IHS CHEMICAL TRENDS IN THE POLYMERS MARKET · TRENDS IN THE POLYMERS MARKET IHS CHEMICAL ... LLDPE...

32

© 2015 IHS TRENDS IN THE POLYMERS MARKET IHS CHEMICAL Jesse Tijerina, Managing Director, Consulting Americas +1 281 752 3251 [email protected]

Transcript of IHS CHEMICAL TRENDS IN THE POLYMERS MARKET · TRENDS IN THE POLYMERS MARKET IHS CHEMICAL ... LLDPE...

© 2015 IHS

TRENDS IN THE POLYMERS MARKET

IHS CHEMICAL

Jesse Tijerina, Managing Director, Consulting Americas

+1 281 752 3251

© 2015 IHS

ENERGY

© 2015 IHS

Crude Production Is Expected to Exceed Market

Demand Through Mid 2016

A Period of Deflated Prices and Squeezed Chemical Margins

28

29

30

31

32

33

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

Q32016

Q42016

Call on OPEC crude OPEC crude production

OPEC balancing

Notes: Call on OPEC crude = total global liquids demand - non-OPEC liquids supply - OPEC condensate and NGL supply - processing gains - biofuel supply - other

liquids supply.

Source: IHS © 2015 IHS

Mil

lio

n b

arr

els

per

da

y

OPEC crude production

above the Call on OPEC

implies a build in global

inventories.

OPEC Quota Increasing Inventories

© 2015 IHS

After Falling from the Cliff, Crude Prices Are Expected

to Bottom at Turn of the Year

Dated Brent and other benchmark crude oil price outlook to 2016

0

20

40

60

80

100

120

140

Brent - WTI

Brent FOB

Dubai FOB

WTI Cushing

© 2015 IHS 5

Presentation Name / Month 2015

Demand improves with lower costs

Competitiveness increases profits as raw

material prices decline for some countries.

Market still focal point for growing North

American supply

Implications of low oil:

Latin America

© 2015 IHS

ECONOMY

© 2015 IHS. ALL RIGHTS RESERVED.

Latin America: Large market with 630 million consumers

of finished goods.

• Mid America: MEX, VEN, COL

• East of Andes: BRA, ARG

• Pacific Coast: CHL, PER

South

America

North

America

Economic

Disparity and Slow

GDP Growth 2015

Politically Stable

Compared to other

Regions

Large Population-

630 Million

Greatest Asset

© 2015 IHS

5.9

4.6

2.9 2.8

1.1

-0.4

0.3

1.9 2.5

3.0 3.1

4.3

3.2 2.6 2.5

2.7 2.5 3.0

3.3 3.3 3.4 3.5

-4.0

-1.5

1.0

3.5

6.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Latin America World USA

Economic Growth in Latin America

GDP Growth, %

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Argentina 9.5 8.4 0.8 2.9 0.5 1.6 0.6 1.5 2.3 2.3 2.5

Brazil 7.6 3.9 1.8 2.7 0.2 -3.0 -1.9 1.4 2.2 2.6 2.8

Chile 5.7 5.8 5.5 4.3 1.8 2.0 2.2 2.7 2.8 3.4 3.6

Colombia 4.0 6.6 4.0 4.9 4.6 2.5 2.4 2.7 2.6 3.1 3.2

Mexico 5.1 4.0 4.0 1.4 2.1 2.2 2.3 2.8 3.2 3.7 3.9

Peru 8.4 6.5 5.9 5.7 2.4 2.3 2.7 3.5 3.7 4.2 4.4

© 2015 IHS

Polymer Industry Overview

© 2015 IHS 10

Latin America’s plastics deficit continues

to increase

(3,500) (3,000) (2,500) (2,000) (1,500) (1,000) (500) -

PE

PP

PS

PVC

PET

2012 2013 2014

000 tons

© 2015 IHS

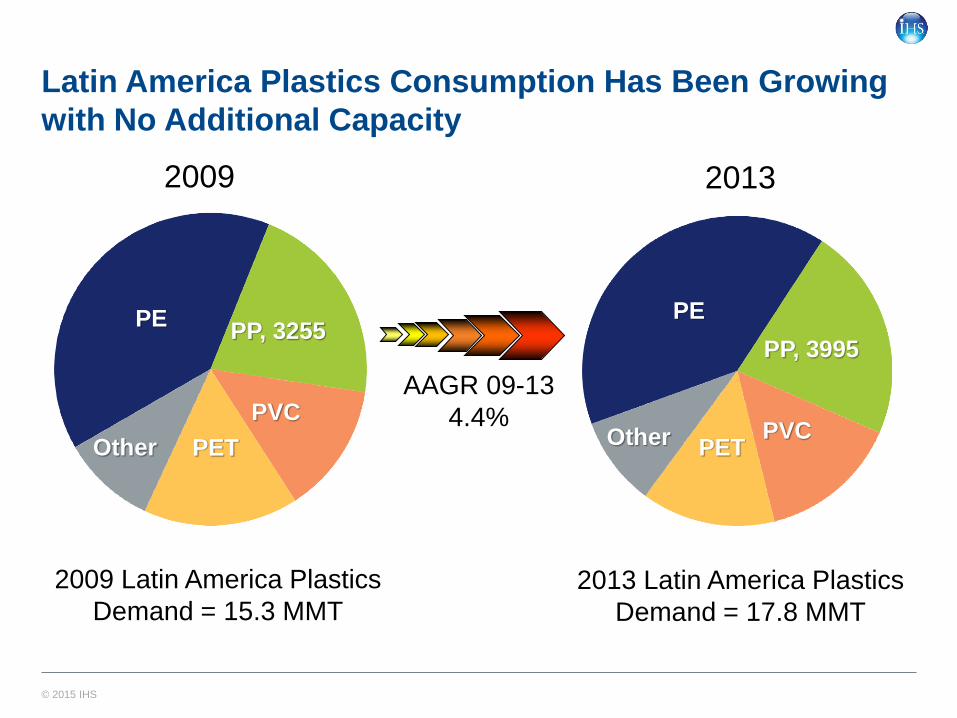

PE

PP, 3995

PVC PET Other

PE PP, 3255

PVC

PET Other

2009 2013

2009 Latin America Plastics

Demand = 15.3 MMT

2013 Latin America Plastics

Demand = 17.8 MMT

AAGR 09-13

4.4%

Latin America Plastics Consumption Has Been Growing

with No Additional Capacity

© 2015 IHS

PE PP

PVC

PET Other

PE PP

PVC

PET Other

2014 2020

2014 Latin America Plastics

Demand = 18.6 MMT

2020 Latin America Plastics

Demand = 22.7 MMT

AAGR 14-20

3.4%

Latin America Plastics Consumption:

Continue to Grow with limited Additional Capacity

© 2015 IHS

South America Will Be More Dependent on Polyethylene

Imports from North America

(Thousand Metric Tons)

*North America Includes Mexico

2010 2015 2020

North America

South America

PE PP

2706

2309

6665

-1352 -1779

-2628

© 2015 IHS

America’s Polyethylene Trade Balance

-8%

-4%

0%

4%

8%

12%

16%

20%

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

09 10 11 12 13 14 15 16 17 18 19 20

SAM Net Trade NAM Net Trade

Americas Net Trade Americas Net Trade as % of NAM Production

Americas PE Net Trade

Source: IHS © 2015 IHS

Ne

t T

rad

e, M

illio

n M

etr

ic T

on

s

Tra

de

as

a %

of

Pro

du

cti

on

By 2020…

HDPE ~15%

LLDPE ~20%

LDPE ~15%

© 2015 IHS

South America Polypropylene Demand and Imports Will

Increase

A Period of Deflated Prices and Squeezed Chemical Margins

(Thousand Metric Tons)

*North America Includes Mexico

2010 2015 2020

PP

North America

South America

523

1020

54

-214 -264

-447

© 2015 IHS

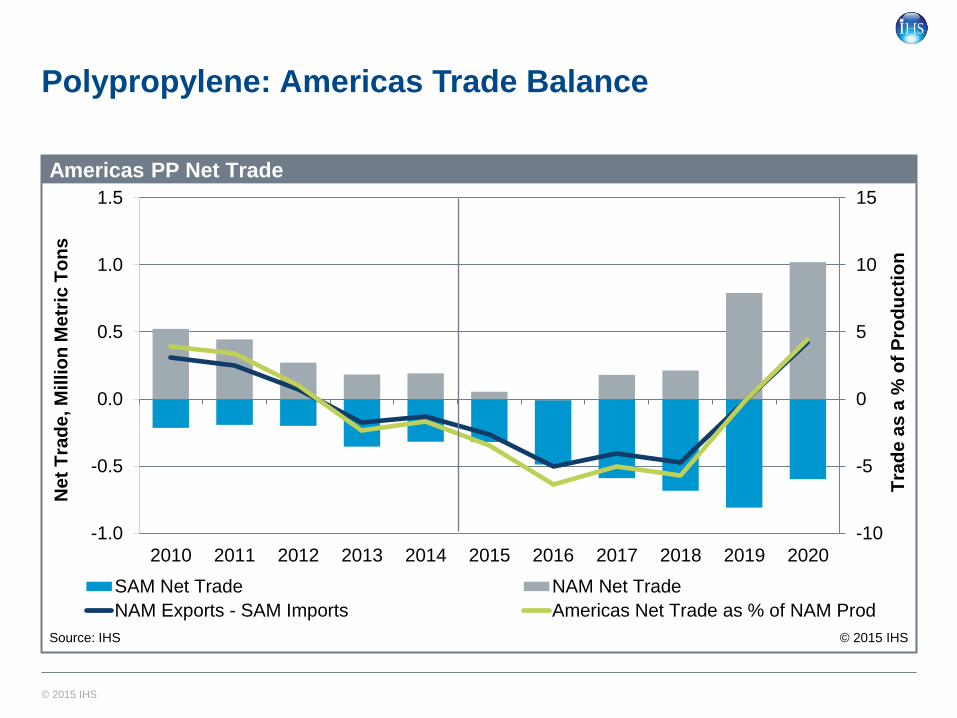

Polypropylene: Americas Trade Balance

-10

-5

0

5

10

15

-1.0

-0.5

0.0

0.5

1.0

1.5

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

SAM Net Trade NAM Net Trade

NAM Exports - SAM Imports Americas Net Trade as % of NAM Prod

Americas PP Net Trade

Source: IHS © 2015 IHS

Ne

t T

rad

e, M

illio

n M

etr

ic T

on

s

Tra

de

as

a %

of

Pro

du

cti

on

© 2015 IHS

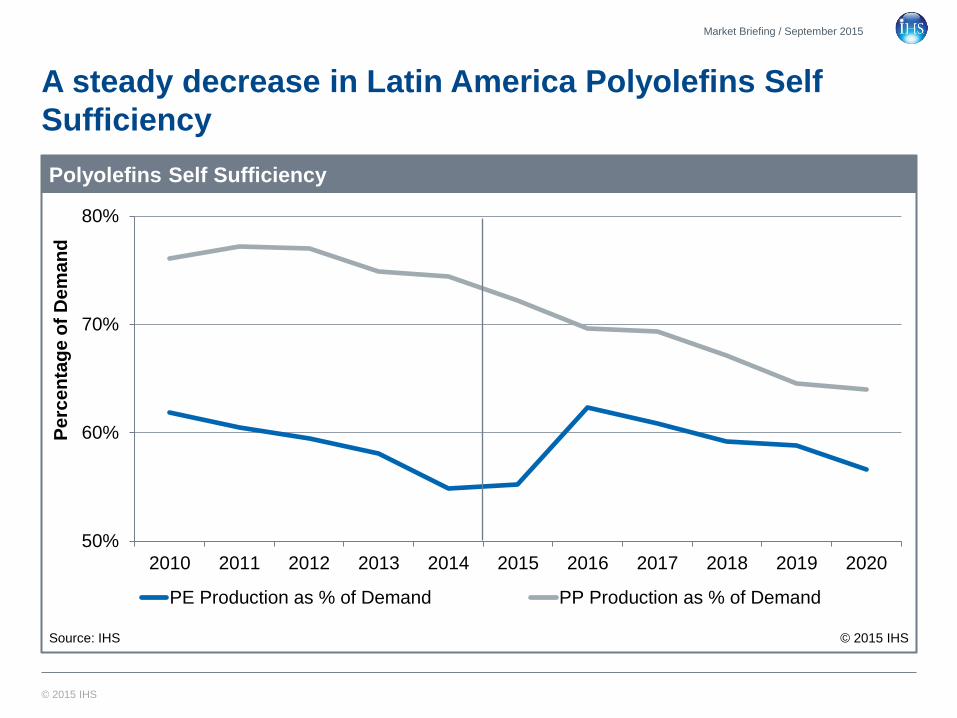

A steady decrease in Latin America Polyolefins Self

Sufficiency

Market Briefing / September 2015

50%

60%

70%

80%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

PE Production as % of Demand PP Production as % of Demand

Polyolefins Self Sufficiency

© 2015 IHS

Pe

rce

nta

ge

of

De

ma

nd

Source: IHS

© 2015 IHS

The story is the same in the other Latin America Plastics

Self-Sufficiency

Market Briefing / September 2015

70%

75%

80%

85%

90%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

PVC Production as % of Demand PS Production as % of Demand

PET Production as % of Demand

Plastics Self Sufficiency

© 2015 IHS

Pe

rce

nta

ge

of

De

ma

nd

Source: IHS

© 2015 IHS

Latin America did not make the Top 5 Countries Adding

Base Chemical Capacity 231 Million Tons from 2010 to 2020

Market Briefing / October 2015

0

20

40

60

80

100

120

China UnitedStates

SaudiArabia

S. Korea India

Chlorine Paraxylene Benzene

Methanol Propylene Ethylene

Million Metric Tons

Top five will add nearly 75%

of base chemical capacity.

China will dominate new

capacity, adding 45% of total

© 2015 IHS

COUNTRY OVERVIEW

© 2015 IHS

Venezuela

• Low crude oil prices and currency crisis

restricted availability of raw materials and

created scarcity of finished goods.

• Most affected by lower crude oil prices..

• Economic downturn and currency crisis

may lead to political unrests.

Colombia

• Ecopetrol focusing on completion of

Cartagena Refinery expansion by YE 2015.

• Economic growth will slow down, but will

still lead Latin America.

• Domestic demand for petrochemicals

increasing.

Mid America: Country Overview

Mexico

• Energy reform is opening new

possibilities. Foreign Direct Investment

will enter slowly.

• Lower electricity costs expected to

increase competitiveness as gas pipeline

carry cheap gas to Mexico.

• Etileno XXI startup end 2015 First new

capacity in North America.

• Demand recovering in 2016 amid lower

petrochemical prices.

© 2015 IHS

Mercosur: Country Overview

Brazil

• Brazil expected to contract by 3.0

• Low crude oil prices and scandals

related to corruption is keeping

investment low.

• Weaker Real slows down purchases

but makes local products more

attractive.

• Drought affecting power & gasoline

supply.

• Petrochemical Projects cancelled. No

Expansions through 2020.

Argentina

• Energy development continues with

focus on Vaca Muerta (Shale - NGL).

• GDP Contracted to nearly zero.

• Presidential elections this year.

Some changes may come after

elections.

• Dow and YPF working to increase

ethane supply to increase capacity in

Bahia Blanca.

© 2015 IHS

Pacific Coast: Country Overview

Chile

• Closure of small ENAP Ethylene &

Petro Dow PE units in Talcahuano in

2014.

• Slowdown in GDP growth from ~5.6%

2010-12 to ~2.2% in 2015-16.

• Increased availability of product from

North America and Asia will continue to

supply product to support local growth

in Chile.

• Convertors will benefit from additional

supply and growth will follow.

Peru

• 2014 was a challenging year for its

economy, but we expect a slight

recovery in 2015 GDP growth.

• Odebrecht awarded contract to build

gas pipeline from Camisea to

Southern Peru.

• This new gas pipeline could

stimulate a Petrochemical project in

the South of Peru.

© 2015 IHS

TRENDS

© 2015 IHS

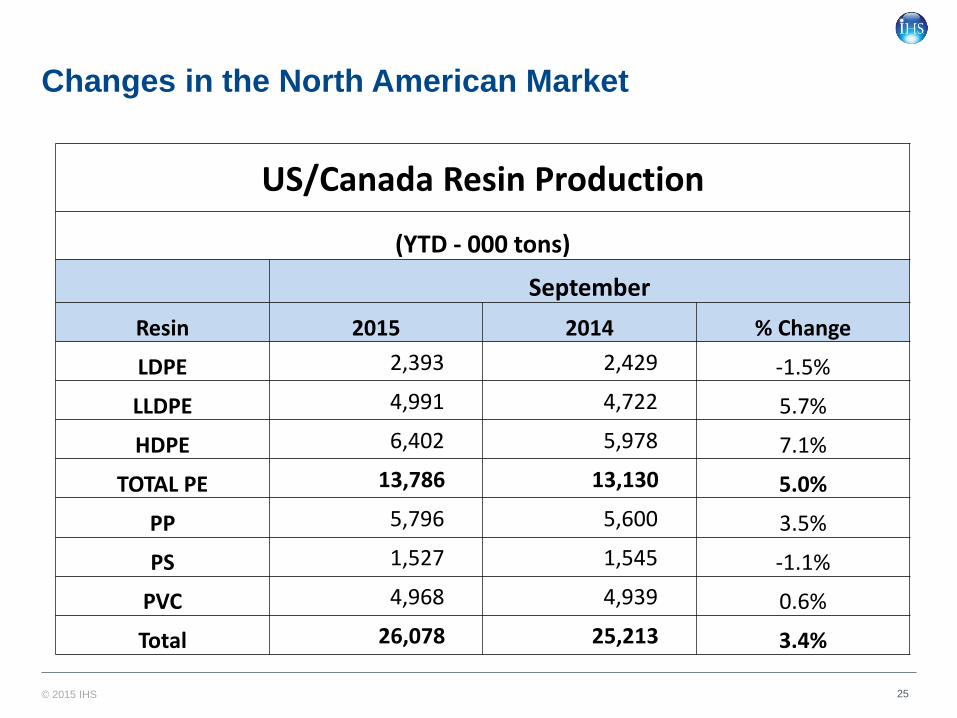

Changes in the North American Market

25

US/Canada Resin Production

(YTD - 000 tons)

September

Resin 2015 2014 % Change

LDPE 2,393 2,429 -1.5%

LLDPE 4,991 4,722 5.7%

HDPE 6,402 5,978 7.1%

TOTAL PE 13,786 13,130 5.0%

PP 5,796 5,600 3.5%

PS 1,527 1,545 -1.1%

PVC 4,968 4,939 0.6%

Total 26,078 25,213 3.4%

© 2015 IHS

Changes in the North American Market

26

US/Canada Resin Sales and Captive Use

(YTD - 000 tons)

September

Resin 2015 2014 % Change

LDPE 2,435 2,392 1.8%

LLDPE 4,971 4,726 5.2%

HDPE 6,364 6,025 5.6%

TOTAL PE 13,770 13,143 4.8%

PP 5,869 5,597 4.9%

PS 1,509 1,523 -0.9%

PVC 3,190 3,171 0.6%

Total 24,338 23,435 3.9%

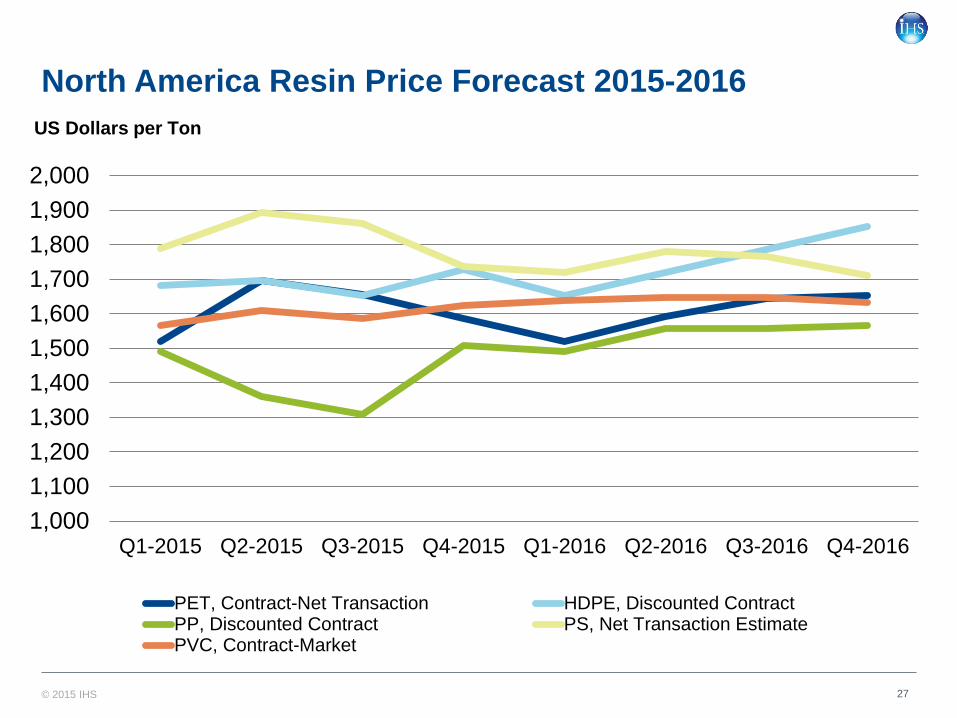

© 2015 IHS 27

North America Resin Price Forecast 2015-2016

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

Q1-2015 Q2-2015 Q3-2015 Q4-2015 Q1-2016 Q2-2016 Q3-2016 Q4-2016

PET, Contract-Net Transaction HDPE, Discounted ContractPP, Discounted Contract PS, Net Transaction EstimatePVC, Contract-Market

US Dollars per Ton

© 2015 IHS 28

North America Resins Market Outlook Short Term.

NORTH AMERICA RESIN HIGHLIGHTS Demand Price

PE

Contract PE prices appear to be heading for a flat settlement in October. PE producers have

moved the previously announced five cent contract price increase out to November 1. The

proposed November increase is likely to face stiff opposition. Product availability remains

sufficient and buyers do not appear to be pre buying ahead of the proposed November

increase.

↔ ↔

PP Demand continues to outpace supply despite very strong year to date operating rates.

Several industry outages are expected to keep market dynamics very tight and likely allow

for further margin expansion in the fourth quarter. ↔ ↗

PS

Price for all grades of PS are likely to roll over in October. With benzene spot prices for

November currently close to the October contract price level, the current IHS forecast for PS

prices in November is for another rollover. Demand in September increased slightly mainly

due to lower prices. Demand in October should be healthy before seeing a seasonal

slowdown in November/ December.

↔ ↔

PVC

Domestic contract PVC prices are likely to see a further downward movement in October.

Soft regional ethylene prices in combination with soft resin export prices are increasing

pressure on domestic PVC producers to narrow the gap between export and domestic

contract pricing. Planned vinyls turnarounds this month have helped to balance the current

softness in the domestic market.

↔ ↘

PET October raw material costs remain unsettled but we expect them to decrease around 1 cpp.

November raws costs look to be relatively flat. Demand is slow though recent preliminary

antidumping duties could slow imports and help domestic demand ↔ ↘

© 2015 IHS. ALL RIGHTS RESERVED.

Increase in Domestic Demand Without Capacity Growth

• With no new capacity additions and increase in

demand, S. American net imports of Polymers will

continue to increase

• No new ethylene or propylene capacity additions in S.

America prior to 2020

• Mexico and US will add significant new ethane

cracking capacity, targeting PE exports to S. America

• NGL production additions from Vaca Muerta

(Argentina), Gran Chaco (Bolivia) and Pre-Salt (Brazil)

may stimulate future capacity additions

• The Southern Gas Pipeline Project (Peru) could also

stimulate a Petrochemical project in the South of Peru

• The region has ample room for several world scale

polyolefin complexes. Who is going to build it?

© 2015 IHS

IHS - Leveraging expertise across industries to provide custom solutions

30

AEROSPACE & DEFENSE

100+ years’ experience

delivering unrivaled news,

insight and intelligence on

defense and security

equipment, markets,

industries and risk

CHEMICAL

Over 200 leading industry authorities creating integrated views and analysis across more than 300 chemical markets and 2,000 processes for 95 industries

FINANCE

Research on 200+

countries and territories

with harmonized indicators

from IHS analysts and

economists

TECHNOLOGY

World’s largest

electronics component

database with more than

350 million parts

AUTOMOTIVE

The world’s largest team

of automotive analysts with

hundreds of experts located

in 15 key markets around

the world covering the entire

automotive value chain

ENERGY

Extensive Oil & Gas well

information on 5.5+ million

wells worldwide dating

back as far as 1860

MARITIME

World’s largest maritime

database with an

information gathering

heritage of 250+ years with

comprehensive information

on all vessels 100 GT and

over

© 2015 IHS

• Technical + Specialties

• World’s leading business research & forecasting service

• Provider of chemical process economics for the global chemical industry

• Trusted authority on chlor-alkali, vinyl chloride, and bleaching chemicals

• Market and pricing data

• 100-year information supplier

• Authoritative chemical business news

• Information resource for high-level industry executives & professionals

• Commercial + Strategic

• Market planning & consulting advisory services

• Analytical & technical expertise

Best-in-class brands brought together

IHS Chemical

© 2015 IHS

Connecting to the whole IHS family

Advancing decisions that advance the world

32

Agricultur

e

Electroni

cs &

Telecom

Governmen

t

Metals

&

Mining

Healthcare

Financial

Military

&

Security

Chemicals

Automotiv

e

Energy

Coal

Transportatio

n

Shippin

g

Aerospac

e &

Defense

Constructi

on

Power &

Utilities

Energy

Oil &

Gas

Consume

r

& Retail