IFRS NEWSLETTER FINANCIAL INSTRUMENTS - … Newsletter: Financial Instruments. highlights ... IFRS 9...

34

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. IFRS NEWSLETTER FINANCIAL INSTRUMENTS Issue 17, November 2013 This month, preparers received a little more clarity on the mandatory effective date of IFRS 9. It is officially no longer 1 January 2015, and will not be before 1 January 2017. Chris Spall KPMG’s global IFRS financial instruments leader The future of IFRS financial instruments accounting This edition of IFRS Newsletter: Financial Instruments highlights the discussions of the IASB in November 2013 on the financial instruments (IAS 39 replacement) project. Highlights l IFRS 9 Financial Instruments (2013), including the new general hedging model, was issued in November and is available for early application. l The IASB tentatively decided that the mandatory effective date of the final IFRS 9 would be no earlier than annual periods beginning on or after 1 January 2017. Classification and measurement l The IASB reached tentative decisions on the business model assessment, including: – the level at which the business model should be assessed; – how sales impact the assessment; and – the addition of a third measurement category – i.e. fair value through other comprehensive income (FVOCI). Impairment l The IASB reached tentative decisions on: – the measurement and presentation of expected credit losses on revolving credit facilities; – the measurement of expected credit losses for financial assets at FVOCI; – the interest revenue calculation; – the treatment of purchased or originated credit-impaired (POCI) assets; and – trade and lease receivables.

Transcript of IFRS NEWSLETTER FINANCIAL INSTRUMENTS - … Newsletter: Financial Instruments. highlights ... IFRS 9...

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

IFRS NEWSLETTERFINANCIAL INSTRUMENTS

Issue 17, November 2013

This month, preparers received a little more clarity on the mandatory effective date of IFRS 9. It is officially no longer 1 January 2015, and will not be before 1 January 2017.

Chris SpallKPMG’s global IFRS financial instruments leader

The future of IFRS financial instruments accounting

This edition of IFRS Newsletter: Financial Instruments highlights the discussions of the IASB in November 2013 on the financial

instruments (IAS 39 replacement) project.

Highlights

l IFRS 9 Financial Instruments (2013), including the new general hedging model, was issued in November and is available for early application.

l The IASB tentatively decided that the mandatory effective date of the final IFRS 9 would be no earlier than annual periods beginning on or after 1 January 2017.

Classification and measurement

l The IASB reached tentative decisions on the business model assessment, including:

– the level at which the business model should be assessed;

– how sales impact the assessment; and

– the addition of a third measurement category – i.e. fair value through other comprehensive income (FVOCI).

Impairment

l The IASB reached tentative decisions on:

– the measurement and presentation of expected credit losses on revolving credit facilities;

– the measurement of expected credit losses for financial assets at FVOCI;

– the interest revenue calculation;

– the treatment of purchased or originated credit-impaired (POCI) assets; and

– trade and lease receivables.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 2

MANDATORY EFFECTIVE DATE DEFERRED TO AT LEAST 2017, AS REDELIBERATIONS CONTINUE

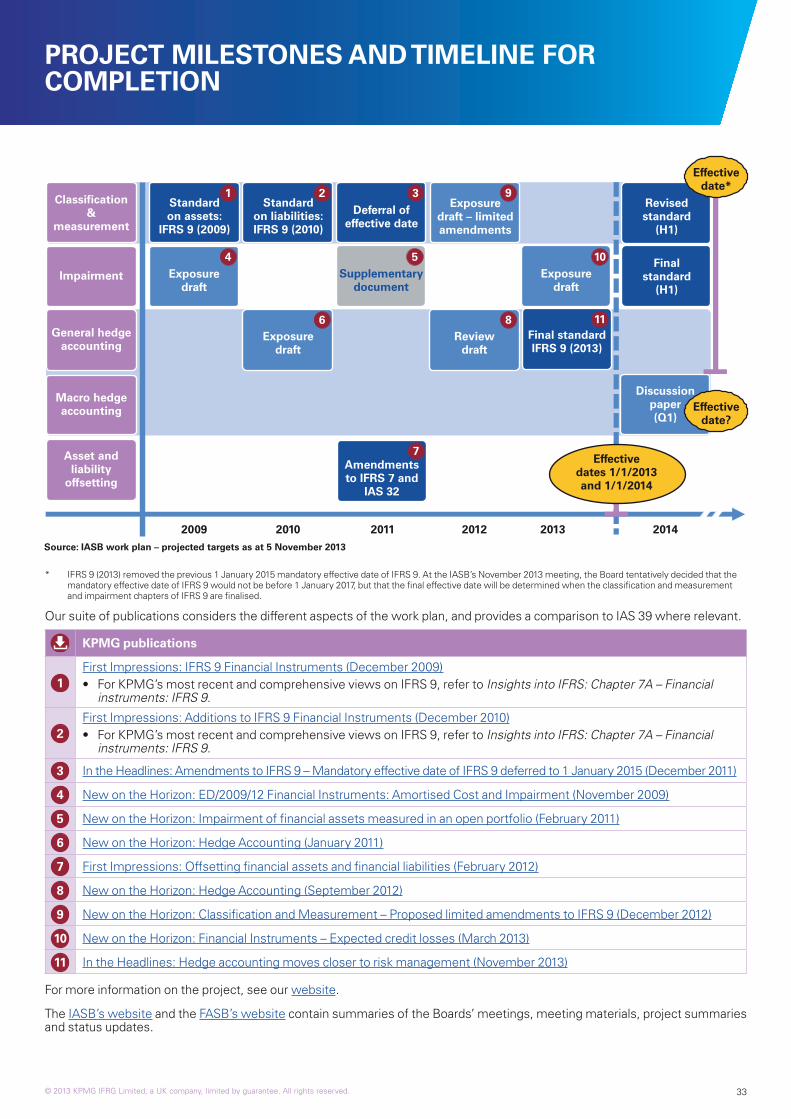

The story so far …Since November 2008, the IASB has been working to replace its financial instruments standard (IAS 39 Financial Instruments: Recognition and Measurement) with an improved and simplified standard. The IASB structured its project in three phases:Phase 1: Classification and measurement of financial assets and financial liabilitiesPhase 2: Impairment methodologyPhase 3: Hedge accounting.

In December 2008, the FASB added a similar project to its agenda; however, the FASB has not followed the same phased approach as the IASB.

Classification and measurementThe IASB issued IFRS 9 Financial Instruments (2009) and IFRS 9 (2010), which contain the requirements for the classification and measurement of financial assets and financial liabilities. In November 2012, the IASB issued an exposure draft (ED) on limited amendments to the classification and measurement requirements of IFRS 9 (the C&M ED).

The FASB issued a revised ED in February 2013 – the proposed Accounting Standards Update, Financial Instruments—Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities (the proposed ASU). Separate and joint redeliberations by the IASB and the FASB (the Boards) on the classification and measurement proposals are ongoing. The IASB plans to issue a final standard by mid-2014.

Impairment

The Boards were working jointly on a model for the impairment of financial assets based on expected credit losses, which would replace the current incurred loss model in IAS 39. The Boards previously published their own differing proposals in November 2009 (the IASB) and in May 2010 (the FASB), and published a joint supplementary document on recognising impairment in open portfolios in January 2011. However, at the July 2012 joint meeting the FASB expressed concern about the direction of the joint project and in December 2012 issued an ED of its own impairment model, the current expected credit loss model. Meanwhile, the IASB continued to develop separately its three-bucket impairment model, and issued a new ED in March 2013 (the impairment ED). Separate and joint redeliberations by the Boards on the impairment proposals are ongoing, and the IASB plans to issue a final standard by mid-2014.

Hedge accounting

The IASB has split the hedge accounting phase into two parts: general hedging and macro hedging. The IASB issued a new general hedging standard as part of IFRS 9 Financial Instruments (2013) in November 2013, and the IASB is working towards issuing a discussion paper (DP) on macro hedging in early 2014.

What happened in November 2013?The final general hedging standard was issued as part of IFRS 9 (2013). This was keenly awaited by some entities who are eager either to:

• early adopt the separate presentation of own credit risk losses on financial liabilities measured at fair value through profit or loss (FVTPL) using the fair value option; or

• early adopt the new general hedging model.

For a high-level summary of the significant changes and their impact on entities, see our In the Headlines: Hedge accounting moves closer to risk management.

In November 2013, the IASB officially removed the previous mandatory effective date of IFRS 9 – i.e. 1 January 2015 – as part of IFRS 9 (2013) and tentatively decided that it would be no earlier than 1 January 2017.

The Boards also reconfirmed the basic approach in the C&M ED and the proposed ASU regarding the business model assessment and provided clarifications to address concerns about the application of the business model test in the C&M ED.

Additionally, the Boards reconfirmed that the revised IFRS 9 would include a third measurement category in which financial assets that meet the cash flow characteristics test would be measured at FVOCI when both collecting contractual cash flows and selling are integral to the performance of the business model.

In the impairment project, the IASB decided to measure the expected credit losses of a revolving credit facility using the behavioural life, rather than the contractual life. The IASB also decided that any expected credit losses related to the undrawn part of a revolving credit facility could be presented together with the loss allowance on any drawn down part of the revolving credit facility, if making an allocation between the two parts is impracticable.

Contents

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 3

KEY DECISIONS MADE THIS MONTH

Mandatory effective date of IFRS 9The IASB tentatively decided that the mandatory effective date of IFRS 9 would be no earlier than 1 January 2017.

Classification and measurementThe Boards reached a number of tentative decisions in the following areas.

Business model assessment

• ‘Business model’ should refer to the way in which financial assets are managed in order to generate cash flows and create value for the entity.

• The business model should be assessed at a level that reflects groups of financial assets that are managed together to achieve a particular objective.

• The Boards provided clarifications on the information that should be considered when making the business model assessment.

• Sales do not drive the business model assessment, and information about sales activity should not be considered in isolation, but as part of an holistic assessment of how the financial assets will be managed.

• A change in business model that results in reclassification would occur only when an entity has either stopped or started doing something on a level that is significant to its operations.

Hold to collect business model

• Insignificant and/or infrequent sales may be consistent with the hold to collect business model, regardless of the reasons for those sales.

Fair value measurement categories

• A third FVOCI measurement category would be retained. It would add complexity to IFRS 9, but this complexity would be justified by the usefulness of the information provided.

• The Boards provided clarifications on the meaning of managing and evaluating assets on a fair value basis.

• Managing financial assets both to collect contractual cash flows and for sale would reflect the way in which financial assets are managed to achieve a particular objective, rather than the objective in itself.

ImpairmentThe IASB reached a number of tentative decisions in the following areas.

Expected credit losses on revolving credit facilities

• Expected credit losses on revolving credit facilities would consider the behavioural life.

• The disconnect between the discount rate on drawn and undrawn components of a revolving credit facility would be addressed.

• Proposals in respect of financial assets measured at FVOCI would be retained, with some clarifications.

Interest revenue calculation

• Proposals in the impairment ED to change the interest revenue calculation from a ‘gross’ to a ‘net’ basis when there is objective evidence of impairment would be retained.

• The criteria in the ED for when the calculation of interest revenue changes to a net basis would be retained.

• Symmetry in the interest revenue calculation would be retained.

Other decisions

• Proposals in respect of POCI assets, and trade and lease receivables would be retained.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 4

MANDATORY EFFECTIVE DATE OF IFRS 9

The mandatory effective date of the final IFRS 9 would be no earlier than annual periods beginning on or after 1 January 2017.

What’s the issue?At its July 2013 meeting, the IASB tentatively decided to defer the mandatory effective date of IFRS 9 to an unspecified date, pending the finalisation of the impairment and classification and measurement phases of the project. The effective date was subsequently removed from IFRS 9 as part of the amendments to the standard issued in November 2013. See our In the Headlines: Hedge accounting moves closer to risk management for more information, and look out in December for our First Impressions, which will provide a detailed analysis of the new standard.

Respondents to the impairment ED generally supported a two- to three-year lead time from the date of issuing the final version of IFRS 9 to implement the standard. Their reasons included:

• the size and complexity of the necessary changes to credit risk management systems;

• the interaction between the proposals and regulatory requirements;

• the desire to run new systems in parallel with the current ones based on IAS 39; and

• the need to inform stakeholders of the accounting, regulatory capital and business impacts before IFRS 9 becomes effective.

Respondents also believed that a mandatory effective date of earlier than 1 January 2017 would compromise the quality of implementation. A few requested that the mandatory effective date of IFRS 9 and the forthcoming standard to replace IFRS 4 Insurance Contracts be aligned.

What did the staff recommend? AThe staff recommended that the IASB should not determine the effective date of IFRS 9 while deliberations on the standard are continuing. However, because of the required lead time and the size of the resulting implementation projects, the staff believed that providing some guidance about the earliest mandatory effective date of IFRS 9 would help preparers in their planning.

On the basis of feedback received, the staff recommended that the mandatory effective date of the final IFRS 9 should be no earlier than annual periods beginning on or after 1 January 2017.

What did the IASB decide?The IASB noted that it will only be able to determine the mandatory effective date after redeliberations of the impairment and classification and measurement requirements have been completed, and once the issue date of the final version of IFRS 9 is known.

However, to help entities in their planning, the IASB agreed with the staff recommendations and tentatively decided that the mandatory effective date of IFRS 9 would be no earlier than annual periods beginning on or after 1 January 2017.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 5

CLASSIFICATION AND MEASUREMENT – OVERALL BUSINESS MODEL ASSESSMENT

What’s the issue? Under IFRS 9, entities classify financial assets based on the business model for managing them (subject to the assessment of the assets’ cash flow characteristics). The proposed ASU provided similar guidance to that in IFRS 9. The C&M ED states that an entity’s business model for managing financial assets is a matter of fact that can be observed by the way the business is managed, and its performance evaluated, by key management personnel.

‘Business model’ should refer to the way in which financial assets are managed in order to generate cash flows and create value for the entity.

Meaning of the term ‘business model’

What did the staff recommend?

The staff acknowledged that the term ‘business model’ can have a broad range of formal and informal definitions. It is often used to describe the core aspects of a business. However, the staff noted that the Boards have used the term ‘business model’ in a particular way – specifically, the objective of the business model assessment is to ensure that financial assets are measured in a way that enables users to predict the likely amounts, timing and uncertainty of future cash flows. Both IFRS 9 and the proposed ASU include a notion of cash realisation.

What did the Boards decide?

The Boards agreed that the application guidance should be supplemented to clarify the following points.

• The term ‘business model’ should refer to the way in which financial assets are managed in order to generate cash flows and create value for the entity – i.e. whether the cash flows will result primarily from the collection of contractual cash flows, sales proceeds or both.

• The business model assessment should result in financial assets being measured in a way that would provide the most relevant and useful information about how activities and risks are managed to create value.

KPMG Insights

We are pleased that the Boards have tentatively decided to provide clarifications to base the business model assessment on a more balanced consideration of which activities are integral and which are incidental to the objectives established for managing groups of financial assets.

The business model should be assessed at a level that reflects groups of financial assets that are managed together to achieve a particular objective.

Level at which a business model is assessed

What did the staff recommend?

IFRS 9 does not mandate the level at which the business model should be assessed. The assessment is not an instrument-by-instrument approach, but should be determined at a higher level of aggregation; furthermore, a single entity may have more than one business model. Therefore, the assessment need not be determined at the reporting entity level.

The staff did not believe that there is a single universal level of aggregation that would be appropriate to all reporting entities in all circumstances.

However, they did recommend clarifying in the application guidance that the business model should be assessed at a level that reflects groups of financial assets that are managed together to achieve a particular objective.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 6

What did the Boards decide?

The Boards agreed with the staff recommendations. In short, the business model assessment should reflect the way in which the business is managed.

Information that should be considered when making the business model assessment

What did the staff recommend?

The staff recommended that the Boards clarify that:

• the business model is often observable through particular activities that are undertaken to achieve the objectives of that business model;

• these business activities usually reflect:

– the way in which the performance of the business is evaluated and reported – i.e. key performance indicators;

– the risks that typically impact the performance of the business model; and

– how those risks are managed; and

• an entity should consider all relevant and objective information, but not every ‘what if’ or worst-case scenario.

What did the Boards decide?

The IASB agreed with the staff recommendations. However, while the FASB agreed with the recommendation to clarify that the business model is often observable through particular activities that are undertaken to achieve the objectives of that business model, it did not come to an agreement over the other staff recommendations.

The Boards provided clarifications on the information that should be considered when making the business model assessment.

Sales do not drive the business model assessment, and information about sales activity should not be considered in isolation, but as part of an holistic assessment of how the financial assets will be managed.

Role of sales in the business model assessment

What did the staff recommend?

Most respondents noted that the application guidance seems to focus on the volume and frequency of sales, rather than the reasons for those sales.

Respondents questioned whether this guidance would result in an implicit tainting notion, and some questioned whether a significant volume of unexpected sales would require the entity to restate prior periods as a result of making an ‘error’.

Therefore, the staff recommended that the application guidance should include the following clarifications.

• Sales do not drive the business model assessment, and information about sales activity should not be considered in isolation, but as part of an holistic assessment of how the financial assets will be managed.

• Historical sales information would help an entity support and verify its business model assessment – i.e. whether cash flows have been realised in a manner that is consistent with the stated objective for managing the assets. Such information should be considered in the context of:

– the reasons for those sales;

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 7

– the conditions that existed at that time;

– the entity’s expectations about future sales activities; and

– the reasons for those expected future sales.

• Fluctuations in sales in a particular period do not necessarily mean that the entity’s business model has changed if the entity can explain:

– the nature of those sales; and

– why they do not indicate a fundamental change in its overall business strategy.

• If cash flows are realised in a way that is different from the entity’s expectations, then this will neither:

– result in the restatement of prior period financial statements; nor

– change the classification of the existing financial assets in the business model

as long as the entity considered all relevant and objective information that was available at the time that it made the assessment.

What did the Boards decide?

The IASB agreed with the staff recommendations. The FASB also agreed with the staff recommendations but did not decide on the recommendation for when cash flows are realised in a way that is different from the entity’s expectations.

In particular, the Boards agreed with the recommendation to clarify that sales do not drive the business model assessment but help to support and verify that assessment.

KPMG Insights

We are pleased that the Boards have responded to concerns that the C&M ED placed too much emphasis on the frequency and significance of sales.

A change in business model that results in reclassification would occur only when an entity has either stopped or started doing something on a level that is significant to its operations.

Change in business model and reclassification date

What did the staff recommend?

The staff recommended that the Boards supplement the existing application guidance to clarify that:

• a change in business model would occur only when an entity has either stopped or started doing something on a level that is significant to its operations; and

• this would generally be the case only when the entity has acquired or disposed of a business line.

What did the Boards decide?

The Boards agreed with the staff recommendations. Some board members expressed concerns that the proposed threshold for reclassification of financial assets was too high; and that it could potentially lead to the classification of similar instruments with the same business model objective into two different measurement categories. However, the Boards decided to retain the existing reclassification requirements in order to avoid frequent reclassifications as they believed

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 8

that it would result in unnecessary complexity and insufficient consistency for users of financial statements.

In response to the concerns expressed by several respondents that the IASB and the FASB define ‘reclassification date’ differently, the FASB tentatively decided to converge the reclassification date in the proposed ASU to that of IFRS 9 – i.e. “the first day of the first reporting period following the change in business model”.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 9

CLASSIFICATION AND MEASUREMENT – HOLD TO COLLECT BUSINESS MODEL

Insignificant and/or infrequent sales may be consistent with the hold to collect business model, regardless of the reasons for those sales.

What’s the issue? Financial assets that meet the hold to collect business model criterion would be eligible for classification at amortised cost, subject to the contractual cash flow characteristics assessment.

Most respondents continued to express support for measuring financial assets at amortised cost if they are held within a business model whose objective is to hold assets to collect contractual cash flows. The staff noted that most of the concerns about the scope of the hold to collect business model were related to the guidance on sales out of that model.

What did the staff recommend?The staff recommendations on the overall business model assessment are relevant. In particular, for the hold to collect model the staff recommended that the Boards:

• reinforce the current hold to collect ‘cash flows (value) realisation’ concept by discussing, and providing examples of, the activities that are commonly associated with the hold to collect business model; and by providing guidance on the nature of information an entity should consider in assessing the hold to collect business model;

• emphasise that insignificant and/or infrequent sales may be consistent with the hold to collect business model, regardless of the reasons for such sales. This determination is a matter of judgement and would be based on facts and circumstances;

• clarify that historical sales information and patterns could provide useful information, but that sales information would not be determinative and should not be considered in isolation; and

• clarify that sales to minimise potential credit risk due to credit deterioration are integral to the hold to collect objective.

What did the Boards decide?The Boards agreed with the staff recommendations. In addition, with regard to the proposed cash flows (value) realisation concept clarification, the FASB tentatively decided that the guidance on the hold to collect business model should emphasise activities aimed at achieving the business model’s objective.

With regard to sales due to concentration risk, the Boards agreed to clarify that sales made in managing concentration of credit risk should be assessed in the same way as any other sales made in the business model.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 10

CLASSIFICATION AND MEASUREMENT – FAIR VALUE MEASUREMENT CATEGORIES

What’s the issue? IFRS 9 currently has two measurement categories – amortised cost and FVTPL. The C&M ED proposed adding a second fair value measurement category – i.e. FVOCI.

Financial assets that meet the ‘hold to collect and sell’ business model criterion would be eligible for measurement at FVOCI – subject to the assessment of the contractual cash flow characteristics. Assets that are neither ‘hold to collect’ nor ‘hold to collect and sell’ would be measured at FVTPL.

The staff analysis and recommendations focused on the two fair value measurement categories, and on clarifying the proposed application guidance.

A third FVOCI measurement category would be retained. It would add complexity to IFRS 9, but this complexity would be justified by the usefulness of the information provided.

A third measurement category – FVOCI

What did the staff recommend?

The staff acknowledged concerns that a third measurement category would add complexity to IFRS 9. However, they believed that this complexity would be justified by the usefulness of the information provided.

Therefore, the staff recommended that the Boards retain two fair value measurement categories – FVOCI and FVTPL.

The staff recommended that the Boards confirm the proposals to:

• define the business model that results in measurement at FVOCI; and

• retain the FVTPL measurement category as the residual category.

What did the Boards decide?

The Boards agreed with the staff recommendations.

The Boards provided clarifications on the meaning of managing and evaluating assets on a fair value basis.

Clarifying the proposed application guidance for the FVTPL measurement category

What did the staff recommend?

To help differentiate the business models and to supplement the guidance on the FVTPL measurement category, the staff recommended that the Boards explain the meaning of managing financial assets on a fair value basis. This could be accomplished by clarifying that:

• when financial assets are either held for trading or managed and evaluated on a fair value basis, the entity makes decisions – i.e. whether to hold or sell the asset – based on changes in, and with the objective of realising, the assets’ fair value;

• the activities that the entity undertakes are primarily focused on fair value information, and key management personnel use that information to assess the assets’ performance and to make decisions accordingly; and

• another indicator is that the users of the financial statements are primarily interested in fair value information on these assets to assess the entity’s performance.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 11

What did the Boards decide?

The IASB agreed with the staff recommendations. However, while the FASB agreed with the recommendation to clarify that when financial assets are measured at FVTPL, the entity makes decisions based on changes in, and with the objective of realising the assets’ fair value, they did not come to an agreement over the other staff recommendations.

Managing financial assets both to collect contractual cash flows and for sale would reflect the way in which financial assets are managed to achieve a particular objective, rather than the objective in itself.

Clarifying the proposed application guidance for the FVOCI measurement category

What did the staff recommend?

The staff made the following recommendations.

• The Boards should clarify that managing financial assets both to collect contractual cash flows and for sale would reflect the way in which financial assets are managed to achieve a particular objective, rather than the objective in itself. Assets that are classified at FVOCI would be managed in order to achieve different business model objectives – e.g. liquidity management, interest rate risk management, yield management and duration mismatch management – both by collecting contractual cash flows and by selling.

• The application guidance should more clearly articulate that FVOCI provides relevant and useful information when both the collection of contractual cash flows and the realisation of cash flows through selling are integral to the performance of the business model.

• The application guidance should describe activities that are typically associated with a business model where financial assets are managed both to collect the contractual cash flows and for sale – for example:

– the key performance indicators include both the interest yield and credit information and fair value changes;

– financial assets are held in a liquidity portfolio and significant portions of the portfolio are frequently sold to meet everyday liquidity needs;

– the durations of the financial assets are matched to those of the liabilities that they are funding by regularly rebalancing the portfolio of financial assets; and

– the entity seeks to maintain a particular yield profile or to manage its exposure to interest rate risk by holding and selling financial assets in accordance with a stated risk management policy.

• There would be no threshold for the frequency or amounts of sales.

What did the Boards decide?

The IASB agreed with the staff recommendations. The FASB also agreed with the staff recommendations except for the recommendation to include contractual interest yield, credit information and fair value changes as key performance indicators. In addition, the FASB tentatively decided to remove the guidance in the FASB’s proposed ASU requiring an individual asset for which an entity has, at initial recognition, not yet determined whether it will hold the financial asset to collect contractual cash flows or sell to be measured at FVOCI.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 12

KPMG Insights

We agree with the Boards that, while a third measurement category adds complexity to IFRS 9, for some financial assets, measurement at FVOCI would appropriately reflect their performance.

However, we do expect that there may remain a degree of judgement around the classification of financial assets into this measurement category.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 13

IMPAIRMENT – REVOLVING CREDIT FACILITIES

Expected credit losses on revolving credit facilities would consider the behavioural life.

Expected credit losses on revolving credit facilities

What’s the issue?

Under the impairment ED, an entity would recognise a provision for expected credit losses on loan commitments and financial guarantees when it has a present contractual obligation to extend credit. The provision would be calculated with reference to the estimated usage behaviour over a period during which a present legal obligation exists to extend credit. The maximum period to consider when estimating the expected credit losses would be the maximum contractual period over which the entity is exposed to credit risk and not a longer period – even if that would be inconsistent with business practice.

Many respondents to the IASB’s proposals believed that expected credit losses for loan commitments – and in particular revolving credit instruments – should be measured over the behavioural life, rather than the contractual life, because measuring on the basis of the contractual period:

• would be inconsistent with how these exposures are treated for risk management and regulatory purposes;

• may result, or be seen to result, in an insufficient allowance being made for credit risk; and

• would result in outcomes for which no actual loss experience exists on which to base the estimate.

The staff noted that – for revolving credit facilities – the contractual ability to demand repayment and cancel the undrawn commitment does not necessarily limit an entity’s exposure to credit loss to the contractual period. This is because there can be no reasonable grounds for the entity to exercise that option for some borrowers but not for others if there has been no change in their credit standing. This raises the question of whether this is a genuine option. Arguably, there may be a constructive obligation to extend credit beyond the contractual cancellation period if an entity does not have a practical ability to withdraw a facility from a customer whose credit risk has not increased up to the point of the draw-down.

What did the staff recommend?

The staff recommended confirming the proposals in the impairment ED:

• that an entity should recognise a provision for expected credit losses resulting from loan commitments and financial guarantee contracts – other than revolving credit facilities – when there is a present contractual obligation to extend credit; and

• to present the expected credit loss allowance of the undrawn commitment of a revolving credit facility as a provision.

The staff also asked the Board if it wanted to reconsider the impairment ED’s proposals to recognise a provision for expected credit losses that result from revolving credit facilities only where there is a present contractual obligation to extend credit. If it did so, the staff recommended that:

• the expected credit losses be estimated over the facility’s behavioural life; and

• the behavioural life should represent the period over which an entity is exposed to credit risk and that faithfully reflects the economics of the transaction. This would include consideration of:

– historic information and experience about the period in which the entity expects the facility to remain open;

– the behaviour patterns of the borrowers and the entity itself; or

– the period over which repayments are made.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 14

What did the IASB decide?

The IASB tentatively decided that for revolving credit facilities:

• expected credit losses – including expected credit losses on the undrawn facility – would be estimated for the period over which an entity is exposed to credit risk and over which future draw-downs cannot be avoided – i.e. considering the behavioural life; and

• the provision for the expected credit losses on the undrawn component of the facility would be presented together with the loss allowance for expected credit losses on the drawn facility if an entity cannot separately identify the expected credit losses associated with the undrawn facility.

These tentative decisions were in respect of revolving credit facilities only. However, the IASB asked the staff to perform further analysis, to determine whether these tentative decisions should apply to a wider scope of loan commitments and financial guarantee contracts.

KPMG Insights

In some jurisdictions, certain loan commitments– e.g. credit cards or overdrafts – can be withdrawn on demand or with very little notice. This means that, for these products, expected credit losses estimated in accordance with the requirements of the impairment ED may have been very small or zero. This result appears counterintuitive, because these products often attract a high level of defaults. Although, contractually, the lender may withdraw the credit line on demand or ask for an immediate repayment of the drawn balance, it would not normally have information on when it would be advisable to do so. Often, the key monitoring tool for such financial instruments is an ‘overdue status’, and by the time the loan is overdue, impairment losses may already have occurred.

We welcome the IASB’s tentative decision to reconsider its previous conclusion and require expected credit losses on revolving facilities to be calculated over the behavioural rather than contractual life of the facilities. We believe that this development would align accounting more closely with the substance of the lending transaction.

The disconnect between the discount rate on drawn and undrawn components of a revolving credit facility would be addressed.

Discounting expected credit losses on the undrawn portion of revolving credit facility guarantees

What’s the issue?

For undrawn loan commitments and financial guarantees, the impairment ED proposed that an entity should use a discount rate that reflects the current market assessment of the time value of money and the risks that are specific to the cash flows. By contrast, for amounts drawn down under the facility the ED would require any reasonable rate that is between (and including) the EIR1.

Most respondents noted that for credit management purposes, the credit facility is viewed as a whole, because there is only one set of cash flows from the borrower that relates to both the drawn and undrawn components. Accordingly, requiring different discount rates for each component of the credit facility would introduce a disconnect in the impairment model.

1 The impairment ED proposed that the discount rate to be used to determine expected credit losses on financial assets could be any reasonable rate that is between (and including) the risk-free rate and the effective interest rate (EIR). Subsequently, at its October 2013 meeting, the IASB tentatively decided to require that the expected credit losses be determined using the EIR or an approximation of it.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 15

What did the staff recommend?

The staff recommended clarifying that the rate used to discount the drawn balance can be regarded as a reasonable approximation of the discount rate for loan commitments and financial guarantees.

What did the IASB decide?

The Board tentatively decided that the expected credit losses on the undrawn part of the revolving credit facility would be discounted using the same EIR, or an approximation thereof, as would be used to discount the drawn part. Also, the Board instructed the staff to perform further analysis to consider whether this decision should be extended to a wider scope of loan commitments and financial guarantee contracts.

KPMG Insights

The IASB’s tentative decision has simplified the requirements and aligned them more closely with the way banks manage their credit risk. This is a welcome development.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 16

IMPAIRMENT – FINANCIAL ASSETS MEASURED AT FVOCI

Proposals in respect of financial assets measured at FVOCI would be retained, with some clarifications.

What’s the issue? The impairment ED included in its scope financial assets mandatorily measured at FVOCI, and proposed that the general model be applied to them. Although the proposal was generally well received, some respondents suggested that the IASB should introduce a practical expedient not to recognise 12-month expected credit losses for FVOCI assets in certain circumstances. Supporters of the practical expedient argued that:

• the practical expedient would reduce the operational burden of assessing significant increases in credit risk and measuring impairment losses;

• the amounts in OCI that would result from a contra entry for impairment loss recognised in profit or loss would not be meaningful; and

• it would not be appropriate to recognise initial expected credit losses for financial assets acquired in an active market, because those losses are already factored into the market price.

Some respondents also asked the Board to clarify whether an entity’s estimate of expected credit losses would be the same as fair value changes attributable to changes in credit risk of the FVOCI assets, because such changes reflect market participants’ view of credit risk and are based on the information available in the market.

What did the staff recommend? The staff recommended that a specific practical expedient should not be introduced for financial assets measured at FVOCI, because:

• a fair value-based practical expedient:

– would be inconsistent with the general model, which is based on an entity’s assessment of the changes in the risk/probability of a default occurring;

– would introduce a different impairment approach, and would be inconsistent with the IASB’s objective of having a single impairment model for all financial assets measured at amortised cost and FVOCI; and

– would result in the treatment in profit or loss not being the same for financial assets measured at amortised cost as for those measured at FVOCI;

• introducing an additional practical expedient based on the ‘low credit risk’ criterion would result in a different impairment model for financial assets measured at FVOCI; this would lead to the information about the non-collectibility of contractual cash flows not being recognised in the same way as for assets measured at amortised cost – despite this information being equally important for both classes of asset; and

• IFRS has an over-riding principle of applicability if the effect is material. An additional exemption for financial assets measured at FVOCI – based on a materiality level – might imply that the same may not be true for other IFRSs.

The staff also recommended that the IASB should:

• clarify that expected credit losses reflect management’s expectation of credit risk rather than the market’s assessment of it; and

• acknowledge that market information is a relevant consideration for management in making that assessment.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 17

What did the IASB decide? The Board tentatively confirmed the proposals in the impairment ED for financial assets measured at FVOCI and decided not to introduce any relief from recognising 12-month expected credit losses.

The Board also decided to clarify in the final standard that expected credit losses reflect management’s expectations of credit losses. The Board also agreed that when considering the ‘best available information’ in estimating expected credit losses, management should consider observable market information about credit risk.

KPMG Insights

The FASB’s Proposed Accounting Standards Update Financial Instruments – Credit Losses (Subtopic 825-15) included a proposed practical expedient permitting an entity not to recognise a credit loss allowance on assets measured at FVOCI if certain conditions are met. However, based on the IASB’s tentative decision, a similar practical expedient will not be available under IFRS.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 18

IMPAIRMENT – INTEREST REVENUE CALCULATION

Proposals in the impairment ED to change the interest revenue calculation from a ‘gross’ to a ‘net’ basis when there is objective evidence of impairment would be retained.

Interest revenue calculation – Change from gross to net basis

What’s the issue?

The impairment ED proposed that interest revenue would generally be calculated by applying the EIR to the gross carrying amount unless there is objective evidence of impairment, in which case interest would be calculated by applying the EIR to the net carrying amount (amortised cost) of an asset.

A large majority of respondents supported the impairment ED’s proposals. However, some suggested applying a non-accrual approach or retaining the requirement to calculate interest revenue on a gross interest basis for all financial assets – primarily for operational reasons.

What did the staff recommend?

The staff recommended retaining the proposal in the impairment ED as they believed, for the reasons set out in the basis for conclusions to the ED, that the net interest approach better reflects the economic yield on an asset for which there is objective evidence of impairment. The staff noted that applying the EIR to the gross carrying amount of such a financial asset might overstate interest revenue while the non-accrual concept is not consistent with amortised cost accounting. They also noted that the majority of respondents agreed with the proposals in the impairment ED.

What did the IASB decide?

The Board agreed with the staff recommendation.

The criteria in the ED for when the calculation of interest revenue changes to a net basis would be retained.

Criteria for the change in interest calculation to a net basis

What’s the issue?

The impairment ED proposed that the basis of calculating interest revenue changes to a net basis when there is objective evidence of impairment for a financial asset. Most respondents who agreed with this proposal also agreed that such a change should take place when there is objective evidence of impairment. Many noted that retaining the concept of objective evidence of impairment from IAS 39 (excluding IBNR) was beneficial – from an operational point of view – because entities are already applying this concept; some, however, questioned whether it was appropriate to retain an aspect of the ‘incurred loss’ model.

What did the staff recommend?

The staff recommended retaining the impairment ED’s proposals that the calculation of interest revenue should change to a net basis for financial assets that have objective evidence of impairment at the reporting date. They noted that this approach:

• would align the recognition of interest on all credit-impaired assets, including those that were credit-impaired at initial recognition; and

• would be operational, because it would result in little change to existing practice.

What did the IASB decide?

The Board agreed with the staff recommendation.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 19

Symmetry in interest revenue calculationSymmetry in the interest revenue calculation would be retained.

What’s the issue?

The impairment ED proposed that the calculation of interest revenue would be symmetrical – i.e. it would revert to the gross basis if there was no longer objective evidence of impairment. Nearly all respondents agreed with the symmetrical treatment.

What did the staff recommend?

The staff recommended that the IASB retain the proposals.

What did the IASB decide?

The Board agreed with the proposals in the impairment ED that the interest revenue calculation would be symmetrical, meaning that the interest revenue would revert to the gross basis if there is no longer objective evidence of impairment.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 20

IMPAIRMENT – OTHER DECISIONS

Proposals in the impairment ED for the treatment of POCI assets would be retained.

Purchased or originated credit-impaired financial assets (POCI assets)

What’s the issue?

The impairment ED proposed the following special rules for measuring and recognising interest income on POCI assets.

• At initial recognition, POCI assets would not carry a loss allowance. Instead, lifetime expected credit losses would be incorporated into the EIR calculation (resulting in a credit-adjusted EIR).

• The cumulative changes in lifetime expected credit losses since initial recognition would be recognised as an impairment gain or loss.

• Interest revenue would be calculated by applying the credit-adjusted EIR to the amortised cost (net carrying amount) of the POCI asset.

Respondents were almost unanimous in their support for these proposals. However, some respondents asked for more guidance on identifying originated credit-impaired financial instruments.

What did the staff recommend?

The staff recommended that the IASB:

• retain the proposals in the impairment ED for measuring and recognising interest income on POCI assets; and

• provide more guidance on when an originated financial asset would be regarded as credit-impaired.

What did the IASB decide?

The IASB agreed with the staff recommendations.

The simplified approach for trade and lease receivables would be retained.

Simplified approach for trade and lease receivables

What’s the issue?

The impairment ED proposed the following simplifications for calculating the credit loss allowance for trade and lease receivables.

Type of financial asset Proposed measurement of loss allowance

Trade receivables that do not constitute a financing transaction

Lifetime expected credit losses.

Trade receivables with a significant financing component and lease receivables

Accounting policy election to measure the loss allowance either:

• in accordance with the general approach; or

• as lifetime expected credit losses.

The entity would have to apply that policy to all such financial assets. However, it may apply the policy election for trade receivables and lease receivables independently of each other.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 21

The impairment ED also proposed that trade receivables that do not constitute a financing transaction would be measured on initial recognition at the transaction price, rather than at fair value, as required for all other financial instruments.

The vast majority of respondents agreed with these proposals, noting that – for trade receivables without a significant financing component – there would be no difference between the lifetime expected credit losses and the 12-month expected credit losses. Also, measuring such receivables at transaction price at initial recognition would align the proposals with the revenue recognition project.

However, some respondents disagreed with the accounting policy choice for trade receivables with a significant financing component and for lease receivables. Some raised the following concerns over lease receivables.

• Lease receivables are similar to other financial assets – e.g. secured loans – and should therefore be accounted for under the general model.

• Entities should be allowed separate accounting policy choices for different types of lease receivables – e.g. finance vs operating leases, or Type A vs Type B leases2.

• Others requested further clarification on the interaction of the impairment ED with the leases project, or said that they would reserve their comments until the leasing project is finalised.

What did the staff recommend?

The staff recommended that the IASB retain the proposals in the ED for trade and lease receivables.

The staff did not recommend allowing a separate accounting policy choice for different types of lease receivables until the leases project has been finalised.

What did the IASB decide?

The Board agreed with the staff recommendations to retain the proposals for trade and lease receivables. The applicability of the accounting policy choice for lease receivables to different populations of those receivables will be further considered when the leases project is finalised.

The IASB agreed to look at future possibilities for convergence.

Next stepsThe staff aim to present final impairment papers in January 2014, with a view to publishing the final standard in the first half of 2014.

At forthcoming meetings, the IASB intends to discuss the following topics:

• disclosures;

• transition and effective date; and

• any potential sweep issues.

The IASB will also consider the future possibilities for convergence after considering any amendments to the proposals in the impairment ED and any changes that have been made by the FASB to its proposals.

2 As defined under exposure draft ED/2013/6 Leases.

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 22

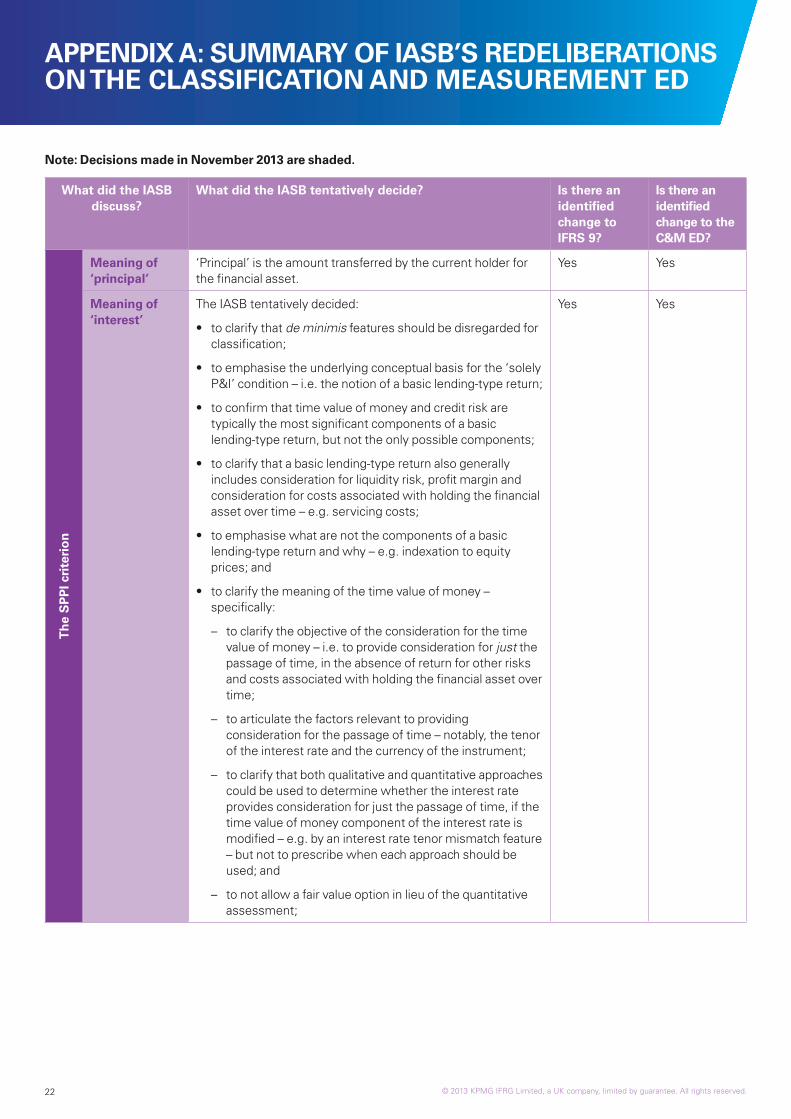

APPENDIX A: SUMMARY OF IASB’S REDELIBERATIONS ON THE CLASSIFICATION AND MEASUREMENT ED

Note: Decisions made in November 2013 are shaded.

What did the IASB discuss?

What did the IASB tentatively decide? Is there an identified change to IFRS 9?

Is there an identified change to the C&M ED?

Th

e S

PP

I cri

teri

on

Meaning of ‘principal’

‘Principal’ is the amount transferred by the current holder for the financial asset.

Yes Yes

Meaning of ‘interest’

The IASB tentatively decided:

• to clarify that de minimis features should be disregarded for classification;

• to emphasise the underlying conceptual basis for the ‘solely P&I’ condition – i.e. the notion of a basic lending-type return;

• to confirm that time value of money and credit risk are typically the most significant components of a basic lending-type return, but not the only possible components;

• to clarify that a basic lending-type return also generally includes consideration for liquidity risk, profit margin and consideration for costs associated with holding the financial asset over time – e.g. servicing costs;

• to emphasise what are not the components of a basic lending-type return and why – e.g. indexation to equity prices; and

• to clarify the meaning of the time value of money – specifically:

– to clarify the objective of the consideration for the time value of money – i.e. to provide consideration for just the passage of time, in the absence of return for other risks and costs associated with holding the financial asset over time;

– to articulate the factors relevant to providing consideration for the passage of time – notably, the tenor of the interest rate and the currency of the instrument;

– to clarify that both qualitative and quantitative approaches could be used to determine whether the interest rate provides consideration for just the passage of time, if the time value of money component of the interest rate is modified – e.g. by an interest rate tenor mismatch feature – but not to prescribe when each approach should be used; and

– to not allow a fair value option in lieu of the quantitative assessment;

Yes Yes

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 23

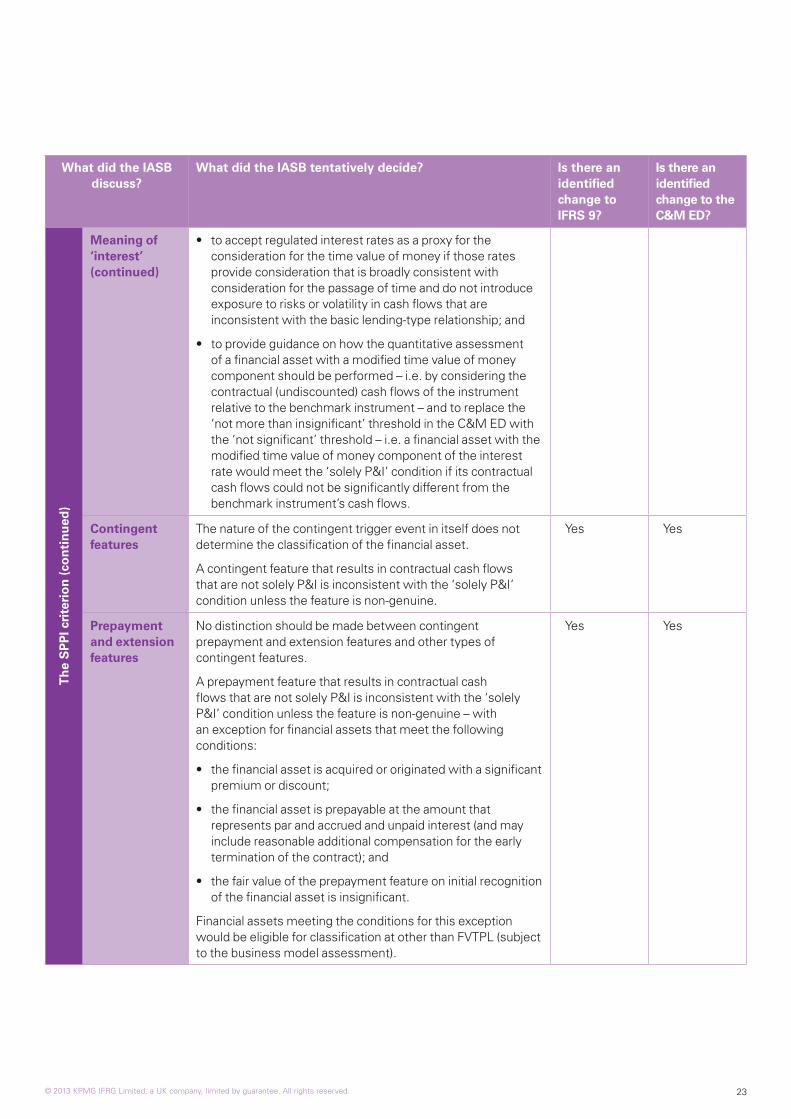

What did the IASB discuss?

What did the IASB tentatively decide? Is there an identified change to IFRS 9?

Is there an identified change to the C&M ED?

Th

e S

PP

I cri

teri

on

(co

nti

nu

ed)

Meaning of ‘interest’ (continued)

• to accept regulated interest rates as a proxy for the consideration for the time value of money if those rates provide consideration that is broadly consistent with consideration for the passage of time and do not introduce exposure to risks or volatility in cash flows that are inconsistent with the basic lending-type relationship; and

• to provide guidance on how the quantitative assessment of a financial asset with a modified time value of money component should be performed – i.e. by considering the contractual (undiscounted) cash flows of the instrument relative to the benchmark instrument – and to replace the ‘not more than insignificant’ threshold in the C&M ED with the ‘not significant’ threshold – i.e. a financial asset with the modified time value of money component of the interest rate would meet the ‘solely P&I’ condition if its contractual cash flows could not be significantly different from the benchmark instrument’s cash flows.

Contingent features

The nature of the contingent trigger event in itself does not determine the classification of the financial asset.

A contingent feature that results in contractual cash flows that are not solely P&I is inconsistent with the ‘solely P&I’ condition unless the feature is non-genuine.

Yes Yes

Prepayment and extension features

No distinction should be made between contingent prepayment and extension features and other types of contingent features.

A prepayment feature that results in contractual cash flows that are not solely P&I is inconsistent with the ‘solely P&I’ condition unless the feature is non-genuine – with an exception for financial assets that meet the following conditions:

• the financial asset is acquired or originated with a significant premium or discount;

• the financial asset is prepayable at the amount that represents par and accrued and unpaid interest (and may include reasonable additional compensation for the early termination of the contract); and

• the fair value of the prepayment feature on initial recognition of the financial asset is insignificant.

Financial assets meeting the conditions for this exception would be eligible for classification at other than FVTPL (subject to the business model assessment).

Yes Yes

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 24

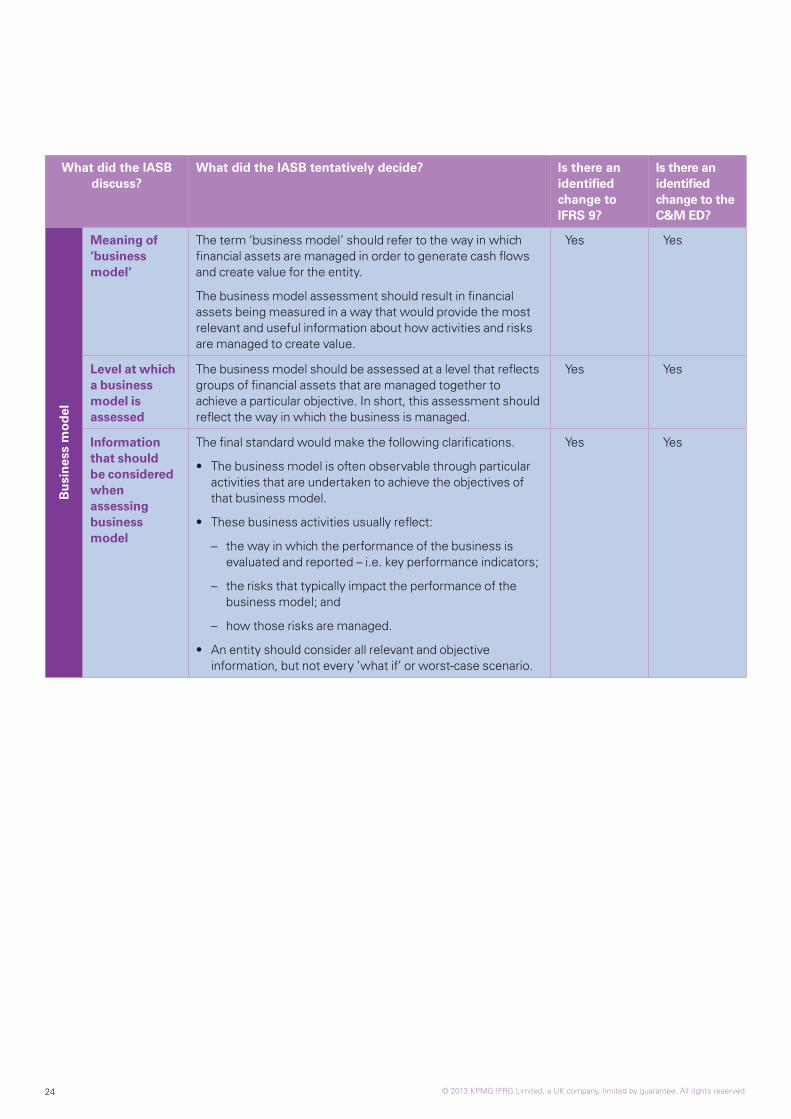

What did the IASB discuss?

What did the IASB tentatively decide? Is there an identified change to IFRS 9?

Is there an identified change to the C&M ED?

Bu

sin

ess

mo

del

Meaning of ‘business model’

The term ‘business model’ should refer to the way in which financial assets are managed in order to generate cash flows and create value for the entity.

The business model assessment should result in financial assets being measured in a way that would provide the most relevant and useful information about how activities and risks are managed to create value.

Yes Yes

Level at which a business model is assessed

The business model should be assessed at a level that reflects groups of financial assets that are managed together to achieve a particular objective. In short, this assessment should reflect the way in which the business is managed.

Yes Yes

Information that should be considered when assessing business model

The final standard would make the following clarifications.

• The business model is often observable through particular activities that are undertaken to achieve the objectives of that business model.

• These business activities usually reflect:

– the way in which the performance of the business is evaluated and reported – i.e. key performance indicators;

– the risks that typically impact the performance of the business model; and

– how those risks are managed.

• An entity should consider all relevant and objective information, but not every ’what if’ or worst-case scenario.

Yes Yes

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 25

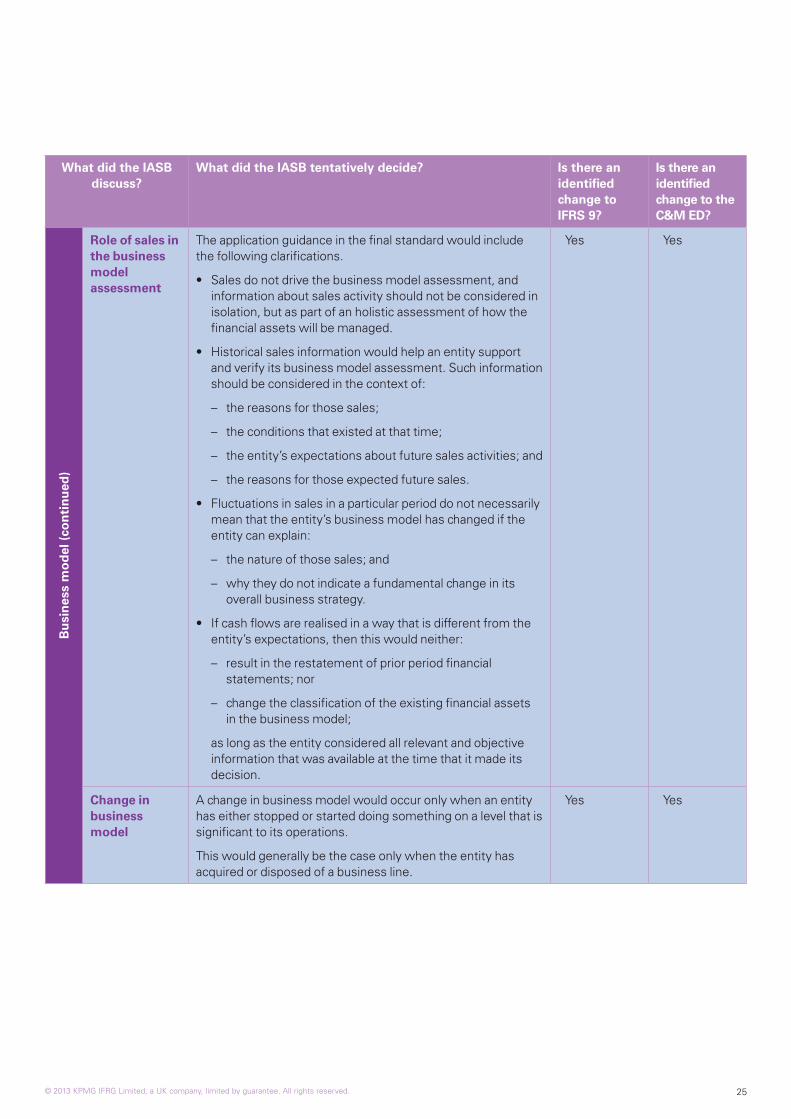

What did the IASB discuss?

What did the IASB tentatively decide? Is there an identified change to IFRS 9?

Is there an identified change to the C&M ED?

Bu

sin

ess

mo

del

(co

nti

nu

ed)

Role of sales in the business model assessment

The application guidance in the final standard would include the following clarifications.

• Sales do not drive the business model assessment, and information about sales activity should not be considered in isolation, but as part of an holistic assessment of how the financial assets will be managed.

• Historical sales information would help an entity support and verify its business model assessment. Such information should be considered in the context of:

– the reasons for those sales;

– the conditions that existed at that time;

– the entity’s expectations about future sales activities; and

– the reasons for those expected future sales.

• Fluctuations in sales in a particular period do not necessarily mean that the entity’s business model has changed if the entity can explain:

– the nature of those sales; and

– why they do not indicate a fundamental change in its overall business strategy.

• If cash flows are realised in a way that is different from the entity’s expectations, then this would neither:

– result in the restatement of prior period financial statements; nor

– change the classification of the existing financial assets in the business model;

as long as the entity considered all relevant and objective information that was available at the time that it made its decision.

Yes Yes

Change in business model

A change in business model would occur only when an entity has either stopped or started doing something on a level that is significant to its operations.

This would generally be the case only when the entity has acquired or disposed of a business line.

Yes Yes

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 26

What did the IASB discuss?

What did the IASB tentatively decide? Is there an identified change to IFRS 9?

Is there an identified change to the C&M ED?

Bu

sin

ess

mo

del

(co

nti

nu

ed)

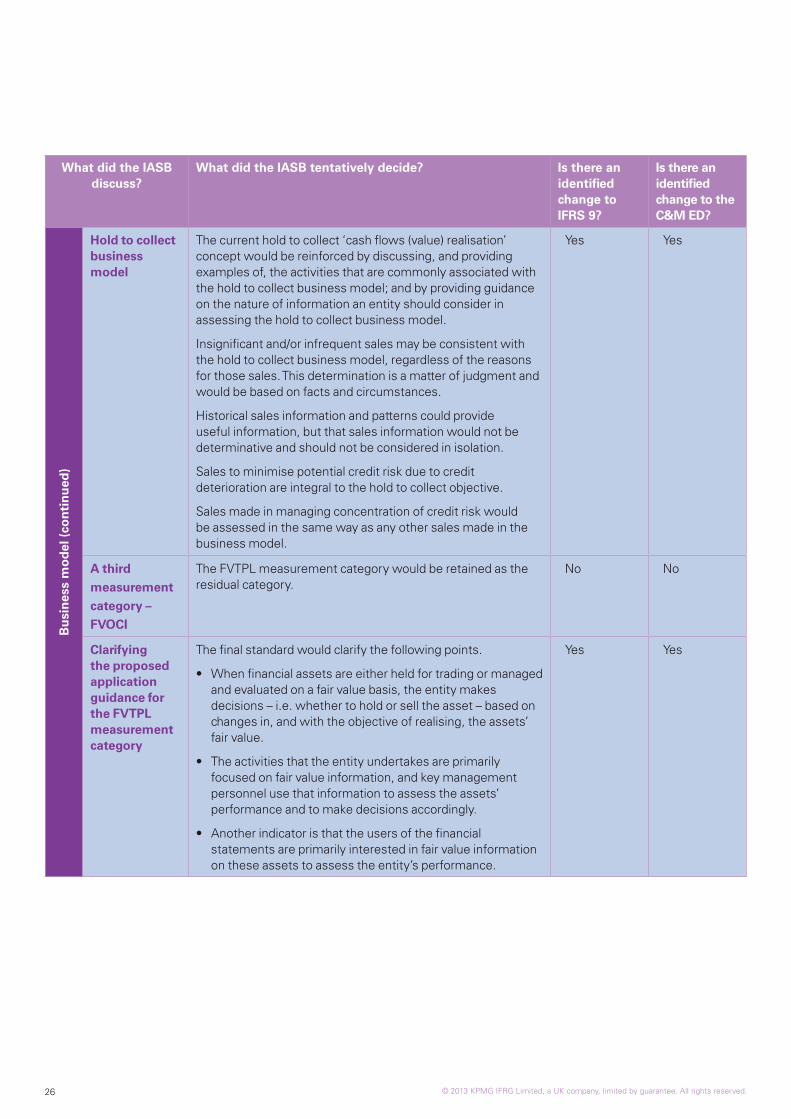

Hold to collect business model

The current hold to collect ‘cash flows (value) realisation’ concept would be reinforced by discussing, and providing examples of, the activities that are commonly associated with the hold to collect business model; and by providing guidance on the nature of information an entity should consider in assessing the hold to collect business model.

Insignificant and/or infrequent sales may be consistent with the hold to collect business model, regardless of the reasons for those sales. This determination is a matter of judgment and would be based on facts and circumstances.

Historical sales information and patterns could provide useful information, but that sales information would not be determinative and should not be considered in isolation.

Sales to minimise potential credit risk due to credit deterioration are integral to the hold to collect objective.

Sales made in managing concentration of credit risk would be assessed in the same way as any other sales made in the business model.

Yes Yes

A third measurement category – FVOCI

The FVTPL measurement category would be retained as the residual category.

No No

Clarifying the proposed application guidance for the FVTPL measurement category

The final standard would clarify the following points.

• When financial assets are either held for trading or managed and evaluated on a fair value basis, the entity makes decisions – i.e. whether to hold or sell the asset – based on changes in, and with the objective of realising, the assets’ fair value.

• The activities that the entity undertakes are primarily focused on fair value information, and key management personnel use that information to assess the assets’ performance and to make decisions accordingly.

• Another indicator is that the users of the financial statements are primarily interested in fair value information on these assets to assess the entity’s performance.

Yes Yes

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 27

What did the IASB discuss?

What did the IASB tentatively decide? Is there an identified change to IFRS 9?

Is there an identified change to the C&M ED?

Bu

sin

ess

mo

del

(co

nti

nu

ed)

Clarifying the proposed application guidance for the FVOCI measurement category

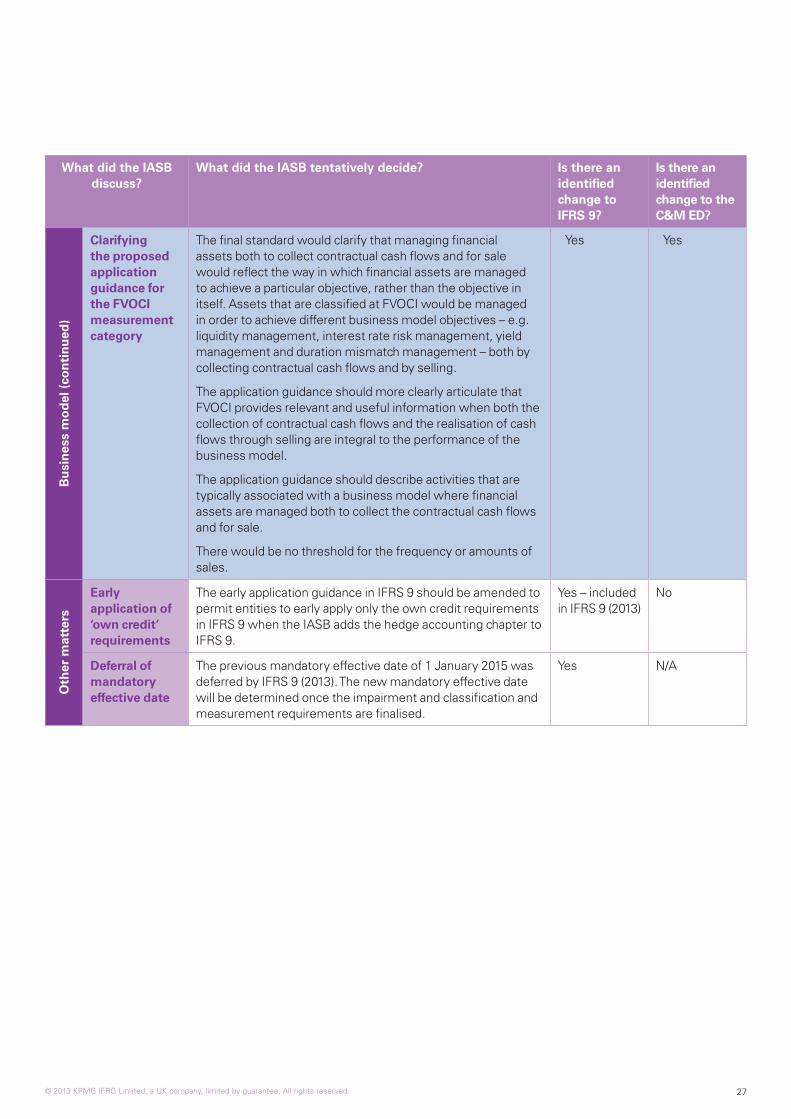

The final standard would clarify that managing financial assets both to collect contractual cash flows and for sale would reflect the way in which financial assets are managed to achieve a particular objective, rather than the objective in itself. Assets that are classified at FVOCI would be managed in order to achieve different business model objectives – e.g. liquidity management, interest rate risk management, yield management and duration mismatch management – both by collecting contractual cash flows and by selling.

The application guidance should more clearly articulate that FVOCI provides relevant and useful information when both the collection of contractual cash flows and the realisation of cash flows through selling are integral to the performance of the business model.

The application guidance should describe activities that are typically associated with a business model where financial assets are managed both to collect the contractual cash flows and for sale.

There would be no threshold for the frequency or amounts of sales.

Yes Yes

Oth

er m

atte

rs

Early application of ‘own credit’ requirements

The early application guidance in IFRS 9 should be amended to permit entities to early apply only the own credit requirements in IFRS 9 when the IASB adds the hedge accounting chapter to IFRS 9.

Yes – included in IFRS 9 (2013)

No

Deferral of mandatory effective date

The previous mandatory effective date of 1 January 2015 was deferred by IFRS 9 (2013). The new mandatory effective date will be determined once the impairment and classification and measurement requirements are finalised.

Yes N/A

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 28

APPENDIX B: SUMMARY OF IASB’S REDELIBERATIONS ON THE IMPAIRMENT ED

Note: Decisions made in November 2013 are shaded.

What did the IASB discuss? What did the IASB tentatively decide? Is there an identified change to the impairment ED?

Th

e ge

ner

al p

rin

cip

les

Responsiveness of the impairment model to forward-looking information

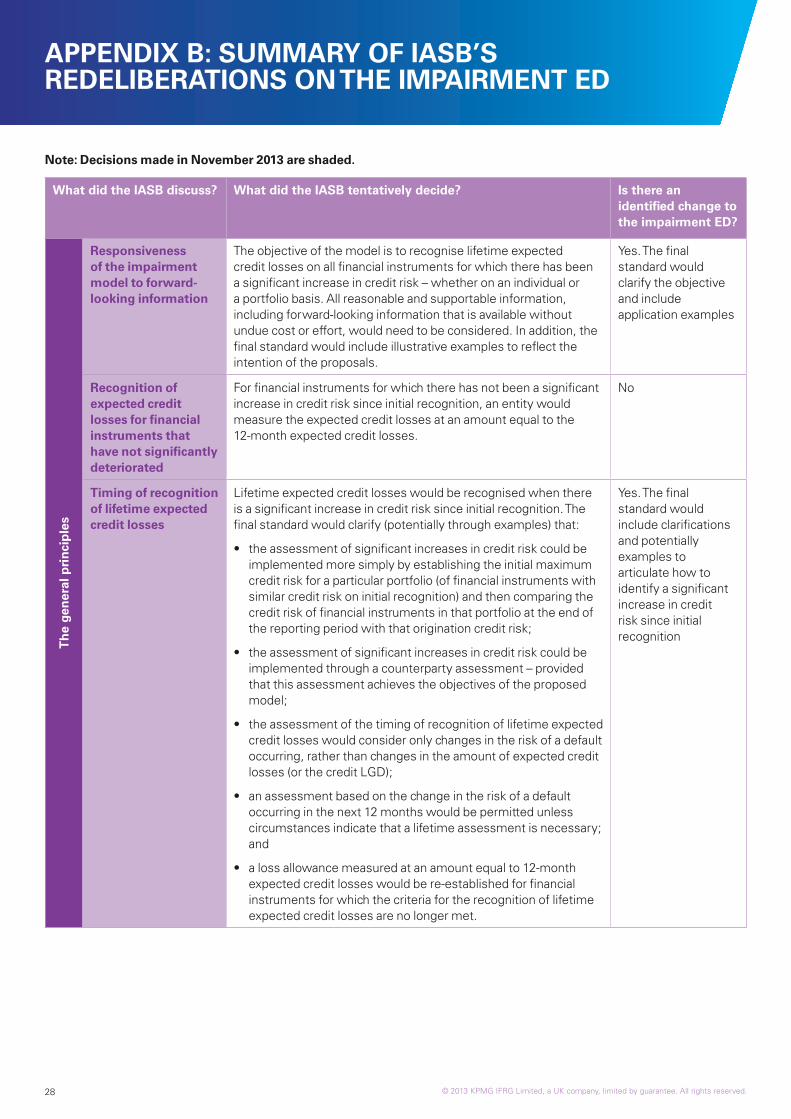

The objective of the model is to recognise lifetime expected credit losses on all financial instruments for which there has been a significant increase in credit risk – whether on an individual or a portfolio basis. All reasonable and supportable information, including forward-looking information that is available without undue cost or effort, would need to be considered. In addition, the final standard would include illustrative examples to reflect the intention of the proposals.

Yes. The final standard would clarify the objective and include application examples

Recognition of expected credit losses for financial instruments that have not significantly deteriorated

For financial instruments for which there has not been a significant increase in credit risk since initial recognition, an entity would measure the expected credit losses at an amount equal to the 12-month expected credit losses.

No

Timing of recognition of lifetime expected credit losses

Lifetime expected credit losses would be recognised when there is a significant increase in credit risk since initial recognition. The final standard would clarify (potentially through examples) that:

• the assessment of significant increases in credit risk could be implemented more simply by establishing the initial maximum credit risk for a particular portfolio (of financial instruments with similar credit risk on initial recognition) and then comparing the credit risk of financial instruments in that portfolio at the end of the reporting period with that origination credit risk;

• the assessment of significant increases in credit risk could be implemented through a counterparty assessment – provided that this assessment achieves the objectives of the proposed model;

• the assessment of the timing of recognition of lifetime expected credit losses would consider only changes in the risk of a default occurring, rather than changes in the amount of expected credit losses (or the credit LGD);

• an assessment based on the change in the risk of a default occurring in the next 12 months would be permitted unless circumstances indicate that a lifetime assessment is necessary; and

• a loss allowance measured at an amount equal to 12-month expected credit losses would be re-established for financial instruments for which the criteria for the recognition of lifetime expected credit losses are no longer met.

Yes. The final standard would include clarifications and potentially examples to articulate how to identify a significant increase in credit risk since initial recognition

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 29

What did the IASB discuss? What did the IASB tentatively decide? Is there an identified change to the impairment ED?

Th

e ge

ner

al p

rin

cip

les

(co

nti

nu

ed)

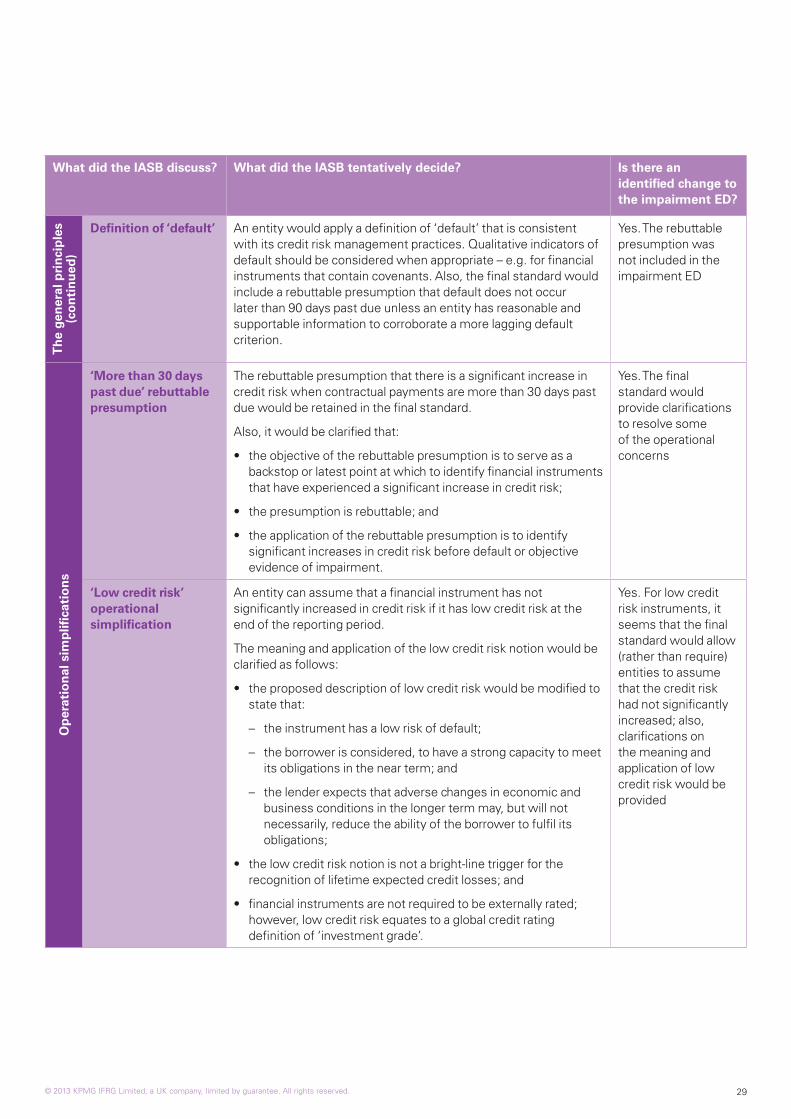

Definition of ‘default’ An entity would apply a definition of ‘default’ that is consistent with its credit risk management practices. Qualitative indicators of default should be considered when appropriate – e.g. for financial instruments that contain covenants. Also, the final standard would include a rebuttable presumption that default does not occur later than 90 days past due unless an entity has reasonable and supportable information to corroborate a more lagging default criterion.

Yes. The rebuttable presumption was not included in the impairment ED

Op

erat

ion

al s

imp

lifica

tio

ns

‘More than 30 days past due’ rebuttable presumption

The rebuttable presumption that there is a significant increase in credit risk when contractual payments are more than 30 days past due would be retained in the final standard.

Also, it would be clarified that:

• the objective of the rebuttable presumption is to serve as a backstop or latest point at which to identify financial instruments that have experienced a significant increase in credit risk;

• the presumption is rebuttable; and

• the application of the rebuttable presumption is to identify significant increases in credit risk before default or objective evidence of impairment.

Yes. The final standard would provide clarifications to resolve some of the operational concerns

‘Low credit risk’ operational simplification

An entity can assume that a financial instrument has not significantly increased in credit risk if it has low credit risk at the end of the reporting period.

The meaning and application of the low credit risk notion would be clarified as follows:

• the proposed description of low credit risk would be modified to state that:

– the instrument has a low risk of default;

– the borrower is considered, to have a strong capacity to meet its obligations in the near term; and

– the lender expects that adverse changes in economic and business conditions in the longer term may, but will not necessarily, reduce the ability of the borrower to fulfil its obligations;

• the low credit risk notion is not a bright-line trigger for the recognition of lifetime expected credit losses; and

• financial instruments are not required to be externally rated; however, low credit risk equates to a global credit rating definition of ‘investment grade’.

Yes. For low credit risk instruments, it seems that the final standard would allow (rather than require) entities to assume that the credit risk had not significantly increased; also, clarifications on the meaning and application of low credit risk would be provided

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 30

What did the IASB discuss? What did the IASB tentatively decide? Is there an identified change to the impairment ED?

Mea

sure

men

t o

f ex

pec

ted

cre

dit

loss

es

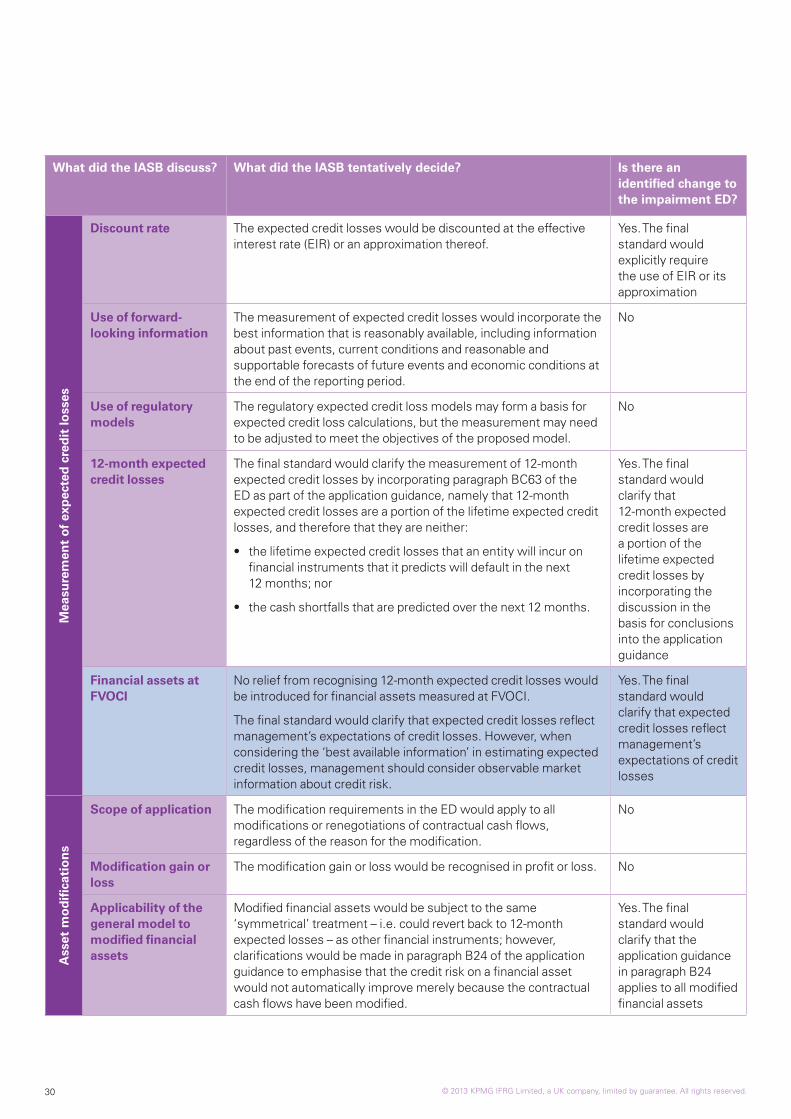

Discount rate The expected credit losses would be discounted at the effective interest rate (EIR) or an approximation thereof.

Yes. The final standard would explicitly require the use of EIR or its approximation

Use of forward-looking information

The measurement of expected credit losses would incorporate the best information that is reasonably available, including information about past events, current conditions and reasonable and supportable forecasts of future events and economic conditions at the end of the reporting period.

No

Use of regulatory models

The regulatory expected credit loss models may form a basis for expected credit loss calculations, but the measurement may need to be adjusted to meet the objectives of the proposed model.

No

12-month expected credit losses

The final standard would clarify the measurement of 12-month expected credit losses by incorporating paragraph BC63 of the ED as part of the application guidance, namely that 12-month expected credit losses are a portion of the lifetime expected credit losses, and therefore that they are neither:

• the lifetime expected credit losses that an entity will incur on financial instruments that it predicts will default in the next 12 months; nor

• the cash shortfalls that are predicted over the next 12 months.

Yes. The final standard would clarify that 12-month expected credit losses are a portion of the lifetime expected credit losses by incorporating the discussion in the basis for conclusions into the application guidance

Financial assets at FVOCI

No relief from recognising 12-month expected credit losses would be introduced for financial assets measured at FVOCI.

The final standard would clarify that expected credit losses reflect management’s expectations of credit losses. However, when considering the ‘best available information’ in estimating expected credit losses, management should consider observable market information about credit risk.

Yes. The final standard would clarify that expected credit losses reflect management’s expectations of credit losses

Ass

et m

od

ifica

tio

ns

Scope of application The modification requirements in the ED would apply to all modifications or renegotiations of contractual cash flows, regardless of the reason for the modification.

No

Modification gain or loss

The modification gain or loss would be recognised in profit or loss. No

Applicability of the general model to modified financial assets

Modified financial assets would be subject to the same ‘symmetrical’ treatment – i.e. could revert back to 12-month expected losses – as other financial instruments; however, clarifications would be made in paragraph B24 of the application guidance to emphasise that the credit risk on a financial asset would not automatically improve merely because the contractual cash flows have been modified.

Yes. The final standard would clarify that the application guidance in paragraph B24 applies to all modified financial assets

© 2013 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved. 31

What did the IASB discuss? What did the IASB tentatively decide? Is there an identified change to the impairment ED?

Rev

olv

ing

cre

dit

faci

litie

s

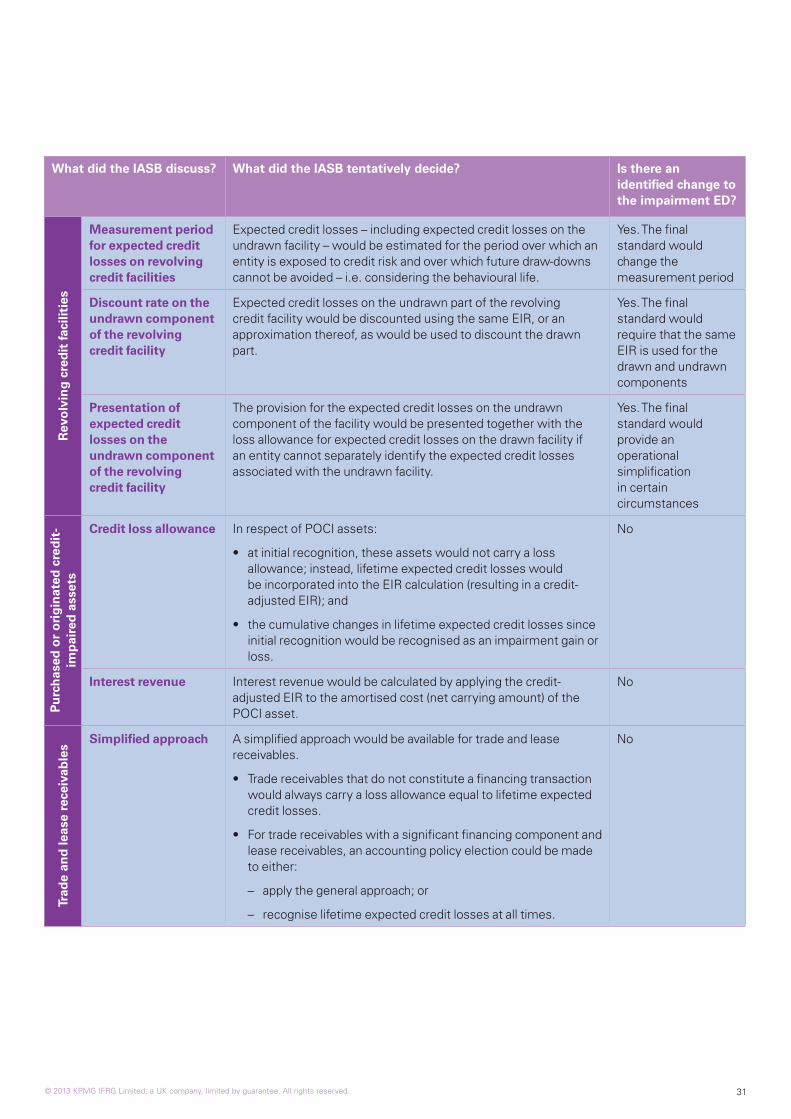

Measurement period for expected credit losses on revolving credit facilities

Expected credit losses – including expected credit losses on the undrawn facility – would be estimated for the period over which an entity is exposed to credit risk and over which future draw-downs cannot be avoided – i.e. considering the behavioural life.

Yes. The final standard would change the measurement period

Discount rate on the undrawn component of the revolving credit facility

Expected credit losses on the undrawn part of the revolving credit facility would be discounted using the same EIR, or an approximation thereof, as would be used to discount the drawn part.

Yes. The final standard would require that the same EIR is used for the drawn and undrawn components

Presentation of expected credit losses on the undrawn component of the revolving credit facility

The provision for the expected credit losses on the undrawn component of the facility would be presented together with the loss allowance for expected credit losses on the drawn facility if an entity cannot separately identify the expected credit losses associated with the undrawn facility.

Yes. The final standard would provide an operational simplification in certain circumstances

Pu

rch

ased

or

ori

gin

ated

cre

dit

-im

pai

red

ass

ets

Credit loss allowance In respect of POCI assets:

• at initial recognition, these assets would not carry a loss allowance; instead, lifetime expected credit losses would be incorporated into the EIR calculation (resulting in a credit-adjusted EIR); and

• the cumulative changes in lifetime expected credit losses since initial recognition would be recognised as an impairment gain or loss.

No

Interest revenue Interest revenue would be calculated by applying the credit-adjusted EIR to the amortised cost (net carrying amount) of the POCI asset.

No

Trad

e an

d le

ase

rece

ivab

les