IFRS 9 : Accounting Meets Risk Management by En Shah Zain

26

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved. Bond Pricing Agency Malaysia IFRS 9 : Accounting Meets Risk Management Challenges and Solutions for Fixed Income Instruments ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD - All rights reserved. Presented by Mohd Shaharul Zain Chief Business Officer, BPAM

-

Upload

albakry-azis -

Category

Economy & Finance

-

view

154 -

download

1

Transcript of IFRS 9 : Accounting Meets Risk Management by En Shah Zain

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Bond Pricing Agency Malaysia

IFRS 9 : Accounting Meets Risk Management Challenges and Solutions for Fixed Income Instruments

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD - All rights reserved.

Presented by Mohd Shaharul Zain

Chief Business Officer, BPAM

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Content

1. Introduction to IFRS 9

2. The Expected Credit Loss Model

3. Data Sources

4. Conclusion and Summary

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Content

1. Introduction to IFRS 9

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

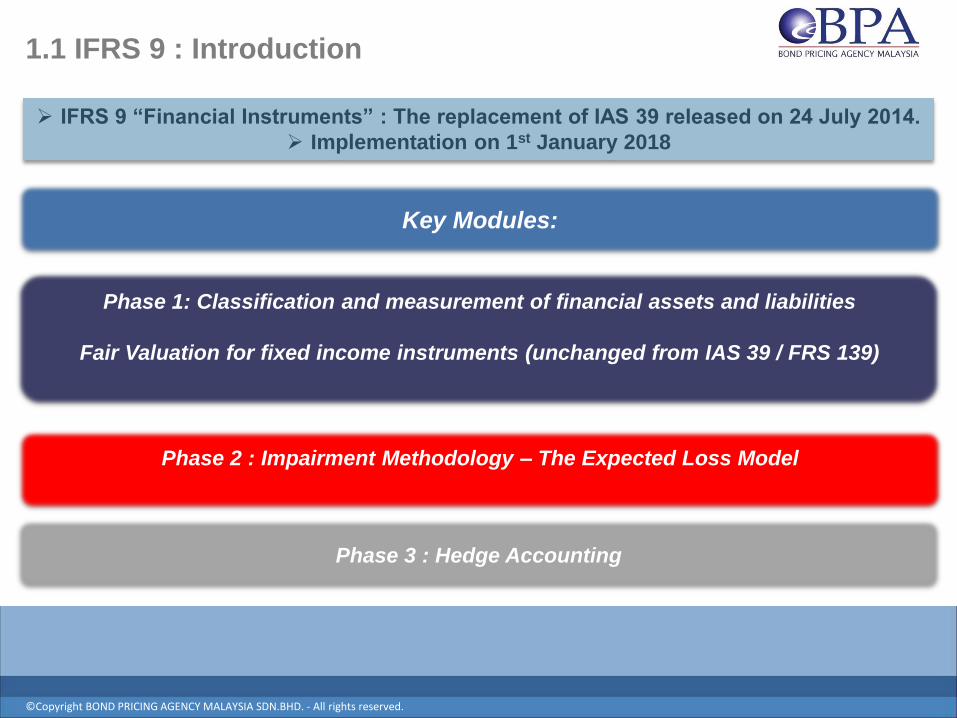

Phase 1: Classification and measurement of financial assets and liabilities

Fair Valuation for fixed income instruments (unchanged from IAS 39 / FRS 139)

IFRS 9 “Financial Instruments” : The replacement of IAS 39 released on 24 July 2014.

Implementation on 1st January 2018

Key Modules:

Phase 2 : Impairment Methodology – The Expected Loss Model

Phase 3 : Hedge Accounting

1.1 IFRS 9 : Introduction

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Determine Business Model

Treatment of Books

AMORTISATION

(HTM Book)

IMPAIRMENT PROVISIONING VIA EXPECTED CREDIT

LOSS MODEL

Fair Value Through

Profit & Loss

(Trading Book)

Mark to Market

FAIR VALUE THROUGH OTHER COMPREHENSIVE

INCOME

(AFS Book)

IMPAIRMENT PROVISIONING VIA EXPECTED CREDIT

LOSS MODEL

1.2 IFRS 9 : New Classification and Treatment

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

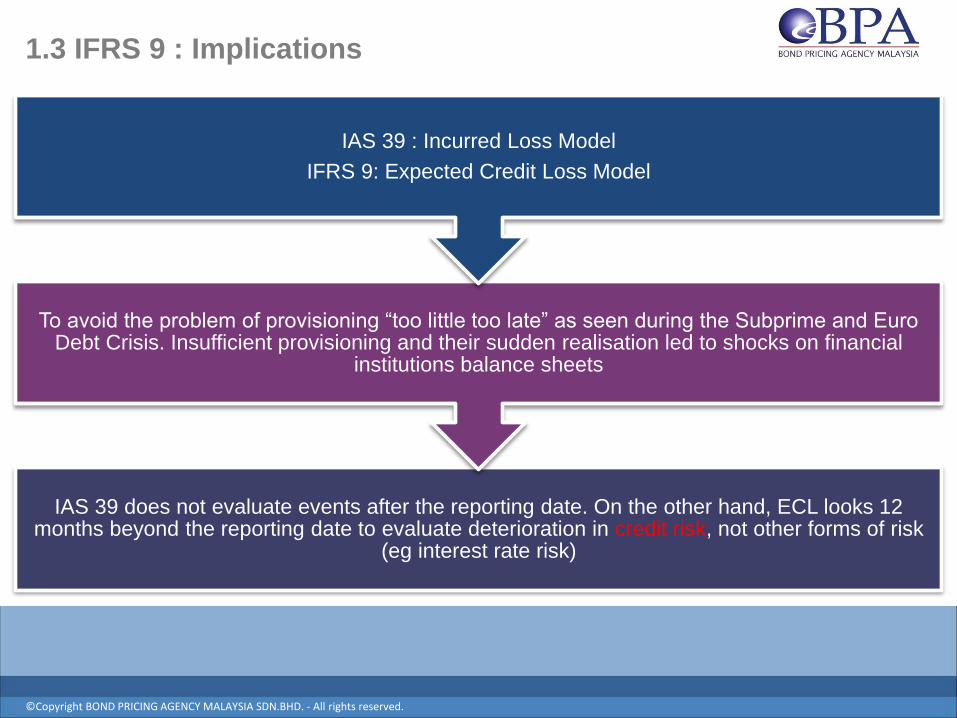

1.3 IFRS 9 : Implications

IAS 39 does not evaluate events after the reporting date. On the other hand, ECL looks 12 months beyond the reporting date to evaluate deterioration in credit risk, not other forms of risk

(eg interest rate risk)

To avoid the problem of provisioning “too little too late” as seen during the Subprime and Euro Debt Crisis. Insufficient provisioning and their sudden realisation led to shocks on financial

institutions balance sheets

IAS 39 : Incurred Loss Model

IFRS 9: Expected Credit Loss Model

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

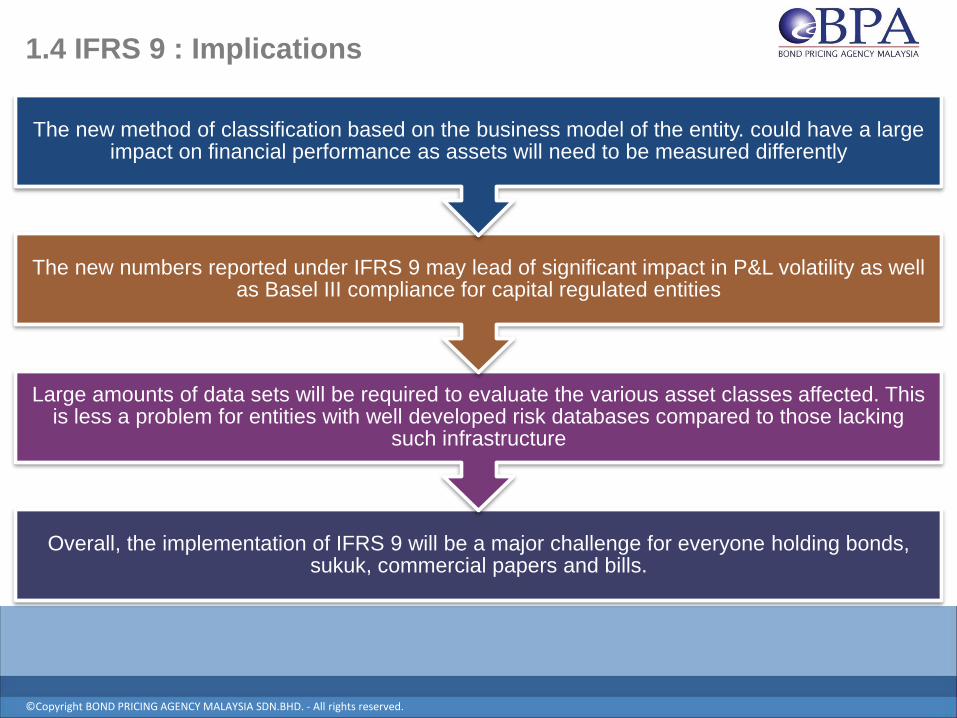

1.4 IFRS 9 : Implications

Overall, the implementation of IFRS 9 will be a major challenge for everyone holding bonds, sukuk, commercial papers and bills.

Large amounts of data sets will be required to evaluate the various asset classes affected. This is less a problem for entities with well developed risk databases compared to those lacking

such infrastructure

The new numbers reported under IFRS 9 may lead of significant impact in P&L volatility as well as Basel III compliance for capital regulated entities

The new method of classification based on the business model of the entity. could have a large impact on financial performance as assets will need to be measured differently

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Content

2. The Expected Credit Loss Model

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

EVALUATING PERFORMANCE

Is there a “significant increase in credit risk’ since initial recognition?

USE IAS 39 / MFRS 139 TRIGGERS AS

“LOSS EVENT” INDICATORS

Disappearance of Active Market

Downgrade of Credit Rating

Decline of Fair Value below

Amortised Cost

Local or National economic

conditions that correlate to the

assets in the group

The lender - granting the borrower a

concession that the lender would not

otherwise consider

Significant financial difficulty of the

issuer

“It may not be possible to identify a single, discreet event that caused the impairment.

Rather the combined effects of several events may cause the impairment”

2.1 IFRS 9 : The Expected Credit Loss Model

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

2.2 IAS 39 / MFRS 139 : Key Excerpts

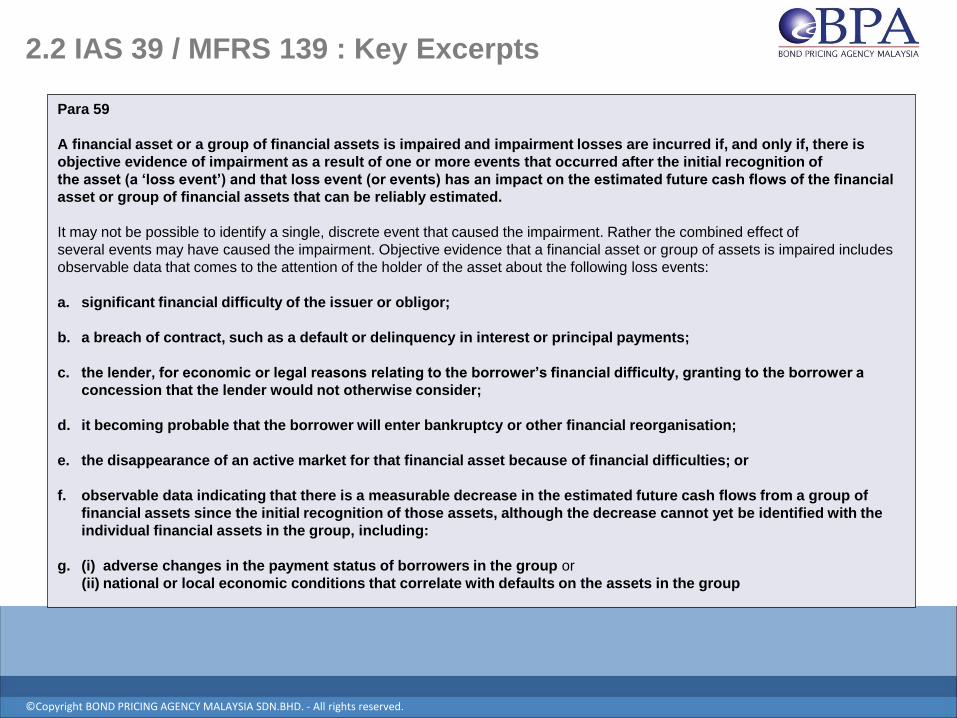

Para 59

A financial asset or a group of financial assets is impaired and impairment losses are incurred if, and only if, there is

objective evidence of impairment as a result of one or more events that occurred after the initial recognition of

the asset (a ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial

asset or group of financial assets that can be reliably estimated.

It may not be possible to identify a single, discrete event that caused the impairment. Rather the combined effect of

several events may have caused the impairment. Objective evidence that a financial asset or group of assets is impaired includes

observable data that comes to the attention of the holder of the asset about the following loss events:

a. significant financial difficulty of the issuer or obligor;

b. a breach of contract, such as a default or delinquency in interest or principal payments;

c. the lender, for economic or legal reasons relating to the borrower’s financial difficulty, granting to the borrower a

concession that the lender would not otherwise consider;

d. it becoming probable that the borrower will enter bankruptcy or other financial reorganisation;

e. the disappearance of an active market for that financial asset because of financial difficulties; or

f. observable data indicating that there is a measurable decrease in the estimated future cash flows from a group of

financial assets since the initial recognition of those assets, although the decrease cannot yet be identified with the

individual financial assets in the group, including:

g. (i) adverse changes in the payment status of borrowers in the group or

(ii) national or local economic conditions that correlate with defaults on the assets in the group

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

2.3 IAS 39 / MFRS 139 : Key Excerpts

Para 60

The disappearance of an active market because an entity’s financial instruments are no longer publicly traded is not

evidence of impairment.

A downgrade of an entity’s credit rating is not, of itself, evidence of impairment, although it may be evidence of

impairment when considered with other available information.

A decline in the fair value of a financial asset below its cost or amortised cost is not necessarily evidence of impairment

(for example, a decline in the fair value of an investment in a debt instrument that results from an increase in the risk-

free interest rate).

Para 61

…..objective evidence of impairment…also includes information about significant changes with an adverse effect that

have taken place in the technological, market, economic or legal environment in which the issuer operates…

Para 62

….an entity uses its experienced judgement to adjust observable data for a group of financial assets to reflect current

circumstances …..The use of reasonable estimates is an essential part of the preparation of financial statements and

does not undermine their reliability

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

2.4 IAS 39 / MFRS 139 : Key Excerpts

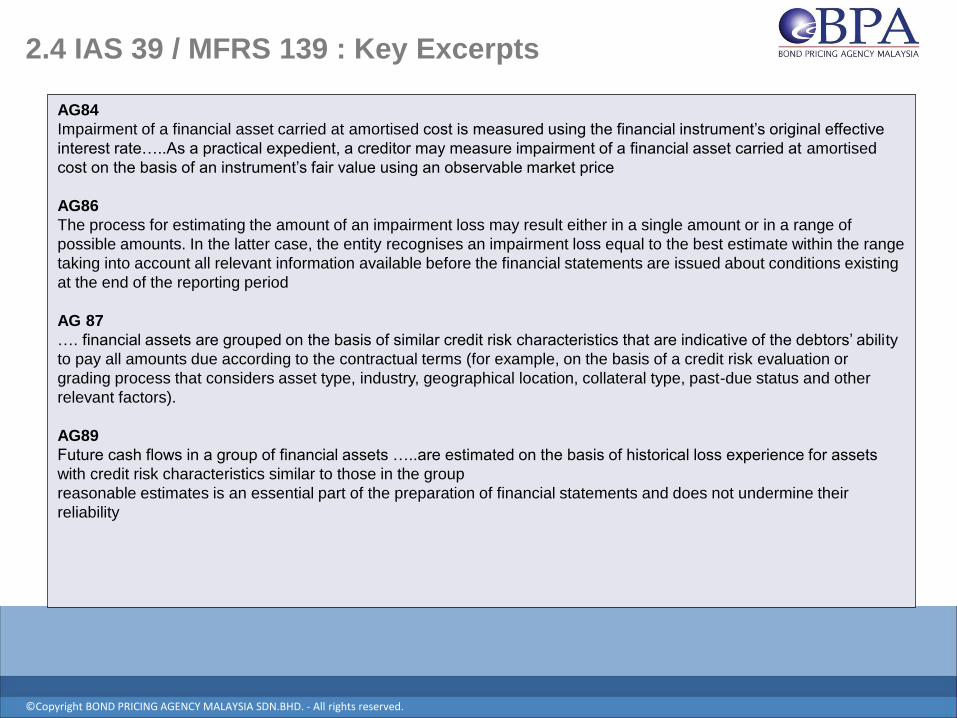

AG84

Impairment of a financial asset carried at amortised cost is measured using the financial instrument’s original effective

interest rate…..As a practical expedient, a creditor may measure impairment of a financial asset carried at amortised

cost on the basis of an instrument’s fair value using an observable market price

AG86

The process for estimating the amount of an impairment loss may result either in a single amount or in a range of

possible amounts. In the latter case, the entity recognises an impairment loss equal to the best estimate within the range

taking into account all relevant information available before the financial statements are issued about conditions existing

at the end of the reporting period

AG 87

…. financial assets are grouped on the basis of similar credit risk characteristics that are indicative of the debtors’ ability

to pay all amounts due according to the contractual terms (for example, on the basis of a credit risk evaluation or

grading process that considers asset type, industry, geographical location, collateral type, past-due status and other

relevant factors).

AG89

Future cash flows in a group of financial assets …..are estimated on the basis of historical loss experience for assets

with credit risk characteristics similar to those in the group

reasonable estimates is an essential part of the preparation of financial statements and does not undermine their

reliability

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

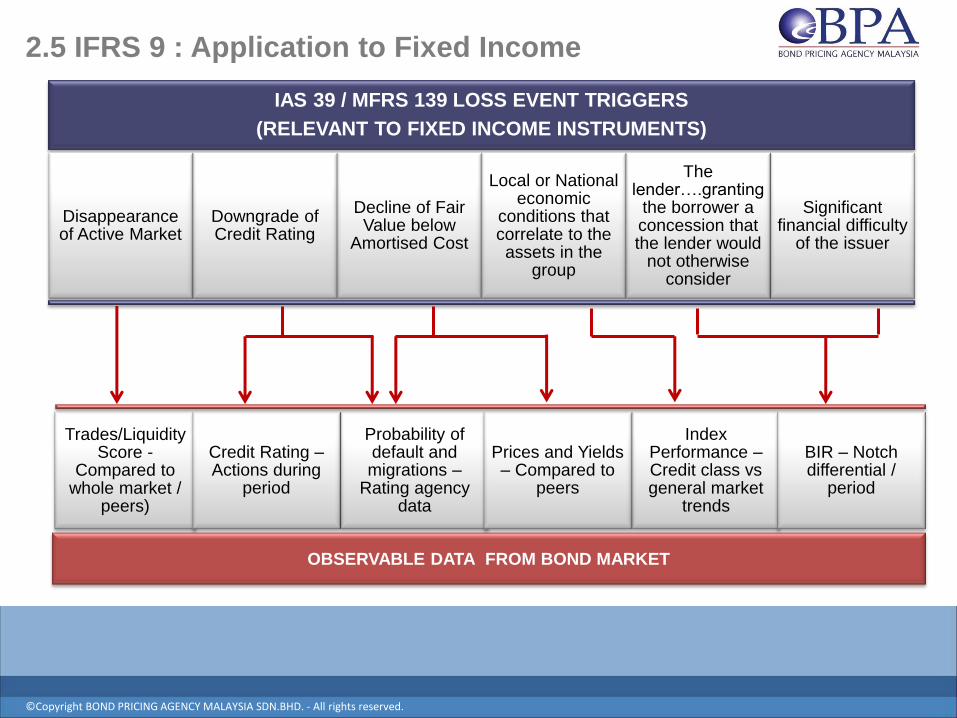

IAS 39 / MFRS 139 LOSS EVENT TRIGGERS

(RELEVANT TO FIXED INCOME INSTRUMENTS)

Disappearance of Active Market

Downgrade of Credit Rating

Decline of Fair Value below

Amortised Cost

Local or National economic

conditions that correlate to the assets in the

group

The lender….granting

the borrower a concession that the lender would

not otherwise consider

Significant financial difficulty

of the issuer

OBSERVABLE DATA FROM BOND MARKET

Trades/Liquidity Score -

Compared to whole market /

peers)

Credit Rating – Actions during

period

Probability of default and migrations –

Rating agency data

Prices and Yields – Compared to

peers

Index Performance – Credit class vs general market

trends

BIR – Notch differential /

period

2.5 IFRS 9 : Application to Fixed Income

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Content

3. Data Sources

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Trigger: Disappearance

of Active Market

Evaluate if there is an

active market

Compare liquidity

relative to the market as

a whole and other

similar bonds

Consider turnover ratio

Source: BPAM Bond

Transparency Tool

.

LIQUID

ILLIQUID

1

5

No. of Trades

Total

Trades

Turnover Ratio

Trade Recency

Trade

Frequency

Trade Turnover

SC

OR

ING

3.1 Data Sources : Liquidity Scores and Trade Data

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

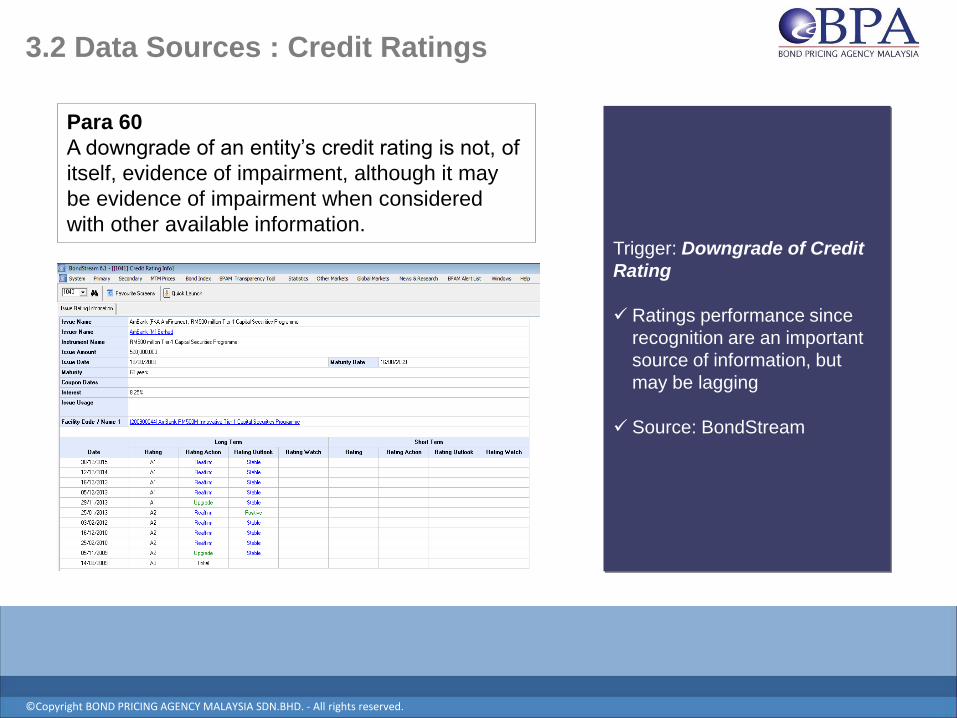

Trigger: Downgrade of Credit

Rating

Ratings performance since

recognition are an important

source of information, but

may be lagging

Source: BondStream

Para 60

A downgrade of an entity’s credit rating is not, of

itself, evidence of impairment, although it may

be evidence of impairment when considered

with other available information.

3.2 Data Sources : Credit Ratings

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Trigger: Downgrade of Credit

Rating

Ratings migration and default

studies over the years give a

probabilistic perspective on

deterioration in quality

The BPAM Default and Rating

report covers the entire

RAM/MARC universe on a

quarterly basis

Source: DaRT Report

3.3 Data Sources : Migration and Default Studies

AG89

Future cash flows…..are estimated on the basis of

historical loss experience for assets with credit risk

characteristics similar to those in the group

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

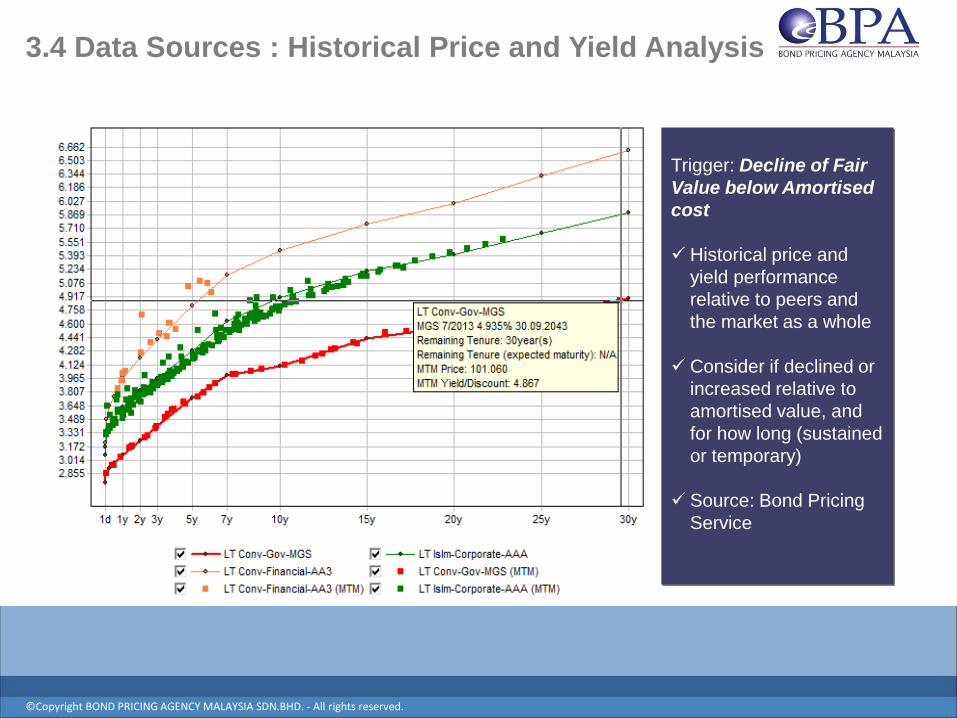

Trigger: Decline of Fair

Value below Amortised

cost

Historical price and

yield performance

relative to peers and

the market as a whole

Consider if declined or

increased relative to

amortised value, and

for how long (sustained

or temporary)

Source: Bond Pricing

Service

3.4 Data Sources : Historical Price and Yield Analysis

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

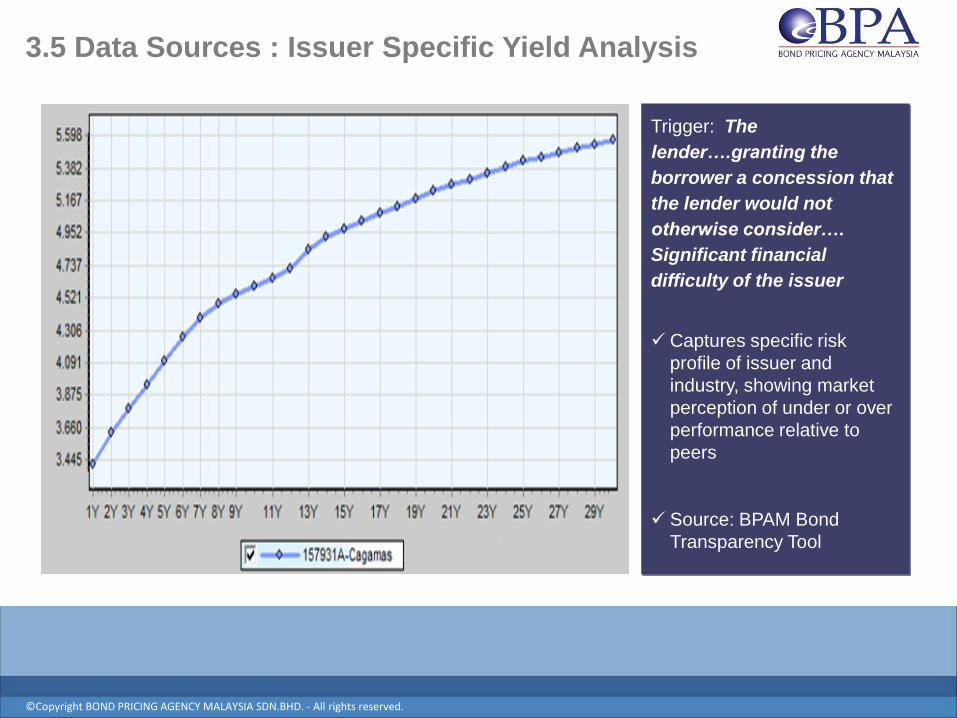

Rating

Trigger: The

lender….granting the

borrower a concession that

the lender would not

otherwise consider….

Significant financial

difficulty of the issuer

Captures specific risk

profile of issuer and

industry, showing market

perception of under or over

performance relative to

peers

Source: BPAM Bond

Transparency Tool

3.5 Data Sources : Issuer Specific Yield Analysis

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Trigger: Local or National

economic conditions that

correlate to the assets in the

group….information about

significant changes with an

adverse effect that have taken

place in the technological,

market, economic or legal

environment in which the

issuer operates…

Indices provide a barometer of

macro market conditions and

can be used to determine if a

certain credit class is

underperforming relative to its

peers

Source: TR-BPAM Index Series

3.6 Data Sources : Indices

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

AAA

AA

A

BBB

Bonds

Bond: A

Tenure: 1 Year

Credit Rating: AAA

BIR: BBB

Bond: B

Tenure: 5 Year

Credit Rating: AA

BIR: AAA

Bond: C

Tenure: 10 Year

Credit Rating: AA

BIR: AA

BIR Regions

Tenure

YT

M-M

GS

Sp

rea

d

Implied Ratings are a market-perceived credit rating, implied via market statistics and

calibrated via financial mathematics

Trigger: The lender….granting the

borrower a concession that the lender

would not otherwise

consider…..Significant financial difficulty

of the issuer

Market reacts immediately to issuer

specific news, some of which may be

privileged

Sustained negative divergence (ie IR < CR)

is a strong leading signal of possible credit

related problems

Comparison between CR and IR thresholds

can give a theoretical range of loss values

as a guide to provisioning

Source: BPAM Market Implied Ratings

3.7 Data Sources : Implied Ratings

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

Content

4. Conclusion & Summary

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

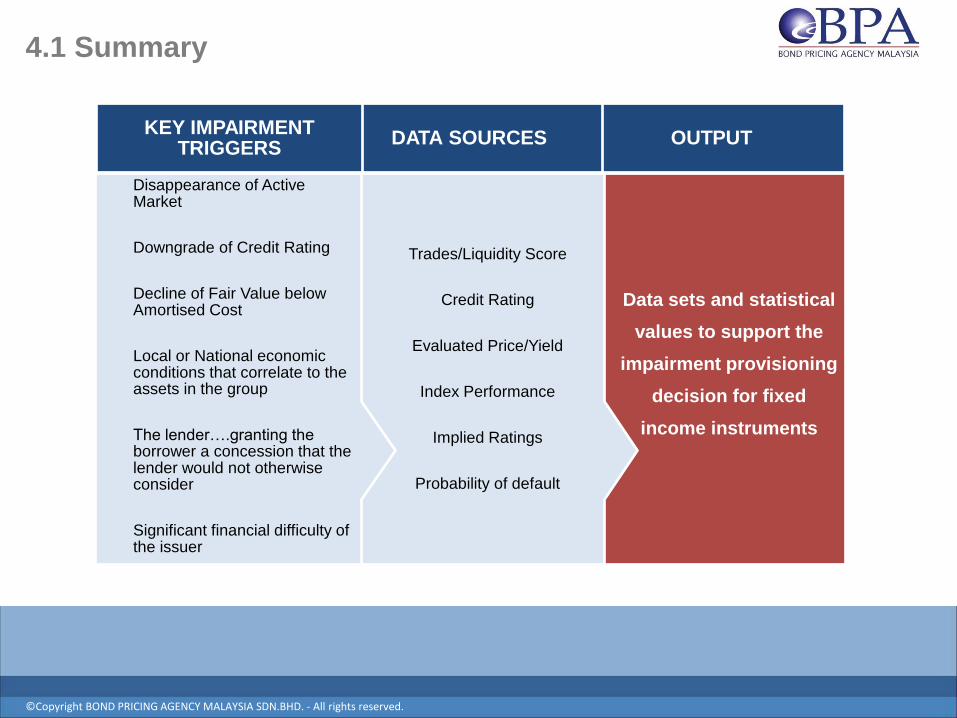

Data sets and statistical

values to support the

impairment provisioning

decision for fixed

income instruments

OUTPUT

Trades/Liquidity Score

Credit Rating

Evaluated Price/Yield

Index Performance

Implied Ratings

Probability of default

DATA SOURCES

Disappearance of Active Market

Downgrade of Credit Rating

Decline of Fair Value below Amortised Cost

Local or National economic conditions that correlate to the assets in the group

The lender….granting the borrower a concession that the lender would not otherwise consider

Significant financial difficulty of the issuer

KEY IMPAIRMENT TRIGGERS

4.1 Summary

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

KEY DATA SETS NEEDED TO CALCULATE

EXPECTED CREDIT LOSSES:

TRIGGER DATA

PROBABILITY OF DEFAULT

LOSS GIVEN DEFAULT

CASH FLOWS

ORIGINAL EFFECTIVE INTEREST RATES

4.2 Conclusion

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

IT’S ALL ABOUT DATA

THE SUCCESFUL IMPLEMENTATION OF IFRS 9 IN AN ENTITY IS

FUNDAMENTALLY DEPENDENT ON THE AVAILABILITY

OF DATA THAT IS:

TIMELY

GRANULAR

ACCURATE

ACCEPTED BY THE AUDIT INDUSTRY

EFFICIENTLY FORMATTED AND DELIVERED

4.3 Conclusion

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD. - All rights reserved.

THANK YOU

No 17-8 & 19-8 , The Boulevard, Mid Valley City, Lingkaran Syed Putra, 59200 Kuala Lumpur, Malaysia

Tel: +603 2772 0889 Fax: +603 2772 0808 Email : [email protected]

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD - All rights reserved.