Indonesian Banking Booklet · Closure of Bank Branch Office 97 ... Product of Islamic Bank and...

218

Indonesian Banking Booklet 2012 Bank Licensing and Banking Information Department

Transcript of Indonesian Banking Booklet · Closure of Bank Branch Office 97 ... Product of Islamic Bank and...

Indonesian BankingBooklet

2012

Bank Licensing and Banking

Information Department

INDONESIANBANKINGBOOKLET

2012

i

FOREWORD

The 2012 edition of Indonesian Banking Booklet is publication media presenting brief information regarding Indonesian banking. It is expected that this booklet will enable the readers to obtain information banking-related policies and regulations published by Bank Indonesia up to March 2012.

The latest information presented in this Booklet includes but not limited to 2012 Banking Policy, Prudential Principle for Commercial Banks in Partly Submitting Work to Other Party, the Application of Anti-Fraud Strategy for Commercial Banks, the Application of Risk Management to Commercial Banks Serving Prime Customers, Guidance in Credit Risk RWA Calculation by Using Standard Approach, Transparency of Prime Lending Rate Information, Function of Compliance of Commercial Banks, Application of Risk Management to Bank Performing Activities Related to Provision of Housing and Car Loan, and several revisions on the preceding banking provisions.

Furthermore, for any further information and explanation with regards to banking provisions, the readers may refer to the provisions issued by Bank Indonesia that may be obtained, among others, from the website of Bank Indonesia (www.bi.go.id).

We hope that, despite the limited information presented in this Indonesian Banking Booklet, the readers may still obtain optimum benefit from this book.

Jakarta, April 2012

Bank Indonesia

Bank Licensing and Banking Information Department

INDONESIANBANKINGBOOKLET2012

ii

CONTENTS

FOREWORD iCONTENT ii

I. BANK INDONESIA 3A. Mission and Vision of Bank Indonesia 3B. Strategic Values of Bank Indonesia 3C. Legal Basis of Bank Indonesia 3D. Important Duties of Bank Indonesia 3E. Detailed Description of Duties 3F. Organization of Bank Indonesia 4

II. BANKING SYSTEM 9 A. Definition 9 B. Operations of Banks 9 Operations of Conventional Commercial Banks 9 Operations of Islamic Commercial Banks 11 Operations of Conventional Rural Banks 13 Operations of Islamic Rural Banks 13 C. Operations Not Permitted for Banks 14 Operations Not Permitted for Conventional Commercial Banks 14 Operations Not Permitted for Islamic Commercial Banks 14 Operations Not Permitted for Conventional Rural Banks 15 Operations Not Permitted for Islamic Rural Banks 15 III. BANK REGULATION AND SUPERVISION 19 A. Objectives of Banking Regulation and Supervision 19 B. Scope of Bank Regulation and Supervision 19 C. Bank Supervision System 20 D. Information System in Supporting Bank Supervisory Tasks 22 E. Banking Investigation and Mediation 25 IV. BANKING POLICY 29 A. Banking Policy Direction in 2012 29 B. Improvement of Financial Inclusion 30 C. Basel II 36 D. Basel III 40 E. Reform of Global Financial Sector 43

INDONESIANBANKINGBOOKLET

2012

iii

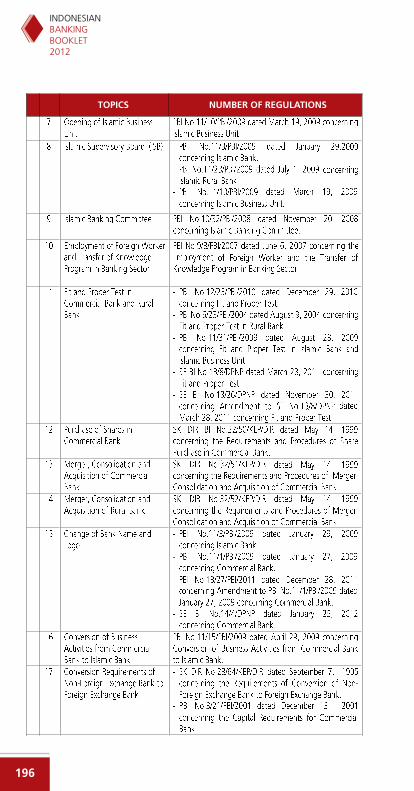

F. BPD as Regional Champion (BRC) 44 G. Development of Islamic Banking 45 H. Development of Rural Banks (BPR) 52 I. Micro, Small and Medium Enterprise (UMKM) Development 57 J. Credit Bureau 60 K. Macroprudential Policy 62 V. KEY BANKING REGULATIONS 67 A. Regulations of Establishment of Banks, Management of Bank and Bank Owner 67 1. Establishment of Banks 67 2. Bank Owners 69 3. The Single Presence Policy In Indonesian Banks 70 4. Management of Banks 71 5. Islamic Supervisory Board 82 6. Islamic Banking Committee 83 7. Employing Foreign Worker and Transfer of Technology Program in Banking Sector 84 8. Fit and Proper Test for Commercial Banks and Rural Banks 85

9. Purchase of Shares in Commercial Banks 90 10. Merger, Consolidation, and Acquisition of Bank 91 11. Establishment of Bank Offices 92 12. Conversion of Bank Name and Logo 95 13. Conversion of Business Activities from Commercial Bank to Islamic Bank 96 14. Closure of Bank Branch Office 97 15. Requirements of Non-Foreign Exchange Bank to

Foreign Exchange Status 98 16. License Modification from Commercial Bank to Rural Bank in the framework of Consolidation 98 17. Supervisory Actions and Designation of Bank Status 98 18. Follow Up Action to Rural Bank under Special Surveillance 104 19. Follow Up Action to Islamic Rural Bank under Special Surveillance 106 20. Bank Liquidation 107

21. Revocation of Business License at the request of Shareholders (Self Liquidation) 107

INDONESIANBANKINGBOOKLET2012

iv

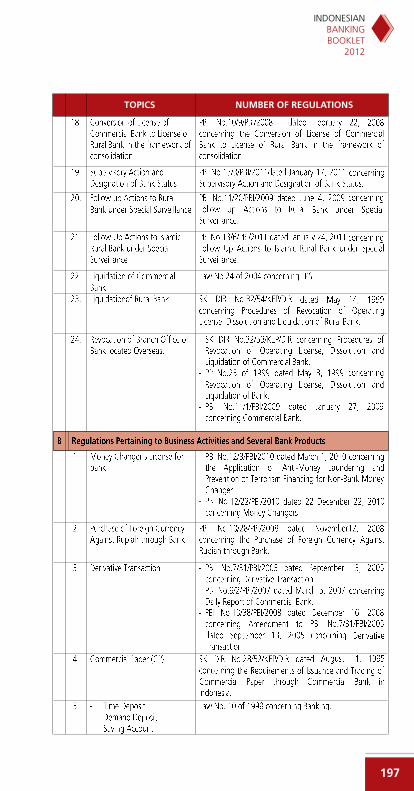

B. Regulations Pertaining to Business Operations and Bank Product 109 1. Money Changer’s License for Bank 109 2. The Purchase of Foreign Currency Versus Rupiah

to Banks 109 3. Derivative Transactions 110

4. Commercial Paper (CP) 110 5. Deposits 111

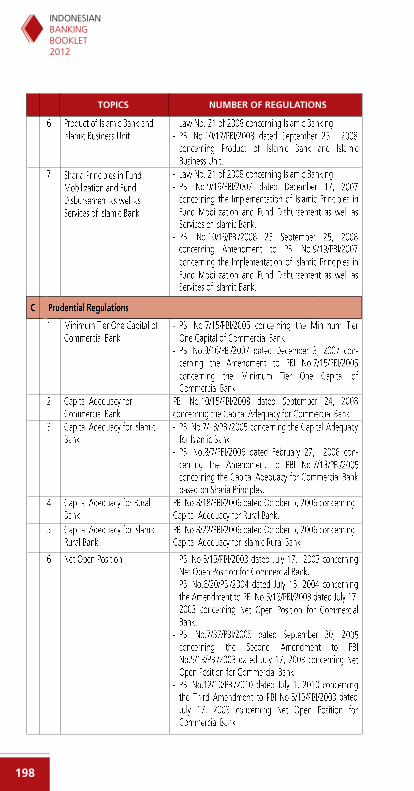

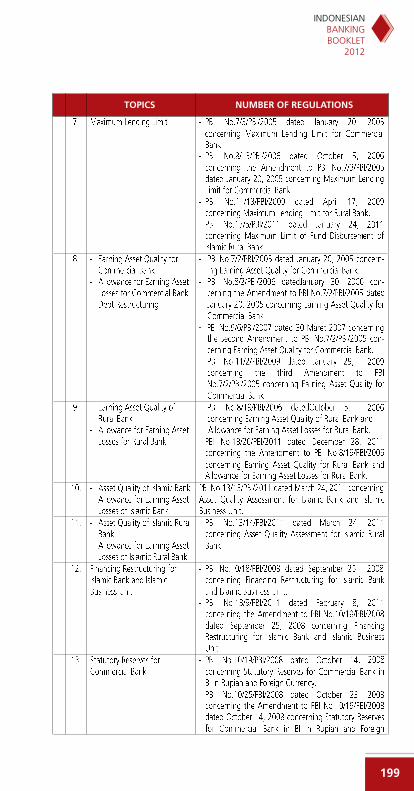

6. Product of Islamic Bank and Islamic Business Unit (UUS) 113 7. The Implementaion of Sharia Principles in Fund Mobilization, Fund Distribution and Islamic Banking Services 113 C. Prudential Regulations 114 1. Minimum Tier One Capital for Commercial Banks 114 2. The Minimum Capital Adequacy Requirement 115 3. Net Open Position (NOP) 117 4. Legal Lending Limit (LLL) 117 5. Earning Assets Quality 120 6. Provision for Assets Losses 124 7. Debt Restructuring 129 8. Financing Restructuring for Islamic Bank and Islamic Business Unit (UUS) 130 9. Statutory Reserves (GWM) 130 10. Transparency of Bank Financial Condition 132 11. Transparency in Bank Product Information and Use of Customer Personal Data 133 12. Prudential Principles in Equity Participation by Commercial Banks 133 13. Prudential Principles in Asset Securitization for Commercial Banks 135 14. Prudential Principles in Structured Product for Commercial Banks 135 15. Prudential Principles in Implementing Agency Activity of Foreign Financial Products by Commercial Banks 136 16. Prudential Principle for Commercial Banks Submitting A Part of the Work to a Third Party 137 17. Implementation of Anti Fraud Strategy for Commercial Banks 138

INDONESIANBANKINGBOOKLET

2012

v

18. Guidelines for the Calculation of Risk-Weighted Assets for Credit Risk Using Standardized Approach 139 D. Regulation of Bank Soundness Rating 140 1. Conventional Commercial Bank 140 2. Islamic Commercial Bank 142 3. Rural Bank 143 4. Islamic Rural Banks 144 E. Self-Regulatory Banking (SRB) Regulations 145 1. Guidelines for Formulation of Bank Credit Policy 145 2. Implementation of Good Corporate Governance (GCG) 145 3. Internal Audit Unit at Commercial Banks 146 4. Compliance Implementation of Commercial Bank 147 5. Business Plan and Annual Budget 148 6. Application of Risk Management in the Use of Information Technology by Commercial Banks 149 7. Application of Risk Management for Commercial Banks 150 8. Consolidated Application of Risk Management by Banks that Control Subsidiaries 152 9. Application of Risk Management in Internet Banking 153 10. Application of Risk Management on Bank Engaging in Joint-Marketing Activity with Insurance Company/Bancassurance 153 11. Application of Risk Management for Banks Conducting Activities Related to Mutual Funds 154 12. Risk Management Certification for Management and Officer of Commercial Banks 155 13. Application of Risk Management to Commercial Bank Offering Prime Customer Services (LNP) 155 14. Application of Risk Management to Bank Offering Mortgages (KPR) and Motor Vehicle (KKB) Loans 156 15. Application of Risk Management for Islamic Bank 157 16. Application of Anti Money Laundering and Prevention of Terrorism Financing Program (APU and PPT Program) 158

INDONESIANBANKINGBOOKLET2012

vi

17. Resolution of Customer Complaint 160 F. Funding Regulations 160 1. Short Term Funding Facility (FPJP) for Commercial Banks 160 2. Short Term Funding Facility (FPJP) for Rural Banks 161 3. Short Term Financing Facility (FPJPS) for Islamic Banks 161 4. Short Term Financing Facility (FPJPS) for Islamic Rural Banks 162 5. Intraday Liquidity Facility (FLI) for Commercial Banks 162 6. Intraday Liquidity Facility (FLIS) for Commercial Banks Based on Sharia Principles 163 7. The Emergency Financing Facility (FPD) 163 G. Related to MSMEs Regulation 164 1 Technical Assistance 164 2 Bussiness Plan 164 3 Legal Lending Limit 164 4 Risk-Weighted Assets for Claim to Micro, Small and Retail Portfolio 165 5 Assessment on Asset Quality 165 H. Other Regulations 165 1. BI Rupiah Deposit Facility (FASBI) 165 2. Bank Foreign Borrowings 165 3. Interbank Money Market Based on Sharia Principles (PUAS) 166 4. Certifying Institution for Rural Bank 166 5. Restrictions on Rupiah Transactions and Foreign Currency Loans By Banks 167 6. National Clearing System 169 7. Real Time Gross Settlement (RTGS) 169 8. BI Certificates (SBI) 169 9. BI Certificates on Sharia Prinsiples (SBIS) 170 10. Government Securities (SUN) 170 11. Bank Secrecy 170 12. Human Resources Development at Banks 171 13. Banking Mediation 172

INDONESIANBANKINGBOOKLET

2012

vii

14. Incentives in The Framework of Bank Consolidation 172 15. Debtor Information System (SID) 173 16. Indonesian Banking Accountancy Guide for Conventional Commercial Banks 173 17. Guidelines for Islamic Banking Accountancy (PAPSI) for Islamic Bank and Islamic Business Unit 174

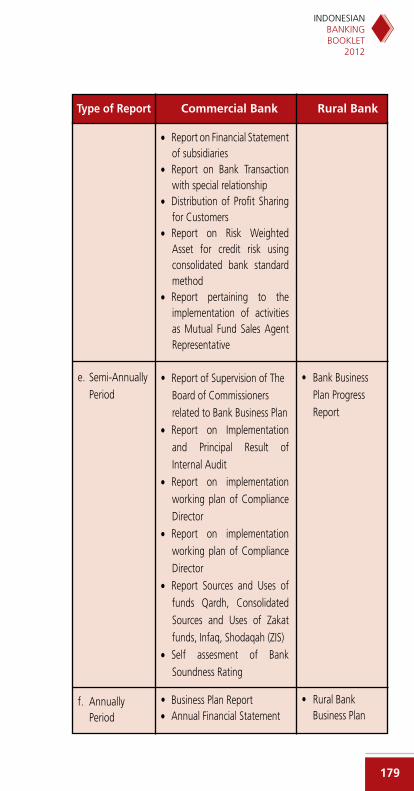

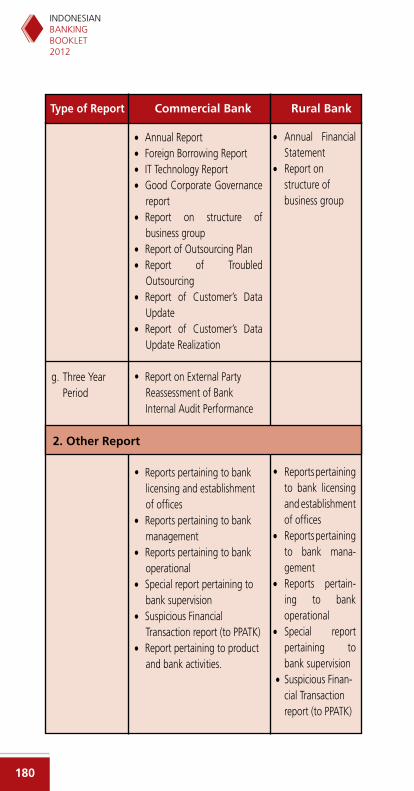

18. Determination of Financial Accountancy Standard for Rural Bank 174 19. Information Transparency on Prime Lending Rate 175 20. Rating Agencies and Ratings Acknowledged by BI 176 I. Bank Reports 177 1. Commercial Bank 2. Rural Bank VI OTHERS 183 A. Banking Popular Terminology 183 B. Role of the Bank in Prevention and Combatting Money Laundering based on Act of the Republic of Indonesia No. 8 of 2010 186 C. Type of Agreement in Islamic Banking Business Activities 190 VII APPENDIX 195

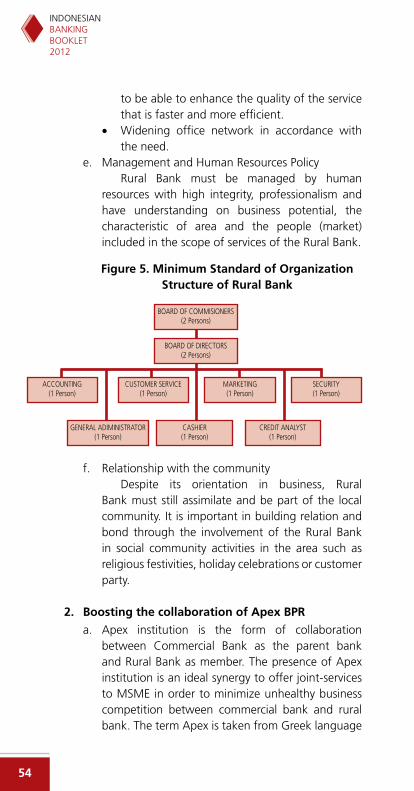

LIST OF FIGURE 1. Bank Indonesia Organization Structure 5 2. Risk Based Supervision Cycle 21

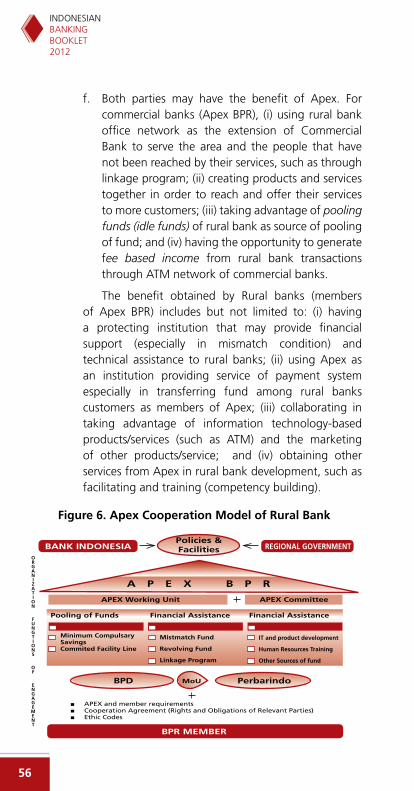

3. Pillar of Financial Inclusive 33 4. Basel II 37 5. Minimum Standard of Organization Structure of Rural Bank 54 6. APEX Cooperation Model of Rural Bank 56

CHAPTER

I

BANK INDONESIA

This page intentionally left blank

INDONESIANBANKINGBOOKLET

2012

�

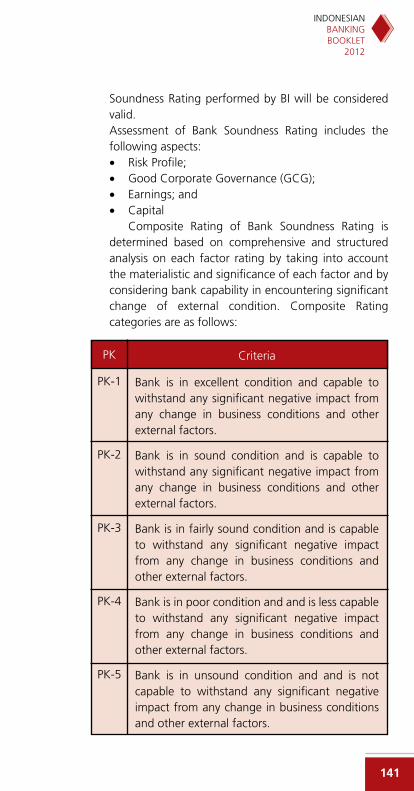

I. BANK INDONESIA

Bank Indonesia (BI) is the Central Bank of the Republic of Indonesia. BI is an independent state institution, which is free from intervention of the government and or other parties, except for matters explicitly prescribed in Act concerning BI.

A. Mission and Vision

1. Mission To achieve and maintain stability in the Rupiah through

management of monetary stability and development of financial system stability in support of long-term, sustainable national development.

2. Vision To be a Central Bank established as institution of trust

with national and international credibility through reinforcing of its strategic values and achievement of stable, low inflation.

B. Strategic Values Competency, integrity, transparency, accountability,

cohesiveness.

C. Legal Basis of Bank Indonesia1. 1945 Constitution of the Republic of Indonesia2. Act of the Republic of Indonesia Number 23 of 1999

concerning BI as amended by Act of the Republic of Indonesia Number 3 of 2004

3. Act No. 6 of 2009 concerning the Stipulation of Government Regulation in Lieu of Law no. 2 of 2008 concerning the Second Amendment of Act No. 23 of 1999 concerning BI to become Law.

D. Important Duties of Bank Indonesia1. Establishment and implementation of monetary

policy;2. Regulation and ensuring the smooth operation of the

payments system;3. Regulation and supervision of banks.

E. Detailed Description of Duties1. Establish monetary targets, taking into account inflation

targeting, conduct monetary control, extend credit

INDONESIANBANKINGBOOKLET2012

�

or financing based on Sharia Principles to overcome short-term financial problem of banks (mismatch), provide Government-funded emergency financing in the event of a bank experiencing financial difficulties with systemic impact that may potentially set off a crisis endangering the financial system, implement exchange rate policy, and manage foreign exchange reserves.

2. Determine the use of payment instruments, regulate the inter-bank clearing system, arrange the final settlement of inter-bank payment transaction, issue and circulate the Rupiah currency as well as to revoke, withdraw and destroy such currency from circulation.

3. Grant and revoke licenses of an institutional and certain business. Prescribe regulations, activities of a bank, conduct banking supervision and impose sanctions on banks in accordance with prevailing regulations.

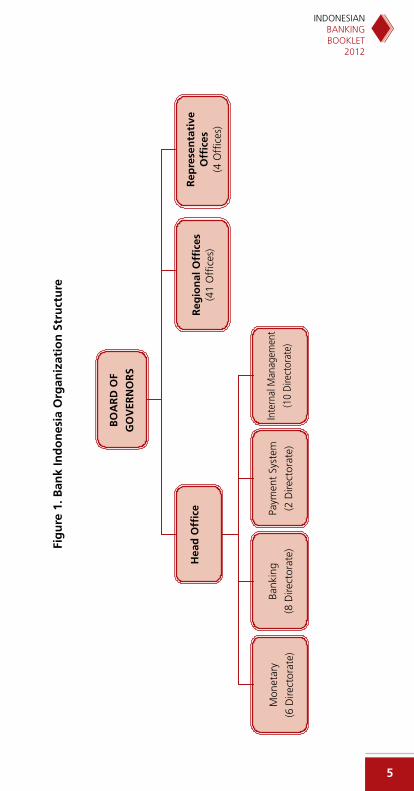

F. Organization of Bank Indonesia

BI is headed by a Board of Governors, consisting of a Governor, a Senior Deputy Governor, and at least four and not more than seven Deputy Governors, nominated and appointed by the President upon the approval of the House of Representatives.

In general terms, BI performs its tasks through four sector units, the BI regional offices, and BI representative offices, all of which are responsible to the Board of Governors.

INDONESIANBANKINGBOOKLET

2012

�

Mon

etar

y

(6 D

irect

orat

e)

Bank

ing

(8 D

irect

orat

e)

Paym

ent

Syst

em

(2 D

irect

orat

e)

Inte

rnal

Man

agem

ent

(10

Dire

ctor

ate)

Reg

ion

al O

ffice

s(4

1 O

ffice

s)

Rep

rese

nta

tive

O

ffice

s(4

Offi

ces)

BO

AR

D O

F

GO

VER

NO

RS

Fig

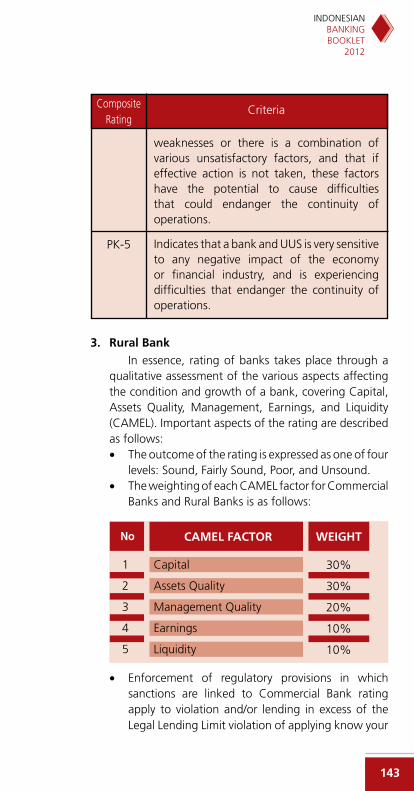

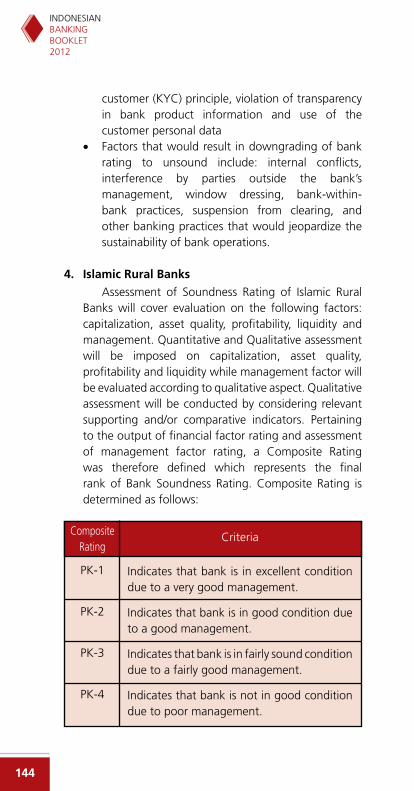

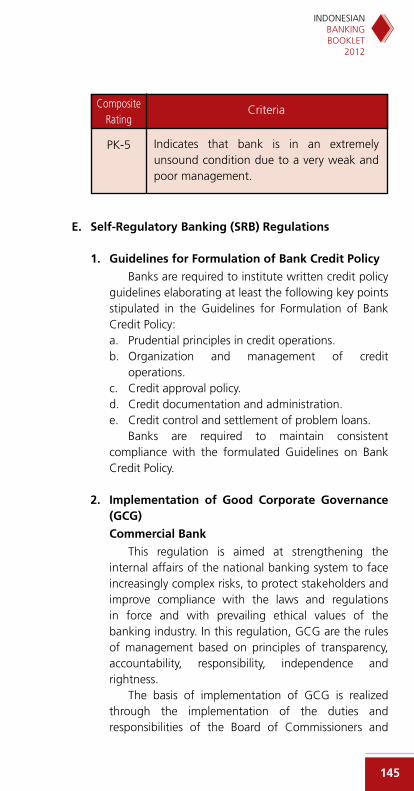

ure

1. B

ank

Ind

on

esia

Org

aniz

atio

n S

tru

ctu

re

Hea

d O

ffice

CHAPTER

II

BANKING SYSTEM

This page intentionally left blank

INDONESIANBANKINGBOOKLET

2012

�

II. BANKING SYSTEM

Banking is defined as all that pertains to banks, including of banking entities and bank offices, scope of banking business, and methods and processes employed in the conduct of banking business.

The key principle for business operations conducted by the Indonesian banking system is economic democracy applied with the use of prudential principles The primary function of the banking system in Indonesia is to mobilize and disburse funds belonging to the public and to support national development to bring about improved equitable distribution, economic growth, and national stability aimed at improving the welfare of the population at large.

The banking system has a strategic role in supporting the smooth operation of the payment system, implementing monetary policy, and achieving financial system stability. To achieve these aims, it is essential to have a sound, transparent, and accountable banking system.

A. Definition

1. Bank is a business entity that mobilizes deposit funds from the public and channels these funds to the public in credit and/or other forms in order to improve the living standards of the population at large.

2. Conventional Bank is a bank conducting conventional business and based on its types consists of Commercial Conventional Bank and Rural Bank.

3. Sharia Bank is bank conducting business based on Sharia Principles and according to its types consists of Islamic Commercial Bank and Islamic Rural Bank.

4. Sharia Principles are principles based on Sharia law in banking activities which are in accordance with fatwa published by institution authorized in defining fatwa in compliance with Sharia Principles.

B. Operations of Banks

Operations of Conventional Commercial Banks

1. Mobilizing funds from the public in the form of deposits comprising demand deposits, time deposits, certificates

INDONESIANBANKINGBOOKLET2012

10

of deposit, savings deposits, and/or other equivalent form;

2. Extending credit;3. Issuing notes;4. Purchasing, selling, or guaranteeing against own risk or

on behalf of and/or at the request of a customer :• Bills of exchange, including banker’s acceptances of

which the maturity is no longer than the common practice of trading such documents;

• Notes and other commercial paper of which the maturity is no longer that the common practice of trading such documents;

• Treasury bills and government guarantees;• BI Certificates (SBIs);• Bonds;• Commercial paper with a maturity of up to 1 (one)

year;• Other securities with a maturity of up to 1 (one)

year;5. Transferring money, either on own behalf or at the

request of a customer;6. Placing funds in, borrowing funds from, or lending funds

to other banks, whether by letter, telecommunications device, or by sight draft, cheques, or other means;

7. Accepting payments in respect or claims for securities, settling accounts with or among third parties;

8. Providing safety deposit boxes for valuable goods and papers;

9. Undertaking custodial activities on behalf of another party based on contracts;

10. Undertaking placement of funds among customers in the form of securities not listed in the stock exchange;

11. Conducting business in factoring, credit cards, and trusteeship;

12. Providing financing and/or conducting other activities based on Sharia Principles in accordance with the regulations stipulated by BI;

13. Conducting other business commonly undertaken by banks providing that such activities shall not be in contravention of Act concerning Banking and prevailing laws;

INDONESIANBANKINGBOOKLET

2012

11

14. Conducting activities in foreign currencies with due observance to the regulation of BI;

15. Conducting equity participation in other banks or business entities operating in financial services, such as leasing, venture capital, securities houses, insurance, and securities clearing house and custodian, with due observance of the regulation stipulated by BI;

16. Conducting temporary equity participation to settle problem of bad debt or bad financing based on Sharia Principles, on the condition that in due time the equity participation shall be withdrawn, with due observance to the regulation stipulated by BI; and

17. Acting as founder and the management of a pension fund in accordance with the prevailing laws on pension funds.

Operations of Islamic Commercial Banks

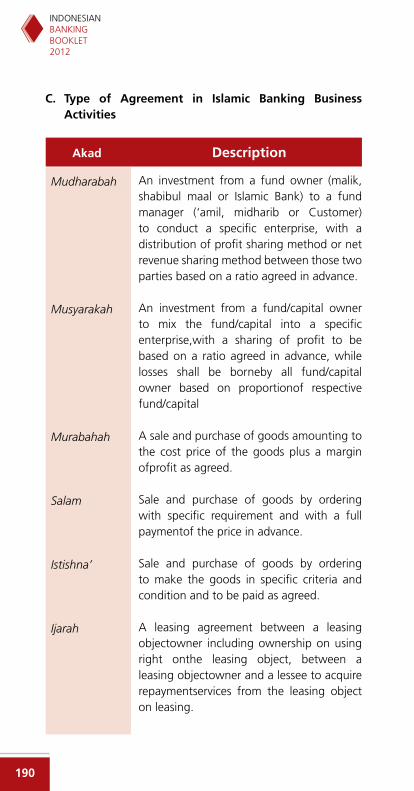

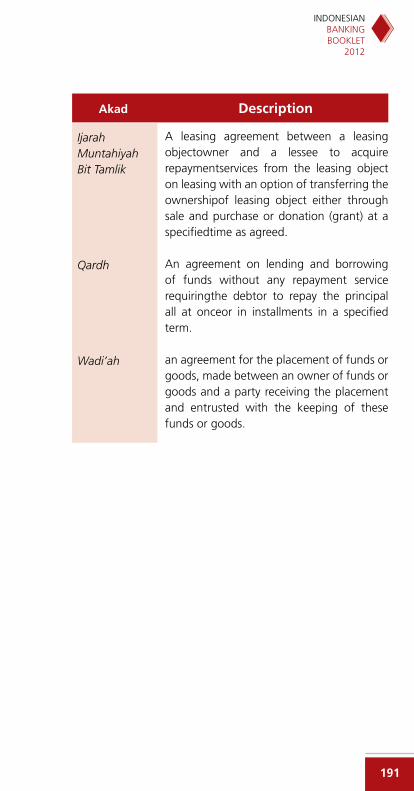

1. Mobilizing fund in the form of saving comprising demand deposit, saving deposit or other equivalent form based on wadi’ah agreement or other agreement not in contravention with Sharia principles;

2. Mobilizing fund in the form of investment comprising Time Deposit, Saving Deposit or other equivalent form based on mudharabah agreement or other agreement not in contravention with Sharia principles;

3. Disbursing profit sharing financing based on mudharabah agreement, musyarakah agreement or other agreement not in contravention with Sharia principles;

4. Disbursing financing based on murabahah agreemnet, salam agreement, istishna’ agreement, or other agreement not in contravention with Sharia principles;

5. Disbursing financing based on qardh agreement or other agreement not in contravention with Sharia principles:

6. Disbursing financing of rental of moving object or non moving object to customer based on ijarah agreement and/or leasing in the form of ijarah muntahiya bittamlik or other agreement which is not in contravention with Sharia principles;

INDONESIANBANKINGBOOKLET2012

12

7. Taking over of receivables based on hawalah agreement or other agreement which is not in contravention with Sharia principles;

8. Conducting business on debit and/or financing cards based on Sharia principles;

9. Purchasing, selling or guaranteeing at own risk third party securities issued based on underlying transaction and based on Sharia principles, such as, ijarah, musyarakah, mudharabah, murabahah, kafal or hawalah agreements;

10. Purchasing securities based on Sharia principles published by the government and/or BI;

11. Accepting payment of liabilites on securities and negotiating with a third party or among third parties based on Sharia principles;

12. Undertaking custodial activities for the interest of other party pertaining to an agreement based on Sharia principles;

13. Providing safety deposits for goods storage and securities based on Sharia principles;

14. Transferring money, either on own behalf or at customer’s interest based on Sharia principles;

15. Conducting trusteeship operation based on wakalah agreement;

16. Providing letter of credit or bank guarantee based on Sharia principles; and

17. Conducting other activities normally undertaken in the field of banking and social insofar as not in contravention with Sharia principles and in accordance with provisions of the applicable laws and regulations;

18. Conducting activities in foreign currency based on Sharia principles;

19. Conducting investment activity in Sharia Commercial Bank or financial institution conducting business based on Sharia principles;

20. Conducting temporary equity participation due to bad financing based on Sharia principles subject to requirement of subsequent withdrawal from equity participation;

21. Acting as the founder and the manager of pension

INDONESIANBANKINGBOOKLET

2012

1�

fund based on Sharia principles; 22. Conducting activity in capital market insofar as not in

contravention with Sharia principles and provisions of applicable laws and regulations in the field of capital market;

23. Organizing activity or banking products based on Sharia principles using electronic facilities;

24. Publishing, offering and trading short term securities based on Sharia principles, directlyor indirectly through money market;

25. Publishing, offering and trading longterm securities based on Sharia principles, directly or indirectly through capital market;

26. Providing products or conducting business activity of other Sharia commercial bank based on Sharia principles.

Operations of Conventional Rural Banks1. Mobilizing funds from the public in the form of deposits

comprising time deposits, savings deposits, and/or other equivalent form;

2. Extending credit;3. Placing funds in BI Certificates (SBIs), time deposits,

certificates of deposit, and/or savings deposits in other banks.

Operations of Islamic Rural Banks1. Public fund collecting in the form of:

a. Saving in the form of saving deposit or equivalent based on the wadi’ah or other agreement which is not in contravention with Sharia principles; and

b. Investment in the form of time deposit or saving deposit or other equal form based on mudharabah agreement or other agreement which is not in contravention with Sharia principles;

2. Fund distribution to public in the form of:a. Profit sharing financing based on mudharabah or

musyarakah agreement; b. Financing for buying and selling transaction based

on murabahah, salam or istishna agreement; c. Lending and borrowing based on qardh

INDONESIANBANKINGBOOKLET2012

1�

agreement; d. Leasing of moving or non moving objects to

customers based on ijarah or leasing agreement in the form of ijarah muntahiya bittamlik; and

e. Undertaking custodial activities of liabilities based on hawalah agreement;

3. Placing fund in other Sharia bank in the form of depository based on wadi’ah agreement of investment based on mudharabah agreement and/or other agreement which is not in contravention with Sharia principles;

4. Transferring money, either on own behalf or for customer’s interest through Islamic Rural Bank existing in Islamic Commecial Bank, Conventional Commercial Bank and Islamic Business Unit; and

5. Providing product or conducting business of other sharia bank in accordance with Sharia principles and subject to the approval of BI.

Supporting the activities of Business

Business support activities are carried out other activities outside the bank in bank operations. Business support activities include those relating to human resources, risk management, compliance, internal audit, accounting and finance, information technology, logistics and security.

C. Operations Not Permitted for Banks

Operations Not Permitted for Conventional Commercial Banks1. Conducting equity participation, with the exception

of those referred to No. 15 and 16 operation for commercial bank above;

2. Conducting business in insurance;3. Undertaking business other than those referred to in

letter B above.

Operations Not Permitted for Islamic Commercial Banks

1. Conducting business activities in contravention with Sharia principles;

INDONESIANBANKINGBOOKLET

2012

1�

2. Conducting activities related to direct buying and selling of shares in capital market;

3. Equity participation except as referred to in point 19 and 20 in Sharia bank business activities;

4. Conducting business in insurance, except if acting as agent of product marketing of sharia insurance.

Operations Not Permitted for Conventional Rural Banks

1. Accepting deposits in the form of demand deposit and participating in transaction;

2. Conducting business in foreign currencies except as money changer;

3. Conducting equity participation;4. Conducting business in insurance;5. Conducting other business other than those referred to

in letter B.

Operations Not Permitted for Islamic Rural Banks

1. Conducting business activities in contravention with Sharia principles;

2. Accepting saving in the form of demand deposit and participating in payment traffic;

3. Conducting business activities in foreign currency, except foreign currency exchange with the approval of BI;

4. Conducting insurance business activities, except as product marketing agent of Sharia insurance;

5. Participation in investment, except in institution established to overcome liquidity difficulties of Sharia Rural Bank; and

6. Conducting business other than business activities as referred to in section B.

INDONESIANBANKINGBOOKLET2012

16

CHAPTER

IIIBANK REGULATION AND

SUPERVISION

This page intentionally left blank

INDONESIANBANKINGBOOKLET

2012

1�

III. BANK REGULATION AND SUPERVISION

As part of its mandate for bank regulation and supervision, BI enacts regulations; issues and revokes licenses for incorporation, establishment of bank offices, and specific bank activities; conducts bank supervision; and imposes sanctions.

A. Objectives of Banking Regulation and Supervision

The primary focus of banking regulation and supervision is to ensure the optimum functioning Indonesia’s banking system with the aim of creating a sound banking system (both overall and in terms of individual banks) capable of safeguarding the public interest, achieving sound growth, and contributing in a useful capacity to the national economy.

B. Scope of Bank Regulation and Supervision

1. Right to license, comprising the right to establish procedures for the licensing and establishment of a bank. The scope of licensing by BI includes issuance and revocation of operating licenses for banks; issuance of licenses for establishment, closure, and change of address of bank offices; approval of bank owners and management; and issuance of licenses for banks to conduct certain business operations.

2. Right to regulate, comprising the right to establish regulations governing banking operations and activities for the purpose of fostering a sound banking system capable of delivering banking services as desired by the public.

3. Right to control, comprising the right to supervise banks:a. On-site supervision may take the form of general

examination and special examination aimed at obtaining a picture of the financial condition of the bank, monitoring the level of bank compliance with prevailing regulations, and ascertaining whether the bank is involved in any unsound practices that may jeopardize the sustainability of bank operations.

b. Off-site supervision is supervision through periodical reports delivered by banks, examination reports,

INDONESIANBANKINGBOOKLET2012

20

and other information. 4. Right to impose sanctions in accordance with laws

and regulations in the event that a bank is not fully compliant or is in non-compliance with regulations. Such actions contain elements of guidance to encourage banks to operate in compliance with sound banking principles.

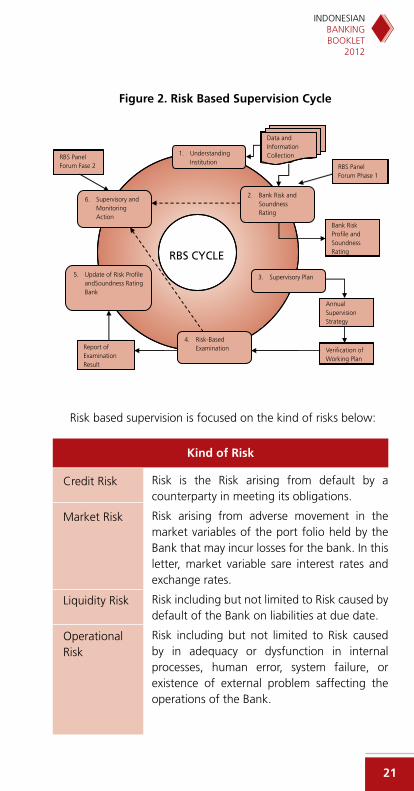

C. Bank Supervision System

In conducting bank supervision, BI currently uses a system applying 2 types of approach:1. Compliance Based Supervision that includes

monitoring of bank compliance with provisions related to bank operation and management in the past with the objective of confirming that bank has been well operated and correctly managed based on prudential principles.

2. Risk-Based Supervision that includes supervision based on forward looking oriented risk focusing on inherent risk on bank functioning activities as well as risk control system. This system will enable the authority of bank supervision to proactively take any preventive actions in facing problems that might potentially arise.

INDONESIANBANKINGBOOKLET

2012

21

Figure 2. Risk Based Supervision Cycle

Risk based supervision is focused on the kind of risks below:

Kind of Risk

Risk is the Risk arising from default by a counterparty in meeting its obligations.

Risk arising from adverse movement in the market variables of the port folio held by the Bank that may incur losses for the bank. In this letter, market variable sare interest rates and exchange rates.

Risk including but not limited to Risk caused by default of the Bank on liabilities at due date.

Risk including but not limited to Risk caused by in adequacy or dysfunction in internal processes, human error, system failure, or existence of external problem saffecting the operations of the Bank.

Credit Risk

Market Risk

Liquidity Risk

Operational Risk

Data and Information Collection 1. Understanding

Institution

RBS CYCLE

2. Bank Risk and Soundness Rating

3. Supervisory Plan

4. Risk-Based Examination

5. Update of Risk Profile andSoundness Rating Bank

6. Supervisory and Monitoring Action

RBS Panel Forum Phase 1

Bank Risk Profile and Soundness Rating

Annual Supervision Strategy

Verification of Working Plan

Report of Examination Result

RBS Panel Forum Fase 2

INDONESIANBANKINGBOOKLET2012

22

D. Information System in Supporting Bank Supervisory Tasks

1. Banking Information System (SIP)

BI has developped the Blue Print of Banking Information System as a guideline in information system development in order to support commercial bank supervision task that is expected to provide quality information through the application of the following principles:a. SIP is directed as business tool functioning at the

same time as a media of information provider. b. SIP provides information on macro basis, individual

bank as well as other information related to the

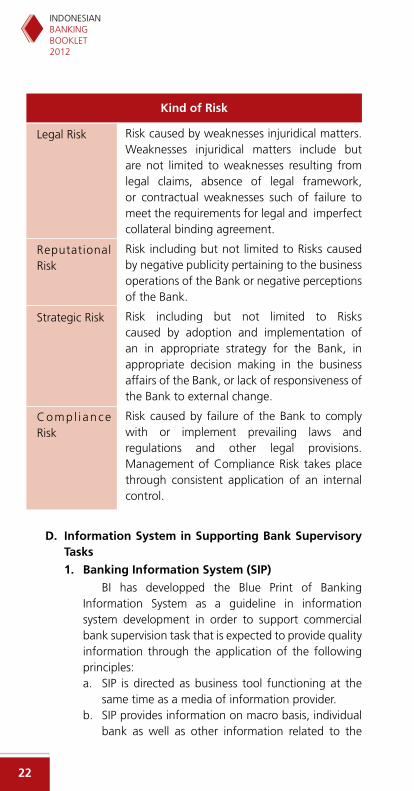

Kind of Risk

Risk caused by weaknesses injuridical matters. Weaknesses injuridical matters include but are not limited to weaknesses resulting from legal claims, absence of legal framework, or contractual weaknesses such of failure to meet the requirements for legal and imperfect collateral binding agreement.

Risk including but not limited to Risks caused by negative publicity pertaining to the business operations of the Bank or negative perceptions of the Bank.

Risk including but not limited to Risks caused by adoption and implementation of an in appropriate strategy for the Bank, in appropriate decision making in the business affairs of the Bank, or lack of responsiveness of the Bank to external change.

Risk caused by failure of the Bank to comply with or implement prevailing laws and regulations and other legal provisions. Management of Compliance Risk takes place through consistent application of an internal control.

Legal Risk

Reputational Risk

Strategic Risk

Comp l i ance Risk

INDONESIANBANKINGBOOKLET

2012

2�

bank business environment. c. SIP presents information collected from mass media,

government agencies as well as other institutions.d. SIP integrates data that are currently dispersed in

different systems.

SIP is developed based on the following Information Systems:a. Supervision Management Information System

(SIMWAS)

SIMWAS is an information system used by bank supervisor in conducting analysis activities on bank condition, accelerating the obtention of information on bank financial condition (including Bank Soundness Rating), enhancing the security and integrity of banking information and data.

b. Information System of Bank in Investigation (SIBADI)

SIBADI is an information system in order to support the implementation of investigation duties related to criminal acts in banks as well as duties related to mediation activities between customer and bank.

In supporting the process of fit and proper test, SIBADI also provides data/information of banking crime suspect.

2. Rural Bank Supervision Management Information System (SIMWAS BPR)

With reference ot the implementation of Rural Bank supervisory tasks, BI has developped and implemented Information System (SI) consisting of these two following units: a. Online reporting system, that enables Rural Bank

to send online periodic reports to BI in order to enhance the effectiveness of reporting and efficiency both from Rural Bank side and BI side. There are 4 types of periodic report submitted on online basis: Monthly Report, Maximum Lending Limit Report, Debtor Report and Rural Bank published financial report.

b. Data processing system, developped to eliminate

INDONESIANBANKINGBOOKLET2012

2�

redundancy of data input and to minimize human error and data inconsistency. Rural periodic report received by BI through reporting system will be processed for the interest of supervision and statistic as a supporting material of rural industrial development policy.

In supporting transparency to public and for the interest of relevant stakeholders, BI facilitates the presentation of rural publication report through BI website (www.bi.go.id) comprising data of Rural Bank industries and addresses of Rural Bank.

Furthermore, in the framework of enhancing the quality of Rural Bank supervision, the Information System of Rural Bank is directed to a more focused supervisory system in terms of offsite and onsite supervision with regards to any condition encountered by the Rural Bank. The development of Early Warning System (EWS) of Rural Bank has the objective of improving offsite monitoring of Rural Bank condition, in addition to soundness rating organized periodically. A tool has been development to support supervisors in performing onsite supervision on rural banks.

BI will continually improve on information system related to Rural Bank supervision so as to develop a system that is expected to become the “window” of information presenting the real condition of rural bank that may be used as materials in determining the improvement to be conducted.

�. Debtor Information System (SID)

SID is an information system providing debtor information, both individual and corporate, developed to support Bank credit risk management and BI supervisory duties. The information gathered in the SID include debtor information, trustees and debtor enterprises, provision of information facilities debtor funds received (credit, loans, securities, irrevocable L/Cs, bank guarantees, investments and/or other bills) collateral, underwriting and financial statements of the debtor. SID uses web-

INDONESIANBANKINGBOOKLET

2012

2�

based technology with extranet network enabling reporting entity to have real-time on-line data access.

E. Banking Investigation and Mediation

1. Policy Related to Banking Investigation For the effectiveness, acceleration, and optimization

in handling presumed banking criminal acts (Tipibank) and pertaining to the more complex the problem and the handling of banking criminal act indication, BI has taken strategic actions to collaborate with other institutions, such as:a. On December 19, 2011, an agreement was signed

between BI, the State Police and the Attorney General’s Office concerning the Coordination in Handling Banking Criminal Acts, No. 13/104/KEP.GBI/2011, No. B/31/XII/2011 and No. Kep-261/A/JA/12/2011, completed by Practical the Guidelines No. 13/10/KEP.DpG/2011, No. B/4768/XII/2011/Bareskrim, No. Kep-04/E/EJP/12/2011 and No. Juk 12/F/Fsp/12/2011 concerning the Coordination in Handling Banking Criminal Acts. This Agreement replaces the Joint-Decree (SKB) between the Attorney General, the Chief of the State Police and the Governor of BI in 2004. Several basic issues set forth in the Joint-Decree and the Practical Guidelines are the scope of coordination, organization and the task of Coordinating Team as well as the implementation of the coordination.

b. The Common-Decree between BI and LPS No.14/1/KEP.DpG/2012, No. KEP.001/KE/I/2012 dated January 4, 2012 concerning the mechanism in handling presumed banking criminal act on bank imposed of revocation of license. Several basic issues set forth in the Common-Decree are the completeness of supporting document, assistance during investigation, discussion of investigation results, development of handling of banking criminal acts, and financing of investigation implementation.

INDONESIANBANKINGBOOKLET2012

26

2. Policy related to Banking Mediation

BI performs banking mediation function based on PBI No.8/5/PBI/2006 concerning Banking Mediation as amended to PBI No. 10/1/PBI/2008. The main objective of banking mediation process is to facilitate the coordination in the settlement of customer’s complaint potentially inflicting customer’s interest and affecting bank reputation. Banking mediation is also conducted to facilitate small-scale customers in seeking banking dispute settlement using a simple, efficient and fast method.

The development of facilities for an easier and faster banking transaction has also increased the potential problem due to this increase. One of them is the opportunity of banking criminal practice using fraud as operation mode and bank account as the media in collecting the earnings of the crime.

With regards to the above mentionned subject, banking sector facilitated by BI prepared By Laws draft concerning Blocking of Customer’s Saving Account. The Bye Laws is aimed at facilitating bank in handling fraudulent act by using fund transfer facility and providing protection for the victim customer. Thenceforth, with the promulgation of Law No. 10 of 2008 concerning Prevention and Fighting Criminal Act of Money Laundering, BI provides banking sector to make amendment to the Bye Laws to be in harmony with the Law of TPPU. One of the subject of amendment is the synchronization of terminology between these two regulations.

In response to the booming delivery of Short Message Service to the public which is considered as one of fraudulent acts involving bank account which is suspected to have been opened using false identity, BI has asked the commitment of banking sector to do the follow up by verifying the account being used for this fraud and to take the necessary measures in providing protection to customers.

CHAPTER

IV

BANKING POLICY

This page intentionally left blank

INDONESIANBANKINGBOOKLET

2012

2�

IV. BANKING POLICY

A. Banking Policy Direction in 2012 In 2012, banking policy is directed to maintain

the stability between competition enhancement and strenghthening of banking resilience by supporting Bank intermediation including widening people’s access to low cost banking services. In the effort of reinforcing banking competitiveness, the policy related to Prime Lending Rate will be continued to ensure that market mechanism works well and policy target may be reached. From bank supervision, law enforcement will be enhanced by requiring bank to submit Bank Business Plan, including targets of efficiency enhancement and lowering loan interest rate at reasonable level.

Policy related to strengthening banking resilience is conducted through capital improvement in supporting economic growth and in anticipating busines cycle change. Aspect related to customer protection and banking management will also be focused. In 2012 BI will continue the policy to improve customer protection and potential customer as well as to improve provision related to financial report transparency, especially published financial report and the public accountant to be used by banking sector. BI continues to review ownership policy in banking sector and multi-license policy in line with bank activities that have become more complex.

In addition to strengthening competitiveness and banking resilience, BI will support banking intermediation through the following measures:1. Continuing the effort to support banking access

expansion (financial inclusion) to the public particularly low cost banking services for rural community, including quality enhancement of Tabunganku program, financial education development, implementation of Financial Identity Number and the implementation of literacy survey.

2. Facilitating intermediation to support financing in various potential sectors in collaboration with various government institutions. Other than that, various constraints in financing will be reviewed for sectors with

INDONESIANBANKINGBOOKLET2012

�0

relatively low credit growth. Pertaining to the need of financing sectors that are not considered commercially eligible by banking sectors but have strategic role in economy, BI in collaboration with the government will develop various financing schemes.

The effort in enhancing competitiveness and establishing better management, product development and business activities are also targetted by the policy direction of islamic banking. Strategy related to Islamic rural bank development will be directed to the strengthening of islamic rural bank characteristics as a sound, strong and productive community bank and may focus on offering financial services to MSME and local community in the rural area.

Macroprudential policy in reinforcing the function and active role of BI as systemic regulator in maintaining financial system stability, the strengthening of systemic regulator function was considered accurate following the validation of Law of Financial Services Authority (OJK) for the transfer of function pertaining to bank regulation and supervision which were previously performed by BI to OJK at the end of 2013.

BI will still escort banking industry with the application of function related to financial system stability, by conducting surveillance to both bank and non-bank, verifying bank in the framework of macroprudential, escorting the efficient function of intermediation as well as coordinating in the framework of crisis prevention and handling. The function and tasks of BI related to financial system stability and the establishment of efficiency in banking industry becomes an important part in the amendment to the Law of BI that has been included in the agenda of National Legislation Program 2012.

B. Improvement of Financial Inclusion

Despite the rapid development of financial industry in the last decades, there are still a part of the community that do not have yet any access to the basic financial services. According to the publication of World Bank 2008, more than 50% of the population of most developing countries do not have any account in a financial institution. Even

INDONESIANBANKINGBOOKLET

2012

�1

in most African countries only less than one-fifth of the society have an account in a financial institution. Whereas access to financial services is a critical aspect in poverty alleviation.

Root of the Problem

Difficulties faced by the community in obtaining access to financial services are generally classified into two major categories namely supply side and demand side.

1. Supply Sidea. Geographical condition. In addition to natural

problems such as people living in remote areas, Leyshon & Thrift study (1994) stated that financial crisis and deregulation are contributing factors impeding people’s access to financial services. Economic crisis has forced investors to withdraw their funds from developing countries leading to massive bank closing. Then deregulation era boosting tight competition, has forced banking sector to enhance efficiency that requires them to be very selective in choosing customers and to close their branch offices located in less profitable areas.

b. Services Design and Pattern. As an example, saving product with high administration fee for people with small purchasing power or unavailability of daily credit service for micro traders. This has thus led them to keep using the services of loan shark who will receive the installment directly from the traders. On the other side, generally banks provide priority to big loan than small scale credit needed by the micro, small and medium size industries.

c. Information gap between the requirements and bank procedures or bank products and those generally known by MSMEs. This gap requires a connection between the society, especially UMKM, and financial institution, especially banking, in order to identify and to solve problems in accordance to the real problem.

INDONESIANBANKINGBOOKLET2012

�2

2. Demand sidea. Education. The low level of education and

knowledge has impeded the society in obtaining financial services. Incapability in preparing financial report and or business prospect analysis has impeded the society in acquiring loan from banks. In addition to this, lack of knowledge on insurance benefit has also contributed to the low penetration of insurance products for low class community.

b. Legal or Formalization gap. Bank and customers are generally attached formally with strict legal requirements. It is generally difficult for micro business to meet bank formal requirements such as business license, assurance in the form of certificate, etc. All this has impeded the poor society in obtaining adequate credit access.

c. Self Exclusion. Other contributing factor for the reluctance in obtaining financial services is religious factor. A part of moslem community believes that receiving interest from conventional bank is riba or against the religion, therefore financial services based on sharia principles are the right solution for this community.

Access to Financial Services

Referring to the report of World Bank in 1995, there are at least four types of vital financial services for the people’s life, they are fund saving, credit facility, payment system and insurance covering pension fund. These four aspects are the basic requirements to be met by every society in order to have a better life.

Despite the existence of various services model of informal micro finance and spontaneous institution providing services to low income community especially in developing countries, these alternative financial institutions are capable to fulfill a small part of the needs of the community. Therefore, good collaboration between formal financial institutions especially banking sector and these micro financial institutions becomes a key element to the success in realizing inclusive financial institutions for all levels of society.

INDONESIANBANKINGBOOKLET

2012

��

National Strategy of Financial Inclusion

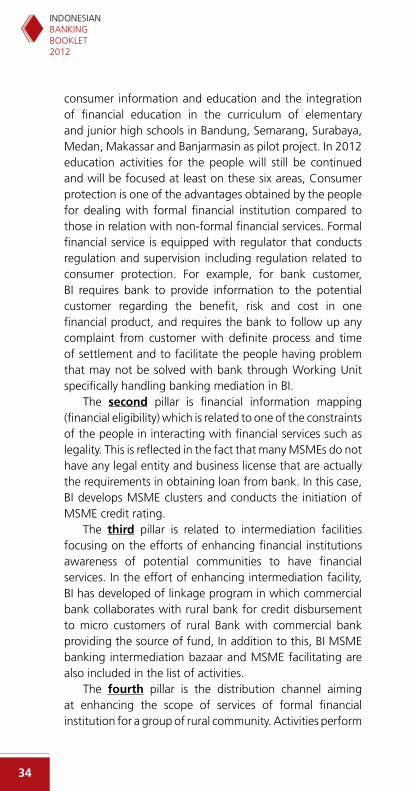

The enhancement of access of the society to financial institution is considered as a complex problem that requires inter-sectoral coordination involving banking authority, non-bank financial services and other ministries interested in the efforts related to education and poverty alleviation. The existence of an overall policy within one national strategy is needed and pertaining to this, 5 pillars of inclusive financial policy were formulated as described in the following chart.

Figure �. Pillar of Financial Inclusive

The descriptions of the pillars are as follows: Providing financial education to the people is one form

of customer protection as reflected from Pillar 1 regarding customer education and protection. Activities related to financial education are activities aimed at improving people’s knowledge and awareness on financial products and services. This knowledge is a part of one of the pillars in financial inclusive activities considering that one of the reasons why the people do not interaction with financial institution is due to lack of people’s understanding regarding financial products and services. BI has conducted several activities related to financial education, such as “Ayo Ke Bank” campaign, provision of website of

Acces forPoor Productive Community

To Bank & Non Bank Financial Institutions

Pilar

Saving

Credit/Financing

PaymentSystem

Insurance

Financial Services forUMKM

FinancialEducation

Financial Eligibility

IntermediationFacilities

Channeling/Distribution

SupportingRegulations

Infrastructure

Description :

: Program has been conducted and will be continued by BI

: Program will implemented by BI

: Program is relevant to other institution / agency outside BI

INDONESIANBANKINGBOOKLET2012

��

consumer information and education and the integration of financial education in the curriculum of elementary and junior high schools in Bandung, Semarang, Surabaya, Medan, Makassar and Banjarmasin as pilot project. In 2012 education activities for the people will still be continued and will be focused at least on these six areas, Consumer protection is one of the advantages obtained by the people for dealing with formal financial institution compared to those in relation with non-formal financial services. Formal financial service is equipped with regulator that conducts regulation and supervision including regulation related to consumer protection. For example, for bank customer, BI requires bank to provide information to the potential customer regarding the benefit, risk and cost in one financial product, and requires the bank to follow up any complaint from customer with definite process and time of settlement and to facilitate the people having problem that may not be solved with bank through Working Unit specifically handling banking mediation in BI.

The second pillar is financial information mapping (financial eligibility) which is related to one of the constraints of the people in interacting with financial services such as legality. This is reflected in the fact that many MSMEs do not have any legal entity and business license that are actually the requirements in obtaining loan from bank. In this case, BI develops MSME clusters and conducts the initiation of MSME credit rating.

The third pillar is related to intermediation facilities focusing on the efforts of enhancing financial institutions awareness of potential communities to have financial services. In the effort of enhancing intermediation facility, BI has developed of linkage program in which commercial bank collaborates with rural bank for credit disbursement to micro customers of rural Bank with commercial bank providing the source of fund, In addition to this, BI MSME banking intermediation bazaar and MSME facilitating are also included in the list of activities.

The fourth pillar is the distribution channel aiming at enhancing the scope of services of formal financial institution for a group of rural community. Activities perform

INDONESIANBANKINGBOOKLET

2012

��

related to the expansion of distribution services are among others optimization of post office network and the study of branchless banking with possibility of applying mobile money in Indonesia by using cellular phone as the means of keeping money in the form of an account in a certain bank. By adopting the concept of branchless banking it is expected that banking facilities may be offered to remote areas without having to provide the infrastructure of bank office.

A study on provisions that may support easy access for the people to financial services is considered necessary and this initiative is included in the fifth pillar. The government and BI will provide their support in the form of publication of regulations that may help the people to have easy access to financial services by using a method based on information technology such as e-payment and branchless banking.

Cross Pillar

The effectiveness in the implementation of the above five pillars may be reached and is inseparable from a number of contributing factors that together may be viewed as cross pillar activities. These activities include but not limited to: a) Enhancement of supporting infrastructure (physical and ICT), b) Database (both from demand and supply sides) that supports the process of inclusive financial policies, c) Boosting the establishment of credit bureau institution to support inclusive financial policies.

The improvement of community access to financial services will enable low-income society will benefit various services such as saving. Financial institution will be able to know more about its customer from the saving pattern of the community thus will give opportunity of financing for prospective customers. Moreover, the easy access to the services of payment system will give impact to the easiness of economic transaction, even to the community residing in remote areas. The activities of buying and selling can be performed more smoothly and the community will be able to use advance technology such as mobile phones to pay the purchase of raw materials from farmers in remote

INDONESIANBANKINGBOOKLET2012

�6

areas. Farmers do not have to sell their products at lower price due to the limited cash provided by collectors because payment can be performed using e-money. This effort will contribute to the strengthening of economic activities that will lead to the quality improvement of the community life. In terms of insurance services, the existence of micro insurance will be able to help the community in facing problems that may be settled by the insurance. These efforts are expected to strengthen the condition of the community in maintaining sustainable activities and to participate in economic activities.

C. Basel II

Minimum Capital Requirement is one of the main focuses of all bank supervisory authority in implementing prudential principles. Therefore it is deemed necessary to formulate regulation regarding capital in order to strengthen banking system and to support potential loss.

Considering the importance of bank capital, Basel Committee on Banking Supervision (BCBS) has issued a concept of capital framework with international standard. The initial concept of bank.

Capital framework was issued in 1988 and improved in 2006 with the publication of International Convergence on Capital Standard (A Revised Framework) or more known by Basel II.

Basel II has the objective to reinforce the security and soundness of financial system by focusing on the calculation of risk-based capital, supervisory review process and markert discipline.

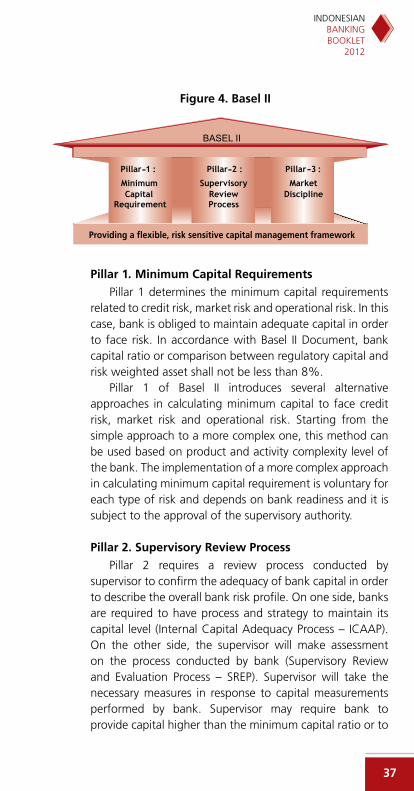

In general, Basel II framework consists of three pillars, namely Pillar 1: minimum capital requirements; Pillar 2, supervisory review process; and Pillar 3: market discipline.

INDONESIANBANKINGBOOKLET

2012

�7

Figure �. Basel II

Pillar 1. Minimum Capital Requirements

Pillar 1 determines the minimum capital requirements related to credit risk, market risk and operational risk. In this case, bank is obliged to maintain adequate capital in order to face risk. In accordance with Basel II Document, bank capital ratio or comparison between regulatory capital and risk weighted asset shall not be less than 8%.

Pillar 1 of Basel II introduces several alternative approaches in calculating minimum capital to face credit risk, market risk and operational risk. Starting from the simple approach to a more complex one, this method can be used based on product and activity complexity level of the bank. The implementation of a more complex approach in calculating minimum capital requirement is voluntary for each type of risk and depends on bank readiness and it is subject to the approval of the supervisory authority.

Pillar 2. Supervisory Review Process

Pillar 2 requires a review process conducted by supervisor to confirm the adequacy of bank capital in order to describe the overall bank risk profile. On one side, banks are required to have process and strategy to maintain its capital level (Internal Capital Adequacy Process – ICAAP). On the other side, the supervisor will make assessment on the process conducted by bank (Supervisory Review and Evaluation Process – SREP). Supervisor will take the necessary measures in response to capital measurements performed by bank. Supervisor may require bank to provide capital higher than the minimum capital ratio or to

- - -

INDONESIANBANKINGBOOKLET2012

�8

take improvement measures such as enhancement of risk management or other actions if the supervisor considers that capital measurement process used by the bank is not adequate and equal to bank risk profil.

There are 4 (four) main principles in Pillar 2 desgined to complete Pillar 1 with respect to calculation of minimum capital requirement and they are:Principle 1. Bank has the obligation to have an assessment

process of overall capital adequacy related to risk profile and strategy in maintaining capital level (Internal Capital Adequancy Assessment Process ICAAP).

Principle 2. Supervisor shall review and evaluate bank ICAAP, including bank capability in monitoring and confirming compliance to provision related to capital ratio and taking correct supervisory measures.

Principle 3. Supervisor has the obligation to require bank to operate over the defined capital ratio and to require bank to provide capital over minimum limit.

Principle 4. Supervisor is obliged to make intervention to avoid any capital decrease to below minimum level required to support banking risk characteristics and is obliged to require bank to conduct an immediate supervisory action.

In conducting SREP as referred to in the above Principle 2, Supervisor can estimate bank capital adequacy towards:1. Risks that that have not been fully estimated in Pillar

1, due to the use of standard approach, such as concentration risk;

2. Risks of Pillar 2, including liquidity risk, interest rate in the banking book, reputation risk and strategic risk. The assessment of some of these risks cannot be carried out quantitatively and there will be more qualitative interpretation including the risks from banking external factor that can appear due to policy and economic or business condition.

INDONESIANBANKINGBOOKLET

2012

��

Pillar �. Market Discipline

In completion to the other pillars, Pillar 3 of Basel II defined the requirements that will enable market players to assess main information regarding the scope of risk, capital, risk exposure, risk assessment process and bank capital adequacy. In principle, the objective of Pillar 3 is to support the establishment of sound banking business environment, by requiring banking sector to disclose all material information and the role of the public in bank supervision.

In order to achieve this objective the following main requirements should be fulfilled: 1. sufficient information available for public regarding

bank condition, and 2. public capability in evaluating bank condition through

the analysis of information provided.

Implementation of Basel II in Indonesia

The implementation of Basel II in Indonesia was conducted gradually starting from the simplest up to the more complex approach. The implementation Basel II in Indonesia has started since 2007 by the publication of provision concerning the measurement of market risk capital weight and ATMR for market risk by using standard method and internal model.

For operational risk, the calculation of Minimum Capital Adequacy (KPPM) uses basic indicator method. BI sets up transition period for the obligation in the calculation of Risk-Weighted Assets of operational risk amounting to 5% of the average yearly positive brut revenue for the last three years for the period of January 1, 2010 to June 30, 2010, 10% for the period of July 1, 2010 to December 31, 2010 and 15% starting from January 1, 2011. Risk-weighted assets of credit risk will be calculated using standard approach starting from January 2012. This calculation will be more risk sensitive compared to the approach used in the preceeding period. This approach is based on debtor/other party category, credit risk indicator is also based on debtor/other party rating published by rating agency acknowledged by BI. Through a more accurate

INDONESIANBANKINGBOOKLET2012

�0

ATMR calculation banking minimum capital requirement is expected to reflect more on credit risk level.

Pertaining to the provisions requiring the use of rating from rating institution, BI has published a list of rating institutions and ratings acknowledged by BI in BI website (www.bi.go.id).

With the overall implementation of Basel II it is expected that Indonesian banking industry will be more sound, more resilient against crisis and more competitive in global financial industry. Thenceforth this will lead to the soundness reinforcement of Indonesian financial system.

D. Basel III

In response to the global financial crisis 2008/2009, Leaders Summit in 2008 in Washington D.C.has agreed on 50 measures in saving world economy or known as Washington Action Plans (WAP). Following this agreement, G-20 initiated to suggest to Basel Committee on Banking Supervision (BCBS) to prepare a global¹ financial reform package aiming at (i) enhancing the capability of banking sector in absorbing econimic and financial crisis; (ii) reinforcing risk management and governance practice as well as strengthening transparency and information in banking sector; and (iii) fostering systemic resolution for banks and in operation in cross border manner.

This global financial reform or known as Basel III is aimed at reinforcing resilience both at micro and macro levels. Resilience enhancement at micro level is performed by strengthening bank capital quality, bank capital ratio, enhancing bank liquidity sufficiency and sustainability and fostering bank1 resilience especially during crisis. Resilience enhancement at macro level is conducted by reform on macroprudential regulation such as applying leverage ratio that may assist in mitigating risk that has potential risk to economic and financial system, minimizing procyclicality and applying countercyclical capital buffer that has to be developed during the improved economic condition, to be

1 BCBS has published 2 (two) documents as part of global financial reform package, namely, A Global Regulatory Framework for More Resilient Bank and Banking System and International Framework for Liquidity Risk Measurement

INDONESIANBANKINGBOOKLET

2012

�1

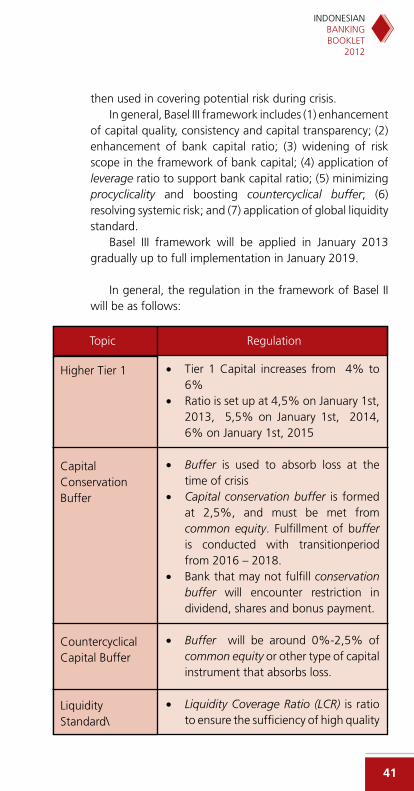

then used in covering potential risk during crisis. In general, Basel III framework includes (1) enhancement

of capital quality, consistency and capital transparency; (2) enhancement of bank capital ratio; (3) widening of risk scope in the framework of bank capital; (4) application of leverage ratio to support bank capital ratio; (5) minimizing procyclicality and boosting countercyclical buffer; (6) resolving systemic risk; and (7) application of global liquidity standard.

Basel III framework will be applied in January 2013 gradually up to full implementation in January 2019.

In general, the regulation in the framework of Basel II

will be as follows:

Topic Regulation

• Tier 1 Capital increases from 4% to 6%

• Ratio is set up at 4,5% on January 1st, 2013, 5,5% on January 1st, 2014, 6% on January 1st, 2015

• Buffer is used to absorb loss at the time of crisis

• Capital conservation buffer is formed at 2,5%, and must be met from common equity. Fulfillment of buffer is conducted with transitionperiod from 2016 – 2018.

• Bank that may not fulfill conservation buffer will encounter restriction in dividend, shares and bonus payment.

• Buffer will be around 0%-2,5% of common equity or other type of capital instrument that absorbs loss.

• Liquidity Coverage Ratio (LCR) is ratio to ensure the sufficiency of high quality

Higher Tier 1

Capital Conservation Buffer

Countercyclical Capital Buffer

Liquidity Standard\

INDONESIANBANKINGBOOKLET2012

�2

Topic Regulation

liquid asset to fulfill bank liquidity need in short term (30 days). This ratio is effective from January 1st, 2015.

• Net Stable Funding Ratio (NSFR) is ratio to measure bank long-term resilience, in the form of a more stable source of fund to support sustainably business activity.

• Matrix liquidity monitoring focusing on maturity mismatch, funding concentration and asset available to be used (unencumbered).

• This ratio is used to measure bank capital adequacy in supporting bank asset and business activity.

• Leverage Ratio is set at minimum of 3%.

• The application is conducted in parallel from 2013-2017 and starting from 2018 will be a part of Pillar 1 (capital adequacy).

• Capital Ratio is set up at least 8% of risk-weighted asset (ATMR).

• Additional Capital Conservation Buffer increases the ratio of minimum capital to 10,5% from risk-weighted asset (ATMR) in which 8,5% must be in the form of Tier 1.

• Tier 3 Capital is annulled

Leverage Ratio

Capital Ratio

INDONESIANBANKINGBOOKLET

2012

��

E. Reform of Global Financial Sector

Financial crisis has taught a valuable lesson related to the management aspect of global financial sector. It was obviously described that global financial sector was triggered by less effective management regime in responding to systemic risk. On the other side, ramification of the crisis was not easily detected due to information asymmetry. Global financial market and institution can transmit crisis rapidly form one economy to other economy due to the integrated global financial market. Meanwhile, key financial institutions globally operated (systemically important financial institutions) do not have adequate capital cushion to absorp their loss. One of the reasons is the weakness of capital regulatory regime bearing tendency for procyclicality amplification.

Pertaining to this issue, G-20 initiated a reform of global financial sector as one of important responses towards global financial crisis. During the meeting of leaders of G-20 countries in Washington in November 2008, an agenda was set forth regarding safety measures for global financial sector. This agenda has been implemented ambitiously since Washington Action Plan (WAP) reflected from the strict deadline applied to its completion. Among the initiatives, the most important reform agenda is a reform of global capital and liquidity regulation regim and procyclicality mitigation commonly known as Basel III. Meanwhile, crisis resolution for financial institution with systemic impact was also enhanced. This reform also linked to the reinforcement of OTC financial market, enhancement of supervisoy intensity as well as the extension of regulatory limits of financial sector in order to remove any fragmentation between banking sector, capital market and non-bank financial institution.

The agenda of reform of financial sector was eventually set up in response to G-20 meetings in Washington DC, London and Pittsburgh. As a member of G-20, Financial Stability Board (FSB) and Basel Committee on Banking Supervision (BCBS), Indonesia is committed to support this reform comprising 12 main agenda, namely:

INDONESIANBANKINGBOOKLET2012

��

1. Building high quality capital and liquidity standards2. Addressing systemically important financial institutions

and cross-border resolutions 3. Reforming compensation practices4. Improving over-the-counter derivative markets 5. Strengthening adherence to international standard6. Strengthening accounting standards 7. Developing macro-prudential policy frameworks and

tools8. Differentiated nature and scope of regulation9. Hedge Funds regulations10. Credit Rating Agencies11. Supervisory Colleges12. Re-launching securitization on sound basis.

F. BPD as Regional Champion (BRC)

Under the framework of Pillar 1 of Indonesian Banking Architecture, Bank Indonesia (BI) together with ASBANDA and BPD (Regional Bank) throughout Indonesia belonging to the working group have completed Regional bank transformation program through reinforcement of competitiveness and Regional bank institution, to be more efficient in their function as agent of development at regional level including its implementation strategy. The preparation of Regional Bank blueprint to become Regional Champion (BRC) will be based on the several factors, such as:a. The capital of Regional Bank (BPD) which lower

compared to average capital of national banking industry has the potential to weaken BPD sustainability in facing competition with other regional banking groups.

b. Unsatisfactory BPD services and low BPD Brand awareness may cause the lack of interest from the community towards BPD products and services and may undoubtedly lead to a lack of trust from the customers.

c. Human resources with low quality and competence in anticipating market development may fail in optimizing the potential of regional economy.

INDONESIANBANKINGBOOKLET

2012

��

d. The relatively low level of credit channeling to productive sector and the tendency of disbursing consumption credit to the employees of the regional government have impeded the role of BPD in regional real sector financing. The opportunity in financing productive sector may have the potential to be performed by other banks thus creates more difficulties for BPD to be the host in its respective region.

BRC vision is “to become a leading regional bank through competitive products and services supported by wide network and professional management in the framework of boosting regional economic growth.” This vision will be reached through various programs classified in the Pillar of strong institutional resilience in order to conduct an efficient operation; capability as an agent of regional development in the framework of supporting regional economic development; and the capability to provide services needed by the society.

To mark the commitment of BPD in implementing the above mentioned programs, on December 21, 2010, the signing of commitment has been performed by all President Directors of BPD and supported by all Governors and President of Commissioners of BPD throughout Indonesia. At this occasion, the Vice-President showed his great support towards the implementation of BRC because without any common effort to transform BPD to have a better resilience and competitiveness, BPD will face difficulties in facing future challenge and in supporting regional economic development. As the follow up of this activity, all BPD have prepared Bank Business Plan (RBB) in compliance with the target of BRC and have been submitted to BI in January 2011. Pursuant to the implementation of the initiative it is expected that several BPD will have become Regional Champions in their respective regions in 2014.

G. Development of Islamic Banking

1. Performance of Islamic Bank

The existence and development of Islamic banking in Indonesia is a reflection of need of an alternative

INDONESIANBANKINGBOOKLET2012

�6

banking system that will give more positive contribution for financial inclusion and financial deepening, as well as enhance system stability of national banking. The present development of Islamic banking industry reflects public demand that requires an alternative banking system that besides providing sound banking/financial services also complies with sharia principles.

With reference to Law No. 21 of 2008 concerning Islamic Banking, BI, as the authority of banking industry, has been assigned to prepare banking finance based on sharia principles.

The objective of Islamic banking is to support the implementation of national development, such as performing the function in supporting real sector through financing based on sharia principles and real transaction (intermediation function), that support national development in the framework of even distribution of people’s welfare. In addition to this, Islamic banking also performs social function such as collecting funds such as Zakat, Infaq, Sadaqah, hibah and other to be disbursed to organizations of zakat management, as one of the forms of Islamic financial institutions receiving religious donation in the form of money (wakaf uang). With these various unique functions, Islamic banking positions itself as bank classified as not just a bank (beyond banking) in national banking map. In line with the improved economic performance, Islamic banking in general is still capable to maintain its positive performance along with the enhancement of its intermediation function. Islamic bank capital is not relatively affected by the turmoil of international financial market, considering the lack of direct exposure in the form of overseas portfolio. The momentum of conducive economic development has given positive impact to the development of Islamic banking. The average annual growth rate of Islamic banking business volume is between 15-20%. Intermediation function of Islamic banking performs well at optimum level, reflected from Financing to Deposit ratio reaching 89.9%.

INDONESIANBANKINGBOOKLET

2012

�7

2. Policy Implementation

With reference to the Law as the authority of Islamic banking, BI has implemented various policies in various sectors. The implementation of these policies is based on 7 (seven) pillars in the Blue Print of Islamic Banking covering: (i) high quality human resources, (ii) effective regulation and supervision, (iii) supportive infrastructure, (iv) effective banking structure, (v) synergic strategic alliance, (vi) effective customer empowerment, and (vii) product and market development. Based on this Blueprint in 2011 BI implemented various policies related to Islamic banking in various types of activity. This activity may be classified into research, development, regulation, supervision and licensing of Islamic bank.

�. Effectiveness Enhancement in Islamic Banking Regulation and Supervision

Review on provisions has been conducted in 2011 to accommodate the development in accordance with Islamic banking condition. The review was conducted in view of synchronization and harmonization with the prevailing regulations and in compliance with the recommendation of international institutions. The result of the review recommended establishment and/or amendment to the prevailing regulations, namely: a. Maximum Limit of Fund Disbursement of Islamic

Bank and Islamic Business Unit;b. Institutional Aspect of Islamic Rural Bank;c. Fit and Proper Test of Islamic Bank;d. Good corporate governance in Islamic Rural Banks;e. Transparency of financial condition of Islamic Rural

Bank; andf. New products and activities of Islamic banking.

�. Direction of Islamic Banking Development

In addition to the effort of accelerating the growth of Islamic banking by still maintaining the robust system stability and adequately fulfilling sharia principles, BI will make a number of strategic initiative that will refer to Indonesian Banking Architecture (API) and Blueprint

INDONESIANBANKINGBOOKLET2012

�8

of Islamic Banking Development that will continuously be improved, by explaining the ideal condition of banking industry with a number of key pillars as its components. This will be completed by the placement of various types of bank at the correct position, in accordance with the reason of each existence that will also include assessment on the position of conventional bank and Islamic bank and how to keep each of them in synergy.

A number of priorities related to the development Islamic banking will be implemented in short term covering the following issues:

a. Human Capital Development of Islamic Banking Industry

In general the direction of human capital development of national Islamic banking is “to develop and manage human capital innovatively in order to support national Islamic banking in reaching its target and strategy through reinforcement of human resources productivity, religion, leadership effectiveness and individual development”. The main objective of human capital development of Islamic banking is to provide human resources in number and competence in accordance with industrial need and to become the strength factor to the competitiveness of sharia banking industry. In the effort of reaching the goal, a number of initiatives related to competency model, link and match program, regulation and capacity will be implemented in the future.

b. Improvement of Supervisory System Quality

In line with the direction of general development, sharia banking supervisory system will be directed to meet international supervisory standard in the form of regulations that are more compatible with international standard and more effective supported by the mechanisme of a more complete and efficient supervisory infrastructure. Several

INDONESIANBANKINGBOOKLET

2012

��

initiative programs to be implemented include regulatory convergence and integrated supervisory platform.

c. Strengthening of industrial infrastructure