Impact of Regulation on Banking and the Economy - … · 2013-02-12 · Impact of Regulation on...

22

Impact of Regulation on Banking Impact of Regulation on Banking and the Economy and the Economy 2 nd FIN-FSA Conference on EU Regulation and Supervision "Banking and Supervision under Transformation" Helsinki 12 February 2012 Helsinki 12 February 2012 John Berrigan European Commission, DG Economic and Financial Affairs

-

Upload

nguyendiep -

Category

Documents

-

view

213 -

download

0

Transcript of Impact of Regulation on Banking and the Economy - … · 2013-02-12 · Impact of Regulation on...

Impact of Regulation on Banking Impact of Regulation on Banking and the Economy and the Economy

2nd FIN-FSA Conference on EU Regulation and Supervision"Banking and Supervision under Transformation"

Helsinki 12 February 2012Helsinki 12 February 2012

John BerriganEuropean Commission, DG Economic and

Financial Affairs

OutlineOutline

Changing focus of EU regulation in response to financial crisis Changing focus of EU regulation in response to financial crisis

Implementation of regulation in post-crisis environment Implementation of regulation in post crisis environment

Moving forward with the regulatory agenda

Ch i f f EU l tiCh i f f EU l tiChanging focus of EU regulationChanging focus of EU regulation

Crisis has altered perceptions Crisis has altered perceptions of of global financeglobal financep pp p gg

• From driver of economic growth to potential source of instability/contagion

• From presumed efficient markets to herd behaviour/sub-optimal equilibria

• From provider of low-cost credit to inconsistent enforcer of policy disciplineo p o de o o cost c ed t to co s ste t e o ce o po cy d sc p e

• From generator of value-added to potential fiscal burden on taxpayer

• From technical obscurity to political limelight

Light-touch regulation replaced by more intrusive approach

Focus of EU Bank Regulation has changed…Focus of EU Bank Regulation has changed…

Pre-crisis:

• Financial integration a key element of Single Market Programme welfare gains via scale/scope economies, competition and choice

I EMU fi i l k d l l f h k b b• In EMU, financial markets expected to play role of shock absorber enhanced economic adjustment via cross-border financial flows

• Regulatory roadmap - FSAP (1999) – focused heavily on efficiency and Regulatory roadmap FSAP (1999) focused heavily on efficiency and competition but less on stability aspects

• Imbalance between pace of market integration and regulatory/supervisory arrangements for managing crises arrangements for managing crises

…as stability has moved to top of policy agenda…as stability has moved to top of policy agenday p p y gy p p y g

Post-crisis:

• EU adopted new regulatory action plan 2008 in line with G20 commitments:

o More solid financial institutions (CRD III/CRD IV/CRR, Solvency II, AIFMD, CRAs)

o Efficient, secure and transparent financial markets (EMIR, MiFID, MAD/MAR,CSD, Securities Law Directive, short selling)

o Consumer protection and confidence: (DGS Mortgage credit SEPA PRIPS UCITS)o Consumer protection and confidence: (DGS, Mortgage credit, SEPA, PRIPS, UCITS)

o Framework for Bank Recovery and Resolution

Assessing regulatory impact Assessing regulatory impact g g y pg g y p

Source: Study by ZEW for European Parliament

Assessing economic impact (1) Assessing economic impact (1) g p ( )g p ( )

• Regulatory agenda implies costs and benefits for the economy

o Costs mainly via lower value-added (first round) and less financing of activity (second round)

o Benefits via increased confidence and greater systemic resilience

• Essential to find appropriate balance between financial stability and economic growth

• Each legislative proposal from Commission subject to thorough impact assessment

• Cumulative impact assessment also – but a greater challenge

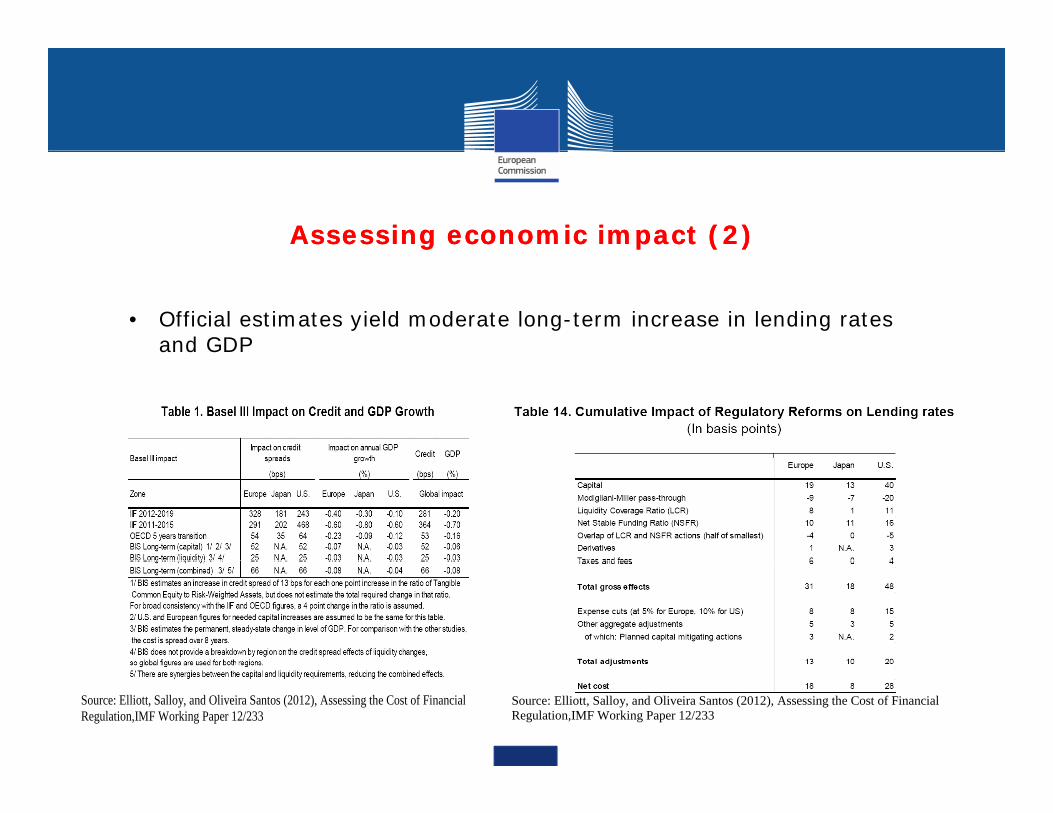

Assessing economic impact (2)Assessing economic impact (2)

• Official estimates yield moderate long-term increase in lending rates and GDP

Source: Elliott, Salloy, and Oliveira Santos (2012), Assessing the Cost of Financial Regulation,IMF Working Paper 12/233

Source: Elliott, Salloy, and Oliveira Santos (2012), Assessing the Cost of Financial Regulation,IMF Working Paper 12/233

Assessing economic impact (3) Assessing economic impact (3) g p ( )g p ( )

• Commission has undertaken internal cumulative impact assessment of costs and benefits of 2008 regulatory action plan

• Several considerations in cumulative approach:o Costs and benefits should be assessedo Costs concentrated, benefits more diffuseo Must take a general equilibrium approach (Quest III) o Model limitations imply need for some qualitative assessment

• Conservative approach adopted:ll l d b f ll l d ho All regulatory measures assumed to be fully implemented, i.e. no phasing

o Modigliani-Miller theorem assumed to hold at 50%o Pre-regulation mark-ups assumed unchangedo Capital requirements assumed at maximum level

• Initial results suggest benefits offset costs in terms of GDP

Assessing economic impact (4) Assessing economic impact (4) g p ( )g p ( )

• Political tolerance for economic cost of regulation has changed

• No longer "It's the economy, stupid" but "Primat der Politik über die Finanzmärkte" (Angela Merkel, 2010)

• Fiscal cost of crisis has sharpened political focus on financial sector e g • Fiscal cost of crisis has sharpened political focus on financial sector, e.g.

Insistence on fair contribution of financial sector to costs of crisis: financial transaction tax, financial stability levies, bail-in procedures

Limits on short-selling to address perception of speculation in sovereign debt markets

Li it ti t i l t f b k Limits on compensation to assure social acceptance of bank rescue measures

Implementation challenges in Implementation challenges in Implementation challenges in Implementation challenges in postpost--crisis environmentcrisis environment

Low economic growthLow economic growthgg

• Large financial crises typically followed by extended period of risk aversion and sub-par growth

• In these conditions, transition to steady-state regulatory regime must be carefully managed to avoid near-term overshooting

• Tensions typically managed via extended phasing-in periods, e.g. capital/liquidity requirements under Basel III

• But, phasing-in not only discussion between regulator and regulated –investors also have a say

Weakness in credit supplyWeakness in credit supplypp ypp y

Weak profitability and deleveraging needs in financial sector may impede credit supply to the real economy

Regulation must take credit supply considerations into account…

… but decisive balance sheet repair essential to restore properly functioning credit channel

Must avoid risk of “Japanese experience” of l d dlost decade

Evidence suggests that SMEs most at risk of credit constraints, but interpretation of data not clear cutnot clear-cut

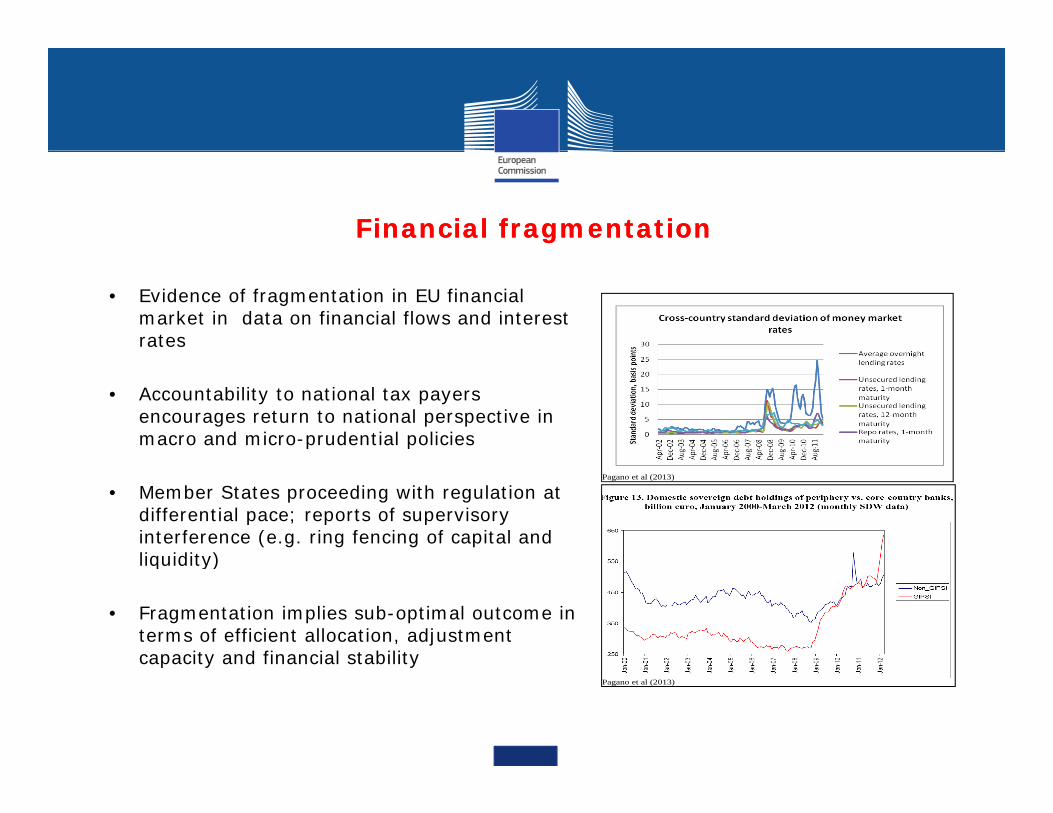

Financial fragmentationFinancial fragmentation

• Evidence of fragmentation in EU financial market in data on financial flows and interest rates

• Accountability to national tax payers encourages return to national perspective in macro and micro-prudential policies

• Member States proceeding with regulation at differential pace; reports of supervisory interference (e.g. ring fencing of capital and liquidity)

Pagano et al (2013)

liquidity)

• Fragmentation implies sub-optimal outcome in terms of efficient allocation, adjustment capacity and financial stabilitycapacity and financial stability

Pagano et al (2013)

Moving forwardMoving forwardMoving forwardMoving forward

Learning by doingLearning by doingg y gg y g

• No long-term trade-off between financial stability and economic growth…g y g

• … but, possible tensions in transition to steady-state regulatory regime

• Quantitative impact assessments imply net benefit from stability-oriented regulation….

• but limitations of model-based estimations must be acknowledged• … but, limitations of model based estimations must be acknowledged

• Need to monitor implementation and re-calibrate, as warranted

Refocusing on growthRefocusing on growthg gg g

• Stability-oriented regulation progressively in place and focus returning to i theconomic growth

• Forthcoming Commission Green Paper on long-term investment on how to channel savings to productive investmentg p

• In focusing on growth, regulatory agenda must, inter alia, consider measures to:

o Expand short-term securities marketso Restore securitisation marketso Develop project bonds

Foster public private co investmento Foster public-private co-investment

Possibility of structural interventions Possibility of structural interventions yy

• EU regulatory agenda designed to foster "organic" change in system…g y g g g g y

• … but, regulation could also imply more direct reform of structures

• Liikanen Report has extended debate on structural reform to the EU

• Commission to consider Liikanen recommendations, based on through impact assessment assessment

• Urgent need for coherent EU response, as MS move ahead independently

Completing EU financial stability architectureCompleting EU financial stability architecturep g yp g y

• EU financial regulation not sufficient to assure systemic stabilityg y y

• Need to reinforce the supervisory framework also

• Continue evolution by building on the Lamfalussy and De Laroisière reforms

• Banking Union (SSM, SRM, [DGS], ESM+) to deepen EMU but also validate cross-border market in financial servicescross border market in financial services

• SSM already underway, Commission proposal on SRM by June 2012, political/technical discussion of ESM+ in parallel

ConclusionsConclusions

• Regulatory agenda of last four years focused on reinforcing stability aspects

• Impact assessments confirm no long-term trade-off between stability and growth

N d t th t iti t t d t t l t i id i d • Need to manage the transition to steady state regulatory regime, amid period of post-crisis financial repair

• Focus of regulation now turning towards enhancing long-term investment and g g g ggrowth

• In parallel, rapid progress required in reinforcing EU supervisory arrangements

Thank you for your attentionThank you for your attentionThank you for your attentionThank you for your attention

John BerriganEuropean Commission, DG Economic and

Financial Affairs