Impairment and provisioning under IFRS. Methodology and...

46

Impairment and provisioning under IFRS. Methodology and solution implementation – – practical experience Natalia Cierna Adam Kołaczyk Bucharest, 11 April 2007

Transcript of Impairment and provisioning under IFRS. Methodology and...

Impairment and provisioning under IFRS. Methodology and solution implementation –– practical experience

Natalia CiernaAdam KołaczykBucharest, 11 April 2007

- 1 - © Deloitte 2007

Introduction1

3 Experience from implementation projects

2 Impairment methodology

4 Impairment methodology

- 2 - © Deloitte 2007

Advantages of implementing provisioning under IFRS

Apart from meeting reporting requirements relating to IFRS introduction, implementing provisioning according to IAS 39 and IAS 37 will result in:

1. Convergence of provisioning methodology with the approach used in credit risk management and Basel 2 e.g. use of PD, LGD, recovery rates, EAD)

2. Better collateral management, ability to analyse collateral efficiency and credit risk measurement.

3. More accurate estimation of loan provisions:

Accounting for bank’s specifics in the area of exposures, internal credit risk assessment methods, effectiveness of receivables and collateral collection processes.

- 3 - © Deloitte 2007

Our experience

Experience in the development of effective interest rate and financial asset impairment methodologies gained in both local and international financial institutions.

Possessing dedicated, tested and working IT solutions – IRR Tool and Impairment Tool – hence we can assure efficient, competent and timely project realization.

Playing active role in Polish Banking Supervision Commission (KNB) and Polish Banking Association working group developing KNB’s impairment implementation recommendation.

Capacity to provide complete services due to possessing a unique team representing comprehensive knowledge and expertise acquired in local and Central European environment in the areas of IFRS implementation, financial instrument accounting, Basel II, risk management, and developing own IT tools related to these areas.

Experience in managing projects which covered both development of methodology and implementing it in IT systems.

Experience in implementing integrated risk management systems covering ALM, FTP, Basel 2 and IAS 39.

Experience in building and implementing IT solutions which support accounting in accordance with IFRS in banks and non-financial institutions:

Impairment tool - system for specific and portfolio provisions according to IFRS;

IRR Tool - system for measurement of debt instruments using effective interest rate;

CRD Synergy Engine – integrated IT solution for Capital Adequacy EU Directive (CRD).

- 4 - © Deloitte 2007

Our experience

Methodology:BRE Bank (Commerzbank Group)Invest Bank (Poland)DZ Bank PolandFortis Bank PolskaOTP Bank Slovakia & RomaniaEFL Leasing (Credit Agricole Group)Santander Consumer Bank (Poland)Hypo-Alpe-Adria banks in Serbia & BosniaCacanska Banka (Serbia)GE Money Bank (Czech Republic)

IT supporting tools:BRE Bank (Commerzbank Group)Invest Bank (Poland)

Impairment

Methodology:Raiffeisen Bank PolskaBank BISE (Poland)Invest Bank (Poland)DZ Bank (Poland)Hypo-Alpe-Adria banks in Serbia & BosniaOTP Bank RomaniaCacanska Banka (Serbia)GE Money Bank (Czech Republic)

IT supporting tools:Raiffeisen Bank PolskaBank BISE (Poland)Invest Bank (Poland)

Effective interest rate

- 5 - © Deloitte 2007

Introduction1

3 Experience from implementation projects

2 Impairment methodology

4 Impairment methodology

- 6 - © Deloitte 2007

Impairment – a reduction of the asset value (recoverable value) below its book value due to the increase in credit risk.

Default – inability to fulfill the contractual obligations. A delay in payment over 90 days is an example of a default indicator.

Loss event – objective evidence of impairment - an event indicating an increased risk of default, e.g. a breach of contractual obligations, bankruptcy, distressed restructuring.

LGD (loss given default) – loss on a loan that has defaulted (1-LGD = recovery rate).

PD (probability of default) – probability of a loan to become defaulted.

IBNR (incurred but not reported) losses – losses which based on statistical data has already occurred but have not been identified individually by the bank

IAS provisioning approach – Terminology

- 7 - © Deloitte 2007

In most jurisdictions IFRS provisioning requirements replace provisioning rules for loans and off-balance sheet exposures, hence new approach must cover both types of exposures:

On-balance sheet exposures

1. Extended loans (all types)

2. Credit card receivables

3. Forced receivables (for example arising from letters of credit, guarantees, debit cards, breach of limits etc.)

4. Breach of limits debits in current and settlement accounts

5. Current account loans

6. Interbank loans

7. Reverse-repo transactions/ buy-sell-back transactions,

8. Commercial papers

Off-balance sheet exposures1. Guarantees

2. Letters of credit

3. Undrawn amounts (including credit cards, credit lines, loans, refinancing lines for banks

Financial assets and off-balance sheet exposures concerned

- 8 - © Deloitte 2007

Main topic areas regarding IAS 39 / IAS 37 provisioning methodology include:

1. Individual vs. portfolio assessment – individually significant and insignificant exposures

2. Client segmentation into homogeneous credit risk groups – for example, according to internal rating, type of product, type of client, past due status

3. Impairment identification:

Occurrence of loss events

Application of PD (Probability of default)

4. Provision calculation

Estimating cash flows from payments made by debtor and collateral realizations (recovery rates, LGD) and calculate provision

Discounting using effective interest rate

5. Recognition of interest income on impaired loans, so called „impairment interest”

No suspended interest concept under IFRS

IAS provisioning approach – major topics

- 9 - © Deloitte 2007

Individual vs. portfolio assessment – segmentation into portfolios

The segmentation of assets into those which are assessed individually and those which are assessed on the portfolio basis in order to identify loss event.

Individually significant items are assessed individually.

Individually insignificant items are assessed either individually or on the portfolio basis (portfolios build based on similar credit risk characteristics)

Assessment of significance should take into account actual management of an exposure (managed on individual basis or group basis)

Those which have been identified as impaired during individual assessment are excluded from the collective assessment

Collective assessment is not possible if the number of homogenous transactions is insufficient

Need to compare model results with the actual losses

- 10 - © Deloitte 2007

In order to establish individual significance the following should be considered:

Credit risk type of given transaction/portfolio and credit risk management method employed by the Bank: retail vs. non-retail exposures – when dividing exposures into those assessed individually and collectively it is important to account for the actual method used to manage given exposures;

Financial report materiality (value of transaction / portfolio – individually / collectively);

Number of transactions of a given type and availability of data relating to those transactions –portfolio approach cannot be used if there is a small number of transactions of a given type.

Individual vs. portfolio assessment – segmentation into portfolios

- 11 - © Deloitte 2007

The next step after dividing exposures into those which will be assessed individually and collectively is the identification of exposures/portfolios where a loss event occurred. Some loss events are universal regardless of client type and product, whereas some are specific to a given client or product type. A sample list of loss event for corporate clients is presented below.

Past due status in principal or interest payments – past due 90 days or more.

Significant breach of contract.

Distressed restructuring:

Change in payment schedule of credit/transaction arising from lack of financial ability on the part of the borrower to make payments specified in the original contract,

The Bank has requested payment of the obligation (in whole), but has not started collateral realization proceedings,

Contract cancellation (in whole or in part) and /or start of collateral realization proceedings.

Decrease in the borrower’s rating.

Information regarding account blocked as of the date of the analysis (for significant reasons).

Decrease in borrower’s rating (into default category or by two grades or more).

Decrease in the value of collateral: increase in LTV (transaction exposure amount / value of realizable collateral) above a certain threshold for project finance transactions and brokerage loans.

Identification of impairment – examples of loss events

- 12 - © Deloitte 2007

Provision calculation – balance sheet exposures

Impairment occurs only when a loss event(s) occurring after the initial recognition of an asset negatively impacts the amount and/or timing of cash flows related to the asset. In this case, the Bank should measure the potential impairment loss amount and related provisions.

Expected losses which may arise due to future events, no matter how likely, are not recognized. However, need to recognise „incurred but not reported” losses (IBNR).

Impairment loss = Carrying amount – recoverable amount

recoverable amount = PV (expected cash flows from the asset) + PV (expected cash flows form collaterals) – PV (collection expenses)

The discount rate used to calculate PV of expected cash flows is the asset’s effective interest rate at the impairment measurement date (for restructured assets – effective interest rate from the moment of restructuring).

Under IFRS interest income is calculated and recognized in income statement on impaired assets (concept of suspended interest is not present in IFRS).

If there is a decrease in impairment loss in a future time period which is caused by events which occurred after the initial impairment recognition, provisions for impairment should be decreased.

- 13 - © Deloitte 2007

Provision for guarantees, letters of credit and unused credit lines calculated under IAS 39 & IAS 37.

The approach to off-balance sheet exposures entails calculating the provision which should be the larger of two values:

best estimate of current obligation calculated under IAS 37 or

fair value as at initial recognition (usually premium received for granting guarantee) adjusted for amortization of the initial fair value according to IAS 18.

Provision amount is decreased by expected recoveries from collateral, unless the collateral constitutes a guarantee or insurance policy provided by a different entity – in this case the collateral is accepted only if its realization is „virtually certain”.

Credit Conversion Factor (CCF) applied for measuring provisions for off-balance sheet exposures.

Provision calculation – off-balance sheet exposures

- 14 - © Deloitte 2007

Loan Originationfees and costs

Provision calculation

(Risk)

Principal and interest

payments

Nominal interest accrual

Booking provisions

(P&L + balance sheet)

Loan book value according to IFRS

Interest income atthe contractual rate

EIR Adjustment

Interest adjustment to impairment interest levelInterest income

according to IFRS

Loan value for the client

Book value of a loan under IFRS

- 15 - © Deloitte 2007

A bank extended a 2 year loan for 100 PLN. The Bank did not take any commissions at loan origination. Consequently, the contractual interest rate on the loan of 10% is equal to the effective interest rate (EIR). The principal is to be repaid in two equal installments at the end of each year.

One year after loan origination, the loan was identified as impaired (the debtor went bankrupt). The book value of the loan at the time of impairment amounted to 110 PLN (100 principal + 10 accrued interest).

The bank assessed the recoverable amount from collateral at 66 PLN to be received in one year. After discounting the recoverable amount using EIR (10%), the present value (PV) of the recoverable amount equals to 60 PLN (66/(1+10%)=60). Consequently, a 50 PLN (110 – 60) provision was created, and consequently the net book value of the loan after provision amounts to 60 PLN.

From this moment interest should still be accrued using to the original EIR (10%), but now applied to the 60 PLN basis. Consequently, after one year accrued interest will equal 6 PLN and the net book value of the loan will equal to 66 PLN (60 + 6), which is the amount the bank estimates to obtain from the collateral realization.

Impairment under IAS 39 – example

- 16 - © Deloitte 2007

1) 100 2) 10 10 2)4) 10 10 4)

5) 46 6)

50 3) 4 5) 3) 50

1) Loan extension2) Contractual interest accrual for first year (before impairment)3) Creation of provision4) Contractual interest accrual for second year5) Interest income adjustment to impairment interest level6) Interest income for second year according to IFRS (impairment interest)

Provision calculation: Impairment interest:Principal 100 Contractual interest 10Accrued interest 10 Loan net book value 60Book value of the loan 110 Interest rate 10%Minus: discounted recovery -60 Impairment interest 6Provision 50 Interest adjustment 4

Loan principal Accrued interest Interest income (P&L)

Provision costs (P&L)ProvisionInterest adjustment

to imp. int. level

Impairment under IAS 39 – example

- 17 - © Deloitte 2007

Introduction1

3 Experience from implementation projects

2 Impairment methodology

4 Impairment methodology

- 18 - © Deloitte 2007

Methodology stream:Analysis of currently used by a bank methodology for assessing and measuring loan provisions in the light of IFRS provisioning requirements.Verification of sufficiency of data collected by the bank in the light of IFRS provisioning requirements.Advisory on developing impairment methodology in accordance with IFRS:

identification of product for which IFRS provisioning methodology should be developed,segmentation of portfolio into exposures for which impairment will be assessed on individual and collective basis,methods for creating homogeneous portfolios (for collective impairment analysis),defining loss events (objective evidence of impairment losses),methods for estimating future cash flows form principal, interest, and collateral for impaired exposures, PD, LGD and EAD parameter calculation / estimation methods,methods for impairment loss calculation and presentation including application of effective interest rate,rules for recording impairment losses in the Bank’s books, balance sheet and profit and loss account.

Methodology developed in the steps described above considers data and credit process limitations. However, we define necessary data requirements i.e. data that needs to be collected in the future in order to satisfy IFRS impairment requirements.

Standard scope of impairment projects – methodology stream

- 19 - © Deloitte 2007

IT stream:

Implementation of Impairment Tool supporting identification, assessment and measurement of impairment losses and IRR Tool supporting effective interest rate calculation and EIR adjustments or alternatively

Supporting internal or external development, implementation, and acceptance test of IT tool supporting impairment identification and measurement of impairment losses and effective interest rate.

Standard scope of impairment projects – IT stream

- 20 - © Deloitte 2007

Special cases

During implementation there is a need to cover special cases for which IAS 39 does not provide direct treatment, for example:

Mismatch between currency of loan (e.g. EUR) and collateral value which is usually assessed in local currency (e.g. RON). Should it be converted using:

spot rate or

forward rate?

Which interest rate use for discounting of recoveries from a loan after troubled restructuring? IAS 39 requires to use the rate prior restructuring. But what to do if, for example:

the rate prior restructuring was floating?

the currency of the loan has changed?

Impairment interest on exposures for which IBNR provision has been created.

- 21 - © Deloitte 2007

Major implementation obstacles

The major obstacle is quality of data:

Lack or insufficient quality of data on historical recoveries, default rates (PD), credit conversion factor (CCF) – extended use of expert judgement.

Too small homogenous portfolios – impossible to apply collective approach.

Lack or insufficient quality of data on current collaterals e.g.:

difficulties in linking collaterals with loans,

inaccurate collateral value entered in the systems,

Difficulties in linking interest rate used for discounting with appropriate loan.

However, there are other problems as well:

Changing mindset of staff involved in assessing individual impairment (e.g. sale staff - credit officers responsible for loans).

Interest income after impairment – adjusting contractual interest calculated by core banking systems – conceptual (e.g. treatment of repayments and other events) and technical (infrastructure) problems.

Lack of data often enforces need for simplifications to methodology.

- 22 - © Deloitte 2007

Assistance in calculating provisions at opening balance and any other dates.

On going consultations on impairment methodology after completing the project.

Organization of the impairment measurement process.

Preparation of internal procedures.

Data mining – gathering data on historical default rates (PD), recoveries (LGD), collaterals etc.

Data cleansing e.g. collateral data.

Implementation of validation procedures to assure high quality of data.

Implementing work flow for bad debt collection department.

Modifying KPI affected by impairment (provisions and interest after impairment).

Modifying budgeting and controlling processes affected by impairment (provisions and interest after impairment).

Additional scope of impairment projects

- 23 - © Deloitte 2007

Polish Banking Supervision Commission (KNB) aimed at developing recommendation (Recommendation R) that would present best practices in implementing impairment requirements under IFRSs, including:

defining roles and responsibilities of bank’s Supervisory Board and Management Board in the impairment process e.g. establishing the process of impairment identification and measurement and internal controls for this process,

defining elements of internal impairment identification and measurement rules and procedures,

defining impairment methodology, including use of expert judgement, valuation models, rules for creating homogenous portfolios, valuation of collaterals, validation tests, collecting historical data,

defining roles of internal audit in relation to impairment process,

explaining IAS 39 impairment concepts especially in the areas where IAS 39 does not provide direct guidance.

The Recommendation is not a binding law – approaches other than those presented in the Recommendation are also acceptable (provided they are in accordance with IFRSs).

Experience from a working group developing National Bank of Poland impairment recommendations

- 24 - © Deloitte 2007

Introduction1

3 Experience from implementation projects

2 Impairment methodology

4 Impairment Tool

- 25 - © Deloitte 2007

The Tool allows to maintain the existing process related to transactional systems operation and processing, that are currently implemented in a bank (IFRS requirements do not override the need to obtain data using the existing methods, e.g. tax, legal, business line performance, client communication).No significant changes to the bank’s reporting process are required: the existing reporting systems and the organization / reconciliation process still apply, but with a new (not critical) component added.The output data may be delivered on various levels to seamlessly integrate with the current bank’s environment:

analytical data extracts required for reporting,stand alone GL as an adjustment to local GAAP GL, ordirect adjustments accounted in the bank’s GL by using the existing interfaces.

The solution is focused on events, which have impact on IFRS valuation (all unadjusted values remain only in the core systems).Effective implementation, fastest processing (less data), transparent and verifiable, integrated into existing architecture.

IFRS adjustments

GL Core system (local GAAP)

IFRS Tool(GL adjustments)

„Nominal values”

10

8

10

BBB

10

8

10

AAA

6

4

6

BBB

6

4

6

AAA

IFRS G/L

6

4

6

BBB

6

4

6

AAA

10

8

10

10

8

10

Impairment Tool implements a transparent and real life proven concept of IFRS adjustments:

Impairment Tool

- 26 - © Deloitte 2007

Impairment Tool – the core functionalityCustomizable / asynchronous processing

Data extraction and loading processes (ETL) for exposures, collateral and contract/client data are implemented on the data layer.The system enables definition of unique processing calendar based on which of the dedicated EOD, EOM, EOY processes are performed.Build in functionality for systematic management of results of all calculation processes and their approval.Historical application results are backed up for reporting and audit.Automatic notification via e-mail, bounded to the chosen events.

Exposure managementCovers broad range of Bank’s assets (installment loans, overdrafts and revolvings, credit card receivables, interbank transactions) with unified set of data for all B/S products and all off-B/Sproducts.Multi-level data access: the system enables to operate on the level of elementary balances (principal, interest, off-balance) as well as on a single transaction or a group of transactions constituting one client’s exposure. Drill down to individual transaction and its risk parameters (e.g. provision) both for individual and portfolio assessment.Dedicated user interfaces for gathering supplementary data, to be used directly by the operational units i.e. defining recovery rates and cash flow schedules for principal, interest, collateral and off-balance sheet exposures.Collateral management module enabling collecting actual recoveries to build own database of historical recoveries.Automatic default identification for the portfolio-managed exposures, and manual for exposures assessed individually (loss events on the transaction or client level).

- 27 - © Deloitte 2007

Impairment Tool – the core functionality

Calculation methodsDifferent methods of impairment calculation enabling convergence with the approach used in credit risk management (expected cash flows –individual method, transition matrices – portfolio method based on risk pools, optional direct input of risk parameters: PD, LGD).Portfolio management basing on characteristics of the chosen transaction and on the expert modelparameterization.Analysis of scenarios and approval of parameters for calculation (PD, RI).Collection of historical recovery data and calculation of historical LGDs.Easily modifiable / extendable (on implementation level) event handling mechanisms for EOD processing.Preparation of reports for the accounting purposes.

Built in GL functionalityMaintaining history of individual postings, triggers (events) for postings, account balances on transaction level.Revaluation mechanisms for foreign currency exposures and other “residential” processes EOM / EOY on single transaction / account level.Possibility of exporting account balances in pre-defined structure (file/DB)Flexible parameterization (on implementation level) of accounting schemes for each defined eventRecognition of interest income on impairedloans and adjustments to bring interest income to the level of impairment interest.

- 28 - © Deloitte 2007

System structure and components

The application is centrally-maintained and is available for the end users via an ergonomic WWW interface (thin client).

The main menu of the system consists of the following sections:

Administration (available for the technical administrator) – enables the administration of users’accounts and changes to the databases.

Exposures (available for the business users) – for the purpose of the individual assessment.

Calculation (available for the business administrator) – for the purpose of the calculation of provision for the individual assessment.

Calculation retail (available for the business administrator) – for the purpose of the calculation of collective provision.

Parameters – used to define parameters necessary for provision calculation.

Work out process (collection process) – allows gathering actual (historical) data on recoveries.

Reports – for the purpose of the report generation.

Requests – for the changes of the user rights.

- 29 - © Deloitte 2007

Individual exposures

Suitable user interface enables user to search (including multiple criteria search), browse and review of the Bank’s exposures. Available exposures may be limited based on users assigned rights.

Exposures matching search criteria listed together with major transaction details (e.gdefault and default acceptance status)

For the chosen exposure the user chooses the loss-event from the predefined list (causing appearance of default flag).

Default has to be approved by supervisor.

Changes made by the user are stored for supporting of audit trail.

- 30 - © Deloitte 2007

Individual provisions – loss events and recoveries

When the user marks the exposure with a default flag, all other exposures of the given client are automatically marked with the default flag.

Classification and „default-flagging” of exposure (including approval process) takes place automatically for the exposures that are portfolio-managed and manually for the exposures assessed individually.For the exposures that are individually assessed loss-events that can be automatically derived from transaction systems (e.g. days overdue) are also processed automatically.For defaulted transaction the user:

Estimate estimated recoveries from principal (repayments expected from the borrower), supported with presented contractual repayment schedule.Estimate recoveries from interest (estimated repayments expected from the borrower).

- 31 - © Deloitte 2007

Individual provisions –off-balance sheet exposures and collaterals

In case of off-balance sheet exposure (e.g. unused credit limit for a loan or issued guarantee) the user, additionally to recovery assessment, assess (or use predefined) CCF parameter (credit conversion factor).

In case of collateralized exposures the system provides details of collaterals and the user is required to estimate recovery from those collaterals (amount and timing).

After all recovery data is entered the system presents transaction and provision summary based on the provided recoveries.

In case of estimating recoveries from tangible assets collaterals (e.g. property, plant and equipment, inventories) the system provides functionality allowing for additional verification of estimated recoveries by experts (bank’s valuators) in particular type of collateral.

- 32 - © Deloitte 2007

Collective impairment – portfolio parameterization

In collective impairment approach the system enables definition of new portfolios for the calculation of PD and RI, basing on chosen transaction’s characteristics (product type, client rating etc.)

Each available product can be assigned to a chosen portfolio.

Definition of particular portfolios is available for the system administrator.

For each type of product additional parameters can be defined to be used in the calculation (CCF, type of the discount rate).

- 33 - © Deloitte 2007

Collective impairment – collateral parameterization

For each collateral category the user defines recovery rates and duration of collection process (used for LGD calculation based on discounted collateral value).

The system enables collecting historical data on collateral recoveries and collection costs, on which recovery rates would be calculated by the system.

- 34 - © Deloitte 2007

Collective impairment – matrixes calculation

Calculation of provision is preceded by the configuration and calculation of transition matrices.

Results of calculation of particular transition matrices performed by the system are available for preview and comparison with each other.

- 35 - © Deloitte 2007

Collective impairment – provisions calculation

Calculation of provision is based on given computational set of data

All results of provision calculation are available in the system. The last accepted provision could be also seen in the detailed view for each separate transaction.

Before generating final report on provisions an approval is required

- 36 - © Deloitte 2007

Recording of historical recoveries and collection costs

The system includes functionality of collecting actual recoveries and collection costs and linking them to particular collateral, customer and exposures. Hence, the system may produce analysis of actual (historical) recoveries and collection costs in various breakdowns e.g. by collateral type, customer type etc.

This functionality enables a bank to build its own database of historical recoveries.

Data collected on actual (historical) recoveries and collection costs are available in various reports.

- 37 - © Deloitte 2007

Interest income after impairment – GL module

The system generates predefined postings based on defined at implementation level configuration of events, measures and account definitions.

The system maintains history of individual postings, triggers (events) for postings, account balances on transaction level.

It uses in-built revaluation mechanisms for foreign currency exposures and other “residential”processes EOM / EOY on single transaction / account level.

Enables exporting account balances in pre-defined structure (file/DB)

- 38 - © Deloitte 2007

Interest income after impairment – GL module

In-built functionality enables the user to input directly information on account numbers (when system is unable to extract it from source data)

The system enables to manually trigger certain events both on global level (EOY) and transaction level (stop).

- 39 - © Deloitte 2007

Administration

The system enables user and privileges management, stores users e-mail addresses and allows automatic notification via e-mail.

During processing and computations the system presents the progress and status of computations.

- 40 - © Deloitte 2007

Additional features

IntegrationWeb user interface can be simply adjusted to different look and feel or translated to a local language (Custom Style Definition and resource bounding are used). Currently Polish version is available due to the clients requirements, an English version is planned.

Application outputs are available in both an extract file (text, Excel), relational data set, or MQ messages.

Either the internal ETL procedures or an external ETL tool may be used to integrate with the data sources.

SecurityImpairment Tool takes advantage of the company global users repository (e.g. LDAP) to align users access with global privileges.

User’s roles are used to define access to the Tool functionality (specific modules and specific functions in modules). Restrictions on transactional data scope might also be implemented.

Security functions are performed at the application server layer and are configured by a system administrator. That allows to define user groups (e.g. managers, operators, administrators) and then to assign users to those groups.

The Tool record the users’ activities in a data base log, providing an audit trail option.

PerformanceThe Tool can be deployed on various system configurations scaling their performance to the provided IT infrastructure.

The Tool implements a multi-tier architecture: each tier can be run on dedicated server in order to achieve the required performance

- 41 - © Deloitte 2007

Impairment assessment processes

(np. Główny cykl obliczeniowy

( etap zatwierdzenia miesiąca w cyklu miesięcznym)

Niezależnie odgłównego cyklu

obliczeń

Automatically (e.g. daily)

According to the working cycle of a Branch, at least as

often as main calculation cycle

Regardless of the main calculation

cycle

Main calculation cycle (monthly cycle –other frequency is possible)

Source data

loading

Automatic default classification

proposal (past due status or “lost” NB

category)

Classification as default (on a

proposal basis)

Recoveries for default

exposures

Verification and confirmation of

default classification

and recoveries calculation

Verification of recoveries

from collaterals for

exposures classified as

defaults

OK ?

NIE

OK ?

NO

YES

YESNO

Calculation parameters and

data control

Results archiving, start

of the new month

Confirmation of the month

Modification of default

classification, recoveries, parameters

Provisions calculation and results review

Freeze the changes in

recoveries till the end of the month

- 42 - © Deloitte 2007

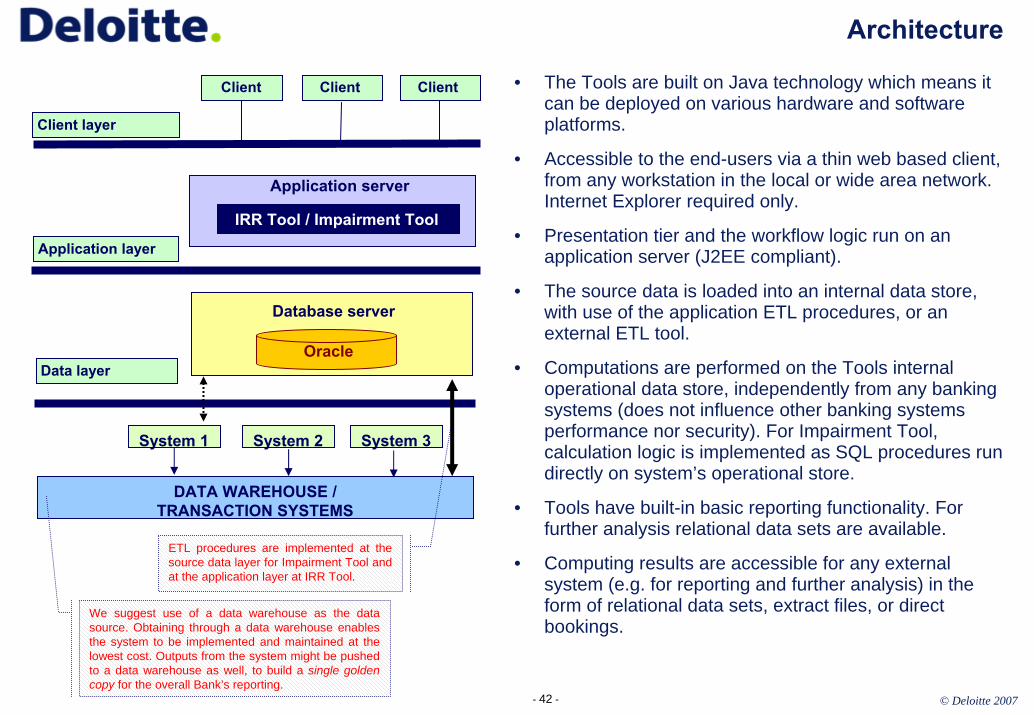

Architecture

• The Tools are built on Java technology which means it can be deployed on various hardware and software platforms.

• Accessible to the end-users via a thin web based client, from any workstation in the local or wide area network. Internet Explorer required only.

• Presentation tier and the workflow logic run on an application server (J2EE compliant).

• The source data is loaded into an internal data store, with use of the application ETL procedures, or an external ETL tool.

• Computations are performed on the Tools internal operational data store, independently from any banking systems (does not influence other banking systems performance nor security). For Impairment Tool, calculation logic is implemented as SQL procedures run directly on system’s operational store.

• Tools have built-in basic reporting functionality. For further analysis relational data sets are available.

• Computing results are accessible for any external system (e.g. for reporting and further analysis) in the form of relational data sets, extract files, or direct bookings.

Client layer

Application layer

Data layer

Application server

Database server

IRR Tool / Impairment Tool

DATA WAREHOUSE /TRANSACTION SYSTEMS

System 1 System 2 System 3

We suggest use of a data warehouse as the data source. Obtaining through a data warehouse enables the system to be implemented and maintained at the lowest cost. Outputs from the system might be pushed to a data warehouse as well, to build a single golden copy for the overall Bank’s reporting.

Oracle

Client Client Client

ETL procedures are implemented at the source data layer for Impairment Tool and at the application layer at IRR Tool.

- 43 - © Deloitte 2007

Logical architecture

System has a clear-cut layered structure that enables effective functional customization.

Adjusting the system to custom requirements might be done effectively due to system layering.

It is possible to change one aspect of the system while others are left untouched.

It is possible to adjust the system to an alternative impairment calculation methodology.

The computation process is run asynchronously, i.e. other functions are still available to the users while daily/monthly computations are being performed.

CALCULATION OF PROVISIONS

SOURCE DATA LOADING

MODEL PARAMETRISATION

PD MODULE IMPAIRMENT AND REPORTS

PORTFOLIO DEFINITION

PREPARATION OF CALCULATION DATA

AUTOMATIC PROCESSES

MANUAL DATA COMPLETION

PROVISIONS CALCULATIONS IMPAIRMENT INTEREST RATE CALCULATIONS

REPORTING AND DATA EXPORT

REPORTS DATA INTEGRATION

INTERFACE

SCENARIO ANALYSIS

COLLATERAL DATA MANAGEMENT

COLLATERAL RECOVERY

DATA COLLECTION

BAD DEBT RECOVERY

DATA COLLECTION

LGD MODULE

DATA LOADING FROM EXTERNAL DATA STORE

LOSS-EVENTS DICTIONARY

DATA SETS

RESULT ARCHIVING

COLLATERAL RECOVERY

VERIFICATION

MANUAL VERIFICATION

- 44 - © Deloitte 2007

Deloitteul. Piekna 1800-549 WarszawaPolandtel. +48 22 511 0077fax. +48 22 511 0813

For any questions contact:

Adam Kolaczyk [email protected]

Deloitte4-8 Titulescu Road, 3rd floor, sector 1, Bucharest, 011141 RomaniaTel. +40 21 222 1661Fax: +40 21 319 5100

For any questions please contact:

Natalia Cierna [email protected]