Indian Banking: Can ADF Compliance Ensure Accurate Regulatory

7

Indian Banking: Can ADF Compliance Ensure Accurate Regulatory Reporting? While the RBI’s ADF project is a step in the right direction, it is not sufficient to meet the objective of automation of banks’ reports to prevent misreporting of important data. Executive Summary The Reserve Bank of India (RBI) launched the Automated Data Flow (ADF) project to ensure accurate regulatory reporting by banks in India. However, there are some challenges that could prevent the ADF project from achieving its objective. Some of these challenges are: unavail- ability of RBI guidelines for some reports, the qual- itative nature of a few reports, banks’ reluctance to go in for core banking system (CBS) enhance- ment rather than just ADF enhancements, some banks’ lack of effort to reengineer the existing process, too many assumptions involved in the automation process, etc. Both banks and the RBI need to come up with additional measures to support the ADF project to meet the objective of automation. Some of these measures could be: a stringent review and audit process, implementation of robust corporate governance within the banks, exhaustive docu- mentation of process workflows after automation, more investments in enhancements of core banking systems, clear guidelines from RBI for each regulatory report, flexibility from RBI in terms of the timeframe for automation based on the process and technology maturity profile of individual banks, etc. Implementation of ADF and the measures suggested above open up some opportunities for technology and consulting firms to help banks. These opportunities include helping banks set up the change management process, consulting around to-be processes using business process modeling (BPM) tools, selling related or comple- mentary software products and services, ADF implementation for new banks, etc. The ADF initiative is indeed a necessary but not sufficient step to achieve the objective of accurate regulatory reporting. The project needs to be complemented by additional measures. Background Banks in India submit a set of 222 regulatory reports at varied frequency to the Reserve Bank of India (RBI). 1 These reports can broadly be classified into 12 categories: • Basic statistical returns. • Department of Banking Supervision (DBS) returns analysis. • Statutory returns analysis. • Delinquency and collections. • Financial statements analysis. • Risk management. • Cognizant 20-20 Insights cognizant 20-20 insights | november 2013

Transcript of Indian Banking: Can ADF Compliance Ensure Accurate Regulatory

Indian Banking: Can ADF Compliance Ensure Accurate Regulatory Reporting?While the RBI’s ADF project is a step in the right direction, it is not sufficient to meet the objective of automation of banks’ reports to prevent misreporting of important data.

Executive SummaryThe Reserve Bank of India (RBI) launched the Automated Data Flow (ADF) project to ensure accurate regulatory reporting by banks in India.

However, there are some challenges that could prevent the ADF project from achieving its objective. Some of these challenges are: unavail-ability of RBI guidelines for some reports, the qual-itative nature of a few reports, banks’ reluctance to go in for core banking system (CBS) enhance-ment rather than just ADF enhancements, some banks’ lack of effort to reengineer the existing process, too many assumptions involved in the automation process, etc.

Both banks and the RBI need to come up with additional measures to support the ADF project to meet the objective of automation. Some of these measures could be: a stringent review and audit process, implementation of robust corporate governance within the banks, exhaustive docu-mentation of process workflows after automation, more investments in enhancements of core banking systems, clear guidelines from RBI for each regulatory report, flexibility from RBI in terms of the timeframe for automation based on the process and technology maturity profile of individual banks, etc.

Implementation of ADF and the measures suggested above open up some opportunities for technology and consulting firms to help banks. These opportunities include helping banks set up the change management process, consulting around to-be processes using business process modeling (BPM) tools, selling related or comple-mentary software products and services, ADF implementation for new banks, etc.

The ADF initiative is indeed a necessary but not sufficient step to achieve the objective of accurate regulatory reporting. The project needs to be complemented by additional measures.

BackgroundBanks in India submit a set of 222 regulatory reports at varied frequency to the Reserve Bank of India (RBI).1 These reports can broadly be classified into 12 categories:

• Basic statistical returns.

• Department of Banking Supervision (DBS) returns analysis.

• Statutory returns analysis.

• Delinquency and collections.

• Financial statements analysis.

• Risk management.

• Cognizant 20-20 Insights

cognizant 20-20 insights | november 2013

2

• Treasury.

• Reconciliation.

• Foreign exchange and international operations.

• Fraud.

• Advances.

• Deposits.

These reports are prepared manually by various operations teams in the banks, which increases the potential for inaccuracies in the data reported. In its approach paper on ADF dated November 2010, RBI had asked all the banks in India to automate the process of regulatory reporting.

As a part of the ADF project, RBI asked banks to build a central data repository (CDR) that would act as a data warehouse for information flowing in automatically from all the core systems of a bank. This automation exercise is to ensure that the information required for RBI reports flows seamlessly from all core systems to a central data warehouse and from this data warehouse into RBI reports, thereby eliminating manual intervention.

Almost three years into the ADF exercise, most banks are at an advanced stage of achieving ADF compliance. This is a good time for the banks and RBI to evaluate whether ADF compliance will by itself solve the data quality issues around regulatory reporting.

ADF ApproachIn its paper of November 2010, RBI suggested two approaches to the ADF project. The standard approach was for banks with little or no infrastruc-ture for automation of regulatory returns. Such banks would adopt an end-to-end roadmap for the automation of all four layers — data acquisition, data integration and storage, data conversion and data submission — required for report generation and submission. The variation approach was for banks with some automation already in place. They would need to implement only some custom-ization to the existing architecture.

The RBI envisaged implementation of ADF in two phases: Phase 1 requires banks to ensure the seamless flow of data from the core systems to their MIS server. Phase 2 requires banks to begin submitting data from this MIS server (CDR) to RBI software using straight-through processing (STP) to do away with manual intervention.

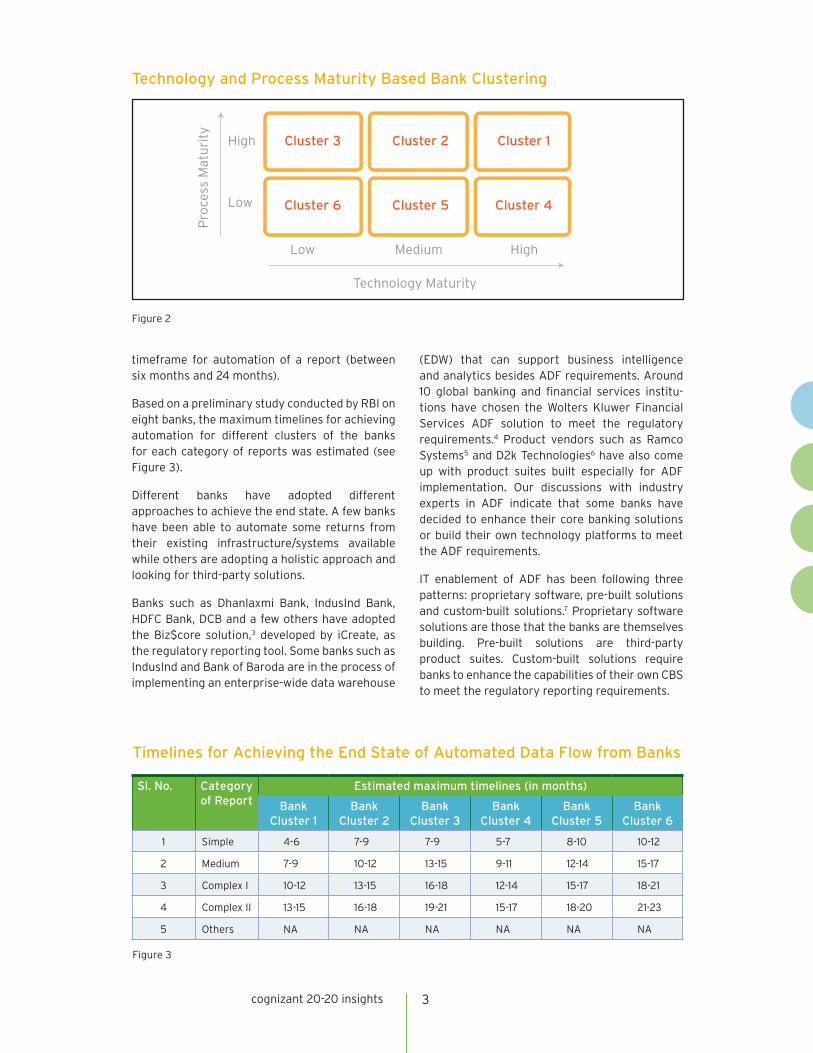

The RBI has advised banks to undertake a self-assessment of the maturity profiles of their technology and processes and place themselves in one of six clusters (see Figure 2, next page). RBI has suggested that banks classify by complexity their 222 regulatory reports into five categories, namely: simple, medium, complex — I, complex — II and “others.” Depending upon the cluster to which it belongs, the bank must decide the

cognizant 20-20 insights

Figure 1

Conceptual End-State Architecture for Banks to Automate Data Submission2

CBS 1

CBS 2

Treasury

Messages

Data Movement

Bank RBI

Messages

Data Acquisition Layer

Data Integration & Storage Layer

Data Conversion Layer

Data Validation Layer

RBI Data Storage Layer

Data Repositoryin RBI

Centralized Data Repository for RBI reporting

Required calculations &

validations done automatically using

this data

Data Submission Layer

Other Systems

DATA

VALIDATION

Dat

a V

alid

atio

n

Dat

a V

alid

atio

n

Dat

a C

onve

rter

Dat

a In

tegr

atio

n

3cognizant 20-20 insights

timeframe for automation of a report (between six months and 24 months).

Based on a preliminary study conducted by RBI on eight banks, the maximum timelines for achieving automation for different clusters of the banks for each category of reports was estimated (see Figure 3).

Different banks have adopted different approaches to achieve the end state. A few banks have been able to automate some returns from their existing infrastructure/systems available while others are adopting a holistic approach and looking for third-party solutions.

Banks such as Dhanlaxmi Bank, IndusInd Bank, HDFC Bank, DCB and a few others have adopted the Biz$core solution,3 developed by iCreate, as the regulatory reporting tool. Some banks such as IndusInd and Bank of Baroda are in the process of implementing an enterprise-wide data warehouse

(EDW) that can support business intelligence and analytics besides ADF requirements. Around 10 global banking and financial services institu-tions have chosen the Wolters Kluwer Financial Services ADF solution to meet the regulatory requirements.4 Product vendors such as Ramco Systems5 and D2k Technologies6 have also come up with product suites built especially for ADF implementation. Our discussions with industry experts in ADF indicate that some banks have decided to enhance their core banking solutions or build their own technology platforms to meet the ADF requirements.

IT enablement of ADF has been following three patterns: proprietary software, pre-built solutions and custom-built solutions.7 Proprietary software solutions are those that the banks are themselves building. Pre-built solutions are third-party product suites. Custom-built solutions require banks to enhance the capabilities of their own CBS to meet the regulatory reporting requirements.

Figure 2

Technology and Process Maturity Based Bank Clustering

High

Low

Low Medium High

Cluster 3 Cluster 2 Cluster 1

Cluster 6 Cluster 5 Cluster 4P

roce

ss M

atu

rity

Technology Maturity

Sl. No. Category of Report

Estimated maximum timelines (in months)

Bank Cluster 1

Bank Cluster 2

Bank Cluster 3

Bank Cluster 4

Bank Cluster 5

Bank Cluster 6

1 Simple 4-6 7-9 7-9 5-7 8-10 10-12

2 Medium 7-9 10-12 13-15 9-11 12-14 15-17

3 Complex I 10-12 13-15 16-18 12-14 15-17 18-21

4 Complex II 13-15 16-18 19-21 15-17 18-20 21-23

5 Others NA NA NA NA NA NA

Figure 3

Timelines for Achieving the End State of Automated Data Flow from Banks

cognizant 20-20 insights 4

Challenges in the Regulatory Reporting Process and ADF ProjectThere are several gaps in the existing regulatory reporting process that will not be addressed by the ADF project. Some of these gaps are as follows.

Unavailability of RBI Master Circulars/Guidelines

Out of the 222 mandated reports to be submitted to RBI, there are quite a few reports for which there are no direct or exhaustive RBI guidelines to use as a source of reference. Some examples are balance sheet analysis, quarterly operating results, risk-based supervision, asset quality and asset liability, off-balance-sheet exposures, etc. In the absence of regulatory guidelines, inter-pretation of the reporting formats is left to the discretion of the bank submitting the report. Some of these reports are complex in nature and present the financial health of the bank in areas of asset liability management, risk management and asset quality. This subjective reporting of critical information can lead to overall under-reporting or over-reporting of data that might impact the macroeconomic decisions taken by RBI.

Qualitative Nature of Reports

Although banks have pushed for automation of as many reports as possible, quite a few reports are left out of the scope of ADF because of the nature of information contained therein. Some examples would be reporting of fraud, reporting of demand and time deposits into various time buckets based on behavioral modeling of historical data, reporting of delinquencies, long form audit report, etc. Data for such reports will still have to be prepared manually outside the core systems and then uploaded as a flat file to the ADF product being used.

Banks’ Reluctance to Undertake CBS Enhancement

Several banks have opted for the regulatory reporting products of third-party vendors instead of building an in-house reporting solution. This approach will work only if the ADF products available in the market act solely as a data warehouse for reports generation, and the necessary enhancements pertaining to regulatory reporting are carried out in the CBS. One of the reasons the RBI took up the ADF project at this point in time is that most banks in India are at an advanced stage of CBS and can leverage its capability for reporting too. However, some banks

in their effort to reduce cost and be ADF-compliant at the earliest have gone for too many customiza-tions to the ADF product instead of enhancing the CBS. This approach does not comply completely with the regulatory reporting automation using CBS capabilities and functionalities.

Lack of Initiatives to Reengineer Existing Process

Ideally, banks should use the automation process as an opportunity to reengineer their existing reporting processes and identify any loopholes that lead to erroneous reporting. However, due to the complexity of the processes involved and the ADF-compliancy deadline, some banks have adopted automation without any change in the underlying as-is process. Hence, the accuracy of the post-automation data remains questionable.

Too Many Assumptions

The ADF has many inherent assumptions, including the following:

• Maintenance of clean data in source systems by front-office teams.

• Minimal operations inefficiencies while doing manual data entry in the source systems.

• Seamless integration of the multiple source systems and the CDR for data sharing.

• Successful execution of the extract transform load (ETL) procedures at pre-defined frequen-cies.

• Technology checks at various points to monitor jobs scheduling.

• Intermediate data quality checks at various stages of report preparation.

• Banks abiding by RBI guidelines in their day-to-day operations.

• Cross validation business rules across reports built in to the ADF system to ensure data integrity.

• Timely report generation and transmission to RBI in defined formats.8

The success of the ADF project is dependent upon each individual function working seamlessly. A glitch in any of the functions mentioned above can lead to issues that might result in incorrect data being reported to the regulator.

A recent example of this breach is the monetary fine imposed by RBI on 22 banks in India that included prominent banks such as Axis, HDFC,

cognizant 20-20 insights 5

ICICI, SBI, Bank of Baroda, Citibank, etc. These banks were found to have violated know your customer (KYC) and anti-money laundering (AML) guidelines. It was observed that the banks did not file cash transaction reports for some deals. Certain gold transactions done via cash beyond a prescribed limit were not reported. The source of non-resident ordinary (NRO) accounts was not ascertained in a few cases. KYC norms were not followed for walk-in customers for sale of third-party products, etc.9

Such incidents would have led to incorrect reporting to RBI as there are regulatory returns that require information on cash transac-tions, NRO accounts and liberalized remittance schemes. Clearly, the issue of incorrect reporting of information will not be resolved by automation.

Additional Measures to Be TakenConsidering the above challenges inherent in the regulatory reporting process and the ADF project, the RBI and reporting banks need to take some additional measures to ensure accurate informa-tion is submitted.

By Banks

Banks should set up robust internal corporate governance specifically for the regulatory reporting process. Internal audit processes should be tightened to prevent fraudulent reporting and to ensure regulatory guidelines are always followed.

Banks should not be completely dependent on third-party vendors to handle maintenance for ADF once the automation exercise is completed. Instead, they should form an internal ADF main-tenance team that will be competent and expe-rienced enough to handle the dynamic nature of the reporting requirements. There should be complete documentation of process workflows highlighting the roles and responsibilities of the operations teams after the automation of the regulatory reports.

There should be an increased effort to leverage the CBS’s capabilities for handling enhancements and customizations pertaining to regulatory reporting. The automation exercise should be used as an opportunity to examine the existing process of reporting. Any deficiencies and gaps should be rectified as a priority.

By Reserve Bank of India

RBI should issue clear and exhaustive guidelines on all the regulatory reports to prevent any subjective interpretation by the reporting banks. A defined communication channel and process should be established with the member banks to address any queries related to reporting.

RBI should be more flexible in terms of the timeframe for automation of regulatory filings based on the technology and process maturity profile of the member banks. The reporting process in the existing scenario is complex and most banks need time to smoothen this process.

RBI should tighten the screws on the auditing process in banks and should impose strict penalties for banks that fail to comply with it.

Opportunities for Technology and Consulting FirmsThough the ADF project began almost three years ago, there are a host of opportunities that technology and consulting firms can still tap in the near future. Some of these are as follows:

ADF Implementation for New Banks

RBI had issued guidelines for new banking licenses earlier this year, and around 26 companies had applied.10 These include India Post, L&T Finance Holdings, LIC Housing Finance, Shriram Capital, etc. Winners of the banking licenses are expected to be announced by the first quarter of 2014.11 Technology and consulting firms should initiate discussions with the likely winners for their ADF-related product and service offerings. Technology firms can pitch for the implementation of ADF product suites whereas consulting firms can offer services such as business analysis, requirements management and managing end-to-end ADF implementation.

Cross-Selling

Mid-size software companies view this as an opportunity to cross-sell related banking software products and services.12 Technology firms can also look to cross-sell product suites on business analytics, which can be used to understand consumer banking trends; on asset liability management, which can be used to handle liquidity management in banks; and on risk management, which can be used to meet the Basel III regulatory guidelines.

cognizant 20-20 insights 6

Change Management

Another area on which both technology and consulting firms should focus is change management. Every year, RBI comes out with revised master circulars/guidelines for the regulatory reports. Based on this, some cus-tomizations would be required in the ADF or some enhancements would be required for the CBS. Even RBI, in its approach paper on ADF, has emphasized the need for a defined change management process to manage and maintain the automated data flow architecture. Firms that have already established a relationship with banks for the ADF engagement can expect a stream of revenue from change management also.

Consulting Using BPM Tools

Most banks are currently at an advanced stage of automation. After the automation phase, the operations team will need a defined process workflow to follow for data validation of the generated report. Consulting firms can offer their

expertise in documenting to-be processes using BPM tools for each of the 222 regulatory reports.

ConclusionRegulatory reporting is a very useful tool for RBI to understand the financial health of the banking sector in India. Information presented via regulatory reporting serves as a key input for certain macroeconomics decisions taken by RBI. It is therefore imperative that correct and accurate information is reported by all the member banks.

The ADF project is a necessary step toward achieving the end state of accurate regulatory reporting. As highlighted in this paper, there are several challenges underlying the regulatory reporting process and the ADF project. Hence, ADF compliance alone is not sufficient and certain additional measures need to be taken by the regulator as well as participating banks to ensure that the objective of accurate regulatory reporting is achieved.

Footnotes1 http://rbidocs.rbi.org.in/rdocs/content/docs/86427.xls.

2 http://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/APSDS101110.pdf.

3 http://www.bizscorebi.com/customers.html.

4 http://www.wolterskluwer.com/Press/Latest-News/Pages/Press%20Releases/2012/pr13Dec2012a.aspx.

5 http://www.ramco.com/industries/bfsi/adf-solution.aspx.

6 http://www.d2kindia.com/left_menu_content.php?page_id=83.

7 http://www.ciol.com/ciol/news/28572/banks-automated-flow.

8 http://www.icreate.in/pdf/iCreate.%20Banking%20Frontiers.%20May%20Issue.pdf.

9 http://www.thehindubusinessline.com/industry-and-economy/banking/rbi-fines-22-banks-for-violating- antimoney-laundering-norms/article4917197.ece.

10 http://articles.economictimes.indiatimes.com/2013-07-03/news/40352228_1_new-bank-licence-user-development-central-bank.

11 http://www.firstpost.com/business/full-list-these-26-companies-have-applied-for-new-banking-licenc-es-920031.html.

12 http://www.business-standard.com/article/finance/rbi-s-automated-data-reporting-norms-to-create-rs-500-cr-mkt-for-it-firms-111101200064_1.html.

About CognizantCognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process out-sourcing services, dedicated to helping the world’s leading companies build stronger businesses. Headquartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technology innovation, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 50 delivery centers worldwide and approximately 164,300 employees as of June 30, 2013, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top performing and fastest growing companies in the world. Visit us online at www.cognizant.com or follow us on Twitter: Cognizant.

World Headquarters500 Frank W. Burr Blvd.Teaneck, NJ 07666 USAPhone: +1 201 801 0233Fax: +1 201 801 0243Toll Free: +1 888 937 3277Email: [email protected]

European Headquarters1 Kingdom StreetPaddington CentralLondon W2 6BDPhone: +44 (0) 20 7297 7600Fax: +44 (0) 20 7121 0102Email: [email protected]

India Operations Headquarters#5/535, Old Mahabalipuram RoadOkkiyam Pettai, ThoraipakkamChennai, 600 096 IndiaPhone: +91 (0) 44 4209 6000Fax: +91 (0) 44 4209 6060Email: [email protected]

© Copyright 2013, Cognizant. All rights reserved. No part of this document may be reproduced, stored in a retrieval system, transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the express written permission from Cognizant. The information contained herein is subject to change without notice. All other trademarks mentioned herein are the property of their respective owners.

About the AuthorsVikas Agarwal is a Consultant with Cognizant Business Consulting. He has more than four years of experience in the banking and financial services sector across investment management, core banking and regulatory reporting in India. Vikas has worked extensively in Automated Data Flow (ADF) implementation engagements for banks based in India and Europe. He can be reached at [email protected].

Ajit Varshney is a Manager within Cognizant Business Consulting, based in Chennai. He has over 16 years of industry experience of which 12 years are in business consulting and banking product transformation programs in Asia Pacific, Europe and North America. His expertise includes business process management, business requirement management, core banking product fitment, GAP analysis and solutioning. Ajit holds a bachelor’s degree from BITS Pilani and is a management graduate from NITIE, Mumbai. He can be reached at [email protected].