In Re: Odyssey Healthcare, Inc. Securities Litigation 04...

54

UNITED STATES DISTRICT COUR T NORTHERN DISTRICT OF TEXA S DALLAS DIVISION In re ODYSSEY HEALTHCARE, INC . SECURITIES LITIGATION § Civil Action No . 3 :04-CV-0844-N § CLASS ACTION § DEMAND FOR JURY TRIAL This Document Relates To : ALL ACTIONS . AMENDED CONSOLIDATED COMPLA IN T FOR VIOLATION OF §§10(b) AND 20(a) OF THE SECURITIES EXCHANGE ACT OF 1934

Transcript of In Re: Odyssey Healthcare, Inc. Securities Litigation 04...

UNITED STATES DISTRICT COURT

NORTHERN DISTRICT OF TEXA S

DALLAS DIVISION

In re ODYSSEY HEALTHCARE, INC .SECURITIES LITIGATION

§ Civil Action No . 3 :04-CV-0844-N

§ CLASS ACTION

§ DEMAND FOR JURY TRIAL

This Document Relates To :

ALL ACTIONS.

AMENDED CONSOLIDATED COMPLAINT FOR VIOLATION OF §§10(b) AND 20(a)OF THE SECURITIES EXCHANGE ACT OF 1934

INTRODUCTION

1 . This is a class action brought on behalf of all persons who purchased Odysse y

HealthCare, Inc. ("Odyssey" or the "Company") common stock between May 5, 2003 an d

October 8, 2004, inclusive (the "Class Period") . This case is about defendants engaging in Medicar e

fraud to create the appearance of profitability and rapid growth at Odyssey while at the same tim e

selling off their own stock at record high prices . Odyssey and the defendants publicly issued fals e

and misleading statements to the investment community about Odyssey's earnings, compliance wit h

applicable Medicare laws, rules and regulations and prospects for future growth. The information

provided by defendants to investors was knowingly false and misleading when issued and had th e

purpose and effect of artificially inflating the market price of Odyssey common stock during th e

Class Period .

2 . Odyssey provides hospice care services to terminally-ill patients and their families .

During 2001 and 2002, Odyssey grew rapidly acquiring existing and opening new hospice car e

centers in several states, which resulted in Odyssey reporting increased revenues, net income an d

earnings per share ("EPS") . As a result, Odyssey stock was a strong performer .

3 . However, by early 2003, Odyssey's business had begun to slowdown as competitio n

in the hospice care sector increased . To overcome this situation, defendants began committin g

Medicare fraud to falsely inflate Odyssey's earnings. Defendants embarked upon a scheme tha t

involved the adoption of a number of unlawful and improper patient admissions, patient retentio n

and billing practices . For example, to artificially inflate the Company's revenues , Odyssey billed

Medicare for services that were never rendered to hospice patients and their families, thereb y

artificially inflating Odyssey's revenues and drastically decreasing its expenses . Odyssey also

routinely admitted patients who were not eligible for hospice care because theyhad a life expectancy

of more than six months . Similarly, when doctors refused to recertify admitted patients as eligibl e

-1-

for hospice care, Odyssey refused to timely discharge them, thereby allowing the Company to bil l

for and receive payment for services rendered to patients who were not eligible for hospice care .

Moreover, since Odyssey recognized revenue on hospice care services in the first month received ,

the Company was able to retain the improper payments for at least 30-90 days, thereby artificially

inflating the Company's revenues and financial results in violation of GAAP .

4. To mask the Medicare fraud and paint a legitimate face on the Company's illega l

earnings, defendants accelerated Odyssey's expansion program and stepped up its patient referra l

and retention efforts. Notwithstanding the fact that this expansion was riddled with operationa l

challenges, defendants falsely represented that Odyssey was pursuing a well-planned strategy o f

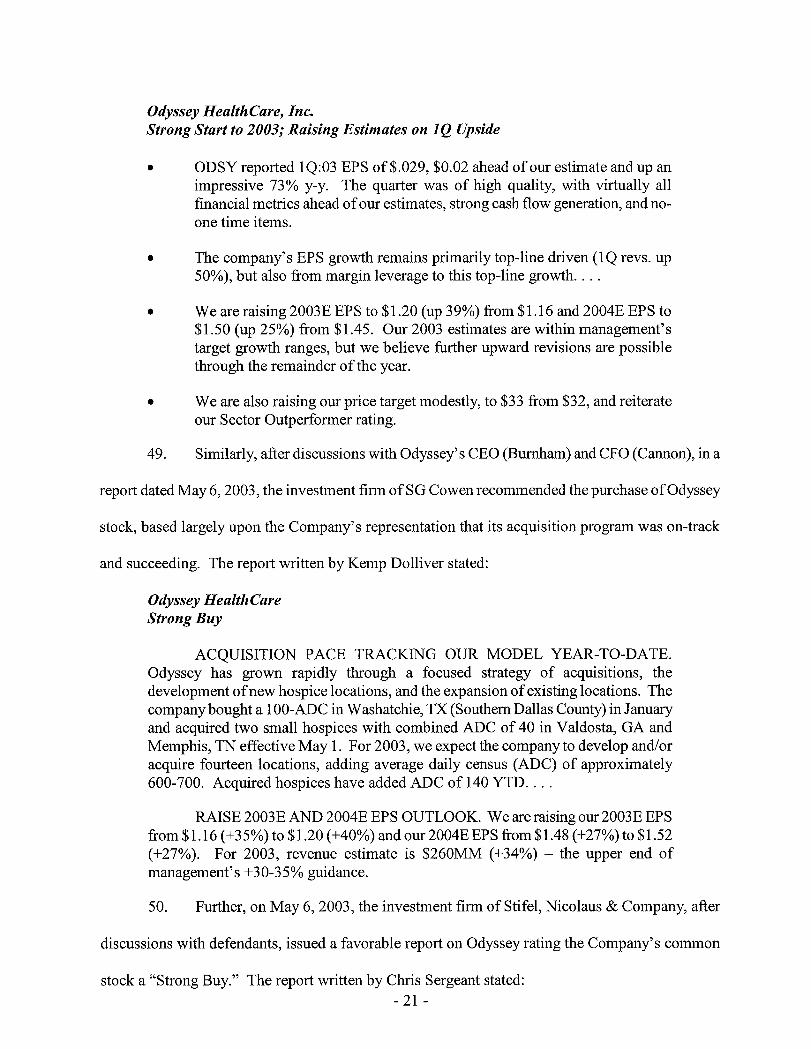

expansion, which would result in steady revenue, net income and EPS growth. Additionally,

defendants represented to investors that Odyssey's centralized operations and information system s

were robust enough to sustain the Company's rapid growth without compromising the quality of it s

hospice services or patient care; that Odyssey was successfully integrating the acquisitions that i t

was making into its business without any problems ; and that Odyssey had professionally traine d

community education representatives who specialized in educating the medical community about th e

benefits hospice care and Odyssey services, thereby increasing patient referrals to Odyssey an d

increasing its revenues and earnings . Thus, according to defendants, Odyssey's expansion program

and highly centralized and closely monitored business model would contribute significantly t o

Odyssey reporting annual earnings growth of 30+%, and FY03 EPS of $1 .20-$1 .25 per share and

FY04 EPS of $ 1 .50-$1 .60 per share , respectively.

As a result of the positive image created by defendants of the Company's illegal

earnings and business prospects, securities analysts repeatedly issued "strong buy," "buy," "marke t

overweight," and "market outperform" recommendations emphasizing Odyssey's ongoing growt h

-2-

and strong growth prospects . For example, a Stifel, Nicolaus & Company analyst, based o n

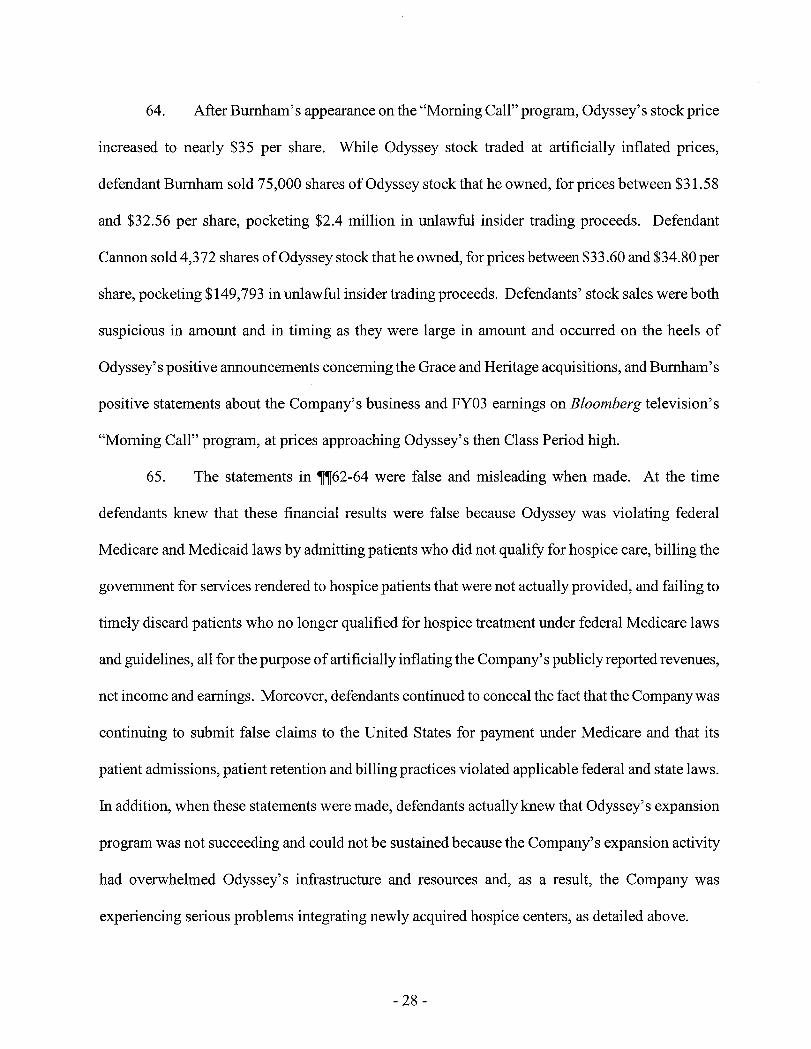

information provided by defendants and with their approval, stated on May 6, 2003 :

Odyssey exceeds our March quarter estimates on every front, with EPS $0 .03better at $0.29 vs. $0.16 prior . Importantly, staffing utilization remains excellent,and the company is on track with its 2003 expansion plans . Strong Buy, $37 [price]target .

We like Odyssey's balanced approach to growth, with a steady blend of smallacquisitions and new office openings, never biting off more than they canchew. We see this strategy as an effective way to maintain momentum in therace for new patients and in maintaining strong operating margins .

At 22x 2003 estimates , and with more than a 25% discount to its growth rate , ODSY shares remain

attractively priced . Strong Buy.

6 . Similarly, based on information provided by defendants and with their approval, S G

Cowen wrote on November 5, 2003 :

Odyssey Health Care : Strong BuyAcquisition Pace Running Ahead Of Our 2003 Thinkin g

Odyssey has completed seven acquisitions this year with ADC of 517, wellahead of the 300 ADC we expected initially this year. The largest, Heritage Hospicein Utah, had ADC of 280 . Management continues to seek acquisitions of many sizes .On the development side, Odyssey has received Medicare certifications for seven ofthe eight offices planned for 2003 : Cleveland, OH; Toledo ; OH, Cincinnati, OH ;Philadelphia, PA; Mobile, AL; Memphis, TN; Portland, OR and Richmond, VA.

Further, a SunTrust Robinson Humphrey analyst, based on information provided b y

defendants and with their approval, stated on December 19, 2003 :

ODSY : Initiating Coverage with Overweight Rating

Initiating coverage with Overweight rating and establishing a valuation rangeof $35-$36 . Our positive investment thesis is underscored by our belief thatODSY is poised to grow EPS 20%-25%, with the potential for 30%+ growthduring FY04 and FY05 .

Importantly, we believe ODSY's highly-evolved corporate /divisionalin frastructure should position it well to exploit both inte rnal growth

-3-

opportunities, as well as acquisition opportunities in the highly fragmentedhospice sector .

8 . The false image of Odyssey created by defendants ' statements to investors and

securities analysts drove Odyssey's stock price to a Class Period high of $37 .35, while Odyssey' s

insiders sold 969,526 shares of Odyssey stock, reaping more than $24 .1 million in unlawful insider

trading proceeds for themselves. In fact, defendant Richard R. Burnham, Odyssey's Chairman an d

CEO (until January 1, 2004), sold 628,769 shares of his personal Odyssey stock, for proceeds o f

$14.8 million, while Odyssey's next two highest ranking officers, David C . Gasmire (President and

CEO (from January 1, 2004 - October 15, 2004)), and Douglas C . Cannon (Senior Vice President

and CFO), sold 277,011 and 63,746 shares of their personal Odyssey stock, for proceeds of $7 . 7

million and $1 .6 million, respectively .

9. Odyssey' s earnings and defendants ' positive statements , creating the impression that

Odyssey was successfully pursuing an aggressive expansion program which would lead to solid an d

dependable revenue and earnings growth, were false and misleading when made, because defendant s

only achieved these earnings through illegal conduct . Defendants misrepresented and failed to

disclose the material facts detailed in ¶¶47-50, 53-54, 56-59, 62-64, 66-68, 71-72, 74-77, 79- 80, 82-

89, 91-92, 94-98 and 104-107 . In particular, Odyssey was, during the Class Period, experiencing

substantial difficulties in profitably integrating the hospice care centers it was acquiring into

Odyssey's business . Again, to make it appear that Odyssey's business was more profitable than i t

actually was, before and during the Class Period, Odyssey engaged in unlawful patient admission ,

patient retention and billing practices which violated Medicare and Medicaid laws, rules and

regulations . Asa result of these practices, Odyssey has been the subject of a federal investigation b y

the Civil Division of the U .S. Department of Justice ("DOJ") under the False Claims Act for wel l

over a year, rendering defendants' statements about Odyssey's compliance with applicable federa l

and state laws, rules and regulations false and misleading when made .

-4-

10. During the Class Period, defendants were acquiring hospice after hospice and valuing

goodwill and other intangibles at inflated p rices in violation of GAAP to hide operational problem s

they were experiencing with their rapid growth, at the same time they were violating Medicare law s

by admitting patients and retaining patients that did not meet Medicare guidelines and double-billin g

to attain their projected earnings. All this had to stop when the DOJ began its investigation into thi s

very activity. Therefore, without the ability to continue their fraudulent course of conduct (becaus e

the DOJ was on defendants' trail), Odyssey was forced to reveal the true condition of its business .

On October 18, 2003 , Odyssey revealed that its 3rd quarter FY04 EPS would be only $0 .24 per

share, sharply below the levels that defendants had previously misled the market to expect . In

revealing this earnings decline, Odyssey also slashed its EPS estimates for 2004 to $0 .94-$0.96 from

$1 .03-$1 .05 . The Company also announced that Odyssey's President and CEO, defendant Gasmire ,

had abruptly resigned and that Odyssey's Chairman, defendant Burnham, would assume the

additional duties of President and CEO. Additionally, defendants acknowledge on October 18, 2004 ,

that due to the Company's patient admission, patient retention and billing practices since 2000 ,

Odyssey was now under investigation for violations of the False Claims Act by the DOJ . As a result

of these shocking revelations, Odyssey's stock price collapsed, falling nearly 48%, to as low a s

$8 .80 per share, on extraordinarily heavy volume of 22 .4 million shares thereby damaging th e

plaintiff stockholders . Clearly, after the revelation of these facts, investors and analysts believed that

the value of the Company's stock was only half of what it was worth when they were not privy t o

this information.

11 . While defendants profited handsomely from their fraudulent scheme, selling 969,526

shares of their personal Odyssey stock , for $24 .1 million in unlawful insider trading proceeds, Lea d

Plaintiffs and the Class did not . Instead, they suffered tens of millions of dollars in damages as a

result of defendants' alleged misconduct . By this action, Lead Plaintiffs and the Class seek to

-5-

recover damages against defendants for their violations of §§10(b) and 20(a) of the Securitie s

Exchange Act of 1934 (the "1934 Act") and Rule lOb-5 promulgated thereunder by the Securitie s

and Exchange Commission (the "SEC") .

JURISDICTION AND VENU E

12 . This Court has jurisdiction over the subject matter of this action under §27 of the

1934 Act . The claims alleged herein arise under §§10(b) and 20(a) of the 1934 Act, 15 U .S .C .

§§78j(b) and 78t-1, and Rule lOb-5 promulgated thereunder by the SEC .

13. Venue is proper in this District under §27 of the 1934 Act, as many of the false and

misleading statements and omissions allegedly made by defendants were made in or issued from thi s

District . Additionally, Odyssey's principal executive offices are in Dallas, Texas, where defendant s

managed and oversaw Odyssey's daily operations .

THE PARTIES

Lead Plaintiffs

14. (a) Lead PlaintiffMassachusetts Laborers Annuity Fund purchased Odyssey

common stock and was damaged thereby.

(b) Lead PlaintiffAlaska Electrical Pension Fundpurchased Odyssey common

stock and was damaged thereby .

Defendants

15. Defendant Odyssey Healthcare, a Delaware corporation, is headquartered and may

be served at 717 N . Harwood , Suite 1500, Dallas, Texas 75201 . Odyssey's common stock trades i n

an efficient market on the NASDAQ National Market System .

16 . Defendant Richard R. Burnham ("Burnham") was, during the Class Period ,

Chairman and CEO (until January 1, 2004) of Odyssey . Prior to joining Odyssey, Burnham was a

Vice President for Vitas Healthcare, Inc., a hospice care provider . Burnham , as a member of th e

Odyssey's small, insular senior management team , personally guided the Company's expansion-6-

program and oversaw Odyssey's business and financial affairs on a daily basis . Burnham sold

628,769 shares of Odyssey common stock that he owned during the Class Period for prices as hig h

as $32 .56 per share, reaping proceeds of $14 .8 million from insider trading activity . These sale s

were unusual in timing and amount in that they came on the heels of Odyssey's positive earning s

announcements, reporting strong 1st, 2nd and 3rd quarter FY03 results, and while Odyssey stock

traded at prices near its then Class Period highs . Burnham maybe served at 2505 Woodbridge Trail,

Mansfield, Texas 76063 .

17. Defendant David C. Gasmire ("Gasmire") was, during the Class Period, President,

CEO (from January 1, 2004 to October 15, 2004) and Director of Odyssey . Prior to joining

Odyssey, Gasmire was the General Manager and Director of Business Development for Vist a

Healthcare , Inc., a hospice care provider . Gasmire , as a member of Odyssey's small , insular senio r

management team, personally guided the Company's expansion program and oversaw Odyssey' s

business and financial affairs on a daily basis . Gasmire sold 277,011 shares of Odyssey commo n

stock that he owned during the Class Period for prices as high as $30 .68 per share, reaping proceeds

of $7.7 million from insider trading activity . These sales were unusual in timing and amount in that

they came on the heels of Odyssey' s positive earnings announcements , repo rting strong 1st, 2nd and

3rd quarter results, and while Odyssey stock traded at prices near its then Class Period highs .

Gasmire maybe served at 5504 Wilts Court, Plano, Texas 75093 .

18 . Defendant Douglas B. Cannon ("Cannon") was, during the Class Period, Senio r

Vice President, CFO, Assistant Secretary and Treasurer of Odyssey . Prior to joining Odyssey,

Cannon was the CFO of Cornerstone Health Management Company, a specialty provider of geriatri c

services to hospitals and operator of long-term acute hospitals . Cannon, as a member of Odyssey' s

small, insular senior management team, personally guided the Company's expansion program an d

oversaw Odyssey's business and financial affairs on a daily basis . Cannon sold 63,746 shares o f

-7-

Odyssey common stock that he owned during the Class Period for prices as high as $34 .70 per share,

reaping proceeds of $1 .6 million from insider trading activity . These sales were unusual in timing

and amount in that they came on the heels of Odyssey's positive earnings announcements, reportin g

strong 1st, 2nd and 3rd quarter results, and while Odyssey stock traded at near its then Class Perio d

highs. Cannon maybe served at 4728 Yorkshire Trial, Plano, Texas 75093 .

19. Burnham, Gasmire and Cannon were the top executives of Odyssey and members o f

its senior management group . They ran Odyssey as "hands -on" managers , dealing with important

issues facing Odyssey's business and representing to the investing public that they were :

(i) successfully managing its expansion program; (ii) profitably growing Odyssey's business by

providing superior patient care and assistance services ; and (iii) complying with all applicable

Medicare and Medicaid laws, rules and regulations ; thereby enabling the Company to continue t o

report 30% - 33% annual revenue and 35% - 40% net income growth in FY03 and beyond .

20. A key factor in the Odyssey "story" was its ability to expand rapidly by opening new

or acquiring and integrating other hospice care companies, while sequentially reporting strong

revenue and earning growth . As defendants stated in Odyssey's 2003 Report on Form 10-K, "[w] e

intend to expand our business by actively pursuing strategic acquisitions of other hospices in new

and existing markets throughout the United States . We believe that significant opportunities exis t

for growth through acquisitions of hospices . . . . We believe that the fragmented nature of th e

hospice industry, combined with these other factors, provides us with significant opportunities to

grow our business through acquisitions . . . ." To capitalize on these opportunities, defendant s

closely monitored and managed every material aspect of Odyssey's expansion program . As a resul t

of this intense focus, defendants knew or recklessly disregarded that, by the beginning of the Clas s

Period, the Company's earlier growth had overwhelmed the Company's infrastructure and

-8-

management capabilities such that its expansion program would have to be curtailed, if no t

abandoned, leading to lower revenue and earnings growth on a going forward basis .

21 . Nevertheless, at every opportunity during the Class Period, defendants flooded the

market with false positive statements about Odyssey's expansion program and their own ability to

successfully open and/or integrate newly acquired hospice care centers into Odyssey's business ,

thereby increasing Odyssey's overall revenues and earnings . Defendants likewise misrepresented ,

for example, in Odyssey's 2003 report on Form 10-K, dated March 11, 2004, that Odyssey was i n

compliance with all applicable Medicare and Medicaid laws, rules and regulations, stating tha t

Odyssey is "in material compliance with all conditions of participation for the Medicare program s

and all eligibility requirements for the Medicard program," as well as "all applicable federal an d

state fraud and abuse laws," when they knew they were committing Medicare violations .

22. Each defendant is liable for making false statement and for failing to disclose advers e

material facts while selling Odyssey stock or for participating in a fraudulent scheme which operate d

as a fraud or deceit on purchasers of Odyssey common stock . They are also liable for the false

statements pled at ¶¶47, 53-54, 56-57, 62, 66, 71-74, 79, 85-86, 94-95 and 100, as those statements

were each collectively-published information for which defendants were collectively responsible as

officers and directors of the Company, as well as for the false statements pled at ¶¶48, 50, 58-59, 67-

68, 76-77, 80, 83-84, 87-89, 92 and 96-98, as those statements were made by defendants to securities

analysts for the purpose of artificially inflating Odyssey's stock price during the Class Period .

23 . In addition to knowing that their Class Period statements were actually false whe n

made, defendants also had the motive and opportunity to perpetrate the fraudulent scheme an d

course of conduct detailed in ¶¶1-11, 24-103 . Specifically, by artificially inflating Odyssey's stock

price by making it appear that Odyssey was a fast growing company with sustainable growth ,

-9-

Odyssey insiders were able to sell 969,526 shares of their personal Odyssey stock during the Class

Period, pocketing over $24 .1 million in unlawful insider trading proceeds .

DEFENDANTS' FRAUDULENT SCHEME TO DEFRAUDINVESTORS AND SCIENTER

24. Formed in 1996 by defendants Burnham and Gasmire, Odyssey grew rapidly during

the late 1990s and the early 2000s and enjoyed steady growth in revenues and earn ings . Through a

series of acquisitions and the development of new hospices, Odyssey grew from a single hospice

program to over 50 Medicare-certified hospice programs to serve patients and their families in mor e

than 20 states . Today, although headquartered in Dallas, Texas, Odyssey 's operations stretch from

coast-to-coast, and involve more than 25,000 patients, nurses, doctors and other healthcare provider s

and suppliers .

lknnc xRhode

rtllnn rv u Islan dAFttngt 2 n tt,. dht _ _ w

r~ ' 3~ 7a NewJsrsay

='~ tta M - Fmn7~, ;;I r,~G, _

~Pm,L~ruh ~tre~~lase~@~la

~., a o e~ItF i >r~lurro~s ~ -- ~~@ilmi~~n'~ N',rm - F3 r cterm altI ani~dc~ £_ '_ ~ ~

In 7l~nn[all.~Irnf te

_

u~yn F G~jr~e

Mchi b- ,~ j4 9 m ardrno

__. . .Lafl AGl~leti. ~

1 .,mcola F e

•

IuL~ - --Alunlcl ~ m _ -

OrangeCounl' nP' 7s i~hoerdr -:,t ~~~eJ f UAmam i

aw

.YiCrn3 C11'i ~~1b :,tt1 0_ I L 1 E 1FJi; i~. ~'1 n'~i!I )hfin ~

.y s L' lJf ^S10 S

l¢:.x~n fml Wngh walla- i .-- .~aoc~so n

-tl Pnsc •:~ ~arnJf? e 4nIJn [n ,tVn~ E7ayt e

dusP.na r ''rte U~te~Eara~ ~

calm7{ II '1ll ' . ~. I~.3 f1 l111FO n.~

lake thadm How afleans

k iw i

~9~p[f~B 3CI9

s Inµnkicm fiiokty

Emµ~ewle Ihfices .

-10-

25 . To effectively oversee and manage Odyssey's far-flung operations on a daily basis ,

defendants invested in and developed a centralized operations and division structure within the

Company. The hub of Odyssey's "centralized operations" is its corporate office in Dallas, Texas .

The Dallas office supports each of the Company's hospice programs by providing coordination ,

centralized resources and corporate services to each of its hospice programs . These include, among

other things: (i) financial accounting systems, including billing, accounts receivable, account s

payable and payroll ; (ii) information and telecommunication systems ; (iii) clinical support services ;

(iv) human resource administration; (v) regulatory compliance and quality assurance ; (vi) marketing

and educational materials; (vii) training and development ; and (viii) centralized cash management

and account payable and payroll processing .

26. In addition, Odyssey processes all billings to the United States, private insurers an d

patients electronically at its corporate office in Dallas . Under the oversight of the defendants, th e

Dallas office bills Medicare monthly and generally receives payment electronically within 1 4

working days . The corporate offices accounting personnel prepare monthly operating statements for

each of the hospice programs and review these statements for operating trends and variances t o

budget forecasts. Defendants, at all relevant times, received the monthly operating statements

mentioned above in parallel with the individual hospice programs .

27. Under defendants' supervision , the Dallas corporate office also prepared annua l

operating budgets for each of the Company's hospice programs, which defendants reviewed and

approved before each fiscal year, as well as used throughout the fiscal year to monitor th e

performance of individual hospice programs, groups of hospice programs, and the Company as a

whole versus its annual budgets and forecasts .

28 . To manage, monitor and oversee Odyssey's daily operations on a real-time basis ,

defendants also developed an extensive information management system . The information system

- 11 -

known, in part, as MUMMS within the Company utilizes multiple server-based systems with lapto p

and desktop computers to connect all of Odyssey 's hospice programs to one another electronically,

and to allow defendants to monitor the performance of individual hospice programs or groups of

hospice programs on demand . To accelerate the payment for services rendered, billings are als o

handled through a centralized server-based systems located at Odyssey's Dallas headquarters . Under

this system, each local office enters all initial patient registration information and updates into th e

billing status through the Company's intranet systems, supposedly resulting in greater accuracy an d

more rapid collections . Through the use of the Company's intranet site, defendants are also able to

facilitate communications and enhance standardization of all of Odyssey's operations throug h

publication and dissemination of a standard vision and a consistent, comprehensive corporat e

direction .

29. Moreover, through the use of the Company's centralized operating model and

information system, defendants were able to, and did in fact, "monitor and manage" the most critica l

and essential elements of Odyssey' s business , i.e ., "admissions , discharges by type of discharge and

admission conversions," on a daily and regular basis, to control costs and thereby maintain or

increase profitability . As defendants stated in Odyssey's 2003 Report on Form 10-K, dated

March 11, 2004 :

We actively manage and monitor several day-to-day indicators, includingadmissions , discharges by type of discharge and admission conversions on a dailybasis . We also track on a regular basis various key measures of our costs per day ofcare, including costs of labor , medications , durable medical equipment, medicalsupplies and mileage expense incurred by our caregivers . . . .

In the same report, regarding their habit of monitoring and managing Odyssey's business an d

progress towards its financial objectives throughout the Class Period, defendants stated: "We

actively manage and monitor several indicators to track performance across our multiple hospic e

programs, which enables us to develop best practices, improve efficiencies and manage costs . . . . "

-12-

30. The centralized and standardized operations and information system developed b y

defendants served Odyssey well during the early phases of its rapid growth . However, by early

2003, Odyssey's expansion had overwhelmed the Company's internal controls and corporate

infrastructure, i.e ., its centralized operations and information systems, thereby impairing th e

Company's ability to profitably expand in existing and new markets via new developments and/o r

acquisitions. As Odyssey's business expanded into new markets and areas, the Company' s

operational challenges grew exponentially, resulting in significant declines in the quality of hospic e

care delivered to patients and their families, and material increases in the Company's drug costs ,

labor costs and associated operating expenses .

31 . For example, former Odyssey staffers complained to management about lack o f

access to supplies and caseload that are heavier than industry norms . In one instance, the lack of

access to supplies was so bad that the attending nurse was unable to give the patient over-the-counte r

Robitussin. And Odyssey's 55-to-1 patient-to-nurse ratio exceeded industry norms by a wide

margin . Although former Odyssey nurses and supervisors reported these problems to defendants ,

they persisted throughout the Class Period unabated .

32 . Patients and their families also reported incidents where Odyssey's rapid growth

resulted in the Company providing a level of care and service below the standards set forth unde r

government guidelines. As Barron's reported on April 12, 2004, a son of an Odyssey patient tol d

"of Odyssey's ignoring calls from a nursing home as the staff sought the assistance of the hospic e

firm [Odyssey] with which he'd contacted ." "Byron `Pat' Connelly hired Odyssey to provide

hospice care for his mother, who [in the summer of 2003] was a patient in Vista Knoll Specialize d

Care Facility in Vista, Calif., dying of congestive heart failure . When her condition began to

deteriorate, Connelly adds, nurses at Vista Knoll said that Odyssey ignored their repeated calls t o

come and care for the 86-year-old woman . `We felt she was not getting the care she should b e

-13-

getting,' Connolly remembers . "I wasn't mad . I was upset." He says that his mother died within a

week of being transferred to another hospice program . "

33 . As a result of this and other reports, in September 2003, the California Department of

Health Services found Odyssey's San Diego hospice program to violate certain patient care

standards after conducting a routine rece rtification survey. The 33-page repo rt detailed numerou s

instances of patients in severe discomfort and distress being cut from the program inappropriately

and without consultation involving all members of the medical team . Drugs, including simple items

such as cough syrup, were not immediately available because the hospice had not contracted with a

pharmacy to pay for them . Volunteer services were not provided and other treatments and services

typically covered were not provided . The California report also found that a lack of communicatio n

and documentation had led to misguided care, because, among other things, Odyssey's clinica l

records were in disarray.

34. Additionally, as Barron's reported, former Odyssey nurses and marketin g

representative told them of patients being kicked out of Odyssey's program after 90 days upon bein g

"reevaluated" or because they required hospital care . According to persons familiar with Odyssey,

this raises the possibility that the patients should not have been admitted into Odyssey's hospic e

program in the first place . In fact, the DOJ is currently looking into this issue as a part of its

investigation under the False Clams Act into Odyssey' s patient admission, patient retention an d

billing practices since 2000 .

35. The increase in Odyssey's operational problems, coupled with the slowdown in it s

business, presented defendants with a desperate situation . On the one hand, to increase Odyssey' s

revenues the Company needed to grow rapidly . However, to grow rapidly, the Company needed to

attract capital by continuing to report strong revenue and earnings growth . Thus, to overcome thi s

situation, as early as 2000, defendants embarked upon a scheme that involved the adoption of a

-14-

number of unlawful and improper patient admissions, patient retention and billing practices . For

example, to artificially inflate the Company's revenues, Odyssey routinely admitted patients wh o

were not eligible for hospice care because they had a life expectancy of more than six months .

Similarly, when doctors refused to recertify admitted patients as eligible for hospice care, Odysse y

refused to timely discharge them, thereby allowing the Company to bill for and receive payment fo r

services render to patients who were not eligible for hospice care . Since Odyssey recognized

revenue on hospice care services in the first month received, the Company was able to retain th e

improper payments for at least 30-90 days, thereby artificially inflating the Company's revenues an d

financial results in violation of GAAP . Moreover, and, perhaps, even worse, Odyssey bille d

Medicare for services that were never rendered to hospice patients and their families, thereb y

artificially inflating Odyssey's revenues and drastically decreasing its expenses .

36. Although defendants succeeded in concealing these unlawful practices and violation s

of the federal securities laws, Medicare laws and state and federal abuse laws from investors and

regulators alike for several years, in September 2004, the DOJ notified the Company that it wa s

under investigation under the False Claims Act for acts and omissions concern ing its patien t

admissions, patient retention and billing practices from January 2001 to September 2004 . 1

37 . Defendants' knowledge of Odyssey's patient admission, retention and billin g

practices, as well as the fact that they violated the applicable Medicare laws, is in little doubt .

According to a former general manager of Odyssey's Oklahoma City hospice center, defendant

Gasmire and others were responsible for the Medicare cap issues and unqualified patient problems i n

Odyssey because Gasmire not only imposed what were unreasonable census goals, but he knew tha t

' Subsequently, the Company announced that two qui tam whistleblower actions relating tothis investigation have been filed and that the DOJ is considering taking those actions over .

-15-

the census results being reported back from the various hospice facilities were inflated wit h

inappropriate admissions . The general manager was aware of instances during a major admissions

campaign when nurses protested directly to defendants and other company officers . According to

the general manager, they were told to "admit them anyway ."

38. Moreover, as defendants stated in Odyssey's 2003 Report on Form 10-K, Odysse y

"actively manage and monitor several day-to-day indicators, including admissions, discharges b y

type of discharge and admission conversions on a daily basis ." Further, as a part of the Company' s

internal auditing and monitoring programs, Odyssey conducted "periodic , at least annual , internal

regulatory audits and mock surveys at each of [its] hospice programs," as well as, "quarterl y

comprehensive audits of patient charts performed by each of [the Company's] hospice programs," as

required under Medicare conditions of participation. In addition, "at least once a year, a

comprehensive audit of patient charts [was] performed on each of [Odyssey's] hospice programs b y

[its] corporate staff. "

39. In light of the Company's "comprehensive" and redundant regulatory complianc e

auditing and monitoring programs, defendants knew, or were reckless in not knowing, tha t

Odyssey's patient admission, patient retention and billing practices violated applicable Medicare an d

federal and state false claims and abuse laws, as well as resulted in the Company materially

overstating its revenues by improperly recognizing revenues on hospice services rendered to patient s

who were ineligible .

40. More particularly, during the Class Period, Odyssey reported as revenue unlawfu l

billings to Medicare and p rivate insurers to which Odyssey was not entitled . In violation of GAAP ,

Odyssey reported revenues that were non-existent and that they knew would have to be returned t o

Medicare or the insurance companies . This was accomplished by means of double billing, billing for

services not rendered, and recognizing revenue that exceeded Medicare caps for reimbursement .

-16-

These revenues had no justification but were made so that defendants could artificially inflat e

Odyssey's publicly reported financial results and financial statements .

41 . For example, during the Class Period, Odyssey routinely billed both Medicare and th e

patients' insurance carriers for the full amount of services rendered to hospice patients and thei r

families . According to a former billing supervisor at Odyssey's headquarters in Dallas who oversa w

all of the hospice programs , the double billing occurred at several of Odyssey' s hospice care centers,

including its hospice center in Detroit . According to the billing supervisor, Odyssey's Detroi t

hospice center was "thriving" because of the improper double billing . In Detroit, there is a large

population of retired auto-workers which comprises the majority of Odyssey's hospice patients . The

auto-workers had Blue Cross/Blue Shield which would supplement Odyssey for whatever amount

that exceeded the patient's allowable Medicare reimbursement . However, Odyssey frequently billed

both Blue Cross/Blue Shield and Medicare for the entire amount, instead of billing the reduced

amount to both, allowing Odyssey to collect reimbursement for the full amount owed from both

Medicare and Blue Cross/Blue Shield. Senior management knew about this practice because th e

billing supervisor reported this activity to senior management and recommended that Odysse y

reimburse Blue Cross/Blue Shield. After senior management failed to take corrective steps, th e

billing supervisor reported Odyssey's double billing to Blue Cross/Blue Shield, which demanded a

refund. Ultimately, Odyssey was forced to reimburse Blue Cross/Blue Shield for the over-payments .

However, Odyssey's practice of double billing Medicare and private insurers continued unabated a t

other hospice sites .

42 . During the Class Period, Odyssey billed for patient services that had not actually been

rendered. In fact, defendants would intimidate the hospice staff with the threat of termination if the y

did not improperly bill the insurance carriers . According to a former reimbursement coordinator ,

he/she was fired because he/she refused to bill for services that had not been rendered in Odyssey' s

-17-

Orange County hospice facility . The root of this activity was that the hospices were understaffe d

and did not have enough resources to provide the proper amount of care . According to a former

Odyssey billing supervisor, the bills generated through Odyssey's MUMMS system which woul d

ultimately reach the insurance companies did not match the "service notes" that had been input b y

nurses at the hospices for the care they had administered to each specific patient . The MUMMS

system electronically linked billing and collections of every Odyssey hospice in the United States t o

the corporate headquarters in Dallas . Odyssey hospice staff would enter patient information and

updates daily into the MUMMS system regarding what kinds of services that had been performed .

The services that had been performed for each patient were compiled at the end of the month b y

billing supervisors at the Dallas headquarters in order to bill Medicare, Medicaid or private insuranc e

companies . The billing supervisors were supposed to also verify the services with patient "servic e

notes ." According to the billing supervisor, often times the "service notes" did not match MUMMS .

This was because the hospices were actually billing for these missing services because they wer e

required to perform them, whether they actually did so or not . The hospices were so understaffed

because of managements' efforts to cut costs and increase profit, that many nurses simply did no t

have the time to see all their patients every day .

43 . For example, Aetna Insurance Company would pay for hospice services for their

insureds for every day in the week, but the "service notes" indicated that Odyssey staff was onl y

providing services a few days out of the week . According to a billing supervisor, one of the hospic e

patients informed Aetna of the situation and this caused Aetna to demand reimbursement, whic h

Odyssey fought but eventually had to give back the fees for that patient . However, Odyssey rarely

got caught and ended up improperly recognizing the improperly obtained revenue .

44 . Odyssey also put a stop to billing supervisors having access to "service notes" after

several of them pointed out the improper billing practices to senior management . This put a stop to

-18-

billing mangers' ability to match services to bills . According to one billing supervisor, a member o f

senior management stated that billing for services not rendered made Odyssey's reported revenu e

"look good . "

45 . Also, during the Class Period the Oklahoma State Attorney's Office was investigatin g

the Oklahoma hospice for Medicare billing fraud as well . According to a former general manager o f

the Oklahoma City hospice , during the investigation it was determined that numerous patients ha d

been admitted in p rior periods were ineligible under Medicare to receive hospice care . This facility

was forced to payback Medicare at least $770,000 . Apparently, this was not unique to Oklahoma, a s

numerous other facilities, including Colorado Springs, Colorado and Wichita, Kansas, were forced t o

pay back millions of dollars to Medicare thus far . Defendants were well aware of this activity yet

hid this information from the public .

46. In addition to the above, Burnham, Gasmire and Cannon each knew about o r

recklessly disregarded the problems with Odyssey's expansion program, patient care, financial

statements, patient admission, patient retention and billing practices alleged in the Complaint an d

were motivated to conceal such problems . As Odyssey's three highest ranking corporate officers ,

and the leaders of its senior management team, Burnham, Gasmire and Cannon were responsible for

Odyssey's financial report ing and communications with the market . They knew or recklessly

disregarded the adverse facts then impacting Odyssey's business detailed in the Complaint . But

nonetheless , they flooded the market with positive statements about Odyssey, its business , expansio n

program, hospice care services , compliance with applicable Medicare requirements, earnings and

prospects for future growth . Defendants did so to demonstrate that they could lead the Compan y

successfully and generate the growth expected by the market, as well as to unload their persona l

Odyssey shares .

-19-

DEFENDANTS' FALSE AND MISLEADING STATEMENT S

1st Quarter FY03

47. On May 5, 2003, Odyssey announced its 1st quarter FY03 results, ended March 31 ,

2003, reporting a 79% increase in net income to $7 .2 million , or $ .29 per share , on a 50% increase in

revenue to $60 .1 million . The Company also announced that its average daily census for the 1s t

quarter FY03 increased 45% to 5,363 patients, days of care for the quarter increased by 44% to

5,533, and that net cash provided by operations for the quarter was $12 .3 million . In the Company' s

1st quarter FY03 earnings release, Burnham, with the approval of Gasmire and Cannon, attribute d

Odyssey's strong performance to the success of its expansion program and the Company's ability to

provide excellent hospice care services to patients, stating :

"Our goal of providing excellent service to an increasing number of patientsand their families and leveraging our existing infrastructure to produce strongfinancial performance is showing very good results," . . . . "As is typical in ourcompany, the increase in days of patient care is primarily attributable to growth inour existing locations . In addition to this internal growth, during the quarter, weacquired a hospice south of Dallas, which complements our Dallas/Fort Worthservice area . "

"We expect revenue growth in 2003 of 30 to 33 percent over 2002 and an increase of35 to 40 percent in net income over 2002," he said. The company had previouslyprovided guidance of 30 percent growth in revenue and 30 to 35 percent growth innet income year over year . "

48. Following the release of the Company's 1st quarter FY 03 earnings press release ,

securities analysts issued reports on Odyssey which were based on and repeated the fals e

information provided by Odyssey 's senior management . For example , on May 5, 2003, CIBC World

Markets issued a report in which it recommended the purchase of Odyssey stock based largely upo n

the Company' s representation of strong revenue and earning growth. The report written by Charle s

W. Lynch stated :

-20-

Odyssey Health Care, Inc.Strong Start to 2003 ; Raising Estimates on IQ Upside

• ODSY reported 1Q:03 EPS of $.029, $0.02 ahead of our estimate and up animpressive 73% y-y. The quarter was of high quality, with virtually allfinancial metrics ahead of our estimates, strong cash flow generation, and no-one time items .

• The company's EPS growth remains primarily top-line driven (1Q revs . up50%), but also from margin leverage to this top-line growth . . . .

• We are raising 2003E EPS to $1 .20 (up 39%) from $1 .16 and 2004E EPS to$1 .50 (up 25%) from $1 .45. Our 2003 estimates are within management'starget growth ranges, but we believe further upward revisions are possiblethrough the remainder of the year .

• We are also raising our price target modestly, to $33 from $32, and reiterateour Sector Outperformer rating .

49. Similarly, after discussions with Odyssey's CEO (Burnham) and CFO (Cannon), in a

report dated May 6, 2003, the investment firm of SG Cowen recommended the purchase of Odyssey

stock, based largely upon the Company's representation that its acquisition program was on-trac k

and succeeding . The report written by Kemp Dolliver stated :

Odyssey Health CareStrong Buy

ACQUISITION PACE TRACKING OUR MODEL YEAR-TO-DATE .Odyssey has grown rapidly through a focused strategy of acquisitions, thedevelopment of new hospice locations , and the expansion of existing locations . Thecompany bought a 100-ADC in Washatchie , TX (Southern Dallas County) in Januaryand acquired two small hospices with combined ADC of 40 in Valdosta, GA andMemphis, TN effective May 1 . For 2003 , we expect the company to develop and/oracquire fourteen locations , adding average daily census (ADC) of approximately600-700. Acquired hospices have added ADC of 140 YTD . . . .

RAISE 2003E AND 2004E EPS OUTLOOK . We are raising our 2003E EPSfrom $1 .16 (+35%) to $1 .20 (+40%) and our 2004E EPS from $1 .48 (+27%) to $1 .52(+27%). For 2003, revenue estimate is $260MM (+34%) - the upper end ofmanagement's +30-35% guidance .

50 . Further, on May 6, 2003, the investment firm of Stifel, Nicolaus & Company, after

discussions with defendants, issued a favorable report on Odyssey rating the Company' s commo n

stock a "Strong Buy." The report written by Chris Sergeant stated :

-21-

Odyssey exceeds our March quarter estimates on every front, with EPS $0 .03better at $0.29 vs. $0 .16 prior. Importantly, staffing utilization remains excellent,and the company is on track with its 2003 expansion plans . Strong Buy, $37 target .

In the break-neck race for territory and patient flow in the for-profit hospicearena, Odyssey kept up the pace in the first quarter . They again exceeded ourestimates on every measure .

Odyssey is on track for its 2003 expansion plans, and they continue to deliveragainst plan .

We like Odyssey's balance approach to growth, with a steady blend of smallacquisitions and new office openings, never biting off more than they canchew. We see this strategy as an effective way to maintain momentum in therace for new patients and in maintaining strong operating margins .

51 . After these announcements, Odyssey's stock price advanced to its then Class Perio d

high of over $22 per share. While Odyssey stock traded at artificially inflated prices, defendan t

Burnham sold 300,000 shares of Odyssey stock that he owned, for prices between $17 .20 and $22 .02

per share, pocketing $5 .4 million in unlawful insider trading proceeds . Defendant Gasmire sol d

69,596 shares of Odyssey stock that he owned , for prices between $19.79 and $22 .80 per share,

pocketing $1 .4 million in unlawful insider trading proceeds . And defendant Cannon sold 19,49 2

shares of Odyssey stock that he owned, for prices between $19 .86 and $20 .16 per share, pocketing

$387,341 in unlawful insider trading proceeds. Defendants' stock sales were both suspicious in

amount and in timing as they were large in amount and occurred on the heels of Odyssey 's positive

earnings announcement, reporting strong revenue and earnings for the 1st quarter of FY03, at price s

approaching Odyssey's then Class Period high .

52. The statements in ¶¶47-50 were false and misleading when made. At the time

defendants knew that these financial results were false because Odyssey was violating federa l

Medicare and Medicaid laws by admitting patients who did not qualify for hospice care, billing th e

government for services rendered to hospice patients that were not actually provided, and failing to

timely discard patients who no longer qualified for hospice treatment under federal Medicare laws-22-

and guidelines, all for the purpose of artificially inflating the Company's publicly reported revenues ,

net income and earnings . Moreover, defendants continued to conceal the fact that the Company wa s

continuing to submit false claims to the United States for payment under Medicare and that it s

patient admissions, patient retention and billing practices violated applicable federal and state laws .

In addition, when these statements were made defendants actually knew that Odyssey's expansio n

program was not succeeding and could not be sustained because the Company's expansion activity

had overwhelmed Odyssey's infrastructure and resources and, as a result, the Company was

experiencing serious problems integrating newly acquired hospice centers, as detailed above .

53. Odyssey's artificially inflated stock p rice enabled the Company to acquire othe r

hospice care centers on more favorable terms by offering the acquiring company the opportunity to

join Odyssey's allegedly rapidly growing enterprise . For example, on May 6, 2003, Odyssey

announced a deal to acquire Mahogany Hospice Care, Inc ., based in Memphis, Tennessee

("Mahogany"), and another deal to acquire Home Care Hospice, Inc., based in Valdosta, Georgia .

Commenting on the Mahogany acquisition, a senior Odyssey official stated :

Odyssey's services are provided in patient homes, long-term care facilities,nursing homes or hospitals . . . . "We are pleased that with the acquisition ofMahogany we will begin providing our high-quality service to Memphis-areapatients immediately ." Odyssey, headquartered in Dallas, Tex ., currently has 67hospice locations in 26 states, including the Mahogany location . During 2003, thecompany has provided care to approximately 5,400 patients . The company provideshospice care in many major metropolitan areas, including Nashville .

54. Based on Odyssey's strong financial performance, on June 27, 2003, it wa s

announced that Odyssey had been added to the S&P 500 stock index . Three weeks later, on July 18 ,

2003, Odyssey announced a "a three-for-two stock split payable in the form of a fifty percent stock

dividend to be distributed on August 12, 2003, to stockholders of record at the close of business o n

July 28, 2003 ." Commenting on the dividend and Odyssey's "strong" operating performance ,

Burnham, with the approval of Gasmire and Cannon, stated :

-23-

"The company has a record of strong operating performance which themarket has recognized," said . Richard R . Burnham, chairman and chief executiveofficer . "We believe the three-for-two split will further improve trading liquidity andbroaden ownership of the company's common stock . "

55. On news of these developments, Odyssey's stock price advanced to over $25 per

share .

2nd Quarter FY03

56. On August 4, 2003, Odyssey announced its 2nd quarter FY03 results, ended June 30 ,

2003, reporting a 60% increase in net income to $7 .6 million, or $0.20 per share (post split), on a

39% increase in revenue to $64 .9 million . The Company also announced that its average daily

census for the 2nd quarter FY03 increased 34% to 5,758 patients, days of care for the quarter

increased 34% to 5,239, and net cash provided by operations for the quarter was $15 .1 million. In

the Company's earnings release, Burnham, with the approval of Gasmire and Cannon, attributed th e

Company's strong performance to the success of its aggressive expansion program, stating :

"We are very pleased with our continued strong financial performance," saidRichard R. Burnham, chairman and chief executive officer. "More importantly, ourexisting programs continue to reach more patients and families, and we are creatingadditional platforms for growth by expanding our programs into new communitiesaround the country."

Because of increased visibility into the remainder of the year, the companynoted that it was increasing its guidance for net income growth in 2003 to 40 to 43percent over 2002 results . The company had previously provided guidance of 35 to40 percent net income growth in 2003 over 2002 .

57 . Following the release of Odyssey's 2nd quarter FY03 results, defendants hosted a

conference call for investors and securities analysts on August 5, 2003 . Commenting on the succes s

of Odyssey's expansion program and the Company's strong performance, Burnham, with the

approval of Gasmire and Cannon, stated :

We are pleased to report very good second-quarter results - a 34 percentincrease in average daily census over second quarter of 2002, a 39 percent increase inrevenues and 60 percent increase in net income . Our margins were 11 .7 percentcompared to 10.1 percent in the second quarter of 2002 .

-24-

All these results I believe continue to show that we are making very goodprogress on our goals . By that I mean our existing programs are growing, we areaggressively expanding into new service areas, and therefore, we continue toleverage our corporate infrastructure across a large number of patients and programs .As you know, approximately 94 percent of our revenue is attributable to Medicare .Each summer the Centers for Medicare and Medicaid Services or CMS as it is knownannounces rate increases . The announcement was made in early July . Hospiceswere provided a 3 .4 percent increase effective October 1, 2003 . However, based onthe information we have now and the growth we are experiencing, we are raising ourbottom-line guidance . Previously we had guided you to a 35 to 40 percent increasein net income for 2003 as compared to 2002 . We are now comfortable with raisingour estimate for our 2003 bottom-line growth to 40 to 43 percent over 2002 results .

58 . Analyst immediately repeated this false information to the market in analysts' reports ,

projecting FY03 and FY04 earnings for Odyssey of $1 .25 and $1 .60, respectively. For example, o n

August 5, 2003, CIBC World Markets issued a report, written by Charles W . Lynch, which stated :

• ODSY reported 2Q :03 EPS of $0 .31, two pennies ahead of our estimate andup 58% y-y . This growth, and the upside to our expectation, was primarilytop-line driven, with patient volumes ahead of our model .

• Based on 2Q : 03 results and increased management guidance, we are raising2003E/04E to $1 .25/$1 .60 from $1 .20/$1 .50 .

• We view our new estimates as a conservative outlook of potential growthover the next two years, given ODSY's patient -volume growth as well as asupportive governmental stance toward Medicare hospice services .

• We continue to view ODSY as an attractive small-cap growth investment andare raising our price target to $45. Reiterate Sector Outperformer rating .

59. Similarly, on August 20, 2003, Stifel, Nicolaus & Company issued a report, writte n

by Chris Sergeant, based on his conversations with Burnham and Cannon du ring Odyssey' s

August 5, 2003 conference call, recommending the purchase of Odyssey stock as a "Buy," an d

noting that "Odyssey is strongly cash flow positive , enjoying a ` self-sustaining growth equation ." '

Stifel, Nicolaus & Company also wrote: "Hospice is a very young and consolidating space - there i s

plenty of green-field and acquisition opportunity out there - and we see continued above averag e

growth at Odyssey for years ahead ."

-25-

60. After these announcements, Odyssey's stock price soared to over $29 per share.

While Odyssey stock traded at artificially inflated prices, defendant Burnham sold 150,500 shares o f

Odyssey stock that he owned, for prices between $30.00 and $32 .56 per share, pocketing $4 . 6

million in unlawful insider trading proceeds . Defendant Gasmire sold 157,416 shares of Odyssey

stock that he owned, for prices between $30 .00 and $30.68 per share, pocketing $7 .5 million in

unlawful insider trading proceeds . And defendant Cannon sold 29,579 shares of Odyssey stock that

he owned, for prices between $28 .90 and $29 .90 per share, pocketing $855,644 in unlawful insider

trading proceeds . Defendants' stock sales were both suspicious in amount and in timing as the y

were large in amount and occurred on the heels of Odyssey's positive earnings announcement ,

reporting strong revenue and earnings for the 2nd quarter of FY03, at prices approaching Odyssey' s

then Class Period high .

61 . The statements in ¶¶53-54, 56- 59 were false and misleading when made . At the time

defendants knew that these financial results were false because Odyssey was violating federa l

Medicare and Medicaid laws by admitting patients who did not qualify for hospice care, billing th e

government for services rendered to hospice patients that were not actually provided, and failing t o

timely discard patients who no longer qualified for hospice treatment under federal Medicare law s

and guidelines, all for the purpose of artificially inflating the Company's publicly reported revenues ,

net income and earnings . Moreover, defendants continued to conceal the fact that the Company was

continuing to submit false claims to the United States for payment under Medicare and that it s

patient admissions, patient retention and billing practices violated applicable federal and state laws .

In addition, when these statements were made, defendants actually knew that Odyssey's expansio n

program was not succeeding and could not be sustained because the Company's expansion activit y

had overwhelmed Odyssey's infrastructure and resources and, as a result, the Company was

experiencing serious problems integrating newly acquired hospice centers, as detailed above .

-26-

62 . As FY03 unfolded, Odyssey's stock price continued to advance to higher levels and

defendants continued to acquire additional hospice care centers on favorable terms . For example, on

September 2, 2003, Odyssey announced a deal to acquire Grace Incorporated ("Grace"), an Omaha ,

Nebraska based hospice program operator, and a second deal to form Odyssey HealthCare of Uta h

by acquiring Heritage Hospice, L.L.C. ("Heritage") based in Utah . Commenting on the Grace an d

Heritage acquisitions, the Company stated :

The Utah hospice program provides care to approximately 280 patients fromSalt Lake City, Ogden and St . George and the surrounding areas . Odyssey, whichoperates in 27 other states, has not previously provided care in Utah .

"Historically, about one-third of Odyssey's annual growth is a result ofacquisitions, and two-thirds is a result of growth in our existing hospice programsand expansion into communities not previously served by the company," notedRichard R. Burnham, chairman and chief executive officer . "We are very pleased tohave the caregivers and staff of Utah's Heritage Hospice join the Odyssey team .They have established a well-respected hospice program, providing compassionateand high-quality care in the major population centers of the state," notedMr. Burnham .

Odyssey's services are provided in patient homes, long-term care facilities,nursing homes or hospitals . The newly acquired healthcare provider will be calledOdyssey HealthCare of Utah .

Separately, the company announced the acquisition of the Omaha, Neb .,hospice program of Grace Incorporated . The acquisition will be merged withOdyssey's current hospice program in Omaha . The Grace hospice program has 35patients .

Including the Utah and Omaha acquisitions, Odyssey has acquired sevenhospice programs in 2003 . The acquired programs had a total of 517 patients at thetime of their purchase .

63 . On September 16, 2003, Burnham appeared on Bloomberg television's "Mornin g

Call" program and, with the approval of Gasmire and Cannon, reaffirmed Odyssey's prior 2003 ne t

income growth stating that the Company expected 2003 net income growth of 40% to 43% ove r

FY02 results . Burnham also confirmed during the program, with Gasmire and Cannon's approval ,

that Odyssey "was comfortable with the First Call Consensus estimate of 83 cents for 2003 ."

-27-

64. After Burnham's appearance on the "Morning Call" program, Odyssey's stock pric e

increased to nearly $35 per share . While Odyssey stock traded at artificially inflated prices ,

defendant Burnham sold 75,000 shares of Odyssey stock that he owned, for prices between $31 .58

and $32 .56 per share, pocketing $2 .4 million in unlawful insider trading proceeds . Defendant

Cannon sold 4,372 shares of Odyssey stock that he owned, for prices between $33 .60 and $34 .80 per

share, pocketing $149,793 in unlawful insider trading proceeds . Defendants' stock sales were both

suspicious in amount and in timing as they were large in amount and occurred on the heels of

Odyssey's positive announcements concerning the Grace and Heritage acquisitions, and Burnham' s

positive statements about the Company's business and FY03 earnings on Bloomberg television's

"Morning Call" program, at prices approaching Odyssey's then Class Period high .

65 . The statements in ¶162-64 were false and misleading when made . At the time

defendants knew that these financial results were false because Odyssey was violating federa l

Medicare and Medicaid laws by admitting patients who did not qualify for hospice care, billing th e

government for services rendered to hospice patients that were not actually provided, and failing t o

timely discard patients who no longer qualified for hospice treatment under federal Medicare law s

and guidelines, all for the purpose of artificially inflating the Company's publicly reported revenues ,

net income and earnings . Moreover, defendants continued to conceal the fact that the Company was

continuing to submit false claims to the United States for payment under Medicare and that its

patient admissions, patient retention and billing practices violated applicable federal and state laws .

In addition, when these statements were made, defendants actually knew that Odyssey's expansio n

program was not succeeding and could not be sustained because the Company's expansion activity

had overwhelmed Odyssey's infrastructure and resources and, as a result , the Company was

experiencing serious problems integrating newly acquired hospice centers, as detailed above .

-28-

3rd Quarter FY03

66. On November 3, 2003, Odyssey announced its 3rd quarter FY03 results, ended

September 30, 2003, repo rting a 45% increase in net income of $7.8 million, or $0.21 per share, on a

40% increase in revenue to $71 .0 million. The Company also announced that its average dail y

census for the 3rd quarter FY03 increased 34% to 6,198 patients, and days of care for the quarte r

increased 34%, to 570,233 . In the Company's earnings release , Burnham , with the approval of

Gasmire and Cannon, attributed the Company's strong performance to the success of its aggressiv e

expansion program, stating :

To date, the company has opened seven start-up programs . During the nine-month period, the company has acquired seven hospices that were servingapproximately 500 patients at the time of their acquisition, including fouracquisitions in the third quarter, as previously announced .

"We are very pleased to repo rt strong growth in revenue and net income" "We have also made excellent progress in expanding into new communitie s

and increasing the number of patients in our existing programs . To continue ourstrong growth, we have accelerated our time frame for new programs and arecurrently working on seven new locations scheduled to open in 2004 . "

67. Following the release of the Company's November 3, 2003 earnings press release ,

securities analysts issued reports on Odyssey which were based on and repeated the fals e

information provided by Odyssey's senior management . For example, on November 5, 2003, S G

Cowen issued a report, written by Kemp Dolliver, in which it recommended the purchase of Odyssey

stock as a "Strong Buy," stating :

Q3 EPS of $0 .21 were essentially in line with consensus and our $0.20E. Odysseyhad announced in September that the month 's average daily census (ADC) wouldexceed 6 ,500. Asa result , revenue of $71 .0MM (+40%) was on target with ADC of6,198 (+34%) below our 6 ,330E, but revenue /day of $125 (+4%) came in above our$123E (+3%) .

The hospice industry's fundamentals are positive with favorable Medicare policy ;roughly 35% market penetration; increasing awareness ; and (for ODSY) a highly-fragmented market . Q3's results were clean without any signs of stress, suggestingour above-consensus 2004E EPS of $1 .11 is achievable . The stock trades at 25x2004E EPS of $1 .11, so we would wait for weakness to add to positions .

-29-

Acquisition Pace Running Ahead Of Our 2003 Thinkin g

Odyssey has completed seven acquisitions this year with ADC of 517, wellahead of the 300 ADC we expected initially this year . The largest, Heritage Hospicein Utah, had ADC of 280 . Management continues to seek acquisitions of many sizes .On the development side, Odyssey has received Medicare certification for seven ofthe eight offices planned for 2003 . . . .

68. Likewise, on November 5, 2003, Jefferies & Company issues a report, written by

Frank G . Morgan , in which it recommended the purchase of Odyssey stock following meetings with

Odyssey senior management (Burnham and Cannon), stating :

ODSY: Solid Third Quarter Results in Line with Consensus

Net patient service revenue increased 40% to $71 .0 million from $50 .7million in 3Q02 . Average daily census for the quarter grew 34%, to 6,198 .Average length of stay increased 14.7 days year over year, to 77 .8 days .After evaluating the wage index factors for Medicare reimbursement in 2004,the company feels confident that it will benefit from a reimbursementincrease of 3 .4% for fiscal 2004 .

Strong revenue growth and same-store maturation resulted in year-over-yearconsolidated EBITDA margin growth of 80 basis points, to 19 .1 % .

We are raising our 2003 EPS estimate, to $0.84 (+47%) from $0.83 . We arealso raising our 2004 EPS estimate, to $1 .09 from $1 .07. Management statedthat it would not give 2004 guidance until the company reports 4Q03 results,but given operating trends, we believe there is good visibility in our estimate .

69. After these announcements, Odyssey's stock continued to trade at artificially inflate d

p rices. During this period, defendant Burnham sold 103 ,269 shares of Odyssey stock that he owned,

for prices between $28 .08 and $31 .06 per share, pocketing $3 million in unlawful insider tradin g

proceeds . Defendant Gasmire sold 50,000 shares of Odyssey stock that he owned, for prices

between $30 .00 and $30.25 per share, pocketing $1 .5 million in unlawful insider trading proceeds .

And defendant Cannon sold 10,304 shares of Odyssey stock that he owned, for prices betwee n

$29.26 and $31 .10 per share, pocketing $306,115 in unlawful insider trading proceeds . Defendants '

stock sales were both suspicious in amount and in timing as they were large in amount and occurre d

-30-

on the heels of Odyssey's positive earnings announcement, reporting strong revenue and earnings fo r

the 3rd quarter of FY03 .

70. The statements in ¶¶66-68 were false and misleading when made . At the time

defendants knew that these financial results were false because Odyssey was violating federa l

Medicare and Medicaid laws by admitting patients who did not qualify for hospice care, billing th e

government for services rendered to hospice patients that were not actually provided, and failing t o

timely discard patients who no longer qualified for hospice treatment under federal Medicare law s

and guidelines, all for the purpose of artificially inflating the Company's publicly reported revenues ,

net income and earnings . Moreover, defendants continued to conceal the fact that the Company wa s

continuing to submit false claims to the United States for payment under Medicare and that its

patient admissions, patient retention and billing practices violated applicable federal and state laws .

In addition, when these statements were made, defendants actually knew that Odyssey's expansio n

program was not succeeding and could not be sustained because the Company's expansion activit y

had overwhelmed Odyssey's infrastructure and resources and, as a result, the Company was

experiencing serious problems integrating newly acquired hospice centers, as detailed above .

71 . As Odyssey's stock price continued to trade at art ificially inflated levels , defendants

continued to acquire other hospice care centers on favorable terms . For example, on November 17 ,

2003, Odyssey announced the acquisition of Hospice Home Care , a hospice provider based in San

Antonio, Texas ("Hospice Home"), and on January 4, 2004, Odyssey announced another deal to

acquire Crown of Texas Hospice, a hospice program then currently serving approximately 40 0

patients and their families in 20 counties in the Texas Panhandle and nine counties surrounding

Conroe, Texas, north of Houston . Commenting on the Hospice Home acquisition, Gasmire, with th e

approval of Burnham and Cannon, stated :

Hospice Home Care is providing care to approximately 100 patients .Odyssey, which provides hospice services in 28 states, including locations

-31-

throughout Texas, will integrate Hospice Home Care into its existing San Antoniohospice program .

The San Antonio acquisition is Odyssey's eighth in 2003 . Including the San Antonioacquisition, the acquired programs had a total of approximately 600 patients at thetime of their purchase .

"We are very pleased to have the caregivers and staff of Hospice Home Carejoin the Odyssey team . . .," noted Mr. Gasmire . "By combining our twoorganizations, we believe we can reach even more patients and families who carebenefit from our services ."

72. Commenting on the Crown of Texas acquisition, defendants Gasmire, with th e

approval of Burnham and Cannon stated :

"Crown of Texas has provided outstanding care to patients and families in theTexas Panhandle and in the counties surrounding Conroe," said David C . Gasmire,president and chief executive officer of Odyssey . "We are pleased to be able tocontinue this strong legacy of care and look forward to being an important part of thehealthcare community in these areas . "

Prior to the acquisition, Odyssey did not have a hospice program in the TexasPanhandle . Odyssey has existing hospice programs along the Texas Gulf Coast,including Houston, however the newly acquired Conroe will continue to be operatedas separate programs .

Odyssey noted that the acquisition is expected to be accretive beginningapproximately mid 2004, following the company's historic pattern of implementingits operating model in newly acquired programs in approximately 90 to 120 days ."While this acquisition is the largest in our history, our focus will remain on organicgrowth," noted Mr. Gasmire .

73 . As a result of these positive announcements , Odyssey's stock price continued to trade

at artificially inflated prices .

4th Quarter and FY03

74. On February 23, 2004, Odyssey announced its year-end FY03 results, ended

December 31, 2003, reporting a 48% increase in net income to $31 .2 million, or $0.84 per share, on

a 41 % increase in revenue to $274 .3 million . In the Company' s earnings release, Gasmire , with the

-32-

approval of Burnham and Cannon, attributed the Company's strong performance to its successfu l

expansion into new communities via start-ups and strategic acquisitions, stating :

For the 2003 fiscal year ended Dec. 31, 2003, net patient service revenuegrew 41 percent to $274.3 million compared to $194 .5 million in 2002 . Net incomein 2003 was $31 .2 million, a 48 percent increase over the $21 .1 million for 2002 .Earnings per diluted share were $0 .84, an increase of 45 percent over the $0 .58 forthe 2002 fiscal year . (Per share information for 2002 has been restated to reflect thecompany's 50 percent stock dividends on Feb . 21 and Aug. 12, 2003 . )

"Our earnings per share for the year exceeded our guidance, and we havemade good progress in expanding into new communities through start-ups andstrategic acquisitions," said David C . Gasmire, president and chief executive officer."The demand for our services remains strong, and we look forward to reaching anever increasing number of patients and their families in 2004 . "

The company noted that it expects its 2004 earnings per share results toreflect a 23 to 25 percent increase over 2003, or $1 .03 to $1 .05 for the year . For thefirst quarter of 2004, the company expects earnings per share of $0.20 to $0.22,compared to $0 .19 for the first quarter of 2003 .

75 . On this news that the Company 's 1st quarter 2004 earnings would be below analysts '

estimates, the Company's stock price declined to $20 .32 per share . However, to maintain Odyssey' s

artificially inflated stock price and to allay investors' concerns that Odyssey's growth had out pace d

the Company's infrastructure, defendants quickly reassured investors and securities analysts tha t

Odyssey's expansion program was still on track and that the Company would continue to gro w

rapidly .

76 . Defendants' scheme succeeded and securities analysts issued favorable reports o n

Odyssey stock. For example, on February 25, 2004, Jefferies & Company issued a report, written b y

Frank G. Morgan, noting that the sell-off of Odyssey stock was "over-done" and increasin g

Odyssey's investment to "Buy," stating :

ODSY: Sell-Off Overdone ; Rating Raised to Buy from Hold

We are raising our rating on shares of Odyssey HealthCare, Inc., to Buy fromHold with a price target of $26. The company reported 4Q03 EPS of $0 .23compared to $0 .19 in 4Q02 . Results were in line with consensus and our

-33-

estimate . . . . In our opinion, yesterday's sell-off in the stock creates an interestingnear-term buying opportunity . Odyssey's fourth quarter results and initial 2004guidance reflect the impact of growth outpacing the company's corporateinfrastructure .

Strong revenue growth of 37.5% was driven by same-store maturation,acquisitions , and de novo development .

77 . Similarly, on February 24, 2004, SG Cowen issues a report, written by Kem p

Dolliver, in which it continued to rate Odyssey stock a "Strong Buy," stating :

• Stay with Strong Buy Rating, But This Stock Will Require Patience .

We expect the stock to drop sharply, discounting this news quickly. Demandacross the industry is solid, so ODSY should continue to post good organic growth .The balance sheet is debt-free and capital needs are minimal .

78. The statements in ¶¶71-72 and 74-77 were false and misleading when made . At the

time defendants knew that these financial results were false because Odyssey was violating federa l

Medicare and Medicaid laws by admitting patients who did not qualify for hospice care, billing th e

government for services rendered to hospice patients that were not actually provided, and failing to

timely discard patients who no longer qualified for hospice treatment under federal Medicare law s

and guidelines, all for the purpose of artificially inflating the Company's publicly reported revenues ,

net income and earnings . Moreover, defendants continued to conceal the fact that the Company was

continuing to submit false claims to the United States for payment under Medicare and that it s

patient admissions, patient retention and billing practices violated applicable federal and state laws .

In addition, when these statements were made, defendants actually knew that Odyssey' s expansio n

program was not succeeding and could not be sustained because the Company's expansion activit y

had overwhelmed Odyssey's infrastructure and resources and, as a result, the Company was