Improved representation of investment decisions ... · Improved Representation of Investment...

42

Gokul C. Iyer, Leon E. Clarke, James A. Edmonds, Brian P. Flannery, Nathan E. Hultman, Haewon C. McJeon, David G. Victor Contents Supplementary Text ........................................................................................................................ 1 1 Background ............................................................................................................................. 1 1.1 Factors affecting investment ............................................................................................ 1 1.2 Special case: Investment in China.................................................................................... 4 2 The cost of capital ................................................................................................................... 5 3 Implications of the logit technology choice formulation ........................................................ 6 4 Sensitivity analyses ................................................................................................................. 7 4.1 Sensitivity of results to global emissions target ............................................................... 8 4.2 Sensitivity of results to FCR assumptions ....................................................................... 8 4.3 High investment risks for fossil-fuel technologies ........................................................... 9 Supplementary Figures ................................................................................................................. 11 Supplementary Tables ................................................................................................................... 33 References ..................................................................................................................................... 38 Supplementary Text 1 Background 1.1 Factors affecting investment Many factors can affect patterns of investment. The vast literature on institutional economics discusses the impact of institutional quality on investment and economy-wide capital formation. Institutions are the formal and informal rules that constrain individual behavior and shape human interaction. Institutions are devised to create order and reduce uncertainty in exchange. A solid institutional framework is necessary to encourage investment. Investors will be reluctant to risk Improved representation of investment decisions in assessments of CO 2 mitigation SUPPLEMENTARY INFORMATION DOI: 10.1038/NCLIMATE2553 NATURE CLIMATE CHANGE | www.nature.com/natureclimatechange 1 © 2015 Macmillan Publishers Limited. All rights reserved.

Transcript of Improved representation of investment decisions ... · Improved Representation of Investment...

1

Improved Representation of Investment Decisions in Assessments of CO2 Mitigation

Gokul C. Iyer, Leon E. Clarke, James A. Edmonds, Brian P. Flannery, Nathan E.

Hultman, Haewon C. McJeon, David G. Victor

Contents Supplementary Text ........................................................................................................................ 1

1 Background ............................................................................................................................. 1

1.1 Factors affecting investment ............................................................................................ 1

1.2 Special case: Investment in China .................................................................................... 4

2 The cost of capital ................................................................................................................... 5

3 Implications of the logit technology choice formulation ........................................................ 6

4 Sensitivity analyses ................................................................................................................. 7

4.1 Sensitivity of results to global emissions target ............................................................... 8

4.2 Sensitivity of results to FCR assumptions ....................................................................... 8

4.3 High investment risks for fossil-fuel technologies ........................................................... 9

Supplementary Figures ................................................................................................................. 11

Supplementary Tables ................................................................................................................... 33

References ..................................................................................................................................... 38

Supplementary Text

1 Background

1.1 Factors affecting investment Many factors can affect patterns of investment. The vast literature on institutional economics

discusses the impact of institutional quality on investment and economy-wide capital formation.

Institutions are the formal and informal rules that constrain individual behavior and shape human

interaction. Institutions are devised to create order and reduce uncertainty in exchange. A solid

institutional framework is necessary to encourage investment. Investors will be reluctant to risk

Improved representation of investment decisions in assessments of CO2 mitigation

SUPPLEMENTARY INFORMATIONDOI: 10.1038/NCLIMATE2553

NATURE CLIMATE CHANGE | www.nature.com/natureclimatechange 1© 2015 Macmillan Publishers Limited. All rights reserved.

2

their capital when property rights are weak and poorly protected, and if, as a result, they fear that

their returns may be appropriated by others.1 Empirical studies on the link between institutions

and investment have confirmed this theory. For example, Acemoglu and Zilibotti 2 showed that

in developing countries that lack large and efficient financial markets, investors tend to invest in

safer projects with lower return because the presence of indivisible projects limits the degree of

risk diversification. Not only does this slow down capital accumulation, but the inability to

diversify idiosyncratic risk also introduces a large amount of uncertainty in the overall economic

growth process. Empirical research also shows that institutional quality affects foreign direct

investment (FDI). Investors considering FDI may be particularly concerned about the likely

exposure to requests for bribes and the need to work through red-tape in host countries.3 In a

related strand of research, scholars have emphasized the importance of protection of investors’

rights in affecting investment. For example, La Porta, Lopez-de-Silanes 4 used a sample of 49

countries and showed that countries with poorer protection of investor rights (that include not

only the rights written into the laws and regulations but also the effectiveness of their

enforcement) have unsophisticated debt and equity markets. Similarly, Clague, Keefer 5 showed

that investment is adversely affected in countries that lack adequate third-party contract

enforcement. Finally, credibility and effectiveness of regulations and hence their ability to

facilitate private investment vary with a country’s institutions.6 For example, the government has

incentives to change taxes or regulations ex-post with the knowledge that investors cannot easily

withdraw.7 Therefore, investors can delay or forego investment, especially if they are large and

irreversible.

Idiosyncrasies related to specific sectors could influence returns to capital in such sectors thereby

affecting investment. The electricity sector is one example of a sector that is expected to require

large investments in the future, particularly in the context of climate change mitigation, and

therefore presents a useful case to investigate. Traditionally, due to network effects and

economies of scale that create high barriers to entry, the electricity sector had remained a natural

monopoly. In the last few decades, however, the electricity sector has undergone reforms all over

the world, leading in some cases, to unbundling of generation from transmission and distribution

which gives scope for competition and private investment in the sector. Nevertheless, because

outputs from this sector are consumed widely by households and industry, politicians, consumers

and interest groups are sensitive to the level of pricing.8, 9

Therefore, governments have

© 2015 Macmillan Publishers Limited. All rights reserved.

3

incentives to behave opportunistically with the investing company. Expropriation of sunk assets

may be profitable for a government if the direct costs (such as loss of reputation or reduced

investment in the future) are small compared to the short-term benefits of such action (such as

achieving re-election by reducing electricity prices for consumers or by attacking the monopoly),

and if the indirect institutional costs (such as disregard of the judiciary or not following the

proper administrative procedures) are not too large.9 This discourages investors by creating

additional risks. For example, using a sample of thirty-four independent power projects in

thirteen countries, Woodhouse 10

showed that regulatory credibility in host countries is

important for risk-averse investors because of the fear that unpredictable changes in regulations

will lead to expropriation of fixed assets. Note that investment patterns in other sectors may be

quite different than for the electricity sector. For example, at the geographical scale used in most

IAMs, investments in power production are likely to be domestic; that may not be the case in the

transportation sector where fuels and vehicles may be imported rather than produced

domestically. Similarly, investments in some sectors may primarily be self-financed by firms

rather than through commercial or development institutions.

Regulatory and policy uncertainty could affect investment in particular technologies. Currently

non-commercial and politically challenged technologies are subject to regulatory challenges (e.g.

safety, proliferation and environmental regulations for nuclear power plants and uncertainty

regarding safety and permanence of CO2 storage for CCS) that could add to risks through

construction delays and interruption or foreclosure of future operations.11

Likewise, scholars

have argued that volatility and uncertainty in carbon price will increase risks and delay

investments in low-carbon technologies.12-14

Newer technologies face a special investment

challenge – because investors are unaware about the performance of new technologies, they will

expect higher rates of return.15

Technologies whose cost structures are fuel-intensive face the

increased risk of exposure to market uncertainties.16

Technologies in the electricity sector face an

additional risk as wholesale electricity prices are volatile due to the homogenous nature of

electricity, its lack of storability, inelastic demand and the steepness of the supply curve as

electricity production nears system capacity.17, 18

Likewise, uncertainty in the price of

commodities and other inputs adds to investment risks. Further, increased penetration of

intermittent technologies such as wind may affect investment in other technologies. For example,

in a market with high penetration of wind which is typically characterized by long periods of low

© 2015 Macmillan Publishers Limited. All rights reserved.

4

prices and short periods of high wholesale prices, investments in other low carbon technologies

such as nuclear will be adversely affected because of its high capital costs and relative

inflexibility.19

Other factors affecting investment at the technology level include unplanned plant

closure, for example, due to unavailability of resources, plant damage or component failure, risk

of a fall in volume of electricity produced due to lack of wind or sunshine, etc. Such factors

affect investments in technologies differently and may lead to a re-ordering of the relative

attractiveness of the various investment options.

Finally, factors at the level of the firm such as ownership structure and size also affect

investment.20

For a public utility, money can be borrowed at relatively low rates because the risk

of default is low. On the other hand, the cost of money would be much higher for a private utility

which is exposed to the uncertainties of the market. This is closely tied with the type of financing

used by the firm. Corporate financing uses corporate credit and general assets of a corporation,

typically a utility, as the basis for credit and collateral. This is less risky compared to project

financing (typically used by independent power producers) in which lenders base credit

appraisals on the estimated cash flows from the facility rather than on the assets or credit of the

corporation.21

Apart from the above factors, several others at the level of the individual such as

information asymmetry between lenders and borrowers and principal-agent problems could

affect investment, especially in the demand-side of the energy sector.22, 23

In this paper, we focus

only on the supply side in the electricity generation sector; a detailed examination of factors in

the demand-side is beyond our scope.

Due to the factors reviewed above, investments may not take place at the socially optimal level.

However, under certain circumstances, investment risks can be mitigated and investment

encouraged. In the following subsection, we consider the case of China, in which investment in

energy is low-risk due to a combination of factors including favorable policy environment and

state-capitalism.

1.2 Special case: Investment in China

Among developing economies, China currently accounts for the largest share of investment

across all major technologies in the electricity sector. For example, in the year 2013, Chinese

investment in renewable energy was the highest, more than even the whole of Europe.24

China

accounts for more than a third of all proposed coal plants and more than a third of all proposed

© 2015 Macmillan Publishers Limited. All rights reserved.

5

nuclear power plants worldwide.25

From the perspective of an investor, investing in the Chinese

electricity sector is relatively low-risk because Chinese electricity demand will continue to grow

and any investment in the electricity sector will provide attractive returns. In addition, China’s

12th Five Year Plan lays emphasis on renewable energy and energy efficiency. This gives clear

signal that investment in these areas will be encouraged.26

Also, policies such subsidies, feed-in-

tariffs and income tax incentives encourage investment.27, 28

Most importantly, China’s system of

“state capitalism” that tries to juxtapose the powers of the state with the powers of capitalism,

allows for a different character of large-scale energy investment that bolsters capital-intensive

technologies and projects with higher market risks. First, the Chinese energy sector is dominated

by state-owned enterprises that are often able to manage risks by shifting them to the

government. Second, financing from Chinese “policy banks” such as the Chinese Development

Bank that finance the construction of new power plants including emerging technologies such as

solar through extremely low interest rates reduces financial risks considerably. In addition, state

support usually limits delays associated with acquiring rights of way or essential permits. Note,

however, that such advantages may not be unique to China, and they often arise when state-

backed firms raise debt; for example, Mexico’s Pemex.27

China is an interesting case because of

the large size of the market in addition to the above characteristics.

The factors reviewed here create nonuniformities in investment risks across regions, sectors and

technologies. Such nonuniformities will have important implications for the large-scale

investments in the energy system required to address the climate change problem because

investors could respond to them by expecting higher returns to invest in a risky project; delaying

or forgoing the investment or investing in existing, familiar technologies.

2 The cost of capital

In this section, we explain the different terms and concepts surrounding the cost of capital.

Typically, firms use a combination of debt and equity to finance their businesses. The cost of

debt is “the amount paid to the holders of debt securities for the use of their money”. 21

The

amount paid, which is the lending interest rate is set by banks. Since the interest is tax-

deductible, the cost of debt is usually calculated on an after-tax basis. The cost of equity refers to

the “the earnings expected by an investor when purchasing equity shares in a company”. 21

Note

that equity is a riskier form of financing compared to debt and so the cost of equity is greater

© 2015 Macmillan Publishers Limited. All rights reserved.

6

than the cost of debt. The expected return on any investment can be written as the sum of the

risk-free rate and a premium to compensate for the risk (the risk-free rate represents the time

value of money and compensates investors for placing money in any investment over a period of

time). The equity risk premium, thus refers to the premium added to the risk-free rate to estimate

the cost of equity. The overall cost of capital is derived from a weighted average of all capital

sources, widely known as the weighted average cost of capital (WACC). The WACC is used as

the discount rate, which reflects the fact that the value of a cash flow depends on the time in

which the flow occurs.

Finally, the Fixed Charge rate (FCR) represents “the before-tax revenue that a profit-maximizing

firm would require annually to cover its cost and carrying charges of an investment and to

achieve its desired after-tax return. Carrying charges include return on debt and equity, income

and property tax, book depreciation, and insurance.” The FCR is a function of the discount rate

and the lifetime of the capital investment and is given by the following expression: 𝐹𝐶𝑅 =

𝐷𝑖𝑠𝑐𝑜𝑢𝑛𝑡 𝑟𝑎𝑡𝑒

1−(1

1+𝐷𝑖𝑠𝑐𝑜𝑢𝑛𝑡 𝑟𝑎𝑡𝑒)𝑙𝑖𝑓𝑒𝑡𝑖𝑚𝑒

× 1−(𝑇 ∗ 𝑃𝑉𝑑𝑒𝑝𝑟𝑒𝑐𝑖𝑎𝑡𝑖𝑜𝑛)

1−𝑇, where T is the marginal income tax rate,

PVDepreciation is the present value of depreciation and lifetime refers to the lifetime of the capital

investment.21

3 Implications of the logit technology choice formulation

As explained in the Methods section, investment in GCAM depends on relative costs and the

distribution among technologies determined using a logit-choice formulation.29-31

The logit

technology choice representation assigns some market share to expensive technologies, which

allows the model to avoid an unrealistic “winner take all” responses based on the notion that

choices are based on other factors besides observed prices or that single observed prices do not

represent the full variation in prices across applications. The logit method is well documented in

the literature (see for example, 29-31

). In this paper, we investigate the impacts of nonuniform

investment risks across technologies and regions on costs and geography of climate change

mitigation. Specific to the present analysis, the logit technology choice formulation has the

following implication in the baseline as well as climate policy scenarios. Under nonuniform

investment risks, higher investment risks for low-carbon technologies (which are assigned higher

costs of capital) raise the costs of electricity generation from them. In spite of higher generation

© 2015 Macmillan Publishers Limited. All rights reserved.

7

costs, low-carbon technologies get deployed, raising electricity prices. This in turn reduces

demand for electricity, reducing overall investment in the electricity generation sector (Figure 2

A to D in the Main Text).

Note that that nonuniform investment risk is one factor among several others that affect

investment. As with other formulations of technology choice (e.g., linear optimization or

production function approaches), the logit representation assumes that investments in

technologies depend on relative costs. The logit approach does also, in theory, account for non-

modeled factors in the parameters of the logit function. However, even if these factors can

ostensibly be captured in the logit parameters, this representation does not provide a clear

structural representation of key social, behavioral and institutional factors that can affect future

investment (see for example, Iyer, Hultman 32

and Hultman, Malone 33

for a review of such

factors). Note that this limitation is equally applicable to all choice methods that are

fundamentally focused on explicit market costs. In this sense, the logit is no more limited or less

appropriate than these other methods. For example, in the case of nuclear energy, there are a

number of challenges to deployment apart from unfavorable economics such as public

perceptions, waste management and proliferation which affect investments in developed as well

as developing countries (see for example, Iyer, Hultman 34

for a review of challenges to

expansion of nuclear energy). One attempt to capture such “non-economic” factors is the study

by Iyer, Hultman 32

—a study that represents the diffusion of low-carbon technologies in a

nuanced manner by specifying a range of growth rates for low-carbon technology deployments

under the assumption that investments in low-carbon technologies may be constrained due to

several factors other than relative costs. Those are important issues, but the focus of the current

analysis is different—it aims to demonstrate improved modeling of one factor, namely

investment risks in IAMs.

4 Sensitivity analyses

Our analysis leads to two key findings. First, under nonuniform investment risks, global costs of

achieving a climate target are higher compared with a world with uniform investment risks

(Figure 3 in Main Text and Supplementary Figure 4). Second, most of the increased costs are

borne by regions with superior institutions (Figure 4 in Main Text and Supplementary Figures

8,10,11). In order to validate the consistency of our findings, we conduct a sensitivity analysis on

© 2015 Macmillan Publishers Limited. All rights reserved.

8

our assumptions. For this purpose, we focus on the following variables: i.) the global emissions

target ii.) assumptions about fixed charge rates (FCRs for low-risk technologies and risk

premium for high-risk technologies) and iii.) technologies considered high-risk. Finally, we also

consider a scenario in which investment risks are higher for fossil-fuel technologies compared to

low-carbon technologies. For the sake of presentation of results of the sensitivity analyses, we

focus on two metrics that summarize our key findings, namely, changes in global carbon prices

and regional mitigation costs under variation of investment risks across technologies and regions

relative to uniform investment risks scenarios.

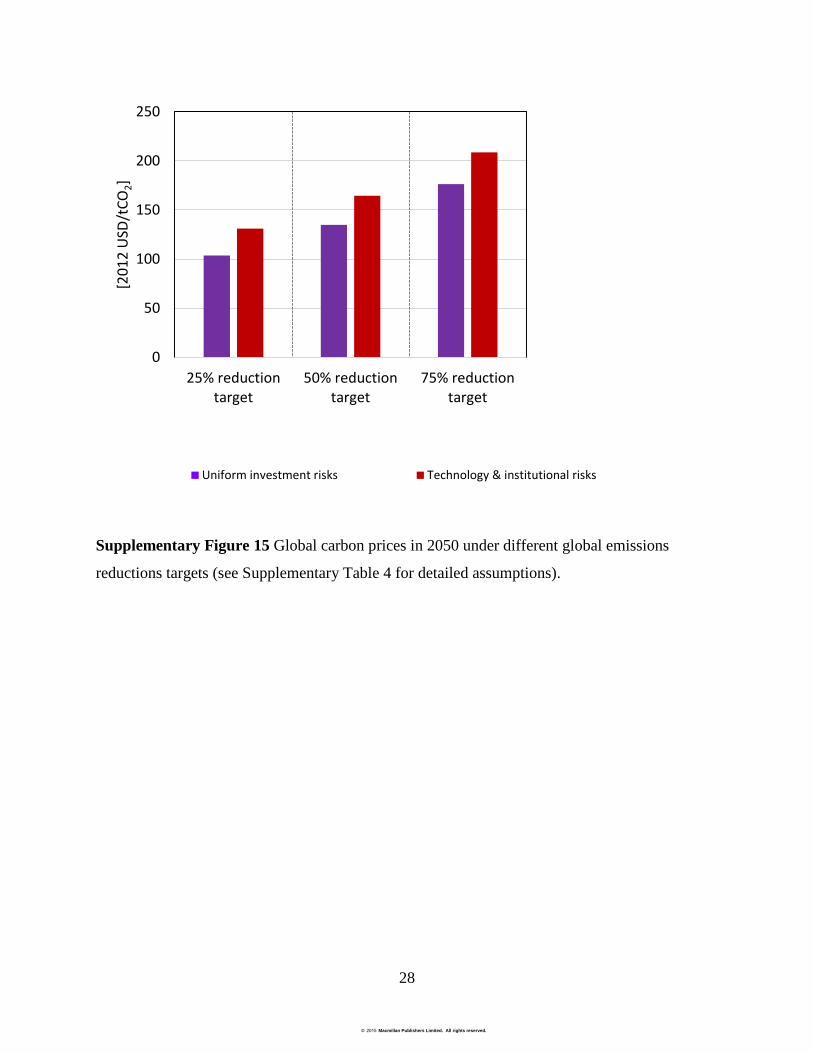

4.1 Sensitivity of results to global emissions target

In the Main Text of the article, we specified a 50% reduction in 2050 global CO2 emissions from

fossil fuels and industry relative to 2005 levels. For the purpose of sensitivity analysis, we

specify 25% and 75% reductions. Global carbon prices and mitigation costs under the 25% and

75% targets are lower and higher respectively, compared to the 50% target (Supplementary

Figures 15 and 16). Nevertheless, under all global emissions targets, global carbon prices are

higher under nonuniform investment risks and increases in regional mitigation costs are higher

for regions with superior institutions.

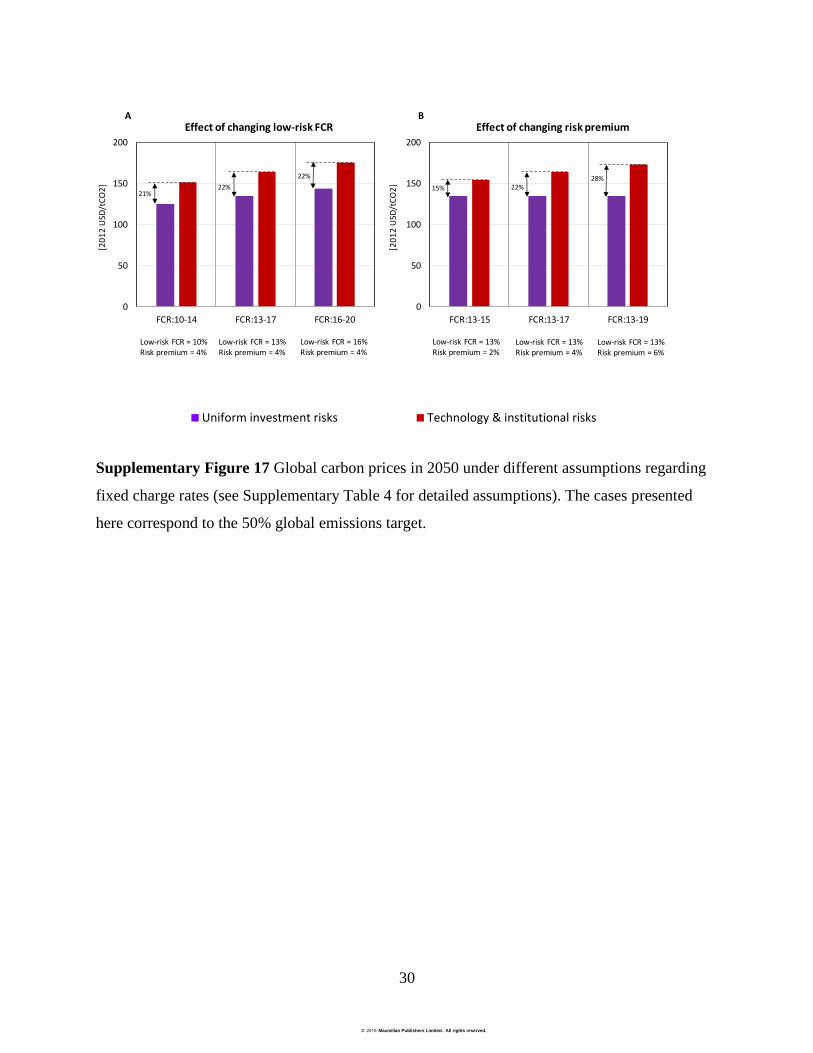

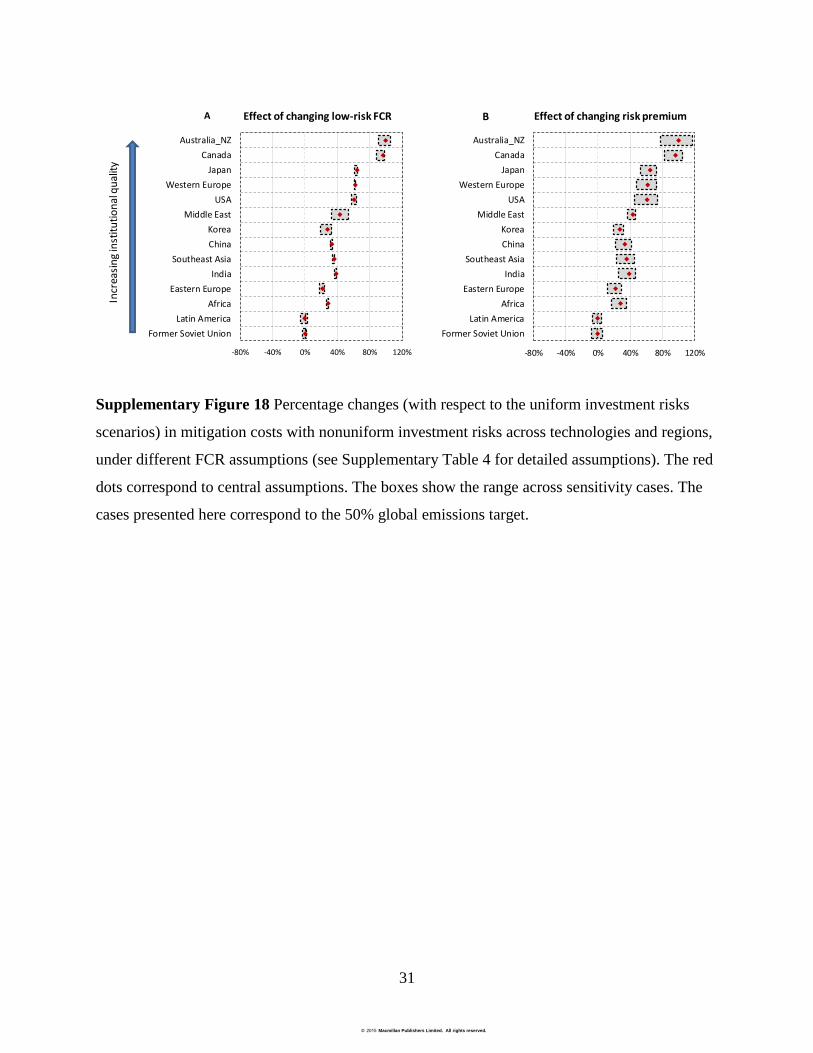

4.2 Sensitivity of results to FCR assumptions

The findings of this study hinge on assumptions about technology costs and fixed charge rates

(FCRs). Previous studies have evaluated sensitivity to technology cost assumptions in the

GCAM model.35, 36

We focus this sensitivity analysis on assumptions regarding FCRs. The main

analysis of this study assumes an FCR of 13% for low-risk technologies and 17% for high-risk

technologies based on a survey of FCRs used for financial analyses in the US (Supplementary

Table 1). Uncertainties in the FCRs obtained for USA can arise due to a number of reasons

including assumptions about equity/debt shares, discount rates, lifespan of investments, tax rates

and depreciation schedules. For the sake of sensitivity analyses, we change the FCR assumptions

for low-risk technologies and the risk premium for high-risk technologies (Supplementary Table

4). Our results indicate that the changes in global and regional mitigation costs under

nonuniform investment risks relative to the uniform investment risks scenarios are more sensitive

to assumptions about the risk premium compared to assumptions about the FCR for low-risk

technologies (Supplementary Figures 17 and 18). For example, the spread in changes in 2050

© 2015 Macmillan Publishers Limited. All rights reserved.

9

global carbon prices under variation of investment risks with technologies and regions relative to

the uniform investment risks scenarios when the FCR for low-risk technologies are varied

between 10% and 16% is small (changes in carbon prices across sensitivity cases are 21%-22). In

contrast, when the risk premium for high-risk technologies is varied between 2% and 6%, the

spread in changes in carbon prices is greater (changes in carbon prices across sensitivity cases

are 15%-28%). This is because, investments in GCAM depend on relative economics of

technologies. Hence, the risk premium for high-risk technologies has a greater influence on the

competitive advantage of such technologies relative to low-risk technologies compared to the

FCR for low-risk technologies. Consequently, the risk premium has a greater influence on the

deployments of low-carbon technologies (which are high-risk) and hence on marginal abatement

costs and carbon prices. Nevertheless, in spite of changes in the magnitudes of the impacts on

carbon prices and regional mitigation costs, the two key findings of our analysis are consistent

across various assumptions about FCRs.

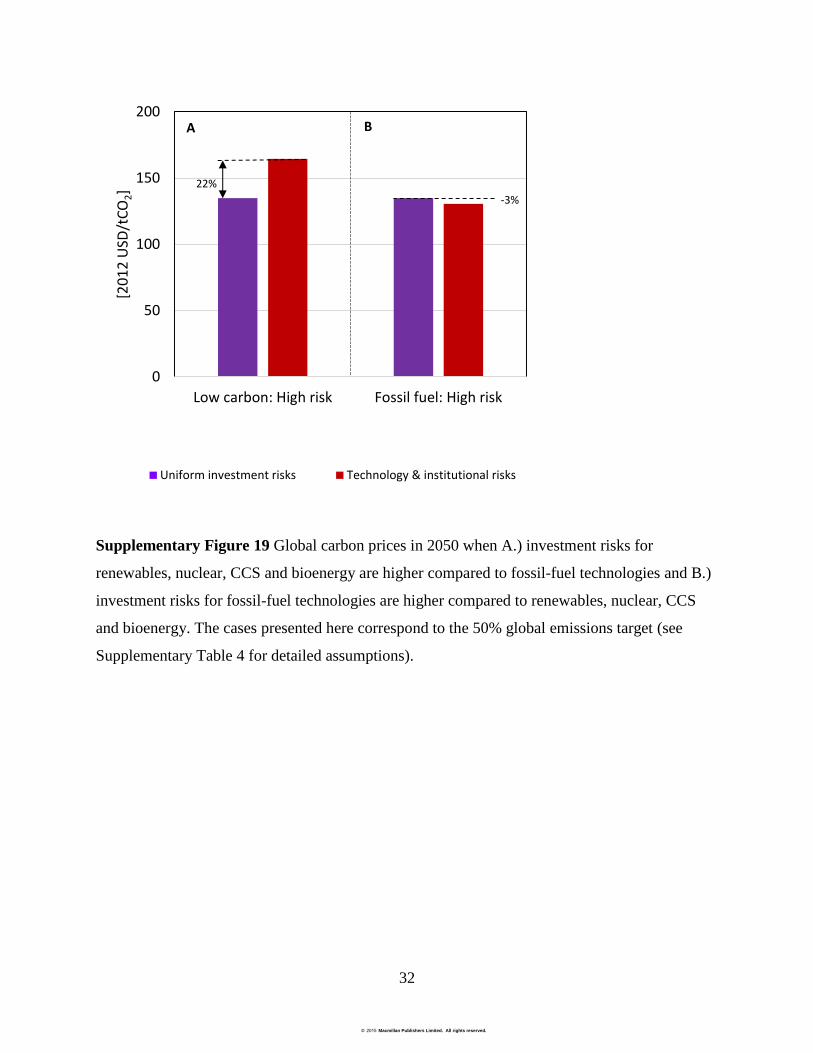

4.3 High investment risks for fossil-fuel technologies

In the investment risk scenarios considered in this study, we specified higher investment risks for

low-carbon technologies and lower investment risks for fossil-fuel technologies. Here, we

consider a scenario in which investment risks are higher for fossil-fuel technologies compared to

low-carbon technologies. Such a scenario is conceivable in a carbon-constrained world in which

a sustained and increasing price on carbon could make investments in fossil-fuel rather than low-

carbon technologies more risky. Governments might adopt policies that favor low-carbon

technologies—as many governments have done already—precisely with the ambition of making

investors view these technologies as less risky. The effect of higher investment risks for fossil-

fuel technologies is to reduce carbon prices relative to the uniform investment risks scenario

(Supplementary Figure 19). This is because, higher investment risks for fossil-fuel technologies

increase the costs of electricity generation from such technologies and improve the competitive

advantage of low-carbon technologies, thus decreasing marginal abatement costs. The effect is,

however, small compared to the increase in carbon prices due to higher investment risks for low-

carbon technologies. For example, the global carbon price in 2050 under higher investment risks

for low-carbon technologies along with variation across regions to achieve a 50% emissions

target is 22% higher compared with the uniform investment risks scenario. In contrast, the

carbon price under higher investment risks for fossil-fuel technologies along with variation

© 2015 Macmillan Publishers Limited. All rights reserved.

10

across regions is lower by only 3%. This is because, fossil-fuel technologies are less capital-

intensive compared to low-carbon technologies. Hence, a risk premium on fossil-fuel

technologies will have a smaller impact on marginal abatement cost curves compared with the

same risk premium on low-carbon technologies, even if the directions of the impacts will be

opposite.

© 2015 Macmillan Publishers Limited. All rights reserved.

11

Supplementary Figures

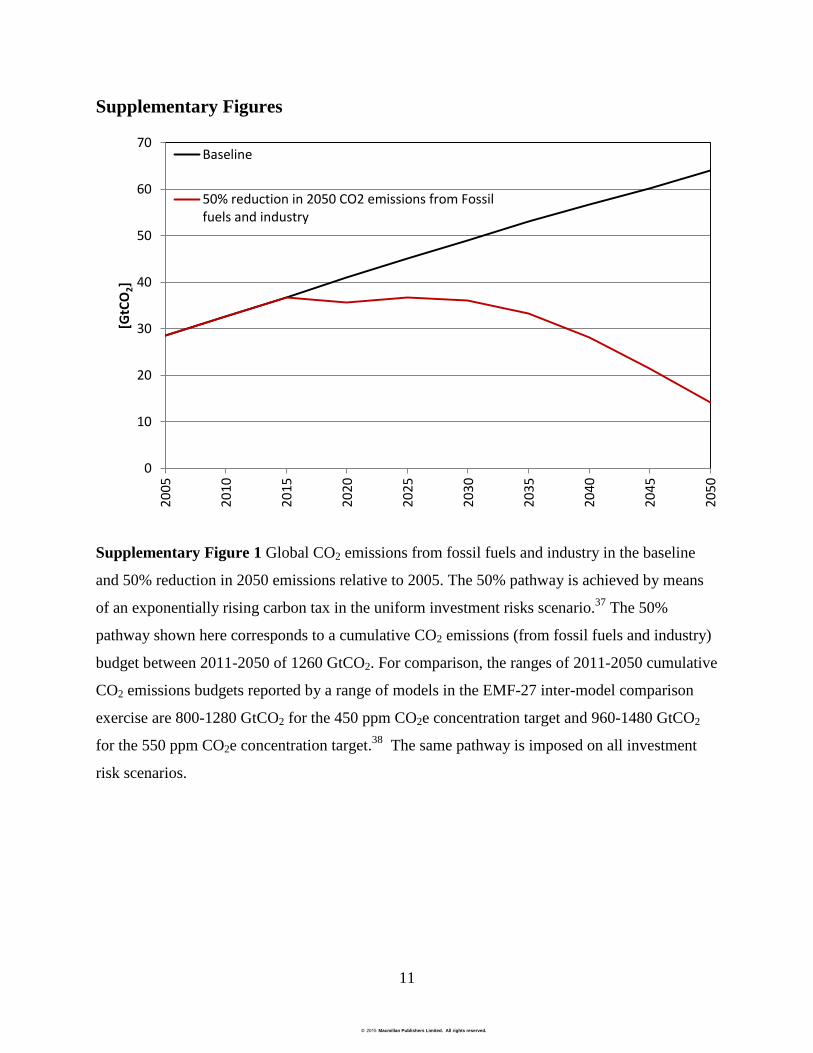

Supplementary Figure 1 Global CO2 emissions from fossil fuels and industry in the baseline

and 50% reduction in 2050 emissions relative to 2005. The 50% pathway is achieved by means

of an exponentially rising carbon tax in the uniform investment risks scenario.37

The 50%

pathway shown here corresponds to a cumulative CO2 emissions (from fossil fuels and industry)

budget between 2011-2050 of 1260 GtCO2. For comparison, the ranges of 2011-2050 cumulative

CO2 emissions budgets reported by a range of models in the EMF-27 inter-model comparison

exercise are 800-1280 GtCO2 for the 450 ppm CO2e concentration target and 960-1480 GtCO2

for the 550 ppm CO2e concentration target.38

The same pathway is imposed on all investment

risk scenarios.

0

10

20

30

40

50

60

7020

05

2010

2015

2020

2025

2030

2035

2040

2045

2050

[GtC

O2]

Baseline

50% reduction in 2050 CO2 emissions from Fossilfuels and industry

© 2015 Macmillan Publishers Limited. All rights reserved.

12

INVESMENT IN ELECTRICITY GENERATION BY TECHNOLOGY IN THE BASELINE CASES

(billion 2012 USD per year)

CHANGES WITH RESPECT TO UNIFORM INVESTMENT RISKS SCENARIO

UNIFORM INVESTMENT

RISKS

TECHNOLOGY

INVESTMENT RISKS

INSTITUTIONAL

INVESTMENT RISKS

TECHNOLOGY &

INSTITUTIONAL RISKS

IND

IA

CA

NA

DA

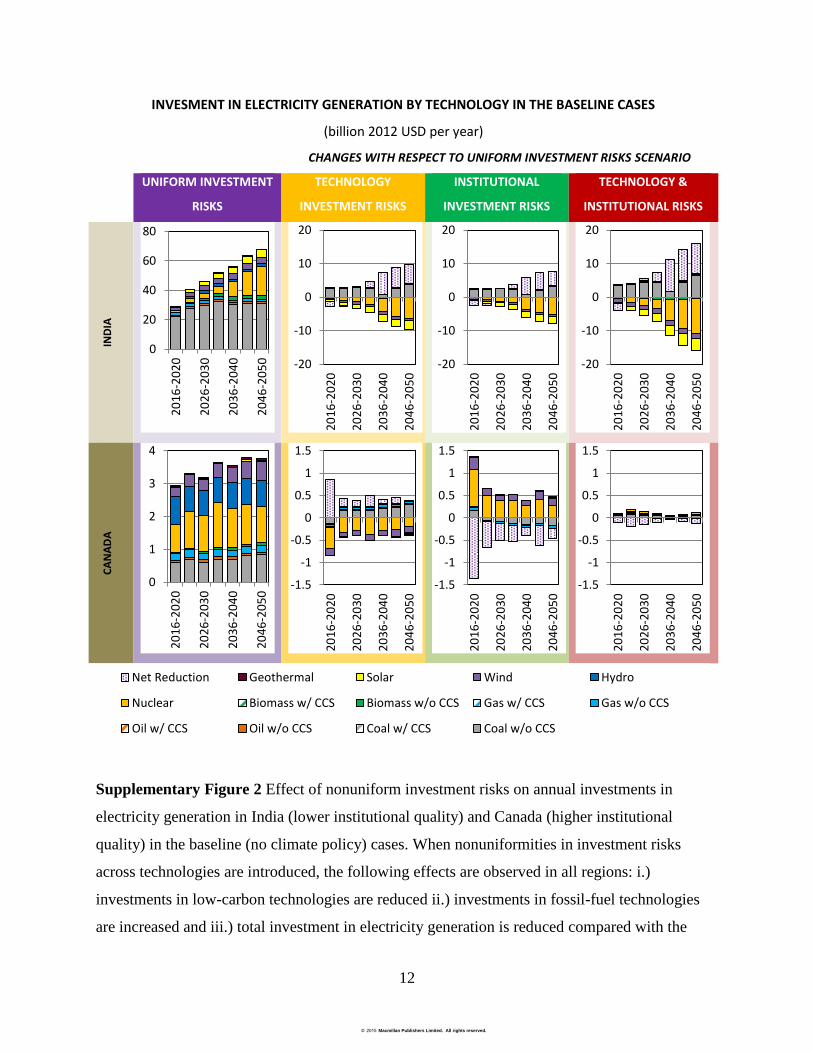

Supplementary Figure 2 Effect of nonuniform investment risks on annual investments in

electricity generation in India (lower institutional quality) and Canada (higher institutional

quality) in the baseline (no climate policy) cases. When nonuniformities in investment risks

across technologies are introduced, the following effects are observed in all regions: i.)

investments in low-carbon technologies are reduced ii.) investments in fossil-fuel technologies

are increased and iii.) total investment in electricity generation is reduced compared with the

0

20

40

60

80

2016

-202

0

2026

-203

0

2036

-204

0

2046

-205

0 -20

-10

0

10

20

2016

-202

0

2026

-203

0

2036

-204

0

2046

-205

0

-20

-10

0

10

20

2016

-202

0

2026

-203

0

2036

-204

0

2046

-205

0

-20

-10

0

10

20

2016

-202

0

2026

-203

0

2036

-204

0

2046

-205

0

0

1

2

3

4

2016

-202

0

2026

-203

0

2036

-204

0

2046

-205

0

-1.5

-1

-0.5

0

0.5

1

1.5

2016

-202

0

2026

-203

0

2036

-204

0

2046

-205

0

-1.5

-1

-0.5

0

0.5

1

1.5

2016

-202

0

2026

-203

0

2036

-204

0

2046

-205

0

-1.5

-1

-0.5

0

0.5

1

1.5

2016

-202

0

2026

-203

0

2036

-204

0

2046

-205

0Net Reduction Geothermal Solar Wind Hydro

Nuclear Biomass w/ CCS Biomass w/o CCS Gas w/ CCS Gas w/o CCS

Oil w/ CCS Oil w/o CCS Coal w/ CCS Coal w/o CCS

© 2015 Macmillan Publishers Limited. All rights reserved.

13

uniform investment risks scenario (see main text for details). When nonuniformities in

institutional qualities are introduced, the above effects are seen in regions with inferior

institutions such as India, where investing in low-carbon technologies is more risky. On the other

hand, in regions with superior institutions such as Canada, where investment risks for investing

in low-carbon technologies may be lower than fossil-fuel technologies, investments in low-

carbon technologies increase and those in fossil-fuel technologies decrease, with a net increase in

investments in electricity generation. The combined effect of nonuniformities across

technologies and regions is to reduce investments in India and increase investments in Canada.

The combined effect on the global level, however, is a decrease in investments in low-carbon

technologies because most of the investments occur in developing regions such as India and

China which have relatively inferior institutional qualities (see Figure 2D in the main text).

© 2015 Macmillan Publishers Limited. All rights reserved.

14

Supplementary Figure 3 CO2 emissions in the baseline (no-climate policy) scenarios. With

nonuniform investment risks across technologies, baseline emissions are higher compared with

the uniform investment risks scenario in all regions. This is because, in this scenario,

deployments of low-carbon technologies are lower and those of fossil-fuel technologies are

higher. Note that although overall electricity generation in this scenario is lower (due to higher

electricity prices), the effect of the change in fuel mix is greater. When nonuniformities across

regions are introduced, baseline emissions in regions with lower institutional qualities, for

0

20

40

60

80

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

[GtC

O2]

Global CO2 emissions

0

2

4

6

8

10

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

[GtC

O2]

India

0

0.2

0.4

0.6

0.8

1

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

[GtC

O2]

Canada

Uniform investment risks Institutional investment risks

Technology investment risks Technology & institutional risks

© 2015 Macmillan Publishers Limited. All rights reserved.

15

example, India are higher due to the effects described above. On the other hand, baseline

emissions in regions with higher institutional qualities, for example, Canada, are lower. This is

because, in these regions, deployments of low-carbon technologies increase and those of fossil-

fuel technologies decrease (see Supplementary Figure 2). The combined effect of

nonuniformities across technologies and regions is to increase baseline emissions in regions with

inferior institutions and decrease them in regions with superior institutions. On the global level,

the combined effect is an increase in baseline emissions as most of the emissions come from

developing regions such as India and China with lower institutional qualities.

© 2015 Macmillan Publishers Limited. All rights reserved.

16

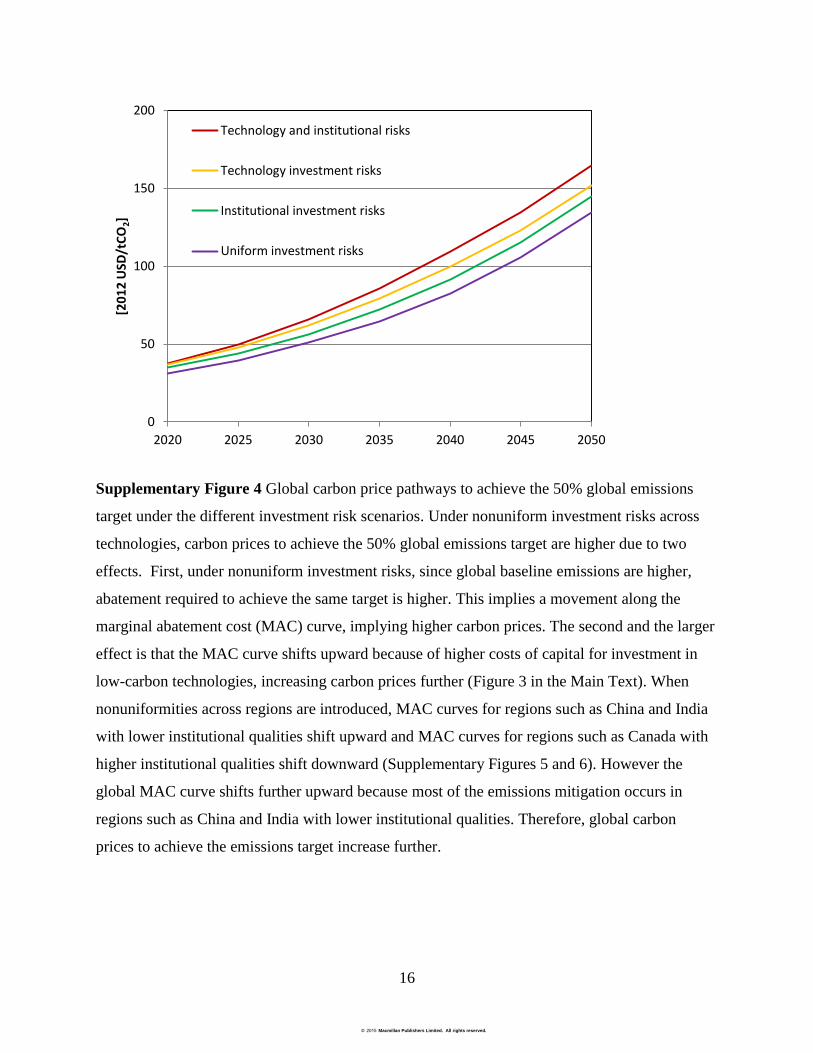

Supplementary Figure 4 Global carbon price pathways to achieve the 50% global emissions

target under the different investment risk scenarios. Under nonuniform investment risks across

technologies, carbon prices to achieve the 50% global emissions target are higher due to two

effects. First, under nonuniform investment risks, since global baseline emissions are higher,

abatement required to achieve the same target is higher. This implies a movement along the

marginal abatement cost (MAC) curve, implying higher carbon prices. The second and the larger

effect is that the MAC curve shifts upward because of higher costs of capital for investment in

low-carbon technologies, increasing carbon prices further (Figure 3 in the Main Text). When

nonuniformities across regions are introduced, MAC curves for regions such as China and India

with lower institutional qualities shift upward and MAC curves for regions such as Canada with

higher institutional qualities shift downward (Supplementary Figures 5 and 6). However the

global MAC curve shifts further upward because most of the emissions mitigation occurs in

regions such as China and India with lower institutional qualities. Therefore, global carbon

prices to achieve the emissions target increase further.

0

50

100

150

200

2020 2025 2030 2035 2040 2045 2050

[20

12

USD

/tC

O2]

Technology and institutional risks

Technology investment risks

Institutional investment risks

Uniform investment risks

© 2015 Macmillan Publishers Limited. All rights reserved.

17

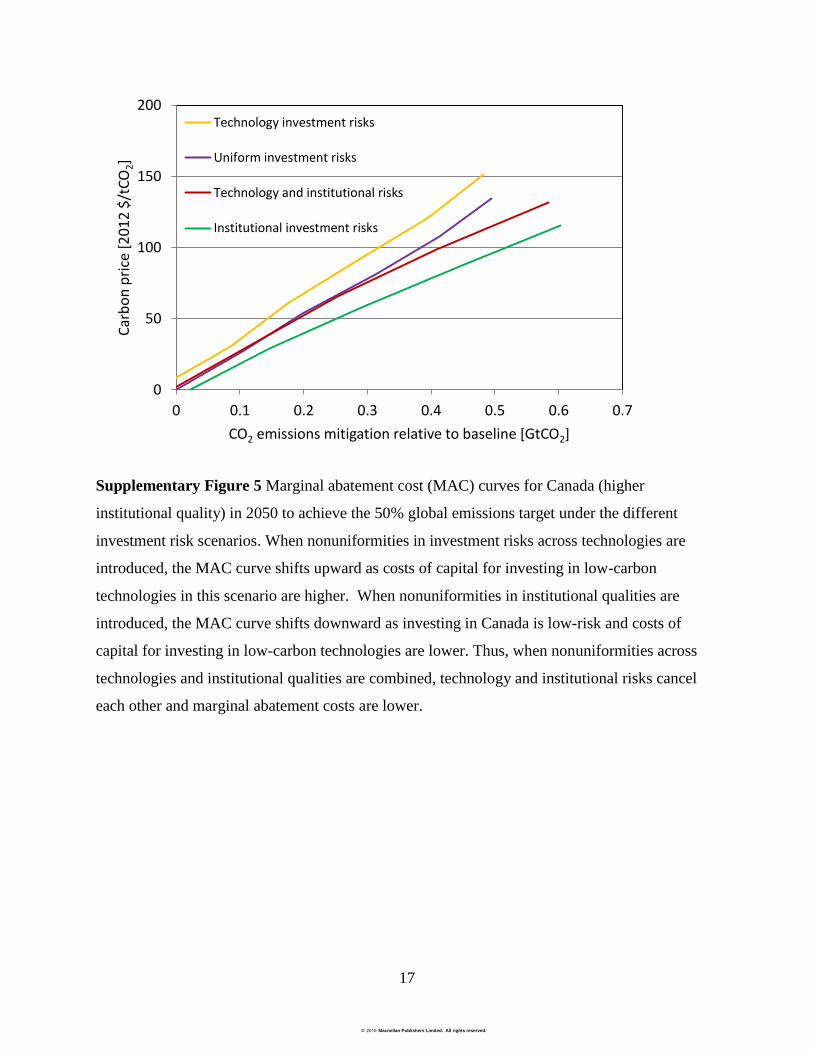

Supplementary Figure 5 Marginal abatement cost (MAC) curves for Canada (higher

institutional quality) in 2050 to achieve the 50% global emissions target under the different

investment risk scenarios. When nonuniformities in investment risks across technologies are

introduced, the MAC curve shifts upward as costs of capital for investing in low-carbon

technologies in this scenario are higher. When nonuniformities in institutional qualities are

introduced, the MAC curve shifts downward as investing in Canada is low-risk and costs of

capital for investing in low-carbon technologies are lower. Thus, when nonuniformities across

technologies and institutional qualities are combined, technology and institutional risks cancel

each other and marginal abatement costs are lower.

0

50

100

150

200

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7

Carb

on p

rice

[201

2 $/

tCO

2]

CO2 emissions mitigation relative to baseline [GtCO2]

Technology investment risks

Uniform investment risks

Technology and institutional risks

Institutional investment risks

© 2015 Macmillan Publishers Limited. All rights reserved.

18

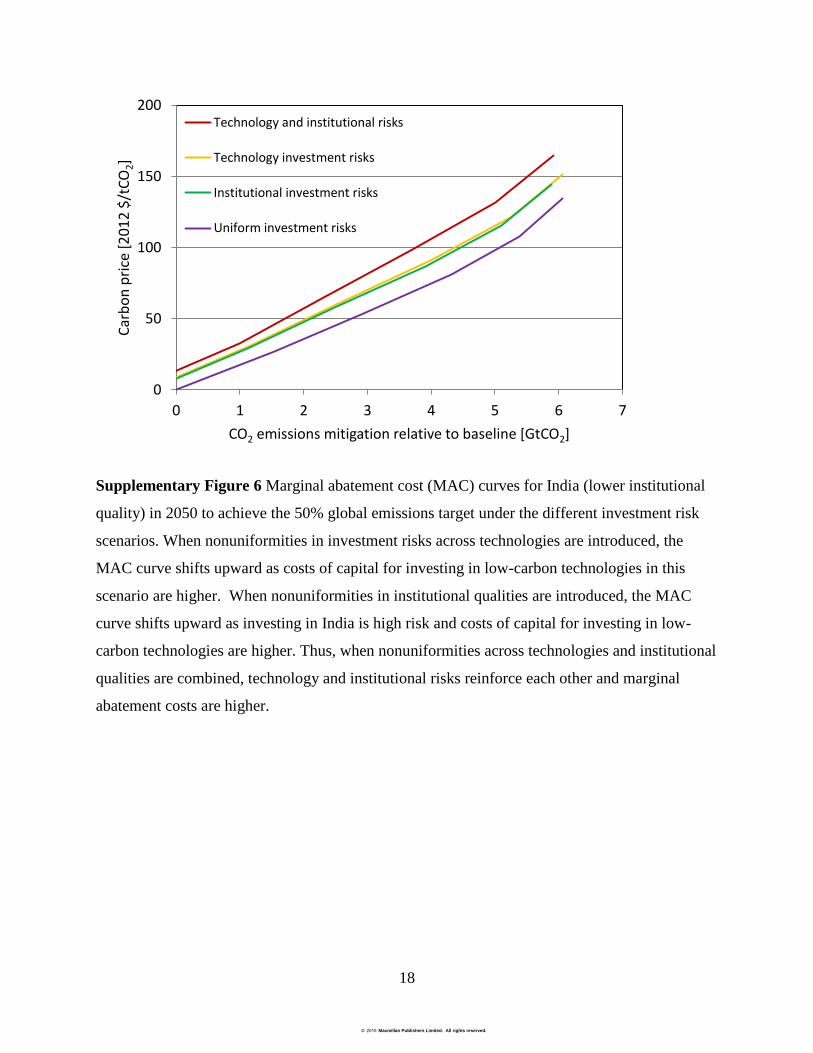

Supplementary Figure 6 Marginal abatement cost (MAC) curves for India (lower institutional

quality) in 2050 to achieve the 50% global emissions target under the different investment risk

scenarios. When nonuniformities in investment risks across technologies are introduced, the

MAC curve shifts upward as costs of capital for investing in low-carbon technologies in this

scenario are higher. When nonuniformities in institutional qualities are introduced, the MAC

curve shifts upward as investing in India is high risk and costs of capital for investing in low-

carbon technologies are higher. Thus, when nonuniformities across technologies and institutional

qualities are combined, technology and institutional risks reinforce each other and marginal

abatement costs are higher.

0

50

100

150

200

0 1 2 3 4 5 6 7

Carb

on p

rice

[201

2 $/

tCO

2]

CO2 emissions mitigation relative to baseline [GtCO2]

Technology and institutional risks

Technology investment risks

Institutional investment risks

Uniform investment risks

© 2015 Macmillan Publishers Limited. All rights reserved.

19

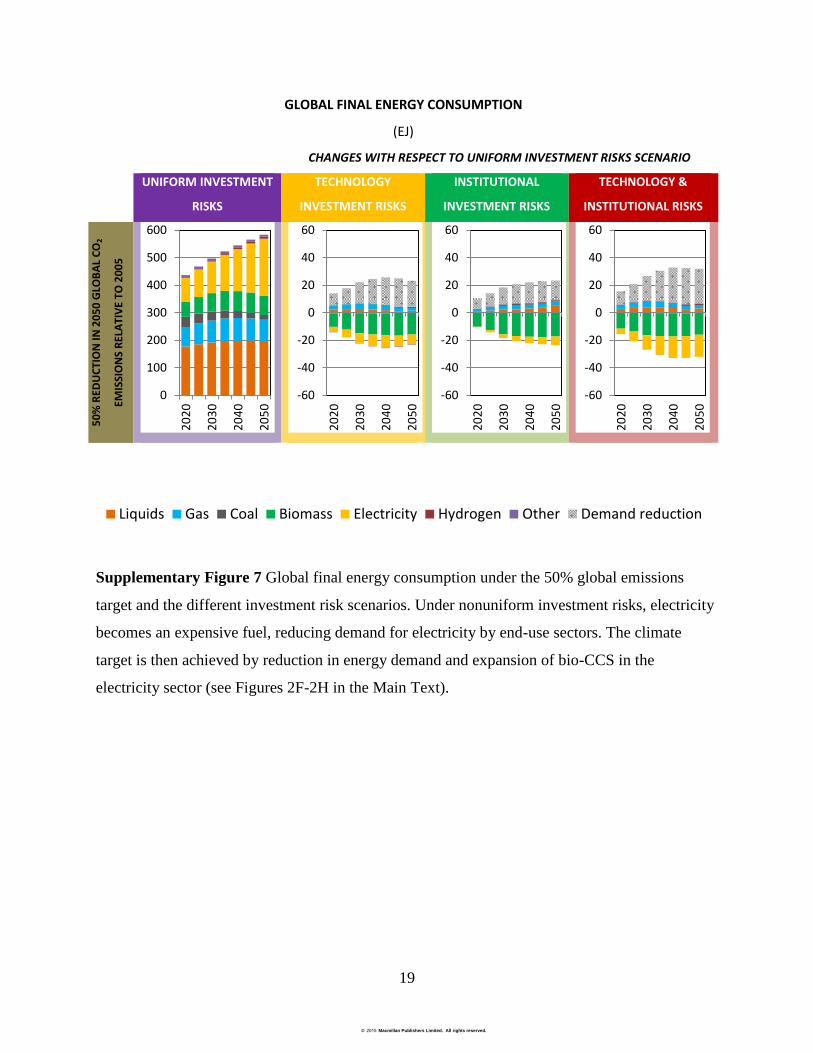

GLOBAL FINAL ENERGY CONSUMPTION

(EJ)

CHANGES WITH RESPECT TO UNIFORM INVESTMENT RISKS SCENARIO

UNIFORM INVESTMENT

RISKS

TECHNOLOGY

INVESTMENT RISKS

INSTITUTIONAL

INVESTMENT RISKS

TECHNOLOGY &

INSTITUTIONAL RISKS

50

% R

EDU

CTI

ON

IN 2

05

0 G

LOB

AL

CO

2

EMIS

SIO

NS

REL

ATI

VE

TO 2

00

5

Supplementary Figure 7 Global final energy consumption under the 50% global emissions

target and the different investment risk scenarios. Under nonuniform investment risks, electricity

becomes an expensive fuel, reducing demand for electricity by end-use sectors. The climate

target is then achieved by reduction in energy demand and expansion of bio-CCS in the

electricity sector (see Figures 2F-2H in the Main Text).

0

100

200

300

400

500

600

2020

2030

2040

2050

-60

-40

-20

0

20

40

60

2020

2030

2040

2050

-60

-40

-20

0

20

40

60

2020

2030

2040

2050

-60

-40

-20

0

20

40

60

2020

2030

2040

2050

Liquids Gas Coal Biomass Electricity Hydrogen Other Demand reduction

© 2015 Macmillan Publishers Limited. All rights reserved.

20

Supplementary Figure 8 A.) Cumulative net present values of regional investments in

electricity generation (2020-2050) under uniform investment risks and B.) Changes (with respect

to the uniform investment risks scenario) in investments under the different investment risk

scenarios considered in this study. The cases presented here correspond to the 50% global

emissions target. Under uniform investment risks, most of the investments occur in developing

regions such as China. This is because, investment depends on the mitigation potential of

different regions. In the baseline, fossil-fuel based electricity generation in regions such as China

increases significantly due to growing population and income. Consequently, it is cheaper to

invest in emissions reductions in such regions. When nonuniformities in investment risks across

technologies are introduced, investments are reduced in all regions. When nonuniformities across

regions are introduced, investments in regions with inferior institutions are reduced and those in

regions with superior institutions are increased (see Supplementary Figure 2). Note that while the

PERCENTAGE CHANGE WITH RESPECT TO

UNIFORM INVESTMENT RISK SCENARIOUNIFORM INVESTMENT RISKS

0 0.5 1 1.5 2 2.5

Former Soviet UnionLatin America

AfricaEastern Europe

IndiaSoutheast Asia

ChinaKorea

Middle EastUSA

Western EuropeJapan

CanadaAustralia_NZ

NPV of investments in electricity generation (2020-2050) [trillion 2012 USD]

A

-80% -40% 0% 40% 80%

B

Incr

easi

ng in

stitu

tiona

l qua

lity

Uniform investment risks Technology investment risks

Institutional investment risks Technology & institutional risks

© 2015 Macmillan Publishers Limited. All rights reserved.

21

effects of nonuniformities across technologies and institutions reinforce each other in regions

with inferior institutions, they act in opposite directions in regions with superior institutions.

© 2015 Macmillan Publishers Limited. All rights reserved.

22

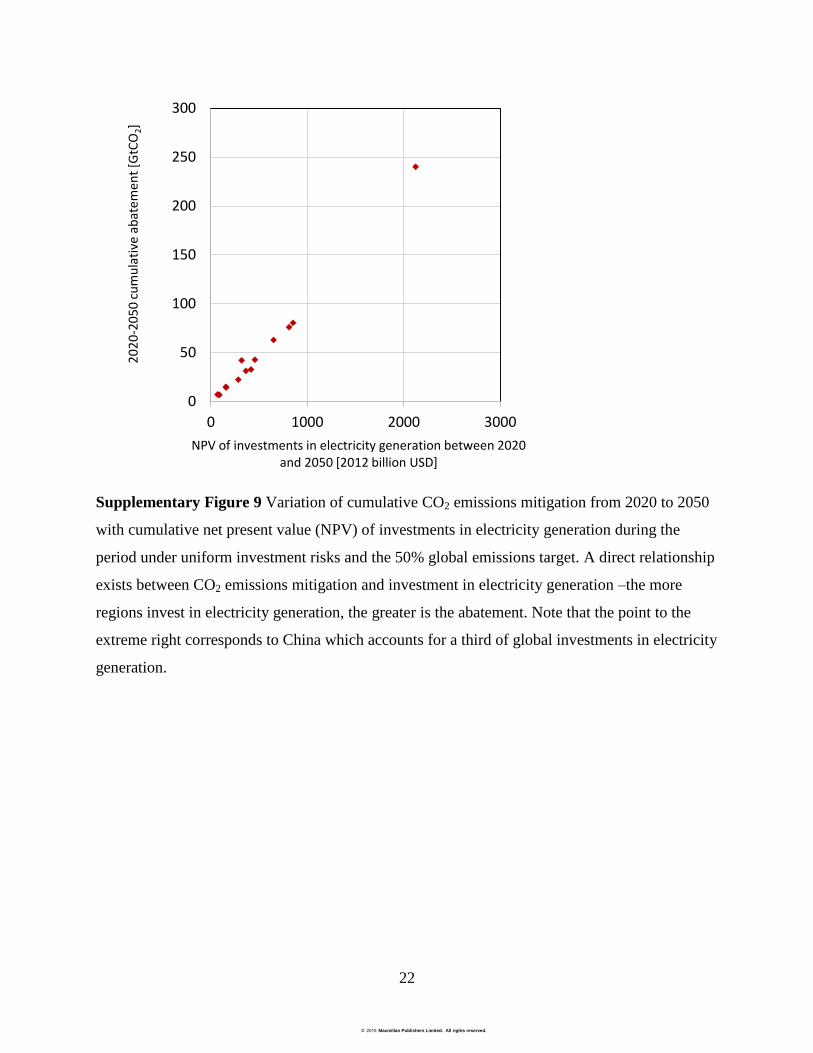

Supplementary Figure 9 Variation of cumulative CO2 emissions mitigation from 2020 to 2050

with cumulative net present value (NPV) of investments in electricity generation during the

period under uniform investment risks and the 50% global emissions target. A direct relationship

exists between CO2 emissions mitigation and investment in electricity generation –the more

regions invest in electricity generation, the greater is the abatement. Note that the point to the

extreme right corresponds to China which accounts for a third of global investments in electricity

generation.

0

50

100

150

200

250

300

0 1000 2000 3000

2020

-205

0 cu

mul

ativ

e ab

atem

ent [

GtCO

2]

NPV of investments in electricity generation between 2020 and 2050 [2012 billion USD]

© 2015 Macmillan Publishers Limited. All rights reserved.

23

Supplementary Figure 10 A.) CO2 emissions mitigation relative to baseline in the uniform

investment risks scenario B.) Changes (with respect to the uniform investment risks scenario) in

CO2 emissions mitigation under the different investment risk scenarios considered in this study.

CO2 emissions mitigation is calculated as cumulative mitigation in CO2 emissions from fossil

fuels and industry relative to the baseline between 2020 and 2050. The cases presented here

correspond to the 50% global emissions target. Under nonuniform investment risks across

technologies and regions, regions with superior institutions mitigate more and regions with

inferior institutions mitigate less compared with the uniform investment risks scenario. This is

because marginal abatement costs in regions with superior institutions are lower and those in

regions with inferior institutions are higher compared with the uniform investment risks scenario

(see Supplementary Figures 5 and 6).

UNIFORM INVESTMENT RISKSPERCENTAGE CHANGE WITH RESPECT TO

UNIFORM INVESTMENT RISK SCENARIOIn

crea

sing

inst

itutio

nal q

ualit

y

0 100 200 300

Former Soviet UnionLatin America

AfricaEastern Europe

IndiaSoutheast Asia

ChinaKorea

Middle EastUSA

Western EuropeJapan

CanadaAustralia_NZ

Cumulative CO2 emissions mitigation (2020-

2050) [GtCO2]

A

-80% -40% 0% 40% 80%

B

Uniform investment risks Technology investment risks

Institutional investment risks Technology & institutional risks

© 2015 Macmillan Publishers Limited. All rights reserved.

24

Supplementary Figure 11 A.) Cumulative net present values of mitigation costs (2020-2050)

under uniform investment risks and B.) Changes (with respect to the uniform investment risks

scenario) in mitigation costs under the different investment risk scenarios considered in this

study. The cases presented here correspond to the 50% global emissions target. Mitigation cost is

calculated as the area under the marginal abatement costs curve. Under nonuniform investment

risks across technologies and regions, increases in mitigation costs relative to the uniform

investment risks scenario in regions with superior institutions are greater as such regions mitigate

more (see Supplementary Figure 10).

UNIFORM INVESTMENT RISKSPERCENTAGE CHANGE WITH RESPECT TO

UNIFORM INVESTMENT RISK SCENARIOIn

crea

sing

inst

itutio

nal q

ualit

y

0 1000 2000 3000 4000

Former Soviet UnionLatin America

AfricaEastern Europe

IndiaSoutheast Asia

ChinaKorea

Middle EastUSA

Western EuropeJapan

CanadaAustralia_NZ

NPV of mitigation costs (2020-2050) [Billion 2012 USD]

A

-80% -40% 0% 40% 80% 120%

B

Uniform investment risks Technology investment risks

Institutional investment risks Technology & institutional risks

© 2015 Macmillan Publishers Limited. All rights reserved.

25

Supplementary Figure 12 Variation of mitigation costs with investments in electricity

generation under uniform investment risks and the 50% global emissions target. Mitigation costs

and investments are calculated as cumulative net present values between 2020 and 2050. A direct

relationship exists between mitigation costs and investment in electricity generation – mitigation

costs are higher for regions that invest more. This observation follows directly from

Supplementary Figure 8: the more regions invest in electricity generation, the greater is the

emissions mitigation. Since mitigation costs are calculated as the area under the marginal

abatement cost curve, greater mitigation implies greater mitigation costs. These findings are

consistent with previous studies.39

Note that the point to the extreme right corresponds to China

which accounts for a third of global investments in electricity generation.

0

500

1000

1500

2000

2500

3000

3500

0 1000 2000 3000

NPV

of M

itiga

tion

cost

s bet

wee

n 20

20 a

nd 2

050

[201

2 bi

llion

USD

]

NPV of investments in electricity generation between 2020 and 2050 [2012 billion USD]

© 2015 Macmillan Publishers Limited. All rights reserved.

26

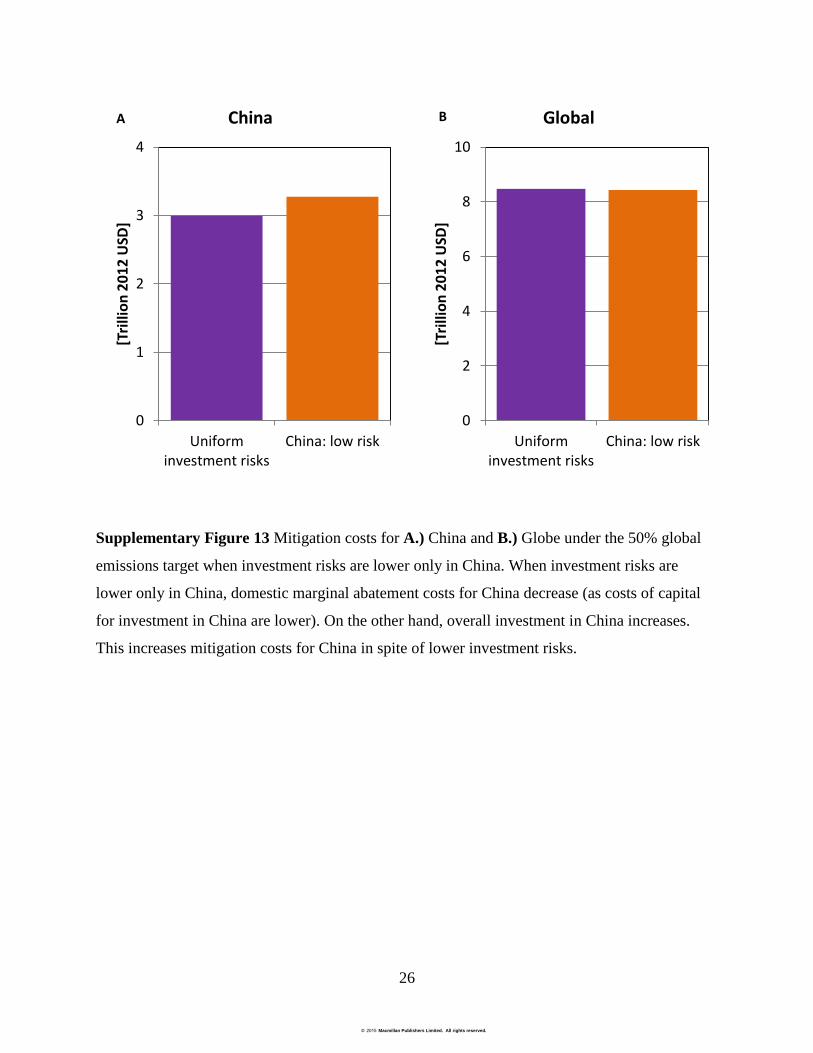

Supplementary Figure 13 Mitigation costs for A.) China and B.) Globe under the 50% global

emissions target when investment risks are lower only in China. When investment risks are

lower only in China, domestic marginal abatement costs for China decrease (as costs of capital

for investment in China are lower). On the other hand, overall investment in China increases.

This increases mitigation costs for China in spite of lower investment risks.

0

1

2

3

4

Uniforminvestment risks

China: low risk

[Tri

llio

n 2

01

2 U

SD]

China A

0

2

4

6

8

10

Uniforminvestment risks

China: low risk[T

rilli

on

20

12

USD

]

Global B

© 2015 Macmillan Publishers Limited. All rights reserved.

27

Supplementary Figure 14 A.) Variation of average lending rates between 2000 and 2012 for

private borrowers with institutional quality. 40

B.) Variation of country risk premiums on the cost

of equity with institutional quality 41, 42

. Data from Damodaran 42

are based on the author’s

calculations and estimates using data from Moody's. Data from Fernandez, Aguirreamalloa 41

are

based on elicitations of experts. The spreads in these data show that investment risks vary

inversely with the quality of institutions. Assuming that FCRs vary with institutional quality

scores according to a log-linear relationship, FCRs for regions other than the U.S. are calculated

using the following expression: 𝐹𝐶𝑅𝑖,𝑗 = 𝐹𝐶𝑅𝑖,𝑈𝑆𝐴 × 𝑓 where 𝐹𝐶𝑅𝑖,𝑗 is the FCR for technology

i in region j and f is given by: 𝑓 = 𝛾0+𝛾1 ln 𝐼𝑄𝑗

𝛾0+𝛾1 ln 𝐼𝑄𝑈𝑆𝐴 , where 𝐼𝑄𝑗 refers to the GDP-weighted

institutional quality score for region j.43, 44

𝛾0 and 𝛾1which are parameters of the log-linear model

are chosen such that the spread in FCRs across GCAM regions is consistent with the spreads

observed in lending rates and costs of equity above. The wide spread in the data indicates that

even countries with lower quality of institutions can have lower interest rates for a variety of

reasons. See Supplementary Text (Section 1.2) for a review of such reasons for the case of China

(China’s institutional quality score is close to the 60th percentile). See also, Supplementary Text

(Section 1.2) for explanations of different terms and concepts related to the cost of capital.

0%

5%

10%

15%

20%

25%

0 2 4 6 8

Lend

ing

rate

[%]

Institutional Quality Score

A

0%

5%

10%

15%

20%

25%

0 2 4 6 8Co

untr

y eq

uity

risk

pre

miu

m [%

]

Institutional Quality score

Damodaran (2013)

Fernandez et al.(2012)

B

© 2015 Macmillan Publishers Limited. All rights reserved.

28

Supplementary Figure 15 Global carbon prices in 2050 under different global emissions

reductions targets (see Supplementary Table 4 for detailed assumptions).

0

50

100

150

200

250

25% reductiontarget

50% reductiontarget

75% reductiontarget

[201

2 U

SD/t

CO2]

Uniform investment risks Technology & institutional risks

© 2015 Macmillan Publishers Limited. All rights reserved.

29

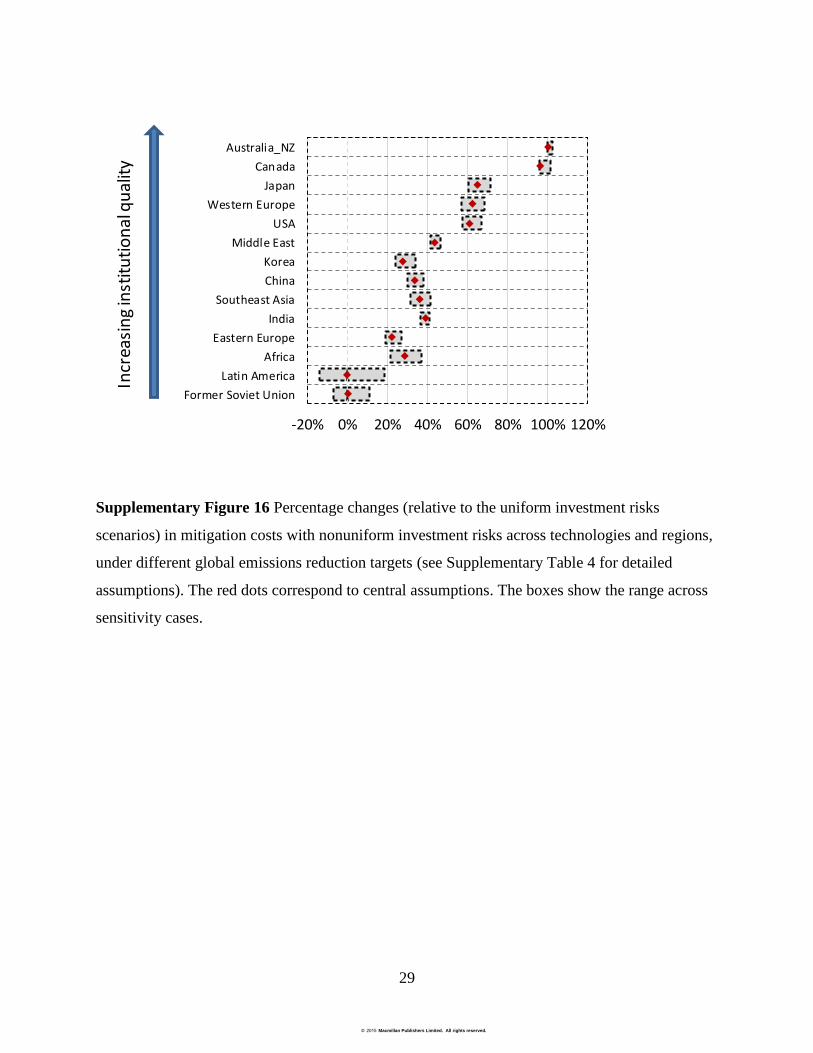

Supplementary Figure 16 Percentage changes (relative to the uniform investment risks

scenarios) in mitigation costs with nonuniform investment risks across technologies and regions,

under different global emissions reduction targets (see Supplementary Table 4 for detailed

assumptions). The red dots correspond to central assumptions. The boxes show the range across

sensitivity cases.

-20% 0% 20% 40% 60% 80% 100% 120%

Former Soviet UnionLatin America

AfricaEastern Europe

IndiaSoutheast Asia

ChinaKorea

Middle EastUSA

Western EuropeJapan

CanadaAustralia_NZ

Incr

easin

gins

titut

iona

l qua

lity

© 2015 Macmillan Publishers Limited. All rights reserved.

30

Supplementary Figure 17 Global carbon prices in 2050 under different assumptions regarding

fixed charge rates (see Supplementary Table 4 for detailed assumptions). The cases presented

here correspond to the 50% global emissions target.

B

[201

2 U

SD/t

CO2]

[201

2 U

SD/t

CO2]

A

0

50

100

150

200

FCR:10-14 FCR:13-17 FCR:16-20

21%22%

22%

0

50

100

150

200

FCR:13-15 FCR:13-17 FCR:13-19

15% 22%28%

Low-risk FCR = 10%Risk premium = 4%

Low-risk FCR = 13%Risk premium = 4%

Low-risk FCR = 16%Risk premium = 4%

Low-risk FCR = 13%Risk premium = 2%

Low-risk FCR = 13%Risk premium = 4%

Low-risk FCR = 13%Risk premium = 6%

Effect of changing low-risk FCR Effect of changing risk premium

Uniform investment risks Technology & institutional risks

© 2015 Macmillan Publishers Limited. All rights reserved.

31

Supplementary Figure 18 Percentage changes (with respect to the uniform investment risks

scenarios) in mitigation costs with nonuniform investment risks across technologies and regions,

under different FCR assumptions (see Supplementary Table 4 for detailed assumptions). The red

dots correspond to central assumptions. The boxes show the range across sensitivity cases. The

cases presented here correspond to the 50% global emissions target.

BA Effect of changing low-risk FCR Effect of changing risk premiumIn

crea

sing

inst

itutio

nal q

ualit

y

-80% -40% 0% 40% 80% 120%

Former Soviet UnionLatin America

AfricaEastern Europe

IndiaSoutheast Asia

ChinaKorea

Middle EastUSA

Western EuropeJapan

CanadaAustralia_NZ

-80% -40% 0% 40% 80% 120%

Former Soviet UnionLatin America

AfricaEastern Europe

IndiaSoutheast Asia

ChinaKorea

Middle EastUSA

Western EuropeJapan

CanadaAustralia_NZ

© 2015 Macmillan Publishers Limited. All rights reserved.

32

Supplementary Figure 19 Global carbon prices in 2050 when A.) investment risks for

renewables, nuclear, CCS and bioenergy are higher compared to fossil-fuel technologies and B.)

investment risks for fossil-fuel technologies are higher compared to renewables, nuclear, CCS

and bioenergy. The cases presented here correspond to the 50% global emissions target (see

Supplementary Table 4 for detailed assumptions).

0

50

100

150

200

Low carbon: High risk Fossil fuel: High risk

[201

2 U

SD/t

CO2]

22% -3%

A B

Uniform investment risks Technology & institutional risks

© 2015 Macmillan Publishers Limited. All rights reserved.

33

Supplementary Tables

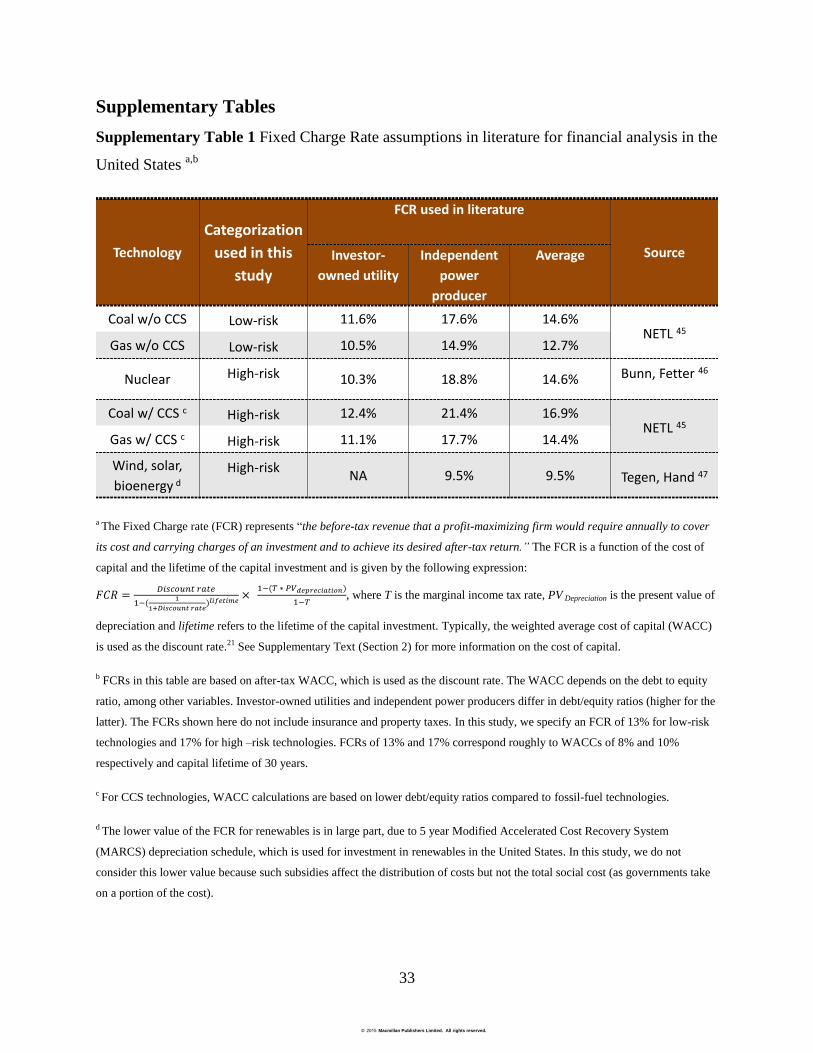

Supplementary Table 1 Fixed Charge Rate assumptions in literature for financial analysis in the

United States a,b

a The Fixed Charge rate (FCR) represents “the before-tax revenue that a profit-maximizing firm would require annually to cover

its cost and carrying charges of an investment and to achieve its desired after-tax return.” The FCR is a function of the cost of

capital and the lifetime of the capital investment and is given by the following expression:

𝐹𝐶𝑅 =𝐷𝑖𝑠𝑐𝑜𝑢𝑛𝑡 𝑟𝑎𝑡𝑒

1−(1

1+𝐷𝑖𝑠𝑐𝑜𝑢𝑛𝑡 𝑟𝑎𝑡𝑒)𝑙𝑖𝑓𝑒𝑡𝑖𝑚𝑒

× 1−(𝑇 ∗ 𝑃𝑉𝑑𝑒𝑝𝑟𝑒𝑐𝑖𝑎𝑡𝑖𝑜𝑛)

1−𝑇, where T is the marginal income tax rate, PV Depreciation is the present value of

depreciation and lifetime refers to the lifetime of the capital investment. Typically, the weighted average cost of capital (WACC)

is used as the discount rate.21 See Supplementary Text (Section 2) for more information on the cost of capital.

b FCRs in this table are based on after-tax WACC, which is used as the discount rate. The WACC depends on the debt to equity

ratio, among other variables. Investor-owned utilities and independent power producers differ in debt/equity ratios (higher for the

latter). The FCRs shown here do not include insurance and property taxes. In this study, we specify an FCR of 13% for low-risk

technologies and 17% for high –risk technologies. FCRs of 13% and 17% correspond roughly to WACCs of 8% and 10%

respectively and capital lifetime of 30 years.

c For CCS technologies, WACC calculations are based on lower debt/equity ratios compared to fossil-fuel technologies.

d The lower value of the FCR for renewables is in large part, due to 5 year Modified Accelerated Cost Recovery System

(MARCS) depreciation schedule, which is used for investment in renewables in the United States. In this study, we do not

consider this lower value because such subsidies affect the distribution of costs but not the total social cost (as governments take

on a portion of the cost).

Technology

Categorization

used in this

study

FCR used in literature

SourceInvestor-

owned utility

Independent

power

producer

Average

Coal w/o CCS Low-risk 11.6% 17.6% 14.6%NETL 45

Gas w/o CCS Low-risk 10.5% 14.9% 12.7%

Nuclear High-risk 10.3% 18.8% 14.6% Bunn, Fetter 46

Coal w/ CCS c High-risk 12.4% 21.4% 16.9%NETL 45

Gas w/ CCS c High-risk 11.1% 17.7% 14.4%

Wind, solar, bioenergy d

High-risk NA 9.5% 9.5% Tegen, Hand 47

© 2015 Macmillan Publishers Limited. All rights reserved.

34

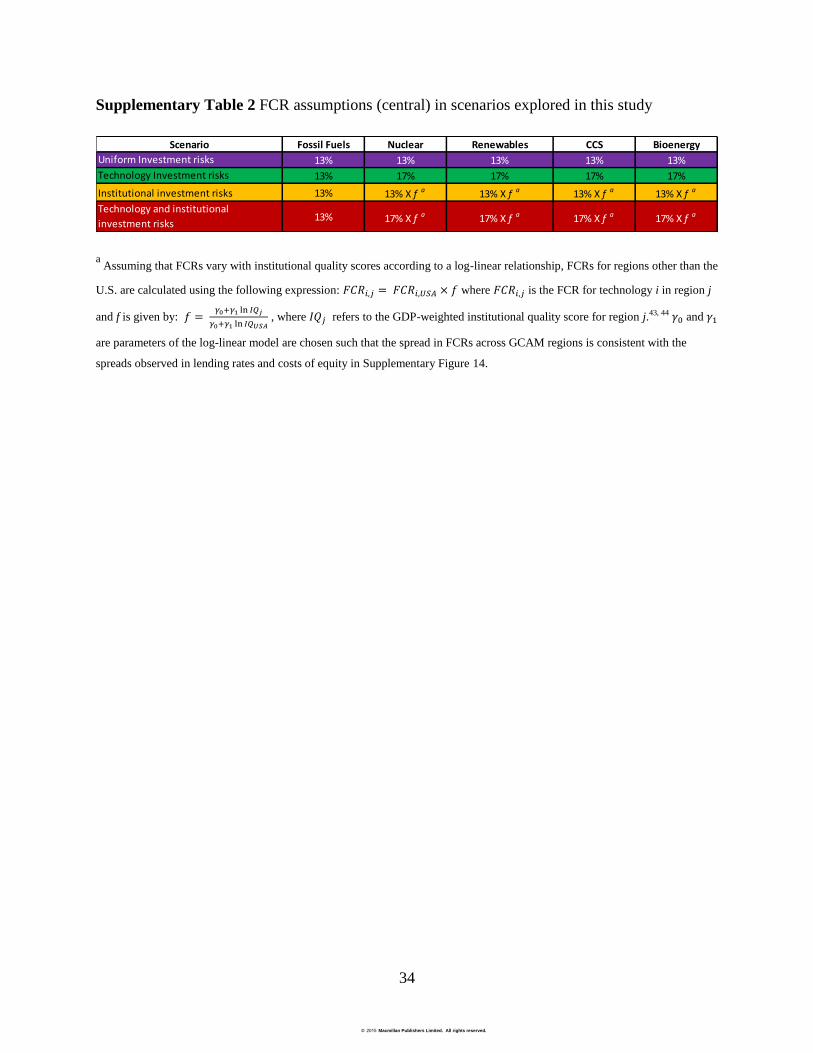

Supplementary Table 2 FCR assumptions (central) in scenarios explored in this study

a Assuming that FCRs vary with institutional quality scores according to a log-linear relationship, FCRs for regions other than the

U.S. are calculated using the following expression: 𝐹𝐶𝑅𝑖,𝑗 = 𝐹𝐶𝑅𝑖,𝑈𝑆𝐴 × 𝑓 where 𝐹𝐶𝑅𝑖,𝑗 is the FCR for technology i in region j

and f is given by: 𝑓 = 𝛾0+𝛾1 ln 𝐼𝑄𝑗

𝛾0+𝛾1 ln 𝐼𝑄𝑈𝑆𝐴 , where 𝐼𝑄𝑗 refers to the GDP-weighted institutional quality score for region j.43, 44 𝛾0 and 𝛾1

are parameters of the log-linear model are chosen such that the spread in FCRs across GCAM regions is consistent with the

spreads observed in lending rates and costs of equity in Supplementary Figure 14.

Scenario Fossil Fuels Nuclear Renewables CCS Bioenergy

Uniform Investment risks 13% 13% 13% 13% 13%Technology Investment risks 13% 17% 17% 17% 17%Institutional investment risks 13% 13% X f a 13% X f a 13% X f a 13% X f a

Technology and institutional investment risks 13% 17% X f a 17% X f a 17% X f a 17% X f a

© 2015 Macmillan Publishers Limited. All rights reserved.

35

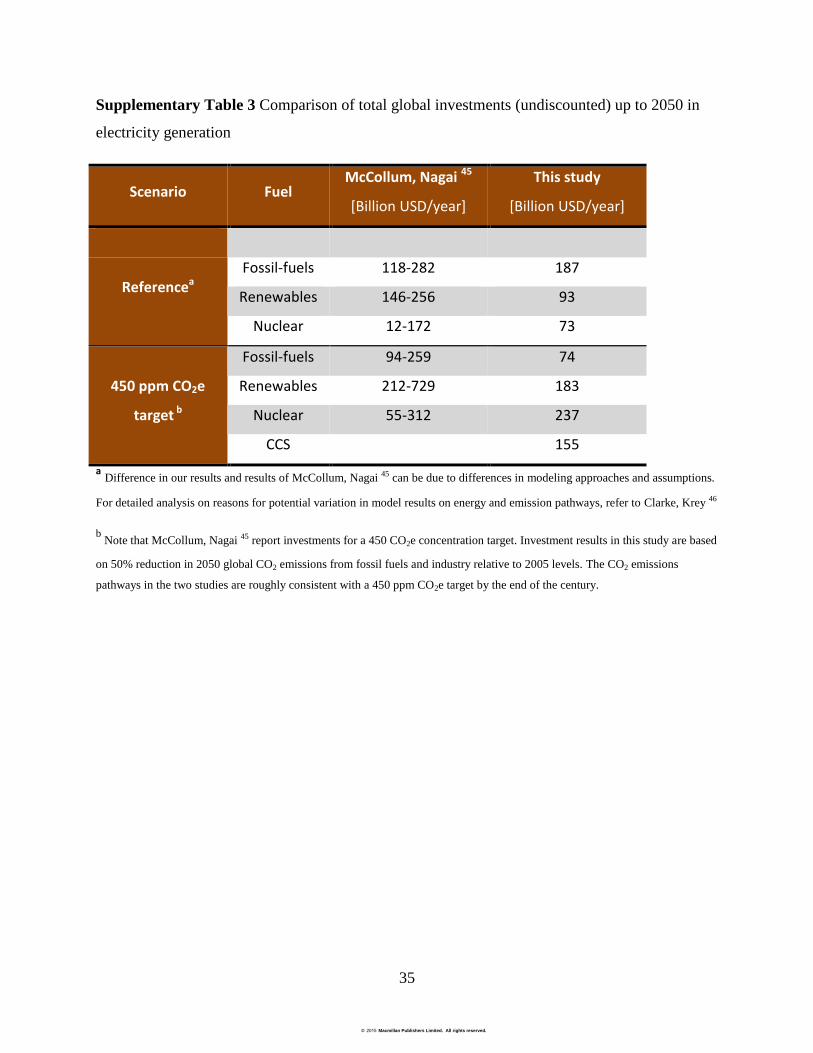

Supplementary Table 3 Comparison of total global investments (undiscounted) up to 2050 in

electricity generation

Scenario Fuel McCollum, Nagai 45

[Billion USD/year]

This study

[Billion USD/year]

Referencea

Fossil-fuels 118-282 187

Renewables 146-256 93

Nuclear 12-172 73

450 ppm CO2e

target b

Fossil-fuels 94-259 74

Renewables 212-729 183

Nuclear 55-312 237

CCS 155 a Difference in our results and results of McCollum, Nagai 45 can be due to differences in modeling approaches and assumptions.

For detailed analysis on reasons for potential variation in model results on energy and emission pathways, refer to Clarke, Krey 46

b Note that McCollum, Nagai 45 report investments for a 450 CO2e concentration target. Investment results in this study are based

on 50% reduction in 2050 global CO2 emissions from fossil fuels and industry relative to 2005 levels. The CO2 emissions

pathways in the two studies are roughly consistent with a 450 ppm CO2e target by the end of the century.

© 2015 Macmillan Publishers Limited. All rights reserved.

36

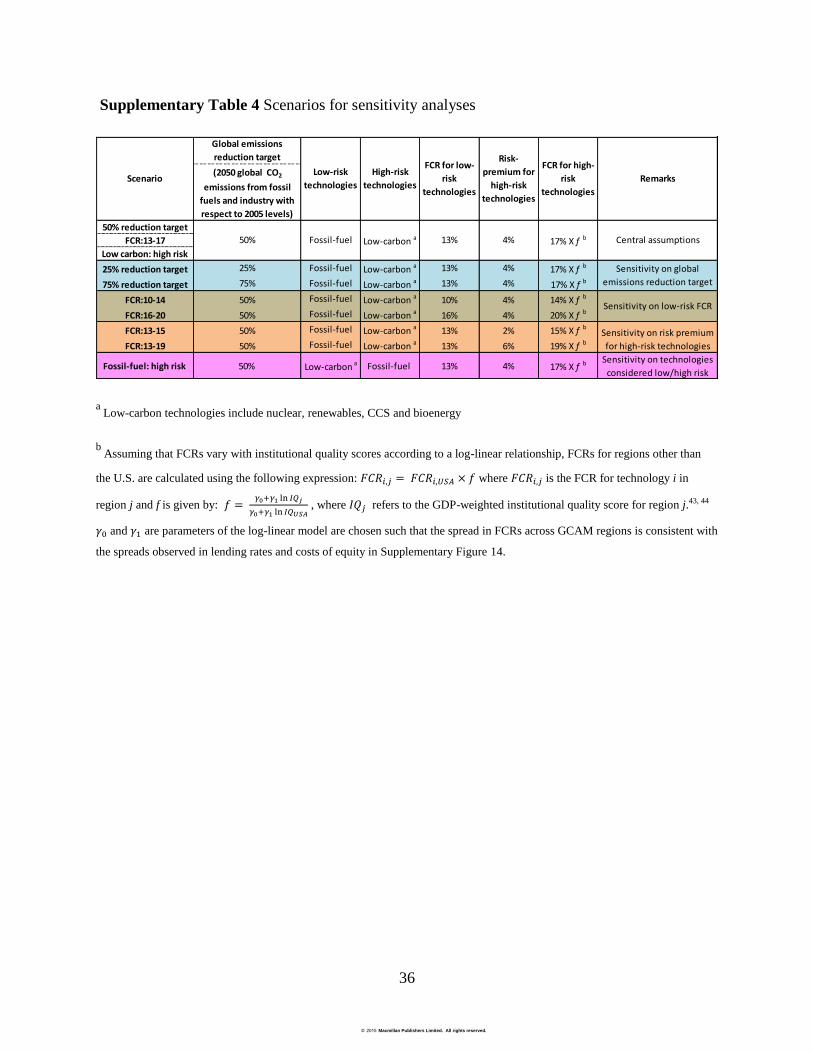

Supplementary Table 4 Scenarios for sensitivity analyses

a Low-carbon technologies include nuclear, renewables, CCS and bioenergy

b Assuming that FCRs vary with institutional quality scores according to a log-linear relationship, FCRs for regions other than

the U.S. are calculated using the following expression: 𝐹𝐶𝑅𝑖,𝑗 = 𝐹𝐶𝑅𝑖,𝑈𝑆𝐴 × 𝑓 where 𝐹𝐶𝑅𝑖,𝑗 is the FCR for technology i in

region j and f is given by: 𝑓 = 𝛾0+𝛾1 ln 𝐼𝑄𝑗

𝛾0+𝛾1 ln 𝐼𝑄𝑈𝑆𝐴 , where 𝐼𝑄𝑗 refers to the GDP-weighted institutional quality score for region j.43, 44

𝛾0 and 𝛾1 are parameters of the log-linear model are chosen such that the spread in FCRs across GCAM regions is consistent with

the spreads observed in lending rates and costs of equity in Supplementary Figure 14.

Global emissions

reduction target

(2050 global CO2

emissions from fossil

fuels and industry with

respect to 2005 levels)

50% reduction target

FCR:13-17

Low carbon: high risk

25% reduction target 25% Fossil-fuel Low-carbon a 13% 4% 17% X f b

75% reduction target 75% Fossil-fuel Low-carbon a 13% 4% 17% X f b

FCR:10-14 50% Fossil-fuel Low-carbon a 10% 4% 14% X f b

FCR:16-20 50% Fossil-fuel Low-carbon a 16% 4% 20% X f b

FCR:13-15 50% Fossil-fuel Low-carbon a 13% 2% 15% X f b

FCR:13-19 50% Fossil-fuel Low-carbon a 13% 6% 19% X f b

Fossil-fuel: high risk 50% Low-carbon a Fossil-fuel 13% 4% 17% X f bSensitivity on technologies

considered low/high risk

Scenario

Sensitivity on global emissions reduction target

Sensitivity on low-risk FCR

Low-risk

technologies

High-risk

technologies

FCR for low-

risk

technologies

Risk-

premium for

high-risk

technologies

FCR for high-

risk

technologies

Remarks

50% Fossil-fuel Low-carbon a 13%

Sensitivity on risk premium for high-risk technologies

4% 17% X f b Central assumptions

© 2015 Macmillan Publishers Limited. All rights reserved.

37

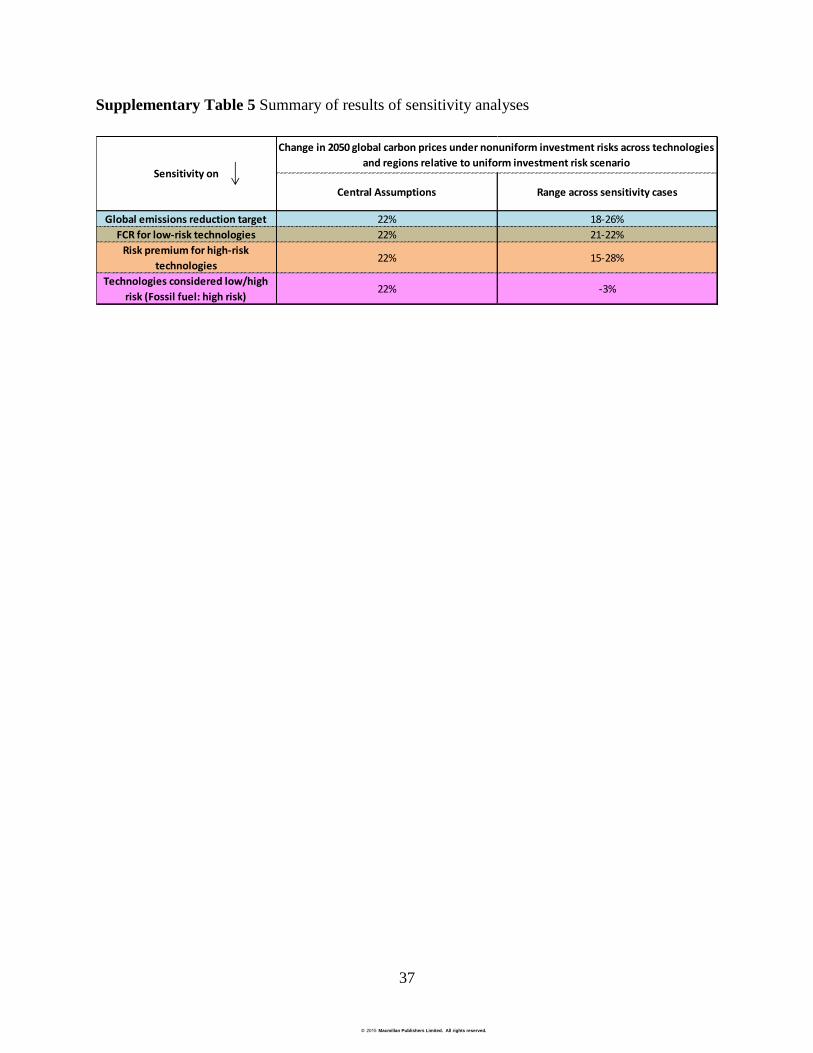

Supplementary Table 5 Summary of results of sensitivity analyses

Central Assumptions Range across sensitivity cases

Global emissions reduction target 22% 18-26%FCR for low-risk technologies 22% 21-22%

Risk premium for high-risk

technologies22% 15-28%

Technologies considered low/high

risk (Fossil fuel: high risk)22% -3%

Change in 2050 global carbon prices under nonuniform investment risks across technologies

and regions relative to uniform investment risk scenarioSensitivity on

© 2015 Macmillan Publishers Limited. All rights reserved.

38

References

1. North DC. Institutions, institutional change and economic performance. Cambridge

university press, 1990.

2. Acemoglu D, Zilibotti F. Was Prometheus Unbound by Chance? Risk, Diversification,

and Growth. Journal of Political Economy 1997, 105(4): 709-751.

3. Faria A, Mauro P. Institutions and the external capital structure of countries. Journal of

International Money and Finance 2009, 28(3): 367-391.

4. La Porta R, Lopez-de-Silanes F, Shleifer A, Vishny RW. Legal Determinants of External

Finance. The Journal of Finance 1997, 52(3): 1131-1150.

5. Clague C, Keefer P, Knack S, Olson M. Contract-intensive money: contract enforcement,

property rights, and economic performance. Journal of Economic Growth 1999, 4(2):

185-211.

6. Levy B, Spiller PT. The Institutional Foundations of Regulatory Commitment: A

Comparative Analysis of Telecommunications Regulation. Journal of Law, Economics,

& Organization 1994, 10(2): 201-246.

7. Stasavage D. Private investment and political institutions. Economics & politics 2002,

14(1): 41-63.

8. Bergara ME, Henisz WJ, Spiller PT. Political Institutions and Electric Utility Investment:

a cross-nation analysis. California management review 1998, 40(2): 18-35.

9. Spiller PT. A Positive Political Theory of Regulatory Instruments: Contracts,

Administrative Law or Regulatory Specificity. Southern California Law Review 1995,

69: 477–515.

10. Woodhouse EJ. Obsolescing Bargain Redux-Foreign Investment in the Electric Power

Sector in Developing Countries. New York University Journal of International Law and

Politics 2006, 38: 121-219.

© 2015 Macmillan Publishers Limited. All rights reserved.

39

11. Ekholm T, Ghoddusi H, Krey V, Riahi K. The effect of financial constraints on energy-

climate scenarios. Energy Policy 2013, 59: 562-572.

12. Fuss S, Szolgayová J, Khabarov N, Obersteiner M. Renewables and climate change

mitigation: Irreversible energy investment under uncertainty and portfolio effects. Energy

Policy 2012, 40: 59-68.

13. Laurikka H, Koljonen T. Emissions trading and investment decisions in the power

sector—a case study in Finland. Energy Policy 2006, 34(9): 1063-1074.

14. Laurikka H. The impact of climate policy on heat and power capacity investment

decisions. In: Antes R, Hansjürgens B, Letmathe P (eds). Emissions Trading and

Business. Physica-Verlag HD, 2006.

15. Jaffe AB, Newell RG, Stavins RN. Environmental policy and technological change.

Environmental and Resource Economics 2002, 22(1): 41-70.

16. Krohn S, Morthorst P-E, Awerbuch S. The Economics of Wind Energy -A report by the

European Wind Energy Association: European Wind Energy Association; 2009.

17. Roques FA, Newbery DM, Nuttall WJ. Investment incentives and electricity market

design: the British experience Review of Network Economics 2005, 4(2): 93-128.

18. Borenstein S. The trouble with electricity markets: understanding California's

restructuring disaster. The Journal of Economic Perspectives 2002, 16(1): 191-211.

19. Steggals W, Gross R, Heptonstall P. Winds of change: How high wind penetrations will

affect investment incentives in the GB electricity sector. Energy Policy 2011, 39(3):

1389-1396.

20. Rose NL, Joskow PL. The diffusion of new technologies: Evidence from the electric

utility industry. Rand Journal of Economics 1990, 21(3): 354-373.

21. Short W, Packey DJ, Holt T. A Manual for the Economic Evaluation of Energy

Efficiency and Renewable Energy Technologies. Golden, Colorado: National Reenwable

Energy Laboratory; 1995.

© 2015 Macmillan Publishers Limited. All rights reserved.

40

22. Stiglitz JE, Weiss A. Credit rationing in markets with imperfect information The

American economic review 1981, 393-410.

23. Jaffe AB, Stavins RN. The energy-efficiency gap - What does it mean? Energy policy

1994, 22(10): 804-810.

24. Frankfurt School-UNEP Centre/BNEF. Global Trends in Renewable Energy Investment

2014. Frankfurt, Germany: Frankfurt School-UNEP Collaborating Centre, the United

Nations Environment Programme (UNEP) and Bloomberg New Energy Finance (BNEF);

2014.

25. WNA. Plans For New Reactors Worldwide. 2013 [cited 2014 7-24]Available from:

http://www.world-nuclear.org/info/current-and-future-generation/plans-for-new-reactors-

worldwide/

26. Sullivan R. Investment-grade climate change policy: financing the transition to the low-

carbon economy; 2011.

27. Victor DG, Hults D, Thurber M. Oil and Governance: State-Owned Enterprises and the

World Energy Supply. Cambridge University Press: Cambridge, 2012.

28. Rong F, Victor DG. What does it cost to build a power plant? San Diego, USA:

Laboratory on International Law and Regulation; 2011.

29. Clarke JF, Edmonds J. Modelling energy technologies in a competitive market.

1993(August 1992): 123-129.

30. McFadden D. Econometric models for probabilistic choice among products. The Journal

of Business 1980, 53(3): S13-S29.

31. Train K. Qualitative choice analysis: theory, econometrics, and an application to

automobile demand MIT Press, 1993.

32. Iyer G, Hultman N, Eom J, McJeon H, Patel P, Clarke L. Diffusion of low-carbon

technologies and the feasibility of long-term climate targets. Technological Forecasting

and Social Change 2013.

© 2015 Macmillan Publishers Limited. All rights reserved.

41

33. Hultman NE, Malone EL, Runci P, Carlock G, Anderson KL. Factors in low-carbon

energy transformations: Comparing nuclear and bioenergy in Brazil, Sweden, and the

United States. Energy Policy 2012, 40: 131-146.

34. Iyer G, Hultman N, Fetter S, Kim SH. Implications of small modular reactors for climate

change mitigation. Energy Economics 2014, 45: 144-154.

35. McJeon HC, Clarke L, Kyle P, Wise M, Hackbarth A, Bryant BP, et al. Technology

interactions among low-carbon energy technologies: What can we learn from a large

number of scenarios? Energy Economics 2011, 33(4): 619-631.

36. Clarke LE, Wise MA, Edmonds JA, Placet M, Kyle P, Calvin K, et al. CO2 Emissions

Mitigation and Technological Advance: An Updated Analysis of Advanced Technology

Scenarios. Richland, WA, 2008: Pacific Northwest National Laboratory; 2008.

37. Peck SC, Wan YS. Analytic Solutions of Simple Optimal Greenhouse Gas Emissions

Models. In: van Ierland EC, Gorka K (eds). Economics of Atmospheric Pollution, vol. 14.

Springer Verlag: Berlin, Heidelberg, 1996, pp 113–121.

38. Kriegler E, Weyant JP, Blanford GJ, Krey V, Clarke L, Edmonds J, et al. The role of

technology for achieving climate policy objectives: overview of the EMF 27 study on

global technology and climate policy strategies. Climatic Change 2014, 123(3-4): 353-

367.

39. Carraro C, Favero A, Massetti E. “Investments and public finance in a green, low carbon,

economy”. Energy Economics 2012, 34: S15-S28.

40. The World Bank. International Debt Statistics. Washington D.C., USA: The World Bank;

2013.

41. Fernandez P, Aguirreamalloa J, Corres L. Market Risk Premium used in 82 countries in

2012: a survey with 7,192 answers IESE Business School; 2012.

42. Damodaran A. Country Default Spreads and Risk Premiums. 2014 [cited 2014 17th

July]Available from:

http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/ctryprem.html

43. Erb CB, Harvey CR, Viskanta TE. Expected returns and volatility in 135 countries. The

Journal of Portfolio Management 1996, 22(3): 46-58.

© 2015 Macmillan Publishers Limited. All rights reserved.

42

44. Benítez PC, McCallum I, Obersteiner M, Yamagata Y. Global potential for carbon

sequestration: Geographical distribution, country risk and policy implications. Ecological

Economics 2007, 60(3): 572-583.

45. McCollum D, Nagai Y, Riahi K, Marangoni G, Calvin K, Pietzcker R, et al. Energy

investments under climate policy: a comparison of global models Climate Change

Economics 2014.

46. Clarke L, Krey V, Weyant J, Chaturvedi V. Regional energy system variation in global

models: Results from the Asian Modeling Exercise scenarios. Energy Economics 2012,

34: S293-S305.

© 2015 Macmillan Publishers Limited. All rights reserved.