In re Goldman Sachs Group, Inc. Securities Litigation...

29

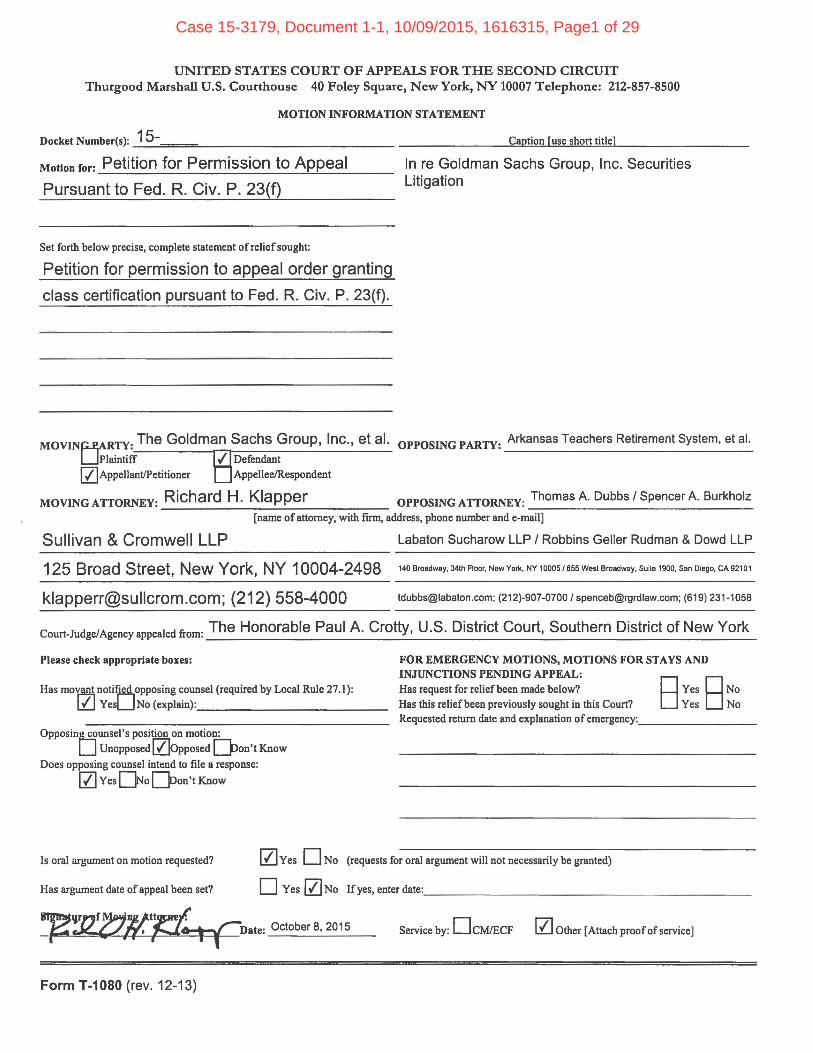

UNITED STATES COURT OF APPEALS FOR THE SECOND CIRCUIT Thurgood Marshall U.S. Courthouse 40 Foley Square, New York, NY 10007 Telephone: 212-857-8500 MOTION INFORMATION STATEMENT Docket Number(s): _1_5---=-===-------------- _______ _,C=a""pt:::io:::n'-'-[=us:.:e-"'sh:::o::.rt:....:tlc:..:. .tl:.:el..._ _______ _ Motion ror: Petition for Permission to Appeal Pursuant to Fed. R. Civ. P. 23(f) Set forth below precise, complete statement ofreliefsought: Petition for permission to appeal order granting class certification pursuant to Fed. R. Civ. P. 23(f). In re Goldman Sachs Group, Inc. Securities Litigation The Goldman Sachs Group, Inc., et al. OPPOSING PARTY: Arkansas Teachers Retirement System, et al. UPiaintiff ./ Defendant [{]Appellant/Petitioner Appellee/Respondent MOVING ATTORNEY: Richard H. Klapper OPPOSING ATTORNEY: Thomas A. Dubbs I Spencer A. Burkholz [name of attorney, with finn, address, phone number and e-mail] Sullivan & Cromwell LLP Labaton Sucharow LLP I Robbins Geller Rudman & Dowd LLP 125 Broad Street, New York, NY 10004-2498 140 Broadway, 34th Floor, NawYork, NY 1ooos/esswastBroadway, suita1900, san D1ego, CA92101 [email protected]; (212) 558-4000 [email protected]; (212)-907-0700 1 [email protected]; (619) 231-1058 court-Judge/Agencyappealedfrom: The Honorable Paul A. Crotty, U.S. District Court, Southern District of New York Please check appropriate boxes: Has counsel (required by Local Rule 27. 1) : l.{J YesUNo (explain): ____________ _ position on motion: U Unopposed [{]opposed Qon 't Know Does opposing counsel intend to file a response: [{]Yes []No Don't Know FOR EMERGENCY MOTIONS, MOTIONS FOR STAYS AND INJUNCTIONS PENDING APPEAL: Dves BNo Oves No Has request for relief been made below? Has this relief been previously sought in this Court? Requested return date and explanation of emergency: _______ _ ls oral argument on motion requested? [{]Yes 0 No (requests for oral argument will not necessarily be granted) Has argument date of appeal been set? 0 Yes [{]No If yes, enter date:. _____________________ _ Service by: DcM/ECF [{]Other [Attach proof of service] Form T-1080 (rev. 12-13) Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page1 of 29

Transcript of In re Goldman Sachs Group, Inc. Securities Litigation...

UNITED STATES COURT OF APPEALS FOR THE SECOND CIRCUIT Thurgood Marshall U.S. Courthouse 40 Foley Square, New York, NY 10007 Telephone: 212-857-8500

MOTION INFORMATION STATEMENT

Docket Number(s): _1_5---=-===-------------- _______ _,C=a""pt:::io:::n'-'-[=us:.:e-"'sh:::o::.rt:....:tlc:..:..tl:.:el..._ _______ _

Motion ror: Petition for Permission to Appeal

Pursuant to Fed. R. Civ. P. 23(f)

Set forth below precise, complete statement ofreliefsought:

Petition for permission to appeal order granting

class certification pursuant to Fed. R. Civ. P. 23(f).

In re Goldman Sachs Group, Inc. Securities Litigation

MOVIN~RTY: The Goldman Sachs Group, Inc., et al. OPPOSING PARTY: Arkansas Teachers Retirement System, et al.

UPiaintiff ./ Defendant [{]Appellant/Petitioner Appellee/Respondent

MOVING ATTORNEY: Richard H. Klapper OPPOSING ATTORNEY: Thomas A. Dubbs I Spencer A. Burkholz

[name of attorney, with finn, address, phone number and e-mail]

Sullivan & Cromwell LLP Labaton Sucharow LLP I Robbins Geller Rudman & Dowd LLP

125 Broad Street, New York, NY 10004-2498 140 Broadway, 34th Floor, NawYork, NY 1ooos/esswastBroadway, suita1900, san D1ego, CA92101

[email protected]; (212) 558-4000 tdubbs@labaton .com; (212)-907-0700 1 [email protected]; (619) 231-1058

court-Judge/Agencyappealedfrom: The Honorable Paul A. Crotty, U.S. District Court, Southern District of New York

Please check appropriate boxes:

Has mo~noti~opposing counsel (required by Local Rule 27.1): l.{J YesUNo (explain): ____________ _

Opposin~unsel's position on motion:

U Unopposed [{]opposed Qon 't Know

Does opposing counsel intend to file a response:

[{]Yes []No Don't Know

FOR EMERGENCY MOTIONS, MOTIONS FOR STAYS AND INJUNCTIONS PENDING APPEAL:

Dves BNo Oves No

Has request for relief been made below? Has this relief been previously sought in this Court? Requested return date and explanation of emergency: _______ _

ls oral argument on motion requested? [{]Yes 0 No (requests for oral argument will not necessarily be granted)

Has argument date of appeal been set? 0 Yes [{]No If yes, enter date:. _____________________ _

Service by: DcM/ECF [{]Other [Attach proof of service]

Form T-1080 (rev. 12-13)

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page1 of 29

15-______IN THE

United States Court of AppealsFOR THE SECOND CIRCUIT

IN RE GOLDMAN SACHS GROUP, INC. SECURITIES LITIGATION

FROM AN ORDER GRANTING CERTIFICATION OF CLASS ENTERED ON SEPTEMBER 24, 2015

BY THE UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF NEW YORK

MASTER FILE NO. 1:10 CIV. 03461 (PAC)

THE HONORABLE PAUL A. CROTTY

PETITION OF DEFENDANTS FOR PERMISSION TO APPEAL

PURSUANT TO FEDERAL RULE OF CIVIL PROCEDURE 23(f )

October 8, 2015

d

RICHARD H. KLAPPER

THEODORE EDELMAN

ROBERT J. GIUFFRA, JR.

DAVID M.J. REIN

BENJAMIN R. WALKER

SULLIVAN & CROMWELL LLP

125 Broad Street

New York, New York 10004

(212) 558-4000

Attorneys for Defendants-Petitioners

The Goldman Sachs Group, Inc.,

Lloyd C. Blankfein, David A.Viniar

and Gary D. Cohn

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page2 of 29

CERTIFICATION PURSUANT TO F.R.A.P. 26.1

Pursuant to Federal Rule of Appellate Procedure 26.1, as to the petitioners

listed below, the identity of their respective parent corporations, and of any

publicly held company that owns 10 percent or more of the identified party’s stock,

are as follows:

The Goldman Sachs Group, Inc.

None.

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page3 of 29

-ii-

TABLE OF CONTENTS

Page

QUESTIONS PRESENTED ................................................................................. 1

INTRODUCTION .................................................................................................. 2

FACTUAL AND PROCEDURAL BACKGROUND ......................................... 7

ARGUMENT ........................................................................................................ 13

I. THIS COURT SHOULD REVIEW THE DISTRICT

COURT’S ERRONEOUS CERTIFICATION OF A CLASS

WHERE DEFENDANTS’ GENERAL, ASPIRATIONAL

STATEMENTS HAD NO STOCK PRICE IMPACT ................................ 14

II. THIS COURT SHOULD REVIEW THE DISTRICT

COURT’S IMPROPER EVIDENTIARY STANDARD FOR

REBUTTING THE BASIC PRESUMPTION ............................................. 15

III. THE DISTRICT COURT ERRONEOUSLY DISREGARD

DEFENDANTS’ UNREBUTTED EVIDENCE SHOWING

THAT THEIR CHALLENGED STATEMENTS HAD NO

PRICE IMPACT .......................................................................................... 16

IV. THE DISTRICT COURT ALSO ERRONEOUSLY

CERTIFIED A CLASS, EVEN THOUGH PLAINTIFFS’

DAMAGES METHODOLOGY ADMITTEDLY DOES NOT

MEASURE DAMAGES FLOWING ONLY FROM THEIR

THEORY OF INJURY ................................................................................ 19

CONCLUSION ..................................................................................................... 20

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page4 of 29

-iii-

APPENDIX:

In re Goldman Sachs Grp., Inc. Sec. Litig., No. 10-cv-3461 (PAC)

(S.D.N.Y.), Opinion & Order, entered on September 24, 2015

(Dkt. No. 163) ..................................................................................................... A-1

Consolidated Class Action Complaint for Violations of Federal

Securities Laws, dated July 25, 2011 (Dkt. No. 68) ......................................... A-16

Declaration of John D. Finnerty, Ph.D., dated January 30, 2015

(Dkt. No. 137) ................................................................................................. A-131

Declaration of Paul Gompers, Ph.D., dated April 6, 2015

(Dkt. No. 144) ................................................................................................. A-407

Declaration of Stephen Choi, Ph.D., dated April 6, 2015

(Dkt. No. 145) ................................................................................................. A-562

Declaration of Charles Porten, CFA, dated April 6, 2015

(Dkt. No. 146) ................................................................................................. A-625

Rebuttal Declaration of John D. Finnerty, Ph.D., dated

May 15, 2015 (Dkt. No. 154) .......................................................................... A-861

In re Goldman Sachs Grp., Inc. Sec. Litig., No. 10-cv-3461 (PAC)

(S.D.N.Y.), Order denying Defendants’ requests for evidentiary

hearing and oral argument, entered on June 8, 2015 (Dkt. No. 158) ........... A-1069

Reply Declaration of Paul Gompers, Ph.D., dated

June 23, 2015 (Dkt. No. 161) ........................................................................ A-1070

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page5 of 29

-iv-

TABLE OF AUTHORITIES

Page(s)

CASES

Amgen Inc. v. Connecticut Retirement Plans & Trust Funds,

133 S. Ct. 1184 (2013) ...................................................................................... 14

Basic Inc. v. Levinson,

485 U.S. 224 (1988) ................................................................................... passim

Boca Raton Firefighters & Police Pension Fund v. Bahash,

506 F. App’x 32 (2d Cir. 2012) .............................................................. 3, 10, 11

Brautigam v. Blankfein,

8 F. Supp. 3d 395 (S.D.N.Y. 2014) .................................................................. 11

Brautigam v. Dahlback,

598 F. App’x 53 (2d Cir. 2015) ........................................................................ 11

Carpenters Pension Trust Fund of St. Louis v. Barclays PLC,

750 F.3d 227 (2d Cir. 2014) ......................................................................... 3, 10

City of Pontiac Policemen’s & Firemen’s Retirement System v. UBS AG,

752 F.3d 173 (2d Cir. 2014) ...................................................................... passim

Comcast Corp. v. Behrend,

133 S. Ct. 1426 (2013) ............................................................................... passim

ECA & Local 134 IBEW Joint Pension Trust of Chicago v.

JP Morgan Chase Co.,

553 F.3d 187 (2d Cir. 2009) ............................................................................... 3

Erica P. John Fund, Inc. v. Halliburton Co.,

No. 02-cv-1152-M, 2015 WL 4522863 (N.D. Tex. July 25, 2015) ........... 16, 18

Ganino v. Citizens Utilities Co.,

228 F.3d 154 (2d Cir. 2000) ............................................................................. 19

Halliburton Co. v. Erica P. John Fund, Inc.,

134 S. Ct. 2398 (2014) ............................................................................... passim

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page6 of 29

-v-

Hevesi v. Citigroup Inc.,

366 F.3d 70 (2d Cir. 2004) ....................................................................... 6-7, 14

In re Goldman Sachs Group, Inc. Securities Litigation,

No. 10-cv-3461 (PAC), 2014 WL 2815571 (S.D.N.Y. June 23, 2014) ....... 3, 11

In re Goldman Sachs Group, Inc. Securities Litigation,

No. 10-cv-3461 (PAC), 2014 WL 5002090 (S.D.N.Y. Oct. 7, 2014) .......... 3, 11

In re Goldman Sachs Group, Inc. Securities Litigation,

No. 10-cv-3461 (PAC), 2015 WL 5613150 (S.D.N.Y. Sept. 24, 2015) ... passim

In re IPO Securities Litigation,

471 F.3d 24 (2d Cir. 2006) ............................................................................... 18

In re Moody’s Corp. Securities Litigation,

274 F.R.D. 480 (S.D.N.Y. 2011) ...................................................................... 17

ITC Ltd. v. Punchgini, Inc.,

482 F.3d 135 (2d Cir. 2007) ............................................................................. 16

Reese v. Bahash,

574 F. App’x 21 (2d Cir. 2014) .................................................................... 3, 11

Richman v. Goldman Sachs Group, Inc.,

868 F. Supp. 2d 261 (S.D.N.Y. 2012) .................................................... 3, 7-8, 9

Roach v. T.L. Cannon Corp.,

778 F.3d 401 (2d Cir. 2015) ............................................................................. 19

Scott v. General Motors Co.,

605 F. App’x 52 (2d Cir. 2015) .......................................................................... 3

RULES

Fed. R. Civ. P. 23 ............................................................................................... 1, 13

Fed. R. Evid. 301 ............................................................................................. 15, 16

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page7 of 29

Defendants-Petitioners The Goldman Sachs Group, Inc. (“Goldman Sachs”

or the “Firm”), Lloyd C. Blankfein, David A. Viniar and Gary D. Cohn

(collectively with Goldman Sachs, “Defendants”) respectfully petition under Fed.

R. Civ. P. 23(f) for permission to appeal from the September 24, 2015 Order of the

United States District Court for the Southern District of New York (Crotty, J.)

certifying a class pursuant to Fed. R. Civ. P. 23(b)(3).

QUESTIONS PRESENTED

1. Whether this Court should review the District Court’s erroneous

decision to certify a multi-year investor class seeking billions of dollars in damages

for alleged securities fraud based solely on the type of general, aspirational

statements about a company’s business principles and internal controls that this

Court has held six times are not actionable, because no reasonable investor would

rely on such statements (and which, therefore, could not have impacted Goldman

Sachs’ stock price as required to invoke the Basic fraud-on-the-market

presumption of classwide reliance)?

2. Whether this Court should review the District Court’s erroneous

ruling that to rebut the Basic presumption of classwide reliance by showing that the

challenged statements did not impact Goldman Sachs’ stock price, as authorized by

Halliburton Co. v. Erica P. John Fund, Inc., 134 S. Ct. 2398, 2414-16 (2014)

(“Halliburton II”), Defendants must “demonstrate a complete absence of price

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page8 of 29

-2-

impact” with “conclusive evidence” (A-10, 13)?

3. Whether this Court should review the District Court’s erroneous

refusal to consider the unrebutted evidence that the challenged general aspirational

statements did not impact Goldman Sachs’ stock price either when made or when

the “truth” about those statements purportedly was disclosed, even though the

Supreme Court has held that courts should consider such evidence in certifying a

class, notwithstanding any overlap with the merits issue of materiality?

4. Whether this Court should review the District Court’s erroneous

certification of a class where Plaintiffs’ proffered classwide damages methodology

admittedly does not, as required by Comcast Corp. v. Behrend, 133 S. Ct. 1426,

1433 (2013), “measure only those damages” resulting from their theory that

Defendants’ general, aspirational statements caused their injury?

INTRODUCTION

Plaintiffs rest their securities fraud claims against Defendants solely on

general, aspirational statements about Goldman Sachs’ efforts to comply with its

business principles and internal controls. In six separate appeals involving UBS,

JP Morgan, Barclays, Standard & Poor’s (“S&P”) and General Motors, this Court

has held that analogous statements were not actionable as a matter of law, because

no reasonable investor would consider such statements as “guarantee[s] of some

concrete fact or outcome.” City of Pontiac Policemen’s & Firemen’s Ret. Sys. v.

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page9 of 29

-3-

UBS AG, 752 F.3d 173, 185-86 (2d Cir. 2014).1 Those holdings, all at the pleading

stage, rest on the legal determination that such general, aspirational statements

could not impact a company’s stock price, because a reasonable investor would not

rely on them.

Because the District Court declined to follow these Second Circuit

decisions,2 including five after it denied Defendants’ motion to dismiss, this action

proceeded to discovery and class certification. In moving for class certification,

Plaintiffs invoked the fraud-on-the-market presumption of reliance under Basic

Inc. v. Levinson, 485 U.S. 224 (1988), which recognizes “that an investor

presumptively relies on a misrepresentation so long as it was reflected in the

market price at the time of his transaction.” Halliburton II, 134 S. Ct. at 2414

(quotation omitted; emphasis added). In response, Defendants invoked their right

under the Supreme Court’s ruling in Halliburton II to rebut the Basic presumption

1 See Scott v. Gen. Motors Co., 605 F. App’x 52 (2d Cir. 2015) (summary order);

Reese v. Bahash, 574 F. App’x 21 (2d Cir. 2014) (summary order) (“Boca II”);

Carpenters Pension Trust Fund of St. Louis v. Barclays PLC, 750 F.3d 227 (2d

Cir. 2014) (“Barclays”); Boca Raton F’fighters & Police Pension Fund v. Bahash,

506 F. App’x 32 (2d Cir. 2012) (summary order) (“Boca I”); ECA & Local 134

IBEW Joint Pension Trust of Chi. v. JP Morgan Chase Co., 553 F.3d 187 (2d Cir.

2009). 2 See Richman v. Goldman Sachs Grp., Inc., 868 F. Supp. 2d 261, 279-80

(S.D.N.Y. 2012) (denying motion to dismiss); In re Goldman Sachs Grp. Inc., Sec.

Litig., 2014 WL 2815571, at *5 (S.D.N.Y. June 23, 2014) (denying

reconsideration); In re Goldman Sachs Grp. Inc. Sec. Litig., 2014 WL 5002090, at

*3 (S.D.N.Y. Oct. 7, 2014) (denying interlocutory appeal).

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page10 of 29

-4-

in opposing class certification by showing that “the asserted misrepresentation (or

its correction) did not affect the market price of the defendant’s stock.” Id.

In rebutting Basic, Defendants noted that this Court’s six precedents

establishing that their challenged statements about business principles and internal

controls were not actionable necessarily meant that those statements could not have

affected the Firm’s stock price as a matter of law. Defendants also presented

unrebutted empirical evidence demonstrating that their statements had no impact

on Goldman Sachs’ stock price when made or on Plaintiffs’ four alleged

“corrective disclosure” dates. This evidence confirmed empirically what this Court

repeatedly has held on the law: investors do not rely on such general, aspirational

statements. In nonetheless certifying a massive class seeking billions in damages

based on general, aspirational statements, the District Court erred in at least four

respects requiring this Court’s immediate intervention:

First, the District Court refused to apply this Court’s six decisions holding

that analogous general, aspirational statements were not actionable as a matter of

law, because no reasonable investor would rely on such statements. (A-12 n.5.)

Applying those decisions would have rebutted the Basic presumption by

establishing no price impact as a matter of law.

Second, the District Court contravened Halliburton II by imposing an

impermissibly high evidentiary burden on Defendants to rebut the Basic

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page11 of 29

-5-

presumption with “conclusive evidence” of a “complete lack of price impact.” (A-

10, 13.)

Third, after imposing its unduly high “conclusive evidence” standard, the

District Court improperly disregarded Defendants’ unrebutted empirical evidence

demonstrating that their challenged statements had no impact on Goldman Sachs’

stock price. The District Court recognized as undisputed facts that (i) “the

misstatements had no impact on the stock price when made”; and (ii) there was “no

movement in Goldman’s stock price” on any of the “34 separate dates” prior to the

alleged “corrective disclosures” when the press reported that Goldman Sachs had

conflicts with clients, including in connection with the collateralized debt

obligation (“CDO”) transactions that form the basis for Plaintiffs’ claims. (A-11.)

The District Court erroneously reasoned that because such evidence overlapped

with the merits issue of materiality, the court should “not consider” it at class

certification (id.), even though Halliburton II expressly held that courts should

consider such evidence in assessing price impact. See 134 S. Ct. at 2417.

Instead, without holding an evidentiary hearing (as Defendants requested) or

undertaking the “rigorous analysis” required to certify a class, Comcast, 133 S. Ct.

at 1433, the District Court simply accepted as “obvious” Plaintiffs’ unsupported

speculation that the declines in Goldman Sachs’ stock price after multiple

publicized reports of enforcement activity by U.S. regulators, including the

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page12 of 29

-6-

Securities and Exchange Commission’s (“SEC”) lawsuit against Goldman Sachs

over one of the CDOs—ABACUS 2007-AC1 (“ABACUS”)—were “the link”

showing that investors were reacting to their first knowledge that the challenged

general, aspirational statements were not true. (A-12.) In accepting Plaintiffs’

speculation, the District Court acknowledged that “the announcements of

enforcement actions would cause a level of decline” (A-12), but ignored evidence

showing that the decline in Goldman Sachs’ stock price after the SEC lawsuit was

consistent with the stock price declines other companies suffered in response to the

overhang and uncertainty of similar enforcement actions.

Fourth, the District Court erred in certifying a class even though Plaintiffs

admittedly did not proffer a damages methodology that, as required by Comcast,

133 S. Ct. at 1433, “measure[d] only those damages” resulting from their theory

that Defendants’ general, aspirational statements caused the declines in Goldman

Sachs’ stock price. Instead, the District Court accepted Plaintiffs’ assurance that

they “will be able to account for” damages stemming from their theory of injury,

while improperly imposing on Defendants the burden to show that “disaggregation

would be impossible.” (A-14 (emphasis added).)

This Court has recognized that orders certifying classes in securities cases

are “likely to escape effective review after entry of final judgment” because “very

few securities class actions are litigated to conclusion.” Hevesi v. Citigroup Inc.,

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page13 of 29

-7-

366 F.3d 70, 80 (2d Cir. 2004). Here, Plaintiffs seek billions in damages,

“plac[ing] inordinate or hydraulic pressure on defendants to settle.” Id. (quotation

omitted). Because Defendants’ general, aspirational statements had no impact on

Goldman Sachs’ stock price as both a matter of law and empirical fact, this Petition

presents the ideal vehicle for this Court to provide needed guidance to lower courts

in this Circuit, the center of the Nation’s securities markets, on how to assess price

impact evidence under Halliburton II when evaluating whether to certify a class.

FACTUAL AND PROCEDURAL BACKGROUND

Defendants’ Challenged General, Aspirational Statements. Plaintiffs’

claims are premised on Defendants’ general, aspirational statements, made

between 2007 and 2010, about the Firm’s efforts to comply with its “conflicts of

interest policies and business practices” (A-1) across its many complex businesses:

“We are dedicated to complying fully with the letter and spirit of the laws, rules

and ethical principles that govern us. Our continued success depends upon

unswerving adherence to this standard.”

“Integrity and honesty are at the heart of our business,” and “[o]ur reputation is

one of our most important assets.”

“Our clients’ interests always come first. Our experience shows that if we serve

our clients well, our own success will follow.”

“[W]e increasingly have to address potential conflicts of interest, including

situations where our services to a particular client or our own proprietary

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page14 of 29

-8-

investments or other interests conflict, or are perceived to conflict, with the

interest of another client. . . .”

“We have extensive procedures and controls that are designed to . . . address

conflicts of interest.”

See Richman, 868 F. Supp. 2d at 277 (citing Compl. ¶¶ 134, 154, 289).

None of the challenged statements referred or related to any particular

transaction or even a line of business, or otherwise guaranteed that the Firm would

achieve its stated goals. Plaintiffs nonetheless claim that these general, aspirational

statements were false because they purportedly were inconsistent with Goldman

Sachs’ allegedly undisclosed conflicts in connection with four CDOs sponsored by

its affiliates in 2006 and 2007 and sold to a small number of highly sophisticated

clients (not Firm shareholders). See id. at 278-80.

Plaintiffs assert that four “corrective disclosures” in 2010 revealed the

purported falsity of Defendants’ general, aspirational statements about Goldman

Sachs’ efforts to comply with its business principles and conflicts controls:

April 16, 2010: The SEC filed a highly publicized enforcement action alleging

that Goldman Sachs and one of its employees misled investors about the

ABACUS CDO by not disclosing that a hedge fund “played an active and

determinative role in the asset selection process.” (A-67-68, 119-20.)

April 26, 2010: The U.S. Senate Permanent Subcommittee on Investigations

“released Goldman internal emails further detailing that Goldman made billions

by betting against the CDOs it sold to its clients.” (A-122.)

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page15 of 29

-9-

April 30, 2010: “[T]he Wall Street Journal reported that Goldman was the

subject of a criminal investigation by the Department of Justice” into

unspecified mortgaged-related matters. (A-122.)

June 10, 2010: “[I]t was reported that the SEC was investigating whether in

connection with the Hudson CDO, Goldman profited by ridding itself of

mortgage backed securities . . . on Goldman’s books that it knew were going to

decline by selling these securities to Goldman’s clients. . . .” (A-123.)

The District Court’s Decisions on Actionability. On June 21, 2012, the

District Court denied Defendants’ motion to dismiss Plaintiffs’ claims based on

Defendants’ general, aspirational statements, holding that they are not “mere

puffery or statements of opinion,” because the Complaint sufficiently alleged that

Defendants “could not have genuinely believed [the statements] were accurate and

complete” in light of the alleged CDO misconduct. Richman, 868 F. Supp. 2d at

279-80. The District Court reiterated its view three more times, including in its

certification opinion (see supra at p. 3 n.2; A-12 n.5), despite this Court’s decisions

holding that “general statements about reputation, integrity, and compliance with

ethical norms are inactionable ‘puffery,’ meaning that they are ‘too general to

cause a reasonable investor to rely upon them.’” UBS, 752 F.3d at 183:

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page16 of 29

-10-

Challenged Statements Statements Held Not Actionable

“We are dedicated to complying fully

with the letter and spirit of the laws,

rules and ethical principles that

govern us.”

UBS goes “above and beyond what laws

and regulations require” and “adheres to

high ethical standards.” (UBS)

“[T]he principles that guide Barclays

business” include “complying with

relevant legal and regulatory

requirements.” (Barclays)

“Integrity and honesty are at the heart

of our business.”

“Our reputation is one of our most

important assets.”

“[P]reserving UBS’s integrity is vital to its

most valuable asset—its reputation.”

(UBS)

“The integrity, reliability and credibility

of S&P has enabled us to compete

successfully in an increasingly global and

complex market . . . ” (Boca I)

“Our clients’ interests always come

first.”

UBS “put[s] the clients at the center of all

we do . . . ” (UBS)

“We are focused on [] supporting our . . .

customers . . . ” (Barclays)

The challenged statements about Goldman Sachs’ conflicts controls also are

no different from similar statements that this Court has held not actionable. In

UBS, for example, the alleged misstatements included that UBS had established a

“comprehensive set of risk factor limits,” and “[one] of [UBS’s] overriding risk

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page17 of 29

-11-

management goals is the avoidance of concentration risks.” UBS, No. 12-4355

(Joint App’x 95, 318). Notwithstanding plaintiffs’ allegations that UBS’s purchase

of more than $100 billion of over-valued subprime mortgage securities showed that

the bank had “neither established [nor] maintained risk concentration controls” (id.

at 384, 393), this Court held that no reasonable investor would rely on UBS’s

statements about its controls as “guarantee[s].” UBS, 752 F.3d at 185-86.3

The District Court tried to distinguish these Second Circuit decisions on the

ground that Goldman Sachs’ statements were “at odds with its alleged conduct” in

the four CDO transactions. Goldman, 2014 WL 2815571, at *5.4 But UBS’s

3 Likewise, in Boca I and II, plaintiffs alleged that S&P’s parent company

repeatedly emphasized that S&P had “institutional safeguards in place to ensure

the independence and integrity of [ratings] opinions” and “endeavor[ed] to . . .

ensure[] that the integrity and independence of [the ratings process] are not

compromised by conflicts of interest.” Boca I, No. 12-1776 (Joint App’x at 253,

278). Even though plaintiffs alleged that the “ratings method was basically a

sham,” and that S&P had not properly managed client conflicts, this Court held the

challenged controls statements were too general to be actionable. 506 F. App’x at

37. 4 The District Court denied reconsideration by applying “clear conviction of error”

review, and the “presumption against amendment of prior orders.” Goldman, 2014

WL 2815571, at *4. The District Court then denied certification of an

interlocutory appeal because Defendants had not shown the required “exceptional

circumstances.” Goldman, 2014 WL 5002090, at *3. The same aspirational

statements were the predicate for a parallel shareholder derivative action the

District Court dismissed because demand was not excused, albeit while reiterating

its view that the statements were actionable. See Brautigam v. Blankfein, 8

F. Supp. 3d 395, 401 n.8 (S.D.N.Y. 2014). This Court affirmed, without reaching

the actionability issue. See Brautigam v. Dahlback, 598 F. App’x 53 (2d Cir.

2015) (summary order).

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page18 of 29

-12-

disclosures about its efforts to limit investment risk were no less “at odds” with its

undisclosed exposure to subprime mortgage securities than Goldman Sachs’

general disclosures about its conflict controls allegedly were “at odds” with the

alleged conflicts in four CDO transactions. Nor did Goldman Sachs’ disclosures

“guarantee” that its controls would be any more effective in avoiding conflicts than

UBS’s controls over taking on excessive investment risk guaranteed that UBS

would not acquire a concentrated position in subprime securities.

The Unrebutted Evidence That Defendants’ General, Aspirational

Statements Had No Impact on Goldman Sachs’ Stock Price. In moving for class

certification, Plaintiffs invoked the Basic presumption of classwide reliance. In

response, Defendants reiterated that their general, aspirational statements by

definition could not cause price impact under this Court’s settled law, and then

submitted unrebutted empirical evidence demonstrating that Goldman Sachs’ stock

price did not react either when these statements were made or when the market

“learned” on dozens of dates prior to the purported “corrective” disclosure dates

about Goldman Sachs’ alleged conflicts of interest, including with CDO investors.

(A-424-40, 632-44, 653-60, 1072-77.) Instead, Goldman Sachs’ stock reacted

adversely only after the market learned of government lawsuits and investigations.

(A-440-54, 574-95, 1077-80.) In response, Plaintiffs submitted no price impact

evidence whatsoever, but only the speculative, circular theory “that the

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page19 of 29

-13-

misstatements simply served to maintain an already inflated stock price,” and that

“on the corrective disclosure dates, information revealing the misstatements to the

market was released, and the stock price dropped.” (A-11-12.)

The District Court’s Class Certification Order. After denying Defendants’

requests for an evidentiary hearing or oral argument (A-1069), the District Court

issued an opinion containing only four pages of legal analysis. (See A-10-14.)

After again declining to follow this Court’s precedents on the actionability of the

challenged statements (A-12 n.5), the District Court created a “conclusive

evidence” standard for rebutting the Basic presumption of reliance (A-12-13), and

then dismissed as “insignificant” and declined to “consider” Defendants’

unrebutted evidence demonstrating the absence of any price impact. (A-11.) The

District Court also rejected Defendants’ attack on Plaintiffs’ failure to present the

type of damages model required by Comcast, shifting to Defendants the burden of

proving that it would be “impossible” for Plaintiffs to construct a damages model

consistent with their liability theory. (A-14.)

ARGUMENT

This Court should grant a Rule 23(f) petition where, as here, (1) “the

certification order will effectively terminate the litigation and there has been a

substantial showing that the district court’s decision is questionable,” or (2) “the

certification order implicates a legal question about which there is a compelling

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page20 of 29

-14-

need for immediate resolution.” Hevesi, 366 F.3d at 76.

I. THIS COURT SHOULD REVIEW THE DISTRICT COURT’S

ERRONEOUS CERTIFICATION OF A CLASS WHERE

DEFENDANTS’ GENERAL, ASPIRATIONAL STATEMENTS HAD

NO STOCK PRICE IMPACT.

This action never should have proceeded past the pleading stage in light of

this Court’s repeated holdings that statements that are “too general to cause a

reasonable investor to rely upon them” are immaterial as a matter of law. UBS,

752 F.3d at 182-83. Those holdings should have led the District Court to deny

class certification, because Defendants’ general, aspirational statements challenged

here could not have impacted Goldman Sachs’ stock price as a matter of law, and

Plaintiffs thus cannot invoke the Basic presumption of classwide reliance. It

cannot be that the same type of general, aspirational statements that this Court has

repeatedly held were not actionable in cases involving other financial firms are

actionable, have price impact and permit the certification of a class seeking billions

in damages in this case.5

5 Nothing in Amgen Inc. v. Conn. Ret. Plans & Trust Funds, which held only that

“proof” of materiality as a factual matter is not required at the class certification

stage, 133 S. Ct. 1184, 1191 (2013), would prevent this Court from holding,

consistent with its six decisions, that no reasonable investor would have relied on

Defendants’ challenged general, aspirational statements as a matter of law, and,

therefore, that the District Court erred in certifying a class premised on application

of the Basic presumption to those statements.

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page21 of 29

-15-

II. THIS COURT SHOULD REVIEW THE DISTRICT COURT’S

IMPROPER EVIDENTIARY STANDARD FOR REBUTTING THE

BASIC PRESUMPTION.

Defendants can defeat class certification by rebutting the Basic presumption

“through direct as well as indirect price impact evidence.” Halliburton II, 134 S.

Ct. at 2417. “Any showing that severs the link between the alleged

misrepresentation and either the price received (or paid) by the plaintiff” is

“sufficient.” Basic, 485 U.S. at 248 (emphasis added). Rather than apply the

Supreme Court’s standard, the District Court created a new standard, putting the

burden on Defendants to “demonstrate a complete absence of price impact” with

“conclusive evidence that no link exists” (A-13), effectively requiring Defendants

to disprove any possibility of price impact.

Basic and Halliburton II do not go so far. As Basic recognized, Fed. R.

Evid. 301 governs “allocating the burdens of proof between parties” when

presumptions apply. 485 U.S. at 245. Under Rule 301, “the party against whom a

presumption is directed has the burden of producing evidence to rebut the

presumption. But this rule does not shift the burden of persuasion, which remains

on the party who had it originally.” Fed. R. Evid. 301. This Court has equated the

showing under Rule 301 to rebut a presumption with the burden to defeat summary

judgment, explaining that “proffered evidence is ‘sufficient’ to rebut a presumption

as long as the evidence could support a reasonable jury finding of ‘the

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page22 of 29

-16-

nonexistence of the presumed fact.’” ITC Ltd. v. Punchgini, Inc., 482 F.3d 135,

149 (2d Cir. 2007) (citation omitted).6 Once Defendants demonstrated that the

challenged statements had no price impact, the burden shifted to Plaintiffs to come

forward with contrary evidence. The District Court erred in failing to require

Plaintiffs to do so.

The implications of this ruling are significant not only for this case, but for

all similar class actions in this Circuit, where the most significant securities class

actions are litigated. The Court should grant certification to clarify and standardize

the evidentiary showing required to rebut the Basic presumption under Halliburton

II.

III. THE DISTRICT COURT ERRONEOUSLY DISREGARDED

DEFENDANTS’ UNREBUTTED EVIDENCE SHOWING THAT

THEIR CHALLENGED STATEMENTS HAD NO PRICE IMPACT.

Defendants presented unrebutted expert evidence, as permitted by

Halliburton II, demonstrating that the challenged statements had no impact on

Goldman Sachs’ stock price either when they were made or on Plaintiffs’ four

purported “corrective disclosure” dates. (See supra at pp. 12-13.) The District

Court committed two significant errors in not considering that evidence.

6 One district court did not apply Rule 301, but that ruling relied on the Halliburton

II concurrence as well as an understanding, not advocated by Defendants here, that

under Rule 301 a plaintiff “would not be afforded an opportunity to … produc[e]

its own reputable expert to challenge [defendant’s].” Erica P. John Fund, Inc. v.

Halliburton Co., 2015 WL 4522863, at *7 (N.D. Tex. July 25, 2015).

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page23 of 29

-17-

First, as contemplated by Halliburton II, Defendants demonstrated that none

of Defendants’ challenged statements caused any increase in the price of Goldman

Sachs’ stock on any of the 18 days when the statements were made. (A-424-32,

1072.) The District Court improperly dismissed this evidence as “insignificant.”

(A-11.)7

Second, the District Court recognized that “there was no movement in

Goldman’s stock price” when press reports alleged “on 34 separate dates prior to

April 16, 2010”—the first alleged corrective disclosure date—that “Goldman had

acted against clients’ interests.” (A-11.) This unrebutted evidence demonstrated

conclusively that on Plaintiffs’ “corrective disclosure” dates the market reacted

negatively to the overhang and uncertainty arising from government enforcement

actions, not to some supposed recognition that Goldman Sachs’ alleged conflicts in

connection with four CDOs had rendered false Defendants’ aspirational statements

about the Firm’s business principles and conflicts controls.8 Had Plaintiffs’

7 See In re Moody’s Corp. Sec. Litig., 274 F.R.D. 480, 493 (S.D.N.Y. 2011) (where

“there [wa]s no date on which any alleged misrepresentation caused a statistically

significant increase in the price,” defendants successfully “severed the link

between the misrepresentation and the price”). 8 Plaintiffs offered no plausible explanation for why Goldman Sachs experienced

no statistically significant price decline on April 26, 2010—the only “corrective

disclosure” date with no news of enforcement activity—but did decline on April

30, 2010, when a newspaper reported rumors of a DOJ investigation but did not

reveal any new alleged facts about Goldman Sachs’ conduct. (A-1076-77.)

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page24 of 29

-18-

liability theory been correct, the price of Goldman Sachs’ stock should have

declined when the allegations were disseminated on those 34 earlier dates well

before the four “corrective disclosure” dates alleged here.9

In expressly refusing to “consider” Defendants’ unrebutted showing of no

price impact, the District Court, citing only Plaintiffs’ brief in support, improperly

held that this evidence constituted a “‘truth on the market’ defense” that “speaks to

the statements’ materiality and not price impact.” (A-11.) As the Supreme Court

expressly recognized in Halliburton II, notwithstanding any factual overlap

between price impact and materiality, “defendants must be afforded an opportunity

before class certification to defeat the presumption through evidence that an

alleged misrepresentation did not actually affect the market price of the stock.”

134 S. Ct. at 2417; see also In re IPO Sec. Litig., 471 F.3d 24, 41 (2d Cir. 2006)

(courts must make “definitive assessment of Rule 23 requirements,

notwithstanding their overlap with merits issues”). The District Court plainly erred

in not allowing Defendants to do so here.10

9 In Halliburton, on remand from the Supreme Court, the district court denied class

certification where, as here, “the information alleged by the [plaintiff] to be

corrective was both already disclosed and caused no statistically significant price

reaction.” 2015 WL 4522863, at *20 (emphasis in original). 10

The District Court also attempted to dismiss Defendants’ evidence as

purportedly revealing “different forms and degrees of misstatements” than those

revealed on the four “corrective disclosure” dates. (A-11-12.) But as Dr. Gompers

demonstrated, virtually all of the factual allegations concerning the CDO conflicts

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page25 of 29

-19-

IV. THE DISTRICT COURT ALSO ERRONEOUSLY CERTIFIED A

CLASS, EVEN THOUGH PLAINTIFFS’ DAMAGES

METHODOLOGY ADMITTEDLY DOES NOT MEASURE

DAMAGES FLOWING ONLY FROM THEIR THEORY OF INJURY.

This Court also should review the District Court’s clear misapplication of

the Supreme Court’s decision in Comcast. As the District Court recognized (but

then ignored), under Comcast Plaintiffs must show “at the class certification stage

. . . that their damages model actually measures damages that result from the

class’s theory of injury.” (A-13 (emphasis added; quoting Roach v. T.L. Cannon

Corp., 778 F.3d 401, 407 (2d Cir. 2015)); see also Comcast, 133 S. Ct. at 1433.

Defendants’ expert demonstrated that the conclusory damages methodology

of Plaintiffs’ expert does not disaggregate the stock price declines supposedly

had been prominently and extensively reported to the public—with no impact on

the Firm’s stock price—long before the corrective disclosure dates. (A-432-40,

543-55, 1078-79.) For example, virtually all of the factual allegations contained in

the SEC’s complaint concerning the ABACUS CDO were the focus of extensive

media coverage, including in a best-selling book published in November 2009.

(A-550-54, 1078-79.) Similarly, the factual allegations concerning the Hudson

CDO were reported in a New York Times front-page article months before the

“truth” purportedly was revealed. (A-551, 1078-79.) This is not, as Plaintiffs

claim, a “truth on the market defense.” Dr. Gompers did not conclude that the

prior conflict allegations revealed the “truth” and thus “dissipated” the supposed

inflationary effects of Defendants’ statements about Goldman Sachs’ business

principles and conflict controls. See Ganino v. Citizens Utilities Co., 228 F.3d

154, 167-68 (2d Cir. 2000) (describing “truth on the market” defense). Instead, he

concluded that the lack of investor reaction to prior disclosures of alleged Goldman

Sachs conflicts shows that the Firm’s stock price was not “inflated” by any

general, aspirational statements about its efforts to comply with its business

principles and conflicts controls.

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page26 of 29

-20-

caused by Plaintiffs’ current theory of classwide injury—premised on Defendants’

general statements about Goldman Sachs’ business principles and conflicts

controls—from other causes, including the disclosures about government lawsuits

and investigations and Plaintiffs’ now-dismissed claim premised on Defendants’

failure to disclose Goldman Sachs’ receipt of an SEC Wells notice relating to the

ABACUS transaction. (A-465-68, 1080.) The District Court erred by accepting

Plaintiffs’ vague assurance that their expert “will be able to [develop a damages

model that] account[s] for any so-called inflation” resulting from “Plaintiff’s

theory of liability,” and improperly shifted the burden to Defendants to show “that

disaggregation would be impossible to determine.”11

(A-13-14 (emphasis added).)

CONCLUSION

For the foregoing reasons, Defendants respectfully request that the Court

grant this Petition.

11

In Comcast, the Supreme Court expressly rejected the District Court’s reasoning

that the failure of Plaintiffs’ purported methodology to measure damages flowing

only from their theory of liability “would not defeat the class’s predominance

because it would affect all class members in the same manner.” (A-14.) “Under

that logic, at the class-certification stage any method of measurement is acceptable

so long as it can be applied classwide, no matter how arbitrary the measurements

may be.” Comcast, 133 S. Ct. at 1433.

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page27 of 29

Dated: October 8, 2015 New York, New York

Respectfully submitted,

1.~.~!~ Theodore Edelman Robert J. Giuffra, Jr. David M.J. Rein Benjamin R. Walker SULLIVAN & CROMWELL LLP 125 Broad Street New York, New York 10004-2498 (212) 558-4000

Attorneys for Defendants-Petitioners The Goldman Sachs Group, Inc., Lloyd C. Blankfein, David A. Viniar and Gary D. Cohn

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page28 of 29

CERTIFICATE OF SERVICE

I hereby certify that on this 8th day of October 2015, I caused true and

accurate copies of the foregoing Petition of Defendants for Permission to Appeal

Pursuant to Federal Rule of Civil Procedure 23(f) and accompanying Appendix

and Motion Information Statement to be served by e-mail, as well as by FedEx,

upon the following counsel:

Thomas A. Dubbs LABATON SUCHAROW LLP 140 Broadway, 34th Floor New York, NY 10005

Spencer Burkholz ROBBINS GELLER RUDMAN & DOWD LLP 655 West Broadway, Suite 1900 San Diego, CA 92101

Co-Lead Counsel for Plaintiffs-Respondents

Jacob E. Cohen

Case 15-3179, Document 1-1, 10/09/2015, 1616315, Page29 of 29