IFRS 9 tools - ey.comFILE/ey... · E x e c u t i v e su m m a r y The IASB has issued the final...

16

IFRS 9 tools Powerful enablers to accelerate your IFRS 9 implementation

Transcript of IFRS 9 tools - ey.comFILE/ey... · E x e c u t i v e su m m a r y The IASB has issued the final...

IFRS 9 toolsPowerful enablers to accelerate your IFRS 9 implementation

ContentsExecutive summary ...........................................................................1

Overview of powerful IFRS 9 tools .....................................................2

EY LIC Solution® ................................................................................3

EY IFRS 9 impairment analyzer .........................................................5

EY IFRS 9 progress analyzer (ECB attention point)............................8

EY IFRS 9 challenger tool (BCBS 350/EBA CP 2016) .........................9

EY IFRS 9 SPPI checklist .................................................................10

EY ICE .............................................................................................11

EY IFRS 9 SPPI engine for loans ......................................................12

Contacts .........................................................................................12

E x e c u t i v e su m m a r y

► The IASB has issued the final version of IFRS 9 that incorporates new regulation on the accounting for financial instruments. The main requirements are:

► Classification and measurement of financial instruments depending on two assessments:

► Their contractual cash flows and

► The entity’s business models

► Impairments, based on either 12-month or lifetime expected credit losses, depending particularly on whether there has been a significant increase in credit risk since initial recognition

► Extensive notes disclosures (IFRS 7)

► With the EU endorsement in Q4 2016, the mandatory date of initial adoption will be 1 January 2018.

► On the basis of various project experience, EY has developed different IFRS 9 tools to facilitate a goal-oriented and quality-assured implementation of IFRS 9.

B a c k g r ou n d1

► Our Financial Services (FS) are an integrated area that includes many professionals and IFRS 9 experts across many countries (UK, Germany, France, India and many more), and collaborates across competencies (Advisory, Assurance, Tax, Transaction Advisory).

► EY has been engaged by many global banks for accounting change projects on a group-wide basis. We thus understand the complexities, challenges and opportunities of implementing IFRS across multiple geographies, business units and diverse portfolios.

► Thus, we are one of the market-leading organizations for IFRS advisory services with particular focus on IFRS 9 end-to-end implementation projects.

► We have gathered extensive IFRS 9 project experience and knowledge regarding key accounting and project decisions to be taken to allow quick and robust IFRS 9 implementation.

► In addition, we have developed several IFRS 9 tools and enablers on all key challenges, such as project management, SPPI testing and impairment calculations.

► These experiences enable us to serve our smaller — or medium-sized clients on their IFRS 9 implementation projects.

W h y E Y3

► We have developed several IFRS 9 tools to facilitate the IFRS 9 implementation at every level dimension, such as:

► SPPI assessment — e.g., the automated ISIN/CUSIP Analyser that provides a completely automated SPPI assessment on the basis of the provided SIN/CUSIP (EY ICE) or the manual SPPI Checklist for those financial assets without an ISIN/CUSIP ID

► ECL measurements — e.g., EY LIC Solution®, as a modular productive system for ECL calculation

► IFRS 9 challenge tool: challenges your IFRS 9 implementation against supervisors expectations

► The usage of the tools allows you to check your actual IFRS 9 implementation status and to accelerate your project.

O v e r v i e w of ou r IFRS 9 t ools2 E Y i s t h e m a r k e t le a d e r f or IFRS 9 e n d - t o- e n d e x e c u t i on p r oj e c t s

Our IFRS 9 in a box-capability enables IFRS

9-implementation within a few months

1IFRS 9 Tools

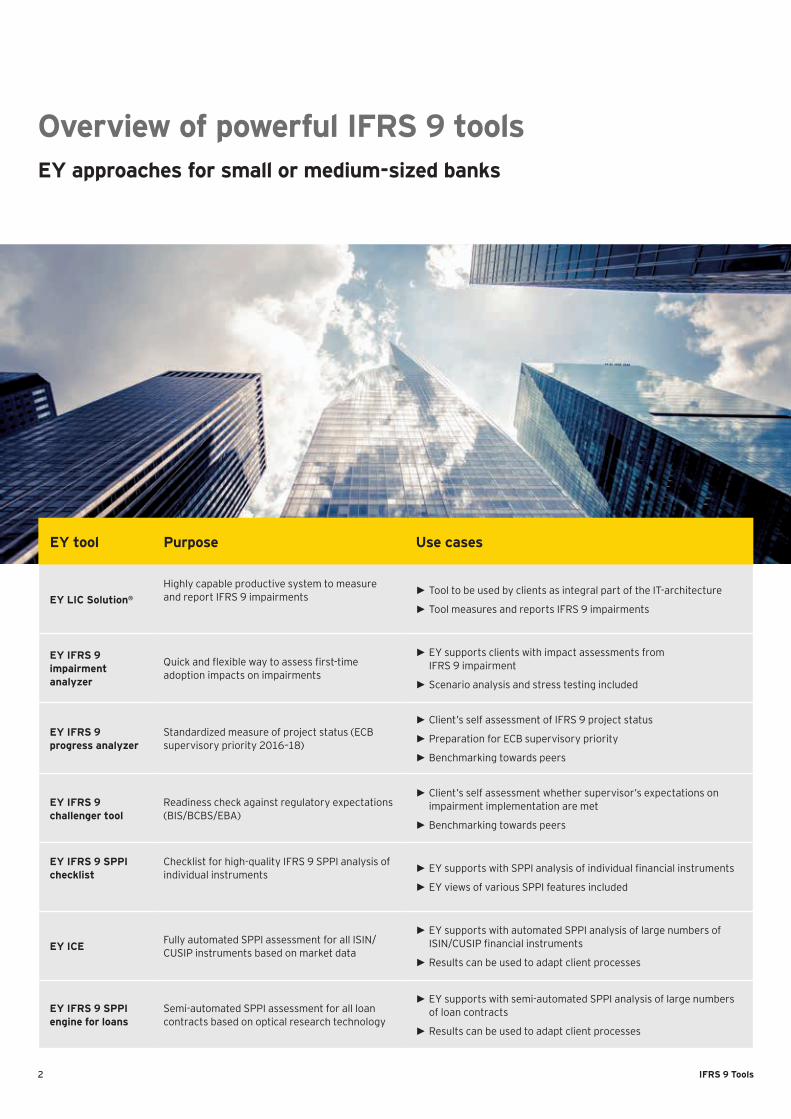

O v e r v i e w of p ow e r f u l IFRS 9 t oolsE Y a p p r oa c h e s f or sm a ll or m e d i u m - si z e d b a n k s

E Y t ool P u r p ose U se c a se s

E Y L IC Solu t i on ®

Highly capable productive system to measure and report IFRS 9 impairments ► Tool to be used by clients as integral part of the IT-architecture

► Tool measures and reports IFRS 9 impairments

E Y IFRS 9 i m p a i r m e n t a n a ly z e r

Quick and flexible way to assess first-time adoption impacts on impairments

► EY supports clients with impact assessments from IFRS 9 impairment

► Scenario analysis and stress testing included

E Y IFRS 9 p r og r e ss a n a ly z e r

Standardized measure of project status (ECB supervisory priority 2016–18)

► Client’s self assessment of IFRS 9 project status

► Preparation for ECB supervisory priority

► Benchmarking towards peers

E Y IFRS 9 c h a lle n g e r t ool

Readiness check against regulatory expectations (BIS/BCBS/EBA)

► Client’s self assessment whether supervisor’s expectations on impairment implementation are met

► Benchmarking towards peers

E Y IFRS 9 SP P I c h e c k li st

Checklist for high-quality IFRS 9 SPPI analysis of individual instruments ► EY supports with SPPI analysis of individual financial instruments

► EY views of various SPPI features included

E Y IC E Fully automated SPPI assessment for all ISIN/CUSIP instruments based on market data

► EY supports with automated SPPI analysis of large numbers of ISIN/CUSIP financial instruments

► Results can be used to adapt client processes

E Y IFRS 9 SP P I e n g i n e f or loa n s

Semi-automated SPPI assessment for all loan contracts based on optical research technology

► EY supports with semi-automated SPPI analysis of large numbers of loan contracts

► Results can be used to adapt client processes

2 IFRS 9 Tools

E Y L IC Solu t i on ® — ov e r v i e w

W h y E Y IFRS 9 E Y L IC Solu t i on ® c a n m a k e a d i f f e r e n c e

W h a t c a n i t d o f or y ou ?

The EY LIC Solution® is a powerful technical platform that enables you to cope with key challenges from IFRS 9 impairment

W h a t d oe s i t n e e d ?

► Basic loan file inputs based on clear data requirements

► Credit risk parameters (probability of default, loss given default), if available

► In case of missing data, flexible solutions can be applied

H ow d oe s i t w or k ?

► The EY LIC Solution® is a modular IFRS 9 solution which can be seamlessly integrated in your IT system architecture

► Based on your input data, the EY LIC Solution® provides you with granular expected credit loss-data for each stage according to IFRS 9

► The EY LIC Solution® covers various functionalities, such as a data interface layer, flexible parametrizations, IFRS 9 stage allocation, expected credit loss calculations (12 month and lifetime), collective or individual assessments, effective interest rate calculations and many more

IFRS 9 f u n c t i on a li t y c ov e r e d

E st a b li sh e d solu t i on a p p r oa c h

► We are able to provide the core required functionality within six months from the project kick-off in line with your release plan

► We team up with integration collaborators to provide you with end-to-end integration of our solution into your existing IT environment

► The solution is ready for parallel runs of IFRS 9, IAS 39 and local standards

► Our IFRS 9 EY LIC Solution® is designed to process large data volumes to calculate expected credit losses according to IFRS 9

► Our IFRS 9 EY LIC Solution® can be seamlessly integrated in your current IT architecture

► Our IFRS EY LIC Solution® has already been tested successfully at many financial institutions and passed several reviews

► Our IFRS 9 EY LIC Solution® covers all functionalities required for LLP calculation, EIR calculation, accounting entries and customized reporting

► The solution is ready for parallel runs of IFRS 9, IAS 39 and local standards

► Delivery toolkit available offering an efficient service by means of a standardized work product

► The approach is already being used by several financial institutions and has proven its capabilities in practice

► Our solution team has international hands-on experience with IAS 39 and IFRS 9 implementation projects

Seamless implementation and flexible integration

P r ov e n t r a c k r e c or d

3IFRS 9 Tools

E Y L IC Solu t i on ® — i m p a i r m e n t c ov e r a g e a n d m od u le b a se d a r c h i t e c t u r e

In t e g r a t i on t o a b a n k ’ s e n v i r on m e n t — i llu st r a t i v e log i c a l sc h e m e

D a t a In t e g r a t i on a n d c on soli d a t i on la y e r

In p u t d a t a q u a li t y v a li d a t i on

O u t p u t d a t a g e n e r a t or

In p u t d a t a t r a n sf or m a t i on a n d loa d

Fu n c t i on a l m od u le sSetup

IT security and auditing module

User management

Configuration module

EIR

EIR calculation

EIR and linear amortization

Unwinding of interest

Allowances

Segmentation

Individual

Portfolio

Stage 1 -> 2 transition

Cash flow generation

PD built-in methods

Exposure modelling

Collateral allocation

LGD built-in methods

Reporting

GL accounting entries engine

Customized Report Builder

Back testing

Core modules

Interfacing Bank systems

Output data integration layer

Input data integration layer

Data transformation

Data extraction

Bank’s target systems

Data migration from source

systems

Bank’s responsibility

Calculation engine

EY responsibility

Data export to target systems

GL, DWHCBS, DWH

E Y

L IC Solu t i on ®

The LIC Solution® is a highly modular product. Functional modules can be plugged in and flexibly configured upon your exact demands on a step-by-step basis. The LIC Solution® has a separate layer for input and output data which represents interface to the bank’s system landscape. We support you during the whole implementation process, provide training to both the users and offer an on-going support services after implementation of the LIC Solution®.

Data flow from source systems to LIC Solution® and back from the solution to bank’s systems is described in the scheme below. Input data are extracted by the bank from source systems and stored in an input data staging area. Both data transformation, upload to LIC Solution® and extraction of output data is processed by EY. Data export and storage in bank’s target systems is carried out by the bank.

4 IFRS 9 Tools

E Y IFRS 9 i m p a i r m e n t a n a ly z e r — ov e r v i e w

W h a t c a n i t d o f or y ou ?

► The EY IFRS 9 Impairment Analyzer is a transparent, flexible and powerful tool developed to quickly and effectively assess options and impacts regarding IFRS 9 expected credit loss methods

► It will support clients in understanding the financial impact of IFRS 9 and its drivers

► The solution is accelerated by a standardized platform, developed specifically for IFRS 9 calculations

H ow d oe s i t w or k ?

► The MS Access based EY Impairment Analyzer is easy to deploy and highly adaptive to client-specific needs in the process of IFRS 9 transition, offering potent visualizations in MS Excel

W h a t d oe s i t n e e d ?

P or t f oli o D a t a :

► Only basic portfolio data is required to run expected credit loss calculations (current exposure, contractual end date, portfolio segmentation)

► Other data can be used and added to obtain more precise results if required

Risk Parameter specific data to model t h e r i sk m e t h od olog y

► PD: Master scale, transition matrix, cumulative PD curve, contract-specific PDs, and more

► LGD: Segmentation, calculation methods, LGD curves, collateral curves, and more

► EAD: Exposure profiles, repayment structure, nominal and effective interest rate (on loan level), and more

► CCF: Segmentation, drawing behavior, and more

Th e E Y IFRS 9 i m p a i r m e n t a n a ly z e r i s u se d i n ov e r 2 5 c ou n t r i e s b y m or e t h a n 8 0 sp e c i a lly t r a i n e d p r of e ssi on a ls

5IFRS 9 Tools

E Y IFRS 9 i m p a i r m e n t a n a ly z e r — f u n c t i on a li t i e s

6 IFRS 9 Tools

Im p a c t St u d y on IFRS 9 i m p a i r m e n t ► Definition of an IFRS 9 compliant concept meeting the clients

needs, data and process impact and establishment of the project structure, timeliness, tasks and dependencies

► Impact assessment of possible methodological options, model setup and calibration

► Simulation using best proxy models to get a first picture

IFRS 9 E C L m od e li n g ► Development of risk parameters with respect to the IFRS 9

requirements (PD, LGD, EAD, CCF)

► Review of adjustment approaches for risk parameter methodologies already developed by the client

► Measurement of loss provision sensitivity with respect to risk parameters

Identification of Significant increase i n C r e d i t Ri sk

► Identification of available data that is suitable to identify credit risk increases

► Development of a methodology for the identification of significant credit risk increases

► Measurement of loss provision sensitivity with respect to the available methodological approaches

E Y IFRS 9 i m p a i r m e n t a n a ly z e r — p r oc e ssEstablished five step process to assess impairment methodology impact

St e p 1 : P or t f oli o D a t a Se le c t i on a n d P r e v i e w ► Portfolios are imported using .txt or .csv files

► Preview of portfolio data, information on format (text, numeric or date) and number of positions

St e p 2 : Fi e ld M a p p i n g a n d P or t f oli o D a t a Im p or t ► Delivered portfolio data is transferred to the data base

► Up to 255 internal fields can be defined using the EY Field Manager to cover significant information (e.g., risk model parameters)

St e p 3 : Tr a n sf or m P or t f oli o D a t a ► Incomplete/false data can be adjusted using custom made rules

► Rules can be performed for different segments of the portfolio

► Audit trail to log the rules applied to the imported data

St e p 4 : Im p a i r m e n t Ru le Se t u p a n d Im p a i r m e n t C a lc u la t i on s

► Rule Developer Module provides functions to set up risk parameters (PD, LGD, EAD, CCF) and stage allocation ranging from simple to complex, individually for each scenario

► “In Tool” analysis of the impairment calculation (aggregated to individual calculation on loan level for fast assessments or in detail)

St e p 5 : Im p a i r m e n t Re su lt V i su a li z a t i on s a n d D a t a E x p or t

► Predefined and custom made visualizations are exported to Excel to assess the impact on the impairment numbers for each scenario

► Custom visualizations are available, e.g., impact assessment, overview table, average risk parameter values per portfolio segment, …

► Possible visualizations: Tables, Bar charts, Pie charts, Bubble charts

K e y Fu n c t i on a li t y : P or t f oli o D a t a P r e - P r oc e ssi n g

K e y Fu n c t i on a li t y : Im p a i r m e n t Sc e n a r i o Se t u p a n d A n a ly si s

7IFRS 9 Tools

Rule Setup and Impairment Calculations

Transform Portfolio Data

Field Mapping and Portfolio Data Import

Portfolio Data Selection and Preview

Visualizations of Impairment Results

E Y IFRS 9 p r og r e ss a n a ly z e r ( E C B a t t e n t i on p oi n t )

B a c k g r ou n d C h a lle n g e s f or c li e n t s

► ECB supervisory priorities announced

► IFRS 9 implementation is one priority

► Focus on current implementation status

► Peer group standing as benchmark

► What‘s the status?

► How to measure across workstreams?

► How to compare with peers?

► How to comply with ECB expectations?

Benefits for clientsE Y IFRS 9 p r og r e ss a n a ly z e r a n d m e t h od olog y

► Standardized measure of project status

► All common workstreams covered

► Benchmarking to peer banks possible

► EY experience on supervisors views

E Y

Self assessment Risk analysis Benchmarking Remediation

W h a t c a n i t d o?

► ECB has announced its priorities for supervisory plans 2016 and beyond. One priority is the implementation status of IFRS 9

► The solution provides clients with an independent project status check and allows benchmarking its implementation status against peers

► On the basis of this, clients may be sensitized toward the ECBs perspective regarding the clients IFRS 9 implementation status

W h a t d oe s i t n e e d ?

► Standardized answers on multiple choice questions

H ow d oe s i t w or k ?

► It works on the basis of a web-based questionnaire that allows quick handling by the client and standardized analysis by EY

► The presentation of results (slides and graphs) will be prepared by the EY teams and provided to the clients

8 IFRS 9 Tools

N e g le c t i n g B C B S 3 5 0 / E B A C P 2 0 1 6 / 1 0 i n IFRS 9 p r oj e c t s m i g h t b e a b a d i d e a …

… a n d se r v e s a s b a si s f or r e m e d i a t i on m e a su r e s.

Tool e x h i b i t s G A P s a g a i n st B C B S 3 5 0 / E B A C P 2 0 1 6 / 1 0 r e a d i n e ss …

… t h a t ‘ s w h y E Y d e v e lop e d t h e IFRS 9 c h a lle n g e r t ool.

E Y

1

42

3

QIS

ANA Credit IFRS 7

CRR IFRS 9

IFRS 13

Local GAAP FINREP

BCBS 239

BCBS 350

Discuss results

Consider benchmarks

Decide on remediations

Execute and close

► Reduction of complexity

► GAP analysis

► Traceable to specific requirements

► Benchmarking possible

IFRS 9 c h a lle n g e r t ool ( B C B S 3 5 0 / E B A C P 2 0 1 6 )

W h a t c a n i t d o?

► The Basel Committee of Banking Supervisors (BCBS) released its final “Guidance on credit risk and accounting for expected credit losses” in December 2015 (BCBS 350)

► This guidance mainly covers the supervisory expectations towards the implementation of the expected credit loss-model (ECL) under IFRS 9

► This guidance has been incorporated in the EBA consultation paper EBA 2016/10 and forms an important indicator of supervisors views on ECL methods

W h a t d oe s i t n e e d ?

► Standardized answers on multiple choice questions

H ow d oe s i t w or k ?

► Based on a web-based questionnaire that allows quick handling by the client and standardized analysis by EY

► The presentation of results (slides & graphs) will be prepared by the EY teams and provided to the clients

9IFRS 9 Tools

► Clear questions, simple to answer

► Focused on most relevant issues

► EY project experience included

BCBS 350/

EBA CP 2016

BCBS 350/

EBA CP 2016/10

IFRS 9

E Y IFRS 9 SP P I c h e c k li st

► Not all assets can be classified automatically (e.g., Non-ISIN assets, results not conclusive)

► Those assets have to be analyzed manually

► There are plenty of features that might harm the SPPI-criterion

C h a lle n g e s f or c li e n t s

► Suitable for all assets including CLIs

► Covers every important issue described in the standard

► Integrated documentation in predefined fields

► Easy to understand with explanations and examples to every relevant feature

E Y SP P I c h e c k li st

Nature of the financial instrument1 Is it a financial asset as defined in IAS 32? Yes No

2 Is is an equity instrument as defined in IAS 32? Yes No

3 Is is a derivative as defined in IFRS 9? Yes No

4 Is it an investment of one or more units of an investment fund? Yes No

5 Is it cash as defined in IAS 7 (not cash equivalents)? Yes No

6 Is it a contractually linked instrument (IFRS 9.B4.120-26)? Yes No

A n a ly si s of i n t e r e st e le m e n t s

7Is the instrument exposed to changes in equity prices, commodity prices or other risks or volatility unrelated to principal and/or interest (IFRS 9.B4.1.7A)?

Yes No

8 Is the instrument leveraged (IFRS 9.B4.1.9)? Yes No

9Does the interest element provide consideration for other risks or costs, i.e., not only for the time value of money (IFRS 9.B4.1.9A)?

Yes No

10Is the time value of money element modified (imperfect, e.g., tenor frequency mismatch, (IFRS 9.B4.1.9B)?

Yes No

10.1 Have you concluded that the Benchmark cash flow test has been passed? Yes No

11 Did a government or a requlatory authority set the interest rate(s) (IFRS 9.B4.1.9E)? Yes No

11.1Is the regulated interest rate “broadly consistent” with the passage of time and does not provide exposure to inconsistent risks or volatility (IFRS 9.B4.1.9E)?

Yes No

W h a t c a n i t d o?

► The EY IFRS 9 SPPI Checklist provides a complete and easy to understand guidance to conduct the manual classification in dependance of various contractual cash flow features (SPPI)

► The tool suggests a clear result on whether the cash flows are solely payments of principle and interest or not (SPPI)

► The tool is designed to facilitate a high quality SPPI-assessment based on a consistent approach covering all relevant IFRS 9 requirements

W h a t d oe s i t n e e d ?

► Contracts and Termsheets

► Answers (yes/no) to predicted questions

H ow d oe s i t w or k ?

► Checklist format that allows quick handling by the client

► Clear output on SPPI result if “fail” or “pass”

10 IFRS 9 Tools

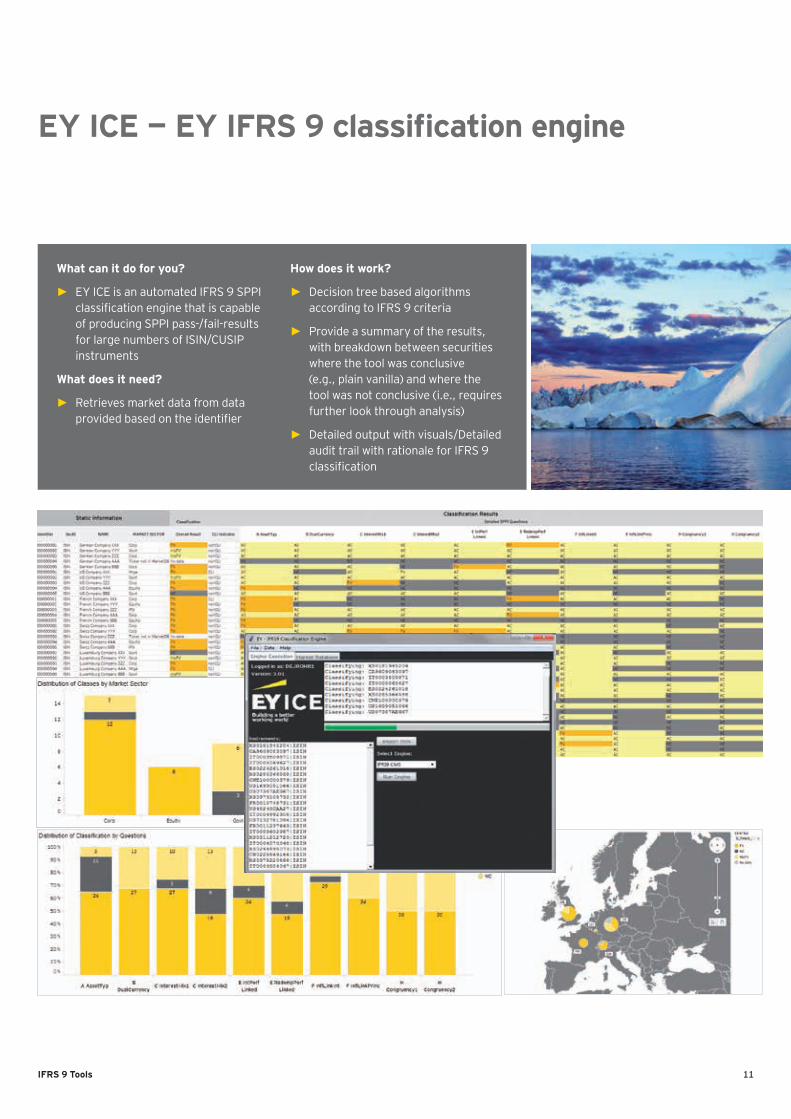

EY ICE — EY IFRS 9 classification engine

W h a t c a n i t d o f or y ou ?

► EY ICE is an automated IFRS 9 SPPI classification engine that is capable of producing SPPI pass-/fail-results for large numbers of ISIN/CUSIP instruments

W h a t d oe s i t n e e d ?

► Retrieves market data from data provided based on the identifier

H ow d oe s i t w or k ?

► Decision tree based algorithms according to IFRS 9 criteria

► Provide a summary of the results, with breakdown between securities where the tool was conclusive (e.g., plain vanilla) and where the tool was not conclusive (i.e., requires further look through analysis)

► Detailed output with visuals/Detailed audit trail with rationale for IFRS 9 classification

11IFRS 9 Tools

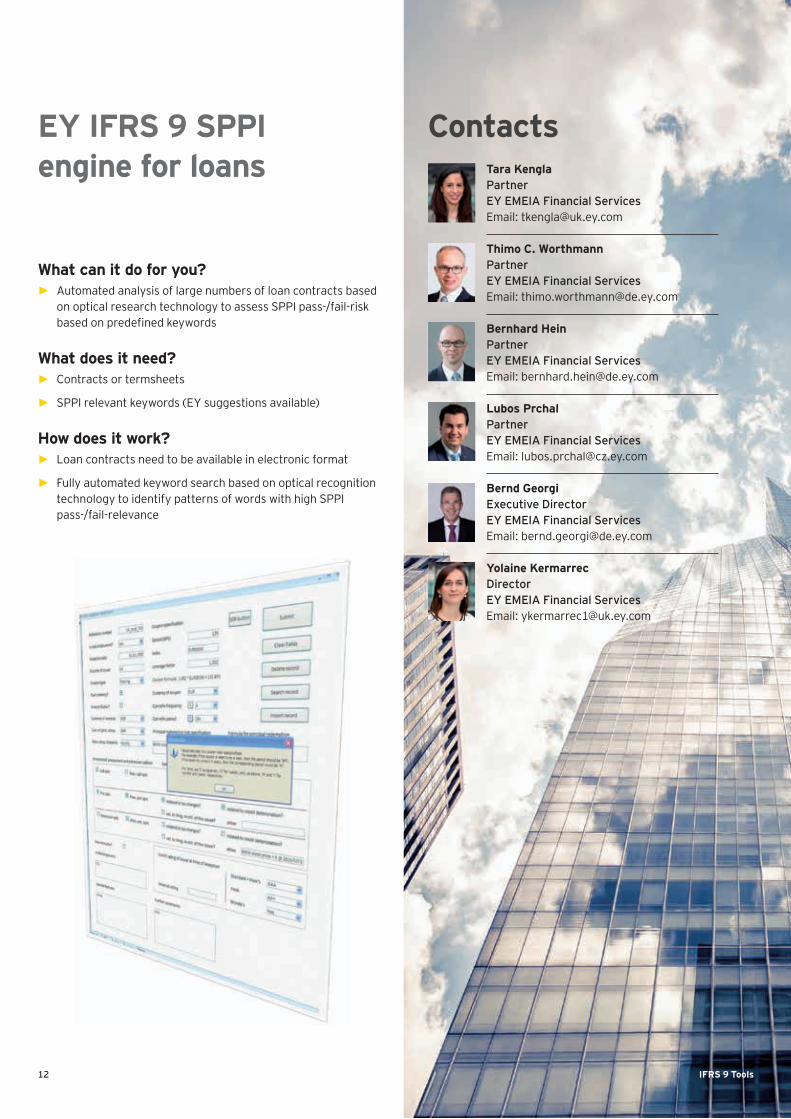

E Y IFRS 9 SP P I e n g i n e f or loa n s

W h a t c a n i t d o f or y ou ? ► Automated analysis of large numbers of loan contracts based

on optical research technology to assess SPPI pass-/fail-risk based on predefined keywords

W h a t d oe s i t n e e d ? ► Contracts or termsheets

► SPPI relevant keywords (EY suggestions available)

H ow d oe s i t w or k ? ► Loan contracts need to be available in electronic format

► Fully automated keyword search based on optical recognition technology to identify patterns of words with high SPPI pass-/fail-relevance

C on t a c t s Ta r a K e n g laPartner EY EMEIA Financial ServicesEmail: [email protected]

Th i m o C . W or t h m a n nPartnerEY EMEIA Financial ServicesEmail: [email protected]

B e r n h a r d H e i nPartnerEY EMEIA Financial ServicesEmail: [email protected]

L u b os P r c h a lPartnerEY EMEIA Financial ServicesEmail: [email protected]

B e r n d G e or g iExecutive DirectorEY EMEIA Financial ServicesEmail: [email protected]

Y ola i n e K e r m a r r e cDirector EY EMEIA Financial Services Email: [email protected]

12 IFRS 9 Tools

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

EY is a leader in serving the financial services industryWe understand the importance of asking great questions. It’s how you innovate, transform and achieve a better working world. One that benefits our clients, our people and our communities. Finance fuels our lives. No other sector can touch so many people or shape so many futures. That’s why globally we employ 26,000 people who focus on financial services and nothing else. Our connected financial services teams are dedicated to providing assurance, tax, transaction and advisory services to the banking and capital markets, insurance, and wealth and asset management sectors. It’s our global connectivity and local knowledge that ensures we deliver the insights and quality services to help build trust and confidence in the capital markets and in economies the world over. By connecting people with the right mix of knowledge and insight, we are able to ask great questions. The better the question. The better the answer. The better the world works.

© 2017 EYGM Limited. All Rights Reserved.

EYG no. 00720-174Gbl

EY-000018841.indd (UK) 02/17. Artwork by CSG London.

ED 0617

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com/fsassurance

![IFRS for SMEs 2009 - Institute of Chartered Accountants of ...1].pdf · Preface to the IFRS for SMEs The IASB P1 The International Accounting Standards Board (IASB) was established](https://static.fdocuments.net/doc/165x107/5ea630a16964022c4a163a06/ifrs-for-smes-2009-institute-of-chartered-accountants-of-1pdf-preface.jpg)