IFTA/IRP Managers and Law Enforcement Workshop September 2012.

8

IFTA/IRP Managers and Law Enforcement Workshop September 2012

-

Upload

reynard-booth -

Category

Documents

-

view

217 -

download

0

Transcript of IFTA/IRP Managers and Law Enforcement Workshop September 2012.

IFTA/IRP Managers and Law Enforcement Workshop

September 2012

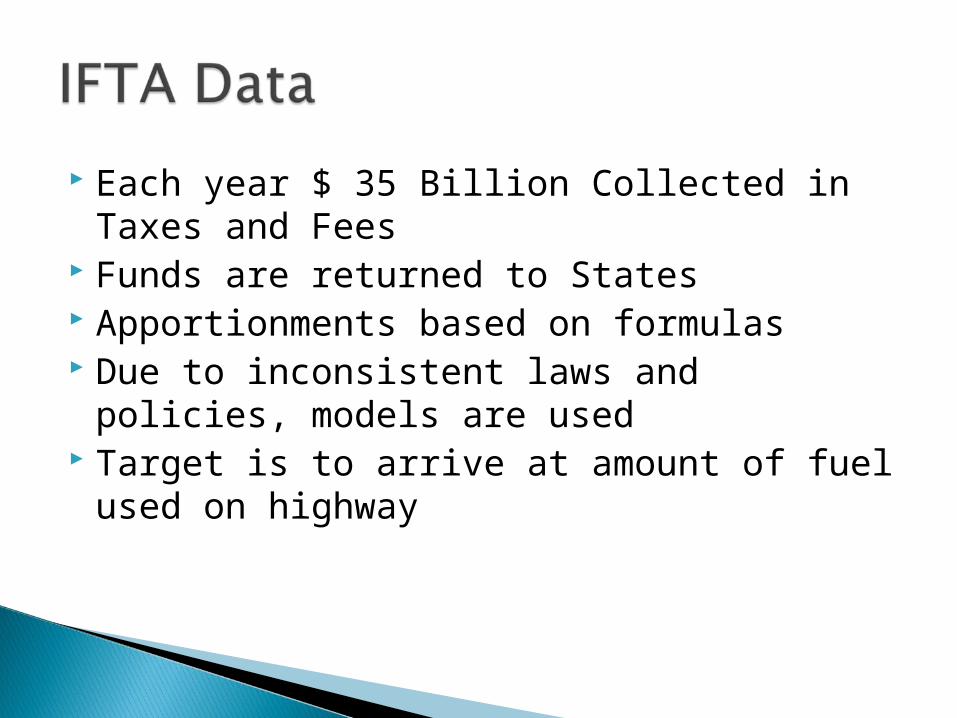

Each year $ 35 Billion Collected in Taxes and Fees

Funds are returned to States Apportionments based on formulas Due to inconsistent laws and policies,

models are used Target is to arrive at amount of fuel used on

highway

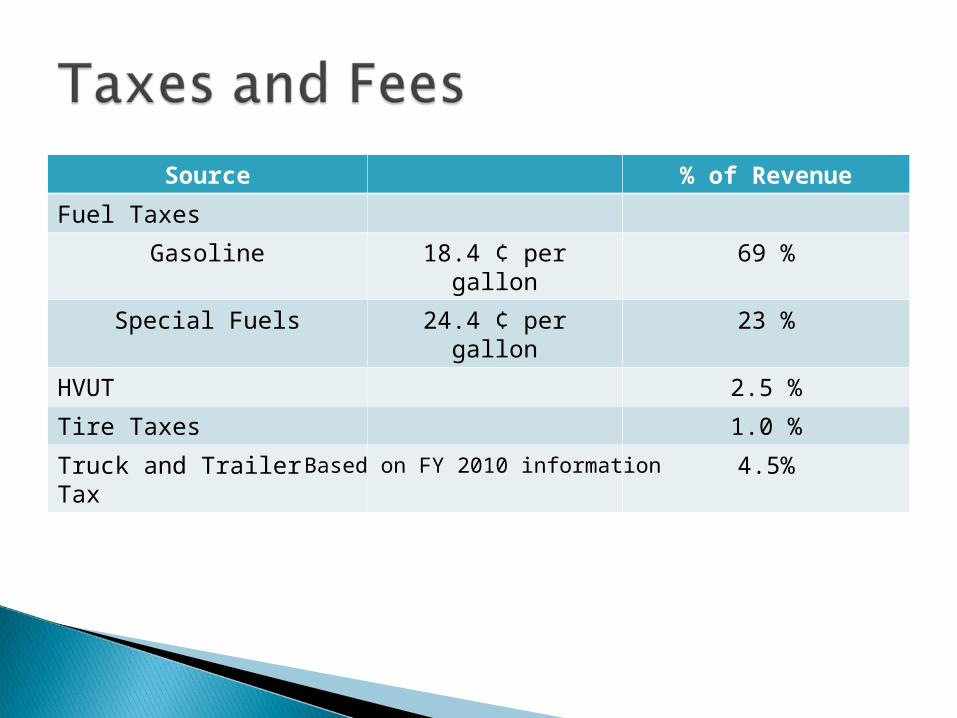

Source % of Revenue

Fuel Taxes

Gasoline 18.4 ¢ per gallon 69 %

Special Fuels 24.4 ¢ per gallon 23 %

HVUT 2.5 %

Tire Taxes 1.0 %

Truck and Trailer Tax 4.5%

Based on FY 2010 information

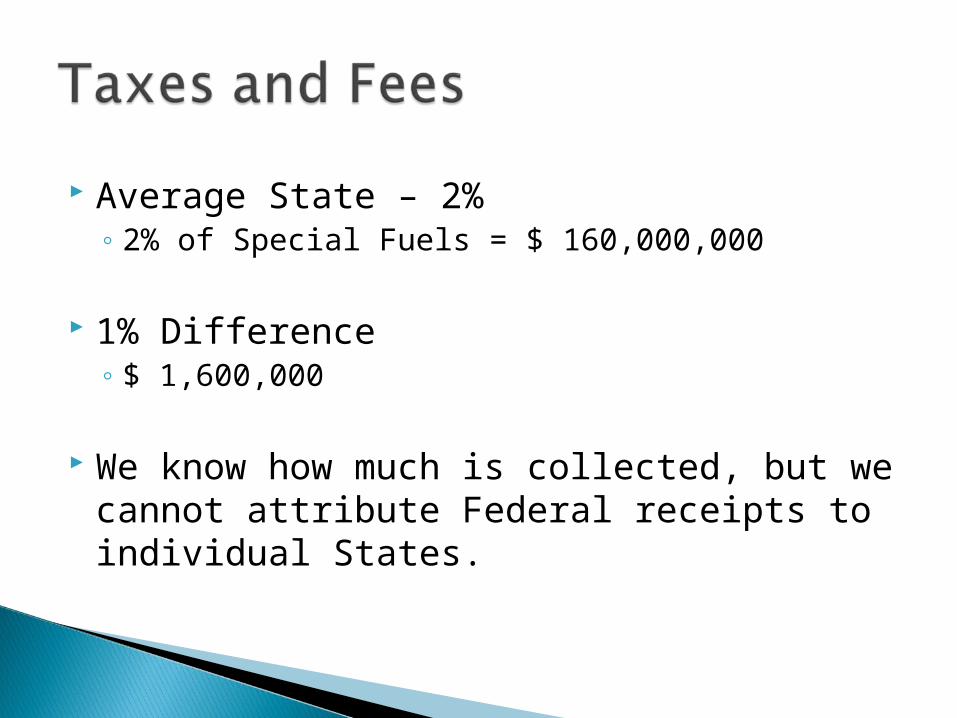

Average State – 2%◦ 2% of Special Fuels = $ 160,000,000

1% Difference◦ $ 1,600,000

We know how much is collected, but we cannot attribute Federal receipts to individual States.

States report amounts monthly to FHWA◦ Total taxable gallons◦ Subtractions

Exemptions Refunds

◦ Need for comparative amounts ◦ Modeling

Based on third-party information May use State or modeled data

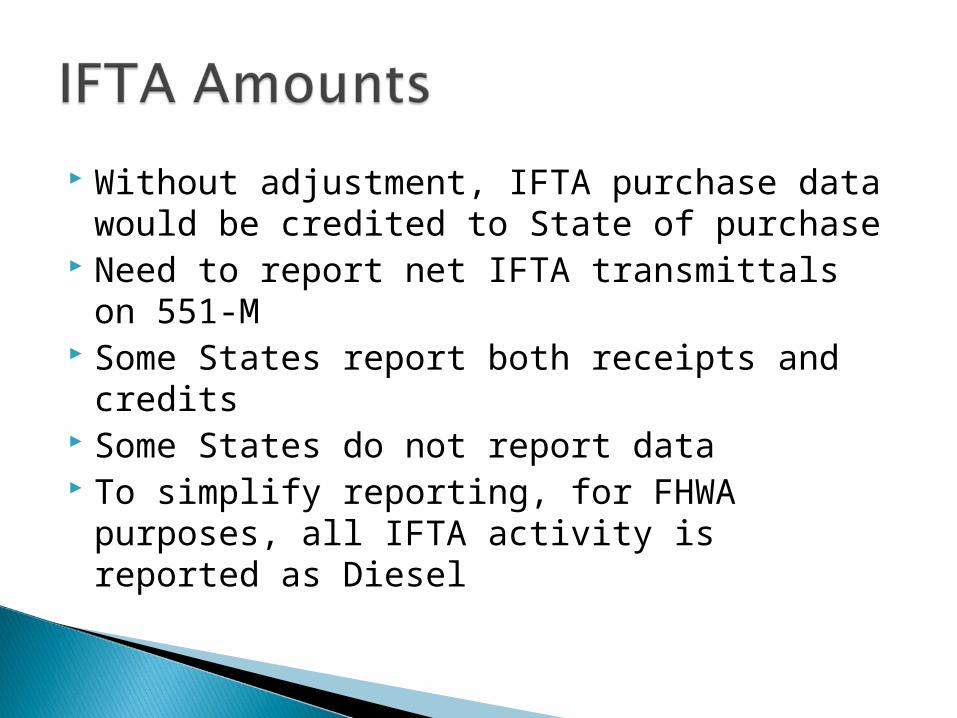

Without adjustment, IFTA purchase data would be credited to State of purchase

Need to report net IFTA transmittals on 551-M

Some States report both receipts and credits

Some States do not report data To simplify reporting, for FHWA purposes,

all IFTA activity is reported as Diesel

Find who in your State files FHWA 551-M report. We can provide the contact name

Make sure consistent data is reported Data is usually reviewed by State

Department of Transportation and Federal Highway Division Office (in each State Capitol)

In MAP-21, apportionments are more reliant on motor fuel data

Contact:◦ Bryant Gross (FHWA)

[email protected] (202) 366-5026

◦ Michael Dougherty (FHWA) [email protected] (202) 366-9234