III Real Estate Conference - Banco Fator

34

1 Corporate Presentation III Real Estate Conference – Banco Fator

-

Upload

direcionalri -

Category

Investor Relations

-

view

238 -

download

0

Transcript of III Real Estate Conference - Banco Fator

1

Corporate Presentation

III Real Estate Conference – Banco Fator

Disclaimer

� This presentation may contain forward-looking statements. Such forward-looking statements are and will be subject tomany risks and uncertainties relating to factors that are beyond Direcional’s ability to control or estimate precisely, suchas future market conditions, competitive environment, currency and inflation fluctuations, changes in governmental andregulatory policies and other factors relating to the operations of Direcional, which may cause actual future results ofDirecional to differ materially from those expressed or implied in such forward-looking statements

� You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date ofthis presentation. Such forward-looking statements shall not be construed as guarantee of future performance.Direcional does not undertake to publicly review or update these forward-looking statements in view of events or

2

Direcional does not undertake to publicly review or update these forward-looking statements in view of events orcircumstances occurring after the date of this presentation

� This presentation does not constitute an offer, or invitation, or solicitation of an offer, to subscribe for or purchase anysecurities. Neither this presentation nor anything contained herein shall form the basis of any contract or commitmentwhatsoever

� This presentation and its contents are proprietary information and may not be reproduced or otherwise disseminated inwhole or in part without Direcional’s prior written consent.

652

2,227

5,359

9,360

12,364

� Start-up in 1981

� Industrial projects acting

as contractor to third

partiesIPO

Over 30 Years of History

A consistent track record and focus

� Capture

significant

market

opportunities

� MCMV II

� Follow-on: $

228.8 million for

What’s Next?

CAGR 06-10: 110%

CAGR 06-10: 100%

67

176

710783

1,067

� Development of projects

focused on the low-

income market

parties

� Beginning of

large scale

developments

for the low-

income market

� Operations

expansion to

PA, RO and ES

IPO � 32% growth in

units launched

from the

previous year

� 57% growth in

contracted PSV

from the

previous year

3Source: Company Reports

Units Launched

� Consolidation

of a leading

position in

Manaus and

Brasilia

� Establishment

of own sales

team

� Important geographic

expansion: Brasília, Rio

de Janeiro and Campinas

1981 - 2005 2006 2007 2008 2009 2010 2011

228.8 million for

the Company

� Increasing

liquidity

PSV Launched (R$ mm)

67

Management Team

Ricardo Valadares Gontijo

Chairman & CEO

Ricardo Valadares Gontijo

Chairman & CEO

• Founder, CEO and Chairman of the Board40 years of construction experience• Civil Engineer graduated by UFMG with Gold Medal Award.

Ricardo Ribeiro Gontijo

Commercial Officer

Ricardo Ribeiro Gontijo

Commercial Officer

Roberto Senna

General Manager

Roberto Senna

General Manager

• Civil Engineer degree from The Universidade Federal da Bahia, MBA degree from FGV and specializationcourses at the Wharton School - University of Philadelphia, and University of Carlifornia - Irvine.• Joined Odebrecht Group in 1979 and has held senior management positions in Brazil and abroad• He was President of Metro-Rio, Director of Telemar Holding and member of the Board of severalcompanies of the group.• He was CEO of Bairro Novo, a real estate subsidiary from Odebrecht Group, focused on residentialdevelopment and construction in the low income

•Board Member and responsible for Marketing, Sales and New Business•Civil Engineer graduated by UFMG with the Gold Medal Award•Joined Direcional in 2004.

4

Commercial OfficerCommercial Officer

Carlos Wollenweber

CFO & IR Officer

Carlos Wollenweber

CFO & IR Officer

Lucas Rocha

Engineering Officer

Lucas Rocha

Engineering Officer

Ana Carolina Huss

Human Resources Officer

Ana Carolina Huss

Human Resources Officer

•Joined Direcional in 2004.

•Extensive experience in the Brazilian real estate market.•From 2007 to 2009, Controller of BR Properties•From 2005 to 2007, Financial Director of Valora•From 2001 to 2005, Financial Manager of Gafisa•Electrical Engineer graduated by PUC / SP has master degree in Economics and Finance at PUC / SP andMBA degree at MIT (Massachusetts Institute of Technology)

•Responsible for the engineering department with more than 30 years of experience in construction•Holds a bachelor’s degree in Civil Engineering•Joined Direcional in 1985

• Psychologist, graduated at University Paulista, MBA in Business Management, post graduate inKnowledge Management at FVG and certified in Bright Link in professional coaching• Human Resources Manager at Natura Cosméticos and Accor Brasil• Responsible for the department ¨People and Organization¨ of the Bairro Novo, a company of the Odebrechtgroup.

Shareholder’s Structure

47.1% 15.0%

FiladélphiaParticipações S.A. 1 Ridgecrest, LLCTarpon2 Other

6.9% 24.4%

GIC

6.6%

51. Holding owbed by Ricardo Valadares Gontijo and his family2. Funds managed by Tarpon Investimentos S.A.

6

Business Model

6

Unique Footprint� Strong footprint in markets with high growth potential, low

competition and high barriers to entry

Low competition in profitable markets

Direcional: A Unique Business Model

The best low-income player in Brazil

The most profitable and efficient player in the low income

sector

‘’’’‘

� Highest efficiency and profitability in the sector

1st Annualized ROE¹ among peers~25.8% of ROE

~22.6% of Net Margin1st Net margin among peers

1

Track Record in Operating in the

Low Income

� Over 30 years of experience� Solid track record in 0-3 minimum wages projects

Low capital commitment, solid

margins and high ROIC

Focus on Large Scale Projects

Verticalized Business Model

� Strong expertise in large scale ventures

� Own work force� Performance-based compensation� Standardized and industrialized production on-site

Large scale operations in the low income

segments, with strict cost control and high

margins

7Source: Company Report in the 4Q101. Annualized ROE: Annualized Quarter’s Net Profit / Average Shareholders' Equity in the same period

2

3

4

AM8.2%

RO4.1%

PA13.2%

Unique Footprint: High Growth Markets with Barriers to Entry

Land Bank Composition Barriers to Entry

� Detailed mapping of logistics and supply

Scarcity of

Suppliers

� Industrialization of raw materials

� Vertically integrated model is rapidly replicated

Direcional's Approach

1

Direcional is the leading company in underpenetrated markets with high growth potential

1

ES1.1%

MG40.3%

SP3.4%

DF27.9%

RJ1.8%

Popular,

79.3%

Upper

middle,

1.6%

Medium,

17.6%

Commercial,

1.4%

8

Complex

Logistics

� Detailed mapping of logistics and supply channels

� Large and vertically integrated projects

Adverse

Weather

Conditions

� Pre-manufactured building materials adapted to diverse climates

� Expertise in coordinating construction cycle and weather demands

Unskilled

Labor

� Highly-trained workers

� Standardized and fully-integrated construction

� Compensation based on performance

“MINHA CASA, MINHA VIDA”

50.6k units elegible for the program

74.2% of total Land bank

Source: Company Report

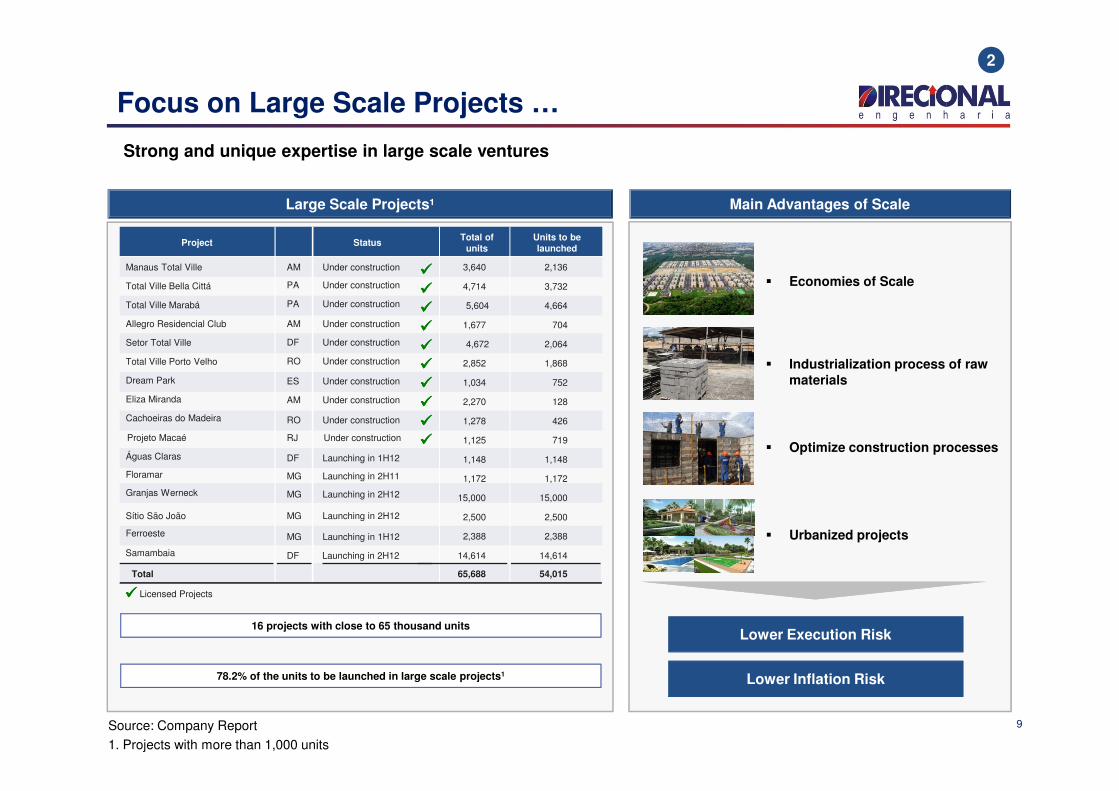

Focus on Large Scale Projects …

Strong and unique expertise in large scale ventures

2

Large Scale Projects¹

Project StatusTotal of

unitsUnits to belaunched

Main Advantages of Scale

� Economies of Scale

� Industrialization process of raw materials

Manaus Total Ville AM Under construction

Total Ville Bella Cittá PA Under construction

Total Ville Marabá PA Under construction

Allegro Residencial Club AM Under construction

Setor Total Ville DF Under construction

Total Ville Porto Velho RO Under construction

Dream Park ES Under construction

Eliza Miranda AM Under construction

3,640 2,136

4,714 3,732

5,604 4,664

1,677 704

4,672 2,064

2,852 1,868

1,034 752

����

����

����

����

����

����

����

����

9Source: Company Report1. Projects with more than 1,000 units

� Optimize construction processes

� Urbanized projects

���� Licensed Projects

Lower Execution Risk

Lower Inflation Risk

Eliza Miranda AM Under construction

Cachoeiras do Madeira RO Under construction

Águas Claras DF Launching in 1H12

Granjas Werneck MG Launching in 2H12

Floramar MG Launching in 2H11

Samambaia DF Launching in 2H12

Projeto Macaé RJ Under construction

Sítio São João MG Launching in 2H12

Ferroeste MG Launching in 1H12

Total

78.2% of the units to be launched in large scale projects1

16 projects with close to 65 thousand units

2,270 128

1,278 426

1,148 1,148

15,000 15,000

1,172 1,172

14,614 14,614

1,125 719

2,500 2,500

2,388 2,388

65,688 54,015

����

����

����

… Through a Verticalized Business Model

More than 10,000 exclusive workers assuring quality, commitment, efficiency and cost control

Verticalized Business Model Ability to Deliver

3

Best Execution in the SectorBest Execution in the Sector

Construction DNAConstruction DNA

Own Work Force

VerticalizationVerticalization

Standardized / Industrialization

10

� Performance Based Compensation

� Capacity to Hire and Train Operational Team

� Lower Turnover

On Schedule:Projects Delivered on Time

With High Quality: Lower Maintenance Cost

On Budget: Margin Stability

Own Work ForceIndustrialization

� Economies of Scale

� All projects are based on few designs

Source: Company Report

Unique Expertise in the Low Income Segment

Solid track record in all the low income segments

Characteristics

� Developer approach

Companies develop projects and sell units to customers

� Price above R$170 k / unit

� CAIXA does not facilitate customer financing

� Developer approach

Companies develop projects and sell units to customers

� Price is capped at R$170 k / unit

� CAIXA facilitates customer financing

� Builder approach

Homebuilders present projects to Caixa for evaluation and approval

� Normally land/infrastructure is given by local Government

� Price is capped at R$51 k / unit

4

Mid / Low Income Low Income (MCMV – 4-10 MW) Very Low Income (MCMV – 0-3 MW)+ +

11

1. Company estimates – maximum cash exposure in % of total PSV

Main Players

Equity Commitment1

Units Launched2010

~5%~15%~20% ~10%

60% / 7,391 units12% / 1,503 units 28% / 3,470 units

PSV Launched2010

36% / R$ 380 mm23% / R$ 245 mm 41% / R$ 441 mm

Top Notch Operational Performance

Direcional has been confirming its efficient cash cycle with sound financial results

Efficient Cash Cycle Highest Results in the Sector

Land

AcquisitionSales

Speed

Land

AcquisitionSales

Speed

38% VSO80% Swaps

19%

24%

MRV

PDG

Helbor

12

Efficient CashCycle

ManagementCash

Collection

Austere

Budget

Client

Financing

Construction

Financing

Cash

Collection

Austere

Budget

Client

Financing

Construction

Financing

Avg. Unit Selling Price

Net

Mar

gin

2010

Source: Company Reports in the 4Q10

80-100% of

construction

cost

G&A of 6%

of Revenues

4%

9%

14%

- 150.000 300.000 450.000

CCDI

Rodobens

PDG

Even

Inpar

Cyrela

Tecnisa

Rossi

Trisul

Gafisa

13

Growth Drivers

13

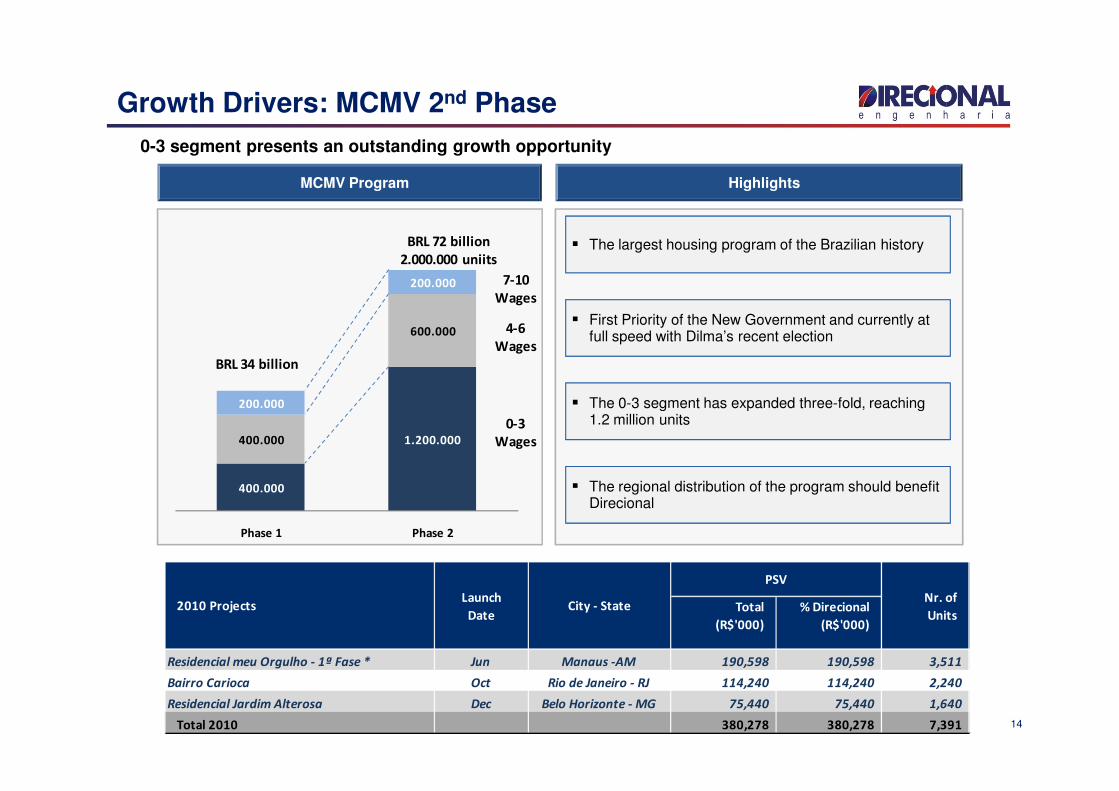

MCMV Program Highlights

� The largest housing program of the Brazilian history

� First Priority of the New Government and currently at full speed with Dilma’s recent election

� The 0-3 segment has expanded three-fold, reaching

600.000

200.000

BRL 34 billion

BRL 72 billion

2.000.000 uniits

4-6

Wages

7-10

Wages

Growth Drivers: MCMV 2nd Phase

0-3 segment presents an outstanding growth opportunity

Total

(R$'000)

% Direcional

(R$'000)

Residencial meu Orgulho - 1ª Fase * Jun Manaus -AM 190,598 190,598 3,511

Bairro Carioca Oct Rio de Janeiro - RJ 114,240 114,240 2,240

Residencial Jardim Alterosa Dec Belo Horizonte - MG 75,440 75,440 1,640

Total 2010 380,278 380,278 7,391

2010 ProjectsLaunch

DateCity - State

PSV

Nr. of

Units

� The 0-3 segment has expanded three-fold, reaching 1.2 million units

� The regional distribution of the program should benefit Direcional

400.000

1.200.000400.000

200.000

Phase 1 Phase 2

0-3

Wages

14

Growth Drivers: Selective Geographic Expansion

Direcional operates in Brazil’s most complex markets and expects to replicate this model in new attractive areas

Development of 0-3 MW Projects

Geographic Expansion Strategy New Sites Selection Criteria

High Housing Demand

Access to Credit Lines

15

Immediate gain of market share and visibility

New projects leveraging on our unique business model

Access to Credit Lines

Operational Complexity & Region Expertise

Land Availability

16

Operating and Financials Highlights

2010 and 1Q11

16

1,067 12,364

Launches

� PSV of R$ 223.3 million, or 1,243 units launched in the 1Q11.� 12,364 units were launched in 2010, totaling a PSV of R$ 1,067 million

Launched PSV - % Direcional

(R$ million)

Launches

(Units)

+58%

36%

-2%

32%

783

1,067

141 223

2009 2010 1Q10 1Q11

9,360

12,364

1,266 1,243

2009 2010 1Q10 1Q11

17

+58% -2%

Total(R$'000)% Direcional

(R$'000)

1 Setor Total Ville - 6ª Etapa FEB Santa Maria - DF 49,775 49,770 416 Popular

2 Parque Silvestre FEB Rio de Janeiro - RJ 19,338 15,857 220 Popular

3 Allegro Mall FEB Manaus - AM 16,716 16,715 29 Commercial

4 Boulevard Esplanada MAR Belo Horizonte - MG 59,137 59,078 258 Medium

5 Brisas do Parque Residencial Club MAR Manaus - AM 81,998 81,916 320 Medium

Launches 1Q11 226,965 223,337 1,243

1Q11 Projects Date City - State Segment# of Units

PSV

39.0%59.8%

40.0%

26.8%

97.8%

51.2%

20.0% 5.1%

46.5%

1.0%7.0%

2.2%1.3% 2.3%

2009 2010 1Q10 1Q11

0 - 3 MW Popular Medium Upper Middle Commercial

13.0%

50.0%

73.3%

28.1%12.0%

11.0%

24.5%

33.5%

75.0%

39.0%

2.2%

38.5%

2009 2010 1Q10 1Q11

North Midwest Southeast

Launches Breakdown

Launches

(Segment Breakdown - Units)

Launches

(Geographic Breakdown - Units)

0 - 3 MW Popular Medium Upper Middle Commercial

18

Boulevard EsplanadaSetor Total Ville

Parque Silvestre

Brisas do Parque

Allegro Mall

Projects Launched in the 1Q11 .

7,824

12,359

661

1037

Sales

Contracted PSV

(R$ million)

Contracted

(Units)

� In the 1Q11 Direcional sold 1,211 units with a total PSV of R$ 175.1 million� In 2010, we sold 12,359 units with total PSV of R$ 1,037 million

+7%

57%

-7%

58%

46.0%59.9%

34.8%25.9%

76.8%54.3%

15.7% 11.1% 17.7%

39.8%

3.5% 2.7% 5.5%3.5%

0.4% 2.4%

2009 2010 1Q10 1Q11

0 - 3 MW Popular Medium Upper Middle Commercial

79.7%

46.4%57.7%

32.0%

7.7%

12.6%

34.6%

25.3%

12.6%

41.1%

7.7%

42.7%

2009 2010 1Q10 1Q11

North Midwest Southeast

1,309 1,211

2009 2010 1Q10 1Q11

164 175

2009 2010 1Q10 1Q11

19

Sales

(Geographic Breakdown - Units)

Sales

(Segment Breakdown - Units)

48%1Q11 48%

33.8%38.3%

23.7%

19.4% 20.8%

27.6%

22.1%

1Q10 2Q10* 3Q10 4Q10* 1Q11

With 0-3 mw projects Without 0-3 mw projects

Sales Speed

� 48% of the 1Q11 of units launched were sold during the 1Q11

� Sales Over Supply of 22.1% in the 1Q11.

Sales Over Supply (VSO)

(Total PSV)

Sales Speed (%)

(# of units)

17%

89%

17%

87%

19%

4%

27%

4%

7%

3%

14%

5%

1%

5%1Q10

2Q10

3Q10

4Q10

3M 6M 9M 12M 15M

91%

58%

97%

53%

1Q10 2Q10* 3Q10 4Q10* 1Q11

201. In 2Q10 and 4Q10, the speed of sales was impacted favorably by the immediate recognition of 0-3 mw projects.

Total % Direcional

Launches 1Q11 126,941 124,519 698 592 52.1%

Launches 4Q10 132,977 77,695 458 442 8.5%

Launches 3Q10 76,919 74,865 773 704 41.0%

Launches 2Q10 62,036 61,974 152 121 3.0%

Launches 1Q10 79,202 71,239 607 560 45.9%

Launches 4Q09 2,071 2,070 18 18 2.1%

Inventory

PSV in Inventory (R$'000)Units in

Inventory

Units in

Inventory

(without swap)

% Units in

Inventory

Inventory

� PSV of R$ 636 million, or 3,804 units;� Inventory of completed units of R$ 20.1 million, or 199 units;� Projects under construction have an average of 86,4% units already sold.

Launches 4Q09 2,071 2,070 18 18 2.1%

Launches 3Q09 86,266 76,129 697 474 11.1%

Launches 2Q09 23,028 19,043 231 116 3.9%

Launches 1Q09 29,733 26,138 214 198 20.8%

Launches 4Q08 61,862 45,576 319 240 19.8%

Launches 3Q08 25,931 20,744 201 89 6.5%

Launches 2Q08 7,820 6,586 67 25 3.4%

Launches 1Q08 6,657 5,858 31 13 3.1%

Previous launches 6,151 3,058 39 13 2.8%

Under Construction 727,595 615,494 4,505 3,605 13.6%

Completed Units 42,467 20,096 224 199 3.8%

Total Inventory 770,062 635,590 4,729 3,804 11.9%

21

Only 3.8% of completed units in the inventory

85

176

37 51

22.5% 22.6% 26.3%21.7%

-90.0%

-70.0%

-50.0%

-30.0%

-10.0%

10. 0%

30. 0%

-

20

40

60

80

100

120

140

160

180

200

2009 2010 1Q10 1Q11

378

782

143 234

2009 2010 1Q10 1Q11

+107%

+64%

Financial Highlights

Adjusted Net Income and Net Margin1Net Revenues

+107%

35%

2009 2010 1Q10 1Q11

Net Margin

2009 2010 1Q10 1Q11

Development,

76.2%

Management

Fee, 0.8%

0-3 MW

Projects, 22.5%

Brokerage, 0.5%

63.4 102.3 263.2 377.6 781.9 234.0

24.0%21.1%

24.5% 22.5% 22.6% 21.7%

2006 2007 2008 2009 2010 2011

Net Revenue Net Margin22

1. Adjusted by non-cash expenses (Stock-Option Program).

Gross Revenue Breakdown: 1Q11

CAGR: 87,4%

Net Revenue and Net Margin Evolution

127

248

50 66

33.7% 31.7%35.1%

28.0%

-20.0%

-10.0%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

-

50

100

150

200

250

300

2009 2010 1Q10 1Q11

Financial Highlights

Gross Profit and Gross Margin

+95%

+31%

2009 2010 1Q10 1Q11Gross Margin

14,9 20,7 33,0 48,2 56,8 48,2 56,8

10,4% 12,5% 15,7% 18,3%24,3%

18,3%24,3%

1Q10 2Q10 3Q10 4Q10 1Q11 4Q10 1Q11% of Revenues

Revenue of Services Evolution

23

281,2% +18%

15.3 20.0

3.9 5.0

1.9% 1.6%

1.9% 2.3%2.4%2.3%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0 %

1.0 %

2.0 %

-

5.0

10.0

15.0

20.0

25.0

2009 2010 4Q10 1Q11

21.8

50.0

8.4 16.2

5.8%6.4% 5.9%

6.9%

-4.0%

-2.0%

0.0 %

2.0 %

4.0 %

6.0 %

8.0 %

-

10.0

20.0

30.0

40.0

50.0

60.0

2009 2010 1Q10 1Q11

Financial Highlights

Adjusted G&A¹ (R$ million) Commercial Expenses (R$ million)

+129%

+94%

+31%

+27%

2009 2010 4Q10 1Q11% of Sales % of Sales without 0-3 mw projects

2009 2010 1Q10 1Q11% of Revenue

106

202

42 58

28.0%25.8%

29.7%

24.7%

0.0 %

5.0 %

10. 0%

15. 0%

20. 0%

25. 0%

30. 0%

-

50

100

150

200

250

2009 2010 1Q10 1Q11Ebitda Margin

24

Adjusted Ebitda and Ebitda Margin¹

+91%

+36%

1. Adjusted by non-cash expenses (Stock-Option Program).

Cash Position 1Q10 4Q10 1Q11 ∆∆∆∆ % ∆∆∆∆ %

(R$'000) (a) (b) (c) (c/a) (c/b)

Loans and Financing 142,672 302,374 348,307 144.1% 15.2%

SFH 138,545 226,056 282,674 104.0% 25.0%

Securitization of receivables - 46,843 36,429 - -22.2%

FINAME and others 4,127 8,882 8,611 108.7% -3.1%

Working Capital - 20,593 20,593 - -

Cash and Cash Equivalents 292,019 190,852 355,410 21.7% 86.2%

Net debt -149,347 111,522 -7,103

Net debt / Equity -21.5% 14.1% -0.9%

SFH, 90.6%

FINAME

and others,

2.8%

Working

Capital,

6.6%

Cash Position

Loans and Financing

(ex- securitization)

Net debt / Equity -21.5% 14.1% -0.9%

14,522

25,312 22,468

32,657

41,236

74,504

86,301

100,873

64,967

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11*

170

111

33 35

2011 2012 2013 +2014

1. Cash Burn: measured by the variation of the net debt, less capital increases and dividends payed* 1Q11: Adjusted by R$ 224 million of follow-on and R$ 40.3 million of dividends payment

25

Amortization Schedule (R$ million)

Cash Burn¹ (R$ million)

-36%

Results to be Recognized (R$'000) 1Q10 4Q10 1Q11 ∆∆∆∆ % ∆∆∆∆ %

(a) (b) (c) (c/a) (c/b)

Deferred revenues 623,125 740,269 762,873 22.4% 3.1%

Deferred costs -372,923 -424,802 -437,186 17.2% 2.9%

Deferred results 250,202 315,467 325,687 30.2% 3.2%

Deferred results - Margin 40.2% 42.6% 42.7%

Estimated schedule for deferred results apropriation 2011 2012 2013+

49.5% 44.7% 5.8%

Results to be Recognized (R$'000) 1Q10 4Q10 1Q11 ∆∆∆∆ % ∆∆∆∆ %

(a) (b) (c) (c/a) (c/b)

Deferred revenues 623,125 740,269 762,873 22.4% 3.1%

Deferred costs -372,923 -424,802 -437,186 17.2% 2.9%

Deferred results 250,202 315,467 325,687 30.2% 3.2%

Deferred results - Margin 40.2% 42.6% 42.7%

Estimated schedule for deferred results apropriation 2011 2012 2013+

49.5% 44.7% 5.8%

Results To Be Recognized

49.5%44.7%

5.8%

2011 2012 2013+

26

REF Recognition Schedule

100

120

140

160

6,000

7,000

8,000

9,000

10,000

Pre

ço d

a A

ção

Vo

lum

e (

R$

mil

) 100

120

140

160

6,000

7,000

8,000

9,000

10,000

Sto

ck P

rice

Vo

lum

e (

R$

'00

0)

Shares Performance Since IPO

Before Follow On After Follow On

0

20

40

60

80

-

1,000

2,000

3,000

4,000

5,000

18

-No

v-0

9

1-D

ec-

09

11

-De

c-0

9

23

-De

c-0

9

8-J

an

-10

20

-Ja

n-1

0

2-F

eb

-10

12

-Fe

b-1

0

26

-Fe

b-1

0

10

-Ma

r-1

0

22

-Ma

r-1

0

1-A

pr-

10

14

-Ap

r-1

0

27

-Ap

r-1

0

7-M

ay-

10

19

-Ma

y-1

0

1-J

un

-10

15

-Ju

n-1

0

25

-Ju

n-1

0

7-J

ul-

10

21

-Ju

l-1

0

3-A

ug

-10

16

-Au

g-1

0

30

-Au

g-1

0

15

-Se

p-1

0

1-O

ct-1

0

14

-Oct

-10

26

-Oct

-10

8-N

ov-

10

23

-No

v-1

0

3-D

ec-

10

17

-De

c-1

0

30

-De

c-1

0

12

-Ja

n-1

1

24

-Ja

n-1

1

4-F

eb

-11

16

-Fe

b-1

1

28

-Fe

b-1

1

14

-Ma

r-1

1

24

-Ma

r-1

1

5-A

pr-

11

15

-Ap

r-1

1

29

-Ap

r-1

1

Pre

ço d

a A

ção

Vo

lum

e (

R$

mil

)

Volume (R$ '000)

0

20

40

60

80

-

1,000

2,000

3,000

4,000

5,000

18

-No

v-0

9

1-D

ec-

09

11

-De

c-0

9

23

-De

c-0

9

8-J

an

-10

20

-Ja

n-1

0

2-F

eb

-10

12

-Fe

b-1

0

26

-Fe

b-1

0

10

-Ma

r-1

0

22

-Ma

r-1

0

1-A

pr-

10

14

-Ap

r-1

0

27

-Ap

r-1

0

7-M

ay-

10

19

-Ma

y-1

0

1-J

un

-10

15

-Ju

n-1

0

25

-Ju

n-1

0

7-J

ul-

10

21

-Ju

l-1

0

3-A

ug

-10

16

-Au

g-1

0

30

-Au

g-1

0

15

-Se

p-1

0

1-O

ct-1

0

14

-Oct

-10

26

-Oct

-10

8-N

ov-

10

23

-No

v-1

0

3-D

ec-

10

17

-De

c-1

0

30

-De

c-1

0

12

-Ja

n-1

1

24

-Ja

n-1

1

4-F

eb

-11

16

-Fe

b-1

1

28

-Fe

b-1

1

14

-Ma

r-1

1

24

-Ma

r-1

1

5-A

pr-

11

15

-Ap

r-1

1

29

-Ap

r-1

1

Sto

ck P

rice

Vo

lum

e (

R$

'00

0)

Average Volume (21 days) Direcional Ibovespa IMOB

27

Follow-On

� 20.8 million new shares were issued in the primary offer and 7.2 million sold in the secondary offering� Increased the free float from 39.5% to 53.0%.

Before Follow On After Follow On

Controlling

60.5%

Tarpon

15.0%

Ridgecrest

8.0% Controlling

47.1%

Tarpon

15.0%

Ridgecrest

6.9%

GIC

6.6%

547.9

2,013.5

Before Follow On After Follow On

86187

224

446

Dec. / 10 Apr. / 11

Investments Funds Individuals 28

60.5% 8.0%

GIC

3.6%Other

12.9%

Average Daily Volume¹

(R$’000)

+268%

+64%

47.1%

Other

24.4%

Total # of Shareholders

1: three months before follow-on and three months after follow-on.

29

Appendix

29

How to Evaluate Direcional

Liquidation Value

NAV

(-) Land Bank (acquisitionprice)

� DCF of the Pipeline

Land Bank – Large scale projects(PSV)

(A) Liquidation Value (B) Land Bank Pipeline DCF (C) 0-3 MW Valuation+

Valuation: (A) + (B) + (C)

� DCF Hiden Value

MCMV Program – 0-3mw segment

= 1,2 million

Projected Direcional’s share: 3%-5% of mkt

+

price)Period: 4-5years

16 projects with close to 65 thousand units

78.2% of the units to be launched in large scale projects

BRL 500 millions of potential value

Projected Direcional’s share: 3%-5% of mktshare (36,000 -60,000 units)

Period: 4 years

Price / unit: 60~65k

Net Margin: 20~22%

30

Rising Income

▲ Basic Goods Basket

▲ Real Minimum Wage

▲ Average Wage (Monthly)

HOUSEHOLDS’ DISPOSABLE INCOME (Jan/03 – Aug/10)

Emerging Class C

EMERGING CLASS C (1)

(% households, 2003 – 2009)

Positive Job Market Trends

Poised to Capitalize on Soaring Demand

+ +

Brazil’s social upward mobility has favored the sector

500

600

115

120

‘04-’10 EMPLOYMENT GROWTH(%, Jan/04 – Nov/10)

50%

58%

27%

38%

5.7%

3%

5%

7%

9%

11%

13%

15%

Jan-04 Aug-05 Apr-07 Nov-08 Jul-10

31

� The steady increase of household disposable income, along with a higher availability of housing credit, drives the search for new homes

� 29 million individuals entered the class C income segment in the last 6 years, and 18 million are expected to join it in the next 5 years

Source: FGV (A Nova Classe Média: O Lado Brilhante dos Pobres), DIEESE, IPEA and McCann Erickson do Brasil1. Households earning R$1,126 to R$4,854 per month.

0

100

200

300

400

Jan-03 Nov-04 Sep-06 Aug-08 Jun-10

90

95

100

105

110

2.2x

1.8x

Jan/04 – Nov/10 %

Min 5.7%Max 13.1%Nov/10 5.7%

Average of 12M 6.9%

UNEMPLOYMENT RATE(%, 12-month moving average)

37%

2003 2009 2014

66mm 95mm+29mm

113mm+18mm

-3%Total Formal Informal

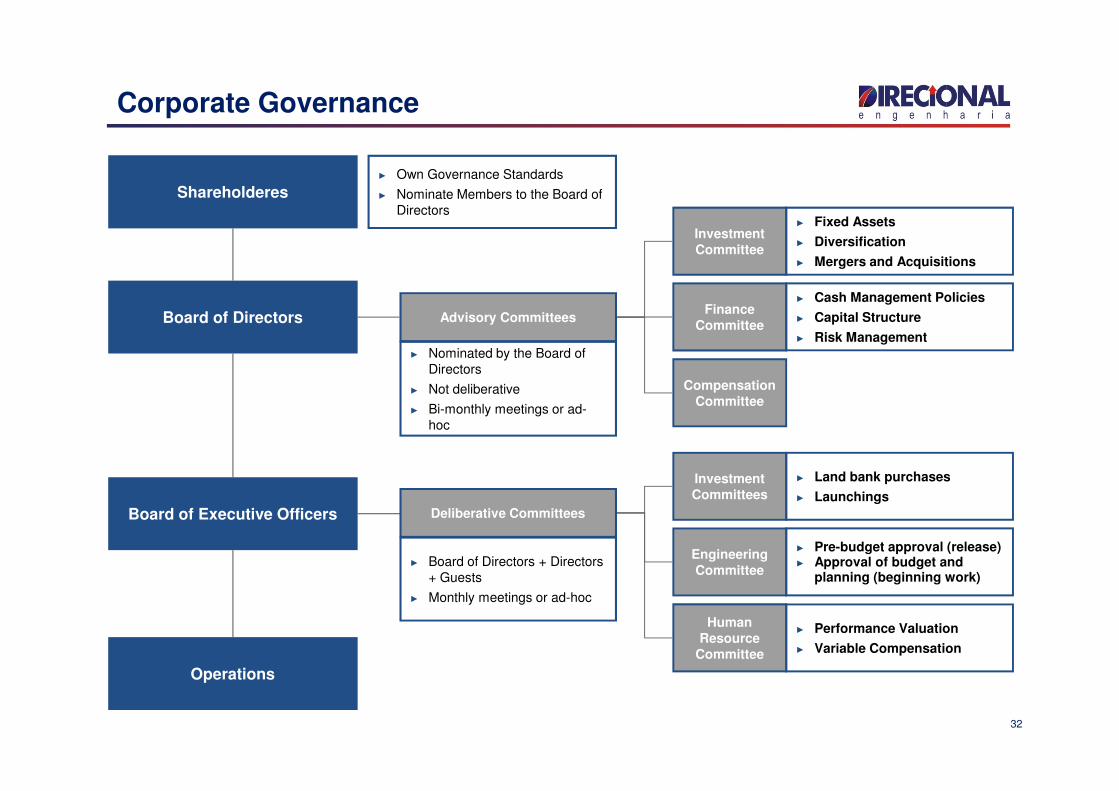

Corporate Governance

Board of Directors

Shareholderes► Own Governance Standards

► Nominate Members to the Board of Directors

Advisory Committees

► Nominated by the Board of Directors

► Not deliberative

Investment Committee

Finance Committee

Compensation Committee

► Fixed Assets

► Diversification

► Mergers and Acquisitions

► Cash Management Policies

► Capital Structure

► Risk Management

Board of Executive Officers

Operations

Not deliberative

► Bi-monthly meetings or ad-hoc

Deliberative Committees

► Board of Directors + Directors + Guests

► Monthly meetings or ad-hoc

Committee

Investment Committees

Engineering Committee

Human Resource

Committee

► Land bank purchases

► Launchings

► Pre-budget approval (release)► Approval of budget and

planning (beginning work)

► Performance Valuation

► Variable Compensation

32

Company Structure

Engineering/Construction

Detailed Design

Health, Safety & Environment

AdministrativeSupport

Quality/Technology

AM

DF,PA,RO

MG,ES

SP,RJ

CFO / IRHR Budget/Supply/

Planning

Sha

reho

lder

sC

lients

33Source: Company

Development / Commercial

Viability Studies

Market Support/Sales

Conceptual Design /Products

Legal (Real Estate)

AM

Special Projects (“0 – 3”)

President CEO

Legal(Corporate)

Comunic. & Market. Corp.

Sustainability/Customer

Relationship

Guidelines

Results

Sha

reho

lder

s

MG,ES

DF,PA,RO

SP,RJ

Clients

Contacts

Carlos WollenweberCFO | IR Officer

Lucas BousasIR Analyst

34

IR Analyst

Paulo SousaIR Assistant

www.direcional.com.br

(55 31) 3214-6200

(55 31) 3214-6450