IMS Latin America Review 2004

137

March 15, 2022 © 2002 IMS Health Incorporated or its affiliates. All rights reserved. Strategic review of the pharmaceutical markets in the Latin America/Canada Region Prepared by IMS for Abbott - January 2004

-

Upload

yolanda-cristina-aguiar-morazzani -

Category

Documents

-

view

218 -

download

0

description

Revisión Mercado Latinoamericanos según IMS

Transcript of IMS Latin America Review 2004

April 15, 2023

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Strategic review of the pharmaceutical markets in the Latin America/Canada Region

Prepared by IMS for Abbott - January 2004

April 15, 20232

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Contents

• Introduction — The Global Pharmaceutical Market

• Latin America/Canada: Regional Overview

• Appendix: Latin America — Country Deep Dive

April 15, 20233

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

The Global Pharmaceutical Market

April 15, 20234

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Global Overview

• Worldwide industry growth slowed

• Cost containment measures universal

• R&D productivity slow to improve

• Generics continue to erode sales growth but not increase volume

Source: IMS Health: MIDAS, MAT September 2003

April 15, 20235

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Economic Environment

• Recovery from the recent economic slowdown has been slower than expected

• Governments are increasing spending in an effort to kick-start growth, but deficits are growing as a result

• Performance of the US economy will continue to have a major impact on global economic growth prospects

Source: IMS Health: IMS Market Prognosis Global Data 2003-2007

April 15, 20236

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

World Population 2003-2007

• World population to reach 6.6 billion by 2007 - growth concentrated in developing regions

• Declining birth rates and increases in life expectancy will continue to drive a gradual shift in the global demographic profile

• These trends will continue to drive up both pharmaceutical consumption and the cost of healthcare provision in both developed and developing countries

Source: IMS Health: IMS Market Prognosis Global Data 2003-2007

April 15, 20237

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

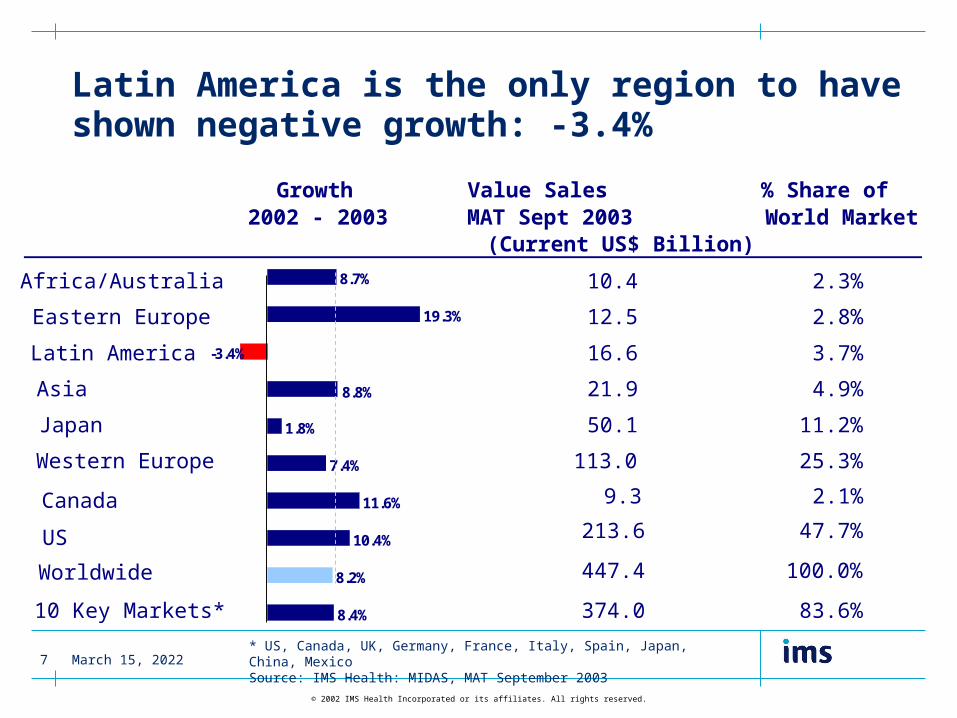

Latin America is the only region to have shown negative growth: -3.4%

Growth2002 - 2003

Value Sales MAT Sept 2003 (Current US$ Billion)

% Share of World Market

Africa/Australia 10.4 2.3%

Eastern Europe 12.5 2.8%

Latin America 16.6 3.7%

Asia 21.9 4.9%

Japan 50.1 11.2%

Western Europe 113.0 25.3%

US 213.6 47.7%

Worldwide 447.4 100.0%

10 Key Markets* 374.0 83.6%8.4%

8.2%

10.4%

11.6%

7.4%

1.8%

-3.4%

19.3%

8.7%

8.8%

* US, Canada, UK, Germany, France, Italy, Spain, Japan, China, MexicoSource: IMS Health: MIDAS, MAT September 2003

Canada 9.3 2.1%

April 15, 20238

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

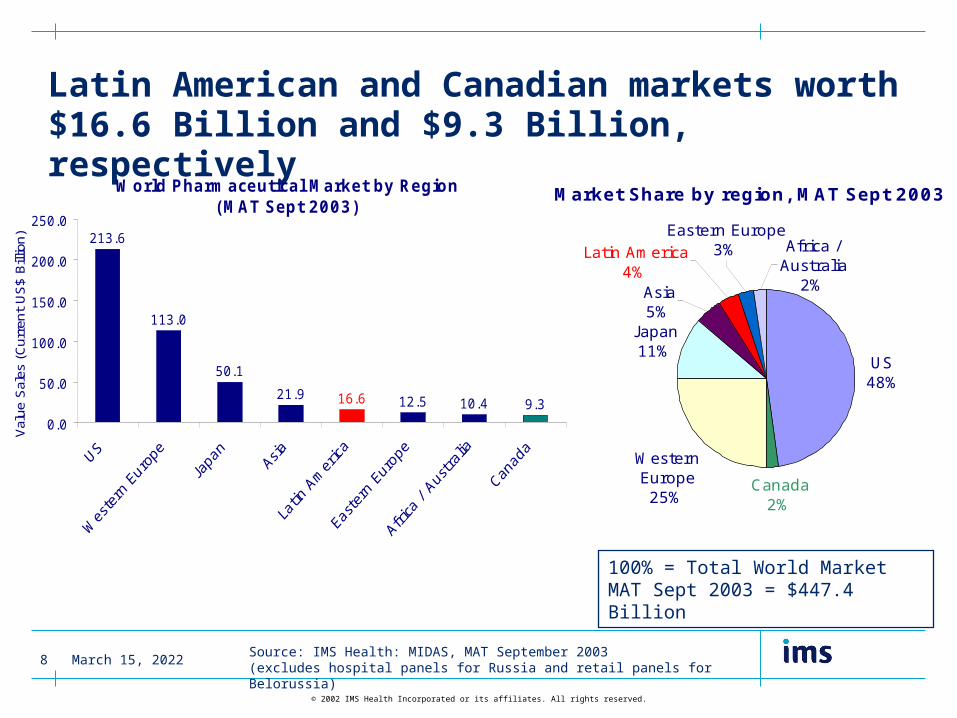

Latin American and Canadian markets worth $16.6 Billion and $9.3 Billion, respectively

World Pharmaceutical Market by Region(MAT Sept 2003)

213.6

113.0

50.1

21.9 12.5 10.4 9.316.6

0.0

50.0

100.0

150.0

200.0

250.0

Val

ue S

ales

(C

urre

nt U

S$

Bill

ion)

100% = Total World Market MAT Sept 2003 = $447.4 Billion

Source: IMS Health: MIDAS, MAT September 2003(excludes hospital panels for Russia and retail panels for Belorussia)

Market Share by region, MAT Sept 2003

Western Europe25%

J apan11%

US 48%

Canada2%

Latin America4%

Asia5%

Eastern Europe3% Africa /

Australia2%

April 15, 20239

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

12.8

0

5

10

15

Australia

12.5

0

5

10

15

USA

7.1

05

1015

LatinAmerica

1.9

0

5

10

15

J apan

10.7

0

5

10

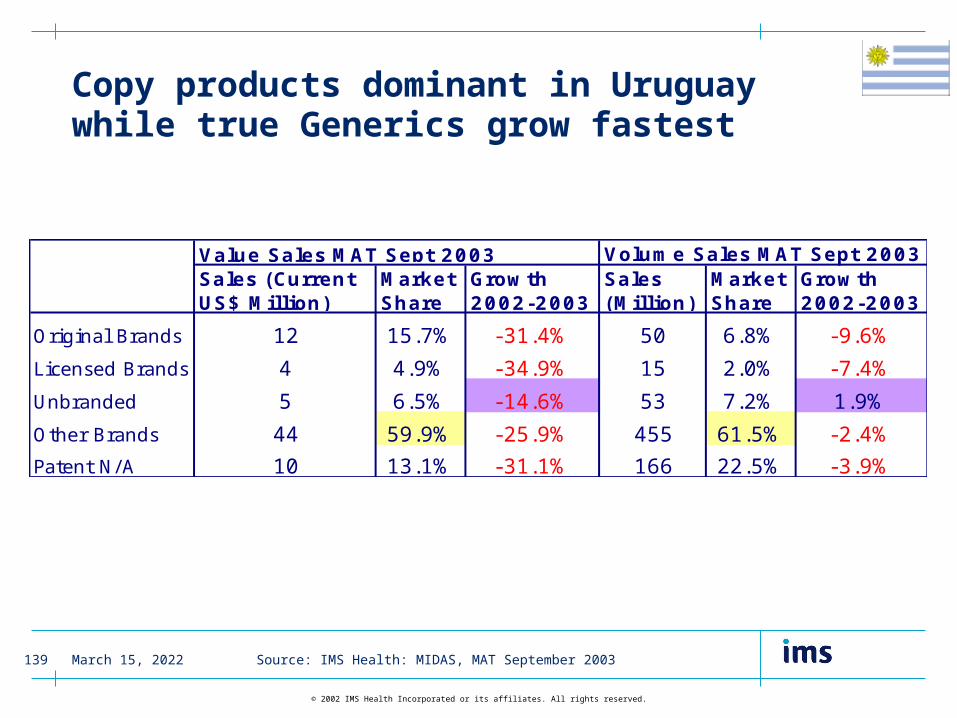

15

Asia

8.0

05

1015

Top 5Europe

9.7

0

5

10

15

Global

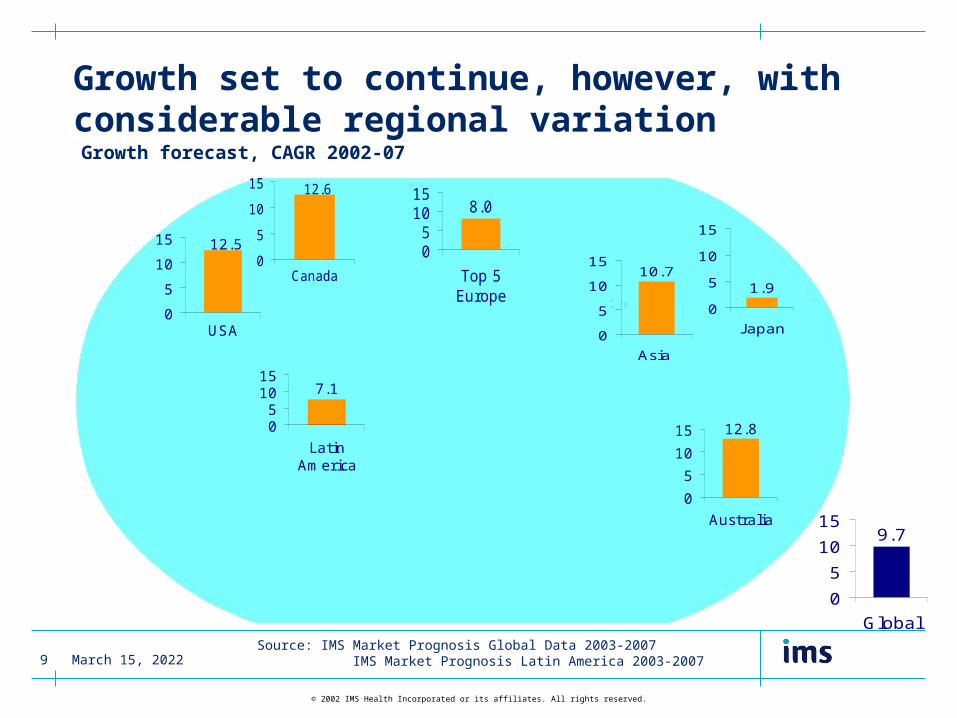

Growth set to continue, however, with considerable regional variationGrowth forecast, CAGR 2002-07

12.6

0

5

10

15

Canada

Source: IMS Market Prognosis Global Data 2003-2007 IMS Market Prognosis Latin America 2003-2007

April 15, 202310

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Latin America/Canada:Regional Overview

• The Pharmaceutical Market

• Political, business & healthcare environment

• Abbott’s performance in the region

April 15, 202311

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

The Latin American/ Canada Pharmaceutical Market, 2003market value (current US$ billion, ex-manufacturer prices)

0 1 2 3 4 5 6 7 8 9 10

Canada

Mexico

Brazil

Argentina

Puerto Rico

Colombia

Venezuela

Central America

Chile

Equador

Peru

Dominican Republic

Uruguay

Other Markets

Canada

Latin America is a highly diverse region Market sizes ranging from US$7.1 Billion in Mexico to US$0.2 Billion in Uruguay

* C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama; Retail/non-retail split not available for Central America and other markets

Source: IMS Market Prognosis Global Data 2003-2007 IMS Market Prognosis Latin America 2003-2007

Retail sales

Unaudited non-retail sales

9.2

7.1

4.9

1.6

1.3

1.2

1.2

0.8

0.6

0.5

0.4

0.3

0.2

0.3

** Canada, Puerto Rico include audited hospital sales

April 15, 202312

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

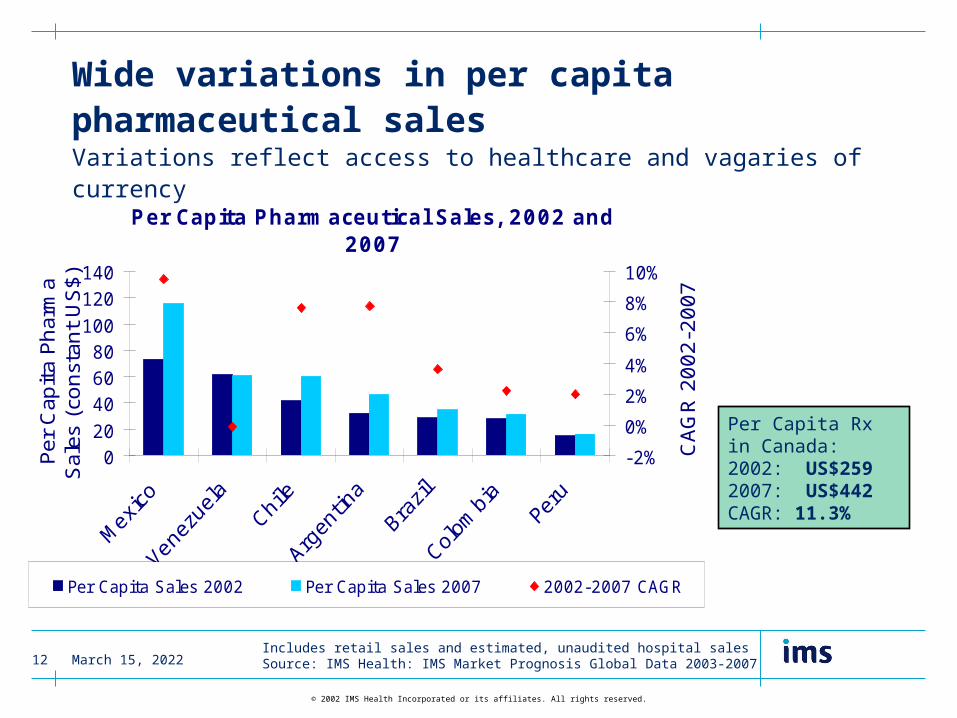

Wide variations in per capita pharmaceutical sales Variations reflect access to healthcare and vagaries of currency

Includes retail sales and estimated, unaudited hospital salesSource: IMS Health: IMS Market Prognosis Global Data 2003-2007

Per Capita Rx in Canada:2002: US$2592007: US$442CAGR: 11.3%

Per Capita Pharmaceutical Sales, 2002 and 2007

020406080

100120140

Per

Cap

ita

Phar

ma

Sal

es (

const

ant

US

$)

-2%

0%

2%

4%

6%

8%

10%

CA

GR

2002-2

007

Per Capita Sales 2002 Per Capita Sales 2007 2002-2007 CAGR

April 15, 202313

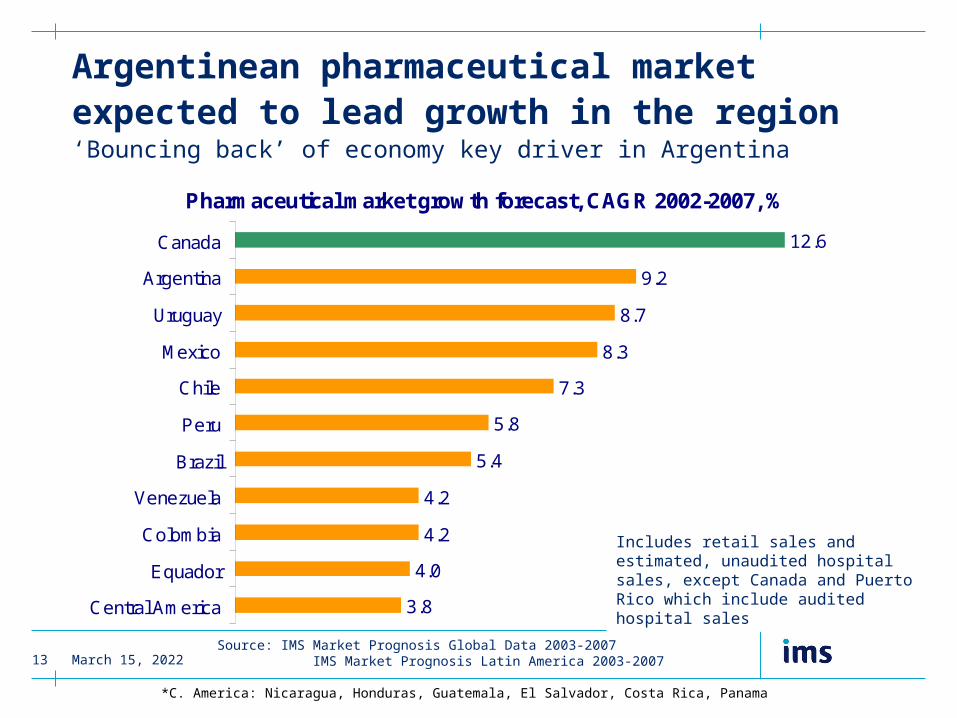

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.*C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama

Pharmaceutical market growth forecast, CAGR 2002-2007, %

3.8

4.0

4.2

4.2

5.4

5.8

7.3

8.3

8.7

9.2

12.6

Central America

Equador

Colombia

Venezuela

Brazil

Peru

Chile

Mexico

Uruguay

Argentina

Canada

Argentinean pharmaceutical market expected to lead growth in the region‘Bouncing back’ of economy key driver in Argentina

Source: IMS Market Prognosis Global Data 2003-2007 IMS Market Prognosis Latin America 2003-2007

Includes retail sales and estimated, unaudited hospital sales, except Canada and Puerto Rico which include audited hospital sales

April 15, 202314

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Considerable variation in size of economies and per capita GDP

Source: Central Banks; World bank; estimated figures

C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama

US GDP:US$10,450 billion

US per capita GDP:US$36,300

GDP (US$ billion)

715

605

453

263

79

77

77

71

58

26

19

0 100 200 300 400 500 600 700 800

Canada

Mexico

Brazil

Argentina

Central America

Venezuela

Colombia

Chile

Peru

Ecuador

Uruguay

Per capita GDP (US$ thousand)

23.1

6.2

2.6

6.9

2.1

3.1

1.8

4.6

2.2

2.0

5.7

0 5 10 15 20 25

Canada

Mexico

Brazil

Argentina

Central America

Venezuela

Colombia

Chile

Peru

Ecuador

Uruguay

April 15, 202315

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

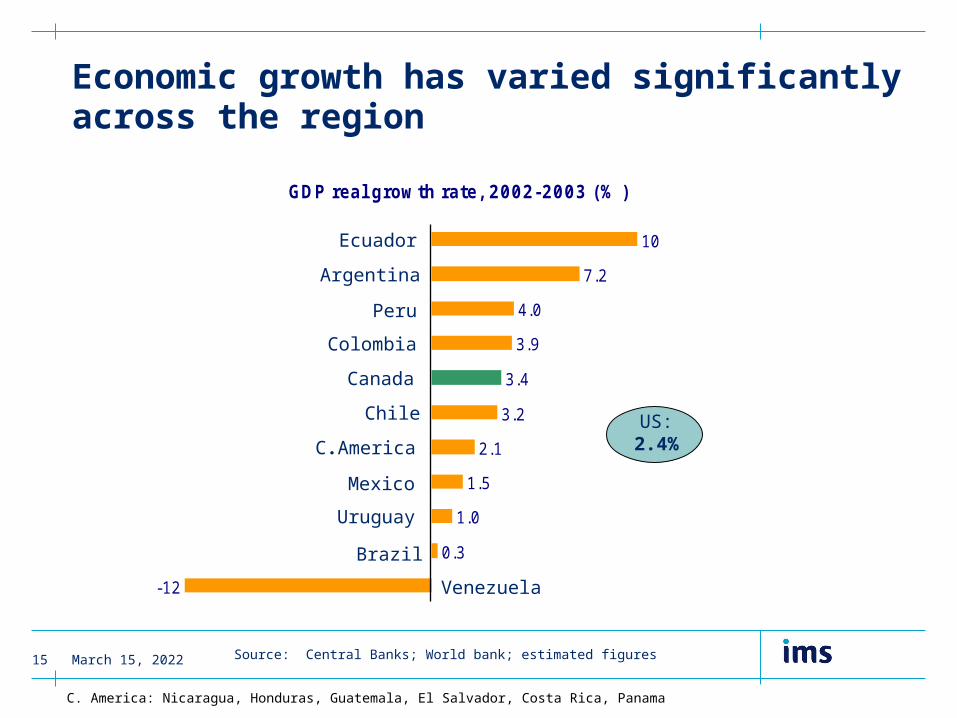

GDP real growth rate, 2002-2003 (% )

10

7.2

4.0

3.9

3.4

3.2

2.1

1.5

1.0

0.3

-12

Economic growth has varied significantly across the region

Canada

Colombia

Mexico

Chile

Peru

Brazil

Venezuela

Uruguay

Argentina

C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama

US:2.4%

Ecuador

Source: Central Banks; World bank; estimated figures

C.America

April 15, 202316

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

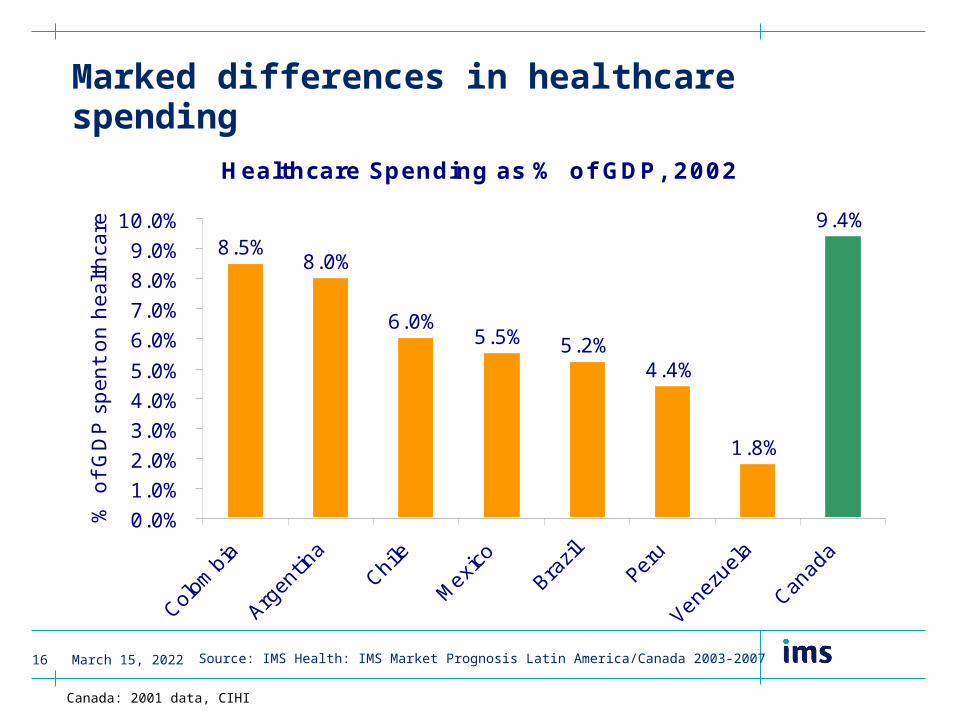

Marked differences in healthcare spending

Source: IMS Health: IMS Market Prognosis Latin America/Canada 2003-2007

Canada: 2001 data, CIHI

Healthcare Spending as % of GDP, 2002

8.5%8.0%

6.0%5.5% 5.2%

4.4%

1.8%

9.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

% o

f G

DP s

pen

t on h

eal

thca

re

April 15, 202318

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

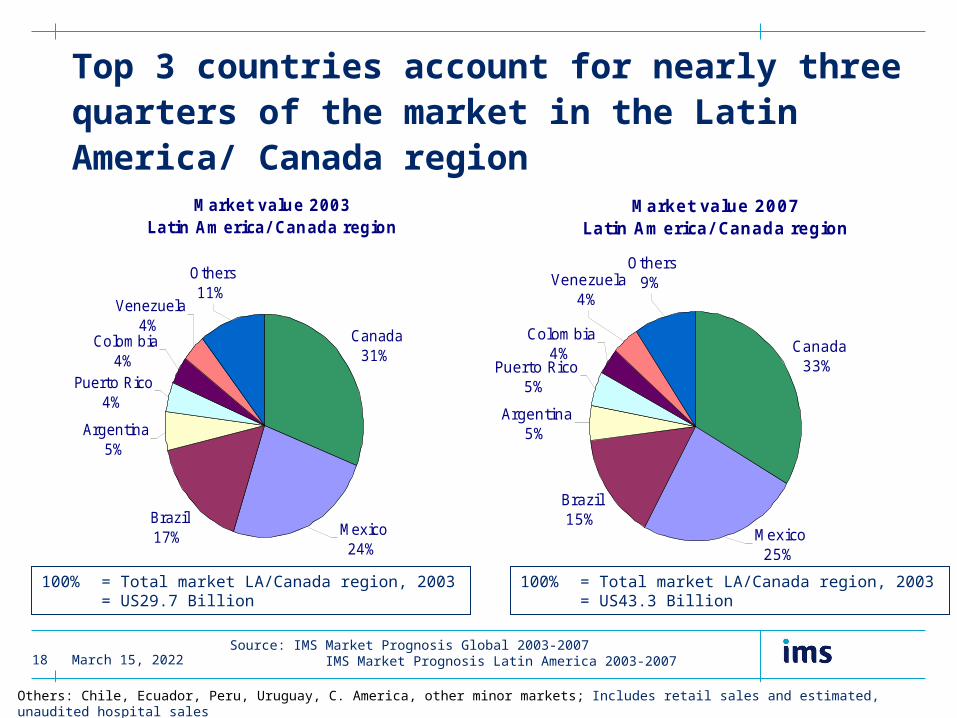

Top 3 countries account for nearly three quarters of the market in the Latin America/ Canada region

Source: IMS Market Prognosis Global 2003-2007 IMS Market Prognosis Latin America 2003-2007

100% = Total market LA/Canada region, 2003 = US29.7 Billion

Market value 2003Latin America/ Canada region

Canada31%

Brazil17%

Argentina5%

Puerto Rico4%

Mexico24%

Colombia4%

Venezuela4%

Others11%

Market value 2007Latin America/ Canada region

Canada33%

Brazil15%

Argentina5%

Puerto Rico5%

Mexico25%

Others9%Venezuela

4%

Colombia4%

100% = Total market LA/Canada region, 2003 = US43.3 Billion

Others: Chile, Ecuador, Peru, Uruguay, C. America, other minor markets; Includes retail sales and estimated, unaudited hospital sales

April 15, 202319

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Market value, 2003 and 2007

0

2

4

6

8

10

12

14

16

Mark

et

valu

e (

curr

en

t U

S$

billion

s)

Canad

a

Mexican and Brazilian markets combined worth US$17.2 Billion by 2007

2003

2007

Source: IMS Market Prognosis Global Data 2003-2007 IMS Market Prognosis Latin America 2003-2007

Others: Chile, Ecuador, Peru, Uruguay, C. America, other minor markets; Includes retail sales and estimated, unaudited hospital sales

7.1

10.7

4.9

6.6

14.4

9.2

April 15, 202320

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

42.6 47.7 52.159.8

46.6 49.6

16.9 2.47.6

4.0

19.1 10.5

21.127.4

18.523.6

12.8 22.2

19.4 22.5 21.812.6

21.5 17.7

Canada Mexico Brazil Argentina Colombia Venezuela

Higher share of ‘other brands’ in Latin American markets due to copy products

C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama

Not yet assigned/not patentable

Original andlicensed brands

Unbranded

Other brands(e.g. branded generics and copy products)

Source: IMS Health: MIDAS, MAT September 2003

100% = Total volume sales 2003

Volume market share by product licensing status, (%)

Canada

April 15, 202321

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

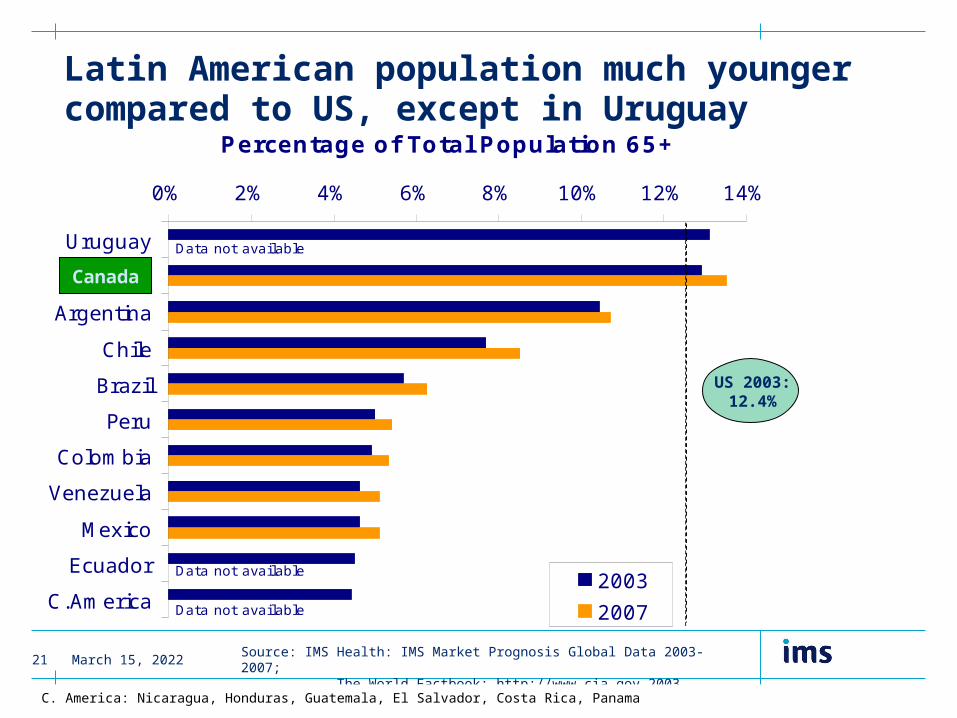

0% 2% 4% 6% 8% 10% 12% 14%

Uruguay

Canada

Argentina

Chile

Brazil

Peru

Colombia

Venezuela

Mexico

Ecuador

C.America

Percentage of Total Population 65+

2003

2007

Data not available

Data not available

Data not available

Latin American population much younger compared to US, except in Uruguay

Source: IMS Health: IMS Market Prognosis Global Data 2003-2007; The World Factbook: http://www.cia.gov 2003

US 2003:12.4%

C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama

Canada

April 15, 202322

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Latin America/Canada: Political, Business and Healthcare Environment

April 15, 202323

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Political and Economic context

• Fragile economies and political instability will continue to affect the operating environment for pharmaceutical companies in most Latin American markets

• The currencies in all Latin American countries tend to be at risk from economic and political problems of their neighbours, while Mexico is particularly susceptible to movement in the US dollar

• The exchange rates are forecast to stabilise from 2004-05 onwards as the Latin American economies recover

• Progress towards increasingly open, market-led economies should benefit the pharmaceutical industry in the medium to long term

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

April 15, 202324

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Economic context

• Canada has had the fastest growing GDP among the G7 group over the past two years, largely driven by buoyant domestic demand

• In addition, Canada has the strongest fiscal position among the G7 group with the Canadian budget in surplus for five consecutive years

• Canada is vulnerable to fluctuations of the US economy:US accounts for 73% of imports and 85% of exports

Source: IMS Market Prognosis Canada 2003-2007

April 15, 202325

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Healthcare environment

• Lack of access to healthcare for large segments of the population in several Latin American countries

• Healthcare primarily provided through the public system, with little in the way of a primary care infrastructure

• Corruption and inefficiency within the public health sectors are rife, despite increasing government attempts to address the problems

• Hard-pressed governments will continue to implement healthcare cost-containment policies wherever possible - pharmaceutical spending being a key target

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

April 15, 202326

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Healthcare environment

• Healthcare in Canada is publicly financed and privately delivered through the Medicare system

• Spiralling costs have prompted calls for a National Healthcare Reform, looking into

– Introducing new protection against ‘catastrophic’ prescription drug expenses

– Establishing a National Drugs Agency to evaluate drugs, regulate pricing, develop a National Formulary and control costs

– Reviewing patent legislation to facilitate access to generics

– Introducing health management approach to primary care

Source: IMS Market Prognosis Canada 2003-2007

April 15, 202327

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Pharmaceutical business environment

• Growth of the pharmaceutical market is mainly driven by increasing demand and introduction of new drugs

• Cost containment measures, including a common drug review process, are putting downward pressure on market growth

– While higher prices for innovative treatment have been widely accepted, drugs categorised as less innovative will be the major target for containing cost

• The operating environment over the next few year looks set to be volatile while the healthcare reform is being debated

• Approval of new drugs by Health Canada is the slowest among OECD countries — 717 days in 2001

Source: IMS Market Prognosis Canada 2003-2007

April 15, 202328

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Pricing

• Prescription drug prices remain free from direct government control in most major markets, with the exception of Brazil

• The reintroduction of government price controls remains a potential threat in Colombia and Argentina

• Given the recent economic turmoil, massive discounting as a marketing tool is widespread across the region

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

April 15, 202329

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Pricing

• Prices of patented drugs in Canada are controlled by the Patented Medicines Prices Review Board (PMPRB)

• The PMPRB monitors Canadian prices in comparison to seven countries: US, UK, France, Germany, Italy, Sweden, Switzerland

• Price increases for individual products are tightly controlled and limited to rises in the Consumer Price Index (CPI)

– Pharmaceutical Manufacturers Price Index (PMPI) has increased by just 0.8% vs. 2.6% increase of the CPI between 1998-2001

• Introduction of the Common Review Process is likely to exert more downward pressure on prices

Source: IMS Market Prognosis Canada 2003-2007

April 15, 202330

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Copy products

• Copy products will continue to account for substantial share of most Latin American markets

• Only gradual improvements in levels of intellectual property protection

• Some governments in the region will hesitate to introduce stronger patent protection - conflict regional/international trade agreements vs. protection of national pharmaceutical industries

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

April 15, 202331

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Generics

• Seen by many governments in the Latin American region as the key to providing quality medicines at affordable prices

• Extensive copy product markets and the brand-consciousness of both prescribers and patients are major barriers to generics uptake

• Brazil has been most successful: true generics claiming 8% share of the Brazilian market by volume just 2 years after the first approval of bio-equivalent products

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

April 15, 202332

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Generics

• While 42% of prescriptions written in Canada are generic, generic drugs accounted for only 14% of the value of the total retail and hospital markets in 2002

• Generics prices are not regulated by the PMPRB; market forces exert downward pressure, e.g., provincial formularies, new entrants, purchasing power of pharmacy chains

• The generics sector has experienced significant consolidation in recent years driven by entry of global players (Teva, Ratiopharm)

• The generics industry would benefit from the healthcare reform, esp. the review of patent legislation

Source: IMS Market Prognosis Canada 2003-2007

April 15, 202333

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Abbott’s performance in the Latin America/Canada region

April 15, 202334

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

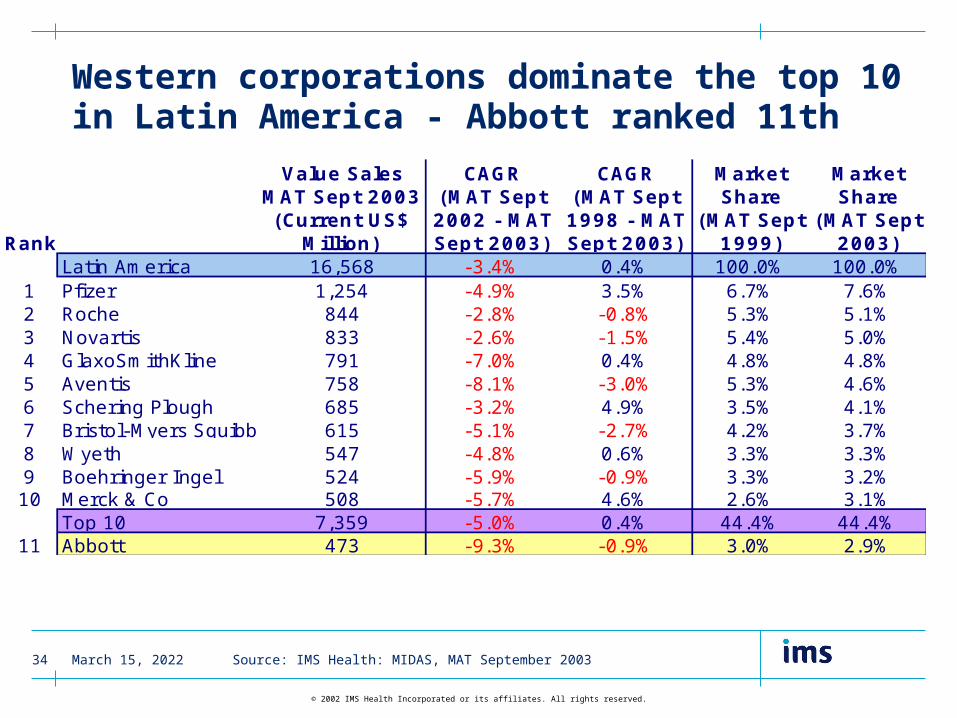

Western corporations dominate the top 10 in Latin America - Abbott ranked 11th

Source: IMS Health: MIDAS, MAT September 2003

Rank

Value Sales MAT Sept 2003 (Current US$

Million)

CAGR (MAT Sept 2002 - MAT Sept 2003)

CAGR (MAT Sept 1998 - MAT Sept 2003)

Market Share

(MAT Sept 1999)

Market Share

(MAT Sept 2003)

Latin America 16,568 -3.4% 0.4% 100.0% 100.0%1 Pfizer 1,254 -4.9% 3.5% 6.7% 7.6%2 Roche 844 -2.8% -0.8% 5.3% 5.1%3 Novartis 833 -2.6% -1.5% 5.4% 5.0%4 GlaxoSmithKline 791 -7.0% 0.4% 4.8% 4.8%5 Aventis 758 -8.1% -3.0% 5.3% 4.6%6 Schering Plough 685 -3.2% 4.9% 3.5% 4.1%7 Bristol-Myers Squibb 615 -5.1% -2.7% 4.2% 3.7%8 Wyeth 547 -4.8% 0.6% 3.3% 3.3%9 Boehringer Ingel 524 -5.9% -0.9% 3.3% 3.2%10 Merck & Co 508 -5.7% 4.6% 2.6% 3.1%

Top 10 7,359 -5.0% 0.4% 44.4% 44.4%11 Abbott 473 -9.3% -0.9% 3.0% 2.9%

April 15, 202335

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Pfizer, Schering-Plough and Merck have strongly out-grown the market over past 5 years

Source: IMS Health: MIDAS, MAT September 2003

Top 11 Corporations in Latin America

PFIZER (1)

ROCHE (2)NOVARTIS (3)

GSK (4)AVENTIS (5)

SCHERING PLOUGH (6)

BRISTOL-MYERS SQB. (7)

WYETH (8)

BOEHRINGER INGEL (9)

MERCK & CO (10)ABBOTT (11)

0%

1%

2%

3%

4%

5%

6%

7%

8%

-4% -2% 0% 2% 4% 6%

CAGR 5 Years (1998-2003)

Mar

ket

Sha

re

LATINAMERICA

April 15, 202336

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

One generics company, Apotex, among the top 10 corporations in Canada

Shading represents Domestic Corporations

Rank Corporation

Value Sales MAT Sept 2003 (Current US$

Million)

Growth (MAT Sept

2002 - MAT Sept 2003)

CAGR (MAT Sept

1999 - MAT Sept 2003)

Market Share

(MAT Sept 1999)

Market Share

(MAT Sept 2003)

Canada 9,826 11.6% 13.9% 100.0% 100.0%1 Pfizer 1,374 11.0% 19.3% 11.6% 14.0%2 GlaxoSmithKline 748 7.3% 11.3% 8.4% 7.6%3 AstraZeneca 652 12.7% 14.9% 6.4% 6.6%4 Merck & Co 614 -0.5% 10.9% 7.0% 6.2%5 J ohnson & J ohnson 566 14.9% 12.3% 6.1% 5.8%6 Apotex 465 10.8% 14.5% 4.6% 4.7%7 Novartis 386 14.5% 11.8% 4.2% 3.9%8 Bristol-Myers Squibb 375 6.7% 5.4% 5.2% 3.8%9 Wyeth 357 16.4% 11.2% 4.0% 3.6%10 Aventis 337 13.9% 22.4% 2.6% 3.4%

Top 10 5,873 10.1% 13.8% 60.1% 59.8%11 Abbott 332 -5.1% 5.3% 4.6% 3.4%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202337

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

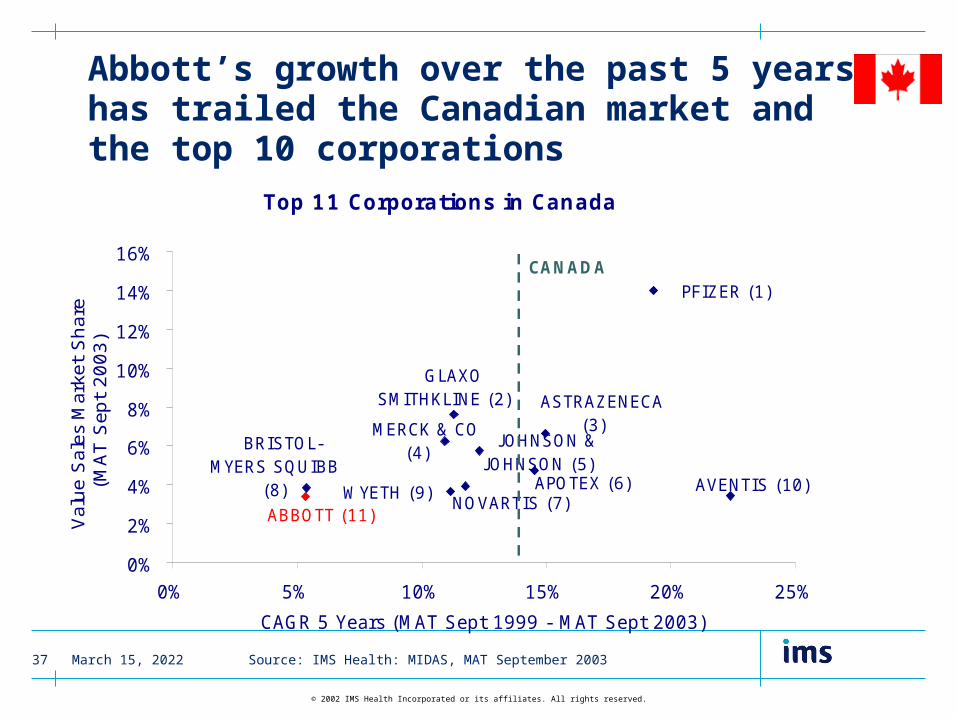

Abbott’s growth over the past 5 years has trailed the Canadian market and the top 10 corporations

Top 11 Corporations in Canada

ABBOTT (11)

AVENTIS (10) WYETH (9)

BRISTOL-MYERS SQUIBB

(8) NOVARTIS (7)

APOTEX (6)

JOHNSON & JOHNSON (5)

MERCK & CO (4)

ASTRAZENECA (3)

GLAXO SMITHKLINE (2)

PFIZER (1)

0%

2%

4%

6%

8%

10%

12%

14%

16%

0% 5% 10% 15% 20% 25%

CAGR 5 Years (MAT Sept 1999 - MAT Sept 2003)

Val

ue

Sal

es M

arke

t S

har

e(M

AT

Sep

t 2

00

3)

CANADA

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202338

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

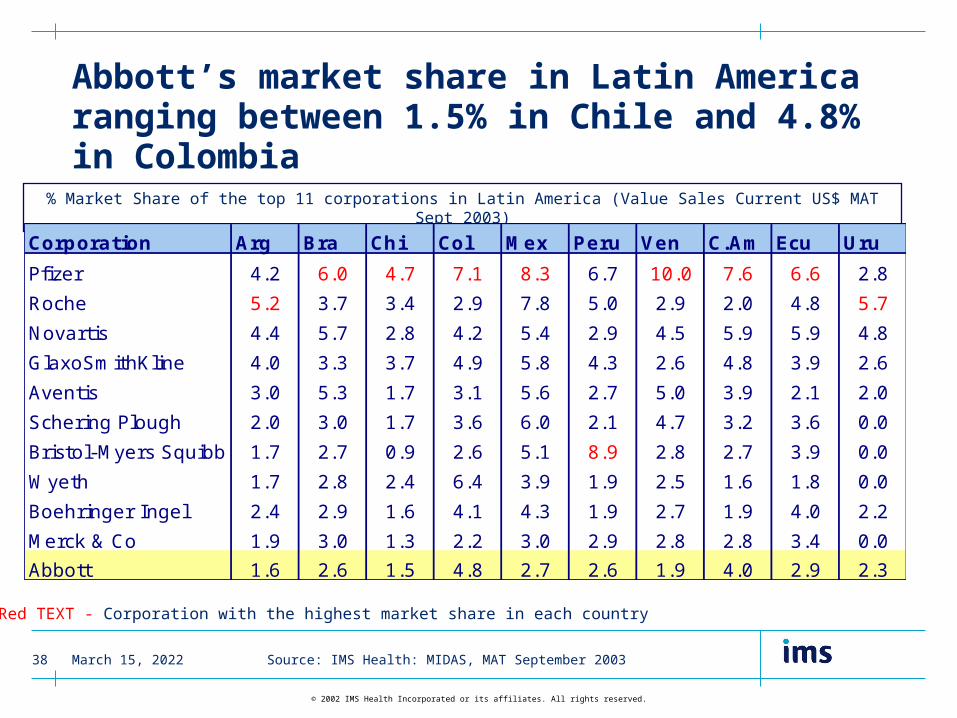

Abbott’s market share in Latin America ranging between 1.5% in Chile and 4.8% in Colombia

% Market Share of the top 11 corporations in Latin America (Value Sales Current US$ MAT Sept 2003)

Corporation Arg Bra Chi Col Mex Peru Ven C.Am Ecu Uru

Pfizer 4.2 6.0 4.7 7.1 8.3 6.7 10.0 7.6 6.6 2.8

Roche 5.2 3.7 3.4 2.9 7.8 5.0 2.9 2.0 4.8 5.7

Novartis 4.4 5.7 2.8 4.2 5.4 2.9 4.5 5.9 5.9 4.8

GlaxoSmithKline 4.0 3.3 3.7 4.9 5.8 4.3 2.6 4.8 3.9 2.6

Aventis 3.0 5.3 1.7 3.1 5.6 2.7 5.0 3.9 2.1 2.0

Schering Plough 2.0 3.0 1.7 3.6 6.0 2.1 4.7 3.2 3.6 0.0

Bristol-Myers Squibb 1.7 2.7 0.9 2.6 5.1 8.9 2.8 2.7 3.9 0.0

Wyeth 1.7 2.8 2.4 6.4 3.9 1.9 2.5 1.6 1.8 0.0

Boehringer Ingel 2.4 2.9 1.6 4.1 4.3 1.9 2.7 1.9 4.0 2.2

Merck & Co 1.9 3.0 1.3 2.2 3.0 2.9 2.8 2.8 3.4 0.0

Abbott 1.6 2.6 1.5 4.8 2.7 2.6 1.9 4.0 2.9 2.3

Red TEXT - Corporation with the highest market share in each country

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202339

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

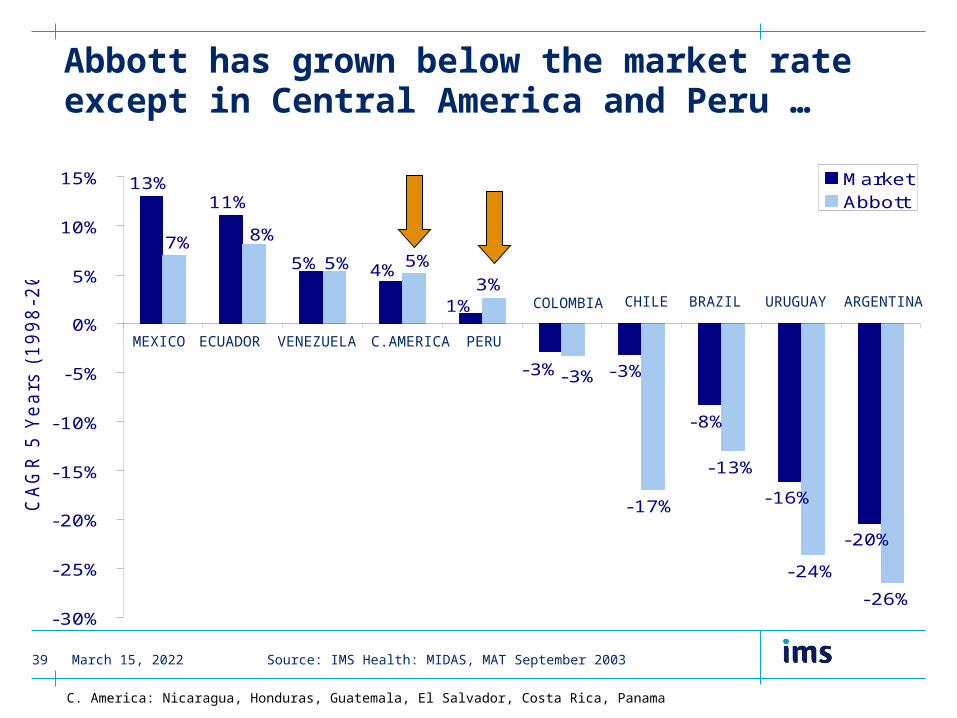

Abbott has grown below the market rate except in Central America and Peru …

13%11%

-3%

-8%

-16%

-20%

3%

-17%

-13%

-24%

-26%

-3%

5% 4%

1%

-3%

5% 5%

8%7%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

CA

GR

5 Y

ears

(1998-2

003)

MarketAbbott

MEXICO ECUADOR VENEZUELA C.AMERICA PERU

COLOMBIA CHILE BRAZIL URUGUAY ARGENTINA

Source: IMS Health: MIDAS, MAT September 2003

C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama

April 15, 202340

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

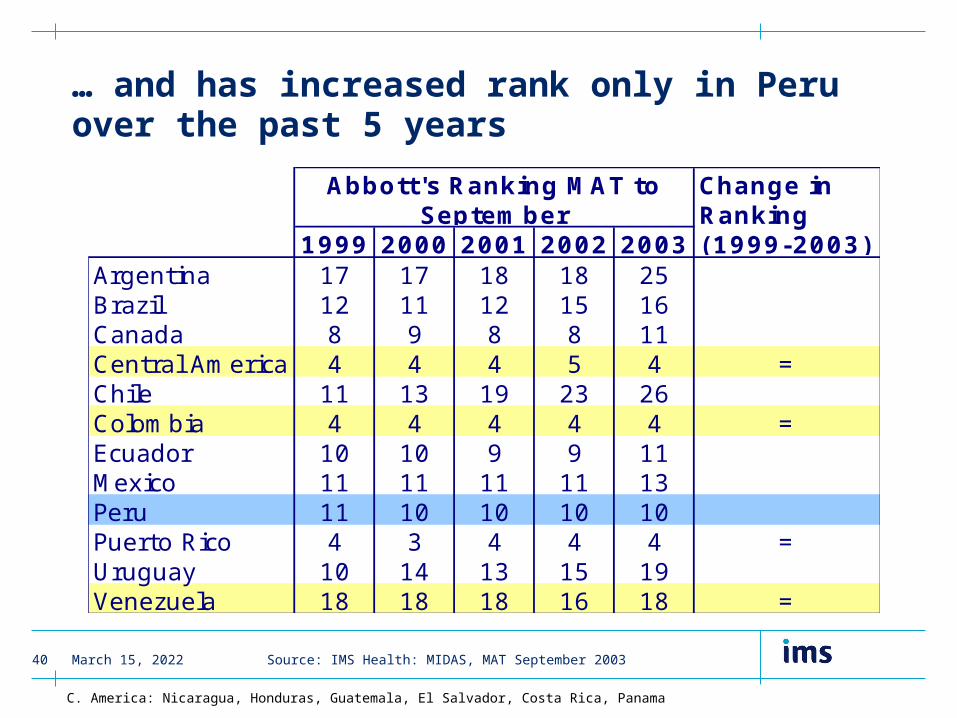

… and has increased rank only in Peru over the past 5 years

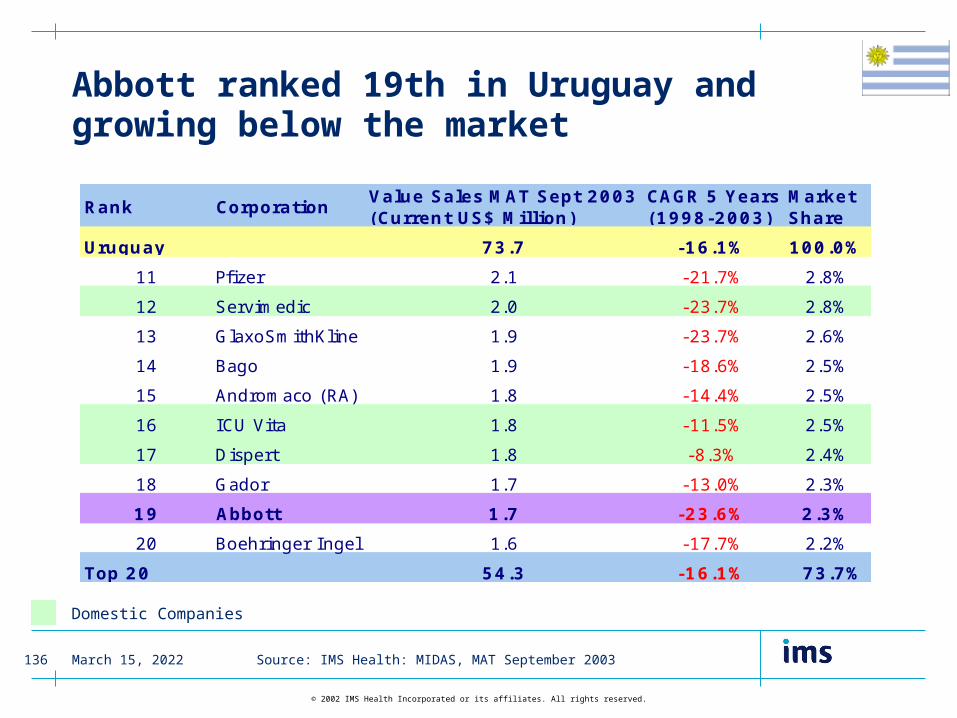

1999 2000 2001 2002 2003Argentina 17 17 18 18 25Brazil 12 11 12 15 16Canada 8 9 8 8 11Central America 4 4 4 5 4 =Chile 11 13 19 23 26Colombia 4 4 4 4 4 =Ecuador 10 10 9 9 11Mexico 11 11 11 11 13Peru 11 10 10 10 10Puerto Rico 4 3 4 4 4 =Uruguay 10 14 13 15 19Venezuela 18 18 18 16 18 =

Abbott's Ranking MAT to September

Change in Ranking (1999-2003)

Source: IMS Health: MIDAS, MAT September 2003

C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama

April 15, 202341

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

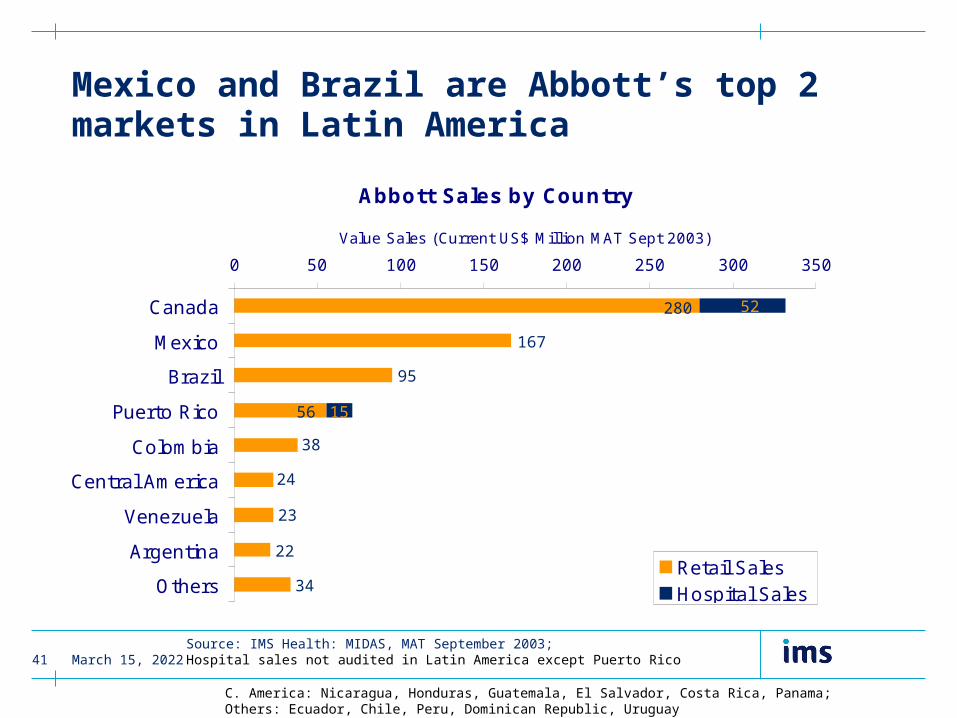

Mexico and Brazil are Abbott’s top 2 markets in Latin America

Abbott Sales by Country

0 50 100 150 200 250 300 350

Canada

Mexico

Brazil

Puerto Rico

Colombia

Central America

Venezuela

Argentina

Others

Value Sales (Current US$ Million MAT Sept 2003)

Retail SalesHospital Sales

Source: IMS Health: MIDAS, MAT September 2003;Hospital sales not audited in Latin America except Puerto Rico

C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama;Others: Ecuador, Chile, Peru, Dominican Republic, Uruguay

167

95

280 52

38

24

23

22

34

56 15

April 15, 202342

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Abbott Latin American country mix benchmark vs top 20 corporations

100% = Total Sales (current US$) by Abbott in Latin America MAT to Sept 2003 = US$473 Million

100% = Total Sales (current US$) of the top 20 global corporations in Latin America MAT to Sept 2003 = US$ 9,884 Million

Abbott's Sales in Latin America

MEXICO35%

BRAZIL20%

PUERTO RICO15%

COLOMBIA8%

CENTRAL AMERICA

5%

VENEZUELA5%

ARGENTINA5%

OTHERS 7%

Top 20 Global Corporation Sales in Latin America

MEXICO43%

BRAZIL20%

PUERTO RICO10%

VENEZUELA7%

ARGENTINA6%

COLOMBIA5%

CENTRAL AMERICA

3%

OTHERS6%

Source: IMS Health: MIDAS, MAT September 2003

Others: Chile, Ecuador, Peru, Uruguay, Dominican Republic

April 15, 202343

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Top 20 corporations more weighted towards Mexico while Abbott’s mix inclined towards Puerto Rico by 5.1%

Source: IMS Health: MIDAS, MAT September 2003

Others: Chile, Ecuador, Peru, Uruguay, Dominican Republic

Abbott's relative presence by countryvs top 20 corporation

-9.1%

0.2%

5.1%

1.5%

-0.6%

0.2%

1.6%1.1%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Devia

tion f

rom

Top 2

0 a

vera

ge

Mexico

Brazil PuertoRico

Colombia

CentralAmerica

Venezuela Argen-tina

Others

April 15, 202344

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

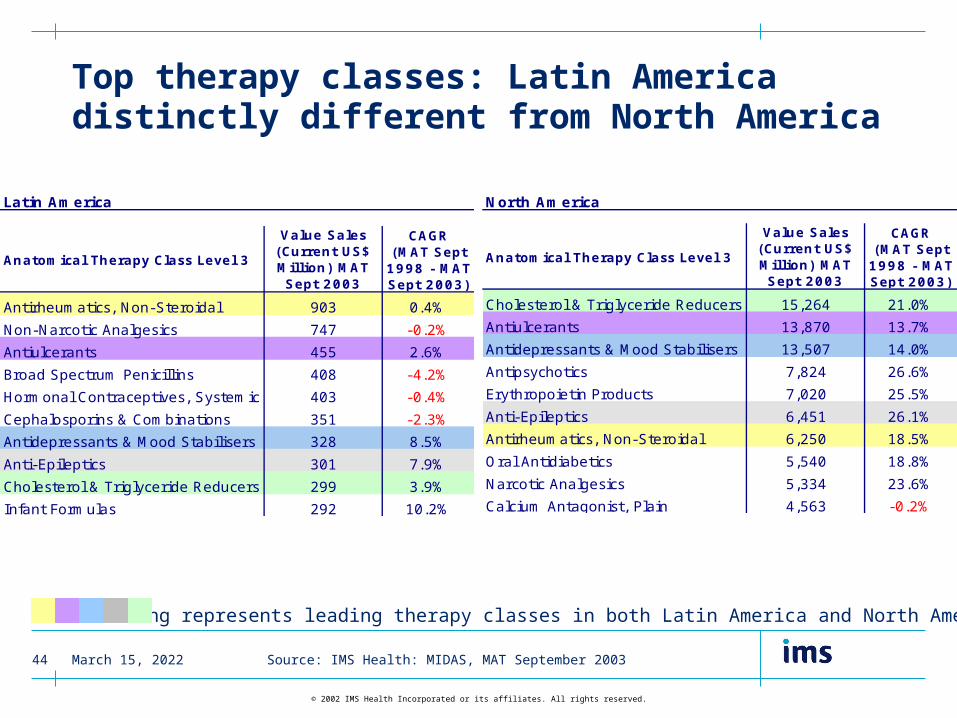

Top therapy classes: Latin America distinctly different from North America

Shading represents leading therapy classes in both Latin America and North America

Source: IMS Health: MIDAS, MAT September 2003

Latin America

Anatomical Therapy Class Level 3

Value Sales (Current US$ Million) MAT Sept 2003

CAGR (MAT Sept

1998 - MAT Sept 2003)

Antirheumatics, Non-Steroidal 903 0.4%

Non-Narcotic Analgesics 747 -0.2%

Antiulcerants 455 2.6%

Broad Spectrum Penicillins 408 -4.2%

Hormonal Contraceptives, Systemic 403 -0.4%

Cephalosporins & Combinations 351 -2.3%

Antidepressants & Mood Stabilisers 328 8.5%

Anti-Epileptics 301 7.9%

Cholesterol & Triglyceride Reducers 299 3.9%

Infant Formulas 292 10.2%

North America

Anatomical Therapy Class Level 3

Value Sales (Current US$ Million) MAT Sept 2003

CAGR (MAT Sept

1998 - MAT Sept 2003)

Cholesterol & Triglyceride Reducers 15,264 21.0%

Antiulcerants 13,870 13.7%

Antidepressants & Mood Stabilisers 13,507 14.0%

Antipsychotics 7,824 26.6%

Erythropoietin Products 7,020 25.5%

Anti-Epileptics 6,451 26.1%

Antirheumatics, Non-Steroidal 6,250 18.5%

Oral Antidiabetics 5,540 18.8%

Narcotic Analgesics 5,334 23.6%

Calcium Antagonist, Plain 4,563 -0.2%

April 15, 202345

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

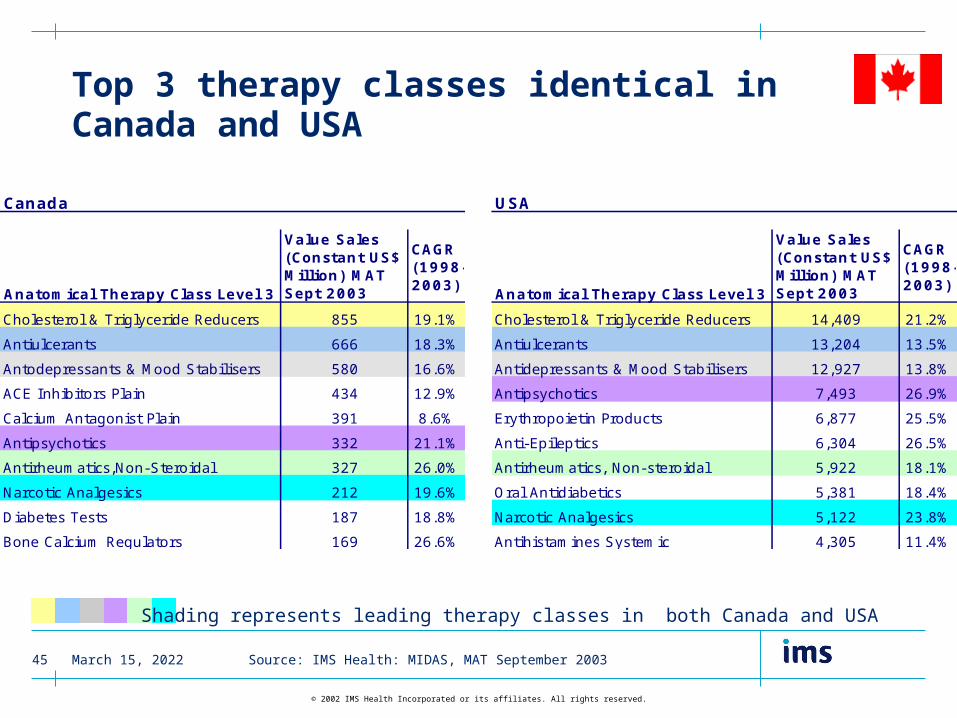

Top 3 therapy classes identical in Canada and USA

Canada

Anatomical Therapy Class Level 3

Value Sales (Constant US$ Million) MAT Sept 2003

CAGR (1998-2003)

Cholesterol & Triglyceride Reducers 855 19.1%

Antiulcerants 666 18.3%

Antodepressants & Mood Stabilisers 580 16.6%

ACE Inhibitors Plain 434 12.9%

Calcium Antagonist Plain 391 8.6%

Antipsychotics 332 21.1%

Antirheumatics,Non-Steroidal 327 26.0%

Narcotic Analgesics 212 19.6%

Diabetes Tests 187 18.8%

Bone Calcium Regulators 169 26.6%

USA

Anatomical Therapy Class Level 3

Value Sales (Constant US$ Million) MAT Sept 2003

CAGR (1998-2003)

Cholesterol & Triglyceride Reducers 14,409 21.2%

Antiulcerants 13,204 13.5%

Antidepressants & Mood Stabilisers 12,927 13.8%

Antipsychotics 7,493 26.9%

Erythropoietin Products 6,877 25.5%

Anti-Epileptics 6,304 26.5%

Antirheumatics, Non-steroidal 5,922 18.1%

Oral Antidiabetics 5,381 18.4%

Narcotic Analgesics 5,122 23.8%

Antihistamines Systemic 4,305 11.4%

Shading represents leading therapy classes in both Canada and USA

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202346

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

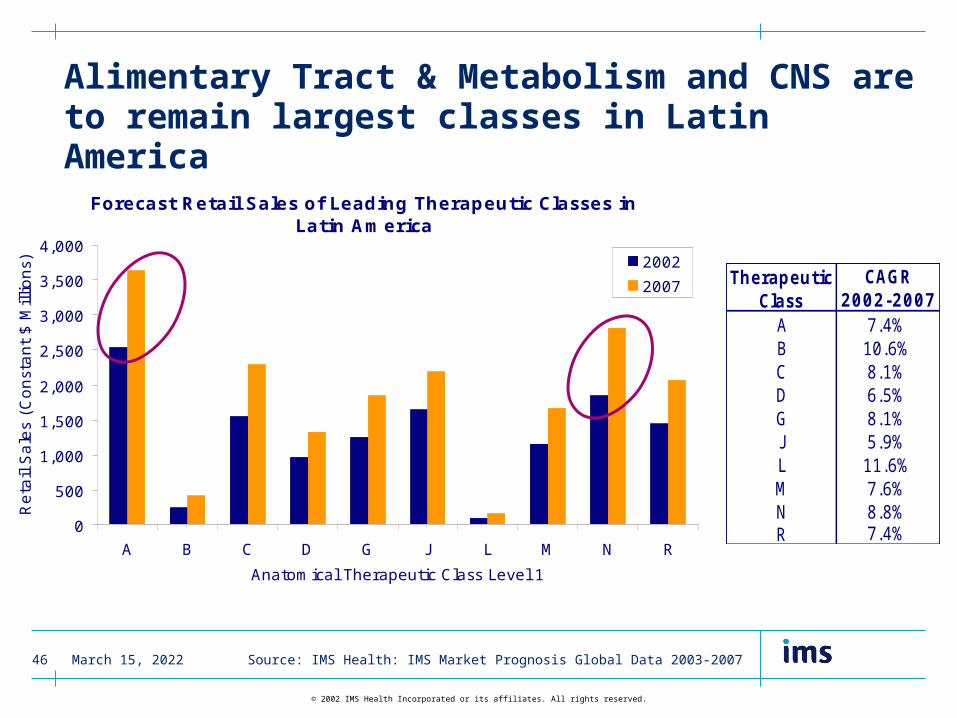

Alimentary Tract & Metabolism and CNS are to remain largest classes in Latin America

Source: IMS Health: IMS Market Prognosis Global Data 2003-2007

Therapeutic Class

CAGR 2002-2007

A 7.4%B 10.6%C 8.1%D 6.5%G 8.1%J 5.9%L 11.6%M 7.6%N 8.8%R 7.4%

Forecast Retail Sales of Leading Therapeutic Classes in Latin America

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

A B C D G J L M N R

Anatomical Therapeutic Class Level 1

Reta

il S

ale

s (C

onst

ant

$ M

illio

ns) 2002

2007

April 15, 202347

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Cardiovascular System and CNS are to remain largest therapy classes in Canada

Therapeutic Class

CAGR 2002-2007

A 12.1%B 13.8%C 12.8%D 10.2%G 11.8%J 11.7%L 15.0%M 11.8%N 13.9%R 10.1%

Forecast Retail and Hospital Sales of Leading Therapeutic Classes in Canada

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

A B C D G J L M N R

Anatomical Therapeutic Class Level 1

Hosp

ital and R

eta

il S

ale

s (U

S$ B

illion)

20022007

Source: IMS Health: IMS Market Prognosis Global Data 2003-2007

April 15, 202348

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

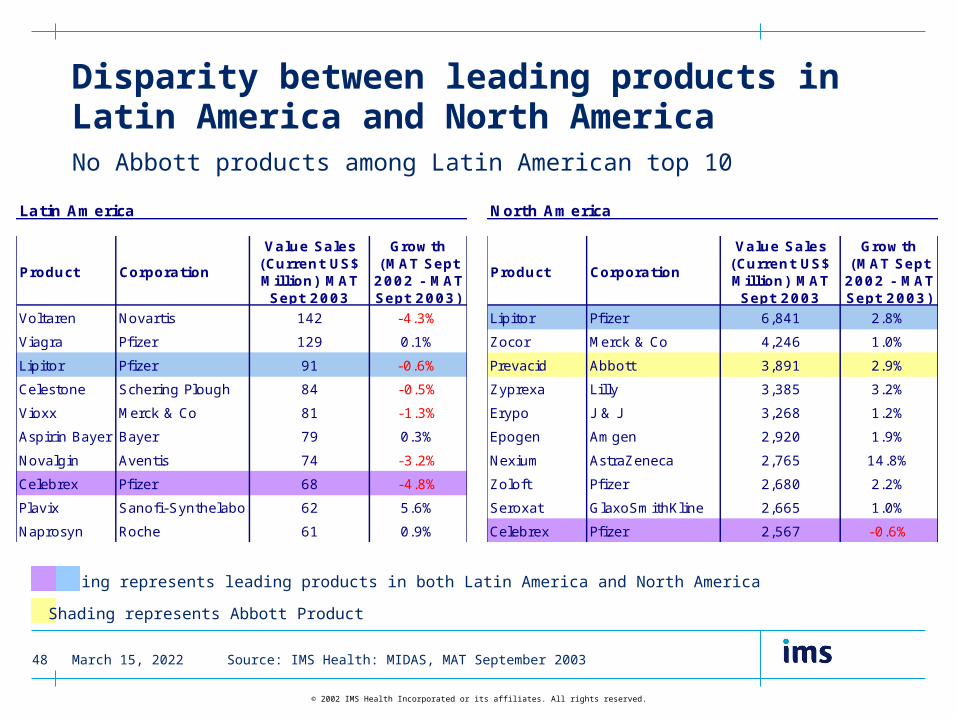

Disparity between leading products in Latin America and North AmericaNo Abbott products among Latin American top 10

Shading represents leading products in both Latin America and North America

Source: IMS Health: MIDAS, MAT September 2003

Shading represents Abbott Product

Latin America

Product Corporation

Value Sales (Current US$ Million) MAT Sept 2003

Growth (MAT Sept

2002 - MAT Sept 2003)

Voltaren Novartis 142 -4.3%

Viagra Pfizer 129 0.1%

Lipitor Pfizer 91 -0.6%

Celestone Schering Plough 84 -0.5%

Vioxx Merck & Co 81 -1.3%

Aspirin Bayer Bayer 79 0.3%

Novalgin Aventis 74 -3.2%

Celebrex Pfizer 68 -4.8%

Plavix Sanofi-Synthelabo 62 5.6%

Naprosyn Roche 61 0.9%

North America

Product Corporation

Value Sales (Current US$ Million) MAT Sept 2003

Growth (MAT Sept

2002 - MAT Sept 2003)

Lipitor Pfizer 6,841 2.8%

Zocor Merck & Co 4,246 1.0%

Prevacid Abbott 3,891 2.9%

Zyprexa Lilly 3,385 3.2%

Erypo J & J 3,268 1.2%

Epogen Amgen 2,920 1.9%

Nexium AstraZeneca 2,765 14.8%

Zoloft Pfizer 2,680 2.2%

Seroxat GlaxoSmithKline 2,665 1.0%

Celebrex Pfizer 2,567 -0.6%

April 15, 202349

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Similarity between leading products in Canada and USA

USA

Product Corporation

Value Sales (Constant US$ Million) MAT Sept 2003

Growth (MAT Sept 2002 - MAT Sept 2003)

Lipitor Pfizer 6,359 2.7%

Zocor Merck & Co 4,109 1.3%

Ogastro Abbott 3,805 2.9%

Zyprexa Lilly 3,223 3.2%

Erypo J & J 3,144 1.2%

Epogen Amgen 2,920 1.9%

Nexium AstraZeneca 2,710 14.7%

Zoloft Pfizer 2,668 2.3%

Seroxat GSK 2,511 1.0%

Celebrex Pfizer 2,447 -0.6%

Canada

Product Corporation

Value Sales (Constant US$ Million) MAT Sept 2003

Growth (MAT Sept 2002 - MAT Sept 2003)

Lipitor Pfizer 481 5.2%

Losec AstraZeneca 282 -0.4%

Norvasc Pfizer 183 3.5%

Triatec Aventis 181 5.6%

Zyprexa Lilly 162 4.6%

Seroxat GSK 155 0.9%

Zocor Merck & Co 137 -6.3%

Effexor Wyeth 136 7.3%

Pantoloc Solvay 127 6.2%

Erypo J & J 124 1.4%

Shading represents leading products in both Canada and USA

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202350

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Pedialyte, an oral electrolyte solution for fluid maintenance in infants & children, is Abbott’s top selling product in Latin America

Top 11 Abbott Products in Latin America

Rank Product Anatomical Therapy Class Level 3

Value Sales MAT Sept 2003 (US$ Million)

Growth (MAT Sept 2002 - MAT Sept 2003)

% of Abbott Sales in Latin America

1 Pedialyte Oral Electyrolyte Replacer 45.9 -6.5% 9.7%2 Ensure Protein Supplement 34.4 -10.1% 7.3%3 Reductil Anti-Obesity Preparations

exc. Dietetics33.6 -15.4% 7.1%

4 Klacid Macrolides & Similar Types 32.1 -12.7% 6.8%5 Lanzoprazole Antiulcerants 31.0 13.1% 6.6%6 Neosaldina* Anti-Migraine Preparations 22.6 -11.9% 4.8%7 Valcote Anti-Epileptics 19.2 12.7% 4.1%8 Similac Advance Infant Formulas 17.3 -11.6% 3.7%9 Lupron Cytostatic Hormones 16.9 -32.2% 3.6%10 Synthroid Thyroid Preparations 14.4 19.5% 3.1%11 Isoptin Calcium Antagonist 13.3 -13.8% 2.8%

Total Abbott Sales in Latin America 473.4 -9.3% 100.0%

Source: IMS Health: MIDAS, MAT September 2003

* sold recently

April 15, 202351

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

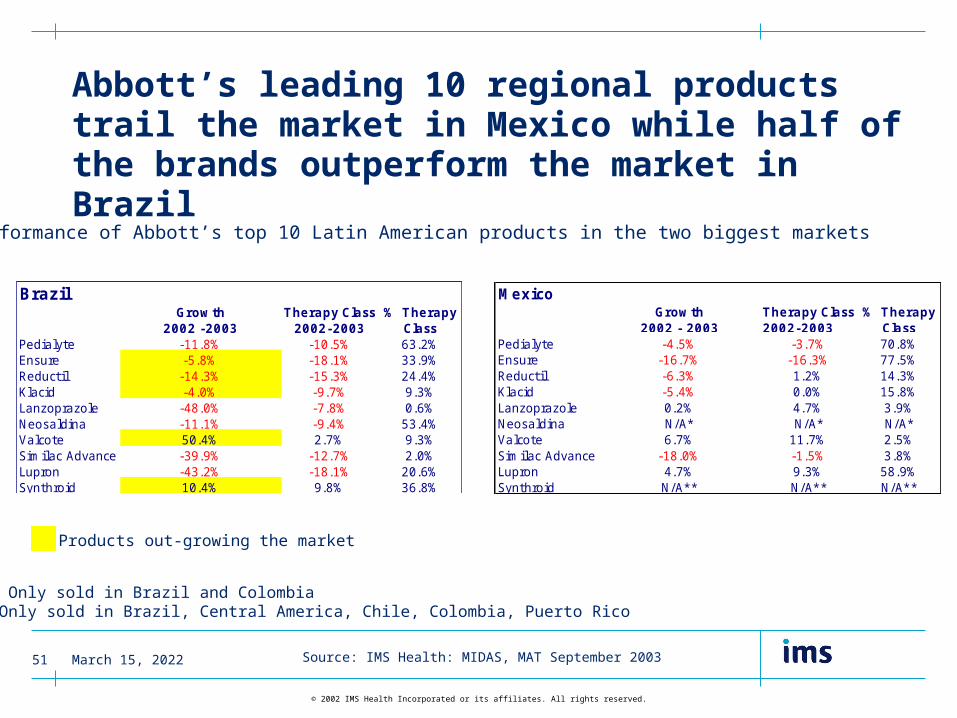

Abbott’s leading 10 regional products trail the market in Mexico while half of the brands outperform the market in Brazil

BrazilGrowth

2002 -2003Therapy Class

2002-2003% Therapy

ClassPedialyte -11.8% -10.5% 63.2%Ensure -5.8% -18.1% 33.9%Reductil -14.3% -15.3% 24.4%Klacid -4.0% -9.7% 9.3%Lanzoprazole -48.0% -7.8% 0.6%Neosaldina -11.1% -9.4% 53.4%Valcote 50.4% 2.7% 9.3%Similac Advance -39.9% -12.7% 2.0%Lupron -43.2% -18.1% 20.6%Synthroid 10.4% 9.8% 36.8%

MexicoGrowth

2002 - 2003Therapy Class2002-2003

% Therapy Class

Pedialyte -4.5% -3.7% 70.8%Ensure -16.7% -16.3% 77.5%Reductil -6.3% 1.2% 14.3%Klacid -5.4% 0.0% 15.8%Lanzoprazole 0.2% 4.7% 3.9%Neosaldina N/A* N/A* N/A*Valcote 6.7% 11.7% 2.5%Similac Advance -18.0% -1.5% 3.8%Lupron 4.7% 9.3% 58.9%Synthroid N/A** N/A** N/A**

Performance of Abbott’s top 10 Latin American products in the two biggest markets

* Only sold in Brazil and Colombia ** Only sold in Brazil, Central America, Chile, Colombia, Puerto Rico

Source: IMS Health: MIDAS, MAT September 2003

Products out-growing the market

April 15, 202354

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

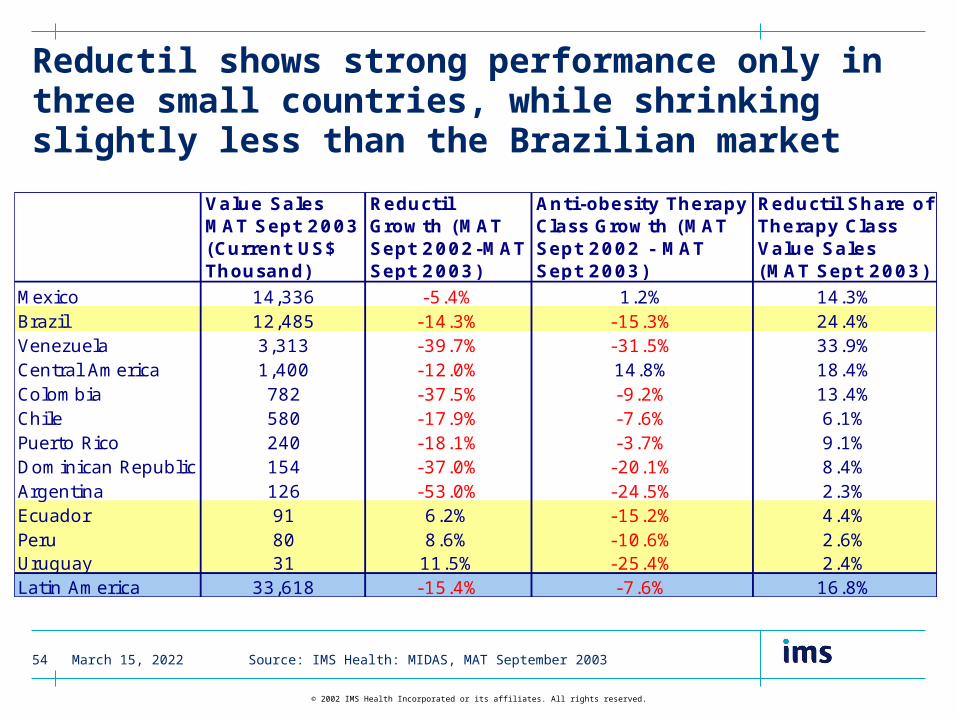

Reductil shows strong performance only in three small countries, while shrinking slightly less than the Brazilian market

Value Sales MAT Sept 2003 (Current US$ Thousand)

Reductil Growth (MAT Sept 2002-MAT Sept 2003)

Anti-obesity Therapy Class Growth (MAT Sept 2002 - MAT Sept 2003)

Reductil Share of Therapy Class Value Sales (MAT Sept 2003)

Mexico 14,336 -5.4% 1.2% 14.3%Brazil 12,485 -14.3% -15.3% 24.4%Venezuela 3,313 -39.7% -31.5% 33.9%Central America 1,400 -12.0% 14.8% 18.4%Colombia 782 -37.5% -9.2% 13.4%Chile 580 -17.9% -7.6% 6.1%Puerto Rico 240 -18.1% -3.7% 9.1%Dominican Republic 154 -37.0% -20.1% 8.4%Argentina 126 -53.0% -24.5% 2.3%Ecuador 91 6.2% -15.2% 4.4%Peru 80 8.6% -10.6% 2.6%Uruguay 31 11.5% -25.4% 2.4%Latin America 33,618 -15.4% -7.6% 16.8%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202355

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Except in Brazil, Klacid under-performs relative to the macrolide therapy class

Value Sales MAT Sept 2003 (Current US$ Thousand)

Klacid Growth (MAT Sept 2002-MAT Sept 2003)

Macrolide Therapy Class Growth (MAT Sept 2002-MAT Sept 2003)

Klacid Share of Therapy Class Value Sales (MAT Sept 2003)

Mexico 16,033 -6.3% 0.0% 15.8%Brazil 3,156 -4.0% -9.7% 9.3%Puerto Rico 3,058 -4.8% 5.9% 14.7%Argentina 2,249 -33.8% -4.5% 13.3%Central America 1,998 -1.9% 7.1% 15.9%Venezuela 1,711 -29.0% -18.0% 8.3%Colombia 1,413 -18.4% -9.1% 13.6%Ecuador 849 -30.1% 2.2% 10.4%Peru 666 -13.9% -12.2% 12.8%Chile 478 -38.4% -10.7% 6.5%Dominican Republic 305 -41.1% -22.8% 9.0%Uruguay 168 -37.2% -25.1% 28.3%Latin America 32,087 -12.7% -4.2% 13.3%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202356

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

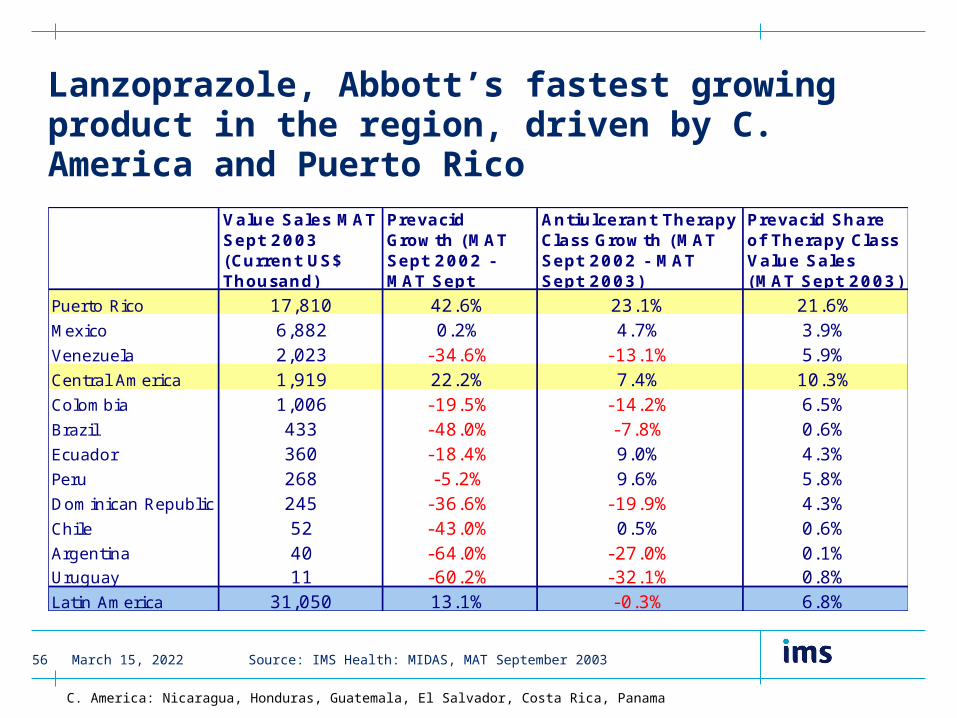

Lanzoprazole, Abbott’s fastest growing product in the region, driven by C. America and Puerto Rico

Value Sales MAT Sept 2003 (Current US$ Thousand)

Prevacid Growth (MAT Sept 2002 - MAT Sept

Antiulcerant Therapy Class Growth (MAT Sept 2002 - MAT Sept 2003)

Prevacid Share of Therapy Class Value Sales (MAT Sept 2003)

Puerto Rico 17,810 42.6% 23.1% 21.6%Mexico 6,882 0.2% 4.7% 3.9%Venezuela 2,023 -34.6% -13.1% 5.9%Central America 1,919 22.2% 7.4% 10.3%Colombia 1,006 -19.5% -14.2% 6.5%Brazil 433 -48.0% -7.8% 0.6%Ecuador 360 -18.4% 9.0% 4.3%Peru 268 -5.2% 9.6% 5.8%Dominican Republic 245 -36.6% -19.9% 4.3%Chile 52 -43.0% 0.5% 0.6%Argentina 40 -64.0% -27.0% 0.1%Uruguay 11 -60.2% -32.1% 0.8%Latin America 31,050 13.1% -0.3% 6.8%

Source: IMS Health: MIDAS, MAT September 2003

C. America: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama

April 15, 202357

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

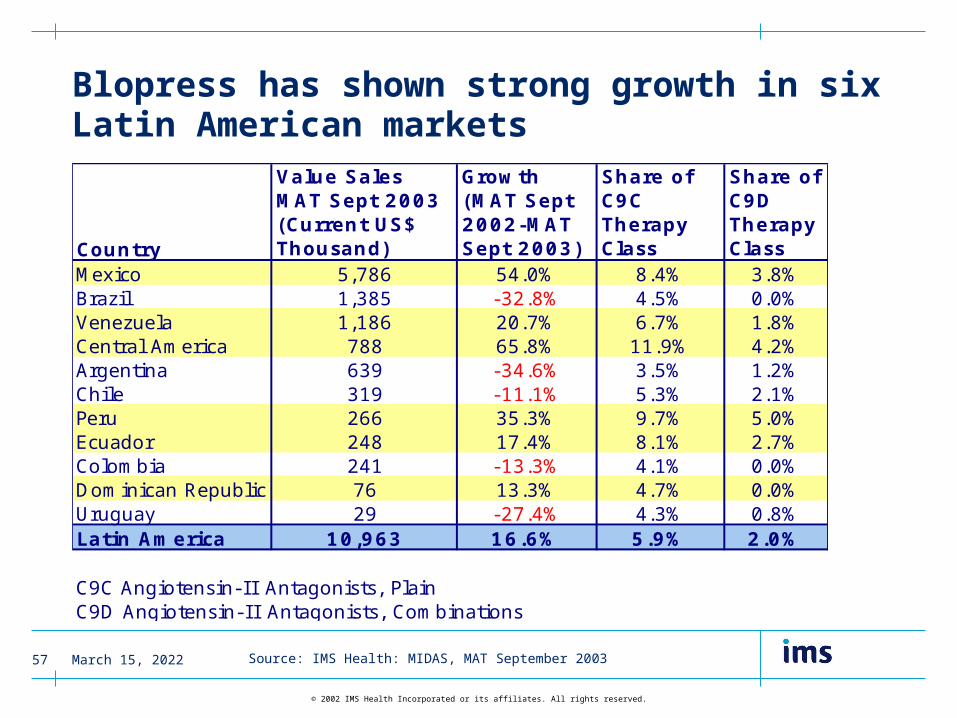

Blopress has shown strong growth in six Latin American markets

Country

Value Sales MAT Sept 2003 (Current US$ Thousand)

Growth (MAT Sept 2002-MAT Sept 2003)

Share of C9C Therapy Class

Share of C9D Therapy Class

Mexico 5,786 54.0% 8.4% 3.8%Brazil 1,385 -32.8% 4.5% 0.0%Venezuela 1,186 20.7% 6.7% 1.8%Central America 788 65.8% 11.9% 4.2%Argentina 639 -34.6% 3.5% 1.2%Chile 319 -11.1% 5.3% 2.1%Peru 266 35.3% 9.7% 5.0%Ecuador 248 17.4% 8.1% 2.7%Colombia 241 -13.3% 4.1% 0.0%Dominican Republic 76 13.3% 4.7% 0.0%Uruguay 29 -27.4% 4.3% 0.8%Latin America 10,963 16.6% 5.9% 2.0%

C9C Angiotensin- I I Antagonists, PlainC9D Angiotensin- I I Antagonists, Combinations

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202358

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Abbott’s Humira ranked #4 in the Latin American M1C market in 2003

Rank Product Corporation Value Sales MAT Sept 2003 (Current US$ Thousand)

Share of Therapy Class

Growth (MAT Sept 2002-MAT Sept 2003)

1 Arava Aventis 10,581 38.6% -5.1%2 Enbrel Amgen 9,503 34.7% 82.6%3 Plaquenil Sanofi-Synthelabo 4,085 14.9% 34.9%4 Humira Abbott 534 1.9% *5 Filartros Ivax Corp. 459 1.7% 28.2%6 Evoquin Ivax Corp. 409 1.5% -9.2%7 Ervemin Ivax Corp. 334 1.2% -1.6%8 Polirreumin TRB Chemedica 300 1.1% 77.9%9 Sufortan Sanfer 265 1.0% 0.1%10 Dimard Metlen Pharma 204 0.7% -10.5%

27,408 100.0% 25%

* No Sales in MAT Sept 2002

Specific Anti-Rheumatics Agents in Latin America

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202359

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Kaletra has been Abbott’s fastest growing drug in Canada

Top 10 Abbott Products in Canada

Rank Product Anatomical Therapy Class Level 3

Value Sales MAT Sept 2003 (Constant US$ Million)

Growth (MAT Sept 2002 - MAT Sept 2003)

% of Abbott Sales in Canada

1 Prevacid Antiulcerants 85.9 17.2% 25.9%

2 Klacid Macrolides & Similar Types 51.9 -1.7% 15.7%

3 Lupron Cytostatic Hormones 32.5 2.8% 9.8%

4 Ensure Other Nutrients 18.9 0.0% 5.7%

5 Synthroid Thyroid Preparations 17.0 11.7% 5.1%

6 Kaletra HIV Antivirals 15.7 37.5% 4.7%

7 Precision Plus Diabetes Tests 13.0 -31.1% 3.9%

8 Precision Xtra Diabetes Tests 9.6 72.6% 2.9%

9 Similac Advance Infant Formulas 7.7 -0.2% 2.3%10 Reductil Anti-Obesity Preparations

Exc. Dietetics7.1 -13.0% 2.1%

331.7 -5.1% 100.0%Total Abbott Sales in Canada

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202360

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

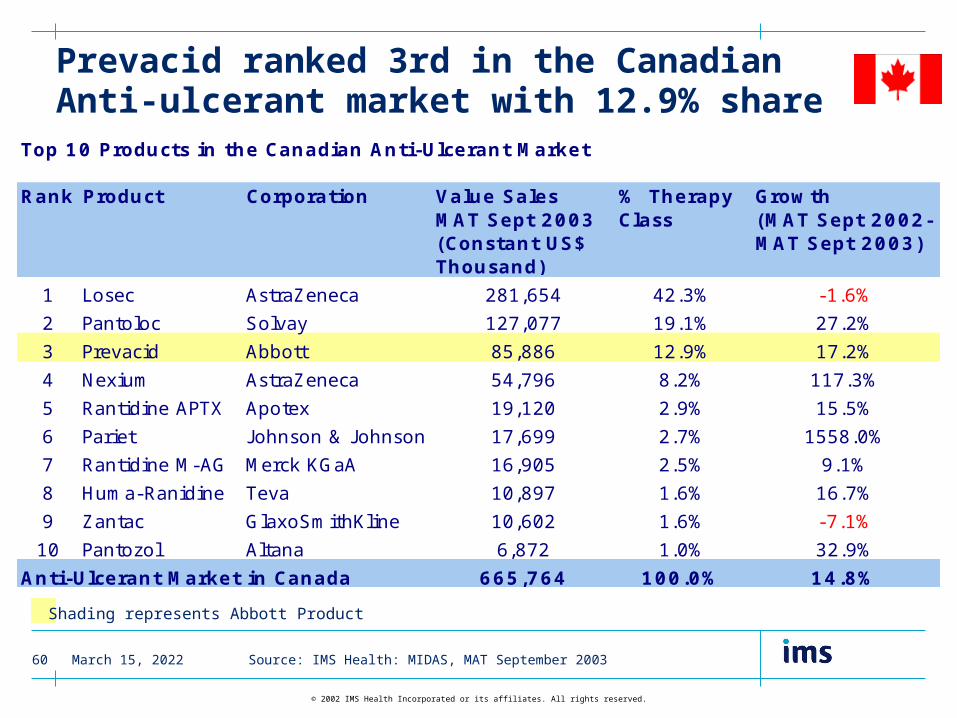

Prevacid ranked 3rd in the Canadian Anti-ulcerant market with 12.9% share

Top 10 Products in the Canadian Anti-Ulcerant Market

Rank Product Corporation Value Sales MAT Sept 2003 (Constant US$ Thousand)

% Therapy Class

Growth (MAT Sept 2002-MAT Sept 2003)

1 Losec AstraZeneca 281,654 42.3% -1.6%

2 Pantoloc Solvay 127,077 19.1% 27.2%

3 Prevacid Abbott 85,886 12.9% 17.2%

4 Nexium AstraZeneca 54,796 8.2% 117.3%

5 Rantidine APTX Apotex 19,120 2.9% 15.5%

6 Pariet J ohnson & J ohnson 17,699 2.7% 1558.0%

7 Rantidine M-AG Merck KGaA 16,905 2.5% 9.1%

8 Huma-Ranidine Teva 10,897 1.6% 16.7%

9 Zantac GlaxoSmithKline 10,602 1.6% -7.1%

10 Pantozol Altana 6,872 1.0% 32.9%

Anti-Ulcerant Market in Canada 665,764 100.0% 14.8%

Source: IMS Health: MIDAS, MAT September 2003

Shading represents Abbott Product

April 15, 202361

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

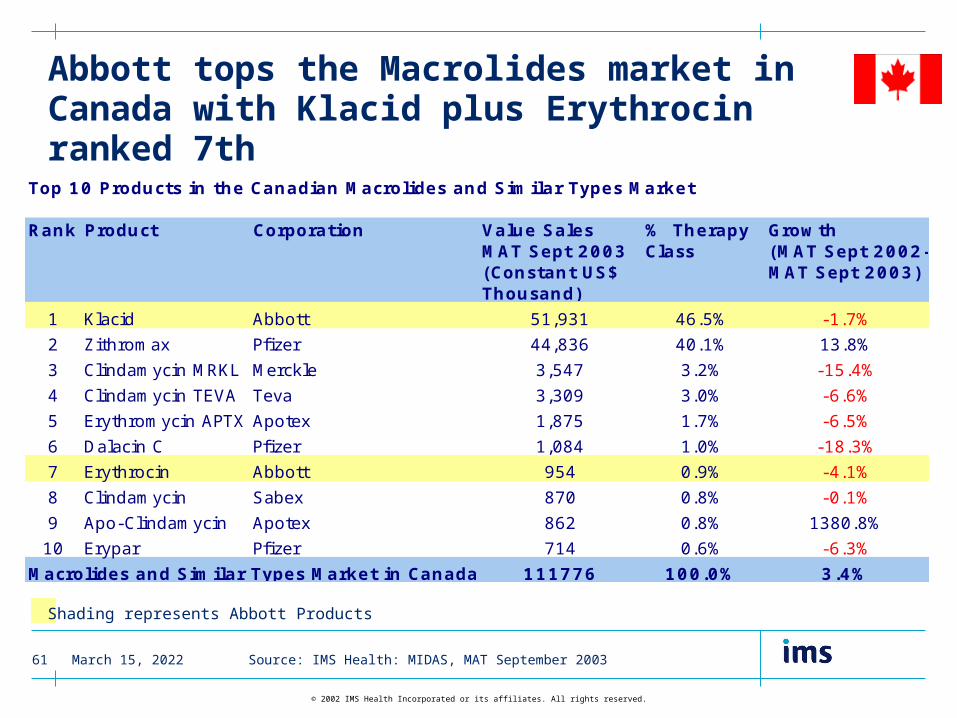

Abbott tops the Macrolides market in Canada with Klacid plus Erythrocin ranked 7th

Top 10 Products in the Canadian Macrolides and Similar Types Market

Rank Product Corporation Value Sales MAT Sept 2003 (Constant US$ Thousand)

% Therapy Class

Growth (MAT Sept 2002-MAT Sept 2003)

1 Klacid Abbott 51,931 46.5% -1.7%

2 Zithromax Pfizer 44,836 40.1% 13.8%

3 Clindamycin MRKL Merckle 3,547 3.2% -15.4%

4 Clindamycin TEVA Teva 3,309 3.0% -6.6%

5 Erythromycin APTX Apotex 1,875 1.7% -6.5%

6 Dalacin C Pfizer 1,084 1.0% -18.3%

7 Erythrocin Abbott 954 0.9% -4.1%

8 Clindamycin Sabex 870 0.8% -0.1%

9 Apo-Clindamycin Apotex 862 0.8% 1380.8%

10 Erypar Pfizer 714 0.6% -6.3%

111776 100.0% 3.4%Macrolides and Similar Types Market in Canada

Source: IMS Health: MIDAS, MAT September 2003

Shading represents Abbott Products

April 15, 202362

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Lupron ranked 2nd with 37.4% share of the Canadian cytostatic hormone marketTop 10 Products in the Canadian Cytostatic Hormone Market

Rank Product Corporation Value Sales MAT Sept 2003 (Constant US$ Thousand)

% Therapy Class

Growth (MAT Sept 2002-MAT Sept 2003)

1 Zoladex AstraZeneca 38044 43.8% 4.2%

2 Lupron Abbott 32466 37.4% 2.8%

3 Suprefact Aventis 12925 14.9% 28.0%

4 Megestrol APTX Apotex 1994 2.3% 43.1%

5 Megace Bristol-Myers Squibb 527 0.6% -33.1%

6 Depo Provera Pfizer 344 0.4% -10.2%

7 Megestrol B-MS Bristol-Myers Squibb 314 0.4% -50.8%

8 Veraplex Teva 232 0.3% -87.0%

9 Honvan Viatris 2 0.0% 2.6%

10 Megestrol Pro Doc 2 0.0% -88.4%

Cytostatic Hormone Market in Canada 86850 100.0% 4.4%

Source: IMS Health: MIDAS, MAT September 2003

Shading represents Abbott Product

April 15, 202363

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Challenges for Abbott in the Latin America/ Canada region

• Performance across the region: How to close the gap and grow at least with the market? Which therapy classes and products, current and future, would drive growth?

• As markets continue to open up, where are opportunities for partnerships and licensing?

April 15, 202364

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Appendix:

Latin America - Country Deep Dive

April 15, 202365

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

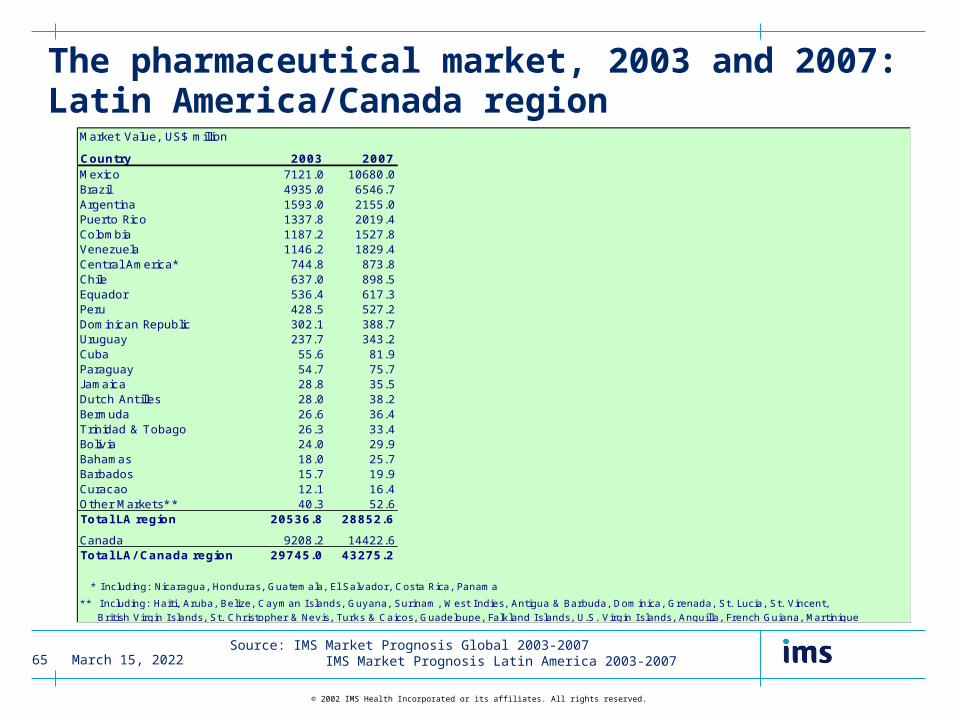

The pharmaceutical market, 2003 and 2007: Latin America/Canada region

Market Value, US$ million

Country 2003 2007Mexico 7121.0 10680.0Brazil 4935.0 6546.7Argentina 1593.0 2155.0Puerto Rico 1337.8 2019.4Colombia 1187.2 1527.8Venezuela 1146.2 1829.4Central America* 744.8 873.8Chile 637.0 898.5Equador 536.4 617.3Peru 428.5 527.2Dominican Republic 302.1 388.7Uruguay 237.7 343.2Cuba 55.6 81.9Paraguay 54.7 75.7J amaica 28.8 35.5Dutch Antilles 28.0 38.2Bermuda 26.6 36.4Trinidad & Tobago 26.3 33.4Bolivia 24.0 29.9Bahamas 18.0 25.7Barbados 15.7 19.9Curacao 12.1 16.4Other Markets* * 40.3 52.6Total LA region 20536.8 28852.6

Canada 9208.2 14422.6Total LA/ Canada region 29745.0 43275.2

* I ncluding: Nicaragua, Honduras, Guatemala, El Salvador, Costa Rica, Panama

** I ncluding: Haiti, Aruba, Belize, Cayman I slands, Guyana, Surinam, West I ndies, Antigua & Barbuda, Dominica, Grenada, St. Lucia, St. Vincent,

British Virgin I slands, St. Christopher & Nevis, Turks & Caicos, Guadeloupe, Falkland I slands, U.S. Virgin I slands, Anguilla, French Guiana, Martinique

Source: IMS Market Prognosis Global 2003-2007 IMS Market Prognosis Latin America 2003-2007

April 15, 202366

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Argentina

April 15, 202367

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

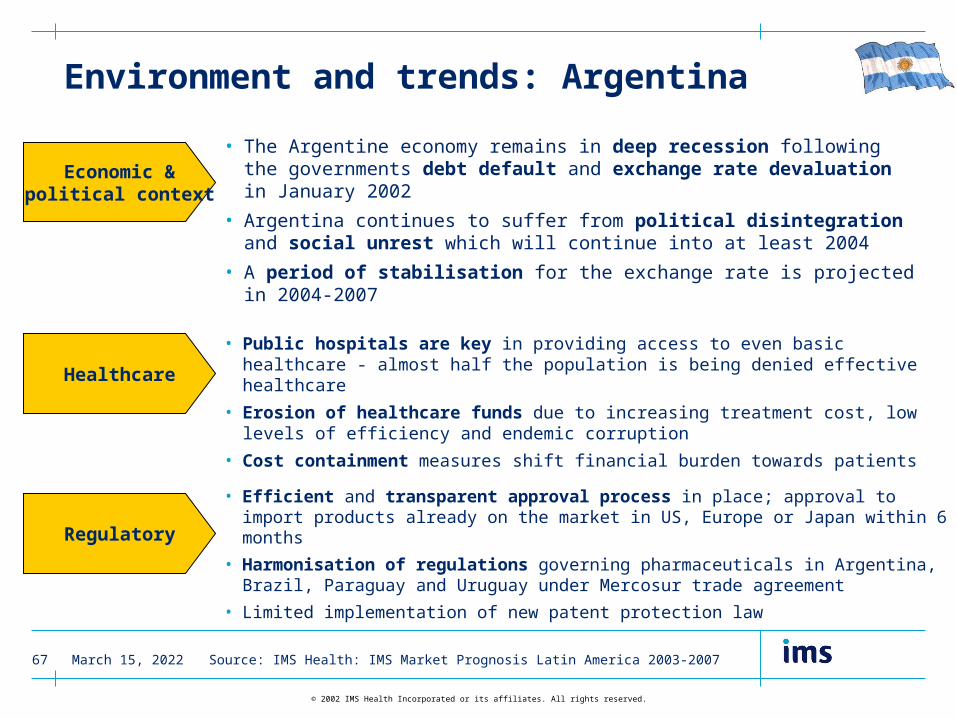

Environment and trends: Argentina

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

Economic &political context

Healthcare

Regulatory

• The Argentine economy remains in deep recession following the governments debt default and exchange rate devaluation in January 2002

• Argentina continues to suffer from political disintegration and social unrest which will continue into at least 2004

• A period of stabilisation for the exchange rate is projected in 2004-2007

• Public hospitals are key in providing access to even basic healthcare - almost half the population is being denied effective healthcare

• Erosion of healthcare funds due to increasing treatment cost, low levels of efficiency and endemic corruption

• Cost containment measures shift financial burden towards patients

• Efficient and transparent approval process in place; approval to import products already on the market in US, Europe or Japan within 6 months

• Harmonisation of regulations governing pharmaceuticals in Argentina, Brazil, Paraguay and Uruguay under Mercosur trade agreement

• Limited implementation of new patent protection law

April 15, 202368

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Pharmaceutical business environment

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

• A number of multinationals pulled out of the Argentinean pharmaceutical market and have found it difficult to regain previously held market shares on their return

• Despite Roemmers and Bago heading the sales rankings in Argentina, the local industry is highly fragmented

• A true Argentinean generics market has yet to emerge; lack of regulations seen as major barrier

• OTC medicines account for <10% of the Argentine market by value

• The complex nature of the distribution system in Argentina limits the margins of individual players, compromises efficiency and encourages corruption

• Widespread discounting as marketing strategy since collapse of the economy

April 15, 202369

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Local manufacturers well representedin the top 10 - Bago, Roemmers, Gador, Elea

Domestic Companies

Rank CorporationValue Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Argentina 1,398.2 -20.4% 100.0%

1 Bago 109.1 -19.5% 7.8%

2 Roemmers 100.4 -21.0% 7.2%

3 Roche 73.0 -21.8% 5.2%

4 Novartis 61.8 -22.4% 4.4%

5 Pfizer 58.9 -24.9% 4.2%

6 GlaxoSmithKline 55.6 -17.6% 4.0%

7 Ivax Corp 51.9 -17.3% 3.7%

8 Gador 50.9 -13.6% 3.6%

9 Elea 46.8 -18.1% 3.3%

10 Aventis 42.5 -22.9% 3.0%

Top 10 650.8 -20.3% 46.5%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202370

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Abbott ranked 25th in Argentina and has negative growth beyond the market Rank Corporation

Value Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Argentina 1,398.2 -20.4% 100.0%

11 Phoenix 39.6 -18.9% 2.8%

12 Bayer 37.6 -19.5% 2.7%

13 Beta 34.2 -19.1% 2.4%

14 Boehringer Ingel 33.1 -22.4% 2.4%

15 Schering Plough 27.9 -21.2% 2.0%

16 Schering Ag 26.8 -18.7% 1.9%

17 Casasco 26.2 -18.1% 1.9%

18 Merck & Co 25.9 -26.2% 1.9%

19 Bristol-Myers Squibb 23.8 -26.5% 1.7%

20 Microsules/Bernabo 23.6 -20.0% 1.7%

Top 20 949.5 -20.6% 67.9%

25 Abbott 21.7 -26.4% 1.6%

Domestic Companies

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202371

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

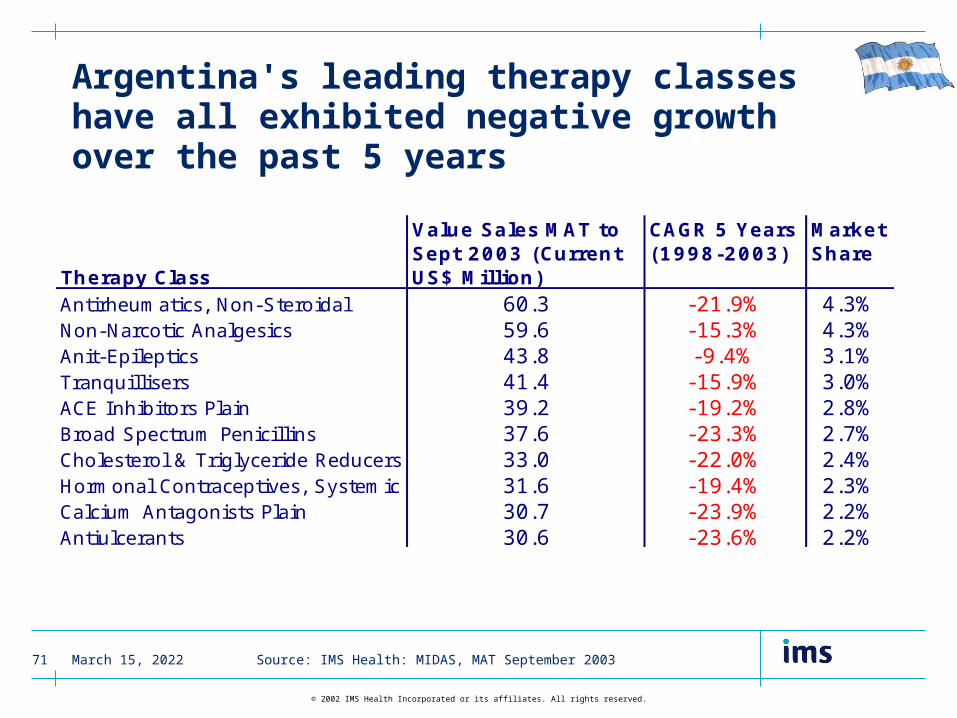

Argentina's leading therapy classes have all exhibited negative growth over the past 5 years

Therapy Class

Value Sales MAT to Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Antirheumatics, Non-Steroidal 60.3 -21.9% 4.3%Non-Narcotic Analgesics 59.6 -15.3% 4.3%Anit-Epileptics 43.8 -9.4% 3.1%Tranquillisers 41.4 -15.9% 3.0%ACE Inhibitors Plain 39.2 -19.2% 2.8%Broad Spectrum Penicillins 37.6 -23.3% 2.7%Cholesterol & Triglyceride Reducers 33.0 -22.0% 2.4%Hormonal Contraceptives, Systemic 31.6 -19.4% 2.3%Calcium Antagonists Plain 30.7 -23.9% 2.2%Antiulcerants 30.6 -23.6% 2.2%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202372

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

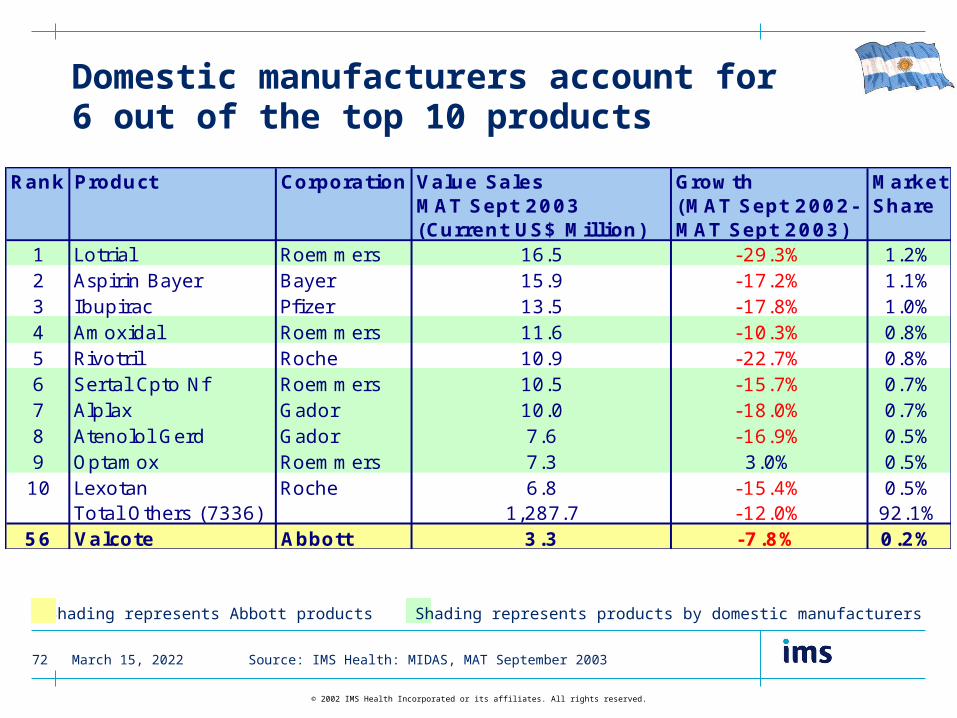

Domestic manufacturers account for 6 out of the top 10 products

Shading represents Abbott products Shading represents products by domestic manufacturers

Rank Product Corporation Value Sales MAT Sept 2003 (Current US$ Million)

Growth (MAT Sept 2002-MAT Sept 2003)

Market Share

1 Lotrial Roemmers 16.5 -29.3% 1.2%2 Aspirin Bayer Bayer 15.9 -17.2% 1.1%3 Ibupirac Pfizer 13.5 -17.8% 1.0%4 Amoxidal Roemmers 11.6 -10.3% 0.8%5 Rivotril Roche 10.9 -22.7% 0.8%6 Sertal Cpto Nf Roemmers 10.5 -15.7% 0.7%7 Alplax Gador 10.0 -18.0% 0.7%8 Atenolol Gerd Gador 7.6 -16.9% 0.5%9 Optamox Roemmers 7.3 3.0% 0.5%10 Lexotan Roche 6.8 -15.4% 0.5%

Total Others (7336) 1,287.7 -12.0% 92.1%56 Valcote Abbott 3.3 -7.8% 0.2%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202373

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

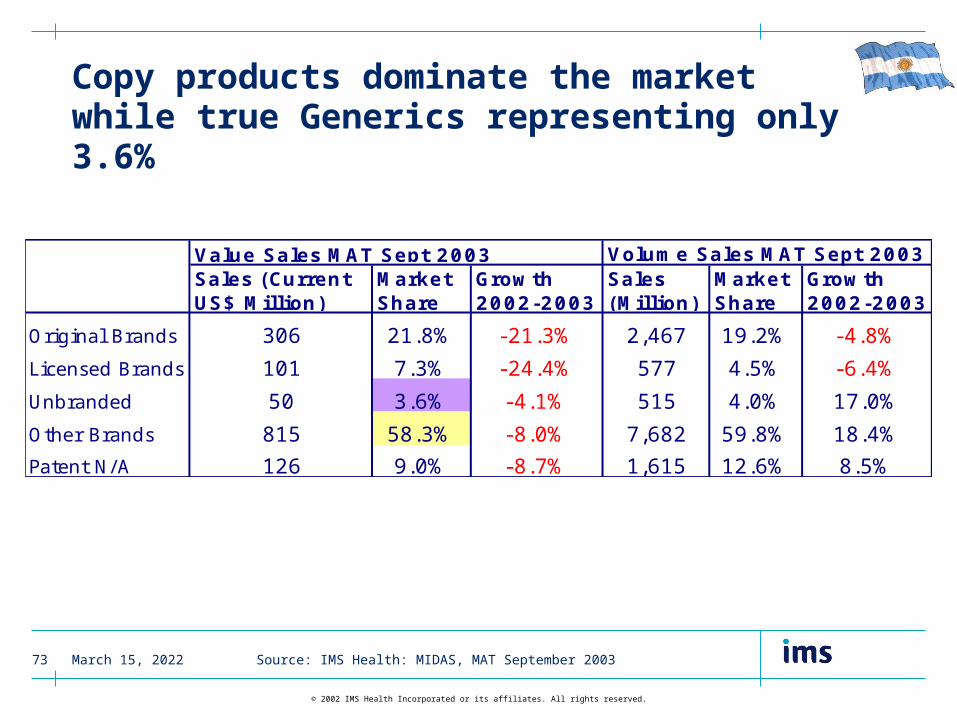

Copy products dominate the marketwhile true Generics representing only 3.6%

Volume Sales MAT Sept 2003Sales (Current US$ Million)

Market Share

Growth 2002-2003

Sales (Million)

Market Share

Growth 2002-2003

Original Brands 306 21.8% -21.3% 2,467 19.2% -4.8%

Licensed Brands 101 7.3% -24.4% 577 4.5% -6.4%

Unbranded 50 3.6% -4.1% 515 4.0% 17.0%

Other Brands 815 58.3% -8.0% 7,682 59.8% 18.4%

Patent N/A 126 9.0% -8.7% 1,615 12.6% 8.5%

Value Sales MAT Sept 2003

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202374

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Brazil

April 15, 202375

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

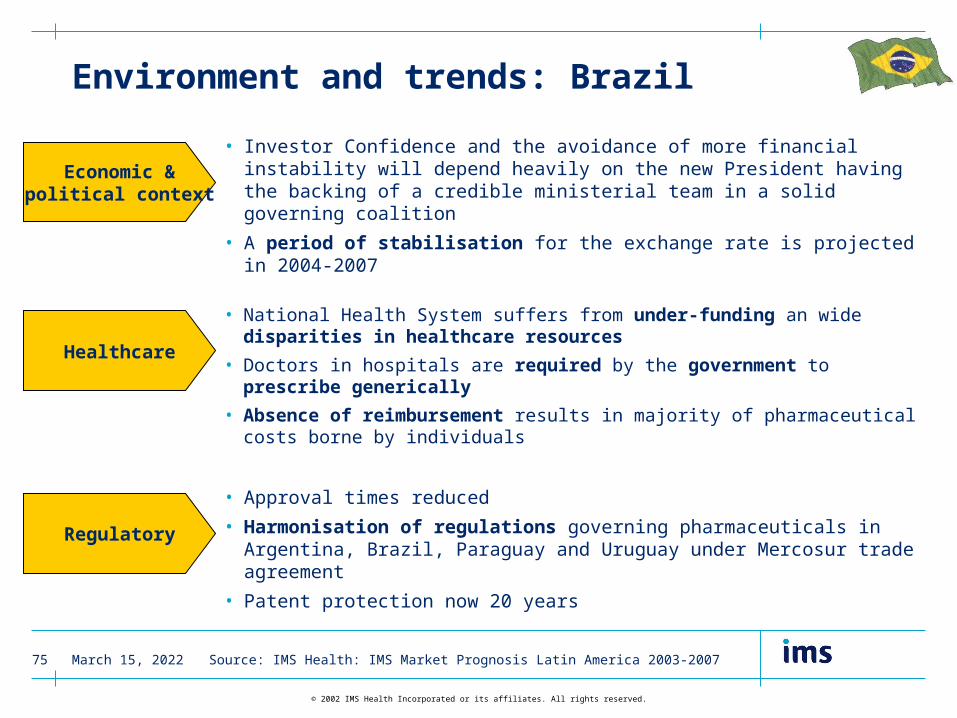

Environment and trends: Brazil

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

Economic &political context

Healthcare

Regulatory

• Investor Confidence and the avoidance of more financial instability will depend heavily on the new President having the backing of a credible ministerial team in a solid governing coalition

• A period of stabilisation for the exchange rate is projected in 2004-2007

• National Health System suffers from under-funding an wide disparities in healthcare resources

• Doctors in hospitals are required by the government to prescribe generically

• Absence of reimbursement results in majority of pharmaceutical costs borne by individuals

• Approval times reduced

• Harmonisation of regulations governing pharmaceuticals in Argentina, Brazil, Paraguay and Uruguay under Mercosur trade agreement

• Patent protection now 20 years

April 15, 202376

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Pharmaceutical business environment

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

• Generic companies gaining market share from original brand manufacturers

• Bioequivalent generics have achieved 5% of total retail market value and 4.5% of volume sales in 2 years

• OTC market ill-defined - many prescription only products sold by pharmacies without a prescription

• Prices frozen since 1999 - government drive to reduce healthcare costs - with occasional prices increases permitted

• Fragmented distribution system moving towards consolidation

April 15, 202377

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Two Brazilian companies among top 10: Ache Labs and EMS, ranked 2nd and 6th

Domestic Companies

Rank CorporationValue Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Brazil 3,722.0 -8.3% 100.0%

1 Pfizer 223.4 -7.9% 6.0%

2 Ache Labs 213.4 -10.2% 5.7%

3 Novartis 213.1 -12.4% 5.7%

4 Aventis 196.2 -13.1% 5.3%

5 Roche 136.5 -12.4% 3.7%

6 EMS 128.5 11.5% 3.5%

7 GlaxoSmithKline 123.8 -16.0% 3.3%

8 Merck & Co 111.2 -12.9% 3.0%

9 Schering Plough 111.0 -10.6% 3.0%

10 Schering Ag 109.7 -2.2% 2.9%

Top 10 1,566.8 -10.1% 42.1%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202378

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

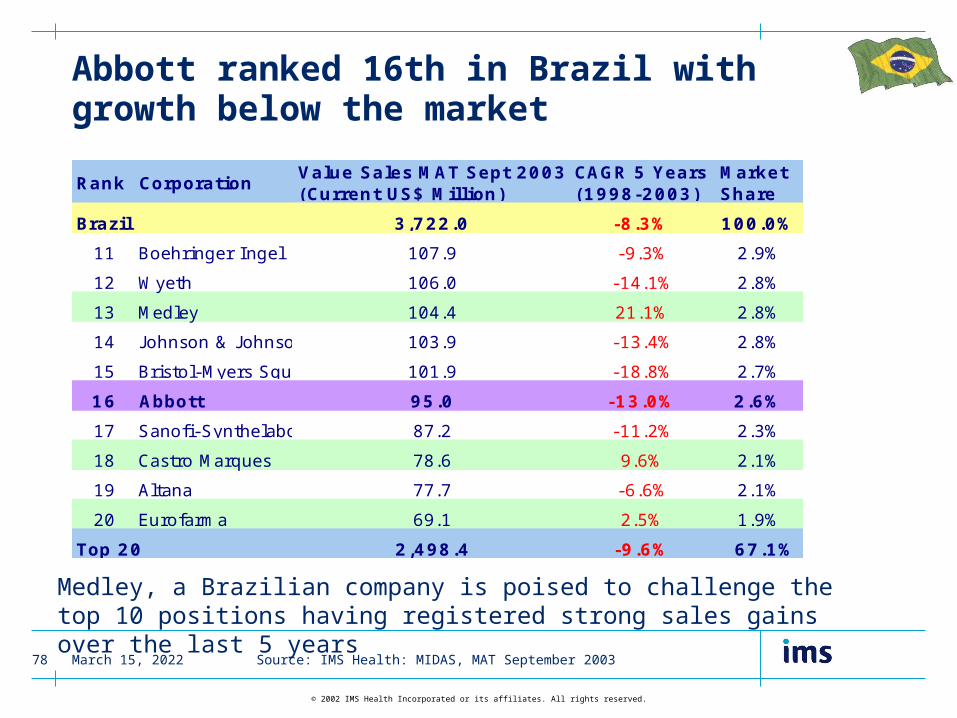

Abbott ranked 16th in Brazil with growth below the market

Medley, a Brazilian company is poised to challenge the top 10 positions having registered strong sales gains over the last 5 years

Rank CorporationValue Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Brazil 3,722.0 -8.3% 100.0%

11 Boehringer Ingel 107.9 -9.3% 2.9%

12 Wyeth 106.0 -14.1% 2.8%

13 Medley 104.4 21.1% 2.8%

14 J ohnson & J ohnson 103.9 -13.4% 2.8%

15 Bristol-Myers Squibb 101.9 -18.8% 2.7%

16 Abbott 95.0 -13.0% 2.6%

17 Sanofi-Synthelabo 87.2 -11.2% 2.3%

18 Castro Marques 78.6 9.6% 2.1%

19 Altana 77.7 -6.6% 2.1%

20 Eurofarma 69.1 2.5% 1.9%

Top 20 2,498.4 -9.6% 67.1%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202379

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Other Urological Preparations are the only class to have shown strong positive growth over the last 5 years

Therapy Class

Value Sales MAT to Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Antirheumatics, Non-Steroidal 187.3 -11.8% 5.0%Hormonal Contraceptives, Systemic 173.7 -2.9% 4.7%Non-Narcotic Analgesics 157.7 -9.5% 4.2%Antidepressants & Mood Stabilisers 106.9 0.6% 2.9%Tranquillisers 73.8 -7.7% 2.0%Other Urological Preparations 69.8 17.7% 1.9%Cholesterol & Triglyceride Reducers 69.6 -2.0% 1.9%Antiulcerants 69.1 -13.2% 1.9%Broad Spectrum Penicillins 62.6 -15.2% 1.7%Topical Nasal Preparations 61.4 -10.5% 1.6%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202380

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Abbott has the 8th highest selling product in Brazil - Neosaldina, a migraine treatment launched in 1972

Shading represents Abbott product

Rank Product Corporation Value Sales MAT Sept 2003(Current US$ Million)

Growth (MAT Sept 2002-MAT Sept 2003)

Market Share

1 Viagra Pfizer 52.6 1.0% 1.4%2 Voltaren Novartis 49.5 -22.5% 1.3%3 Miotan Aventis 32.0 -3.4% 0.9%4 Tylenol J & J 30.1 -25.3% 0.8%5 Vioxx Merck & Co 24.8 3.6% 0.7%6 Lipitor Pfizer 22.0 0.2% 0.6%7 Diane Schering AG 20.7 -0.6% 0.6%8 Neosaldina Abbott 19.9 -11.1% 0.5%9 Lexotan Roche 18.7 -18.5% 0.5%10 Novalgin Aventis 17.6 -20.4% 0.5%

Total Others (7336) 3,434.0 -8.6% 92.3%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202381

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

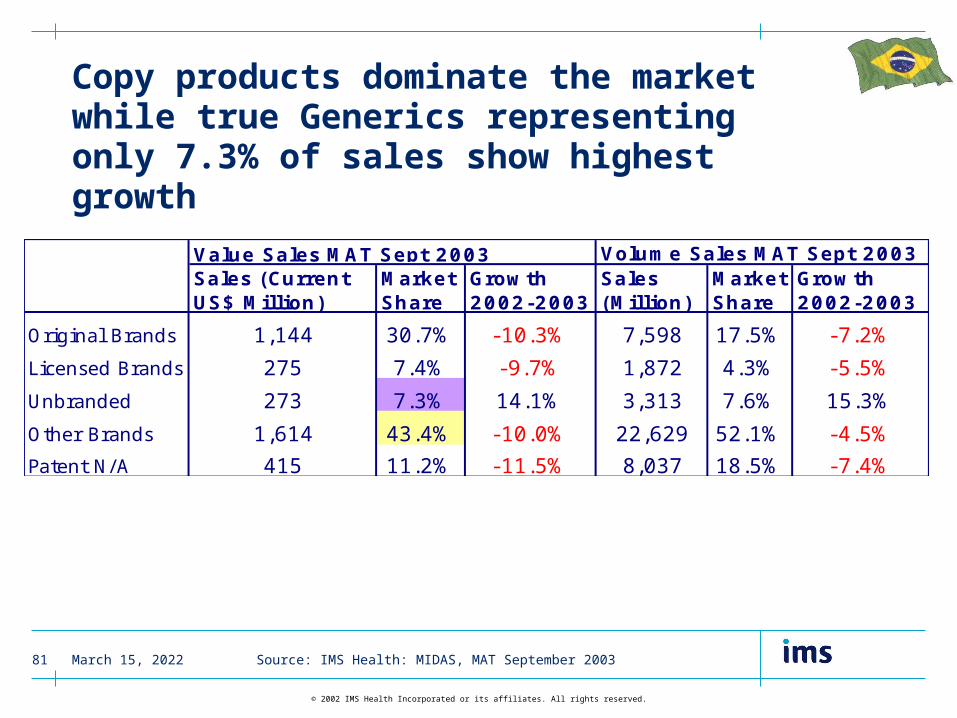

Copy products dominate the marketwhile true Generics representing only 7.3% of sales show highest growth

Volume Sales MAT Sept 2003Sales (Current US$ Million)

Market Share

Growth 2002-2003

Sales (Million)

Market Share

Growth 2002-2003

Original Brands 1,144 30.7% -10.3% 7,598 17.5% -7.2%

Licensed Brands 275 7.4% -9.7% 1,872 4.3% -5.5%

Unbranded 273 7.3% 14.1% 3,313 7.6% 15.3%

Other Brands 1,614 43.4% -10.0% 22,629 52.1% -4.5%

Patent N/A 415 11.2% -11.5% 8,037 18.5% -7.4%

Value Sales MAT Sept 2003

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202382

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Chile

April 15, 202383

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

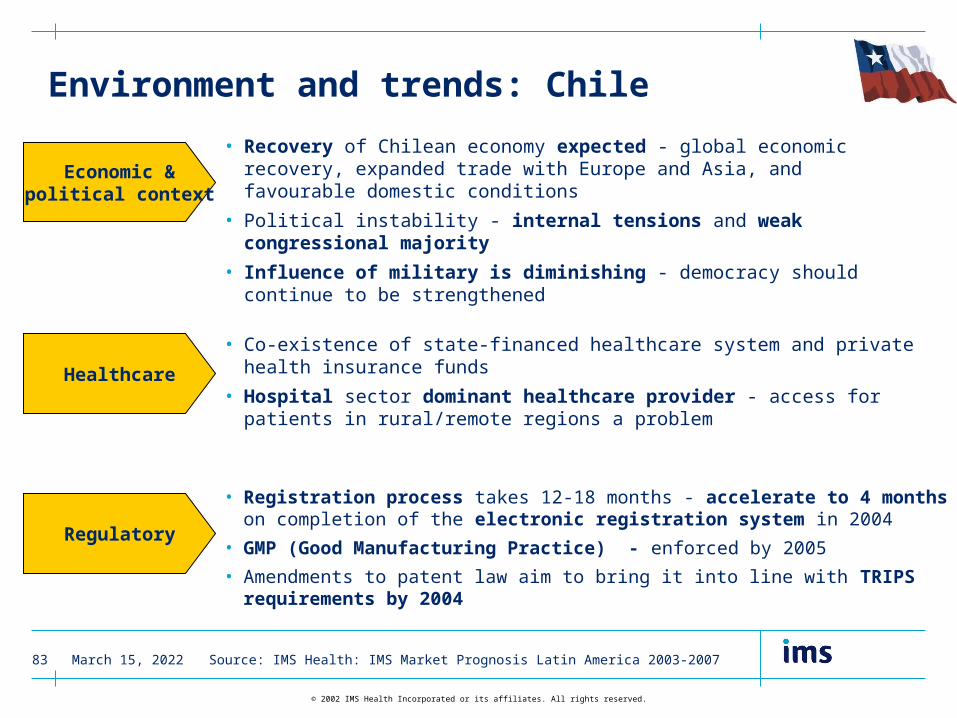

Environment and trends: Chile

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

Economic &political context

Healthcare

Regulatory

• Recovery of Chilean economy expected - global economic recovery, expanded trade with Europe and Asia, and favourable domestic conditions

• Political instability - internal tensions and weak congressional majority

• Influence of military is diminishing - democracy should continue to be strengthened

• Co-existence of state-financed healthcare system and private health insurance funds

• Hospital sector dominant healthcare provider - access for patients in rural/remote regions a problem

• Registration process takes 12-18 months - accelerate to 4 months on completion of the electronic registration system in 2004

• GMP (Good Manufacturing Practice) - enforced by 2005

• Amendments to patent law aim to bring it into line with TRIPS requirements by 2004

April 15, 202384

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Pharmaceutical business environment

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

• No signs of recovery for pharmaceutical market - depressed economic climate and shift in buying patterns to cheaper drugs

• Local industry thriving - 55% of Chilean market by value and 78% by volume - but threatened by globalisation trend

• Survival option - Local industry to seek alliances/licensing agreements with international companies

• Legislation governing generic substitution is ambiguous - practise of substitution widespread

• OTC market represents 19.4% of value sales and 27.7% of volume sales - good growth predicted

• High level of discounting in retail market is unsustainable in the long run

April 15, 202385

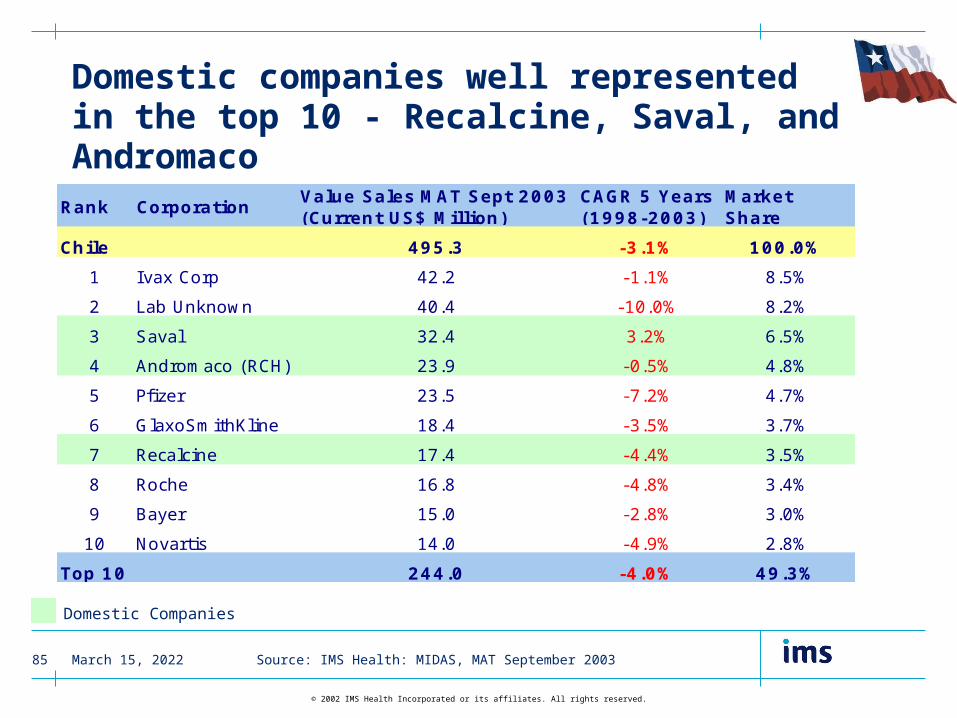

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Domestic companies well representedin the top 10 - Recalcine, Saval, and Andromaco

Domestic Companies

Rank CorporationValue Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Chile 495.3 -3.1% 100.0%

1 Ivax Corp 42.2 -1.1% 8.5%

2 Lab Unknown 40.4 -10.0% 8.2%

3 Saval 32.4 3.2% 6.5%

4 Andromaco (RCH) 23.9 -0.5% 4.8%

5 Pfizer 23.5 -7.2% 4.7%

6 GlaxoSmithKline 18.4 -3.5% 3.7%

7 Recalcine 17.4 -4.4% 3.5%

8 Roche 16.8 -4.8% 3.4%

9 Bayer 15.0 -2.8% 3.0%

10 Novartis 14.0 -4.9% 2.8%

Top 10 244.0 -4.0% 49.3%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202386

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

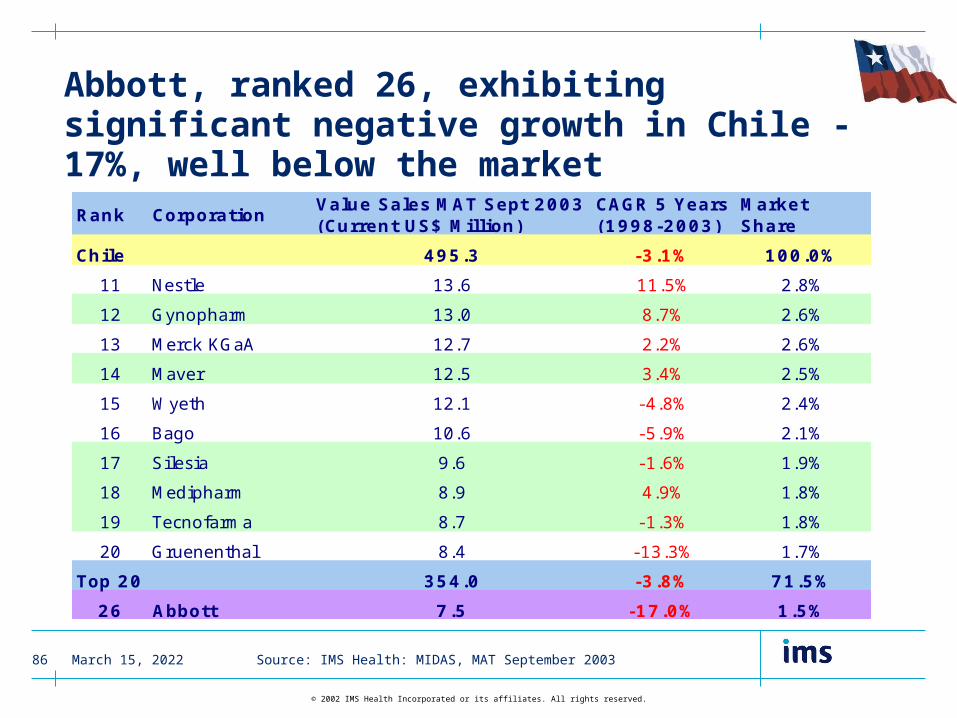

Abbott, ranked 26, exhibiting significant negative growth in Chile -17%, well below the market

Rank CorporationValue Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Chile 495.3 -3.1% 100.0%

11 Nestle 13.6 11.5% 2.8%

12 Gynopharm 13.0 8.7% 2.6%

13 Merck KGaA 12.7 2.2% 2.6%

14 Maver 12.5 3.4% 2.5%

15 Wyeth 12.1 -4.8% 2.4%

16 Bago 10.6 -5.9% 2.1%

17 Silesia 9.6 -1.6% 1.9%

18 Medipharm 8.9 4.9% 1.8%

19 Tecnofarma 8.7 -1.3% 1.8%

20 Gruenenthal 8.4 -13.3% 1.7%

Top 20 354.0 -3.8% 71.5%

26 Abbott 7.5 -17.0% 1.5%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202387

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Non-narcotic analgesics top therapyclass but anti-epileptics and infant formulas have exhibited the highest growth

Therapy Class

Value Sales MAT to Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Non-Narcotic Analgesics 27.3 -3.8% 5.5%Antirheumatics, Non-Steroidal 24.2 -2.8% 4.9%Hormonal Contraceptives, Systemic 22.4 -1.8% 4.5%Antidepressants & Mood Stabilisers 18.0 1.7% 3.6%Infant Formulas 13.3 12.4% 2.7%Cholesterol & Triglyceride Reducers 12.2 0.0% 2.5%Cold Preparations 10.6 -4.2% 2.1%Anti-Epileptics 9.7 12.9% 2.0%Anti-Obesity Preparations exc Dietetics 9.5 -6.9% 1.9%Antiulcerants 9.3 -8.4% 1.9%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202388

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

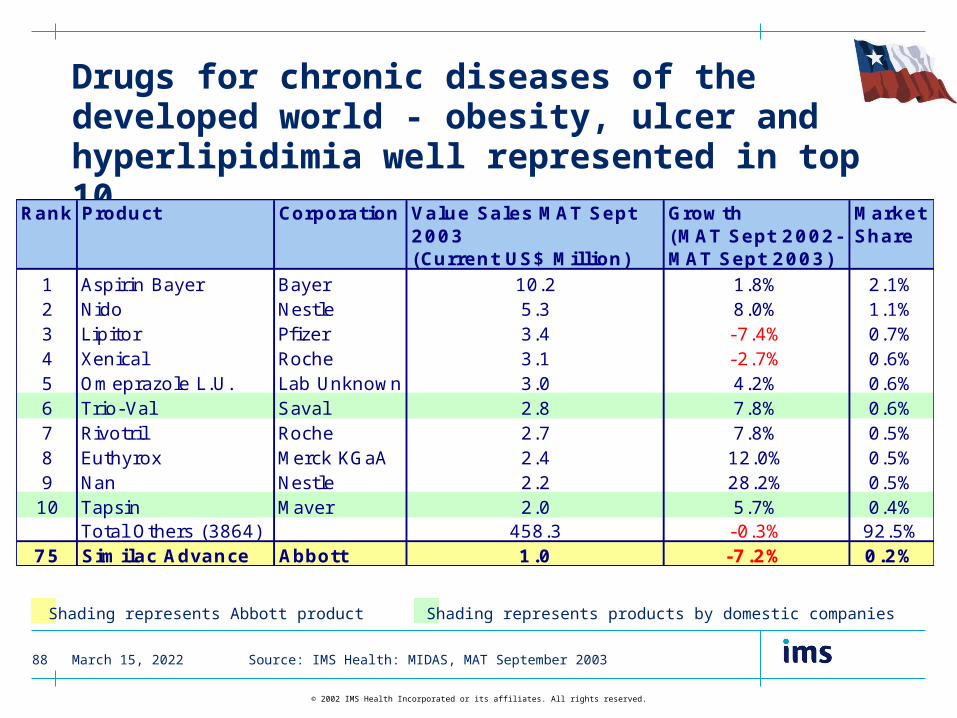

Drugs for chronic diseases of the developed world - obesity, ulcer and hyperlipidimia well represented in top 10

Rank Product Corporation Value Sales MAT Sept 2003(Current US$ Million)

Growth (MAT Sept 2002-MAT Sept 2003)

Market Share

1 Aspirin Bayer Bayer 10.2 1.8% 2.1%2 Nido Nestle 5.3 8.0% 1.1%3 Lipitor Pfizer 3.4 -7.4% 0.7%4 Xenical Roche 3.1 -2.7% 0.6%5 Omeprazole L.U. Lab Unknown 3.0 4.2% 0.6%6 Trio-Val Saval 2.8 7.8% 0.6%7 Rivotril Roche 2.7 7.8% 0.5%8 Euthyrox Merck KGaA 2.4 12.0% 0.5%9 Nan Nestle 2.2 28.2% 0.5%10 Tapsin Maver 2.0 5.7% 0.4%

Total Others (3864) 458.3 -0.3% 92.5%75 Similac Advance Abbott 1.0 -7.2% 0.2%

Shading represents products by domestic companies

Source: IMS Health: MIDAS, MAT September 2003

Shading represents Abbott product

April 15, 202389

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

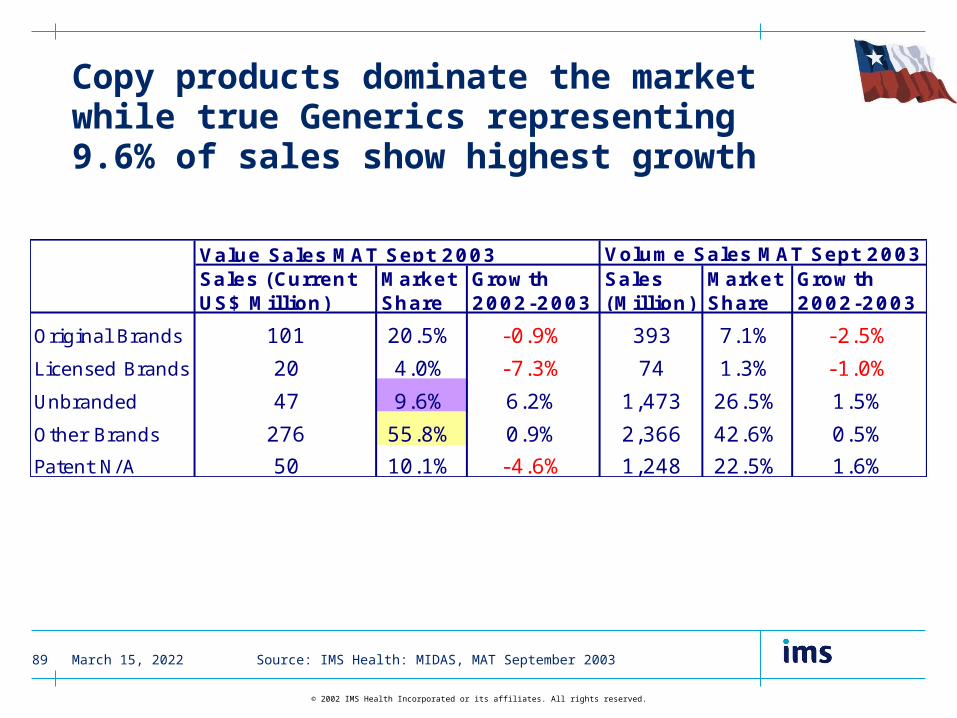

Copy products dominate the marketwhile true Generics representing 9.6% of sales show highest growth

Volume Sales MAT Sept 2003Sales (Current US$ Million)

Market Share

Growth 2002-2003

Sales (Million)

Market Share

Growth 2002-2003

Original Brands 101 20.5% -0.9% 393 7.1% -2.5%

Licensed Brands 20 4.0% -7.3% 74 1.3% -1.0%

Unbranded 47 9.6% 6.2% 1,473 26.5% 1.5%

Other Brands 276 55.8% 0.9% 2,366 42.6% 0.5%

Patent N/A 50 10.1% -4.6% 1,248 22.5% 1.6%

Value Sales MAT Sept 2003

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202390

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Colombia

April 15, 202391

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Environment and trends: Colombia

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

Economic &political context

Healthcare

Regulatory

• The Colombian economy remains sluggish

• Long running Colombian civil war continues - attacks from rebel armed forces aimed at destabilising the political environment

• Currency depreciation risks remain - renewed rebel violence and widening public sector debt

• Healthcare reforms high on the governments agenda - expand healthcare coverage

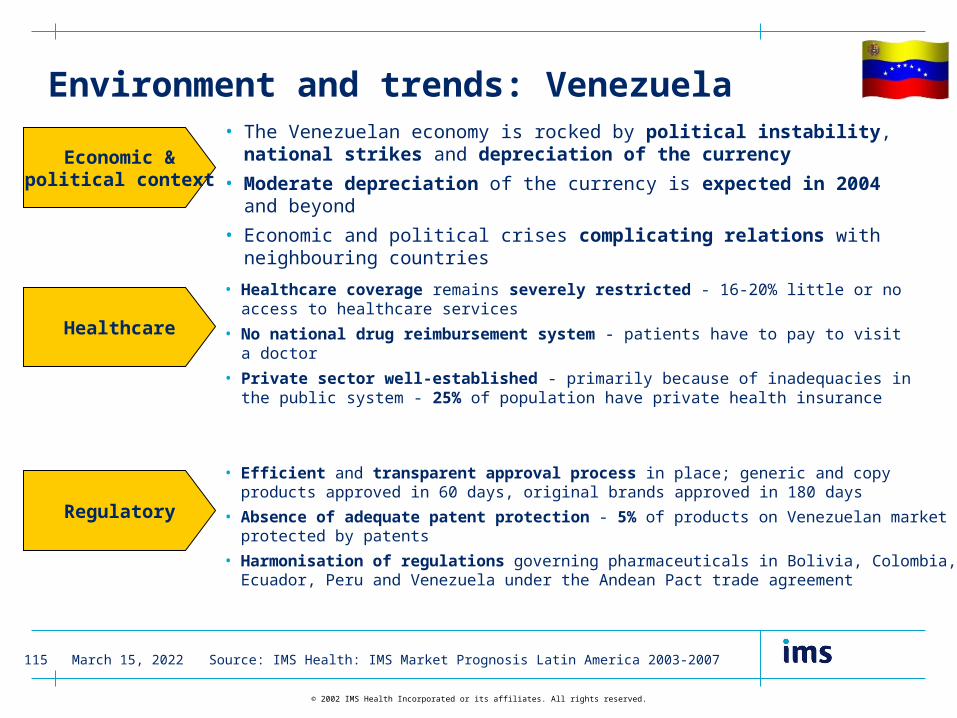

• GP referral system introduced - shortage of doctors affects rural areas

• 7% of population have private health insurance

• Bioavailability and bioequivalence studies mandatory for generics - uncertainty about which products to comply

• Harmonisation of regulations governing pharmaceuticals in Bolivia, Colombia, Ecuador, Peru and Venezuela under the Andean Pact

• Improved intellectual property protection of pharmaceutical patents

April 15, 202392

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Pharmaceutical business environment

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

• Colombian pharmaceutical market driven by price rather than volume growth

• Local pharmaceutical industry developed strongly - ability to copy new products

• Manufacturing by multinationals driven out - lawlessness and civil war

• Generics culture - doctors in public sector legally obliged to prescribe generically - generics companies gaining market share from original brand manufacturers

• Illegal OTC dispensing of prescription drugs - adoption of International Classification System for OTC medicines should help

April 15, 202393

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Abbott ranked 4th in Colombia with below market growth

Rank CorporationValue Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Colombia 798.5 -2.9% 100.0%

1 Pfizer 56.7 -8.9% 7.1%

2 Wyeth 50.7 -2.5% 6.4%

3 GlaxoSmithKline 39.3 -4.1% 4.9%

4 Abbott 38.2 -3.3% 4.8%

5 Novartis 33.2 -2.9% 4.2%

6 Boehringer Ingel 32.4 -4.8% 4.1%

7 Nestle 31.6 2.7% 4.0%

8 Schering Ag 31.6 5.5% 4.0%

9 Schering Plough 28.4 -4.3% 3.6%

10 Bayer 26.7 -8.3% 3.3%

Top 10 368.8 -3.8% 46.2%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202394

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Domestic/regional players are the only companies ranked 11-20 to exhibit positive growth

Domestic Companies

Rank CorporationValue Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Colombia 798.5 -2.9% 100.0%

11 Aventis 24.5 -9.4% 3.1%

12 Genfar 23.8 2.9% 3.0%

13 Roche 23.5 -3.0% 2.9%

14 Bristol-Myers Squibb 21.2 -10.6% 2.6%

15 Lafrancol 18.4 6.7% 2.3%

16 Sanofi-Synthelabo 18.2 -1.6% 2.3%

17 Merck & Co 17.9 -2.8% 2.2%

18 Tecnoquimicas 14.9 3.2% 1.9%

19 Merck KGaA 13.8 -2.6% 1.7%

20 Grupo Farma 12.8 4.8% 1.6%

Top 20 557.7 -3.4% 69.8%

Source: IMS Health: MIDAS, MAT September 2003

Venezuelan Company

April 15, 202395

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

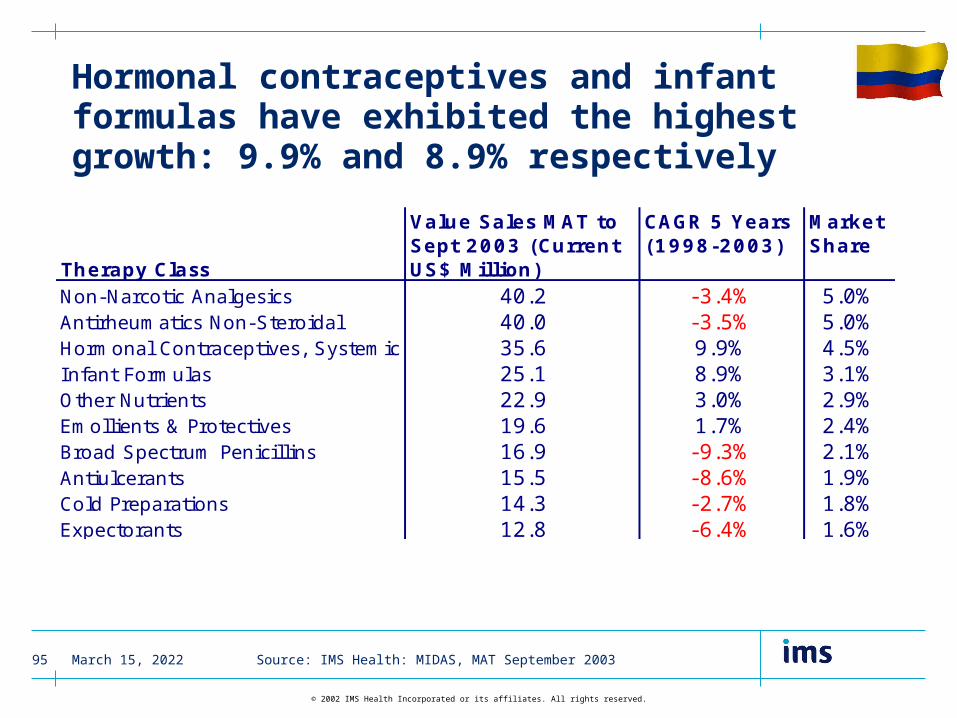

Hormonal contraceptives and infant formulas have exhibited the highest growth: 9.9% and 8.9% respectively

Therapy Class

Value Sales MAT to Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Non-Narcotic Analgesics 40.2 -3.4% 5.0%Antirheumatics Non-Steroidal 40.0 -3.5% 5.0%Hormonal Contraceptives, Systemic 35.6 9.9% 4.5%Infant Formulas 25.1 8.9% 3.1%Other Nutrients 22.9 3.0% 2.9%Emollients & Protectives 19.6 1.7% 2.4%Broad Spectrum Penicillins 16.9 -9.3% 2.1%Antiulcerants 15.5 -8.6% 1.9%Cold Preparations 14.3 -2.7% 1.8%Expectorants 12.8 -6.4% 1.6%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202396

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

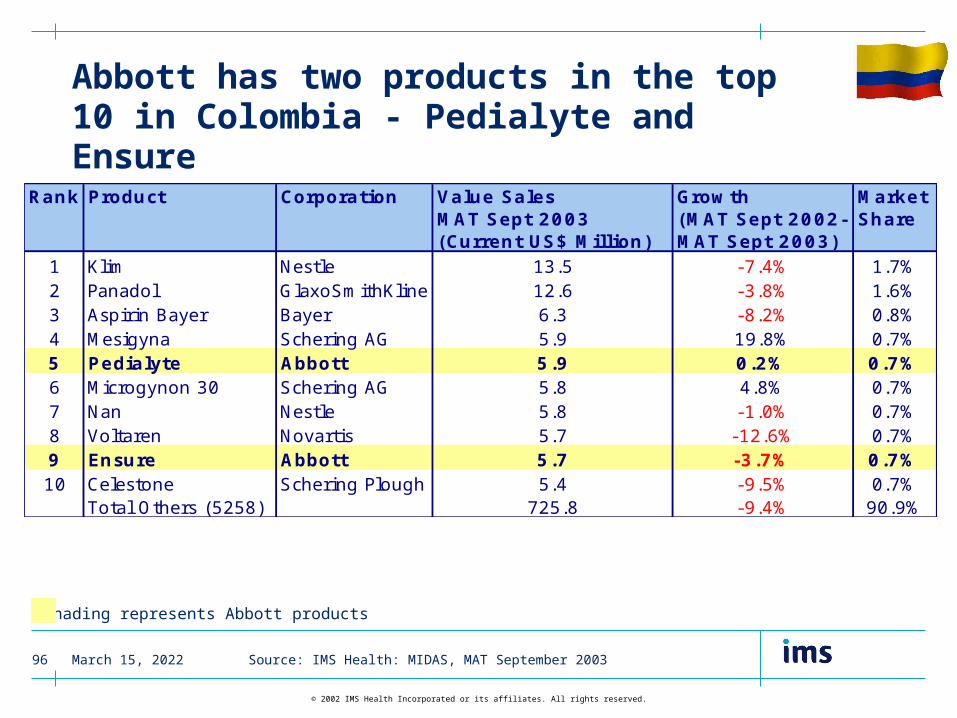

Abbott has two products in the top 10 in Colombia - Pedialyte and Ensure

Shading represents Abbott products

Rank Product Corporation Value Sales MAT Sept 2003 (Current US$ Million)

Growth (MAT Sept 2002-MAT Sept 2003)

Market Share

1 Klim Nestle 13.5 -7.4% 1.7%2 Panadol GlaxoSmithKline 12.6 -3.8% 1.6%3 Aspirin Bayer Bayer 6.3 -8.2% 0.8%4 Mesigyna Schering AG 5.9 19.8% 0.7%5 Pedialyte Abbott 5.9 0.2% 0.7%6 Microgynon 30 Schering AG 5.8 4.8% 0.7%7 Nan Nestle 5.8 -1.0% 0.7%8 Voltaren Novartis 5.7 -12.6% 0.7%9 Ensure Abbott 5.7 -3.7% 0.7%10 Celestone Schering Plough 5.4 -9.5% 0.7%

Total Others (5258) 725.8 -9.4% 90.9%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202397

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

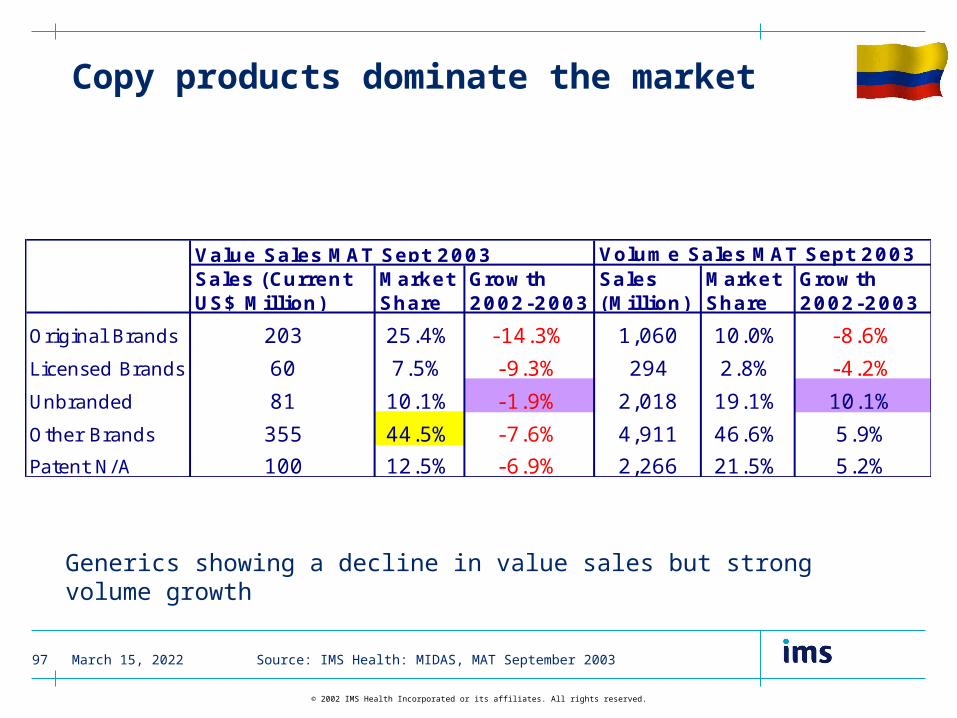

Copy products dominate the market

Generics showing a decline in value sales but strong volume growth

Volume Sales MAT Sept 2003Sales (Current US$ Million)

Market Share

Growth 2002-2003

Sales (Million)

Market Share

Growth 2002-2003

Original Brands 203 25.4% -14.3% 1,060 10.0% -8.6%

Licensed Brands 60 7.5% -9.3% 294 2.8% -4.2%

Unbranded 81 10.1% -1.9% 2,018 19.1% 10.1%

Other Brands 355 44.5% -7.6% 4,911 46.6% 5.9%

Patent N/A 100 12.5% -6.9% 2,266 21.5% 5.2%

Value Sales MAT Sept 2003

Source: IMS Health: MIDAS, MAT September 2003

April 15, 202398

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Mexico

April 15, 202399

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

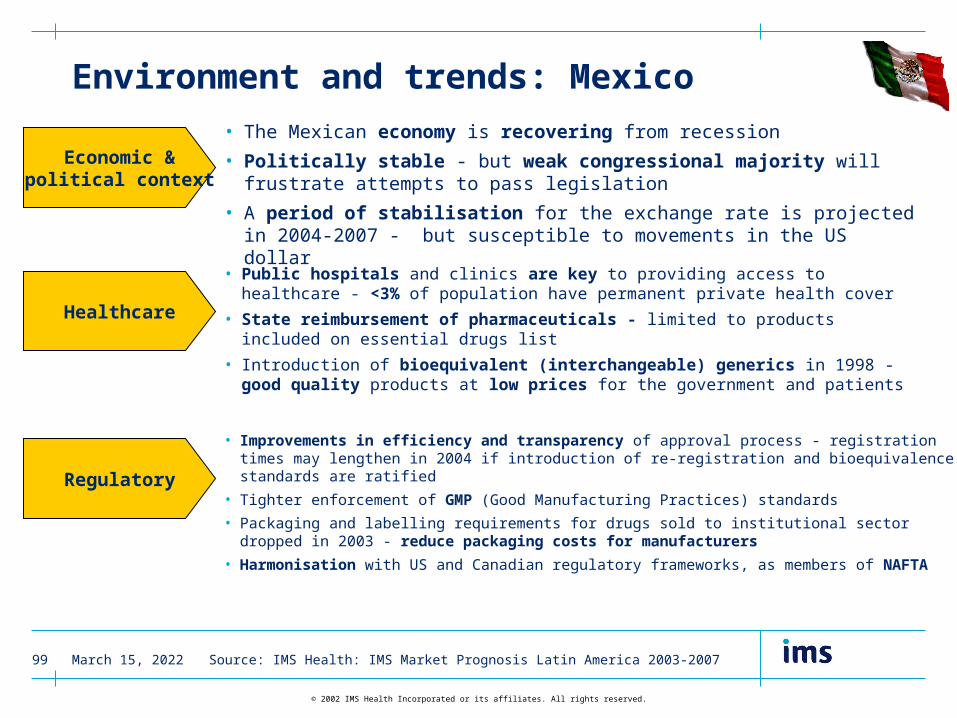

Environment and trends: Mexico

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

Economic &political context

Healthcare

Regulatory

• The Mexican economy is recovering from recession

• Politically stable - but weak congressional majority will frustrate attempts to pass legislation

• A period of stabilisation for the exchange rate is projected in 2004-2007 - but susceptible to movements in the US dollar

• Public hospitals and clinics are key to providing access to healthcare - <3% of population have permanent private health cover

• State reimbursement of pharmaceuticals - limited to products included on essential drugs list

• Introduction of bioequivalent (interchangeable) generics in 1998 - good quality products at low prices for the government and patients

• Improvements in efficiency and transparency of approval process - registration times may lengthen in 2004 if introduction of re-registration and bioequivalence standards are ratified

• Tighter enforcement of GMP (Good Manufacturing Practices) standards

• Packaging and labelling requirements for drugs sold to institutional sector dropped in 2003 - reduce packaging costs for manufacturers

• Harmonisation with US and Canadian regulatory frameworks, as members of NAFTA

April 15, 2023100

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

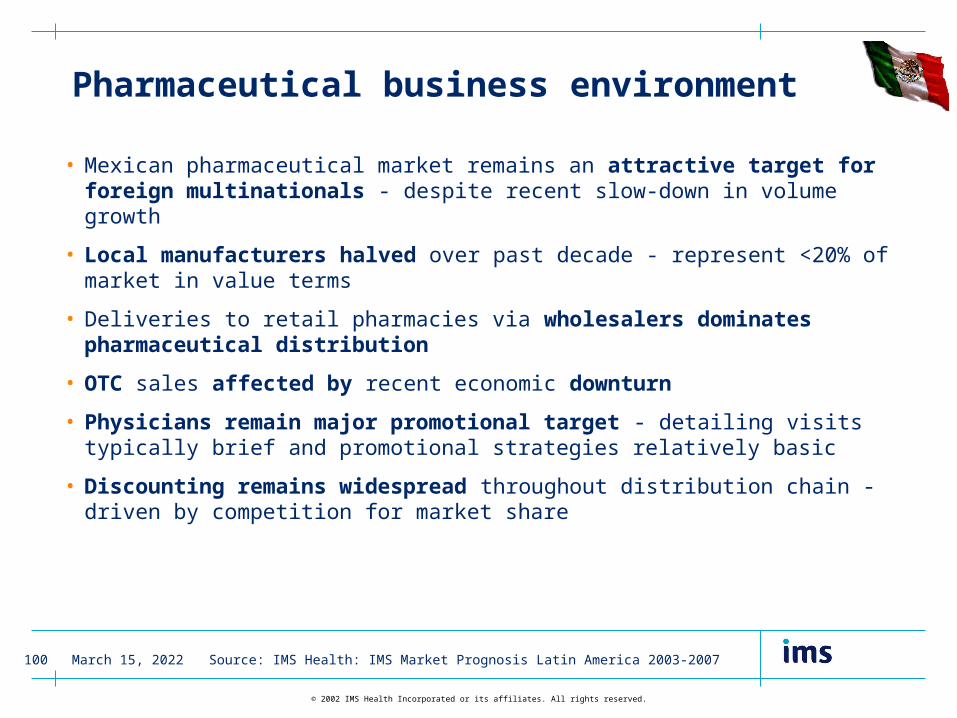

Pharmaceutical business environment

Source: IMS Health: IMS Market Prognosis Latin America 2003-2007

• Mexican pharmaceutical market remains an attractive target for foreign multinationals - despite recent slow-down in volume growth

• Local manufacturers halved over past decade - represent <20% of market in value terms

• Deliveries to retail pharmacies via wholesalers dominates pharmaceutical distribution

• OTC sales affected by recent economic downturn

• Physicians remain major promotional target - detailing visits typically brief and promotional strategies relatively basic

• Discounting remains widespread throughout distribution chain - driven by competition for market share

April 15, 2023101

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

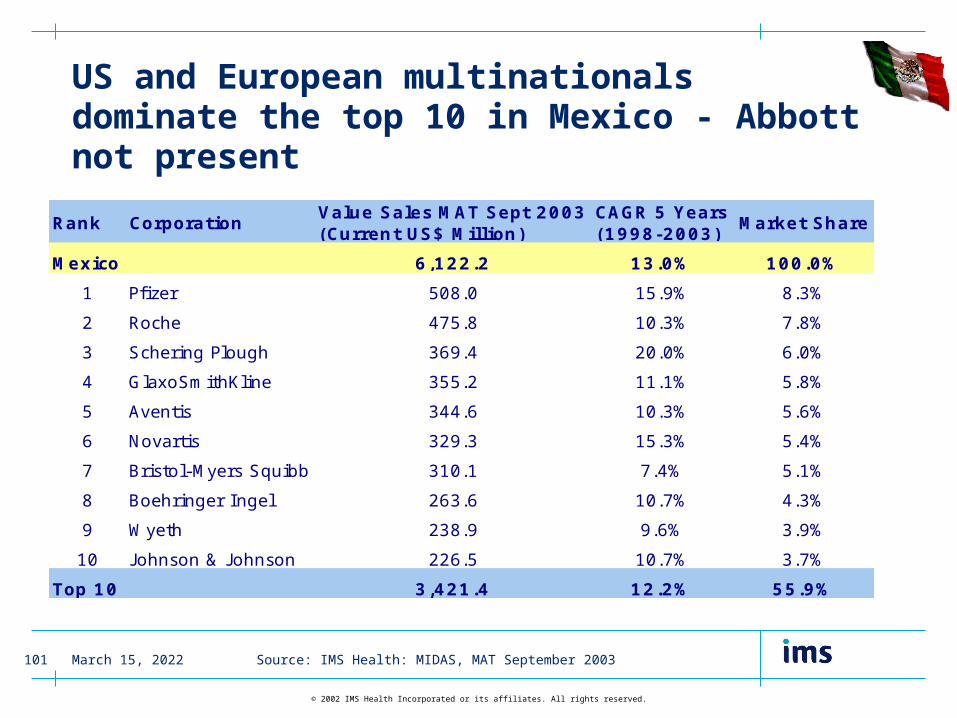

US and European multinationals dominate the top 10 in Mexico - Abbott not present

Rank CorporationValue Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Mexico 6,122.2 13.0% 100.0%

1 Pfizer 508.0 15.9% 8.3%

2 Roche 475.8 10.3% 7.8%

3 Schering Plough 369.4 20.0% 6.0%

4 GlaxoSmithKline 355.2 11.1% 5.8%

5 Aventis 344.6 10.3% 5.6%

6 Novartis 329.3 15.3% 5.4%

7 Bristol-Myers Squibb 310.1 7.4% 5.1%

8 Boehringer Ingel 263.6 10.7% 4.3%

9 Wyeth 238.9 9.6% 3.9%

10 J ohnson & J ohnson 226.5 10.7% 3.7%

Top 10 3,421.4 12.2% 55.9%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 2023102

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

Abbott ranked 13th but trails the market in terms of growth

Rank CorporationValue Sales MAT Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Mexico 6,122.2 13.0% 100.0%

11 Merck & Co 185.6 25.4% 3.0%

12 Bayer 171.8 9.1% 2.8%

13 Abbott 166.5 7.0% 2.7%

14 Altana 160.1 18.2% 2.6%

15 Senosiain 151.5 12.8% 2.5%

16 AstraZeneca 133.4 18.1% 2.2%

17 Merck KGaA 120.6 14.8% 2.0%

18 Sanofi-Synthelabo 117.7 12.6% 1.9%

19 ICN 114.5 11.2% 1.9%

20 Lilly 107.8 20.0% 1.8%

Top 20 4,850.9 12.8% 79.2%

Source: IMS Health: MIDAS, MAT September 2003

Domestic Companies

April 15, 2023103

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

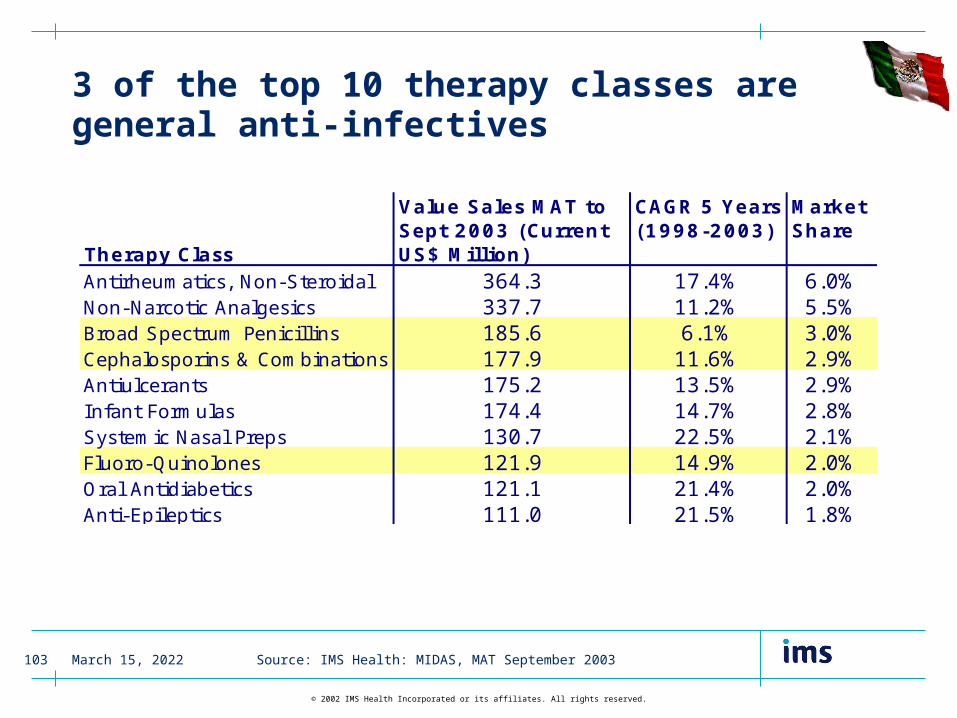

3 of the top 10 therapy classes are general anti-infectives

Therapy Class

Value Sales MAT to Sept 2003 (Current US$ Million)

CAGR 5 Years (1998-2003)

Market Share

Antirheumatics, Non-Steroidal 364.3 17.4% 6.0%Non-Narcotic Analgesics 337.7 11.2% 5.5%Broad Spectrum Penicillins 185.6 6.1% 3.0%Cephalosporins & Combinations 177.9 11.6% 2.9%Antiulcerants 175.2 13.5% 2.9%Infant Formulas 174.4 14.7% 2.8%Systemic Nasal Preps 130.7 22.5% 2.1%Fluoro-Quinolones 121.9 14.9% 2.0%Oral Antidiabetics 121.1 21.4% 2.0%Anti-Epileptics 111.0 21.5% 1.8%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 2023104

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

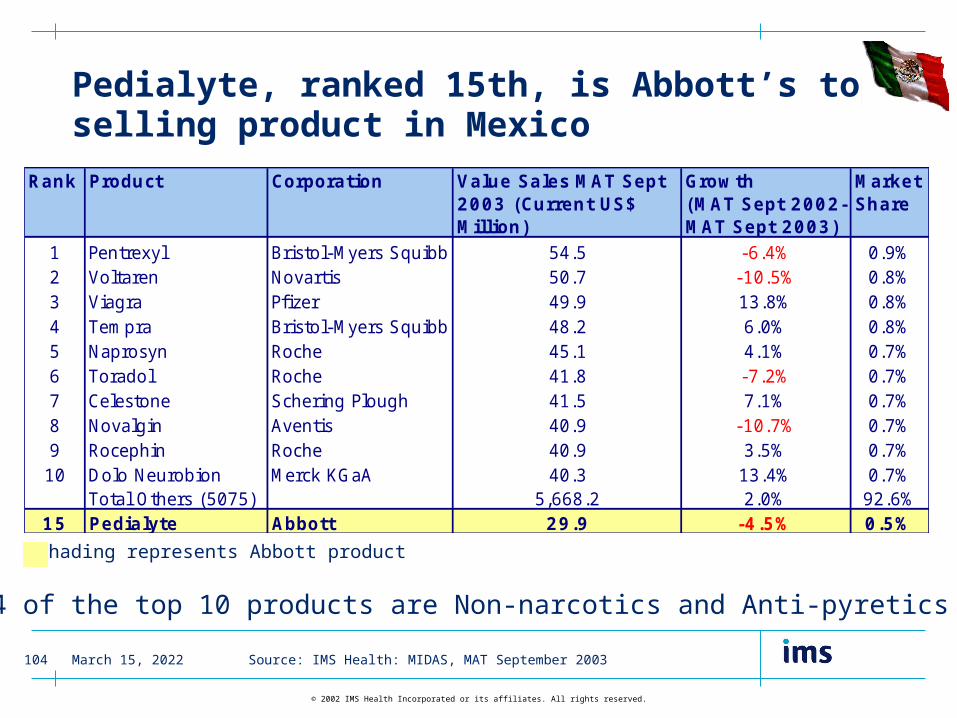

Pedialyte, ranked 15th, is Abbott’s top selling product in Mexico

Shading represents Abbott product

4 of the top 10 products are Non-narcotics and Anti-pyretics

Rank Product Corporation Value Sales MAT Sept 2003 (Current US$ Million)

Growth (MAT Sept 2002-MAT Sept 2003)

Market Share

1 Pentrexyl Bristol-Myers Squibb 54.5 -6.4% 0.9%2 Voltaren Novartis 50.7 -10.5% 0.8%3 Viagra Pfizer 49.9 13.8% 0.8%4 Tempra Bristol-Myers Squibb 48.2 6.0% 0.8%5 Naprosyn Roche 45.1 4.1% 0.7%6 Toradol Roche 41.8 -7.2% 0.7%7 Celestone Schering Plough 41.5 7.1% 0.7%8 Novalgin Aventis 40.9 -10.7% 0.7%9 Rocephin Roche 40.9 3.5% 0.7%10 Dolo Neurobion Merck KGaA 40.3 13.4% 0.7%

Total Others (5075) 5,668.2 2.0% 92.6%15 Pedialyte Abbott 29.9 -4.5% 0.5%

Source: IMS Health: MIDAS, MAT September 2003

April 15, 2023105

© 2002 IMS Health Incorporated or its affiliates. All rights reserved.

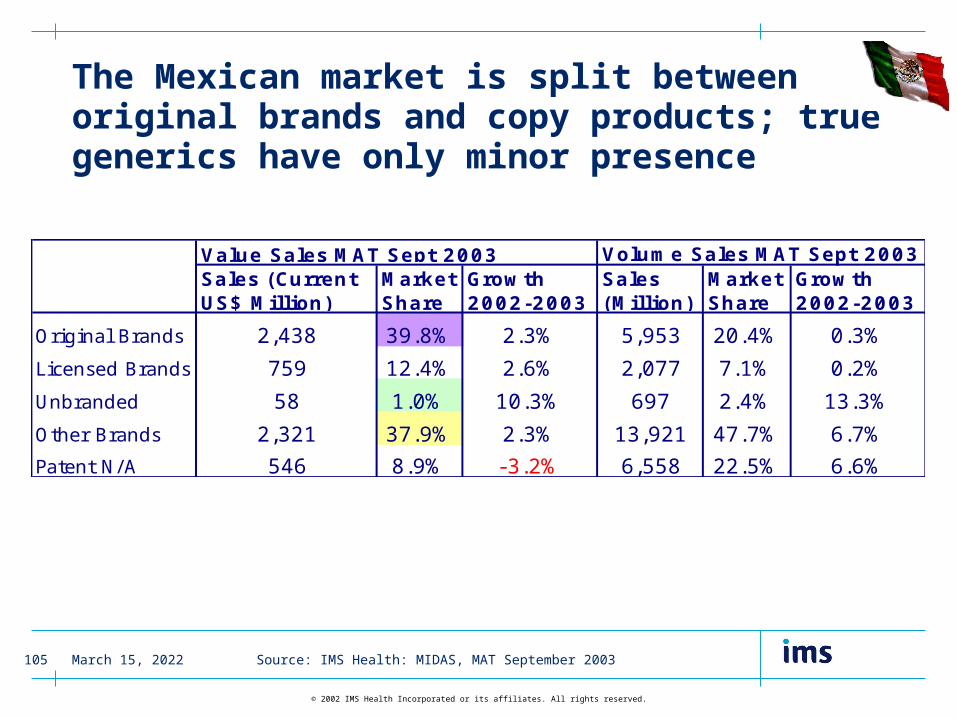

The Mexican market is split between original brands and copy products; true generics have only minor presence

Volume Sales MAT Sept 2003Sales (Current US$ Million)

Market Share

Growth 2002-2003

Sales (Million)

Market Share