Illustrative Integrated Annual Report IFRS Entity 31 ... · The illustrative financial statements...

46

Illustrative Integrated Annual Report IFRS Entity 31 December 2015

Transcript of Illustrative Integrated Annual Report IFRS Entity 31 ... · The illustrative financial statements...

Illustrative

Integrated Annual Report

IFRS Entity

31 December 2015

IFRS Entity Financial Statements For the year ended 31 December 2015

Introduction

A cornerstone of accountability is fair and transparent reporting of transactions and events. Transparency cannot be measured in degrees, it is a yes/no test. Entities either are, or are not transparent. Increasingly regulation drives entities to provide more and more information. However providing more information does not of itself improve transparency. The IASB has undertaken a great deal of work on what Listed Entities should be reporting and in 2010 issued its Best Practice Statement ‘Management Commentary.’ That work has been developed by the International Integrated Reporting Committee and in 2013 it issued its Integrated Reporting Framework. We consider the work of both parties in this issue. The Abu Dhabi Accountability Authority (ADAA) does not suggest you make publically available information you do not need to, or is sensitive to you. However we do recommend that you consider the matters raised carefully and implement as much as you can, at least for internal stakeholder consumption. ADAA has for the last six years published its Accountability Report, in which we address many if not all of the matters raised. It can be found here www.adaa.abudhabi.ae. We include the requirements of the IASB’s Best Practice Statement on Management Commentary and IFRS 8 Segment Information and recommend Subject Entities include Commentary and Segment Reporting in their reporting as it gives management a good opportunity to communicate to stakeholders an insight of their stewardship of Subject Entities. ADAA also publishes a monthly IFRS Digest that addresses topical accounting issues. Publications are available on www.adaa.abudhabi.ae. This publication provides an illustrative set of entity financial statements prepared in accordance with International Financial Reporting Standards (IFRS) based on the requirements of IFRS for the financial year ended 31 December 2015.

ADAA also publishes accounting briefing papers. Issues covered include; Leasing, Investment Entity Amendment, Depreciation, Government Related Party disclosures, Investment Entities, IFRS Disclosures, Investment Property, Fair Value measurement, Impairment and Transactions with Government. Papers are available on www.adaa.abudhabi.ae

Audit firms BDO International, Deloitte, EY, KPMG and PWC provide free high quality comprehensive illustrative IFRS financial statements on their websites, some of which are tailored to specific industries. We suggest you make

use of those financial statements too by following the links provided; PWC , KPMG EY , Deloitte , BDO International In addition the audit firms provide cross references to the requirements of the disclosure paragraph in the relevant accounting standard.

Should you wish to discuss any of the items raised in this publication please contact the Accounting and Auditing Standards Desk, within the Financial Audit and Examination Group of ADAA.

IFRS Entity is an existing preparer of IFRS financial statements. The transitional provisions of IFRS 1 have not therefore been covered. In order to keep the financial statements to a manageable size, the notes to the financial statements have not always been provided in full, where this is the situation, it has been stated.

The illustrative financial statements are written by the Accounting and Auditing Standards Desk (AASD) of the Financial Audit and Examination Group of the Abu Dhabi Accountability Authority (ADAA). All rights reserved.

The illustrative financial statements are intended as information for the reader only and none of the content is intended as accounting advice. Entities should refer to ADAA direct if advice is required for a particular issue.

Abu Dhabi Accountability Authority accepts no responsibility for loss or damage caused to any party who acts or refrains from acting in reliance on this publication, whether such loss is caused by negligence or otherwise.

IFRS Entity Financial Statements For the year ended 31 December 2015

Contents

Page Number

Integrated Reporting 1

Management Commentary 10

Income Statement 12

Statement of Comprehensive Income 12

Statement of Financial Position 13

Statement of Changes in Equity 14

Statement of Cash Flows 15

Notes to the Financial Statements 16

Appendix I New standards and amendments 38

Appendix II Forthcoming requirements 41

*Prepared utilising EY’s illustrative financial statements for 2015 year-ends accessible here

IFRS Entity Financial Statements For the year ended 31 December 2015

1

Integrated Reporting

Introduction The International Integrated Reporting Committee (IIRC) is one organizations at the forefront of the development of new ideas regarding integrated reporting: IIRC was formed in 2010 under the aegis of the Prince of Wales Accounting for Sustainability Project and the Global Reporting Initiative (GRI). In addition to business executives and investors, representatives from the major accounting bodies, standards setters and security regulators sit on this committee. Integrated reporting combines different strands of reporting; financial, management commentary, governance and remuneration, and sustainability reporting into a coherent whole that explains an organization’s ability to create and sustain value. The output of integrated reporting is an integrated report; a single report that the IIRC expects will become an organization’s primary report. An integrated report is not easy to prepare and because it is new there is not a huge number of examples to follow. The International Integrated Reporting <IR> Framework (the “<IR> Framework”) issued in December 2013 by the IIRC provides guidance. Fundamentally the guidance enables an organisation to explain in understandable terms how it creates and sustains value in the short, medium and longer term.

On the next few pages we set out the <IR> Framework guidance and provide some examples we have found.

Extracted from Integrated Reporting Framework Issued by IIRC

IFRS Entity Financial Statements For the year ended 31 December 2015

2

Value Creation Process: An Integrated Report explains how the Inputs and Business activities drive the Outputs and Outcomes for an organisation. The main elements of an Integrated Report are:

Organizational overview and external environment

Governance and remuneration

Business Model

Strategy and resource allocation

Performance:

Future outlook The following pages include a summarised description for each element and examples of reporting (where possible). Organizational overview and external environment

The Integrated report answers the question: What does the organization do and what are the circumstances under which it operates? To achieve this the organization explains its mission and vision, and provides context of how it goes about achieving them by identifying matters such as the organisation’s:

Culture, ethics and values

Ownership and operating structure

Principal activities and markets

Competitive landscape and market positioning considering factors such as o Threat of competition and o Substitute products or services, o Bargaining power of customers and suppliers, and o Intensity of competitive rivalry

Position within the value chain

Key quantitative data such as the number of employees and number of countries in which the organization

operates and highlighting, in particular, significant changes from prior periods.

Significant factors affecting the external environment and the organization’s response.

Governance & remunerations An integrated report answers the question: How does the organization’s governance structure support its ability to create value in the short, medium and long term?

IFRS Entity Financial Statements For the year ended 31 December 2015

3

Here an organisation sets out:

Its leadership structure, the skills and diversity (range of backgrounds, gender, competence and experience) of those charged with governance and if regulatory requirements influence the design of its governance arrangements.

The organization’s culture, ethics and values and how those are reflected in its use of and effects on its capitals (capitals being resources of cash, people, etc) and its relationships with key stakeholders.

The specific processes used to make strategic decisions and to establish and monitor the culture of the

organization, including its attitude to risk and mechanisms for addressing integrity and ethical issues.

The responsibility those charged with governance take for promoting and enabling innovation.

How remuneration and incentives are linked to value creation in the short, medium and long term, including how they are linked to the organization’s use of and effects on the capitals.

Below is an example of how these matters might be described in an Integrated Report: The Board of Directors comprises xxx members, xxx of whom are independent. The independent members have no links to the signatories to the shareholders’ agreement, in compliance with prevailing legislation. An equal number of independent members compared to non independent members are required to constitute a formal Board meeting. Board meetings take place at least xxx times a year and all Board members should be present on all occasions, as well as all meetings of the committees on which they serve.

List Members of the Board of Directors and related biographies.

List Board Committees (e.g., Audit & Risk Committee, Finance Committee, Personnel & Remuneration Committee, Sustainability Committee….) the Committees responsibilities and members.

Provide explanation of Board Remuneration policy.

Provide information on Code of conduct and training for employees and Whistleblowing channels.

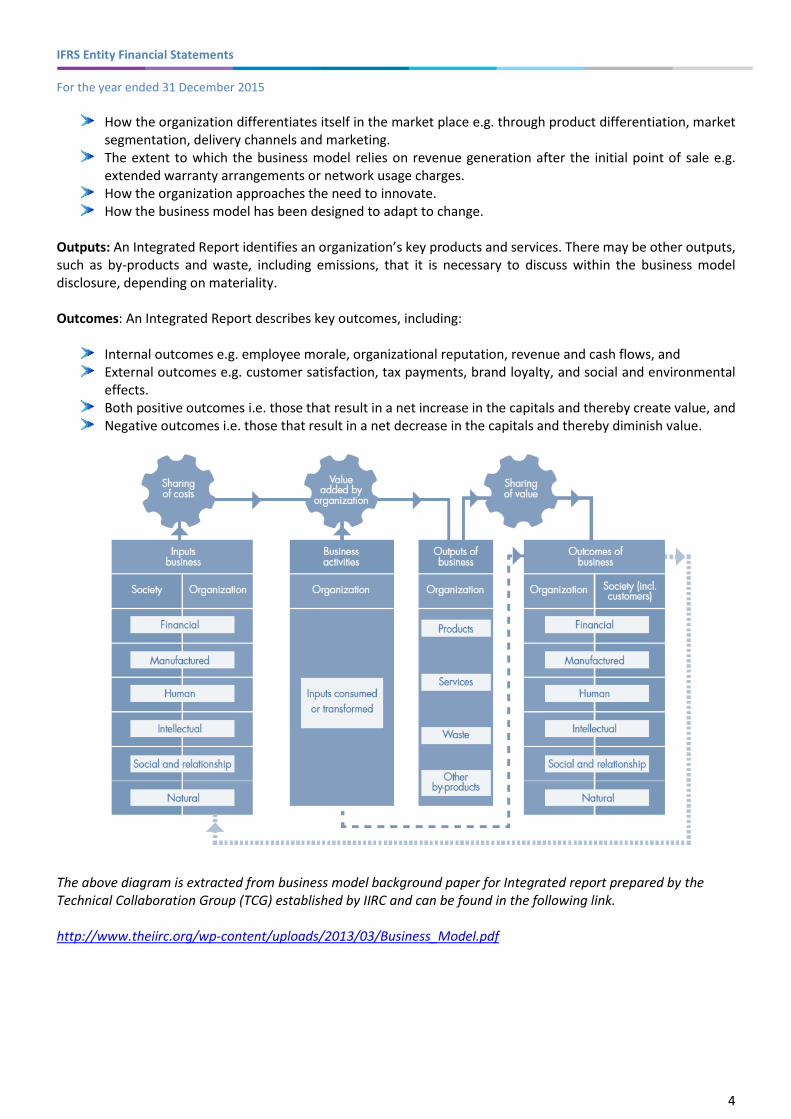

Business model

An Integrated Report answers the question: What is the organization’s business model? An organization’s business model is its system of transforming inputs, through its business activities, into outputs and outcomes that aims to fulfil the organization’s strategic purposes and create value over the short, medium and long term. Inputs: An Integrated Report shows how key inputs relate to the capitals (resources) on which the organization depends, or that provide a source of differentiation for the organization, to the extent they are material to understanding the robustness and resilience of the business model. Business activities: An Integrated Report describes the key business activities: This can include:

IFRS Entity Financial Statements For the year ended 31 December 2015

4

How the organization differentiates itself in the market place e.g. through product differentiation, market segmentation, delivery channels and marketing.

The extent to which the business model relies on revenue generation after the initial point of sale e.g. extended warranty arrangements or network usage charges.

How the organization approaches the need to innovate. How the business model has been designed to adapt to change.

Outputs: An Integrated Report identifies an organization’s key products and services. There may be other outputs, such as by-products and waste, including emissions, that it is necessary to discuss within the business model disclosure, depending on materiality. Outcomes: An Integrated Report describes key outcomes, including:

Internal outcomes e.g. employee morale, organizational reputation, revenue and cash flows, and External outcomes e.g. customer satisfaction, tax payments, brand loyalty, and social and environmental

effects. Both positive outcomes i.e. those that result in a net increase in the capitals and thereby create value, and Negative outcomes i.e. those that result in a net decrease in the capitals and thereby diminish value.

The above diagram is extracted from business model background paper for Integrated report prepared by the Technical Collaboration Group (TCG) established by IIRC and can be found in the following link. http://www.theiirc.org/wp-content/uploads/2013/03/Business_Model.pdf

IFRS Entity Financial Statements For the year ended 31 December 2015

5

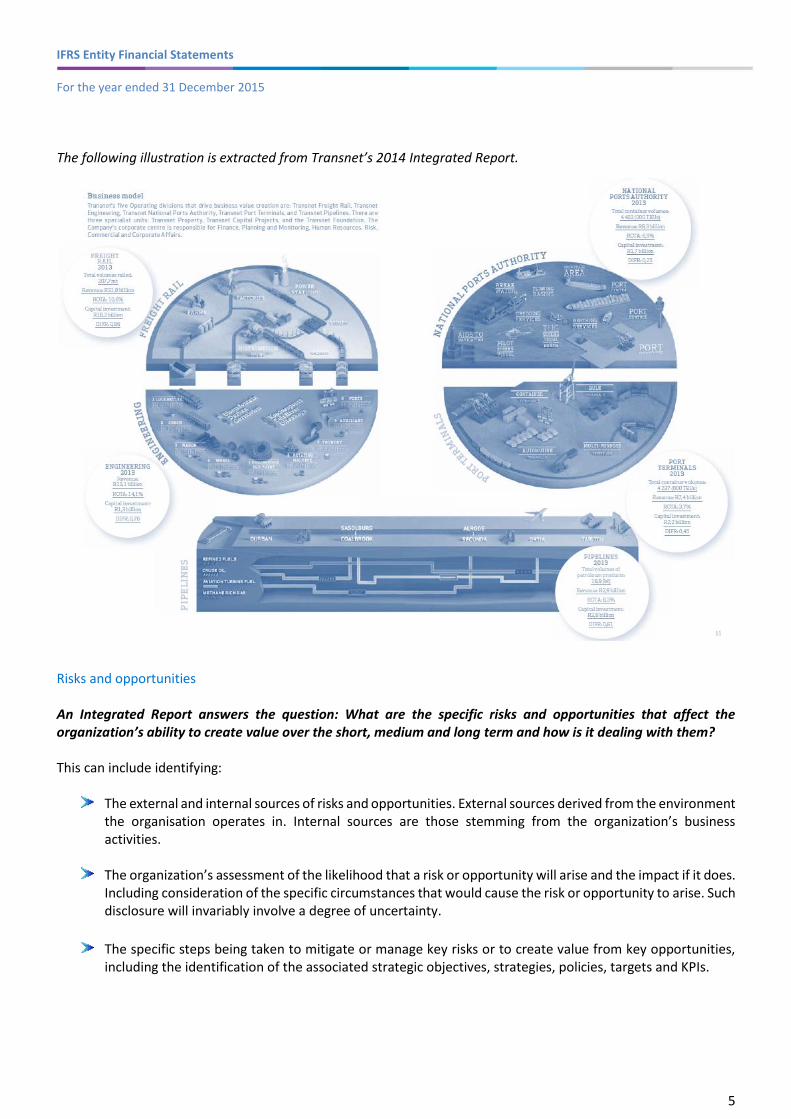

The following illustration is extracted from Transnet’s 2014 Integrated Report.

Risks and opportunities An Integrated Report answers the question: What are the specific risks and opportunities that affect the organization’s ability to create value over the short, medium and long term and how is it dealing with them? This can include identifying:

The external and internal sources of risks and opportunities. External sources derived from the environment

the organisation operates in. Internal sources are those stemming from the organization’s business activities.

The organization’s assessment of the likelihood that a risk or opportunity will arise and the impact if it does.

Including consideration of the specific circumstances that would cause the risk or opportunity to arise. Such disclosure will invariably involve a degree of uncertainty.

The specific steps being taken to mitigate or manage key risks or to create value from key opportunities, including the identification of the associated strategic objectives, strategies, policies, targets and KPIs.

IFRS Entity Financial Statements For the year ended 31 December 2015

6

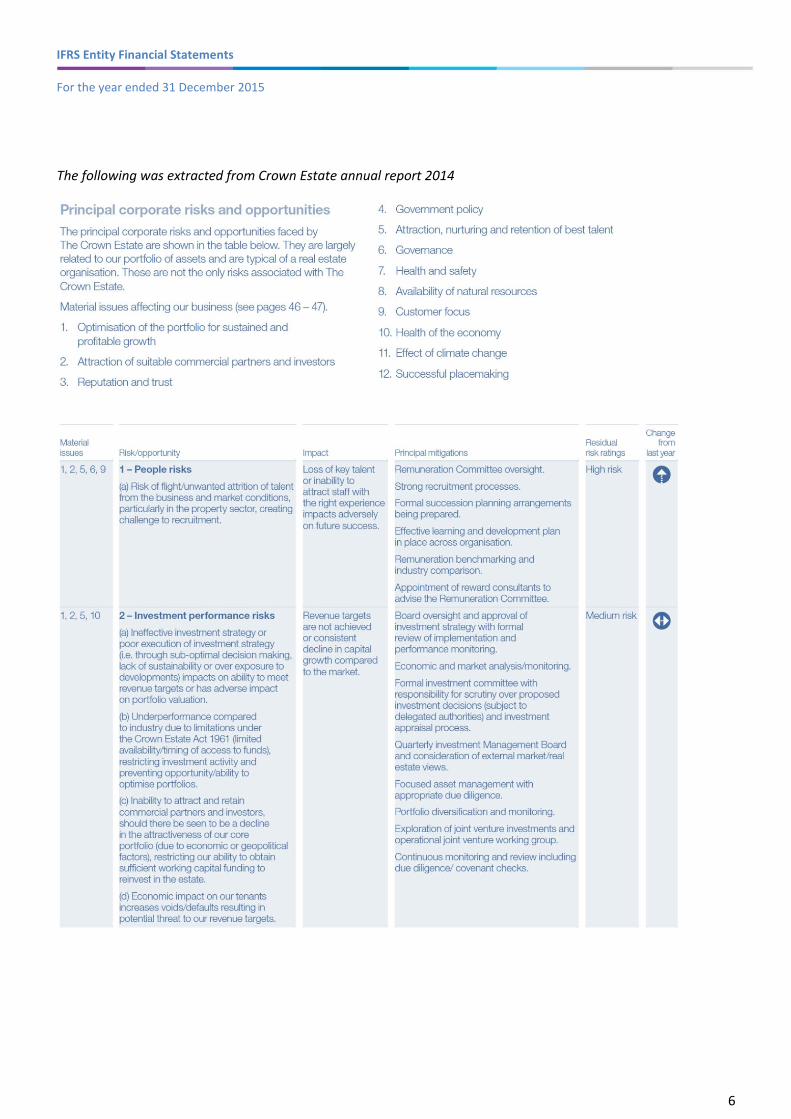

The following was extracted from Crown Estate annual report 2014

IFRS Entity Financial Statements For the year ended 31 December 2015

7

Strategy and resource allocation

An integrated report answers the question: Where does the organization want to go and how does it intend to get there?

An integrated report ordinarily identifies: The organization’s short, medium and long term

strategic objectives. The strategies it has in place, or intends to

implement, to achieve those strategic objectives. The resource allocation plans it has to implement

its strategy. How it will measure achievements and target

outcomes for the short, medium and long term. This can include describing:

The linkage between the organization’s strategy and resource allocation plans, and the information covered by other content, including how its strategy and resource allocation plans:

o Relate to the organization’s business model, and what changes to that business model might be necessary to implement chosen strategies, to provide an understanding of the organization’s ability to adapt to change,

o Are influenced by/respond to the external environment and the identified risks and opportunities.

The figure to the right side is extracted from ABSA Integrated annual report 2011.

Extracted from ABSA integrated annual report 2011

Performance An Integrated Report answers the question: To what extent has the organization achieved its strategic objectives for the period and what are its outcomes in terms of effects on its capitals? An Integrated Report contains qualitative and quantitative information about performance, such as:

Quantitative indicators with respect to targets and risks and opportunities, explaining their significance, their implications, and the methods and assumptions used in compiling them.

The organization’s effects (both positive and negative) on the capitals, including material effects on capitals up and down the value chain.

IFRS Entity Financial Statements For the year ended 31 December 2015

8

The state of key stakeholder relationships and how the organization has responded to key stakeholders’ legitimate needs and interests.

The linkages between past and current performance, and between current performance and the organization’s outlook.

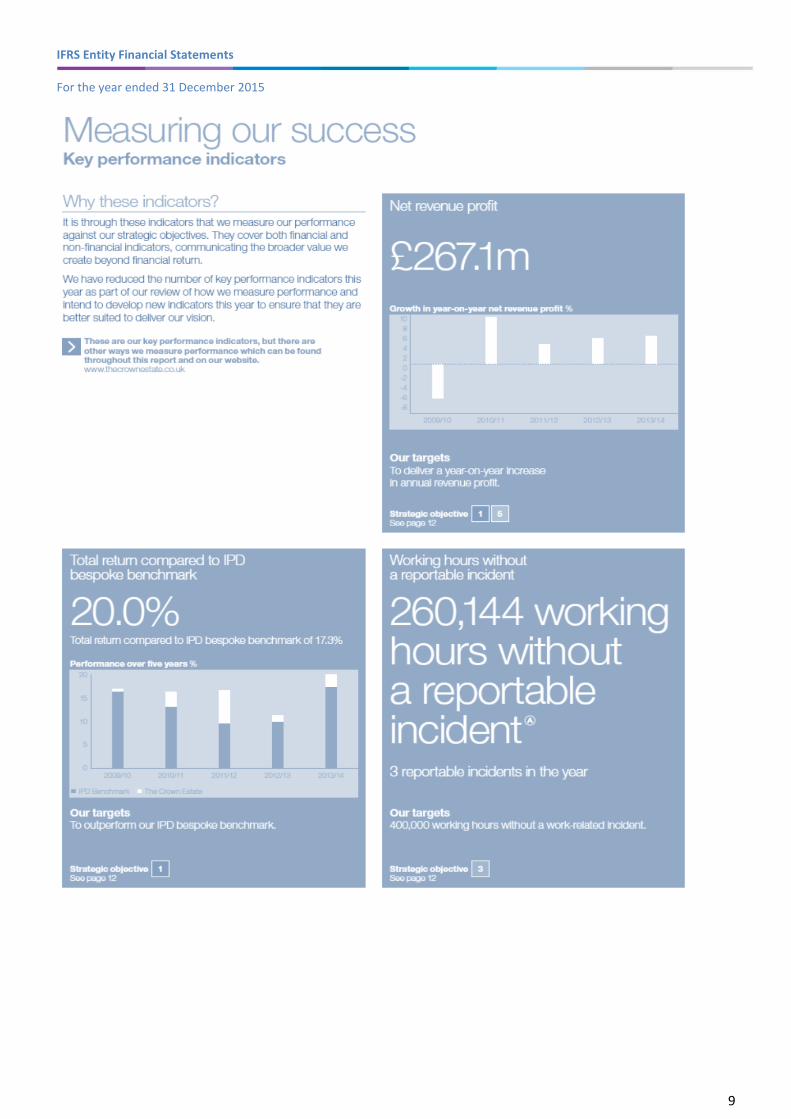

The following illustration is from the Crown Estate Annual Report 2014

IFRS Entity Financial Statements For the year ended 31 December 2015

9

IFRS Entity Financial Statements For the year ended 31 December 2015

10

Future Outlook An Integrated Report answers the question: What challenges and uncertainties is the organization likely to encounter in pursuing its strategy, and what are the potential implications for its business model and future performance? An integrated report highlights anticipated changes over time and provides information, built on sound and transparent analysis, about:

The organization’s expectations about the external environment the organization is likely to face in the short, medium and long term.

How that environment will affect the organization.

How the organization is currently equipped to respond to the critical challenges and uncertainties that are likely to arise.

IFRS Entity Financial Statements For the year ended 31 December 2015

11

Management commentary guidance

Introduction The IASB Practice Statement - Management Commentary provides guidance for the presentation of narrative reporting to accompany financial statements prepared in accordance with IFRSs. The objective of the practice statement is “to assist management in presenting useful management commentary that relates to financial statements prepared in accordance with IFRSs”. [PS (MC) para 1] The Practice Statement requires disclosure about the most important resources, risks and relationships that affect an entity’s value and how they are managed. It enables explanation of the main trends and factors that might affect future performance, and how an entity expects to grow or change in current and future periods. Hence, it combines information about the past, the present and the future. It is applicable prospectively from 8 December 2010. Because of the absence of numbers in this publication it is not possible for a proforma management commentary to be presented therefore we have provided guidance on the questions (by segment, where appropriate) that management in preparing a commentary should seek to address: What is the nature of the entity’s business? In which industries does the entity operate? PS MC 26

Depending on the nature of the business, include an integrated discussion of the following types of information:

a) the industries in which the entity operates; b) the entity's major markets and competitive position within those markets; c) significant features of the legal, regulatory and macro-economic environments that influence the entity and

the markets in which the entity operates; d) the entity’s main products and services, business processes and distribution methods; and e) the entity’s structure and how it creates value. What is the entity’s objective and its business model? What are the entity’s strategies for achieving its objectives? PS MC 27

Statements of objectives and strategies should provide the detail that enables investors to understand the priorities for action or the resources that must be managed to deliver results, as well as explaining how success will be measured and over what period of time. What are the entity’s resources? PS MC 30

Set out the critical financial and non-financial resources available to the entity and how those resources are used in meeting management’s stated objectives for the entity. Useful disclosures may include:

a) Analysis of the adequacy of the entity’s capital structure. b) Financial arrangements (whether or not recognised in the statement of financial position). c) Liquidity and cash flows. d) Human and intellectual capital. e) Surplus resources and identified and expected inadequacies.

What are the risks that will affect sustainability of the performance? What are the plans and strategies for bearing or mitigating risks? How effective were risk management policies? PS MC 31-32

Include a description of the entity’s principal risks and any changes thereto, together with a commentary on management’s plans and strategies for bearing or mitigating those risks and the effectiveness of risk management policies. It is important that entities distinguish their principal risks and uncertainties, rather than list all possible risks without highlighting which are the most important in assessing the potential success of the entity’s strategy. Entities should disclose the strategic, commercial, operational and financial risks where these may significantly affect the entity's strategies and progress of the entity's value.

IFRS Entity Financial Statements For the year ended 31 December 2015

12

What are relationships with stakeholders? PS MC 33

Disclose significant relationships with stakeholders and how they are likely to influence the business performance and its value, and how the entity manages those relationships.

The types of significant relationship that may be appropriate to disclose include:

a) Shareholders – including controlling parties and parties with significant influence over the entity, their involvement in running the business.

b) Customers – this may include management of customer services, details of customer losses and gains − in particular, those on which the entity has a degree of reliance − and new business development.

c) Suppliers – ability to source appropriate suppliers, consideration of raw material availability and prices and vetting of supplier behaviour, etc.

d) Employees – including satisfaction surveys, recruitment and retention, training and development, diversity, health and safety, employee communications, productivity, human rights and ethical trading.

e) Societies and communities in which the entity operates– including environmental impact (for example, noise, pollution and waste), product safety, product responsibility, charitable donations’ and community projects.

f) Lenders and creditors – including, negotiations of credit facilities and other arrangements with lenders and the impact of macro-economic factors on availability of credit.

g) Regulators – including licenses to operate, pricing restrictions, tax negotiations and government discussions on legislation affecting the company.

h) Strategic alliances – including joint ventures, business partnerships, sub-contractors and franchises.

How does the entity measure the extent to which it has achieved its objectives? PS MC 37-40

The practice statement does not prescribe specific performance measures or indicators (KPIs) that entities should disclose however comparability will clearly be enhanced if the measures or indicators are accepted and widely used within an industry sector. Entities are encouraged to disclose the definition of each KPI and its calculation method and explain why the measures are relevant in the context of the chosen strategies and objectives. Where possible entities should also provide sufficient detail on measurement methods to allow users to make comparisons to other entities’ choice of KPI where they wish to do so. When multiple performance measures are disclosed, management should explain which are most important to managing the business. How has the entity performed in the current year compared with the objectives it set in previous periods? To what extent is the performance based on recurring transactions or ‘one-off’ events? PS MC 34

Management commentary should include explanations of the entity’s performance and progress during the period and its position at the end of that period. The analysis of results should be set in the context of the entity’s key performance measures and indicators. Management should provide discussion and analysis of significant changes in financial position, liquidity and performance compared with those of the previous period or periods Unusual, non-recurring or exceptional items should be discussed and fully explained. Entities may express figures in terms of constant currency, so as to show the trends in performance, excluding the effect of exchange rates The management commentary should include a discussion and analysis of significant changes in the entity's financial position and liquidity. What are the entity’s future prospects? What constraints exist that may hamper the entity’s plans? PS MC 36

Management should provide an analysis of the entity's prospects, which may include targets for financial and non-financial measures. When targets are quantified, management should explain the risks and assumptions necessary for users to assess the likelihood of achieving those targets.

IFRS Entity Financial Statements For the year ended 31 December 2015

13

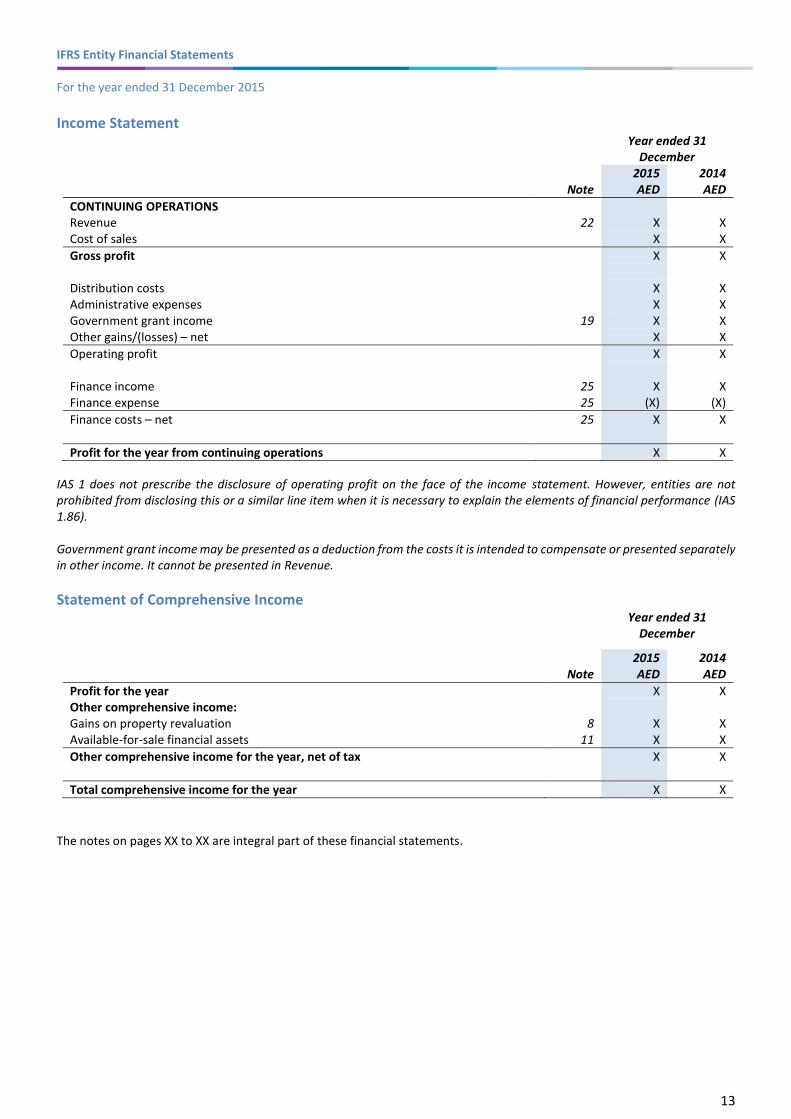

Income Statement

Year ended 31

December

Note 2015 AED

2014 AED

CONTINUING OPERATIONS Revenue 22 X X Cost of sales X X

Gross profit X X Distribution costs X X Administrative expenses X X Government grant income 19 X X Other gains/(losses) – net X X

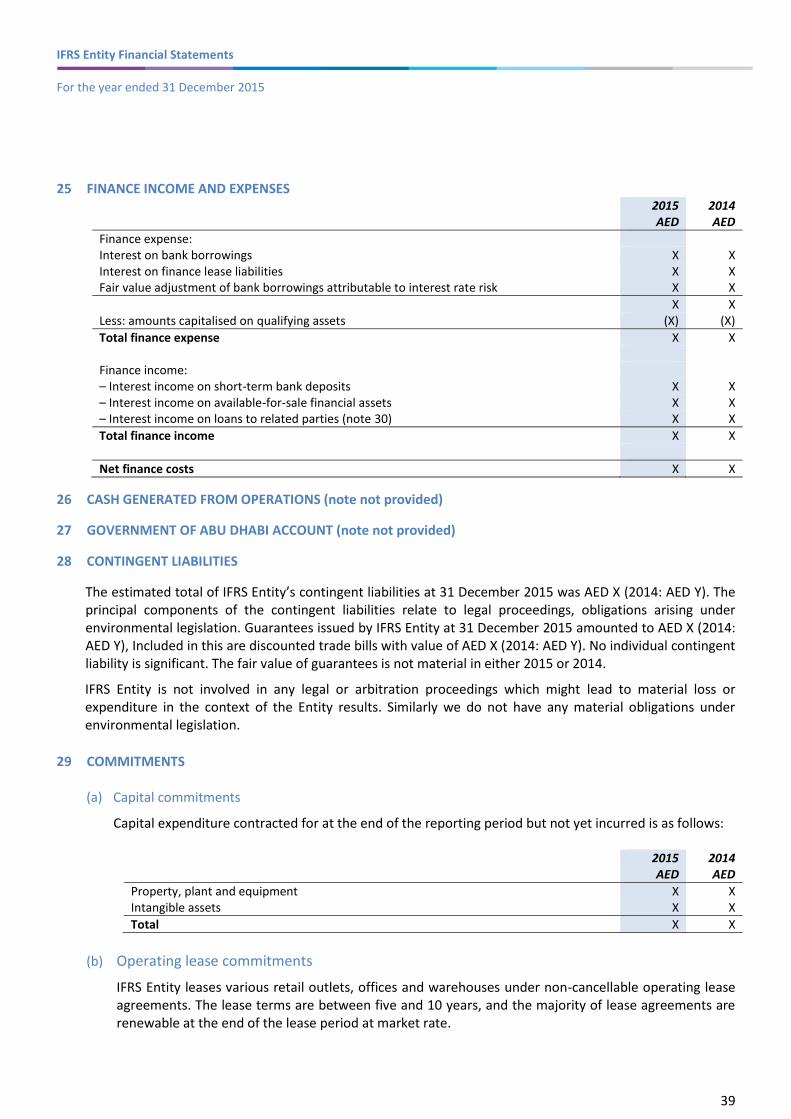

Operating profit X X Finance income 25 X X Finance expense 25 (X) (X)

Finance costs – net 25 X X

Profit for the year from continuing operations X X

IAS 1 does not prescribe the disclosure of operating profit on the face of the income statement. However, entities are not prohibited from disclosing this or a similar line item when it is necessary to explain the elements of financial performance (IAS 1.86). Government grant income may be presented as a deduction from the costs it is intended to compensate or presented separately in other income. It cannot be presented in Revenue.

Statement of Comprehensive Income

Year ended 31 December

Note 2015 AED

2014 AED

Profit for the year X X Other comprehensive income: Gains on property revaluation 8 X X Available-for-sale financial assets 11 X X

Other comprehensive income for the year, net of tax X X

Total comprehensive income for the year X X

The notes on pages XX to XX are integral part of these financial statements.

IFRS Entity Financial Statements For the year ended 31 December 2015

14

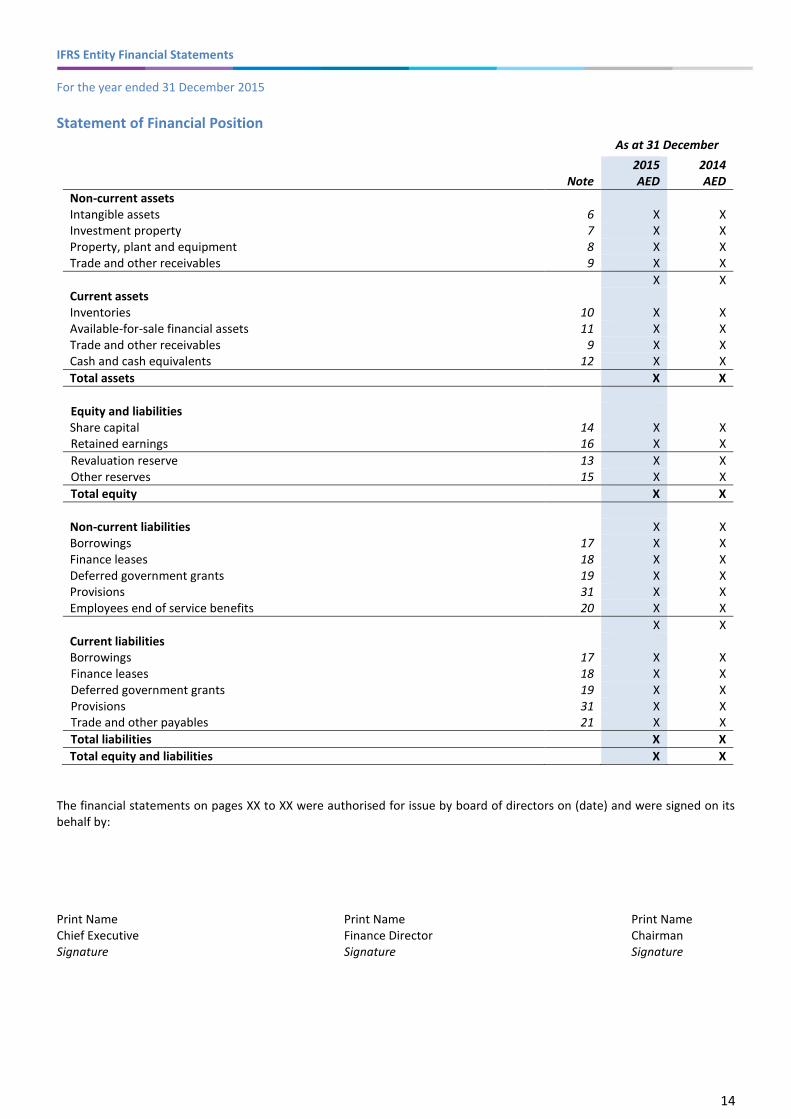

Statement of Financial Position

As at 31 December

Note 2015 AED

2014 AED

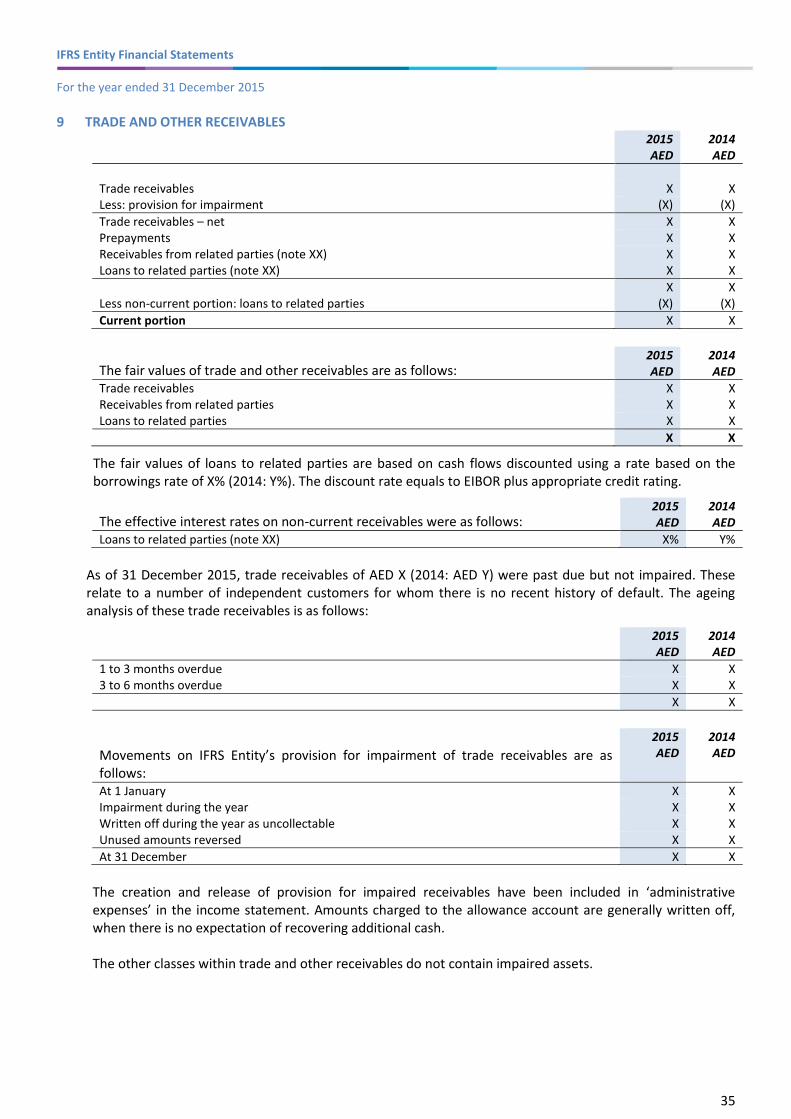

Non-current assets Intangible assets 6 X X Investment property 7 X X Property, plant and equipment 8 X X Trade and other receivables 9 X X

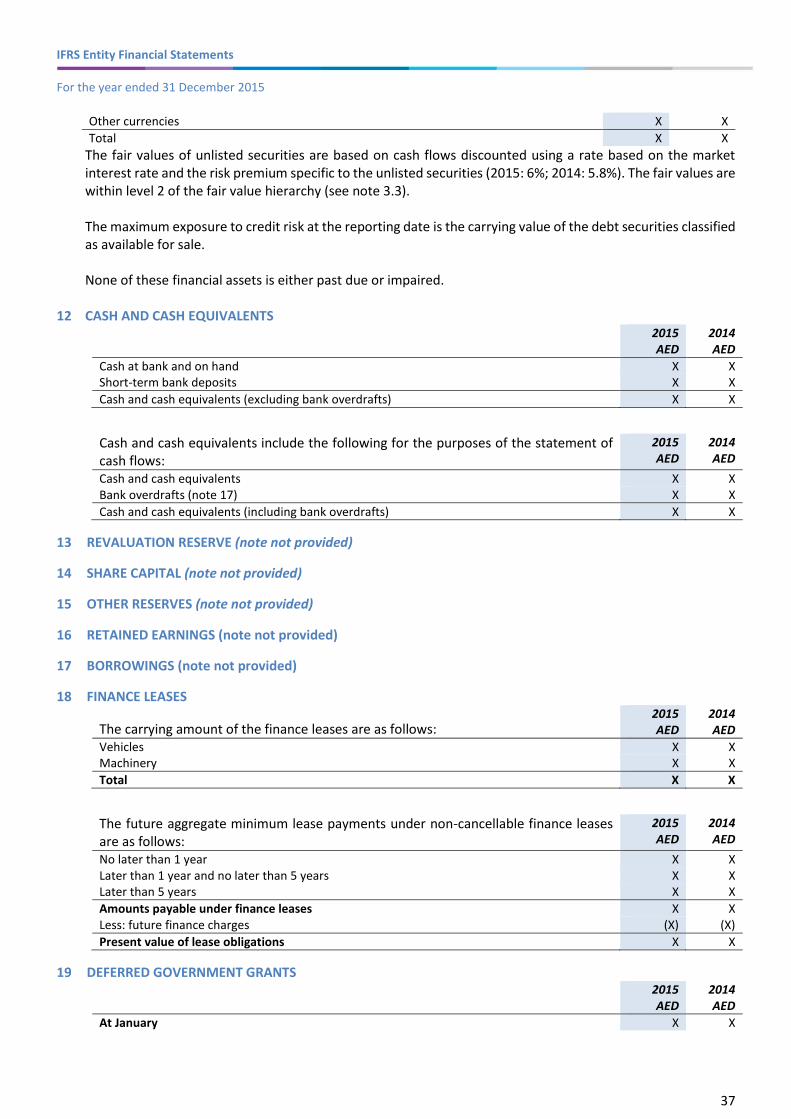

X X Current assets Inventories 10 X X Available-for-sale financial assets 11 X X Trade and other receivables 9 X X Cash and cash equivalents 12 X X

Total assets X X

Equity and liabilities Share capital 14 X X Retained earnings 16 X X

Revaluation reserve 13 X X Other reserves 15 X X

Total equity X X

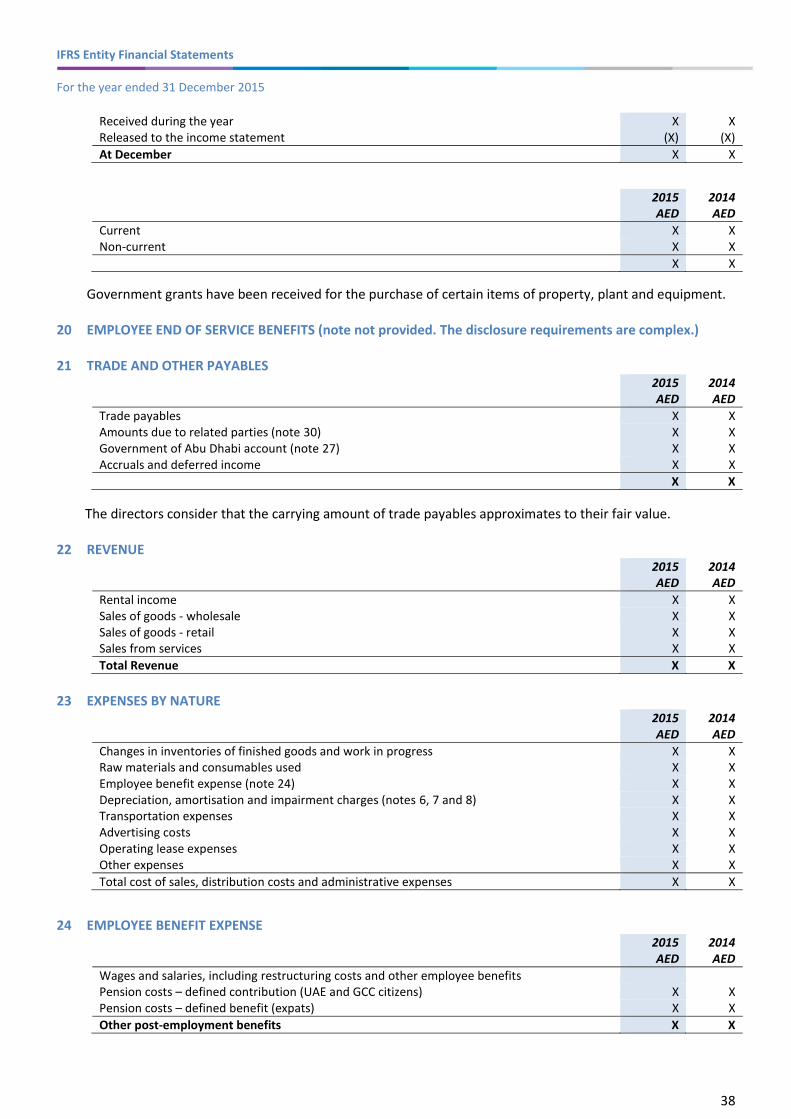

Non-current liabilities X X Borrowings 17 X X Finance leases 18 X X Deferred government grants 19 X X Provisions 31 X X Employees end of service benefits 20 X X

X X Current liabilities Borrowings 17 X X Finance leases 18 X X Deferred government grants 19 X X Provisions 31 X X Trade and other payables 21 X X

Total liabilities X X

Total equity and liabilities X X

The financial statements on pages XX to XX were authorised for issue by board of directors on (date) and were signed on its behalf by: Print Name Print Name Print Name Chief Executive Finance Director Chairman Signature Signature Signature

IFRS Entity Financial Statements For the year ended 31 December 2015

15

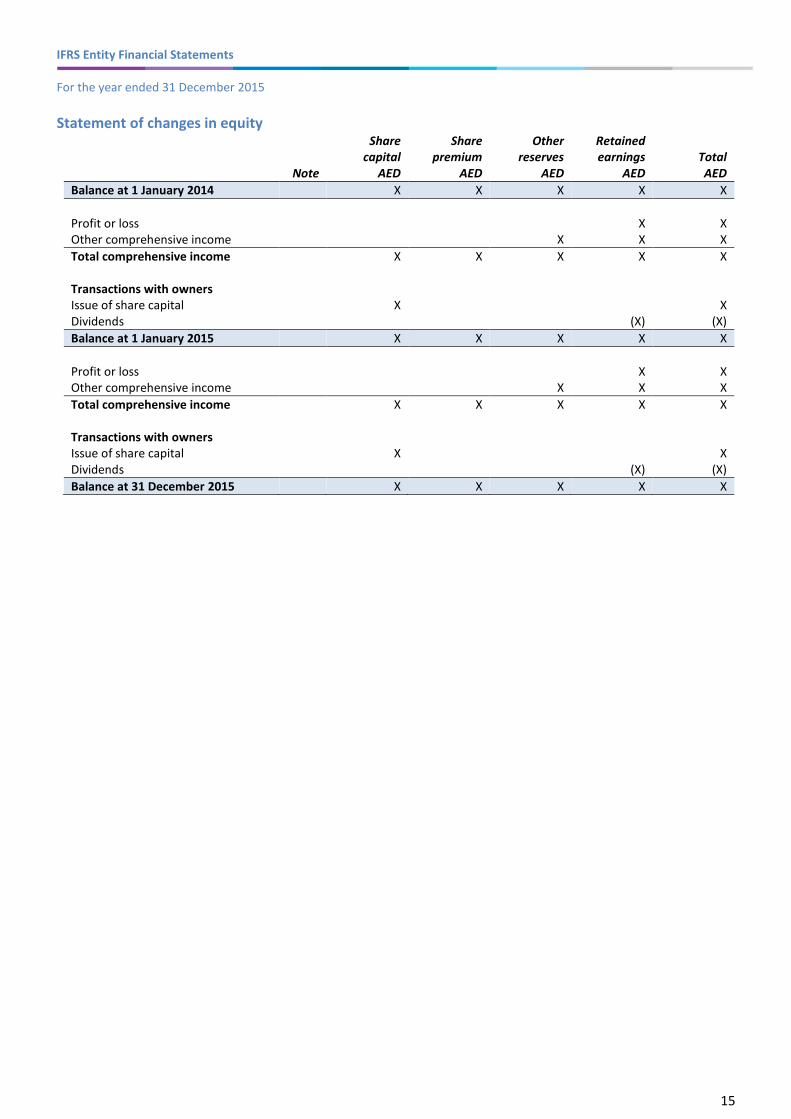

Statement of changes in equity

Note

Share capital

AED

Share premium

AED

Other reserves

AED

Retained earnings

AED Total AED

Balance at 1 January 2014 X X X X X

Profit or loss X X Other comprehensive income X X X

Total comprehensive income X X X X X Transactions with owners Issue of share capital X X Dividends (X) (X)

Balance at 1 January 2015 X X X X X

Profit or loss X X Other comprehensive income X X X

Total comprehensive income X X X X X Transactions with owners Issue of share capital X X Dividends (X) (X)

Balance at 31 December 2015 X X X X X

IFRS Entity Financial Statements For the year ended 31 December 2015

16

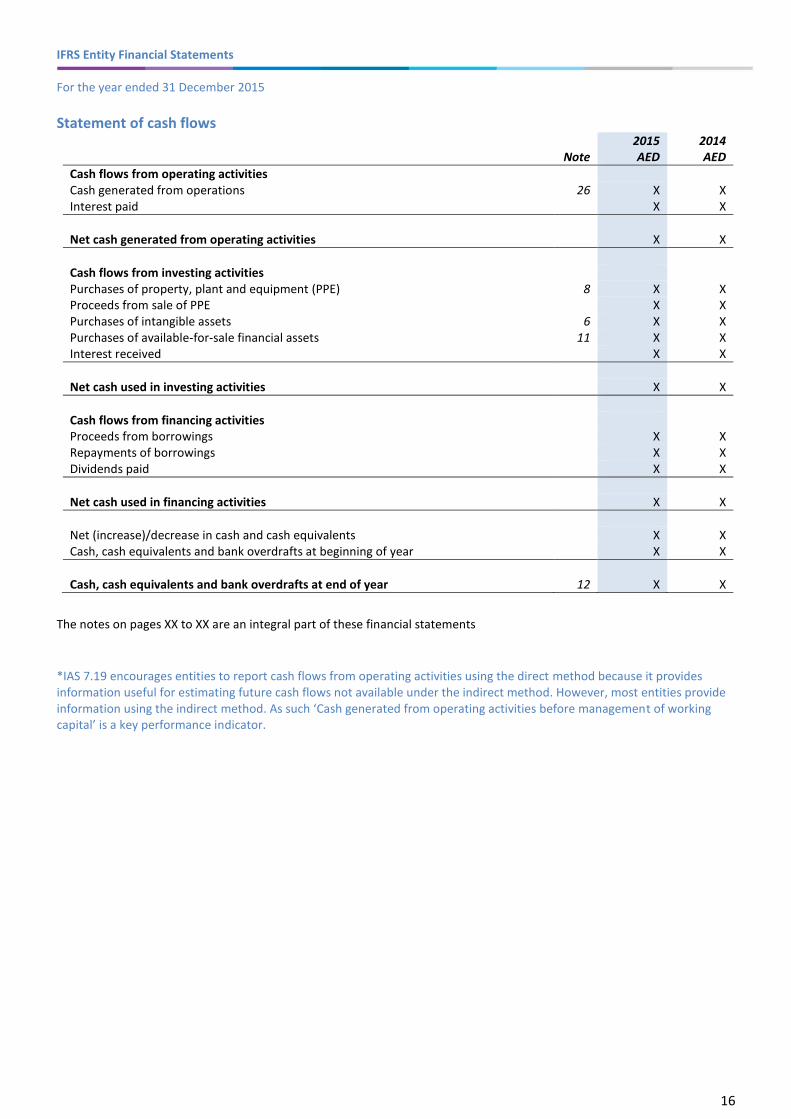

Statement of cash flows

Note 2015 AED

2014 AED

Cash flows from operating activities Cash generated from operations 26 X X Interest paid X X

Net cash generated from operating activities X X

Cash flows from investing activities Purchases of property, plant and equipment (PPE) 8 X X Proceeds from sale of PPE X X Purchases of intangible assets 6 X X Purchases of available-for-sale financial assets 11 X X Interest received X X

Net cash used in investing activities X X

Cash flows from financing activities Proceeds from borrowings X X Repayments of borrowings X X Dividends paid X X

Net cash used in financing activities X X

Net (increase)/decrease in cash and cash equivalents X X Cash, cash equivalents and bank overdrafts at beginning of year X X

Cash, cash equivalents and bank overdrafts at end of year 12 X X

The notes on pages XX to XX are an integral part of these financial statements

*IAS 7.19 encourages entities to report cash flows from operating activities using the direct method because it provides information useful for estimating future cash flows not available under the indirect method. However, most entities provide information using the indirect method. As such ‘Cash generated from operating activities before management of working capital’ is a key performance indicator.

IFRS Entity Financial Statements For the year ended 31 December 2015

17

Notes to the financial statements

1 GENERAL

Disclose:

Name of the reporting entity.

Description of the nature of the entity's operations and its principal activities.

Name of the parent and the ultimate parent of IFRS Entity.

Place of incorporation and domicile, its legal form, country of incorporation, address of registered office and information regarding the length of its life if it is limited life.

2 BASIS OF PREPARATION

The financial statements of IFRS Entity have been prepared in accordance with International Financial Reporting Standards and IFRIC interpretations. The financial statements have been prepared under the historical cost convention, as modified by the revaluation of land and buildings and available-for-sale financial assets.

The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgment in the process of applying IFRS Entity’s accounting policies. The areas involving a higher degree of judgment or complexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in note 3 below.

3 CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS

Estimates and judgments are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

3.1 Critical accounting estimates and assumptions

IFRS Entity makes estimates and assumptions concerning the future. The resulting accounting estimates will, by definition, seldom equal the related actual results. The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are addressed below.

(a) Trade receivables provision

3.2 Critical judgments in applying the entity’s accounting policies

(a) Classification of finance and operating leases Give sufficient details of each estimate/judgement to comply with IAS 1.129 a) b) c) d).

IFRS Entity Financial Statements For the year ended 31 December 2015

18

4 SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated. The requirement in IAS 1.117 is to disclose “significant accounting policies comprising the measurement basis (or bases) used in preparing the financial statements and the other accounting policies used that are relevant to an understanding of the financial statements.” This is not a requirement to disclose all accounting policies including those not material or not relevant. Accounting policies are best understood when they are tailored for an entity and not a reprint of the accounting standard.

4.1 Changes in accounting policy and disclosures

(a) New and amended standards and interpretations

The entity applied for the first time certain standards and amendments, which are effective for annual periods beginning on or after 1 January 2015. The Entity has not early adopted any other standard, interpretation or amendment that has been issued but is not yet effective. These new standards and amendments applied for the first time in 2015, they did not have a material impact on the annual financial statements of the Entity.

Amendments to IAS 19 Defined Benefit Plans: Employee Contributions.

Annual Improvements 2010-2012 Cycle and 2011-2013 Cycle.

Although IAS 8.28 requires an explanation of the change. It is not provided as the explanation can be easily researched and the impact is not relevant to an understanding of the financial statements of IFRS Group. IFRS Entity has not early adopted any other standard, interpretation or amendment that has been issued but is not yet effective.

(b) New standards, amendments and interpretations not yet adopted (IAS 8.30)

(c) “When an entity has not applied a new IFRS that has been issued but is not yet effective, the entity shall disclose:

(d) (a) this fact; and (e) (b) known or reasonably estimable information relevant to assessing the possible impact that

application of the new IFRS will have on the entity's financial statements in the period of initial application.

(f) (g) 31. In complying with paragraph 30, an entity considers disclosing: (h) (a) the title of the new IFRS; (i) (b) the nature of the impending change or changes in accounting policy; (j) (c) the date by which application of the IFRS is required; (k) (d) the date as at which it plans to apply the IFRS initially; and (l) (e) either: (m) (i) a discussion of the impact that initial application of the IFRS is expected to have on the entity's

financial statements; or (ii) if that impact is not known or reasonably estimable, a statement to that effect.”

There are three significant IFRSs issued that are not yet effective: IFRS 9 Financial Instruments. IFRS 15 Revenue from contracts with customers, and IFRS 16 Leases.

IFRS Entity Financial Statements For the year ended 31 December 2015

19

The standards and interpretations that are issued, but not yet effective, up to the date of issuance of the Entity’s financial statements are disclosed below. The Entity intends to adopt these standards, if applicable, when they become effective. IFRS 9 Financial Instruments

In July 2014, the IASB issued the final version of IFRS 9 Financial Instruments that replaces IAS 39 Financial Instruments: Recognition and Measurement and all previous versions of IFRS 9. IFRS 9 brings together all three aspects of the accounting for financial instruments project: classification and measurement, impairment and hedge accounting. IFRS 9 is effective for annual periods beginning on or after 1 January 2018, with early application permitted. Except for hedge accounting, retrospective application is required but providing comparative information is not compulsory. For hedge accounting, the requirements are generally applied prospectively, with some limited exceptions. (a) Classification and measurement

The Entity does not expect a significant impact on its balance sheet or equity on applying the classification and measurement requirements of IFRS 9. It expects to continue measuring at fair value all financial assets currently held at fair value. Quoted equity shares currently held as available-for-sale with gains and losses recorded in OCI will be measured at fair value through profit or loss instead, which will increase volatility in recorded profit or loss. The AFS reserve currently in accumulated OCI will be reclassified to opening retained earnings. Debt securities are expected to be measured at fair value through OCI under IFRS 9 as the Entity expects not only to hold the assets to collect contractual cash flows but also to sell a significant amount on a relatively frequent basis. The equity shares in non-listed companies are intended to be held for the foreseeable future. The Entity expects to apply the option to present fair value changes in OCI, and, therefore, believes the application of IFRS 9 would not have a significant impact. If the Entity were not to apply that option, the shares would be held at fair value through profit or loss, which would increase the volatility of recorded profit or loss.

Loans as well as trade receivables are held to collect contractual cash flows and are expected to give rise to cash flows representing solely payments of principal and interest. Thus, the Entity expects that these will continue to be measured at amortised cost under IFRS 9. However, the Entity will analyse the contractual cash flow characteristics of those instruments in more detail before concluding whether all those instruments meet the criteria for amortised cost measurement under IFRS 9. (b) Impairment

IFRS 9 requires the Entity to record expected credit losses on all of its debt securities, loans and trade receivables, either on a 12-month or lifetime basis. The Entity expects to apply the simplified approach and record lifetime expected losses on all trade receivables. The Entity expects a significant impact on its equity due to unsecured nature of its loans and receivables, but it will need to perform a more detailed analysis which considers all reasonable and supportable information, including forward-looking elements to determine the extent of the impact. The statement above appears to be the industry’s default position. HSBC reports “HSBC intends to quantify the potential impact of IFRS 9 once it is practicable to provide reliable estimates, which will be no later than in the Annual Report and Accounts 2017.” HSBC annual report. RBS reports “A single bank-wide programme has been established to implement the necessary changes in the modelling of credit loss parameters, and the underlying credit management and financial processes; this programme is jointly led by Risk and Finance. The inclusion of loss allowance on all financial assets will tend to result in an increase in overall impairment balances when compared with the existing basis of measurement under IAS 39.” RBS Annual report.

IFRS Entity Financial Statements For the year ended 31 December 2015

20

PWC provide Illustrative disclosures: IFRS 9 Financial Instruments on the types of disclosures that would be required if a fictitious company, VALUE IFRS 9 Plc, had decided to adopt IFRS 9 for its reporting period ending 31 December 2015. Supporting commentary is also provided. Available to PWC Inform users. IAS 8 BC 31 states that the requirement to disclose information only if it is known, or reasonably estimable. This clarification responded to comments on the Exposure Draft that the proposed disclosures would sometimes be impractical. (c) Hedge accounting

The Entity believes that all existing hedge relationships that are currently designated in effective hedging relationships will still qualify for hedge accounting under IFRS 9. As IFRS 9 does not change the general principles of how an entity accounts for effective hedges, the Entity does not expect a significant impact as a result of applying IFRS 9. The Entity will assess possible changes related to the accounting for the time value of options, forward points or the currency basis spread in more detail in the future.

IFRS 14 Regulatory Deferral Accounts

IFRS 14 is not relevant to ADAA Subject Entities and therefore any reference to it can be omitted. IFRS 15 Revenue from Contracts with Customers

The impact of IFRS 15 is difficult to discern. It is a much longer standard than IAS 18 it replaces. It is accompanied by very detailed basis of conclusions and numerous illustrative examples. IAS 18 was a risk and rewards based standard. IFRS 15 is controls based. Sector specific issues are emerging. KPMG IFRS 15 for sectors. Oil & Gas. Telcos. Housebuilders. Power & Utilities. Transport. Consumer goods. Insurance. Construction. IFRS 15 was issued in May 2014 and establishes a five-step model to account for revenue arising from contracts with customers. Under IFRS 15, revenue is recognised at an amount that reflects the consideration to which an entity expects to be entitled in exchange for transferring goods or services to a customer. The new revenue standard will supersede all current revenue recognition requirements under IFRS. Either a full retrospective application or a modified retrospective application is required for annual periods beginning on or after 1 January 2018, when the IASB finalises their amendments to defer the effective date of IFRS 15 by one year. Early adoption is permitted. The Entity plans to adopt the new standard on the required effective date using the full retrospective method. During 2015, the Entity performed a preliminary assessment of IFRS 15, which is subject to changes arising from a more detailed ongoing analysis. Furthermore, the Entity is considering the clarifications issued by the IASB in an exposure draft in July 2015 and will monitor any further developments. The Entity is in the business of providing fire prevention and electronics equipment and services. The equipment and services are sold both on its own in separate identified contracts with customers and together as a bundled package of goods and/or services. (a) Sale of goods

Contracts with customers in which equipment sale is the only performance obligation are not expected to have any impact on the Entity. The Entity expects the revenue recognition to occur at a point in time when control of the asset is transferred to the customer, generally on delivery of the goods. In applying IFRS 15, the Entity considered the following:

(i) Variable consideration

Some contracts with customers provide a right of return, trade discounts or volume rebates. Currently, the Entity recognises revenue from the sale of goods measured at the fair value of the consideration received or receivable, net of returns and allowances, trade discounts and volume rebates. If revenue cannot be reliably measured, the Entity defers revenue recognition until the uncertainty is resolved. Such provisions give rise to

IFRS Entity Financial Statements For the year ended 31 December 2015

21

variable consideration under IFRS 15, and will be required to be estimated at contact inception. IFRS 15 requires the estimated variable consideration to be constrained to prevent over-recognition of revenue. The Entity continues to assess individual contracts to determine the estimated variable consideration and related constraint. The Entity expects that application of the constraint may result in more revenue being deferred than is under current IFRS. (ii) Warranty obligations

The Entity provides warranties for general repairs and does not provide extended warranties or maintenance services in its contracts with customers. As such, the Entity determines that such warranties are assurance type warranties which will continue to be accounted for under IAS 37 Provisions, Contingent Liabilities and Contingent Assets consistent with its current practice. (iii) Loyalty points programme

The Entity determines that the loyalty programme offered within its electronic segment gives rise to a separate performance obligation because it provides a material right to the customer. Thus, it will need to allocate a portion of the transaction price to the loyalty programme based on relative stand-alone selling price instead of the allocation methodologies allowed under IFRIC 13 Customer Loyalty Programmes. As a result, the Entity expects a change in the allocation of the consideration received and consequently the timing of the amount of revenue recognised in relation to the loyalty programme may be impacted. Consistent with current requirements in IFRIC 13, the Entity expects that the revenue will still be recognised when the loyalty points are redeemed or expire. The Entity is still analysing contracts with customers that have such elements and will need to perform further assessments in the future to quantify the financial impact to its financial statements. (b) Rendering of services

The Entity provides installation services within the fire prevention segment. These services are sold either on their own in contracts with the customers while others may be bundled together with the sale of equipment to a customer. The Entity has preliminarily assessed that the services are satisfied over time given that the customer simultaneously receives and consumes the benefits provided by the Entity. Consequently, the Entity does not expect any significant impact to arise from these service contracts. Equipment received from customers

When an entity receives, or expects to receive, non-cash consideration, IFRS 15 requires that the fair value of the non-cash consideration is included in the transaction price. An entity would have to measure the fair value of the non-cash consideration in accordance with IFRS 13 Fair Value Measurement. The Entity receives transfers of moulds and other tools for its manufacturing process from customers, which are recognised at fair value as property, plant and equipment under IFRIC 18 Transfers of Assets from Customers. This is consistent with the requirements of IFRS 15 and the Entity does not expect equipment received from customers to have any resultant significant impact. The current response from IFRS reporters to IFRS 16 is similar to Vodafone’s report “Revenue from Contracts with Customers” was issued in May 2015; although it is effective for accounting periods beginning on or before 1 January 2017, the IASB has proposed to defer the mandatory adoption date by one year. IFRS 15 has not yet been adopted by the EU. IFRS 15 will have a material impact on the Group’s reporting of revenue and costs as follows:

IFRS 15 will require the Group to identify deliverables in contracts with customers that qualify as “performance obligations”. The transaction price receivable from customers must be allocated between the Group’s performance obligations under the contracts on a relative stand-alone selling price basis. Currently revenue allocated to deliverables is restricted to the amount that is receivable without the delivery of additional goods or services; this restriction will no longer be applied under IFRS 15. The primary impact on revenue reporting will be that when the Group sells subsidised devices together with airtime service agreements to customers, revenue allocated to equipment and recognised when control

IFRS Entity Financial Statements For the year ended 31 December 2015

22

of the device passes to the customer will increase and revenue recognised as services are delivered will reduce.

Under IFRS 15, certain incremental costs incurred in acquiring a contract with a customer will be deferred on the balance sheet and amortised as revenue is recognised under the related contract; this will generally lead to the later recognition of charges for some commissions payable to third party dealers and employees.

Certain costs incurred in fulfilling customer contracts will be deferred on the balance sheet under IFRS 15 and recognised as related revenue is recognised under the contract. Such deferred costs are likely to relate to the provision of deliverables to customers that do not qualify as performance obligations and for which revenue is not recognised; currently such costs are generally expensed as incurred.

The Group is currently assessing the impact of these and other accounting changes that will arise under IFRS 15; however, the changes highlighted above are expected to have a material impact on the consolidated income statement and consolidated statement of financial position. It is expected that the Group will adopt IFRS 15 on 1 April 2018.” Vodafone annual report. PWC provide Illustrative IFRS 15 disclosures that would be required if a fictitious company, VALUE IFRS Plc, had decided to adopt IFRS 15,' Revenue from contracts with customers', for its reporting period ending 31 December 2015. Supporting commentary is also provided. Available to PWC Inform users. And in KPMG Guide to annual financial statements – IFRS 15 supplement. We consider entities should make an informed estimate and provide a number or a range of numbers, and if not they should explain what information they don’t have that is necessary in order to make the estimate and the stage they have reached in their project to acquire the necessary information. IFRS 16 leases

IFRS already requires disclosure of the period and amounts payable for operating and finance leases. Therefore the impact of IFRS 16 should not be that difficult to estimate. It too is much longer standard than IAS 17 it replaces. It is also accompanied by very detailed basis of conclusions and numerous illustrative examples. IAS 17 was a risk and rewards based standard. IFRS 16 is controls based. IFRS 16 was issued in January 2016. The Entity plans to adopt the new standard on the required effective date. Under the new Standard, a lessee recognizes a right-of-use asset and a lease liability. The right-of-use asset is treated similarly to other non-financial assets and depreciated accordingly. The liability accrues interest. This will typically produce a front-loaded expense profile (whereas operating leases under IAS 17 would typically have had straight-line expenses). A front-loaded expense profile arises, for example, when a lessee recognizes: (i) a right of use (ROU) asset which is typically amortized on a straight line basis; and (ii) a liability to pay lease rentals, which would be accounted for like a mortgage loan with higher interest charges in the early years. The combined effect is a front-loaded expense in the income statement, even if the lessee pays the same amount of rent each period. The lease liability is initially measured at the present value of the lease payments payable over the lease term, discounted at the rate implicit in the lease if that can be readily determined. If that rate cannot be readily determined, the lessee shall use their incremental borrowing rate. With respect to identifying a lease, a contract is, or contains, a lease if it conveys the right to control the use of an identified asset for a period of time in exchange for consideration. Control is conveyed where the customer has both the right to direct the identified asset’s use and to obtain substantially all the economic benefits from that use. The new Standard includes certain recognition exemptions. Instead of applying the recognition requirements of IFRS 16 described above, a lessee may elect to account for lease payments as an expense on a straight-line basis over the lease term or another systematic basis for the following two types of leases: (i) leases with a lease term of 12 months or less and containing no purchase options – this election is made by class of

IFRS Entity Financial Statements For the year ended 31 December 2015

23

underlying asset; and (ii) leases where the underlying asset has a low value when new (such as personal computers or small items of office furniture) – this election can be made on a lease-by-lease basis. IFRS 16 is effective for annual reporting periods beginning on or after January 1, 2019. Earlier application is permitted if IFRS 15, Revenue from Contracts with Customers, has also been applied.

Other standards amended that are not likely to have any significant impact

Amendments to IFRS 11 Joint Arrangements: Accounting for Acquisitions of Interests

Amendments to IAS 16 and IAS 38: Clarification of Acceptable Methods of Depreciation and Amortisation

Amendments to IAS 16 and IAS 41 Agriculture: Bearer Plants

Amendments to IAS 27: Equity Method in Separate Financial Statements

Amendments to IFRS 10 and IAS 28: Sale or Contribution of Assets between an Investor and its Associate

or Joint Venture

Annual Improvements 2012-2014 Cycle

IFRS 5 Non-current Assets Held for Sale and Discontinued Operations

IFRS 7 Financial Instruments: Disclosures

IAS 19 Employee Benefits Amendments to IAS 1 Disclosure Initiative

Amendments to IFRS 10, IFRS 12 and IAS 28 Investment Entities: Applying the Consolidation Exception

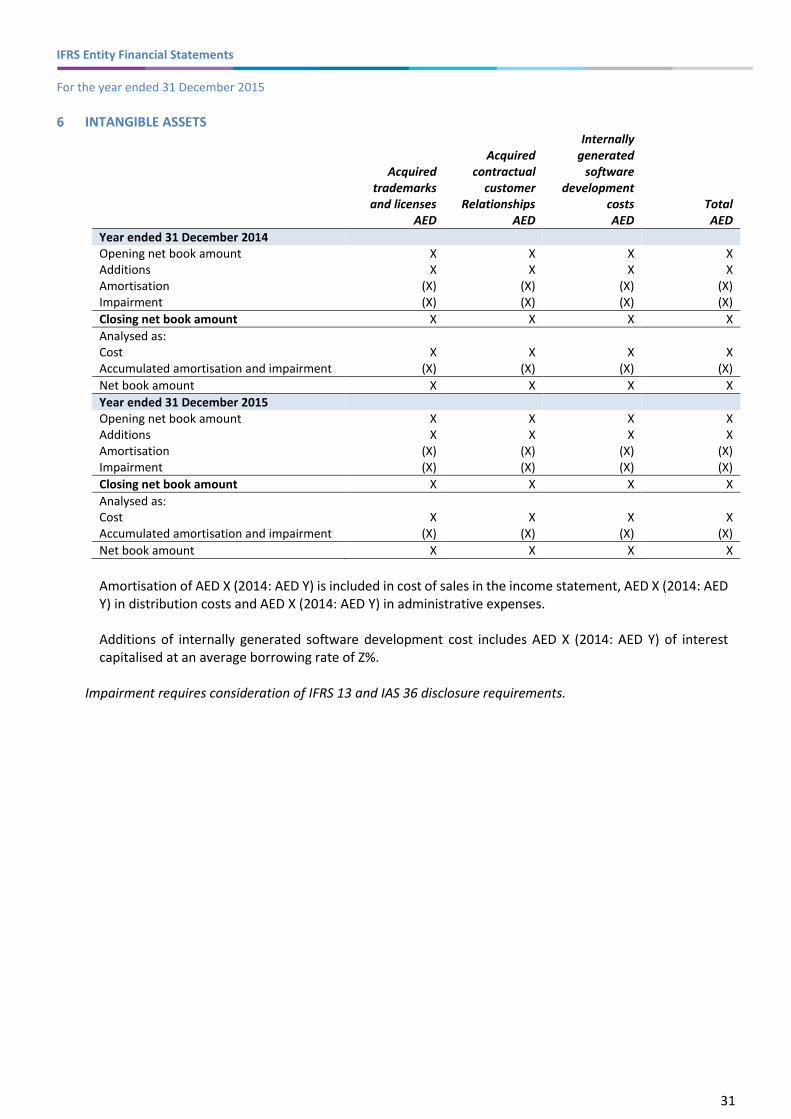

4.2 Intangible assets

Intangible assets that have an indefinite useful life or intangible assets not ready to use are not subject to amortisation and are tested annually for impairment. Assets that are subject to amortisation are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs of disposal and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are largely independent cash inflows (cash-generating units). Prior impairments of non-financial assets (other than goodwill) are reviewed for possible reversal at each reporting date.

(a) Contractual customer relationships

Contractual customer relationships acquired from third parties are recognised at cost at the acquisition date. The contractual customer relationships have a finite useful life and are carried at cost less accumulated amortisation. Amortisation is calculated using the straight-line method over the expected life of the customer relationship.

(b) Trademarks and licenses

Separately acquired trademarks and licenses are shown at historical cost. Trademarks and licenses have a finite useful life and are carried at cost less accumulated amortisation. Amortisation is calculated using the straight-line method to allocate the cost of trademarks and licenses over their estimated useful lives of 15 to 20 years.

(c) Computer software

Costs associated with maintaining computer software programmes are recognised as an expense as incurred. Development costs that are directly attributable to the design and testing of identifiable and unique software products controlled by IFRS Entity are recognised as intangible assets when the following criteria are met:

It is technically feasible to complete the software product so that it will be available for use;

IFRS Entity Financial Statements For the year ended 31 December 2015

24

Management intends to complete the software product and use or sell it; and there is an ability to use or sell the software product;

It can be demonstrated how the software product will generate probable future economic benefits;

Adequate technical, financial and other resources to complete the development and to use or sell the software product are available; and

The expenditure attributable to the software product during its development can be reliably measured.

Directly attributable costs that are capitalised as part of the software product include the software development employee costs and an appropriate portion of relevant overheads. Other development expenditures that do not meet these criteria are recognised as an expense as incurred. Development costs previously recognised as an expense are not recognised as an asset in a subsequent period.

Computer software development costs recognised as assets are amortised over their estimated useful lives, which does not exceed three years.

4.3 Impairment of non-financial assets Intangible assets that have an indefinite useful life or intangible assets not ready to use are not subject to amortisation and are tested annually for impairment. Assets that are subject to amortisation are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs of disposal and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are largely independent cash inflows (cash-generating units). Prior impairments of non-financial assets (other than goodwill) are reviewed for possible reversal at each reporting date.

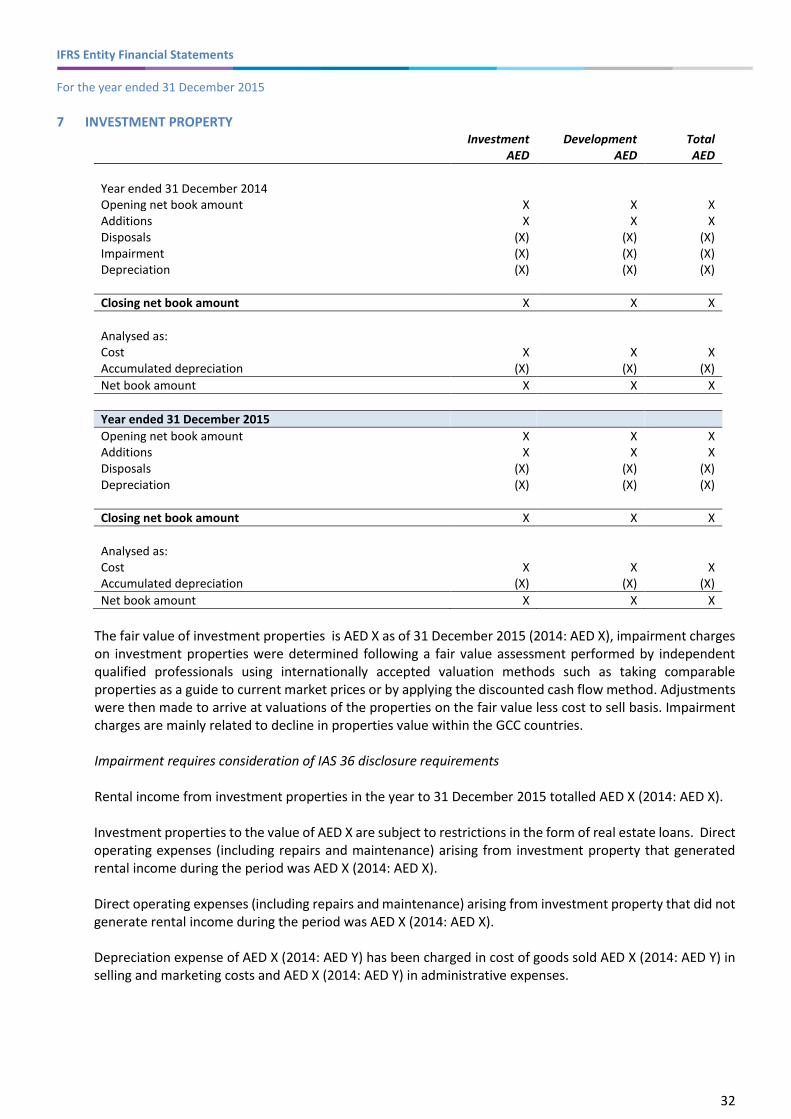

4.4 Investment property

Investment property is property held to earn rental income and/or for capital appreciation rather than for the purpose of operating activities. Investment property assets are carried at cost less accumulated depreciation and any recognised impairment in value. The depreciation policies for investment property are consistent with those for buildings within the category of Property, Plant and Equipment.

For disclosure purposes fair values are evaluated annually by an accredited external, independent valuer, applying a valuation model recommended by the International Valuation Standards Committee.

Disposals are recognised on completion: profits and losses arising are recognised through the income statement, the profit on disposal is determined as the difference between the sales proceeds and the carrying amount of the asset.

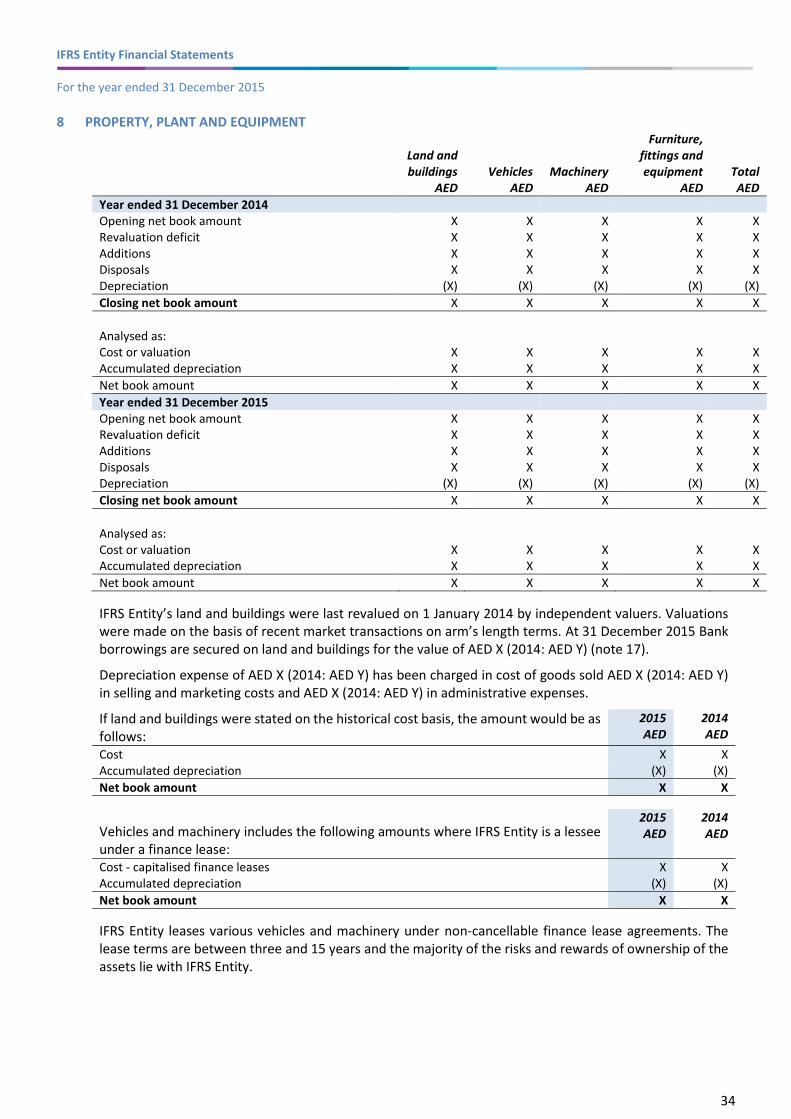

4.5 Property, plant and equipment

After initial recognition land and buildings are carried at fair value, (being the fair value at the date of revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses) with sufficient regularity to ensure that its carrying amount is not materially different from its fair value at the end of the reporting period. Fair value is usually determined from market based evidence by appraisal that is normally undertaken by professionally qualified valuers. All other property, plant and equipment is stated at historical cost less depreciation. Historical cost includes expenditure that is directly attributable to the acquisition of the items.

Land is not depreciated. Depreciation on other assets is calculated using the straight-line method to allocate their cost or revalued amounts to their residual values over their estimated useful lives, as follows:

IFRS Entity Financial Statements For the year ended 31 December 2015

25

Asset class Life

Buildings 25-40 years Machinery 10-15 years Vehicles 3-5 years Furniture, fittings and equipment 3-8 years

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at the end of each reporting period.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount. Gains and losses on disposals are determined by comparing the proceeds with the carrying amount and are recognised within ‘Other gains/ (losses) – net’ in the income statement.

The frequency of revaluations depends upon the changes in fair values of the items of property, plant and equipment being revalued. When the fair value of a revalued asset differs materially from its carrying amount, a further revaluation is required.

4.6 Trade receivables

Trade receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision for impairment.

If collection is expected in one year or less (or in the normal operating cycle of the business if longer), they are classified as current assets. If not, they are classified as non-current assets.

4.7 Inventories

Inventories are stated at the lower of cost and net realisable value. Cost is determined using the first-in, first-out (FIFO) method. The cost of finished goods and work in progress comprises design costs, raw materials, direct labour, other direct costs and related production overheads (based on normal operating capacity). It excludes borrowing costs.

Net realisable value is the estimated selling price in the ordinary course of business, less applicable variable selling expenses.

4.8 Available for-sale financial assets

Available-for-sale financial assets are non-derivatives that are either designated in this category or not classified in any of the other categories. They are included in non-current assets unless the investment matures or management intends to dispose of it within 12 months of the end of the reporting period.

Regular purchases and sales of financial assets are recognised on the trade-date the date on which IFRS Entity commits to purchase or sell the asset. Investments are initially (and subsequently) recognised at fair value and transaction costs are expensed in the income statement. Financial assets are derecognised when the rights to receive cash flows from the investments have expired or have been transferred and IFRS Entity has transferred substantially all risks and rewards of ownership.

Gains or losses arising from changes in the fair value of available for sale financial assets are recognised in other comprehensive income in the period in which they arise. Dividend income from financial assets is recognised as part of other income when IFRS Entity’s right to receive payments is established. On sale accumulated gains and losses on available for sale financial assets recognised in other comprehensive income are included in the Income Statement within ‘other gains and losses – net.’

IFRS Entity assesses at the end of each reporting period whether there is objective evidence that a financial asset or a group of financial assets is impaired. For equity investments classified as available-for-sale, a significant or prolonged decline in the fair value of the security below its cost is evidence that the assets are

IFRS Entity Financial Statements For the year ended 31 December 2015

26

impaired. If any such evidence exists for available-for-sale financial assets, the cumulative loss-measured as the difference between the acquisition cost and the current fair value, less any impairment loss on that financial asset previously recognised in profit or loss is recognised in the income statement. Impairment testing of trade receivables is described in note 9.

4.9 Offsetting financial instruments

Financial assets and liabilities are offset and the net amount reported in the balance sheet when there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis or realise the asset and settle the liability simultaneously. The legally enforceable right must not be contingent on future events and must be enforceable in the normal course of business and in the event of default, insolvency or bankruptcy of the company or the counterparty.

4.10 Cash and cash equivalents

In the statement of cash flows, cash and cash equivalents includes cash in hand, deposits held at call with banks, other short-term highly liquid investments with original maturities of three months or less and bank overdrafts. In the statement of financial position, bank overdrafts are shown within borrowings in current liabilities.

4.11 Share capital

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new ordinary shares or options are shown in equity as a deduction, from the proceeds.

4.12 Borrowings

Borrowings are recognised initially at fair value, net of transaction costs incurred. Borrowings are subsequently carried at amortised cost; any difference between the proceeds (net of transaction costs) and the redemption value is recognised in the income statement over the period of the borrowings using the effective interest method.

4.13 Trade payables

Trade payables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method.

Accounts payable are classified as current liabilities if payment is due within one year or less (or in the normal operating cycle of the business if longer). If not, they are presented as non-current liabilities.

4.14 Leases

Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments made under operating leases (net of any incentives received from the lessor) are charged to the income statement on a straight-line basis over the period of the lease. In determining whether a lease is a finance lease or an operating lease careful consideration is given to:

a) The period of the lease term, whether there are any options to extend and the likelihood of IFRS entity opting to extend.

b) Payments described as contingent payments or contingent rent. If the nature of the contingent amount is such that it is more likely than not to become payable under IFRS Entity’s normal or (expected) business operations, then these payments are not contingent and are deemed part of the normal lease payments.

IFRS Entity leases certain property, plant and equipment. Leases of property, plant and equipment where IFRS Entity has substantially all the risks and rewards of ownership are classified as finance leases. Finance leases are capitalised at the lease’s commencement at the lower of the fair value of the leased property and the present value of the minimum lease payments.

IFRS Entity Financial Statements For the year ended 31 December 2015

27

Each lease payment is allocated between the liability and finance charges. The corresponding rental obligations, net of finance charges, are included in current or non-current liabilities. The interest element of the finance cost is charged to the income statement over the lease period so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period. Property, plant and equipment acquired under finance lease are depreciated over the shorter of the useful life of the asset and the lease term.

4.15 Revenue recognition

Revenue comprises the fair value of the consideration received or receivable for the sale of goods and services in the ordinary course of IFRS Entity’s activities. Revenue is shown net of returns, rebates and discounts.

Revenue is recognised when the amount of revenue can be reliably measured, it is probable that future economic benefits will flow to the entity and when specific criteria have been met for each of the Company’ activities as described below. IFRS Entity bases its estimates on historical results, taking into consideration the type of customer, the type of transaction and the specifics of each arrangement.

Sales of goods – wholesale

IFRS entity manufactures and sells a range of products in the wholesale market.

Sales of goods are recognised when IFRS Entity has delivered products to the wholesaler, the wholesaler has full discretion over the channel and price to sell the products, and there is no unfulfilled obligation that could affect the wholesaler’s acceptance of the products. Delivery does not occur until the products have been shipped to the specified location, the risks of obsolescence and loss have been transferred to the wholesaler, and either the wholesaler has accepted the products in accordance with the sales contract, the acceptance provisions have lapsed or IFRS Entity has objective evidence that all criteria for acceptance have been satisfied.

The products are often sold with volume discounts; customers have a right to return faulty products in the wholesale market. Sales are recorded based on the price specified in the sales contracts, net of the estimated volume discounts and returns at the time of sale. Accumulated experience is used to estimate and provide for the discounts and returns. The volume discounts are assessed based on anticipated annual purchases. No element of financing is deemed present as the sales are made with a credit term of 30 days, which is consistent with the market practice.

Sales of goods – retail

IFRS Entity operates a chain of retail outlets.

Sales of goods are recognised when IFRS Entity sells a product to the customer. Retail sales are usually in cash or by credit card. It is IFRS Entity’s policy to sell its products to the retail customer with a right to return within 28 days. Accumulated experience is used to estimate and provide for such returns at the time of sale. IFRS Entity does not operate any loyalty programmes.

Sales of services

IFRS Entity sells design services and transportation services to other manufacturers.

These services are provided on a time and material basis or as a fixed-price contract, with contract terms generally ranging from less than one year to three years.

Revenue from time and material contracts, typically from delivering design services, is recognised under the percentage-of-completion method. Revenue is generally recognised at the contractual rates. For time contracts, the stage of completion is measured on the basis of labour hours delivered as a percentage of total hours to be delivered. For material contracts, the stage of completion is measured on the basis of direct expenses incurred as a percentage of the total expenses to be incurred.

IFRS Entity Financial Statements For the year ended 31 December 2015

28

Revenue from fixed-price contracts for delivering design services is also recognised under the percentage-of-completion method. Revenue is generally recognised based on the services performed to date as a percentage of the total services to be performed.

Revenue from fixed-price contracts for delivering transportation services is generally recognised in the period the services are provided, using a straight-line basis over the term of the contract.

If circumstances arise that may change the original estimates of revenues, costs or extent of progress toward completion, estimates are revised. These revisions may result in increases or decreases in estimated revenues or costs and are reflected in income in the period in which the circumstances that give rise to the revision become known by management.

Rental income from investment property

Rental income is recognised on an accruals basis.

4.16 Employee benefits

(a) IFRS Entity makes pension contributions on behalf of UAE in accordance with Law no. 2 of 2000. The contributions are treated as payments to a defined contribution pension plan. A defined contribution plan is a pension plan under which fixed contributions are paid into a separate pension fund. IFRS Entity has no legal or constructive obligations to pay further contributions if the pension fund does not hold sufficient assets to pay all employees the benefits relating to employee service in the current and prior periods. The contributions are recognised as employee benefit expense when they are due. Prepaid contributions are recognised as an asset to the extent that a cash refund or a reduction in the future payments is available.

(b) IFRS Entity provides end of services benefits for its expatriate employees. The entitlement to these benefits is based upon the employees’ length of service and completion of a minimum service period. The expected costs of these benefits are based on an actuarial assessment of the liabilities using the projected unit credit method and are accrued over the period of employment.

4.17 Dividends

Dividends to IFRS Entity’s shareholders are recognised as a liability in the financial statements in the period in which the dividends are approved by IFRS Entity’s shareholders.

4.18 Government grants

The Government of Abu Dhabi owns more than 50% of the equity of IFRS Entity. Accordingly transactions with the Government must be assessed to determine if the transaction is a transaction with a shareholder in their capacity as a shareholder and therefore transacted in equity or, a government grant and therefore dealt with in income or deferred income.

Grants from the government are recognised at their fair value where there is a reasonable assurance that the grant will be received and the entity will comply with all attached conditions. Government grants relating to costs are deferred and recognised in the income statement over the period necessary to match them with the costs that they are intended to compensate.

Government grants relating to property, plant and equipment are included in non-current liabilities as deferred government grants and are credited to the income statement on a straight-line basis over the expected lives of the related assets.

4.19 Segment reporting

Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision-maker. The chief operating decision-maker, who is responsible for allocating resources

IFRS Entity Financial Statements For the year ended 31 December 2015

29

and assessing performance of the operating segments, has been identified as the steering committee that makes strategic decisions.

5 FINANCIAL RISK MANAGEMENT

IFRS Entity transacts wholly in the UAE and maintains its bank accounts in Dirhams. As a result it is not exposed to currency risk. IFRS entity is exposed to fair value interest rate risk, cash flow interest rate risk and price risk. IFRS entity is also exposed to credit risk and liquidity risk. Risk management is carried out by the Board of Directors. A treasury report is submitted periodically to the Board. The treasury report evaluates financial risk.

Market risk

(i) Price risk

IFRS Entity is exposed to equity securities price risk because of investments held and classified on its statement of financial position as available-for-sale. IFRS Entity is not exposed to commodity price risk. To manage its price risk arising from investments in equity securities, IFRS Entity diversifies its portfolio. Diversification of the portfolio is done in accordance with the limits set by the Board of Directors.

IFRS Entity’s equity investments in other entities are publicly traded on Abu Dhabi equity indexes. The table below summarises the impact of increases/decreases of the Abu Dhabi stock exchange on the profit for the year and on equity. The analysis is based on the assumption that the equity indexes had increase/decreased by 5% with all other variables held constant and all the equity instruments moved according to the historical correlation with the index:

Impact on profit Impact on equity

2015 2014 2015 2014

Increase X X X X Decrease X X X X

(ii) Cash flow and fair value interest rate risk

IFRS Entity’s interest rate risk arises from long-term borrowings. Borrowings issued at variable rates expose IFRS Entity to cash flow interest rate risk which is partially offset by cash held at variable rates. Borrowing issued at fixed rates exposes IFRS Entity to fair value interest rate risk.

Credit risk

Credit risk arises from cash and cash equivalents, and deposits with banks and financial institutions, as well as credit exposure to wholesale and retail customers, including outstanding receivables and committed transactions. For banks and financial institutions, only independently rated parties with a minimum rating of ‘AAA’ are accepted. If wholesale customers are independently rated, those ratings are used. If there is no independent rating, risk control assesses the credit quality of the customer, taking into account its financial position, past experience and other factors, individual risk limits are set based on internal or external rating in accordance with limits set by the board. The utilisation of credit limits is regularly monitored. Sales to retail customers are settled in cash or using major credit cards.

Liquidity risk

The Board of Directors monitors rolling forecasts of IFRS Entity’s liquidity requirements to ensure it has sufficient cash to meet operational needs while maintaining sufficient headroom on its undrawn committed borrowing facilities (note 17) at all times so that IFRS Entity does not breach borrowing limits or covenants (where applicable) on any of its borrowing facilities. Such forecasting takes into consideration IFRS Entity’s

IFRS Entity Financial Statements For the year ended 31 December 2015

30

debt financing plans, covenant compliance, compliance with internal statement of financial position ratio targets and, if applicable external regulatory or legal requirement, for example, currency restrictions.

Surplus cash held over and above the balance required for working capital management is invested in interest bearing current accounts, time deposits, money market deposits and marketable securities. Instruments are chosen with appropriate maturities or sufficient liquidity to provide sufficient head-room as determined by the above-mentioned forecasts. At the reporting date, IFRS Entity held money market funds of AED X (2014: AED Y) and other liquid assets of AED X (2014: AED Y) that are expected to readily generate cash inflows for managing liquidity risk.

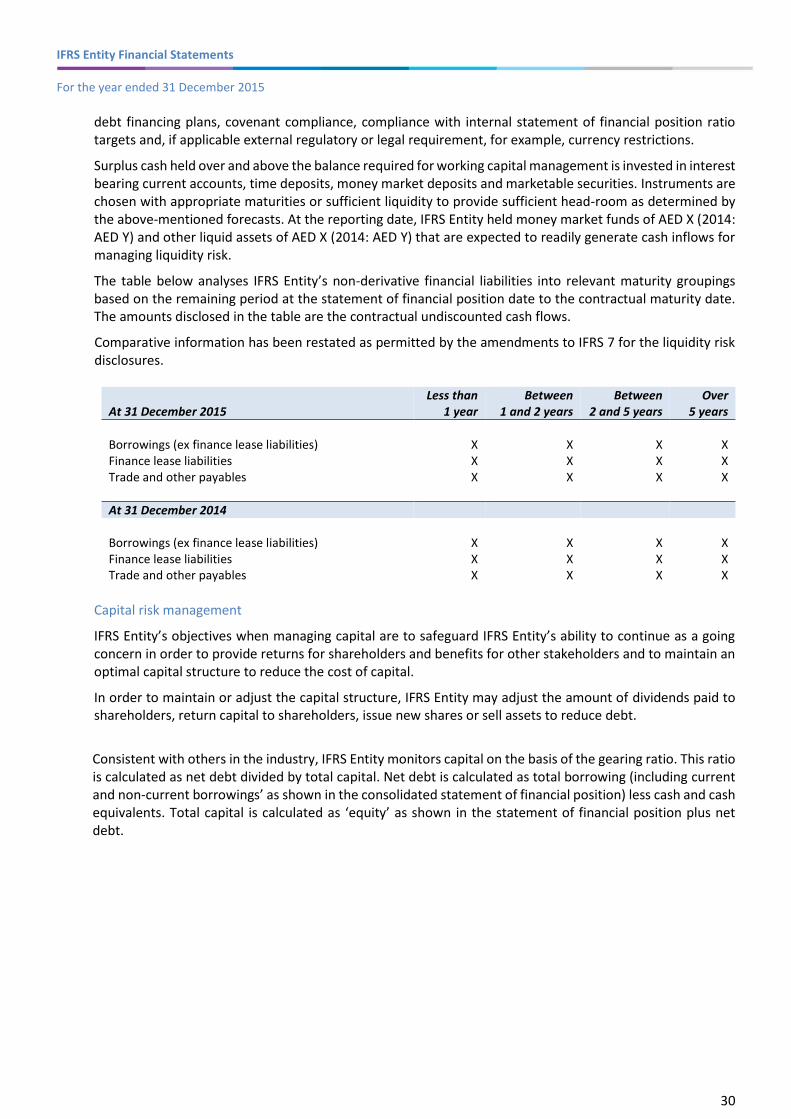

The table below analyses IFRS Entity’s non-derivative financial liabilities into relevant maturity groupings based on the remaining period at the statement of financial position date to the contractual maturity date. The amounts disclosed in the table are the contractual undiscounted cash flows.

Comparative information has been restated as permitted by the amendments to IFRS 7 for the liquidity risk disclosures.

At 31 December 2015 Less than

1 year Between

1 and 2 years Between

2 and 5 years Over

5 years

Borrowings (ex finance lease liabilities) X X X X Finance lease liabilities X X X X Trade and other payables X X X X

At 31 December 2014 Borrowings (ex finance lease liabilities) X X X X Finance lease liabilities X X X X Trade and other payables X X X X

Capital risk management

IFRS Entity’s objectives when managing capital are to safeguard IFRS Entity’s ability to continue as a going concern in order to provide returns for shareholders and benefits for other stakeholders and to maintain an optimal capital structure to reduce the cost of capital.