Income Computation and Disclosure Standard (ICDS) CA Sanjeev... · Income Computation and...

31

Income Computation and Disclosure Standard (ICDS) • ICDS II – Valuation of Inventories • ICDS III – Construction Contracts • ICDS IV – Revenue Recognition Sanjeev Pandit CA

Transcript of Income Computation and Disclosure Standard (ICDS) CA Sanjeev... · Income Computation and...

Income Computation and Disclosure Standard (ICDS)

• ICDS II – Valuation of Inventories

• ICDS III – Construction Contracts

• ICDS IV – Revenue Recognition

Sanjeev Pandit CA

• Based on AS – 2

• Scope:

Includes WIP of service provider (Not specifically mentioned in scope or definition of Inventories)

Excludes Machinery Spares used in connection with tangible fixed assets.

• Inventories valued at cost or NRV, whichever is lower.

Sanjeev Pandit CA

ICDS II – Valuation of Inventories

Measurement of Cost

• Cost of Inventories

– Costs of purchases,

– Costs of services,

– Costs of conversion and

– Other costs incurred in bringing the inventories to their present location and condition.

Sanjeev Pandit CA

ICDS II – Valuation of Inventories

• Costs of Purchases: Recoverable taxes and duties to form part of cost. (Section 145A)

• Costs of Services (New Insertion)

• Cost of Conversion: As per AS – 2

• Other Costs: As per AS – 2

ICDS II – Valuation of Inventories

Sanjeev Pandit CA

Cost of Services

• Includes:

– Labour and other costs of personnel directly engaged in providing

services

– Supervisory personnel

– Attributable overheads

• ICDS on Revenue Recognition

ICDS II – Valuation of Inventories

Sanjeev Pandit CA

Cost Formulae

• Permits FIFO and Weighted Average Cost Method

• “Fairest Possible Approximation” – Is concept of `Materiality’ built-in ?

• Standard Cost – Whether permitted ?

– AS – 2 Para 18

– Final Report of TAS Committee.

Sanjeev Pandit CA

ICDS II – Valuation of Inventories

ICDS II – Valuation of Inventories

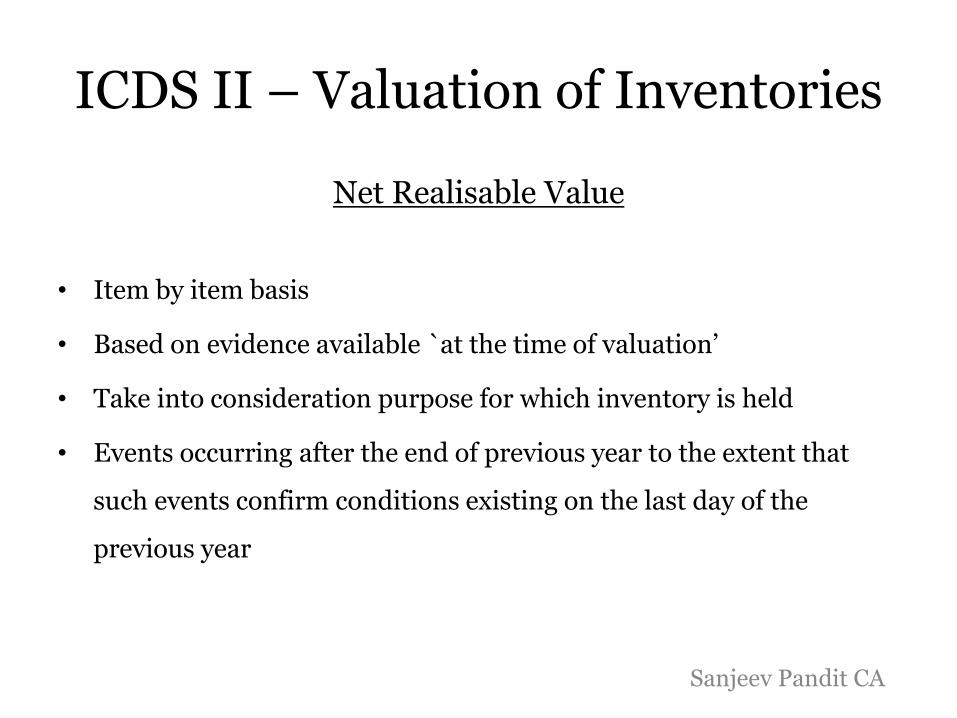

Net Realisable Value

• Item by item basis

• Based on evidence available `at the time of valuation’

• Take into consideration purpose for which inventory is held

• Events occurring after the end of previous year to the extent that

such events confirm conditions existing on the last day of the

previous year

Sanjeev Pandit CA

Value of Opening Inventory

• On Commencement of Business – Capital assets converted into stock-in-trade

Change in Method of Valuation

• “Reasonable Cause” for the purpose of change in method of valuation of inventories.

Sanjeev Pandit CA

ICDS II – Valuation of Inventories

Dissolution of Partnership, AOP & BOI

• Valuation to be done only at Net Realisable Value

– Impact.

Sanjeev Pandit CA

ICDS II – Valuation of Inventories

Transitional Provision

• Interest & Other Borrowing costs included in cost of inventory as on 1st day of April, 2015 will continue to remain included on 31st

March, 2016 if inventory items remains in stock.

Disclosures

• Correspond to AS – 2

ICDS II – Valuation of Inventories

Sanjeev Pandit CA

• Based on AS – 7

• Scope (As per AS – 7):

– To be applied in determination of Income for a construction contract of a contractor

– Applied separately for each construction contract

– Combining and Segmenting of contracts

ICDS III – Construction Contracts

Sanjeev Pandit CA

• Definitions:

– Construction contract

– Fixed price contract

– Cost plus contract

– Retentions

– Progress billings

– Advances

Correspond to definitions in AS – 7

Sanjeev Pandit CA

ICDS III – Construction Contracts

Contract Revenue

• Recognised when there is reasonable certainty of ultimate collection.

• Variations in contract work, claims and incentive payment forms part of contract revenue:

− To the extent it is probable they will result in revenue and can be reliably measured.

− Can contract revenue be revised – Upward or Downward ?

• Revenues once recognised, if not collectible – Recognised as an expense and not adjusted against revenue.

ICDS III – Construction Contracts

Sanjeev Pandit CA

Contract Revenue

• Retention Money

• Whether right to receive the retention money accrues only after the obligations under the contract are fulfilled ?

• Case Law:– CIT v. Simplex Concrete Piles (India) Pvt. Ltd (1989) 179 ITR 8 (Cal.)

– CIT v. Associated Cables (P) Ltd. (2006) 286 ITR 596 (Bom.)

– CIT v. Ignifuild Boilers (I) Ltd. (2006) 283 ITR 295 (Mad)

ICDS III – Construction Contracts

Sanjeev Pandit CA

Contract Costs

• Include:

– Costs related directly to the specific contract

– Costs attributable to contract activity in general that can be

allocated

– Costs specifically chargeable to customers

– Allocated borrowing costs in accordance with ICDS on

Borrowing Costs. (New Insertion)

ICDS III – Construction Contracts

Sanjeev Pandit CA

Contract Costs

• Costs incurred for securing contract

• Reduced by incidental income

• Interest, dividend, capital gain not to be reduced from costs

• Exclude:

− Costs that cannot be attributed or cannot be allocated

− Costs relating to future activity and advances to sub-contractors

Sanjeev Pandit CA

Recognition of Contract Revenues and Expenses

• Recognised with reference to Stage of Completion of contract

• Major deviation from AS – 7

– Condition of ability to estimate reliably the outcome of

contract absent (Except in early stages)

– Expected loss on construction contract cannot be recognised

• Accounting of actual loss, for example by storm

ICDS III – Construction Contracts

Sanjeev Pandit CA

Recognition of Contract Revenues and Expenses

Determination of Stage of Completion

• Proportion of cost incurred to estimated total cost

• Survey of work

• Completion of physical work

Progress payments and advances not determinative of stage of

completion

ICDS III – Construction Contracts

Sanjeev Pandit CA

ICDS III – Construction Contracts

Recognition of Contract Revenues and Expenses

Application of Stage of Completion

− On cumulative basis each year

− Taking current estimates of contract revenue and contract costs

− Changed estimates are used

Sanjeev Pandit CA

Recognition of Contract Revenue and Expenses

• Early Stage of a contract

– When outcome of the contract cannot be estimated reliably -Contract Revenue to be recognised only to the extent of costs incurred.

– Early stage of a contract shall not extend beyond 25% of the stage of the completion.

• Deviation from AS – 7

ICDS III – Construction Contracts

Sanjeev Pandit CA

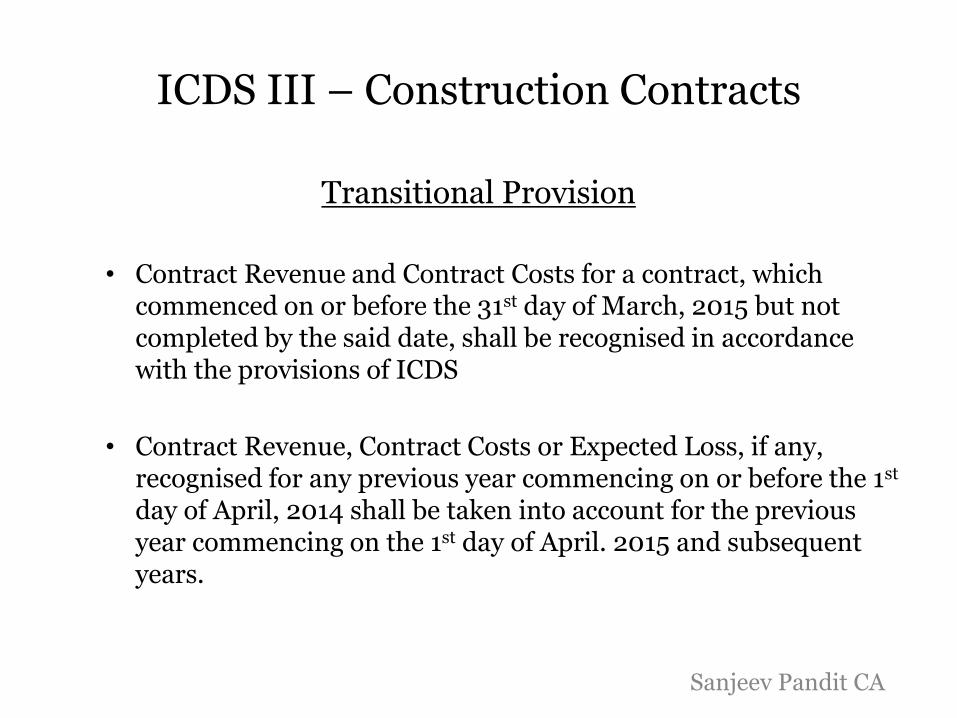

Transitional Provision

• Contract Revenue and Contract Costs for a contract, which commenced on or before the 31st day of March, 2015 but not completed by the said date, shall be recognised in accordance with the provisions of ICDS

• Contract Revenue, Contract Costs or Expected Loss, if any, recognised for any previous year commencing on or before the 1st

day of April, 2014 shall be taken into account for the previous year commencing on the 1st day of April. 2015 and subsequent years.

ICDS III – Construction Contracts

Sanjeev Pandit CA

Disclosures

• ICDS omits one disclosure requirement:-

– The methods used to determine the contract revenue recognised in the period

ICDS III – Construction Contracts

Sanjeev Pandit CA

Scope

Deals with the bases for recognition of revenue arising in the course

of the ordinary activities of a person from:-

– The sale of goods

– The rendering of services

– The use by others of the person’s resource yielding interest,

royalties or dividends

Same as per AS – 9

ICDS IV – Revenue Recognition

Sanjeev Pandit CA

• Does not deal with the aspects of revenue recognition which is dealt with by other ICDS’s

– Construction contracts

– Government grants

Sanjeev Pandit CA

ICDS IV – Revenue Recognition

Revenue Definition

• Omits:

– Revenue is measured by the charges made to customers or

clients for goods supplied and services rendered to them and by

the charges and rewards arising from the use of resources by

them.

Sanjeev Pandit CA

ICDS IV – Revenue Recognition

Recognition

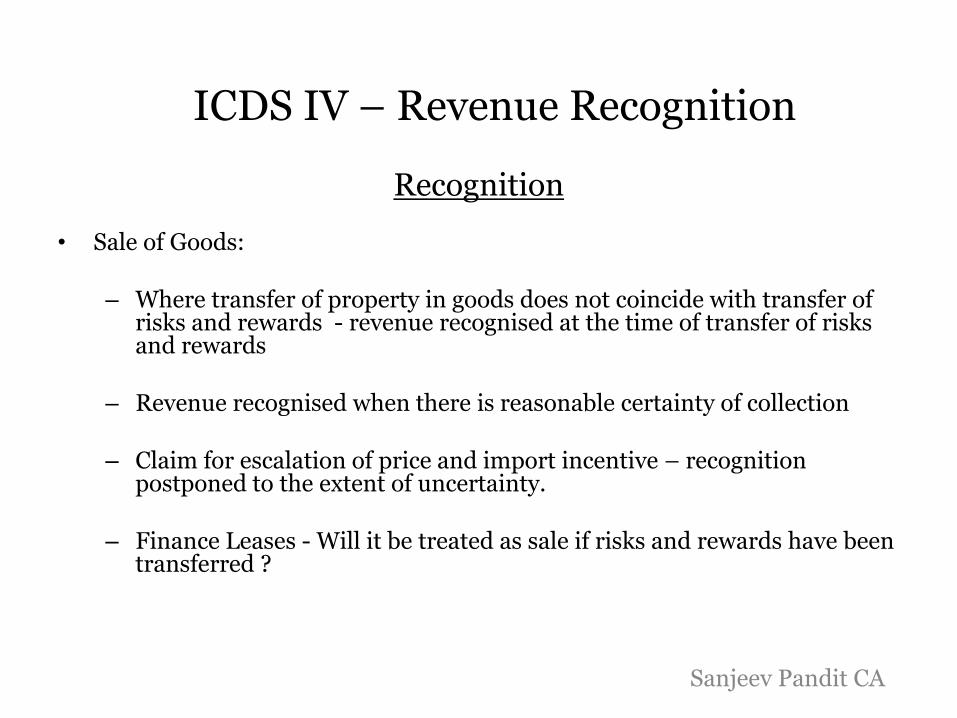

• Sale of Goods:

– Where transfer of property in goods does not coincide with transfer of risks and rewards - revenue recognised at the time of transfer of risks and rewards

– Revenue recognised when there is reasonable certainty of collection

– Claim for escalation of price and import incentive – recognition postponed to the extent of uncertainty.

– Finance Leases - Will it be treated as sale if risks and rewards have been transferred ?

Sanjeev Pandit CA

ICDS IV – Revenue Recognition

• Rendering of Services:

– Recognition of revenue cannot be postponed in case of significant uncertainties ?

– Permits only Percentage of Completion Method.

– Recognition on straight line method over a period of time not mentioned.

– Provisions of ICDS on construction contracts made applicable.

– Completed Service Contract method not permitted.

ICDS IV – Revenue Recognition

Sanjeev Pandit CA

• The use of Resources by Others yielding Interest, Royalties or Dividends

– Interest to be recognised on time basis.

– Interest on Bonds, Debentures, Savings Accounts etc. may create problem.

– Dividends are recognised in accordance with the provisions of the Act.

• Revenue from Rental not covered.

ICDS IV – Revenue Recognition

Sanjeev Pandit CA

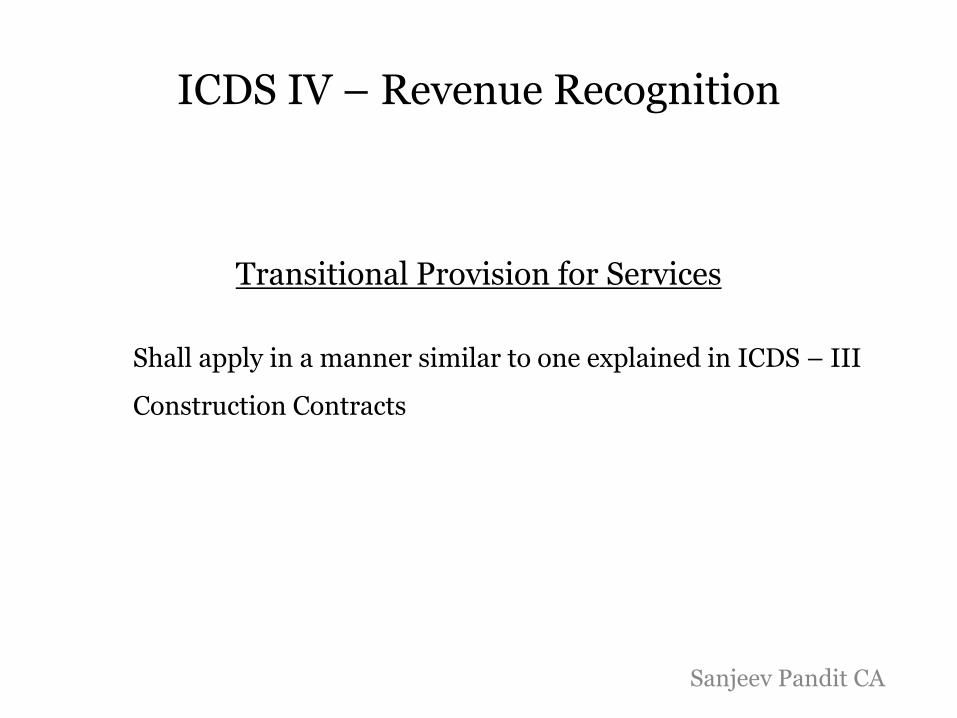

Transitional Provision for Services

Shall apply in a manner similar to one explained in ICDS – III

Construction Contracts

Sanjeev Pandit CA

ICDS IV – Revenue Recognition

Disclosures (Substantially New)

• Sale of Goods

– Total amount not recognised as revenue due to lack of reasonable certainty of its ultimate collection along with nature of uncertainty

• Rendering of Services

– Amount of Revenue from service transactions recognised as revenue.

– Method used to determine the stage of completion

– In case of service transactions in progress:• Costs incurred and recognised profits (less recognised losses)• The amount of advances received• The amount of retentions

Sanjeev Pandit CA

ICDS IV – Revenue Recognition

Thank You

-- Sanjeev Pandit CA

![DRAFT INCOME COMPUTATION AND DISCLOSURE ... Releases...2015/01/08 · Income Computation and Disclosure Standard [ICDS] Accounting Policies Preamble This Income Computation and Disclosure](https://static.fdocuments.net/doc/165x107/6083f1186324d247d57da594/draft-income-computation-and-disclosure-releases-20150108-income-computation.jpg)

![DRAFT INCOME COMPUTATION AND DISCLOSURE …2).pdfIncome Computation and Disclosure Standard [ICDS] Accounting Policies Preamble This Income Computation and Disclosure Standard is applicable](https://static.fdocuments.net/doc/165x107/5f93ba5c79d5986f47034079/draft-income-computation-and-disclosure-2pdf-income-computation-and-disclosure.jpg)