Impact of Bonus Issue on Market Price

111

Impact of Bonus Issue on Market Price Research Extract Bonus shares, as the name suggests, are issued free to existing stockholders in proportion to the number of stocks held by them. It is essentially a book transfer by which a sum of money equal to the value of the bonus shares is transferred from the reserves to the equity capital in the company’s books of accounts Companies issue shares in lieu of consideration. The consideration may be either in the form of cash or kind. Bonus shares are issued to the existing shareholders without payment of any consideration, either in cash or kind. Bonus shares are issued by conversion of the reserves and surplus of the company into shares. Bonus shares can be issued only by companies which have accumulated large free reserves i.e. reserves not set apart for any specific purpose and which can be distributed as dividend. However, bonus shares can be issued out of balance in the share premium account. Stock split: A stock split is a corporate action that increases the number of the corporation's outstanding shares by dividing each share, which in turn diminishes its price. The stock's market capitalization, however, remains the same, just like the value of the $100 bill does not change if it is exchanged for two $50s. For example, with a 2-for-1 stock split, each stockholder receives an additional share for each share held, but the value of each share is reduced by half: two shares now equal the original value of one share before the split. The Oxford College Of Business Management Page 1

Transcript of Impact of Bonus Issue on Market Price

Impact of Bonus Issue on Market Price

Research Extract

Bonus shares, as the name suggests, are issued free to existing stockholders in proportion to the

number of stocks held by them. It is essentially a book transfer by which a sum of money equal

to the value of the bonus shares is transferred from the reserves to the equity capital in the

company’s books of accounts

Companies issue shares in lieu of consideration. The consideration may be either in the form of cash or

kind. Bonus shares are issued to the existing shareholders without payment of any consideration, either in

cash or kind. Bonus shares are issued by conversion of the reserves and surplus of the company into

shares. Bonus shares can be issued only by companies which have accumulated large free reserves i.e.

reserves not set apart for any specific purpose and which can be distributed as dividend. However, bonus

shares can be issued out of balance in the share premium account.

Stock split: A stock split is a corporate action that increases the number of the corporation's

outstanding shares by dividing each share, which in turn diminishes its price. The stock's market

capitalization, however, remains the same, just like the value of the $100 bill does not change if

it is exchanged for two $50s. For example, with a 2-for-1 stock split, each stockholder receives

an additional share for each share held, but the value of each share is reduced by half: two shares

now equal the original value of one share before the split.

The prices of 5 company’s share that is 15 days before the issue of bonus share and 15 days after

the issue of bonus share were taken into consideration. The companies are Reliance Industry,

Jindal Steel, TCS, Anu’s Laboratories, Falcon Tyres.

We can notice that in some cases prices rise much before the event date, Where the information

announced on the event date do not impact the market in many cases .this is because of Leakage

of information

In the case of other companies the share price is increasing after the bonus issue because of

proper issue and good will.

The Oxford College Of Business Management Page 1

Impact of Bonus Issue on Market Price

INTRODUCTION

Over the years the relationship between bonus issues and stock prices has been the subject of

much empirical discussion within the finance literature. Bonus issues increase the number of

equity stocks outstanding but have no effect on stockholder’s proportional ownership of stocks.

The bonus issue date is known well in advance and therefore should contain no new information.

But one should not expect any significant price reaction on bonus issue announcement.

However empirical studies of bonus issues and stock dividends have documented a statistically

significant market price reaction. It is, therefore, a matter of concern that firms announcing

bonus issues experience rise in their stock prices on an average supporting semi-strong form

Efficient Market Hypothesis (EMH). Generally, the investigation of semi-strong form market

efficiency has been limited to the study of well-developed stock markets.

The aim is to examine the stock price reaction to information release of bonus issues with a view

of examining whether the Indian stock market is semi-strong efficient or not. The event study

methodology has been used to contribute further evidence on the efficiency characteristics of the

Indian stock market.

Bonus Share

Companies issue shares in lieu of consideration. The consideration may be either in the form of cash or

kind. Bonus shares are issued to the existing shareholders without payment of any consideration, either in

cash or kind. Bonus shares are issued by conversion of the reserves and surplus of the company into

shares. Bonus shares can be issued only by companies which have accumulated large free reserves i.e.

reserves not set apart for any specific purpose and which can be distributed as dividend. However, bonus

shares can be issued out of balance in the share premium account.

For some years now, the issue of bonus equity shares has been a common phenomenon on the

Indian bourses. However, one reads about other types of bonuses being issued by companies to

shareholders. While some issue bonus dividends, while others proposes to issue bonus preference

shares. The big question: what will be the tax treatment of the different types of bonuses, and

which is more beneficial?

The Oxford College Of Business Management Page 2

Impact of Bonus Issue on Market Price

Advantages of issuing Bonus Shares

1. It bridges the gap between capital and fixed assets

2. Increases the market price of its shares

3. Creates confidence for the investors / shareholders in the company

4. Good market reputation

5. Increases Liquidity of Shares.

Disadvantages

1. Shares are issued without any actual money coming in.

2. Leads to reduction in Earning per Share

3. There are cost implications such as stamp duty, printing & stationery, etc

4. Reduces accumulated profits earned in past years.

Things to remember before considering Bonus Issue

1. Bonus shares cannot be issued if the company has come out with any public / rights issue in

the past 12 months.

2. Bonus shares cannot be issued in lieu of Dividend.

3. Bonus shares can be issued only out of free reserves (i.e. reserves not set apart for any specific

purpose) built out of the genuine profits or share premium collected in cash only.

4. Bonus shares cannot be issued out of the reserves created by revaluation of fixed assets.

5. If the existing shares are partly paid up, the company cannot issue Bonus Shares. It will be

appropriate to first make the shares fully paid up before issuing Bonus Shares.

6. It should be ensured that the company has not defaulted in payment of interest or principal in

respect of fixed deposits and interest on existing debentures or principal on redemption thereof

and

7. It should be ensured that the company has sufficient reason to believe that it has not defaulted

in respect of the payment of statutory dues of the employees such as contribution to provident

fund, gratuity, bonus etc.

The Oxford College Of Business Management Page 3

Impact of Bonus Issue on Market Price

8. If the company has already issued either fully convertible debentures or partly convertible

debentures than in that case the company is required to extend similar benefits to such holders of

securities through reservation of shares in proportion to their holding or in proportion to such

convertible part. The Bonus Shares so reserved may be allotted to such holders at the time of

conversion.

9. It should be checked whether Articles of Association contains the provision of capitalization of

reserves. If no such provisions are contained steps should be taken by altering the Articles of

Association by the consent of the members of the Company.

10. It should be checked whether the post bonus capital is within the limits of authorized share

capital. If it is not so, steps should be taken to increase the authorized share capital by amending

memorandum and articles of association.

11. It is very important for a company to implement the bonus proposal within a period of six

months from the date of approval at the meeting of the Board of Directors. The company has no

option to change the decision.

12. All the shares so issued by way of bonus will rank pari-passu with the existing shares. The

company cannot create any other rights for the bonus shares.

What happens when bonus shares are issued?

It does not mean they are credited to your de-mat account immediately. You need to know what

you can and cannot do with your portfolio during this interval. Investors have been flooded with

bonus issues from a lot of companies and this has made most of them quite happy. One must

know that the whole process involves knowing that there could be a time difference from the

moment the price is adjusted in the secondary market and when the bonus shares actually come

into the investor's account. This can also be better understood by looking at the procedural

aspects that can impact the way investors make their investment decisions. First, consider the

steps in the entire bonus process. The company announces a bonus ratio and will undertake

compliance with the necessary legal requirements to complete the process. Thus, for example,

where the bonus shares are issued in a ratio of 1: 1, it means that one share would be allotted for

The Oxford College Of Business Management Page 4

Impact of Bonus Issue on Market Price

Every share already held in the company. Similarly, a ratio of 2:1 would mean that two shares

are allotted for one existing share in the company. The record date is announced and the

investors wait for the specific date to get the required benefits. The record date is important

because holders of the shares on this particular day will be entitled to the bonus shares. There is

another date that has to be noted carefully by the investors, which is the date when the shares go

'ex bonus'. What happens is that on this day, the share prices adjust in the bonus ratio so that it

reflects the actual situation on the ground. The reason why the price reflects the situation on the

ground is that after the price is adjusted, investors will be ineligible for the actual bonus shares.

Often, there is a time when there might be a no-delivery period on the stock exchanges and due

to this; the ex-bonus date has to be noted carefully. Up to this stage, everything is fine as things

are in tune with the normal procedure that many investors understand but now comes a surprise

that many will not be prepared for. On the date the shares go ex-bonus, the price of the share

corrects in the market, so, for example, a share with a price of Rs 200 will become Rs 100 in the

case of a bonus issue in the ratio of 1: 1. Now, watch out for the time when the new shares are

credited to the account. Often, it takes quite some time for the shares to actually come into the

account. Assume that the shares come into the account after 15 days of the share price correction

for the issue. During this time interval, the shareholders find themselves in a peculiar situation

because they are stuck with a lesser portfolio value. Thus, if the portfolio value of scrip for an

investor was, say, Rs 1lakh, then till the time the new shares come into the account, it could

show as Rs 50,000 and there is little that the investor can do till the bonus shares are credited into

the account. This impacts the investors in different ways. The first is that the value of their

portfolio goes down temporarily without them doing anything. So, investors analyzing their

portfolio in the relevant time period need to keep this in mind. The second is that till the time the

new shares come into the account, there is nothing that the investor can do about trading in these

shares and hence, that part of the portfolio is not accessible for the intervening period. One has to

be very careful because selling shares without them being present in the de-mat account, can

cause problems for investors. Investors have only one way to tackle this issue and that is by

being aware of the situation so that they do not plan and implement transactions dealing with

The Oxford College Of Business Management Page 5

Impact of Bonus Issue on Market Price

such shares till they are credited to their accounts. It has to be remembered that the original

shares remain with the investor so that they can make use of these but plans for the new shares

will have to wait. The time period of the share transfer can also stretch to more than a couple of

weeks as has been seen in several well known issues and this also have to be taken into

consideration.

Do stock prices in an efficient market follow a random walk?

We can answer the question by looking at the meaning of efficient market and random walk.

Take Company X. If there is good information flow in the market, its stock price will reflect all

information that is publicly available. If the company, for instance, has bagged a contract from a

major client, the current price of the stock will reflect that information. We can then say that the

investors have "efficiently" priced the stock. Now extend this concept to the entire market. If

prices in the stock market reflect all available information on each company, we can say that the

market is "efficient".

When the stock price reflects all public and private information, we say that the market is strong

form efficient. If the stock price reflects only public information, we say that the market is either

weak form or semi-strong form efficient. So, how does efficient market help us in understanding

stock price movements? We know that information drives stock prices. It follows logically that

the change in stock price will be driven by the arrival of new information. But we do not know

when a new of set of information will arrive in the market. To use a financial parlance, we can

say that information arrival is a random process. If the arrival of new information itself is a

random process, the change in stock price should also follow a random process. So, we say that

stock price follows a random process or a random walk. Of course, the assumption is that

investors do not have access to inside information on the company. For investors who do, the

market may not be "efficient", and may not, hence, follow a random walk.

The Oxford College Of Business Management Page 6

Impact of Bonus Issue on Market Price

Semi Strong Form Efficiency

1. Share prices adjust instantaneously and in an unbiased fashion to publicly available new

information, so that no excess returns can be earned by trading on that information.

2. Semi-strong-form efficiency implies that Fundamental analysis techniques will not be able to

reliably produce excess returns.

3. To test for semi-strong-form efficiency, the adjustments to previously unknown news must be

of a reasonable size and must be instantaneous. To test for this, consistent upward or downward

adjustments after the initial change must be looked for. If there are any such adjustments it

would suggest that investors had interpreted the information in a biased fashion and hence in an

inefficient manner.

Event studies

The greatest amount of research in finance has been devoted to the effect of an announcement on

share price. These studies are known as .Event Studies. Initially event studies were undertaken to

examine whether markets were efficient, in particular, how fast the information was incorporated

in share price. For example, when a firm announces earnings will be much larger than expected,

will this be reflected in share price the same day or over the next week? Dozens of studies

confirmed that share prices reacted rapidly to announcements, and in expected ways where the

direction of the price change and the likely impact were clear. Consequently, many authors

accept that information is rapidly incorporated in share price and use event studies to determine

what information is reflected in price and, if its impact is unclear, to determine whether the

announcement is good or bad news

Conducting Event Studies

1. Collect a sample of firms that had issued bonus.

2. Determine the precise day of the announcement and designate this day as zero

3. Define the period to be studied

4. For each of the firms in the sample, compute the returns on each of the days being studied

5. Compute the abnormal. Return’s for each of the days being studied for each firm in the sample

The Oxford College Of Business Management Page 7

Impact of Bonus Issue on Market Price

6. Compute for each day in the event period the average abnormal return for all the firms in the

sample

7. Often the individual day’s abnormal return is added together to compute the cumulative

abnormal return from the beginning of the period

8. Examine and discuss the results

Whether Bonus shares are miraculous?

Few things match the sheer joy of getting a fat bonus at work. That is what shareholders of a

good company feel when their company decides to throw a few shares (free of cost) in their

direction. Here’s explaining what bonus shares are all about and why investors like investing in

such companies. Free shares are given to you and are called bonus shares. Make money with

shares. They are additional shares issues given without any cost to existing shareholders. These

shares are issued in a certain proportion to the existing holding. So, a 2 for 1 bonus would mean

you get two additional shares -- free of cost -- for the one share you hold in the company. If you

hold 100 shares of a company and a 2:1 bonus offer is declared, you get 200 shares free. That

means your total holding of shares in that company will now be 300 instead of 100 at no cost to

you. Bonus shares are issued by cashing in on the free reserves of the company. The assets of a

company also consist of cash reserves. A company builds up its reserves by retaining part of its

profit over the years (the part that is not paid out as dividend). After a while, these free reserves

increase, and the company wanting to issue bonus shares converts part of the reserves into

capital.

What is the biggest benefit in issuing bonus shares is that its ads to the total number of shares in

the market. Say a company had 10 million shares. Now, with a bonus issue of 2:1, there will be

20 million shares issues. So now, there will be 30 million shares. This is referred to as a dilution

in equity. Now the earnings of the company will have to be divided by that many more shares.

Since the profits remain the same but the number of shares has increased, the EPS

(Earnings per Share = Net Profit/ Number of Shares) will decline. Theoretically, the stock price

should also decrease proportionately to the number of new shares. But, in reality, it may not

happen.

The Oxford College Of Business Management Page 8

Impact of Bonus Issue on Market Price

A bonus issue is a signal that the company is in a position to service its larger equity.

What it means is that the management would not have given these shares if it was not Confident

of being able to increase its profits and distribute dividends on all these shares in the future.

A bonus issue is taken as a sign of the good health of the company.

When a bonus issue is announced, the company also announces a record date for the issue. The

record date is the date on which the bonus takes effect, and shareholders on that date are entitled

to the bonus. After the announcement of the bonus but before the record date, the shares are

referred to as cum-bonus. After the record date, when the bonus has been given effect, the shares

become ex-bonus.

Issue of bonus shares

Bonus shares are issued by converting the reserves of the company into share capital. It is

nothing but capitalization of the reserves of the company. There are some conditions

Which need to be satisfied before issuing Bonus shares?

1) Bonus shares can be issued by a company only if the Articles of Association of the

Company authorizes a bonus issue. Where there is no provision in this regard in the

Articles, they must be amended by passing special resolution act at the general meeting of the

company.

2) It must be sanctioned by shareholders in general meeting on recommendations of BOD of

company.

3) Guidelines issue by SEBI must be complied with. Care must be taken that issue of bonus

shares does not lead to total share capital in excess of the authorized share capital. Otherwise, the

authorized capital must be increased by amending the capital clause of the Memorandum of

association. If the company has availed of any loan from the financial institutions, prior

permission is to be obtained from the institutions for issue of bonus shares. If the company is

listed on the stock exchange, the stock exchange must be informed of the decision of the board to

issue bonus shares immediately after the board meeting. Where the bonus shares are to be issued

to the non-resident members, prior consent of the Reserve Bank should be obtained.

The Oxford College Of Business Management Page 9

Impact of Bonus Issue on Market Price

Only fully paid up bonus share can be issued. Partly paid up bonus shares cannot be issued since

the shareholders become liable to pay the uncalled amount on those shares. It is important to note

here that Issue of bonus shares does not entail release of company’s assets. When bonus shares

are issued/credited as fully paid up out of capitalized accumulated profits, there is distribution of

capitalized accumulated profits but such distribution does not entail release of assets of the

company.

Issue of Bonus Shares by Public Sector Undertakings

It has come to the notice of the Government that a number of Central Government Public Sector

Undertakings are carrying substantial reserves in their balance sheets against a relatively small

paid up capital base. The question of the need for these enterprises to capitalize a portion of their

reserves by issuing Bonus Shares to the existing shareholders has been under consideration of the

Government. The issue of Bonus Shares helps in bringing about at proper balance between paid

up capital and accumulated reserves, elicit good public response to equity issues of the public

enterprises and helps in improving the market image of the company. Therefore, the Government

has decided that the public enterprises, which are carrying substantial reserves in comparison to

their paid up capital sold issue Bonus Shares to capitalize the reserves for which the certain

norms/conditions and criteria may be followed and fulfilled. There are some SEBI guidelines for

Bonus issue which are contained in Chapter XV of SEBI (Disclosure & Investor Protection)

Guidelines, 2000 which should be followed in deciding the correct proportion of reserves to be

capitalized by issuing Bonus Shares.

Private sector banks, whether listed or unlisted, can also issue bonus and rights shares without

prior approval from the Reserve Bank of India. Liberalizing the norms for issue and pricing of

shares by private sector banks, the RBI said that the bonus issue would be delinked from the

rights issue. However, central bank approval will be required for Initial Public Offerings (IPOs)

and preferential shares. These measures are seen as part of the RBI's attempt to confine it-self to

banking sector regulation and leave the capital market entirely to the SEBI. Under the guidelines,

private sector banks have also been given the freedom to price their subsequent issues once their

shares are listed on the stock exchanges. The issue price should be based on merchant bankers'

recommendation, the RBI has said. It means though RBI approval is not required but pricing

The Oxford College Of Business Management Page 10

Impact of Bonus Issue on Market Price

should be as per SEBI guidelines. The RBI, however, clarified that banks will have to meet

SEBI's requirements on issue of bonus shares. As per current regulations, private sector banks

whose shares are not listed on the stock exchange are required to obtain prior approval of the

RBI for issue of all types of shares such as public, preferential, rights or special allotment to

employees and bonus. Banks whose shares are listed on the stock exchanges need not seek prior

approval of the RBI for issue of shares except bonus shares, which was to be linked with rights

or public issues by all private sector banks.

Bonus Issue & SEBI Guidelines

The SEBI has issued guidelines for Bonus issue which are contained in Chapter XV of

SEBI( Disclosure & Investor Protection) Guidelines, 2000. A company issuing Bonus Shares

should ensure that the issue is in conformity with the guidelines for bonus issue laid down by

SEBI (Disclosure & Investor Protection) Guidelines, 2000. It is a detailed guideline which talks

about that the bonus issue has to be made out of free reserves, the reserves by revaluation should

not be capitalized. Bonus issue should not be made in lieu of dividend. There should be no

default in respect to fixed deposits. Bonus issue should be made within 6 month from date of

approval. This is not exhaustive but a lot of things are more in the guidelines regarding this.

The Balance-Sheet perspective

Rewarding by bonus shares means actual capitalization of reserves. Rewarding by split does not

mean anything from the balance-sheet perspective. It only increases the liquidity of stock by

reducing the paid-up capital. If the corporate comes up with further new share issues, by way of

private placement, the lower base of the paid-up capital and the higher percentage stake of new

investors can be attractive features if the capital has only been split. If expanded by bonus shares,

then, the existing shareholders would already have a higher stake vis-à-vis further new issue size.

Of course, the equity dilution will be lower in that case.

The Oxford College Of Business Management Page 11

Impact of Bonus Issue on Market Price

As per Section 55 of The Income-Tax Act, 1961 bonus shares entail zero costs while all the

purchase cost can be loaded on to the original shares. For bonus shares, the one-year holding

requirement for Long-Term Capital Asset (LTCA) eligibility starts from the allotment date of

bonus shares. In the case of split, the one-year eligibility is along with the original form of

capital, which is split. In other words, the one-year does not start on the split date but on the date

of purchase of original shares.

Capital v/s Revenue Expenditure: Fusion & Confusion

It is said that India has the most complex Income-tax legislation. The tax system bristles with

complexities and uncertainties. Consequent upon this there are problems of evasions and

avoidance. As such, let us probe two fiercely debated concepts of taxation laws i.e. Capital &

Revenue Expenditure which is very much relevant mentioning here. These two propositions are

rays with different wave-lengths but from the same source. While the former is susceptible to tax

being more extensive, the latter is advantageous to assess.

This is being done with regard to the issuance of bonus shares but simultaneously dealing with

other tests mechanism. The controversy was whether the expenditure incurred by the assessee

Company on account of issue of bonus shares was Revenue Expenditure or a Capital

Expenditure. This was remotely connected with Section 37 of The Income Tax Act, 1961 and

Section 75 (1)(c)(I) of the Companies Act, 1956. On this issue, there was a conflict of opinion

between the High Courts of Bombay & Calcutta on the one hand and Gujarat & Andhra Pradesh

on the other. The Bombay and Calcutta High Courts were of the view that the expenses incurred

in connection with bonus shares is a revenue expenditure whereas Gujarat and Andhra Pradesh

High courts have taken a contrary view and have ruled that the expenses incurred in connection

with the bonus shares is in the nature of capital expenditure because it expanded the capital base

of the Company.

This matter went to the Apex Court in the case of CIT, Mumbai v. General Insurance

Corporation. In the instant case before their Lordships the assessee Company had during the

concerned accounting year - incurred expenditure separately for the increase of its authorized

share capital and the issue of bonus shares. The assessee being unsuccessful at various forums

The Oxford College Of Business Management Page 12

Impact of Bonus Issue on Market Price

finally went to the Supreme Court on the second category i.e. the nature of expenditure incurred

in the issuance of bonus shares. In Empire Jute Company Ltd v.CIT Supreme Court laid down

the test for determining whether a particular expenditure is revenue or capital expenditure. It was

observed that there was no all-embracing formula, which could provide ready solution to the

problem, and that no touchstone had been devised. It laid down that every case had to be decided

on its own canvass keeping in mind the broad picture of the whole operation in respect of which

the expenditure has been incurred.

The Apex Court endorsed the text laid down by Lord Cave, LC, in Altherton v. British Insulated

and Helsby Cables Ltd. In this case it was observed that when an expenditure was made, not only

once and for all but with a view to bringing into existence an asset of advantage for the enduring

benefit of a trade then there was a very good reason for treating such an expenditure as properly

attributable not to Revenue but to Capital. This brings us to the crux of the problem. One of the

arguments that could be advanced is that the expenses incurred towards issue of bonus shares

conferred an enduring benefit to the Company, which resulted in an impact on the capital

structure of the Company, and in that perception it should be regarded as capital expenditure.

Conversely, the issuance of bonus shares by capitalization of reserves was merely reallocation of

a company’s fund and there was no inflow of fresh funds or increase in the capital employed

which remained the same therefore did not result in conferring an enduring benefit to the

Company and therefore the same should be regarded as revenue expenditure. The “enduring

benefit” is of paramount importance while examining the rival contentions with which these two

concepts are interwoven. There is also no unanimity in verdicts of various High Courts. In the

back ground, the Supreme Court laid down the test whether a particular expenditure was

Revenue or Capital in Empire Jute Company Ltd. v. CIT whereas the cases of Karnataka and

Gujarat High Court dealt with the issuance of fresh shares and therefore the ratio decided of

these courts did not apply to the issuance of bonus shares. However, the view as taken appears to

be as laying down correct law. The Supreme Court did not agree with the observation of learned

author A. Ramaiya which was of the view that while issuing bonus shares a Company converts

the accumulated large surplus into Capital and divides the Capital among the members in

The Oxford College Of Business Management Page 13

Impact of Bonus Issue on Market Price

proportion to their rights. The learned author felt that the bonus shares went by the modern name

“Capitalization of Shares”. The Apex Court has, therefore, marshaled the entire arithmetic and

chemistry of the two very important propositions of the taxation law i.e. Capital expenditure and

Revenue expenditure and made over a conceptual clarity by reiterating the evolved principle of

“enduring benefit” vis-à-vis reallocation of a Company’s fund. The court has also laid down acid

test for determining these two contingencies although the occasion was the event of issuance of

bonus shares. The Capital expenditure is expenditure for long-term betterments or additions. This

expenditure is in the nature of an investment for future chargeable to capital asset account

whereas revenue expenditure is incurred in the purchase of goods for resale, in selling those

goods and administering and carrying of the business of the Company. The freewheeling

dissections by the Apex Court in Commissioner of Income Tax v. General Insurance Corporation

of the various limbs of these twin concepts have cleared much of the haze. The Court held that

the expenditure incurred in connection with the issuance of bonus shares is in the nature of

revenue expenditure. The Bench said “the issue of bonus shares by capitalization of reserves is

merely a reallocation of company’s funds. There is no inflow of fresh funds or increase in the

capital employed, which remains the same. If that be so, then it cannot be held that the Company

has acquired a benefit or advantage of enduring nature. The total funds available with the

company will remain the same and the issue of bonus shares will not result in any change in the

capital structure of the company. Issue of bonus shares does not result in the expansion of capital

base of the company.”

Conclusion

The economy is booming, the markets are buoyant, and Indian companies are increasing their

profitability. Consequential of all this, many companies have announced issues of bonus shares

to their shareholders by capitalizing their free reserves this year. In this bullish market,

shareholders have benefited tremendously, even after accounting the inevitable reduction in

share prices post-bonus, since the floating stock of shares increases. The whole purpose is to

capitalize profits. We can say that Bonus shares go by the modern name of “Capitalization

Share”. Fully paid bonus shares are not a gift distributed of capital under profit. No new funds

The Oxford College Of Business Management Page 14

Impact of Bonus Issue on Market Price

are raised. Earlier there was also a lot of confusion & chaos between the two fiercely debated

concepts of taxation laws i.e. Capital & Revenue Expenditure which was finally settled after the

case which come up in SC in 2006, named Commissioner of Income Tax v.General Insurance

Corporation. Now it is also settled law that a bonus issue in the form of fully paid share of the

company is not income for the Income Tax purpose. The undistributed profit of the company is

applied and appropriated for the issue of bonus shares.

What are bonus shares?

Bonus shares, as the name suggests, are issued free to existing stockholders in proportion to the

number of stocks held by them. It is essentially a book transfer by which a sum of money equal

to the value of the bonus shares is transferred from the reserves to the equity capital in the

company’s books of accounts. The issue of bonus stocks enlarges a stockholder’s stockholding

without any dilution in his proportionate ownership of the company. These shares are issued in a

particular proportion to the existing holding. For example, 1 for 1(written as 1:1) bonus would

mean you get one additional shares, without paying anything at all, for the one share you hold in

the company. Similarly if the company has declared 2:1 bonus share that means you will get two

shares for one share you have. Thus a shareholder holding two shares, post bonus holds three

shares of the company. Or, if you hold 100 shares of a company and a 2:1 bonus offer is

declared, you get 200 shares free. After the bonus issue, total number of shares of that company

will now be 300 instead of 100 at no extra cost. The company also announces a record date for

the issue of bonus shares. The record date is the date on which the bonus takes effect, and

shareholders on that date are entitled to the bonus. After the announcement of the bonus but

before the record date, the shares are referred to as cum-bonus. After the record date, when the

bonus has been given effect, the shares become ex-bonus.

Is it actually free?

Though, bonus shares don’t cost to shareholders technically, bonus shares are not free.

Companies do not generally distribute their entire profits to the stockholders as dividends. A

fairly large part of the profit is retained and added on to what is commonly called the reserves of

The Oxford College Of Business Management Page 15

Impact of Bonus Issue on Market Price

the company. Reserves are back up funds which a company keeps for meeting unforeseen

increases in expenditure, and for financing its future expansion or diversification programmers.

But when the reserves have more cash than required for the reinvestment, then companies use

these free cash reserves for issuing bonus shares to share holders. For this, the company transfers

some amount from the reserves account to the share capital account by a mere book entry. Bonus

shares are issued by cashing in on the free cash reserves of the company. As, shareholders do not

pay; the company’s profits are also not affected by issuing these bonus shares. Bonus shares

increase the total number of shares of the company in the market, i.e. after the bonus issue a

company will have more free floating shares in the market.

Let’s see how. Suppose initially, a company had 10 million shares. This year the company

decides to issue bonus shares in 2:1 proportion. With a bonus issue of 2:1, there will be 20

million shares issues in addition to 10 million existing shares in the market. So now, there will be

total 30 million shares. This is also referred to as equity dilution. The earnings of the company

will also have to be divided by the increased number of shares. Since, bonus issue has no impact

on the profit, it remains the same but the number of shares has increased, the EPS will decline.

Will the price change after a bonus issue?

Ideally, the stock price should also decrease proportionately to the number of new shares issued.

But, in reality, proportionate price changes may not occur. That happens mainly because of

increased liquidity and enhanced investor confidence in the company’s management. After the

bonus issue, the stock becomes more liquid which makes it is easier to buy and sell. Also, issuing

bonus shares signals that the company is in a position to service its larger equity. A company will

not normally issue bonus stocks unless it is confident that its future growth prospects justify an

expansion in its equity capital. Therefore, the expectation of a bonus issue by any company

normally creates a climate of optimism and cheer in the stock markets and usually results in a

rise in the price of a company’s stocks just before or upon the announcement by it of a bonus

issue.

The Oxford College Of Business Management Page 16

Impact of Bonus Issue on Market Price

Does bonus issue increase your gains?

Though, getting bonus shares is a positive development for the investors, bonuses may not

necessarily generate free gains for investors. Bonus issue does create a tiny upward and short-

lived bias because of above mentioned reasons. But for most of the companies this appreciation

in price dies in the long run. If we look in Indian stock market, we see that except for some large

companies like TCS, bonus issues did not add much to investor wealth, especially in the long

run. In fact, investors in several companies have lost substantially, even after taking into account

extra shares they received through bonus issues. Anu’s Lab is a notable example of this

phenomenon. Anu’s Lab gained more than 19% the day it became ex-bonus but its price started

slumping soon after. Currently Anu’s Lab is trading at 44% lower price compared to its pre-

bonus price (see the list).

Below table gives a list of 40 companies which issued bonus shares in FY 2009-10. As expected,

most of the companies (32 out of 40) reported appreciation in stock prices soon after they

became ex-bonus. But this euphoria could not stay very long for most of the companies. Out of

these 40 companies, only 21 companies could maintain their price appreciation (as on 5th Feb

2010). Out of these 21 companies, only 16 companies are reporting more than 15% price

appreciation. Companies like Anu’s lab, Vishal InfoTech, Country Condo, Veer energy and Anil

Modi Oil are trading way below their pre-bonus prices. Investors, who invested in these

companies with the motive of handsome appreciation in future, must have burnt their fingers

badly. Investment in such companies has resulted into depletion of wealth instead of appreciation

of investor’s wealth. So we can say that buying a share solely because of the bonus issue is a

“purely speculative” trade. It has very little to do with enhancing investors wealth. Though

companies with bonus issues attract a lot of interest in the current market which creates an up

move in stock prices, the long run sustainability of the up-trend mainly depends on other factors

like fundamentals of the company and general market conditions. Before making any investment

decision, investors need to do through fundamental analysis of bonus-issuing companies.

Stock split:

The Oxford College Of Business Management Page 17

Impact of Bonus Issue on Market Price

All publicly-traded companies have a set number of shares that are outstanding on the stock

market. A stock split is a decision by the company's board of directors to increase the number of

shares that are outstanding by issuing more shares to current shareholders. For example, in a 2-

for-1 stock split, every shareholder with one stock is given an additional share. So, if a company

had 10 million shares outstanding before the split, it will have 20 million shares outstanding after

a 2-for-1 split. A stock's price is also affected by a stock split. After a split, the stock price will

be reduced since the number of shares outstanding has increased. In the example of a 2-for-1

split, the share price will be halved. Thus, although the number of outstanding shares and the

stock price change, the market capitalization remains constant.

A stock split is usually done by companies that have seen their share price increase to levels that

are either too high or are beyond the price levels of similar companies in their sector. The

primary motive is to make shares seem more affordable to small investors even though the

underlying value of the company has not changed.

A stock split can also result in a stock price increase following the decrease immediately after the

split. Since many small investors think the stock is now more affordable and buy the stock,

they end up boosting demand and drive up prices. Another reason for the price increase is that a

stock split provides a signal to the market that the company's share price has been increasing and

people assume this growth will continue in the future, and again, lift demand and prices. Another

version of a stock split is the reverse split. This procedure is typically used by companies with

low share prices that would like to increase these prices to either gain more respectability in the

market or to prevent the company from being delisted (many stock exchanges will delist stocks if

they fall below a certain price per share). For example, in a reverse 5-for-1 split, 10 million

outstanding shares at 50 cents each would now become two million shares outstanding at $2.50

per share. In both cases, the company is worth $50 million.

The bottom line is a stock split is used primarily by companies that have seen their share prices

increase substantially and although the number of outstanding shares increases and price per

share decreases, the market capitalization (and the value of the company) does not change. As a

The Oxford College Of Business Management Page 18

Impact of Bonus Issue on Market Price

result, stock splits help make shares more affordable to small investors and

provide greater marketability and liquidity in the market.

What is a stock split?

A stock split is a corporate action that increases the number of the corporation's outstanding

shares by dividing each share, which in turn diminishes its price. The stock's market

capitalization, however, remains the same, just like the value of the $100 bill does not change if

it is exchanged for two $50s. For example, with a 2-for-1 stock split, each stockholder receives

an additional share for each share held, but the value of each share is reduced by half: two shares

now equal the original value of one share before the split.

Let's say stock A is trading at $40 and has 10 million shares issued, which gives it a market

capitalization of $400 million ($40 x 10 million shares). The company then decides to implement

a 2-for-1 stock split. For each share shareholders currently own, they receive one share,

deposited directly into their brokerage account. They now have two shares for each one

previously held, but the price of the stock is split by 50%, from $40 to $20. Notice that the

market capitalization stays the same - it has doubled the amount of stocks outstanding to 20

million while simultaneously reducing the stock price by 50% to $20 for a capitalization of $400

million. The true value of the company hasn't changed one bit.

The most common stock splits are, 2-for-1, 3-for-2 and 3-for-1. An easy way to determine the

new stock price is to divide the previous stock price by the split ratio. In the case of our example,

divide $40 by 2 and we get the new trading price of $20. If a stock were to split 3-for-2, we'd do

the same thing: 40/(3/2) = 40/1.5 = $26.6.

It is also possible to have a reverse stock split: a 1-for-10 means that for every ten shares you

own, you get one share. Below we illustrate exactly what happens with the most popular splits in

regards to number of shares, share price and market cap of the company splitting its shares.

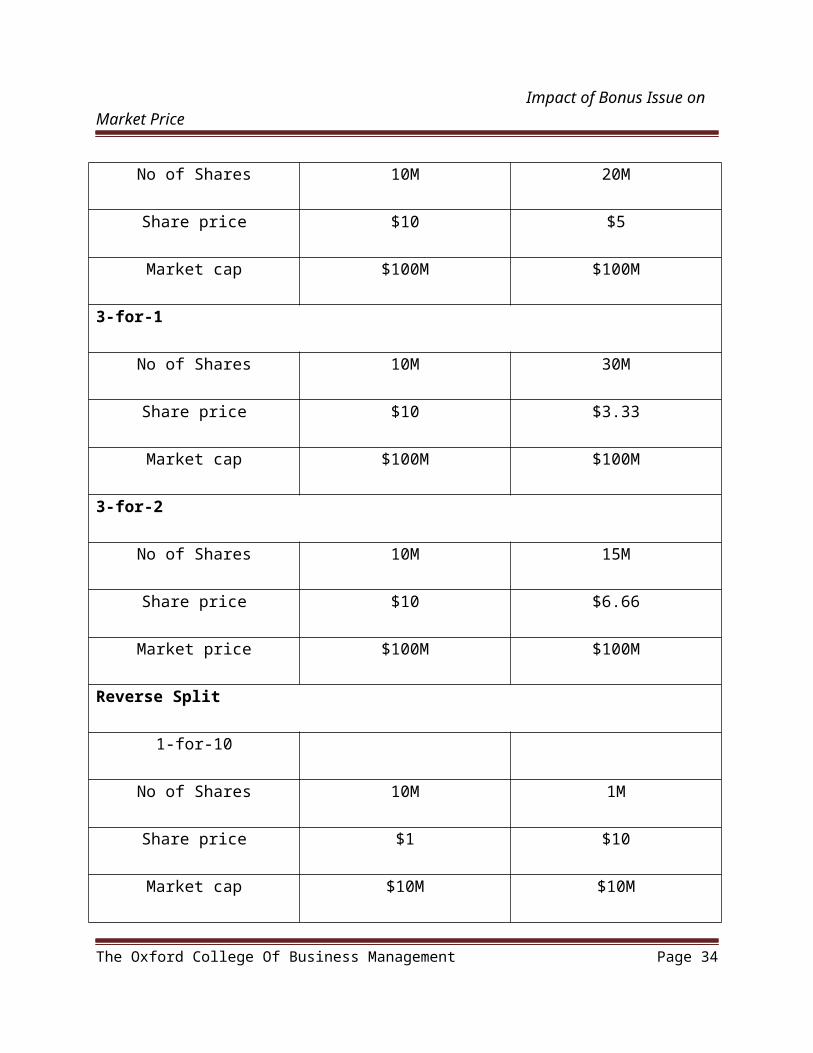

Table No 1: Table showing how Stock Split takes place

The Oxford College Of Business Management Page 19

Impact of Bonus Issue on Market Price

Stock Split Pre-Split Post-Split

2-for-1

No of Shares 10M 20M

Share price $10 $5

Market cap $100M $100M

3-for-1

No of Shares 10M 30M

Share price $10 $3.33

Market cap $100M $100M

3-for-2

No of Shares 10M 15M

Share price $10 $6.66

Market price $100M $100M

Reverse Split

1-for-10

No of Shares 10M 1M

Share price $1 $10

Market cap $10M $10M

Why do companies issue splits if you still have the same amount of money?

The Oxford College Of Business Management Page 20

Impact of Bonus Issue on Market Price

Liquidity, some companies believe that their stock should be inexpensive so more people can

buy it. This creates a condition where more of the company's stock is bought and sold (this is

called "increased liquidity"). The problem, in theory, is that the increased activity will also leads

to bigger gains and drops in the stock, making it more volatile.

Many investors believe splits are a good thing. (Their thinking goes "Well, if the stock was at

$15, and now it's at $7.50, it has to go back up to where it was!) This is wrong. The stock is

where it was... remember that each share now represents half of the equity in the company that it

did before the split. That means that each share is entitled to half the dividend, half the earnings,

and half of the assets that it once was.

A few corporations have been famous for their no-split policies. The Washington Post has traded

well into the $600 per share range, and Berkshire Hathaway, which was at $8 a share in the

1960's, has traded as high as $150,000. This has created the welcome condition of a stable

shareholder base.

Reasons for a Stock Split

If a stock split doesn't change anything, why do it? There are several reasons executives decide

to split their stock, or not, mostly involving trader psychology. If a stock price rises too rapidly

new investors might hesitate to put new money into the stock. A stock split resets the price lower

and may make new purchases more palatable to less savvy investors. Stock splits are also used to

bring a company's share price in line with other companies in the sector. On the other hand, some

companies refuse to split their stocks to foster the impression of superiority and success. Warren

Buffet's Berkshire Hathaway, the stock of which trades at tens of thousands of dollars per share,

is a classic example of this, as is Google.

Ratios, Reverses and Other Considerations

While 2 for 1 is a very common ratio for a stock split, any ratio is theoretically possible

depending on the company's needs; 3 for 1, 5 for 3, if the split creates fractional shares the

The Oxford College Of Business Management Page 21

Impact of Bonus Issue on Market Price

company will keep the piece and compensate the investor in cash. Some splits, such as a 1 for 2

or 1 for 3, actually reduce the number of shares outstanding. These are called reverse splits, but

function in essentially the same way. The value of the company doesn't change, but the price per

share increases as the number of shares decreases. Reverse splits are often used to meet listing

requirements for the major exchanges. A final consideration is the effect a split can have on

options traders. The Options Trading Board splits options contracts to reflect changes in a stock,

sometimes resulting in a new trading symbol for the series. Options traders should be aware of

how changes in the strike price and number of contracts owned affects their exposure to

volatility and time decay.

Legal framework for stock splits: The stock splits can be carried out under section 92(1)

c of the Companies Ordinance, 1984. The section reads: “A company limited by shares, if so

authorized by its articles, may alter the condition of its memorandum so as to subdivide its

shares, or any of them into shares of smaller amount then is fixed by the memorandum.” This is

subject to the usual condition that the right attached to the shares must remain the same before

and after the division. Under 92(3), the company can exercise the powers conferred by 92(1)

only in a general meeting. The law also allows reverse splits or share consolidation under 92(1) b

subject to the same conditions.

The Central Depository Company’s regulations also allow share splits under chapter 8D

“Consolidation or sub-division of securities”, the regulations of the exchanges are silent on the

issue of splits. Clearly, the legal framework for stock splits is in place and it is not cumbersome

either.

Bringing About stock splits: So far there hasn’t been any case of a listed company splitting its

shares. Ironically, there has been one case of reverse splits, i.e. share consolidation of Indus

Dying& Manufacturing Limited, listed at the KSE. Why is that? We are of the view that splits

have not happened because having adequate liquidity in their stock is not a significant concern of

the management in our corporate sector.

The Oxford College Of Business Management Page 22

Impact of Bonus Issue on Market Price

Since operational complexity creates hidden costs, exchanges and National Clearing Corporation

have also not been vocal in making a case for standardization of market lots and share splits.

Splits change the par value. The concept of par, however, already has been made obsolete in a

number of jurisdictions because of its economic irrelevance. It should not be a consideration in

bringing about stock splits. In the absence of sufficient incentive for the corporate to go for the

split, the exchange should make splits mandatory through its regulation once a stock meets pre-

specified criteria.

Why Split?

Perception – Some companies worry when the per share price gets too high that it will

scare off some investors, especially small investors. Splitting the stock brings the per

share price down to a reasonable level.

Liquidity – If a stock’s price rises into the hundreds of dollars per share, it may reduce

the trading volume. Increasing the number of outstanding shares at a lower per share

price aids liquidity.

Criteria for splits: The regulatory criteria for mandatory splits should include price, free

float and investor interest in a stock. There are 25 companies listed at the KSE, which have a

price above Rs100 as of January 22, 2003. These include: the unlived, the PSO, the shell, the

Pakistan Oilfields, the Wyeth etc.

In our opinion, a price above Rs100 is on the higher side. In some of these stocks investor

interest and free float are virtually non-existent. Increasing or decreasing their market lots would

not influence their liquidity or encourage entry of small investors. The exchange can simply

bring their market lots to multiples of 500 without bothering about splits.

One can say that if we are going to have a market lot of only 500 shares, then splits should be

made such that every existing shareholder gets a market lot. For instance, if someone subscribed

to only 100 shares at the time of their public offer, then raising the market lot to 500 would turn

these lots into odd lots, which cannot be traded on the main board. Selling an odd lot is difficult

The Oxford College Of Business Management Page 23

Impact of Bonus Issue on Market Price

and usually an investor has to pay a discount from the prevailing price to be able to sell it. Either

the investors with odd lots would have to bear some costs for the benefit of investor at large or

odd lots would have to be facilitated.

Is it good for Investors?

Some investors say a stock split is a sign that a stock is doing well and they consider it a buy

signal. I would caution reading too much into a stock split by itself. You should always look at

the whole picture before making an investment decision. If you want to use stock splits as a

marker for stocks to consider for further evaluation, that is a reasonable idea, but don’t stop there

with your research. If you are interested in following stock splits, MSN Money publishes a stock

split calendar that lists upcoming splits.

Caution

You should watch out for one type of split as a possible danger signal and that’s the reverse split.

In a reverse split, the company reduces the number of outstanding shares and the per share price

rises accordingly.

For example: a company might execute a 1-for-2 reverse stock split, which means for every two

shares you own, you would now own one and the per share price doubles. A reverse stock split is

often used to prop up a stock’s price, since the price rises on the split. Often a company will do a

reverse split to keep the stock price from falling below the minimum required by the stock

exchange where it is listed. Clearly, this is a sign that something is wrong if a company can’t

keep its stock price above the exchange’s minimum listing price and caution is advised.

Conclusion

When you paid stockbrokers based on the number of shares you purchased, it made sense to buy

a stock before it split. However, most brokers now charge a flat fee, so timing a purchase before

or after a split doesn’t make much sense from that perspective. Ultimately, you should buy a

stock based on whether it meets the fundamental standards you require and not on whether it will

or will not split. Say you had a $100 bill and someone offered you two $50 bills for it. Would

The Oxford College Of Business Management Page 24

Impact of Bonus Issue on Market Price

you take the offer? This might sound like a pointless question, but the action of a stock split puts

you in a similar position. In this article we will explore what a stock split is, why it's done and

what it means to the investor. 2Say you had a $100 bill and someone offered you two $50 bills

for it. Would you take the offer? This might sound like a pointless question, but the action of a

stock split puts you in a similar position. In this article we will explore what a stock split is, why

it's done and what it means to the investor.

The most important thing to know about stock splits is that there is no effect on the worth (as

measured by market capitalization) of the company. A stock split should not be the deciding

factor that entices you into buying a stock. While there are some psychological reasons why

companies will split their stock, the split doesn't change any of the business fundamentals. In the

end, whether you have two $50 bills or one $100 bill, you have the same amount in the bank.

Reasons for issuing bonus shares

1. The bonus issue-tends to bring the market price per share within a more popular range.

2. It increases the number of outstanding shares. This promotes more active trading.

3. The nominal rate of dividend tends to decline.

4. The share capital base increases and the company may achieve a more respectable, size

in the eyes of investing community.

5. Shareholders regard a bonus issue as a firm indication that’ the prospects of the company

have brightened and they can reasonably look for an increase in total dividend.

6. It improves the prospects of raising additional funds. In recent years many firms have

issued bonus shares prior to the issue of convertible debentures or other financing

instruments.

Regulations for issue of bonus shares

Listed companies have to follow the provisions of chapter Xth of SEBI (Disclosure and investor

protection) Guidelines, 2000 while issuing Bonus share.

The Oxford College Of Business Management Page 25

Impact of Bonus Issue on Market Price

The following are the pre-condition to be complied with by the Listed Companies.

(A)Legal

1. If the authorized capital is not sufficient, the Authorized capital should be first increased

which will enable further issue of share. Then the issue of bonus shares shall be considered.

2. It should be checked whether-the Articles of Association of the Company should be amended

first.

3. There are no restrictions regarding the ratio at which share can be issued. It can be issued

grater than1:1 also.

(B) Legal requirements

1. Bonus shares shall be issued only out of free reserves built out of genuine profits or shares

Premium Company held in cash equally.

2. Reserves created by revaluation of fixed assets cannot be capitalized.

3. Bonus shares shall be issued in lieu of dividend.

4. All the partly paid share, if any, should be first made fully paid up.

5. There should not be any default in

(a) Payment of interest on fixed deposits.

(b) Payment of principal on fixed deposits.

(c) Payment of interest on debentures.

(d) Payment of principal on redemption of debentures.

The Oxford College Of Business Management Page 26

Impact of Bonus Issue on Market Price

(e) Payment of statutory dues to the employees on contribution of provident fund,

gratuity, Bonus, etc.

6. When convertible debentures/partially convertible debentures are pending for conversion into

equity shares, the company shall not issue Bonus shares to the existing shareholders without

extending such benefit to the holders of these instruments also on issued at the time of

conversion of the debentures.

(c) Other condition:

1. The proposal to issue Bonus shares should be implemented within six months from the date of

Board resolution.

2. The decision to issue Bonus shares shall not be reversed by the Board Approach required.

(a) The Board of Directors of the Company will have to first consider the proposal and approve

the same and call a general meeting of members to approve the proposal.

(b) Shareholders have to approve the issue of bonus shares.

(c) A record date has to be fixed thereafter by giving notice of 42 days to the stock Exchanges

and a list of shareholders who are eligible to receive Bonus shares have to be determined.

Income tax angle per section 55(2) (3a) of the income tax act, 1961, in the case of issue of bonus

shares, the cost acquisition will be taken as nil.

In the case of sale of these shares, it will attract capital gain tax. (13) Applicable for issue by a

Designated Financial institution Designated Financial Institution (DFI) is one. Which a public

financial institution is as defined under section 4A of the companies act, 1956 or an industrial!

Development Corporation established by state Government or a financial institution approved

under section 36(I) (Vii) of income tax act, 1961. Chapter XII in SEBI Guidelines covers issues

by Designated Financial Institutions including issue of Bonus shares by DFIs.

Conditions:

The Oxford College Of Business Management Page 27

Impact of Bonus Issue on Market Price

The following are the conditions to be complied with by a DFI:

(a) The bonus issue is made out of free reserves built out of genuine profits or share

premium collected in cash.

(b) Reserves created by revaluation or sale of fixed assets are not capitalized.

(c) The residual reserves after the proposed capitalization shall be at least forty percent of

the increased paid up capital.

(d) The following reserves can be considered as free reserves for the purpose of calculation

of residual reserves only. Any special reserve created for the purpose of seeking tax

benefits. Capital reserves created as a result of sale of assets. Any reserve created without

accrual of cash resources, and. Any other reserve not being in the nature of free reserves,

even though it cannot be capitalized.

(e) All contingent liabilities disclosed in the audited accounts shall be taken into account in

the calculation of the residual reserves, namely they shall be deducted from reserves.

(f) Thirty percent of average profit before tax for the previous three years shall yield a rate

of dividend the expanded capital at ten percent at least.

(g) The DFR should not have failed in the maintenance of required DER, NDSCR, during

the last three years.

(h) There should not be any default in: payment of principal on fixed deposits payment of

interest on debentures/bonds. Payment of statutory dues to the employees on contribution

to provident fund, Gratuity, bonus etc.

(i) When fully convertible debentures/partially convertible debentures are pending for

conversion into equity shares, the OFI shall not issue Rights shares or bonus shares to the

(j) Existing shareholders without extending such benefit through reservation to the holders

of these instruments falling due within twelve months from the call: Of issue/bonus issue

and the shares reserved shall be issued at the time of conversion of the debentures. Bonus

shares shall not be issued in lieu of dividend.

(k) All the partly paid shares, if any, should be first made fully paid up.

(l) The proposal to issue Bonus shares should- be implemented within six months from the

date of approval By the Board or general body whichever is later.

The Oxford College Of Business Management Page 28

Impact of Bonus Issue on Market Price

(m)The shareholders shall be informed about the ability of the estimated rate of dividend

payable during the year or the next following year after issue of bonus shares.

SEBI role in issue of bonus shares by companies:

SEBI is playing a vital role in regulating capital markets. Offer Document / prospectus for almost

all types of issues are sent to SEBI for their comments. SEBI has framed guidelines for all types

of issues including Bonus issue.

In case of Bonus Issue, there is no offer document as there is no involvement of any

consideration. No funds are coming into the corpus of the company. Therefore, companies are

required to just follow the guidelines issued by SEBI. Companies are not required to take any

specific approval from SEBI

Things to remember before considering Bonus Issue:

1) Bonus shares cannot be issued if the company has come out with any public rights

issue in the past 12 months.

2) Bonus shares cannot be issued in lieu of dividend.

3) Bonus shares can be issued only out of free reserves (i.e. reserves not set apart for any

specific purpose)built out the genuine profits or share premium out of the genuine

profits or share premium collected in cash only.

4) Bonus shares cannot be issued out of the reserves created by revaluation of fixed

assets.

5) If the company has already issued either fully convertible debentures or partly

convertible debentures than in that case the company is required to extend similar

benefits to such holders of securities through reservation of shares in proportion for

their holding or in proportion to such convertible part. The Bonus shares so reserved

may be allotted to such holders at the time of conversion.

6) If the existing shares are partly paid up, the company cannot issue Bonus shares. It

will be appropriate to first make the shares fully paid up before issuing Bonus shares.

The Oxford College Of Business Management Page 29

Impact of Bonus Issue on Market Price

7) It should be checked whether Articles of association contains the provision of

capitalization of reserves. If no such provisions are contained steps should be taken

by altering the Articles of Association by the consent of the members of the company.

8) It should be checked whether the post bonus capital is within the limits of authorized

share capital. If it so, steps should be taken to increase the authorized share capital by

amending memorandum and articles of association.

9) It is very important for a company to implement the bonus proposal within a period of

six months from the date of approval at the meeting of the Board of Directors. The

company has no option to change the decision.

10) All the shares so issued by way of bonus will rank pari-passu with the existing shares.

The company cannot create any other rights for the bonus shares.

Steps involved in issuing Bonus shares:

a) As per the listing agreement, at least 7 days prior to the board meeting in which bonus

will be considered, a notice has to be given to each stock exchange where securities of

the companies are listed about the declaration of bonus shares.

b) At the Board meeting approve the following.

c) Bonus Ratio

d) Fixation of Record Date or Book Closure Notice

e) Notice convening general meeting for increase in authorized share capital and

capitalization of reserves and amendment in memorandum & articles of association

thereof.

f) Intimate to such stock exchanges on the same day about the result of the board meeting

immediately after the closure of the market hours.

g) Intimate at least 42 days in advance to such stock exchanges about the closure of register

of member or fixing of record date fixed for allotting bonus shares to such shareholders.

h) If the company intend to close its register of members at least 7 days prior to the book

closure, a notice has to be issued in the newspaper circulating in the district in which

registered office of the company is situated.

The Oxford College Of Business Management Page 30

Impact of Bonus Issue on Market Price

i) Send at least 21 days clear notice to all such a shareholders about the General meeting

Convene and pass resolution for amending Memorandum & Articles of association

pertaining to increase in authorized share capital and capitalization of reserves.

j) File Form No.23 with ROC regarding amendment made in memorandum &

articles of association along with certified true copy of the resolutions passed,

explanatory statement and prescribed fees.

k) For increase in authorized share capital, affix stamp duty as applicable on

Form No.5 and along with the prescribed fees file the same with ROC.

l) Give effect to all the transfers received before the closure of register of members or

fixing of record date.

m) Convene a Board meeting to allot shares to those shareholders whose name appears in

the register of members as on record date or at the time of closure of register of members.

n) Make arrangements for the printing of share certificates. Issue share certificates in

accordance with the rules prescribed for issuing share certificates (see to it that common

seal and stamp duty is affixed on it and signed by two directors and an authorized

signatory as per the board resolution).

o) File Form No. 2 with ROC along with the list of shareholders and prescribed fees. It is

very important to note that Bonus shares have to be issued within a period of 6 months

from the date of Board meeting at which the bonus issue was declared.

Steps to be taken in regard to a Bonus Issue

1) Fixing the ratio.

2) Intimation to stock exchange about Board meeting if applicable.

3) Approval from the Board of Directors.

4) Approval from RBI for issue of shares to Non – resident Indians.

5) Approval from the shareholders Record date (42 days).

6) To prepare a list of proposed allotters obtaining approval of State Government for bulk

payment of stamp fees wherever considered necessary Allotment of Bonus shares by

Board/Committee.

The Oxford College Of Business Management Page 31

Impact of Bonus Issue on Market Price

7) Issue of share certificates, issue of Bonus Shares by Unlisted Companies.

The aforesaid guidelines of SEBI do not apply to unlisted companies such as public companies

whose shares are not listed on any recognized Stock Exchange, private companies and deemed

public companies. These companies shall follow the provisions in their Articles of Association

and Departmental Circulars and clarifications issued in this regard.

The Circular No. 9/94 dated 6-9-1994 issued by the Department of Company Affairs, advises the

existing private/closely held and unlisted companies not to issue bonus shares out of reserves

created by revaluation of fixed assets.

The Guidelines Note issued by the Institute of Chartered Accountants of India stipulates that

bonus shares cannot be issued by capitalizing revaluation reserves. The non-observance of this

will attract qualification in the Auditor’s report.

Guidelines for Bonus Issue

The Controller of Capital Issues follows these guidelines while examine the proposal of bonus

issue. Such guidelines are:-

(i) Bonus issues are not permitted in lieu of dividend.

(ii) There must be an internal of at least 40 months between two successive announcements of

bonus issues by a company.

(iii) Not more than two bonus issues are allowed over a period of five years.

(iv) Bonus issues are not permitted unless partly paid up shares, if any, are made fully paid up.

(v) Bonus issues are permitted only out of free reserves built out of genuine profits or share

premium collected in cash only. Development Rebate Reserve is considered to be a free reserve

but reserves created by revaluation of fire assets or without accrual of cash resources are not

permitted to be capitalized for this purposes.

The Oxford College Of Business Management Page 32

Impact of Bonus Issue on Market Price

(vi) At any one time, the total amount permitted to be capitalized for issue of bonus shares out of

free reserves shall not exceed the paid up equity capital of the company.

(vii) The residual reserves after the proposed capitalization should be at least 33 1/3% of the

increased paid up capital, In calculating the minimum capital Reserve 33 1/3 %, the

Development Rebate Reserve is taken into account but Capital Redemption Reserve is excluded.

Any Capital Reserve on revaluation of assets or without actual of cash resources are also

excluded. For this purpose, all contingent liabilities bearing on net profits shall be taken into

account.

(viii) 30 % of the average amount of pre-tax profits of previous three years should yield return of

at least 9 % on the increased capital of the company.

(ix) A resolution should be passed approving the proposed capitalization of profits before an

application is made to the Controller of Capital Issues. The resolution should clearly mention

their decision regarding the rate of dividend payable on the increased capital in the year

immediately after the bonus issue is made.

New Guidelines for Bonus Issue

A company may apply such bonus in making the partly paid up shares fully paid up without

asking for cash from the shareholders. Generally, a company issues bonus shares when it has

sufficient Reserves and surplus but no cash to pay off dividend.

The company Law restricts the issue of bonus shares but imposing the following conditions to be

compiled with by the company:-

(i) The Article of Association permit the issue of Bonus Shares.

(ii) Such shares can be issued only out of; Accumulated Profits' or 'Share Premium Account' or

'capital Redemption Reserve Account'.

The Oxford College Of Business Management Page 33

Impact of Bonus Issue on Market Price

(iii) Permission of the Controller of Capital Issues has been obtained irrespective of the amount

Involved.

(iv) The proposal of the Board of Directors had been duly approved by the shareholders in the

general meeting.

The company shall file a return stating the number and nominal amount of bonus shares issued

together with the name and addresses of the allottees and a copy of resolution authorizing such

issue within 30 days from the date of allotment. (Sec. 75)

Impact of Bonus Issue on Market Price

We have discussed the advantages of bonus issue from the point of view of the company and

the shareholders n the above lines. Now, we shall discuss its impact on the market priced of the

equity shares.

The main advantage of bonus issue to the shareholders is that they get more cash dividend in

future years if company maintains the pre-bonus rate dividend on equity shares. But the question

is whether the company will be in position to maintain the rate of dividend after issuing bonus

shares or mere capitalizing the accumulated profits it depends solely on the earnings capacity of

the company. The future rate of dividend will naturally be lower as because the number of equity

shares will be increased without any increase in its earning capacity of thus the total profits

would be divisible among the larger number of shares thus lowering down the dividend per

share. Dividend at the lower rate would adversely affect the share price in the market. But if the

total cash-dividend to be received by a shareholder after bonus issue, is protected or it marginally

increases, share price would not be affected much. On the other hand, if the issue of bonus shares

is used as a speculative tool by the administrator or persons having vested interest in the