Indusind Bank - initiating coverage-Jun-12-EDEL

40

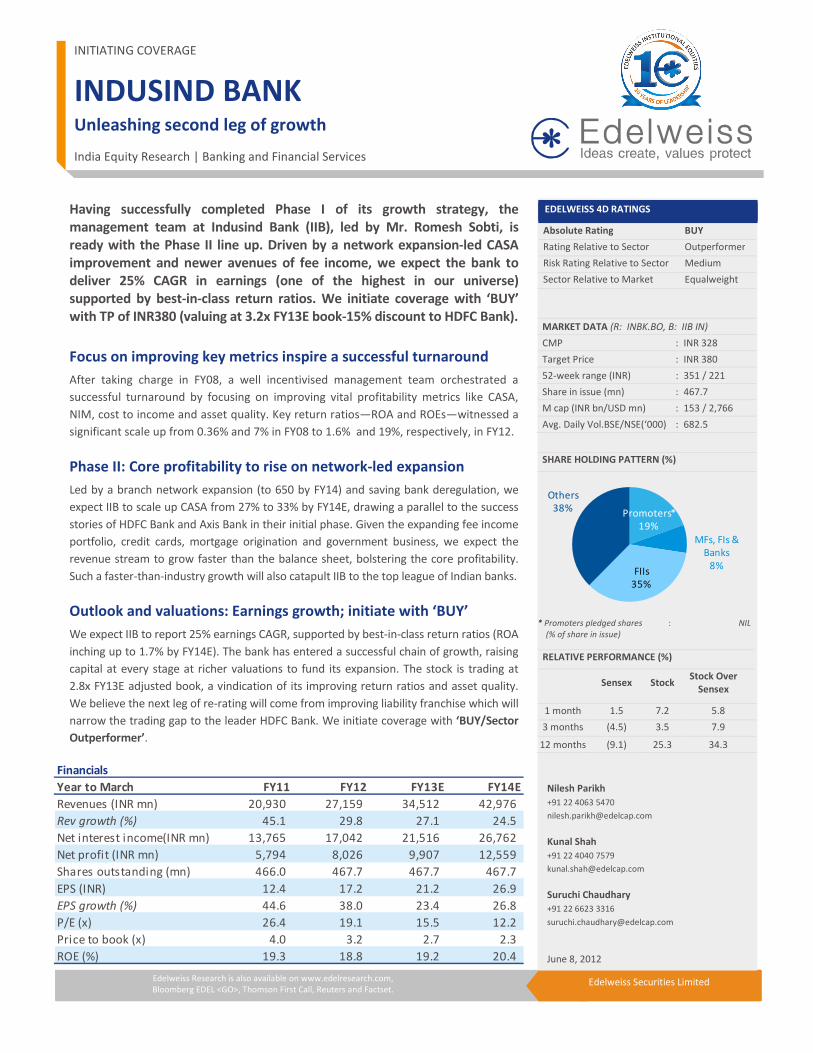

1 Edelweiss Securities Limited Edelweiss Research is also available on www.edelresearch.com, Bloomberg EDEL <GO>, Thomson First Call, Reuters and Factset. Edelweiss Securities Limited INDUSIND BANK Unleashing second leg of growth India Equity Research | Banking and Financial Services Having successfully completed Phase I of its growth strategy, the management team at Indusind Bank (IIB), led by Mr. Romesh Sobti, is ready with the Phase II line up. Driven by a network expansion-led CASA improvement and newer avenues of fee income, we expect the bank to deliver 25% CAGR in earnings (one of the highest in our universe) supported by best-in-class return ratios. We initiate coverage with ‘BUY’ with TP of INR380 (valuing at 3.2x FY13E book-15% discount to HDFC Bank). Focus on improving key metrics inspire a successful turnaround After taking charge in FY08, a well incentivised management team orchestrated a successful turnaround by focusing on improving vital profitability metrics like CASA, NIM, cost to income and asset quality. Key return ratios—ROA and ROEs—witnessed a significant scale up from 0.36% and 7% in FY08 to 1.6% and 19%, respectively, in FY12. Phase II: Core profitability to rise on network-led expansion Led by a branch network expansion (to 650 by FY14) and saving bank deregulation, we expect IIB to scale up CASA from 27% to 33% by FY14E, drawing a parallel to the success stories of HDFC Bank and Axis Bank in their initial phase. Given the expanding fee income portfolio, credit cards, mortgage origination and government business, we expect the revenue stream to grow faster than the balance sheet, bolstering the core profitability. Such a faster-than-industry growth will also catapult IIB to the top league of Indian banks. Outlook and valuations: Earnings growth; initiate with ‘BUY’ We expect IIB to report 25% earnings CAGR, supported by best-in-class return ratios (ROA inching up to 1.7% by FY14E). The bank has entered a successful chain of growth, raising capital at every stage at richer valuations to fund its expansion. The stock is trading at 2.8x FY13E adjusted book, a vindication of its improving return ratios and asset quality. We believe the next leg of re-rating will come from improving liability franchise which will narrow the trading gap to the leader HDFC Bank. We initiate coverage with ‘BUY/Sector Outperformer’. INITIATING COVERAGE EDELWEISS 4D RATINGS Absolute Rating BUY Rating Relative to Sector Outperformer Risk Rating Relative to Sector Medium Sector Relative to Market Equalweight MARKET DATA (R: INBK.BO, B: IIB IN) CMP : INR 328 Target Price : INR 380 52-week range (INR) : 351 / 221 Share in issue (mn) : 467.7 M cap (INR bn/USD mn) : 153 / 2,766 Avg. Daily Vol.BSE/NSE(‘000) : 682.5 SHARE HOLDING PATTERN (%) * Promoters pledged shares (% of share in issue) : NIL RELATIVE PERFORMANCE (%) Sensex Stock Stock Over Sensex 1 month 1.5 7.2 5.8 3 months (4.5) 3.5 7.9 12 months (9.1) 25.3 34.3 June 8, 2012 Nilesh Parikh +91 22 4063 5470 [email protected] Kunal Shah +91 22 4040 7579 [email protected] Suruchi Chaudhary +91 22 6623 3316 [email protected] Promoters* 19% MFs, FIs & Banks 8% FIIs 35% Others 38% Financials Year to March FY11 FY12 FY13E FY14E Revenues (INR mn) 20,930 27,159 34,512 42,976 Rev growth (%) 45.1 29.8 27.1 24.5 Net interest income(INR mn) 13,765 17,042 21,516 26,762 Net profit (INR mn) 5,794 8,026 9,907 12,559 Shares outstanding (mn) 466.0 467.7 467.7 467.7 EPS (INR) 12.4 17.2 21.2 26.9 EPS growth (%) 44.6 38.0 23.4 26.8 P/E (x) 26.4 19.1 15.5 12.2 Price to book (x) 4.0 3.2 2.7 2.3 ROE (%) 19.3 18.8 19.2 20.4

Transcript of Indusind Bank - initiating coverage-Jun-12-EDEL

1 Edelweiss Securities Limited

Edelweiss Research is also available on www.edelresearch.com,

Bloomberg EDEL <GO>, Thomson First Call, Reuters and Factset. Edelweiss Securities Limited

INDUSIND BANK

Unleashing second leg of growth

India Equity Research | Banking and Financial Services

Having successfully completed Phase I of its growth strategy, the

management team at Indusind Bank (IIB), led by Mr. Romesh Sobti, is

ready with the Phase II line up. Driven by a network expansion-led CASA

improvement and newer avenues of fee income, we expect the bank to

deliver 25% CAGR in earnings (one of the highest in our universe)

supported by best-in-class return ratios. We initiate coverage with ‘BUY’

with TP of INR380 (valuing at 3.2x FY13E book-15% discount to HDFC Bank).

Focus on improving key metrics inspire a successful turnaround

After taking charge in FY08, a well incentivised management team orchestrated a

successful turnaround by focusing on improving vital profitability metrics like CASA,

NIM, cost to income and asset quality. Key return ratios—ROA and ROEs—witnessed a

significant scale up from 0.36% and 7% in FY08 to 1.6% and 19%, respectively, in FY12.

Phase II: Core profitability to rise on network-led expansion

Led by a branch network expansion (to 650 by FY14) and saving bank deregulation, we

expect IIB to scale up CASA from 27% to 33% by FY14E, drawing a parallel to the success

stories of HDFC Bank and Axis Bank in their initial phase. Given the expanding fee income

portfolio, credit cards, mortgage origination and government business, we expect the

revenue stream to grow faster than the balance sheet, bolstering the core profitability.

Such a faster-than-industry growth will also catapult IIB to the top league of Indian banks.

Outlook and valuations: Earnings growth; initiate with ‘BUY’

We expect IIB to report 25% earnings CAGR, supported by best-in-class return ratios (ROA

inching up to 1.7% by FY14E). The bank has entered a successful chain of growth, raising

capital at every stage at richer valuations to fund its expansion. The stock is trading at

2.8x FY13E adjusted book, a vindication of its improving return ratios and asset quality.

We believe the next leg of re-rating will come from improving liability franchise which will

narrow the trading gap to the leader HDFC Bank. We initiate coverage with ‘BUY/Sector

Outperformer’.

INITIATING COVERAGE

EDELWEISS 4D RATINGS

Absolute Rating BUY

Rating Relative to Sector Outperformer

Risk Rating Relative to Sector Medium

Sector Relative to Market Equalweight

MARKET DATA (R: INBK.BO, B: IIB IN)

CMP : INR 328

Target Price : INR 380

52-week range (INR) : 351 / 221

Share in issue (mn) : 467.7

M cap (INR bn/USD mn) : 153 / 2,766

Avg. Daily Vol.BSE/NSE(‘000) : 682.5

SHARE HOLDING PATTERN (%)

* Promoters pledged shares

(% of share in issue)

: NIL

RELATIVE PERFORMANCE (%)

Sensex Stock Stock Over

Sensex

1 month 1.5 7.2 5.8

3 months (4.5) 3.5 7.9

12 months (9.1) 25.3 34.3

June 8, 2012

Nilesh Parikh

+91 22 4063 5470

Kunal Shah

+91 22 4040 7579

Suruchi Chaudhary

+91 22 6623 3316 [email protected]

Promoters*

19%

MFs, FIs &

Banks

8%FIIs

35%

Others

38%

Financials

Year to March FY11 FY12 FY13E FY14E

Revenues (INR mn) 20,930 27,159 34,512 42,976

Rev growth (%) 45.1 29.8 27.1 24.5

Net interest income(INR mn) 13,765 17,042 21,516 26,762

Net profit (INR mn) 5,794 8,026 9,907 12,559

Shares outstanding (mn) 466.0 467.7 467.7 467.7

EPS (INR) 12.4 17.2 21.2 26.9

EPS growth (%) 44.6 38.0 23.4 26.8

P/E (x) 26.4 19.1 15.5 12.2

Price to book (x) 4.0 3.2 2.7 2.3

ROE (%) 19.3 18.8 19.2 20.4

2 Edelweiss Securities Limited

Banking and Financial Services

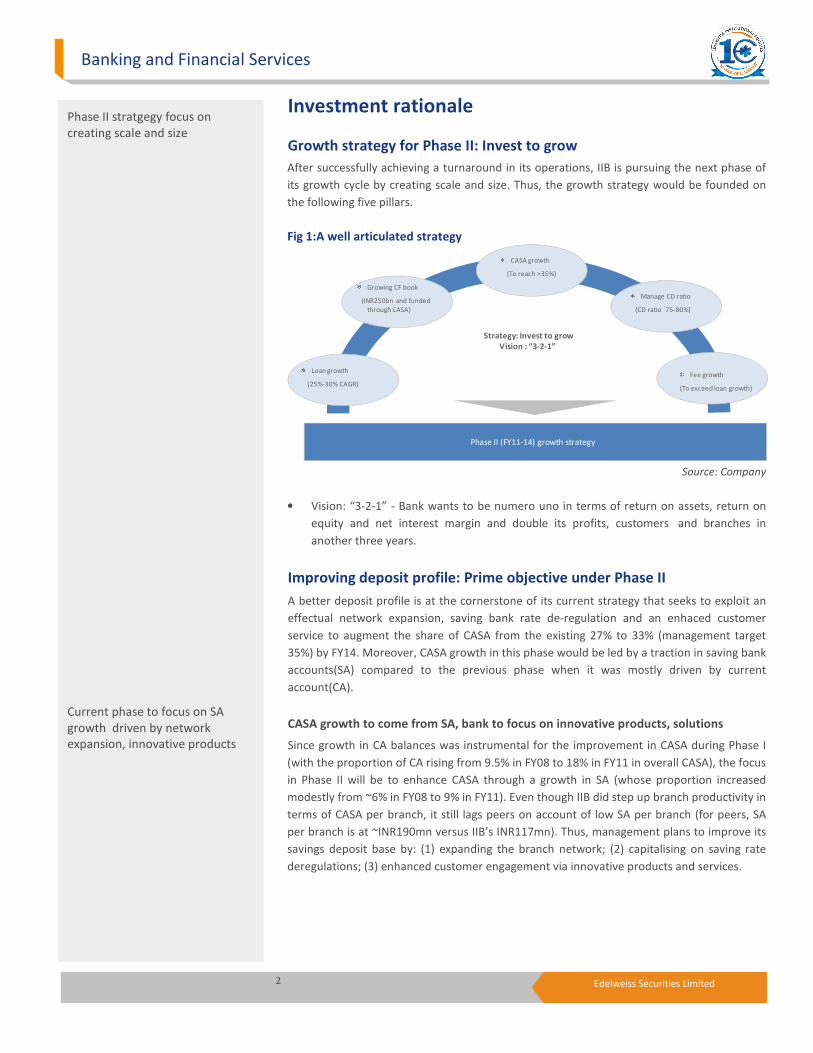

Investment rationale

Growth strategy for Phase II: Invest to grow

After successfully achieving a turnaround in its operations, IIB is pursuing the next phase of

its growth cycle by creating scale and size. Thus, the growth strategy would be founded on

the following five pillars.

Fig 1:A well articulated strategy

Strategy: Invest to grow

Vision : “3-2-1”

Loan growth

(25%-30% CAGR)

Growing CF book

(INR250bn and funded

through CASA)

CASA growth

(To reach >35%)

Fee growth

(To exceed loan growth)

Manage CD ratio

(CD ratio 75-80%)

Phase II (FY11-14) growth strategy

Source: Company

• Vision: “3-2-1” - Bank wants to be numero uno in terms of return on assets, return on

equity and net interest margin and double its profits, customers and branches in

another three years.

Improving deposit profile: Prime objective under Phase II

A better deposit profile is at the cornerstone of its current strategy that seeks to exploit an

effectual network expansion, saving bank rate de-regulation and an enhaced customer

service to augment the share of CASA from the existing 27% to 33% (management target

35%) by FY14. Moreover, CASA growth in this phase would be led by a traction in saving bank

accounts(SA) compared to the previous phase when it was mostly driven by current

account(CA).

CASA growth to come from SA, bank to focus on innovative products, solutions

Since growth in CA balances was instrumental for the improvement in CASA during Phase I

(with the proportion of CA rising from 9.5% in FY08 to 18% in FY11 in overall CASA), the focus

in Phase II will be to enhance CASA through a growth in SA (whose proportion increased

modestly from ~6% in FY08 to 9% in FY11). Even though IIB did step up branch productivity in

terms of CASA per branch, it still lags peers on account of low SA per branch (for peers, SA

per branch is at ~INR190mn versus IIB’s INR117mn). Thus, management plans to improve its

savings deposit base by: (1) expanding the branch network; (2) capitalising on saving rate

deregulations; (3) enhanced customer engagement via innovative products and services.

Phase II stratgegy focus on

creating scale and size

Current phase to focus on SA

growth driven by network

expansion, innovative products

3 Edelweiss Securities Limited

Indusind Bank

Chart 1:SA/branch vis-à-vis peers

0

70

140

210

280

350

Axis Bank HDFC Bank Kotak Mahindra

Bank

IndusInd Bank Yes Bank

(IN

R m

n)

Saving Deposit / branch

Source: Company

Massive branch expansion to create nationwide presence and build density

In the initial part of Phase I (FY09-10), IIB had focused on improving productivity by

reorganising the branch architecture and, hence, opened only 30 branches. From FY11 , the

bank has stepped up branch expansion, which we expect to continue in Phase II. The bank

currently has a nationwide presence with 400 branches and 674 ATMs. Further, it intends to

widen the reach and exit FY14 with 650 branches, entailing opening around 125 branches

over the next two years. The strategy for branch expansion would revolve around creating

density—as 75% of the new branches will be set up in existing centres.

With most of the regulatory compliance (in terms of branch opening) in place and the RBI

relaxing its stance on branch opening, we believe IIB will close in on its target to open ~650

branches by FY14E. This spurt in number of branches will provide the bank with the much

needed visibility, which in turn will help it ramp up new client acquisition (by having an

increased distribution capability) thus helping it maintain desired growth .

Capitalising on savings rate deregulation to accelerate deposit base

With the saving bank rate deregulation already coming to the fore, the management

capitalised on the opportunity by hiking interest rates on its savings bank deposits (5.5% for

<INR0.1mn and 6% for >INR0.1mn accounts). The bank’s rate are currently at a level greater

than its peers by ~150-200bps. The effect of this can be seen in the increased savings base

(from INR33bn in Q2FY12 to INR47bn in Q4FY12 , 93% QoQ increase in new to bank clients

saving deposits).

Enhanced customer engagement

With the focus on improving SA base, management launched various innovative initiatives

like allowing customers to choose the denomination of bank notes at ATMs, enabling

customers/family to withdraw from ATMs without using cards, cheques scan on bank

statements etc., to enhance customer service standards and customer engagement. We

expect these initiatives to enhance the bank’s visibility in tier 2 cities, which in turn will help

attract new customer base.

Branch network to reach 650 by

FY14 – focusing on creating

density

4 Edelweiss Securities Limited

Banking and Financial Services

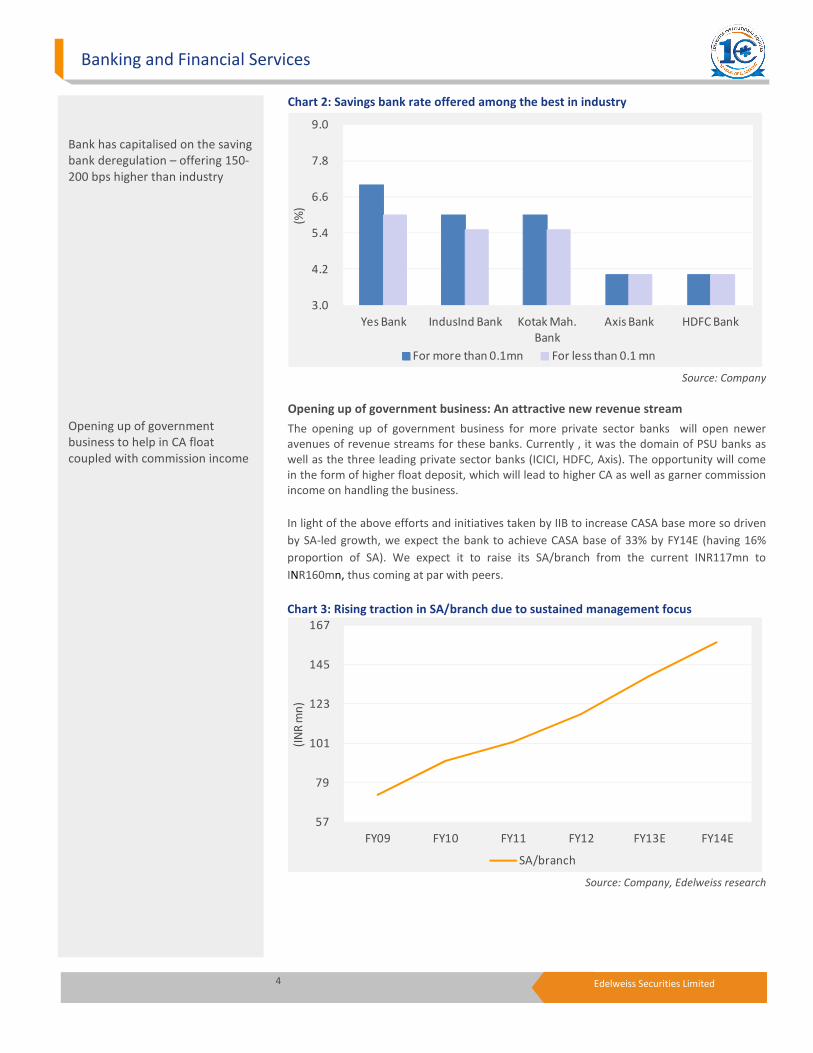

Chart 2: Savings bank rate offered among the best in industry

3.0

4.2

5.4

6.6

7.8

9.0

Yes Bank IndusInd Bank Kotak Mah.

Bank

Axis Bank HDFC Bank

(%)

For more than 0.1mn For less than 0.1 mn Source: Company

Opening up of government business: An attractive new revenue stream

The opening up of government business for more private sector banks will open newer

avenues of revenue streams for these banks. Currently , it was the domain of PSU banks as

well as the three leading private sector banks (ICICI, HDFC, Axis). The opportunity will come

in the form of higher float deposit, which will lead to higher CA as well as garner commission

income on handling the business.

In light of the above efforts and initiatives taken by IIB to increase CASA base more so driven

by SA-led growth, we expect the bank to achieve CASA base of 33% by FY14E (having 16%

proportion of SA). We expect it to raise its SA/branch from the current INR117mn to

INR160mn, thus coming at par with peers.

Chart 3: Rising traction in SA/branch due to sustained management focus

57

79

101

123

145

167

FY09 FY10 FY11 FY12 FY13E FY14E

(IN

R m

n)

SA/branch Source: Company, Edelweiss research

Bank has capitalised on the saving

bank deregulation – offering 150-

200 bps higher than industry

Opening up of government

business to help in CA float

coupled with commission income

5 Edelweiss Securities Limited

Indusind Bank

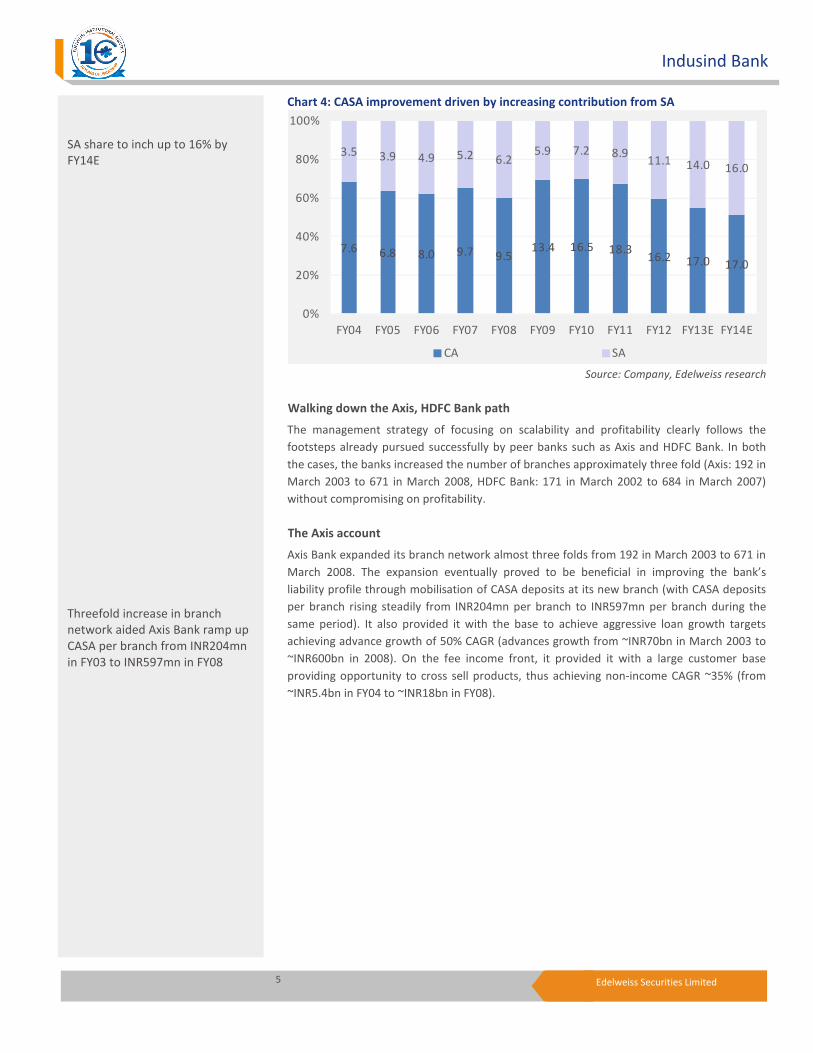

Chart 4: CASA improvement driven by increasing contribution from SA

7.6 6.8 8.0 9.7 9.513.4 16.5 18.3

16.2 17.0 17.0

3.5 3.9 4.9 5.2 6.25.9 7.2 8.9

11.1 14.0 16.0

0%

20%

40%

60%

80%

100%

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E

CA SA

Source: Company, Edelweiss research

Walking down the Axis, HDFC Bank path

The management strategy of focusing on scalability and profitability clearly follows the

footsteps already pursued successfully by peer banks such as Axis and HDFC Bank. In both

the cases, the banks increased the number of branches approximately three fold (Axis: 192 in

March 2003 to 671 in March 2008, HDFC Bank: 171 in March 2002 to 684 in March 2007)

without compromising on profitability.

The Axis account

Axis Bank expanded its branch network almost three folds from 192 in March 2003 to 671 in

March 2008. The expansion eventually proved to be beneficial in improving the bank’s

liability profile through mobilisation of CASA deposits at its new branch (with CASA deposits

per branch rising steadily from INR204mn per branch to INR597mn per branch during the

same period). It also provided it with the base to achieve aggressive loan growth targets

achieving advance growth of 50% CAGR (advances growth from ~INR70bn in March 2003 to

~INR600bn in 2008). On the fee income front, it provided it with a large customer base

providing opportunity to cross sell products, thus achieving non-income CAGR ~35% (from

~INR5.4bn in FY04 to ~INR18bn in FY08).

SA share to inch up to 16% by

FY14E

Threefold increase in branch

network aided Axis Bank ramp up

CASA per branch from INR204mn

in FY03 to INR597mn in FY08

6 Edelweiss Securities Limited

Banking and Financial Services

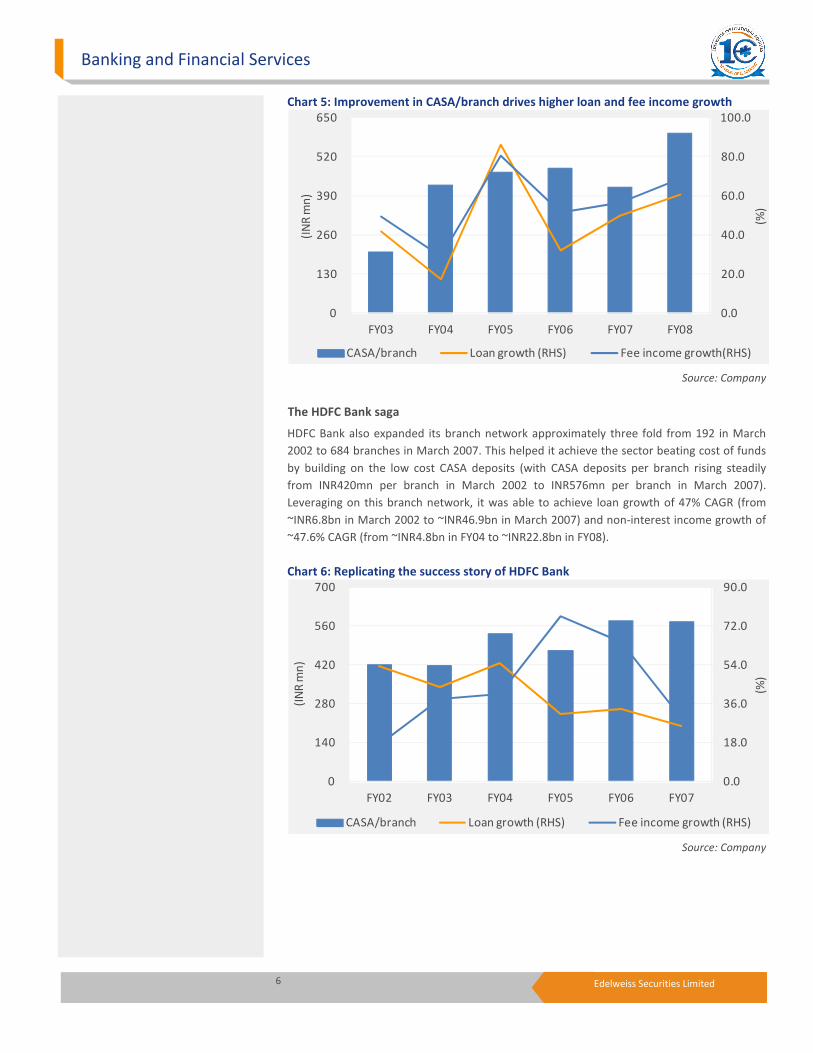

Chart 5: Improvement in CASA/branch drives higher loan and fee income growth

0.0

20.0

40.0

60.0

80.0

100.0

0

130

260

390

520

650

FY03 FY04 FY05 FY06 FY07 FY08

(%)

(IN

R m

n)

CASA/branch Loan growth (RHS) Fee income growth(RHS)

Source: Company

The HDFC Bank saga

HDFC Bank also expanded its branch network approximately three fold from 192 in March

2002 to 684 branches in March 2007. This helped it achieve the sector beating cost of funds

by building on the low cost CASA deposits (with CASA deposits per branch rising steadily

from INR420mn per branch in March 2002 to INR576mn per branch in March 2007).

Leveraging on this branch network, it was able to achieve loan growth of 47% CAGR (from

~INR6.8bn in March 2002 to ~INR46.9bn in March 2007) and non-interest income growth of

~47.6% CAGR (from ~INR4.8bn in FY04 to ~INR22.8bn in FY08).

Chart 6: Replicating the success story of HDFC Bank

0.0

18.0

36.0

54.0

72.0

90.0

0

140

280

420

560

700

FY02 FY03 FY04 FY05 FY06 FY07

(%)

(IN

R m

n)

CASA/branch Loan growth (RHS) Fee income growth (RHS)

Source: Company

7 Edelweiss Securities Limited

Indusind Bank

Higher-than-industry loan growth

IIB has laid emphasis on achieving 25% loan growth over the next 2-3 years (above the

industry average loan growth of 16-17%). Having increased the share of consumer finance

(CF) from 44% in FY11 to ~50% in FY12 on back of strong growth in CVs, we believe going

forward CF and corporate banking (CCB) growth will track similar run-rate, in line with

management strategy of maintaining loan mix at 50% .

Chart 7: IIB loan growth to be above industry average

12.0

17.8

23.6

29.4

35.2

41.0

FY09 FY10 FY11 FY12 FY13E FY14E

(%)

Loan growth Industry loan growth

Source: Company, Edelweiss research

Chart 8: Optimal loan book mix of ~50% CF and 50% CCB to be maintained

5745 44 49 50

4355 56 51 50

0%

20%

40%

60%

80%

100%

FY09 FY10 FY11 FY12 FY14E

Consumer finance Corporate and commercial banking

Source: Company, Edelweiss research

Focusing on CF

At the beginning of Phase II, the management had articulated the intention of achieving an

equal mix between corporate and consumer book and to fund the increase in the consumer

book via CASA base. During FY12, given the elevated interest rates, – bank consciously

choose to scale up the fixed rate – commercial vehicles segment to restrict the decline in

NIMs on the existing fixed rate book . This, along with the opportunity thrown up by the CV

segment , consumer finance (CF) segment scaled up to ~50% in FY12 itself. On the other

Target of 25% CAGR over the next

2 years – higher than industry

CF book to retain 50% share

driven by CVs and stepping up of

the LAP portfolio

8 Edelweiss Securities Limited

Banking and Financial Services

hand, also as part of the conscious strategy, IIB restricted growth in corporate book by selling

down loans via inter-bank participation. We believe that CF book will post ~25% CAGR over

FY12-14E comprising ~50% of the total loan book. We expect growth to be driven by: (1)

increased sales in commercial vehicle segment (with increased thrust towards LCV and entry

level four-wheelers); (2) commercial equipment; (3) used vehicle segment; and (4) loan

against property segment which is expected to scale up about ~15% of the CF book. This

renewed focus on used vehicle segment, in turn, will help maintain the desired NIMs (as

these have high yields).

Chart 9: -Proportion of LAP and credit cards increasing in CF book

CV loans

47.9%

UN

loans

7.2%

Small CV

11.1%

Two

Wheeler

Loans

8.7%Car Loans

8.1%Equip.

Financing

12.4%

Credit

Card

1.4%

LAP

2.4%

Others(

Home,

Personal,)

0.8%

Other

4.6%

Source: Company, Edelweiss research

Difficult to penetrate niche market position

Given the structure of CV market where most of the banks and NBFCs finance large fleet

operators, where as small fleet operators are largely financed by NBFCs, IIB holds a niche

position in financing small road transport operators given its tremendous reach and

experience in this field (operating out of 600 specialised outlets/offices across the country).

Also, given the expectation of the segment growth of 10% and difficult to penetrate

segment (due to customer profile and reach requirements) we believe the bank will continue

to grow in this segment.

Increasing focus on used vehicle segment

Strong presence in rural and semi-urban areas and a loyal and vast customer base (enhanced

by inherited strong distribution network and skill set from Ashok Leyland Finance) will help

IIB grow in the used CV market. We believe this segment presents the bank with vast

opportunity to grow, thus improving NIMs (as yield around 18% vis-à-vis ~14% for new

vehicle financing). But this growth opportunity comes with a caveat as this segment is

marked with higher delinquencies thus may put pressure on asset quality.

Vehicles

82%

Credit

Cards

3%

LAP

15%

FY14E

Niche position in small road

transport operating given its

reach and experience a key

positive

9 Edelweiss Securities Limited

Indusind Bank

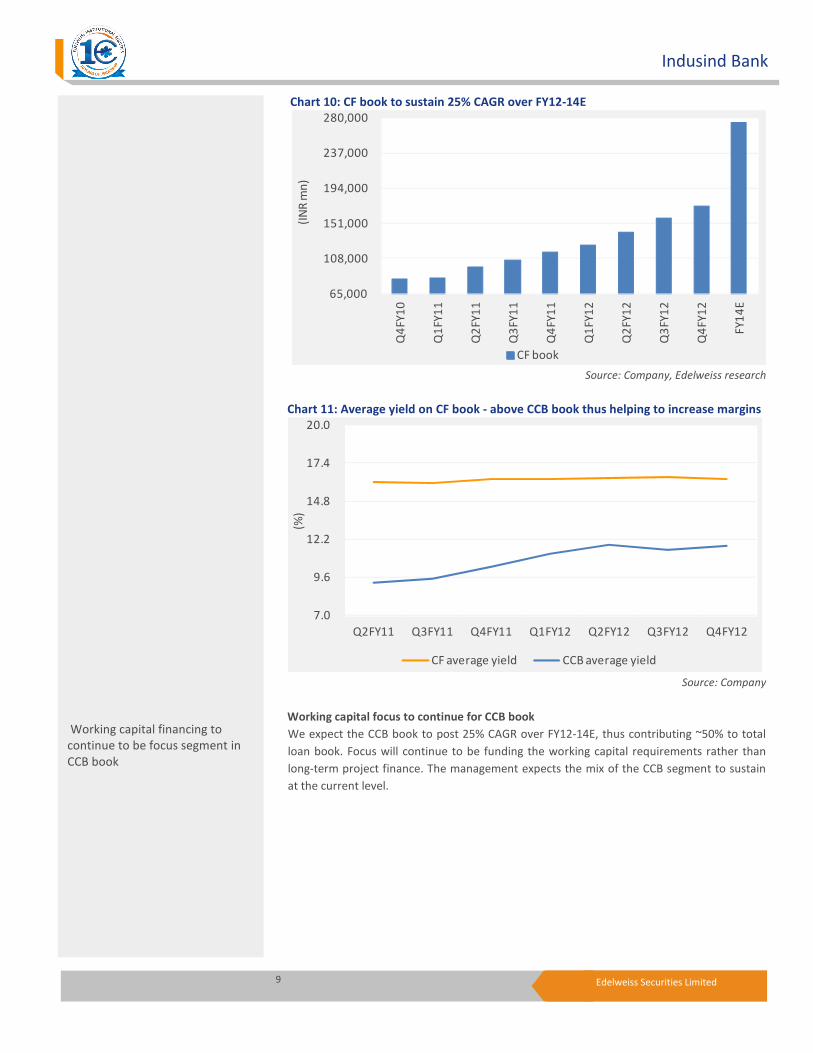

Chart 10: CF book to sustain 25% CAGR over FY12-14E

65,000

108,000

151,000

194,000

237,000

280,000

Q4

FY

10

Q1

FY

11

Q2

FY

11

Q3

FY

11

Q4

FY

11

Q1

FY

12

Q2

FY

12

Q3

FY

12

Q4

FY

12

FY

14

E

(IN

R m

n)

CF book

Source: Company, Edelweiss research

Chart 11: Average yield on CF book - above CCB book thus helping to increase margins

7.0

9.6

12.2

14.8

17.4

20.0

Q2FY11 Q3FY11 Q4FY11 Q1FY12 Q2FY12 Q3FY12 Q4FY12

(%)

CF average yield CCB average yield

Source: Company

Working capital focus to continue for CCB book

We expect the CCB book to post 25% CAGR over FY12-14E, thus contributing ~50% to total

loan book. Focus will continue to be funding the working capital requirements rather than

long-term project finance. The management expects the mix of the CCB segment to sustain

at the current level.

Working capital financing to

continue to be focus segment in

CCB book

10 Edelweiss Securities Limited

Banking and Financial Services

Chart 12: Growth in CCB book to be driven by working capital finance

47.9 48.655.8 55.3

47.054.9 54.5 54.4 53.3

37.2 36.830.6 31.3

34.827.6 28.1 28.5 29.9

14.9 14.6 13.6 13.4 18.2 17.5 17.4 17.0 16.8

0%

20%

40%

60%

80%

100%

Q4FY10 Q1FY11 Q2FY11 Q3FY11 Q4FY11 Q1FY12 Q2FY12 Q3FY12 Q4FY12

Corp and inv. banking Commercial banking Loan to small businesses

Source: Company

Chart 13: Superior quality as majority of lending figures in investment grade

Source: Company

Focus on non-interest income growth

IIB plans to strengthen its fee income (targeting to grow fee income more than loan growth)

by focusing on (new) fee enhancers, coupled with raising growth momentum in existing

segments of structured trade ,treasury products and foreign exchange business.

• Scaling up of investment banking practice

With the unit housing strong capabilities across areas, viz., debt syndication, credit

structuring and advisory and private equity advisory, management strategy is to

leverage the bank’s client base and strong relationships to provide highly customised

investment banking solutions so that effective partnership can be extended to clients in

their growth.

Investment grade Sub investment grade

Fee income growth to grow faster

than balance sheet

11 Edelweiss Securities Limited

Indusind Bank

• Full suite asset portfolio

The bank plans to energize its retail bank offering by providing full suite asset portfolio

by leveraging on products like LAP (loan against property), credit card, and mortgage

origination for HDFC.

• Leveraging on credit card business acquired from Deutsche Bank

The bank could have developed the credit card business organically, but it bid for the

Deutsche bank’s card portfolio in India to grab the opportunity to jump start the

business. Key benefits that management has by this acquisition are: 1) An evolved and

stable system platform and 2) strong product range with deep relationships with credit

card programme partners. Further, management as its part of strategy aims to grow this

credit card portfolio to ~INR8bn(~1.3% of loan book ) from INR 2.7 bn currently, with

focus on affluent customers.

• Fee for mortgage origination for HDFC

It has recently tied up with HDFC Ltd to sell its mortgage product for fee-based income.

It is likely to earn a fee of 90bps on these loans; if it also cross-sells mortgage insurance

products, it will earn an additional fee of 50bps (currently, the conversion rate is 1 out

of 3), with an option to buy back 30% of the book. The management plans to leverage

this relationship to increase its fee-based component (given that mortgage product is

not the bank’s expertise, it does not intent to focus on it fully).

Chart 14: Contributors to the core fee income

0%

20%

40%

60%

80%

100%

FY10 FY11 FY12 FY13E FY14E

Trade & Remittances Foreign Exchange Income

TPP Distribution Income (Insurance, MF) General Banking Fees

Loan Processing Fees Investment Banking Source: Company, Edelweiss research

Credit cards portfolio to reach

INR 8 bn (1.3% of loan book)

12 Edelweiss Securities Limited

Banking and Financial Services

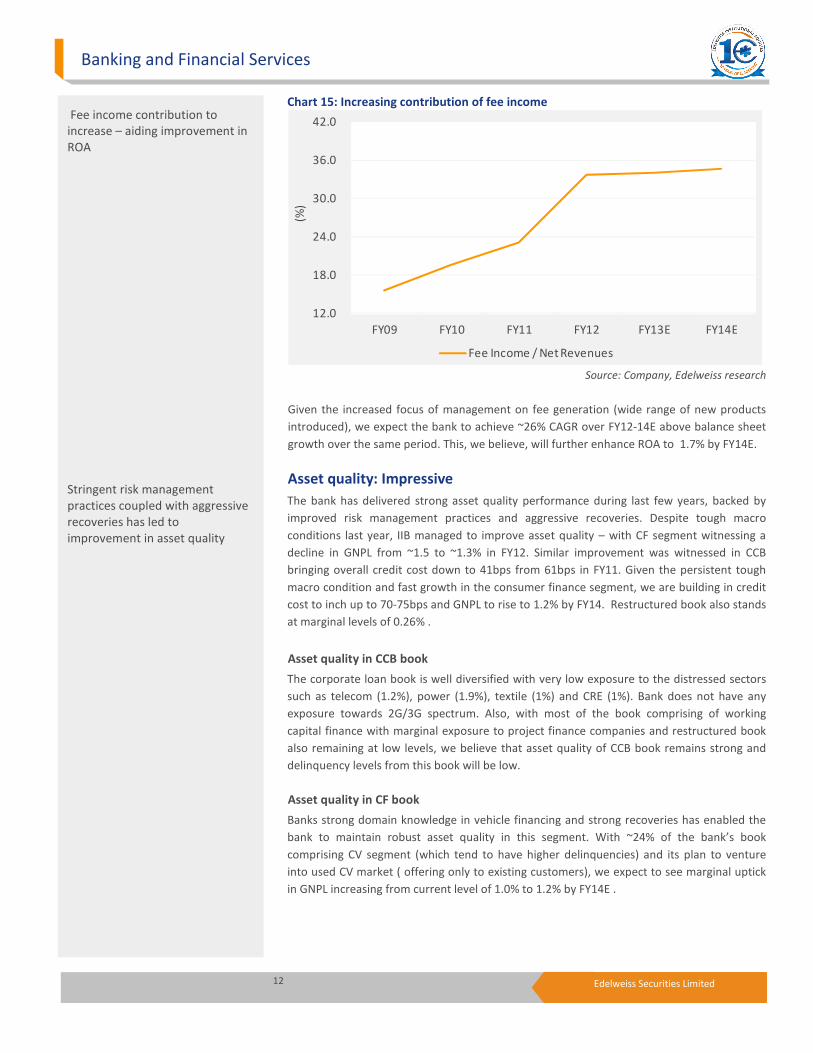

Chart 15: Increasing contribution of fee income

12.0

18.0

24.0

30.0

36.0

42.0

FY09 FY10 FY11 FY12 FY13E FY14E

(%)

Fee Income / Net Revenues Source: Company, Edelweiss research

Given the increased focus of management on fee generation (wide range of new products

introduced), we expect the bank to achieve ~26% CAGR over FY12-14E above balance sheet

growth over the same period. This, we believe, will further enhance ROA to 1.7% by FY14E.

Asset quality: Impressive

The bank has delivered strong asset quality performance during last few years, backed by

improved risk management practices and aggressive recoveries. Despite tough macro

conditions last year, IIB managed to improve asset quality – with CF segment witnessing a

decline in GNPL from ~1.5 to ~1.3% in FY12. Similar improvement was witnessed in CCB

bringing overall credit cost down to 41bps from 61bps in FY11. Given the persistent tough

macro condition and fast growth in the consumer finance segment, we are building in credit

cost to inch up to 70-75bps and GNPL to rise to 1.2% by FY14. Restructured book also stands

at marginal levels of 0.26% .

Asset quality in CCB book

The corporate loan book is well diversified with very low exposure to the distressed sectors

such as telecom (1.2%), power (1.9%), textile (1%) and CRE (1%). Bank does not have any

exposure towards 2G/3G spectrum. Also, with most of the book comprising of working

capital finance with marginal exposure to project finance companies and restructured book

also remaining at low levels, we believe that asset quality of CCB book remains strong and

delinquency levels from this book will be low.

Asset quality in CF book

Banks strong domain knowledge in vehicle financing and strong recoveries has enabled the

bank to maintain robust asset quality in this segment. With ~24% of the bank’s book

comprising CV segment (which tend to have higher delinquencies) and its plan to venture

into used CV market ( offering only to existing customers), we expect to see marginal uptick

in GNPL increasing from current level of 1.0% to 1.2% by FY14E .

Fee income contribution to

increase – aiding improvement in

ROA

Stringent risk management

practices coupled with aggressive

recoveries has led to

improvement in asset quality

13 Edelweiss Securities Limited

Indusind Bank

Chart 16: Segmental composition of GNPLs in CF book

0.0

1.0

2.0

3.0

4.0

5.0

CV Uitlity Const equip 3W 2W Cars

(%)

Q4FY11 Q4FY12

Source: Company

Chart 17: Marginal decline in asset quality due to increased focus on used vehicles

0.0

0.4

0.8

1.2

1.6

2.0

FY09 FY10 FY11 FY12 FY13E FY14E

(%)

GNPA NNPA

Source: Company, Edelweiss research

We have build in marginal uptick

in NPLs due to higher share of

used vehicles segment

14 Edelweiss Securities Limited

Banking and Financial Services

Financial outlook

We expect the bank to grow its net profit by 25% CAGR to INR12.6bn over FY12-14E. Key

driver for higher-than-industry earnings growth will be improving margins and faster than

balance sheet fee income growth which will offset some increase being built for provisioning

cost. Pre-provisioing profit growth is expected to trend higher, given strong operating

profitability .

Chart 18: Earning to post 25% CAGR over FY12-14E

18.0

47.6

77.2

106.8

136.4

166.0

1,186

3,985

6,784

9,582

12,381

15,180

FY09 FY10 FY11 FY12 FY13E FY14E

(%)

(IN

R m

n)

PAT PAT growth (RHS)

Source: Company, Edelweiss research

NIMs set to improve

Margins for the bank have been continuously improving, up from ~1.46% in FY08 to ~3.56%

in FY11.This can be attributed to rising share of CASA deposits from ~15% in FY08 to ~27% in

FY11, helping the bank to lower COF from 7.6% in FY08 to 5.9% in FY11. However, in FY12,

we saw margins coming off 21bps as cost of funds moved up, whereas lending yield was

restricted due to the fixed nature of the consumer finance book. Going forward, we expect

margins to improve 20bps to 3.6% (calculated) as multiple levers come to play: 1) CASA

moving up from current levels of 27% to 33% by FY14; 2) stable lending yield, despite

likelihood of borrowing cost coming down over next 2 years, due to fixed nature of the book;

3) increase in share of high yielding CV book offseting the rise in share of LAP (lower yield

compared with the overall CF book). Better NIMs, coupled with steady 20%+ earnings asset

growth, will ensure a robust ~25% CAGR in NII over FY12-14.

We expects NIMs to improve by

20 bps by FY14

15 Edelweiss Securities Limited

Indusind Bank

Chart 19: NIMs to inch up ~20bps to 3.6% by FY14E

1.0

1.8

2.6

3.4

4.2

5.0

FY09 FY10 FY11 FY12 FY13E FY14E

(%)

NIMs Source: Company, Edelweiss research

Fee income growth outpaces balance sheet

With increased focus on fee income by: 1) Scaling up its investment banking practice and 2)

introducing new products – credit cards, mortgage orgination, we expect fee income to grow

more than balance sheet growth reflecting further upside to earnings.

Better cost-to-income ratio

Cost-to-income ratio for the bank has been consistently improving after the new

management came to fore, basically on account of improved productivity combined with

improved revenue traction. With the management guidance of scaling up branch network to

650 by FY14E (also leading to growth in employee base), we expect cost–to-income to come

under some pressure. This will, however, be more than offset by increase in revenue stream

and higher productivity. Thus, we expect cost-income ratio to initially increase, but then

come off in coming years (to the level to ~48% by FY14E) as and when branches are fully

integrated to achieve synergy thus increasing productivity.

Chart 20: Steady cost to income ratio over FY14E

38.0

44.8

51.6

58.4

65.2

72.0

FY09 FY10 FY11 FY12 FY13E FY14E

(%)

C/I

Source: Company, Edelweiss research

Cost-to-income ratio to remain

steady despite network expansion

given the ramp up in revenue

16 Edelweiss Securities Limited

Banking and Financial Services

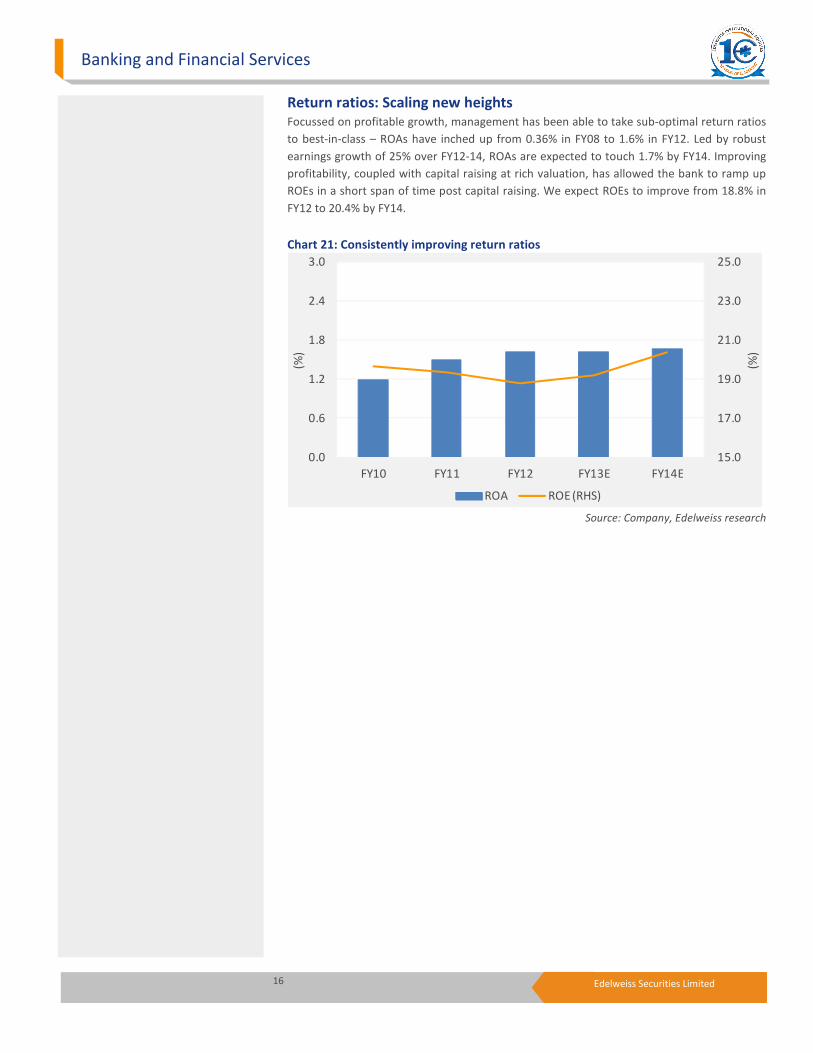

Return ratios: Scaling new heights

Focussed on profitable growth, management has been able to take sub-optimal return ratios

to best-in-class – ROAs have inched up from 0.36% in FY08 to 1.6% in FY12. Led by robust

earnings growth of 25% over FY12-14, ROAs are expected to touch 1.7% by FY14. Improving

profitability, coupled with capital raising at rich valuation, has allowed the bank to ramp up

ROEs in a short span of time post capital raising. We expect ROEs to improve from 18.8% in

FY12 to 20.4% by FY14.

Chart 21: Consistently improving return ratios

15.0

17.0

19.0

21.0

23.0

25.0

0.0

0.6

1.2

1.8

2.4

3.0

FY10 FY11 FY12 FY13E FY14E

(%)

(%)

ROA ROE (RHS) Source: Company, Edelweiss research

17 Edelweiss Securities Limited

Indusind Bank

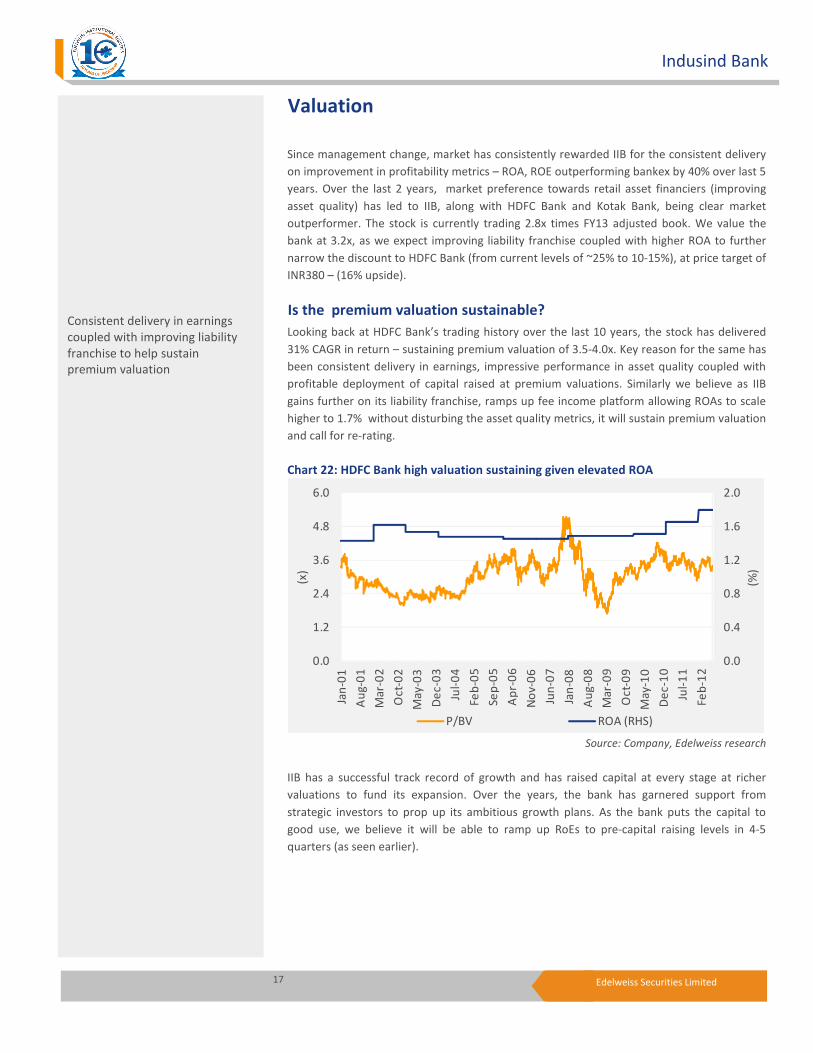

Valuation

Since management change, market has consistently rewarded IIB for the consistent delivery

on improvement in profitability metrics – ROA, ROE outperforming bankex by 40% over last 5

years. Over the last 2 years, market preference towards retail asset financiers (improving

asset quality) has led to IIB, along with HDFC Bank and Kotak Bank, being clear market

outperformer. The stock is currently trading 2.8x times FY13 adjusted book. We value the

bank at 3.2x, as we expect improving liability franchise coupled with higher ROA to further

narrow the discount to HDFC Bank (from current levels of ~25% to 10-15%), at price target of

INR380 – (16% upside).

Is the premium valuation sustainable?

Looking back at HDFC Bank’s trading history over the last 10 years, the stock has delivered

31% CAGR in return – sustaining premium valuation of 3.5-4.0x. Key reason for the same has

been consistent delivery in earnings, impressive performance in asset quality coupled with

profitable deployment of capital raised at premium valuations. Similarly we believe as IIB

gains further on its liability franchise, ramps up fee income platform allowing ROAs to scale

higher to 1.7% without disturbing the asset quality metrics, it will sustain premium valuation

and call for re-rating.

Chart 22: HDFC Bank high valuation sustaining given elevated ROA

0.0

0.4

0.8

1.2

1.6

2.0

0.0

1.2

2.4

3.6

4.8

6.0

Jan

-01

Au

g-0

1

Ma

r-0

2

Oc

t-0

2

Ma

y-0

3

De

c-0

3

Jul-

04

Fe

b-0

5

Se

p-0

5

Ap

r-0

6

No

v-0

6

Jun

-07

Jan

-08

Au

g-0

8

Ma

r-0

9

Oc

t-0

9

Ma

y-1

0

De

c-1

0

Jul-

11

Fe

b-1

2

(%)

(x)

P/BV ROA (RHS) Source: Company, Edelweiss research

IIB has a successful track record of growth and has raised capital at every stage at richer

valuations to fund its expansion. Over the years, the bank has garnered support from

strategic investors to prop up its ambitious growth plans. As the bank puts the capital to

good use, we believe it will be able to ramp up RoEs to pre-capital raising levels in 4-5

quarters (as seen earlier).

Consistent delivery in earnings

coupled with improving liability

franchise to help sustain

premium valuation

18 Edelweiss Securities Limited

Banking and Financial Services

Chart 23: ROE ramp up in 4-5 quarters to pre-issue level

12.0

15.2

18.4

21.6

24.8

28.0

(1) 0 1 2 3 4

(%)

ROE (Prefrential issue) ROE (Isuued to QIP) Source: Company, Edelweiss research

Given the challenging macro conditions persist, we believe in the near-term retail asset

financiers (especially those who are able to maintain asset quality at impressive levels)

would continue to find favour.

Chart 24: Price performance (relative to bankex) better for retail asset quality book

(15.0)

(3.2)

8.6

20.4

32.2

44.0

17.0

26.8

36.6

46.4

56.2

66.0

HD

FC

Ba

nk

Ko

tak

Ma

h.

Ind

usI

nd

ICIC

I Ba

nk

ING

Vy

sya

SIB

Fe

de

ral

Ax

is

(%)

(%)

Retail Proportion Price Performance (RHS) Source: Company, Edelweiss research

In conclusion, improving liability franchise and above average earnings growth at strong

return ratios will ensure that IIB will be able to bridge the gap in discount to HDFC Bank from

current levels of ~25% to 15% and trade 3.2x FY13E adjusted book, implying a target price of

INR380 – 16% upside on offer. We initiate coverage with ‘BUY/Sector Outpeformer’.

IIB has displayed capabilities to

ramp up ROEs in short span of

time

19 Edelweiss Securities Limited

Indusind Bank

Chart 25: Discount to HDFC Bank dipping as difference in ROA is declining

0.0

0.3

0.5

0.8

1.0

1.3

0.0

18.0

36.0

54.0

72.0

90.0

Jan

-08

Ap

r-0

8

Jul-

08

Oc

t-0

8

Jan

-09

Ap

r-0

9

Jul-

09

Oc

t-0

9

Jan

-10

Ap

r-1

0

Jul-

10

Oc

t-1

0

Jan

-11

Ap

r-1

1

Jul-

11

Oc

t-1

1

Jan

-12

Ap

r-1

2

(%)

(%)

Discount to HDFC Bank ROA differential to HDFC Bank (RHS) Source: Company, Edelweiss research

Table 1: Valuation snapshot

Rating CMP Mcap EPS CAGR (%)

(INR) (USD bn) FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E FY12-14E FY13E FY14E FY13E FY14E

Private Banks

Axis BUY 1,049 7.8 643 761 1.6 1.4 119 140 8.8 7.5 16.6 19.8 19.6 1.6 1.5

Federal BUY 431 1.3 353 414 1.2 1.0 51 64 8.5 6.8 18.5 14.3 16.0 1.4 1.5

HDFC Bank HOLD 539 22.8 147 174 3.7 3.1 26 33 20.7 16.2 22.8 19.9 20.5 1.9 2.0

ICICI Bank* BUY 659 17.2 513 569 1.3 1.2 66 77 10.0 8.6 16.8 12.0 12.8 1.6 1.7

ING Vysya BUY 343 0.9 266 320 1.3 1.1 34 43 10.0 8.0 18.4 11.5 13.9 1.1 1.1

South Indian HOLD 24 0.5 20 24 1.2 1.0 3 5 6.9 4.7 19.1 21.3 21.9 1.1 1.1

Yes BUY 345 2.2 163 201 2.1 1.7 35 43 9.8 8.1 24.5 22.2 23.5 1.6 1.5

IndusInd Bank BUY 328 2.8 118 141 2.8 2.3 21 27 15.5 12.2 25.1 19.2 20.4 1.6 1.7

Kotak REDUCE 574 7.7 192 220 3.0 2.6 26 31 22.0 18.6 18.3 14.8 15.2 2.4 2.4

ROA (%)ROE (%)Adj. BV P/ABV EPS (INR) P/E (x)

Source: Edelweiss research

Note: * Adjusted for subsidiaries

20 Edelweiss Securities Limited

Banking and Financial Services

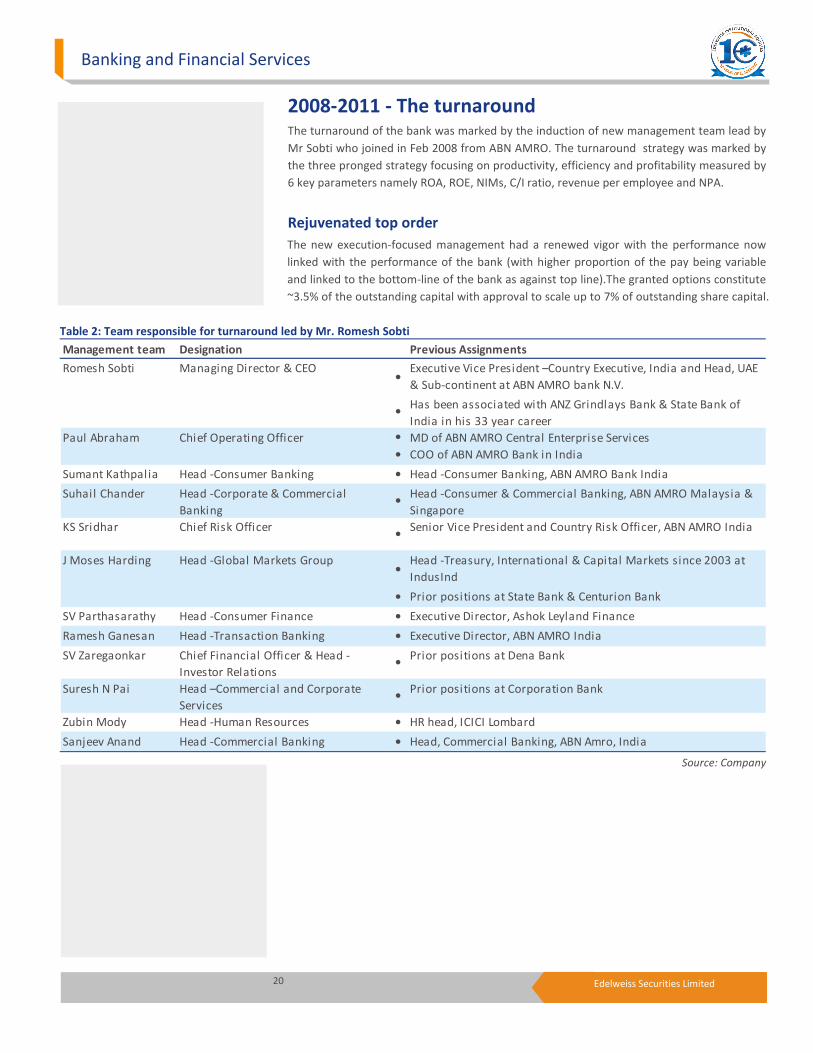

2008-2011 - The turnaround The turnaround of the bank was marked by the induction of new management team lead by

Mr Sobti who joined in Feb 2008 from ABN AMRO. The turnaround strategy was marked by

the three pronged strategy focusing on productivity, efficiency and profitability measured by

6 key parameters namely ROA, ROE, NIMs, C/I ratio, revenue per employee and NPA.

Rejuvenated top order

The new execution-focused management had a renewed vigor with the performance now

linked with the performance of the bank (with higher proportion of the pay being variable

and linked to the bottom-line of the bank as against top line).The granted options constitute

~3.5% of the outstanding capital with approval to scale up to 7% of outstanding share capital.

Table 2: Team responsible for turnaround led by Mr. Romesh Sobti

Management team Designation Previous Assignments

Romesh Sobti Managing Director & CEO�

Executive Vice President –Country Executive, India and Head, UAE

& Sub-continent at ABN AMRO bank N.V.

�Has been associated with ANZ Grindlays Bank & State Bank of

India in his 33 year career

Paul Abraham Chief Operating Officer � MD of ABN AMRO Central Enterprise Services

� COO of ABN AMRO Bank in India

Sumant Kathpalia Head -Consumer Banking � Head -Consumer Banking, ABN AMRO Bank India

Suhail Chander Head -Corporate & Commercial

Banking�

Head -Consumer & Commercial Banking, ABN AMRO Malaysia &

Singapore

KS Sridhar Chief Risk Officer�

Senior Vice President and Country Risk Officer, ABN AMRO India

J Moses Harding Head -Global Markets Group�

Head -Treasury, International & Capital Markets since 2003 at

IndusInd

� Prior positions at State Bank & Centurion Bank

SV Parthasarathy Head -Consumer Finance � Executive Director, Ashok Leyland Finance

Ramesh Ganesan Head -Transaction Banking � Executive Director, ABN AMRO India

SV Zaregaonkar Chief Financial Officer & Head -

Investor Relations�

Prior positions at Dena Bank

Suresh N Pai Head –Commercial and Corporate

Services�

Prior positions at Corporation Bank

Zubin Mody Head -Human Resources � HR head, ICICI Lombard

Sanjeev Anand Head -Commercial Banking � Head, Commercial Banking, ABN Amro, India

Source: Company

21 Edelweiss Securities Limited

Indusind Bank

Fig. 2: Key objectives and measurement metrics adopted by management

Ob

ject

ive

s

Me

asu

red

By

ProfitabilityRoA

Productivity

Efficiency

RoE

Net Interest Margins

Cost-to-Income Ratio

Revenue per Employee

Net NPAs

Source: Company

Fig. 3: Key steps taken by the bank

• Change in the structure of the organisation to boost profitability

• Ramped up workforce and branch network

• Improving liability side of balance sheet size

• Right pricing the asset book

• Introduction of risk management policies and framework

• Introduction of product suite , utilise existing client base and re-pricing of

products to boost revenue generation capability

• Building the brand

Source: Company, Edelweiss research

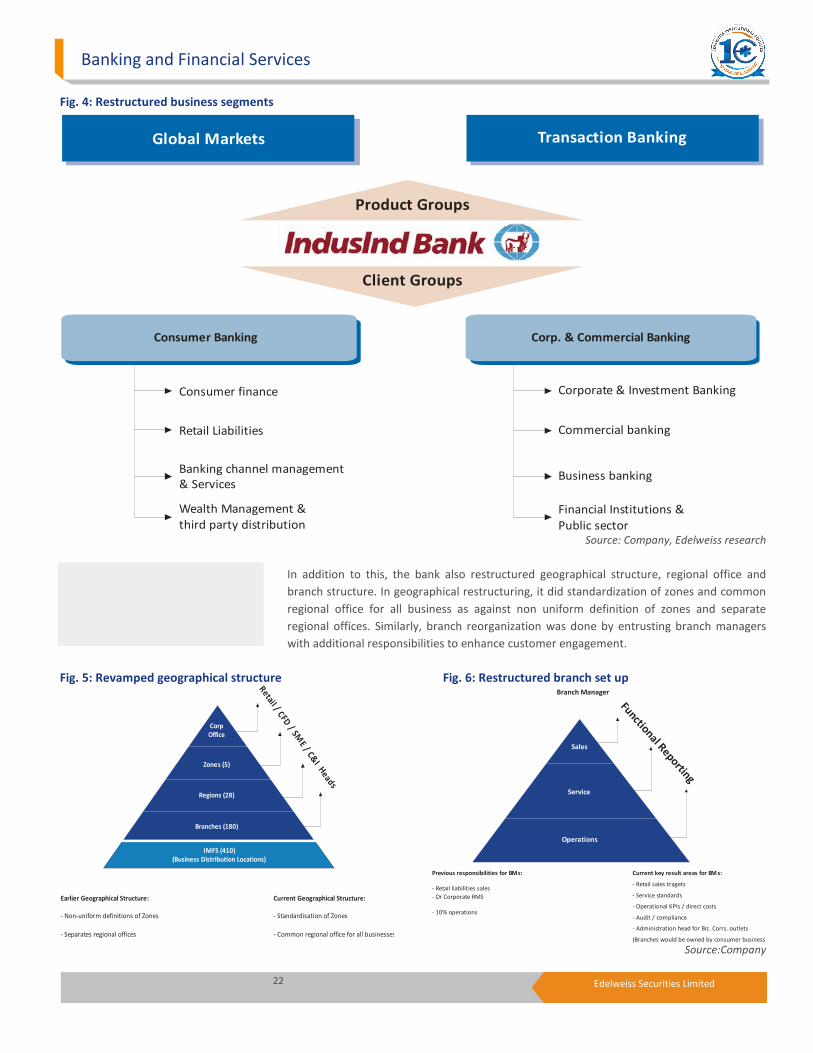

Change in organisational structure

The new management made a major revamp in the organization structure. The

reorganization was done into the client based units (consumer banking, corporate and

commercial banking) and product groups (global markets group, transaction banking group)

that work across various client groups to enhance focus, customer orientation and service

levels.

22 Edelweiss Securities Limited

Banking and Financial Services

Fig. 4: Restructured business segments

Global Markets Transaction Banking

Consumer Banking Corp. & Commercial Banking

Consumer finance

Retail Liabilities

Banking channel management

& Services

Wealth Management &

third party distribution

Corporate & Investment Banking

Commercial banking

Business banking

Financial Institutions &

Public sector

Product Groups

Client Groups

Source: Company, Edelweiss research

In addition to this, the bank also restructured geographical structure, regional office and

branch structure. In geographical restructuring, it did standardization of zones and common

regional office for all business as against non uniform definition of zones and separate

regional offices. Similarly, branch reorganization was done by entrusting branch managers

with additional responsibilities to enhance customer engagement.

Fig. 5: Revamped geographical structure Fig. 6: Restructured branch set up

IMFS (410)

(Business Distribution Locations)

Branches (180)

Regions (28)

Zones (5)

Corp

Office

Retail / CFD / SM

E / C&I H

eads

Earlier Geographical Structure:

- Non-uniform definitions of Zones

- Separates regional offices

Current Geographical Structure:

- Standardisation of Zones

- Common regional office for all businesses

Source:Company

Operations

Service

Sales

Functional Reporting

Previous responsibilities for B s:M

- Retail liabilities sales

- Or Corporate RMS

- 10% operations

Current key result areas for B s:M

- Retail sales tragets

- Service standards

- Operational KPIs / direct costs

- Audit / compliance

- Administration head for Biz. Corrs. outlets

(Branches would be owned by consumer business)

Branch Manager

23 Edelweiss Securities Limited

Indusind Bank

Energising the workforce

The bank added new workforce especially on the client facing roles to match its business

expansion initiatives. Introduction of performance linked /variable pay in line with industry

best practices enabled the bank to attract talent with majority of the pool being drawn from

peer banks and foreign banks. As a result, number of employees increased significantly from

2869 in FY08 to 7008 in FY11.

Improving liability side of balance sheet

Building CASA

1) Launching of new product suite

2) Specialised team for CASA expansion

3) Focus on propriety and small business

4) Restructuring branch network

Realization of term deposits

Increased focus on below INR1.5mn

accounts

Broad basing wholesale deposits

Set up teams to tap corporative banks and PSUs to increase client base for such

deposits

Tenor mapping

Focus on well matched short term loans to mitigate this risk

Improving Liability side of Balance Sheet

Source: Company

Right-pricing the asset book

The new management adopted a strategy to rightly price its asset book by: 1) Differential

risk-based loan pricing for each customer segments; 2) increasing focus on small business

and mid corporate; 3) gaining strong traction in high yielding consumer finance division; 4)

churning old loans with new higher yielding loans; and 5) focusing on priority sector lending,

thereby achieving the RBI prescribed targets (thus, not having to invest in low-yield RIDF

bonds).

Revamping risk organisation

Asset quality has been key focus area for the new management across both corporate and

commercial banking book and consumer financing book. In CF book, the bank took

aggressive move to clean up the books, better risk management practices (has set up

centralized risk and strong risk management functions) and leveraged on its strong domain

knowledge (as a result of merger with ALFL). In addition to this vehicle loans were only

sourced by banks own branches and agents under IMFSL * (which has better knowledge of

customer profile and better collection efficiency) rather than through DSA route thus

improving the asset quality.

*Note IMFSL is IndusInd Marketing and Financial Services Limited

24 Edelweiss Securities Limited

Banking and Financial Services

Revenue generation capability

Prior to FY08 the banks poor profitability was due to low income generation capability. The

non interest income generation was also weak because of its limited product suite. This

prompted management to broaden the fee income base and increase its contribution to

bank’s bottom-line. The new management under took several steps to build its capabilities in

corporate and investment banking space and in the fee based product space.

Fig. 7: Steps taken to enhance revenue generation capabilities

New product group to

increse the product suite

• Introduction of two

groups

• Transaction banking

• Cash Management

• Trade and Financing

• Supply Chain Financing

• Global Remitances

• Commodity

Financing

• Global Market Group

• Corporate Forex

• Propriety Trading

• Money and Capital Market services

Leveraging the existing

customer base

• Focus on cross selling

of products

• Use of relationship manager and managed

sales to increase

customer engagement

• Enhanced loan

processing charges and fee from transactional

services

Improved pricing power

• Realignment of pricing

of its basic products

• Demand drafts

• Lockers

• Increased focus on building momentum in

third party sales

• Insurance

• Mutual funds

Source: Company

Branding

Fig. 8: Campaigns launched in various media to increase brand visibility

Source: Company

25 Edelweiss Securities Limited

Indusind Bank

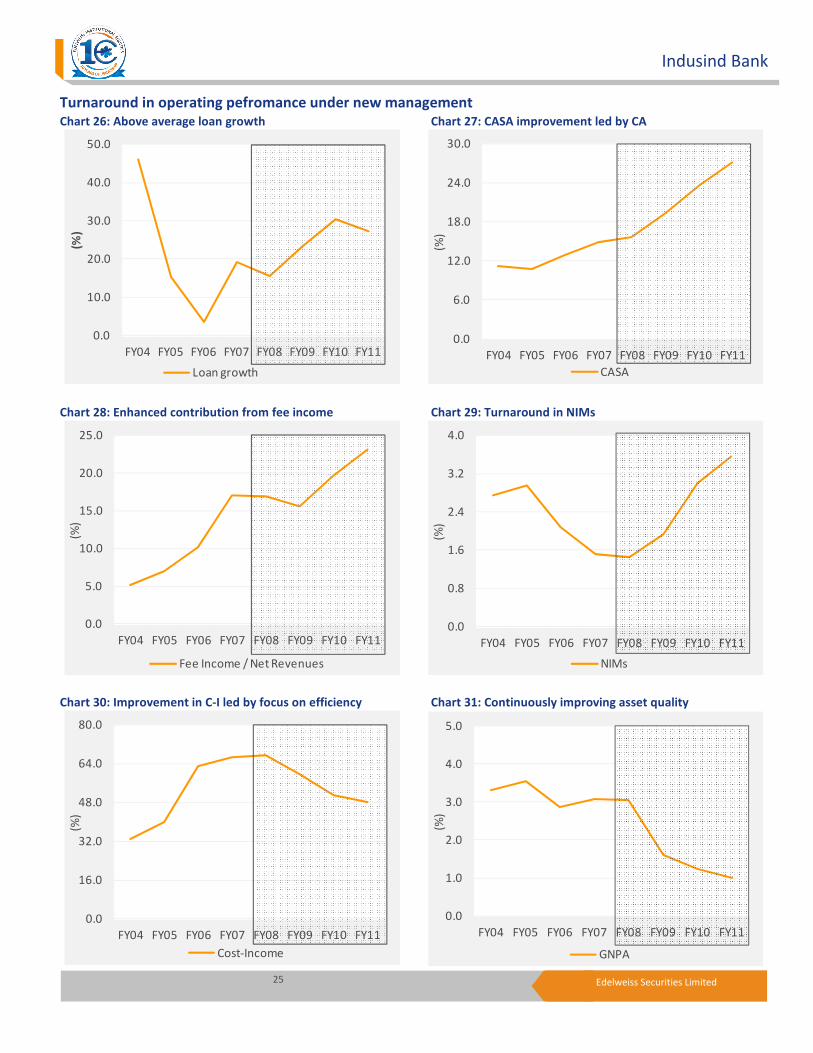

Turnaround in operating pefromance under new management

Chart 26: Above average loan growth Chart 27: CASA improvement led by CA

0.0

10.0

20.0

30.0

40.0

50.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

(%)

Loan growth Chart 28: Enhanced contribution from fee income Chart 29: Turnaround in NIMs

0.0

5.0

10.0

15.0

20.0

25.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

(%)

Fee Income / Net Revenues

Chart 30: Improvement in C-I led by focus on efficiency Chart 31: Continuously improving asset quality

0.0

16.0

32.0

48.0

64.0

80.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

(%)

Cost-Income

0.0

6.0

12.0

18.0

24.0

30.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

(%)

CASA

0.0

0.8

1.6

2.4

3.2

4.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

(%)

NIMs

0.0

1.0

2.0

3.0

4.0

5.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

(%)

GNPA

26 Edelweiss Securities Limited

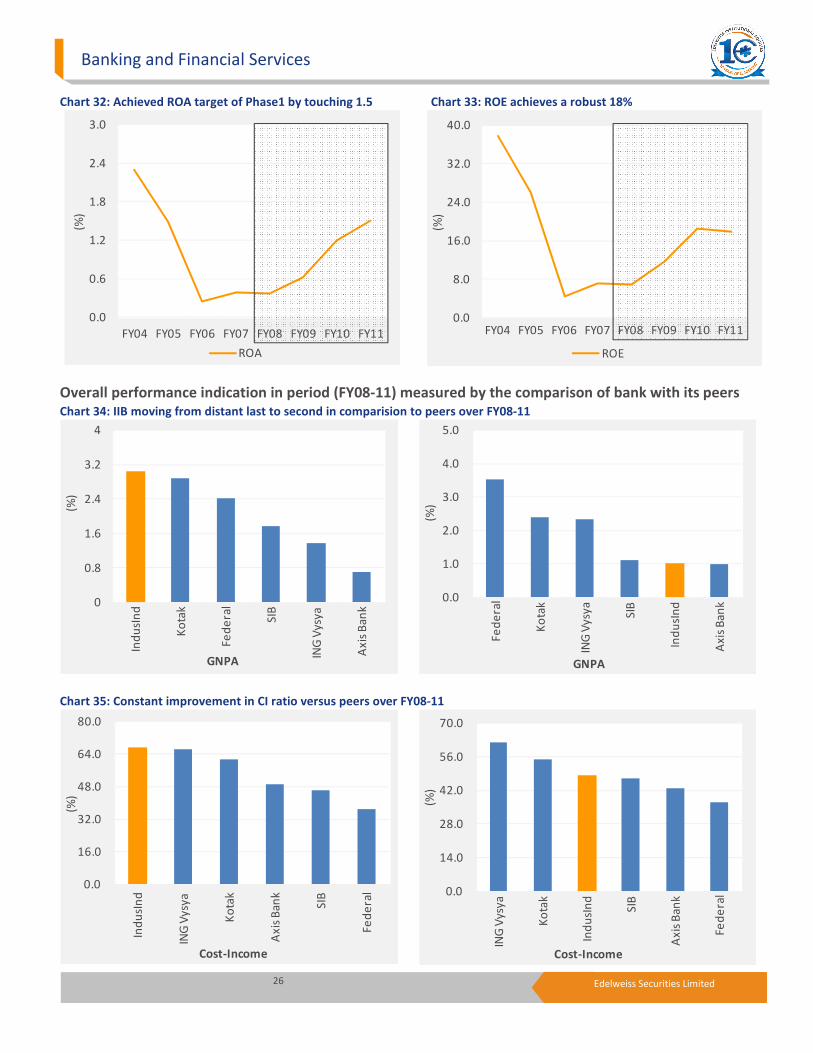

Banking and Financial Services

Chart 32: Achieved ROA target of Phase1 by touching 1.5 Chart 33: ROE achieves a robust 18%

0.0

0.6

1.2

1.8

2.4

3.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

(%)

ROA

Overall performance indication in period (FY08-11) measured by the comparison of bank with its peers Chart 34: IIB moving from distant last to second in comparision to peers over FY08-11

0

0.8

1.6

2.4

3.2

4

Ind

usI

nd

Ko

tak

Fe

de

ral

SIB

ING

Vy

sya

Ax

is B

an

k

(%)

GNPA

Chart 35: Constant improvement in CI ratio versus peers over FY08-11

0.0

16.0

32.0

48.0

64.0

80.0

Ind

usI

nd

ING

Vy

sya

Ko

tak

Ax

is B

an

k

SIB

Fe

de

ral

(%)

Cost-Income

0.0

1.0

2.0

3.0

4.0

5.0

Fe

de

ral

Ko

tak

ING

Vy

sya

SIB

Ind

usI

nd

Ax

is B

an

k

(%)

GNPA

0.0

14.0

28.0

42.0

56.0

70.0

ING

Vy

sya

Ko

tak

Ind

usI

nd

SIB

Ax

is B

an

k

Fe

de

ral

(%)

Cost-Income

0.0

8.0

16.0

24.0

32.0

40.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

(%)

ROE

27 Edelweiss Securities Limited

Indusind Bank

Chart 36: Drastic improvement in CASA/branch vis-à-vis peers over FY08-11

58

194

330

466

602

738A

xis

Ba

nk

Ko

tak

Ind

usI

nd

ING

Vy

sya

Fe

de

ral

SIB

(IN

R m

n)

CASA/Branch

Chart 37: Sustained improvemt in margins over FY08-11

0.0

1.2

2.4

3.6

4.8

6.0

Ko

tak

Fe

de

ral

Ax

is B

an

k

SIB

ING

Vy

sya

Ind

usI

nd

(%)

NIMs

Chart 38: ROA moving from a distant last to third in comparison with peers over FY08-11

0.0

0.4

0.8

1.2

1.6

2.0

Fe

de

ral

Ko

tak

Ax

is B

an

k

SIB

ING

Vy

sya

Ind

usI

nd

(%)

ROA

Source:Company

0

120

240

360

480

600

Ax

is B

an

k

Ind

usI

nd

Ko

tak

Fe

de

ral

ING

Vy

sya

SIB

(IN

R m

n)

CASA/Branch

2.0

3.0

4.0

5.0

6.0

7.0

Ko

tak

Fe

de

ral

Ind

usI

nd

Ax

is B

an

k

ING

Vy

sya

SIB

(%)

NIMs

0.0

0.5

1.0

1.5

2.0

2.5

Ko

tak

Ax

is B

an

k

Ind

usI

nd

Fe

de

ral

SIB

ING

Vy

sya

(%)

ROA

28 Edelweiss Securities Limited

Banking and Financial Services

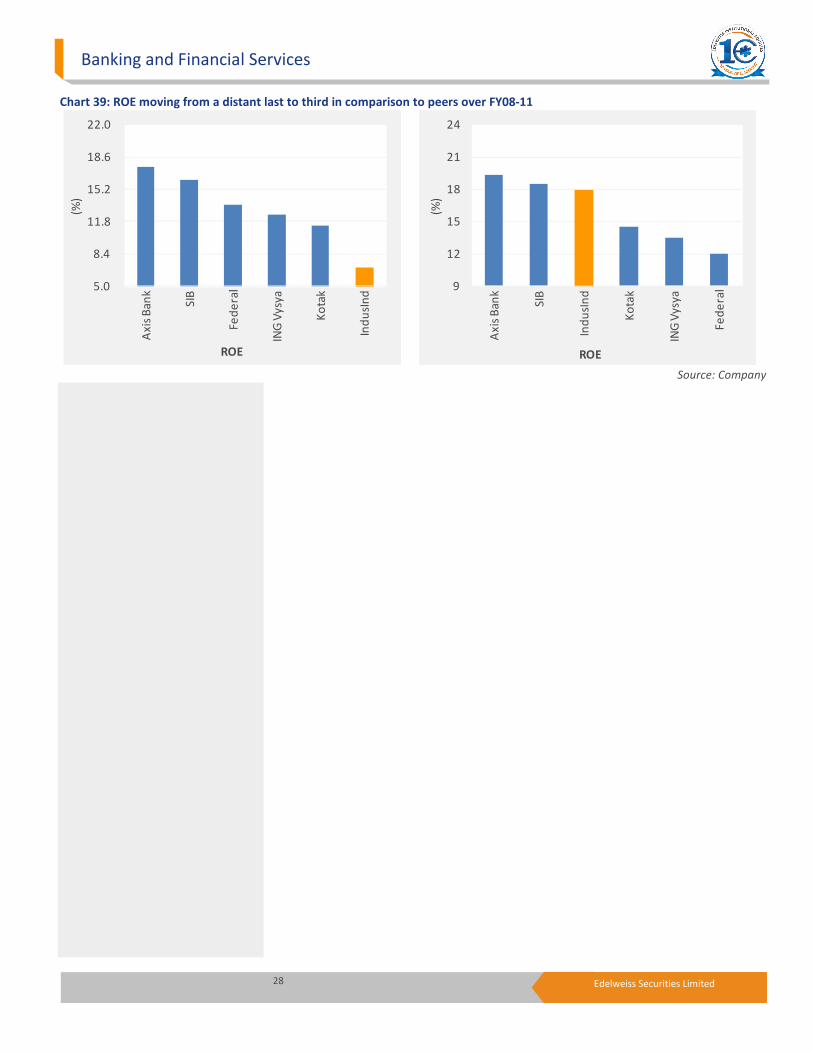

Chart 39: ROE moving from a distant last to third in comparison to peers over FY08-11

5.0

8.4

11.8

15.2

18.6

22.0

Ax

is B

an

k

SIB

Fe

de

ral

ING

Vy

sya

Ko

tak

Ind

usI

nd

(%)

ROE

Source: Company

9

12

15

18

21

24

Ax

is B

an

k

SIB

Ind

usI

nd

Ko

tak

ING

Vy

sya

Fe

de

ral

(%)

ROE

29 Edelweiss Securities Limited

Indusind Bank

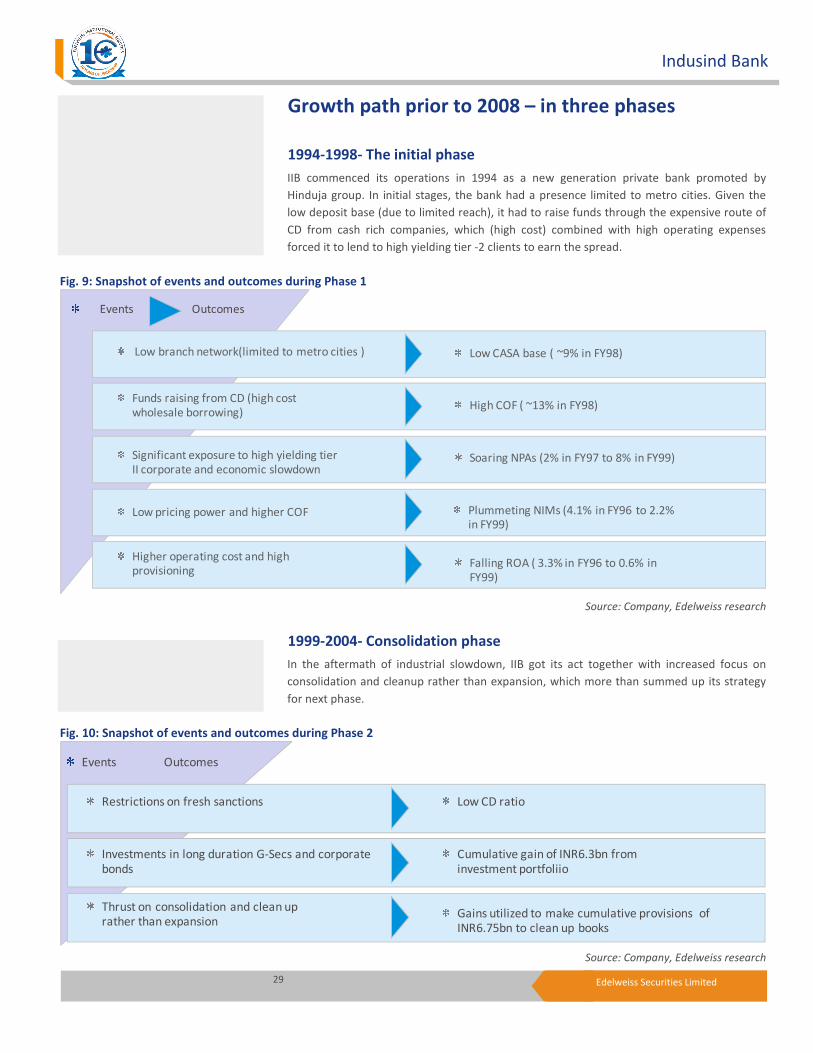

Growth path prior to 2008 – in three phases

1994-1998- The initial phase

IIB commenced its operations in 1994 as a new generation private bank promoted by

Hinduja group. In initial stages, the bank had a presence limited to metro cities. Given the

low deposit base (due to limited reach), it had to raise funds through the expensive route of

CD from cash rich companies, which (high cost) combined with high operating expenses

forced it to lend to high yielding tier -2 clients to earn the spread.

Fig. 9: Snapshot of events and outcomes during Phase 1

Events Outcomes

Low branch network(limited to metro cities )

Funds raising from CD (high cost

wholesale borrowing)

Significant exposure to high yielding tier

II corporate and economic slowdown

Low pricing power and higher COF

Higher operating cost and high

provisioning

Low CASA base ( ~9% in FY98)

High COF ( ~13% in FY98)

Soaring NPAs (2% in FY97 to 8% in FY99)

Plummeting NIMs (4.1% in FY96 to 2.2%

in FY99)

Falling ROA ( 3.3% in FY96 to 0.6% in

FY99)

Source: Company, Edelweiss research

1999-2004- Consolidation phase

In the aftermath of industrial slowdown, IIB got its act together with increased focus on

consolidation and cleanup rather than expansion, which more than summed up its strategy

for next phase.

Fig. 10: Snapshot of events and outcomes during Phase 2

Events Outcomes

Restrictions on fresh sanctions

Investments in long duration G-Secs and corporate

bonds

Thrust on consolidation and clean up rather than expansion

Low CD ratio

Cumulative gain of INR6.3bn from

investment portfoliio

Gains utilized to make cumulative provisions of INR6.75bn to clean up books

Source: Company, Edelweiss research

30 Edelweiss Securities Limited

Banking and Financial Services

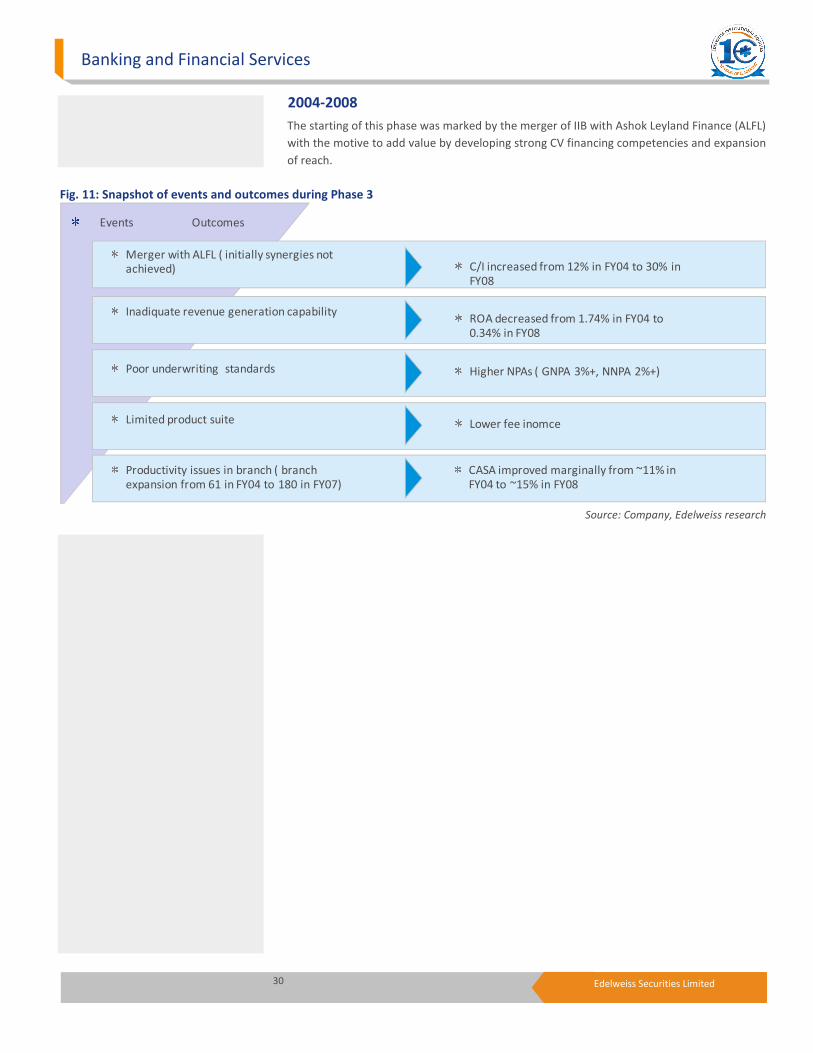

2004-2008

The starting of this phase was marked by the merger of IIB with Ashok Leyland Finance (ALFL)

with the motive to add value by developing strong CV financing competencies and expansion

of reach.

Fig. 11: Snapshot of events and outcomes during Phase 3

Events Outcomes

Merger with ALFL ( initially synergies not

achieved)

Inadiquate revenue generation capability

Poor underwriting standards

Limited product suite

Productivity issues in branch ( branch

expansion from 61 in FY04 to 180 in FY07)

C/I increased from 12% in FY04 to 30% in

FY08

ROA decreased from 1.74% in FY04 to

0.34% in FY08

Higher NPAs ( GNPA 3%+, NNPA 2%+)

Lower fee inomce

CASA improved marginally from ~11% in

FY04 to ~15% in FY08

Source: Company, Edelweiss research

31 Edelweiss Securities Limited

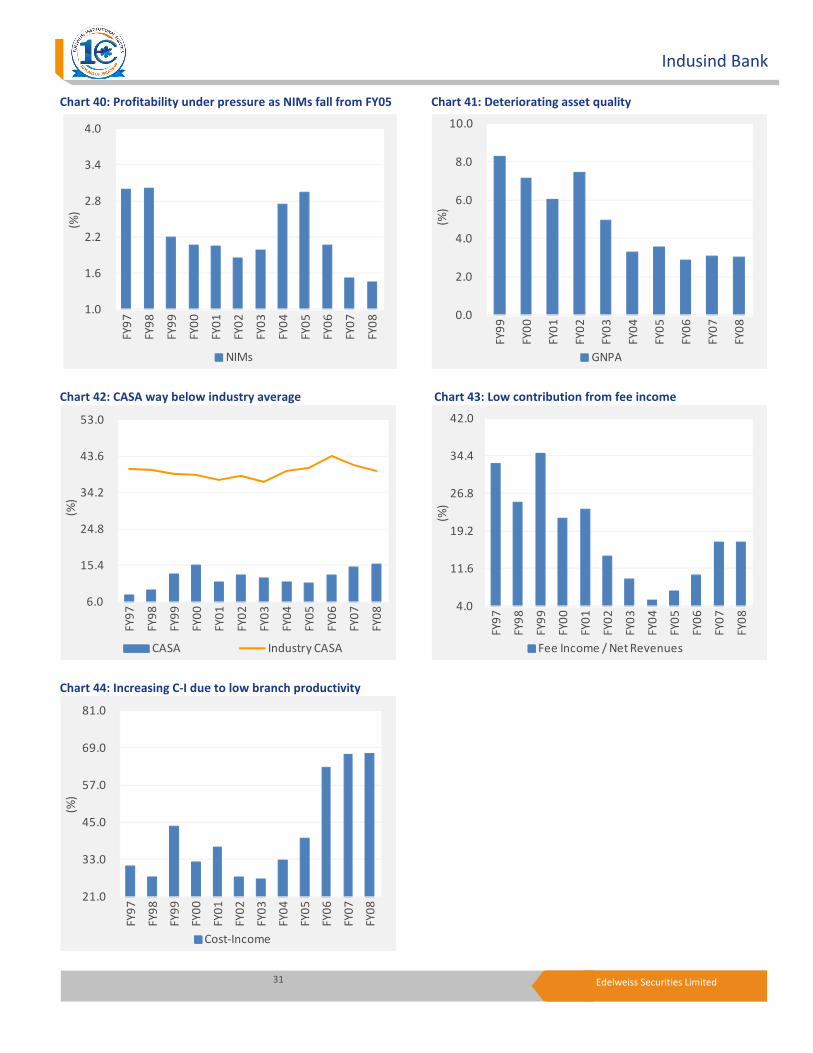

Indusind Bank

Chart 40: Profitability under pressure as NIMs fall from FY05 Chart 41: Deteriorating asset quality

1.0

1.6

2.2

2.8

3.4

4.0 F

Y9

7

FY

98

FY

99

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

(%)

NIMs Chart 42: CASA way below industry average Chart 43: Low contribution from fee income

6.0

15.4

24.8

34.2

43.6

53.0

FY

97

FY

98

FY

99

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

(%)

CASA Industry CASA Chart 44: Increasing C-I due to low branch productivity

21.0

33.0

45.0

57.0

69.0

81.0

FY

97

FY

98

FY

99

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

(%)

Cost-Income

0.0

2.0

4.0

6.0

8.0

10.0

FY

99

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

(%)

GNPA

4.0

11.6

19.2

26.8

34.4

42.0

FY

97

FY

98

FY

99

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

(%)

Fee Income / Net Revenues

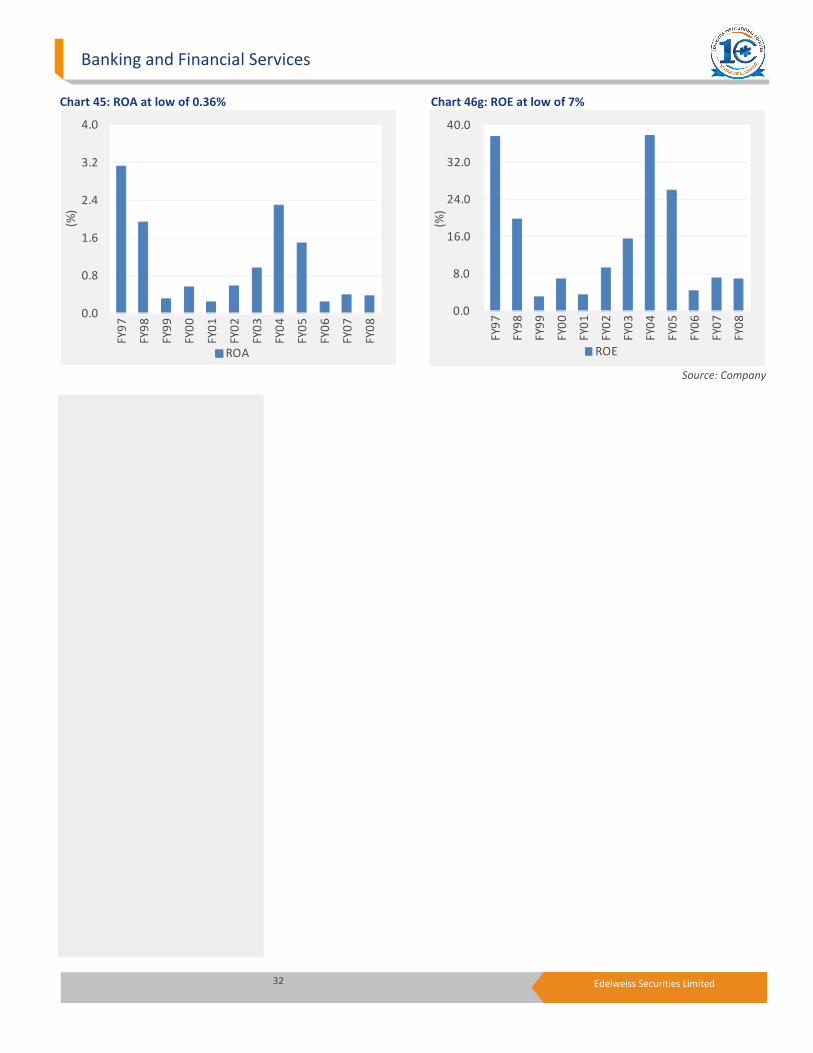

32 Edelweiss Securities Limited

Banking and Financial Services

Chart 45: ROA at low of 0.36% Chart 46g: ROE at low of 7%

0.0

0.8

1.6

2.4

3.2

4.0F

Y9

7

FY

98

FY

99

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

(%)

ROA Source: Company

0.0

8.0

16.0

24.0

32.0

40.0

FY

97

FY

98

FY

99

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

(%)

ROE

33 Edelweiss Securities Limited

Indusind Bank

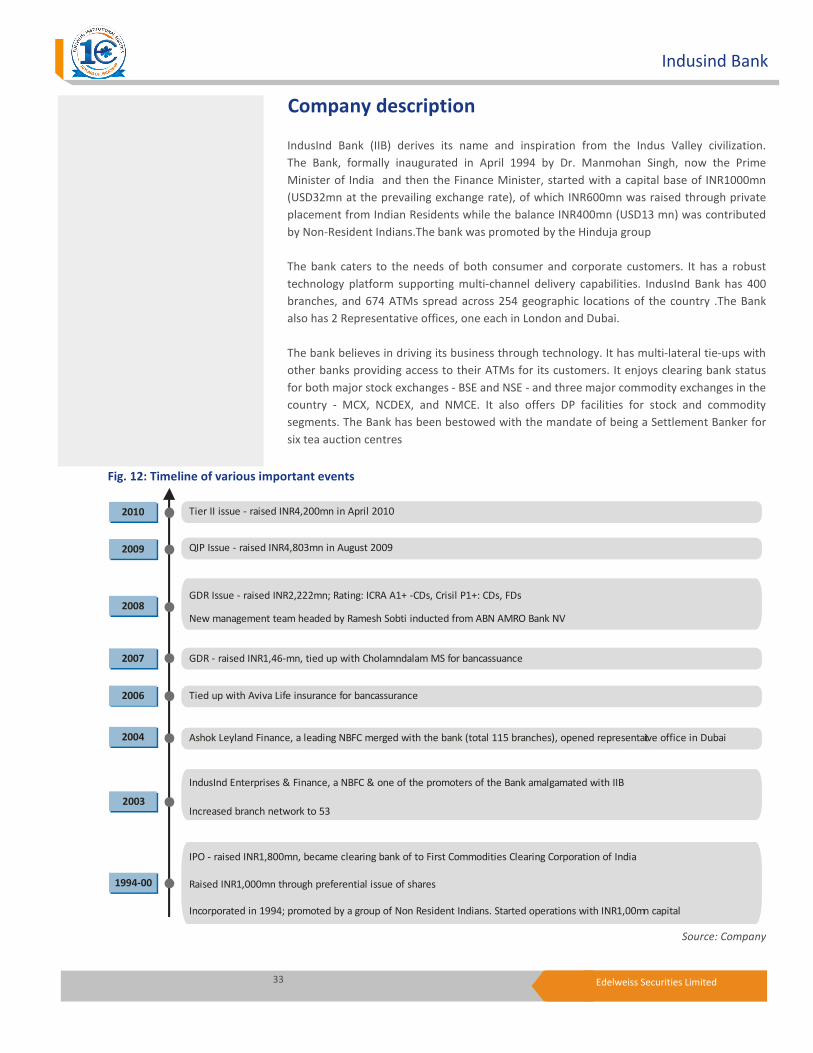

Company description

IndusInd Bank (IIB) derives its name and inspiration from the Indus Valley civilization.

The Bank, formally inaugurated in April 1994 by Dr. Manmohan Singh, now the Prime

Minister of India and then the Finance Minister, started with a capital base of INR1000mn

(USD32mn at the prevailing exchange rate), of which INR600mn was raised through private

placement from Indian Residents while the balance INR400mn (USD13 mn) was contributed

by Non-Resident Indians.The bank was promoted by the Hinduja group

The bank caters to the needs of both consumer and corporate customers. It has a robust

technology platform supporting multi-channel delivery capabilities. IndusInd Bank has 400

branches, and 674 ATMs spread across 254 geographic locations of the country .The Bank

also has 2 Representative offices, one each in London and Dubai.

The bank believes in driving its business through technology. It has multi-lateral tie-ups with

other banks providing access to their ATMs for its customers. It enjoys clearing bank status

for both major stock exchanges - BSE and NSE - and three major commodity exchanges in the

country - MCX, NCDEX, and NMCE. It also offers DP facilities for stock and commodity

segments. The Bank has been bestowed with the mandate of being a Settlement Banker for

six tea auction centres

Fig. 12: Timeline of various important events

Tier II issue - raised INR4,200mn in April 2010

QIP Issue - raised INR4,803mn in August 2009

GDR Issue - raised INR2,222mn; Rating: ICRA A1+ -CDs, Crisil P1+: CDs, FDs

New management team headed by Ramesh Sobti inducted from ABN AMRO Bank NV

GDR - raised INR1,46-mn, tied up with Cholamndalam MS for bancassuance

Tied up with Aviva Life insurance for bancassurance

Ashok Leyland Finance, a leading NBFC merged with the bank (total 115 branches), opened representative office in Dubai

IndusInd Enterprises & Finance, a NBFC & one of the promoters of the Bank amalgamated with IIB

Increased branch network to 53

IPO - raised INR1,800mn, became clearing bank of to First Commodities Clearing Corporation of India

Raised INR1,000mn through preferential issue of shares

Incorporated in 1994; promoted by a group of Non Resident Indians. Started operations with INR1,00mn capital

2010

2009

2008

2007

2006

2004

2003

1994-00

Source: Company

34 Edelweiss Securities Limited

Banking and Financial Services

Keys risks

� The bank plans to achieve the desired CASA growth by expanding its branch network

from a current level of 400 branches to 650 branches by FY14E. Risk emanates from the

fact that if the bank is not able to achieve the desired level of integration among

branches then cost may shoot up.

• A major risk that the bank is facing is human capital risk. With most of the core team

members coming from ABN, a unique concentration of employees have been created.

Thus, when Mr Romesh Sobti leaves or retires and if this team also moves away for

some reason, there is risk of a huge human capital crunch situation.

• The promoter stake in the bank is currently high at ~20% and needs to be pruned down

to 10% by December 2012 (RBI directive). This poses dilution risk for the bank.

35 Edelweiss Securities Limited

Indusind Bank

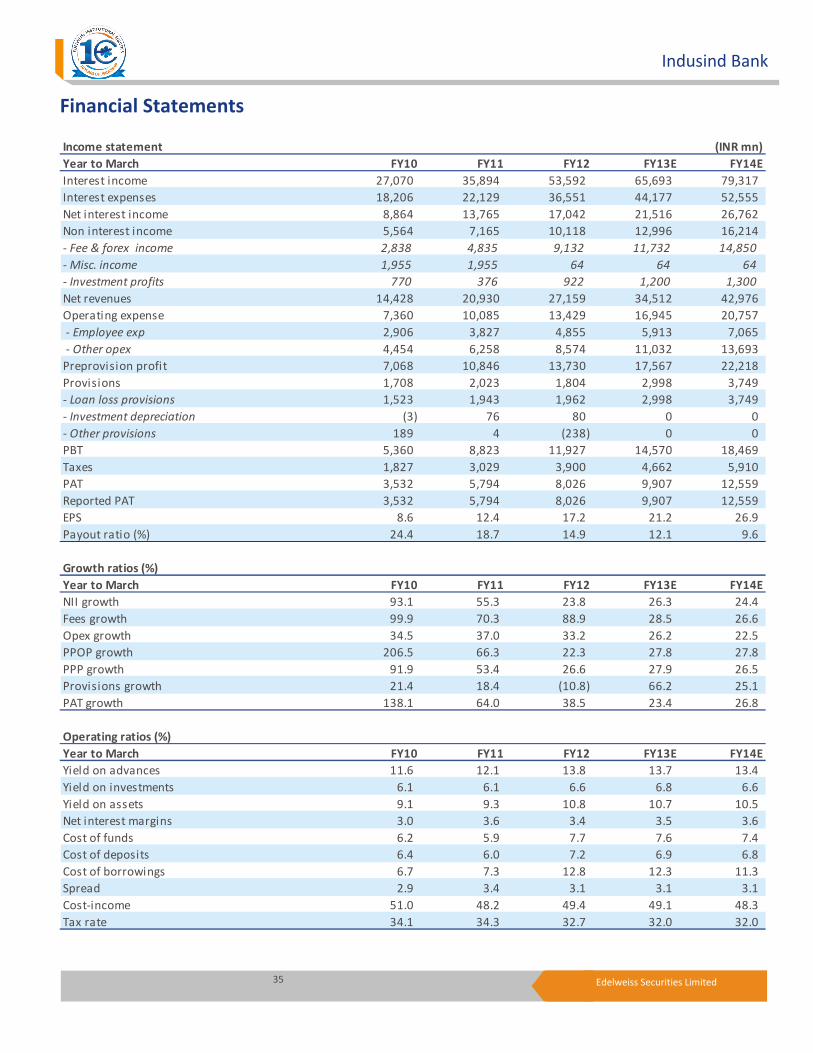

Financial Statements Income statement (INR mn)

Year to March FY10 FY11 FY12 FY13E FY14E

Interest income 27,070 35,894 53,592 65,693 79,317

Interest expenses 18,206 22,129 36,551 44,177 52,555

Net interest income 8,864 13,765 17,042 21,516 26,762

Non interest income 5,564 7,165 10,118 12,996 16,214

- Fee & forex income 2,838 4,835 9,132 11,732 14,850

- Misc. income 1,955 1,955 64 64 64

- Investment profits 770 376 922 1,200 1,300

Net revenues 14,428 20,930 27,159 34,512 42,976

Operating expense 7,360 10,085 13,429 16,945 20,757

- Employee exp 2,906 3,827 4,855 5,913 7,065

- Other opex 4,454 6,258 8,574 11,032 13,693

Preprovision profit 7,068 10,846 13,730 17,567 22,218

Provisions 1,708 2,023 1,804 2,998 3,749

- Loan loss provisions 1,523 1,943 1,962 2,998 3,749

- Investment depreciation (3) 76 80 0 0

- Other provisions 189 4 (238) 0 0

PBT 5,360 8,823 11,927 14,570 18,469

Taxes 1,827 3,029 3,900 4,662 5,910

PAT 3,532 5,794 8,026 9,907 12,559

Reported PAT 3,532 5,794 8,026 9,907 12,559

EPS 8.6 12.4 17.2 21.2 26.9

Payout ratio (%) 24.4 18.7 14.9 12.1 9.6

Growth ratios (%)

Year to March FY10 FY11 FY12 FY13E FY14E

NII growth 93.1 55.3 23.8 26.3 24.4

Fees growth 99.9 70.3 88.9 28.5 26.6

Opex growth 34.5 37.0 33.2 26.2 22.5

PPOP growth 206.5 66.3 22.3 27.8 27.8

PPP growth 91.9 53.4 26.6 27.9 26.5

Provisions growth 21.4 18.4 (10.8) 66.2 25.1

PAT growth 138.1 64.0 38.5 23.4 26.8

Operating ratios (%)

Year to March FY10 FY11 FY12 FY13E FY14E

Yield on advances 11.6 12.1 13.8 13.7 13.4

Yield on investments 6.1 6.1 6.6 6.8 6.6

Yield on assets 9.1 9.3 10.8 10.7 10.5

Net interest margins 3.0 3.6 3.4 3.5 3.6

Cost of funds 6.2 5.9 7.7 7.6 7.4

Cost of deposits 6.4 6.0 7.2 6.9 6.8

Cost of borrowings 6.7 7.3 12.8 12.3 11.3

Spread 2.9 3.4 3.1 3.1 3.1

Cost-income 51.0 48.2 49.4 49.1 48.3

Tax rate 34.1 34.3 32.7 32.0 32.0

36 Edelweiss Securities Limited

Banking and Financial Services

Balance sheet (INR mn)

Year to March FY10 FY11 FY12E FY13E FY14E

Liabilities

Equity capital 4,107 4,660 4,677 4,677 4,677

Reserves 17,550 33,589 42,631 51,338 62,697

Net worth 21,656 38,249 47,308 56,015 67,374

Sub bonds/pref cap 0 0 600 1,100 1,600

Deposits 267,102 343,654 423,616 518,931 639,849

Borrowings 49,343 55,254 86,220 103,853 129,771

Other l iabil ities 13,278 17,496 18,108 11,551 14,274

Total 351,379 454,652 575,851 691,450 852,868

Assets

Loans 205,506 261,657 350,640 438,299 547,874

Gilts 85,251 100,219 99,876 124,557 153,924

Others 18,768 35,290 45,844 50,577 55,832

Cash & equi 26,032 40,246 55,396 59,627 73,567

Fixed assets 4,132 3,711 6,459 7,139 7,767

Other assets 11,691 13,531 17,638 11,251 13,903

Total 351,379 454,652 575,851 691,450 852,868

Balance sheet ratios (%)

Credit growth 30.3 27.7 34.0 25.0 25.0

Deposit growth 20.8 28.7 23.3 22.5 23.3

EA growth 30.2 30.4 26.1 22.0 23.5

SLR ratio 26.9 25.1 19.6 20.0 20.0

C-D ratio 77.0 76.4 83.1 84.8 85.9

Low-cost deposits 23.7 27.2 27.3 31.0 33.0

Gross NPA ratio 1.2 1.0 1.0 1.1 1.2

Net NPA ratio 0.5 0.3 0.3 0.3 0.3

Provision coverage 60.1 72.6 72.7 72.5 72.0

Incremental sl ippage 1.4 0.9 1.4 1.5 1.5

Net NPA / Equity 4.7 1.9 2.0 2.4 2.8

Capital adequacy 15.3 15.9 13.9 13.4 12.9

- Tier 1 9.7 12.3 11.4 10.9 10.4

Book value 52.7 82.1 101.1 119.8 144.1

ROA decomposition (%)

Year to March FY10 FY11 FY12E FY13E FY14E

Net interest income/Assets 3.0 3.6 3.4 3.5 3.6

Fees/Assets 1.6 1.8 1.9 1.9 2.0

Investment profits/Assets 0.3 0.1 0.2 0.2 0.2

Net revenues/Assets 4.9 5.4 5.5 5.6 5.7

Operating expense/Assets (2.5) (2.6) (2.7) (2.8) (2.8)

Provisions/Assets (0.6) (0.5) (0.4) (0.5) (0.5)

Taxes/Assets (0.6) (0.8) (0.8) (0.8) (0.8)

Total costs/Assets (3.7) (3.9) (3.9) (4.0) (4.0)

ROA 1.2 1.5 1.6 1.6 1.7

Equity/Assets 6.1 7.7 8.6 8.4 8.2

ROAE 19.7 19.3 18.8 19.2 20.4

37 Edelweiss Securities Limited

Indusind Bank

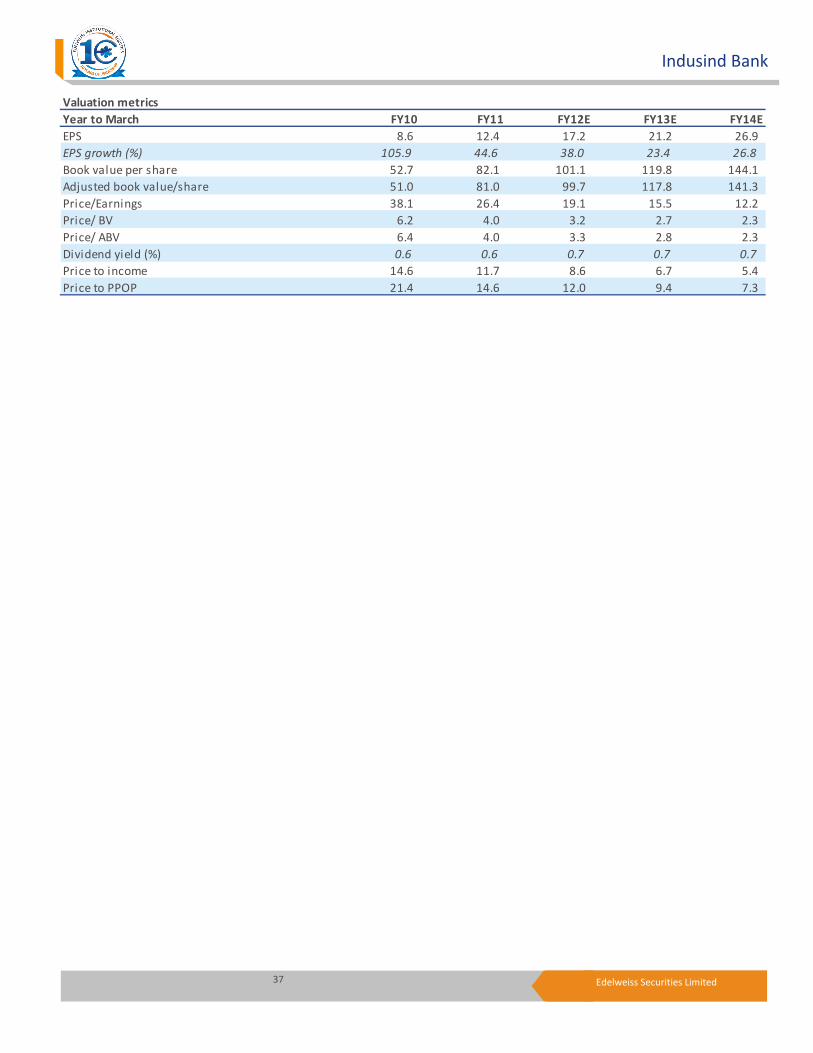

Valuation metrics

Year to March FY10 FY11 FY12E FY13E FY14E

EPS 8.6 12.4 17.2 21.2 26.9

EPS growth (%) 105.9 44.6 38.0 23.4 26.8

Book value per share 52.7 82.1 101.1 119.8 144.1

Adjusted book value/share 51.0 81.0 99.7 117.8 141.3

Price/Earnings 38.1 26.4 19.1 15.5 12.2

Price/ BV 6.2 4.0 3.2 2.7 2.3

Price/ ABV 6.4 4.0 3.3 2.8 2.3

Dividend yield (%) 0.6 0.6 0.7 0.7 0.7

Price to income 14.6 11.7 8.6 6.7 5.4

Price to PPOP 21.4 14.6 12.0 9.4 7.3

38 Edelweiss Securities Limited

Banking and Financial Services

Company Absolute

reco

Relative

reco

Relative

risk

Company Absolute

reco

Relative

reco

Relative

Risk

Allahabad Bank REDUCE SU H Axis Bank BUY SO M

Bank of Baroda HOLD SP L Federal Bank BUY SO M

HDFC HOLD SP L HDFC Bank HOLD SP L

ICICI Bank BUY SO L Indian Overseas Bank HOLD SU H

Infrastructure Development Finance Co

Ltd

BUY SO M ING Vysya BUY SO M

Karnataka Bank BUY SO L Kotak Mahindra Bank REDUCE SU L

LIC Housing Finance HOLD SP M Mahindra & Mahindra Financial

Services

BUY SO M

Manappuram General Finance HOLD SU M Multi Commodity Exchange BUY SO M

Power Finance Corp BUY SO L Oriental Bank Of Commerce BUY SO H

Reliance Capital BUY SO M Punjab National Bank REDUCE SU M

Shriram City Union Finance BUY SO H Rural Electrification Corporation BUY SO L

State Bank of India HOLD SP M South Indian Bank HOLD SP M

Yes Bank BUY SO M Union Bank Of India HOLD SP H

RATING & INTERPRETATION

ABSOLUTE RATING

Ratings Expected absolute returns over 12 months

Buy More than 15%

Hold Between 15% and - 5%

Reduce Less than -5%

RELATIVE RETURNS RATING

Ratings Criteria

Sector Outperformer (SO) Stock return > 1.25 x Sector return

Sector Performer (SP) Stock return > 0.75 x Sector return

Stock return < 1.25 x Sector return

Sector Underperformer (SU) Stock return < 0.75 x Sector return

Sector return is market cap weighted average return for the coverage universe

within the sector

RELATIVE RISK RATING

Ratings Criteria

Low (L) Bottom 1/3rd percentile in the sector

Medium (M) Middle 1/3rd percentile in the sector

High (H) Top 1/3rd percentile in the sector

Risk ratings are based on Edelweiss risk model

SECTOR RATING

Ratings Criteria

Overweight (OW) Sector return > 1.25 x Nifty return

Equalweight (EW) Sector return > 0.75 x Nifty return

Sector return < 1.25 x Nifty return

Underweight (UW) Sector return < 0.75 x Nifty return

39 Edelweiss Securities Limited

Indusind Bank

Edelweiss Securities Limited, Edelweiss House, off C.S.T. Road, Kalina, Mumbai – 400 098.

Board: (91-22) 4009 4400, Email: [email protected]

Vikas Khemani Head Institutional Equities [email protected] +91 22 2286 4206

Nischal Maheshwari Co-Head Institutional Equities & Head, Research [email protected] +91 22 4063 5476

Nirav Sheth Head Sales [email protected] +91 22 4040 7499

Coverage group(s) of stocks by primary analyst(s): Banking and Financial Services

Allahabad Bank, Axis Bank, Bank of Baroda, Federal Bank, HDFC, HDFC Bank, ICICI Bank, Infrastructure Development Finance Co Ltd, Indian Overseas Bank,

Karnataka Bank, Kotak Mahindra Bank, LIC Housing Finance, Manappuram General Finance, Mahindra & Mahindra Financial Services, Oriental Bank Of

Commerce, Punjab National Bank, Power Finance Corp, Reliance Capital, Rural Electrification Corporation, State Bank of India, Shriram City Union Finance,

South Indian Bank, Union Bank Of India, ING Vysya, Yes Bank

Distribution of Ratings / Market Cap

Edelweiss Research Coverage Universe

Rating Distribution* 104 60 18 183

* 1 stocks under review

Market Cap (INR) 114 58 11

Date Company Title Price (INR) Recos

Recent Research

31-May-12 MCX A rare commodity; Initiating

Coverage

935 Buy

31-May-12 Axis

Bank

The axiom of profitable

growth;

Visit Note

1,001 Buy

24-May-12 Rural

Electrification

Corporation

In fine fettle, but restructuring

rears its head;

Result Update

171 Buy

> 50bn Between 10bn and 50 bn < 10bn

Buy Hold Reduce Total

Rating Interpretation

Buy appreciate more than 15% over a 12-month period

Hold appreciate up to 15% over a 12-month period

Reduce depreciate more than 5% over a 12-month period

Rating Expected to

40 Edelweiss Securities Limited

Banking and Financial Services

Access the entire repository of Edelweiss Research on www.edelresearch.com

DISCLAIMER General Disclaimer:

This document has been prepared by Edelweiss Securities Limited (Edelweiss). Edelweiss, its holding company and associate companies are a full service, integrated

investment banking, portfolio management and brokerage group. Our research analysts and sales persons provide important input into our investment banking

activities. This document does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other sources believed to be reliable, but we do not represent that it is accurate or

complete and it should not be relied on as such. Edelweiss or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that

may arise to any person from any inadvertent error in the information contained in this report. This document is provided for assistance only and is not intended to

be and must not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this

document should make such investigation as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to

in this document (including the merits and risks involved), and should consult his own advisors to determine the merits and risks of such investment. The investment

discussed or views expressed may not be suitable for all investors. We and our affiliates, group companies, officers, directors, and employees may: (a) from time to

time, have long or short positions in, and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving

such securities and earn brokerage or other compensation or act as advisor or lender/borrower to such company (ies) or have other potential conflict of interest

with respect to any recommendation and related information and opinions. This information is strictly confidential and is being furnished to you solely for your

information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in

whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located

in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would

subject Edelweiss and affiliates/ group companies to any registration or licensing requirements within such jurisdiction. The distribution of this document in certain

jurisdictions may be restricted by law, and persons in whose possession this document comes, should inform themselves about and observe, any such restrictions.

The information given in this document is as of the date of this report and there can be no assurance that future results or events will be consistent with this

information. This information is subject to change without any prior notice. Edelweiss reserves the right to make modifications and alterations to this statement as

may be required from time to time. However, Edelweiss is under no obligation to update or keep the information current. Nevertheless, Edelweiss is committed to

providing independent and transparent recommendation to its client and would be happy to provide any information in response to specific client queries. Neither

Edelweiss nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special