Indirect-Cost Management Guide - Defense Acquisition University

134

INDIRECT-COST MANAGEMENT GUIDE NAVIGATING THE SEA OF OVERHEAD Third Edition October 2001 Web edition only (not in print) PUBLISHED BY THE DEFENSE SYSTEMS MANAGEMENT COLLEGE PRESS FORT BELVOIR, VA 22060-5426

Transcript of Indirect-Cost Management Guide - Defense Acquisition University

i

INDIRECT-COSTMANAGEMENT GUIDE

NAVIGATINGTHE

SEA OF OVERHEAD

Third EditionOctober 2001

Web edition only (not in print)

PUBLISHED BY THEDEFENSE SYSTEMS MANAGEMENT COLLEGE PRESS

FORT BELVOIR, VA 22060-5426

ii

For sale by the U.S. Government Printing OfficeSuperintendent of Documents, Mail Stop: SSOP, Washington, DC 20402-9328

Editing and Desktop Publishing: Kathryn E. Sondheimer

iii

PREFACE

DoD management has become increasingly concerned with broad-based increases in defense con-tractor indirect-cost rates. Many factors have contributed to these rate increases — the major factoris the significant reduction in the business base for most defense contractors due to the decliningdefense budget. As a result, DoD has expanded efforts to strengthen monitoring indirect costs. Ithas become important for acquisition management personnel to thoroughly understand the com-plex and sensitive subject of indirect-cost management.

By teaching various program management classes at the Defense Systems Management College(DSMC), I have found that the subject of indirect cost or overhead is commonly misunderstood andis usually referred to in unfavorable terms. It is thought to be virtually uncontrollable from a gov-ernment program management perspective. In addition, the large number of indirect rates one en-counters in the defense industry significantly contributes to the confusion our students experience.The objective of writing this guide is to demystify what many refer to as the “sea of overhead.” Nosingle published source for the general audience of acquisition personnel provides a complete over-view of indirect-cost management. This guide is intended to fill that void.

From the government perspective, monitoring indirect cost is exceptionally broad in scope; andmany people are involved. So it is essential for acquisition managers to thoroughly understand theinterrelationships of numerous DoD team members and how they improve the monitoring process.

This Second Edition incorporates Navy shipbuilding into government indirect-cost monitoring,describes the major new initiatives undertaken by DCMA and DCAA to accelerate settlement offinal overhead rates, identifies several changes made in various contractor system review require-ments, updates information related to executive compensation and restructuring costs, and elimi-nates prior coverage of functional reviews no longer performed by the DCMA.

To gain background information, I conducted onsite interviews with personnel actively performingindirect-management functions in industry and indirect-cost monitoring functions in the govern-ment. The arrangements were made through contacts with industry and government students atDSMC in our Advanced Program Management Courses. Recognizing that indirect rates are highlyproprietary information, my interest was not in the quantification of indirect-rate data but in thebusiness processes used to manage these difficult-to-control costs. Several contractors and govern-ment offices provided assistance to DSMC. I would like to express special appreciation to bothcontractor and government personnel located at Pratt-Whitney, Sikorsky, Loral Imagining Systems,and Boeing. I would also like to express appreciation to personnel in the DCMA Headquarters Over-head Center and in DCAA Headquarters who provided information relating to current issues andinitiatives in their organizations.

DSMC is the controlling agency for this guide. Comments and recommendations are solicited.

Jack D. CashProfessor of Business ManagementBusiness Management DepartmentDefense Systems Management College

iv

v

TABLE OF CONTENTS

PageChapter 1 — Introduction

Objective .......................................................................................................................... 1-1Significance of Indirect or Overhead Costs ..................................................................... 1-1Difficulty of Control ........................................................................................................ 1-4Current Environment ....................................................................................................... 1-5Importance of a Team Approach ...................................................................................... 1-5

Chapter 2 — Essentials for Understanding Indirect CostsIntroduction ..................................................................................................................... 2-1Direct or Indirect ............................................................................................................. 2-1Variable or Fixed Costs .................................................................................................... 2-4Allowable or Unallowable Costs ..................................................................................... 2-7Capitalized Versus Expensed ........................................................................................... 2-7Controllable or Noncontrollable Costs ............................................................................ 2-8

Chapter 3 — Typical Indirect-Cost PoolsOverhead Pools ................................................................................................................ 3-1Service Centers ................................................................................................................ 3-4General and Administrative Expense Pool ...................................................................... 3-4Major Categories of Indirect Expenses ............................................................................ 3-5

Chapter 4 — Allocation of Indirect CostsAllocation of Overhead.................................................................................................... 4-1Allocation of General and Administrative Expenses ....................................................... 4-6

Chapter 5 — Defense Industry Management of Indirect CostsIntroduction ..................................................................................................................... 5-1Planning ........................................................................................................................... 5-2Forecasting....................................................................................................................... 5-7Budgeting ...................................................................................................................... 5-10Control ........................................................................................................................... 5-13Variance Analysis .......................................................................................................... 5-15Ratio Analysis ................................................................................................................ 5-15Trend Analysis ............................................................................................................... 5-17

vi

Management Metrics ..................................................................................................... 5-18Regression Analysis ....................................................................................................... 5-20Industrial Engineering Analysis ..................................................................................... 5-22Contractor Actions to Reduce Overhead ....................................................................... 5-22

Chapter 6 — Impact of Government Contracting RequirementsIntroduction ..................................................................................................................... 6-1Relevance of Contract Type ............................................................................................. 6-2Federal Acquisition Regulation (FAR) Requirements ..................................................... 6-5

Cost Allowability ................................................................................................. 6-6Reasonableness .................................................................................................... 6-6Allocability .......................................................................................................... 6-6Generally Accepted Accounting Practices ........................................................... 6-7Contract Terms..................................................................................................... 6-7

Selected Costs .................................................................................................................. 6-7Advance Agreements ....................................................................................................... 6-9Certification of Indirect Costs ......................................................................................... 6-9Unusual Indirect-Cost Requirements............................................................................. 6-10

Independent Research and Development/Bid and Proposal Expenses .............. 6-10Cost of Money ................................................................................................... 6-13

Current Issues ................................................................................................................ 6-15Restructuring Costs ........................................................................................... 6-15Executive Compensation ................................................................................... 6-18Expiration of Funds ........................................................................................... 6-19

Chapter 7 — Cost Accounting Standards RequirementsIntroduction ..................................................................................................................... 7-1Applicability .................................................................................................................... 7-2Disclosure Statement ........................................................................................................ 7-3Cost Accounting Standards Relating to Indirect Costs ..................................................... 7-3

CAS 401 .............................................................................................................. 7-3CAS 402 .............................................................................................................. 7-4CAS 403 .............................................................................................................. 7-5CAS 404 .............................................................................................................. 7-6CAS 406 .............................................................................................................. 7-6CAS 410 .............................................................................................................. 7-7CAS 418 .............................................................................................................. 7-8CAS 420 ............................................................................................................ 7-11

Contract Price Adjustments ............................................................................................ 7-12

Chapter 8 — How the Government Monitors Indirect CostsIntroduction ...................................................................................................................... 8-1DCMA Overhead Center ................................................................................................. 8-2Relationship to Program Offices ...................................................................................... 8-3

vii

Government Team ............................................................................................................ 8-3Procurement Contracting Officer (PCO) .............................................................. 8-3Administrative Contracting Officer (ACO) .......................................................... 8-4Corporate Administration Contracting Officer/

Defense Corporate Executive (CACO/DCE) ........................................... 8-4Defense Contract Audit Agency (DCAA) ........................................................... 8-5Other Team Members .......................................................................................... 8-5

Monitoring Techniques .................................................................................................... 8-5Forward-pricing Rates ......................................................................................... 8-6Billing Rates ........................................................................................................ 8-9Final Rates ......................................................................................................... 8-10Tracking Indirect Costs ...................................................................................... 8-13Contractor Systems Reviews ............................................................................. 8-14

Contractor Purchasing System Reviews (CPSRs) ................................. 8-14Estimating System Reviews (ESRs) ...................................................... 8-15Compensation System Reviews (CSRs) ................................................ 8-15Contractor Insurance/Pension Reviews (CIPRs) ................................... 8-16Material Management and Accounting System (MMAS) Reviews ...... 8-17Earned Value Management Systems (EVMSs) ..................................... 8-17

DCAA Operational Audits................................................................................. 8-19DCAA Systems Reviews ................................................................................... 8-20

Accounting System Reviews ................................................................. 8-20Electronic Data Processing System Reviews......................................... 8-21Contractor Budget and Planning System Reviews ................................ 8-21Labor System Reviews .......................................................................... 8-22Billing System Reviews ......................................................................... 8-22

DoD “Should-Cost” Reviews ............................................................................ 8-22Correction of Problems ...................................................................................... 8-24Program Office and DCMA Relationship .......................................................... 8-24

Summary ...............................................................................................................................Sum-1

viii

1-1

11INTRODUCTION

OBJECTIVE

This guide provides acquisition managementpersonnel, especially personnel who are work-ing in program offices, with an insight into theprocess by which defense contractors manageand government personnel monitor indirectcosts. Although program office personnel arenot involved in indirect-cost management atcontractors’ facilities on a real-time basis, theyneed to thoroughly understand the nature ofthese costs and to know who to contact whenquestions or problems arise. Indirect costs havea significant cost impact upon all weapon sys-tem acquisition programs. Therefore, a primaryobjective of this guide is to explain the rolesand relationships of the many key governmentpersonnel involved with the indirect-cost man-agement process. Further, this guide promotesthe utilization of a team concept and highlightsareas for strengthening the management ofindirect-costs.

The level of detail in this guide is directed tononfinancial personnel because of the variedand broad backgrounds of people working inprogram management. It is not intended as adetailed “how-to” guide for industry or govern-ment functional managers but rather as a com-prehensive overview of basic principles and is-sues related to indirect costs.

The guide is organized to walk the reader throughthe many aspects of indirect-cost manage-ment. This introductory chapter discusses thesignificance of indirect costs, the complexityof managing them, and the necessity for a team

approach. There are chapters that define basicconcepts and terms, explain how indirect costsare allocated to contracts, explore how defensecontractors manage these costs, and discussrecent actions taken by defense contractors toreduce indirect costs. These chapters also ex-plain unique government requirements relatedto indirect costs; define who the various gov-ernment team members are as well as what theydo; and, finally, discuss current managerial is-sues.

SIGNIFICANCE OF INDIRECT OROVERHEAD COSTS

Whether cost is classified as direct or indirectmakes a tremendous difference in defense con-tracting. For example, when there is a diversebusiness base, the government pays 100 per-cent of all direct costs but only a portion of in-direct costs under its negotiated contracts. How-ever, the standard for determining what is adirect and what is an indirect cost is far fromuniversal in the defense industry — or in anyindustry for that matter. But the classificationof direct and indirect costs must be very exactat a specific defense contractor’s plant, and thissubject is presented in considerable detail in alater chapter.

For introductory purposes, indirect costs arethose costs incurred for the general operationof the business and are not specifically appli-cable to any one product line, program, or con-tract. Direct costs are associated with a specific“final cost objective” such as a specific defensecontract; indirect costs are associated with com-

1-2

mon or joint cost objectives such as the work onseveral contracts.

Indirect costs, in the aggregate, represent thelargest class of expense incurred under de-fense contracts. Recent estimates made by theDefense Contract Management Command(DCMA), in conjunction with discussionswith defense contractor top management ontheir DCMA Overhead Initiative, indicate thatindirect costs constitute approximately $90billion of the $170 billion total DoD work inprocess at all defense contractor plants. See“Exhibit 1. Significance of Indirect Costs” fora breakout between direct and indirect costsfor this estimate of work in process. Asshown, the indirect costs of 16 percent in-curred by subcontractors and vendors and the37 percent incurred by prime contractors (in-plant) represented approximately 53 percentof the total cost.

Of course, the ratio of indirect cost to total costvaries significantly among contractors withinthe defense industry because it depends uponmany factors. That is to say, there are numer-ous differences in both workforce and account-ing classifications as to direct or indirect costs,types of products, production methods used,degree to which materials are furnished by thegovernment, extent to which subcontractors areused, and the composition of facilities owner-ship. For these reasons, it is not meaningful toattempt to continuously track an exactindustry-wide ratio of indirect-to-total cost. Butregardless of the many differences betweencompanies, the indirect costs of doing businesswill at least roughly equal the direct costs inmost cases. Since indirect costs are such asignificant portion of current and future totalweapon system cost, program managers and oth-ers in the acquisition community must have a thor-ough understanding of these costs to ensure thatthe costs of weapons systems are kept on target.

At the outset, one should clearly recognize thatthe very nature of defense industry productsoften dictates high indirect costs on a per-unitbasis. The defense industry is critically depen-dent upon tremendous investments in fixed as-sets. The sheer size of some weapons systemsrequires huge buildings, sometimes coveringscores of acres. These large state-of-the-art fa-cilities suggest major depreciation, mainte-nance, property taxes, and other large, fixed in-direct or overhead costs. Large-scale researchand development projects are necessary for acompany to stay competitive in the defense in-dustry; and research and development work,which is necessary to produce a new weaponsystem, normally takes many years to complete.

Because DoD demands more and more techni-cal advancements, a company is often requiredto develop totally new materials in order to stayon the leading edge of technology and to con-tinue to remain competitive. This will mostlikely require new processes, tooling, machin-ery, and personnel. Product testing and evalua-tion is unusually expensive as it often involvesproduction of prototype products. In additionto the research, development, and manufactur-ing efforts of defense prime contractors, theyare responsible for overseeing the work of manysubcontractors and vendors who are producingnew, highly technical products. Defense con-tractors are required to make large investmentsin bid and proposal expenses in response tocomplex government requests for proposals. So-phisticated management control systems are re-quired in order to comply with stringent gov-ernment specifications for engineering,manufacturing, and product support.

Contractual reporting requirements are farmore detailed and expensive than those in thecommercial world. Environmental and safetyrequirements are substantial. Special producthandling and security requirements are char-

1-3

Exhibit 1. Significance of Indirect Costs

DoD Work inProcess

$170.0 Billion IndirectLabor &Fringe

Benefits58%

Depreciation10%

Occupancy10%

ComputerServices

9%

Utilities4%

Supplies,Services &

Travel3%

CorporateAllocations

2%

Miscellaneous4%

Indirect Focus$90 Billion

53% of Workin Process

SubcontractorVendorMaterial

18%

In-PlantIndirect

37%

In-PlantDirectLabor20%

SubcontractorVendorDirectLabor

9%

SubcontractorVendorIndirect

16%

acteristic of defense industry. All of these ex-penses are usually indirect or overhead coststhat must be absorbed by all contracts if thecontractor is to stay in business. In addition,defense contractors normally produce non-standard, tailored, and highly sophisticatedproducts in relatively low volumes. Assemblyis usually an intense, highly engineering-oriented process with small production quan-tities; and a low volume results in high indi-rect rates. This topic is discussed later in thisguide.

The defense budget has been in a continuingstate of decline during the past several years.In particular, the continuous and large-scaledecline in the defense procurement budget andin the research, development, test, and evalua-tion (RDT&E) budget has caused the defenseindustry to incur a steep drop-off in the busi-ness base. As a result, many defense contrac-tors’ indirect rates have increased significantly

as the value of contracts awarded by DoD hasdeclined. The remaining DoD contracts are nec-essarily forced to absorb additional indirectcosts that cannot be quickly eliminated. Dur-ing the 1980s, the indirect rates of most defensecontractors were safeguarded by a nearly con-tinuous increase in the business base. However,the demise of the Soviet Union ended this con-tinuity. During the 1990s, the annual procure-ment budgets of DoD have been essentially cutin half; and significant increases cannot reason-ably be expected in the immediate future.

A fundamental change in defense requirementshas brought about a significant financial im-pact: an increase in indirect rates. These in-creases result not only from the business-basedecline but also from the increase in indirectexpenses. For example, when the businessbase declines, the contractor is forced to layoff large numbers of direct employees; theirseverance pay is an indirect expense. One tech-

1-4

nological factor that drives increases in over-head expenses is the substitution of expensive,computer-operated, and laborsaving machinesfor direct labor in the manufacturing area. Thissubstitution simultaneously increases the over-head expenses (added depreciation and main-tenance charges) and also decreases the allo-cation base if it is direct labor dollars or hours.The financial impact is an immediate increasein indirect rates.

Many indirect efforts are, to a large extent, dis-cretionary in nature and can be reduced or elimi-nated by management if conditions warrant. Soindirect costs demand constant attention if thecontractor is to control them effectively. Froman industry perspective, there is probably noother area of management where the concen-tration of executive talent can be more effec-tive. Defense contractor managers are now tak-ing significant actions to reduce indirect costs.(See Chapter 5.)

From the government’s perspective, where ad-equate competitive market conditions are absent,there is a compelling need for a sound systemfor monitoring indirect costs to ensure that suchsignificant costs are managed efficiently. Thegovernment program manager needs to motivatethe contractors to exercise management controlsthat keep indirect costs at the lowest reasonablelevel and, in future contract prices, to includeonly those indirect costs that are reasonable andproperly allocated to the contracts. It is interest-ing to note that, when the volume of contractsdeclines, a contractor quickly incurs less directcontract costs. But indirect costs may not declineas rapidly since many fixed expenses may re-main in overhead pools, e.g., the leased cost fora building, supervisory labor, power, and prop-erty insurance. Consequently, government pro-gram managers should ensure that companymanagement is reducing indirect costs as rap-idly as prudent judgment allows.

DIFFICULTY OF CONTROL

The management of indirect costs has long beenrecognized as one of the most difficult areas tomanage. There is often no clear-cut relation-ship between these expenses and profit as thereis with direct cost. For example, material andlabor costs are very visible to management andcan be estimated and controlled directly. How-ever, the nature of indirect cost is such that theexpenses are spread over a number of expenseaccounts with various types of expenditures oc-curring sporadically over the year. Most defensecontractors have hundreds of expense accountsin each indirect-cost pool. Many different per-sons are responsible for incurring expenses. Theindirect totals that are reported every month onvarious cost reports are aggregates of hundredsof unrelated indirect expenses. Further increasesin indirect expenses occur more slowly, resultfrom a large number of unrelated actions takenby numerous managers, and may be less ap-parent. Management must constantly be awareof and understand the detailed composition ofsuch costs in order to effectively control them.

Many contractors who produce military hard-ware also produce similar hardware for com-mercial applications within the same divisionof the corporation. This is very advantageousto both the contractor and the government be-cause it enables each to become more effi-cient by capitalizing on significant economiesof scale. Unfortunately, this also creates am-biguity in the allocation of indirect costs be-tween defense and commercial contracts. Theacceptance by the government of what is con-sidered to be a “fair and reasonable” amountfor indirect costs has generated some of themost difficult problems relating to govern-ment contracts. As a result, most governmentcost regulations, which are contained in theFederal Acquisition Regulation (FAR), areassociated with the coverage of indirect costs.A thorough understanding of the regulatory

1-5

provisions, discussed in considerable detail inthis guide, is essential to understanding indi-rect costs.

Government acquisition management person-nel generally view indirect costs as vague andexcessive. They understand very well what gen-erates direct labor, direct material, and subcon-tract costs; but they are much less aware of whatgenerates indirect costs. They generally do notappreciate that indirect costs are generated bythe contractor’s total business volume and notby the volume of any specific contract. Indirectcosts lose their identity when allocated to con-tracts from common-cost pools; and, unlike di-rect costs, they cannot be analyzed on acontract-by-contract basis. Although monitor-ing indirect cost is often time-consuming andcomplex, it is absolutely essential for propervisibility of the weapon system acquisitionprocess.

CURRENT ENVIRONMENT

From a financial perspective, at no time in re-cent history have defense industry and gov-ernment acquisition personnel been faced witha greater challenge. Given the current envi-ronment of less large-scale manufacturing andmore prototyping, indirect rates are expectedto increase in the future, i.e., less productionand less manufacturing direct labor with moreengineering changes result in higher indirectrates. Also during the past few years, DoDhas changed the methods by which it contractsfor research and development. The shift placesa major emphasis on using cost-type contractsas opposed to fixed-price contracts and placesDoD in the position of assuming more costrisk. The results of a significant decline in thedefense business base of a company, alongwith DoD’s shift in how it contracts, places avery high probability for growth in indirect rates.

Schedule delays are frequently encountered onmany defense programs. The delays may becaused by unpredictable technical problems en-countered in research and development pro-grams, engineering changes to take advantageof technology improvements, budgetary uncer-tainties, and political decisions. These extendeddelays may cause significant increases in indi-rect costs.

In a declining business environment, rising in-direct rates generally mean that a contractor’sallocation base for distributing indirect or over-head costs, which are often direct labor hoursor direct labor dollars, is decreasing faster thanthe contractor can reduce indirect costs. Theremay be a delay in reducing indirect costs be-cause the base falls away on a continuous ba-sis, and the indirect budgets are usually deter-mined on an annual or semiannual basis. Again,continued oversight of the indirect-cost man-agement process and cost-containment mea-sures must be maintained.

IMPORTANCE OF A TEAMAPPROACH

From the government’s perspective, the ap-proach to monitoring indirect costs is to moni-tor the contractors management processes, notindividual indirect expenditures, with the ex-ception of samples to test the satisfactory orunsatisfactory operation of the managementcontrol system. The government expects thecontractor to manage its own indirect costs; but,at the same time, the government has a majorrole to play. The government’s objective is toinfluence the contractor’s process and to takeappropriate action before, not after, the costsare incurred. This focus is discussed in detail later(Chapter 8) with the primary emphasis beingplaced on negotiation of forward pricing rates.

1-6

Government acquisition management personnelmust understand that overhead costs relate to allbusiness in the contractor’s plant, not just to oneprogram. Therefore, the responsibility for moni-toring indirect costs necessarily rests with theAdministrative Contracting Officer (ACO), whois the government-responsible person located atthe contractor’s facility. However, the ACO’s jobcannot be performed adequately without assis-tance from program offices. This task requiresteamwork and a close working relationship be-tween the ACO and program managers at buy-ing activities. In particular, major program man-agers should expect the ACOs to depend upontheir input regarding the accuracy of the

contractor’s sales forecasts. At the buying activ-ity, the program manager has up-to-date knowl-edge of specific forecasts relating to programcost, schedule, and technical information. At thecontractor’s plant, the ACO is concerned withensuring that the right types of business processesexist and are being used to support all govern-ment programs at the contractor’s facility. TheACO’s interest in indirect cost is the assurancethat the costs are no higher than necessary andthat the government is not paying more than itsfair share. In order to function as a successfulacquisition team, each team member must un-derstand and support the roles played by theother members.

2-1

22ESSENTIALS FOR UNDERSTANDING

INDIRECT COSTS

INTRODUCTION

Due to the nature of defense business, DoDrequires a detailed knowledge of the internalcost structure of contractors; however, com-mercial customers do not require such knowl-edge. This situation developed because DoDnegotiates the price of many contracts basedupon the contractor’s cost rather than uponprice determined in a competitive market-place. The reader should also keep in mindthat the level of indirect costs is not necessar-ily an indicator of inefficiency. All businesseshave indirect costs, and they are a normal andnecessary part of doing business.

The use of ambiguous terms throughout theindirect cost management process creates realproblems for those uninitiated in governmentcontracting terminology. This is true in bothindustry and government. For example, inpractice, many people in both industry andgovernment commonly use the term “over-head” interchangeably with the term “indirectcost.” We will use the term “indirect cost”rather than “overhead” and will later discussthe differences between overhead and generaland administrative expenses, which are bothindirect costs. Many terms that have the samemeaning as overhead are used interchangeablyin industry: “burden,” “loading,” “add-on,”“management,” and “factory expense.” Thereare several classifications of costs as “either/or.” These costs require a detailed explanation.

DIRECT OR INDIRECT

Understanding details about indirect cost re-quires a regulatory understanding of severalterms. Direct costs must be understood beforelearning about costs. In this chapter, the dif-ference between direct and indirect costs, willbe clarified; and an understanding of the term“final cost objective,” will be provided. Also,examples of the types of direct and indirectcosts typically found in defense contractingare provided. There are many differences ofopinion and disputes about whether certaincosts should be classified as direct or indirect,therefore it is necessary to refer to the FederalAcquisition Regulation (FAR) for key defini-tions.

FAR 31.001 defines a cost objective as a func-tion, organizational subdivision, contract, orother work unit for which cost data are de-sired and for which provisions are made to ac-cumulate and measure the cost of processes,products, jobs, capitalized projects, etc. A fi-nal cost objective is a cost objective that hasboth direct and indirect costs allocated to it.Also, in the contractor’s accumulation system,the final cost objective is one of the final ac-cumulation points. In this guide, a final costobjective is a specific contract.

FAR 31.202 defines a direct cost as any costthat can be identified specifically with a par-ticular final cost objective. Costs identified spe-cifically with a contract are direct costs of thatcontract and are charged directly to the contract.

2-2

All costs specifically identified with other fi-nal cost objectives of the contractor are directcosts of those cost objectives and are notcharged to the contract directly or indirectly.Simply stated, costs are designated as directcosts because they are traceable to, and iden-tified with, a specific contract.

Direct material refers to all material costs thatare used in making a product and that are di-rectly associated with a change in the product.It includes raw materials, purchased parts, andsubcontracted items required to manufactureand assemble completed products. The easewith which direct material can be traced to thefinal product has a great deal to do with whetherthe material is considered as direct material. Forexample, miscellaneous small parts used inmanufacturing aircraft may be considered toosmall and too inexpensive to justify either thecost or time required to keep track of their costapplicable to specific aircraft. For practical rea-sons, they may be classified as an indirect ex-pense.

Direct labor is the labor identified with a par-ticular final cost objective or contract. Engineer-ing direct labor is that engineering work that isreadily identified with the end product, such asdesign, testing, reliability, maintainability, qual-ity, etc. Manufacturing direct labor includes fab-rication, assembly, inspection, and testing re-quired for producing the end product. The em-phasis on direct versus indirect labor in the de-fense contracting environment is significant tothe extent that many companies designate eachemployee as being either a direct or indirectemployee. In an effort to more accurately drivecost to the appropriate contract or project andto reduce indirect costs, some companies mayhave labor that is referred to as “direct distrib-uted,” “prorate,” “program direct support,” or assome other company-specific term. These costs,such as engineering administration, programsupport, scheduling, and engineering liaison, are

of an indirect nature; but they are distributedas direct costs based upon the direct area sup-ported.

Direct costs that are not materials or labor aregenerally referred to as Other Direct Costs(ODC). This cost is one that, by its nature, maybe considered indirect but, under some circum-stances, can be identified specifically with a par-ticular contract. ODC has all of the properties ofdirect material or direct-labor cost, yet it mayor may not be a tangible part of the final prod-uct. As an example, if a consultant providesassistance on several diverse and generalprojects, the cost is considered indirect and isincluded in overhead. However, if the time theconsultant spent benefited only one particularcontract, the cost is charged to the contract onwhich the consultant worked and is classifiedas ODC. Other examples of such direct costscould include special expenses for tooling, testequipment, insurance, travel, packaging, plantprotection, and computer expenses. These“special costs” are direct because they aretraceable to, and identified with, a specificcontract.

From an accounting standpoint, a job or work-order system is normally used by defense con-tractors to accumulate the direct costs of de-signing and manufacturing a company’s prod-ucts or of the performance of services under con-tracts. A separate series of work orders is openedfor each contract, to accumulate costs for vari-ous tasks, such as engineering, tooling, fabri-cation, and assembly. These work orders of-ten number in the hundreds and thousands.

FAR 31.203 defines an indirect cost as any costnot directly identified with a single, final costobjective; but it is identified with two or morecost objectives or an intermediate cost objective.Stated differently, after direct costs have beendetermined and charged directly to the contractor other work, indirect costs are those remain-

2-3

ing to be charged to the several cost objec-tives. The regulation further provides that anindirect cost is not allocated to a final cost ob-jective if those costs that are incurred in similarcircumstances and for the same purpose are in-cluded as a direct cost of that or any other costobjective.

Unlike direct costs, indirect costs cannot be eas-ily identified with one product or service. Be-cause indirect costs are generally plant-widecosts, contractor concern for control is notsolely motivated by any one contract. An ex-ample of such an indirect cost is the cost for heat-ing in a fabrication area that houses the work ofmany contracts. The heating benefits all contractsand cannot practically be identified with a spe-cific contract. Other examples of indirect costsinclude salaries and wages of supervisors, fore-men, and other indirect employees; nonproduc-tive time of direct employees; fringe benefits forall employees; depreciation; insurance; taxes;rent; retirement plan contributions; and corpo-rate management expenses allocated from thecorporate office.

A full understanding of the regulatory aspectscannot be achieved without recognizing that in-direct cost primarily comprises two components:overhead and general and administrative ex-pense. Overhead is that indirect cost related to aparticular part of the company or plant, suchas engineering or manufacturing. General andadministrative (G&A) expense is that indirectcost that supports the company as a whole, suchas the chief executive’s salary. The Cost Ac-counting Standards, which are discussed lateras unique government requirements, distin-guish between overhead and G&A and requirethat certain allocation bases be used in somecases. The differences in overhead, G&A ex-pense, and the various types of overhead costpools that are typically found in defense con-tracting will be discussed in greater depth inChapter 3.

“Exhibit 2; “Components of Contract Price”summarizes the composition of a typical gov-ernment contract. As shown, there are two costcomponents—direct and indirect. Again, di-rect costs are identifiable to a particular con-tract and are categorized as direct labor, di-rect material, and other direct costs. Indirectcosts relate to two or more contracts and areallocated to the appropriate contracts based onsome beneficial or casual relationship. Thetotal cost of a contract, then, is the sum ofdirect and indirect cost allocable to that con-tract. There are many methods for allocatingindirect cost to contracts, which will be cov-ered in Chapter 4. Note that an unusual item,called “cost of money” is also shown as anindirect cost. This very unusual indirect costand the unique government requirements re-lating to indirect costs are addressed later inChapter 6.

It is important to keep in mind that the meth-ods used by individual contractors to classifydirect and indirect cost are very different. Theaccounting method selected by a contractor isinfluenced by several factors, for example, thenumber and type of contracts in the plant, com-petitive environment, personal preferences ofmanagement, and allocation methods used.However, to adequately manage its costs in agovernment contracting environment, a com-pany must set firm criteria for the designationof all costs as direct or indirect. Later, underthe subject of cost accounting standards, moredetails will be provided on how some contrac-tors are required to submit a disclosure state-ment. A disclosure statement is a comprehen-sive document in which the company describes,in detail, how it accumulates and allocatescosts, including the specific identification ofdirect and indirect classifications.

In summary, if the cost is identifiable and if itbenefits a specific contract, it is charged directlyto that contract. If the expense cannot be iden-

2-4

tified with or does not benefit a particular con-tract, it is charged to overhead or G&A ex-pense; and it is allocated to those contractsthat do receive some benefit from it.

VARIABLE OR FIXED COSTS

An important step in the control of indirect oroverhead costs is the breakdown of all costs intotwo groups—fixed and variable. The variousindirect costs do not all behave in the same wayas production volume or business activity in-creases or decreases. One indirect cost may in-crease as a result of a new contract award whileanother may remain unchanged. Knowledgeof cost behavior is, therefore, very importantfor indirect cost forecasting and control. Thereare three broad categories of costs based uponthe criteria of behavior over business volume:variable, fixed, and semivariable costs.

Variable costs fluctuate directly and proportion-ally with business activity, i.e., production vol-ume or level of services provided. Without pro-duction there are theoretically, no variable costs.As “Exhibit 3. Cost Behavior” shows, variablecosts are constantly increasing as productionincreases. Labor, whether direct or indirect, isusually variable. For example, fabrication andassembly hours in the manufacturing area willincrease or decrease with the quantity produced.Any change in manufacturing processes, laborrates, or employee training will affect variablelabor costs. Other typical examples of variablecosts found in the defense contracting environ-ment are direct materials, fringe benefits, em-ployer payroll taxes, royalties, testing, and mis-cellaneous small parts. Production support costsalso are often variable. For example, the costof electricity varies with machine use, which,in turn, varies with the volume of production.Also, numerous miscellaneous factory supplies

Exhibit 2. Components of Contract Price

Cost ofMoney

MaterialHandling

MfgSupport

EngSupport

InterdivisionTransfers

CommercialItems

PurchasedParts

RawMaterials

Subcontracts

MfgLabor

EngLabor

Direct Labor Direct MaterialODC

Direct Cost Indirect Cost

Overhead G&A

Contract Price = Cost + Profit

2-5

and expenses are planned in relation to the vol-ume of direct manufacturing labor hours. Sincevariable costs are directly and proportionatelyrelated to productive activity, they are consid-ered much more controllable than fixed costs.

Fixed costs are relatively constant and, withinreasonable limits of plant capacity, do notvary with changes in production volume inthe short run. As Exhibit 3 shows, fixed costsare charted as a horizontal line; they have thesame total regardless of the volume or othermeasure of business activity. Many fixed-costitems relate to capacity. Some of these itemsare depreciation of buildings and machinery,real and personal property taxes on buildings,equipment and inventories, property and li-ability insurance, and rent. In the future, morecosts can be expected to become fixed ratherthan variable because of increasing use of

machinery as a replacement for manpower.Fixed costs are sometimes called “periodcosts” because they relate primarily to a pe-riod of time. Of course, if the period is longenough, all expenses will become variable.However, in the short run, a capacity cost of-ten cannot be changed and, therefore, is con-sidered to be fixed.

Fixed costs are established by management ona total-plant basis for a broad range of activi-ties, and they will remain unchanged withinthat “relevant range.” Theoretically, the rel-evant range represents the levels of activityover which cost relationships remain constant.That is, if volume increases (decreases), vari-able costs will increase (decrease) proportion-ately; however, fixed costs will stay fixedwithin the relevant range. If volume levels in-crease, capacity may be strained and additional

Exhibit 3. Cost Behavior

VARIABLE FIXED

SEMIVARIABLE

DIRECT LABORDIRECT MATERIALSALES COMMISSIONS

DEPRECIATIONRENTREAL ESTATE TAXESPROPERTY INSURANCEADMINISTRATIVE SALARIES

UTILITIESMAINTENANCE

UNITSUNITS

UNITS

$

$STEP-FIXED

INDIRECT LABOREQUIPMENT RENTAL

UNITS

$

$

2-6

fixed cost capability will be required. Althoughfixed costs are not initially established on acontract-by-contract basis, an award of a largecontract could produce a significant change inproduction volume and in the required level offacilities. Conversely, the loss of a large con-tract could result in idle capacity, which producesserious overhead cost problems.

Fixed costs are often referred to as discretion-ary costs, which indicate that control over theseexpenses rests with top management, who de-termine the amount of corporate investmentin plants, equipment, and organizational size.Two large discretionary costs in a defense con-tracting environment are Independent Researchand Development (IR&D) expenses and Bidand Proposal (B&P) expenses. These indirectcosts may often be increased, even when cur-rent business volume is decreasing. For ex-ample, management’s objective may be to gaina competitive advantage and to increase fu-ture business opportunities. Also, certain keypersonnel involved in research or proposal de-velopment activities might be so valuable tothe company that they would be retained evenif large volume decreases were experienced.It is interesting to note that some fixed costsare more fixed than others. For example, IR&Dand B&P expenses are usually budgeted bymanagement on an annual basis; and theycould, therefore, be considered fixed for theyear. However, these expenses could also bechanged quickly by a management decision.On the other hand, investments in plant andequipment are fixed for much longer periodsof time and cannot be quickly changed.

During production, few indirect expenses be-have as purely fixed or purely variable. A largenumber of expenses contain both fixed andvariable components. As Exhibit 3 shows,these expenses often remain relatively fixedbetween various ranges of volumes and thenadvance or decline in a step-type function as

volume changes occur. An expense of thisnature might be the cost of renting a machinethat, once available, can provide per-unit costsavings by handling a greater volume. Onceits capacity is reached, however, greater vol-ume can be achieved only by renting an ad-ditional machine. Semivariable costs varywith volume but not proportionally. Examplesof semivariable expenses are supervisory la-bor, repairs and maintenance, factory officesalaries, social security taxes, and some utili-ties, such as telephones and electricity. Man-agement control of semivariable expenses isaccomplished by dividing them into fixed andvariable portions and treating them accord-ingly. The fixed portion is considered to bethe necessary expense at the lower level ofthe expected volume, and the difference be-tween this lower level and the higher level istreated as variable.

The fixed and variable analysis of indirect costswon’t be found in published financial reports;but, in all probability, the company will sepa-rate indirect costs into fixed and variable com-ponents for internal decision-making purposes.Most business decisions involve the selectionof alternatives such as whether or not to makeor buy, to accept a special offer at a lower price,or to increase capacity. A fixed versus variableanalysis is needed for making such manage-ment decisions. Although a fixed and variableanalysis should be available internally withinevery company, what is called a fixed cost atone firm may be considered variable cost atanother. The analysis of costs into fixed andvariable components is a powerful tool for ana-lyzing indirect costs. Rarely does the defensebusiness volume remain at one level. The pro-cess of classifying costs according to the be-havior of the costs relative to changes in busi-ness volume leads the decision maker to be-come more knowledgeable about the cost driv-ers of indirect costs within a particular com-pany.

2-7

The relative proportion of fixed and variablecosts is referred to as a company’s cost struc-ture. The more fixed cost in a company’s coststructure, the more volatile will be changes inoverhead rates. This will become more appar-ent when the development of overhead rates isdiscussed in Chapter 4.

ALLOWABLE OR UNALLOWABLECOSTS

Unfortunately for defense contractors, one ofthe most significant factors affecting indirectcosts as well as profitability is the differencebetween allowable and unallowable costs. Thisdifferentiation does not exist in the commer-cial world. From the contractor’s perspective,many normal and necessary expenses, forwhich the government will not pay, exist foroperating a business. From the government’sperspective, there are many expenses that areconsidered unnecessary for government workor contrary to public policy for various rea-sons.

The specific criteria for cost allowability iscontained in FAR Section 31.201. Factors tobe considered in determining the allowabilityof individual items of cost include: (1) rea-sonableness, (2) allocability, (3) CASs pub-lished by the Cost Accounting StandardsBoard or from generally accepted accountingprinciples, (4) terms of the contract, and (5)any limitations in the Federal AcquisitionRegulation (FAR). There are about 50 selectedcost items spelled out in FAR Section 31.205for special consideration as to the allowabilityof the costs on government contracts. Theseselected items, subject to frequent change, arecommonly referred to in practice as the “CostPrinciples.” Both contractor and governmentpersonnel working on negotiated defense con-tracts must have personnel who are very fa-miliar with these rules and regulations.

Due to the recent media attention, many con-tractors have adopted an additional “mediasensitivity” test for allowability: “Before I in-clude this cost in an overhead claim to the gov-ernment, would I want to read about it in thenewspaper in the morning?” As a result of con-gressional interest during the past few years,emphasis has been placed on increasing thetypes of costs that are unallowable. Also, theCongress has enacted statutes providing forstrong penalties if contractors do not complywith unallowable cost provisions. Most recently,Congress has passed limitations on the com-pensation for individuals that can be chargedto defense contracts. Such congressional ac-tions have been highly controversial in indus-try. Since most unallowable-type costs are ofan indirect or overhead nature, they are dis-cussed in more detail and examples are pro-vided in Chapter 6.

CAPITALIZED VERSUS EXPENSED

Whether a particular cost is capitalized or ex-pensed makes a tremendous difference to thegovernment and the contractor. This conceptmust be grasped before indirect costs in thedefense industry can be understood. From anaccounting standpoint, the total costs of itemsthat are acquired for relatively small amountsand for general-purpose use are: (1) typicallyclassified as expenses and (2) placed intoindirect-cost pools for subsequent allocationto many contracts. However, the costs of suchitems for relatively larger amounts are classi-fied as assets and are considered to be capital-ized. In the case of capitalized items, only aportion of the costs is placed into indirect-costpools in the form of a depreciation expenseeach year.

In general, the capital versus expense distinc-tion normally relates to plants, equipment, andother fixed assets. For example, when a com-pany buys a machine that is not intended for

2-8

sale, it generally expects to use the machine overand over again for the benefit of many contractsover a number of years. Therefore, the companyrecords the cost of the machine as an asset andnot as an expense. An asset is simply a valuableitem that is owned or controlled by the company.In each subsequent accounting period when themachine is put into use, an appropriate portion ofthe cost of the machine is written off as an ex-pense based on the estimated service life of themachine. This expense is called depreciation andrepresents the systematic allocation of the cost ofthe asset over its estimated useful life. It also rep-resents the decline, due to wear and tear from useand passage of time, in the useful value of theasset.

As an example, assume that a general-purposemachine to be used in the manufacturing areais purchased by a contractor for $120,000. Theinstallation and checkout costs are $40,000. Fur-ther, assume that the machine has an expecteduseful life of 8 years; has no salvage value; andis placed into use at the beginning of the year.Using a “straight-line” method of depreciation,allow $20,000 ($160,000 divided by 8 years) ofthe total cost of the machine for each year as anindirect expense for depreciation. Recognizethat there are many acceptable ways of depre-ciating assets in addition to the straight-linemethod, but this method is the simplest. Re-gardless of the method of computation, as a gen-eral rule, depreciation expenses for all assetsare indirect or overhead costs. It is importantto note that the entire $160,000 is not classi-fied as an indirect expense in the first year. Thisis particularly important from a defense con-tracting perspective because a contractor canbill the government immediately under a cost-type contract for an appropriate allocation ofindirect expenses. However, the contractor can-not bill for the fully capitalized amount of theasset at the time that it is purchased.

It is important to realize that many companiesfollow a business practice of charging all as-set expenditures of relatively small amountsto expense instead of recording them as as-sets; thus, they avoid excessive accountingwork. Given the large investments in assetsand complexity of the defense business alongwith its many cost-based contracts, very spe-cific rules governing the capitalization andexpensing of assets can be expected. This topicis discussed further in Chapter 7 in the CASssection specifically CAS 404, “Capitalizationof Tangible Assets.”

Amortization, which is similar to deprecia-tion, is a term commonly used in the defenseindustry. Amortization is the periodic write-off or expensing over the estimated life ofcertain, often program related, unique assets,such as special tooling, special test equip-ment, and initial computer programmingcosts. Amortization and depreciation expensesare usually substantial amounts of indirector overhead cost for weapon system contrac-tors.

CONTROLLABLE OR NONCONTROL-LABLE COSTS

Since indirect costs relate to and are allocatedto more than one cost objective, they are muchmore difficult for management to control thandirect costs. To deal with this problem, somecompanies follow an internal practice of break-ing down indirect or overhead-type costs or-ganizationally as either controllable or non-controllable. This classification is based uponthe ability of a given manager to personallycontrol the costs. The concept provides anexcellent managerial tool for relating organi-zational structure and decision-making author-ity to specific activities that caused the coststo be incurred.

2-9

This managerial control technique, sometimescalled “responsibility accounting,” is discussedin further detail in Chapter 5, when the topicon how the defense industry typically man-ages indirect costs is discussed. Bear in mindthat company organizations differ, and thereare substantial differences in how companiesbreak down indirect costs between controllableand noncontrollable elements.

The basic principle of responsibility account-ing is that indirect costs should not be allo-cated to a manager unless the manager can ex-ercise control over costs incurred. The man-ager of a parts fabrication shop, for example,has direct control over and is concerned withthe amount of direct labor, direct material,and other direct costs expended on specificshop orders for building detailed parts to befed into assemblies. In addition, the managermay control over such indirect costs as the la-bor of foremen, training time, overtime, timespent waiting for work, and the call-in ofmanufacturing engineering. However, there areusually other costs charged to the manager’sorganization that cannot be controlled, for ex-ample, depreciation of the building, deprecia-tion of the machinery and tooling used by thepersonnel, or the allocation of costs from ser-vice organizations, such as the computer cen-ter. Such allocated expenses are often sepa-rated from nonallocated or controllable ex-penses in order to focus the manager’s atten-tion on the expenses that can be controlled.

In the short run, there are many indirect coststhat cannot be quickly reduced and, conse-quently, are considered to be uncontrollable.They typically include expenses for taxes, suchas state income, sales, and franchise taxes; lo-cal property taxes; royalties; insurance pre-

miums; employer payroll taxes; and deprecia-tion. However, in the long run, almost all costsare controllable to a certain degree by someonein the corporation. Costs incurred beyond thecontrol of a department manager are uncontrol-lable costs to the department; but generally arecontrollable by a higher manager, such as theplant manager. Examples of these plant-widecosts are employee welfare expenses for suchcosts as operating a company cafeteria, opera-tion of a medical facility, and providing an an-nual summer picnic for all employees. A por-tion of these costs would have to be allocated toall departments.

The costs of service departments may presentmanagerial control problems. For example,the cost of a large computer services depart-ment is the overall responsibility of the com-puter services department head. However, ser-vice costs that can be controlled by operat-ing departments, such as requests for specificcomputer services, should be the responsibil-ity of operating department managers.

Recently, some defense companies have beenmoving away from the classification of costsas controllable and noncontrollable. Some arevery opposed to, and do not allow the useof, the term “noncontrollable cost.” Their ba-sic tenet is that there is no such thing as anuncontrollable indirect cost, and they do notwant their managers to think in these terms.Defense companies want classification to fo-cus on a management philosophy, i.e., all costsmust be controlled at every organizationallevel and any cost that is allocated to their or-ganization should be questioned. This man-agement view is covered further in Chapter 5,when the topic of what defense contractors haverecently done to reduce overhead costs is ad-dressed.

2-10

3-1

33TYPICAL INDIRECT-COST POOLS

Establishing separate indirect-cost pools im-proves the visibility of difficult-to-control costsand facilitates the monitoring of similar typesof expenses. Depending on contractor needs forpricing and control, indirect costs are groupedinto logical cost pools relating to major func-tions and activities, types of products, company-specific organizational structure, market, andother considerations. Contractors whose prod-ucts, services, or contracts are substantially dif-ferent naturally require more detailed cost pools.The type or number of indirect-cost pools nec-essary for a contractor’s business segment is notspecified by industry standards or governmentregulations and, consequently, varies signifi-cantly.

Once indirect costs are properly pooled, theyare distributed to cost objectives using a direct-cost distribution base common to all cost ob-jectives to which indirect costs are allocated.The various methods of distributing or allocat-ing overhead costs to contracts is discussed indetail in Chapter 4.

Indirect-cost pools are categorized as overhead,service center, or general and administrative(G&A) expense pools. The primary distinctionbetween overhead and G&A cost pools is thatoverhead costs only benefit a part of a businesssegment, e.g., a functional organization such asengineering or manufacturing, while the G&Aexpense pool benefits the entire organization.“Exhibit 4. Typical Contractor Cost Hierarchy”shows the three broad categories of indirect-cost pools that require assignment or allocationto contracts, i.e., service centers, overhead

pools, and the G&A pool. The contractor’s busi-ness segment has three major contracts and sev-eral independent research and development/bidand proposal (IR&D/B&P) projects; all of theseprojects use direct material, direct labor, andother direct cost as well as four service centers,eight overhead pools, and one G&A cost pool.Of course, if a contractor expects to make aprofit, all costs must be assigned to contractsor final-cost objectives.

OVERHEAD POOLS

It is very common to find separate overheadpools for engineering, manufacturing, materialhandling, and for certain off-site activities, par-ticularly those performed at government facili-ties as opposed to contractor-owned facilities.Yet, it is conceivable that a small contractorcould have only one overhead pool. However,since defense industry products and services areusually complex and are procured under vari-ous types of contracts, defense contractors nor-mally have multiple overhead pools. Generally,the accuracy of cost information and manage-ment visibility are improved by the introduc-tion of additional indirect-cost pools. Again, thetype and number of indirect-cost pools vary sig-nificantly. One contractor may have 8 overheadpools; another may have more than 100. Eventhe same corporation may have totally differ-ent overhead pool structures for various busi-ness segments or separate divisions within thecorporation. More detailed government regu-latory requirements are in the Cost AccountingStandards (CASs) and the Federal AcquisitionRegulations (FARs); these requirements relate

3-2

Exhibit 4. Typical Contractor Cost Hierarchy

(1) Some overhead pools, such as Product A, may not apply to all contracts.(2) A service center, such as computer services, may perform work on specific contracts (as other direct

costs) and support overhead pools, such as engineering.(3) Use and occupancy includes depreciation of the plant and equipment, maintenance, insurance,

taxes, facilities engineering, janitorial services, etc.(4) Operations includes manufacturing planning, production control, quality inspection, graphics,

reproduction, etc.(5) IR&D/B&P expenses are indirect expenses, e.g., direct labor, direct materials, and allowable

overhead, that are collected on a project basis similar to contracts. They are accumulated and thentransferred for allocation as an indirect expense.

TRANSFERRED

TO

G&A

INDIRECT

COST

DIRECT

COST

COMPUTERSERVICES

USE ANDOCCUPANCY (3)

CONTRACT A

DIRECT MATERIALSDIRECT LABOR

OTHER DIRECT COSTS

SERVICE CENTERS (2)

CONTRACT B

DIRECT MATERIALSDIRECT LABOR

OTHER DIRECT COSTS

CONTRACT C

DIRECT MATERIALSDIRECT LABOR

OTHER DIRECT COSTS

IR&D/B&PPROJECTS (4)

DIRECT MATERIALSDIRECT LABOR

OTHER DIRECT COSTS

ENGINEERING PRODUCT A PRODUCT B ASSEMBLY FABRICATION TOOLINGMATERIALHANDLING

OPERATIONS (4) INDUSTRIALENGINEERING

CORPORATE OFFICE EXPENSE ALLOCATIONSEGMENT GENERAL AND ADMINISTRATIVE EXPENSES

INDEPENDENT RESEARCH AND DEVELOPMENT EXPENSESBID AND PROPOSAL EXPENSES

G&A

CONTRACTOR BUSINESS SEGMENT

OVERHEAD COST POOLS (1)

OFF-SITE

3-3

to the criteria for accumulating indirect costsinto cost pools. This topic is discussed in moredetail in Chapter 7.

Most defense contractors have separate over-head pools for engineering and manufacturing.Engineering overhead includes the costs of di-recting and supporting all engineering-orga-nization related activities that cannot be as-signed to specific contracts. Engineeringoverhead typically includes engineering super-vision, engineering policies and procedures, en-gineering buildings and equipment deprecia-tion, software, training, maintenance, supplies,scientific library, and fringe benefits. Manufac-turing overhead, sometimes called factory over-head or factory burden, usually includes allitems of production costs except direct mate-rial, direct labor, and other direct costs. Thecomponent elements of manufacturing over-head typically consist of several major catego-ries of expense, including supervision, admin-istration, time standards engineering,manufacturing research, tool cribs, mainte-nance, indirect supplies (such as small tools),grinding wheels, and cleaning supplies. It usu-ally includes costs associated with factory la-bor fringe benefits, such as social security taxes,leave, group health insurance, etc. It also in-cludes factory-related fixed charges for depre-ciation, insurance, rent, and property taxes.

Manufacturing overhead is often broken downinto several overhead pools rather than one over-all manufacturing pool. This is particularly truewhen several different products require vary-ing amounts of overhead support. For example,separate overhead pools are often found for as-sembly, fabrication, tooling, and quality. Engi-neering and manufacturing overhead pools aresometimes referred to as resource pools becausethey collect or pool the costs of administrativeand other indirect expenses associated with cen-tralized resource organizations that supportmultiple products.

If a contractor’s activities are spread out geo-graphically, the use of separate off-site indirect-cost pools for each geographic location willusually produce more accurate allocations ofindirect cost than the use of in-plant orcompany-wide pools. Overhead pools estab-lished for off-site or remote locations shouldbe based on eliminating indirect costs, whichdo not provide a benefit for the off-site activi-ties, from the overhead pool. For example, oc-cupancy costs would be eliminated from off-site pools for work performed at governmentfacilities because government facilities are usedrather than the contractor’s. If a substantial trav-eling distance is involved, a reduction could alsobe made for management and supervisory ex-penses. Rather than having separate rates foreach site, some contractors have establishedfield service overhead pools to cover all workat customer locations away from the main plant.

Defense contractors sometimes establish prod-uct pools with the objective of increasing thedirect traceability of costs to individual prod-uct lines. Such pools are often established fordedicated program or product engineering, pro-curement, spares, or other elements in order toidentify similar product overhead costs withbenefiting contracts or final cost objectives.Product pools may be established for new pro-grams during the bid phase and discontinuedwhen the effort is complete and all programcosts are recorded. If a program phases downto a small effort over an extended time, the poolmay be merged with another pool. Examplesof product pools are missile systems, electronicsystems, advanced projects, special projects, orspace systems.

Material overhead, commonly called materialhandling, includes the functions of purchasing;receiving and inspection; handling and storage;inventory control; and expediting materials re-quired for contracts. Other examples of sepa-rate overhead cost pools often found in defense

3-4

industry include overhaul and repair, modifica-tion, manufacturing development, subcontractadministration, testing, packing and crating,customer service, product support, and fringebenefits.

SERVICE CENTERS

Service centers are departments or other func-tional organizations that perform specific tech-nical or administrative work for the benefit ofother organizational units. Their costs may beallocated, based on some measure of usage,partially to contracts as direct costs and par-tially to other indirect-cost pools. For example,the cost of the computer service center could becharged directly to contracts or to other indirect-cost pools on the basis of the hours worked byprogrammers.

Programmers could scientifically program aspecific engineering contract, program numeri-cally controlled machines for the manufactur-ing overhead function, update an inventory con-trol system for the material handling overheadfunction, or modify a payroll system for ac-counting, which would be a G&A function. Ofcourse, the programmers could not charge bothdirect and indirect costs for the same task. Eachtask performed must have only one labor charge.Use and occupancy is another example of a verylarge service center commonly found in thedefense industry. This service center is usuallydistributed based upon square footage occupiedby users. It includes the costs for depreciation,maintenance, utilities, leases, security and fireprotection, environmental cleanup, and facili-ties engineering.

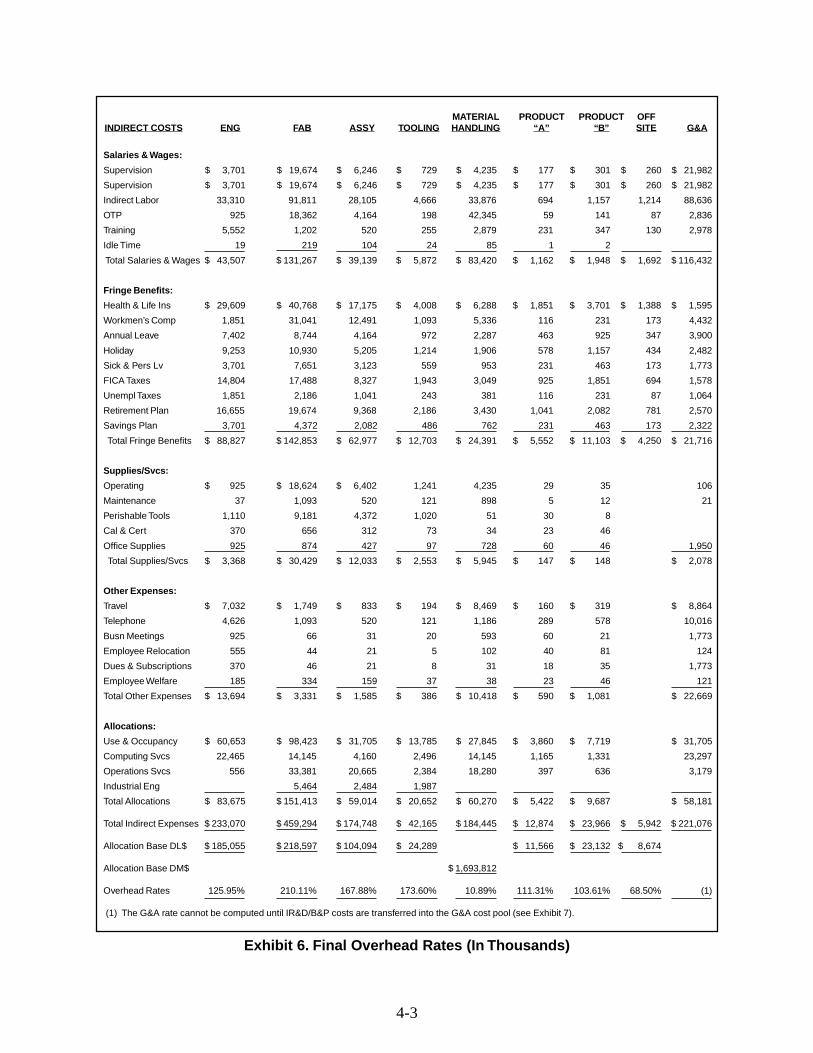

From an accounting standpoint, service centersare usually closed out each month by transfer-ring or allocating the cost of operating the ser-vice to the responsible users. “Exhibit 4. Typi-cal Contractor Cost Hierarchy” shows servicecenters for computer services, operations, in-

dustrial engineering, and use and occupancy.“Exhibit 5. Final Overhead Pools” shows howan appropriate amount of these service centercosts might be allocated to various final over-head pools. These amounts are shown at thebottom of the exhibit under the category of“Allocations.” Recognize that some service cen-ter costs will be charged directly to contracts,based upon use.

Other examples of service centers often foundin defense industry are print shops, graphic arts,reproduction services, communication services,motor pools, mail rooms, technical publications,calibration labs, wind tunnels, and corporate air-craft. Some contractors refer to service centersas secondary pools, support pools, or proratedepartments. In government contract accountingterms, they are referred to as intermediate costobjectives because costs are temporarily col-lected in the service center as an intermediatestep before they are later allocated to final costobjectives, such as specific contracts.

GENERAL AND ADMINISTRATIVEEXPENSE POOL

G&A expenses represent the cost of activitiesnecessary to the overall operation of the busi-ness as a whole, but a direct relationship to anyparticular cost objective cannot be shown. G&Aexpenses include the top management functionsfor executive control and direction over all per-sonnel, facilities, and activities of a businesssegment. Typically, G&A expenses include hu-man resources, accounting, finance, public re-lations, contract administration, legal, selling,independent research and development, bid andproposal expenses, and an expense allocationfrom the corporate home office.

A contractor’s selling expenses may be includedin the G&A expense pool or may be accountedfor in a separate cost pool. Selling expenses arethe efforts to market a contractor’s products or

3-5

services and include expenses for advertising,corporate image enhancement, market planning,and direct selling.

Since G&A usually includes executive bonuses,incentive awards, stock options, and businessentertainment expenses, it represents the mostcontroversial area for questioning the reason-ableness of cost allocations to government con-tracts. In this regard, the government does notallow profit on G&A cost when computing itsprofit objective for negotiating flexibly pricedcontracts. Therefore, the defense contractorcould be expected to minimize indirect costclassified as G&A. The government position ofnot recognizing profit on G&A may not be ap-parent when examining a billing submitted bya contractor on a cost-type contract. The profitrate on the billing may be applied to the totalcost incurred, which includes G&A. However,government personnel do not consider G&Aas a profit-bearing cost when arriving at theprofit-rate objective prior to negotiations.

Since G&A costs relate to the operation of thebusiness as a whole, any cost directly distrib-uted to both government and commercial workof the contractor should be removed from G&Aand distributed to the appropriate cost objec-tive, such as a contract or appropriate overheadcost pool. Each contractor business segment hasits own G&A cost pool and, while there can bemany overhead pools, there is only one G&Apool for a business segment. Note in Exhibit 4that a contractor’s business-segment G&A ex-penses usually include major costs for segment-level G&A expenses, an appropriate allocationof corporate home-office expenses, independentresearch and development expenses, and bid andproposal expenses. However, note in “Exhibit5. Final Overhead Cost Pools,” the G&A costpool does not include IR&D/B&P expenses.IR&D/B&P is absent from this exhibit becausethese costs must be handled in a prescribed wayin accordance with government contract re-

quirements. Before the proper treatment ofIR&D/B&P expenses is addressed, it is impor-tant to know how overhead rates are computed.This topic will be revisited in Chapter 4 whenthe requirements for deriving the total cost ofIR&D/B&P projects and then transferring thesevery significant costs to the G&A cost pool isaddressed.

MAJOR CATEGORIES OFINDIRECT EXPENSES

Since each overhead pool normally includeshundreds of individual indirect expense ac-counts, contractors will summarize these ac-counts within each cost pool into major subdi-visions or categories for management controlpurposes. Exhibit 5 summarizes the many in-direct expense accounts into five primary clas-sifications of salaries and wages, fringe ben-efits, supplies and services, other expenses, andservice center allocations. There is no pre-scribed way of doing this, and all companiessummarize as they choose.

Many overhead costs are for personnel, andthese costs usually represent a significantamount of overhead costs. Personnel costs in-clude salaries and wages of indirect labor (thoseemployees needed to run the organization butwhose work bears no direct relationship to anyspecific contract) and fringe benefits for bothdirect and indirect employees. Fringe benefitsare costs associated with labor, such as healthand life insurance, leave, social security taxes,and pensions. It is not unusual in the defenseindustry for fringe benefits to approximate 50percent of labor costs. Supplies and services arethose indirect items, such as lubricating oil, per-ishable tools, nuts and bolts, and calibration,that are not assignable as direct costs to a con-tract; but they relate to all contracts. “Other ex-penses” is a catch-all category that includesmiscellaneous items such as travel, telephone,telegraph, and employee relocation.

3-6

MATERIAL PRODUCT PRODUCT OFFINDIRECT COSTS ENG FAB ASSY TOOLING HANDLING “A” “B” SITE G&A

Salaries & Wages:

Supervision $ 3,701 $ 19,674 $ 6,246 $ 729 $ 4,235 $ 177 $ 301 $ 260 $ 21,982

Indirect Labor 33,310 91,811 28,105 4,666 33,876 694 1,157 1,214 88,636

OTP 925 18,362 4,164 198 42,345 59 141 87 2,836

Training 5,552 1,202 520 255 2,879 231 347 130 2,978

Idle Time 19 219 104 24 85 1 2 3

Total Salaries & Wages $ 43,507 $ 131,267 $ 39,139 $ 5,872 $ 83,420 $ 1,162 $ 1,948 $ 1,692 $ 116,432

Fringe Benefits:

Health & Life Ins $ 29,609 $ 40,768 $ 17,175 $ 4,008 $ 6,288 $ 1,851 $ 3,701 $ 1,388 $ 1,595

Workmen’s Comp 1,851 31,041 12,491 1,093 5,336 116 231 173 4,432

Annual Leave 7,402 8,744 4,164 972 2,287 463 925 347 3,900

Holiday 9,253 10,930 5,205 1,214 1,906 578 1,157 434 2,482