In hc-deloitte-india-annual-compensation-trends-survey-report-fy-2016-noexp

24

Annual Compensation & Benefits Trends Survey India FY 2015-16 Human Capital Consulting April 2015

-

Upload

abhisek-gupta -

Category

Education

-

view

273 -

download

0

Transcript of In hc-deloitte-india-annual-compensation-trends-survey-report-fy-2016-noexp

Annual

Compensation & Benefits

Trends Survey

India

FY 2015-16

Human Capital Consulting

April 2015

Scope,

approach

and

methodology

Executive

summary

Sector-wise

analysis

About

Deloitte

Human

Capital

Consulting

Overall

industry

report

Table of Contents

To receive sector-wise analysis, please visit contact us

section at the end of this report

Scope, approach &

methodology

Scope, approach and methodology

Scope of the survey

The Deloitte India Compensation Trends Survey is an annual study conducted by

Human Capital Consulting. The objective of the study is to understand the key

compensation and benefits trends across sectors in the Indian market.

Organizations Sectors

Increment &

variable Pay

projections for

FY 2016 and

comparison

with FY 2015

Attrition

rates, key

levers for

mitigation

and talent

attraction

Key benefits

given across

sectors

Managing

and

rewarding

critical

talent

250 18

4© 2015 Deloitte Touche Tohmatsu India Private Limited

Scope, approach and methodology

Survey methodology

Design the survey instrument

The parameters of the study were finalized and

a structured questionnaire was

designed as a primary data collection tool

Finalize the target basket

The sectors covered in the study were finalized along with the leading

organizations from each sector

Invite participationA formal invitation e-mail and online questionnaire was sent to the Human Resources teams in the chosen organizations

requesting for participation

Collect and validate dataThe responses received from all participants were validated and checked for

accuracy and intended interpretation

Analyze dataThe data received was

collated and analyzed to get detailed insights on sector wise practices,

compensation and benefits trends

Generate the

Compensation Trends

Survey Report (FY 2015-

16)

5© 2015 Deloitte Touche Tohmatsu India Private Limited

Scope, approach and methodology

Definitions

10P/The lower decile position (where

one-tenth of the sample has lower

data)

25P/The lower quartile position (where

one quarter of the sample has lower

data)

50P/The middle position (where half of

the sample has lower and half has

higher data)

75P/The upper quartile position (where

three-quarters of the sample has

lower data)

90P/The upper decile position (where

nine-tenth of the sample has lower

data)

Top

Management

The most senior executive in the organization (CEO), coordinating a

full range of functions, providing leadership, overall direction and

control of company operations. Also, includes key executives

(direct reportees to CEO) within the organization, heading key

functions, businesses and geographies

Senior

Management

Executives who directly report to the Top Management, and manage

a range of functions. However, they are not regarded as Top

Management. This also includes direct reportees to different key

functional, business and geographical heads

Middle

Management

Includes executives who directly report to Senior Management,

with supervisory responsibility for a sub-function, part of a

business, geography etc.

Junior

Management

Includes supervisory staff usually involved in the day to day

functioning of a small team (First Level of Management Cadre).

Also, includes entry level employees with professional qualification

Includes non-management staff who work as individual contributors

reporting to ManagementClerical

Percentile definitions

6© 2015 Deloitte Touche Tohmatsu India Private Limited

Scope, approach and methodology

Participant profile

** Others include companies in Hospitality, Professional Services, Agriculture, Aviation, Export and Social Services sectors. Considering the limited number of responses

from these sectors within the specified timelines, separate sector reports have not been published

4.0% (10)

ChemicalConsumer

businessEnergy Hi-Tech ITeS

Infrastructure

& real estateLogistics

Auto & auto

Comp.BFSI Media &

advertising

Pharma, life

sciencesRetail Others**

(38)

Annual

revenue

1.6% 6.0%

13.6%

32.8%

46.0%

<100 Crore

100-300 Crore

300-500 Crore

500-1000 Crore

>1000 Crore

2.4%

9.2%

16.8%

20.4%22.4%

28.8%

< 500

500 - 2000

2000 - 5000

5000 - 10000

10000 - 25000

> 25000

Employee

strength

Engineering &

manufacturing

6.0% (15)

8.0% (20)

4.8% (12)

7.2 % (18)

15.2% (38)

12.0% (30)

10.0% (25)

4.8% (12)

3.2% (8)

4.8% (12)

8.0% (20)

6.0% (15) 6.0% (15)

250 organizations from 18 sectors have participated in the Compensation Trends Survey for FY 2016

7© 2015 Deloitte Touche Tohmatsu India Private Limited

Executive summary

Executive summary

Key findings

Increment

The average salary increment across sectors is projected at 10.7% in FY

2016, which is 0.4% points higher than the previous FY 2015 (10.3%)

Voluntary attrition

In FY 2015 highest attrition across industries was seen in the ITeS

sector (21.9%) whereas the lowest attrition was seen in the Energy &

natural resources sector (10.5%)

Variable pay

The average variable pay across sectors is projected at 17.4% in

FY 2016, which is 0.4% points higher than the previous FY 2015

(17.0%)

Top compensation levers for retention

Long term incentive plans, strong performance based variable pay,

and monetary / non monetary recognition awards are the three most

widely used compensation levers for employee retention

Reasons for attrition

Better pay, better career opportunities and need for work life balance

have emerged as top reasons for attrition across industries

The highest projected

average increment is in

the Pharma sector at

12.1%, and the lowest

projection is observed in

the Retail sector at 9.4%

The highest projected

increments across

industries are at the

Junior Management

level at 11.0%

The highest projected

average variable pay is

in the BFSI sector at

19.4%, and the lowest

projection is observed in

the Logistics sector at

15.6%

The Consumer Business

sector shows

conservative projections

towards increments

along with an increased

focus towards variable

pay

9© 2015 Deloitte Touche Tohmatsu India Private Limited

Executive summary

Industry snapshotIn %

Auto and auto components 10.2 10.4 0.20

BFSI 9.7 10.0 0.30

Chemical 11.0 11.4 0.40

Consumer business 10.9 10.8 -0.10

Energy & natural resources 10.1 10.3 0.20

Engineering & manufacturing 10.4 10.6 0.20

Hi-Tech 10.6 10.9 0.30

ITeS 10.6 10.8 0.20

Infrastructure & real estate 10.2 12.0 1.80

Logistics 9.6 9.8 0.20

Media & advertising 10.0 10.9 0.90

Pharma, life sciences & healthcare 12.0 12.1 0.10

Retail 9.5 9.4 -0.10

Overall industry 10.3 10.7 0.40

SectorsActual Projected Change

Average increments

Actual

indicates

actual

figures for

FY 2014-15

Projected

Indicates

projected

figures for

FY 2015-16

Projected

Rank

17.0 17.4 0.40

16.5 16.7 0.20

19.4 20.1 0.70

16.3 16.5 0.20

19.2 19.6 0.40

15.9 16.2 0.30

16.7 17.0 0.30

17.2 17.6 0.40

17.1 17.5 0.40

17.6 18.2 0.60

15.3 15.6 0.30

15.7 16.1 0.40

18.3 18.7 0.40

16.0 16.3 0.30

Actual Projected Change

9

11

3

6

10

8

4

6

2

12

4

1

13

8

8

1

9

2

11

7

5

6

4

13

3

10

8

12

Average variable pay

Projected

Rank

10© 2015 Deloitte Touche Tohmatsu India Private Limited

Overall industry

report

Overall industry analysis

Average annual increments FY 2016 (projections) vis-à-vis FY 2015 (Actuals)

(Actuals)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

OverallIndustry

Auto BFSI Chem CB Energy Engg Hi-Tech ITeS Infra Log Media Pharma Retail

FY 2015 FY 2016

10.3 10.2 9.7 11.0 10.9 10.1 10.4 10.6 10.6 10.2 9.6 10.0 12.0 9.5

10.7 10.4 10.0 11.4 10.8 10.3 10.6 10.9 10.8 12.0 9.8 10.9 12.1 9.4

FY 2015

FY 2016

In %

Consumer business and

Retail sectors show a

decrease in projected

increments for FY 2016

vis-à-vis last FY

Infrastructure and real

estate has the maximum

increase in projected

average increments over

previous FY

In Pharma, Media, Hi-Tech

and ITeS sectors, the

projected increments are

significantly higher than

Industry average whereas

Logistics and Retail have

lower than industry average

increment projections

12© 2015 Deloitte Touche Tohmatsu India Private Limited

Overall industry analysis

Average annual increments FY 2016 (projections) vis-à-vis FY 2015

In % 10P 50P 90P Avg

Clerical 7.4 10.7 14.2 10.8

JM 7.6 11.1 14.5 11.0

MM 7.3 10.6 14.1 10.6

SM 7.1 10.5 13.8 10.5

TM 7.0 10.5 13.8 10.4

Level-wise increment percentiles (FY 2016) Average increments across levels

10.8

11.0

10.610.5

10.4

10.410.6

10.310.1

10.0

9.4

9.6

9.8

10.0

10.2

10.4

10.6

10.8

11.0

11.2

Clerical JM MM SM TM

FY 2016 FY 2015

In %

In % 10P 50P 90P Average

FY 2015 6.7 10.2 14.0 10.3

FY 2016 6.9 10.6 14.4 10.7

13© 2015 Deloitte Touche Tohmatsu India Private Limited

Overall industry analysis

Annual increments FY 2016 (projections)

In %Comparison of level-wise average increments across sectors

10.8 10.5 10.1 11.4 10.8 10.7 10.4 10.9 10.9 12.1 9.8 11.0 12.2 9.4

11.0 10.8 10.511.9 11.2 11.0 10.8 11.3 11.2

12.510.3

11.312.5

9.8

10.6 10.4 9.911.3

10.7 10.5 10.3 10.8 10.711.8

9.710.8

11.9

9.3

10.5 10.2 9.6

11.110.5 10.3 10.1

10.6 10.6

11.6

9.5

10.6

11.7

9.2

10.4 10.29.6

11.110.5 10.3 10.1

10.6 10.5

11.5

9.4

10.6

11.6

9.1

OverallIndustry

Auto BFSI Chem CB Eng Energy Hi-Tech ITeS Infra Log Media Pharma Retail

TM

SM

MM

JM

CL

The average increment

projections at Top, Senior

and Middle management

level are lower than the

projected Industry

average at 10.7%

The average increments at

all levels in Pharma,

Infrastructure and

Chemicals sectors are

significantly higher than the

respective level-wise

industry average

The average increments at

all levels in BFSI, Logistics

and Retail are lower than

respective level-wise

industry average

14© 2015 Deloitte Touche Tohmatsu India Private Limited

Overall industry analysis

Average annual variable pay FY 2016 (projections) vis-à-vis FY 2015

(Actuals)

0.0

5.0

10.0

15.0

20.0

25.0

OverallIndustry

Auto BFSI Chem CB Energy Engg Hi-Tech ITeS Infra Log Media Pharma Retail

FY 2015 FY 2016

17.0 16.5 19.4 16.3 19.2 15.9 16.7 17.2 17.1 17.6 15.3 15.7 18.3 16.0

17.4 16.7 20.1 16.5 19.6 16.2 17.0 17.6 17.5 18.2 15.6 16.1 18.7 16.3

FY 2015

FY 2016

In %

BFSI and Infrastructure

and real estate have the

maximum increase in

projected average variable

pay over previous FY

Logistics and Media have

projected lower than

average industry average

variable pay

In BFSI, Pharma and

consumer business, the

projected average variable

pay are significantly higher

than Industry average

15© 2015 Deloitte Touche Tohmatsu India Private Limited

Overall industry analysis

Average annual variable pay FY 2016 (projections) vis-à-vis FY 2015

In % 10P 50P 90P Avg

Clerical 5.6 10.3 18.2 10.4

JM 7.5 13.6 23.6 13.5

MM 10.2 17.6 29.4 17.5

SM 14.8 22.1 34.5 22.1

TM 16.5 24.3 38.1 24.2

Level-wise variable pay percentiles (FY 2016) Average variable pay across levels

10.4

13.5

17.5

22.1

24.2

10.2

13.1

17.2

21.7

23.7

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

Clerical JM MM SM TM

FY 2016 FY 2015

In %

In % 10P 50P 90P Average

FY 2015 5.6 17.1 34.8 17.0

FY 2016 5.9 17.6 35.3 17.4

16© 2015 Deloitte Touche Tohmatsu India Private Limited

Overall industry analysis

Annual variable pay FY 2016 (projections)

In %Comparison of level-wise average increments across sectors

10.4 9.7 11.9 9.5 11.8 9.9 9.2 10.6 10.5 10.9 8.6 9.1 10.7 9.3

13.5 12.715.2

12.614.9

12.9 12.3 13.7 13.6 14.111.6 12.2 13.9 12.4

17.5 16.5

19.8

16.419.3

16.8 16.217.5 17.5 18.0

15.6 16.218.4

16.1

22.121.4

25.3

21.2

24.6

21.8 20.922.4 22.3 23.0

20.2 20.8

23.6

21.0

24.223.3

27.4

23.1

26.8

23.722.8

24.4 24.3 24.9

22.5 22.6

25.6

22.8

OverallIndustry

Auto BFSI Chem CB Eng Energy Hi-Tech ITeS Infra Log Media Pharma Retail

TM

SM

MM

JM

CL

The average variable pay

projections at Clerical and

Junior management level

are lower than the

projected Industry

average at 17.4%

The average variable pay

projections at all levels in

BFSI and Consumer

Business sectors are

significantly higher than the

respective level-wise

industry average

The average projected

variable pay at all levels in

Logistics, Media and

Energy is lower than

respective level-wise

industry average

17© 2015 Deloitte Touche Tohmatsu India Private Limited

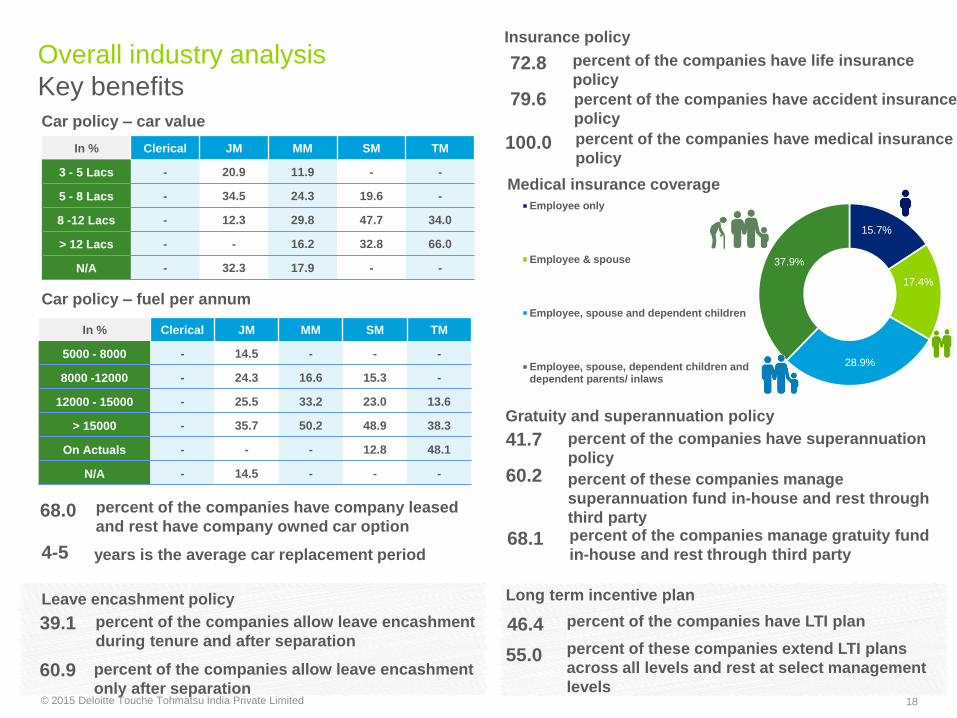

Overall industry analysis

Key benefits

Car policy – car value

In % Clerical JM MM SM TM

3 - 5 Lacs - 20.9 11.9 - -

5 - 8 Lacs - 34.5 24.3 19.6 -

8 -12 Lacs - 12.3 29.8 47.7 34.0

> 12 Lacs - - 16.2 32.8 66.0

N/A - 32.3 17.9 - -

Car policy – fuel per annum

In % Clerical JM MM SM TM

5000 - 8000 - 14.5 - - -

8000 -12000 - 24.3 16.6 15.3 -

12000 - 15000 - 25.5 33.2 23.0 13.6

> 15000 - 35.7 50.2 48.9 38.3

On Actuals - - - 12.8 48.1

N/A - 14.5 - - -

percent of the companies have company leased

and rest have company owned car option

Insurance policy

15.7%

17.4%

28.9%

37.9%

Employee only

Employee & spouse

Employee, spouse and dependent children

Employee, spouse, dependent children anddependent parents/ inlaws

Medical insurance coverage

years is the average car replacement period

percent of the companies allow leave encashment

during tenure and after separation

percent of the companies allow leave encashment

only after separation

Leave encashment policy

percent of the companies have life insurance

policy

percent of the companies have accident insurance

policy

percent of the companies have superannuation

policy

percent of these companies manage

superannuation fund in-house and rest through

third party

Gratuity and superannuation policy

percent of the companies manage gratuity fund

in-house and rest through third party

percent of the companies have medical insurance

policy

Long term incentive plan

percent of the companies have LTI plan

percent of these companies extend LTI plans

across all levels and rest at select management

levels

68.0

39.1

4-5

60.9

72.8

79.6

100.0

41.7

60.2

68.1

46.4

55.0

18© 2015 Deloitte Touche Tohmatsu India Private Limited

Overall industry analysis

Voluntary attrition analysis

0

5

10

15

20

25

OverallIndustry

Auto BFSI Chem CB Eng Energy Hi-Tech ITeS Infra Log Media Pharma Retail

FY 2014 FY 2015

16.2 11.4 18.7 10.6 18.4 10.9 10.4 19.4 21.5 17.5 16.6 17.2 18.2 18.9

16.5 11.6 18.9 10.7 18.7 11.1 10.5 19.9 21.9 17.8 16.8 17.5 18.6 19.4

FY 2014

FY 2015

In %

Comparison of level-wise voluntary attrition rate across sectors

Voluntary attrition rate across sectors

In %

24.8 22.228.4

16

26.317.5 15.2

29.8 32.328.1 24.6 25.8 26.1 29.2

19.317.2

21.2

13.3

20.6

14.311.4

2124

20.921.5 21.2 21.1

23.1

9.8

8.2

10.3

7.5

10.4

9.3

7.3

10.6

11.2

10.110.3 10.8 10.2

10.74.8

3.1

5.1

2.6

5.8

4.1

2.2

5.8

6.1

4.94.5 4.9 5.5

6.63.3

2.5

4.6

1.8

4.1

2.8

1.6

4.8

4.9

3.9 2.3 2.7 3.1 4.2

OverallIndustry

Auto BFSI Chem CB Eng Energy Hi-Tech ITeS Infra Log Media Pharma Retail

TM

SM

MM

JM

CL

19© 2015 Deloitte Touche Tohmatsu India Private Limited

Overall industry analysis

Attrition trends – reasons and mitigation measures

Top three

reasons for

attrition

Top three

compensation

levers for

talent retention

Top three

compensation

levers for

talent

attraction

Better pay elsewhere1

2

3

Better career opportunities

Better work life balance

Sign on bonuses1

2

3

Guaranteed incentives / variable pay

Attractive benefits offerings

1

2

3

Long term incentive plans

Performance based variable pay

Recognition awards (cash/non-cash)

20© 2015 Deloitte Touche Tohmatsu India Private Limited

About Deloitte Human

Capital Consulting

About Deloitte

Human Capital ConsultingDeloitte Consulting’s Human Capital practice is a leading global advisor and implementation partner working with companies, governments,

and organizations around the world. Our goal is to improve our clients’ organizational results and impact by focusing on challenges at the

intersection of business and people.

Our global network of more than 5,000 Human Capital professionals serves 100 countries. The scale of our global Human Capital partner

and practitioner network allows us to provide global and national clients with a network, which can respond quickly, flexibly, and at scale to

meet client challenges. Our practice goes to market applying deep industry experience and globally recognized HR, talent, and organization

transformation skills and capabilities. We offer a focused combination of breadth and expertise across HR service lines.

Our India offerings:

Organization Transformation,

Talent & Rewards

HR

Transformation

Strategic Change

Culture

Leadership Development

Organization Design

Technology Adoption

Talent Strategies:

• Career Development and Succession

• Diversity and Inclusion

• Performance, Engagement, and Retention

• Talent Sourcing

• Talent Strategies for Growth Markets

Learning Solutions

Sales Force Effectiveness

Rewards

• Job Evaluation

• Structuring & Benchmarking

• Incentive Plan Design

HR Transformation Strategy and Planning

HR Technology Strategy

HR Service Delivery:

• HR Shared Services

• High Impact HR Operating Model

• Outsourcing Advisory

HR Technologies:

• Oracle - EBS, HCM Cloud, PeopleSoft and Taleo

• SAP / SuccessFactors

• Salesforce.com

• Workday

• Cornerstone

• HR Technology – Other

Workforce Analytics

India Operations Setup:

• India Operations HR Setup

• Location Feasibility Study

• Rules And Regulations

• Employment Contract

Mergers, Acquisitions and Restructuring

22© 2015 Deloitte Touche Tohmatsu India Private Limited

Contact us

For sector specific reports and technical queries, please reach

out to:

Dr. Vishalli Dongrie, Sr. Director, Human Capital Consulting

Tel/Direct: +91 (22) 6185 4280 l Mobile: +91 98 3397 3458 l E-mail: [email protected]

Saptarshi Chatterjee, Senior Manager, Human Capital Consulting

Tel/Direct: +91 (22) 6185 4280 l Mobile: +91 98 1995 1648 l E-mail: [email protected]

Mandar Ranade, Senior Consultant, Human Capital Consulting

Tel/Direct: +91 (22) 6185 4280 l Mobile: +91 98 3369 1813 l E-mail: [email protected]

Malvika Sharma, Consultant, Human Capital Consulting

Tel/Direct: +91 (22) 6185 4280 l Mobile: +91 98 1991 2990 l E-mail: [email protected]

23© 2015 Deloitte Touche Tohmatsu India Private Limited

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and

their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not

provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

This survey is a general survey carried out by Deloitte Touche Tohmatsu India Private Limited (DTTIPL) and data or information provided by you will be used

in connection with this survey, other studies or analyses performed by DTTIPL. This survey and the survey results are the proprietary property of DTTIPL and

will be disclosed only if required by law or in connection with this survey or such studies, analyses or services, however the data or information provided would

not contain any information that identifies you or associates with you the responses you have provided.

None of DTTIPL or its affiliate entities (Deloitte Network) are by means of this survey or the survey results, rendering professional advice or services. Neither

this survey nor the survey results is a substitute for any kind of professional advice or services. The Deloitte network is not responsible for any loss

whatsoever sustained by any person who relies on this survey or the survey results.

©2015 Deloitte Touche Tohmatsu India Private Limited. Member of Deloitte Touche Tohmatsu Limited

![HD Видеокамера HC-V770 HC-V760 HC-VX870 HC-VX870M · hc-v770 [v770] Серияv770 / серия [v770] hc-v770m [v770m] hc-v760 [v760] – Данная инструкция](https://static.fdocuments.net/doc/165x107/5e697831d35b2b14c40ee20b/hd-hc-v770-hc-v760-hc-vx870-hc-vx870m-hc-v770-v770-v770.jpg)