IIFT InFINeeti Annual Issue Sept 2012

23

ANNUAL ISSUE SHOULD BANKS BE GIVEN MORE AUTONOMY? MIST VS BRICS INDIAN TAX REFORMS Analysis of BASEL III Norms SEPTEMBER 2012 THE FINANCE MAGAZINE OF IIFT

description

IIFT InFINeeti Annual Issue Sept 2012

Transcript of IIFT InFINeeti Annual Issue Sept 2012

ANNUAL ISSUE SHOULD BANKS BE GIVEN MORE AUTONOMY?

MIST vS BRICS INDIAN TAX REFORMS

Analysis of BASEL III Norms

SEPTEMBER 2012THE FINANCE MAGAZINE OF I IFT

MEE T THE TEAMCREDITS

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

2

P I Y U S H M A R WA H A i s a s o f t -

w a r e e n g i n e e r w i t h k e e n i n t e r -

e s t i n f i n a n c e . H e h a s i n t e r n e d

i n Tr i d e n t L i m i t e d i n f o r e x d i v i -

s i o n . H e r e g u l a r l y t r a c k s s t o c k s

a n d c o m m o d i t i e s m a r k e t s .

R I T E S H G U P TA i s s p e c i a l i s i n g i n

f i e l d o f f i n a n c e . H e h a s i n t e r n e d

w i t h R e l i g a r e E n t e r p r i s e s L i m i t e d

in the cor porate ser v ices d iv is ion .

H e p l a n s t o w o r k i n B a n k i n g a n d

f inance . industr y post graduat ion.

S H I L P I G H O S H i s s p e c i a l i z i n g t h e

f ields of marketing and f inance. She

h a s i n t e r n e d w i t h M e r c k S h a r p &

Dohme in the cr i t ica l care div is ion.

She plans to work in the pharmaceu-

t ica l industr y af ter her graduat ion.

R O H I T K H AT TA R i s s p e c i a l i z i n g

i n Fi n a n ce . H e h a s i n te r n e d w i t h

Ta t a C o n s u l t a n c y S e r v i c e s i n i t s

Financia l S olut ions business unit .

Post graduation, he intends to work

in the Financia l S er v ices industr y.

SOURAV DUT TA is a graduate of NIT

D u r g a p u r w i t h d i v e r s i f i e d i n t e r -

e s t s . H e h a s i n t e r n e d w i t h L & T

i n t h e f i e l d o f R i s k M a n a g e m e n t .

E D I TO R - I N - C H I E F

Soumya J yot i S en

E D I TO R I A L B OA R D

Rohit K hattar

Piyush Mar waha

R itesh Gupta

Sourav Dutta

ASSOCIATE EDITORS

Vedik a G aner iwala

Shi lpi Ghosh

CONTRIBUTIONS FROM

Aak anksha Hajela

Bhushan k anathe

Md. Umair Ansar i

Vaibhav G arg

D E S I G N

Team I nFINeet i

F E E D B AC K / q U E R I E S

inf ineet i@i i f t .ac. in

inf ineet i@gmai l .com

P u b l i s h e d b y s t u d e n t s o f I n d i a n Institute of Foreign Trade, New Delhi and Kolk ata

ALL RIGHTS RESER VED

» p.3 » p.11 » p.17

5 DEBT MARKETSAn analys is of the I ndian bond

m a r k e t s a n d t h e c h a l l e n g e s

f a c e d i n t h e I n d i a n s c e n a r i o.

The ar t ic le presents a detai led

v i e w o n t h e n e e d fo r a l i q u i d

debt market and the necessar y

s t e p s t o e n h a n c e l i q u i d i t y i n

I ndian markets.

9 BANKINGBank ing reforms is one of the

m o s t i m p o r t a n t i s s u e s b e i n g

r a i s e d i n t h e g l o b a l f i n a n c i a l

m a r k e t s . W e a n a l y z e t h e

p r o s p e c t s o f b a n k i n g s e c t o r

being more regulated or more

autonomous.

13 TAxATIONT h e i n d i a n e c o n o m y h a s

s t r u g g l e d f o r t h e m o s t

p a r t o f F Y 1 3 . I t h a s l i s t i t s

a t t r a c t i v e n e s s a s a b u s i n e s s

d e s t i n a t i o n . I n d i a i s w o r k i n g

o n t w o m a j o r t a x r e f o r m s .

DTC (Direc t Tax Code) and GST

(Goods and Ser v i ces Tax) . The

ar t ic le presents a v iew on the

need of the tax reforms

17 WORLD ECONOMY Fo r ye a r s , t h e U S d o l l a r h a s

s e v e d a s t h e r e s e r v e c u r -

r e n c y f o r n a t i o n s b u t w i t h

t h e f o c u s s h i f t i n g t o t h e

d e v e l o p i n g c o u n t r i e s i n

As ia , has dol lar lost i ts wor th

a s t h e r e s e r v e c u r r e n c y ?

20 CORPORATE TALK G ain ins ights about the cor-

porate culture and economic

scenario from Barclays Limited

23 ECONOMYT h e i n d i a n g r o w t h s t o r y

h a s h i t a m a j o r r o a d b l o c k .

I s m o n e t a r y p o l i c y t h e

r e a l a n s w e r t o c o n t r o l l i n g

inf lat ion?

27 BANKING NORMSW i t h t h e i n t r o d u c t i o n o f

BASEL I I I norms, the bank ing

i n d u s t r y a c ro s s t h e g l o b e i s

trying to analyze the impact of

the new reforms. We analyze

t h e i m p a c t o f t h e B A S E L I I I

norms on the I ndian bamk ing

industr y.

29 GLOBAL ECONOMY B R I C S , o n e o f t h e m o s t

p r o m i s i n g g r o u p o f c o u n -

t r i e s i s l o s i n g i t s s h e e n .

I s t h i s t h e r i s e o f M I S T ?

32 SUMMER ExPERIENCE

Students from I IFT share their

summer internship experience

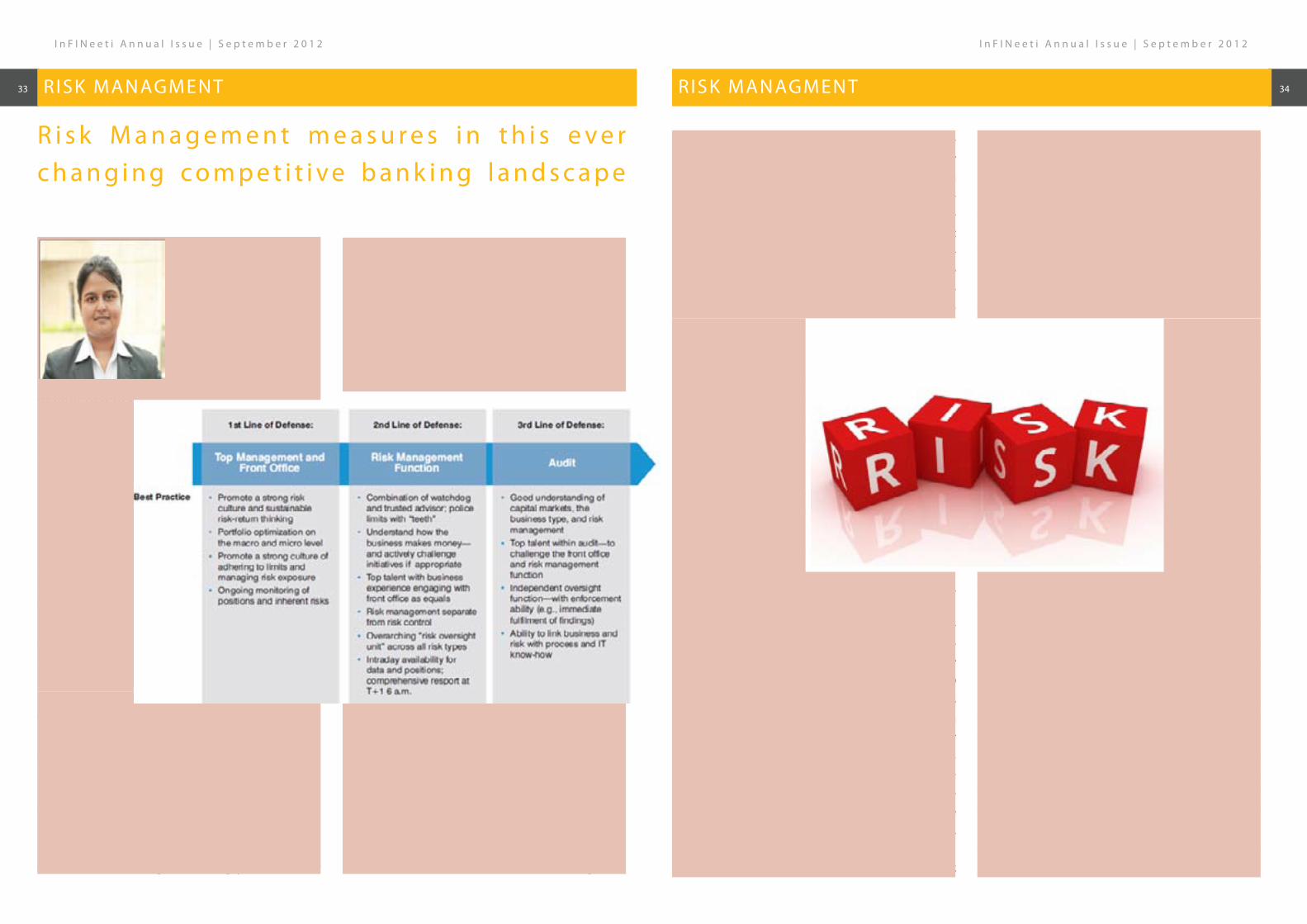

34 RISK MANAGEMENT

W i t h t h e r i s i n g i s s u e s i n

w o r l d e c o n o m y, r i s k m a n -

a g e m e n t i n b a n k i n g s e e m s

to b e t t h e n e e d o f t h e h o u r.

H o w w i l l i t b e e f f e c t i v e

i n t h e p r e s e n t l a n d s c a p e ?

REGULARS

37 MONTHLY CHRONICLES

40 FUN WITH FIN

I n t h e c o v e r s t o r y, o u r

e d i t o r i a l t e a m p r e s e n t s

t h e n e w e r a o f r e g u l a -

t ion in bank ing industr y.

The issue ta lks about the

p ro s a n d c o n s o f m o n e -

t a r y p o l i c y i n I n d i a a n d

the ways to enhance l iquidit y in the market .

I t a lso takes a c loser look on the tax reforms

with a focus on dol lar as the wor ld ’s reser ve

currenc y.

T h e b a n k i n g i n d u s t r y a l l o v e r t h e w o r l d i s

s e t to c h a n g e fo r t h e b e t te r. I t i s i m p o r t a nt

to explore the poss ib le long-ter m ef fe c t s of

t h e f a s t - m ov i n g e c o n o m i c c h a n g e s a n d t h e

host of new oppor tunit ies and r isks are being

unleashed. This i ssue t r ies to address a range

of t imely oppor tunit ies and chal lenges spe -

ci f ic to investment community but relevant to

a l l g lobal investors. With a rat ional ist ic com-

parison of MIST vs BRIC, a detai led explanation

of the need of regulat ion in bank ing industr y

has been c lear ly la id out . Fina l ly a long with

the regular columns, a c loser look at the Basel

3 norms and their impac t on I ndian banks has

been analyzed.

A s b a n k s s t r i v e t o e m e r g e f r o m t h e g l o b a l

f inancia l cr is is , they are encounter ing a new

era of bank ing. I t is one marked by continuing

regulator y uncer tainty and economic instabi l-

i t y, which is h inder ing banks’ abi l i t y to move

f o r w a r d . T h e b a n k i n g i n d u s t r y h a s b e e n

f a c i n g l o t s o f u p s a n d d ow n s ove r t h e p a s t

few years . With scandals happening a l l ove r

the wor ld l ike L IBOR rates being r igged, inves-

tors cannot trust even the wor ld ’ s most stable

f inancia l inst i tut ions. This has generated a lot

of d iscuss ion among bank ing industr y exper ts

about the prerequis i tes for the smooth func -

t ioning of the sec tor. S ome has put stress on

severe regulat ions whereas some are in favour

of automation as the need of the hour. To forge

ahead, industr y leaders say banks must inno -

vate whi le apply ing the lessons of the global

f inancial crisis. To do this, banks are encouraged

to e m p l oy “d i s c i p l i n e d i n n ov a t i o n ,” p u r s u i n g

growth through reasonable r isks. This edit ion

mainly revolves around th is i s sue keeping in

mind the several changes incorporated in the

bank ing industr y in the recent past .

Happy Reading! !

With Warm regards,

Team I nFINeet i

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

3 4CONTENTS MESSAGE FROM THE EDITOR-IN- CHIEF

Soumya Sen i s specia l iz ing in f inance and trade. He has

inter ned at ICF I nter nat ional and has deep interests in

cor porate and t rade f inance.Post h is MBA,he wants to

pursue a career in bank ing.

The debt markets lack of l iquid-i t y, which makes investor demand higher y ie lds on these bonds. Thus mak ing these markets uncompetit ive compared to foreign markets.

I ntroduc t ion

W h e n e v e r t h e

Government announces

i t s b o r r o w i n g c a l e n -

d a r, t h e r e i s h a v o c i n

market with Corporates

being pushed out and interest rates r is ing thus

mak ing pr ivate players look for e i ther expen-

s ive bank f inancing or dol lar/euro/yen denom-

inated ECBs (Ex ternal Commercial Borrowings) .

But inspi te of such a huge demand for rupee

denominated markets only ver y few companies

ra ise money in these markets. The problem is

t h e l a c k o f l i q u i d i t y w h i c h m a k e s t h e i nve s -

tors demand higher yields on these bonds, thus

making these markets uncompetit ive compared

t o fo re i g n m a r k e t s e ve n a f t e r t a k i n g c a re o f

t h e exc h a n g e rate h e d gi n g co s t . Th e n e e d o f

the hour is to take steps to increase l iquidit y

in these markets by lay ing down proper regu-

lat ions and also promoting entr y of big foreign

players l ike FI Is and Domestic Players l ike insur-

a n c e c o m p a n i e s , m u t u a l f u n d s e t c . i n o r d e r

to i n c re a s e p a r t i c i p at i o n a n d h e n ce l i q u i d i t y

i n t h e I n d i a n r u p e e c o r p o r a t e d e b t m a r k e t s .

Current Problems

I n d i a’s s o v e r e i g n b o n d m a r k e t s a t i s f i e s t h e

i m m e d i a c y a n d d e p t h c o n d i t i o n s o n l y f o r

“on-the -run” government bonds ( i .e. , the most

recent ly- issued government bond of a speci f ic

matur i t y ) . O ther wise, the domest ic sovereign

b o n d m a r k e t i s l a rg e l y i n e f f i c i e nt . E xce p t fo r

about 8-10 secur i t ies at a t ime for which t wo

way quotes are avai lable in the market , other

p a r t s o f t h e y i e l d c u r ve re p re s e n t s e c u r i t i e s

t h a t a re n o t a c t i ve l y t r a d e d. Ac t i v i t y i s c o n -

centrated in a few secur it ies due to the market

conf idence in them and the abi l i t y to l iquidate

posit ions quick ly for these speci f ic bonds at a

fa i r value. I n the corporate debt market , inves-

t o r b a s e i s m o s t l y c o n f i n e d t o b a n k s , i n s u r -

a n c e c o m p a n i e s , p r o v i d e n t f u n d s , P r i m a r y

D ealers (PDs) and pension funds. O f late, the

retai l investors have been showing interest in

co r p o r a te b o n d s, e s p e c i a l l y b o n d s i s s u e d by

t h e i n f r a s t r u c t u re c o m p a n i e s t h a t e n t a i l t a x

Enhancing Liquidity in the Debt market : A panacea for India

incent ive. Whi le investors are not shy of debts

i ssued by the top rated f i r ms, they are re luc -

t a n t t o s u b s c r i b e t o t h e l o w e r r a t e d i n s t r u -

ments. This i s an anomaly because lower rated

companies do have access to bank f inancing.

C r e d i t e n h a n c e m e n t b y b a n k s c a n p e r h a p s

m a k e s u c h i n s t r u m e n t s a t t r a c t i v e t o i n v e s -

tors. But on the f l ip s ide, credit enhancement

essent ia l ly involves t ransfer of the credit r i sk

t o b a n k s a n d t h i s w i l l n o t o n l y h a m p e r t h e

d e v e l o p m e n t o f c o r p o r a t e b o n d m a r k e t b y

stunt ing the pr ice d iscover y process but a lso

i n c re a s e t h e r i s k i n t h e b a n k i n g s y s t e m . Th e

fo c u s m u s t b e o n d e - r i s k i n g b a n k i n g s ys te m ,

a n d a t t h e s a m e t i m e, b u i l d i n g / e n c o u r a g i n g

inst i tut ions that provide credit enhancement.

T h e p ro b l e m w i t h a n i n e f f i c i e n t a n d i l l i q u i d

d e b t m a r k e t i s t h a t i t m a k e s c o m p a n i e s g o

o u t s i d e to b o r row t h u s i n c re a s i n g t h e e x te r -

nal debt of the countr y ; a lso i t makes the debt

more prone to change in the exchange rates.

An ef f ic ient debt market wi l l a lso open a new

ave n u e fo r i nve s t o r s w h e re t h e y wo u l d h ave

a b e n e f i t o f g e t t i n g h i g h y i e l d s w i t h o u t t h e

o b l i g a t i o n o f h o l d i n g t h e b o n d t o m a t u r i t y.

M arket Struc ture in Developed M arkets

C o r p o r a t e s i n m a n y d e v e l o p e d m a r k e t s –

p re d o m i n a n t l y i n t h e U S a n d i n c re a s i n g l y i n

other jur isdic t ions - have a marked preference

t o t a p t h e b o n d m a r k e t r a t h e r t h a n t o s e e k

bank loans for meet ing their ex ternal f inance

r e q u i r e m e n t s . I n I n d i a , h o w e v e r, c o m p a n i e s

c o n t i n u e t o d e p e n d o n t h e b a n k i n g s y s t e m

f o r f u n d s b e c a u s e o f e a s e o f a v a i l i n g b a n k

f inance, absence of credit r isk mitigation mech-

a n i s m s a n d a h o s t o f o t h e r f a c t o r s , s u c h a s ,

absence of sound bank ruptc y f ramewor k and

l a c k o f a c t i ve i nte re s t o f l o n g - te r m i nve s to r s

l i k e i n s u r a n c e c o m p a n i e s . Co r p o r a t e s p re fe r

r a i s i n g f u n d s t h ro u g h p r i v a t e p l a c e m e n t s a s

against public issuances because of operational

ease of issuance under pr ivate placements with

minimum disc losures, low cost of i ssuance and

the speed of raising funds. The issuance process

is also impacted by costs, such as, stamp duties,

t r a n s fe r c o s t s , e t c . w h i c h n e e d s r a t i o n a l i z a -

t ion. Preference for pr ivate p lacement i s a lso

d i c t a t e d b y t h e p ro f i l e o f i nve s t o r s w h i c h i s

most ly inst i tut ional and a narrow base at that .

N e e d s fo r a n e f f i c i e nt l i q u i d d e b t m a r k e t in I ndia :

a) Ensur ing f inancia l system stabi l i t y :

A l iquid corporate bond market can play a cr i t-

ica l ro le because i t supplements the bank ing

s ys te m to m e e t t h e re q u i re m e n t s o f t h e co r -

porate sec tor for long-term capita l investment

a n d a s s e t c r e a t i o n . B a n k i n g s y s t e m s c a n n o t

b e t h e s o l e s o u r c e o f l o n g - t e r m i nv e s t m e n t

c a p i t a l w i t h o u t m a k i n g a n e co n o my v u l n e ra -

b l e t o e x t e r n a l s h o c k s . H i s t o r i c a l a n d c ro s s -

sec t ional exper ience has shown that systemic

p r o b l e m s i n t h e b a n k i n g s e c t o r c a n i n t e r -

r u p t t h e f l o w o f f u n d s f ro m s a ve r s t o i nve s -

t o r s f o r a d a n g e r o u s l y l o n g p e r i o d o f t i m e .

I n d e e d , o n e o f t h e l e s s o n s f r o m t h e 1 9 9 7

A s i a n f i n a n c i a l c r i s i s h a s b e e n t h e i m p o r -

t a n c e o f h a v i n g n o n - b a n k f u n d i n g c h a n -

n e l s o p e n . I n t h e a f t e r m a t h o f t h i s c r i s i s , a

n u m b e r o f co u nt r i e s i n t h e re gi o n , i n c l u d i n g

K o r e a , M a l a y s i a , S i n g a p o r e a n d H o n g K o n g,

h a v e m a d e p r o g r e s s i n b u i l d i n g t h e i r o w n

c o r p o r a t e d e b t m a r k e t s . S p r e a d i n g c r e d i t

r i s k f ro m b a n k s b a l a n ce s h e e t s m o re b ro a d l y

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

5 6 INDIAN ECONOMY INDIAN ECONOMY

t h r o u g h t h e f i n a n c i a l s y s t e m w o u l d l o w e r

t h e r i s k s t o f i n a n c i a l s t a b i l i t y. B o n d f i n a n c -

i n g r e d u c e s m a c r o e c o n o m i c v u l n e r a b i l i t y

t o s h o c k s a n d s y s t e m i c r i s k t h r o u g h d i v e r -

s i f i c a t i o n o f c r e d i t a n d i n v e s t m e n t r i s k .

b ) E n a b l i n g m e a n i n g f u l cove r a g e o f re a l sec tor needs:

The f inancia l sec tor in I ndia is much too smal l

to cater to the needs of the rea l economy. A

c o m p a r i s o n o f t h e a s s e t s i z e o f t h e t o p t e n

Corporates and that of the top f ive banks (as

shown in Figure 1 below) reveals that banks in

I ndia are unable to meet the scale or sophis-

t i c a t i o n o f t h e n e e d s o f c o r p o r a t e I n d i a .

N e e d l e s s t o s a y, t h e f i n a n c i a l s y s t e m i s n o t

b i g e n o u g h t o m e e t t h e n e e d s o f s m a l l a n d

medium-sized enterpr ises e i ther. Whi le these

are pointers to the fact that the banking sector

i n I n d i a n e e d s t o b e l a r g e r t h a n i t s c u r r e n t

s i z e , t h e y a re a l s o c l e a r i n d i c a t o r s t h a t d e b t

markets need to grow manifold to ensure that

the f inancia l sec tor becomes adequate for an

economy as large and as ambit ious as I ndia’s .

c ) Creat ing new c lasses of investors :

C o m m e r c i a l b a n k s f a c e a s s e t - l i a b i l i t y m i s -

m a t c h i s s u e s i n p r o v i d i n g l o n g e r - m a t u -

r i t y credi t . D e velopment of a cor porate debt

market wi l l enable par t ic ipat ion f rom inst i tu-

t i o n s t h a t h ave t h e c a p a c i t y a s we l l a s a p t i -

tude for longer matur i t y exposures. Financia l

i n s t i t u t i o n s l i k e i n s u r a n c e c o m p a n i e s a n d

provident funds have long-term l iabi l i t ies and

d o n o t h ave a cce s s to a d e q u ate h i gh qual i t y

long-term assets to match them. Creat ion of a

deep corporate bond market can enable them

t o i nv e s t i n l o n g - t e r m c o r p o r a t e d e b t , t h u s

ser ving the twin goals of diversifying corporate

INDIAN ECONOMY

r i s k a c ro s s t h e f i n a n c i a l s e c to r a n d e n a b l i n g

these inst i tut ions to access high qual i t y long-

t e r m a s s e t s . T h u s , a c c e s s t o l o n g - t e r m d e b t

opens up the market to new classes of investors

with an appetite for longer matur ity assets and

t h e re b y h e l p s p re ve n t m a t u r i t y m i s m a t c h e s .

d) Reduced currenc y mismatches :

T h e d e v e l o p m e n t o f l o c a l c u r r e n c y b o n d

m a r k e t s h a s b e e n s e e n a s a w a y t o a v o i d

cr is is , not only by supplementing bank credit

b u t a l s o b e c a u s e t h e s e m a r k e t s h e l p re d u c e

p o t e n t i a l c u r re n c y m i s m a t c h e s i n t h e f i n a n -

c i a l s y s t e m . C u r r e n c y m i s m a t c h e s c a n b e

a v o i d e d b y i s s u i n g l o c a l c u r r e n c y b o n d s .

Thus, wel l - developed and l iquid bond markets

c a n h e l p f i r m s r e d u c e t h e i r o v e r a l l c o s t o f

capi ta l by a l lowing them to ta i lor the i r asset

a n d l i a b i l i t y p r o f i l e s t o r e d u c e t h e r i s k o f

b o t h m a t u r i t y a n d c u r r e n c y m i s m a t c h e s .

e ) Te r m s t r u c t u re a n d e f fe c t i ve t ra n s m i s -s ion of monetar y pol ic y :

T h e c re a t i o n o f l o n g - t e r m d e b t m a r k e t s w i l l

a lso enable the generat ion of market interest

rates at the long end of the y ie ld cur ve – thus

f a c i l i t a t i n g t h e d e ve l o p m e n t o f a m o re co m -

plete term structure of interest rates. A deeper,

more responsive interest rate market would in

turn provide the central bank with a mechanism

for ef fec t ive t ransmiss ion of monetar y pol ic y.

Conclus ion

T h e i m p l e m e n t a t i o n o f v a r i o u s m e a s u re s fo r

i n c re a s i n g t h e e f f i c i e n c y a n d l i q u i d i t y o f t h e

INDIAN ECONOMY

Panel A : Assets of top 10 Cor porates (2011) Panel B : Capita l funds and exposure l imits of top 15

banks (2011)

d e b t m a r k e t s w i l l h e l p t o m a i n t a i n f i n a n -

c i a l s t a b i l i t y a n d p r o v i d e a m o r e o p t i m a l

w a y f o r C o r p o r a t e s t o r a i s e a n d i n v e s t o r s

t o i nve s t m o n e y t h e re b y b e n e f i t i n g t h e re a l

s e c t o r w h i l e a l s o i m p r o v i n g t h e t r a n s m i s -

s i o n o f m o n e t a r y p o l i c y i n t h e e c o n o m y.

R ahul Bakshi-The author is a student of I IM- I ndore

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

7 8

regulat ion of the f inancia l system. The recent

developments raise debates about the need for

improved regulat ion of bank ac t ivity for f inan-

c ia l s tabi l i t y.

The recent histor y of regulator y reform in Bank ing

T h e d i m i n i s h i n g e f fe c t i ve n e s s o f t r a d i t i o n a l

controls due to f inancia l innovat ion and rapid

technological development, the development

of regulator y avoidance, competit ion between

international f inancial centers are some reasons

why reform was needed.

U n t i l e a r l y 1 9 7 0 ’s t h e B a n k i n g s y s t e m c o n -

t r o l l e d t h e

pr ices, quan-

t it ies of busi-

n e s s c o n -

d u c t e d a n d

t h e m a r k e t

a c c e s s . B u t

s i n c e m i d

1 9 7 0 ’s t h e r e

i s a s i g n i f i -

c a n t p ro c e s s

of regulator y

r e f o r m i n

m o s t c o u n -

t r i e s a n d a

shi f t towards

m o r e m a r k e t - o r i e n t e d f o r m s o f r e g u l a t i o n -

L i b e r a l i ze d I n te re s t R a te , I nve s t m e n t s , L i n e -

of-business, ownership l ink ages and entr y of

B a n k i n g i s a m o n g t h e

wor ld ’s most t ight ly re g u-

lated businesses. But most

of the economic problems

i n t h e p a s t t w o h u n d r e d

years were caused by banks

and speculators . Af ter the

g r e a t d e p r e s s i o n , s o u n d

bank ing reforms ensured economic stabi l i t y

and prosperity for many years. Post sub-prime

cr is is , the Banks are re luc tant to implement

the regulator y reforms saying it inhibits inno-

v a t i o n a n d r a i s e s b a r r i e r s to e n t r y. Ca n we

t rust the Banks to regulate themselve s ?The

re c e n t t i m e s re ve a l m a ny f i n a n c i a l i n s t i t u -

t ions fa i l ing. I n this ar t ic le we deal with the

b e n e f i t s a n d co s t

a s s o c i a t e d w i t h

the bank ing regu-

lation, how auton-

o my c a n h e l p t h e

b a n k s a n d w h a t

i s r e a l l y n e e d e d

c o n s i d e r i n g t h e

c u r r e n t f i n a n c i a l

s i tuat ion.

I ntroduc t ion

T h e r e c e n t

h o u s i n g b o o m ,

bust , the f inancial

cr is is and severe recession that fol lowed, con-

t inue to af fec t us. These events have shaped

the economic recover y and transformed the

S h o u l d b a n k s w o r l d w i d e b e g i v e n m o r e autonomy- the need of the hour?

foreign f inancia l inst i tut ions. Bank branching

restr ictions were phased out and in a number of

European countries by the early 1990s.Breaking

down the barr iers imposed by the (1933) Glass-

Steagal l Ac t , the Gramm-Leach-Bl i ley Financial

S er v ice M oder nizat ion Ac t of 1999 per mitted

f inancia l holding company.

Benef i ts

Some benef i ts are :

1.Freedom to adopt the most eff icient practices

& develop new produc ts and ser v ices.

2.Competit ion-forcing the exit or consolidation

of re lat ively inef f ic ient f i rms.

3 . I m p r o v e m e n t s i n t h e q u a l i t y, v a r i e t y a n d

access to new f inancia l instruments &ser vices.

4 . I mproved wor ld a l locat ion of resources due

to the removal of the barr iers to internat ional

capita l f lows.

Regulator y reform and competit ion expanded

the reach of bank ing to the under pr iv i leged.

R e g u l a t i o n i s e s s e n t i a l b e c a u s e t h e l i q u i d i t y

of bank l iabi l i t ies i s a publ ic good. The uncer-

ta int y is an unquant i f iable r isk- a learning gap

w h i c h c a n n e v e r b e c l o s e d . B a n k i n g r e g u l a -

t ion & super vis ion suppor ts the evolut ion of a

bank ing system which produces money as an

asset to hold in t imes of par t icular uncer tainty.

The struc ture of the f inancia l system has been

u n d e r g o i n g m a j o r c h a n g e , w h i c h c e r t a i n l y

involves a major rethink about regulat ion.

Free banker ’s cr t iques

They say that the uncer tainty can be el iminated

and f inancia l assets can be valued in the same

w ay a s g o o d s, s o t h a t t h e re i s n o re a s o n fo r

banks to be regulated. I nstabi l i t y i s a result of

unwise por tfolio decision. In the absence of reg-

ulat ion, the market disc ipl ine banks adopting

prudent por tfol ios.Free bankers argue that the

r isk of contagion does not just i fy the need for

regulat ion.They say that deposits could s imply

be t ransferred f rom banks with unsound por t-

fol io to banks with sounder por t fol ios thereby

having sound por tfol io management.

Co n t ra r y a rg u m e n t : As s e t v a l u e s c a n b e p re -

d i c t e d , b u t v a l u a t i o n s a r e c o n t i n g e n t o n

a r a n g e o f u n k n o w n s. I t i s d i f f i c u l t e ve n fo r

centra l bankers to deter mine whether a bank

h a s a l i q u i d i t y / s o l v e n c y p r o b l e m . I f t a c t i c s

l ike deposit insurance and lender- of- last-resor t

faci l it ies were applied successfully, banks could

b e p r o t e c t e d f r o m f a i l u r e i n a f r e e b a n k i n g

system but that i s a far cr y and the f ree bank-

er ’s argument ignores the potential for systemic

instabi l i t y.

Why regulate stable, d ivers i f ied banks?

Autonomy entai ls operational f reedom. I t faci l -

i tates pr ice and f inancia l sec tor stabi l i t y that

are impor tant for achieving sustainable growth.

BANKING

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

9 10 BANKING

M o n e t a r y p o l i c y i s s u p e r e s s e nt i a l fo r w h i c h

the bank should be given some AUTONOMOUS

p o we r. A s o u n d a n d s t a b l e f i n a n c i a l s y s t e m

including an ef f ic ient payment system is a lso

impor tant for a market economy to real ize i ts

ful l potential. Accountabil ity, transparency and

good governance should be present .

Fi t c h R a t i n g s r e c e n t l y s a i d t h a t t h e c a p i t a l

r e q u i r e m e n t s a s p e r B A S E L I I I w i l l i n c r e a s e

t h e l e n d i n g r a t e , i m p a c t t h e e c o n o m i c

output thereby ex tend the current recess ion.

Fur thermore, in Europe the government bonds’

y i e l d i s i n c re a s i n g, t h a t i s , t h e b o n d s a re n o

more attrac t ive. This in turn wi l l squeeze the

m a r k e t t h a t b a n k s c a n u s e t o m e e t t h e n e w

capita l requirements.

Government and tax payers are not at the r isk

for bai l ing out the depositors i f insured banks

f a i l b e c a u s e , t h e y j u s t h a ve t o m a k e u p t h e

di f ference when the loss exceeds the amount

accumulated through premiums.

Flaw in the f inancia l regulat ion system

Some macrolevel shor tcomings were:

•No attent ion to the stabi l i t y of the f inancia l

system as a whole.

•No measurement of the degree to which the

turmoi l in the f inancia l system can af fec t the

economy.

• I nadequate concentrat ion on the safet y and

soundness of individual depositor y institutions

in an age of g lobal interdependenc y.

We ex p e r i e n ce d t h e co l l a p s e o f b a n k i n g a n d

s av i n g s - a n d - l o a n i n d u s t r i e s , w i t h h u g e co s t s

t o t a x p a y e r s a n d t h e e c o n o my. T h e f a c t t h a t

this happened to heavi ly regulated industr ies

makes us think whether regulat ion does more

harm than good?

The reason for moral hazard is the absence of

market disc ipl ine because of government reg-

ulator y pol ic ies . D epositors and shareholders

we re lu l le d by pre v ious ac t ions of regulators

into bel ieving that even i f the inst itution fai led

they would somehow be protec ted.

Cost of bank ing regulat ion

Bank ing regulation curbs the abi l i ty of bank ing

houses to move out of recess ion and re -boot

t h e e c o n o my. A n e x a m p l e o f re s t r i c t i n g a n d

costly bank ing regulat ion is Obama’s trenchant

and restr ic t ive Dodd-Franck ac t .

The ‘quasi-nationalization’ of the banking sector

through a policy that combines a high degree of

regulat ion and bai louts wi l l d isrupt long-term

economic growth. Apar t f rom restr ic t ing credit

through profit loss on regulator y compliance, it

may result in the shi f t of r i sk to general credit

t ra n s a c t i o n s. O n t h e b a c k o f t h e J . P. M o rg a n’s

b i l l i o n d o l l a r l o s s e s , t h e re i s n o w a t e m p t a -

t ion in the EU to pass a measure s imi lar to the

Volcker rule in the U.S Dodd’s-Franck Ac t .

Wh a t m a k e s u s re a l i s e t h e i m p o r t a n ce o f regulat ion?

I n 1970,the debt cr is is i l lustrated the need for

centra l bank ing func t ions that natural ly ar ise

i n a d e r e g u l a t e d e nv i r o n m e n t . W h a t m o s t o f

u s d i d n’t k n ow b e fo re 2 0 0 7 w a s e x a c t l y h ow

they made prof i ts . But the banks over-reached

themselves. They expanded too rapidly. In 2007

a n d 2 0 0 8 , t h e i r s c h e m e s b e g a n t o u n r a v e l .

We l e a r n t a b o u t s u b - p r i m e m o r t g a g e s , l i a r s ’

loans, and derivatives where loans were repack-

aged, sold and re -sold so that any connec t ion

b e t w e e n b o r r o w e r a n d t h e f i n a l l e n d e r w a s

broken.

The recent a l legat ions were Barc lays -M ar ket

interest rate manipulation, HSBC-Mexican drug

m o n e y l a u n d e r i n g a n d S t a n d a r d C h a r t e r e d -

Iranian oil money laundering.The culture began

in 1986, when Margaret Thatcher ’s government

i n t r o d u c e d t h e “ B I G B A N G ” D E R E G U L AT I O N

that introduced the culture of r isk-tak ing, b ig

bonuses and a focus on shor t-term returns.The

f inancia l instruments are so complex i t of ten

takes months to f igure out how much was lost

and where the money went .Banks used higher

leverage to maximize prof i ts f rom D er ivat ive

produc ts. One example is the recent col lapse

of MF Global .

Dodd-Frank has tr ied to reduce the costs asso -

ciated with the regulation by focusing on inst i-

tut ions whose operat ions bear most cr i t ica l ly

o n t h e s t a b i l i t y o f t h e f i n a n c i a l s y s t e m a s a

whole. I t addressed the too -big-to -fai l problem

by a l l ow i n g t ro u b l e d s y s te m i c a l l y i m p o r t a n t

f inancia l inst i tut ions to be shuttered.

T h e b a n k i n g s e c t o r h a s u n d e r g o n e m a j o r

c h a n g e s ove r t h e l a s t fe w ye a r s . Th e re g u l a -

t ion rests on economic role of money andun-

cer ta int y.This uncer ta int y in turn renders f ree

b a n k i n g u nwo r k a b l e . R a t h e r t h a n s ay i n g re g -

ulat ion i s unnecessar y, the more appropr iate

response is to consider how to improve the reg-

ulat ion. Good regulator y pol ic y should take a

broad view of the way rules affect economy and

s o c i e t y, w h i l e m a i n t a i n i n g a s u i t a b l e d e g re e

o f h u m i l i t y a b o u t t h e a b i l i t y t o a c c u r a t e l y

q u a nt i f y t h e re l e va nt b e n e f i t s a n d co s t s . Th e

bank ing industr y should have ef fec t ive chan-

n e l s f o r v o i c i n g c o n c e r n s a b o u t b u r d e n o r

about lack of c lar ity regarding regulator y stan -

dards and super visor y expec tat ions.A for ward-

look ing macro prudent ia l approach must con-

sider how the f inancial system is l ikely to evolve

over t ime. For example, what systemic i ssues

are ra ised by new f inancia l produc ts , such as

complex derivatives? We want a dist inct regime

for systemical ly impor tant inst i tut ions.

S o w r i r a j a n S a n d R a m a n a i d u D. S . T-T h e a u t h o r s a r e

s t u d e n t s o f I n s t i t u e f o r F i n a n c i a l M a n a g e m e n t a n d

Reseacrh,Chennai

BANKING BANKING

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

11 12

GOVERNMENT AND TAxES

Tax Reforms:An I ndian Perspec t ive

I n order to make i tse l f an

a t t r a c t i ve b u s i n e s s d e s t i -

nat ion and to increase tax

receipts, India is working on

two major tax reforms. DTC

(Direc t Tax Code) and GST

(G o o d s a n d S e r v i ce s Ta x ) .

Let ’s look at the trend in combined tax receipts

for Union and the States.The trend looks hear t-

e n i n g . I n f a c t t h e r a t e o f g r o w t h h a s o u t -

paced the GDP growth rate by a huge margin.

B u t , i f w e l o o k a t t h i s w i t h a b a c k d r o p o f

t h e p i l i n g f i s c a l d e f i c i t , p l u m m e t i n g i n v e s -

t o r c o n f i d e n c e a n d w i d e n i n g t r a d e d e f i c i t

we’ l l u n d e r s t a n d w hy t h e f i n a n ce m i n i s t r y i s

busy look ing for avenues to increase receipts.

The broad struc ture of the tax system and the

associated tax reforms are shown in the f igure

Direc t Tax

DTC i s s a i d t o r e p l a c e t h e e x i s t i n g I n d i a n

I ncome Tax Ac t , 1961. I t seeks to consol idate

a n d a m e n d t h e l aw s u n d e r I T Ac t a n d f a c i l i -

tate voluntar y compliance to help increase the

t a x- G D P r a t i o. Le t ’s fo c u s o n t h e t a x re fo r m s

I ncome Tax

What percentage of over 1 .21 bi l l ion popula-

t ion of the countr y pays income tax?

J u s t a b o u t 2 . 8 % ! C o m p a r e t h i s w i t h o v e r

4 5 % f o r U S A . T h u s t h e r e i s a n e e d t o b r i n g

m o re p e o p l e u n d e r t h e a m b i t o f t h e I n c o m e

Ta x . DTC i s p r o p o s e d t o a c h i e v e t h i s g o a l .

S o m e o f i t s s a l i e n t fe a t u re s a re a b o l i t i o n o f

s u r c h a r g e , e d u c a t i o n c e s s a n d L e a v e Tr a v e l

Al lowance. Deduc t ions up to 1 .5 lak hs, under

‘S ec 80C ’, to be a l lowed. No d i f ference in tax

slabs for male and females and many more. These

changes a im to increase the compl iance base

and thus increase the Tax receipts. The changes

are being implemented step by step ever y year.

Corporate Tax

I n d i a h a s e n t e r e d i n t o D o u b l e Ta x a t i o n

A v o i d a n c e A g r e e m e n t ( D TA A ) ; w i t h d i f f e r -

ent countr ies . S ome mult inat ional companies

operat ing in I ndia exploit the loopholes in the

DTAA by rout ing their investment through the

countr ies I ndia has DTAA with . Whi le there i s

no wrong in having a holding company there,

i t o f t e n t u r n s o u t t o b e a s h e l l c o m p a n y.

T h u s , t o t a x s u c h t r a n s a c t i o n s , G A A R

( G e n e r a l A n t i A v o i d a n c e R u l e s ) w a s i n t r o -

d u c e d i n t h e U n i o n B u d g e t o f 2 0 1 2 - 1 3 .

B u t , i t w a s r e c e i v e d w i t h a p p r e h e n s i o n

b e c a u s e o f l a c k o f c l a r i t y a n d c e r t a i n p r o -

v i s i o n s r e l a t e d t o i t s r e t r o s p e c t i v e n a t u r e .

The investor conf idence took a dip and the F I I

inflows took a U-turn. In contrast to high invest-

ment in stock market in the Jan-Mar quar ter, FI I

inf lows were negat ive for the month of Apr i l .

The stock market saw a gradual fa l l f rom about

1 7 5 0 0 p o i n t s i n M a r c h e n d t o a b o u t 1 6 0 0 0

points in May end. Thus to boost investor confi-

dence CBDT, in May, formed a s ix-member com-

mittee to draf t guidel ines for enforc ing GAAR.

GOVERNMENT AND TAxES

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

13 14

D r a f t g u i d e l i n e s r e l e a s e d i n

J u n e e n d m a j o r l y i n c l u d e d -

1 . The tax rules wi l l apply to income accruing

only on or after April 1, 2013 and that a monetary

threshold is a must for invoking GAAR provisions.

2 . G A A R w i l l b e i n v o k e d o n l y i f a n

F I I t a k e s t h e b e n e f i t o f a n y D T A A .

3 . G A A R p r o v i s i o n s w i l l n o t a p p l y i n c a s e s

where tax t reat y agreements are not invoked.

4 . S e t t i n g u p a n a p p r o v i n g p a n e l

o f n o t l e s s t h a n t h r e e m e m b e r s .

I t a l s o p ro v i d e d a n i n d i c a t i ve l i s t o f d e a l s /

t r a n s a c t i o n s / a r r a n g e m e n t w h e r e G A A R w i l l

be invoked. Whi le tax mit igat ion us ing avai l -

a b l e p r o v i s i o n s i n t h e l a w i s a l l o w e d , i t

i s t a x a v o i d a n c e t h a t G A A R w a s t o d e t e r.

These new guidel ines too did not go wel l with

all the stake holders.Thus, PM Manmohan Singh,

in charge of the f inance por t fol io in June, set

up a committee to begin the process of con -

s u l t at i o n s w i t h va r i o u s s t a k e h o l d e r s i n a b i d

to f i n e - t u n e w h a t h a d h i t h e r to b e e n v i e we d

as controvers ia l provis ions and usher in more

clar ity and transparency in the draft guidelines.

T h e o v e r a l l s e n t i m e n t s i n c e t h e n h a s

b e e n p o s i t i v e a n d t h e r e t u r n o f c o n f i -

d e n c e i s e v i d e n t b y t h e r a l l y a t t h e s t o c k

m a r k e t s f r o m a l o w a b o u t 1 6 t h o u s a n d

points in M ay end to about 17500 in August .

I ndirec t Tax

GST (Goods & Ser vices Tax) is an ambitious prop-

osit ion to create a seamless nat ional common

market, by subsuming most of the indirect taxes

i m p o s e d b y t h e s t a t e a n d t h e g o v e r n m e n t .

Indirect taxes are a hotch-potch of Union Excise

Duty, State Excise Duty, Addit ional Excise Duty,

S e r v i c e Ta x , S a l e s Ta x , C u s t o m s , A d d i t i o n a l

Customs Duty, Special Additional Duty, VAT etc.

Viewed through a f iscal lens, the countr y is not

one market, but 28 states, each with its own tax-

raising powers, which they are not afraid to use.

Compl icated laws, cascading, squabbl ing over

what constitutes a good and what is a service etc are

some major issues with the present web of taxes.

T h i s m u l t i p l e t a x r e g i m e a c r o s s s e c t o r s o f

p r o d u c t i o n a n d s t a t e s l e a d s t o d i s t o r t i o n s

i n a l l o c a t i o n o f r e s o u r c e s t h u s i n t r o d u c -

i n g i n e f f i c i e n c i e s i n d o m e s t i c p r o d u c t i o n .

O n ce G S T i s i m p l e m e nte d a p a r t f ro m m a k i n g

l i f e e a s y f o r l o c a l i n d u s t r i e s , i t w i l l a t t r a c t

fo re i gn f u n d f l ows. Acco rd i n g to e s t i m ate s i t

wi l l lead to an increase in GDP of 0 .7% to 1 .7%.

O n e o f t h e m a j o r c h a l l e n g e s i n i m p l e m e n t -

i n g G S T i s a r r i v i n g at a re ve n u e n e u t ra l rate .

A revenue -neutra l rate is one at which a state

would not record any gain or loss af ter switch-

ing to GST. The higher a state’s revenue -neutral

rate, the more compensation it would seek from

t h e Ce n t re . O t h e r c h a l l e n g e s i n c l u d e i m p l e -

mentat ion of IT I nf rastruc ture, Const i tut ional

A m e n d m e n t , D i s p u t e r e s o l u t i o n m e c h a -

n i s m a n d c r e d i t m e c h a n i s m b e t w e e n s t a t e s .

S er vice Tax Regime

S h a r e o f s e r v i c e s e c t o r i n c o u n t r y ’s G D P

h a s r i s e n f ro m 5 0 . 4 % i n 2 0 0 0 - 0 1 t o 5 9 . 0 % i n

2 0 1 1 - 1 2 . B u t , s h a re o f S e r v i c e Ta x i s a l i t t l e

m o r e t h a n 1 % o f t h e G D P. We h a v e c o m e a

l o n g w a y s i n c e 1 9 9 4 w h e n t h e s e r v i c e t a x

w a s i n t r o d u c e d . S i n c e t h e n a p o s i t i v e l i s t

approach. i .e . ser v ices included in the l i s t wi l l

h a v e t o p a y s e r v i c e t a x , h a s b e e n fo l l o w e d .

There is an alternate concept of international ly

followed negative list according to which the ser-

vices included in the negative list will be exempt,

rest al l ser vices wil l have to pay the ser vice tax.

A s a m o v e t o w a r d s i m p l e m e n t i n g t h e G S T,

s e r v i c e t a x r e g i m e b a s e d o n n e g a t i v e l i s t

w a s i m p l e m e n t e d f r o m J u l y 1 s t . , 2 0 1 2

St ate s h ave ra i s e d co n ce r n s to ce r t a i n i te m s,

w h i c h t h e y s a y a r e l e a d i n g t o d o u b l e t a x a -

t ion. As of now some of these i tems have been

added to the negative l ist and a consensus wi l l

b e re a c h e d w h e n t h e G S T g e t s i m p l e m e nte d.

Conclus ion

These tax reforms would def in i te ly help us in

substant iat ing our stance and would strongly

portray our image of being the – ‘Incredible India’ .

G aurav Tiwar i -The author is a student of I IFT

GOVERNMENT AND TAxES GOVERNMENT AND TAxES

26328

35228

1792

-4896

3222 1180

-10000

0

10000

20000

30000

40000

Jan Feb Mar Apr May Jun

FII Investment

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

15 16

I s i t t h e e n d o f D o l l a r a s Wo r l d ’s r e s e r v e Currenc y?

A Br ief H istor y of the US

Dol lar

The dol lar was chosen as

t h e c u r r e n c y o f U n i t e d

S t a t e s b y t h e p a s s a g e

o f t h e C o i n a g e A c t o f

1 7 9 2 , r e c o m m e n d e d b y

A l e x a n d e r H a m i l t o n , t h e t r e a s u r y s e c r e t a r y

t h e n . M a n y t h e o r i e s e x i s t o n t h e o r i g i n o f

t h e s y m b o l o f t h e d o l l a r ( $ ) s u c h a s Th e Pe s o

Abbreviat ion Theor y(the most widely accepted

theor y now) , The US Abbreviat ion Theor y, The

S h i l l i n g A b b r e v i a t i o n T h e o r y, e t c . T h e Pe s o

Abbreviat ion Theor y puts for ward the fac t that

the dol lar symbol is der ived f rom the Spanish

Peso.

Dol lar izat ion

I t was in 1944 the US dol lar replaced the UK ’s

Po u n d S t e r l i n g a s t h e wo r l d ’s re fe re n c e c u r-

renc y. This was agreed af ter the Bretton Woods

Conference of 1944 ,when the exchange rates

were pegged against the US Dollar which could

be exchanged for a f ixed amount of gold thereby

strengthening the posit ion of US Dol lar as the

wor ld currenc y. The col lapse of the USSR re in-

forced the predominance of dol lar as a wor ld

currency. Stabil ity has been a key factor for the

adopt ion of US D ol lar as of f ic ia l cur renc y by

several countr ies. Devaluat ion has never hap -

pened with the US Dollar. The emergence of the

Japanese Yen in 1980’s posed a ser ious threat

to the Dol lar as wor ld currenc y but thanks to

the recess ion in Japan in 1990’s aver ted that

threat . The arr ival of the Euro had a lso posed

a threat to the Dol lar as wor ld currenc y.

Threat to the Dol lar ?

T h e s h i f t i n t h e e c o n o m i c p o w e r f r o m t h e

western hemisphere to the eastern hemisphere

i s t h e e m i n e n t d a n g e r t h a t l u r k s o v e r t h e

supremac y of the US Dollar. A study conducted

by IMF has projec ted the sh i f t in Purchas ing

Power Par i t y of the wor ld f rom the west to the

east within a t ime span of 18 years .The most

l ikely contender to substitute the Dollar would

be the Chinese Yuan. The growth tra jec tor y of

China shows that it would over take the US to be

the world’s largest economy by 2020(Economic

Times Repor t) . Some of the banks have already

star ted given a higher impor tance to the Yuan

i n co m p a r i s o n to t h e U S D o l l a r by a d o p t i n g

Yuan as the S ett lement Currenc y.

From the forecast above , the emphasis should

be la id on the emergence of 2 new economic

superpowers – China & I ndia . The role played

by the t radit ional economic powerhouses l ike

J a p a n & G e r m a ny a l o n g w i t h t h e U S w i l l b e

The US Abbreviation Theory states that the dollar sign has been derived from the initials of the US

Unofficial Dollarization might lead to inability of local governments to control inflation & fiscal policy

s i d e l i n e d l e a d i n g t o a s h i f t i n t h e e c o n o m i c

power balance as stated ear l ier.

The future of the present ly a i l ing US economy

w o u l d b e i n f l u e n c e d g r e a t l y b y s h o r t t e r m

g l o b a l f a c t o r s l i k e a n o i l s h o c k o r a n a t u r a l

d isaster ,etc. The sustenance of the US Dol lar

h e g e m o n y w o u l d d e p e n d u p o n t h e p e r f o r -

mance of the US Economy. A potent ia l threat

to t h e U S e co n o my co u l d b e t h e o p e n i n g u p

of another war f ront in a place l ike I ran/Syr ia .

The fai lure of a couple of Major US banks could

p l u n g e t h e U S e co n o my i nto a d e e p e r a bys s .

These are some of the major fac tors that could

affec t the US economy thereby having a poten-

t ia l to inf l ic t severe damage on the s tatus of

the US Dollar as the world’s reference currenc y.

The present economic cr is is has also led the US

Government to reduce the interest rates to the

minimum possible so as to stimulate investment

in the economy. However, th is move wi l l be a

d e t e r re n t fo r t h e O P E C n a t i o n s ( b a r r i n g I r a n

) to co n d u c t O i l Tra n s a c t i o n s i n D o l l a r s . Th i s

i s because the petrodol lar system wi l l be less

a l lur ing to them on account of the lower inter -

est rates that the US Secur i t ies would provide

them. This wi l l lead to the shi f t ing away of the

O P E C co u n t r i e s f ro m t h e Pe t ro d o l l a r s y s te m .

I n such a scenar io , petro leum being a major

commodity transacted in the world market, wil l

c a u s e t h e b r e a k d o w n o f d o l l a r a s t h e w o r l d

reference cur renc y as major i t y of the nat ions

would not purchase Petroleum from the OPEC

countr ies us ing Dol lars but by some other cur-

renc y that gives better returns.

A Wor ld without Dol lar ?

This could be a real i t y within a generat ion. I f

at a l l the Dol lar i s ousted as the reference cur-

renc y and i f there is no currenc y to occupy that

p o s i t i o n , t h e n g l o b a l i n f l at i o n wo u l d r i s e a s

impor tant commodities l ike oi l ,precious metals

& a gr i c u l t u ra l g o o d s wo u l d r i s e s u b s t a nt i a l l y

to compensate for the same. This wi l l h i t the

emerging markets l ike China, I ndia ,etc.

H owe ve r, we s h o u l d a l s o a n a l y ze t h e s u b s t i -

t u te s av a i l a b l e , o t h e r t h a n t h e C h i n e s e Yu a n

which has been discussed ear l ier. Let us look

at the some of the different possible substitues

1.Euro - I f we look at the European Union now ,

what is visible is that there are a large number of

countr ies that are fac ing sovereign debt cr is is .

Some of them are tr ying to distance themselves

from the Euro. This is primari ly due to the differ-

ent growth rates of countries that have adopted

a s ingle currenc y, Euro. I t becomes di f f icult to

maintain the same interest rate throughout a l l

the member countr ies because of the var y ing

growth rates. Hence the inherent instabi l i t y in

the Euro Zone deems the Euro unf i t to replace

the Dol lar as a wor ld reference currenc y.

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

17 18 WORLD ECONOMY WORLD ECONOMY

2.Japanese Yen- The locat ion of Japan in “ The

R i n g o f Fi re” w i l l n e ve r e n s u re t h e s t a b i l i t y

of the Yen as the countr y wi l l be f reque nt ly

h i t by n a t u r a l d i s a s te r s w h i c h i n t u r n wo u l d

a f fe c t t h e s to c k m a r k e t s a s we l l a s t h e c u r-

rency of the concerned countr y as we had seen

subsequent to occurrences of ear thquakes in

Japan. Hence the this inval idates the compe -

t i t ion posed by Yen.

3 . Gold- Though gold is one among the oldest

fo r m s o f m o n e y , t h e co s t i nvo l ve d i n u s i n g

gold in t ransac t ions a long with the integr i t y

o f t h o s e t r a n s a c t i o n s re n d e r s g o l d a c o s t l y

replacement for dol lar as a wor ld currenc y.

The Euro is adopted by top performing economies like Germany & France as well as by faltering economies like Greece & Spain.

M r. S i d d h a r t h K u m a r - A s s i s t a n t V i c e President, Investment Bank ing, Barclays

Capita l

q uest ion: You have had an

e x p e r i e n c e o f w o r k i n g i n

the I ndian Capita l Markets,

especia l ly the debt market ,

fo r a s p a n o f 5 ye a r s . H ow

has your ent i re exper ience

o f wo r k i n g i n t h i s p a r t i c u -

lar market been?

Answer : The Indian Debt Capital Market is quite

a c t i ve. Wh e n I j o i n e d, t h e I n d i a n m a r k e t wa s

not real ly in i ts formative phase; rather, i t had

developed to quite an ex tent . Speak ing of the

n a t u re o f t h e m a r k e t , i t d o e s n o t h ave m u c h

s i m i l a r i t y w i t h t h e m a r k e t s i n t h e d e ve l o p e d

world. So, to an extent, a niche market is devel-

oping in I ndia .

The exper ience, as such, has been ver y enr ich-

ing, given the fac t that the scenar io of a c lass-

room is ver y dif ferent from that of a work place.

I t feels good to be in the middle of ac t ion.

question: Given the current context, do you see

a major t rend developing in this market?

A n s w e r : C o n s i d e r i n g a t i m e f r a m e o f 1 2 - 1 8

months, the trend wil l l ikely be of more domes-

t ic ac t iv i t y in the mar kets . This i s mainly due

to the fac t that there is lack of fa i th of foreign

investors in the Indian capital markets, coupled

with the fac t that capr ic ious pol ic y mak ing by

the government has put barr iers for their entr y.

q u e s t i o n : A re ce n t re p o r t s t a te d t h a t 1 0 . 6 %

o f t h e G D P o f C h i n a i s f u n d e d b y Co r p o r a t e

Bonds, whi le for Japan this stat ist ic goes up to

40%. So, can we conclude that there is a corre -

lat ion bet ween a countr y ’s economic develop -

ment and the evolut ion of i ts debt market? Or

should we say that i t i s just another stat ist ic?

Answer : As the economies develop, the evolu-

t i o n o f c a p i t a l m a r k e t s i s a n at u ra l o u tco m e,

r e g a r d l e s s o f w h e t h e r t h e m a r k e t i s d o m i -

n a t e d b y d e b t i n s t r u m e n t s o r e q u i t y i n s t r u -

m e n t s . S o, o n e c a n s ay t h a t t h e re i s a co r re -

l a t i o n t o t h e e x t e n t t h a t a s e c o n o m i e s g row

and progress , bor rowing and lending tend to

i nc re as e. Howe ve r, on e c an n ot co n cl u de t h at

o n e p a r t i c u l a r p a r a m e t e r w i l l i n f l u e n c e t h e

other parameter.

q u e s t i o n : I s l a m i c b o n d s t o o k o f p r e t t y w e l l

in 2007. S o, ta lk ing of them along with other

S h a r i a t c o m p l i a n t p r o d u c t s , d o t h e y h a v e a

future, i f launched in I ndia?

Answer : Wel l to be honest , speak ing of I s lamic

b o n d s a n d o t h e r S h a r i at co m p l a i nt p ro d u c t s ,

I do not see them having much of a future in

I ndia . The spi r i t and or igin of I s lamic f inance

is f rom countr ies where i t i s regarded a taboo

t o c h a rg e i n te re s t . S o, i n t h i s g i ve n co n te x t ,

consider ing that I ndia is essent ia l ly a democ-

rac y, i t won’t be feas ible for I s lamic bonds to

be launched in I ndia .

H e n c e , w h a t i s e v i d e n t i s t h a t t h o u g h t h e

dol lar is in a danger zone , but with no suitable

replacement to being seen to be around and the

gold standard being brought again to be ver y

unl ikely in the nex t t wo decades, dol lar would

st i l l cont inue to be the exchange currenc y of

the wor ld for at least a couple of decades.

Sanoop Sreedhar-The author is a student of FMS ,Delhi

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

19 20 WORLD ECONOMY CORPORATE TALK

question: Recently the FI I l imit has been raised

by U S D 5 B i l l i o n . A l s o, a n e w s e t o f re fo r m s

are tak ing place. I n this scenar io what reforms

t h a t y o u t h i n k w i l l h e l p i n d e v e l o p i n g t h e

debt market and help the changing c l imate of

capita l in I ndia?

Answer : The government increas ing the l imit

by 5 b i l l i o n f ro m 2 0 b i l l i o n to 2 5 b i l l i o n i s a

reform that i s not going to make a great deal

of change.For instance, the tax on offshore bor-

rowing has been reduced f rom 20% to 5%. But

instruments l ike credit default swaps have not

re a l l y t a k e n o f f. I n a l l , t h e o n e s i m p l e t h i n g

that the government can do is to be more con-

s istent with their pol ic y mak ing. The pol ic ies

should not be such that the gover nment can

claw back money that the investors have made

on their investment.

O ther than that , I ndia is coming up with sov-

ereign bonds could draw more attention to the

countr y. This may enable investors from Europe

and United States to become more open about

enter ing the I ndian market .

question: Given the current economic outlook ,

do you think i t i s ac tual ly correc t for I ndia to

come up with sovereign bonds?

Answer : Wel l , in the coming year or so, i f the

government is able to show some progress with

respec t to pol ic y a long with reforms then they

should come up with that .The RBI has a cap on

how much I ndian companies are permitted in

the form of ECB from offshore markets, mak ing

i t a lmost imposs ible for I ndian companies to

tap capita l f rom the of fshore markets. Hence,

increasing the cap put on the Indian companies

would a lso be benef ic ia l . 1

question: How the various experiences you had

in your 2 years of MBA from I IFT has helped you

in your career?

Answer : Wel l , I IFT is the place where I had my

f i rst exposure to Finance as a domain. I had a

good internship with Adit ya Bir la Group, so my

i nte re s t i n f i n a n ce s t a r te d f ro m t h e re. I n t h e

2nd year, we had some ver y good professors ,

who helped in nur tur ing my interest in f inance.

Also, the batch that I was a par t of had a set of

co m m o n i nte re s t s , w h i c h we s h a re d amongst

ourselves. Hence, the two years of MBA gave me

a hol ist ic development f rom al l aspec ts.

q u e s t i o n : W h a t a c c o rd i n g t o yo u s h o u l d t h e

col lege do to engage more a lumnis?

Answer : The col lege should look to being more

proac t ive in reaching out to the a lumni , bas i -

c a l l y h av i n g a n ‘ i n yo u r f a ce a p p ro a c h’. I fe e l

t h at e ve r y a l u m n u s o f t h e co l l e g e d o e s h ave

some feeling of aff i l iation to his alma mater and

wa nt s to co nt r i b u te to t h e co l l e g e. H owe ve r,

due to var ious reasons, they are not able to do

so. The basic fac t is that you have to be in their

face. They may ignore you, but they won’t turn

you down.

M r. S i d d h a r t h K u m a r i s t h e A s s i s t a n t V i c e Pre s ide nt of the I nves tment Bank ing d iv is ion at t B a rc l ays Ca p i t a l . Pr i o r to j o i n i n g B a rc l ays Capital, he worked as the manager of the global invetment banking division at ICICI bank. He has a total exper ience of more than 5 years in the bank ing and f inance industr y. His area of inter-est inc ludes Struc tured Finance, D ebt Capita l M arkets, Syndicated Loans, S ecur i t izat ionThe views expressed above are of the author and in no way reflect the opinion of the firm

D o e s t h i s h o l d t r u e i n

t o d a y ’s s c e n a r i o ? C a n

this be sa id for the coun-

tr ies i r respec t ive of their

e c o n o m i c s t r u c t u r e ?

I n f l a t i o n r e p r e s e n t s a n

i n c re a s e i n t h e p r i c e l e ve l o f t h e g o o d s a n d

ser v ices in the economy as a whole. I nf lat ion

rate refers to a general r i se in pr ices measured

against a standard level of purchasing power.

T h e m o s t w e l l k n o w n m e a s u r e s o f I n f l a t i o n

are the CPI which measures consumer pr ices ,

a n d t h e G D P d e f l a t o r, w h i c h m e a s u re s i n f l a -

t i o n i n t h e w h o l e o f t h e d o m e s t i c e c o n o my.

India faced a high of 14.97% (CPI) inflation rate in

FY09; RBI was par tial ly able to control the inf la -

t ion rate and has brought i t down to 6 .87% in

July ’12. China raised interest rates for the fourth

t ime s ince the end of the global f inancial cr is is

to restra in inf lat ion and l imit the r isk of asset

bubbles in the fastest-growing major economy.

I n f l a t i o n a f fe c t s t h e d i f fe re n t s e c t o r s o f t h e

economy and i f kept unchecked can shake the

e c o n o m i c s t a b i l i t y o f a n a t i o n . Fo r i n s t a n c e,

Zimbabwe’s hyper- Inf lat ion of 24,000% in 2009

was par t ia l ly a result of the monetar y author-

i t y i r re s p o n s i b l y b o r row i n g m o n e y to p ay a l l

i ts expenses and funding quasi - f iscal ac t iv i t ies

(which are normally left to Central Government).

I s Monetar y Pol ic y the best answer we have for I nf lat ion?

“I nf lat ion is a lways and ever y where a monetar y phenomenon.”-M i l ton Fr iedman

F e w o f t h e p r o m i n e n t

e f f e c t s o f i n f l a t i o n c a n

b e j o t t e d d o w n a s u n d e r

1.Buying power of the cur-

renc y is eroded

2.Real wage rate decreases

3.Real rate of return for debt holders decreases

4. I nstead of saving, consumers may star t bor-

row i n g. Co n s u m e r s te n d to b o r row m o re a n d

spend even more.

5 . I nf lat ion causes uncer ta int y which increases

r isk . Higher r isk means businesses are less l ikely

to invest .

6 . B u s i n e s s c o s t s r i s e s a s i n p u t p r i c e s ( r a w

m a t e r i a l s , w a g e s a n d s u p p l i e s ) r i s e . Wa g e s

are of ten the largest business cost , and there

could be a danger of a ‘wage -price’ spiral where

r i s i n g c o s t s l e a d s t o h i g h e r p r i c e s , w o r k e r s

a s k fo r a p a y r i s e i n c o m p e n s a t i o n , s o c o s t s

r i s e a g a i n , s o p r i c e s r i s e a g a i n , a n d s o o n .

To get to the crux of i t , we need to understand

the bas ics of inf lat ion and fac tors giv ing r i se

to i t . There is no s ingle cause which is agreed

u p o n by a l l , b u t t h e re a re a t l e a s t t wo t h e o -

r ies which are general ly accepted: Demand-Pull

I nf lat ion Theor y & Cost-Push I nf lat ion Theor y

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

21 22 CORPORATE TALK INDIAN ECONOMY

Th e s e c a n b e e x p l a i n e d i n te r m s o f i n te r s e c-

t ion of shor t run aggregate supply (SRAS) and

a g g r e g a t e d e m a n d c u r v e s a s s h o w n i n t h e

f i g u re . I n a s h o r t t i m e s p a n Lo n g r u n a g g re -

g a t e s u p p l y ( L R A S ) c u r v e i s a s s u m e d c o n -

s t a n t a n d i s t h e l e ve l o f G D P a t e q u i l i b r i u m .

D e m a n d P u l l : W h e n S R A S b e c o m e s i n e l a s -

t ic and there is fu l l employment of resources,

a n i n c r e a s e i n d e m a n d l e a d s t o i n c r e a s e o f

pr ices. This increase in demand may be due to:-

1 .A reduc t ion in di rec t or indirec t taxat ion

2.The rapid growth of the money supply

3 .A depreciat ion of the exchange rate

T h i s e f f e c t i s e x p l a i n e d i n t h e d i a g r a m .

H e r e i n c r e a s e i n d e m a n d h a s c a u s e d

p r i c e s o f g o o d s i n e c o n o m y t o i n c r e a s e .

C o s t P u s h I n f l a t i o n : O n t h e o t h e r h a n d ,

C o s t - P u s h I n f l a t i o n o c c u r s w h e n t h e p r i c e s

i n c r e a s e d u e t o r i s i n g p r o d u c t i o n c o s t s ,

i n o r d e r t o m a i n t a i n t h e i r p r o f i t m a r g i n s .

I n c r e a s e i n c o s t m a y h a p p e n d u e t o :

1 .R is ing impor ted raw mater ia ls costs

2 .R is ing labour costs

3 . H i g h e r i n d i r e c t t a x e s i m p o s e d b y t h e

government

Co s t - p u s h i n f l a t i o n c a n b e i l l u s t r a t e d b y a n

inward shi f t of the shor t run aggregate supply

curve. This is shown in the diagram below. A fall in

SRAS causes a contraction of real national output

together with a r ise in the general level of prices.

Fo r ye a r s n ow, t h e m o s t co m m o n

t o o l w h i c h c e n t r a l b a n k e r s h a v e

in their hand to control the inf la-

t ion is temper ing with the money

s u p p l y. I d e a b e h i n d i t b e i n g t h at

money supply controls the growth

o f d e m a n d t h r o u g h a n i n c r e a s e

i n i n t e r e s t r a t e s a n d a c o n t r a c -

t i o n i n t h e r e a l m o n e y s u p p l y.

Few of the measures adopted are : -

Bank rate pol ic y : Dur ing inf lat ion i t i s seen as

a ver y crucia l instrument of monetar y control .

The increase in bank rate increases the cost of

INDIAN ECONOMY

b o r row i n g w h i c h re d u c e s c o m m e rc i a l b a n k s’

b o r ro w i n g f ro m t h e c e n t r a l b a n k . T h i s l e a d s

in reduc t ion of cash f low from the commercia l

banks to the public. Thus, inflation is controlled

t o a n e x t e n t i t ’s c a u s e d b y t h e b a n k c r e d i t .

Ca s h R e s e r ve R at i o (C R R ) : B y ra i s i n g t h e C R R

central bank tr ies to reduce the lending capac-

i t y of the commerc ia l banks, so as to contro l

i n f l a t i o n . T h i s l e a d s i n r e d u c t i o n o f c a s h

f l o w f ro m c o m m e rc i a l b a n k s t o p u b l i c . T h i s ,

c o n t r o l l i n g t h e r i s e i n p r i c e s t o t h e e x t e n t

i t i s c a u s e d b y b a n k s c r e d i t s t o t h e p u b l i c .

O p e n M a r k e t O p e rat i o n s : O p e n m a r k e t o p e r -

a t i o n s re fe r to s a l e a n d p u rc h a s e o f g ove r n -

m e n t s e c u r i t i e s a n d b o n d s b y t h e c e n t r a l

bank . Centra l bank sel ls the government secu-

r i t i e s to t h e p u b l i c t h ro u g h t h e b a n k s re s u l -

t i n i n t r a n s fe r o f a p a r t o f b a n k d e p o s i t s t o

centra l bank account and reduces credi t c re -

a t i o n c a p a c i t y o f t h e c o m m e r c i a l b a n k s .

But are such monetar y pol ic ies the only source

of inf lat ion control? Or are they enough con-

s ider ing the current wor ld scenar io where a l l

e co n o m i e s a re m u c h m o re co m p l i c a te d t h a n

ever before? Effect ive pol ic ies to control inf la-

t i o n n e e d to fo c u s o n t h e u n d e r l y i n g c a u s e s

of inf lat ion in the economy. I f cost-push inf la-

t ion is the root cause, produc t ion costs need

to be control led for the problem to be reduced.

To ser ve this purpose var ious methods can be

a d o p te d fo r s h o r t te r m o r l o n g te r m e f fe c t s .

S h o r t - t e r m p o l i c i e s . A n a p p r e c i a t i o n o f t h e

exchange rate

There are several impac ts at enterpr ise level of

appreciation of the domestic exchange rates. I t

should make expor ts more expensive and thus

reduce the volume of expor ts. As a result f i rms

f ind them in a posit ion where they have to keep

thei r cost down to remain compet i t ive in the

world market. Also a stronger currenc y reduces

impor t pr ices and this makes f i rms’ raw mater i -

als and components cheaper, therefore helping

them control costs.

T h e r e a r e s e v e r a l m e c h a n i s m s fo r e xc h a n g e

r a t e a p p r e c i a t i o n w h i c h c a n b e e m p l o y e d .

S o m e o f t h e m a re : i n c re a s e i n t h e re a l i nte r -

e s t o f t h e e c o n o m y ; o p e n m a r k e t o p e r -

a t i o n s b y c e n t r a l b a n k i n f o r e x m a r k e t s .

Direc t wage controls - incomes pol ic ies

A d i r e c t w a g e c o n t r o l l i m i t s t h e r a t e o f

g r o w t h o f n o m i n a l w a g e s a n d t h u s h a s t h e

p o t e n t i a l t o r e d u c e c o s t i n f l a t i o n . T h o u g h

n o t b e i n g u s e d f r e q u e n t l y i n c u r r e n t t i m e s ,

t h i s p o l i c y s t i l l t r y t o l i m i t w a g e g r o w t h b y

r e s t r i c t i n g p a y r i s e s i n t h e p u b l i c s e c t o r.

Long-term pol ic ies.

Fiscal Pol ic y

1.H igher di rec t taxes (causing a fa l l in dispos-

able income)

2. Lower Government spending

3 . A reduc t ion in the amount the government

sec tor borrows each year

T h e s e f i s c a l p o l i c i e s l i m i t t h e c i r c u l a r f l o w

o f m o n e y a n d r e d u c e f u r t h e r i n j e c t i o n s

i n t o t h e f l o w o f i n c o m e . T h i s i s a i m e d t o

r e d u c e d e m a n d p u l l i n f l a t i o n a n d a t t h e

c o s t o f s l o w e r g r o w t h a n d u n e m p l o y m e n t .

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

23 24 INDIAN ECONOMY

INDIAN ECONOMY

Labour market reforms

Over a period of t ime depletion of power vested

i n t ra d e u n i o n s, t h e grow t h o f p a r t - t i m e a n d

temporar y wor k ing a long with the expansion

o f f l e x i b l e w o r k i n g h o u r s h a v e r e s u l t e d i n

increased f lex ibi l i t y in the labour market . This

a l l ows f i r m s to co n t ro l t h e i r l a b o u r co s t a n d

t h u s re d u c e c o s t p u s h i n f l a t i o n a r y p re s s u re .

I n re ce n t ye a r s t h e U K a n d G e r m a n e co n o my

h a s n o t s e e n t h e a c c e l e r a t i o n i n w a g e i n f l a -

t ion normal ly associated with several years of

s u s t a i n e d e co n o m i c grow t h a n d f a l l i n g i n f l a -

t ion. This can be attr ibuted to shif t ing of power

a w a y f r o m e m p l o y e e s t o w a r d s e m p l o y e r s .

Supply-s ide reforms

To a c h i e v e s u s t a i n e d e c o n o m i c g r o w t h

without worr y ing for inf lat ion, greater output

i s r e q u i r e d t o b e p r o d u c e d a t a l o w e r c o s t

p e r u n i t . A l o n g te r m s u s t a i n a b l e i n c re a s e i n

a g g re g a t e s u p p l y ( p o t e n t i a l G D P ) i s t h e k e y

o b j e c t i ve o f a g o ve r n m e n t e c o n o m i c p o l i c y.

A c l a s s i c e x a m p l e i s o f Tu r k e y ’s c e n t r a l

b a n k r e d u c i n g i n t e r e s t r a t e s t o s h i e l d t h e

e c o n o m y f r o m t h e i m p a c t o f t h e E u r o p e a n

d e b t c r i s i s a n d s l o w i n g g r o w t h i n t h e U. S .

Supply side reforms aim to enhance the produc-

tivity of the economy over a long run and increase

the t rend rate of growth of fac tor of produc-

t ions i .e. labour and total factor productivity. A

number of supply-side policies have been intro-

duced into the Brit ish economy in recent years. .

C l e a r l y i t c a n b e s e e n t h a t i n f l a t i o n c u r b i n g

t o d a y n e e d s m u c h m o re t h a n j u s t m o n e t a r y

p o l i c i e s a n d t h e k e y t o c o n t ro l l i n g i n f l a t i o n

i n t h e l o n g r u n i s fo r t h e a u t h o r i t i e s to k e e p

control of aggregate demand (through fiscal and

monetar y pol ic y) and at the same t ime seek to

achieve improvements to the supply s ide of the

economy. The credibil ity of inflation control pol-

ic ies can a lso be enhanced by the introduc t ion

of inf lat ion targets which should be met with .

H imanshu Kundoo and Palnik a Hemnani-The authors are

students of I IFT

BANKING

Impact of BASEL I I I norms on Indian Banking Sec tor

“ W hatever was on the

le f t -hand s ide ( l iabi l i t ies )

w a s n o t r i g h t a n d w h a t -

ever was on the r ight-hand

s ide (assets) was not lef t ”-

T h i s q u o t e c h a r a c t e r i z e d

the world’s bank ing system during ear ly 2008

and ushered in the global f inancial cr is is that

sent tremors across economies the world over.

This was in spite of the protective safeguards

of the BASEL I I norms and has led the Basel

Committee on Bank ing Super vis ion (BCBS) to

co m e o u t w i t h t h e B A S E L I I I n o r m s p rov i d -

ing a broadened f ramework of t ighter regu-

lat ions a imed at st rengthening both s ides of

the balance sheet for banks around the world.

The Basel I I I guidel ines envisage increase in

capital and l iquidity requirements worldwide.

I n e a r l y M a y 2 0 1 2 , R B I a n n o u n c e d n e w

n o r m s f o r t h e I n d i a n b a n k i n g s e c t o r w i t h

s t r i c t e r r e g u l a t i o n s t h a n t h e B A S E L I I I t o

be ef fec ted in a phased manner with in f ive

f i s c a l y e a r s s t a r t i n g f r o m J a n u a r y, 2 0 1 3 .

L e t u s l o o k a t t h e s e n o r m s a n d t h e i r

p r o b a b l e i m p a c t o n t h e I n d i a n B a n k s .

The rules can be broadly classif ied as bellow :-

• T h e c a p i t a l r e q u i r e m e n t s f o r t h e i m p l e -

m e n t a t i o n o f B a s e l I I I g u i d e l i n e s m a y

b e l o w e r d u r i n g t h e i n i t i a l p e r i o d s

a n d h i g h e r d u r i n g t h e l a t e r y e a r s .

• T h e g u i d e l i n e s r e q u i r e

b a n k s t o m a i n t a i n a

minimum tota l capi ta l o f

9 p e r c e n t a g a i n s t 8 p e r

c e n t p r e s c r i b e d b y t h e

B a s e l c o m m i t t e e o f t o t a l

r i s k w e i g h t e d a s s e t s .

•Common Equity Tier 1 (CET1) capital must be at

least 5.5 per cent of RWA’s. (Risk Weighted Assets)

U n d e r t h e s e n o r m s b a n k s w i l l h ave t o m a i n -

t a i n t h e i r t o t a l c a p i t a l r a t i o a t 9 % , h i g h e r

t h a n t h e m i n i m u m r e c o m m e n d e d r e q u i r e -

m e n t o f 8 % u n d e r t h e B a s e l I I I n o r m s . T h e

n o r m s a l s o r e q u i r e b a n k s t o m a i n t a i n T i e r

I c a p i t a l a t 7 % o f r i s k w e i g h t e d a s s e t s .

F o l l o w i n g i s t h e s u m m a r y o f t h e r u l e s

p e r t a i n i n g t o t h e I n d i a n s c e n a r i o : -

2 0 1 3 M i n i m u m c a p i t a l r e q u i r e m e n t s :

S t a r t o f t h e g r a d u a l p h a s i n g - i n o f t h e

h i g h e r m i n i m u m c a p i t a l r e q u i r e m e n t s .

2 0 1 5 M i n i m u m c a p i t a l r e q u i r e m e n t s :

H i g h e r m i n i m u m c a p i t a l r e q u i r e -

m e n t s t o b e f u l l y i m p l e m e n t e d .

2 0 1 6 C o n s e r v a t i o n b u f f e r : I n i t i a t i o n o f t h e

gradual phasing- in of the conser vat ion buffer.

2 0 1 9 Cy c l i c a l C o n s e r v a t i o n b u f fe r : T h e c o n -

s e r v a t i o n b u f f e r t o b e f u l l y i m p l e m e n t e d .

2 0 1 1 S u p e r v i s o r y m o n i t o r i n g : D e v e l o p i n g

I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2 I n F I N e e t i A n n u a l I s s u e | S e p t e m b e r 2 0 1 2

25 26

t e m p l a t e s t o t r a c k t h e l e v e r a g e r a t i o

a n d t h e u n d e r l y i n g c o m p o n e n t s .

2 0 1 3 Pa r a l l e l r u n I : T h e l e v e r a g e r a t i o a n d

i t s co m p o n e n t s to b e t ra c k e d by s u p e r v i s o r s

w h i c h a r e n e i t h e r d i s c l o s e d n o r m a n d a t o r y.

2 0 1 5 P a r a l l e l r u n I I : T h e l e v e r a g e r a t i o

a n d i t s c o m p o n e n t s t o b e t r a c k e d w h i c h

a r e n e i t h e r d i s c l o s e d n o r m a n d a t o r y .

2 0 1 7 Fi n a l a d j u s t m e nt s : B a s e d o n t h e re s u l t s

o f t h e p a r a l l e l r u n p e r i o d , a ny f i n a l a d j u s t -

m e n t s t o t h e l e v e r a g e r a t i o t o b e m a d e .

2018 Mandatory requirement: The leverage ratio to

become a mandatory part of Basel III requirements.

The I ndian regulator has been more str ingent .

For I ndian banks, common equit y should be at

least 5.5% of the asset base, whereas the interna-

tional norm suggests 4.5%.Tier I capital, or core

capital, includes a bank ’s equity capital and dis-

c losed reser ves. Capital rat io is the percentage

of a bank ’s capita l to i ts r i sk-weighted assets.