IFRS - Impact on India Businesses and SAP Solution_Malolan Patanki, SAP Consulting

Upload

dawson-brittoCategory

view

222download

0

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 1/12

IFRS

Presenters-

Rakesh Kumar

Dawson Britto

Pankaj Singla

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 2/12

Diversity of international accounting practice

Accounting practices can differ substantially across

countries for instance. Development Expenses can becapitalised in Australia subject to criteria but are notallowed to be capitalised in United States

Other factors leading to diversity:

Culture

Religion

Why IFRS

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 3/12

International adoption of IFRS

Apparently diversity creates challenges for

international business and investments.

As a result, accounting standard setters andgovernments have been working on reducing diversityand align accounting requirements worldwide.

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 4/12

Harmonisation, convergence and adoption

Both of these process take place overtime but differ infollowing respect:

Harmonisation implies reconciling different points of view and reducing diversity, while allowing countriesto have different sets of accounting standards

Convergence implies adoption of one set of standardsacross the globe. This is often referred to as ‘Adoption

‘and ‘Standardisation’.

The objective of IASC was harmonisation while IASB isfocused on convergence.

Know the Difference

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 5/12

Benefits of Full Adoption

Cost effective to implement a comprehensive system

of accounting standards e.g.. Reduced cost of

financial reporting and auditing for MNC’s Enhances the operation and globalisation of capital

markets

Increased comparability of financial statements

Improved allocation of capital by global investors Reduced risk in international investing diversification

portfolio

Benefits of convergence

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 6/12

Limitations of Full Adoption

Conflicts with the economic, social and cultural context of different accounting systems. Also, the costs associated toovercome these issues

Conflicts with some manifestations of national sovereignty

Conflicts with the motive of reporting

Unlikely to benefit entities operating in single jurisdiction ascompared to MNC’s. Inturn increased compliance costs mayeffect negatively.

Issues with fair value adoption

Limitations of convergence

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 7/12

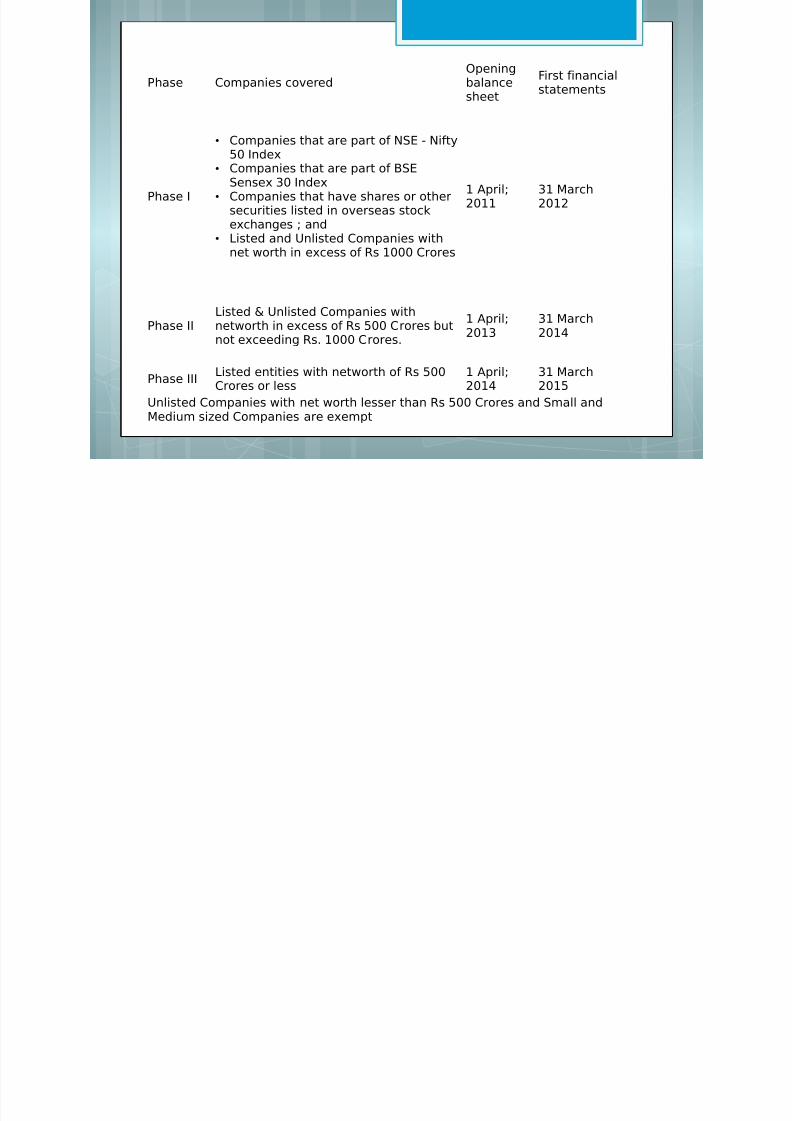

IFRS reporting in India - Proposed Timelines

The Ministry of Corporate Affairs (MCA) issued a press release on January 22, 2010 on the much awaited roadmap on India’sconvergence to IFRS.

As per this roadmap, there will be two separate sets of AccountingStandards under Section 211(3C) of the Companies Act, 1956

(India).

The first set would comprise Indian Accounting Standards which areconverged with the IFRSs (‘Converged Standards’) and will beapplicable to the specified class of companies.

The second set would comprise existing Indian Accounting Standardsand will be applicable to other companies, including Small andMedium Companies (SMCs).

The Converged Standards would apply in a Phased manner asindicated below:

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 8/12

Phase Companies coveredOpeningbalancesheet

First financialstatements

Phase I

• Companies that are part of NSE - Nifty50 Index

• Companies that are part of BSESensex 30 Index

• Companies that have shares or other

securities listed in overseas stockexchanges ; and• Listed and Unlisted Companies with

net worth in excess of Rs 1000 Crores

1 April;2011

31 March2012

Phase II

Listed & Unlisted Companies with

networth in excess of Rs 500 Crores butnot exceeding Rs. 1000 Crores.

1 April;2013 31 March2014

Phase IIIListed entities with networth of Rs 500Crores or less

1 April;2014

31 March2015

Unlisted Companies with net worth lesser than Rs 500 Crores and Small andMedium sized Companies are exempt

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 9/12

Convergence with IFRSs: Indian Perspective

Indian Accounting Standards (ASs) are formulated on the basis of the

IFRSs. While formulating ASs, the endeavor of the ICAI remains to converge

with the IFRSs. The ICAI has till date issued 29 ASs corresponding to IFRSs.

Some recent ASs, issued by the ICAI, are totally at par with thecorresponding IFRSs, e.g., the Standards on ‘Impairment of Assets’ and

‘Construction Contracts’. While formulating Indian Accounting Standards, changes from the

corresponding IAS/ IFRS are made only in those cases where these areunavoidable considering: Legal and/ or regulatory framework prevailing in the country. To reduce or eliminate the alternatives so as to ensure

comparability. State of economic environment in the country Level of preparedness of various interest groups involved in

implementing the accounting standards.

T N Manoharan ( President, ICAI)

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 10/12

Benefits of convergence to India

High comparability and credibility with enhancedconducive investment environment.

Easy access to finance

Increased global investors confidence

Enhanced business opportunities

Opportunity for Indian accounting professionals on a

global frontier

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 11/12

Investment obstacles in Indian markets from perspective of an international investor

Higher Risk

Lacks comparability

Unfamiliar cultural and political circumstances

Reduced economic growth rate

Onerous monetary policy and stringent FDIinvestment licencing laws.

7/28/2019 IFRS and INdia

http://slidepdf.com/reader/full/ifrs-and-india 12/12

References http://business.blogs.cnn.com/2012/12/18/counting-indias-obstacl

/

http://www.grantthornton.in/html/services/ifrs.php