business in East Africa

77.88

70.31

57.06

53.63

47.41

35.34

56.94

0 20 40 60 80 100

RWANDA (RANK 29)

KENYA (RANK 61)

UGANDA (RANK 127)

TANZANIA (RANK144)

BURUNDI (RANK 168)

SOUTH SUDAN (RANK 185)

REGIONAL AVERAGE (RANK 119)

Source: World Bank Doing Business Report, 2019

Note: An economy’s ease of doing business score is reflected on a scale from 0 to 100, where 0 represents the

lowest and 100 represents the best performance. The rank is out of 190 countries..

PwC

Uganda National Budget 2019/20 June 2019

7

Economic performanceThe economy sustained its recovery inFY18/19, growing by 6.1%. The economyis projected to grow by 6.3% in FY19/20and continues to bounce from the lowgrowth of 3.9% in 2017, mainly driven byincreased private and public sectoractivity across all sectors and improvedweather conditions.

Inflation remained stable at 3.1% (10months to April 2019), due to increasedfood supplies in the markets, relativelystable exchange rate and effective co–ordination of monetary and fiscal policies.Domestic revenue collection increasedsignificantly with the ratio of domesticrevenue to GDP estimated at 15.2%compared to 14.4% achieved last year.

Government prioritiesThe government’s current prioritiesinclude:

• Expanding the industrial base of theeconomy;

• Exploiting natural resourceendowments with environmentalprotection in mind; and

• Providing affordable financing forproduction and business.

Economic drivers FY19/20

The government has identified theeconomic drivers to include:

• Peace, security, good governanceand an efficient judicial system;

• Reliable, efficient and affordableelectricity supply;

• Water transport and communicationsinfrastructure;

• A healthy, well educated and skilledworkforce; and

• An effective government machinery.

The EconomyUganda

%

Source: Background to Budget Chapters 4 & 7

FY 17/18Actual

FY 18/19Projected

GDP Growth 6.2% 6.1%

Domestic revenue as% of GDP (incl. oil)

14.4% 15.2%

Total Govt spending inUGX

20.1 trillion 24.3 trillion

Expenditure as % ofGDP

20.1% 22.1%

Budget deficit as % ofGDP (incl. grants)

-4.9% -5.8%

Public debt in USD USD 10.7b(June 18)

USD 12.1b(June 19)

Public debt as % ofGDP (nominal)

41.5% 42.2%

Headline inflation 3.4% 3.1%(10 mths)

Key economic indicators

PwC

Uganda National Budget 2019/20 June 2019

8

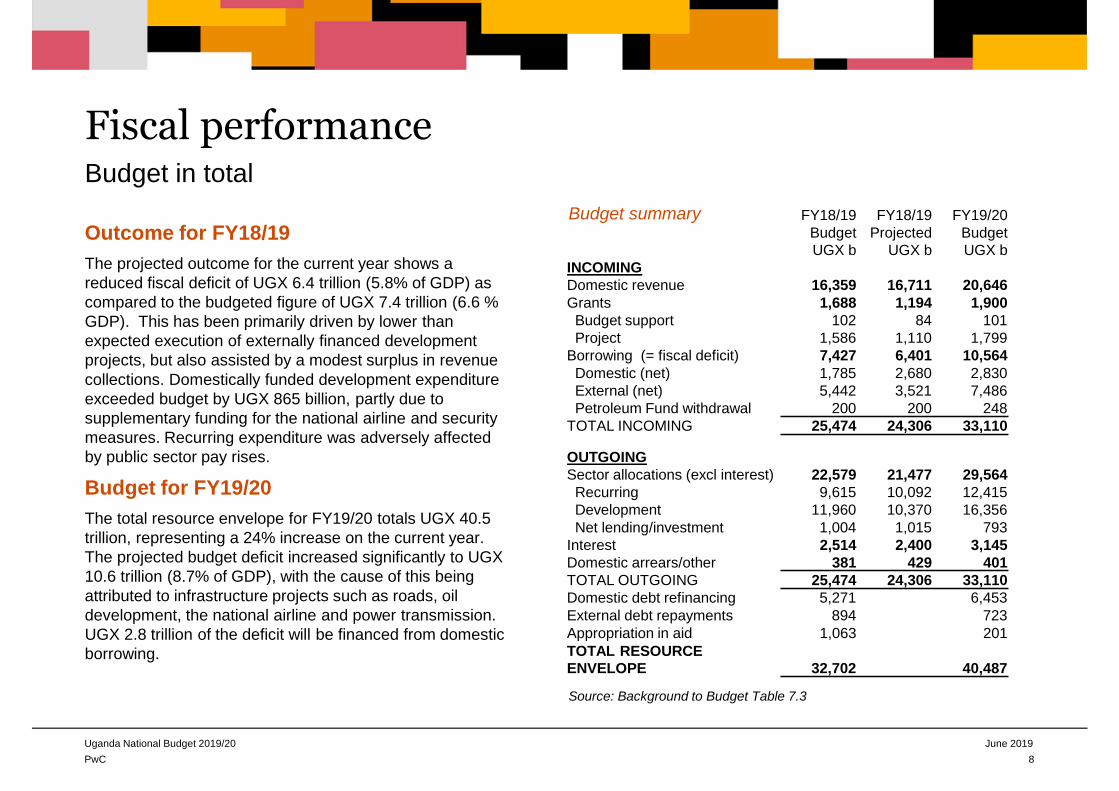

Outcome for FY18/19

The projected outcome for the current year shows areduced fiscal deficit of UGX 6.4 trillion (5.8% of GDP) ascompared to the budgeted figure of UGX 7.4 trillion (6.6 %GDP). This has been primarily driven by lower thanexpected execution of externally financed developmentprojects, but also assisted by a modest surplus in revenuecollections. Domestically funded development expenditureexceeded budget by UGX 865 billion, partly due tosupplementary funding for the national airline and securitymeasures. Recurring expenditure was adversely affectedby public sector pay rises.

Budget for FY19/20

The total resource envelope for FY19/20 totals UGX 40.5trillion, representing a 24% increase on the current year.The projected budget deficit increased significantly to UGX10.6 trillion (8.7% of GDP), with the cause of this beingattributed to infrastructure projects such as roads, oildevelopment, the national airline and power transmission.UGX 2.8 trillion of the deficit will be financed from domesticborrowing.

Fiscal performanceBudget in total

FY18/19BudgetUGX b

FY18/19Projected

UGX b

FY19/20BudgetUGX b

INCOMINGDomestic revenue 16,359 16,711 20,646Grants 1,688 1,194 1,900Budget support 102 84 101Project 1,586 1,110 1,799

Borrowing (= fiscal deficit) 7,427 6,401 10,564Domestic (net) 1,785 2,680 2,830External (net) 5,442 3,521 7,486Petroleum Fund withdrawal 200 200 248

TOTAL INCOMING 25,474 24,306 33,110

OUTGOINGSector allocations (excl interest) 22,579 21,477 29,564Recurring 9,615 10,092 12,415Development 11,960 10,370 16,356Net lending/investment 1,004 1,015 793

Interest 2,514 2,400 3,145Domestic arrears/other 381 429 401TOTAL OUTGOING 25,474 24,306 33,110Domestic debt refinancing 5,271 6,453External debt repayments 894 723Appropriation in aid 1,063 201TOTAL RESOURCEENVELOPE 32,702 40,487

Budget summary

Source: Background to Budget Table 7.3

PwC

Uganda National Budget 2019/20 June 2019

9

Fiscal performanceDomestic revenue

Outcome for FY18/19

The URA is expecting to exceed its revenue target for theyear, with a surplus UGX 353 billion (2.2%)

The surpluses mainly arise from corporate income tax,PAYE, and VAT (both domestic and imports). A componentof the surplus arises from improved recoveries of tax arrears,with UGX 456 billion being recovered in the period to April2019.

The main shortfall arose in local excise duty, largelyattributed to a deficit in collection of the new OTT tax whichis blamed on the use of virtual private networks. Collectionsof the new 0.5% excise duty on mobile money withdrawalsare stated to be UGX 45 billion ahead of target (up to April2019)

FY18/19TargetUGX b

FY18/19Projected

UGX bSurplusUGX b

Surplus%

Tax revenue 15,939 16,181 242 1.5%

Non tax revenue 420 531 111 26.4%

Total revenue 16,359 16,712 353 2.2%

Budget for FY19/20

The URA is charged with collecting total revenue of UGX 20.6 trillionin the coming year, representing an increase of 23.5%. The increasein tax revenue is expected to be largely driven by positive economicconditions and improved tax administration measures, rather thanspecific new taxes or increased tax rates. A large part of the increasein non tax revenue arises from appropriation in aid, which the URAwill now be collecting directly on behalf of the respective governmentdepartments/agencies.

The revenue performance for the two years to FY19/20 meets thetargeted annual improvement in the revenue to GDP ratio of 0.5%,with a medium-term target of 18% under the Domestic RevenueMobilisation Plan.

FY17/18ActualUGX b

FY18/19Projected

UGX b

FY19/20BudgetUGX b

IncreaseFY19/20 v.

prior year%

Tax revenue 14,076 16,181 18,877 16.7%

Non tax revenue 431 531 1,571 195.9%

Oil revenues 0 0 198

Total domestic revenue 14,507 16,712 20,646 23.5%

% of GDP

Tax revenue 14.0% 14.7% 15.5% 0.8%

Domestic rev. excl. oil 14.4% 15.2% 16.8% 1.6%

Domestic rev. incl. oil 14.4% 15.2% 17.0% 1.8%

PwC

Uganda National Budget 2019/20 June 2019

10

Fiscal performanceGovernment spending

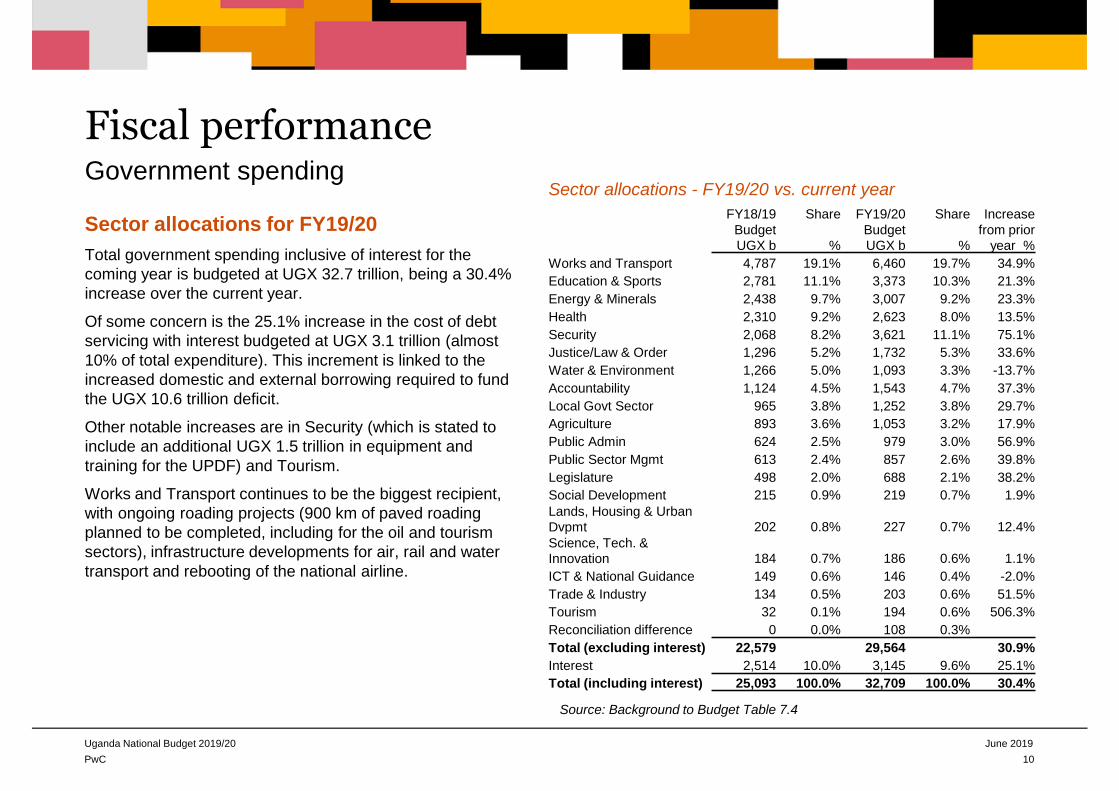

Sector allocations for FY19/20

Total government spending inclusive of interest for thecoming year is budgeted at UGX 32.7 trillion, being a 30.4%increase over the current year.

Of some concern is the 25.1% increase in the cost of debtservicing with interest budgeted at UGX 3.1 trillion (almost10% of total expenditure). This increment is linked to theincreased domestic and external borrowing required to fundthe UGX 10.6 trillion deficit.

Other notable increases are in Security (which is stated toinclude an additional UGX 1.5 trillion in equipment andtraining for the UPDF) and Tourism.

Works and Transport continues to be the biggest recipient,with ongoing roading projects (900 km of paved roadingplanned to be completed, including for the oil and tourismsectors), infrastructure developments for air, rail and watertransport and rebooting of the national airline.

FY18/19BudgetUGX b

Share

%

FY19/20BudgetUGX b

Share

%

Increasefrom prior

year %

Works and Transport 4,787 19.1% 6,460 19.7% 34.9%

Education & Sports 2,781 11.1% 3,373 10.3% 21.3%

Energy & Minerals 2,438 9.7% 3,007 9.2% 23.3%

Health 2,310 9.2% 2,623 8.0% 13.5%

Security 2,068 8.2% 3,621 11.1% 75.1%

Justice/Law & Order 1,296 5.2% 1,732 5.3% 33.6%

Water & Environment 1,266 5.0% 1,093 3.3% -13.7%

Accountability 1,124 4.5% 1,543 4.7% 37.3%

Local Govt Sector 965 3.8% 1,252 3.8% 29.7%

Agriculture 893 3.6% 1,053 3.2% 17.9%

Public Admin 624 2.5% 979 3.0% 56.9%

Public Sector Mgmt 613 2.4% 857 2.6% 39.8%

Legislature 498 2.0% 688 2.1% 38.2%

Social Development 215 0.9% 219 0.7% 1.9%Lands, Housing & UrbanDvpmt 202 0.8% 227 0.7% 12.4%Science, Tech. &Innovation 184 0.7% 186 0.6% 1.1%

ICT & National Guidance 149 0.6% 146 0.4% -2.0%

Trade & Industry 134 0.5% 203 0.6% 51.5%

Tourism 32 0.1% 194 0.6% 506.3%

Reconciliation difference 0 0.0% 108 0.3%

Total (excluding interest) 22,579 29,564 30.9%

Interest 2,514 10.0% 3,145 9.6% 25.1%

Total (including interest) 25,093 100.0% 32,709 100.0% 30.4%

Source: Background to Budget Table 7.4

Sector allocations - FY19/20 vs. current year

PwC

Uganda National Budget 2019/20 June 2019

Our Tax Watch of April 2019 set out theexpected tax changes as reflected in the2019 Tax Bills. The final amendmentshave since been passed by Parliamentand are awaiting Presidential assent. Wesummarise below the amendments thatare expected to come into effect on 1July 2019.

Corporate Income Tax

Ring fencing of rental income

The proposal for companies earningrental income from more than one rentalproperty to account for the income andexpenses on each property separatelywas rescinded.

Accordingly companies earning rentalincome from multiple properties willcontinue to be entitled to offset the profits

and losses from each property.

Tax Incentives for Investors

The 2018 exemptions linked to industrialparks and free zones have beenamended or extended as follows:

• Ten year exemption for income of adeveloper from letting or leasingfacilities in an industrial park or freezone with an investment of USD 50million or more. The amendmentincreases the existing exemptionperiod (from five years) and reducesthe investment threshold (from USD100 million).

• Ten year exemption for income of anoperator within an industrial park orfree zone, or other person carrying onbusiness outside the industrial park orfree zone, whose investment capital isat least USD 10 million for a foreigneror USD 2 million for citizens. Theamendment increases the existingexemption period (from five to tenyears), and reduces the investment

threshold (from USD 15 million to USD10 million for foreigners and from USD 5million to USD 2 million for citizens).

• Introduction of an exemption for incomeof an operator within an industrial park orfree zone, or an operator who owns asingle factory or other business outsidethe industrial park of free zone, whoseinvestment capital is at least USD 10million for a foreigner or USD 2 millionfor a citizen. The exemption is limited tothe following activities:

– Processing of agricultural goods;

– manufacture or assembly medicalappliances, building materials,automobiles, household appliances;

– manufacture of furniture;

– vocational or technical institutes;

– logistics and warehousing,information technology or commercialfarming.

11

Tax amendmentsCorporate income tax

PwC

Uganda National Budget 2019/20 June 2019

12

• Other requirements are that 50% ofraw materials should be locallysourced, subject to availability, andthe operator should employ at least60% citizens. This new exemptionfavours industrialisation using localmaterials.

Definition of citizen

Linked to the tax incentives above, thereis a new definition of the term “citizen” tomean:

a) a natural person who is a citizen of aPartner State of the East AfricanCommunity (EAC);

b) a company or body incorporatedunder the laws of a Partner State ofthe EAC in which at least 51% of theshares are held by a person who is acitizen.

A citizen was not defined before, andtherefore was only expected to captureUgandan nationals and businesses.

The proposed definition is also included inthe Amendment Acts for VAT, excise dutyand stamp duty.

EAC citizens and entities will thereforealso benefit from preferential benefits suchas lower capital investment requirementsand duty exemptions on specified itemsunder the respective Acts. The inclusion islinked to the commitments in the EACtreaty on equal treatment of goods,services and persons from partner states.

TIN requirement forgovernment licences

Every local authority, governmentinstitution or regulatory body will nowrequire to see a Tax Identification Number(TIN) before issuing a licence or any formof authorisation to any person forpurposes of conducting a business inUganda. This is intended to catch personscarrying on trading activity without taxregistration, and will apply for both start-ups and annual renewals

12

Tax amendmentsCorporate income tax

Definition of beneficial ownerto restrict tax treaty benefits?

A new provision defines a “beneficialowner” to mean a natural person (i.e. anindividual). Coupled with a relatedamendment to section 88(5), thisappears to mean that tax treaty benefitswill only be available to foreignindividuals (and consequently will not beavailable to foreign entities). Theintention behind this change is unclearand we await to see how it will beapplied in practice.

Exemption for interest paidon “infrastructure bonds”

This new exemption applies to listedbonds, notes or other similar securitiesused to fund public infrastructure orsocial services with a maturity period ofat least ten years. This is designed toencourage infrastructure development

PwC

Uganda National Budget 2019/20 June 2019

Exclusion of financial sectorfrom interest restriction

Financial institutions and insurancecompanies will be excluded from theinterest deduction limitation in section 25(whereby interest deductibility is limitedto 30% of Tax EBITDA). This is awelcome amendment as the financialservices sector has been advocating forthe pre-July 2018 position to be restored.The previous exclusion appears to havebeen an oversight when the new ruleswere introduced last year, this changerestores the previous status quo.

Turnover tax on loss-makers

A proposed amendment seeking tointroduce a 0.5% turnover tax ontaxpayers returning assessed losses fora period exceeding seven years wasrescinded. A similar measure wasrejected in 2018.

WHT on purchase of abusiness or business asset

A resident person who purchases abusiness or business asset will berequired to withhold tax at a rate of 6%on the gross payment.

This change will impact on business andproperty acquisitions by businesses. Theterm “business asset” is defined toinclude any asset for use in a businessbut it is not clear if this is to bedetermined from the point of view of thevendor or purchaser (we would expectthe latter).

Such transactions will not be eligible forexemption under the existing WHTexemption list. This new withholding taxwill apply to all resident purchasersnotwithstanding that many taxpayers arealready required to deduct 6% WHT onpurchases of goods and services.

Reduced 10% WHT on longterm government securities

Government securities will now besubject to a reduced 10% WHT rate ongovernment securities with a maturityperiod of at least 10 years. This incentivewill apply to both local and foreigninvestors and is aimed at encouraginginvestors to lend to the government on along term basis.

Short term (less than 10 year)government securities will continue to besubject to the existing WHT rate of 20%.

Repeal of 1% WHT onagricultural supplies

The 1% WHT on agricultural suppliesintroduced in 2018 has been repealed,and such supplies are now alsospecifically exempted from the general6% WHT on goods and services.

13

Tax amendmentsCorporate income tax

PwC

Uganda National Budget 2019/20 June 2019

14

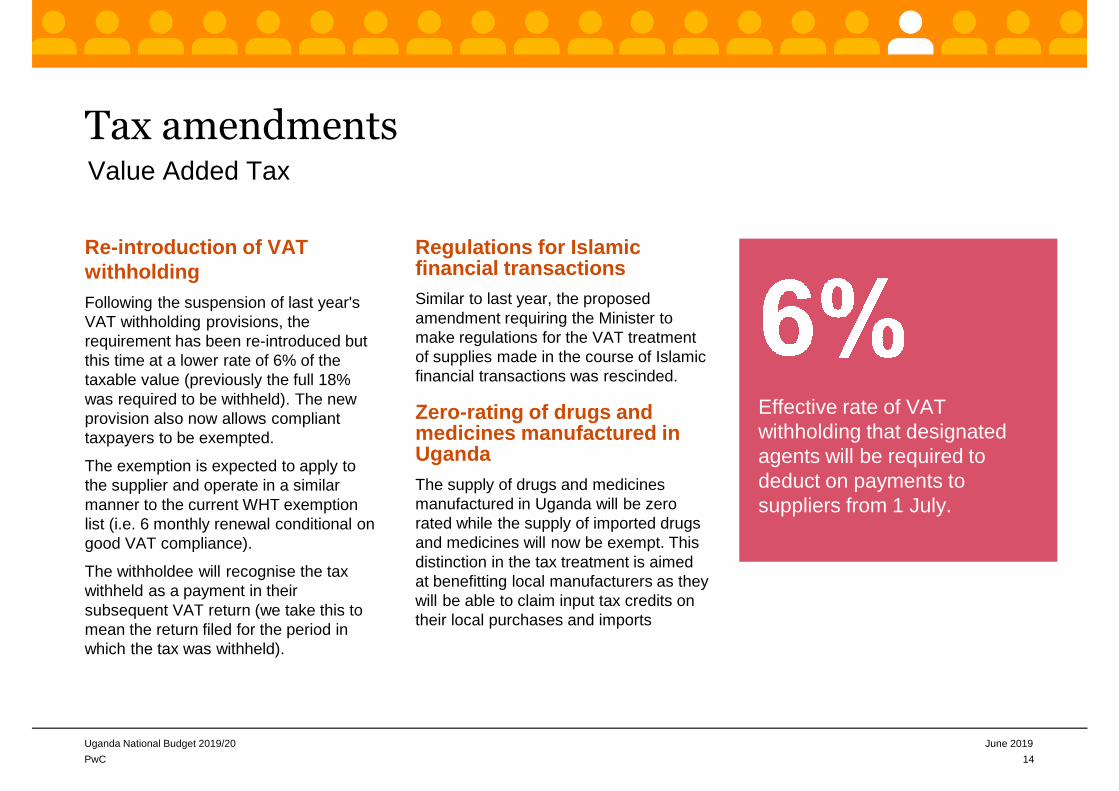

Re-introduction of VATwithholding

Following the suspension of last year'sVAT withholding provisions, therequirement has been re-introduced butthis time at a lower rate of 6% of thetaxable value (previously the full 18%was required to be withheld). The newprovision also now allows complianttaxpayers to be exempted.

The exemption is expected to apply tothe supplier and operate in a similarmanner to the current WHT exemptionlist (i.e. 6 monthly renewal conditional ongood VAT compliance).

The withholdee will recognise the taxwithheld as a payment in theirsubsequent VAT return (we take this tomean the return filed for the period inwhich the tax was withheld).

Regulations for Islamicfinancial transactions

Similar to last year, the proposedamendment requiring the Minister tomake regulations for the VAT treatmentof supplies made in the course of Islamicfinancial transactions was rescinded.

Zero-rating of drugs andmedicines manufactured inUganda

The supply of drugs and medicinesmanufactured in Uganda will be zerorated while the supply of imported drugsand medicines will now be exempt. Thisdistinction in the tax treatment is aimedat benefitting local manufacturers as theywill be able to claim input tax credits ontheir local purchases and imports

Tax amendmentsValue Added Tax

Effective rate of VATwithholding that designatedagents will be required todeduct on payments tosuppliers from 1 July.

PwC

Uganda National Budget 2019/20 June 2019

15

Exempt supplies

The list of exempt supplies in the SecondSchedule has been expanded to includethe following:

• aircraft insurance services;

• rice mills;

• agricultural sprayers;

• drugs and medicines not manufacturedin Uganda;

• imported mathematical sets andgeometry sets used for technical andvocational education;

• woodworking machines;

• welding machines and sewing machines.

Tax amendmentsValue Added Tax

In addition the thresholds for the existingVAT exemption introduced last year havebeen reduced from USD 15 million to USD10 million (for foreigners) and from USD 5million to USD 2 million (for citizens) tomatch the thresholds for income tax andother incentives. Specifically this applies tothe supply of services to conduct afeasibility study and design, the supply oflocally produced materials for theconstruction of a factory or a warehouseand the supply of locally produced rawmaterials and inputs or machinery andequipment to an operator within anindustrial park or free zone, or to anoperator who owns a single factory orother business outside the industrial parkor free zone, for investment in a range ofspecific manufacturing or service sectors.

• Imported crayons, coloured pencils,lead pencils, rulers, erasers, serials,technical drawing sets, educationalcomputer tablets, educationalcomputer applications or labchemicals for teaching sciencesubjects used in educational services.

Tax incentives for investors

The Act introduces a new tax incentivethat exempts services for feasibilitystudies, design and construction, locallyproduced materials for construction ofpremises or infrastructure and furnitureor fittings for technical or vocationalinstitute operators whose investmentcapital is at least USD 10 million in caseof foreigners or USD 2 million in case ofcitizens.

PwC

Uganda National Budget 2019/20 June 2019

16

Public International Organisations

The United Nations Entity for Gender Equality andthe Empowerment of Women (UN Women) hasbeen added to the list of Public InternationalOrganisations in the First Schedule to the VATAct. This means that the entity will be entitled toexemption or refund of VAT on imports and localpurchases.

16

Tax amendmentsValue Added Tax

PwC

Uganda National Budget 2019/20 June 2019

17

Regulations for Islamicbanking

The proposal for the Minister to makeRegulations prescribing the equivalentexcise duty treatment of supplies madein the course of Islamic financialtransactions was rescinded.

Registration requirement

The current licensing requirements underthe Excise Duty Act have been replacedwith a new process for annualregistration of the premises ofmanufacturers, importers, and providersof excisable goods and services.

The general registration approach issimilar to the current licensing processbut reflects the following changes:

• removal of application and renewalfees for a license;

• exclusion of retailers and retailingactivity;

• provides a timeframe within which aregistered person should apply forrenewal of the certificate ofregistration, being 30 days before theexpiry of the existing certificate;

• imposition of a fine of UGX 400,000for each day that a person operateswithout a certificate of registration.

Interest on unpaid dutyThe Act introduces a uniform interestpenalty of 2% per month, compounded,on late payment of all excise duty.Currently there is an interest penalty onunpaid duty in relation to manufacturedor imported goods, but no penalty appliesto excisable services.

Duty rates

Contrary to normal expectation, therehave been no adjustments to the dutyrates. The proposed rate reduction fornon-alcoholic beverages (from 12% to11%) was rescinded.

Incentives for InvestorsThere is new exemption for materialsused in the construction of premises andother infrastructure, machinery andequipment or furnishings and fittings fortechnical or vocational institute operatorswhose investment capital is at least USD10 million (foreigners) or USD 1 million(citizens).

There are also amendments to align thecapital investment thresholds for theexisting duty exemptions on constructionmaterials for developers of industrialparks and free zones (reduced from USD100 million to USD 50 million) and forinvestors in certain sectors (reduced toUSD 10 million and USD 1 million forforeigners and citizens respectively).

Tax amendmentsExcise duty

PwC

Uganda National Budget 2019/20 June 2019

Protective rate increases

To support local manufacturers, importduties have been increased on thefollowing products for a period of one year.

Duty rate of 35% instead of 25%

• Imported television sets

• Imported toys

• Granite, marble and clay (ceramic) tiles

• Tomato paste and other preservedtomatoes

• Imported toothpaste and other mouthwash preparations

• Shoe polish

• Wigs, false beards, eyebrows, andeyelashes, etc, human hair

• Doors, windows, and their frames andthresholds for doors of iron and steel andplastic polymers, furniture and its parts;

• Chewing gum, chocolates, sweets

Tax amendmentsCustoms duty

• Mixes and doughs for thepreparation of bakers’ wares

• Tarpaulins

• Cartons, boxes, cases, bags andother packing containers of paper

• Trade advertising material, Pictures,designs, and photographs,Instructional charts and diagrams

• Lubricants in liquid form andlubricating greases

• Blankets, mattress supports andmattresses

• Electric accumulators

Duty rate of 60% instead of 25%

• Cooked potatoes, fresh or chilledother than seed, potato and othercrisps

• Mineral water and imported ready todrink juices

• Honey

• Processed coffee and tea

• Imported ginger, jams, marmalades,jellies and similar products

• Frozen meats of chicken, bovineanimals, meat of swine, meat ofsheep

• Onions, shallots, garlic, leeks, etc,fresh or chilled

• Peanut butter, bread spreads, butterand other fats and oils derived frommilk, dairy spreads

• Refined cottonseed oil, refinedsunflower seed or safflower oil

• Cocoa powder in packing with a netcontent exceeding, and chocolate andother food preparations containingcocoa

• Biscuits

• Tomato sauce

• Toilet paper, toothbrushes

• Exercise books, ball point pens

Duty rate of 10% instead of 0%

• Partly refined base oil

18

PwC

Uganda National Budget 2019/20 June 2019

19

Tax amendmentsCustoms duty

Stay of execution of EAC CET rate onthe following:

• Iron or steel wool, not scourers andscouring or polishing pads, gloves andsimilar products – duty of 25%.

• Coated electrodes of base metal, forelectric arc-welding – duty of 35%

• Safety matches - 25% or USD 1.35per kg whichever is higher;

• Wheat – 35% instead of 10%.

Specific duty rates for thesteel sector

• Flat rolled products of iron or non-alloysteel products of iron or non-alloysteel - 25% or USD 200/MT whicheveris higher.

• Flat rolled products of iron or non-alloysteel – 25% or USD 250/MT,whichever is higher.

• Steel articles comprising of corrugatediron sheets, pre-painted coils, Hoopiron, twisted bars, flat bars and mildsteel plates - 25% or USD 350MTwhichever is higher.

Other customs duty changes

Duty has been remitted on the following:

• Buses for transportation with seatingcapacity of 25 persons subject to dutyof 25% instead of 10%.

• New pneumatic tyres of rubber usedon motorcycles - from 10% to 35% tosupport the motor cycle tyresproduction in Uganda.

• Raw materials and industrial inputs -Odoriferous mixtures of a kind used asraw materials in the food or drinkindustries and flavours – import dutyof 10% instead of 0%.

PwC

Uganda National Budget 2019/20 June 2019

Revision of stamp duty rateon bank guarantees,insurance performance bondsand indemnity bonds

The Amendment Act sets a new fixedstamp duty rate of UGX 100,000 for thefollowing instruments:

• bank guarantees;

• insurance performance bonds;

• indemnity bonds;

• similar debt instruments.

Bank guarantees are currently not listedseparately and have been subject to dutyof UGX 15,000 (which is the dutyapplicable to bonds) while insuranceperformance bonds have been subject toa fixed rate of UGX 50,000. For theseinstruments the duty rate has beenincreased

However, indemnity bonds are currentlysubject to duty at the rate of 1% of thetotal value, so the new rate will provide afixed cap.

This will provide a uniform duty rate fortransactional documents issued by banksand insurance companies.

However, it does not address theuncertainty between a “bond” and an“indemnity bond”, which has been acontentious issue for banks that issuebonds to their customers. The rate ofstamp duty applicable to a “bond”remains at UGX 15,000 while certainsecurity bonds remain subject to a rate of1%.

Incentives for investors

In line with the changes for other taxincentives, the investment thresholds forthe Strategic Investment Projectexemptions have been reduced to USD50 million for developers of industrialparks or free zones, and to USD 10million and USD 2 million for foreignersand citizens respectively in relation tospecific sectors. In addition, there is anew exemption for certain instrumentsexecuted by a vocational instituteoperator meeting the USD 10 million(foreigner) or USD 2 million (citizen)investment thresholds.

20

Tax amendmentsStamp duty

PwC

Uganda National Budget 2019/20 June 2019

21

Definition of Tax Return

The definition of “tax return” has beenamended to mean a return or otherdocument listed under Schedule 4.

The new Schedule 4 lists VAT, incometax, withholding tax, excise duty, lotteriesand gaming tax and stamp duty returns.The stamp duty return has been addeddespite the Stamp Duty Act not being atax law to which the Tax ProceduresCode Act applies. The Schedule 4 list isalso different from the list of tax returnsalready provided in section 16(7) of theAct.

Payments to informers

The payment made to tax-informers whoprovide information to URA that results ina recovery of tax or duty, is reducedfrom 10% to 5% of the amountrecovered.

Government payment of taxon behalf of taxpayers

A new section 40A imposes a specificrequirement for the Minister to pay anytax arising from a commitment made bythe Government to pay tax on behalf of aperson or owed from Government for aidfunded projects. This section providesstatutory support to situations where theGovernment has entered into anagreement to pay tax on behalf of ataxpayer, for example under aninvestment incentive arrangement.

Furthermore, all outstanding taxes notpaid by Government as at 30 June 2019will be written off. This will ensure thatthe back log of accumulated taxes notpaid in the past is waived andGovernment starts the next fiscal yearwith a clean slate.

Tax amendmentsTax Procedures Code

Voluntary disclosure ofoffences

The new section 66(1a) allowscompounding of an offence with waiverof interest or fines when a taxpayervoluntarily discloses the offence to URAprior to commencement of courtproceedings and makes full payment ofthe outstanding tax. This will encouragevoluntary disclosure of past taxomissions with reduced fiscalconsequences.

PwC

Uganda National Budget 2019/20 June 2019

22

East Africa highlightsKenya

Summary of growth in 2019

Kenya registered economic growth of 6.3%in 2018 compared to 4.9% in 2017. Thisgrowth is the highest recorded for the past 8years.

The growth was anchored on relativelystable macroeconomics and wasattributable to increased agriculturalproduction, accelerated manufacturingactivities, sustained growth in transportationand vibrant service sector activities.

Inflation remained low at 4.8% in 2018compared to 8% in 2017 majorly as a resultof considerable decline in prices of food.

Growth of economy is projected to remainstrong in 2019 at almost same level as in2018, with 7% growth expected over themedium term.

Economic drivers in 2018

• Increased agro-processing activitiesduring the year;

• Favorable weather conditions for bothcrops and livestock production due tolong rains in 2018; and

• Stable political environment,withdrawal of travel advisories,improved security and investorconfidence in the country.

Government priorities for theyear

The government plans to prioritize itsspending towards laying the foundationfor the Big Four agenda.

The identified key initiatives to achieve theagenda and accelerate economic growthare:

• Creating an enabling environment forbusiness;

• Prudent and efficient spending;

• Mobilization of domestic resources tofund priority projects/programmes;

• Stabilizing and reducing debt; and

• Implementing reforms that will enhanceefficiency and competitive advantage

PwC

Uganda National Budget 2019/20 June 2019

23

East Africa highlightsKenya

Key tax changes

Income Tax

• Increase of Capital Gains Tax ratefrom 5% to 12.5%;

• Exemption of CGT on gains arisingfrom group re-organizations;

• Expansion of the scope of servicesattracting withholding taxes other thanmanagement and professional fees;

• Reduced corporate tax rate to 15% inthe first five years for companiesengaged in recycling plastics;

• Tax exemption on the income earnedfrom housing funds; and

• Tax exemption on income earned byindividuals under the Ajira Digitalprogram.

VAT

• Adjustment of the VAT refund formulato ensure that inputs relating to zero-rated supplies are factored in therefund process;

• Reduction of the Withholding VAT ratefrom 6% to 2%;

• Introduction of VAT exemption forlocally manufactured motherboardsand all inputs used in theirmanufacture;

• VAT exemption on all services offeredto plastic recycling plants and supplyof machinery and equipment used inthe construction of the plants.

Customs

• Retention of the import duty rate oniron and steel products at 35% withthe corresponding specific duty ratefor the products produced in Kenya;and

• Reduction of import duty on rawtimber from 10% to 0%.

Excise Duty

• Introduction of Excise duty on bettingactivities at a rate of 10% of thestaked amount;

• Reduction of the excise duty rate onmotor vehicles which are purelyelectric from 20% to 10%; and

• Increase of excise duty on tobaccoproducts, wines and spirits by 15%.

PwC

Uganda National Budget 2019/20 June 2019

24

East Africa highlightsTanzania

Summary of growth

Tanzania recorded real GDP growth ratein 2018 of 7.0% compared to 6.8% in2017. The GDP growth was driven byincreased investment especially ininfrastructure, stable supply of electricity,improvement in transport services andfavourable weather conditions thatresulted in an increased food harvest andother crops.

Government priorities

The priority for 2018/19 will be onflagship infrastructure projects and increating a conducive environment forinvestment and business byimplementing the Blueprint forRegulatory Reforms to improve thebusiness environment.

The focus will be on the following priorityareas:

• Agriculture:

• Industries:

• Livestock and fisheries:

• Economic growth and humandevelopment

• Improvement of enabling businessenvironment and investment climate

Revenue policies

The Government is committed toincreasing and strengthening domesticrevenue collections by pursuing thefollowing policies:

• Increase efficiency in administrationand collection of domestic revenue;

• Widen the tax base throughidentification and registration of newtax payers and formalization of theinformal sector;

• Strengthen capacity for monitoringand controlling of transfer pricing;

• Enhance administration of taxexemptions; and

• Improve efficiency in domesticrevenue collection;

PwC

Uganda National Budget 2019/20 June 2019

25

East Africa highlightsTanzania

Key tax changes

Value added tax

Exemptions proposed include:

• Imported refrigeration boxes, graindrying equipment, aircraft lubricantsby domestic operators, National AirForce and Airlines recognised underbilateral air service agreement.

Zero rating proposed:

• Supply of electricity from Tanzaniamainland to Zanzibar

Exemptions abolished: Sanitary pads

Income tax

• Reduction of the CIT rate for newinvestors in the production of sanitarypads from 30% to 25%.

• Increase in minimum turnover requiredfor a taxpayer to prepare auditedfinancial statements to TZS 100m.

• Changes in presumptive tax rates andnow applies to taxpayers with annualturnover up to TZS 100m.

Withholding tax

Proposed changes includes:

• Exemptions on fees charged toGovernment on loans received fromnon residential banks and otherinternational financial institutions.

Excise duty

Proposed impositions

• 10% on locally made artificial hair and25% on imported ones.

• 10% on pipes and plastics materials

• Exemptions-Aircraft lubricants bydomestic operators, National Air Forceand airlines.

Customs

• To protect local industries, duties havebeen increased on the followingimported products: roasted coffee, flat-rolled products of iron or non-alloysteel ,flat-rolled products of iron ornon-alloy steels, reinforcement barsand hollow profiles, horticulturalproducts and monofilament.

• Duties have been decreased/remittedon the following products: babydiapers, equipment and appurtenantused for polishing and heat treatmentof gemstones, papers used as rawmaterials for manufacturing ofpackaging materials for export ofhorticulture products, agriculturalseeds packaging materials andaluminium alloys used as rawmaterials to manufacture aluminiumpots.

PwC

Uganda National Budget 2019/20 June 2019

26

East Africa highlightsRwanda

Summary of growth in 2019

Rwanda’s economy is estimated to growby 8.6% by the end of the fiscal yearFY18/19 which is 1.4% above thegovernment’s initial projected target of7.2%. Industry and services sectors arethe main contributors to this growth

Economic drivers 2019

• Industry sector -This grew by 10%,much higher than its 5 years’ average,and accounted for 16% of the totalGDP. The industry was boosted by therecovery of the construction sector,which grew by 14%, as well asrecovery in beverages and tobaccoindustries.

• Continuing good performance in textileproduction also contributed to thepositive growth of the sector.

• Services sector - The service sectorgrew by 9%, mainly driven by arecovery in wholesale and retail tradeand continuing expansion of the airtransport segment

• Agriculture sector - This grew by 6%following favourable weatherconditions and various governmentmeasures to increase food and otheragricultural production.

Government priorities

Economic Transformation Pillar:

• Accelerate inclusive economic growthand development founded on theprivate sector, knowledge basedeconomy and Rwanda’s naturalresources.

Social Transformation Pillar:

• Develop Rwandans into a capableand skilled people with qualitystandards of living and a stable andsecure society.

Transformational Governance Pillar:

• Consolidate good governance andjustice as, building blocks forequitable and sustainable NationalDevelopment.

Key tax changes

No major changes were proposed,except for a reiteration that increasedtax collection will mainly be supportedby continued improvement in taxadministrative measures including:

• Revision of the law on tax proceduresrequiring every person carrying outcommercial activities to use the new“EBM for all” expanding coverage tonon-VAT registered persons;

• Revision of the consumption tax lawaimed at increasing tax collectionwhile at the same time discouragingconsumption of some unhealthyproducts; and

• Fiscal incentives will be granted tosome strategic sectors in a bid tosupport “Made in Rwanda” initiativeand the development of a cashlesseconomy.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not actupon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) isgiven as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC does not accept orassume any liability,responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the informationcontained in this publication or for any decision based on it.

© 2019 PricewaterhouseCoopers Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Limited which is a memberfirm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

www.pwc.com/ug

Kenya

Nelson OgaraAssociate Director+254 (20) 285 [email protected]

Tom KavoiSenior Manager+254 (20) 285 [email protected]

Uganda

Pamela N BahumwirePartner+256 (0) 312 [email protected]

Trevor LukangaSenior Manager+256 (0) 312 [email protected]

Rwanda

Moses NyabandaPartner+250 (252) 588203/4/5/[email protected]

Frobisher MugambwaAssociate Director+250 (252) 588203/4/5/[email protected]

Tanzania

David TarimoPartner+255 (0) 22 219 [email protected]

Rishit ShahPartner+255 (0) 22 219 [email protected]

Contacts