IHS Screen Digest Insight Report Ultra High Definition ... · Authors Tom Morrod, Senior Principal...

26

Authors Tom Morrod, Senior Principal Analyst, TV and Broadcast Technology, IHS Screen Digest Ed Border, Senior Analyst, TV Technology, IHS Screen Digest IHS Screen Digest Insight Report Ultra High Definition: The next generation of high resolution content

Transcript of IHS Screen Digest Insight Report Ultra High Definition ... · Authors Tom Morrod, Senior Principal...

AuthorsTom Morrod, Senior Principal Analyst, TV and Broadcast Technology, IHS Screen Digest

Ed Border, Senior Analyst, TV Technology, IHS Screen Digest

IHS Screen Digest Insight Report

Ultra High Definition: The next generationof high resolution content

August 2013 ihs.com

IHS Electronics & Media Insight Report

TV Technology and TV SystemsIntelligence Services

Territories covered in this reportAsia Pacific, China, Eastern Europe, Japan, Latin America, Middle East and Africa, North America, Western Europe

[email protected]+44 (0) 203 159 3300

Company SymbolAUO NYSE: AUO

BBC -

Chimei Innolux TWE: 3481

Eutelsat PAR: ETL

Intelsat NYSE: I

LG KSE: 066570

NHK -

Samsung KSE: 005930

SES LUX: SESG

Sharp TYO: 6753

Sony TYO: 6758

Telesat -

Viasat NASDAQ: VSAT

Formerly: iSuppli, Screen Digest, Displaybank and IMS Research

COPYRIGHT NOTICE AND LEGAL DISCLAIMER© 2013 IHS. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS. Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more information, please contact IHS at [email protected], +1 800 IHS CARE (from North American locations), or +44 (0) 1344 328 300 (from outside North America).

IHS Electronics & Media

© 2013 IHS

Ultra High Definition: The next generation of high resolution contentTom Morrod, Senior Director, TV Technology Ed Border, Senior Analyst, TV Technology

•The technical systems for a wider 4K Ultra High Definition (UHD) launch will be ready by 2016/2017, while it is expected to achieve commercial mass market by 2022/2023

•By 2020, there will be 213 UHD channels, 140m TV households with at least one UHD TV and over 50m UHD set-top boxes (STBs) installed

•Take up of UHD-capable TVs will be spurred on by TV manufacturers for screen sizes of 50-inches and above. By 2025, nearly half of all TVs shipped will be UHD-capable, and a quarter of all households will have at least one UHD TV

•The benefits of HEVC towards HD and IP distribution will create an early market for HEVC-compatible set-top boxes

•UHD channels will launch primarily based on higher-tier drama, documentary, movie and sporting content, with more than 1000 UHD channels worldwide on satellite

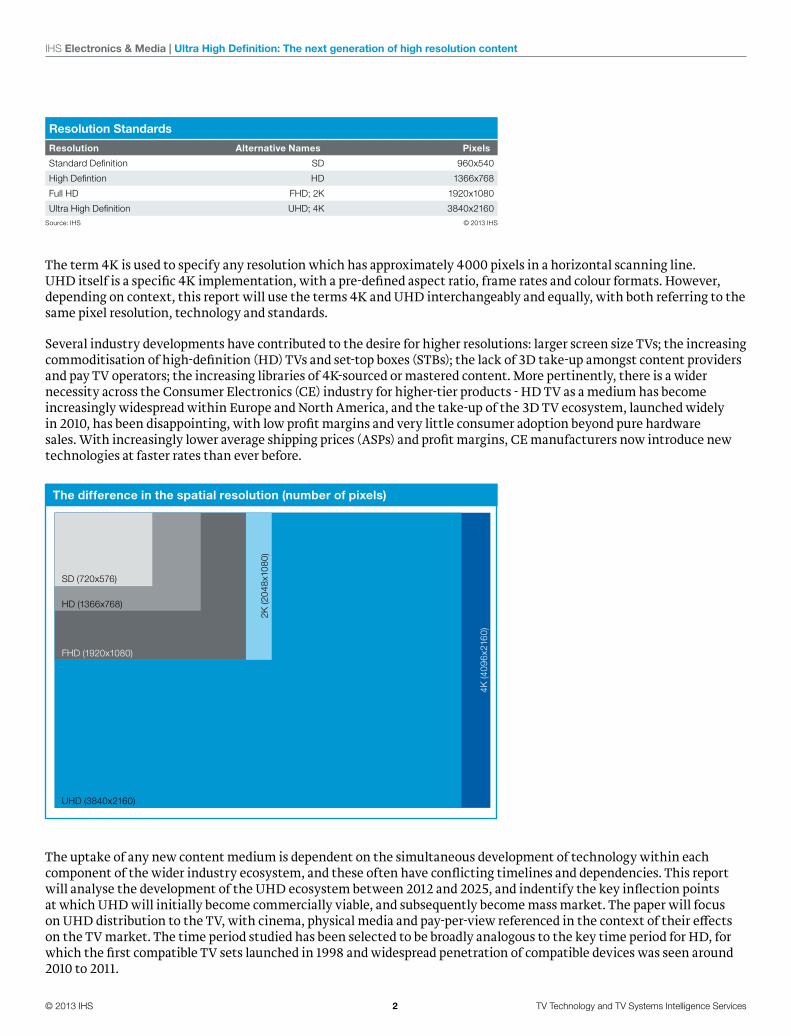

IntroductionIn 2012, the International Telecommunication Union (ITU) ratified two new standards for higher resolution viewing, UHD-1 and UHD-2. The two standards are extensions of the current 1920x1080 pixel Full HD (FHD; 2K) resolution format, with UHD-1 (interchangeably known as Ultra High Definition, UHD or 4K) measuring twice the vertical and horizontal resolution, at 3840x2160 pixels, and UHD-2 (interchangeably known as Super Hi-Vision, or 8K) comprising a further extension, at 7680x4320 pixels.

© 2013 IHS 2 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

Resolution Standards

Resolution Alternative Names Pixels

Standard Definition SD 960x540

High Defintion HD 1366x768

Full HD FHD; 2K 1920x1080

Ultra High Definition UHD; 4K 3840x2160Source: IHS © 2013 IHS

The term 4K is used to specify any resolution which has approximately 4000 pixels in a horizontal scanning line. UHD itself is a specific 4K implementation, with a pre-defined aspect ratio, frame rates and colour formats. However, depending on context, this report will use the terms 4K and UHD interchangeably and equally, with both referring to the same pixel resolution, technology and standards.

Several industry developments have contributed to the desire for higher resolutions: larger screen size TVs; the increasing commoditisation of high-definition (HD) TVs and set-top boxes (STBs); the lack of 3D take-up amongst content providers and pay TV operators; the increasing libraries of 4K-sourced or mastered content. More pertinently, there is a wider necessity across the Consumer Electronics (CE) industry for higher-tier products - HD TV as a medium has become increasingly widespread within Europe and North America, and the take-up of the 3D TV ecosystem, launched widely in 2010, has been disappointing, with low profit margins and very little consumer adoption beyond pure hardware sales. With increasingly lower average shipping prices (ASPs) and profit margins, CE manufacturers now introduce new technologies at faster rates than ever before.

The difference in the spatial resolution (number of pixels)

SD (720x576)

2K (2

048x

1080

)

4K (4

096x

2160

)

HD (1366x768)

FHD (1920x1080)

UHD (3840x2160)

The uptake of any new content medium is dependent on the simultaneous development of technology within each component of the wider industry ecosystem, and these often have conflicting timelines and dependencies. This report will analyse the development of the UHD ecosystem between 2012 and 2025, and indentify the key inflection points at which UHD will initially become commercially viable, and subsequently become mass market. The paper will focus on UHD distribution to the TV, with cinema, physical media and pay-per-view referenced in the context of their effects on the TV market. The time period studied has been selected to be broadly analogous to the key time period for HD, for which the first compatible TV sets launched in 1998 and widespread penetration of compatible devices was seen around 2010 to 2011.

© 2013 IHS 3 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

This report will focus on both technological developments and consumer uptake among four key sections of industry:

The challenge of generating 4K content: the re-mastering and restoration of existing 4K assets; the current content library of 4K movies and TV shows; the upscaling of 2K content to 4K resolution; the penetration of 4K-capable cameras within studios; and the data storage and transfer costs associated with larger 4K production assets.

Bottlenecks and bandwidth scarcity: the available bandwidth for distribution; the role of high-bandwidth, in particular via satellite where UHD is likely to launch; the development of next-generation transmission technologies such as DVB-S2x, and the HEVC codec; conditions for simulcasting SD/HD/3D/UHD feeds.

Pay TV operator and channel strategy: channel strategy for UHD launches; launch of HEVC and UHD STBs; operator launch strategy based on UHD TV household penetration.

Sufficiency of UHD hardware installed base: TV set launches and strategy by brand for 2013; the launch of 4Kx1K, cheaper UHD resolution panels; household penetration forecasts to 2025; and next-generation games consoles and Blu-ray Disc (BD) players.

Background and case studies

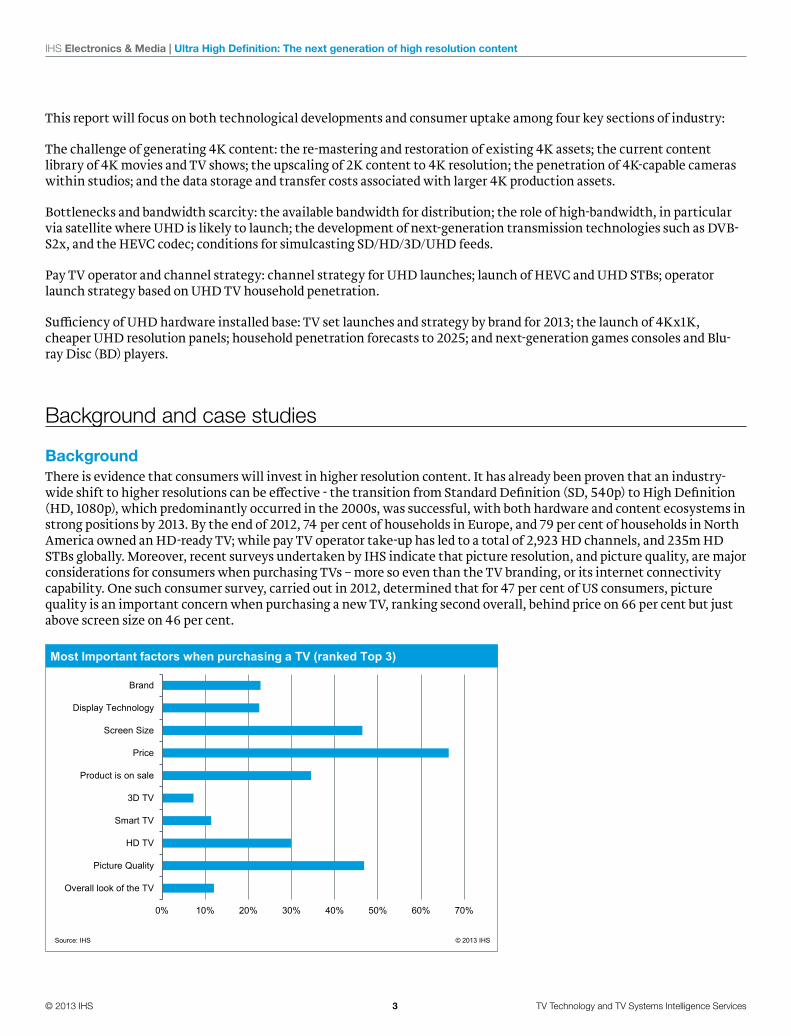

BackgroundThere is evidence that consumers will invest in higher resolution content. It has already been proven that an industry-wide shift to higher resolutions can be effective - the transition from Standard Definition (SD, 540p) to High Definition (HD, 1080p), which predominantly occurred in the 2000s, was successful, with both hardware and content ecosystems in strong positions by 2013. By the end of 2012, 74 per cent of households in Europe, and 79 per cent of households in North America owned an HD-ready TV; while pay TV operator take-up has led to a total of 2,923 HD channels, and 235m HD STBs globally. Moreover, recent surveys undertaken by IHS indicate that picture resolution, and picture quality, are major considerations for consumers when purchasing TVs – more so even than the TV branding, or its internet connectivity capability. One such consumer survey, carried out in 2012, determined that for 47 per cent of US consumers, picture quality is an important concern when purchasing a new TV, ranking second overall, behind price on 66 per cent but just above screen size on 46 per cent.

0% 10% 20% 30% 40% 50% 60% 70%

Overall look of the TV

Picture Quality

HD TV

Smart TV

3D TV

Product is on sale

Price

Screen Size

Display Technology

Brand

Most Important factors when purchasing a TV (ranked Top 3)

Source: IHS © 2013 IHS

© 2013 IHS 4 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

Given the likelihood of consumer interest in UHD content, the chief challenge is widespread industry adoption. Revenue success throughout the supply chain, whether within content capture, production, distribution, transmission or broadcast, is ultimately dependent on end-consumer desire to pay a premium for enhanced TV experience due to higher resolution, along with richer colour and field depth - in the form of paid-for content, either via the cinematic, physical media, pay-per-view or pay TV distribution window. The new format must be a differentiator from previous formats, and the content produced must be compelling enough to generate additional consumer revenue – lest the additional costs of generating the content become an industry-wide burden.

Camera Blu-ray player

Pay TV operator

Encoding

Productionworkflow

Set-top box

Games console

TV

Third party OTT provider

Modulation

Public/private broadcaster

Satellite/IP/DTT/Cable

Ho

me

net

wo

rk

Content creation

Consumer equipment

Content aggregation

Distribution

The content distribution industry

The primary developments that need to take place for adoption of a new content medium tend to be twofold: the development of technologies to ensure more efficient transmission of larger quantities of data; and an increased household penetration of compatible TVs. Once the installed base of compatible devices reaches a satisfactory initial threshold (usually between 3 and 10 per cent of households), larger pay TV operators begin to launch specialist channels and services. Consumer take-up of these services can subsequently drive the creation of compatible TV content.

However, a switch-out of content media is not a common occurrence – such events occur over many years, such as the switch from black-and-white TV to colour TV. As such there is no fixed timeline for how developments unfold. It can be instructive instead to look at how the content ecosystem developed in two case studies from the more recent past – the evolution from SD to HD content; and the launch of 3D services.

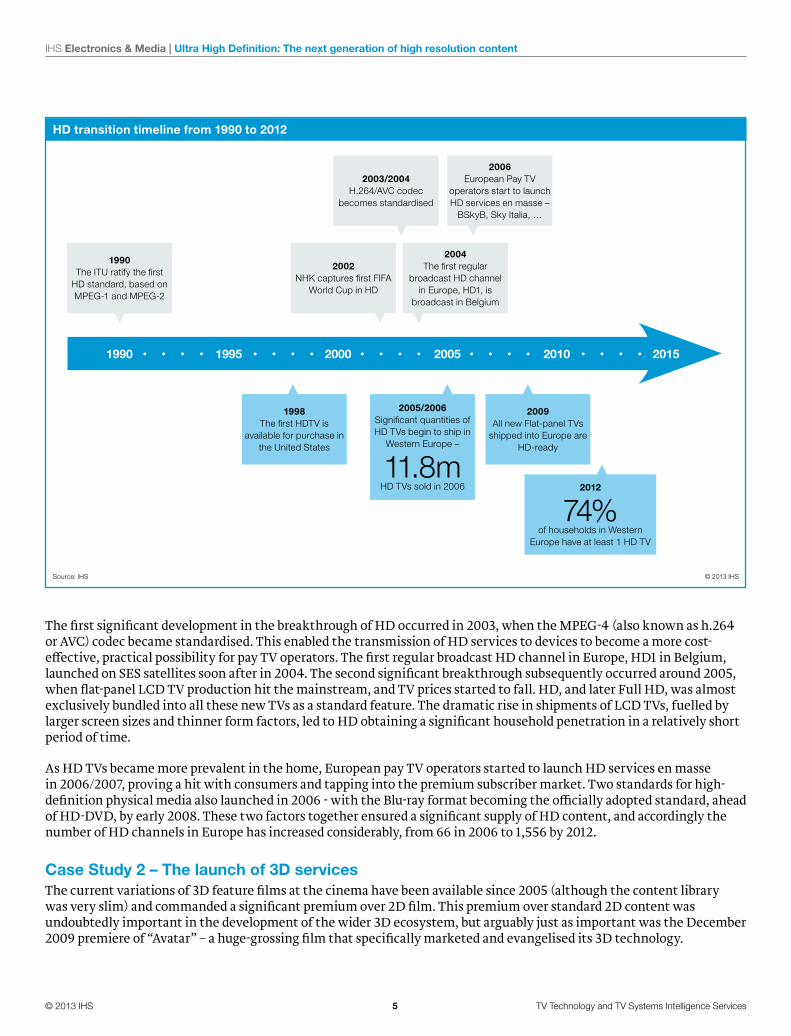

Case Study 1 – The SD to HD transitionThe emergence of HD primarily unfolded in the 2000s, but the original groundwork was laid in 1990, when the ITU ratified the original HD standard. Initially this was based on the early MPEG-1 and MPEG-2 encoding standards, neither of which was particularly practical for HD transmission. Following a period in which there were very few developments, the first MPEG-2 HD TVs became available for purchase in the US from 1998 onwards – with cumulative sales of just 5m between 1998 and 2003, 3.2 per cent of all TVs shipped.

© 2013 IHS 5 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

HD transition timeline from 1990 to 2012

1990 1995 2000 2005 2010 2015

1990The ITU ratify the first

HD standard, based on MPEG-1 and MPEG-2

2002NHK captures first FIFA

World Cup in HD

2003/2004H.264/AVC codec

becomes standardised

1998The first HDTV is

available for purchase in the United States

2009All new Flat-panel TVs

shipped into Europe are HD-ready

Source: IHS © 2013 IHS

2005/2006Significant quantities of HD TVs begin to ship in

Western Europe –

11.8m HD TVs sold in 2006 2012

74% of households in Western

Europe have at least 1 HD TV

2006European Pay TV

operators start to launch HD services en masse –

BSkyB, Sky Italia, …

2004The first regular

broadcast HD channel in Europe, HD1, is

broadcast in Belgium

The first significant development in the breakthrough of HD occurred in 2003, when the MPEG-4 (also known as h.264 or AVC) codec became standardised. This enabled the transmission of HD services to devices to become a more cost-effective, practical possibility for pay TV operators. The first regular broadcast HD channel in Europe, HD1 in Belgium, launched on SES satellites soon after in 2004. The second significant breakthrough subsequently occurred around 2005, when flat-panel LCD TV production hit the mainstream, and TV prices started to fall. HD, and later Full HD, was almost exclusively bundled into all these new TVs as a standard feature. The dramatic rise in shipments of LCD TVs, fuelled by larger screen sizes and thinner form factors, led to HD obtaining a significant household penetration in a relatively short period of time.

As HD TVs became more prevalent in the home, European pay TV operators started to launch HD services en masse in 2006/2007, proving a hit with consumers and tapping into the premium subscriber market. Two standards for high-definition physical media also launched in 2006 - with the Blu-ray format becoming the officially adopted standard, ahead of HD-DVD, by early 2008. These two factors together ensured a significant supply of HD content, and accordingly the number of HD channels in Europe has increased considerably, from 66 in 2006 to 1,556 by 2012.

Case Study 2 – The launch of 3D servicesThe current variations of 3D feature films at the cinema have been available since 2005 (although the content library was very slim) and commanded a significant premium over 2D film. This premium over standard 2D content was undoubtedly important in the development of the wider 3D ecosystem, but arguably just as important was the December 2009 premiere of “Avatar” – a huge-grossing film that specifically marketed and evangelised its 3D technology.

© 2013 IHS 6 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

The subsequent push to bring 3D TV into the home became more widespread in 2010, and CE manufacturers began offering 3D-capable TV sets from Q2 onwards. Despite the widely reported impression that 3D TVs have been a disappointment, actual pure hardware sales since then have been reasonably impressive, particularly when compared to the early years of other technologies such as Smart TVs and HD. By 2012, 16 per cent of all TVs shipped globally were 3D TVs, whilst 8 per cent of all Western European households owned at least one 3D TV. However, it is fair to say that early 3D TV shipments were beneath expectations for manufacturers – with just 4m 3D TVs shipped in 2010, inventory of 3D TVs was high, and price reduction occurred faster than expected, reducing the 3D premium paid by consumers. But these were not hindrances to the wider TV ecosystem – if anything, early commoditisation of the technology should have increased the installed base more quickly.

Where 3D TV really struggled, and continues to struggle now, is with the content. Pay TV operators, or at least the higher-end pay TV operators such as BSkyB and DirecTV, were relatively quick to launch 3D TV channels, and by the end of 2011 there were 18 3D TV channels available across Europe. But these channels lacked broader content offerings outside of sport and some film, which was due, in the main, to the lack of specialist TV content produced in 3D. 3D capture and production required new investment in camera equipment; it required specialist training for staff to use; it did not benefit the capture of the equivalent HD content; and in the case of many genres, such as drama or comedy, it offered no significant enhancement to existing products. All of this led to doubling of costs, as 3D workflow could not generate 2D workflow. Attempting to reverse this by engineering 3D workflow from 2D workflow using post-production also required significant time and costs.

Overall, difficulties in producing 3D content were compounded by a fundamental lack of consumer demand. In the context of feature films, and perhaps certain sporting events, the 3D experience can command an audience, as a special, more involving experience. But for the vast majority of current content 3D increases overhead costs (and interrupts the typical TV experience by requiring the use of glasses), whilst not significantly enhancing viewing.

Content capture and productionThe initial stage of the UHD ecosystem revolves around content capture and production. Prior to any channel launches or broadcasts, cinematic and TV-specific content will need to be available. From a professional standpoint this first requires the creation of a 4K asset by a studio, whether from existing sources or freshly captured, and second the production of the content, in which a 4K asset is stored, backed-up, edited, and compressed.

Existing UHD contentThe UHD content ecosystem is already on its way to establishment. As of the end of 2012, there are currently 150 films and TV shows which have a 4K master copy, and can thus be distributed in UHD immediately; and 793 films and TV shows which remain captured in 4K source format, and would need to be rendered again for UHD distribution.

© 2013 IHS 7 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

0

50

100

150

200

250

300

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

YTD

(201

3)

Film

and

TV

show

s us

ing

4K(#

)

Master Source

4K Content: Cinema and Television

Source: IHS © 2013 IHS

The first, and possibly most immediate, method of expanding the current UHD content library is through restoring and re-mastering content initially released in other formats. There are over 100,000 films and TV shows which were originally captured in 35mm analogue film. It is impossible to state precisely the resolution of a 35mm shot film – pixels are a digital measure, and the data captured within each pixel during the transition from analogue to digital depends on factors such as the exposure, lighting, focus and the degree of chemical blurring on the film. What matters is not the number of pixels captured – analogue film is continuous, and could be theoretically sampled at any resolution chosen. What matters is the number of “good” pixels which can be extracted from the film, or, more accurately, how much useful information can be extracted from the film for each site (pixel) in a sample at a given resolution. Analogue film has already been successfully over-sampled at 4K and 6K and is then processed to the Full HD (2K) format, which contains just over 2m pixels. Estimates for the number of “good pixels” captured within each analogue film shot vary between about 5 to 15 million. With UHD requiring approximately 8.2m pixels worth of information per frame (3840x2160), the vast majority of older analogue films could be re-mastered to be UHD-ready.

This creates a tempting prospect for content owners to cash in on their existing assets – Sony Pictures has recently started on a much publicized initiative to restore and re-master the “important” films in its back-catalogue, whilst the TV show “Breaking Bad” was also shot on film and is set to be re-mastered in 4K. However, the process can be difficult, and time-consuming. Restoration of these negatives is a meticulous process; to give an indication of the time involved, the restoration and re-mastering of Lawrence of Arabia took three years (although that film is over 50 years old, and more recently shot content will typically be able to bypass restoration and be re-mastered directly from the original negative). The challenge is not strictly technical either - a UHD scan demands creative input when being restored and colour corrected. Re-visiting a historic film in this way requires sensitivity to the original artistic vision, and great care must be taken that the extra resolution does not detract from the original experience.

An alternative process to this is to “upscale” Full HD content to UHD, either within the TV itself or through an associated set-top device. This is an interim solution to the content gap, which requires advanced imaging techniques to analyse a 1920x1080 image and then “fill in the gaps” to scale upwards to a 3840x2160 image. This is primarily an implementation for higher-tier TV manufacturers, who are going to market early with UHD products, and wish to pre-empt the “lack of content” issue which damaged 3D.

Content CaptureAs of the end of 2012, UHD camera adoption amongst studios has been progressing smoothly. A major study conducted by IHS into camera ownership by studios within Europe showed that just over 10 per cent of studios owned at least one

© 2013 IHS 8 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

4K-capable camera in 2012. Moreover, within the total installed base of all cameras in Europe, 6.5 per cent were digital cameras that had resolutions of between 2K and 4K, while 3.5 per cent were full 4K cameras. The primary reason studios gave for early adoption of 4K cameras was the production of non-live genres, typically favoured by those seeking a film-like look for artistic reasons (as 4K cameras to date have typically been using a single, large-format image sensor which creates a similar shallow depth of field as is seen in film production).

45%

31%

2%

7%

3%

9%3%

Studio ENG DSLR Film-like digital (between 2k and 4k) Prosumer Other Full 4K

European Studio Survey: Cameras by Type

Source: IHS © 2013 IHS

The development of 4K capabilities on cameras at increasingly lower price points is analogous to the proliferation of film-like cameras that was sparked by video on DSLRs. In that instance, the latent demand identified by DSLR manufacturers highlighted a price band where ‘indie’ content creators were willing to invest and where larger established studio content creators are willing to experiment. IHS believes the equivalent price point for 4K to be below €15,000; offering 4K at this price point will help push the medium to the mainstream of content creators. Sony (the largest manufacturer by market share of professional cameras), Canon, Red and JVC have all introduced 4K capabilities at these price points.

There are image quality considerations beyond resolution that dictate the choice of camera for different productions. Large budget films are likely to always use cameras an order of magnitude more expensive than €15,000, and add-ons like long-range lenses with glass quality needed for 4K production are important costs, often more than the body of the camera. Meanwhile, studio adoption of UHD-capable cameras and camcorders is likely to rapidly increase, irrespective of whether the studio in question decides to produce in UHD or not. A 4K-capable camera provides inherent advantages even when filming and producing HD content – allowing for digital zooms, flexible framing, increased exposure latitude and a wider array of colour options.

© 2013 IHS 9 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

4K Camera Prices (Apr 2013)

Company Camera Value (€)

BlackMagic Production Camera 4K 3,100

Canon EOS C500 23,500

Canon EOS 1DC 10,600

For-A FT-One 105,600

Go pro Hero3 500

JVC GY-HMQ10 4,700

Red Scarlet 8,200

Red Epic 16,400

Sony PMW-F5 14,100

Sony PMW-F55 25,800

Sony PMW-F65 46,900

Vision Research Phantom 65 Gold 105,600

Vision Research Phantom Flex 4K 84,000Source: IHS © 2013 IHS

This allows for a flexible range of use-cases; in live sports, for example, a broadcaster may employ a 4K camera to improve replay footage, as a digital zoom on a contentious decision allows for more insight into the action without a loss in resolution. As such, UHD has a clear use-case for studios at capture, even while the rest of the production chain evolves to handle the larger assets and increased data rates all the way to distribution. This is an important differentiator of 4K from 3D; where 3D cameras had one use-case and required specific skill-sets to operate, 4K cameras cover more use-cases and allow for an evolution of skills that offers content creators the ability to shore up expertise on the format without taking on heavy risks.

ProductionAlthough the range of available 4K cameras is spreading, there is currently a limited offering of 4K production hardware for niche production machines such as monitors, switchers and recorders. Manufacturers, however, have committed to developing this area and the product pipeline looks promising, with launches expected in the near future. The purchase of 4K capable hardware will most likely be part of the content creator’s upgrade cycle, which will see different parts of the workflow become 4K ready in different timeframes. Acquisition will be (or has already become in some cases) the first piece of the puzzle in place.

The largest challenge for UHD production is the storage and the speed of storage. UHD assets can typically be very large; a finished film can represent 5TB whittled down from 300TB of raw footage. Content creators will have to contend with the fact that 4K means storing, archiving and backing up all assets from acquisition to the final product, with each stage of the process being between 4 to 8 times ‘heavier’ than HD demands. Inevitably, this will cause storage costs to rise – even whilst per gigabyte costs enjoy a continual decline.

This represents not only a capacity problem, but also a speed problem – the additional gigabytes take longer to move around the workflow, creating shifts in workflow processes. This is potentially more of an issue, as the premium paid for speed of storage is a much more stubborn price point than per gigabyte costs. At capture, uncompressed 4K can reach 6 Gb/s, a data rate catered for by only the highest end solid-state drives (SSDs). Lossless compression at capture can mitigate this, but many manufacturers will opt for the uncompressed route – generating issues for the content creator instead.

This is arguably a larger problem for television productions that are kept to strict schedules. Keeping a UHD production within an HD schedule requires specialist equipment and facilities. The individual hardware components with associated processing power increases and storage upgrades are available and will become increasingly affordable, but the wider infrastructure that connects the chain will be a heavy investment. IHS estimates that at least a 10 Gb/s infrastructure is needed to allow a 4K workflow to become as seamless as current HD ones. The current Serial Digital Interface (SDI) standards for transmission of uncompressed professional video are HD-SDI and 3G-SDI, each of which can only support data transfer of up to 3 Gb/s.

© 2013 IHS 10 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

Broadcast and transmissionOnce UHD content is available, the next challenge is to broadcast it to the consumer. This challenge comes in several forms: different platforms must be capable of dealing with the content distribution, whether cable, satellite, IP or terrestrial; transmission and encoding standards must be specified, with suitable CE devices available in households that can receive the signal; channel groups and operators have to purchase rights to, and aggregate, the content; and then pay TV operators need to create packages which encourage subscribers to pay for these new services.

This report will focus on the distribution of content via satellite. The reasons for this are multiple: firstly, satellite is itself a major TV distribution platform, comprising 34 per cent of all TV households in Europe, 29 per cent in North America and over 70 per cent across key markets in Africa and the Middle East; secondly, cable and terrestrial retransmission often relies on contributing channels to the operator headend via satellite; and thirdly, the bandwidth, cost and flexibility of satellite architecture is more suited to UHD deployments, and as such forecast that to 2025 the success of UHD will be significantly determined by the roll-out within the satellite industry. With many cable operators locked into MPEG-2 relay infrastructure and specific security systems (such as CableCARD in the US) satellite will lead the market for launching UHD.

Market SummaryWith four times the resolution of HD, the introduction of UHD content will be even more demanding than HD in terms of capacity and data transmission. Even when encoded, it will still take up at least twice the bandwidth on a satellite transponder than its predecessor. The key question is not whether satellites can accommodate UHD, but instead how this distribution can be cheaper and more efficient. In a world where broadcasters are trying to reduce the capital expenditure needed to acquire new customers, any form of cost cutback is welcomed.

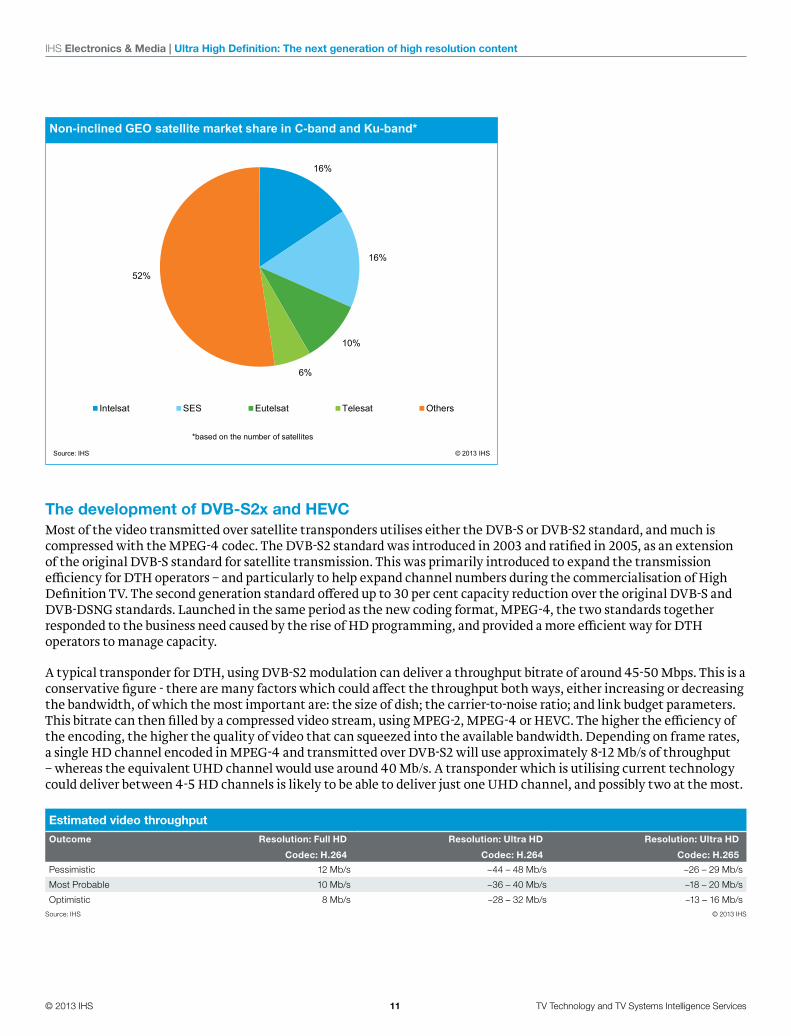

There are nearly 250 satellites operating in either Ku-band or C-band, including those in inclined orbits, all of which would hypothetically be able to deliver UHD content to households. These satellites are primarily either operator-owned or operated by four major independent market players: Eutelsat, Intelsat, SES and Telesat. Video contribution in a form of either Direct-to-Home (DTH) or retransmission of channels for delivery on cable, IPTV or terrestrial services is one of the largest pieces of business for every one of the major satellite operators. DTH distribution is the most efficient form of large scale consumer broadcast and major DTH platforms typically maintain reasonably stable contracts having large numbers of subscribers typically pointing home satellite dishes at a particular satellite location in the sky.

As a point-to-multipoint transmission system, there is no maximum capacity issue for the number of households a satellite can transmit to within its area of coverage. A content provider therefore does not pay annual fees for satellite based on the number of people covered, but rather based on the competitiveness of the markets covered and the lease capacity of a single transponder, or multiple, on the satellite.

© 2013 IHS 11 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

16%

16%

10%

6%

52%

Intelsat SES Eutelsat Telesat Others

Non-inclined GEO satellite market share in C-band and Ku-band*

Source: IHS © 2013 IHS

*based on the number of satellites

The development of DVB-S2x and HEVCMost of the video transmitted over satellite transponders utilises either the DVB-S or DVB-S2 standard, and much is compressed with the MPEG-4 codec. The DVB-S2 standard was introduced in 2003 and ratified in 2005, as an extension of the original DVB-S standard for satellite transmission. This was primarily introduced to expand the transmission efficiency for DTH operators – and particularly to help expand channel numbers during the commercialisation of High Definition TV. The second generation standard offered up to 30 per cent capacity reduction over the original DVB-S and DVB-DSNG standards. Launched in the same period as the new coding format, MPEG-4, the two standards together responded to the business need caused by the rise of HD programming, and provided a more efficient way for DTH operators to manage capacity.

A typical transponder for DTH, using DVB-S2 modulation can deliver a throughput bitrate of around 45-50 Mbps. This is a conservative figure - there are many factors which could affect the throughput both ways, either increasing or decreasing the bandwidth, of which the most important are: the size of dish; the carrier-to-noise ratio; and link budget parameters. This bitrate can then filled by a compressed video stream, using MPEG-2, MPEG-4 or HEVC. The higher the efficiency of the encoding, the higher the quality of video that can squeezed into the available bandwidth. Depending on frame rates, a single HD channel encoded in MPEG-4 and transmitted over DVB-S2 will use approximately 8-12 Mb/s of throughput – whereas the equivalent UHD channel would use around 40 Mb/s. A transponder which is utilising current technology could deliver between 4-5 HD channels is likely to be able to deliver just one UHD channel, and possibly two at the most.

Estimated video throughput

Outcome Resolution: Full HD

Codec: H.264

Resolution: Ultra HD

Codec: H.264

Resolution: Ultra HD

Codec: H.265

Pessimistic 12 Mb/s ~44 – 48 Mb/s ~26 – 29 Mb/s

Most Probable 10 Mb/s ~36 – 40 Mb/s ~18 – 20 Mb/s

Optimistic 8 Mb/s ~28 – 32 Mb/s ~13 – 16 Mb/sSource: IHS © 2013 IHS

© 2013 IHS 12 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

Whilst UHD can therefore be distributed using current technology, a more commercially viable launch of UHD requires both improved transmission efficiency and increased capacity on transponders. Key to this is the development of HEVC (High Efficiency Video Codec, also known as H.265), ratified in January 2013 and conceptualized initially as a response to IP transmission bandwidth restrictions, which have a significant impact on HD transmission. Together with DVB-S2x, the third generation DVB-S format which offers 20-25% per cent net efficiency on a transponder, HEVC will even offer cost advantage solutions for non-UHD ecosystems. HEVC is still in its early stages, and it is not yet certain how vast the improvement on MPEG-4 will be. However, at least a 35-40 per cent bit rate reduction compared to MPEG-4 has been confirmed, with the possibility of more.

36 MHz~ 50 Mb/s

36 MHz~ 60 Mb/s

The effect of DVB-S2x and HEVC

1 UHDChannel~40 Mb/s

2 UHDChannels~20 Mb/s

3 UHDChannels~20 Mb/s

1 HDChannel~10 Mb/s

2 HDChannels~5 Mb/s

DVB-S2MPEG-4

DVB-S2HEVC

DVB-S2xHEVC

* Conservative approach, numbers do not represent any specific satellite

Same transponder

with HEVC and DVB-S2x*

Average transponder in

2012*

Bearing this in mind, a future UHD channel modulated with DVB-S2x and encoded with HEVC should be able to achieve a throughput of approximately 20 Mb/s. When combined with the additional channel capacity achieved through DVB-S2x within a transponder, this could allow up to three UHD channels to exist within a single transponder, more than current capacity enables, additionally a transponder which is transmitting five HD channels at 10 Mb/s could instead deliver two UHD channels and as many as four HD channels. The combination of HEVC and DVB-S2x is a commercially viable distribution model for broadcasters via satellite, which not much additional bandwidth to the initial premium HD channels.

Picture Quality ImprovementsThe development of HEVC, once implemented, offers potential new availability of bandwidth for operators. Aside from a greater number of channels, one obvious usage of this, as mentioned above, is the transfer of more detailed images with a greater array of pixels (resolution), as defined for the UHD standard. However, adding more pixels is just one way to increase image quality, along with appending more colour information per pixel (colour sampling) and more frequent pixel refreshes (frame rate). Initial UHD trials have been run at 24 frames per second (fps), which is the current standard for HD broadcast. However, with a greater level of detail visible per UHD frame, the effects at 24fps can appear blockier as the illusion of seamless motion is harder to achieve at higher resolutions. The UHD standard is defined to allow for higher frame rates, with both 50/60 fps (as seen recently in the cinematic release of “The Hobbit”) and 120fps theoretically possible. Similarly, the increase in resolution could necessitate a rise in colour resolution too, from 4:2:0 (currently used in HD TV) to either 4:2:2, 4:4:2 or even 4:4:4 sampling rates.

The trade-off in this situation is the increased bandwidth required for each improvement to the overall picture quality. The difference in resolution between FHD and UHD required twice the vertical and horizontal resolutions, hence four

© 2013 IHS 13 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

times the bandwidth; a move to 50 fps would require twice the amount of information sent; and colour sampling at 4:4:4 requires more than twice the bandwidth again than 4:2:0. Comparing to the 20 Mb/s throughput for 4:2:0, 24 fps, HEVC-compressed UHD streams mentioned above; we can see that even with HEVC a 4:4:4, 48fps UHD stream would potentially require somewhere in the region of 80 Mb/s.

However, this is still highly theoretical. Higher resolution, in the form of UHD, is already far more advanced in market terms, and will clearly be essential for any higher quality picture video. A move towards higher frame rate seems likely, with talks on-going amongst standards bodies towards 50/60 fps rates. What all this could necessitate, two or three years further on, is a need for even further compression standards, with a potential extension to HEVC a possibility, in order to accommodate increases in temporal and colour resolution.

Channel and operator strategies

UHD channel launch strategyWith the exception of loss-leading early launches, which will be used by operators to increase premium ARPUs and differentiate product offerings, both free and paid 4K content distributed will require long-term profitability. Channels carrying the content will have to generate more money in the form of advertising and carriage fees than it costs to produce/buy, edit, market, transmit, and finally sell the programming.

To drive carriage fees higher than those enjoyed by its HD counterpart, a 4K channel must add significant, monetizeable value to the consumer. A 4K channel must attract an audience large enough to offset operational and distribution costs, but also carry enough of a premium to offset the fact that some channels will be partially cannibalistic in nature - a proportion of the subscriber base of the pay TV channel being subscribers to existing feeds.

It is likely therefore that when UHD channels are initially distributed the channels will be packaged carefully, to both ‘test the waters’ and to prevent immediate cannibalization of existing HD channels. Premium sports and movie channels are often offered in bundles covering the range of genres available, or allow for multiple events to be covered at the same time. UHD sports and movie channels will initially be added as a up-sold premium buy through if owned by a group, or if owned by the platform operator, may be offered as a ‘loss leading reward’ to entice (and reward) customers to buy a fuller range offered. It is also likely that a UHD channel will be adopted ahead of the rest of the market by operators that also produce content – analogous to the early adoption of 3D by the Sky platform in both the UK and Italy.

© 2013 IHS 14 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

0

50

100

150

200

250

300

350

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Num

ber

of c

hann

els

Europe MENA Latam US APAC

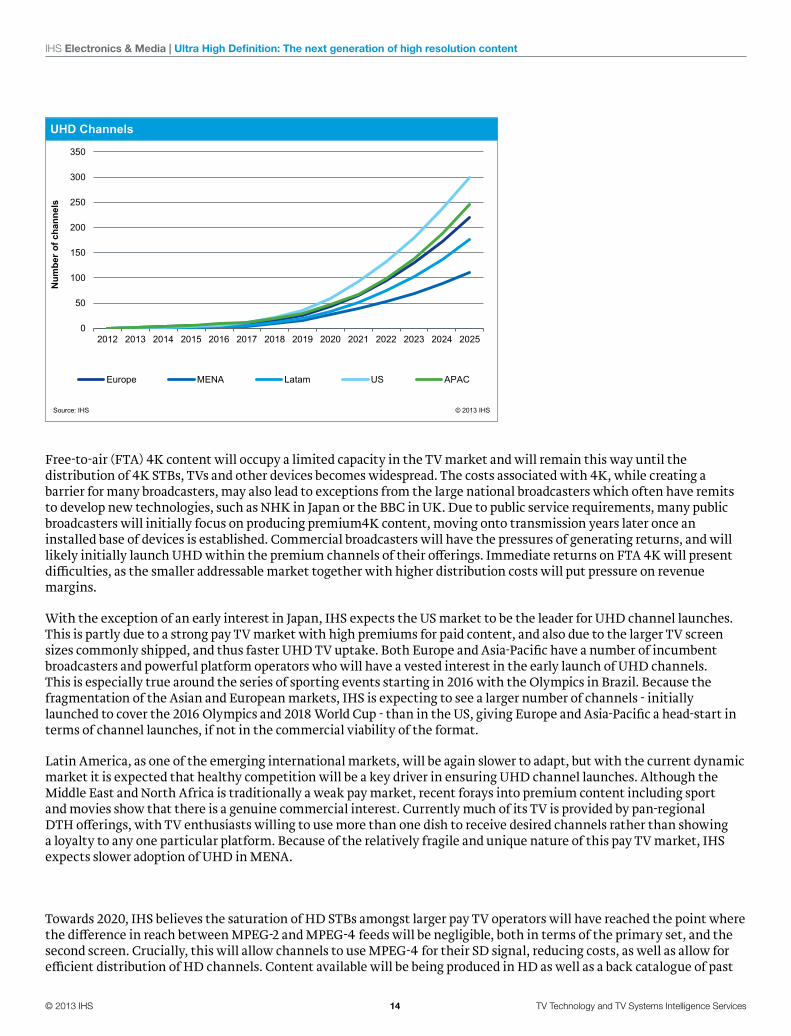

UHD Channels

Source: IHS © 2013 IHS

Free-to-air (FTA) 4K content will occupy a limited capacity in the TV market and will remain this way until the distribution of 4K STBs, TVs and other devices becomes widespread. The costs associated with 4K, while creating a barrier for many broadcasters, may also lead to exceptions from the large national broadcasters which often have remits to develop new technologies, such as NHK in Japan or the BBC in UK. Due to public service requirements, many public broadcasters will initially focus on producing premium4K content, moving onto transmission years later once an installed base of devices is established. Commercial broadcasters will have the pressures of generating returns, and will likely initially launch UHD within the premium channels of their offerings. Immediate returns on FTA 4K will present difficulties, as the smaller addressable market together with higher distribution costs will put pressure on revenue margins.

With the exception of an early interest in Japan, IHS expects the US market to be the leader for UHD channel launches. This is partly due to a strong pay TV market with high premiums for paid content, and also due to the larger TV screen sizes commonly shipped, and thus faster UHD TV uptake. Both Europe and Asia-Pacific have a number of incumbent broadcasters and powerful platform operators who will have a vested interest in the early launch of UHD channels. This is especially true around the series of sporting events starting in 2016 with the Olympics in Brazil. Because the fragmentation of the Asian and European markets, IHS is expecting to see a larger number of channels - initially launched to cover the 2016 Olympics and 2018 World Cup - than in the US, giving Europe and Asia-Pacific a head-start in terms of channel launches, if not in the commercial viability of the format.

Latin America, as one of the emerging international markets, will be again slower to adapt, but with the current dynamic market it is expected that healthy competition will be a key driver in ensuring UHD channel launches. Although the Middle East and North Africa is traditionally a weak pay market, recent forays into premium content including sport and movies show that there is a genuine commercial interest. Currently much of its TV is provided by pan-regional DTH offerings, with TV enthusiasts willing to use more than one dish to receive desired channels rather than showing a loyalty to any one particular platform. Because of the relatively fragile and unique nature of this pay TV market, IHS expects slower adoption of UHD in MENA.

Towards 2020, IHS believes the saturation of HD STBs amongst larger pay TV operators will have reached the point where the difference in reach between MPEG-2 and MPEG-4 feeds will be negligible, both in terms of the primary set, and the second screen. Crucially, this will allow channels to use MPEG-4 for their SD signal, reducing costs, as well as allow for efficient distribution of HD channels. Content available will be being produced in HD as well as a back catalogue of past

© 2013 IHS 15 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

material that can be used. At this point we will see a number of more popular and well know film and TV brands, which are already running an HD simulcast, turn off their SD feeds as every home will be able to decode an HD signal as well as an SD signal, negating the need for simulcast SD and HD. Whilst this is by no means a pre-requisite for UHD channel launches, the transition away from MPEG-2 towards MPEG-4 and HEVC will continue to stimulate the growth of HD and UHD channels.

Set-top box strategyFor pay TV operators to deploy UHD services, they will need to ensure that UHD-compatible STBs are present in the home. However, current HD STBs are not compatible with expected UHD broadcasts. The major source of this incompatibility is the compression standard used - current HD STBs can decode MPEG-2 and MPEG-4 signals but cannot decode the HEVC transmissions which will provide the most commercially viable UHD transmission. Operators must deploy UHD-compatible STBs to launch UHD services. This is largely dependent on the availability of UHD HEVC compatible STB silicon. HEVC was ratified in January 2013, and UHD-capable STB silicon is expect to be available in volume towards the middle of 2015. STB OEMs are unlikely to be able to ship UHD units in volumes which support significant UHD services until the end of 2015 and most likely early 2016.

2016 will be a significant year for UHD launches because of the Olympic Games. Many HD TV launches were coincident with major sporting events, with operators using these to drive uptake of the enhanced viewing experience. NHK captured the 2002 FIFA World Cup in HD but it wasn’t until the build-up to the 2004 Olympic Games that operators began launching HD services. This was mainly in North America, Japan and South Korea. European HD launches were typically later, synchronised with 2006 FIFA World Cup, as well as being a product of slower HD TV set uptake compared with the US and Japan. UHD is expected to follow this trend. NHK will capture the 2014 FIFA World Cup in UHD, but pay TV operators will not be able to deploy UHD STBs in time to launch services to capitalise on this momentum. Instead, the 2016 Olympic Games will likely be the first major sporting event to catalyse UHD service launches in North America and Japan, with European launches happening in time for the 2018 FIFA World Cup.

Time series of significant events

2014 2015 2016 2017 2018 2019

UHD content won’t be the only driver for operators to deploy UHD-capable STBs. The HEVC compression used in UHD STBs can also enable operators to use the bandwidth to deliver more HD and SD content. HEVC will also significantly reduce operating costs for over-the-top (OTT) video-on-demand (VoD) and multiscreen TV services whilst simultaneously improving their Quality of Service (QoS), hence overall enrich the consumer experience. There was also a similar situation with HD STBs. Many of the HD STBs launched by operators from 2006 were also IP-connectable, with their MPEG-4 decoding capabilities enabling video to be compressed enough to allow IP delivery. It was much later after the launch of HD, starting in 2010, that operators began launching services such as OTT VoD and multi-room DVR which made use of this functionality. Supporting multiscreen and OTT video is, currently, a much more immediate problem for operators than UHD. As mentioned, HEVC was initially conceptualized as a solution to transmitting HD over IP, and it could be that IP video delivery acts as the major driver for the initial deployment of UHD-compatible boxes.

For larger, higher ARPU pay TV operators the transition towards all MPEG-4 STBs is already in the latter stages. For the most part this is occurring organically through subscribers upgrading to HD packages and multi-room DVR. Many of the major operators, particularly in Europe, have already implemented HD-only STB procurement strategies, giving all new

© 2013 IHS 16 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

subscribers HD STBs regardless of their subscription tier – which in turn gives rise to a mid-term need for a new premium product, which UHD can fill.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Hou

seho

ld p

enet

ratio

n (%

)

Shaw Direct (Canada) Bell Expressvu (Canada) DirecTV (US) SkyPerfecTV (Japan)Dish Network (US) KT Skylife (South Korea) BSkyB (UK) Canal Digital (Denmark)Canalsat (France) Cyfra+ (Poland) Multichoice (South Africa) Sky Deutschland (Germany)Sky Italia (Italy)

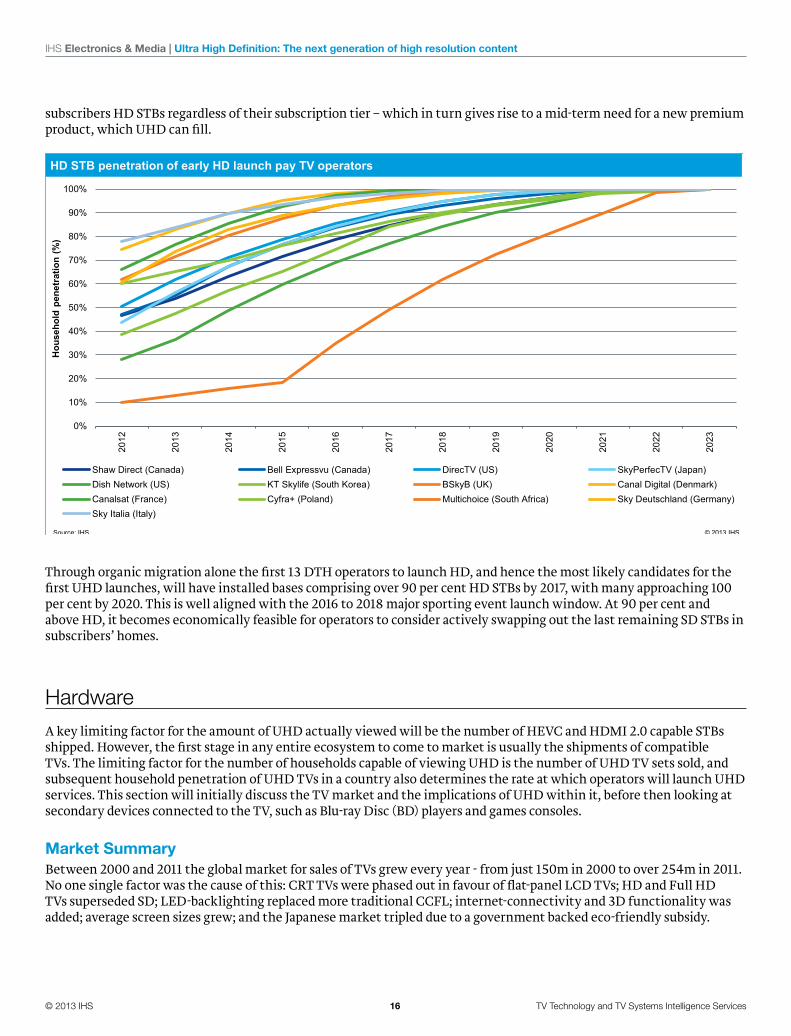

HD STB penetration of early HD launch pay TV operators

Source: IHS © 2013 IHS

Through organic migration alone the first 13 DTH operators to launch HD, and hence the most likely candidates for the first UHD launches, will have installed bases comprising over 90 per cent HD STBs by 2017, with many approaching 100 per cent by 2020. This is well aligned with the 2016 to 2018 major sporting event launch window. At 90 per cent and above HD, it becomes economically feasible for operators to consider actively swapping out the last remaining SD STBs in subscribers’ homes.

HardwareA key limiting factor for the amount of UHD actually viewed will be the number of HEVC and HDMI 2.0 capable STBs shipped. However, the first stage in any entire ecosystem to come to market is usually the shipments of compatible TVs. The limiting factor for the number of households capable of viewing UHD is the number of UHD TV sets sold, and subsequent household penetration of UHD TVs in a country also determines the rate at which operators will launch UHD services. This section will initially discuss the TV market and the implications of UHD within it, before then looking at secondary devices connected to the TV, such as Blu-ray Disc (BD) players and games consoles.

Market SummaryBetween 2000 and 2011 the global market for sales of TVs grew every year - from just 150m in 2000 to over 254m in 2011. No one single factor was the cause of this: CRT TVs were phased out in favour of flat-panel LCD TVs; HD and Full HD TVs superseded SD; LED-backlighting replaced more traditional CCFL; internet-connectivity and 3D functionality was added; average screen sizes grew; and the Japanese market tripled due to a government backed eco-friendly subsidy.

© 2013 IHS 17 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

0

50,000

100,000

150,000

200,000

250,000

300,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Ship

men

ts (0

00s)

CRT TV LCD - CCFL LCD - LED PDP TV RPTV OLED TV

TV shipments: 2000 to 2011

Source: IHS © 2013 IHS

But perhaps the single most important trend was that of price decline. The component costs for LCD TVs fell significantly over the past 10 years, with manufacturing centralised around China and South Korea. The panels required for LCD TVs are now primarily produced by 5 sources: AUO and Innolux (Taiwan); LG and Samsung (South Korea); and Sharp (Japan). This has subsequently lowered the barrier of entry to the TV market, and greatly increased competition. In developed markets, many smaller brands now offer low-priced models, and particularly retailers such as Walmart and BestBuy in the US and Tesco in the UK now offer a range of own-brand TVs; whilst in markets in Asia Pacific, China and Africa, Chinese manufacturers have increased brand awareness and market share significantly.

However, in 2012 the global TV market fell, by over 6 per cent to 238m units. This fall was precipitated by both the demand and supply side: demand in developed markets such as Japan, North America and Western Europe declined significantly following the saturation of TVs in past years and the conclusion of digital switchovers; whilst on the supply side, Japanese manufacturers such as Panasonic, Sony and Sharp have suffered TV-related operating losses from 2011 onwards due to the fierce price competition, and have downsized volumes, looking to re-establish themselves as smaller, higher-tier competitors.

© 2013 IHS 18 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

0

50,000

100,000

150,000

200,000

250,000

300,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Ship

men

ts (0

00s)

Asia Pacific China Eastern Europe Japan

Latin America Middle East and Africa North America Western Europe

TV set supply by region: 2000-2011

Source: IHS © 2013 IHS

The TV market is now in a period of transition. Demand will decrease slightly in 2013, stabilise in 2014, and growth through to 2017 will be driven by the so-called “developing markets” in Asia-Pacific, Eastern Europe, Latin America, Middle-East and Africa. Manufacturers looking to achieve volume will target markets such as Brazil, China, India, Indonesia, Mexico and Russia. Manufacturers looking to achieve value will look to expanding new technologies in more developed markets within China, Japan, North America and Western Europe, targeting larger screen sizes and more advanced features sets.

UHD TV StrategyAmongst all the relevant parties, TV manufacturers have been the first to bring UHD products to market, with initial 3840x2160 resolution TV sets introduced to the market in Q4 2012. In a sense, this is inevitable – as the case of 3D showed, launching services without a sizeable installed base of compatible TVs leads to severe difficulties – but it is also a reaction to the competitive landscape of the TV market. To capitalise on the higher margin early-adoption market, manufacturers look to higher-tier products, and are motivated towards pushing new features, which in recent years have included Full HD, Smart TV, LED backlighting and 3D TV.

Timeline series of TV product innovation

2007 2008 2009 2010 2011 2012 2013 2014

Initial launch

Marketingpush

The widespread 2013 launch of UHD features models from all major TV manufacturers and are primarily found in the range of 55-inch to 110-inch TVs. In its infancy UHD will be almost exclusively dominated by large, 50-inch plus screen sizes. This is a necessity from both a practical and technical viewpoint: UHD itself is best contrasted to Full HD when viewed at larger dimensions; and as a premium product, with significant expenses, it is best marketed within a range of

© 2013 IHS 19 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

larger-sized, higher-tier models. This is unlikely to change in the future - it makes sense long-term for screen sizes below a certain size to have lower price points, analogous to how current TVs below 32-inch still tend to be HD rather than Full HD. IHS believes that shipments of UHD TVs will predominantly be 50-inch plus, although there will be some 39-inch plus models. The range of specific screen sizes actually currently available is limited, brought on by the range of UHD LCD panels available from the core suppliers. Samsung Display initially planned to launch UHD at extremely large sizes of 75-inch, 85-inch, 95-inch and 110-inch models, whilst LG Display has an 84-inch model available. The lower screen sizes are primarily produced by Taiwanese manufacturers AUO (55-inch and 65-inch) and Innolux (39-inch, 50-inch, 58-inch and 65-inch), although Samsung Display is now planning 55-inch and 65-inch panels too. While consumer demand for larger screen sizes will typically grow, there is a longer-term question as to whether the pixel density of smaller sized UHD TVs will actually be visible to consumers. While this is still to be determined, the biggest issue with smaller sized UHD TVs, that of cost of production, may not be as much of a constraint as would initially seem to be the case – the argument being that since consumers won’t be able to discern all the pixels, the percentage of dead-pixels at point of production can be higher than currently accepted and consumers would not be able to see the errors, thereby increasing yields at smaller sizes. The exact economics of small-sized UHD production are still to be determined, but the market may migrate to smaller sizes than 50-inch over time.

Product launch by screen size

110” 110” 110” 110”

95”

85” 84” 84” 84” 84” 84” 84”

75” 75”

65” 65” 65” 65” 65” 65” 65”

58” 58” 58”

55” 55” 55” 55” 55” 55” 55”

With manufacturers essentially showcasing a subset of panels from a small set of panel makers, much of the opportunity for UHD differentiation lies instead in the technology utilised to process imaging. TV models launched in 2013 will not be able to receive UHD due to a lack of home networking standards, and instead content will come via upscaling. The number of T-cons, or “logic boards”, within the TV dictates the actual picture resolution displayed. A typical Full HD LCD TV currently uses 2 T-cons - but for displaying UHD images, with 4 times the number of pixels, it becomes necessary to extend this to 4 T-cons and additional chips, significantly increasing the price. However, the smaller sized UHD panels currently produced by CMI only contain 2 T-cons, and a minimal number of additional chips, to two main effects: firstly, despite the 4Kx2K pixel resolution, the TV itself can only display an effective 4Kx1K resolution (half the vertical resolution); and secondly, that the price differential is significantly lower, with just a 35 per cent premium over same-sized Full HD panels.

This is a short-term strategic product, until the prices for “full” UHD panels fall – but at the same time it represents a lower entry level for UHD in the short-term, and is likely to boost global shipments significantly in the coming years. To take an example from the US market – in H1 2013, the cheaper UHD panels are being used for the Seiki 50-inch UHD TV retailing for $1,499 and the Westinghouse 50-inch UHD TV available for $2,499, whilst the higher-end UHD panels used in Sony 55-inch and 65-inch models are retailing for $4,999 and $6,999 respectively. While much of this cost is borne by the panel and panel drivers, there is currently a large associated cost with the silicon required for UHD upconversion in particular. Currently the chipsets needed to run any moderately comprehensive upconversion from HD to UHD cost approximately $1000 per TV. This not only differentiates the higher-end, “full” UHD TVs, but creates a much higher starting price for consumers. As TV volumes start to increase, the kind of specialist silicon currently needed (called

© 2013 IHS 20 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

FPGA, or programmable chips) will start to commoditise towards fixed-application chips, called ASICs, which are much more cost effective. As UHD TV volumes reach around 1-2m units per year, the upconversion silicon should drop from $1,000 of FPGA towards $200 of ASIC. Once volumes rise higher still this price will fall significantly again, until it is finally integrated within the standard system-on-chip silicon that runs the bulk of video processing, at which point the cost becomes essentially negligible. With this in mind, it is likely that 4Kx1K UHD TVs will be in the market for perhaps two or three years while there is a meaningful price differentiation, before being superseded by “true” 4Kx2K resolution UHD TVs.

The launch of OLED TVs in H1 2013 will not be a stimulus to UHD in the short-term, as the technology for high-yields and mass production of OLED is still nascent, and the economies of making OLED are only just making sense for Full HD resolutions, let alone UHD. Although Sony and Panasonic demonstrated UHD OLED at CES 2013, these were professional-grade displays, and the early launches of commercial OLED screens will be Full HD resolution only. However, towards 2015 and 2016, as OLED production becomes more large scale, IHS expects OLED to become more of a driver for UHD, with a range of 55-inch plus models available.

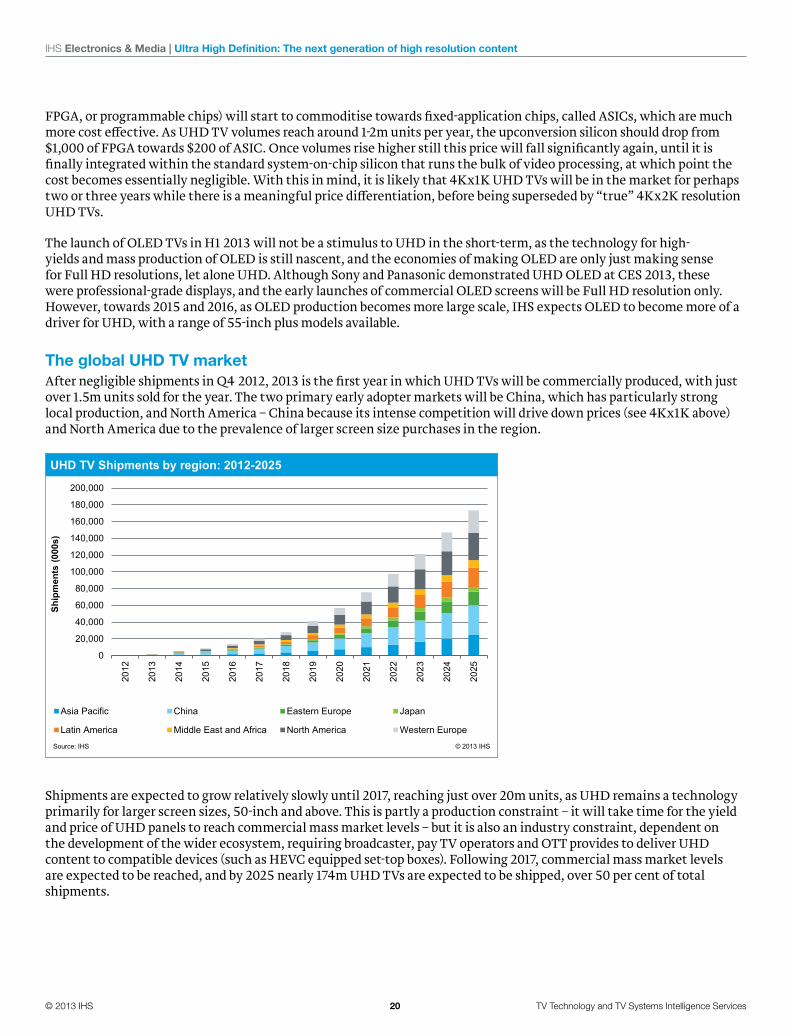

The global UHD TV marketAfter negligible shipments in Q4 2012, 2013 is the first year in which UHD TVs will be commercially produced, with just over 1.5m units sold for the year. The two primary early adopter markets will be China, which has particularly strong local production, and North America – China because its intense competition will drive down prices (see 4Kx1K above) and North America due to the prevalence of larger screen size purchases in the region.

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Ship

men

ts (0

00s)

Asia Pacific China Eastern Europe Japan

Latin America Middle East and Africa North America Western Europe

UHD TV Shipments by region: 2012-2025

Source: IHS © 2013 IHS

Shipments are expected to grow relatively slowly until 2017, reaching just over 20m units, as UHD remains a technology primarily for larger screen sizes, 50-inch and above. This is partly a production constraint – it will take time for the yield and price of UHD panels to reach commercial mass market levels – but it is also an industry constraint, dependent on the development of the wider ecosystem, requiring broadcaster, pay TV operators and OTT provides to deliver UHD content to compatible devices (such as HEVC equipped set-top boxes). Following 2017, commercial mass market levels are expected to be reached, and by 2025 nearly 174m UHD TVs are expected to be shipped, over 50 per cent of total shipments.

© 2013 IHS 21 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

0

0.5

1

1.5

2

2.5

3

3.5

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

TVs

per h

ouse

hold

(#)

Asia Pacific China Eastern EuropeJapan Latin America Middle East and AfricaNorth America Western Europe

TV sets per household: 2005-2017

Source: IHS © 2013 IHS

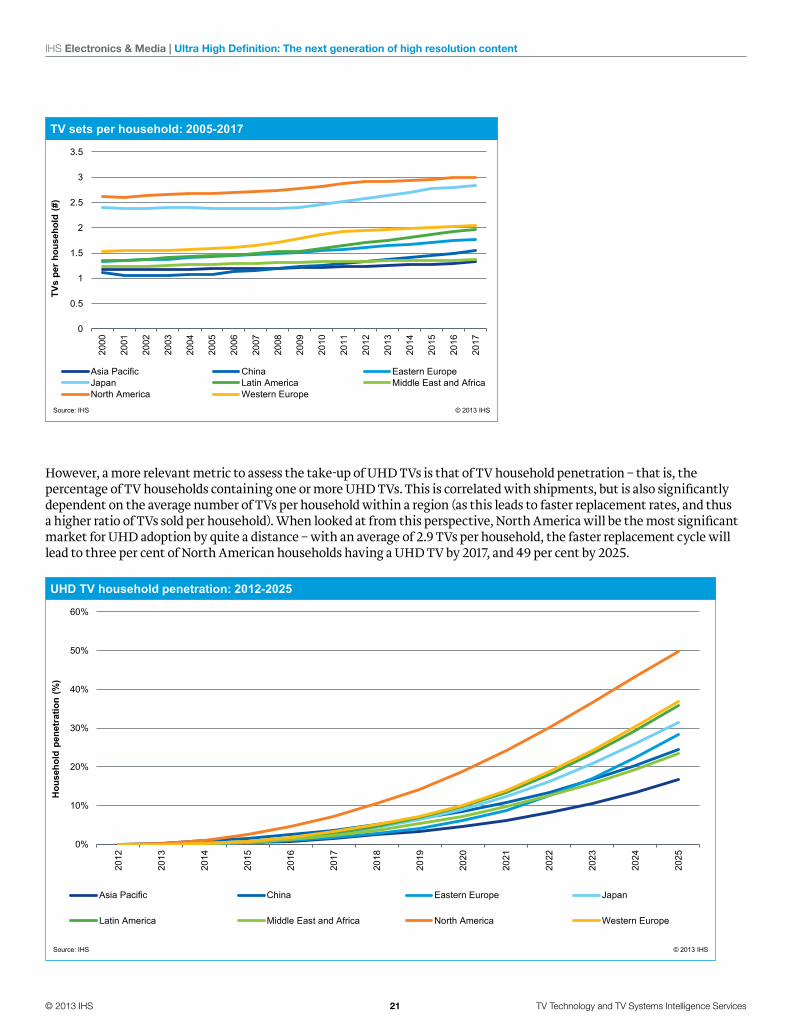

However, a more relevant metric to assess the take-up of UHD TVs is that of TV household penetration – that is, the percentage of TV households containing one or more UHD TVs. This is correlated with shipments, but is also significantly dependent on the average number of TVs per household within a region (as this leads to faster replacement rates, and thus a higher ratio of TVs sold per household). When looked at from this perspective, North America will be the most significant market for UHD adoption by quite a distance – with an average of 2.9 TVs per household, the faster replacement cycle will lead to three per cent of North American households having a UHD TV by 2017, and 49 per cent by 2025.

0%

10%

20%

30%

40%

50%

60%

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Hou

seho

ld p

enet

ratio

n (%

)

Asia Pacific China Eastern Europe Japan

Latin America Middle East and Africa North America Western Europe

UHD TV household penetration: 2012-2025

Source: IHS © 2013 IHS

© 2013 IHS 22 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

By the same logic, Western Europe will be the next key market for UHD in household penetration terms, with 37 per cent by 2025, and Japan and Latin America will follow, each with around 32 per cent of homes owning a UHD TV in 2025. From a wider industry perspective this makes sense – as the most developed pay TV markets, these regions tend to also have a larger secondary TV installed base, which leads to faster household penetration. This faster household penetration, allied with the presence of many larger, higher ARPU pay TV operators, makes these markets the most attractive markets for early UHD service launches.

Other connectable devicesAside from an STB, 4K content could also be brought to the TV via a BD player or a next-generation games console. The first step for the launch of 4K BD services is the creation of a 4K-compatible standard profile. The launch of BD profile 5.0, which is the standard defining 3D-capability, occurred in December 2009, predating even the launch of 3D-capable TVs. It is therefore likely that a BD profile defining 4K-comptibility will launch in 2013 or 2014, following the ratification of HEVC. But it will take time for CE manufacturers to start manufacturing true 4K BD players, although Panasonic in Q1 2013 has already launched a BD player with 4K upscaling capability.

This is because whilst the BD player format was built to be future proof, there may be limitations within the current hardware which will slow the advance of 4K BD. A typical BD disc is either 25 Gb (single layer) or 50 Gb (double layer), and a standard 2K movie compressed in MPEG-4 typically takes up between 25-45 Gb of space, depending on the frame rate and movie length. With a 4K asset compressed using HEVC, files sizes will be between twice and three times larger than current 2K assets, as there will be four times the amount of data with between 30 and 40 per cent more efficient compression via HEVC. This indicates an average file size of around 100Gb for a 4K movie. For current technologies this would necessitate a move up from dual layer Blu-ray discs, with either triple layer (100 Gb) or quadruple layer (150Gb) required. However, the yield for triple layer and quadruple layer Blu-ray discs is still very low, and this is likely to remain an issue until manufacturers begin to order in bulk – which in turn will require a demonstrable market, most likely once UHD TV penetration has increased. Furthermore, low-volume replication runs would add to the cost-per-disc in the early stages.

Moreover, any BD player which is UHD-compatible will need to be HEVC-compatible, and also backwards compatible with previous generations of MPEG-4 and MPEG-2 based Blu-ray Discs. These factors will add extra costs to both the players and the discs. The final issue for consideration is the cost of authorship – that is, the cost for studios to have cinematic content specially rendered and compressed for home-viewing. The additional data processing required for UHD BD will raise this price – which combined to the cost-per-disc issues associated with low-volume production will make UHD BD content more of a loss leader in the early stages.

Meanwhile, Sony has confirmed that the next generation of its PlayStation games console, the PS4, will support 4K movies, although not 4K gaming. With Sony pushing its own UHD content and UHD TVs this makes sense, and should provide another method for consumers to access 4K by downloading UHD content straight to the games console. There has not yet been an official announcement of whether the next generation Xbox from Microsoft will be 4K-compatible.

© 2013 IHS 23 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

Conclusion

Timeline

UHD TV timeline

2012 2014 2016 2018 2020 2023

2013HEVC/H.265 ratified and

DVB-S2x expected by year end

2013The first UHD channel

launched

2018European Pay TV

operators start to launch UHD services en masse

2018First FIFA World Cup to be broadcast en masse

2021: Almost 300 UHD channels will be

broadcast worldwide

202313% of households in Western Europe will

have at least 1 UHD TV

2012The ITU ratify both 4K and 8K UHD profiles

2012The first UHD TV is

available for purchase in the United States

2014First UHD STBs deployed

by pay TV operators

2014NKH captures first FIFA

World Cup in UHD

2017North America UHD TV set household

penetration crosses 3% barrier

2018Western European

UHD TV set household penetration approaches

3% barrier

202338% of Global STB

shipments will be UHD capable

Source: IHS © 2013 IHS

2012 saw the introduction of 4K as a TV medium, with the ratification of the UHD profile and the launch of small volumes of UHD-compatible TV sets. Shipments of UHD TVs are expected to grow significantly in 2013, to 1.5m units, with China and North America key markets. The HEVC codec which will be used for encoding UHD streams was ratified in January 2013, and the next-generation DVB-S2x modulation standard is expected to be ratified by late 2013 or early 2014. This will foster the launch of UHD channels, and these will initially be test channels using DVB-S2. Launches will begin in earnest once DVB-S2x is ratified, with 10 channels expected to be running globally by the end of 2014. The FIFA Football World Cup in 2014 is an ideal event to demonstrate the technology and principles of live broadcasting an event in UHD, and NHK in Japan have already confirmed plans to captures the games in 4K. Some pay TV operators will begin experimenting with UHD channels in 2014, particularly those such as Sky that also produce content.

It will be 2016 and 2017 when the technical systems will be in place for a range pay TV operators to launch UHD services. Global household penetration of UHD TVs will have reached over 3.5 per cent by 2017, with some regions such as North America and Western Europe on 7 per cent and 3 per cent respectively. With many new service launches event-driven, the Olympic Games in 2016 will be an ideal opportunity for many operators in North America in particular, whilst the European Football Championships in 2016 and the FIFA World Cup in 2018 will drive European launches. By 2018 there will be 58 specialist UHD channels available globally, with 80 per cent of these in China, Europe and the North America.

© 2013 IHS 24 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

The widespread commercial mass market of UHD will occur around 2023. By this stage, nearly 19 per cent of all households will have a UHD TV, with 17 per cent in China, 30 per cent in North America and 24 per cent in Western Europe. UHD TVs will account for just under a third of all shipments in the global market, and the mass market effect will lower the component costs for panels and chips significantly. With significant UHD household presence, higher-tier operators will be able to begin moving towards all-HEVC deployment strategies for STBs, analogous to the current trend of all MPEG-4 deployments. There will be almost 350 channels available globally; over 100 in North America, and more than 70 in each of Europe and Asia-Pacific (including China). By 2023 we will be at an approximate equivalent to the HD market in 2006 – widespread technology, proven business models and commercial mass-market opportunities. Over the course of the next 10 years, IHS expects the required ecosystem of devices, technologies and strategies to replicate much of the success of HD.

SummaryThe launch of Ultra High Definition TV depends on uptake across several key areas of the broadcasting and CE industries. In general, the signs are positive that consumer demand for UHD exists, and that the key companies themselves see UHD as a beneficial technology. TV manufacturers in particular have incentives to push larger screen sizes with higher-end features; pay TV operators and channel groups can raise premium ARPUs through new programming content; HEVC will provide much of the efficiencies needed for channels to deliver UHD content while simultaneously benefiting from a close integration with IP delivery both in and out of the home; and content creators and producers can and are improving current HD workflows through the capture of additional pixels during filming. In each case, from a hardware perspective, the switch to UHD technology is potentially beneficial for existing HD broadcast too, creating a reason for consumers to buy into UHD without making it a business necessity that they immediately start paying in full for it. IHS believes that by 2025 the roll-out of UHD TVs and HEVC-compatible STBs will be significant, and that several hundred dedicated UHD channels will have launched globally.

Getting free-to-air and advertising-funded commercial TV channels up will be a slower process, although once pay TV operators launch early UHD channels and public broadcasters produce early UHD content there will be pressure to upgrade premium event programming to UHD. However, it is not the total channel market that is most important to UHD development, rather it is the premium documentaries, drama, movie and sports content from the international channel groups. These groups will continue to use the lowest priced medium available to reach the mass market, or price the highest premium product where they can maximise consumer revenue. By 2025, pay or mini-pay channels will be predominantly HD, as customers paying for content will want better picture, whilst the top tier premium channels will be UHD, to both leverage additional subscribers and to compete with other channels.

As the ecosystem for UHD evolves, there will be several unexpected benefits. Higher resolution content will benefit production processes, and provide better quality archives for future generations. More efficient compression will aid delivery of low quality video further, bridging the global technology divide, open up possibilities for a greater number of niche channels, and allow better quality images to be transmitted than ever before. More complex devices in the home will not only allow for better pictures, but more flexibility in viewing, and will likely be associated with trends towards universal home automation and peripheral benefits such as remote health monitoring, teleconferencing and in-home video-walls. While looking out 12 years is perhaps ambitious, the lessons of history and the logic of ecosystem development suggest that UHD is poised to be an important development in the world of video delivery, creating new revenue opportunities for premium markets.

© 2013 IHS 25 TV Technology and TV Systems Intelligence Services

IHS Electronics & Media | Ultra High Definition: The next generation of high resolution content

North AmericaUSA1700 East Walnut AvenueSuite 600El Segundo, CA 90245Phone: 310.524.4000

Public Relations:Jon [email protected]

John [email protected]

Irene LiuChina)[email protected] & Products:[email protected]

California2901 Tasman Drive, Suite 201Santa Clara, CA 95054Phone: 408.654.1700

Minnesota5720 Smetana DriveSuite 218Minnetonka, MN 55343United StatesPhone: 952.935.0400

AsiaChinaHong Kong8/f - No 1 Chatham Road SouthKowloon, Hong Kong 80HGK1Main Telephone: +852-2368-5733Contact: Jason MaEmail: [email protected]: +852.2834.7833

ShanghaiRoom 1401, BaoAn TowerDongfang Road 800Shanghai, P.R. China 200122Contact: Raymond HanEmail: [email protected]: +86 21-5831-5606

ShenzhenRoom 1805, Block A, World Trade Pla-za, 9 Fuhong Road, Futian DistrictShenzhen, P.R. China 518033Contact: Irene LiuEmail: [email protected]: +86.755.8364.3145

JapanTokyoBUREX Kyobashi, 2-7-14 KyobashiChuo-ku, Tokyo 104-0031, JapanContact: Mayuko KataokaEmail: [email protected]:+ 81.0.3.3562.1580

KyotoKyoto Research Park Building4-3F 1 Awata-cho Chudoji Shimogyo-kuKyoto 600-8815Contact: Junzo (Jim) MasudaEmail: [email protected]: +81.075.315.8930www.iSuppli.co.jp

KoreaSeoul2003 Suseo-Hyundai-Venturebil713 Suseo-dong, Kangnam-guSeoul, Korea 135-884Contact: J.H. SonEmail: [email protected]: 82.2.2040.611

TaiwanTaiwanRoom 618, 6 Floor,No. 1 Industry E. 2nd RoadScience Park, Hsin-Chu, TaiwanROCContact: Mavis WangEmail: [email protected]: +886.3.578.3538

EuropeUK133 HoundsditchLondonEC3A 7BX+44 (0) 203 159 3300

Sales & Products:+44 (0) 203 159 [email protected]

France16/18 rue du Quatre Septembre75002 ParisFranceContact: Jacques NoirbentEmail: [email protected]: +33.1.7676.3064

GermanySpiegelstrasse 281241 MunichGermanyContact: Manfred ThielEmail: [email protected]: +49.89.2070.260.5