Indonesia Consumer Survey 2016 - Credit Suisse

126

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 05 April 2016 Asia Pacific/Indonesia Equity Research Food Producers / Tobacco / Personal Products / Soft Drinks (Consumer Staples ID (Asia)/Healthcare ID (Asia)) Indonesia Consumer Survey 2016 CONNECTIONS SERIES Rise and shine Credit Suisse Indonesia Consumer Survey: Key themes……………………….. 4 The sixth Credit Suisse Indonesia Consumer Survey……………………………12 Key sectors………………………..………………………..……………………….. 29 Top picks………………………..………………………..……………………….….81 Research Analysts Ella Nusantoro 62 21 255 37917 [email protected] Priscilla Tjitra 62 21 2553 7906 [email protected] Christy Halim Michael Pranata

Transcript of Indonesia Consumer Survey 2016 - Credit Suisse

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

05 April 2016

Asia Pacific/Indonesia

Equity Research

Food Producers / Tobacco / Personal Products /

Soft Drinks (Consumer Staples ID (Asia)/Healthcare ID (Asia))

Indonesia Consumer Survey 2016

CONNECTIONS SERIES

Rise and shine

Credit Suisse Indonesia Consumer Survey: Key themes……………………….. 4

The sixth Credit Suisse Indonesia Consumer Survey……………………………12

Key sectors………………………..………………………..……………………….. 29

Top picks………………………..………………………..……………………….….81

Research Analysts

Ella Nusantoro

62 21 255 37917

Priscilla Tjitra

62 21 2553 7906

Christy Halim

Michael Pranata

05 April 2016

Indonesia Consumer Survey 2016 2

Introduction We are delighted to publish the sixth edition of Credit Suisse Research Institute’s

Emerging Consumer Survey—a project reflecting the results of nearly 16,000 detailed

face-to-face interviews with consumers across nine major emerging economies of Brazil,

China, India, Indonesia, Mexico, Russia, Saudi Arabia, South Africa and Turkey. In

conjunction with this publication, our investment bank research analysts publish the EM

Consumer Playbook, which focuses on related investment recommendations.

With investor sentiment now showing signs of improvement in emerging markets, our

study provides investors timely insights with regard to the powerful theme of a fast-

developing consumer culture shaped by technological innovation. Should there be doubt

as to the significance of the story, our analysis suggests that nearly 100 mn new

households in our survey countries have found their way into the middle-class territory in

the last two years.

These signs of improvement do of course come after a torrid 2015 for investors in the

region, and our barometers of consumer confidence reflect this. The percentage of our

respondents who now consider it a good time to make a major purchase has fallen by 10%

against a year ago. Similar indicators for Brazil and Russia have dropped sharply. The

countries that top our Emerging Consumer Scorecard are India, China and Saudi Arabia.

Supportive momentum to personal incomes is the common factor.

The weakest countries (Brazil, Russia and South Africa) shared a difficult economic

cocktail of weak currencies, commodity exposure and political risk in 2015. We show how

a weak currency is negative for consumer confidence. Hence, a revival in fortunes of the

countries above and on-going support for emerging consumers rest more widely on the

stability of their currencies in 2016. The good news is that the improving relative growth

projections for emerging markets coupled with currencies that seem intrinsically

undervalued suggests that this could be the case.

We also find that the rise of the emerging consumer is defined as much by age as

nationality. In nearly every surveyed country, the income prospects of the youngest age

brackets are the most optimistic. When we drill down into how this youthful dollar is spent,

a 'lifestyle' theme emerges and specifically is one of a growing healthy lifestyle.

'Premiumisation' is the other watchword to come through in our interviews. The on-going

sharp growth in e-commerce activity and the developing 'sharing economy' provide a

broader backdrop. In e-commerce specifically, we illustrate how online retail markets

across the key countries surveyed can more than triple annual revenue to reach US$2.5 tn

by 2025.

Finally, a legitimate question to pose is whether the structural themes that we seek to draw

out here actually matter for an investor amid economic stress. Clearly, the tailwind of a

cycle on the upswing and a healthy degree of risk appetite are optimal. However, if

investors had simply exited emerging markets as relative growth momentum began to flag

in 2010, a five-fold increase in the online penetration of retail sales in China would have

passed them by, as would the opportunities from the rural transformation in India and

successive years of growth in healthcare provision.

Even when the cycle is a challenge, structural themes can and do still deliver. We believe

that this year’s Survey and Playbook should continue to provide an instructive guide for

investors.

Giles Keating, Vice

Chairman of Investment

Solutions & Products

Stefano Natella, Head of

Global Markets Research

05 April 2016

Indonesia Consumer Survey 2016 3

Credit Suisse's Indonesia Research Team

Research analysts Telephone Email

Jahanzeb Naseer +62 21 2553 7977 [email protected]

Ella Nusantoro +62 21 2553 7917 ella.nusantoro@credit suisse.com

Priscilla Tjitra +62 21 2553 7906 [email protected]

Ari Jahja +62 21 2553 7976 [email protected]

Sanjay Jain +852 2101 6088 [email protected]

Laurensius Teiseran +62 21 2553 7931 [email protected]

Colin McCallum +852 2101 6514 [email protected]

Anand Swaminathan +65 6212 3012 [email protected]

Santitarn Sathirathai +65 6212 5675 [email protected]

05 April 2016

Indonesia Consumer Survey 2016 4

Credit Suisse Indonesia Consumer Survey 2016: Key themes Figure 1: Emerging consumer survey scorecard 2014 vs 2015

Rankings Personal

finances

Inflation

expectations

Household income

expectation

Time for a major

purchase

Income history Rank based on

five factors

(6-12m horizon) 2014 2015 2014 2015 2014 2015 2014 2015 2014 2015 2014 2015

India 2 3 3 4 3 2 2 2 1 1 1 1

China 4 1 4 3 5 4 3 3 4 4 5 2

Saudi Arabia 5 4 5 2 5 5 1 1 3 3 4 2

Indonesia 3 2 6 7 2 1 4 4 2 2 3 4

Turkey 9 6 1 1 9 7 7 8 7 5 6 5

Mexico 6 5 7 6 4 8 9 5 8 8 7 6

Brazil 1 6 2 8 1 3 4 9 5 9 2 7

South Africa 7 8 8 9 8 6 8 6 9 6 9 7

Russia 8 9 9 5 7 9 6 7 6 7 8 9

Note: Ranking is on a score of 1-9 for the nine countries surveyed. Source: Credit Suisse Emerging Consumer Survey 2016.

Figure 2: Indonesia's GDP peaked in 4Q10 and reached its

lowest in 2Q15...

Figure 3: Food spending increased to 50% in 2015 from

28% in 2010

6.0

6.3

5.8

6.8

6.5

6.3

6.0 5.9

6.1 6.2

5.9 5.9

5.5 5.6 5.5

5.6

5.1

5.0 5.0 5.0

4.7 4.7

4.7

5.0

4.5

5.0

5.5

6.0

6.5

7.0

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

GD

P g

row

th (%

)

Housing

8% Auto2% Education

4%

Food50%

Home and Personal Care

8%

Health Care6%

Savings18%

Entertainment4%

Source: Bloomberg Source: Credit Suisse Emerging Consumer Survey 2016

Figure 4: Indonesia's spending momentum 2015 vs 2010—what has changed in behaviour from six years ago

Carbonated drinksBottled water

Dairy products Instant noodles

Cigarettes

Tissues

Feminine hygiene

Cosmetics

Basic mobile phone

Smartphone

Cars

Internet access

Computers

Property

Holiday

Motorcycle

Fashion apparel

Sport shoes and wear

Watches

Jewellery

Perfumes

(30)

(20)

(10)

-

10

20

30

40

- 10 20 30 40 50 60 70 80 90 100

Reco

rded

spen

ding

in 2

015

vs. 2

010

2015 respondents that own/have bought each item (%)

Source: Credit Suisse Emerging Consumer Survey 2016

05 April 2016

Indonesia Consumer Survey 2016 5

Key themes from the emerging consumer survey in 2016

(1) The emerging consumer in 2016

Weak markets and currencies, and downgraded growth expectations have provided

the backdrop of this year's Emerging Consumer Survey. The Indian and Chinese

consumers are still the most robust, while the picture in weak-currency countries such

as Brazil and Russia is poor.

(2) It's all about the currency

While there is a debate of cause and effect, the currency effectively serves as a

transmission of hardship to the consumer via imported inflation on the one

consumption item that typically consumes more of the household budget than any

other—food. EM currencies have rarely been so far from estimates of purchasing

power parity (PPP). Clearly these currencies do not operate in a vacuum. As much as

the local factors such as politics, commodities and risk appetite are at work, they

reflect the broad deterioration in the economic momentum in the emerging versus the

developed word that we have seen in recent years.

(3) The EM consumer through a global lens

Confidence of many of the EM countries, particularly our top countries of India, Saudi

Arabia, China, and Indonesia, rank head and shoulders above many of the DM

consumers in the current environment.

(4) What does an optimistic consumer look like?

The broad themes that emerge have a resonance with previous surveys in that the

urban, young and higher-income earners offer the greatest degree of optimism.

(5) And who's buying what?

In terms of spending intention, we find the low ticket categories are the ones showing

the strongest momentum in every country compared to our previous survey. The

categories with highest spending intention and strongest momentum include fashion

items, sports shoes, perfumes and cosmetics. Categories with low spending intention

and weak momentum include foreign holidays, cars and electronics. Smartphones

show the weakest momentum of all; however, its penetration rates have risen rapidly

which naturally reduce spending intention. Fashion items and especially sports shoes

appear to be underpenetrated and still offer longer term potential as discretionary

spending increases.

(6) Structural growth in e-commerce

Data from this year's EMC survey clearly supports an on-going positive view on the

outlook for e-commerce, despite softer macro conditions in emerging economies. We

believe the softening economic conditions might actually improve the relative

competitive position of online operators, versus the more traditional "brick and mortar"

companies. The further expansion of the middle class, along with rising smartphone

ownership and related internet access also support a positive view on the e-

commerce growth story.

05 April 2016

Indonesia Consumer Survey 2016 6

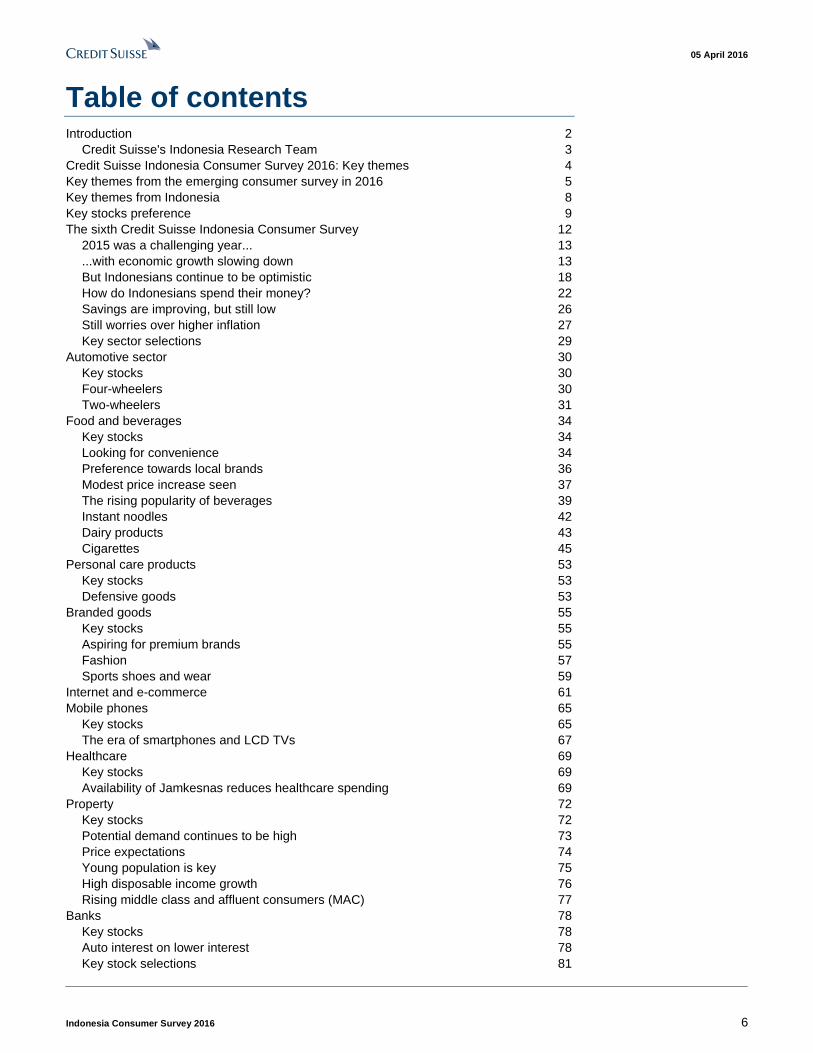

Table of contents Introduction 2

Credit Suisse's Indonesia Research Team 3 Credit Suisse Indonesia Consumer Survey 2016: Key themes 4 Key themes from the emerging consumer survey in 2016 5 Key themes from Indonesia 8 Key stocks preference 9 The sixth Credit Suisse Indonesia Consumer Survey 12

2015 was a challenging year... 13 ...with economic growth slowing down 13 But Indonesians continue to be optimistic 18 How do Indonesians spend their money? 22 Savings are improving, but still low 26 Still worries over higher inflation 27 Key sector selections 29

Automotive sector 30 Key stocks 30 Four-wheelers 30 Two-wheelers 31

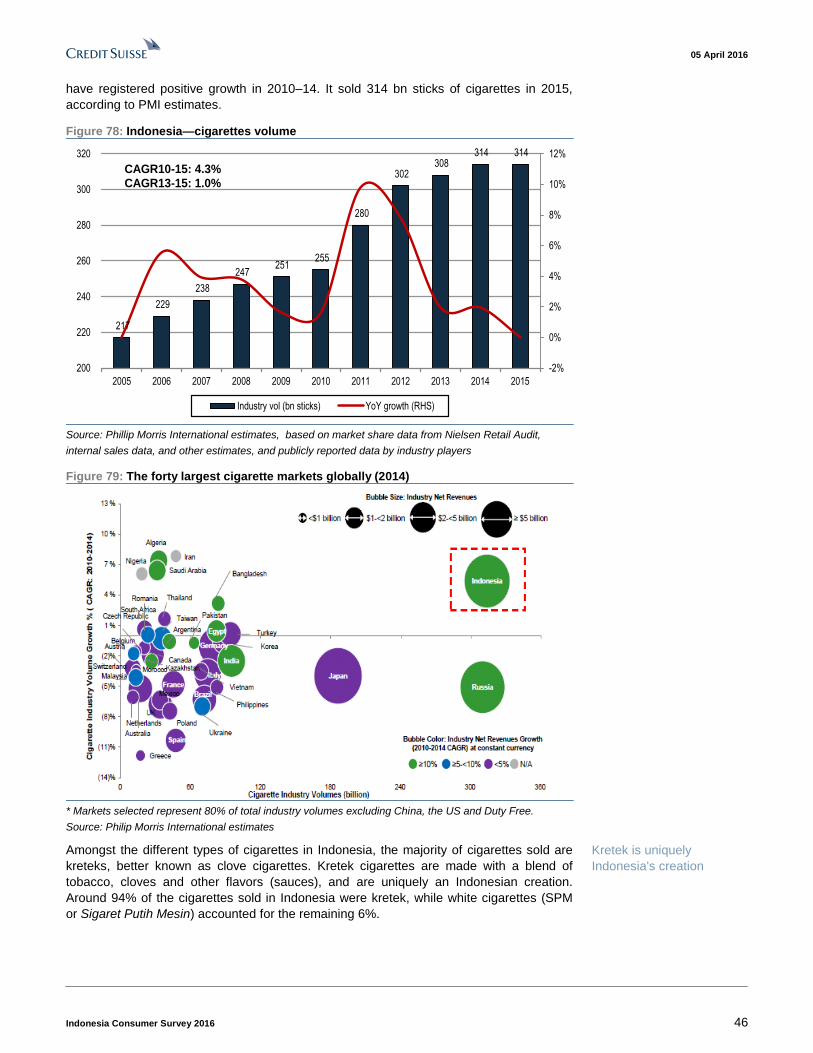

Food and beverages 34 Key stocks 34 Looking for convenience 34 Preference towards local brands 36 Modest price increase seen 37 The rising popularity of beverages 39 Instant noodles 42 Dairy products 43 Cigarettes 45

Personal care products 53 Key stocks 53 Defensive goods 53

Branded goods 55 Key stocks 55 Aspiring for premium brands 55 Fashion 57 Sports shoes and wear 59

Internet and e-commerce 61 Mobile phones 65

Key stocks 65 The era of smartphones and LCD TVs 67

Healthcare 69 Key stocks 69 Availability of Jamkesnas reduces healthcare spending 69

Property 72 Key stocks 72 Potential demand continues to be high 73 Price expectations 74 Young population is key 75 High disposable income growth 76 Rising middle class and affluent consumers (MAC) 77

Banks 78 Key stocks 78 Auto interest on lower interest 78 Key stock selections 81

05 April 2016

Indonesia Consumer Survey 2016 7

Telkom (Telekomunikasi Indo.) (TLKM.JK / TLKM IJ) 82 Astra International (ASII.JK / ASII IJ) 84 Indofood CBP (ICBP.JK / ICBP IJ) 86 Indofood Sukses Makmur (INDF.JK / INDF IJ) 88 Matahari Department Store (LPPF.JK / LPPF IJ) 90 Summarecon Agung Tbk (SMRA.JK / SMRA IJ) 92 Bank Tabungan Pensiunan Nasional Tbk (BTPN.JK / BTPN IJ) 94 Link Net Tbk (LINK.JK / LINK IJ) 96 Siloam International Hospitals (SILO.JK / SILO IJ) 98 Tiphone Mobile Indonesia (TELE.JK / TELE IJ) 100 Appendix 1: Respondents' summary 102

Demographics 102 Income and others 103 Auto 106 Food and beverages 107 Personal care 108 Luxury goods 109 Technology and Internet 111 Telecommunications 112 Travel 114 Education 115 Healthcare 116

Appendix 2: Indonesia macro 117

05 April 2016

Indonesia Consumer Survey 2016 8

Key themes from Indonesia We present you the sixth Credit Suisse Indonesia Consumer Survey, for which we

conducted a survey on 1,530 participants from ten exclusive areas.

2015 was a challenging year...

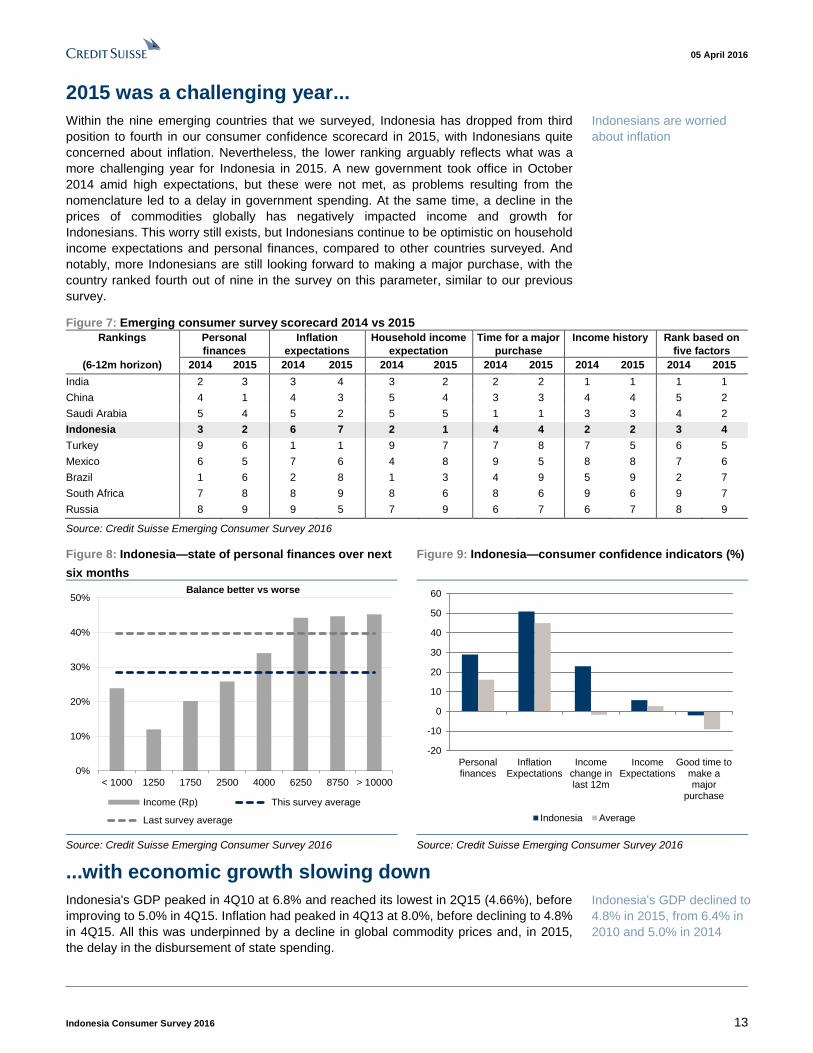

Within the nine emerging countries that we surveyed, Indonesia has dropped from the third

ranked to the fourth in our consumer confidence scorecard in 2015, with Indonesians being

quite concerned on inflation. Nevertheless, the lower ranking arguably reflects what was a

more challenging year for Indonesia in 2015. A new government took office in October 2014

amid high expectations, but they were not met, as problems resulting from the nomenclature

led to a delay in government spending. And at the same time, declining prices of commodities

globally have negatively impacted the source of income and growth for Indonesians.

But Indonesians continue to be optimistic

Despite disappointment related to Indonesia's weak economic conditions, purchasing power,

the government, etc., its GDP growth at 4.8% in 2015 is still one of the highest among other

emerging countries. Indonesia is the most optimistic country, based on our survey, whereby

26% of our respondents are optimistic about having higher income of more than 10% in the

next 12 months, while majority of Indonesians (69%) are expecting flat to 10% higher income,

and only 4% of Indonesians are expecting lower to flat income over the next twelve months,

which is the lowest as compared to other emerging countries that we surveyed. We believe

that despite a challenging 2015, the improvement seen in 2H15 created a feeling of optimism.

Our survey was conducted between October and November 2015, at the time when the

economy was starting to recover and the GoI was starting to spend. We note that by the end

of 2015, the Indonesian government had announced eight stimulus policy packages (of a total

of ten), which have started to generate some optimism.

How do Indonesians spend their money?

We have been conducting the survey for the past six years and over these years, we

continue to see the largest monthly spending is on food, which has increased to 50% of

household spending in 2015 (vs 38% in 2010). And food spending in Indonesia is much

higher from our overall survey average. The second largest spending is for savings, but

even though it has increased, it is still low as compared to the overall survey average. On

the other hand, the decline in spending is seen on auto (from 8% to 2%), housing (from

12% to 8%), education (from 9% to 4%), and healthcare (from 7% to 6%) between 2010

and 2015. We believe the spending decline in auto and housing is due to weaker

purchasing power, while the decline in education is due to the availability of the

government's programme for free education, and the decline in healthcare spending is due

to the implementation of the government's programme on National Health Care Insurance.

Meanwhile, spending on home & personal care and healthcare have maintained at 8%

and 6% of the total household spending, respectively.

Savings are improving but still low

Indonesians are still low on savings as compared to the other emerging countries that we

surveyed. However, compared to six years ago, this has actually marginally improved, with

significant improvement in urban areas. In 2010, Indonesians were saving 10.8% of their

income, while in 2015, it only reached 11%. The decline in employment opportunities in

the resource-based areas led to a decline in income.

Still worry on higher inflation

Although inflation has been coming down, Indonesians are still quite concerned about

higher inflation, which means higher living costs. That is why we think that savings are the

right mode at this time. Most respondents (64%) still think that inflation is going to be

higher than the past twelve months.

Indonesia is the most

optimistic country with

regards to future income

expectations

Largest spending is on food

(50%) followed by savings

(18%)

Compared to other

emerging countries, savings

are still low in Indonesia

05 April 2016

Indonesia Consumer Survey 2016 9

Key stocks preference Telkom (TLKM.JK, Rp3,350.00, OUTPERFORM, TP Rp3,800.00)

Indonesia’s cellular market continues to look attractive, with good monetisation of very high demand for cellular data services (driven by social networking). This has been made possible by an improving competitive environment, as the industry consolidates towards a three-player market. There is still a long way to go in growing data volumes; smartphone penetration on Telkomsel's network reached just 40.4% as at December 2015. In addition, 4G launch can add further impetus to this improving monetisation, with an additional 40% uplift in ARPU from 3G to 4G currently being experienced.

Astra International (ASII.JK, Rp7,325.00, OUTPERFORM, TP Rp7,600.00)

Improvement in macroeconomic conditions and launch of new models should support 4W

sales volume growth. Monetary easing (75 bp BI cut) should come into full effect in one to

two quarters, resulting in cheaper financing for cars and motorcycles.

Indofood CBP (ICBP.JK, Rp15,325.00, OUTPERFORM, TP Rp18,300.00)

Noodles division will continue to be the company's backbone although it is already highly

penetrated. The driver going forward will be product innovation and new product launches.

Indofood Sukses Makmur (INDF.JK, Rp7,225.00, OUTPERFORM, TP Rp8,700.00)

Fully integrated food company in Indonesia, with most of its earnings derived from the

listed Indofood CBP (ICBP). With slight recovery seen on CPO prices, its agribusiness

should see improvement.

Matahari Department Store (LPPF.JK, Rp18,175.00, OUTPERFORM, TP Rp19,400.00)

We believe Matahari will be the main beneficiary on the back of a rising middle class

segment. Its main exclusive label, Nevada, continues to be the top fashion brand favoured

by our respondents. We believe this is due to its nice design and quality supported by its

affordable price points.

Summarecon Agung (SMRA.JK, Rp1,620.00, OUTPERFORM, TP Rp1,960.00)

It has a good track record in township development in Indonesia and has been successful

in strengthening recurring income through rental income from retail spaces. Around 70%

of SMRA’s operating income is still being generated from the property development

segment. Additionally, we like the name given its exposure to medium segment as well as

its diversified land bank.

Bank Tabungan Pensiunan Nasional (BTPN.JK, Rp2,795.00, OUTPERFORM, TP

Rp3,500.00)

As the central bank now embarks on a lower rate environment with policy rate standing at

6.75% currently, BTPN having 85% deposits as time deposit should benefit most

compared to other banks under our coverage. For this year, we expect another 25 bp of

rate cut bringing policy rate down to 6.5%. As a reminder, when BI hiked its policy rate by

175 bp between June and November 2013, the net interest margins of the top-four banks

expanded, while that of second-tier banks compressed sharply over the next quarters.

Link Net (LINK.JK, Rp4,035.00, OUTPERFORM, TP Rp8,300.00)

Fixed internet access is also undergoing something of a renaissance in Indonesia, as demand for access to high-speed content and gaming increases. Thus, it is still our view that there is plenty of room for growth in the Indonesian broadband market. We expect that as the market develops, competitors will learn to target their rollouts in greenfield areas which are not yet covered by an existing player (such as Link Net), since it will result in a much higher return on their investment. Link Net offers high growth and high return on invested capital, and therefore offers an attractive way to invest in rising fixed internet penetration in Indonesia.

05 April 2016

Indonesia Consumer Survey 2016 10

Siloam International Hospitals (SILO.JK, Rp7,450.00, OUTPERFORM, TP

Rp13,000.00)

We expect Siloam's top-line growth to continue with its pipeline expansion plans and the

increase in healthcare spend as a percentage of total spend. By 2017, Siloam targets to

achieve 10,000 beds from the current 4,800 and have over 50 hospitals in more than 25

cities.

We believe that in the medium term. Siloam could be the best play to leverage on the

healthcare under-penetration story in Indonesia as it builds a hospital network unrivalled in

scope and scale across Indonesia. Margin issues are likely to be shortlived.

Tiphone Mobile Indonesia (TELE.JK, Rp775.00, OUTPERFORM, TP Rp900.00)

As the largest prepaid mobile phone voucher distributor in Indonesia, Tiphone Mobile

Indonesia is a beneficiary of higher data service consumption from rising internet access

needs.

Telkomsel owns a 25% stake (effective from Sep-2014); thus it is now an exclusive

distributor for Telkomsel, a market leader in Indonesia’s telecom industry (30% market

share in Telkomsel distribution). It is the only dealer that distributes through three

diversified channels (traditional, modern retail, and banks).

05 April 2016

Indonesia Consumer Survey 2016 11

Figure 5: Indonesia's consumer related names valuation

Company Ticker Price Rtg Mkt cap TP 16E

PE (x)

EPS growth P/E (x) EV-EBITDA

(x)

PB (x) ROE ADTV

3mos

(Rp) (US$mn) (Rp) at TP 16E 17E 16E 17E 16E 17E 16E 17E 16E 17E (US$

mn)

AUTOMOBILES & COMPONENTS 15.3 16.3% 17.9% 14.8 12.5 13.3 11.4 2.7 2.5 18.6% 19.7% 21.8

Astra International ASII.JK 7,325 O 22,477 7,600 15.3 16.3% 17.9% 14.8 12.5 13.3 11.4 2.7 2.5 18.6% 19.7% 21.8

BANKS 12.8 2.8% 16.5% 13.8 12.1 9.7 8.6 2.2 1.9 15.6% 15.8% 18.3

BTPN BTPN.JK 2,795 O 1,225 3,500 9.5 18.8% 15.2% 7.6 6.6 5.2 4.5 1.0 0.9 13.6% 13.5% 0.3

Bank Central Asia BBCA.JK 13,300 U 24,855 10,900 16.0 5.4% 8.0% 19.6 18.1 14.5 13.4 3.1 2.7 15.9% 15.2% 19.4

Bank Danamon BDMN.JK 3,795 U 2,729 3,500 10.3 36.7% 30.4% 11.1 8.5 2.5 1.9 1.0 0.9 8.9% 10.7% 0.6

Bank Jabar Banten BJBR.JK 900 O 655 1,200 7.9 6.0% 16.2% 5.9 5.1 3.4 2.9 0.9 0.8 14.9% 15.9% 1.1

Bank Mandiri BMRI.JK 10,100 N 17,684 9,800 11.8 -4.4% 21.0% 12.1 10.0 8.3 6.8 1.9 1.7 15.4% 16.8% 18.9

Bank Negara Indonesia BBNI.JK 5,100 O 7,137 5,650 10.2 14.5% 25.9% 9.2 7.3 6.4 5.0 1.2 1.0 12.7% 14.3% 12.5

Bank Rakyat BBRI.JK 11,100 N 20,756 11,400 11.7 -5.2% 16.9% 11.4 9.7 8.6 7.3 2.0 1.7 17.5% 17.0% 23.5

Bank Tabungan Negara BBTN.JK 1,730 N 1,388 1,850 8.4 26.4% 30.8% 7.8 6.0 (0.4) (0.3) 1.1 1.0 14.6% 16.1% 3.2

CONSUMER 38.0 13.9% 11.2% 37.0 33.2 26.0 23.3 24.8 21.8 56.4% 55.9% 6.1

HM Sampoerna HMSP.JK 99,000 O 34,914 108,500 42.2 14.8% 9.4% 38.5 35.2 28.6 26.0 14.4 13.3 37.4% 37.8% 5.9

Unilever Indonesia UNVR.JK 43,175 U 24,970 41,400 45.8 14.0% 12.4% 49.0 43.2 34.7 30.8 57.8 49.9 117.6% 115.4% 7.4

Gudang Garam GGRM.JK 65,200 O 9,509 61,500 19.6 9.2% 16.6% 20.8 17.8 12.6 11.2 3.1 2.8 14.9% 15.6% 5.8

Indofood CBP ICBP.JK 15,325 O 6,773 18,300 27.8 18.1% 12.0% 23.3 20.8 14.1 12.4 4.9 4.3 21.0% 20.8% 3.4

Indofood Sukses Makmur INDF.JK 7,225 O 4,809 8,700 18.7 9.0% 6.2% 17.4 16.3 7.3 6.6 2.1 2.0 12.3% 12.1% 5.5

Kino Indonesia KINO.JK 3,780 O 539 5,900 23.5 26.5% 18.5% 15.1 12.7 9.1 7.7 3.5 3.1 17.3% 17.9% 0.2

HEALTHCARE 38.9 19.8% 23.1% 36.7 29.5 23.8 19.8 6.6 5.7 18.9% 19.7% 4.9

Kalbe Farma KLBF.JK 1,450 U 5,152 1,350 24.5 16.2% 16.3% 26.3 22.6 17.7 15.4 5.5 4.7 20.8% 21.0% 6.6

Mitra Keluarga MIKA.JK 2,475 N 2,730 2,500 52.8 16.5% 23.6% 52.3 42.3 38.4 30.9 9.3 8.0 17.8% 19.0% 2.2

Siloam Hospitals SILO.JK 7,450 O 653 13,000 94.3 61.9% 74.9% 54.0 30.9 11.1 8.0 4.6 4.1 8.5% 13.1% 2.7

MEDIA 24.4 17.4% 22.7% 23.6 19.3 15.8 13.4 8.6 7.1 34.0% 34.0% 2.5

Media Nusantara MNCN.JK 2,150 O 2,327 2,165 18.6 20.1% 27.1% 18.4 14.5 10.2 8.6 2.8 2.4 15.0% 16.9% 3.6

Surya Citra Media SCMA.JK 3,245 N 3,596 3,400 28.1 15.7% 19.9% 26.9 22.4 19.5 16.5 12.5 10.1 46.4% 45.1% 1.9

REAL ESTATE 14.5 13.6% 16.6% 12.3 10.5 9.0 7.8 2.1 1.8 17.2% 17.2% 2.8

Alam Sutera ASRI.JK 376 N 560 450 7.3 8.0% 9.7% 6.1 5.6 6.4 6.0 0.9 0.8 14.7% 14.1% 1.3

Bumi Serpong Damai BSDE.JK 1,815 O 2,648 2,260 15.1 5.0% 11.2% 12.1 10.9 9.8 8.6 1.5 1.3 12.4% 12.2% 3.7

Ciputra Development CTRA.JK 1,285 O 1,493 1,310 12.9 14.9% 17.5% 12.7 10.8 7.7 6.5 2.1 1.8 16.2% 16.7% 1.8

Pakuwon Jati PWON.JK 492 O 1,796 580 13.0 22.4% 22.1% 11.0 9.0 8.0 6.6 2.6 2.1 23.2% 22.8% 2.7

Summarecon SMRA.JK 1,620 O 1,771 1,960 18.7 18.3% 20.5% 15.4 12.8 10.8 9.5 3.1 2.6 20.0% 20.3% 3.0

RETAILING 24.5 60.8% 17.8% 23.9 20.1 14.7 13.3 6.6 5.6 27.5% 27.3% 3.6

Ace Hardware ACES.JK 885 N 1,150 870 23.1 10.0% 5.4% 23.4 22.2 16.9 16.5 4.9 4.2 20.9% 19.0% 0.5

Erajaya Swasembada ERAA.JK 695 O 153 825 9.2 10.3% 15.5% 7.7 6.7 5.8 5.3 0.6 0.6 7.9% 8.6% 0.4

Matahari Department Store LPPF.JK 18,175 O 4,020 19,400 26.1 22.0% 15.8% 24.4 21.1 17.6 15.6 9.5 8.0 38.8% 38.1% 6.2

Matahari Putra Prima MPPA.JK 1,700 N 693 1,550 22.5 102.3% 29.6% 24.7 19.1 11.6 10.1 3.0 2.6 12.0% 13.9% 1.1

Mitra Adiperkasa MAPI.JK 4,925 O 620 4,500 35.4 424.8% 47.8% 38.8 26.2 9.0 8.0 3.0 2.7 7.7% 10.4% 0.2

Ramayana Lestari RALS.JK 715 O 385 900 16.6 14.7% 8.5% 13.2 12.1 4.7 4.4 1.4 1.3 10.8% 11.0% 0.2

Tiphone TELE.JK 775 O 418 900 13.9 25.7% 17.0% 12.0 10.3 7.7 6.9 1.8 1.5 14.6% 15.1% 0.2

TELECOMMUNICATION SERVICES 19.9 7.4% 15.0% 17.9 15.7 7.1 6.5 4.6 4.0 26.0% 26.6% 17.8

Indosat ISAT.JK 6,125 N 2,523 5,800 22.3 -207.9% 14.1% 23.6 20.6 4.7 4.5 2.5 2.4 10.6% 11.4% 0.2

Link Net LINK.JK 4,035 O 931 8,300 29.9 32.0% 40.6% 14.5 10.3 6.8 5.4 2.8 2.4 19.5% 23.0% 0.3

Protelindo TOWR.JK 4,295 N 3,322 4,200 17.7 39.4% 17.3% 18.1 15.4 12.2 10.8 6.1 5.1 33.8% 33.1% 0.1

Telkom TLKM.JK 3,350 O 25,595 3,800 19.9 22.7% 10.7% 17.5 15.8 6.1 5.7 4.1 3.8 23.1% 23.8% 23.9

Tower Bersama TBIG.JK 5,850 N 2,127 5,650 15.9 16.9% 53.4% 16.4 10.7 14.0 12.0 11.4 7.5 69.6% 69.6% 0.7

* Share price as of 01 April 2016

Source: Thomson Reuters, company data, Credit Suisse estimates

05 April 2016

Indonesia Consumer Survey 2016 12

The sixth Credit Suisse Indonesia Consumer Survey This is our sixth Credit Suisse Indonesia Consumer Survey, one part of a survey that the

Credit Suisse Research Institute conducts in nine emerging countries (Brazil, China, India,

Indonesia, Russia, Saudi Arabia, South Africa, Turkey, and Mexico). The Credit Suisse

Research Institute engaged The Nielsen Company, a leader in data measurement and

information across a wide range of industries and regions, to conduct face-to-face

interviews with nearly 16,000 participants. This survey is a comprehensive and exclusive

study of the consumption patterns in each country as well as individuals' outlook about the

future.

For Indonesia, we conducted the survey on 1,530 participants from ten exclusive areas,

similar to previous surveys. This includes six in Java (Jakarta, Jabotabek, Surabaya,

Gresik/Lamongan/Sidoarjo, Bandung, and Kabupaten Bandung) and four outside Java

(Medan, Deli Serdang, Makassar, and Gowa). We believe that these areas sit well with

Indonesia's economy and population given that around 65% of GDP is derived from Java

and the remaining 35% from outside Java, according to BPS (the Indonesia Bureau of

Statistics).

Similar to our previous five surveys, 66% of our participants live in urban areas with the

remaining 34% in rural areas, while 51% are female and 49% male. Most of the

respondents (72%) are below 45 years old, in keeping with Indonesia's young

demographic profile.

Each respondent was asked 180 questions, divided into 12 categories: (1) screening; (2)

autos; (3) food and beverage; (4) personal care; (5) branded goods; (6) computers and

TV; (7) mobile phones; (8) internet; (9) travel; (10) property; (11) education; and (12)

healthcare.

Figure 6: Indonesia's survey summary and key economic indicators

Source: IMF, EIU, UN, Credit Suisse Indonesia Consumer Survey 2016

We have undertaken our

sixth year of survey to

identify Indonesian

consumer behaviour

1,530 respondents in ten

areas (six in Java, four

outside Java)

Some 66% live in urban

areas and 34% in rural

areas, while 72% are young,

aged less than 45 years old

05 April 2016

Indonesia Consumer Survey 2016 13

2015 was a challenging year...

Within the nine emerging countries that we surveyed, Indonesia has dropped from third

position to fourth in our consumer confidence scorecard in 2015, with Indonesians quite

concerned about inflation. Nevertheless, the lower ranking arguably reflects what was a

more challenging year for Indonesia in 2015. A new government took office in October

2014 amid high expectations, but these were not met, as problems resulting from the

nomenclature led to a delay in government spending. At the same time, a decline in the

prices of commodities globally has negatively impacted income and growth for

Indonesians. This worry still exists, but Indonesians continue to be optimistic on household

income expectations and personal finances, compared to other countries surveyed. And

notably, more Indonesians are still looking forward to making a major purchase, with the

country ranked fourth out of nine in the survey on this parameter, similar to our previous

survey.

Figure 7: Emerging consumer survey scorecard 2014 vs 2015

Rankings Personal

finances

Inflation

expectations

Household income

expectation

Time for a major

purchase

Income history Rank based on

five factors

(6-12m horizon) 2014 2015 2014 2015 2014 2015 2014 2015 2014 2015 2014 2015

India 2 3 3 4 3 2 2 2 1 1 1 1

China 4 1 4 3 5 4 3 3 4 4 5 2

Saudi Arabia 5 4 5 2 5 5 1 1 3 3 4 2

Indonesia 3 2 6 7 2 1 4 4 2 2 3 4

Turkey 9 6 1 1 9 7 7 8 7 5 6 5

Mexico 6 5 7 6 4 8 9 5 8 8 7 6

Brazil 1 6 2 8 1 3 4 9 5 9 2 7

South Africa 7 8 8 9 8 6 8 6 9 6 9 7

Russia 8 9 9 5 7 9 6 7 6 7 8 9

Source: Credit Suisse Emerging Consumer Survey 2016

Figure 8: Indonesia—state of personal finances over next

six months

Figure 9: Indonesia—consumer confidence indicators (%)

0%

10%

20%

30%

40%

50%

< 1000 1250 1750 2500 4000 6250 8750 > 10000

Income (Rp) This survey average

Last survey average

Balance better vs worse

-20

-10

0

10

20

30

40

50

60

Personalfinances

InflationExpectations

Incomechange inlast 12m

IncomeExpectations

Good time tomake amajor

purchase

Indonesia Average

Source: Credit Suisse Emerging Consumer Survey 2016 Source: Credit Suisse Emerging Consumer Survey 2016

...with economic growth slowing down

Indonesia's GDP peaked in 4Q10 at 6.8% and reached its lowest in 2Q15 (4.66%), before

improving to 5.0% in 4Q15. Inflation had peaked in 4Q13 at 8.0%, before declining to 4.8%

in 4Q15. All this was underpinned by a decline in global commodity prices and, in 2015,

the delay in the disbursement of state spending.

Indonesians are worried

about inflation

Indonesia's GDP declined to

4.8% in 2015, from 6.4% in

2010 and 5.0% in 2014

05 April 2016

Indonesia Consumer Survey 2016 14

Figure 10: Indonesia's GDP peaked in 4Q10 and reached

its lowest in 2Q15 ...

Figure 11: ... with inflation is starting to decline in 4Q15

6.0

6.3

5.8

6.8

6.5

6.3

6.0 5.9

6.1 6.2

5.9 5.9

5.5 5.6 5.5

5.6

5.1

5.0 5.0 5.0

4.7 4.7

4.7

5.0

4.5

5.0

5.5

6.0

6.5

7.01Q

102Q

103Q

104Q

101Q

112Q

113Q

114Q

111Q

122Q

123Q

124Q

121Q

132Q

133Q

134Q

131Q

142Q

143Q

144Q

141Q

152Q

153Q

154Q

15

GD

P g

row

th (%

)

3.6

4.4

6.2 6.3

6.8

5.9

4.6

4.1

3.7

4.4 4.0

3.9

4.5

5.1

8.0 8.0 7.8

7.1

4.4

6.5 6.5

7.1 7.1

4.8

3

4

5

6

7

8

9

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

Infla

tion

(%)

Source: Bank Indonesia (BI) Source: Bank Indonesia (BI)

Figure 12: Palm oil (MYR/ton) Figure 13: Coal (USD/tonne)

1700

2200

2700

3200

3700

4200

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-14

Mar

-15

Sep

-15

Mar

-16

MY

R /

tonn

e

Palm Oil (MYR/ton)

Avg 2011: 3,273Avg 2012: 2,853Avg 2013: 2,383Avg 2014: 2,419Avg 2015: 2,160YTD 2016: 2,341

45

55

65

75

85

95

105

115

125

135

145

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-14

Mar

-15

Sep

-15

Mar

-16

US

D/m

etric

tonn

e

Coal (USD / metric ton)

Avg 2010: 99Avg 2011: 121Avg 2012: 94Avg 2013: 84Avg 2014: 70Avg 2015: 59YTD 2016: 50

Source: Bloomberg Source: Bloomberg

Indonesia's mining and quarrying sector witnessed 5% lower growth YoY in 2015,

whereas the sector's contribution to GDP declined to 8% in 2015, from 10% in 2010. This

is nevertheless evident in the weaker growth of mineral resources areas, such as

Kalimantan. Its GDP growth declined from 3.3% in 2014 to 1.3% in 2015, and Kalimantan

accounts for 8.8% of national GDP. The Sumatra area, known for its agriculture and

forestry, also saw its GDP lowered from 4.6% in 2014 to 3.5% in 2015. Sumatra is the

second-largest GDP contributor accounting for 21.7% of the nation's GDP. On the other

hand, Java, which is the largest GDP contributor (58.1%) and depends mostly on

manufacturing, reported only a slight decline in GDP, from 5.6% in 2014 to 5.5% in 2015.

Weak commodity prices

slowed economic growth,

particularly in the commodity

resources regions like

Kalimantan and Sumatra

05 April 2016

Indonesia Consumer Survey 2016 15

Figure 14: GDP growth, by region—weakness seen in Kalimantan

Source: Bank Indonesia (BI)

Figure 15: GDP breakdown by segment Figure 16: GDP breakdown by sector

54% 54% 55% 54% 55% 54%

12% 12% 12% 12% 12% 12%

31% 32% 33% 32% 33% 33%

2% 1% 2% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015

Private consumption Government consumption Investment Net exports

14% 14% 13% 13% 13% 13%

10% 10% 10% 10% 9% 8%

22% 22% 22% 22% 22% 22%

13% 14% 14% 14% 14% 13%

9% 9% 9% 9% 10% 10%

4% 4% 4% 4% 4% 4%4% 4% 4% 4% 4% 5%4% 4% 4% 4% 3% 3%

20% 19% 20% 21% 21% 22%

0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014 2015

Agriculture, forestry, and fishery Mining & quarrying

Manufacturing Wholesale and retail trades

Construction Transport & storage

Information & communication Public administration & defence

Others

Source: Bank Indonesia (BI) Source: Bank Indonesia (BI)

05 April 2016

Indonesia Consumer Survey 2016 16

Figure 17: GDP growth, by segment

-2%

0%

2%

4%

6%

8%

GDP Private consumption Government consumption Investment Net exports

2010 2011 2012 2013 2014 2015

Source: Bank Indonesia (BI)

Figure 18: GDP growth, breakdown by sector

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Ag

ricul

ture

, fo

rest

ry,

and

fish

ery

Min

ing

& q

uar

ryin

g

Man

ufa

ctur

ing

Ele

ctric

ity &

ga

s su

pply

Wat

er

supp

ly,

sew

era

ge, w

ast

em

ana

gem

ent

& r

em

edi

atio

nac

tiviti

es Co

nstr

uctio

n

Who

lesa

le a

nd r

eta

il tr

ades

, re

pair

of m

oto

r ve

hicl

es &

mot

orc

ycle

s

Tra

nspo

rt &

sto

rage

Acc

om

oda

tion

& f

ood

se

rvic

eac

tiviti

es

Info

rmat

ion

& c

omm

uni

catio

n

Fin

anci

al &

insu

ranc

e s

erv

ices

Re

al e

stat

e a

ctiv

ities

Bu

sin

ess

serv

ices

Pu

blic

adm

inis

trat

ion

& d

efe

nce;

com

pul

sory

so

cial

sec

urity

Ed

ucat

ion

Hu

ma

n h

ealth

& s

ocia

l wor

kac

tiviti

es

Oth

er

serv

ices

act

iviti

es

2011 2012 2013 2014 2015

Source: Bank Indonesia (BI)

The continuous economic slowdown has stemmed from the delay in Government of

Indonesia (GoI) spending in 1H15, where the GoI was faced with the nomenclature issue.

This resulted in both the consumer confidence and retail salex indexes, as measured by

the Bank of Indonesia, plummeting to below 100 in August 2015. The rupiah also

weakened by around 20% to as low as Rp14,700/US$, with inflation peaking at 7.2% in

3Q15. All this was in reverse by the end of 3Q15, when the GoI started to spend—mostly

on infrastructure—the IDR/USD exchange rate started to stabilise. Sentiment thus turned

more positive, continuing into early 2016, when the GoI lowered retail fuel prices and

reduced electricity tariffs as global oil prices declined.

Things started to look better

from the end of 3Q15

onwards

05 April 2016

Indonesia Consumer Survey 2016 17

Figure 19: Brent crude oil price (USD/barrel) Figure 20: Indonesia's retail fuel price (Rp/lt)

30

40

50

60

70

80

90

100

110

120

130M

ar-1

0

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-14

Mar

-15

Sep

-15

Mar

-16

US

D/b

arre

l

Brent crude oil (USD/barrel)

Avg 2010: 81Avg 2011: 112Avg 2012: 112Avg 2013: 108Avg 2014: 98Avg 2015: 54YTD 2016: 34

4000

4500

5000

5500

6000

6500

7000

7500

8000

8500

9000

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-14

Mar

-15

Sep

-15

Mar

-16

Rp7,050/litre

Source: Bloomberg Source: Bloomberg

Figure 21: Indonesia's GDP per capita (USD) Figure 22: Average exchange rate IDR/USD

3268

37563780

3682

3573

3401

3200

3300

3400

3500

3600

3700

3800

2010 2011 2012 2013 2014 2015

11200

11700

12200

12700

13200

13700

14200

14700

Mar-14 Sep-14 Mar-15 Sep-15 Mar-16

Rp/

US

D

Avg 2014: Rp11,870

Avg 2015: Rp13,457

YTD 2016: Rp13,644

Source: Bank Indonesia Source: Bloomberg

Figure 23: Consumer confidence index Figure 24: Retail sales index

95

98

101

104

107

110

113

116

119

122

Feb-14 May-14 Aug-14 Nov-14 Feb-15 May-15 Aug-15 Nov-15 Feb-16

110

140

150

160

170

180

190

200

210

Feb-14 May-14 Aug-14 Nov-14 Feb-15 May-15 Aug-15 Nov-15 Feb-16

192

Source: Bank Indonesia Source: Bank Indonesia

05 April 2016

Indonesia Consumer Survey 2016 18

But Indonesians continue to be optimistic

Nevertheless, despite disappointments in relation to Indonesia's lower purchasing power,

weak economic conditions, etc., its GDP growth at 4.8% in 2015 was still one of the

highest among the other emerging countries, but behind China (6.9%) and India (7.3%) in

2015. And with regards to GDP growth, only three countries that we surveyed reported

higher growth (India, Turkey and Mexico).

Figure 25: Real GDP growth among the emerging countries in 2014 and 2015E

7.3%

6.9%

5.0%

3.5%

2.9%

2.1% 1.6%

0.1%

0.7%

6.9%

7.3%

4.8%

3.4%3.1%

2.5%

1.3%

-3.8%

0.0%

6.5%

7.8%

5.2%

2.5%

3.5%

3.0%

1.6%

-3.5%

1.0%

-4%

-2%

0%

2%

4%

6%

8%

China India Indonesia Saudi Arabia Turkey* Mexico South Africa Brazil Russia

2014 2015 2016E

* Turkey is estimated data.

Source: Company data, Credit Suisse estimates

Indonesia is the most optimistic country, based on our survey, whereby 26% of our

respondents are optimistic about having higher income or incomes growing more than

10% in the next 12 months, while most Indonesians (69%) are expecting flat to 10% higher

incomes, compared to only 64% of those in India. In addition, only 4% of Indonesians are

expecting lower to flat incomes over the next 12 months, which is the lowest compared to

the other emerging countries that we surveyed. We believe that despite a challenging

2015, the improvement seen in 2H15 created a feeling of optimism. Our survey was

conducted between October and November 2015, when the economy was starting to

recover and the GoI had just started to spend. We note that by the end of 2015, the

Indonesian government had announced eight stimulus policy packages (out of a total of

ten), which have started to generate some optimism.

Optimism remains

05 April 2016

Indonesia Consumer Survey 2016 19

Figure 26: Indonesians are the most confident country in terms of income expectations in the next 12 months followed

by India and Brazil

6.5

5.0

9.8

4.6 4.9

2.7

5.7

3.6

9.1

4.3

8.6

1.0

2.5

8.8

4.3

9.3

5.9

7.4

2.5

0.5

2.1

8.1

1.6

7.4

4.1

3.2 2.7

0.2

3.9

2.7

6.8

4.1

8.0

3.7 3.7

1.4

0.5

4.0

2.0

5.8

5.0

4.5

3.6

2.6

1.5 1.2

0.5

0

1

2

3

4

5

6

7

8

9

10

Indonesia India Brazil China Saudi South Africa Turkey Mexico Russia

%

2010 2011 2012 2013 2014 2015

Question: In what way do you expect your household income to change in the next 12 months?

Source: Credit Suisse Indonesia Consumer Survey 2016

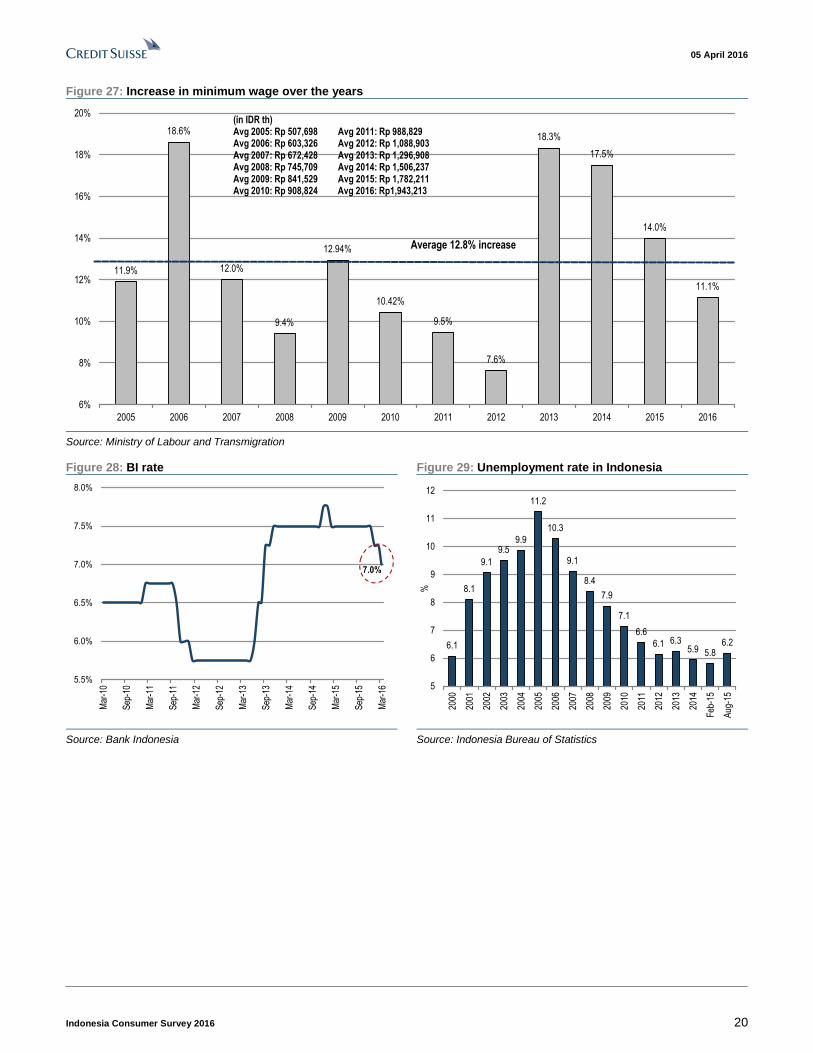

Minimum wages continued to be increased in 2015 by an average of 14%. This is lower

than the previous year's 17.5%, but is off a higher nominal base. Minimum wages vary by

region, with an average of Rp1.78 mn in 2015 compared to Rp1.5 mn in 2014. In 2016, the

GoI regulated the increase in minimum wage to give more certainty on the annual rise. It

applies a formula based on the sum of nominal GDP growth and the inflation rate. As

such, in 2016, we see an average minimum wage rise of 11.1% nationwide to Rp1.94 mn.

In our survey, we saw a significant hike in wages in 2014, then a drop in 2015, which we

view as a normalisation after the significant increases in 2013 and 2014, consecutively.

Respondents continue to be optimistic about future incomes, as the majority (69%) are still

expecting between flat to a 10% rise in incomes in the next 12 months, while those

expecting down to flat incomes were only 4% of respondents.

Unemployment has been declining to its lowest at 5.94% in 2014. However, with the

slowdown in economic growth, the unemployment rate picked up to 6.18% in August 2015,

based on data from BPS. We believe that the rate could already have peaked, as the

economy started to recover from 2H15 with government spending and GDP growth in

4Q15 reaching 5%.

GoI starts to regulate the

increase in minimum wage

in 2016

Normalisation of wage

increases

A rising unemployment rate

05 April 2016

Indonesia Consumer Survey 2016 20

Figure 27: Increase in minimum wage over the years

11.9%

18.6%

12.0%

9.4%

12.94%

10.42%

9.5%

7.6%

18.3%

17.5%

14.0%

11.1%

6%

8%

10%

12%

14%

16%

18%

20%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(in IDR th)Avg 2005: Rp 507,698 Avg 2011: Rp 988,829Avg 2006: Rp 603,326 Avg 2012: Rp 1,088,903Avg 2007: Rp 672,428 Avg 2013: Rp 1,296,908Avg 2008: Rp 745,709 Avg 2014: Rp 1,506,237Avg 2009: Rp 841,529 Avg 2015: Rp 1,782,211Avg 2010: Rp 908,824 Avg 2016: Rp1,943,213

Average 12.8% increase

Source: Ministry of Labour and Transmigration

Figure 28: BI rate Figure 29: Unemployment rate in Indonesia

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-14

Mar

-15

Sep

-15

Mar

-16

7.0%

6.1

8.1

9.1

9.59.9

11.2

10.3

9.1

8.4

7.9

7.1

6.6

6.1 6.35.9 5.8

6.2

5

6

7

8

9

10

11

12

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Feb

-15

Aug

-15

%

Source: Bank Indonesia Source: Indonesia Bureau of Statistics

05 April 2016

Indonesia Consumer Survey 2016 21

Figure 30: Indonesians have seen certainty over income rises in the past 12 months

% of Area Region Age Income*

respondent Total Urban Rural Java Ex Java 18-29 30-45 46-55 56-65 Low Mid High

2015

Down to flat 12% 13% 10% 12% 15% 12% 11% 15% 14% 20% 12% 5%

Flat to +10% 75% 72% 80% 73% 74% 76% 74% 74% 69% 74% 75% 60%

> +10% 13% 15% 9% 14% 11% 13% 15% 10% 17% 6% 13% 35%

2014

Down to flat 11% 9% 15% 11% 12% 10% 12% 10% 21% 18% 10% 12%

Flat to +10% 76% 75% 76% 74% 81% 74% 77% 78% 71% 87% 77% 72%

> +10% 13% 16% 9% 15% 7% 16% 12% 12% 7% 6% 13% 16%

2010

Down to flat 14% 15% 12% 12% 16% 11% 15% 15% 11% 14% 13% 0%

Flat to +10% 77% 76% 80% 79% 72% 78% 76% 76% 84% 83% 75% 81%

> +10% 9% 9% 9% 9% 12% 11% 9% 9% 5% 4% 11% 19%

Question: In what way do you expect your household income to change in the past 12 months

* Income is on monthly basis—low < Rp1.5 mn, mid Rp1.5-7.5 mn, high > Rp7.5 mn

Source: Credit Suisse Indonesia Consumer Survey 2016

Figure 31: …and continue to be optimistic for the next 12 months

% of Area Region Age Income*

respondents Total Urban Rural Java Ex Java 18-29 30-45 46-55 56-65 Low Mid High

2015

Down to flat 4% 5% 3% 5% 4% 5% 5% 6% 6% 8% 8% 5%

Flat to 10+% 69% 65% 76% 65% 77% 68% 67% 70% 68% 80% 77% 76%

>+10% 26% 30% 21% 30% 19% 26% 28% 23% 25% 12% 15% 19%

2014

Down to flat 3% 3% 3% 3% 4% 2% 2% 4% 8% 6% 3% 2%

Flat to +10% 69% 69% 71% 65% 81% 68% 70% 72% 71% 76% 70% 68%

> +10% 28% 28% 26% 33% 15% 30% 28% 24% 21% 18% 28% 29%

2010

Down to flat 4% 4% 2% 3% 4% 2% 4% 4% 4% 6% 4% 0%

Flat to +10% 70% 69% 77% 73% 67% 72% 70% 71% 81% 80% 68% 57%

> +10% 26% 27% 21% 23% 28% 26% 26% 25% 14% 14% 28% 43%

Question: In what way do you expect your household income to change in the next 12 months

* Income is on monthly basis—low < Rp1.5 mn, mid Rp1.5-7.5 mn, high > Rp7.5 mn

Source: Credit Suisse Indonesia Consumer Survey 2016

We also found that most Indonesians do not migrate to other places. Compared to China

and India, we see that fewer Indonesians tend to migrate from their hometown. As such, if

Indonesians do migrate, the urge for better income is much higher compared to those in

China and India.

Migration is not popular

among Indonesians

05 April 2016

Indonesia Consumer Survey 2016 22

Figure 32: Have you migrated from your hometown to

where you are currently living?

Figure 33: Did you migrate to earn a better income?

24 26

19

76 74

81

0

10

20

30

40

50

60

70

80

90

China India Indonesia

Yes No

66

79

93

34

21

7

0

10

20

30

40

50

60

70

80

90

100

China India Indonesia

Yes No

Source: Credit Suisse Indonesia Consumer Survey 2016 Source: Credit Suisse Indonesia Consumer Survey 2016

How do Indonesians spend their money?

Over the past six surveys, we continue to see the largest monthly spending is on food,

with food spending in Indonesia much higher than our overall survey average. In fact,

spending on food has increased to 50% of household spending in 2015 compared to 38%

in 2010. The second-largest spending is for savings. Even though we saw that savings

increased from 16% in 2010 to 18% in 2015, this is still low compared to the overall survey

average.

On the other hand, declines in spending were seen for auto (from 8% to 2%), housing

(from 10% to 8%), education (from 9% to 4%) and healthcare (from 7% to 6%) between

2010 and 2015. We believe the spending declines for auto and housing are due to weaker

purchasing power, while for education it is due to the availability of government

programmes for free education. For healthcare, the fall is due to the implementation of the

government's programme on National Health Care Insurance .

Meanwhile, spending on home, and personal care and entertainment is maintained at 8%

and 4% of total household spending, respectively.

Figure 34: Indonesian monthly spending by category vs overall survey average

0%

5%

10%

15%

20%

25%

30%

35%

Housin

g +

Pu

blic

Utilit

ies

Food

Tra

vel &

En

tert

ain

me

nt

Au

tos

Healthca

re

Ed

uca

tion

HP

C

Sa

vings

Pro

pert

y +

Local T

axe

s

Clo

thin

g

Oth

er

Indonesian monthly spend Overall survey average

Source: Credit Suisse Emerging Consumer Survey 2016

Largest spending is on food

(50%) followed by savings

(18%)

05 April 2016

Indonesia Consumer Survey 2016 23

Figure 35: Food spending increased to 50% in 2015 ... Figure 36: ...from 38% in 2010

Housing8% Auto

2% Education4%

Food50%

Home and Personal Care

8%

Health Care6%

Savings18%

Entertainment4%

Housing10%

Auto8%

Education9%

Food38%

Home and Personal Care

8%

Health Care7%

Savings16%

Entertainment4%

* As a % of total spending

Source: Credit Suisse Indonesia Consumer Survey 2016

* As a % of total spending

Source: Credit Suisse Indonesia Consumer Survey 2016

Figure 37: Indonesia's rising middle class and affluent (MAC) population, 2012-20

Note: Monthly household expenditure numbers are stained in real 2011 terms (adjusted for inflation) and include regular household

expenditures such as food, utilities, transportation, communication, and regular household supplies and exclude discretionary spending such as

entertainment, restaurant dining and similar categories. Note that the expenditure level is based on data from BPS, which uses regression

analysis to remove irregular expenditures. The spending levels used to define wealth classes in this model may differ from those used by market

research agencies to define socioeconomic status levels because of different data collection methodologies and models.

Source: BCG Population and Household Expenditure Database 2012; BCG analysis; Indonesian Government Statistics Office (BPS).

Indonesians continue to be conservative about wanting to make major purchases

compared to other emerging countries. Indonesia ranked fourth in the category with only

35% of respondents thinking this is an excellent/good time to make major purchases.

Obviously, compared to 2010, the time where Indonesia's GDP grew at 6.4%, a majority of

Indonesians (56%) thought it was an excellent time to make a major purchase. As such,

we believe that the decline in economic growth has led to a preference for larger savings,

instead of spending.

It is not the time to make

major purchases

05 April 2016

Indonesia Consumer Survey 2016 24

Figure 38: In your opinion, is now a good time to make a major purchase? (Area)

2015 2014 2010

% of respondents Total Urban Rural Java Ex Java Total Urban Rural Java Ex Java Total Urban Rural Java Ex Java

Excellent time 5 6 4 5 5 1 1 1 0 3 6 7 5 5 7

Good time 30 31 28 30 29 35 33 38 35 38 50 48 54 54 40

Not such a good time 59 57 61 58 59 59 62 52 59 50 40 40 39 37 48

A bad time 7 6 7 7 6 6 5 8 6 9 4 5 3 5 4

Source: Credit Suisse Indonesia Consumer Survey 2016

Figure 39: In your opinion, is now a good time to make a major purchase? (Age)

2015 2014 2010

% of respondents Total 18-29 30-45 46-55 56-65 Total 18-29 30-45 46-55 56-65 Total 18-29 30-45 46-55 56-65

Excellent time 5 5 5 6 4 1 1 1 0 0 6 6 6 6 6

Good time 30 28 33 27 25 35 37 34 34 28 50 53 49 50 45

Not such a good time 59 59 56 62 64 59 58 59 58 63 40 38 40 39 45

A bad time 7 7 6 6 8 6 4 6 8 9 4 3 5 4 4

Source: Credit Suisse Indonesia Consumer Survey 2016

Figure 40: In your opinion, is now a good time to make a major purchase? (Income)

2015 2014 2010

% of respondents Total Low Mid High Total Low Mid High Total Low Mid High

Excellent time 5 1 6 6 1 1 1 0 6 3 7 4

Good time 30 27 30 27 35 24 36 33 50 45 51 68

Not such a good time 59 64 57 66 59 68 58 63 40 46 38 21

A bad time 7 8 7 2 6 7 6 3 4 5 4 7

* Income is on monthly basis—low < Rp1.5mn, mid Rp1.5mn-Rp7.5mn, high > Rp7.5mn

Source: Credit Suisse Indonesia Consumer Survey 2016

With Indonesia's GDP per capita at around US$3,000, Indonesians tend to spend most on

lifestyle items, such as smartphones and internet access. Interestingly, this has been a

similar trend over the past six years since our first survey. This is in addition to basic

mobile phones and motorcycles. Instant noodles continue to be the most popular product,

despite already being highly penetrated, because of their affordability. This is followed by

bottled water, feminine hygiene, carbonated drinks and dairy products.

Rising need for

smartphones and internet

access

05 April 2016

Indonesia Consumer Survey 2016 25

Figure 41: Indonesia’s spending momentum 2015 vs 2014 (a year ago)

Carbonated drinks

Bottled water

Dairy Instant noodlesCigarettes

Tissues

Feminine hygiene

Cosmetics

Basic mobile phone

Smartphone

Cars

Internet access

Computers

PropertyHoliday

Motorcycle

Fashion apparel

Sport shoes and wear

WatchesJewellery

Perfumes

Leather goods, bags, and shoes

(10)

(5)

-

5

10

15

- 10 20 30 40 50 60 70 80 90 100

Re

cord

ed

sp

en

din

g in

20

15

vs.

20

14

2015 respondents that own/have bought each item (%)

Source: Credit Suisse Indonesia Consumer Survey 2016

Figure 42: Indonesia's spending momentum 2015 vs 2010—what has changed in behaviour from six years ago

Carbonated drinksBottled water

Dairy products Instant noodles

Cigarettes

Tissues

Feminine hygiene

Cosmetics

Basic mobile phone

Smartphone

Cars

Internet access

Computers

Property

Holiday

Motorcycle

Fashion apparel

Sport shoes and wear

Watches

Jewellery

Perfumes

(30)

(20)

(10)

-

10

20

30

40

- 10 20 30 40 50 60 70 80 90 100

Re

cord

ed

sp

en

din

g in

20

15

vs.

20

10

2015 respondents that own/have bought each item (%)

Source: Credit Suisse Indonesia Consumer Survey 2016

05 April 2016

Indonesia Consumer Survey 2016 26

Figure 43: Indonesian’s future item preference

Source: Credit Suisse Indonesia Consumer Survey 2016

Savings are improving, but still low

Indonesians still have low savings versus other emerging countries that we surveyed.

However, compared to six years ago, this has marginally improved, with significant

improvements in the urban areas. In 2010, Indonesians saved 10.8% of their income,

while in 2015, it only reached 11%. However, those in urban areas actually save more

than those living rurally. In urban areas, savings improved from 10.8% in 2010 to 12.4% in

2015, while in rural areas, savings declined from 10.5% to 6.2% over the same period.

Interestingly, those outside Java used to save more in 2010—16.1% of their income—but

this figure plummeted to 9.8% in 2015, due to, we believe, the significant decline in

employment opportunities in the resource-based area that led to income declines.

Figure 44: China has the highest savings % of total income

33%

20%

13% 13%

11% 11%

9% 9%

7%

0%

5%

10%

15%

20%

25%

30%

35%

China Saudi India Turkey Indonesia Russia Brazil Mexico South Africa

Sav

ings

as

% o

f inc

ome

Source: Credit Suisse Indonesia Consumer Survey 2016

Compared to other

emerging countries, savings

are still low in Indonesia

05 April 2016

Indonesia Consumer Survey 2016 27

Figure 45: Indonesia—savings as a percentage of income Figure 46: Indonesia—income versus savings (Rp mn)

10.8%10.8% 10.5%

8.8%

16.1%

11.0%

12.4%

6.2%

11.0%

9.8%

5%

7%

9%

11%

13%

15%

17%

Tot

al

Urb

an

Rur

al

Java

Ex

Java

Tot

al

Urb

an

Rur

al

Java

Ex

Java

Sav

ing

as %

of i

ncom

e

2010 2015

2.8

3.2

3.8

3.4

0.2

0.5 0.4 0.3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Java Ex Java Java Ex Java

Income Savings

2010 2015

Source: Credit Suisse Indonesia Consumer Survey 2016 Source: Credit Suisse Indonesia Consumer Survey 2016

Still worries over higher inflation

Despite inflation coming down, Indonesians still worry about it being higher, as it means

higher living costs and so we think that saving is the right mode at this time. Most of the

respondents (64%) still think that inflation is going to be higher than in the past 12 months.

Figure 47: Inflation is expected to decline or at least remain stable

83

14

2

76

21

4

64

31

5

73

24

4

64

31

5

0

10

20

30

40

50

60

70

80

90

It will be higher than the last 12 months It will be the same as the last 12 months It will be lower than the last 12 months

2011 2012 2013 2014 2015

Source: Credit Suisse Indonesia Consumer Survey 2016

05 April 2016

Indonesia Consumer Survey 2016 28

Figure 48: Inflation component breakdown (2015) Figure 49: Inflation component breakdown (2010)

8.1%

7.2%

6.4% 6.3%5.8%

4.2%

3.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

ProcessedFood,

Beverages,Tobacco

Food Transport,Comm.

andFinance

Housingand

Utilities

Health Education,Recreation

andSports

Clothing

9.4%

7.9%

4.6%

3.5%3.0%

2.7%

1.8%

0%

2%

4%

6%

8%

10%

Food ProcessedFood, Beverages,

Tobacco (BF)

Clothing Education,Recreation

and Sports (ER)

Housingand

Utilities

Health Transport,Comm. and

Finance

Source: Indonesia Bureau of Statistics Source: Indonesia Bureau of Statistics

05 April 2016

Indonesia Consumer Survey 2016 29

Key sector selections

05 April 2016

Indonesia Consumer Survey 2016 30

Automotive sector Key stocks

Astra International

■ Improvement in macroeconomic conditions and the launch of new models should

support 4W sales volume growth.

■ Monetary easing (a 75 bp BI cut) should come into full effect in one to two quarters,

resulting in cheaper financing for cars and motorcycles.

Four-wheelers

Four-wheeler (4W) penetration in Indonesia remained low at 7%, although the trend shows

an improvement from 6% in 2010. This improvement is on the back of several factors: (1)

affordable LCGC (low cost green car) models (US$8-9k); (2) attractive financing rates; and

(3) the need to be more mobile given there is no improvement in public transportation.

Compared to our previous surveys, people with low “incomes” are better off now, with 4%

of the respondents surveyed in the lower bracket having cars versus 3% in 2014 and 1%

in 2010. Further, last year's survey also booked an improvement compared to the 2010

survey when only 7% of the respondents were willing to purchase a car in the next 12

months. However, this year's weaker result compared to last year's is likely due to weaker

economic growth from 2Q-3Q15, coupled with high inflation and the rupiah’s weakening.

Figure 50: Four-wheeler penetration remains low, while people with higher incomes need to be more mobile

Area Region Age Income*

% of respondents Total Urban Rural Java Ex Java 18-29 30-45 46-55 56-65 Low Mid High

2015

Four-wheeler ownership 7 7 6 7 6 6 7 5 9 4 6 25

Prob. of purchase in 12M

Potentially Yes 8 9 7 9 8 9 8 11 4 6 8 17

Unsure 25 25 25 27 23 23 27 27 27 21 26 27

Potentially No 67 65 68 64 70 68 65 62 69 73 66 56

2014

Four-wheeler ownership 7 7 6 7 8 7 7 7 9 3 7 18

Prob. of purchase in 12M

Potentially Yes 14 14 14 13 16 14 14 14 6 13 14 18

Unsure 32 31 34 35 26 32 33 30 30 37 32 27

Potentially No 54 55 52 52 58 53 52 56 63 50 54 55

2010

Four-wheeler ownership 6 6 5 6 5 3 7 6 10 1 6 50

Prob. of purchase in 12M

Potentially Yes 7 8 5 6 9 5 8 10 6 3 8 39

Unsure 25 26 22 26 22 29 22 24 23 20 26 39

Potentially No 68 66 72 67 69 66 70 66 71 77 66 21

* Income is on a monthly basis—low < Rp1.5 mn, mid Rp1.5-7.5 mn, high > Rp7.5 mn

Source: Credit Suisse Indonesia Consumer Survey 2016

Toyota maintains its market leader position, while Honda is catching up

Toyota remained the preferred brand for car purchases, although there was a noticeable

decline in market share from 52% in 2010 to 23% in 2015. Honda is catching up with 22%

in 2015 versus 16% in 2010. We believe the decline in Toyota is attributed to it not

launching good new models, while Honda launched several hits (Mobilio, BRV, HR-V, and

Freed, among others). A deeper dive into the result also showed mixed results. The

younger population (18-29 years old) preferred Honda (25%) versus Toyota (13%), while

We like Astra on the back of

improvements in

macroeconomic conditions

and the launches of new

models

Honda is catching up with

22% of our respondents

preferring the brand in 2015

versus 16% in 2010. Toyota

is still the market leader with

a 23% market share

05 April 2016

Indonesia Consumer Survey 2016 31

Toyota's dominance remained resilient among the middle aged (30-45 years old). People

with higher monthly incomes also prefer Honda more now versus Toyota.

Figure 51: Toyota remains the market leader, with Honda catching up

% of respondents Area Region Age Income*

Total Urban Rural Java Non-Java 18-29 30-45 46-55 56-65 Low Mid High

2015

Toyota 23 18 36 19 36 13 36 20 17 27 23 20

Honda 22 24 18 21 24 25 18 24 33 18 21 38

Daihatsu 10 12 6 11 6 9 12 8 17 0 11 8

Nissan 6 6 3 6 3 4 2 13 17 0 7 0

BMW 8 11 3 9 6 11 8 8 0 8 9 0

Suzuki 3 5 0 3 3 0 4 8 0 0 3 8

Mitsubishi 1 0 3 1 0 2 0 0 0 0 1 0

Others 26 23 31 29 22 38 20 20 17 47 24 26

2014

Toyota 30 29 28 24 39 24 29 45 17 19 30 37

Honda 23 27 17 18 34 19 24 31 33 13 24 31

Daihatsu 9 5 15 10 6 5 12 10 0 7 10 5

Nissan 5 4 3 3 6 5 5 0 0 7 4 0

BMW 2 3 2 2 3 4 1 0 0 7 2 0

Suzuki 2 2 3 3 1 0 4 3 0 0 2 5

Mitsubishi 1 1 2 1 2 2 1 0 0 0 1 0

Others 29 29 30 40 9 40 25 11 50 49 26 21

2010

Toyota 52 49 58 47 64 43 50 63 62 58 50 64

Honda 16 14 19 13 15 17 15 15 13 16 16 8

Daihatsu 10 13 3 15 2 11 13 4 0 9 11 0

Nissan 3 3 3 3 2 3 5 0 0 0 3 11

BMW 1 1 3 1 2 0 2 0 13 9 1 0

Suzuki 3 4 0 4 0 3 3 4 0 0 4 0

Mitsubishi 2 3 0 4 0 0 3 4 0 0 2 8

Others 13 13 13 13 15 23 9 11 12 9 14 9

* Income is on monthly basis—low < Rp1.5mn, mid Rp1.5-7.5 mn, high > Rp7.5 mn

Source: Credit Suisse Indonesia Consumer Survey 2016

Two-wheelers

Motorcycles remain the wheels that move Indonesia's economy. Penetration remains high

at 84%, slightly lower than last year’s 86% but higher than 2010’s 73%. Among those

surveyed, 37% of respondents owning a motorcycle claimed that they have more than

one. The average age of a motorcycle is 3.7 years while the average ownership turnover

for them is 5.7 years.

It is noteworthy that the confidence of customers is eroding, in line with the trend seen for

four-wheelers. Only 28% of respondents are willing to purchase motorcycles in the next 12

months, down from 39% last year. This is likely due to high inflation in 2Q and 3Q last year

which resulted in people deferring their motorcycle purchases to buy staples. However, we

are more positive heading into 2016, as inflation has fallen and GDP rebounded in 4Q15.

Further, the BI cut its reference rate by 75 bp which should translate into cheaper

financing. Motorcycles continue to be popular and affordable in Indonesia as a result of a

poor public transportation system.

Motorcycle penetration

remains high at 84%,

although lower than last

year's 86%

05 April 2016

Indonesia Consumer Survey 2016 32

Figure 52: Two-wheeler ownership remains high in Indonesia

Area Region Age Income*

Total Urban Rural Java Non-Java 18-29 30-45 46-55 56-65 Low Mid High

2015

2-wheeler ownerships % respondents 84 85 82 72 65 86 86 77 81 63 87 91

No of 2Ws per household

1 motorcycle % owners 63 63 64 63 63 62 71 51 57 79 62 63

>1 motorcycles % owners 37 37 36 37 37 38 29 49 43 21 38 37

When was it purchased? Years ago 3.7 3.7 3.7 3.8 3.7 3.4 3.8 3.9 4.7 4.4 3.7 3.3

Motorcycle ownership turnover Years 5.7 5.8 5.5 5.8 5.5 4.9 5.9 6.5 7.2 5.3 5.7 5.4

Probability of purchase in 12M

Potentially Yes % respondents 28 29 26 27 32 29 31 27 14 26 29 25

Unsure % respondents 26 25 27 26 25 24 26 26 29 22 25 31

Potentially No % respondents 46 46 46 47 43 46 43 47 57 52 46 44

2014

2-wheeler ownerships % respondents 86 87 85 70 69 89 87 86 73 73 88 92

No of 2Ws per household

1 motorcycle % owners 64 65 63 65 62 65 65 60 68 78 64 47

>1 motorcycles % owners 36 35 37 35 38 35 35 40 32 22 36 53

When was it purchased? Years ago 3.7 3.7 3.8 3.7 3.7 3.3 3.9 3.7 5.0 4.3 3.7 3.7

Motorcycle ownership turnover Years 5.9 5.8 6.1 5.9 5.9 5.3 6.2 6.5 6.2 5.5 6.1 5.1

Probability of purchase in 12M

Potentially Yes % respondents 39 39 39 39 40 42 40 34 24 37 40 43

Unsure % respondents 30 29 33 32 26 29 31 29 36 35 29 31

Potentially No % respondents 31 32 28 29 34 28 29 37 40 28 31 26

2010

2-wheeler ownerships % respondents 73 74 70 68 70 73 72 80 63 54 79 92

No of 2Ws per household

1 motorcycle % owners 71 69 76 73 69 69 77 61 67 86 68 72

>1 motorcycles % owners 29 31 24 27 31 31 23 39 33 14 32 28

When was it purchased? Years ago 3.3 3.3 3.2 3.2 3.3 3.2 3.3 3.2 3.5 3.3 3.2 2.8

Motorcycle ownership turnover Years 5.6 5.4 6.0 5.5 5.9 4.9 5.8 6.6 5.9 5.5 5.7 6.5

Probability of purchase in 12M

Potentially Yes % respondents 26 29 22 27 24 23 31 22 27 16 28 55

Unsure % respondents 28 27 28 32 18 27 27 32 21 25 27 28

Potentially No % respondents 46 44 50 41 58 51 42 46 53 59 45 18

* Income is on monthly basis—low < Rp1.5mn, mid Rp1.5-7.5 mn, high > Rp7.5 mn

Source: Credit Suisse Indonesia Consumer Survey 2016

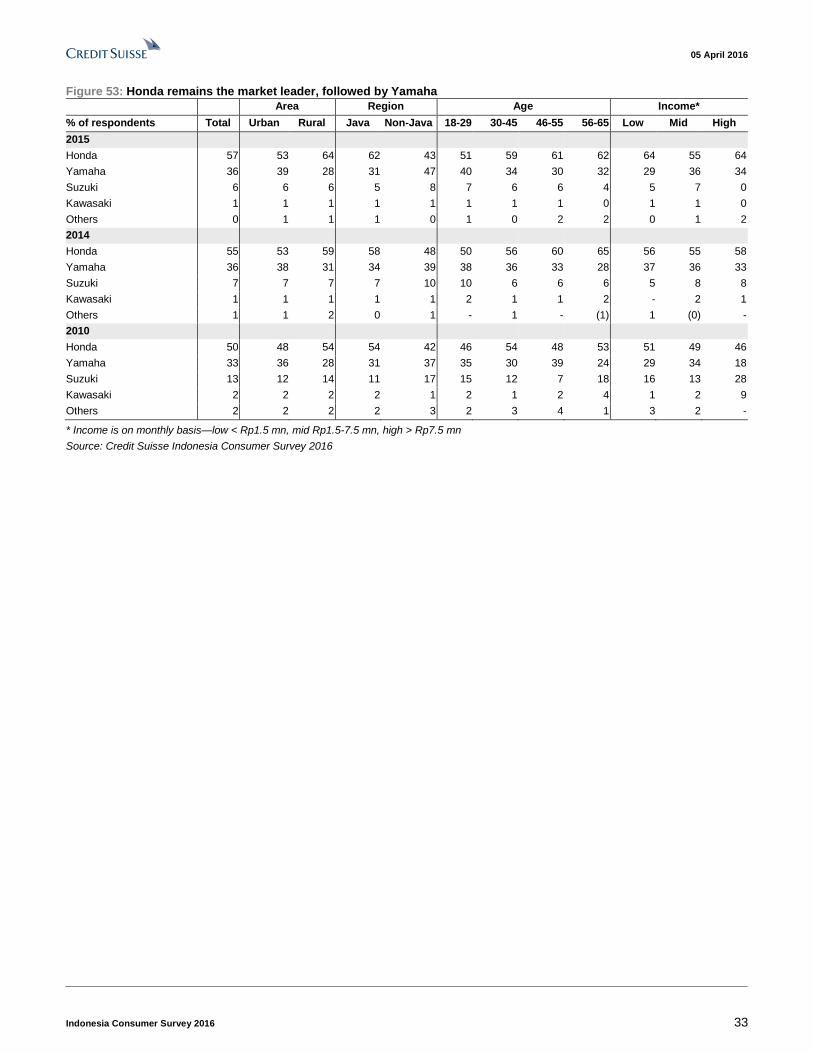

Honda consolidating its position as the market leader in 2W industry

Honda and Yamaha remain the two favourite brands for motorcycles, accounting for 93%

of the total market, based on our survey. There is a noticeable drop in Honda's non-Java

market share, although aggregately Honda and Yamaha are gaining more market share.

Honda is slowly eliminating competition through its strong network and after-sales service,

in addition to the introduction of attractive new models.

Honda and Yamaha remain

the two favourite brands for

motorcycles, accounting for

93% of the total market as

per our survey

05 April 2016

Indonesia Consumer Survey 2016 33

Figure 53: Honda remains the market leader, followed by Yamaha

Area Region Age Income*

% of respondents Total Urban Rural Java Non-Java 18-29 30-45 46-55 56-65 Low Mid High

2015

Honda 57 53 64 62 43 51 59 61 62 64 55 64

Yamaha 36 39 28 31 47 40 34 30 32 29 36 34

Suzuki 6 6 6 5 8 7 6 6 4 5 7 0

Kawasaki 1 1 1 1 1 1 1 1 0 1 1 0

Others 0 1 1 1 0 1 0 2 2 0 1 2

2014

Honda 55 53 59 58 48 50 56 60 65 56 55 58

Yamaha 36 38 31 34 39 38 36 33 28 37 36 33

Suzuki 7 7 7 7 10 10 6 6 6 5 8 8

Kawasaki 1 1 1 1 1 2 1 1 2 - 2 1

Others 1 1 2 0 1 - 1 - (1) 1 (0) -

2010

Honda 50 48 54 54 42 46 54 48 53 51 49 46

Yamaha 33 36 28 31 37 35 30 39 24 29 34 18

Suzuki 13 12 14 11 17 15 12 7 18 16 13 28

Kawasaki 2 2 2 2 1 2 1 2 4 1 2 9

Others 2 2 2 2 3 2 3 4 1 3 2 -

* Income is on monthly basis—low < Rp1.5 mn, mid Rp1.5-7.5 mn, high > Rp7.5 mn

Source: Credit Suisse Indonesia Consumer Survey 2016

05 April 2016

Indonesia Consumer Survey 2016 34

Food and beverages Key stocks

Indofood CBP:

■ The noodles division will continue to be the company's backbone and generate strong

free cash flow, despite it being already highly penetrated, as it has absolute pricing

power. The driver going forward will be product innovation and new product launches.

■ The luxury of having a strong cash flow has allowed the company to expand into other

products in its portfolio, such as dairy and beverages, as well as diapers.

Indofood Sukses Makmur:

■ A fully integrated food company in Indonesia, with most of its earnings derived from

the listed Indofood CBP (ICBP). It is also a parent company of the listed agribusiness

(IFAR), the flour milling company (Bogasari), and distribution company (Indomarco).

HM Sampoerna:

■ The largest cigarette company in Indonesia, and with main product on the SKM LTLN

(machine-made, kretek cigarettes, low-tar low-nicotine) that is well targeted to the

rising middle and upper market segment, and younger generation.

Gudang Garam.

■ It is the second largest cigarette company in Indonesia with main product on the SKM

FF (machine-made, kretek cigarettes, full-flavoured) that is well targetted to the middle

market segment.

Looking for convenience