Indian Financial System: a complete guide to indian financial system Bba ifs

Upload

muninarayanappa-munishamappaCategory

view

203download

0

1

Notes

On

PAPER 2.5 INDIAN FINANCIAL SYSTEM

Submitted to

DIRECTORATE OF DISTANCE & CORRESPONDENCE EDUCATION

BANGALORE UNIVERSITY

By

Dr. M. Muninarayanappa

Professor – Department Of Commerce

Bangalore University, Bangalore.

2

PAPER 2.5

INDIAN FINANCIAL SYSTEM

SYLLABUS

Objective: The objective of this subject is to familiariz e the students with

regard to structure, organization and working of financial system in India.

Unit 1: FINANCIAL SYSTEM

Introduction – Meaning – Classification of Financial System.Financial Markets – Functions

and Significance of Primary Market, Secondary Market, Capital Market, & Money Market.

Unit 2: FINANCIAL INSTITUTIONS

Types of Banking and Non-Banking Financial Institutions.Constitution, objectives &

functions of IDBI, sfcs, sidcs, LIC, EXIM Bank.Meaning and scope of Mutual Funds.

Unit 3: COMMERCIAL BANKS Introduction – Role of Commercial Banks – Functions of Commercial Banks – Primary

Functions and Secondary Functions – Investment Policy of Commercial Banks.

UNIT 4: CO-OPERATIVE BANKS

Meaning – definition – features - functions – types – merits and demerits - Lending policies –

priority areas of lending – role of co-operative banks for agricultural development.

UNIT 5: RURAL FINANCE

RRBS: Meaning – definition – features - functions – types – merits and demerits- Lending

policies – priority areas of lending – Role of RRBS in rural development. Micro finance:

micro finance products and services – role of Self Help Groups – post office –role of

companies in micro finance as a part of social responsibilities.

UNIT 6: CAPITAL MARKET

Stock market: Meaning – functions – primary – secondary – functionaries in stock market -

D-mat Accounts – listing requirements – role of stock exchange in capital mobilization

.

Unit 7: REGULATORY INSTITUTIONS

Introduction.RBI – Organization – Objectives – Role and Functions.The Securities and

Exchange Board of India – Organization and Objectives – IRDA and its functions.

Unit 8: FINANCIAL SERVICES

Introduction – Meaning – Features – Importance. Types of Financial Services – factoring,

leasing, venture capital, Consumer finance; housing & vehicle.

3

Content

1.1 Introduction to Financial System 1.2 Meaning 1.3 Financial Institutions

1.4 Capital Markets 1.5 Primary Market

1.6 Secondary Market 1.7 Long Term Loan Market 1.8 Money Market

1.9 Stock Exchange 2.1 Monetary Establishments

2.2 Banking Institutions 2.3 The Organised Non-Banking Financial Institutions 2.4 Mutual Funds

3.1 Introduction 3.2 Functions Of Commercial Banking

3.3 Types Of Deposits 3.4 Lending Of Funds 3.5 Discounting Of Bills Of Exchange

3.6 Investment Of Funds On Securities 3.7 Creation Of Credit Or Creation Of Money

3.8 Secondary Functions Of Commercial Banks 3.9 Miscellaneous Or General Utility Services 3.10 Investment Norms:

4.1 Introduction 4.2Meaning 4.3 Definition

4.4 Types & Perform Of Co-Operative Banks, India 4.5 Primary Co-Operative Credit Society

4.6 Central Co-Operative Banks 4.7 State Co-Operative Bank 4.8 Land Development Banks

4.9 Urban Co-Operative Banks 4.10 Functions Of Co-Operative Banks

4.11 Problems Of Co-Operative Banks 4.12 Advantages Of Cooperative Banks 4.13 Disadvantages Of Cooperative Banks:

4.14 Role Of Co-Operative Banks For Agricultural Development. 5.1 Regional Rural Banks:

5.2 Objectives Of RRB’s 5.3 Areas Of Operations Of RRB 5.4Micro Finance: Meaning

5.5Micro Finance Products 5.6Role of Self help group

5.7Micro Finance-the role of Post Offices 5.8Role of Companies in Micro Finance 6.0 Meaning

6.1 Choices Of Capital Market 6.2 Importance Of Capital Market

6.3 Classification Of Capital Market 6.4 Primary Market

4

6.5 Functions Or Services Of Primary Market Or New Issue Market 6.6 Secondary Market

6.7 Functioning Of Secondary Market 6.8 Primary And Secondary Markets – Similarities

6.9 Characteristics/ Functions Of Capital Market 6.10 Demat Account 6.11 Procedure

7.1 Meaning And Significance: 7.2 Need / Importance:

7.3 Types 7.4 Organization Of Rbi: 7.5 Objectives:

7.6 Functions: 7.7 Main Functions:

7.7 Supervisory Functions: 7.8 Promotional Functions: 7.9 Methods Of Credit Control

7.10 Quantitative Methods: 7.11 Securities And Exchange Board Of India (SEBI)

8.1 Introduction

8.2 Meaning

8.3 Choices Of Economic Services

8.4 Importance Of Economic Services

8.5 Styles Of Economic Services

8.6 Factoring:

8.7Partitioning Mechanism

8.8 Steps In Partitioning

8.9 Services Rendered By The Difficulty

8.10 Features Of Leasing

8.11 Venture Capital:

8.12 Features Of Venture Capital

5

Unit 1

FINANCIAL SYSTEM

Structure

1.10 Introduction

1.11 Meaning

1.12 Financial Institutions

1.13 Capital Markets

1.14 Primary Market

1.15 Secondary Market

1.16 Long Term Loan Market

1.17 Money Market

1.18 Stock Exchange

Introduction – Meaning – Classification of Financial System. Financial Markets – Functions

and Significance of Primary Market, Secondary Market, Capital Market, & Money Market.

OBJECTIVES: You understand the financial systems how it works in the Indian market. The

importance of primary, secondary market and shorter money market are explained. The roles

of stock exchanges in the primary and secondary market can also be understood. The role of

intermediaries and the importance of financial instruments in the financial market are also

explained in brief.

1.1 INTRODUCTION

6

Organization of the financial system

Financial Intermediaries Financial Markets Financial

Assets/Instruments

Banks NBFCMutual

Funds

Insurance

Organization

Leasing Companies

Hire-Purchase/Consumer Finance

Companies

Housing Finance Companies

Venture Capital Funds

Merchant Banking Organization

Credit Rating Agencies

Factoring and Forfeiting Org.,

Stock broking firms

Depositories

Money

MarketCapital/Securities Market

Primary Market Secondary

Market

Primary/Direct Indirect Derivatives

Equity

Preference

Debentures

Innovative debt

instruments

Forward

Futures

OptionsConvertible Debentures

Non- Convertible

Debentures

Secured Premium Notes

Warrants

Mutual Fund-units

Security Receipts

Pass Through

Certificates

Source: Prof. Augustin Amaladas & Prof. Amala Shanthi - slide share, St. Joseph’s College

of Commerce, Bangalore.

The financial system links between the savers and users to promote faster economic development.

A lender (saver) believes that he/she could enjoy the future money than present money. A

borrower (user) believes that he gets maximum enjoyment of the present than future money. A

well organised financial system is a backbone of the Economic development of any country. Its

Financial inputs from financial system for the production of goods and servic es which in turn

promote the well being and standard of living of the people of a country. Financial markets and

financial institutions are supportive mechanism of a financial system which requires money and

money assets. Mobilisation of savings and investing in productive ventures are the responsibility

of a financial system.

7

Post-1991 Phase Organization of the Indian financial System

Privatization of

financial

institution

Banks

Mutual-Fund

Insurance

Companies

Reorganization of Structure

DFIs/PFIs Banks NBFCs Mutual-funds Capital

Market

Money-

Market

PrimaryStock-

exchange

Investor Protection:

SEBI

Prudential Norms:

Credit/advance

portfolio

Investment

Portfolio

Capital adequacy

Exposure

Norms:

Securitisation,

Asset

Reconstruction

And Enforcement

Of Security

Interest

Asset-Liability

Management Credit Risk

Management

Country Risk

Management

Source: Prof. AugustinAmaladas& Prof. AmalaShanthi - Slide Share, St. Joseph’s College of

Commerce, Bangalore.

1.2 MEANING

The term national economy may be a set of inter-related activities or services

operating along to realize some pre-determined purpose or goal. It includes totally different

markets the establishments, instruments, services and mechanisms that influence the

generation of savings, investments, capital formation and growth.

1.2.1 DEFINITION

Van Horne has outlined the national economy as “the purpose of economic markets to assign

savings expeditiously in an economy to final users either for investment in real assets or for

consumption”.

2. Consistent with Robinson, the first operate of the system is “to give a link between savings

and investment for the creation of latest wealth and allow portfolio adjustment within the

composition of the prevailing wealth”.

8

1.2.2 ROLE OF FUNCTIONS OF ECONOMIC SYSTEM

A national economy performs the subsequent functions:

1. It is a link between savers and investors. It helps in utilizing the mobilized savings of the

scattered savers in additional economical and effective manner. It channelizes flow of savings

in to productive investment.

2. It provides a payment mechanism for the exchange of products and services.

3. It provides a mechanism for the transfer of resources across geographic boundaries.

4. It provides a mechanism for managing and dominant the chance concerned in mobilizing

savings and allocating credit.

5. It promotes the method of capital formation by transferrable along the availability of

savings and also the demand for investible funds.

6. It helps in lowering the value of transactions and increase returns. Reduced value

motivates folks (groups) to save lots of additional.

7. It provides elaborated info to the operators/players within the market like people, business

homes, government etc.

1.2.3 CLASSIFICATION OF ECONOMIC SYSTEM

The following are the four major classification of Indian monetary System:

1. Monetary establishments

2. Monetary Markets

.

3. Monetary Instruments/ assets/ securities

1. Financial Services

9

1.3 FINANCIAL INSTITUTIONS

Financial establishments are the intermediaries who facilitate sleek functioning of the

national economy by creating investors and borrowers meet. They mobilize savings of the

excess units and apportion them in productive activities promising a stronger rate of returns.

Financial establishments are termed as money intermediaries as a result of they act as

middleman between the savers and borrowers.

Financial market

1.3.1 MEANING

A market could be a place or mechanism that

facilitates the transfer of resources from one

entity to a different. A money market is an

establishment or arrangement that facilitates the

exchange of monetary instruments like shares,

debentures, loans etc. In different words, a

market wherever in money instruments like

money claims, assets and securities are unit listed is understood as “a money market”.

Money market transactions might occur either at a selected place or location.

Eg: banks, stock exchanges or through different mechanisms like telephone, telex or fax or

different electronic media.

1.3.2 DEFINITION In line with Brigham Eugene. F. “The place wherever individuals and organizations needing

to borrow money are unit brought alongside those having surplus funds is named a money

10

market”. One in every of the necessary requisites for the accelerated development of

associate economy is that the existence of a dynamic money market. A money market is of

nice use for a rustic because it helps the economy in many ways that.

1.3.3 ROLE OR IMPORTANCE OF MONEY MARKET

The role or importance of money market is as follows:

1. Transfer of resources:

Money market facilitates the transfer of resources from one person to another.

2. Growth in income:

Money market permits the lender to earn interest and dividend on their surplus investible

funds, so conducive to extend in their financial gain.

3. Productive usage:

Money market yield the productive use of funds employed in finance system, so enhancing

the financial gain and therefore the gross national production.

4. Capital formation:

Money market provides a channel through that the new savings flow to help capital

formation.

5. Worth discovery or worth determination:

Money markets yield the determination of the worth of listed money assets through the

interaction of various set of participants.

6. Sale mechanism:

Money market provides a mechanism for commerce of monetary assets by associate capitalist

and provides the advantages of marketability and liquidity of such assets.

7. Data availability:

The data generated in money market is helpful to numerous parties participating in economic

system. Thus, a money market could be a primary constituent of monetary system. The

money market not solely helps within the transfer of savings from new trade or production,

however conjointly provides opportunities for money investment to earn financial gain.

In different words, money markets perform each money and non-financial functions. The

money market permits finance of not solely physical capital formation i.e. Tangible mounted

assets and inventories, however conjointly consumption expenditure.

That is why money markets manage the flow of funds not solely between individual savers

11

and investors however conjointly between institutional savers and investors.

1.3.4 CLASSIFICATION OF MONETARY MARKETS

The Classification of monetary markets in India is as follows:

1. Unorganized markets:

In these markets there are unit variety of money lenders, bankers, and traders etc. United

Nations agency lends money to the general public. Bankers conjointly collect deposits from

the general public. There are non-public finance firms, invoice funds etc, whose activities

aren't controlled.

2. Organized markets:

In the organized markets, there are unit standardized rules and rules governing their money

dealings. There's conjointly a high degree of institutionalization and instrumentalisation.

These markets are unit subject to strict oversight and management by the run batted in or

different restrictive bodies.

These organized markets may be additional classified into 2 viz.

I. Capital market.

II. Securities Market.

1.4 CAPITAL MARKET

The capital market could be a marketplace

for monetary assets that have a protracted

or indefinite maturity. Typically it deals

with long run securities that have a

maturity amount of higher than one year.

It includes establishments and mechanism

for the effective pooling of long term funds from people and institutional investors and

creating them accessible industrial undertakings. Capital market in brief, deals in shares,

debentures, bonds and securities.

1.4.1 OPTIONS OF CAPITAL MARKET

1. It deals in long and medium term funds.

2. It consists of primary market and secondary market and special monetary establishments.

3. It covers each individual and institutional investor.

4. It makes funds accessible to industrial and industrial undertakings.

12

1.4.2 IMPORTANCE OF CAPITAL MARKET

Absence of capital market acts as a deterrent issue to capital formation and economic process.

Resources would stay idle if finances don't seem to be funneled through capital market.

The importance of capital market may be in brief summarized as follows:

1. The capital market is a vital supply for the productive use of economy’s savings. It

mobilizes the savings of the folks for more investment, and therefore avoids their wastage in

unproductive uses.

2. It provides incentives to saving and facilitates capital formation by giving appropriate rates

of interest because the value of capital.

3. It provides anas avenue for investors, significantly the social unit sector to speculate in

monetary assets that are a lot of productive than physical assets.

4. It facilitates increase in production and productivity within the economy and therefore

enhances the economic welfare of the society.

5. The operations of various establishments within the capital market induce economic

process. They furnish qualitative directions to the flow of funds and convey concerning

rational allocation of scarce resources.

6. A healthy capital market consisting of knowledgeable intermediaries promotes stability in

values of securities representing capital funds.

7. Moreover, it is a vital supply for technological upgradation within the industrial sector by

utilizing the funds endowed by the general public.

Thus, a capital market is a vital link between |people who} save and people who draw a bead

on to speculate these savings.

1.4.3 CLASSIFICATION OF CAPITAL MARKET

Capital market may be classified into three, viz,

i. Industrial exchange.

ii. Government exchange.

iii. Long run loan market.

iv. Industrial securities market:

It implies, It is a marketplace for industrial securities, viz,

i. Equity shares or stock

ii. Preferred shares.

iii. Debentures or bonds.

13

It is a market wherever industrial considerations raise their capital or debt by

supplying applicable instruments. It may be more divided into two:-

• Primary market or new issue market

• Secondary market or exchange.

1.5 PRIMARY MARKET

Primary market may be a marketplace for

new issue or new monetary claims. Thus It is

additionally known as New Issue Market.

The first market deals with those securities

that are unit issued to the general public for

the primary time. Within the primary market,

borrowers exchange new monetary securities

for future funds. Thus, the first market facilitates capital formation.

There are three ways by that an organization might raise capital in a very primary market.

They are:

Public issue.

Rights issue.

Private placement.

The foremost common methodology of raising capital by new corporations is through sale of

securities to the general public. It is known as public issue. Once associate existing company

needs to boost extra capital, securities are unit initial offered to the present shareholders on

preventive basis. It is known as offer. Non-public placement may be a manner of

commercialism securities in private to little cluster of investors.

1.5.1 FUNCTIONS OR SERVICES OF PRIMARY MARKET OR NEW ISSUE

MARKET

1. The transfer: A vital perform rendered by primary market is to permit the transfer of

resources from capitalist to entrepreneurs who establish new corporations. It is additionally

known as the perform of origination. The transfer perform is expedited by specialist agencies

that assist in numerous activities related to such transfer.

2. Investigatory services: The investment bankers and different agencies concerned in

primary market offer the investigatory services. These embrace, economic analysis, technical

14

analysis, monetary associate analysis of the businesses wherever a capitalistants to take a

position. This data helps the investors in creating a transparent selection on the kind, quality

and amount of investment to form.

3. Consultative and data services: Numerous consultative services are unit out there in

primary market with a read to up the standard of capital problems in primary market. The

relevant services embrace crucial the kind, the mix, the price, the timing, the size, the

commercialism ways and therefore the terms and conditions of issue of securities etc.

4. The guarantee: If the corporate, getting into capital market isn't positive of raising full

quantity of funds from the market, there are unit bound mechanism there by success of such

issue are secured. It is known as underwriting. Underwriting aims at guaranteeing the

subscription of public issue. Underwriters guarantee roaring subscription of the problem by

endeavor to require up the securities within the event of the general public failing to

subscribe a similar. It advantages all those concerned in pr imary market just like the

provision company, the investment public and capital market generally. The perform of

underwriting is undertaken for a commission.

5. The distribution: The perform that facilitates the sale of securities from company to

investors is termed ‘Distribution’. The perform of distribution is rendered by the specialised

agencies like brokers and dealers in securities. They maintain a relentless and an in depth link

with the issuers on the one hand and therefore the final investors on the opposite.

1.6 SECONDARY MARKET

Secondary market may be a marketplace for secondary sale of securities. In different words,

securities that have already competent the new issue market are unit listed during this market.

Generally, such securities are unit quoted within the exchange and it provides a nonstop and

regular marketplace for shopping for and commercialism of securities. This market consists

of all stock exchanges recognized by the government of India. The stock exchanges in India

are regulated under the Securities Contracts (Regulation) Act 1956. The Bombay exchange is

that the principal exchange in India that sets the tone of the opposite stock markets.

The secondary market provides liquidity to monetary instruments that are unit already issued

in primary market. In a very exchange, purchases and sales of securities whether or not of

state or semi-government bodies or different public bodies and additionally shares and

15

debentures issued by non-public joint stock corporations are unit done.

Functioning of secondary market:

For the effective functioning of secondary market, correct management should be exercised.

At present, management is exercised through the subsequent 3 necessary processes.

1. Recognition of stock exchanges:

As an area of secondary market operation the stock exchanges got to be recognized by

regulatory agency. The securities that are unit issued in primary market are listed solely in

recognized exchanges like Bombay stock exchange, NSE, Bombay exchange etc. In indiasebi

is recognizing the stock exchanges.

2.Listing of securities available exchanges:

Once the stock exchanges are recognized the securities that are needed to be listed like shares

debentures etc. Should be listed available exchanges

3.Recognition of broker:

The intermediaries, WHO facilities swish functioning of secondary market like brokers, deal

in secondary market. Sub-brokers got to be recognized by SEBI, them solely the desire be

able to interchange stock exchanges.

1.6.1 FUNCTIONS OR SERVICES OF SECONDARY MARKET

The Secondary market or exchange occupies a important position within the national

economy. In perform many economic functions and render valuable services to the investors,

corporations and to the economy as whole. They are as follows:

1. Liquidity of Securities:

Stock exchanges offer liquidity to securities, since securities is regenerate in to money at any

time in step with the discretion of the capitalist by commercialism tem at the listed costs.

2. Marketability to Securities:

Secondary market facilitate shopping for and commercialism of securities at listed costs by

providing continuous marketability to the investors in respect of securities they hold or will

hold. Therefore they produce a prepared marketplace for securities.

3. Safety of Funds happiness to investors:

Stock exchanges facilitate in maintaining safety of funds endowed as a result of they need to

perform below strict rules and rules and therefore the bye-laws are meant to make sure safety

of investible funds. These rules are framed by SEBI. This is able to strengthen the investor’s

confidence and promote larger investment.

16

4. Availableness of future funds to companies:

The securities listed within the stock, market are negotiable and transferable. Because it is

transferred from one capitalist to a different, one capitalist is substituted by another; however

the corporate is secured of future availableness of funds.

5. Flow of funds to profitable projects:

The profit and recognition of corporations are mirrored available costs. The costs quoted

indicate the relative profit and performance of corporations. Funds tend to be attracted

towards securities of profitable corporations and this facilitates of profitable corporations and

these facilities the flow of capital in to profitable channels.

6. Motivation for improved performance by companies:

The performance of an organization is mirrored on worths the costs quoted within the

exchange price of economic assets depends upon the company’s performance. These costs

are additional visible within the eyes of the general public. Exchange provides space for this

worth quotation for those securities listed by it. This airing makes an organization tuned in to

its standing within the market and it acts as a motivation to enhance its performance

additional.

7. Promotion of investment opportunities:

Stock exchanges mobilize the savings of the general public and promote investment through

capital problems. Unless there's a good secondary market, investment opportunities won't be

with investors.

8. Availableness of Business Information:

The dynamical business conditions within the economy are immediate mirrored on the

secondary market/stock exchanges. Booms and depressions is known through the dealings

within the stock exchanges. Relying upon the prevailing data policies is taken by the

government. Therefore an exchange reflects the prevailing economic state of affairs to ball

involved. In order that appropriate actions is taken.

9. Promoting of latest problems by companies:

If the new problems are listed available exchanges They are without delay acceptable to the

general public, since, listing is finished when analysis of such securities by involved

exchange authorities. Prices of underwriting such problems would be less public response to

such new problems would be comparatively terribly high. Therefore a exchange helps within

the promoting of latest problems additionally.

17

10. Different services:

Exchange allows the investors to scale back their risks by heterogeneous portfolio of

investment. It additionally develops savings habits among the community and paves the

manner for capital formation. It helps the investors in selecting securities by supply the daily

quotation of listed securities and by revealing the trends of dealings on the exchange. It

allows corporations and therefore the government to boost funds by providing a prepared

marketplace for their securities.

1.6.2 Primary and Secondary Markets – Similarities:

Both the first and secondary markets are closely reticular. This is often clear from the

following:

1. Trading:

If securities are to be listed within the stock exchange/ secondary market, It is necessary that

They are initial issued within the primary market.

2.Listing:

Solely those shares that are capable of listing in some purported stock exchanges are totally

signed in primary market.

3.Regulation:

The rules with reference to each primary yet as secondary market are regulated by the SEBI

and exchange. The thing is to motivate orderliness in each primary and secondary market.

4. Marketability:

The advantage of marketability provided by the secondary market greatly helps the

subscribers within the primary market. As an example, the positive trends prevailing within

the secondary market vastly facilitate the investors to scale back their holdings and acquire

new shares within the secondary market.

5. Conditional Prevailing:

The conditions prevailing within the secondary market have an effect on success or failure of

the problem created within the primary market. Consequently, wherever the conditions are

therefore favorable within the secondary market that prime market costs prevail, the

problems created within the primary market can end up to be encouraging and roaring.

Problems would fetch smart premiums.

6. Survival:

The survival of the secondary market depends upon the potency of the first market. There

may well be no stock exchanges if there's no primary market, within the same manner there'll

be no primary market within the absence of associate economical functioning of exchange.

18

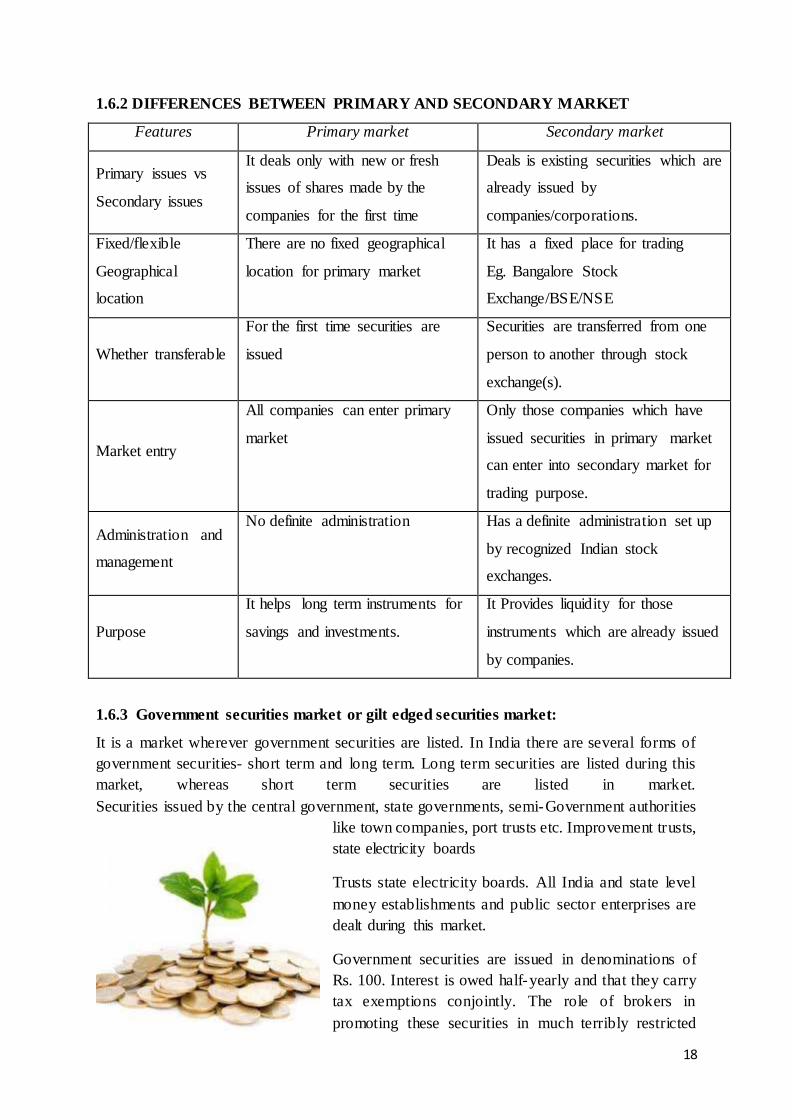

1.6.2 DIFFERENCES BETWEEN PRIMARY AND SECONDARY MARKET

Features Primary market Secondary market

Primary issues vs

Secondary issues

It deals only with new or fresh

issues of shares made by the

companies for the first time

Deals is existing securities which are

already issued by

companies/corporations.

Fixed/flexible

Geographical

location

There are no fixed geographical

location for primary market

It has a fixed place for trading

Eg. Bangalore Stock

Exchange/BSE/NSE

Whether transferable

For the first time securities are

issued

Securities are transferred from one

person to another through stock

exchange(s).

Market entry

All companies can enter primary

market

Only those companies which have

issued securities in primary market

can enter into secondary market for

trading purpose.

Administration and

management

No definite administration Has a definite administration set up

by recognized Indian stock

exchanges.

Purpose

It helps long term instruments for

savings and investments.

It Provides liquidity for those

instruments which are already issued

by companies.

1.6.3 Government securities market or gilt edged securities market:

It is a market wherever government securities are listed. In India there are several forms of

government securities- short term and long term. Long term securities are listed during this

market, whereas short term securities are listed in market.

Securities issued by the central government, state governments, semi-Government authorities

like town companies, port trusts etc. Improvement trusts,

state electricity boards

Trusts state electricity boards. All India and state level

money establishments and public sector enterprises are

dealt during this market.

Government securities are issued in denominations of

Rs. 100. Interest is owed half-yearly and that they carry

tax exemptions conjointly. The role of brokers in

promoting these securities in much terribly restricted

19

and also the major participant during this market is that the “Commercial Banks” as a result

of they hold to satisfy their SLR necessities.The secondary marketplace for these securities is

incredibly slender since most of the institutional investors tend to retain these securities till

maturity.

The government securities are in several forms viz,

A. Stock certificates.

B. Speech act notes.

C. Bearer bonds which might be discounted.

1.7 LONG TERM LOANS MARKET

Development banks and industrial banks play a major role during this market by activity long

term to company customers. Long run loans market might any be classified into:

a. Term loans market:

In India, several industrial funding establishments are

created by the government each at the national and

regional levels to provide long run and medium term

loans to company customers directly likewise as

indirectly. These development banks dominate the

commercial finance in Republic of India.

Establishments like IDBI, IFCI, ICICI, and different

state money firms return below this class.

B. Mortgages:

The mortgages market refers to those centers that provide real estate loan chiefly to

individual customers. A real estate loan may be a loan against the protection of immoveable

property like property. The transfer of interest in an exceedingly specific immoveable

property to secure a loan is named mortgages.

C. Money Guarantee Market:

A Guarantee market may be a centre wherever finance is provided against the guarantee of a

purported person within the money circle. Guarantee may be a contract to discharge the

liability of a third party just in case of his default. Guarantee acts as a security from the

20

creditors’ purpose of read. Just in case the borrowers fail to repay the loan, the liability fails

on the shoulders of the warranter. Hence, the warranter should be acknowledged each to the

recipient and also the below and he should have suggests that to discharge his liability.

1.8 MONEY MARKET

Money market contains a marketplace for short term loan or money assets. It is a marketplace

for the disposition and borrowing of short terms funds. Because

the name implies, it doesn't truly deal in money or money.

However it truly deals with close to substitutes for money or

close to money like trade bills, speech act notes and government

papers drawn for a brief amount not exceptional one year. These

short term instruments are often reborn into money promptly

with none loss and at low dealings value.

The money market doesn't seek advice from a specific place

wherever short term funds are affect. It includes all individual,

establishments and intermediaries handling short term funds.

The transactions between borrowers, lenders and middlemen

happen through telephone, telegraph, mail and agents.

No personal contact or presence of the two parties is important for negotiations in a very

market. However, a geographical name is also given to a market in step with its location. For

instance, the London markets operators from Lombard Street and also the big apple money

market operators from Wall Street. But, they attract funds from everywhere the world.

Similarly, the Mumbai market is that the center for short-run loan ready funds of not solely

Mumbai, however conjointly the complete of India.

1.8.1 Definition

Geoffrey Crow her in his book “A define of money” has explicit “Money market could be a

collective name given to numerous the varied the assorted forms and establishments that deal

within the various grades of close to money”.

The assets that are used as credit instruments are referred to as “Near money assets”.

1.8.2 Features of a money market:

The subsequent are the overall options of a market are:

1. It is a market strictly for brief term funds or money assets referred to as close to money.

2. It deals with money assets having a maturity amount up to 1 year solely.

21

3. It deals with solely those assets which might be reborn into money promptly while not loss

and with minimum dealings value.

4. Typically transactions happen through i.e., language, relevant documents and written

communications are often changed later. There is no formal place like stock market as within

the case of a capital market.

5. Transactions have to be compelled to be conducted while not the assistance of brokers.

6. It is not one homogenized market. It contains of many sub-markets, every specializing in a

very specific style of finance. Eg: decision market, acceptance market, bill market and

shortly.

7. The elements of a market are the financial organization, industrial banks, non-banking

money corporations, discount homes and acceptance homes. Industrial banks typically play a

dominant role during this market.

1.8.3 Significance/importance/functions of money market

A developed business plays a crucial role within the financial set-up of a rustic by provision

short term funds adequately and quickly to trade and industry. The money market is associate

integral a part of a country’s economy. Therefore, a developed market is very indispensable

for the speedy development of the economy. A developed market helps within the swish

functioning of the financial set-up in any economy within the following ways:

1. Economic development:

The money market provides short term funds to each public and personal establishments.

These establishments would like money to finance their capital wants [ In alternative words,

the money market assures offer of funds, the finance is completed through discounting of the

trade bills, industrial banks, acceptance homes, discount houses]. During this means, the

money market facilitates within the economic development by providing money help to trade,

commerce and business.

2.Profitable investment:

The industrial banks affect the deposits of their customers(The banks are needed to place

their assets into money type to fulfill the directions of the financial organization on the one

hand, whereas on the opposite, they need to place their excess reserves into productive

channels to earn financial gain on them). The aim of the industrial banks is to maximise

profits. The surplus reserves of the banks are endowed in close to money assets. The aim is to

make sure liquidity while not fore going profits utterly.

22

3. Borrowings by the government:

The money market helps the government in borrowing short term funds at terribly low

interest rates. The borrowing is completed on the idea of treasury bills.

4. Importance for central bank:

If the money market is well developed, the financial organization implements the financial

policy with success. It is solely through the money market that the financial organization will

manage the industry and therefore contribute to the event of trade and commerce.

5. Mobilization of funds:

The money market helps in transferring funds type one sector to another. The event of any

economy depends on accessibility of finance. No country will develop its trade, commerce

and business till and unless the money resources are mobilized.

6. Independency of economic banks:

Just in case of the prevalence of a developed market, the industrial banks need not borrow

from the financial organization. Just in case the industrial banks have insufficiency of

resources, they will meet their necessities by recalling a number of their loans from rather

than borrowing from the financial organization at the next rate of interest.

7. Savings and investments:

Another purpose of importance of the money market is that it helps in promoting liquidity

and safety of economic assets. By doing therefore, it will facilitate in encouraging savings

and investment.

1.8.4 Objectives Of Money Market

The subsequent are the necessary objectives of a market are:

1. To supply a parking place to use short-run surplus funds, primarily of economic banks.

2. To supply space for overcoming short-run deficits.

3. To alter the financial organization to influence and regulate liquidity within the economy

through its intervention during this market.

4. To supply an affordable access to users of short-run funds to fulfill their necessities

quickly, adequately and at affordable prices.

1.8.5 Characteristics/Features of a developed money market

So as to meet the on top of objectives, the money market ought to be totally developed and

economical.(In each country of the globe some style of market exists. A number of them are

extremely developed, whereas others don't seem to be well developed. Prof. S.N. subunit has

23

represented bound essential options of a developed market. They are as follows:

1. Extremely organized banking system:

The industrial banks are the nerve centre of the complete market. They are the most suppliers

of short-run funds. Their policies concerning loans and advances have impact on the whole

market. The industrial banks function an important link between the financial organization

and also the varied segments of the money market. Consequently a well-developed market

and a extremely organized industry co-exist.

2. Presence of a central bank:

The financial organization acts because the banker’s bank. It keeps their money reserves and

provides them money accommodation in times of difficulties by discounting their eligible

securities. Through its open market operations, the financial organization absorbs surplus

money throughout off-seasons and provides extra liquidity within the busy seasons. Thus, the

financial organization is that the leader, guide and controller of the money markets.

3. Accessibility of correct credit instruments :

A developed market needs a nonstop accessibility of promptly acceptable negotiable

securities like bill of exchange, treasury bills etc…. Within the market. There ought to be

variety of dealers within the market to interact in these securities. Accessibility of negotiable

securities and also the presence of dealers and brokers in giant numbers to interact in these

securities are required for the existence of a developed market.

4. Existence of sub-markets:

The quantity of sub-markets determines the event of a market. The larger the quantity of sub-

markets, the broader and additional development is the structure of money market. The

many sub-markets along create a coherent (united) market.

5. Ample resources:

There should be accessibility of spare funds to finance transactions within the sub-markets.

These funds could return from among the country and conjointly from foreign countries. The

London, New York and Paris money markets attract funds from everywhere the globe.

6. Existence of secondary market:

There ought to be a vigorous secondary market in these instruments.

7. Demand and provide of funds:

There ought to be an oversized demand and provide of short-run funds and it ought to have

adequate quantity of liquidity within the variety of large amounts maturing among a brief

amount.

24

8. Alternative factors:

Besides the on top of, alternative factors conjointly contribute to the event of a market.

Speedy industrial development resulting in the emergence of stock exchanges giant volume

of international trade resulting in the system of bills of exchange, political stability,

favourable conditions for foreign investment, worth stabilization etc… are the opposite

factors that facilitate the event of money market within the country.

London market could be a extremely developed market as a result of it satisfies all the

necessities of a developed market. If anyone or additional of those factors are absent, then the

money market is named associate beneath developed one.

1.8.6 Composition of Money Market

The money market could also be sub-divided into four, viz..,

1. Decision money market:

The decision securities industry could be a marketplace for very short amount loans say in

some unspecified time in the future to 14 days. So, It is extremely liquid. The loans are due

on demand at the opinion of either the loaner or the recipient. In India, decision money

markets are related to the presence of stock exchanges and thence, they are situated in major

industrial cities like Mumbai, Calcutta, Chennai, Delhi, Ahmadabad etc… the special options

of this market is that the rate of interest varies from day to day and even from hour to hour

and Centre to Centre. It is terribly sensitive to changes in demand and provide of decision

loans.

2. Industrial bills market:

It is a marketplace for bills of exchange (arising out of real trade transactions). Within the

case of credit sale, the vendor could draw a bill of exchange on the customer. The customer

accepts such a bill promising to pay at a later date per the bill. The sellers needn't to attend till

the maturity date of the bill. Instead, he will get money by discounting the bill.

In India, the bill market is beneath developed. The run has taken several steps to develop a

sound bill market. The run has enlarged the list of participants within the bill market. The

discount and finance house of India was setup in 1988 to push secondary market in bills. In

spite of these, the expansion of the bill market is slow in India. There are not any specialised

agencies for discounting bills. The industrial banks play a major role during this market.

3. Treasury bills market:

It is a marketplace for treasury bills that have ‘short term’ maturity. A Treasury bill could be

a certificate of indebtedness or a finance bill issued by the government. It is extremely liquid

25

as a result of its reimbursement is secure by the government.. It is a crucial instrument for

short borrowing of the government.. There are 2 sorts of treasury bills viz.,

a) Ordinary or regular and

b) Adhoc treasury bills popularly called ‘adhocs’.

Normal treasury bills are issued to the general public, banks and different monetary

establishments with a read to raising resources for the central government to fulfill its short

monetary desires.

Adhoc treasury bills are issued in favour of the run solely. They are not sold through tender

or auction. They will be purchased by the run solely. Adhocs do not seem to be marketable in

India, however holders of those bills will sell them back to run.

Treasury bills have a maturity amount of ninety one days or 182 days or 364 days solely.

Monetary intermediaries will park their temporary surpluses in these instruments and earn

financial gain.

4. Short loan market:

It is a market wherever short are given to company customers for meeting their capital needs.

Industrial banks play a major role during this market. Industrial banks give short loans within

the variety of money credit and order of payment.

Order of payment facility is especially given to business folks wherever as money credit is

given to industrialists. Order of payment is only a short lived accommodation and It is given

within the accounting itself. However money street credit is for a amount of 1 year and It is

sanctioned during a separate account.

1. 9 STOCK EXCHANGES:

Stock exchanges could be a market during which securities are bought &sold and It is a vital

marketplace for developing a capital market.

The Securities Contracts (Regulation) Act 1956 defines stock market as “an association

organization or body of people whether or not incorporated or not, established for the aim of

26

helping, control and dominant business in shopping for mercantilism and dealing in

securities”.

1. 9.1 FUNCTIONS OF STOCK EXCHANGES

A stock market discharges many functions. It provides a market place to sell and get freely

the stocks & shares through the licensed brokers. The important functions of stock exchanges

are as follows:

1. Market place for stock:

Stock exchanges provides a market place for mercantilism and shopping for of securities

freely by the brokers for his or her purchasers.

2. Prepared and continuous market:

Stock exchanges offer prepared and continuous marketplace for stocks & shares. This

provides prepared liquidity, price, continuity and negotiability to the capital bolted up in

securities.

3. Assessment of securities:

The stock exchanges ensures correct appraisal of security. The free play of demand for &

offer of securities determines value ceaselessly.

4.Stock exchanges forecast the future:

Besides, providing continuous market, stock exchanges, render statement operate. The worth

movements for securities replicate and forecast the longer term happenings in business

operations.

5. Mobilization of savings:

The stock markets are excellent markets that facilitate to mobilize the savings of the

individuals to productive channels.

6. Capital formation:

Besides causation public to avoid wasting & invest in securities, the exchange promotes

capital formation and provides necessary funds to the necessitous industries.

7. Economic barometer:

27

Like measuring instrument that indicates the variation in temperature of the surroundings at

any purpose of your time, the stock market indicates the health of the economy. Value trends

on a stock market replicate the economic progress & socio-political conditions of a rustic. It

indicates the boom or depression existing within the country.

8. Management of company enterprises:

To induce the stocks & shares listed on stock exchanges, the businesses got to follow sure

rules and laws. “Listing” means that obtaining the name of the corporate registered with the

stock market to trot out its securities formally on the exchange. When listing the safety, the

corporate has got to follow the official policies of the exchange whereas managing its

securities. Thus, exchange exercise healthy management over the businesses.

9. Speculation:

The operators on the stock market are licensed agents. They are referred to as by totally

different names. These operators hold company securities new and previous for a brief

amount significantly the new shares, owing to temporary holding by monetary intermediaries

referred to as “speculators”. Speculators can have a seasoning amount. The speculators who

would like to form profit out of variation in costs of securities, operate skillfully and offer

sensible liquidity position to the securities. Speculation, though affects the share costs badly

at sure time, it plays an important role in moving the capital markets. These facilities are for

speedy economic development & honest dealing on shopping for & mercantilism of

securities.

10. Management of public deposits:

The government of India & all state governments are engaged in planned economic

development. Owing to this planned growth, government need Brobdingnagian capital &

they need to float loan, bonds & alternative securities to induce a locality of finance for these

securities to induce a locality of finance for these comes. These securities also are trot out

within the stock exchanges. The governments’ monetary desires within the variety of debt are

glad by stock exchanges by providing marketplace for these securities.

28

11. Alternative functions:

Stock market offer facilities like giving business info of the company sector. Each listed

company of the company sector. Each listed company has got to submit annually the audited

monetary statements to the exchange. Numerous styles of reports also are submitted to the

exchange. This can be complied by the exchange and acts as a information of company

sector. This ensures most promotional material of company operations and dealing.

1. 9.2 NATIONAL STOCK EXCHANGE(NSE):

Stock exchanges may be a market throughout that

securities are bought & sold-out & it is a important

marketplace for developing a capital market.

The Securities Contracts (Regulation) Act 1956

defines stock exchange as “an association organization

or body of individuals whether or not or not

incorporated or not, established for the aim of serving

to, management and dominant business in buying & mercantilism & dealing in securities”.

1. 9.3 FUNCTIONS OF STOCK EXCHANGES

A stock exchange discharges several functions. It provides a market place to sell and find

freely the stocks & shares through the commissioned brokers. The vital functions of stock

exchanges are as follows:

1. Market place for stock:

Stock exchanges provide a market place for mercantilism and buying of securities freely by

the brokers for his or her purchasers.

2. Ready and continuous market:

Stock exchanges supply ready and continuous marketplace for stocks & shares. This provides

ready liquidity, price, continuity and negotiability to the capital fastened up in securities.

3. Assessment of securities:

The stock exchanges ensures correct appraisal of security. The free play of demand for &

supply of securities determines price endlessly.

29

4. Stock exchanges forecast the future:

Besides, providing continuous market, stock exchanges, render statement operate. The price

movements for securities replicate and forecast the long term happenings in business

operations.

5. Mobilization of savings:

The stock markets are glorious markets that facilitate to mobilize the savings of the people to

productive channels.

6. Capital formation:

Besides deed public to avoid wasting & invest in securities, the exchange promotes capital

formation and provides necessary funds to the indigent industries.

7. Economic barometer:

Like measuring device that indicates the variation in temperature of the environment at any

purpose of it slow, the stock exchange indicates the health of the economy. Price trends on a

stock exchange replicate the economic progress & socio-political conditions of a country. It

indicates the boom or depression existing at intervals the country.

8. Management of company enterprises:

To induce the stocks & shares listed on stock exchanges, the companies need to follow

certain rules & laws. “listing” implies that getting the name of the company registered with

the stock exchange to upset its securities formally on the exchange. Once listing the security,

the company has to follow the official policies of the exchange whereas managing its

securities. Thus, exchange exercise healthy management over the companies.

9. Speculation:

The operators on the stock exchange are commissioned agents. They are said as by whole

totally different names. These operators hold company securities new and former for a short

quantity considerably the new shares, because of temporary holding by financial

intermediaries said as “speculators”. Speculators will have a seasoning quantity. The

speculators who would love to create profit out of variation in prices of securities, operate

skillfully & supply wise liquidity position to the securities.

Speculation affects the share prices badly at certain time. It plays a very important role in

moving the capital markets. This facilities increase the speed of economic development,

honest dealing on buying and mercantilism of securities.

10. Management of public deposits:

The Government of India and all state governments measures are engaged in planned

economic development. Because of this planned growth, government would like broadening

30

of capital & they have to float loan, bonds & various securities to induce a region of finance

for these securities. These securities are also upset at intervals the stock exchanges. The

government’s financial needs at intervals the range of debt is met by stock exchanges by

providing marketplace for these securities.

11. Various functions:

Stock markets supply facilities like giving business data of the corporate sector Every listed

company has to submit annually the audited financial statements to the exchange. Varied

types of reports are also submitted to the exchange. This may be complied by the exchange

and acts as a info of company sector. This ensures most publicity of company operations and

dealing.

Summary

The financial system consists of financial institutions, intermediaries and financial

instruments. There are various financial markets such as primary, secondary, capital, money

and money markets. Primary market plays an important role in the initial issue whereas

secondary market plays in the resale of stock s and shares of the holders. The secondary

market plays a vital role in identifying the development and growth of the company and

economy. Short term market is known as money market. Stock exchanges are regulated by

SEBI.

KEYWORD/GLOSSARY

National economy as “the purpose of economic markets to assign savings expeditiously in

an economy to final users either for investment in real assets or for consumption”.

Financial institutions: Financial establishments are the intermediaries who facilitate sleek

functioning of the national economy by creating investors and borrowers meet.

Money market facilitates the transfer of resources from one person to another.

Unorganized markets: In these markets there are unit variety of money lenders, bankers,

and traders etc.

Organized markets: In the organized markets, there are unit standardized rules and rules

governing their money dealings.

The capital market could be a marketplace for monetary assets that have a protracted or

indefinite maturity.

Primary market may be a marketplace for new issue or new monetary claims.

Secondary market may be a marketplace for secondary sale of securities.

31

Government securities market or gilt edged securities market: It is a market wherever

government securities are listed.

Long term loans market: Development banks and industrial banks play a major role during

this market by activity long term to company customers.

Stock Exchanges: It provides a market place to sell and get freely the stocks & shares

through the licensed brokers.

Speculation: The operators on the stock market are licensed agents.

National stock exchange(nse): The aim of serving to, management and dominant business in

buying & mercantilism & dealing in securities. Securities are bought & sold-out & it is a

important marketplace for developing a capital market.

1) What do you mean by financial system?

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………

2) What is primary market?

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………

3) What is the classification of financial system?

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………

4) What do mean by capital market?

………………………………………………………………………………………

………………………………………………………………………………………

ANSWER TO CHECK YOUR PROGRESS

(2 MARKS)

32

………………………………………………………………………………………

………………………………………

5) What is money market?

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………

1. Write a note on primary market.

2. Write a note on secondary market.

3. What are the functions of primary market?

4. Write a note on financial institutions.

5. What are the differences between primary and secondary market?

6. Distinguish between capital market and money market.

1. Meir Kohn: Financial Institutions and Markets, Tata mcgrah Hill

2. L M Bhole: Financial Institutions and Markets, Tata Mcgrah Hill

3. D.K. Murthy &Venugopal : Indian Financial System , I.K. Intl

4. M Y Khan: Indian Financial System, TMH

5. E Gardon & K Natarajan: Financial Markets & Services.

Web:

All pictures are taken from Google Images as on 14/10/2014

SUGGESTED BOOKS/ ARTICLES

QUESTIONS (5 MARKS)

33

Unit 2

FINANCIAL INSTITUTIONS

2.1 Monetary Establishments

2.2 Banking Institutions

2.3 The organised Non-Banking Financial Institutions

2.4 Mutual Funds

Types of Banking and Non-Banking Financial Institutions.Constitution, objectives &

functions of IDBI, SFCS, SIDCS, LIC, EXIM Bank.Meaning and scope of Mutual Funds.

Objectives of the study

Financial establishments are termed as monetary intermediaries as a result of they act as

middleman between the savers and borrowers. There are banking and non-banking financial

institutions. There are long term lending institutions such as IDBI, IFC, LIC and commercial

banks lends for short term as well as long term. We understand all of the above how they

function for the economic development of our country.

2.0 Introduction

The principle objective of SFC’s is to provide medium short term and long term financial

assistance to small industries particularly in a circumstance when normal banking assistance

is not available. SIDC are setup in various states under the companies Act of 1956 to later the

primary development needs of tiny, small, village industries in the state.

Insurance organization in India comprise of government organization namely, life

insurance corporation of India and general insurance corporation of India. LIC collects large

amount of funds from the public and deploys to the savings, the best advantage of the policy

holders for the industrial development as a whole. EXIM bank provides re- finance facilities

to the commercial banks and other financial institutions against their export and import

financial activities. A mutual fund collects the savings from little investors, invest them in

government and alternative company securities and earn financial gain through interest and

dividends, besides capital gains. It works on the principle of ‘small drops of water build an

enormous ocean’.

34

2.1 Monetary Establishments

A financial organization is essentially a term financial institution, providing medium and

future monetary help to industrial and business units, for promoting industrial and economic

development within the country.

Financial establishments are the intermediaries World Health Organization facilitates swish

functioning of the national economy by creating investors and borrowers meet. They

mobilize savings of the excess units and allot them in productive activities pro mising a more

robust rate of returns.

Financial establishments are termed as monetary intermediaries as a result of they act as

middleman between the savers and borrowers.

2.1.1 FORMS OF MONETARY INSTITUTIONS

Monetary establishments may be classified into 2 categories:

1. Banking institutions

35

2. Non-banking institutions.

2.2 Banking Institutions

Indian banking system is subject to the financial institution. I.e., banking company of

our country RBI because the apex bank establishment organizes runs, supervises, regulates

and develops the medium of exchange and therefore the national economy of the country.

The most legislation governing industrial banks in India is the Banking Regulation Act,

1949. The banking establishments is loosely classified into two categories:

A. Organized sector.

B. Unorganized sector.

36

2.2.1 ORGANIZED SECTOR

The organized sector consists of economic banks, co-operative banks & regional rural banks.

I. Industrial banks

Traditionally, industrial banks accepted deposits and met the short and medium term funding

wants of the business. But now, since 1990’s banks are funding the future wants of the

business notably the infrastructure sector. The alleviation measures initiated within the Indian

economy, light-emitting diode to the entry of enormous non-public sector banks in 1993. This

has exaggerated competition among non-public and public sector banks and quality of

services has improved.

II. Co-operative banks

Source: Google image as on 15/10/2014

An important section of the organized sector of Indian Banking is that the co-operative

banking. This section is delineate by a gaggle of societies registered underneath the acts

of the states about co-operative societies. Co-operative societies could credit or non-credit

societies.

Different kinds of co-operative credit societies are in operation within the Indian

economy. These establishments may be classified into two broad categories:

a. Rural credit societies that are primarily agricultural

b. Urban credit societies that are primarily non- agricultural.

37

III. Regional Rural Banks

RRBS were found out by the regime and therefore the sponsoring business banks with the

target of developing the agricultural economy. RRBS give credit facilities and banking

services to little farmers, little entrepreneurs within the rural areas. The regional rural

banks were found out with a read to produce credit facilities to weaker areas.

IV. Foreign banks:

Foreign banks are in India from British days. These banks have targeting company

purchasers and are specializing in areas about International banking.

2.2.2 Unorganized sector

People engaged in unorganized banking sector are the indigenous bankers, money

lenders, Seth, sahukars effecting the operate of banking.

Indigenous bankers are the forefathers of contemporary business banks. These are the

people or partnership corporations playing the banking functions. They are the native

bankers. The geographical region coated by the native bankers is far larger than the realm

coated by the business banks. Few characteristics of native are as follows:

• Indigenous bankers are often seen from the actual fact that they not solely provided

credit to trade & commerce, however now and then to the government of the day

additionally.

• Indigenous bankers raise funds from the general public additionally.

• They raise funds from the general public additionally.

38

• They give finance for productive functions directly and indirectly to trade and trade.

• They detain bit with traders and little industrialists and finance, selling on a sizeable scale. Disposition is conducted on the premise of dedication notes.

2.2.3 Money Lenders

Money lenders rely entirely on their own funds for the capital. Money lenders is also rural or

urban, skilled or non-professional. They embody giant farmers, traders, merchants,

goldsmiths, village shopkeepers, sardars of laborers etc. The most characteristics of money

lenders are the following:

• Their funds are own funds.

• Their purchasers are principally the weaker sections of the society.

• Their loans are extremely exploitive. They charge terribly high rate of interest.

• Their operations are entirely unregulated.

• The credit is prompt & versatile.

2.2.2 Non-banking Institutions

The non-banking establishments is also classified loosely into 2 groups:

A. Organized monetary establishments.

B. Unorganized monetary establishments.

A. Organized monetary Institutions:

39

Source: http://www.cfp.altius.ac.in/fpsb_india.html

2.3 The Organized Non-Banking Financial Institutions include

2.3.1 Development Finance Institutions:

• The establishments like IDBI, ICICI and IIBI in any respect India level.

• SFCS, SIDCS at the state level.

• Agricultural development finance establishments as NABARD, LDBS etc.

Development money establishments give medium and future finance to the company and

industrial sector and additionally take up promotional activities for economic development of

the country.

40

• IDBI- Industrial Development Bank of India.

• ICICI- Industrial Credit Investment Corporation of India.

• IIBI- Industrial Investment Bank of India.

• SFCS- State Finance Corporation

• SIDCS- State Industrial Development Corporation.

• LDBS- Land Development Banks.

• NABARD- National Bank for Agriculture & Rural Development.

• LDBS-Land Development Banks

2.3.2 Investment Institutions

It includes those money establishments that mobilize savings of the general public at

giant through varied schemes and invest these funds in company and government

securities. These embrace LIC, GIC, UTI and Mutual funds.

2.3.2.1 INDUSTRIAL DEVELOPMENT BANK OF INDIA (IDBI)

It is started by run in 1964. Later in 1975 it had been taken by Central government. (Indira

Gandhi emergency period) In 1995, seventy two of capital is maintained by government and

also the remaining is given to others i.e., 28%. LIC, GIC etc. For public.

It was established in July 1964 underneath IDBI Act as an entirely closely-held by run and it

had been separated by run in 1975.

A Government of India taken and disinvested its shares in 1995 to the extent of twenty eighth

& maintained to the extent of seventy two.

Role:

1. It is allotted the role of principle financial organisation for coordinative the activities of all

the financial organisation engaged in funding promoting and developing the industries.

41

2. It helps within the designing, promoting & developing the industries to fill the gaps within

the industrial development.

3. It provides technical & body help for the promotion, management & enlargement of

business.

4. It undertakes market & investment researches, surveys & techno-economic studies to contribute to the event of the business.

Constitution:

1. The share capital of IDBI was control by run until 1975.

2. The share capital was transferred to the government of India and it became government

closely-held establishment.

3. Nowadays government holds seventy two of the share capital LIC, UTI, SBI and EXIM

bank along hold Sep 11 foreign establishment investors third and also the balance is control

by the general public.

Financial Resources: The main sources of funds to the IDBI are some capital, reserves &

surplus, borrowing from run, market borrowing each in India & abroad by supply certificate

of deposits, mounted deposits & financial gain bonds. Ex: IDBI flexi bonds.

Functions: IDBI performs sort of functions all those are teams into three categories:

i) Direct functions

ii) Indirect functions

iii) Promotional activities.

I) Direct functions:

• They embrace, Term loans are provided to the industries for a amount starting from 10-

12 years together with capital.

• Underwriting the securities direct subscription to shares and debentures guarantees the

loan, risk capital.

• Equipment leasing/ lease financing: It provides lease for the acquisition of equipme nts

for amount of 5-8 years.

42

II) Indirect function:

• Refinancing of commercial loans to the IFCI, SFC, business banks, SIDC’s and co-

operative banks from 10-25 years.

• Resource support to the money establishments by subscribing shares and lo ans of

economic establishments.

• Discounting of bills.

III) Promotional Activities:

It refers to the efforts taken by the IDBI to market the expansion of industries within the

country by giving help to backward areas, little scale sectors and through different

development of entrepreneurs.

Direct help to backward areas within the type of concessional loans, longer

reimbursement amount, versatile debt equity quantitative relation.

IDBI conducting service of the backward space for assessing the commercial potential,

resource accessible, infrastructure facilities then on. Help to little scale sector industries

includes re-finance to state level establishments, finance to SFC’s, contribution to shares

and debentures, putting in of national equity fund and introducing of single window

theme for grant of loans.

Development of entrepreneurs has been one in all the foremost activities of IDBI by

providing seed capital help, re- finance against loans up to 21lakhs, 100% re-finance in

respect of composite loans, offer of knowledge, preparation of project profiles, technical

and management practice and coaching programs to the entrepreneurs.

Recent Trends of IDBI:

After 1991, IDBI enlarged their activities to hide merchandiser banking (advice & service

for rising capital, issue management informative services for mergers and acquisition and

loan syndication), debentures, trust territory, for-ex services, facility participant, started

subsidiaries, IDBI capital market securities restricted and IDBI investment management

company restricted was started for rising the debt, public issue and investment company

schemes.

43

2.3.2.2 STATE FINANCIAL CORPORATION (SFC)

State Financial Corporation are established under the state financial corporation Act of

1951 with the view to providing medium and long term finance to the medium and small

industries. There are 18 SFCs operating in different states of our country.

At the time of setting up of IFCI the necessity to for assisting smaller industrial establishment

has been recognized because it was not possible for a single institution to satisfy the capital

needs of small concerns spread all over the country.

Punjab government took the lead in organizing the financial corporation and setup state

financial corporation in 1953. Gradually, financial institutions started in different states.

Normally, the area of operation of an SFC is confined to one stage to extend financial helps

to small enterprises. However, the activities of some of the state financial corporations cover

the neighboring states / unions territories which do not have SFCs of their own.

To reach the small concerns financial needs SFCs are opened number of regional / branch

officers.

Objectives and Scope:

1. The principle objective of SFC’s is to provide medium short term and long term

financial assistance to small industries particularly in a circumstance when normal

banking assistance is not available.

2. SFCs collectively serve the broad national objectives of economic growth through the

promotion of small industries balanced regional growth and widening of industries

through the encouragement of new entrepreneurs.

3. To provide assistance to new as well as existing industries for the purpose of

establishment, modernization, renovation, expansion and diversification of public

44

limited companies, private companies, partnership and proprietor concerns engaged in

manufacturing, mining, hotel, road transport, generation and distribution of electricity

development of lands, fishing and to provide technical services.

4. To provide for discounting of bills of exchange and direct subscription to equity as

debentures of industries and to enhance the loan ceiling from 30, 00,000 to 90,

00,000.

Functions:

1. Granting loans and advances / subscribing to debentures of industrial concerns,

repayable within 20 years.

2. Guarantying the loans raised by the industrial concerns on such terms and conditions

as may be mutually agreed upon.

3. Guarantying of such deferred payment of any industrial concern.

4. Underwrite the issue of shares and debentures.

5. Provides foreign exchange loans.

6. Participating in equity capital of small scale industrial units coming up in back ward

areas.

7. Besides, the SFC A ct as an agent of the Central government, State government, IFCI

on any other institution providing financial assistance to the industries.

Operational policies of State Financial Corporation:

1. Policy on size of assistance is Rs.60, 00,000 in case of co-operative societies.

2. Policy on forms of assistance, through granting and guarantying.

3. Policy on duration of assistance to the maximum of 20 years.

4. Policy on nature of industrial products to be assisted to the small scale units.

5. Policy on security: They provide secured loans on fixed assets.

6. Their interest rate policy: The lending rates of the SFC’s are normally linked to the

bank rate.