Digital forensics track schroader-rob when forensics collide

IIA Chicago Chapter 53rd Annual SeminarApril 15, 2013, Donald E. Stephens Convention Center

@IIAChicago

#IIACHI

A Look Ahead: Supply Chain Forensics

Combine Data Mining and Forensic Accounting to Combat Financial & Fraud Risks within Supply Chains

Mark PearsonSenior Manager, Deloitte ForensicsDeloitte Financial Advisory Services

Clarke WarrenDirector Forensic InvestigationsJohnson Controls

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 2

Agenda – Supply Chain Forensics

I. The Issue

II. Common Supply Chain Risks and Typical Overspend

III. Use Supply Chain Forensics to Save Money and Reduce Risk

IV. Data Mining Component

V. Forensic Accounting Component

VI. Conclusion

The Issue

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 4

The Issue

Persistent pressure upon companies to do more with less - Management must produce

increasing profits and return on assets.

To achieve results, organizations increasingly rely upon

business partnerships, which have become

progressively more complex.

The complexity of this reliance can mask

a myriad of financial, regulatory and legal

risks.

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 5

News Headlines

China e-commerce giant Alibaba announced the departure of two executives

after probe showed 2,326 suppliers defrauded online customers.

22 February 2011 Caixin Online, accessed October 12, 2011.

Navy Setting up Contract Fraud Investigation Unit

Alibaba Executives Resign

on Supplier Fraud Scandal

Common Supply Chain Fraud Risks & Typical Overspend

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 7

Common Supply Chain Risks

Lost Revenues

Underreporting of revenue tied to royalties

Missed Cost Savings

Vendor overcharges

Damaged Business Relationship

Over time, a small difference in interpretation can have large impact

Litigation

Reactive alternative that can be very costly and damaging to reputation

Regulatory Inquiries

Supply Chain details may impact financial reporting

Reputational Risks

Transacting business with unsavory entities or people

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 8

Typical Overspend – High Risk Spend Categories

Labor

Overtime rate versus straight-time rate

Labor charged for people not on payroll (ghost employees)

Rates charged are higher than contractually agreed rates

Allocated or Shared Expenses

Facility overhead allocation (or any other allocated expenses)

Shared advertising or marketing costs

Cost Plus Transactions

Vendor is incentivized to go with highest cost provider

Third Party Passthrough's

3rd party pass-through expenses may in fact be for related-party

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 9

Case Study – Supply Chain Fraud: Excerpt from vendor invoice #1095

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 10

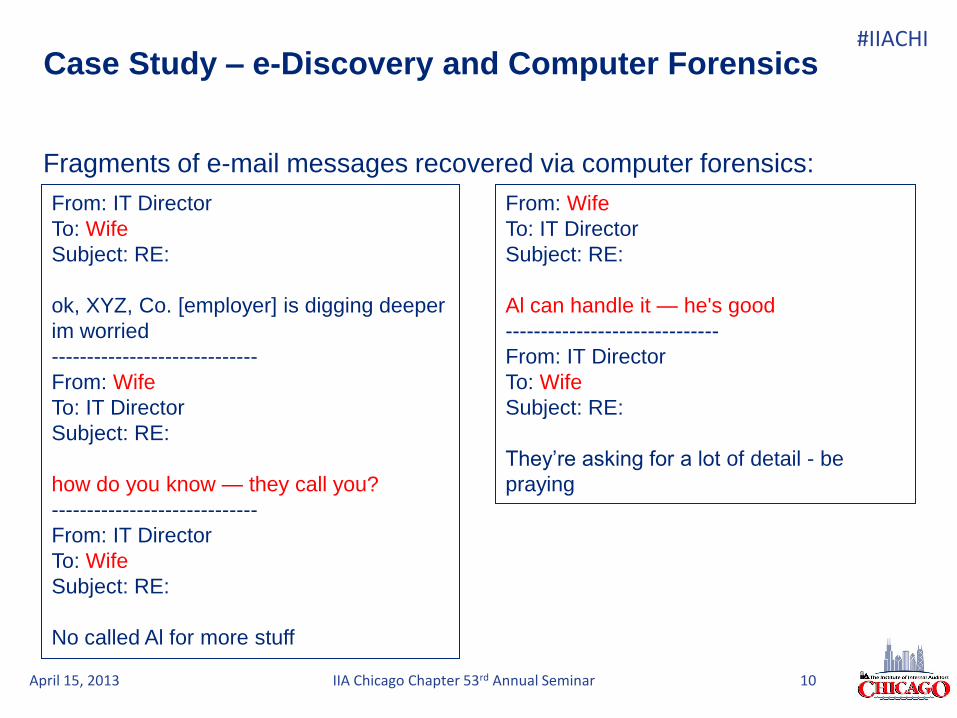

Fragments of e-mail messages recovered via computer forensics:

Case Study – e-Discovery and Computer Forensics

From: IT Director

To: Wife

Subject: RE:

ok, XYZ, Co. [employer] is digging deeper

im worried

-----------------------------

From: Wife

To: IT Director

Subject: RE:

how do you know — they call you?

-----------------------------

From: IT Director

To: Wife

Subject: RE:

No called Al for more stuff

From: Wife

To: IT Director

Subject: RE:

Al can handle it — he's good

------------------------------

From: IT Director

To: Wife

Subject: RE:

They‘re asking for a lot of detail - be

praying

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 11

Photo of recovered document detailing the 3-way split of the payment of

invoice #1095

Case Study – ―Smoking gun‖ document recovered

1

32

1 — IT Director2 — Bank Computer Leasing Mgr.3 — Crooked Vendor

1

2

13

3

Use Supply Chain Forensics to Save Money and Reduce Risk

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 13

Supply Chain Forensics Goals

• Identify fraud risks &

areas to recover

potential

overpayments or

underpayments

• Identify procedural

inconsistencies that

could help the

company strengthen

processes

• Revise agreements

by identifying and

eliminating

accounting loopholes

• Identify payments

that company is not

obligated to make

• Include the ‗right to

audit‘ in future

agreements

• Perform due

diligence on vendor

track record

• Identify relationships

between vendors and

possible related

entities

Identify &

RecoverOverpayments

Negotiate Terms of Future

Agreements

ControlSupply Chain Performance Criteria and Evaluation

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 14

Supply Chain Forensics Process

Due Diligence

& Risk AnalysisData

Mining

Forensic

Accounting

Control &

Remediation

Step 1 Step 2 Step 3 Step 4

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 15

Due Diligence – Visual Relationship Mapping

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 16

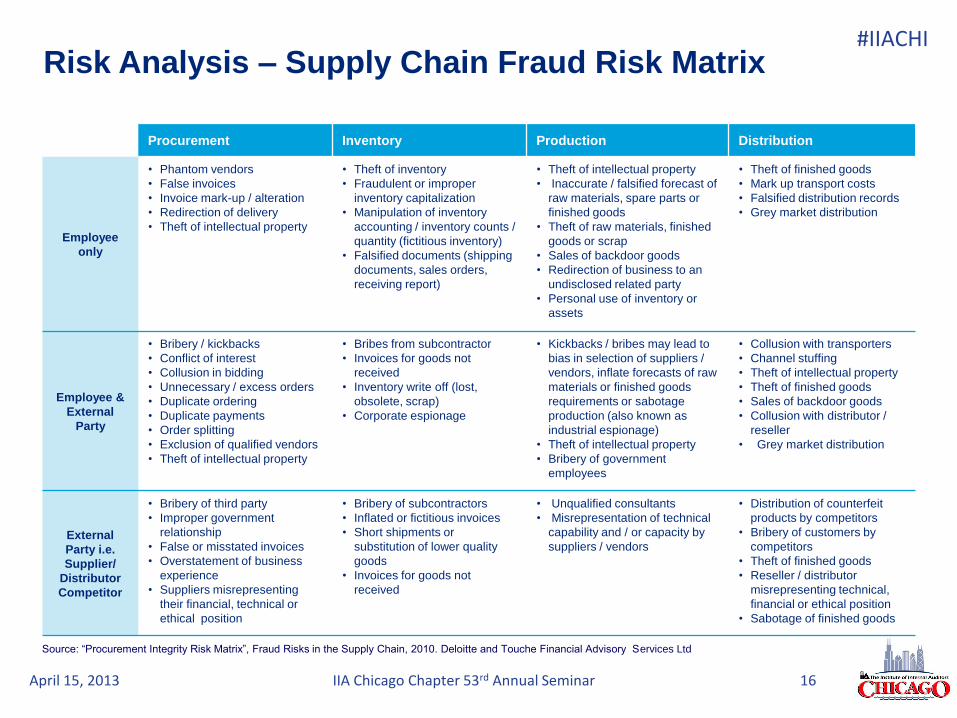

Risk Analysis – Supply Chain Fraud Risk Matrix

Source: ―Procurement Integrity Risk Matrix‖, Fraud Risks in the Supply Chain, 2010. Deloitte and Touche Financial Advisory Services Ltd

Procurement Inventory Production Distribution

Employee

only

• Phantom vendors

• False invoices

• Invoice mark-up / alteration

• Redirection of delivery

• Theft of intellectual property

• Theft of inventory

• Fraudulent or improper

inventory capitalization

• Manipulation of inventory

accounting / inventory counts /

quantity (fictitious inventory)

• Falsified documents (shipping

documents, sales orders,

receiving report)

• Theft of intellectual property

• Inaccurate / falsified forecast of

raw materials, spare parts or

finished goods

• Theft of raw materials, finished

goods or scrap

• Sales of backdoor goods

• Redirection of business to an

undisclosed related party

• Personal use of inventory or

assets

• Theft of finished goods

• Mark up transport costs

• Falsified distribution records

• Grey market distribution

Employee &

External

Party

• Bribery / kickbacks

• Conflict of interest

• Collusion in bidding

• Unnecessary / excess orders

• Duplicate ordering

• Duplicate payments

• Order splitting

• Exclusion of qualified vendors

• Theft of intellectual property

• Bribes from subcontractor

• Invoices for goods not

received

• Inventory write off (lost,

obsolete, scrap)

• Corporate espionage

• Kickbacks / bribes may lead to

bias in selection of suppliers /

vendors, inflate forecasts of raw

materials or finished goods

requirements or sabotage

production (also known as

industrial espionage)

• Theft of intellectual property

• Bribery of government

employees

• Collusion with transporters

• Channel stuffing

• Theft of intellectual property

• Theft of finished goods

• Sales of backdoor goods

• Collusion with distributor /

reseller

• Grey market distribution

External

Party i.e.

Supplier/

Distributor

Competitor

• Bribery of third party

• Improper government

relationship

• False or misstated invoices

• Overstatement of business

experience

• Suppliers misrepresenting

their financial, technical or

ethical position

• Bribery of subcontractors

• Inflated or fictitious invoices

• Short shipments or

substitution of lower quality

goods

• Invoices for goods not

received

• Unqualified consultants

• Misrepresentation of technical

capability and / or capacity by

suppliers / vendors

• Distribution of counterfeit

products by competitors

• Bribery of customers by

competitors

• Theft of finished goods

• Reseller / distributor

misrepresenting technical,

financial or ethical position

• Sabotage of finished goods

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 17

Summary of checks paid for false purchase orders

Case Study – Processing through shared services

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 18

Case Study – Processing through shared services

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 19

Case Study – Processing through shared services

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 20

Case Study – Processing through shared services

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 21

Case Study – Bypassing vendor add process

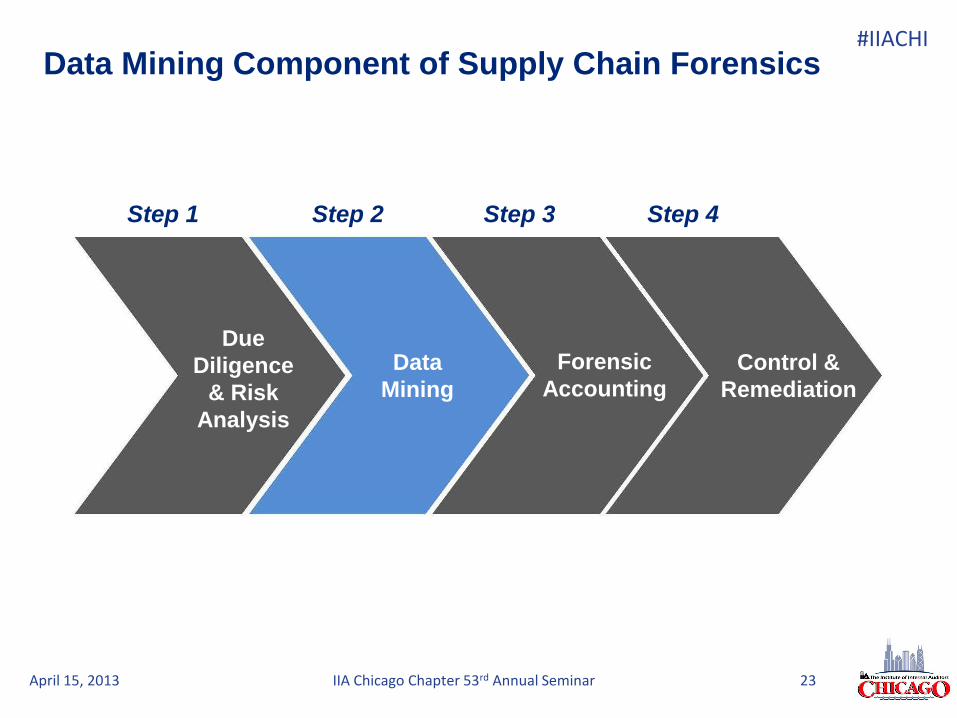

Data Mining Component of Supply Chain Forensics

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 23

Due

Diligence

& Risk

Analysis

Data

Mining

Forensic

AccountingControl &

Remediation

Step 1 Step 2 Step 3 Step 4

Data Mining Component of Supply Chain Forensics

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 24

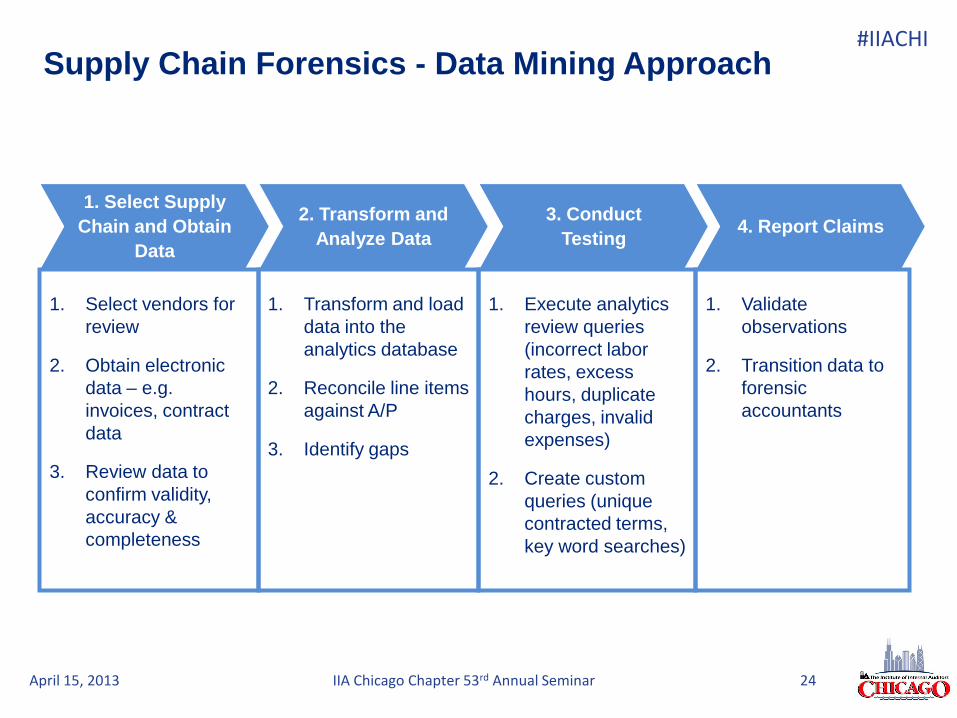

Supply Chain Forensics - Data Mining Approach

1. Select Supply

Chain and Obtain

Data

2. Transform and

Analyze Data

3. Conduct

Testing4. Report Claims

1. Select vendors for

review

2. Obtain electronic

data – e.g.

invoices, contract

data

3. Review data to

confirm validity,

accuracy &

completeness

1. Transform and load

data into the

analytics database

2. Reconcile line items

against A/P

3. Identify gaps

1. Execute analytics

review queries

(incorrect labor

rates, excess

hours, duplicate

charges, invalid

expenses)

2. Create custom

queries (unique

contracted terms,

key word searches)

1. Validate

observations

2. Transition data to

forensic

accountants

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 25

Supply Chain Forensics - Typical Data Required

1. Select Supply Chain

and Obtain Data

2. Transform and

Analyze Data3. Conduct Testing 4. Report Claims

Common to All Invoices

Labor Invoice Detail

Equipment/Consumables Invoice Detail

Worker Expense Detail

Personnel File

Payroll Records

Agreements

Financial

Additional Information

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 26

Common Database Library

CDL

Transform and Analyze Data

Agreements

• Rates and

Terms

Invoice

Support

•Line item

details

Ancillary

• Personnel

and Assets

Financial

• AP, Invoices

and Credits

Conduct Testing - Execute Queries (canned and custom)

Report Claims

Data

Flo

w

Reconcile

Normalize

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 27

Labor

• Duplicate labor charges

• Incorrect labor rate charges

• Position changes

• Excess overtime charged

• Reasonable hours charged

• Ghost Employees charged

• Labor charged after termination or before hire

• Incorrect Consultant charges

Equipment

• Incorrect equipment rate charges

• Duplicate equipment charges

• Equipment invoiced versus

Fixed Asset Register

Conduct Testing - Types of Analytical Queries

Invoice

• Duplicate invoices

• Duplicate 3rd party invoices

Consumables

• Duplicate material charges

• Incorrect material rate charges

Labor Expenses

• Duplicate out of pocket expense

• Invalid Per Diem charges

Subcontractor

• Duplicate subcontractor charges

• Incorrect mark up

Common data mining analytical queries are listed below:

1. Select Supply Chain

and Obtain Data

2. Transform and

Analyze Data3. Conduct Testing 4. Report Claims

Forensic Accounting Component of Supply Chain Forensics

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 29

Supply Chain Forensic Accounting Component

Due

Diligence

& Risk

Analysis

Data

Mining &

Analytics

Forensic

AccountingControl &

Remediation

Step 1 Step 2 Step 3 Step 4

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 30

Step 1

• Vendor Interviews

Step 2

• Define Population & Determine Sample

Step 3

• Forensic Accounting Procedures

Step 4

• Vet findings with Vendor

Step 5

• Extrapolate Sample Results

Forensic Accounting Approach

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 31

Supply Chain Forensics – Forensic Accounting Approach

1. Forensic

Interviews & Risk

Analysis

2. Choose

Transactions to

Test

3. Conduct

Testing4. Report Claims

1. Select vendors for

review

2. Obtain background

information on

vendor

3. Interview vendor

personnel to

broaden

intelligence about

processes &

transactions

4. Develop risk-

ranking of

transaction types &

characteristics

1. Combine

transaction risk-

ranking with all

available

information to

create populations

2. Provide input to

forensic data

mining query

structure

3. Determine sample

of transactions for

testing

1. Vet query results to

supporting

documentation

(fixed asset

registers, payroll

reports, etc.)

2. Ensure transactions

show:

1. Authorization

2. Existence

3. Approval

3. Manually test non-

queriable

transactions (sub-

contractor rates tie

to agreement?)

1. Validate

observations with

vendor

2. Bifurcate findings

into those that

have a chance of

recovery, and

those that are

process-oriented.

3. Work with legal

counsel and

vendor to reach

mutually

agreeable

settlement of

findings.

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 32

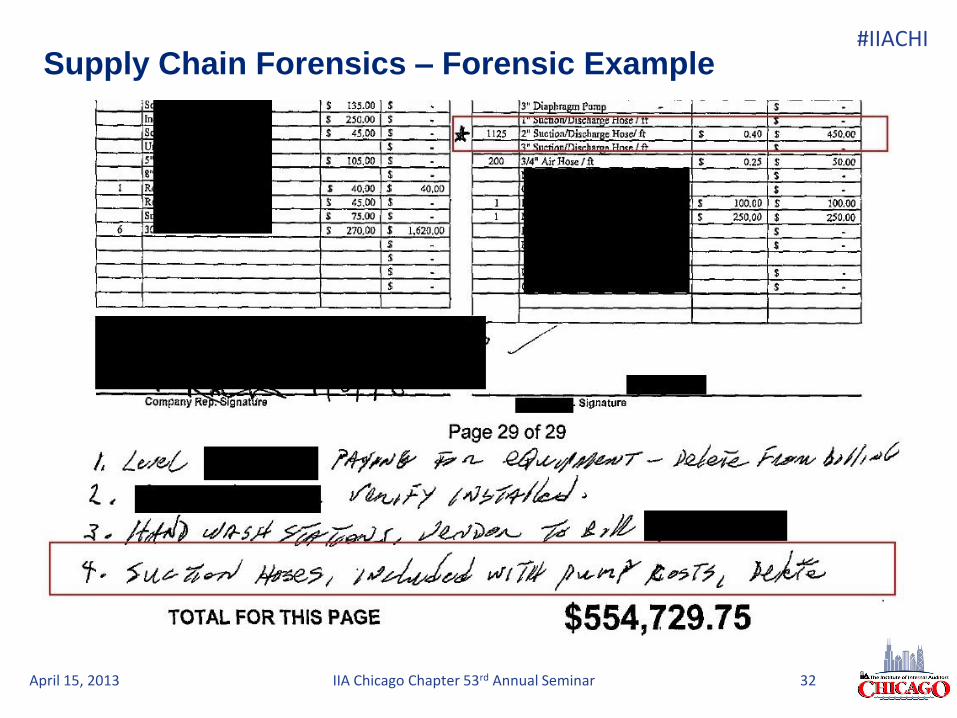

Supply Chain Forensics – Forensic Example

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 33

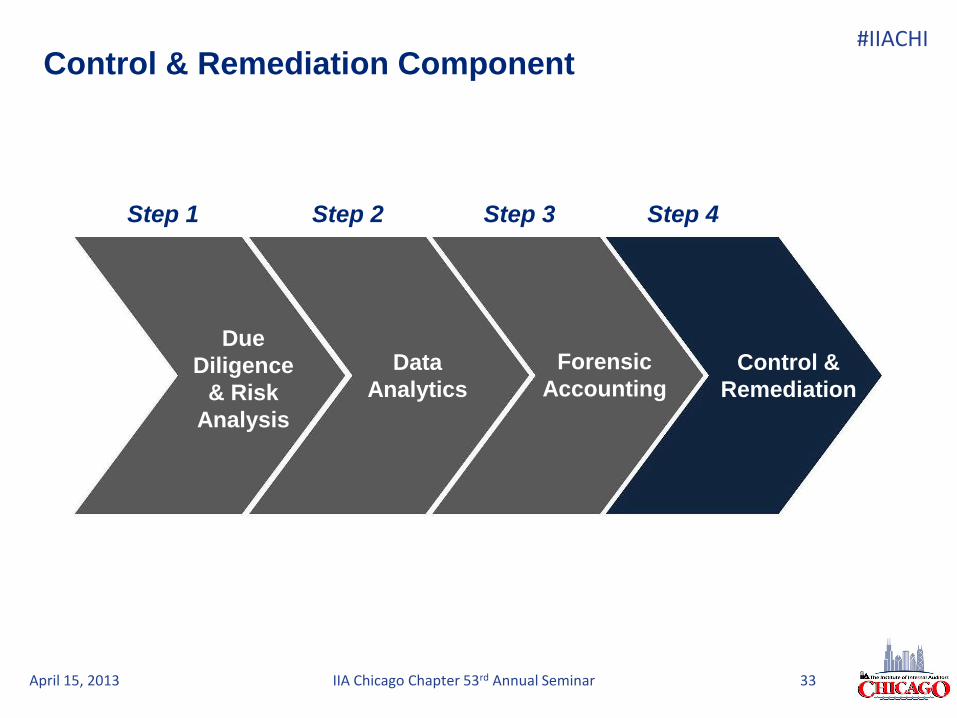

Control & Remediation Component

Due

Diligence

& Risk

Analysis

Data

Analytics

Forensic

AccountingControl &

Remediation

Step 1 Step 2 Step 3 Step 4

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 34

Most Supply Chain Forensic examinations can be dealt with in a mutually

agreeable manner.

However, litigation & dispute resolution can help in cases where

commercial settlement becomes necessary.

Litigation & Dispute resolution helps counsel with

challenging financial and economic issues in

complex litigation and other business disputes

relating to supply chain fraud.

Utilize tools, methodologies and technology that

include data mining and mapping, electronic discovery

and computer forensic capabilities.

Supply Chain Litigation & Dispute Resolution

#IIACHI

April 15, 2013 IIA Chicago Chapter 53rd Annual Seminar 35

More efficient,

Supply Chains,

additional profits &

reduced risk

Conclusion - Supply Chain Forensics

Data Mining

Due Diligence & Risk

Analysis

Remediation

Forensic Accounting

What do you think?Share your thoughts about this presentation on Twitter using the hashtag #IIACHI

@IIAChicago

Visit our Social Media booth in the Exhibit Hall to join the conversation today!

Not on Twitter?

Follow us on Twitter