Strenghtening collaboration with Serbia - IPA4 Project expected outcomes

TRACKING FINANCIAL CAPABILITY

Identify and Prioritize Your Expected Outcomes

JANUARY 2015

Identify and Prioritize Your Expected Outcomes

Tracking Financial Capability 2

AUTHORS

Pamela Chan, Kori Hattemer, Emily Hoagland and Elizabeth McGuinness

ABOUT CFED

CFED empowers low- and moderate-income households to build and preserve assets by advancing policies and programs that help them achieve the American Dream, including buying a home, pursuing higher education, starting a business and saving for the future. As a leading source for data about household financial security and policy solutions, CFED understands what families need to succeed. We promote programs on the ground and invest in social enterprises that create pathways to financial security and opportunity for millions of people.

Established in 1979 as the Corporation for Enterprise Development, CFED works nationally and internationally through its offices in Washington, DC; Durham, North Carolina; and San Francisco, California.

ABOUT BANK OF AMERICA CORPORATE SOCIAL RESPONSIBILITY

We have a clear purpose to help make financial lives better for those we serve. Our corporate social responsibility (CSR) efforts are a demonstration of how we live our purpose, and play a key role in our business strategy of responsible growth. These efforts guide how we operate in a socially, economically, financially and environmentally responsible way around the world, to deliver for shareholders, customers, clients and employees. One area of focus is the role we play to enable and promote financial empowerment, helping individuals and communities to thrive. We do this through the products we create, the education and resources we provide broadly to consumers, and the more personalized, hands-on opportunities we help enable through partnerships in our local communities. Through our partnership with non-profit online education innovator Khan Academy, we provide BetterMoneyHabits.com, a free education resource aimed at empowering people to be more confident in their financial decision making. The program pairs Khan Academy’s expertise in online learning with our financial know-how to deliver unbiased and easy-to-understand information on a wide range of personal finance topics including budgeting, savings and credit. Learn more at bankofamerica.com/about and BetterMoneyHabits.com.

Identify and Prioritize Your Expected Outcomes

Monitoring Financial CapabilityCorporation for Enterprise Development 3Tracking Financial Capability 3

Financial capability programs aim to change the lives of their participants and improve the financial health of the larger community. Sometimes, however, it can be hard to know if a program is achieving its intended results and to demonstrate this impact to funders and policymakers. Identifying and measuring program outcomes can help you understand how well your program is working, identify areas for improvement and provide the evidence necessary to attract continued funding.

1 Using Outcome Information: Making Data Pay Off (Washington, DC: The Urban Institute, 2004). In an independent survey, 400 program directors of health and human services programs agreed or strongly agreed that outcome measurement assisted their organizations in these ways.

An important part of program design is determining how to assess the program’s effects on the clients and their community. Typically, we assess program effectiveness by measuring the changes in outcomes—the changes in the conditions of your clients, their families and their communities—that occur due to participation in your program. Developing and executing an outcome measurement plan can assist organizations such as yours1 with:

� Focusing staff on shared goals. � Communicating results to stakeholders. � Clarifying your program’s purpose. � Identifying effective practices. � Competing for resources. � Keeping records. � Making improvements to service delivery.

This guide is the first in a three-part series, Tracking Financial Capability:

Guide #1: Identify and Prioritize Your Expected OutcomesGuide #2: Build Your Logic ModelGuide #3: Select and Collect Indicator Data

This series is designed for frontline organizations that plan to provide, or are already providing, services to help clients manage their financial resources more effectively and become more financially secure. The three guides in this series will help you establish processes to track your programs to ensure they are being implemented as planned and resulting in the outcomes you set out to achieve. These guides will help you clearly state up front what you hope to achieve as a result of these services, how you plan to bring about these changes in your clients’ lives (as depicted in your logic model), and how you will collect data to track your progress.

Outcomes are best identified during the program design phase and kept in mind throughout the design and implementation processes. They provide the basis for measuring the program’s success in achieving its mission. High-quality outcome data will support your organization in making strategic

Identify and Prioritize Your Expected Outcomes

In general, outcomes are the state or condition of the clients and community that a program is trying to change. For financial capability programs, outcomes are the knowledge, skills, attitudes, behaviors and life conditions an organization hopes to influence within the population(s) they serve. Outcomes are related directly to your program’s goals. For example, better financial skills, as measured by improved scores on a financial skills test or clients’ improved credit scores, are examples of outcomes. Keep in mind that not everything a program measures is necessarily an outcome. The number of financial education classes offered is not an outcome because it describes a program’s output; it’s not an indicator of the change a program has made in a client’s life. Program outputs are tangible products and services resulting from program activities. Program outcomes, on the other hand, are the benefits that participants realize as a result of using the outputs (program products and services).

Tracking Financial Capability 4

Step 1: Understand Financial Capability Outcomes

TIPS: Distinguishing Outcomes from Outputs

DDOutputs relate to what the program does. Outcomes relate to what difference the program makes.

DDMeasuring outputs often involves counting (e.g., number of students taught, number of students completing a budgeting exercise, etc.).

DDOutcomes always refer to characteristics that in principle could be observed for individuals or situations that have not received program services. Program outputs are only experienced by program participants (e.g., increased balance in savings account, increased trust in financial institutions, etc.).

For financial capability programs, outcomes are the knowledge, skills, attitudes, behaviors and life conditions an organization hopes to influence within the population(s) they serve.

1 Understand what financial capability outcomes are.

2 Identify desired financial capability outcomes for your clients.

3 Prioritize which financial capability outcomes to track.

decisions on how to refine and improve your program, as well as to track the benefits of the program for your clients. This guide will assist you in identifying and selecting relevant outcome measures for financial capability programs by helping you to:

Tracking Financial Capability

Identify and Prioritize Your Expected Outcomes

Step 2: Identify Desired Outcomes for Your Clients

2 Michelle Bertrand, Sendhil Mullainathan and Eldar Shafir, “Behavioral Economics and Marketing in Aid of Decision Making Among the Poor,” Journal of Public Policy & Marketing 25 no. 1 (2006).

5

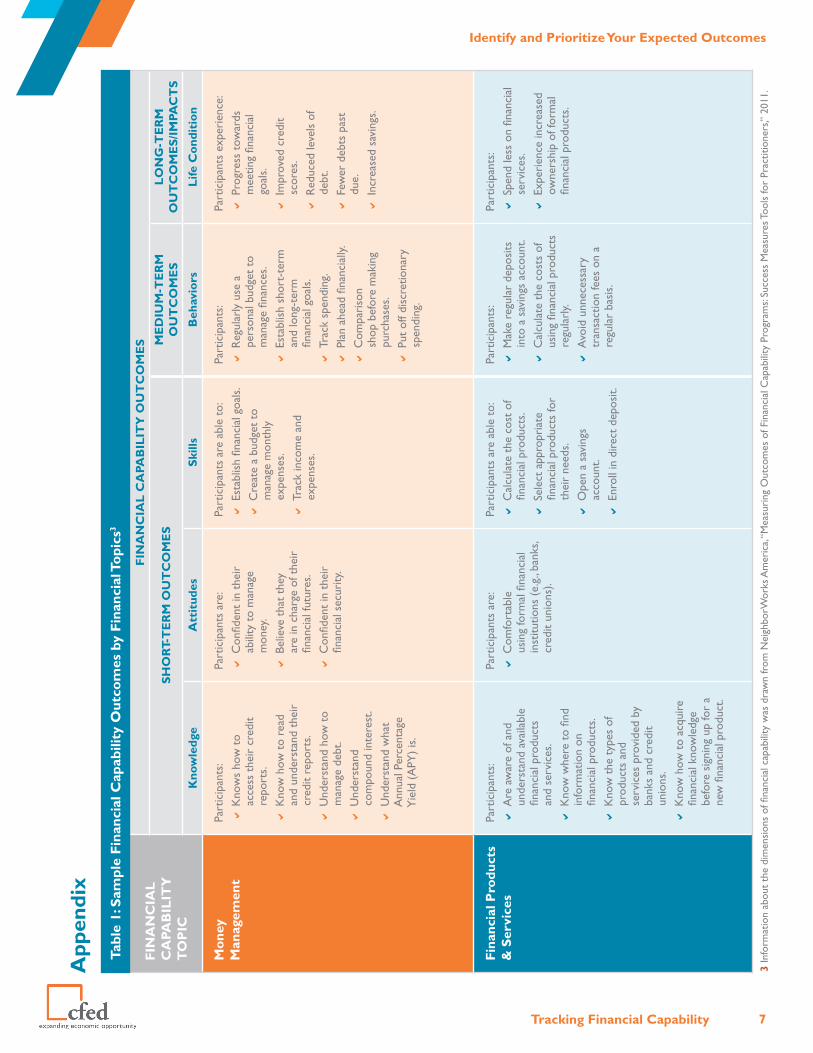

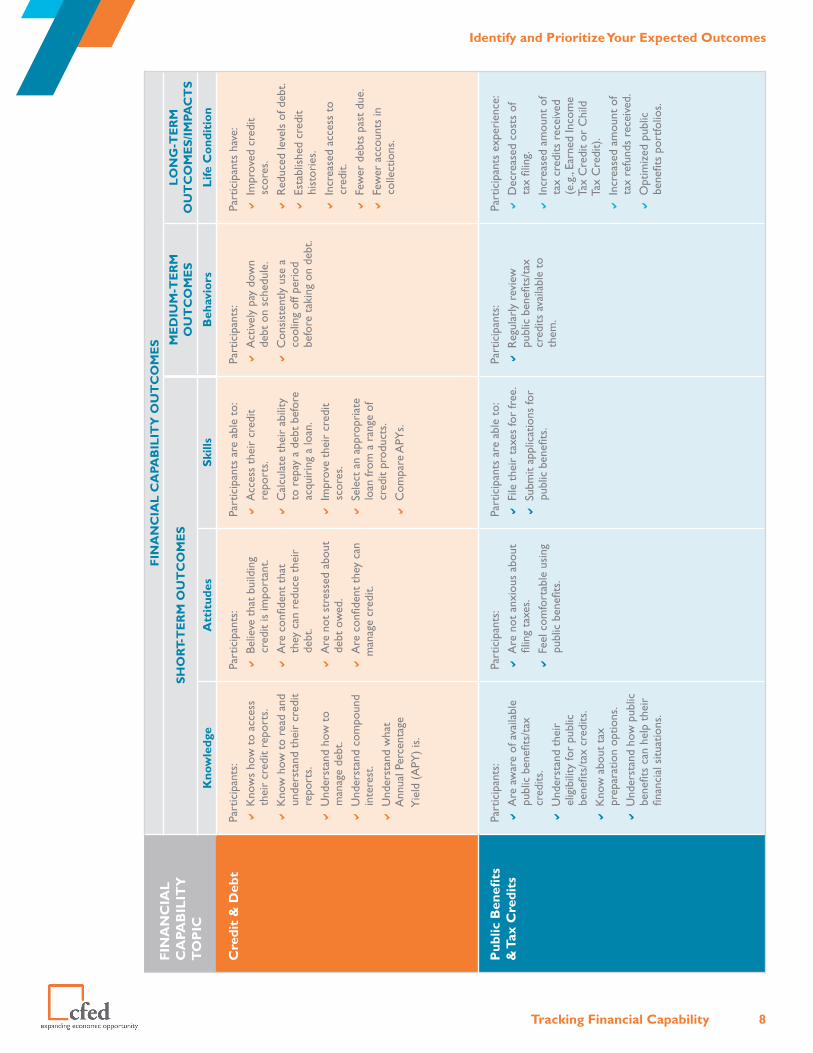

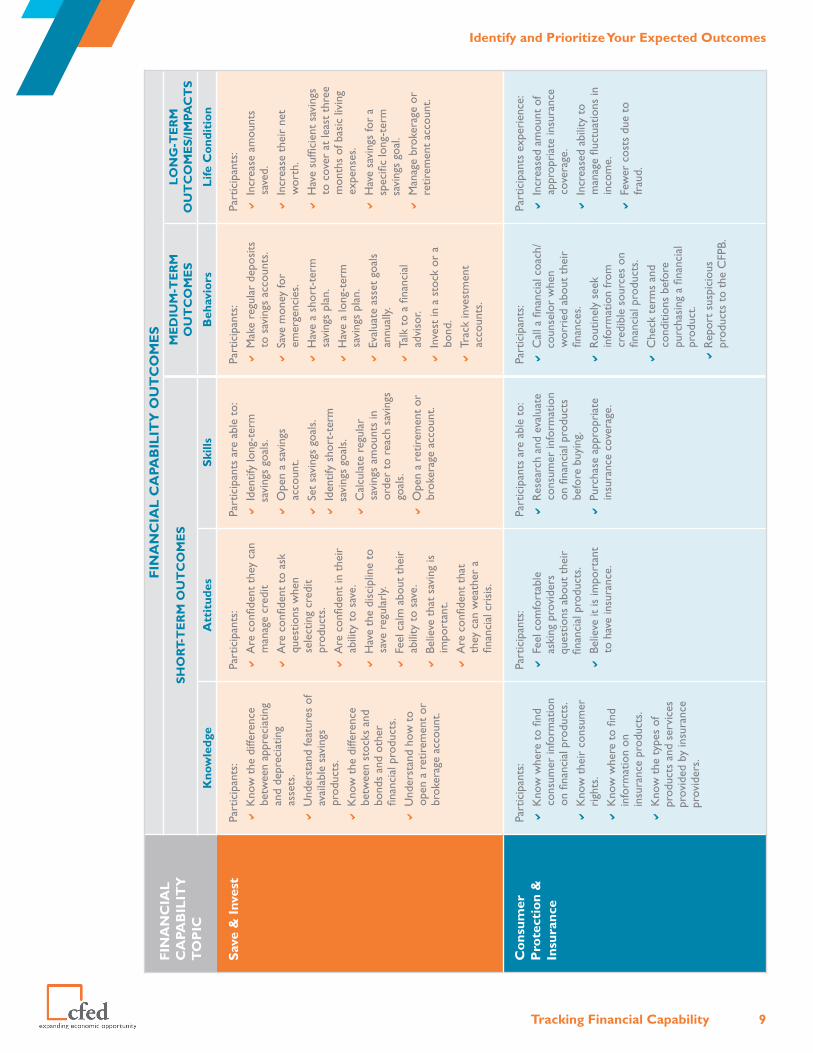

Financial capability programs can affect a whole host of outcomes, from changes in the number of savings deposits to the use of insurance products, to improved credit scores. Table 1 in the Appendix provides a sample list of financial capability outcomes. The list is organized by financial capability topic. The table includes six different subject areas that are commonly covered in financial capability programs. It is intended to serve as a general guide for thinking about what kind of outcomes could be expected as a result of providing different financial capability services.

As you identify your outcomes, check to make sure that they:

� Are observable and can be measured to determine whether change has taken place. � Represent a potential benefit for the target population. � Are realistic and attainable for participants. � Can be sensibly claimed as something your program can influence. � Are accepted as valid outcomes by your key stakeholders.

Tracking Financial Capability

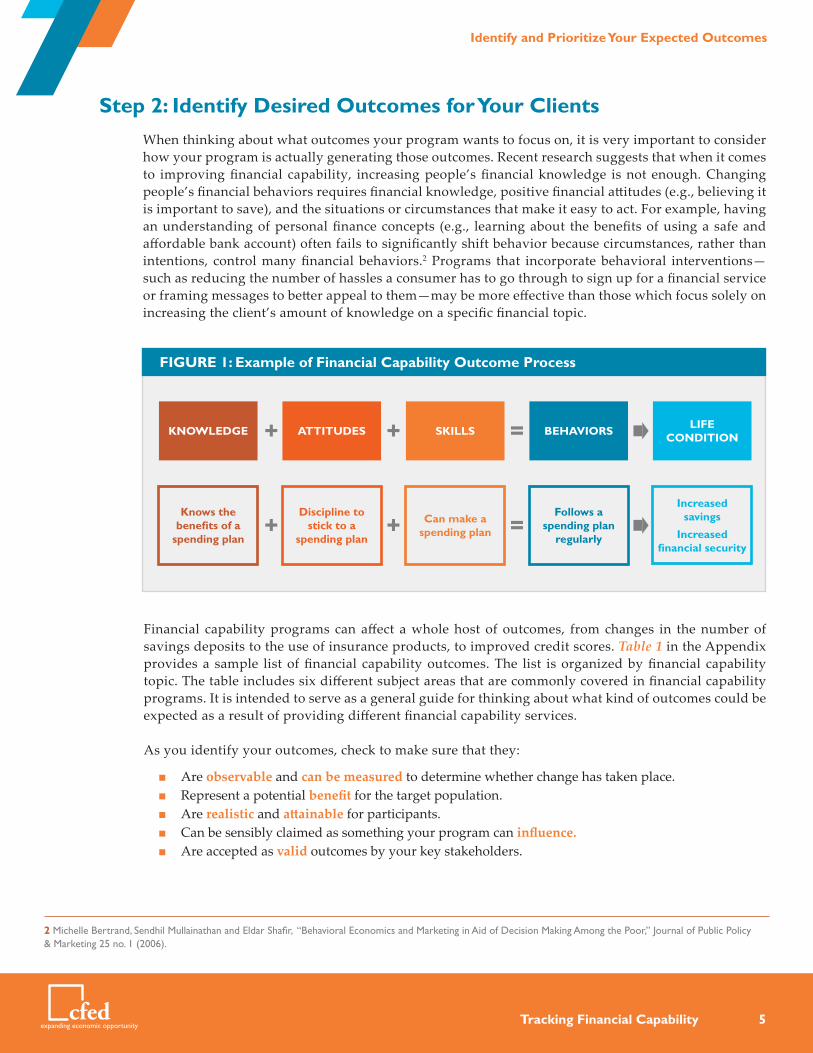

KNOWLEDGE

Knows the benefits of a

spending plan

ATTITUDES

Discipline to stick to a

spending plan

SKILLS

Can make a spending plan

BEHAVIORS

Follows a spending plan

regularly

LIFE CONDITION

Increased savings

Increased financial security

+

+

+

+

=

=

FIGURE 1: Example of Financial Capability Outcome Process

When thinking about what outcomes your program wants to focus on, it is very important to consider how your program is actually generating those outcomes. Recent research suggests that when it comes to improving financial capability, increasing people’s financial knowledge is not enough. Changing people’s financial behaviors requires financial knowledge, positive financial attitudes (e.g., believing it is important to save), and the situations or circumstances that make it easy to act. For example, having an understanding of personal finance concepts (e.g., learning about the benefits of using a safe and affordable bank account) often fails to significantly shift behavior because circumstances, rather than intentions, control many financial behaviors.2 Programs that incorporate behavioral interventions—such as reducing the number of hassles a consumer has to go through to sign up for a financial service or framing messages to better appeal to them—may be more effective than those which focus solely on increasing the client’s amount of knowledge on a specific financial topic.

Tracking Financial Capability 6

Identify and Prioritize Your Expected Outcomes

6

While you may want a program to influence a very broad set of outcomes, often it is not operationally feasible to measure all expected outcomes initially. A logic model can lay out your program’s processes and connect them to your desired program outcomes in a reasoned way. (See the second guide in this series, Build Your Logic Model.) Listing your outcomes as part of a logic model can help you to prioritize the most important ones for your program. The logic model allows you to easily see which short- and medium-term outcomes lead to the most important long-term outcomes. At the same time, you can select specific outcomes that best meet the criteria listed above.

There is no ideal or standard number of outcomes to select for a particular program. However, prioritizing outcomes and honing in on a few key ones is critical to creating an effective financial capability program. Particularly in the early days, focusing more narrowly and improving your program’s ability to change a few specific outcomes may lead to greater impact than a broader, more diffuse strategy. Similarly, measuring a few key outcomes well will have more value for your program than measuring a larger number of outcomes poorly. Before finalizing your list of outcomes, ask yourself a series of questions to assess whether each outcome is important, reasonable and realistic. Refine your list based on the results. Before you finish, consider whether there are any potentially negative outcomes of your program and add these to this list to ensure that you watch out for them in your evaluation work. Then, make sure all the outcomes in your logic model can be linked to at least one output.

Looking Ahead: Building a Logic ModelNow that you have identified and prioritized outcomes, the next step is to build your logic model. (For more on logic models, see the second guide in this series.) As you create your logic model, you may want to revisit and further streamline your outcomes to guarantee that you will have a manageable and effective tracking program when you are finished. Developing logic models is often an iterative task which requires time and attention to detail in order to obtain good results.

In the third guide in this series, Select and Collect Indicator Data, we will show you how to take your logic model and turn it into a rich set of data that can be used to assess how you are doing with your program, determine whether or not you need to refine your program, communicate your program’s potential and lay the foundation for a formal impact evaluation.

To learn more about identifying and prioritizing outcomes and about tracking finanacial capabilty in general, the following resources are helpful guides:

� Handling Data: From Logic Model to Final Report by Gail V. Barrington. � Evaluation: A Systematic Approach by Peter H. Rossi, Mark W. Lipsey and Howard E. Freeman. � Enhancing Program Performance with Logic Models, University of Wisconsin-Extension. � Finding a Yardstick: Field Testing Outcome Measures for Community-based Financial Coaching

and Capability Programs by J. Michael Collins. � Measuring Outcomes of Financial Capability Programs: Success Measures Tools for Practitioners,

NeighborWorks America.

Additional Resources

Step 3: Prioritize Which Outcomes to Track

Tracking Financial Capability 7

Identify and Prioritize Your Expected Outcomes

FIN

AN

CIA

L

CA

PAB

ILIT

Y

TO

PIC

FIN

AN

CIA

L C

APA

BIL

ITY

OU

TC

OM

ES

SHO

RT-T

ER

M O

UT

CO

ME

S M

ED

IUM

-TE

RM

O

UT

CO

ME

SLO

NG

-TE

RM

O

UT

CO

ME

S/IM

PAC

TS

Kno

wle

dge

Att

itud

esSk

ills

Beh

avio

rsLi

fe C

ondi

tion

Mo

ney

M

anag

emen

tPa

rtic

ipan

ts:

DD

Kno

ws

how

to

a

cces

s th

eir

cred

it

rep

orts

.DD

Kno

w h

ow t

o re

ad

and

und

erst

and

thei

r

c

redi

t re

port

s.

DD

Und

erst

and

how

to

man

age

debt

.DD

Und

erst

and

com

poun

d in

tere

st.

DD

Und

erst

and

wha

t

A

nnua

l Per

cent

age

Yie

ld (

APY

) is

.

Part

icip

ants

are

:DD

Con

fiden

t in

the

ir

a

bilit

y to

man

age

mon

ey.

DD

Belie

ve t

hat

they

a

re in

cha

rge

of t

heir

fina

ncia

l fut

ures

. DD

Con

fiden

t in

the

ir

fi

nanc

ial s

ecur

ity.

Part

icip

ants

are

abl

e to

:DD

Esta

blis

h fin

anci

al g

oals

. DD

Cre

ate

a bu

dget

to

man

age

mon

thly

e

xpen

ses.

DD

Trac

k in

com

e an

d

e

xpen

ses.

Part

icip

ants

:DD

Reg

ular

ly u

se a

per

sona

l bud

get

to

m

anag

e fin

ance

s.DD

Esta

blis

h sh

ort-

term

and

long

-ter

m

fi

nanc

ial g

oals

. DD

Trac

k sp

endi

ng.

DD

Plan

ahe

ad fi

nanc

ially

.DD

Com

pari

son

sho

p be

fore

mak

ing

pur

chas

es.

DD

Put

off d

iscr

etio

nary

spe

ndin

g.

Part

icip

ants

exp

erie

nce:

DD

Prog

ress

tow

ards

mee

ting

finan

cial

goa

ls.

DD

Impr

oved

cre

dit

sco

res.

DD

Red

uced

leve

ls o

f

deb

t.DD

Few

er d

ebts

pas

t

d

ue.

DD

Incr

ease

d sa

ving

s.

Fin

anci

al P

rodu

cts

& S

ervi

ces

Part

icip

ants

:DD

Are

aw

are

of a

nd

u

nder

stan

d av

aila

ble

fina

ncia

l pro

duct

s

a

nd s

ervi

ces.

DD

Kno

w w

here

to

find

inf

orm

atio

n on

fina

ncia

l pro

duct

s.DD

Kno

w t

he t

ypes

of

p

rodu

cts

and

ser

vice

s pr

ovid

ed b

y

b

anks

and

cre

dit

uni

ons.

DD

Kno

w h

ow t

o ac

quir

e

fi

nanc

ial k

now

ledg

e

b

efor

e si

gnin

g up

for

a

n

ew fi

nanc

ial p

rodu

ct.

Part

icip

ants

are

:DD

Com

fort

able

usi

ng fo

rmal

fina

ncia

l

ins

titut

ions

(e.

g., b

anks

,

cre

dit

unio

ns).

Part

icip

ants

are

abl

e to

:DD

Cal

cula

te t

he c

ost

of

fi

nanc

ial p

rodu

cts.

DD

Sele

ct a

ppro

pria

te

fi

nanc

ial p

rodu

cts

for

the

ir n

eeds

.DD

Ope

n a

savi

ngs

acc

ount

.DD

Enro

ll in

dir

ect

depo

sit.

Part

icip

ants

:DD

Mak

e re

gula

r de

posi

ts

i

nto

a sa

ving

s ac

coun

t.DD

Cal

cula

te t

he c

osts

of

u

sing

fina

ncia

l pro

duct

s

reg

ular

ly.

DD

Avo

id u

nnec

essa

ry

t

rans

actio

n fe

es o

n a

reg

ular

bas

is.

Part

icip

ants

:DD

Spen

d le

ss o

n fin

anci

al

s

ervi

ces.

DD

Expe

rien

ce in

crea

sed

ow

ners

hip

of fo

rmal

fina

ncia

l pro

duct

s.

Tabl

e 1:

Sam

ple

Fin

anci

al C

apab

ility

Out

com

es b

y F

inan

cial

To

pics

3

3 In

form

atio

n ab

out

the

dim

ensi

ons

of fi

nanc

ial c

apab

ility

was

dra

wn

from

Nei

ghbo

rWor

ks A

mer

ica,

“Mea

suri

ng O

utco

mes

of F

inan

cial

Cap

abili

ty P

rogr

ams:

Succ

ess

Mea

sure

s Too

ls fo

r Pr

actit

ione

rs,”

2011

.

App

endi

x

Tracking Financial Capability 8

Identify and Prioritize Your Expected Outcomes

FIN

AN

CIA

L

CA

PAB

ILIT

Y

TO

PIC

FIN

AN

CIA

L C

APA

BIL

ITY

OU

TC

OM

ES

SHO

RT-T

ER

M O

UT

CO

ME

S M

ED

IUM

-TE

RM

O

UT

CO

ME

SLO

NG

-TE

RM

O

UT

CO

ME

S/IM

PAC

TS

Kno

wle

dge

Att

itud

esSk

ills

Beh

avio

rsLi

fe C

ondi

tion

Cre

dit

& D

ebt

Part

icip

ants

:DD

Kno

ws

how

to

acce

ss

t

heir

cre

dit

repo

rts.

DD

Kno

w h

ow t

o re

ad a

nd

u

nder

stan

d th

eir

cred

it

rep

orts

. DD

Und

erst

and

how

to

man

age

debt

.DD

Und

erst

and

com

poun

d

int

eres

t.DD

Und

erst

and

wha

t

A

nnua

l Per

cent

age

Yie

ld (

APY

) is

.

Part

icip

ants

:DD

Belie

ve t

hat

build

ing

cre

dit

is im

port

ant.

DD

Are

con

fiden

t th

at

t

hey

can

redu

ce t

heir

deb

t. DD

Are

not

str

esse

d ab

out

d

ebt

owed

.DD

Are

con

fiden

t th

ey c

an

m

anag

e cr

edit.

Part

icip

ants

are

abl

e to

:DD

Acc

ess

thei

r cr

edit

r

epor

ts.

DD

Cal

cula

te t

heir

abi

lity

to

repa

y a

debt

bef

ore

acq

uiri

ng a

loan

.DD

Impr

ove

thei

r cr

edit

sco

res.

DD

Sele

ct a

n ap

prop

riat

e

l

oan

from

a r

ange

of

c

redi

t pr

oduc

ts.

DD

Com

pare

APY

s.

Part

icip

ants

:DD

Act

ivel

y pa

y do

wn

deb

t on

sch

edul

e.DD

Con

sist

ently

use

a

c

oolin

g of

f per

iod

bef

ore

taki

ng o

n de

bt.

Part

icip

ants

hav

e:DD

Impr

oved

cre

dit

sco

res.

DD

Red

uced

leve

ls o

f deb

t.DD

Esta

blis

hed

cred

it

h

isto

ries

.DD

Incr

ease

d ac

cess

to

cre

dit.

DD

Few

er d

ebts

pas

t du

e.DD

Few

er a

ccou

nts

in

c

olle

ctio

ns.

Pub

lic B

enefi

ts

& T

ax C

redi

tsPa

rtic

ipan

ts:

DD

Are

aw

are

of a

vaila

ble

pub

lic b

enefi

ts/t

ax

c

redi

ts.

DD

Und

erst

and

thei

r

e

ligib

ility

for

publ

ic

b

enefi

ts/t

ax c

redi

ts.

DD

Kno

w a

bout

tax

pre

para

tion

optio

ns.

DD

Und

erst

and

how

pub

lic

b

enefi

ts c

an h

elp

thei

r

fi

nanc

ial s

ituat

ions

.

Part

icip

ants

:DD

Are

not

anx

ious

abo

ut

fi

ling

taxe

s. DD

Feel

com

fort

able

usi

ng

p

ublic

ben

efits

.

Part

icip

ants

are

abl

e to

:DD

File

the

ir t

axes

for

free

. DD

Subm

it ap

plic

atio

ns fo

r

pub

lic b

enefi

ts.

Part

icip

ants

:DD

Reg

ular

ly r

evie

w

p

ublic

ben

efits

/tax

cre

dits

ava

ilabl

e to

the

m.

Part

icip

ants

exp

erie

nce:

DD

Dec

reas

ed c

osts

of

t

ax fi

ling.

DD

Incr

ease

d am

ount

of

t

ax c

redi

ts r

ecei

ved

(e.

g., E

arne

d In

com

e

T

ax C

redi

t or

Chi

ld

T

ax C

redi

t).

DD

Incr

ease

d am

ount

of

t

ax r

efun

ds r

ecei

ved.

DD

Opt

imiz

ed p

ublic

ben

efits

por

tfolio

s.

Tracking Financial Capability 9

Identify and Prioritize Your Expected Outcomes

FIN

AN

CIA

L

CA

PAB

ILIT

Y

TO

PIC

FIN

AN

CIA

L C

APA

BIL

ITY

OU

TC

OM

ES

SHO

RT-T

ER

M O

UT

CO

ME

S M

ED

IUM

-TE

RM

O

UT

CO

ME

SLO

NG

-TE

RM

O

UT

CO

ME

S/IM

PAC

TS

Kno

wle

dge

Att

itud

esSk

ills

Beh

avio

rsLi

fe C

ondi

tion

Cre

dit

& D

ebt

Part

icip

ants

:DD

Kno

ws

how

to

acce

ss

t

heir

cre

dit

repo

rts.

DD

Kno

w h

ow t

o re

ad a

nd

u

nder

stan

d th

eir

cred

it

rep

orts

. DD

Und

erst

and

how

to

man

age

debt

.DD

Und

erst

and

com

poun

d

int

eres

t.DD

Und

erst

and

wha

t

A

nnua

l Per

cent

age

Yie

ld (

APY

) is

.

Part

icip

ants

:DD

Belie

ve t

hat

build

ing

cre

dit

is im

port

ant.

DD

Are

con

fiden

t th

at

t

hey

can

redu

ce t

heir

deb

t. DD

Are

not

str

esse

d ab

out

d

ebt

owed

.DD

Are

con

fiden

t th

ey c

an

m

anag

e cr

edit.

Part

icip

ants

are

abl

e to

:DD

Acc

ess

thei

r cr

edit

r

epor

ts.

DD

Cal

cula

te t

heir

abi

lity

to

repa

y a

debt

bef

ore

acq

uiri

ng a

loan

.DD

Impr

ove

thei

r cr

edit

sco

res.

DD

Sele

ct a

n ap

prop

riat

e

l

oan

from

a r

ange

of

c

redi

t pr

oduc

ts.

DD

Com

pare

APY

s.

Part

icip

ants

:DD

Act

ivel

y pa

y do

wn

deb

t on

sch

edul

e.DD

Con

sist

ently

use

a

c

oolin

g of

f per

iod

bef

ore

taki

ng o

n de

bt.

Part

icip

ants

hav

e:DD

Impr

oved

cre

dit

sco

res.

DD

Red

uced

leve

ls o

f deb

t.DD

Esta

blis

hed

cred

it

h

isto

ries

.DD

Incr

ease

d ac

cess

to

cre

dit.

DD

Few

er d

ebts

pas

t du

e.DD

Few

er a

ccou

nts

in

c

olle

ctio

ns.

Pub

lic B

enefi

ts

& T

ax C

redi

tsPa

rtic

ipan

ts:

DD

Are

aw

are

of a

vaila

ble

pub

lic b

enefi

ts/t

ax

c

redi

ts.

DD

Und

erst

and

thei

r

e

ligib

ility

for

publ

ic

b

enefi

ts/t

ax c

redi

ts.

DD

Kno

w a

bout

tax

pre

para

tion

optio

ns.

DD

Und

erst

and

how

pub

lic

b

enefi

ts c

an h

elp

thei

r

fi

nanc

ial s

ituat

ions

.

Part

icip

ants

:DD

Are

not

anx

ious

abo

ut

fi

ling

taxe

s. DD

Feel

com

fort

able

usi

ng

p

ublic

ben

efits

.

Part

icip

ants

are

abl

e to

:DD

File

the

ir t

axes

for

free

. DD

Subm

it ap

plic

atio

ns fo

r

pub

lic b

enefi

ts.

Part

icip

ants

:DD

Reg

ular

ly r

evie

w

p

ublic

ben

efits

/tax

cre

dits

ava

ilabl

e to

the

m.

Part

icip

ants

exp

erie

nce:

DD

Dec

reas

ed c

osts

of

t

ax fi

ling.

DD

Incr

ease

d am

ount

of

t

ax c

redi

ts r

ecei

ved

(e.

g., E

arne

d In

com

e

T

ax C

redi

t or

Chi

ld

T

ax C

redi

t).

DD

Incr

ease

d am

ount

of

t

ax r

efun

ds r

ecei

ved.

DD

Opt

imiz

ed p

ublic

ben

efits

por

tfolio

s.

FIN

AN

CIA

L

CA

PAB

ILIT

Y

TO

PIC

FIN

AN

CIA

L C

APA

BIL

ITY

OU

TC

OM

ES

SHO

RT-T

ER

M O

UT

CO

ME

S M

ED

IUM

-TE

RM

O

UT

CO

ME

SLO

NG

-TE

RM

O

UT

CO

ME

S/IM

PAC

TS

Kno

wle

dge

Att

itud

esSk

ills

Beh

avio

rsLi

fe C

ondi

tion

Sav

e &

Inv

est

Part

icip

ants

:DD

Kno

w t

he d

iffer

ence

bet

wee

n ap

prec

iatin

g

a

nd d

epre

ciat

ing

ass

ets.

DD

Und

erst

and

feat

ures

of

a

vaila

ble

savi

ngs

pro

duct

s.DD

Kno

w t

he d

iffer

ence

bet

wee

n st

ocks

and

bon

ds a

nd o

ther

fina

ncia

l pro

duct

s.DD

Und

erst

and

how

to

ope

n a

retir

emen

t or

bro

kera

ge a

ccou

nt.

Part

icip

ants

: DD

Are

con

fiden

t th

ey c

an

m

anag

e cr

edit

DD

Are

con

fiden

t to

ask

que

stio

ns w

hen

sel

ectin

g cr

edit

pro

duct

s.DD

Are

con

fiden

t in

the

ir

a

bilit

y to

sav

e.DD

Hav

e th

e di

scip

line

to

s

ave

regu

larl

y.DD

Feel

cal

m a

bout

the

ir

a

bilit

y to

sav

e.DD

Belie

ve t

hat

savi

ng is

im

port

ant.

DD

Are

con

fiden

t th

at

t

hey

can

wea

ther

a

fi

nanc

ial c

risi

s.

Part

icip

ants

are

abl

e to

:DD

Iden

tify

long

-ter

m

s

avin

gs g

oals

.DD

Ope

n a

savi

ngs

acc

ount

.DD

Set

savi

ngs

goal

s. DD

Iden

tify

shor

t-te

rm

s

avin

gs g

oals

.DD

Cal

cula

te r

egul

ar

s

avin

gs a

mou

nts

in

o

rder

to

reac

h sa

ving

s

goa

ls.

DD

Ope

n a

retir

emen

t or

bro

kera

ge a

ccou

nt.

Part

icip

ants

:DD

Mak

e re

gula

r de

posi

ts

t

o sa

ving

s ac

coun

ts.

DD

Save

mon

ey fo

r

e

mer

genc

ies.

DD

Hav

e a

shor

t-te

rm

s

avin

gs p

lan.

DD

Hav

e a

long

-ter

m

s

avin

gs p

lan.

DD

Eval

uate

ass

et g

oals

ann

ually

.DD

Talk

to

a fin

anci

al

a

dvis

or.

DD

Inve

st in

a s

tock

or

a

b

ond.

DD

Trac

k in

vest

men

t

a

ccou

nts.

Part

icip

ants

:DD

Incr

ease

am

ount

s

s

aved

.DD

Incr

ease

the

ir n

et

w

orth

.DD

Hav

e su

ffici

ent

savi

ngs

to

cove

r at

leas

t th

ree

mon

ths

of b

asic

livi

ng

e

xpen

ses.

DD

Hav

e sa

ving

s fo

r a

s

peci

fic lo

ng-t

erm

sav

ings

goa

l.

DD

Man

age

brok

erag

e or

ret

irem

ent

acco

unt.

Co

nsum

er

Pro

tect

ion

&

Insu

ranc

e

Part

icip

ants

:DD

Kno

w w

here

to

find

con

sum

er in

form

atio

n

o

n fin

anci

al p

rodu

cts.

DD

Kno

w t

heir

con

sum

er

r

ight

s.DD

Kno

w w

here

to

find

inf

orm

atio

n on

ins

uran

ce p

rodu

cts.

DD

Kno

w t

he t

ypes

of

p

rodu

cts

and

serv

ices

pro

vide

d by

insu

ranc

e

p

rovi

ders

.

Part

icip

ants

: DD

Feel

com

fort

able

ask

ing

prov

ider

s

q

uest

ions

abo

ut t

heir

fina

ncia

l pro

duct

s.DD

Belie

ve it

is im

port

ant

to

have

insu

ranc

e.

Part

icip

ants

are

abl

e to

:DD

Res

earc

h an

d ev

alua

te

c

onsu

mer

info

rmat

ion

on

finan

cial

pro

duct

s

b

efor

e bu

ying

.DD

Purc

hase

app

ropr

iate

ins

uran

ce c

over

age.

Part

icip

ants

:DD

Cal

l a fi

nanc

ial c

oach

/

cou

nsel

or w

hen

wor

ried

abo

ut t

heir

fina

nces

.DD

Rou

tinel

y se

ek

i

nfor

mat

ion

from

cre

dibl

e so

urce

s on

fina

ncia

l pro

duct

s.DD

Che

ck t

erm

s an

d

c

ondi

tions

bef

ore

pur

chas

ing

a fin

anci

al

p

rodu

ct.

DD

Rep

ort

susp

icio

us

p

rodu

cts

to t

he C

FPB.

Part

icip

ants

exp

erie

nce:

DD

Incr

ease

d am

ount

of

a

ppro

pria

te in

sura

nce

cov

erag

e.DD

Incr

ease

d ab

ility

to

man

age

fluct

uatio

ns in

inc

ome.

DD

Few

er c

osts

due

to

fra

ud.