In Re Neustar, Inc. Securities Litigation 14-CV-00885...

72

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 1 of 72 Page ID# 229 UNITED STATES DISTRICT COURT EASTERN DISTRICT OF VIRGINIA ALEXANDRIA DIVISION IN RE NEUSTAR, INC. SECURITIES Case No. 14-CV-00885 JCC TRJ LITIGATION CONSOLIDATED AMENDED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS

Transcript of In Re Neustar, Inc. Securities Litigation 14-CV-00885...

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 1 of 72 Page ID# 229

UNITED STATES DISTRICT COURT EASTERN DISTRICT OF VIRGINIA

ALEXANDRIA DIVISION

IN RE NEUSTAR, INC. SECURITIES Case No. 14-CV-00885 JCC TRJ LITIGATION

CONSOLIDATED AMENDED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 2 of 72 Page ID# 230

TABLE OF CONTENTS

1. NATURE OF THE ACTION ............................................................................. 1

II. JURISDICTION AND VENUE ......................................................................... 5

III. PARTIES ............................................................................................................ 6

A. Lead Plaintiff ............................................................................................. 6

B. Defendants ................................................................................................. 6

C. Relevant Non-Party.................................................................................... 8

IV. FACTUAL BACKGROUND AND SUBSTANTIVE ALLEGATIONS .......... 8

A. Number Portability and Neustar's Longstanding Role as the Sole Local Number Portability Administrator.................................

B. Telcordia Successfully Petitions the FCC to Reintroduce Competition to Number Portability

Administration, Threatening Neustar's Monopoly Profits ........................ 12

C. The NAPM Unexpectedly Extends the Deadline for Competing Bidders to Submit Proposals, Putting

Neustar's Competitive Standing at Significant Risk ................................. 15

D. The NAPM Unexpectedly Delays the Timeline for the Selection Process, Heightening Investor

Concerns About Neustar's Competitive Standing ..................................... 18

E. The NAPM Initiates a Best and Final Offer Process for Neustar and Telcordia to

Submit Their Most Competitive Proposals................................................ 18

F. Defendants, Knowing Neustar Has Been Outbid By Telcordia, Secretly Submit an Unsolicited Revised BAFO and Repeatedly

Ask FoNPAC to Reopen the Bidding Process ........................................... 19

G. Price Was the Determining Factor Separating the Neustar and Telcordia BAFOs, and the Price

Difference Alone Justified Selecting Telcordia......................................... 20

H. Defendant Hook Breaches Protocol and

Appeals Directly to the Chairman of the FCC........................................... 23

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 3 of 72 Page ID# 231

I. Defendants Belatedly Reveal Part of

Their Secret Efforts to Edge Out Telcordia .......................... 25

J. Defendants Continue to Scramble to Avoid

Losing the NPAC Contracts to Telcordia ............................ 25

K. The NANC Unanimously Recommends

That the FCC Select Telcordia as Sole LNPA...................... 28

L. The NANC Recommendation Leads Neustar to

Consider Selling Itself to a Private Equity Firm................... 29

V. DEFENDANTS' MATERIALLY FALSE AND MISLEADING

STATEMENTS AND OMISSIONS OF MATERIAL FACT ...... 30

A. April 18, 2013 "Statement" on

Extension of RFP Submission Deadline ............................... 30

B. May 2, 2013 First Quarter

Press Release and Conference Call....................................... 32

C. July 30, 2013 Second Quarter Conference Call .................... 34

D. October 30, 2013 Third Quarter

Press Release and Conference Call....................................... 36

VI. THE TRUTH BEGINS TO EMERGE .......................................... 38

A. January 29, 2014 Partially Corrective

"Update" and Conference Call ............................................ 38

B. Continued Material Misstatements in the April 16, 2014

First Quarter Press Release and Conference Call ................. 41

C. The NANC's Recommendation of Telcordia Over

Neustar Is Revealed, Fully Correcting the Market ............... 44

VII. ADDITIONAL INDICIA OF SCIENTER .................................... 45

VIII. THE STATUTORY SAFE HARBOR AND BESPEAKS

CAUTION DOCTRINE ARE INAPPLICABLE .......................... 51

IX. LOSS CAUSATION...................................................................... 52

X. CONTROLLING PERSON ALLEGATIONS .............................. 53

XI. CLASS ACTION ALLEGATIONS .............................................. 54

11

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 4 of 72 Page ID# 232

XII. LEAD PLAINTIFF AND CLASS MEMBERS ARE ENTITLED TO A PRESUMPTION OF RELIANCE ........................... 57

XIII. CAUSES OF ACTION ........................................................................... 59

COUNT I Asserted Against Defendant Neustar for Violations of Section 10(b) of the Securities Exchange Act of 1934 and SEC Rule lOb-S Promulgated Thereunder................... 59

COUNT II Asserted Against the Individual Defendants for Violations of Section 10(b) of the Securities Exchange Act of 1934 and SEC Rule lOb-S Promulgated Thereunder................... 62

COUNT III Asserted Against the Individual Defendants for Violations of Section 20(a) of the Securities Exchange Act of 1934 ..... 66

XIV. PRAYER FOR RELIEF ......................................................................... 67

XV. JURY DEMAND .................................................................................... 68

111

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 5 of 72 Page ID# 233

Court-appointed Lead Plaintiff Indiana Public Retirement System ("Lead Plaintiff' or

"INPRS"), by and through its undersigned counsel, alleges the following individually and on

behalf of a class of all persons and entities that purchased or otherwise acquired the publicly

traded securities of Neustar, Inc. ("Neustar" or the "Company") between April 19, 2013 and June

6, 2014, inclusive (the "Class Period" and the "Class," as further defined herein), upon

information and belief, except as to those allegations concerning Lead Plaintiff, which are

alleged upon personal knowledge. Lead Plaintiff's allegations are based upon the investigation

of its counsel, which included a review of reports filed by Neustar with the U.S. Securities and

Exchange Commission ("SEC"); press releases and other public statements issued by Neustar;

documents filed by Neustar, Telcordia Technologies, Inc. d/b/a iconectiv ("Telcordia"), and

others with the Federal Communications Commission ("FCC"); securities analysts' reports about

Neustar; media and news reports related to Neustar; data and other information concerning

Neustar securities; and other publicly available information concerning the Company and the

Individual Defendants (as defined below); as well as discussions with consulting experts. Lead

Plaintiff believes that substantial additional evidentiary support will exist for the allegations set

forth herein after a reasonable opportunity for discovery.

I. NATURE OF THE ACTION

1. This securities class action concerns a high-stakes competition between an

incumbent and a challenger to be selected by the FCC to serve as the next Local Number

Portability Administrator ("LNPA"). Number portability emerged in the late 1990s and enables

telephone customers to retain their phone number in the same location if they switch telephone

service providers. The LNPA manages the Number Portability Administration Center

("NPAC"), a large central data registry that includes essentially all of the wireline and wireless

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 6 of 72 Page ID# 234

telephone numbers in the United States, and allows numbers to be ported from one service

provider to another.

2. Since 1997, when the NPAC was implemented, Neustar has been the sole LNPA

for the United States. Neustar's monopoly over number portability administration has been

increasingly lucrative. In 2013, Neustar generated more than $440 million—nearly half of its

annual revenue—from its NPAC Contracts, and enjoys remarkable profit margins, exceeding 60

percent, on these high technology services. Beginning in 2007, after telecommunications

companies began to voice concerns about the cost and structure of the NPAC Contracts,

Telcordia, a leading competitor of Neustar, successfully petitioned the FCC to conduct the first

competitive bidding process for number portability administration since 1996. The FCC directed

the North American Numbering Council (the "NANC"), the federal advisory committee that

advises the FCC on telephone numbering issues, to make a recommendation to the FCC as to

which bidder to select as the next LNPA starting in July 2015.

3. This case is about Defendants' materially false and misleading statements

regarding Neustar's competitive standing in the selection process and the significant and

increasing risk that the Company, after 17 years as the sole LNPA, would lose the NPAC

Contracts to Telcordia.

4. Given the Company's sole and incumbent status and the importance and

complexity of NPAC administration, Defendants initially believed that the FCC would once

again renew Neustar's NPAC Contracts. Neustar, in fact, nearly avoided having to compete for

the NPAC Contracts at all, after Telcordia apparently failed to meet the submission requirements

by the April 2013 deadline. The deadline was subsequently extended by two weeks, however,

after Neustar submitted its confidential proposal, to allow competing bidders to participate.

2

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 7 of 72 Page ID# 235

Defendants complained bitterly to the FCC, asserting that the deadline extension was seriously

prejudicial to Neustar by, among other things, perversely favoring that bidders that could not

meet the deadline and raising the risk that Neustar's bid was leaked to competing bidders.

5. While Defendants were crying foul to the FCC, however, they were repeatedly

assuring investors that Neustar was well-positioned to win renewal of the NPAC Contracts and

that the Company's long track record and high quality of service set it apart from its competitors.

And as Neustar's competitive standing worsened during the Class Period, Defendants continued

to reassure investors of their confidence in their proposal when, in fact, they were scrambling

behind the scenes to stay competitive and beat Telcordia.

6. In August 2013, after the FCC's designees reviewed Neustar's and Telcordia's

initial proposals, they were asked to submit their most competitive best and final offers

("BAFO5"). Both did so in September. Neustar's BAFO, however, did not offer the Company's

most competitive price for the NPAC Contracts, and instead reflected Defendants' effort to

preserve the large premium associated with Neustar's monopoly and incumbent status. And, as

Defendants soon came to learn, their effort to perpetuate their monopoly profits resulted in

submitting a BAFO that was priced so much higher than Telcordia's BAFO that it seriously

jeopardized Neustar's chances. According to reports, Telcordia was "now likely to win the

LNPA contract outright because its bid [BAFO] came in significantly lower than Neustar's."

Indeed, "the gap between bids [was] so significant as to make it very difficult for Neustar to win

the contract."

Defendants, in fact, became so certain they were going to lose their coveted

NPAC Contracts that only a month later, in an underhanded effort to edge out Telcordia, Neustar

secretly submitted an unsolicited second BAFO (the "October Revised BAFO"), together with a

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 8 of 72 Page ID# 236

request that bidding be reopened. The October Revised BAFO reportedly was "very different"

than Neustar's initial BAFO, and was carefully priced "to come in 'just under' Telcordia's bid."

Plainly, and as reported, Neustar improperly received "detailed knowledge" about Telcordia's

confidential BAFO and tried to capitalize on it outside the approved bidding process. None of

this, however, was disclosed during the Company's quarterly earnings call with securities

analysts at the end of October, only nine days later.

8. In November 2013, after not receiving a sufficiently prompt response to its

October submission, Defendants urged for a second time, again in secret, that their October

Revised BAFO be considered in place of the initial BAFO. And in January 2014, amid growing

concerns at the Company, Neustar's CEO broke protocol and called the Chairman of the FCC to

appeal to him directly to have the October Revised BAFO considered.

9. This conduct, which crossed the line with respect to the selection process, was

entirely inconsistent with Defendants' positive reassurances to investors during the Class Period

regarding Neustar's competitive standing and likelihood of winning the contract renewal.

10. Matters worsened for Neustar. The day after the CEO reached out to the FCC

Chairman, Defendants were informed that the October Revised BAFO was rejected—"returned

unopened" in FCC parlance. Defendants recognized that they could no longer hide their cynical

machinations from investors, and on January 29, 2014, Neustar stunned the market by

announcing that it had submitted a BAFO in September, that in October and again in November

it had submitted a revised BAFO and asked that bidding be reopened, and that the revised BAFO

would not be considered. Neustar common stock fell nearly 20 percent.

11. By this point, Defendants saw their sinecure and half the Company's revenues

slipping away, and knew that they would lose the NPAC Contracts unless they could

4

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 9 of 72 Page ID# 237

fundamentally change the dynamics of the selection process, including by convincing the FCC

itself to intervene and direct that the October Revised BAFO be treated as Neustar's operative

proposal. None of this was disclosed on January 29, however, as Defendants put a brave face on

their chances and reiterated their confidence that Neustar ultimately would be selected.

12. In February and March 2014, Neustar made a flurry of efforts before the FCC to

salvage its position. This campaign culminated in Neustar's CEO personally offering a $50

million credit against the Company's fees on the NPAC Contracts if the NANC would delay its

recommendation decision by several months, during which time Neustar naturally would stay on

as sole LNPA.

13. Defendants continued to mislead investors as to Neustar's competitive standing

into April 2014, but its last-ditch efforts to change the game were failing. On June 6, 2014, it

was revealed that the NANC had unanimously recommended to the FCC that Telcordia replace

Neustar as the next LNPA.

14. The FCC and Neustar confirmed the news, and Neustar common stock lost

another 8 percent of its value. By the end of the Class Period, Neustar stock had lost more than

42 percent of its value from the start of the Class Period, and more than 56 percent of its value

from its Class Period high, costing Lead Plaintiff and members of the Class hundreds of millions

of dollars in damages.

II. JURISDICTION AND VENUE

15. The claims asserted herein arise under Sections 10(b) and 20(a) of the Securities

Exchange Act of 1934 (the "Exchange Act"), 15 U.S.C. §§ 78j(b) and 78t(a), and the rules and

regulations promulgated thereunder by the SEC, including Rule lOb-5, 17 C.F.R. § 240. lOb-S.

16. This Court has jurisdiction over the subject matter of this action pursuant to

Section 27 of the Exchange Act, 15 U.S.C. § 78aa, and 28 U.S.C. § 1331.

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 10 of 72 PagelD# 238

17. Venue is proper in this District pursuant to Section 27 of the Exchange Act, 15

U.S.C. § 78aa, and 28 U.S.C. § 1391(b). The Company maintains its principal place of business

in this District and many of the acts that constitute the violations of law complained of herein,

including dissemination of materially false and misleading information to the investing public,

occurred in or were issued from this District.

18. In connection with the acts alleged in this Complaint, Neustar and the Individual

Defendants, directly or indirectly, used the means and instrumentalities of interstate commerce,

including, but not limited to, the mails, interstate telephone communications, and the facilities of

the national securities markets.

III. PARTIES

A. Lead Plaintiff

19. Lead Plaintiff Indiana Public Retirement System ("INPRS") is a pension system

of the State of Indiana. INPRS is responsible for the investment of approximately $30 billion in

net assets in multiple defined benefit and defined contribution retirement plans. INPRS presently

serves the needs of approximately 450,000 members and retirees representing more than 1,100

employers including public universities, school corporations, municipalities and state agencies.

20. INPRS purchased shares of Neustar common stock during the Class Period, as set

forth in the certification previously filed with the Court, and suffered damages as a result of the

federal securities law violations alleged herein. By Order dated October 7, 2014, the Court

appointed INPRS as the Lead Plaintiff in this action.

B. Defendants

21. Defendant Neustar, Inc. ("Neustar" or the "Company") is a communications data

processing company that provides directory and analytic services to telecommunications

companies and internet service providers. Neustar describes itself as "a neutral and trusted

6

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 11 of 72 PagelD# 239

provider of real-time information services and analytics, using authoritative, hard-to-replicate

datasets and proprietary analytics to help our clients promote and protect their businesses."

Neustar was incorporated in Delaware in 1998 and maintains its principal executive offices at

21575 Ridgetop Circle, Sterling, Virginia 20166. Neustar's common stock trades under the

ticker symbol "NSR" on the New York Stock Exchange ("NYSE"), which is an efficient market.

22. Defendant Lisa A. Hook ("Hook") is President and Chief Executive Officer of

Neustar and a member of the Company's Board of Directors. Hook has served as President since

joining Neustar in January 2008, as CEO since October 2010, and as a director since November

2010. As President and CEO, Hood is an Executive Officer of the Company.

23. Defendant Paul S. Lalljie ("Lalljie") has served as Senior Vice President and

Chief Financial Officer of Neustar since June 2009, and is an Executive Officer of the Company.

Lalljie served as Senior Vice President, Interim CFO and Treasurer from January 2009 to June

2009, and as Vice President, Financial Planning & Analysis and Treasurer from December 2006

to January 2009. From 2000 through December 2006, Lalljie served in a variety of roles in

corporate finance at the Company, including accounting, financial planning and analysis,

treasury and investor relations.

24. Defendant Steven J. Edwards ("Edwards") has served as Senior Vice President,

Data Solutions since October 2013, and is an Executive Officer of the Company. Edwards

served as Senior Vice President, Carrier Services from 2011 until October 2013. Prior to

becoming Senior Vice President, Carrier Services, Edwards served in a variety of Carrier

Services roles at Neustar from August 2008 through August 2011.

7

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 12 of 72 PagelD# 240

25. Defendants Hook, Lalijie, and Edwards are referred to herein collectively as the

"Individual Defendants." Defendant Neustar and the Individual Defendants are referred to

herein together as "Defendants."

C. Relevant Non-Party

26. Telcordia Technologies, Inc. d/b/a iconectiv ("Telcordia"), based in Piscataway,

New Jersey, is a world leader in number portability administration and provides services in 19

countries. Formerly Bell Communications Research, Inc. or Bellcore, Telcordia was the

telecommunication research and development company created as part of the 1982 break-up of

AT&T. In 2012, Telcordia was acquired by telecommunications giant Ericsson. In February

2013, Ericsson announced that its interconnection business, known previously as Telcordia

Interconnection Solutions, had been renamed iconectiv. The iconectiv unit covers such areas as

number portability, device theft and counterfeit prevention, information services, numbering and

addressing, mobile messaging and spectrum management.

IV. FACTUAL BACKGROUND AND SUBSTANTIVE ALLEGATIONS

A. Number Portability and Neustar's Longstanding Role as the Sole Local Number Portability Administrator

27. Local number portability ("LNP"), also known as number portability and number

porting, enables consumers to keep their telephone number when switching from one

telecommunications service provider to another. Before LNP was introduced, changing service

providers meant consumers had to get a new telephone number. Number portability enables

consumers to retain the same telephone number when changing service providers.

28. LNP was a revolutionary idea when it was first considered in the mid-1990s, and

was mandated in the Telecommunications Act of 1996. Congress and the FCC recognized that

successful implementation of LNP would foster competition in the telephone business, which

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 13 of 72 PagelD# 241

was a key goal of the Telecommunications Act. Number portability originally was mandated

only for wireline services. Wireless number portability was implemented in 2004.

29. The North American Numbering Council ("NANC") is a federal advisory

committee established by the FCC in October 1995 to advise the agency on telephone numbering

issues and to make recommendations that foster efficient and impartial administration of the

North American Numbering Plan ("NANP"). The NANP is the telephone numbering plan for

the United States and its territories, Canada, Bermuda, and 17 Caribbean nations. The NANC's

current membership represents a broad cross-section of the U.S. telecommunications industry,

with representatives from local exchange carriers, interexchange carriers, wireless providers,

manufacturers, state regulators, consumer interests, and telecommunications industry

associations. The NANC's 29 voting members presently include several state public utility

commissioners, telecommunications companies like AT&T, Verizon, Vonage, Sprint and T-

Mobile, and industry and consumer associations.

30. In 1997, the FCC adopted the NANC's recommendation that there should be

seven regionally deployed number portability databases, one for each of the original Regional

Bell Operating Company ("RBOC") regions, 1 and "multiple database administrators to permit

competition in both the initial and future competitive bidding and selection processes." The

industry eventually agreed on an industry-operated limited liability structure approved by the

FCC for oversight, management, and contracting with potential database administrators.

31. Originally, eight regional limited liability corporations ("LLC5") were formed by

the telephone companies to represent them in contracting with database administrators, one LLC

The seven independent RBOCs (AmeriTech, Bell Atlantic, BellSouth, NYNEX, Pacific Telesis, Southwestern Bell, and US West), also known as "Baby Bells," were formed in 1984 as a result of the divestiture of AT&T's Bell Operating Companies that had provided local telephone service in the United States up to that point.

9

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 14 of 72 PagelD# 242

for each of the original RBOC regions and one for Canada. After an open competition,

Lockheed-Martin Information Management Services ("Lockheed-Martin") and Perot Systems

were selected as the initial database administrators. Each was granted a five-year contract by the

LLCs to provide services until 2003. Perot Systems dropped out when its service could not be

ready on time, however, and the LLCs that had contracted with Perot Systems signed contracts

with Lockheed-Martin.

32. In 1999, the seven U.S. LLCs merged into a single private-sector entity, the North

American Portability Management LLC (the "NAPM"), which represents all of the

telecommunications service providers in the United States. In November 1999, because of

concerns about neutrality, Lockheed-Martin was spun off from the parent Lockheed-Martin

corporation and renamed Neustar.

33. Since 1997, through its contracts with the NAPM or predecessor LLCs ("NPAC

Contracts"), Neustar has served as the sole Local Number Portability Administrator ("LNPA")

for the United States. In its role as LNPA, Neustar manages the Number Portability

Administration Center ("NPAC"). NPAC, implemented in 1997, consists of the eight regional

U.S. and Canadian number portability databases and is the world's largest number portability

registry. NPAC manages more than 500 million wireline and wireless telephone numbers,

enables approximately 4,800 telecommunications carriers to route billions of phone calls and text

messages daily, and allows customers to transfer their phone numbers from one carrier to another

(collectively, "NPAC Services").

34. The FCC has plenary authority over the administration of number portability (and

indeed all issues relating to telephone numbers) in the United States, but is not itself a party to

10

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 15 of 72 PagelD# 243

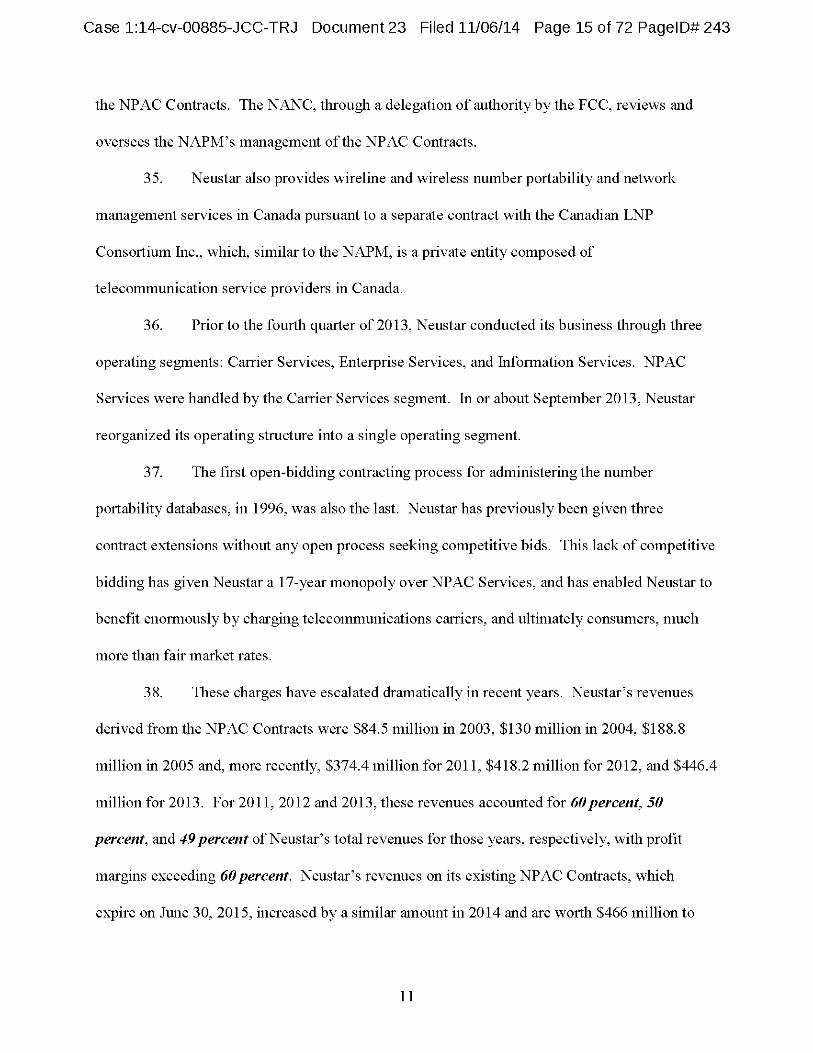

the NPAC Contracts. The NANC, through a delegation of authority by the FCC, reviews and

oversees the NAPM's management of the NPAC Contracts.

35. Neustar also provides wireline and wireless number portability and network

management services in Canada pursuant to a separate contract with the Canadian LNP

Consortium Inc., which, similar to the NAPM, is a private entity composed of

telecommunication service providers in Canada.

36. Prior to the fourth quarter of 2013, Neustar conducted its business through three

operating segments: Carrier Services, Enterprise Services, and Information Services. NPAC

Services were handled by the Carrier Services segment. In or about September 2013, Neustar

reorganized its operating structure into a single operating segment.

37. The first open-bidding contracting process for administering the number

portability databases, in 1996, was also the last. Neustar has previously been given three

contract extensions without any open process seeking competitive bids. This lack of competitive

bidding has given Neustar a 17-year monopoly over NPAC Services, and has enabled Neustar to

benefit enormously by charging telecommunications carriers, and ultimately consumers, much

more than fair market rates.

38. These charges have escalated dramatically in recent years. Neustar's revenues

derived from the NPAC Contracts were $84.5 million in 2003, $130 million in 2004, $188.8

million in 2005 and, more recently, $374.4 million for 2011, $418.2 million for 2012, and $446.4

million for 2013. For 2011, 2012 and 2013, these revenues accounted for 60 percent, SO

percent, and 49 percent of Neustar's total revenues for those years, respectively, with profit

margins exceeding 60 percent. Neustar's revenues on its existing NPAC Contracts, which

expire on June 30, 2015, increased by a similar amount in 2014 and are worth $466 million to

11

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 16 of 72 PagelD# 244

Neustar—nearly half a billion dollars for one year of services, and again expected to constitute

approximately half of the Company's total revenue. Neustar has realized more than $3 billion in

total revenue from its NPAC Contracts since it began serving as sole LNPA in 1997. Telcordia

has estimated that, over the course of the NPAC Contracts, telecommunications carriers and

consumers have paid Neustar more than $2 billion in additional fees owing to the absence of a

competitive bidding process.

39. Accordingly, the importance to Neustar's business of the NPAC Contracts and its

position as sole LNPA cannot be overstated. As Neustar acknowledged in its Form 10-K Annual

Report for 2013, filed with the SEC on February 28, 2014:

The revenue we receive under our seven contracts with North American Portability Management LLC represents, in the aggregate, a substantial portion of our overall revenue. These contracts are not exclusive and could be terminated or modified in ways unfavorable to us. These contracts are due to expire in June 2015 and are currently subject to a competitive proposal process. If we are not selected to continue to provide these services on the same terms and conditions, or at all, our business, prospects, financial condition and results of operations will be materially adversely affected . 2

40. Indeed, Neustar, faced with the NANC's adverse recommendation to the FCC and

the likely loss of the NPAC Contracts, has recently begun to explore selling itself in a going-

private transaction.

B. Telcordia Successfully Petitions the FCC to Reintroduce Competition to Number Portability Administration, Threateniiw Neustar' s Monopoly Profits

41. Alarmed by the escalating costs of the NPAC Contracts, which they ultimately

bear themselves, and Neustar's entrenched position, telecommunications companies began to

express concerns to the FCC about the cost and structure of the NPAC Contracts. In June 2007,

2 Throughout this Complaint, emphases in quotations are added.

12

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 17 of 72 PagelD# 245

Telcordia petitioned the FCC to direct the NAPM to conduct a competitive bidding process for

NPAC Services. The FCC took no action.

42. Two years later, in June 2009, Telcordia filed another petition with the FCC to

abrogate the then-existing NPAC Contracts and initiate a government-managed procurement

process for the selection of the next LNPA. In this petition, Telcordia reminded the FCC of

President Obama's March 4, 2009 Memorandum for the Heads ofExecutive Departments and

Agencies, Subject: Government Contracting, which warned that "Feixcessive reliance by

executive agencies on sole-source contracts . . . creates a risk that taxpayer funds will be spent on

contracts that are wasteful, inefficient, subject to misuse, or otherwise not well designed to serve

the needs of the Federal Government or the interests of the American taxpayer." This

Memorandum, as cited by Telcordia, further declared that "executive agencies shall not engage

in noncompetitive contracts except in those circumstances where their use can be fully justified

and where appropriate safeguards have been put in place to protect the taxpayer."

43. The FCC listened. On September 23, 2010, the FCC's Wireline Competition

Bureau ("WCB") issued a Public Notice announcing that the NAPM would be developing a

Request for Proposal ("RFP") for local number portability database platforms and services, and

stating that the NAPM would issue a Request for Information later in 2010 to begin pre-

qualifying potential vendors. The Public Notice made clear that the FCC was encouraging "full

competition" in the selection process.

44. On March 8, 2011, the FCC issued an Order and Request for Comment

announcing that the WCB was taking four actions in furtherance of the selection of the next

LNPA. First, the WCB delegated authority to the NANC, working in consultation with the

NAPM, to implement a process for selecting the next LNPA. Second, the WCB sought comment

13

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 18 of 72 PagelD# 246

on the specific process that the NANC and NAPM would use. Third, the WCB directed the

NANC to recommend to the FCC one or more independent, non-governmental entities to serve

as the next LNPA. Fourth, the WCB outlined its own role in overseeing the LNPA selection

process.

45. On May 16, 2011, after receiving comments from various parties including

Neustar and Telcordia, the FCC issued a further Order detailing the procedures the NANC and

NAPM must follow in the LNPA selection process, and outlining the WCB's role in overseeing

that process.

46. On August 13, 2012, the FCC issued a Public Notice seeking comment on the

proposed RFP procurement documents.

47. On February 5, 2013, after receiving comments from various parties including

Neustar and Telcordia, the FCC issued a Public Notice releasing the final Request for Proposal

for LNP database platforms and services in the United States, developed by the NAPM and

termed the "2015 LNPA RFP," and put the LNPA contracts up for public bid for the first time in

17 years. The deadline to submit proposals was April 5, 2013.

48. Securities analysts expected that Neustar would win renewal of the NPAC

Contracts and remain the sole LNPA. William Blair & Co. wrote on February 6, 2013 that "[w]e

continue to believe that NeuStar remains the heavy favorite as the incumbent vendor for the

NPAC service in the United States and based on the company's neutral standing (a key criteria,

as we have stated in prior notes), as well as the company's capability and support ratings. We

expect competitor Telcordia to be a bidder on the contract, but believe neutrality concerns

regarding Telcordia's parent company Ericsson could lead NeuStar to hold a significant

advantage." RBC Capital Markets wrote the same day that "we continue to see

14

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 19 of 72 PagelD# 247

Telcordia/Ericsson as the most natural contender given its international experience, though it

does not have similar credentials to support NPAC-like scale and reliability as NeuStar has," and

concluded that "NeuStar remains the front runner given its incumbency and strong track record;

and although pricing/terms are yet to be determined, impact may be lower than prior rounds on

possible cost savings." Oppenheimer & Co. wrote that Neustar "remains well positioned in the

long term given its monopolistic presence in number management. With its highly predictable

business model driven by 90% recurring revenues, we believe FY13 looks positive."

C. The NAPM Unexpectedly Extends the Deadline for Competing Bidders to Submit Proposals, Putting Neustar's Competitive Standing at Siuificant Risk

49. On April 5, 2013, Neustar announced that it timely submitted its proposal to the

NAPM in response to the 2015 LNPA RFP. Consistent with governing procedure, the proposal

was submitted confidentially and remained nonpublic until a public version with pricing and

other information redacted was filed with the FCC after the Class Period.

50. On April 17, 2013, the NAPM unexpectedly announced that, with the approval of

the FCC, it was extending the deadline for the submission of proposals to April 22, 2013. The

NAPM stated that the extension was "[fln order to promote competition and ensure that all

potential offerors have a common understanding of proposal submission requirements and an

adequate opportunity to compete." This meant that Neustar was the sole, unchallenged bidder as

of the April 5 deadline, the 60-day period to submit proposals had made it difficult for non-

incumbents to submit competing bids, and the NAPM wanted to enable such non-incumbents to

participate.

51. From April 17, 2013 on, Defendants knew or recklessly disregarded that the

extension of the RFP submission deadline seriously prejudiced Neustar's competitive standing

and significantly increased the risk that Neustar would be replaced by Telcordia as LNPA, and

15

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 20 of 72 PagelD# 248

that the Company's revenue and profits would be decimated as a result. In particular,

Defendants knew or recklessly disregarded that Neustar's pricing reflected its monopolistic and

incumbent position, that it was possible for the LNPA to earn a reasonable profit at significantly

lower prices, and that the extension of the submission deadline permitted Telcordia or other

potential competitors to structure a bid that was priced significantly lower than Neustar's

proposal. Defendants misrepresented and failed to disclose to the investing public what they

knew or recklessly disregarded as to the significantly enhanced nature of these risks.

52. Telcordia submitted its proposal on or about April 22, 2013. Like Neustar's bid,

and in accordance with governing procedure, Telcordia submitted its proposal confidentially and

it remained nonpublic until a public version with pricing and other information redacted was

filed with the FCC after the Class Period. No other bidders came forward.

53. Defendants knew long before April 17, 2013 that Telcordia, a significant player in

number portability administration, would bid for the NPAC Contracts. It was Telcordia that had

originally petitioned the FCC to put the NPAC Contracts up for public bid, and Telcordia,

together with Neustar, was involved in the pre-bid negotiations regarding the protocols for the

selection process and the language and requirements of the RFP procurement documents. In its

public comments on those RFP documents, filed in September 2012, Telcordia confirmed that it

"looks forward to competing in the upcoming procurement for NPAC Administrators."

54. Moreover, Neustar was closely monitoring Telcordia's activities in and around

the bid submission deadline and indeed throughout the RFP process. Neustar asserted in an

August 2014 FCC filing that on April 5, 2013, the original submission deadline, a Telcordia

employee posted on social media: "I'm exhausted and still have to write the Exec Summary for

this 85 page document. Coffee is failing. Been here 66 straight hours now. . .

16

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 21 of 72 PagelD# 249

55. Defendants were deeply concerned about the impact of the deadline extension on

the fairness of the bidding process and the Company's prospects to continue as the LNPA. On

April 24, 2013, Neustar filed a letter with the FCC strenuously objecting to the extension of the

submission deadline. Neustar stated that extending the deadline after the Company submitted its

proposal "perversely favorFedi bidders unable to meet the deadline," and "raises the risk that

aspects of its confidential bid have been disclosed to other bidders prior to the extended deadline,

including potentially through inadvertent disclosure, which would seriously prejudice Neustar."

The Company reminded the FCC and NAPM that "[flhe RFP process is confidential, and the

disclosure of any aspect of Neustar's proposal . . . would violate the terms of the RFP and give

rise to potentially serious harm to Neustar." Neustar observed that such disclosure would

constitute "a federal crime," and reiterated that "the deadline extension increases the risk that

bidders would have received some sort of feedback on their failed initial submission prior to the

extended deadline—to the prejudice of Neustar and any other bidders who met the deadline."

56. Neustar complained further that the decision to extend the deadline "gives rise to

concerns about the ability of one or more bidders to obtain favorable action based on undisclosed

communications with the NAPM or with regulators," and demanded "an explanation for this

extraordinary departure" from established procedure. Neustar concluded that the extension

"must shake the confidence of those who are depending on NAPM and the [FCC] to run a

process that ensures even-handed competition, not special accommodations for favored private

interests."

57. Neither the FCC nor the NAPM responded directly to the April 24, 2013 letter or

gave an explanation for extending the submission deadline.

17

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 22 of 72 PagelD# 250

D. The NAPM Unexpectedly Delays the Timeline for the Selection Process, Heightening Investor Concerns About Neustar's Competitive Standing

58. Then, on July 23, 2013, the NAPM delayed the timeline for FCC selection of the

next LNPA by four months, from September 20, 2013 to January 20, 2014. The NAPM gave no

explanation for the extension.

59. This delay heightened investors' concerns that Neustar was facing formidable and

lower-priced competition in the RFP. J.P. Morgan stated in an analyst report the same day that

"[t]his is the first time the contract is being put out for bid, and so the additional extension begs

questions about if/why there is more intense consideration on important topics like pricing and

competition."

E. The NAPM Initiates a Best and Final Offer Process for Neustar and Telcordia to Submit Their Most Competitive Proposals

60. The NAPM apparently was unsatisfied with Neustar's confidential proposal. On

August 15, 2013, the NAPM, acting through its advisory Future of the NPAC Subcommittee

("F0NPAC"), issued a Best and Final Offer ("BAFO") process for vendors to submit updated

and more competitive proposals.

61. Neustar and Telcordia each submitted confidential BAFOs on or about September

18, 2013, the deadline set by FoNPAC. As with their initial proposals, Neustar's and Telcordia's

September BAFOs each remained nonpublic until a public version with pricing and other

information redacted was filed with the FCC after the Class Period.

62. Unbeknownst to investors, Neustar's BAFO and initial proposal did not offer the

Company's most competitive price for the NPAC Contracts, and instead reflected Defendants'

effort to preserve the large premium associated with the Company's monopoly and incumbent

status. And, as they came to learn, Defendants' effort to perpetuate their monopoly profits

18

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 23 of 72 PagelD# 251

resulted in submitting a BAFO that was priced so much higher than Telcordia's BAFO that it

seriously jeopardized Neustar's chances of being selected as the next LNPA.

F. Defendants, Knowing Neustar Has Been Outbid By Telcordia, Secretly Submit an Unsolicited Revised BAFO and Repeatedly Ask FoNPAC to Reopen the Biddiiw Process

63. Defendants became so certain that they were going to lose the coveted NPAC

Contracts that on October 21, 2013, in an attempt to underbid Telcordia, Neustar secretly

submitted an unsolicited, significantly reduced BAFO (the "October Revised BAFO") to

FoNPAC together with a request that FoNPAC entertain a further round of bids. This was only a

month after Neustar submitted its September BAFO in response to FoNPAC's invitation.

64. Defendants' unilateral submission of the October Revised BAFO was not a shot

in the dark or guesswork. Defendants knew exactly what price to offer in their October Revised

BAFO in order to underbid Telcordia, while not offering too low a price and potentially leaving

money on the table. As reported by The Capitol Forum on March 19, 2014, Telcordia, according

to "[a] source close to the Local Number Portability Administrator (LNPA) selection process,"

was "now likely to win the LNPA contract outright because its bid [BAFO] came in

significantly lower than Neustar's." The source added, in fact, that "the gap between bids is so

significant as to make it very diffi cult for Neustar to win the contract." 3

65. According to the same source, as reported further by The Capitol Forum on

March 26, 2014:

The Capitol Forum is a highly regarded subscription news service that provides comprehensive news coverage of competition policy as well as in-depth market and political analysis of specific transactions and investigations. The Capitol Forum delivers its news reports to subscribers by e-mail. The Capitol Forum's e-mail distribution list for its news reports numbered approximately 500 readers as of March 2014. Because subscribers generally are permitted to designate multiple individual users to receive the reports, the number of subscribers as of March 2014 likely was fewer than 500. Subscriptions cost $15,000 annually.

19

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 24 of 72 PagelD# 252

[A]fter the conclusion of the BAFO (which was issued August 16, 2013), Telcordia had outbid Neustar. In October 2013, Neustar then submitted a request for another round of BAFO bids, along with another, lower BAFO bid, to which NAPM did not respond. Neustar 's unsolicited second BAFO was very different from its initial BAFO, and was low enough to come in "just under" Telcordia's bid. According to the source, there is awareness within the agency that this is how the rounds of bidding occurred and staff are more skeptical of Neustar's actions as a result. Neustar 's apparent detailed knowledge of Telcordia 's bid, according to our source, could complicate Neustar's legal challenge.

66. Thus, there was a "significant gap" separating Neustar's and Telcordia's

respective September BAFOs, Neustar's unilateral October Revised BAFO was "very different"

than its September BAFO, and it was low enough that it came in "just under" Telcordia's

BAFO. Defendants could not conceivably have priced their October Revised BAFO to come in

just under Telcordia's September BAFO without "detailed knowledge of Tel cordia's bid'

knowledge Defendants were not entitled to possess under the RFP protocols into which they had

had substantial input.

67. Defendants' doubts regarding their chances of winning the renewed contract

continued to grow. On November 4, 2013, after not receiving a sufficiently prompt response

from FoNPAC, Defendants secretly urged FoNPAC for a second time to re-open the bidding

process and submitted an additional copy of their October Revised BAFO.

G. Price Was the Determining Factor Separating the Neustar and Telcordia BAFOs, and the Price Difference Alone Justified Selectiiw Telcordia

68. Price, and not the myriad technical and management criteria also at issue, was

indeed the determining factor separating the Neustar and Telcordia proposals. The RFP

procurement documents advised vendors that "[t]he Technical and Management criteria when

combined are significantly more important than the Cost criterion alone," but made clear that

20

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 25 of 72 PagelD# 253

"[iif Respondents' Technical and Management merits are not significantly disparate, the Cost

may become determinative." Telcordia argued in public comments filed with the FCC on July

25, 2014 that "Loin the issue of price . . . it was no contest," and characterized the difference in

price between its and Neustar's BAFOs as "astounding." Neustar's public comments filed the

same day were consistent with these assertions, arguing instead that the NANC's

recommendation of Telcordia over Neustar "Flout[ed] the RFP by Largely Ignoring Technical

and Management Criteria in Favor of Price."

69. The NAPM, in its own comments filed with the FCC in August 2014, confirmed

that pricing was the distinguishing and deciding factor:

[T]he content of the NANC Recommendation itself reflects the fact that the NAPM LLC found, and the SWG [Selection Working Group within the NANC] and NANC unanimously agreed, that both bidders met the technical qualifications and are equally capable of serving as the LNPA for each of the seven regional databases. And to be clear, the NAPM LLC thoroughly analyzed, debated, and scored bidders with respect to all relevant capabilities - including their ability to satisfy all national security, public safety, and other law enforcement requirements. The actual scoring of the bidders for these and all non-price points was very similar.

The NAPM LLC's evaluation process was extensive and fully vetted by all interested parties. But at the end of that process the only significant difference in scoring between the bidders was with respect to pricing which - in light of the bidders' parity on the other criteria - was determinative even under the weighted scoring formula. Consequently, the NANC was able to compile a concise report that focused on the factors that directly contributed to the recommendation of [Telcordia] over Neustar. [Footnotes omitted]

70. Although Neustar's and Telcordia's September BAFOs were submitted

confidentially, and pricing information is redacted from the public versions filed with the FCC,

certain information in post-Class Period FCC filings allows an estimation of the approximate

amounts of the competing bids. In particular, the public version of Neustar's September BAFO

21

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 26 of 72 PagelD# 254

includes a section titled "Improved Pricing Terms" which states that its proposal "Felxtends year-

one savings to [redacted] reducing 2016 industry fees to pre-2012 levels." The term "pre-2012

levels" suggests that annual industry fees to Neustar would have been approximately $385-$410

million, with the final price determined after deduction of certain unspecified incentive credits

and rebates also noted in the September BAFO. Because Neustar has disclosed that its revenue

from the NPAC Contracts in 2011 was $374.4 million, the final price of Neustar's September

BAFO is likely in the range of $374-$385 million. This is in comparison to the $466 million

Neustar will earn from the NPAC Contracts in 2014.

71. CTIA—The Wireless Association and the United States Telecom Association

(together, "CTIAIUSTe1ecom") are telecommunications industry associations that are voting

members of the NANC. In comments filed jointly with the FCC in July and August 2014,

CTIAIUSTe1ecom observed that Neustar's current LNPA contract includes a price escalation

clause of 6.5 percent above a base amount of more than $440 million, meaning that any

extension of the current contract beyond its June 30, 2015 expiration will automatically trigger

that clause, bringing a windfall to Neustar of approximately $40 million per month.

CTIAIUSTe1ecom observed further that every day of delay in implementing a new contract

beyond July 1, 2015 would add more than $1 million in charges to telecommunications carriers

and ultimately their customers. Neustar has not publicly contradicted these assertions.

72. In other words, according to CTIA/USTelecom's review of the confidential

September BAFOs, having Neustar continue as LNPA on and after July 1, 2015 under an

extension to its current contract, versus having Telcordia take over as LNPA on that date under a

new contract priced consistent with its September BAFO, will cost an extra $1 million a day. if

extending Neustar's current contract will result in fees of approximately $40 million a month, or

22

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 27 of 72 PagelD# 255

approximately $1,333,333 a day, and the selection of Telcordia would save $1 million a day,

then Telcordia's fees under its September BAFO would be approximately $333,333 a day, or

approximately $121.7 million a year.

73. This $121.7 million estimate for Telcordia's BAFO is 67percent less than $375

million, the low end of the range of Neustar's September BAFO as estimated above. This very

large difference is consistent with The Capitol Forum's reports and the public comments of

Telcordia, Neustar, and the NAPM as alleged above.

H. Defendant Hook Breaches Protocol and Appeals Directly to the Chairman of the FCC

74. Defendants' doubts that the Company would be awarded the new NPAC

Contracts became so severe in and after November 2013 that on January 21, 2014, Defendant

Hook called Tom Wheeler, Chairman of the FCC. Hook called Chairman Wheeler to urge that

Neustar's October Revised BAFO be considered. This call followed a letter Neustar delivered

privately to the FCC on January 15, 2014, in which Neustar complained that FoNPAC should

consider its unsolicited October Revised BAFO and respond to the Company's repeated requests

to reopen the bidding process. Contrary to FCC rules, the public version of the January 15 letter

was redacted in its entirety; the document was a blank sheet of paper with a redaction legend.

75. The fact of the exparte telephone conversation between Hook and Chairman

Wheeler was disclosed in a January 23, 2014 letter filed with the FCC that referenced the

January 15, 2014 letter. Contrary to FCC rules, the January 23 letter omitted a summary of the

substance of the telephone conversation.

76. In response, Telcordia filed a letter with the FCC the same day stating that

"Neustar's [January 15, 2014] filing is extremely irregular, given that the Commission is

currently conducting a procurement for one or more LNPA vendors, if what Neustar has done is

23

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 28 of 72 PagelD# 256

to unilaterally seek to alter the terms of its Best and Final Offer, that would be improper and

should be disregarded entirely." Telcordia added that "if bidding is going to be re-opened, it is

the Commission (or its Bureaus acting on delegated authority) that should make that

determination; it would be highly improper were Neustar to attempt to force the Commission to

do so by unilaterally submitting amendments to its Best and Final Offer."

77. That is precisely what Neustar was attempting to do, and Neustar's sudden,

unsolicited, submission of the October Revised BAFO was entirely improper. Neustar had no

reasonable expectation that there would be more than one round of BAFOs. The RFP

emphasized, in fact, that a decision might be made based on initial proposals, and thus Neustar

had no basis to demand or expect even one BAFO, let alone two.

78. Indeed, Neustar's demand for a second round of BAFOs was a complete about-

face from its previous position that multiple BAFOs were unnecessary. In a November 6, 2012

letter to the FCC concerning procedures for the RFP, Neustar had argued that "[i]f the FoNPAC

is not satisfied with the form or substance of any potentially competitive bid, it has the ability to

seek improved proposals through the best-and-final-offer process. . . . As Neustar has explained

previously, in a confidential RFP process, there is no reason to mandate the solicitation of

multiple best-and-final offers." As the name "best and final offer" suggests, Neustar's

September BAFO could have and should have been its most competitive "best" and "final" offer.

79. To date, Neustar has not publicly provided any rational explanation for requesting

a second round of BAFOs. The only plausible explanation, in fact, is that Defendants knew that

their September BAFO was comparatively weak and would fail.

24

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 29 of 72 PagelD# 257

I. Defendants Belatedly Reveal Part of Their Secret Efforts to Edge Out Telcordia

80. On January 24, 2014, the day after Defendant Hook appealed to Chairman

Wheeler, the NAPM advised Defendants that their October Revised BAFO would not be

considered. In FCC parlance, the October Revised BAFO was "returned unopened."

81. At this point, as alleged further below, Defendants finally recognized that they

had to start to come clean with investors, and disclosed on January 29, 2014 that the NAPM had

rejected the October Revised BAFO.

82. Also on January 29, 2014, Neustar, under pressure from Telcordia, filed with the

FCC a less-redacted version of its January 15, 2014 letter concerning the October Revised

BAFO. The filing, which was timed to coincide with the January 29 disclosure to investors,

makes clear that Defendant Hook called Chairman Wheeler to discuss Neustar's secret efforts to

pry open the bidding process and substitute its October Revised BAFO for the September BAFO.

J. Defendants Continue to Scramble to Avoid Losing the NPAC Contracts to Telcordia

83. No later than January 24, 2014, Defendants clearly knew that they would lose the

NPAC Contracts to Telcordia unless they could fundamentally shake up the dynamics of the

selection process, including by convincing the FCC itself to step in.

84. On February 3, 2014, Neustar filed a letter with the FCC arguing that "the process

utilized to date has been flawed" and declaring that "Lilt is time for the Commission to intervene"

and direct FoNPAC to consider the October Revised BAFO.

85. Telcordia responded in a letter filed with the FCC on February 6, 2014. Telcordia

objected to Neustar's requests for a second round of BAFOs, stating that the timing and the

Company's inability to provide any rational explanation for additional BAFOs strongly

suggested that Neustar has obtained confidential, nonpublic information about its competitive

25

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 30 of 72 PagelD# 258

standing and price relative to other bidders. As Telcordia observed, Neustar clearly chose not to

offer its most competitive price in either its initial proposal or its September BAFO, and was

instead trying to preserve the premium associated with its monopoly and incumbent status.

86. On February 11, 2014, Julie A. Veach, the Chief of the FCC's Wireline

Competition Bureau, sent a letter to the Hon. Betty Ann Kane, Chairman of the NANC,

concerning the February 3 and 6 letters. Ms. Veach directed Chairman Kane to thoroughly

investigate "all claims of potential unfairness" including Telcordia's specific charge of receiving

nonpublic information, and to address whether they have been any attempts, outside of the

ordinary process contemplated by the RFP, to influence NANC or NAPM representatives

involved in the selection process. Ms. Veach further directed Chairman Kane to consider the

results of such investigations in issuing its recommendation for the selection of the next LNPA,

and to submit detailed findings to the FCC as to whether the process was conducted in a fair and

impartial manner. Ms. Veach also confirmed that Neustar's February 3 letter request to the FCC

to direct the FoNPAC to consider additional BAFOs was rejected.

87. The next day, February 12, 2014, Neustar filed a formal petition with the FCC

seeking a declaratory ruling directing the NAPM to consider its October Revised BAFO.

Neustar reiterated its assertion that the NAPM's extension of the April 5, 2013 bid submission

deadline was prejudicial to Neustar and put the Company at a competitive disadvantage. Neustar

also insisted in the petition, while attempting to sound neutral, that the process followed by the

NAPM will ultimately cause "the public and the industry [to] be deprived of the best and most

cost-effective proposals from all qualified offerors. This approach cannot result in the selection

of the most advantageous proposal."

26

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 31 of 72 PagelD# 259

88. On March 7, 2014, Neustar piled on by initiating a formal dispute before the

NANC. Neustar once again challenged the NAPM's extension of the April 2013 bid submission

deadline and FoNPAC's refusal to consider Neustar's October Revised BAFO.

89. On March 13, 2014, the FCC announced that a closed meeting of the NANC on

March 26, 2014 would precede the NANC's regular meeting on March 27, 2014. The sole item

on the agenda for the closed meeting was discussion of Neustar and Telcordia bids and a vote on

submitting the NANC's recommendation to the FCC.

90. This announcement sent Defendants into full panic mode. On March 19, 2014,

Neustar followed-up on its formal dispute by sending an unusual letter to NANC Chairman

Kane, signed by Defendant Hook. Hook wrote to "express Neustar's concerns about the Local

Numbering Portability Administrator vendor selection process" and sought to appeal to the

NANC as effectively the final decision-maker and a body that, having a broader constituency

than the NAPM, could see the bigger picture and appreciate Neustar's predicament. Hook wrote

plaintively near the end of the letter: "Chairman Kane, it is not too late to fix this process."

91. This time, however, Neustar went further than to repeat its concerns about

FoNPAC's refusal to consider its October Revised BAFO. Neustar also begged the NANC to

delay its upcoming decision to recommend Neustar or Telcordia to the FCC, and stated that the

Company "is willing to extend the current contract by three months, if required, and to

demonstrate our commitment to 'get it right' for all interested parties, we will offer a credit of up

to $SOM, if necessary, and regardless of the outcome." Regardless of Neustar's attempt to

sound magnanimous, its willingness to forego $50 million in fees can only be interpreted to

mean that Defendants knew the writing was on the wall.

27

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 32 of 72 PagelD# 260

K. The NANC Unanimously Recommends That the FCC Select Telcordia as Sole LNPA

92. Defendants' last-ditch efforts failed. On June 6, 2014, sometime before 4:00

p.m., the FCC inadvertently disclosed a confidential e-mail revealing that the NANC had

recommended Telcordia over Neustar to serve as the next and sole LNPA. The e-mail, sent by

the NANC to the FCC, was posted to the FCC's public docket and later removed.

93. Neustar confirmed this disclosure in a press release issued on June 9, 2014, before

the opening of trading, stating in part that "Loin Friday, June 6, a copy of a confidential email

dated April 28, 2014, sent by an aide to the chair of the [NANC] to the FCC was posted in the

FCC docket and made available to the public. . . . The email indicates the NANC recommends

that the FCC award the next LNPA contract to iconectiv, an operating unit of Ericsson."

94. On June 9, 2014, the FCC issued a Public Notice formally reporting that on April

24, 2014, the NANC submitted its recommendation to the FCC to select Telcordia as the next

LNPA. The Public Notice reported that the voting members of the NANC reached their

recommendation unanimously, with one abstention, during the NANC's closed meeting on

March 26, 2014.

95. Together with its recommendation, the NANC forwarded investigative reports

that responded to the FCC's February 11, 2014 directive to review and evaluate any and all

claims of potential unfairness in the RFP process, including Telcordia's claim that Neustar

obtained confidential, nonpublic information about its competitive standing and price relative to

other bidders. The several reports concerning the NANC's recommendation and associated

investigations were submitted to the FCC confidentially, and have not been made public.

96. The FCC generally defers to the NANC's decisions. In an April 11, 2014 article

about the NPAC contract issue, The Capitol Forum reported that "[a] former NANC member

28

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 33 of 72 PagelD# 261

stated in an interview that in considering NANC's decision making, the FCC is 'pretty

deferential to the recommendations of the people they consider the experts' and that the agency

'wouldn't be terribly likely' to overturn a decision deliberated on by NANC."

97. The FCC's June 9, 2014 Public Notice sought comments from interested parties

and the public on the NANC's recommendation and the associated materials. Multiple

commenters, including Neustar, Telcordia, the NAPM, and CTIA/USTelecom as alleged above,

filed detailed comments beginning on July 25, 2014. Other than Neustar itself, not a single

commenter has asked the FCC to award the next NPAC Contracts to Neustar.

98. According to a source close to the selection process, as reported by The Capitol

Forum on August 4, 2014, Neustar's comments challenging the NANC's recommendation were

viewed "at the agency as 'nothing earth shattering and nothing new," and, according to the

source, "there were no signs that the agency would change its planned course of action in

accepting NANC's recommendation."

L. The NANC Recommendation Leads Neustar to Consider Selliiw Itself to a Private Equity Firm

99. On August 22, 2014, Reuters reported that Neustar was considering a potential

sale amid interest from private equity firms. In particular, according to this news report, Neustar

was working with the investment bank JPMorgan Chase & Co. on possible options following a

more than 40 percent drop in its share price since the beginning of 2014.

100. The article noted that potential sale process was motivated by "a major

government contract [Neustar] stands to lose to Ericsson AB subsidiary Telcordia

Technologies," and noted further that "[going private could allow Neustar to restructure its

operations, should it lose the government contract, without having to worry about its share price

performance."

29

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 34 of 72 PagelD# 262

V. DEFENDANTS' MATERIALLY FALSE AND MISLEADING STATEMENTS AND OMISSIONS OF MATERIAL FACT

A. April 18, 2013 "Statement" on Extension of RFP Submission Deadline

101. On April 18, 2013, after the close of trading, Neustar issued a press release titled

"Neustar Statement on Extension of NPAC RFP Submission Deadline." The press release was

filed with the SEC the same day as an exhibit to a Form 8-K Current Report dated April 18,

2013, and signed by Defendant Lalljie.

102. Defendant Edwards was quoted in this Statement on behalf of Neustar:

Neustar successfully submitted its proposal on April 5, 2013, which was the deadline previously announced by the NAPM. The RFP process has been a matter of public record since May 2011, was subject to a robust public comment process, and the deadline for submission of responses was published 60 days in advance of the filing deadline. The process was designed to promote competition and provided interested parties with sufficient time to meet the submission requirements. Neustar filed its response in a timely manner and in accordance with the RFP submission requirements. We remain confident in the strength of our proposal and the value to be gained by the industry and consumers if we are awarded the contract to continue in July 2015 as the local number portability administrator.

103. The statements set forth in Paragraph 102 above were materially false and

misleading when made, and omitted material facts necessary to make the statements, in light of

the circumstances under which they were made, not misleading.

104. Defendants' April 18, 2013 Statement conveyed to investors that they were

unconcerned about the NAPM's decision to extend the 2015 LNPA RFP deadline from April 5

to 22, 2013, and that the Company, based on the strength of its timely April 5 bid, would once

again be awarded the NPAC Contracts. The Statement further conveyed to investors that

Neustar was not likely to face any competing bidders because 60 days was sufficient time for

qualified vendors to meet the submission requirements, and if no qualified vendor was able to

30

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 35 of 72 PagelD# 263

meet those requirements within 60 days, then no qualified vendor was likely to meet those

requirements within 74 days.

105. As alleged in Paragraphs 50-54 above, Defendants knew or recklessly

disregarded, however, that the deadline extension seriously prejudiced Neustar's competitive

standing and increased the risk that Neustar would be replaced by Telcordia as sole LNPA, and

that the Company's revenue accordingly would be decimated. Further, Defendants knew or

recklessly disregarded that Neustar's pricing reflected its monopoly and incumbent position, that

it was possible for the LNPA to earn a reasonable profit at significantly lower prices, and that the

extension of the submission deadline permitted Telcordia or other potential competitors to

structure a bid that was priced significantly lower than Neustar's proposal.

106. This is reflected in Neustar's April 24, 2013 letter to the FCC, filed just four

business days after Defendants issued the April 18 Statement. In this letter, as alleged in

Paragraphs 55-56 above, Defendants strongly objected to the deadline extension, asserting that it

perversely favored bidders unable to meet the deadline, that it seriously prejudiced Neustar by

raising the risk that the Company's proposal had been disclosed to other bidders, and that it

suggested that certain bidders obtained the extension through improper, undisclosed

communications with the NAPM or the FCC. Given that Neustar has adduced no evidence of

such improper disclosure, these objections were the result of an effort by Neustar to get by the

original 60-day submission period with a high-priced, anticompetitive proposal that reflected

Neustar's monopoly and incumbent status, and Defendants' recognition that the extension of the

deadline was likely to thwart that effort.

107. Defendants' views expressed to the FCC on April 24, 2013 were contrary to their

expression of confidence to the investing public that the Company would once again be awarded

31

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 36 of 72 PagelD# 264

the NPAC Contracts, and that Neustar was in fact not likely to face any competition for renewal

of the NPAC Contracts. Accordingly, regardless of how "strong" Neustar believed its April 5

proposal was, Defendants' April 18 Statement misled investors with respect to the potential risks

and consequences of the NAPM's unanticipated decision to extend the RFP submission deadline.

B. May 2, 2013 First Quarter Press Release and Conference Call

108. On May 2, 2013, Neustar issued a press release titled "Neustar Reports Results

for First Quarter 2013," announcing the Company's financial results for the first quarter of 2013.

The press release was filed with the SEC the same day as an exhibit to a Form 8-K Current

Report dated May 2, 2013 and signed by Defendant Lalljie.

109. Defendant Hook stated in this press release: "We submitted our proposal for the

NPAC contract in early April, and we remain confident in our ability to provide world class

service to the communications industry."

110. Neustar held a conference call with securities analysts the same day to discuss the

first quarter financial results and the status of the 2015 LNPA REP. Defendants Hook and

Lalljie, and Neustar's head of investor relations, participated in the call on behalf of Neustar.

111. In her opening remarks, Defendant Hook disclosed the existence of the April 24,

2013 letter to the FCC, describing it as "emphasizing our concern that extending the deadline

was inconsistent with the industry's and the FCC's commitment to manage a transparent and

timely RFP process." Hook then explained the status of the bidding process by emphasizing that

"we are confident in the strength of our proposal and it remained unchanged after the deadline

extension." Later in the conference call, Hook stated that Neustar "delivered a strong proposal to

renew the NPAC contract." She concluded the call by reiterating that the Company "submittLedi

a compelling proposal to renew the NPAC contract."

32

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 37 of 72 PagelD# 265

112. The statements set forth in Paragraphs 109 and 111 above were materially false

and misleading when made, and omitted material facts necessary to make the statements, in light

of the circumstances under which they were made, not misleading.

113. Defendants Hook's statement in the May 2, 2013 press release and expressions

during the conference call of "confidence in the strength of our proposal," "a strong proposal,"

and "a compelling proposal," conveyed to investors that the Company was well-positioned to

win the NPAC Contract renewal and would continue to serve as the sole LNPA. These

assurances continued to misrepresent and conceal from investors and market participants the true

nature and extent of Defendants' concerns about the significantly increased risk to Neustar's

competitive standing in the LNPA selection process. Defendants knew or recklessly disregarded

that Neustar's pricing reflected its monopoly and incumbent position, that it was possible for the

LNPA to earn a reasonable profit at significantly lower prices, and that the extension of the

submission deadline permitted Telcordia or other potential competitors to structure a bid that was

priced significantly lower than Neustar's proposal. As alleged in Paragraphs 50-56 above, this

was reflected in the NAPM's unexpected decision about two weeks earlier to extend the bid

submission deadline to allow competitors to challenge Neustar, and Neustar's April 24, 2013

letter to the FCC, which had been filed just one week earlier.

114. Although Defendant Hook disclosed the existence of the April 24, 2013 letter

during the conference call, she strategically described it during the conference call in the context

of "the industry's and the FCC's commitment to manage a transparent and timely RFP process,"

and made no mention of the heightened risks and potentially serious prejudice to Neustar's

competitive standing versus Telcordia.

33

Case 1:14-cv-00885-JCC-TRJ Document 23 Filed 11/06/14 Page 38 of 72 PagelD# 266

115. Defendant Hook's sleight-of-hand with investors was successful. Oppenheimer &

Co. titled its May 3, 2013 research report on the Company's first quarter results "NeuStar Inc.:

So Reliant You Could Set A Watch By It," and repeated its bottom line from February 6, 2013

that Neustar "remains well positioned in the long term given its monopolistic presence in number

management." William Blair & Co. stated in its May 5, 2013 research report that Neustar "did

not have any new announcements related to the continuing RFP process for the NPAC contract.

Neustar has submitted its RFP and because of nondisclosure agreements did not have additional

details to disclose." In its May 3, 2013 research report, Deutsche Bank took note of the deadline

extension but found significant that Neustar "apparently did not use the extended window to

make any updates." Deutsche Bank concluded that "[w]e continue to believe that NSR's

chances of winning the re-bid are very good given their 15-year track record of delivering high

quality of service." None of these analyst reports referenced Neustar's April 24, 2013 letter to

the FCC or its contents.

C. July 30, 2013 Second Quarter Conference Call

116. On July 30, 2013, Neustar held a conference call with securities analysts to

discuss the Company's financial results for the second quarter of 2013 and the status of the 2015

LNPA RFP. Defendants Hook and Lalljie, and Neustar's head of investor relations, participated

in the call on behalf of Neustar.

117. Defendant Hook acknowledged the NAPM's July 23, 2013 decision, one week

earlier, to delay the timeline for FCC selection of the next LNPA by four months, but once again

reassured investors and the market that "[w]e remain confident that our NPAC proposal is