IFX Day 2011 - Infineon

25

Page 1 Copyright © Infineon Technologies 2011. All rights reserved. IFX Day 2011 Campeon – 07 June 2011 Dominik Asam Member of the Management Board Chief Financial Officer

Transcript of IFX Day 2011 - Infineon

Page 1Copyright © Infineon Technologies 2011. All rights reserved.

IFX Day 2011Campeon – 07 June 2011

Dominik AsamMember of the Management BoardChief Financial Officer

Page 2Copyright © Infineon Technologies 2011. All rights reserved.

Table of Contents

07 June 2011

Introduction

Explaining the Target Operating Model

FX, Interest, Tax and Working Capital

Investments and D&A

Capital Structure and Use of Cash

Summary

Page 3Copyright © Infineon Technologies 2011. All rights reserved.

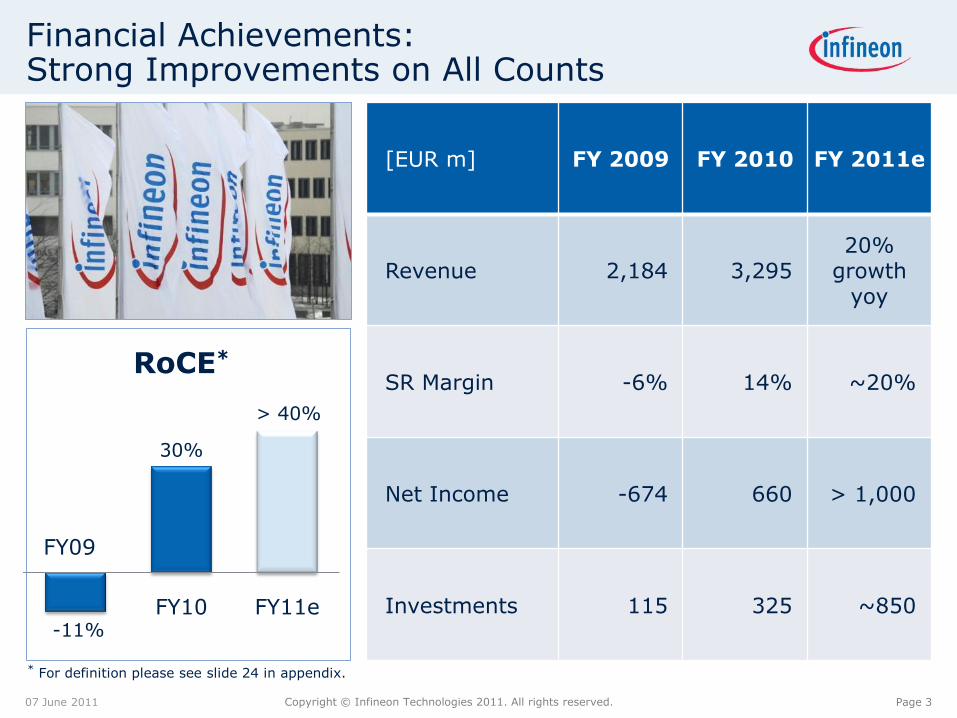

Financial Achievements:Strong Improvements on All Counts

07 June 2011

-11%

30%

FY10 FY11e

RoCE*

[EUR m] FY 2009 FY 2010 FY 2011e

Revenue 2,184 3,29520%

growthyoy

SR Margin -6% 14% ~20%

Net Income -674 660 > 1,000

Investments 115 325 ~850

FY09

> 40%

* For definition please see slide 24 in appendix.

Page 4Copyright © Infineon Technologies 2011. All rights reserved.

Table of Contents

07 June 2011

Introduction

Explaining the Target Operating Model

FX, Interest, Tax and Working Capital

Investments and D&A

Capital Structure and Use of Cash

Summary

Page 5Copyright © Infineon Technologies 2011. All rights reserved.

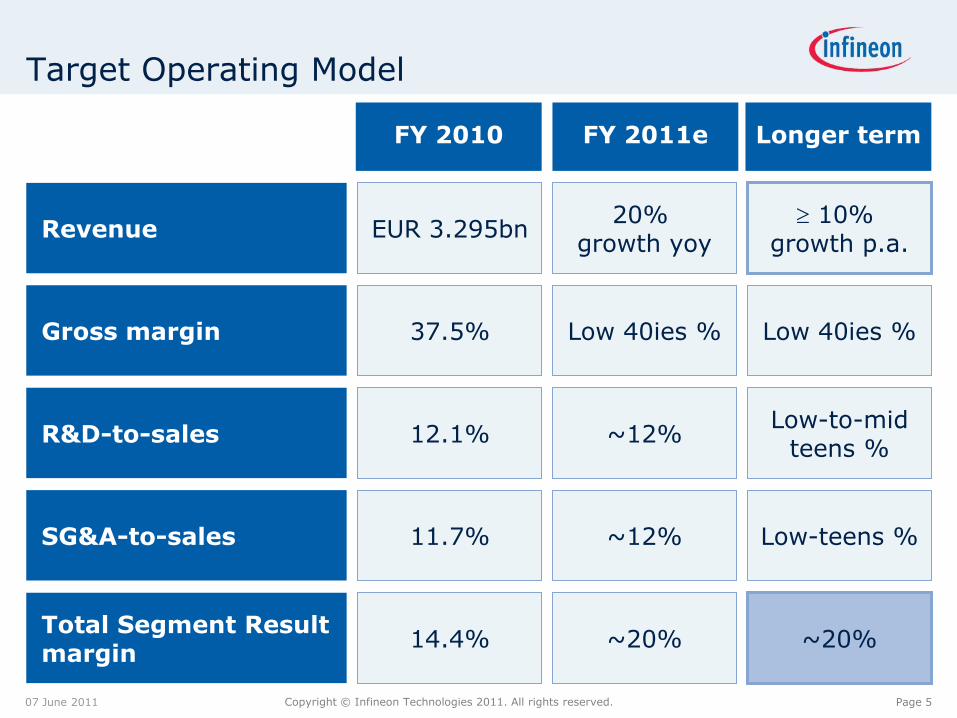

Target Operating Model

07 June 2011

Revenue

Gross margin

R&D-to-sales

SG&A-to-sales

Total Segment Result margin

14.4%

FY 2010 FY 2011e Longer term

EUR 3.295bn

37.5%

12.1%

11.7%

20% growth yoy

Low 40ies %

~12%

~12%

~20%

10% growth p.a.

Low 40ies %

Low-to-midteens %

Low-teens %

~20%

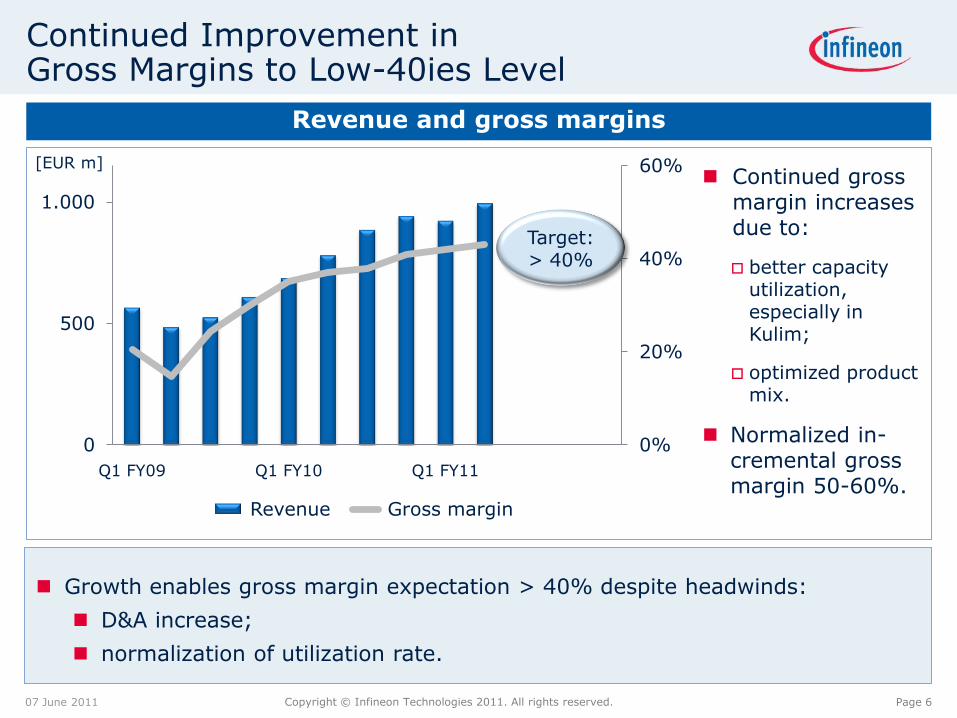

Page 6Copyright © Infineon Technologies 2011. All rights reserved.

0%

20%

40%

60%

0

500

1.000

Q1 FY09 Q1 FY10 Q1 FY11

Revenue Gross margin

Continued Improvement inGross Margins to Low-40ies Level

07 June 2011

Revenue and gross margins

[EUR m]

Growth enables gross margin expectation > 40% despite headwinds:

D&A increase;

normalization of utilization rate.

Continued grossmargin increasesdue to:

better capacityutilization, especially in Kulim;

optimized productmix.

Normalized in-cremental grossmargin 50-60%.

Target:> 40%

Page 7Copyright © Infineon Technologies 2011. All rights reserved.

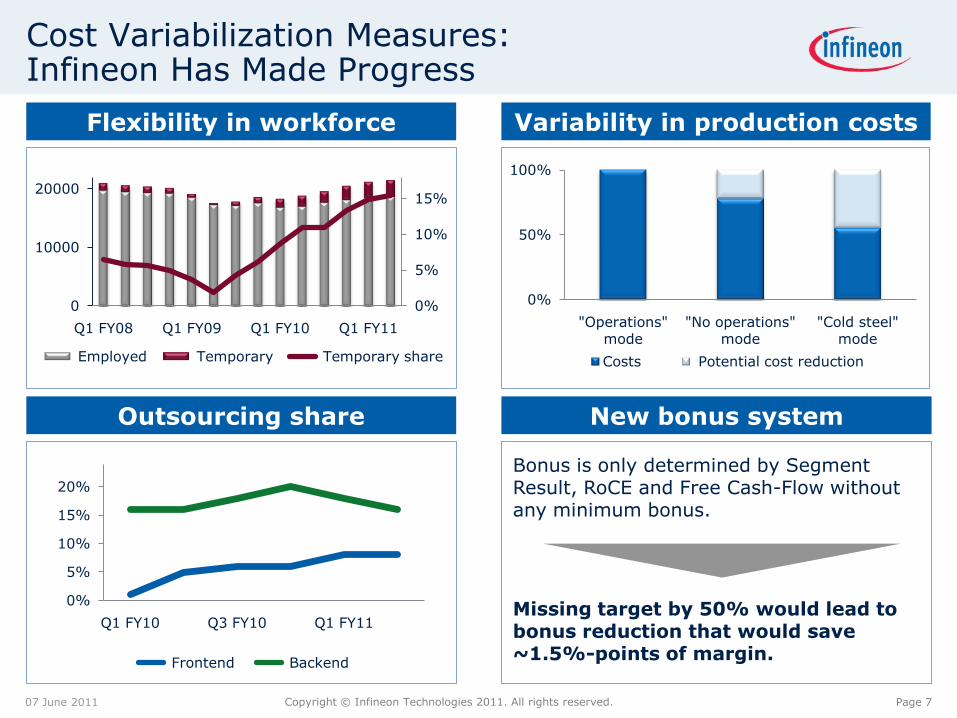

Cost Variabilization Measures:Infineon Has Made Progress

07 June 2011

Flexibility in workforce

Bonus is only determined by Segment Result, RoCE and Free Cash-Flow without any minimum bonus.

Missing target by 50% would lead to bonus reduction that would save ~1.5%-points of margin.

Variability in production costs

Outsourcing share New bonus system

0%

5%

10%

15%

0

10000

20000

Q1 FY08 Q1 FY09 Q1 FY10 Q1 FY11

Employed Temporary Temporary share

0%

50%

100%

"Operations"mode

"No operations"mode

"Cold steel"mode

Costs Potential cost reduction

0%

5%

10%

15%

20%

Q1 FY10 Q3 FY10 Q1 FY11

Frontend Backend

Page 8Copyright © Infineon Technologies 2011. All rights reserved.

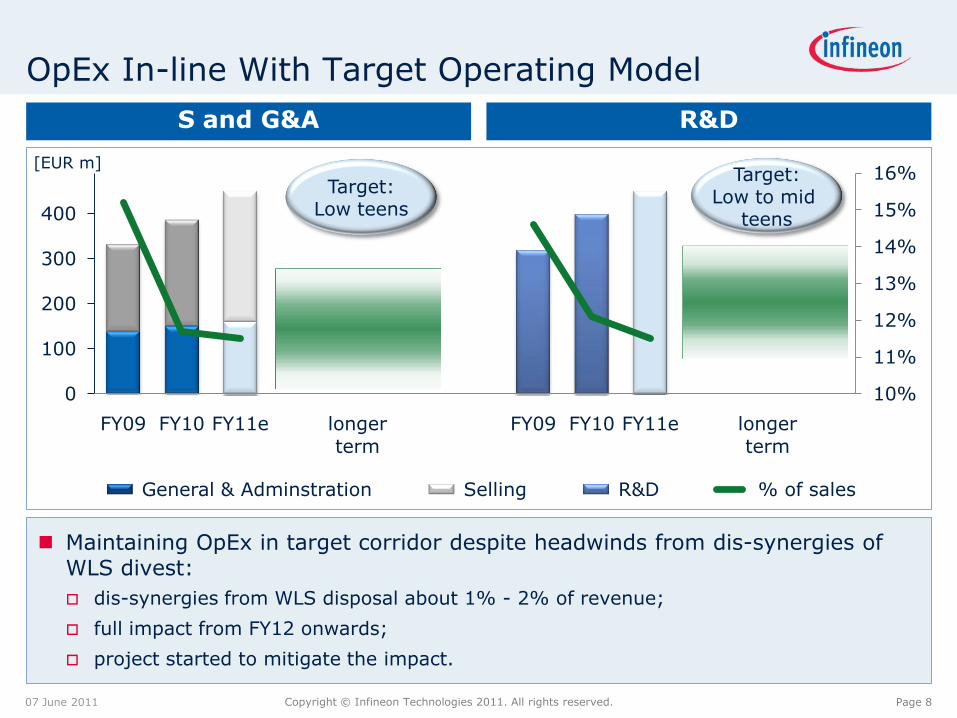

10%

11%

12%

13%

14%

15%

16%

0

100

200

300

400

FY09 FY10 FY11e longer term

FY09 FY10 FY11e longer term

General & Adminstration Selling R&D % of sales

OpEx In-line With Target Operating Model

07 June 2011

S and G&A R&D

[EUR m]

Maintaining OpEx in target corridor despite headwinds from dis-synergies of WLS divest:

dis-synergies from WLS disposal about 1% - 2% of revenue;

full impact from FY12 onwards;

project started to mitigate the impact.

Target:Low to mid

teens

Target:Low teens

Page 9Copyright © Infineon Technologies 2011. All rights reserved.

Table of Contents

07 June 2011

Introduction

Explaining the Target Operating Model

FX, Interest, Tax and Working Capital

Investments and D&A

Capital Structure and Use of Cash

Summary

Page 10Copyright © Infineon Technologies 2011. All rights reserved.

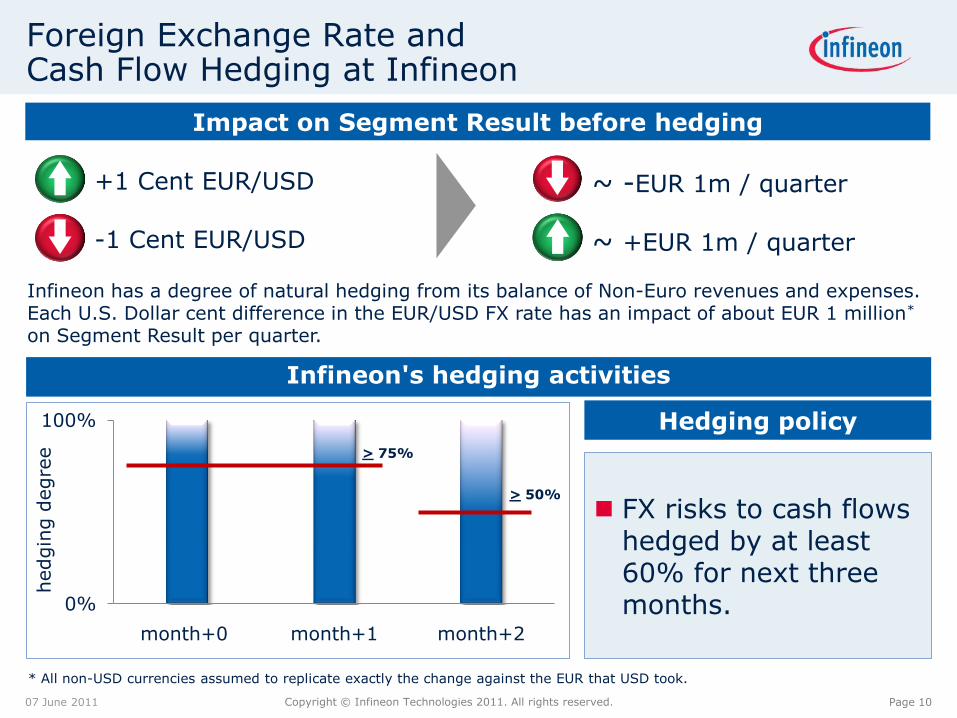

0%

100%

month+0 month+1 month+2

Foreign Exchange Rate and Cash Flow Hedging at Infineon

07 June 2011

Infineon's hedging activities

Impact on Segment Result before hedging

FX risks to cash flowshedged by at least 60% for next threemonths.

Infineon has a degree of natural hedging from its balance of Non-Euro revenues and expenses. Each U.S. Dollar cent difference in the EUR/USD FX rate has an impact of about EUR 1 million*

on Segment Result per quarter.

+1 Cent EUR/USD ~ -EUR 1m / quarter

-1 Cent EUR/USD ~ +EUR 1m / quarter

hedgin

gdegre

e

> 50%

> 75%

Hedging policy

* All non-USD currencies assumed to replicate exactly the change against the EUR that USD took.

Page 11Copyright © Infineon Technologies 2011. All rights reserved.

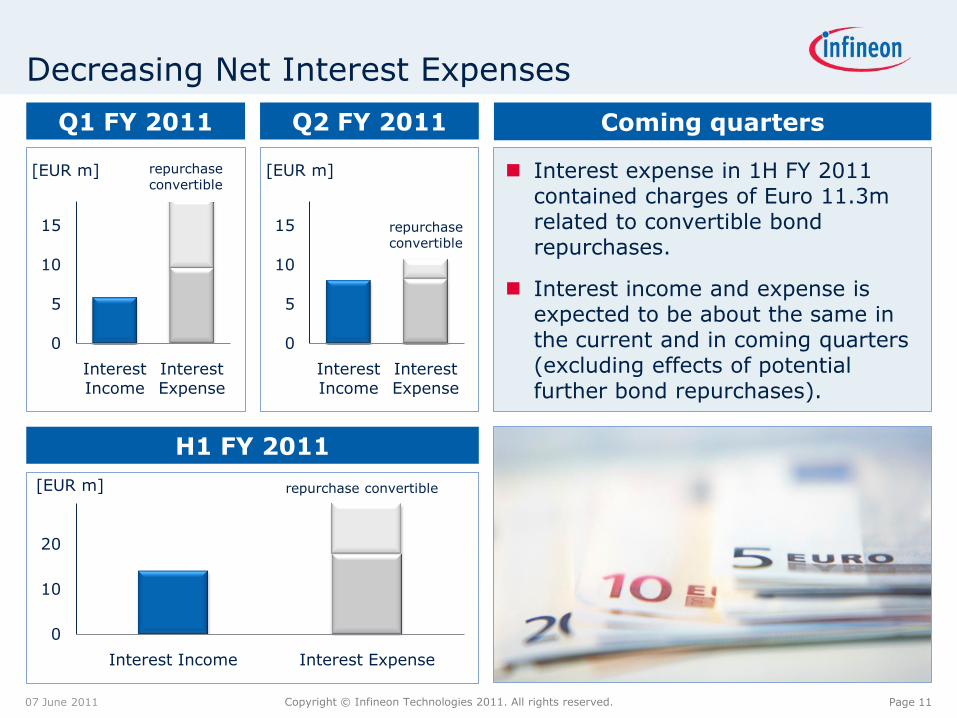

Q1 FY 2011 Coming quarters

Interest expense in 1H FY 2011 contained charges of Euro 11.3m related to convertible bondrepurchases.

Interest income and expense isexpected to be about the same in the current and in coming quarters(excluding effects of potential further bond repurchases).

Decreasing Net Interest Expenses

07 June 2011

[EUR m]

0

5

10

15

Interest Income

Interest Expense

Q2 FY 2011

0

5

10

15

Interest Income

Interest Expense

H1 FY 2011

0

10

20

Interest Income Interest Expense

[EUR m]

[EUR m] repurchase convertible

repurchaseconvertible

repurchaseconvertible

Page 12Copyright © Infineon Technologies 2011. All rights reserved.

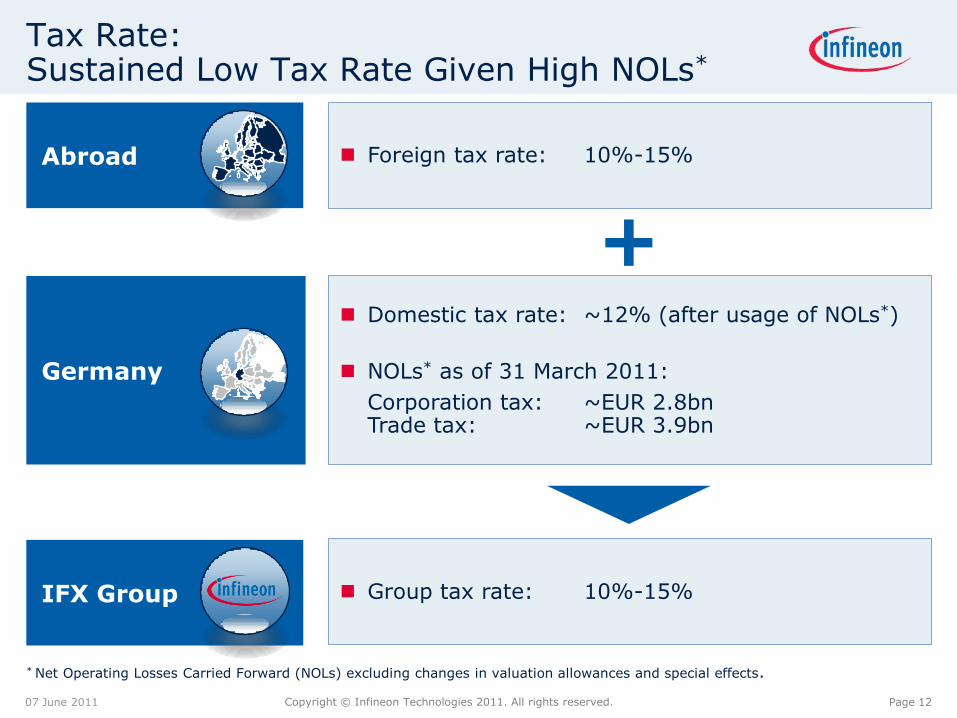

IFX Group

Germany

Abroad

Domestic tax rate: ~12% (after usage of NOLs*)

NOLs* as of 31 March 2011:

Corporation tax: ~EUR 2.8bnTrade tax: ~EUR 3.9bn

* Net Operating Losses Carried Forward (NOLs) excluding changes in valuation allowances and special effects.

Tax Rate:Sustained Low Tax Rate Given High NOLs*

07 June 2011

Foreign tax rate: 10%-15%

+

Group tax rate: 10%-15%

Page 13Copyright © Infineon Technologies 2011. All rights reserved.

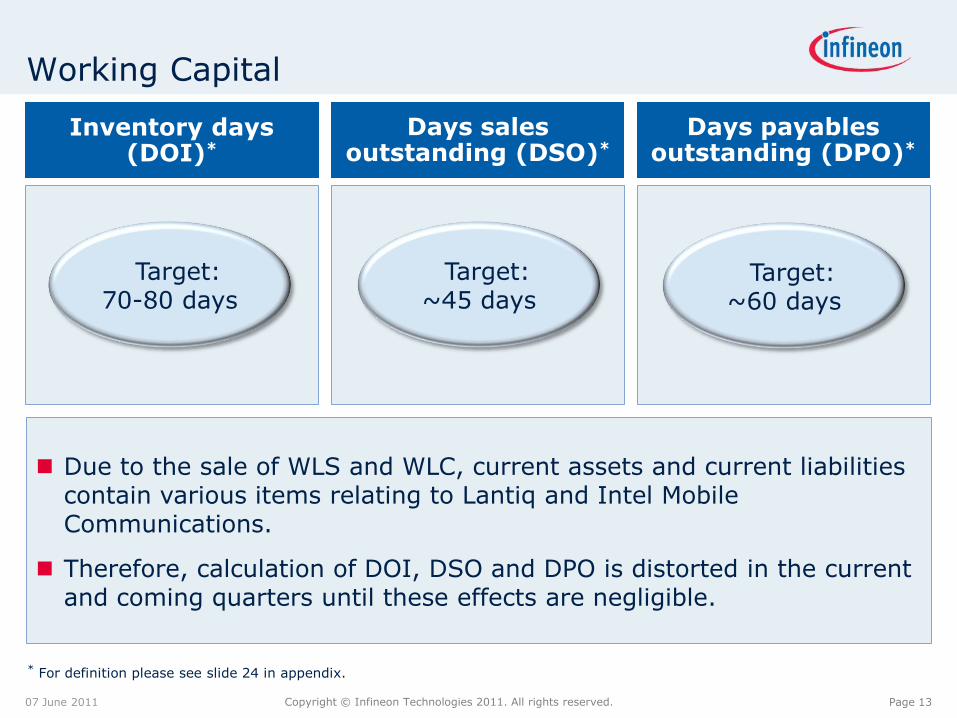

Working Capital

07 June 2011

16% 16% 17% 17% 19%

25% 25%24%22%18%

10% 13%10%5%3%

Due to the sale of WLS and WLC, current assets and current liabilitiescontain various items relating to Lantiq and Intel Mobile Communications.

Therefore, calculation of DOI, DSO and DPO is distorted in the currentand coming quarters until these effects are negligible.

Inventory days (DOI)*

Days payables outstanding (DPO)*

Target:70-80 days

Target:~45 days

Target:~60 days

Days sales outstanding (DSO)*

* For definition please see slide 24 in appendix.

Page 14Copyright © Infineon Technologies 2011. All rights reserved.

Table of Contents

07 June 2011

Introduction

Explaining the Target Operating Model

FX, Interest, Tax and Working Capital

Capital Structure and Use of Cash

Summary

Investments and D&A

Page 15Copyright © Infineon Technologies 2011. All rights reserved.

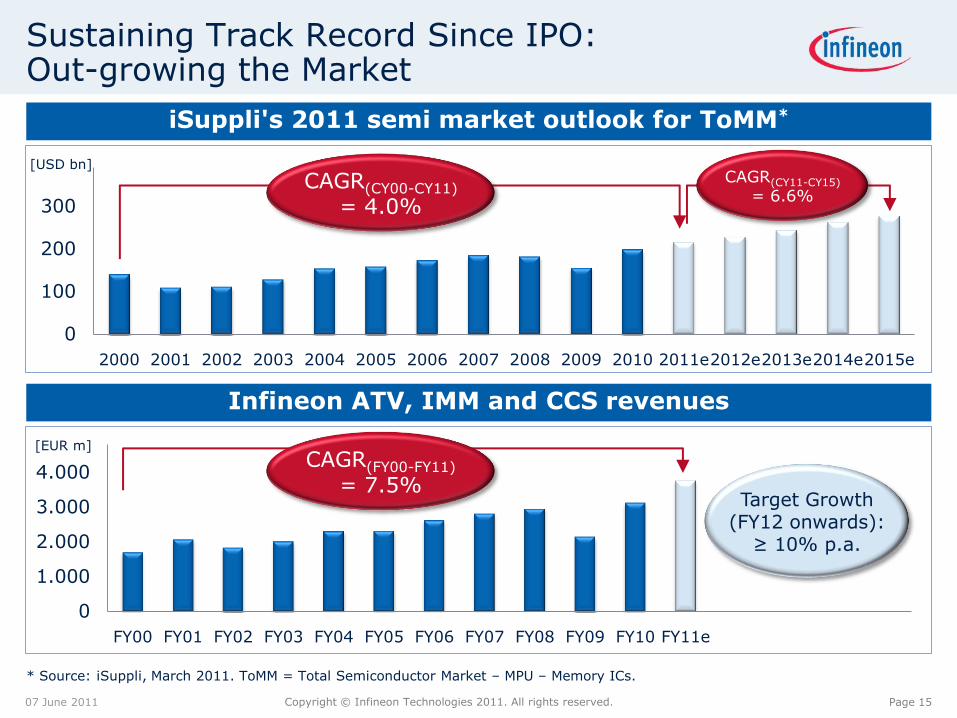

Sustaining Track Record Since IPO:Out-growing the Market

07 June 2011

* Source: iSuppli, March 2011. ToMM = Total Semiconductor Market – MPU – Memory ICs.

0

100

200

300

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011e2012e2013e2014e2015e

0

1.000

2.000

3.000

4.000

FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11e

iSuppli's 2011 semi market outlook for ToMM*

Infineon ATV, IMM and CCS revenues

[USD bn]

[EUR m]

Target Growth(FY12 onwards):

≥ 10% p.a.

CAGR(CY00-CY11)

= 4.0%

CAGR(CY11-CY15)

= 6.6%

CAGR(FY00-FY11)

= 7.5%

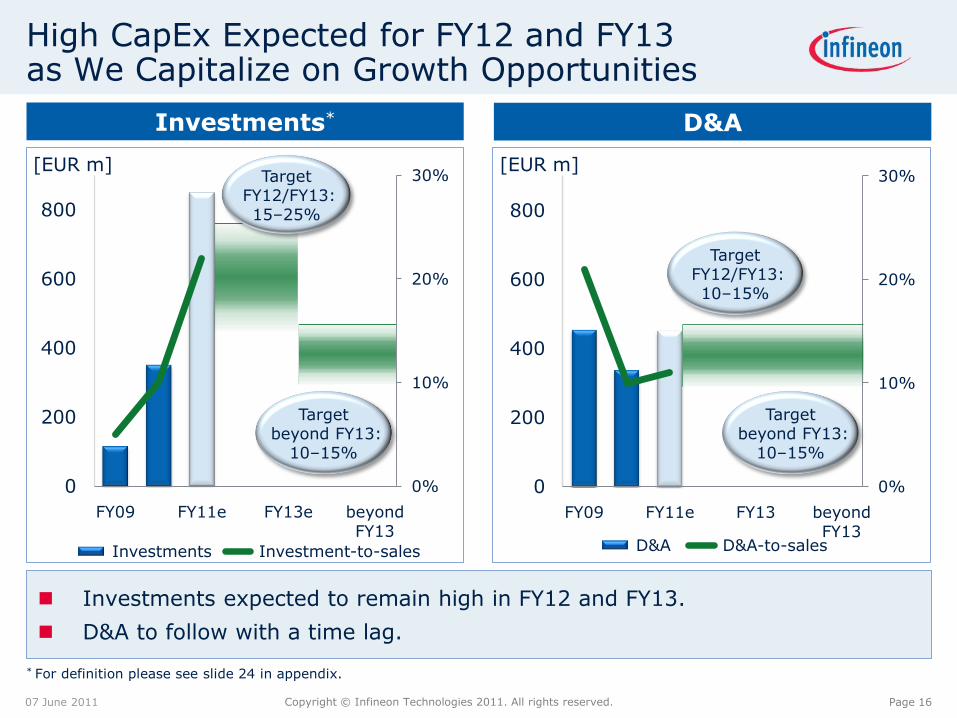

Page 16Copyright © Infineon Technologies 2011. All rights reserved.

0%

10%

20%

30%

0

200

400

600

800

FY09 FY11e FY13e beyond FY13

Investments Investment-to-sales

0%

10%

20%

30%

0

200

400

600

800

FY09 FY11e FY13 beyond FY13

D&A D&A-to-sales

High CapEx Expected for FY12 and FY13 as We Capitalize on Growth Opportunities

07 June 2011

* For definition please see slide 24 in appendix.

D&A

[EUR m]

Investments*

[EUR m]

Targetbeyond FY13:

10–15%

Targetbeyond FY13:

10–15%

TargetFY12/FY13:10–15%

Investments expected to remain high in FY12 and FY13.

D&A to follow with a time lag.

TargetFY12/FY13:15–25%

Page 17Copyright © Infineon Technologies 2011. All rights reserved.

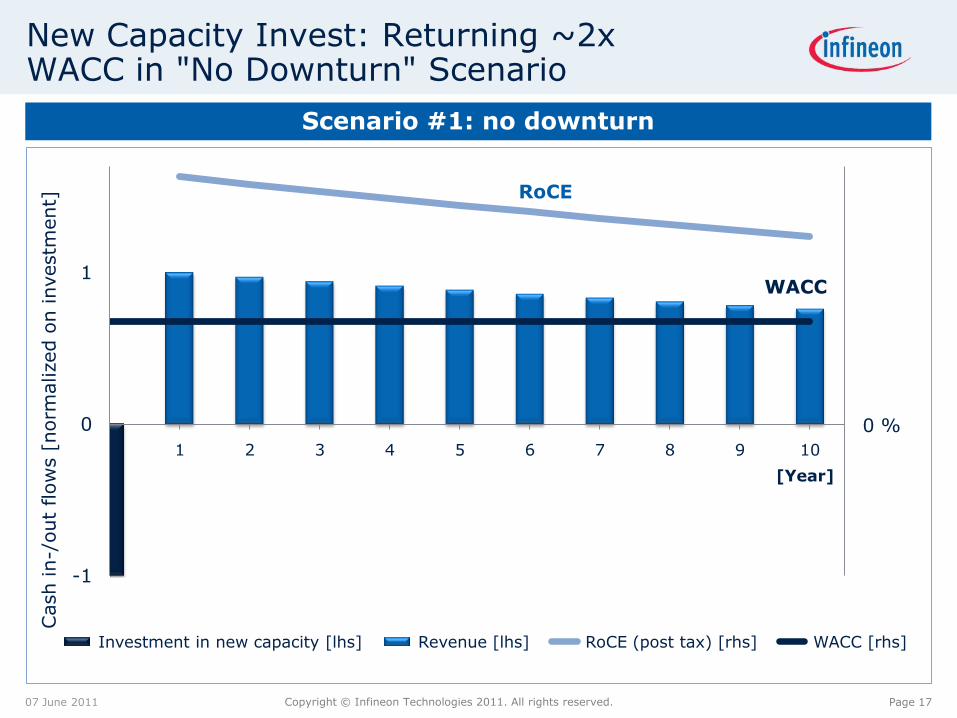

New Capacity Invest: Returning ~2x WACC in "No Downturn" Scenario

07 June 2011

-1

0

1

1 2 3 4 5 6 7 8 9 10

Investment in new capacity [lhs] Revenue [lhs] RoCE (post tax) [rhs] WACC [rhs]

Cash in-/

out

flow

s[n

orm

alized

on investm

ent]

Scenario #1: no downturn

WACC

RoCE

0 %

[Year]

Page 18Copyright © Infineon Technologies 2011. All rights reserved.

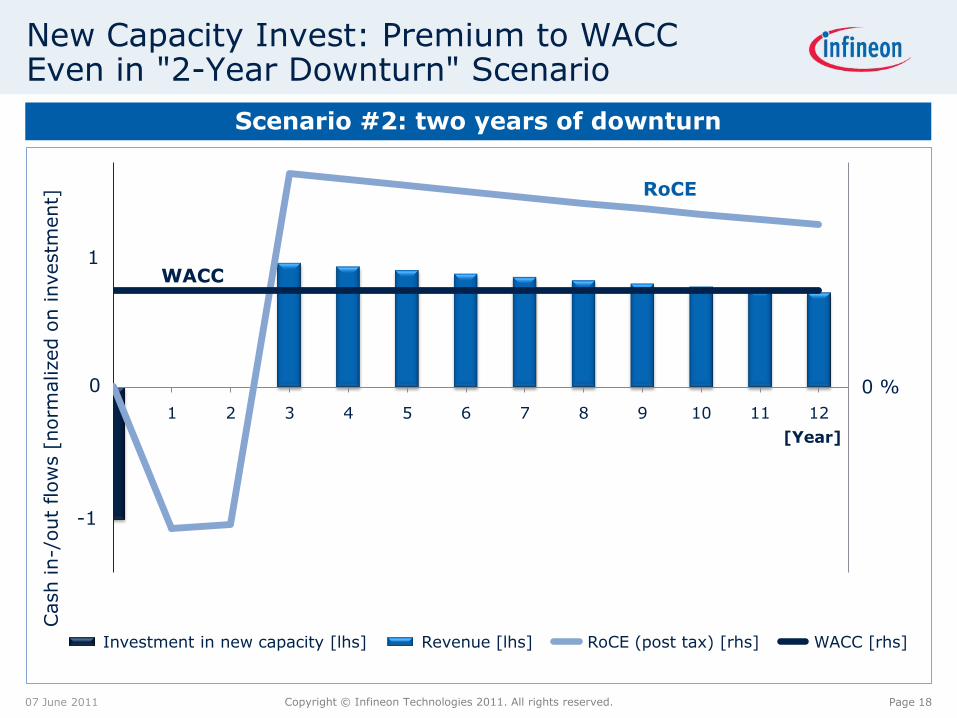

New Capacity Invest: Premium to WACC Even in "2-Year Downturn" Scenario

1 2 3 4 5 6 7 8 9 10 11 12

Investment in new capacity [lhs] Revenue [lhs] RoCE (post tax) [rhs] WACC [rhs]

Scenario #2: two years of downturn

WACC

-1

1

0 %0

[Year]

RoCE

Cash in-/

out

flow

s[n

orm

alized

on investm

ent]

07 June 2011

Page 19Copyright © Infineon Technologies 2011. All rights reserved.

Table of Contents

07 June 2011

Introduction

Explaining the Target Operating Model

FX, Interest, Tax and Working Capital

Investments and D&A

Summary

Capital Structure and Use of Cash

Page 20Copyright © Infineon Technologies 2011. All rights reserved.

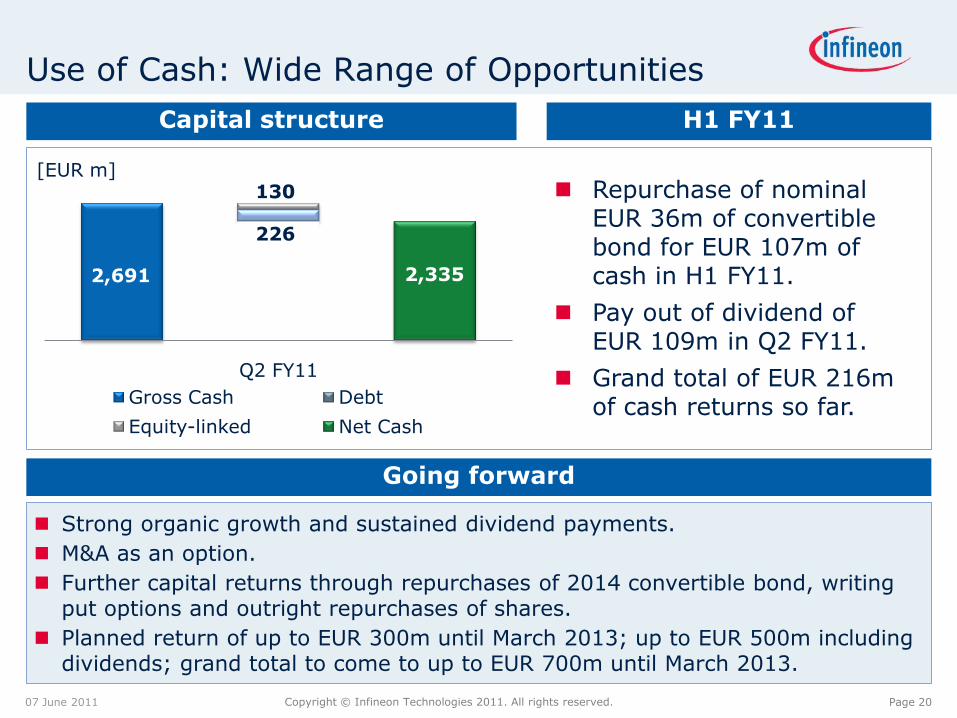

Use of Cash: Wide Range of Opportunities

07 June 2011

Going forward

H1 FY11Capital structure

2335

226

130

Q2 FY11

Gross Cash Debt

Equity-linked Net Cash

[EUR m] Repurchase of nominal

EUR 36m of convertible bond for EUR 107m of cash in H1 FY11.

Pay out of dividend ofEUR 109m in Q2 FY11.

Grand total of EUR 216m of cash returns so far.

Strong organic growth and sustained dividend payments.

M&A as an option.

Further capital returns through repurchases of 2014 convertible bond, writingput options and outright repurchases of shares.

Planned return of up to EUR 300m until March 2013; up to EUR 500m includingdividends; grand total to come to up to EUR 700m until March 2013.

2,691 2,335

Page 21Copyright © Infineon Technologies 2011. All rights reserved.

Table of Contents

07 June 2011

Introduction

Explaining the Target Operating Model

FX, Interest, Tax and Working Capital

Summary

Investments and D&A

Capital Structure and Use of Cash

Page 22Copyright © Infineon Technologies 2011. All rights reserved.

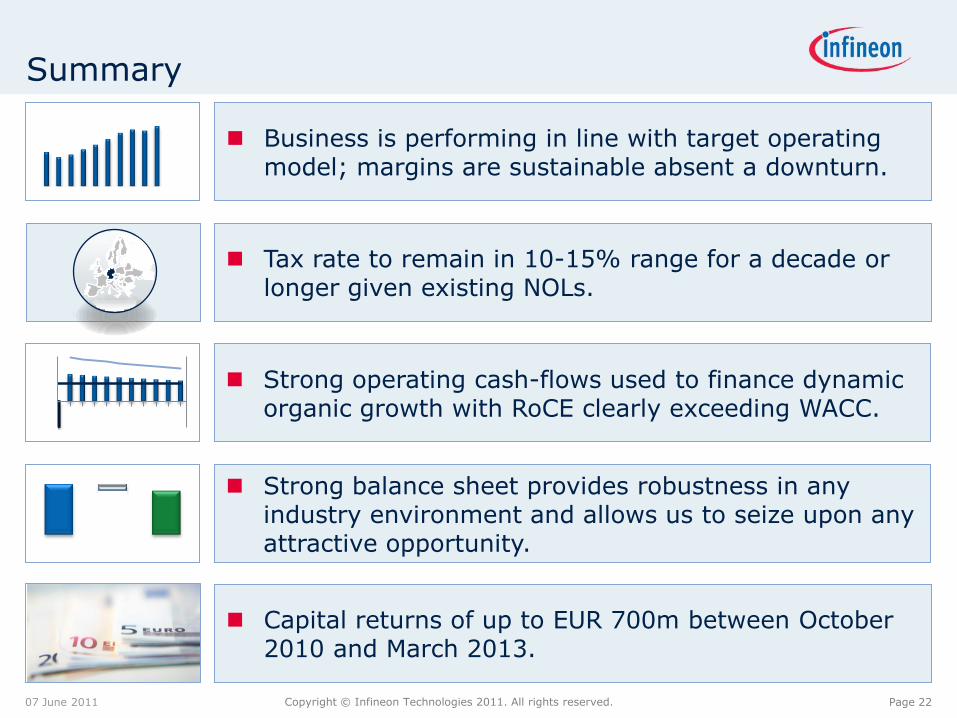

Summary

07 June 2011

Business is performing in line with target operating model; margins are sustainable absent a downturn.

Strong balance sheet provides robustness in any industry environment and allows us to seize upon any attractive opportunity.

Strong operating cash-flows used to finance dynamic organic growth with RoCE clearly exceeding WACC.

Tax rate to remain in 10-15% range for a decade or longer given existing NOLs.

Capital returns of up to EUR 700m between October2010 and March 2013.

-1

0

1

Page 24Copyright © Infineon Technologies 2011. All rights reserved.

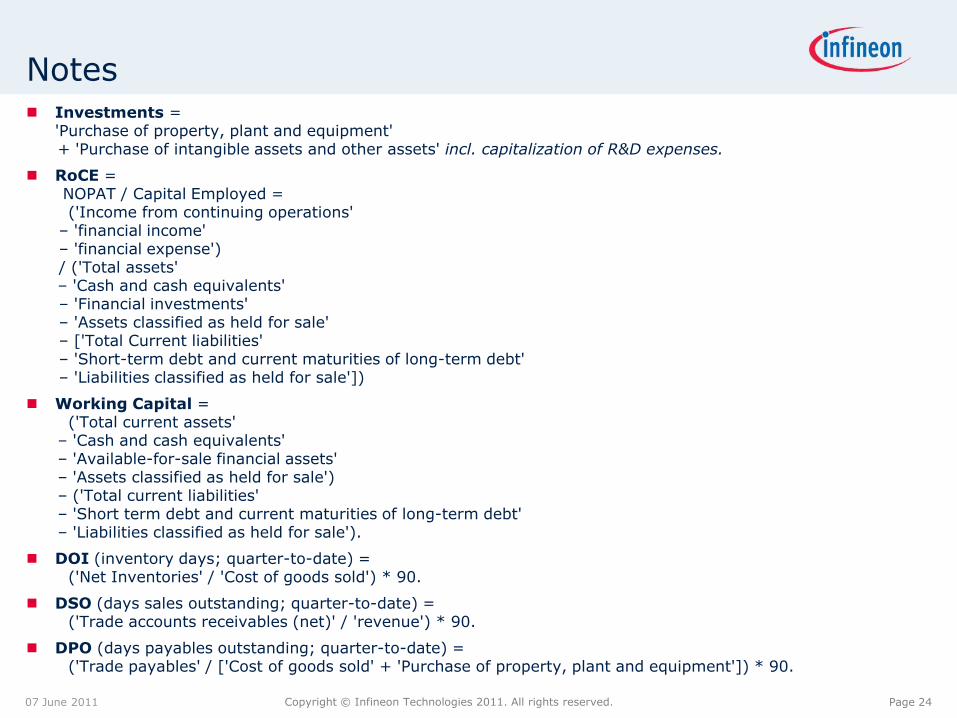

Notes

07 June 2011

Investments = 'Purchase of property, plant and equipment'+ 'Purchase of intangible assets and other assets' incl. capitalization of R&D expenses.

RoCE =NOPAT / Capital Employed = ('Income from continuing operations'

– 'financial income'– 'financial expense')/ ('Total assets'– 'Cash and cash equivalents'– 'Financial investments'– 'Assets classified as held for sale'– ['Total Current liabilities'– 'Short-term debt and current maturities of long-term debt'– 'Liabilities classified as held for sale'])

Working Capital =('Total current assets'

– 'Cash and cash equivalents'– 'Available-for-sale financial assets'– 'Assets classified as held for sale')– ('Total current liabilities'– 'Short term debt and current maturities of long-term debt'– 'Liabilities classified as held for sale').

DOI (inventory days; quarter-to-date) = ('Net Inventories' / 'Cost of goods sold') * 90.

DSO (days sales outstanding; quarter-to-date) = ('Trade accounts receivables (net)' / 'revenue') * 90.

DPO (days payables outstanding; quarter-to-date) = ('Trade payables' / ['Cost of goods sold' + 'Purchase of property, plant and equipment']) * 90.

Page 25Copyright © Infineon Technologies 2011. All rights reserved.

Disclaimer

This presentation was prepared as of June 7, 2011 and is current only as of that date.

This presentation includes forward-looking statements and assumptions about the future of Infineon's business and the industry in which we operate. These include statements and assumptions relating to general economic conditions, future developments in the world semiconductor market, our ability to manage our costs and to achieve our growth targets, the resolution of Qimonda's insolvency proceedings and the liabilities we may face as a result of Qimonda's insolvency the benefits of research and development alliances and activities, our planned levels of future investment, the introduction of new technology at our facilities, our continuing ability to offer commercially viable products, and our expected or projected future results.

These forward-looking statements are subject to a number of uncertainties, such as broader economic developments, including the sustainability of recent improvements in the market environment; trends in demand and prices for semiconductors generally and for our products in particular, as well as for the end-products, such as automobiles and consumer electronics, that incorporate our products; the success of our development efforts, both alone and with partners; the success of our efforts to introduce new production processes at our facilities; the actions of competitors; the continued availability of adequate funds; any mergers, acquisitions or dispositions we may undertake; the outcome of antitrust investigations and litigation matters; and the resolution of Qimonda's insolvency proceedings; as well as the other factors mentioned in this presentation and those disclosed at other occasions.

As a result, Infineon's actual results could differ materially from those contained in or suggested by these forward-looking statements. You are cautioned not to place undue reliance on these forward-looking statements. Infineon does not undertake any obligation to publicly update or revise any forward-looking statements in light of developments which differ from those anticipated.

07 June 2011