Important Pension Changes From D.C. - What Do You Need to Know?

35

Important Pension Changes From D.C. - What Do You Need to Know? Marcia S. Wagner, Esq.

description

Important Pension Changes From D.C. - What Do You Need to Know?. Marcia S. Wagner, Esq. Transforming the Retirement System. Regulatory landscape is changing. DOL is rolling out new rules for 2012. Fee disclosures for plan sponsors Participant-level fee disclosures - PowerPoint PPT Presentation

Transcript of Important Pension Changes From D.C. - What Do You Need to Know?

Important Pension Changes From D.C. - What Do You Need to Know?

Marcia S. Wagner, Esq.

2

Transforming the Retirement SystemRegulatory landscape is changing.DOL is rolling out new rules for 2012.◦ Fee disclosures for plan sponsors◦ Participant-level fee disclosures◦ Participant investment advice

Proposed RulemakingDOL Interaction with White House◦ Working with White House’s Middle Class Task Force◦ Coordinated actions to improve retirement security

3

1. Fee Disclosures to Participants2. Participant Investment Advice3. 408(b)(2) Disclosures4. Broader “Fiduciary” Definition5. Default Investments - TDFs 6. Lifetime Income Options

Fee Disclosures to ParticipantsPractical Implications

To-Do List:Discuss with plan’s recordkeeper the impact of the new rules on existing fee disclosures.Meet with participants and review investment and fee information through educational sessions.Administrative fees and investment fees should not come as a “surprise”.If plan sponsor has fee-related concerns, remind plan sponsor that its fiduciary review process can be enhanced.Research benchmarking for administrative fees.

4

5

1. Fee Disclosures to Participants2. Participant Investment Advice3. 408(b)(2) Disclosures4. Broader “Fiduciary” Definition5. Default Investments - TDFs 6. Lifetime Income Options

6

How Can Inv. Advice Be Conflicted?Non-fiduciary provider receives variable

compensation from plan’s investments.◦ Broker-dealer receives different 12b-1 fees.◦ Fund platform offers proprietary funds to plan clients.

Provider has incentive to steer participants.◦ Cannot provide fiduciary advice to participants.◦ Conflicted advice triggers prohibited transaction (PT).◦ PT occurs even if advice provided in good faith.

7

DOL Final Rules for Participant AdvicePension Protection Act included statutory

exemption for participant-level advice.◦ Fiduciary Adviser must be RIA, bank, insurer or

broker-dealer.◦ Eligible Investment Advice Arrangement must have: (1) Fee-Leveling (Fiduciary Adviser’s fees do not vary) (2) Computer Model certified by expert.

Other conditions for exemption.◦ Authorization from separate plan fiduciary.◦ Annual review by independent auditor.◦ Advance notice to participants with disclosures for

fees and material affiliations of parties (i.e., conflicts).

8

Fee-Leveling ArrangementFiduciary Adviser’s fee must not vary.◦ Fiduciary Adviser’s employee/rep must receive level

compensation.◦ Fiduciary Adviser’s affiliate may receive variable

compensation.

Example: ABC Fund Platform for Plan Clients◦ Plan invests in ABC Funds and third party funds.◦ ABC Fund Manager cannot give participant advice (due to

incentive to steer participants to ABC Funds).◦ New affiliate, ABC Fiduciary Adviser, is created to provide

advice to participants.◦ DOL imposes fee-leveling on ABC Fiduciary Adviser.◦ But ABC Fund Manager can earn compensation that varies

with participants’ allocation decisions.

9

Computer Model ArrangementAdvice must be from computer model.◦ Model must be certified by investment expert.◦ Must consider participant’s personal info.◦ Fiduciary Adviser may receive variable compensation.

Does DOL favor index funds?◦ Proposed rules suggested that model should favor

cheapest menu option in each asset class.◦ Fortunately, DOL backed away from this approach.

Can a Computer Model be used for IRAs?◦ DOL permits it.◦ But are Computer Models capable of advising IRA

owners?DOL rules became effective on Dec. 27, 2011.

Participant Investment Advice Practical Implications

Most advisors will continue to rely on pre-PPA DOL guidance.

Benefit platform providers may find the fee-leveling exemption useful:◦RIA receives level fees.◦Affiliated recordkeepers receive variable fees from funds

in a plan’s menu.Individual advisors dislike computer model

advice:◦Model portfolio creation is advisor’s job.◦ It should not be delegated to a computer program.

10

11

1. Fee Disclosures to Participants2. Participant Investment Advice3. 408(b)(2) Disclosures4. Broader “Fiduciary” Definition5. Default Investments - TDFs 6. Lifetime Income Options

12

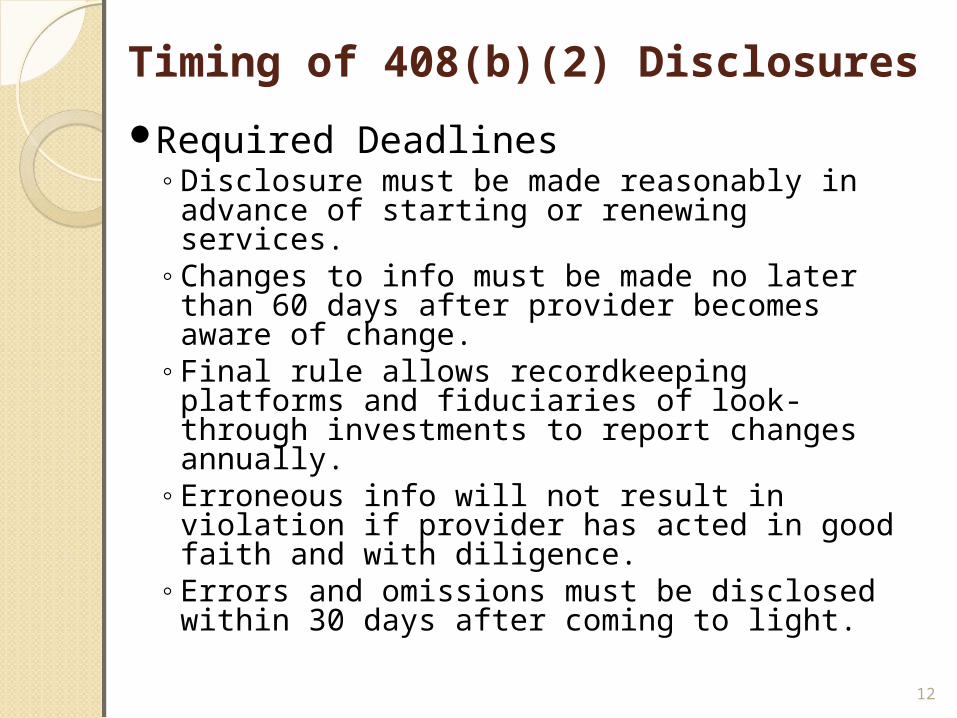

Timing of 408(b)(2) Disclosures

Required Deadlines◦Disclosure must be made reasonably in advance of

starting or renewing services.◦Changes to info must be made no later than 60

days after provider becomes aware of change.◦Final rule allows recordkeeping platforms and

fiduciaries of look-through investments to report changes annually.

◦Erroneous info will not result in violation if provider has acted in good faith and with diligence.

◦Errors and omissions must be disclosed within 30 days after coming to light.

13

Prohibited Transactions and 408(b)(2) Regulations

If provider fails to make disclosure, plan’s payment of fees is a prohibited transaction.◦Disclosure failures can be cured.◦Plan must make written request for information, and

provider must respond within 90 days.◦Refusal or inability to comply with request requires

plan fiduciary to notify DOL, and decide whether to terminate service arrangement, with presumption being termination.

Marketing Tip – if 408(b)(2) notice is incomplete, remind plan sponsors of this vendor termination presumption.

14

Best Practices for Fiduciary Review of Fees

ERISA 408(b)(2) effectively “raises the bar” for fiduciary review of plan fees.◦ Consider adopting best practices for evaluating fee

disclosures.◦ Establish prudent review process.

Basic Procedural Steps and Principles◦ Focus on provider’s qualifications and provider’s

quality of services (in addition to considering fees).◦ Conduct reviews regularly.◦ Consider provider’s total compensation.◦ Evaluate fees in proper context.◦ Document reviews.

15

Best Practices – Value Proposition and FPS

Consider provider’s value proposition.◦ Don’t look for provider with cheapest fees.◦ Make inquiries about service offering.◦ Evaluate fees in light of services provided.

Adopt a fee policy statement (FPS).◦ FPS offers procedural discipline for plan fiduciary’s

review of fees.◦ Reviews under FPS should be coordinated with IPS.◦ FPS itself can help demonstrate procedural prudence.

16

1. Fee Disclosures to Participants2. Participant Investment Advice3. 408(b)(2) Disclosures4. Broader “Fiduciary” Definition 5. Default Investments - TDFs 6. Lifetime Income Options

17

DOL’s Campaign to Expose ConflictsDOL Strategy

◦ Roll out new fee disclosure rules.◦ Impose fiduciary status on more providers.◦ Force non-fiduciary advisors to make disclaimers.

DOL releases proposed reg’s on Oct. 21, 2010.◦ Broadens “investment advice fiduciary” definition.◦ Withdrawn on September 19, 2011.◦ To be re-proposed with more input from public.

If you provide investment advice, you are automatically deemed a fiduciary.

DOL’s current definition for investment advice is based on 5-factor test.

18

Overview of DOL’s Initial Proposal

Existing Definition◦ Advice may be investment advice if it is a primary

basis for plan decisions and given on regular basis.

DOL’s Initial Proposal◦ Include any advice that may be considered by plan.◦ May include casual advice or one-time advice.◦ Non-fiduciary advisors must make disclaimer: (1) advisor is acting as seller of securities. (2) advisor’s interests are adverse to client. (3) advice is not impartial.

19

Broader “Fiduciary” DefinitionPractical Implications

Non-Fiduciary Advisors◦ Would need to change service model.◦ Must disclose they are not providing impartial

advice.◦ Or they could accept fiduciary status and become

subject to ERISA.

Re-proposed Rule in 2012◦ New definition to include individualized advice only.◦ Will be similar in approach to DOL’s initial proposal.◦ DOL is coordinating with SEC.

Broader “Fiduciary” DefinitionPractical Implications

DOL proposal likely to pressure advisors to provide fiduciary services for level fees.◦ Advisors unwilling to serve plan clients on these terms

may be forced out of retirement space.

Advisors, especially non-fiduciaries, should re-evaluate business model for plan clients.◦ Explore working with recordkeeping platforms that have

ability to offer level payouts.◦ Explore use of ERISA fee recapture accounts to ensure

advisor retains level fee only.◦ Consider becoming “dual registrant” and charge level

asset-based fee as RIA.◦ No easy “one size fits all” solution for firms.

20

21

1. Fee Disclosures to Participants2. Participant Investment Advice3. 408(b)(2) Disclosures4. Broader “Fiduciary” Definition5. Default Investments - TDFs 6. Lifetime Income Options

22

Background on Target Date Funds

Popular default investment vehicle for 401(k) plans.

Typically, formed as open-end investment companies registered under the Inv. Co. Act.

Defining characteristic – “glide path” which determines the overall asset mix of the fund.

Performance issues in 2008 raise concerns, especially for near-term TDFs.◦ Based on SEC analysis, the average loss for TDFs with

a 2010 target date was -25%.◦ Individual TDF losses as high as -41%.

23

Recent Developments for TDFsDOL and SEC at Senate Special Committee on

Aging hearing on TDFs (Oct. 28, 2009).◦ Investor Bulletin jointly released by DOL and SEC.◦ DOL’s fiduciary checklist on TDFs is pending.

SEC proposal for TDF advertising materials.◦ If name has target date, “tag line” disclosure needed.◦ Advertising must include glide path information.

On Nov. 30, 2010, DOL proposes rules on TDF disclosures for participants, amending:◦ QDIA reg’s issued under PPA of 2006◦ Participant-level fee disclosure reg’s that were

finalized on Oct. 14, 2010 but are not yet effective.

24

DOL’s Proposed Changes to QDIA Reg’sBackground on QDIA Reg’s◦ Participant deemed to be directing investment to

default choice if QDIA requirements are met.◦ Default investment must be a QDIA, and QDIA notices

must be provided to participants.

DOL proposes change to QDIA notice for TDFs.◦ Explanation and illustration of TDF’s glide path.◦ Relevance of target date (e.g., 2030) in TDF name.◦ Disclaimer that TDF may lose money after retirement.

DOL also proposes general changes to QDIA notice (even if not a TDF).

25

DOL’s Proposed Changes to Participant-Level Fee Disclosure Reg’s

Background (recap)◦ New rules will require disclosure of plan-related fees

and annual comparative chart for plan’s investments.

DOL proposes change to annual comparative chart for TDFs (even if not a QDIA).◦ Must include appendix with additional TDF info. ◦ Same info as required for QDIA notice.

Informal follow-up guidance from DOL◦ TDF prospectus is unlikely to satisfy QDIA notice and

annual comparative chart requirements, as proposed.

◦ DOL will not provide “model” target date disclosures.

26

Conflicts of Interest in TDFsConflicts arise when a “fund of funds” invests

in affiliated underlying funds.◦ Conflicts are permitted because fund managers are

carved out from ERISA’s fiduciary requirements.Are fund managers ever subject to ERISA? ◦ Firm requested clarification on scope of carve-out.◦ In Adv. Op. 2009-04A (Avatar Associates), DOL

declined to rule that the TDF managers are fiduciaries.

Implications of DOL guidance◦ Plan sponsors are alone in their fiduciary obligation.◦ Must ensure TDFs (and underlying funds) are

appropriate plan investments.

27

Congressional Proposal for TDFs

Senator Kohl announced his intent to introduce new legislation (Dec. 2009).◦ Concerns over high fees, low performance or

excessive risk in many TDFs.◦ Would impose ERISA fiduciary status on TDF

managers when TDF used as QDIA in 401(k) plans.

28

Default Investments – TDFs Practical Implications

Provide meaningful TDF disclosures to participants as a “best practice” right now.◦ Provide key information about TDF’s glide path,

landing point and potential volatility.

Also facilitate sponsor’s prudent review of the plan’s TDF series.◦ Assist in the fiduciary review of the “fund of funds”

structure, glide path, underlying funds and risk.◦ Special review of TDFs for participants in or nearing

retirement (e.g., 2015 TDF).

29

1. Fee Disclosures to Participants2. Participant Investment Advice3. 408(b)(2) Disclosures4. Broader “Fiduciary” Definition5. Default Investments - TDFs 6. Lifetime Income Options

30

Retirement Security and AnnuitizationObama Administration believes lifetime income

options facilitate retirement security.◦ Initiative to reduce barriers to annuitization of 401(k) plan

assets.◦ DOL / IRS issue joint release with requests for information on

Feb 2, 2010.◦ RFI addresses education, disclosure, tax rules, selection of

annuity providers, 404(c) and QDIAs.

The Retirement Security Project◦ Released 2 white papers on DC plan annuitization.◦ Proposed use of annuities as default investment.◦ Utility of default annuities limited because of different needs

to retirees and difficulty in reversal.

31

Other Recent Developments in DC Plan Annuitization

Two types of legislative proposals.◦ Encourage annuitization with tax breaks: Lifetime

Pension Annuity for You Act, Retirement Security for Life Act.

◦ Annual disclosure of what 401(k) plan balance would be worth as annuity: Lifetime Income Disclosure Act.

32

Joint Hearing by DOL, IRS and Treasury in September 2010

Purpose is to investigate 5 focused topics.2 areas of general policy-related interest.◦ Specific concerns raised by participants.◦ Alternative designs of in-plan and distribution lifetime

income options.

3 areas of specific interest.◦ Fostering “education” to help participants make informed

retirement income decisions.◦ Disclosure of account balances as monthly income streams.◦ Modifying fiduciary safe harbor for selection of issuer or

product.

33

IRS TAX RELIEF for Lifetime Income OptionsProposed Regs and Rulings on Required Minimum

Distributions◦PLR 200951039: no surprises as to age 70 ½ interpretations.◦Proposed Reg. (Feb. 2012): longevity annuity beginning at

age 80 or 85 will not violate required minimum distribution rules. Annuity premium lesser of $100,000 or 25% of account balance.

◦Proposed Reg. (Feb. 2012): split distribution options consisting of annuity and lump sum approved.

◦Rev. Rul. 2012-4: participants can rollover 401(k) balance to same employer DB plan and convert to annuity from DB plan.

◦Rev. Rul. 2013-3: deferred annuities in 401(k) plan will not trigger IRS death benefits for surviving spouse.

Lifetime Income Options Practical Implications

Anticipate future legislation or regulation.Most likely: DC plans must disclose

monthly or yearly lifetime income that account balance can provide through annuity purchase.

Also possible: DC plans must offer life annuities as benefit distribution option.

Be prepared to explain concept of longevity annuities.

34

35

Important Pension Changes From D.C. - What Do You Need to Know?

Marcia S. Wagner, Esq.

99 Summer Street, 13th FloorBoston, MA 02110

Tel: (617) 357-5200 Fax: (617) 357-5250 Website: www.wagnerlawgroup.com

[email protected] A0084287