ICIS Power & Carbon Seminar - Amazon S3

227

ICIS Power & Carbon Seminar First Day 14-15 November 2018 Berlin, Germany

Transcript of ICIS Power & Carbon Seminar - Amazon S3

ICIS Power amp Carbon Seminar

First Day

14-15 November 2018Berlin Germany

ICIS is a world leading price reporting agency and analytics powerhouse for commodity markets

Prices News Analytics Data

Petro-Chemical

Energy Fertilizers

1030-1100Keynote AddressBarbara Lempp Managing Director EFET

Dr Tobias Paulun EEX

1100-1145 Forecasting European power marketsPhilipp Ruf ICIS

1245-1315 QampA with the European CommissionPeter Zapfel European Commission

Coffee Break

1215-1245What is behind the latest carbon price

moveStefan Feuchtinger ICIS

Lunch Break

1415-1445What to look out for ndash a mid- to long-term

forecast for Europersquos carbon marketMarcus Ferdinand ICIS

1445-1530Southern Europe A renewable revolution

in Italy and SpainMatteo Mazzoni amp Matt Jones ICIS

1800Networking ReceptionSponsored by EEX

Melia Hotel Tapas Bar

Coffee Break

1600-1730Coal phase-out ndash key for low carbon

transitionMarcus Ferdinand amp Matt Jones amp Vija Pakalkaite ICIS

Keynote

Address

Barbara LemppManaging Director EFET

Dr Tobias PaulunChief Strategy Office EEX

Forecasting European Power Markets

This is a sample text Insert your

desired text here Philipp RufDirector ndash Carbon amp Power Analytics

copyright copy 2018 ICIS wwwiciscom 7

We are scaling up our country coverage to build a pan-European service on power price forecasting

Sep 2018

bullBiggest countries and central Western Europe

bullAT BE DE ES FR IT NL PL UK

Dec 2018

bullBaltics

bullEE LT LV

Jan 2019

bullNordics and Czech

bullCZ DK FI NO SE

H1 2019

bullSouth-East EU and remaining

bullConstant publication

bullBG CH GR HU HR IE PT RO SI SK

copyright copy 2018 ICIS wwwiciscom 8

Model methodology

Overall methodology

Dispatch model ndash we are modelling

the hourly dispatch mimicking how

the market clearing works

Global optimization model that

minimizes all system costs subject

to a number of constrains (or

maximization of social welfare)

Formulated as a linear programming

model

Features

Optimal dispatch of generation including trade

Incorporation of start-up costs

Full EU integration capacities of all major interconnectors

Detailed hydro modelling

Accurate cycling of thermal generation

Taking into account technical restrictions part-load efficiencies reservoir levels ramping restrictions

copyright copy 2018 ICIS wwwiciscom 9

Capacity assumptions

Existing Capacities

TSO Data

hellip

Nuclear

bull Project based new capacity

bull Decommissioning based on plant by plant approach

Fossil (lignite coal gas)

bull Project based new capacity

bull Decommissioning on announced closures coal phase-out plans and lifetime approach

Renewables

bull New capacity based on subsidy systems (incl auctions) as well as long-term country strategies

bull Only minor decommissioning expected

Future Capacities

copyright copy 2018 ICIS wwwiciscom 10

What does that mean Where are capacities going

0

100

200

300

400

500

600

700

800

900

1000

ca

pa

city

Capacity Development of Modelled Countries

Nuclear Lignite Coal Gas Oil Hydropower Bio Wind Solar

copyright copy 2018 ICIS wwwiciscom 11

Trend 1 ndash coal phase-outs all over Europe

Phase-outs planned in all

modelled countries

except Poland

Some are fixed in

legislation (AT FR ES

NL UK)

Others not (DE IT)

Total reduction of

capacity

Lignite 105GW or -38

Coal 512GW or -68

0

100

200

300

400

500

600

700

800

900

1000

ca

pa

city

Capacity Development of Modelled Countries

Nuclear Lignite Coal Gas Oil Hydropower Bio Wind Solar

copyright copy 2018 ICIS wwwiciscom 12

Trend 2 ndash increase of renewables

All modelled countries

have a significant

increase of renewables

We expect the largest

increase in wind

capacity with 131GW

additional or +120

Solar will deliver

second with 118GW

additional or +77

0

100

200

300

400

500

600

700

800

900

1000

ca

pa

city

Capacity Development of Modelled Countries

Nuclear Lignite Coal Gas Oil Hydropower Bio Wind Solar

copyright copy 2018 ICIS wwwiciscom 13

Fuel price assumptions mixture of internal modelling and external benchmarks

Carbon ICIS carbon forecast

Lignite based on own assumptions

Coal Based on forward curve

(API2) and extrapolated behind the

curve

Gas Forward curve based on ICIS

price assessments behind the

forward curve we utilise World

Banklsquos natural gas forecast

000

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

price

Fuel Price Assumptions

carbon [EURtonne] lignite [EURtonne]

coal [USDtonne] gas [EURMWh]

copyright copy 2018 ICIS wwwiciscom 14

Trend 3 ndash we expect carbon prices to increase rapidly in the early years of the 2020s and relax in the later years

Political context post-2020 reform with the strengthened MSR is cutting supply short and is a game changer for the system

Participants in the last month the increased political stability incentivised financial players to participate in the system

Volume Due to the MSR abatement in the future will be necessary and will have to be delivered through fuel switch in the power sector and carbon efficiency measures in industry

000

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

price

Fuel Price Assumptions

carbon [EURtonne] lignite [EURtonne]

coal [USDtonne] gas [EURMWh]

copyright copy 2018 ICIS wwwiciscom 15

Trend 4 Brexit

Power Markets

Link to internal energy markets at risk

As UK is highly dependent on electricity imports the continued functioning of the interconnectors are crucial

Long-term policies are defined independently of Brexit

Future of UK power market highly dependent on party manifestos

Carbon Markets

Creating sentiment effect in the last weeks

Short-term effects of hard Brexit selling by utilities and industrials

Long-term solution requires adjustment of the system

Both ambition levels for carbon reduction UK and EU should not be seriously affected

copyright copy 2018 ICIS wwwiciscom 16

The base case power price forecasts

4500

5000

5500

6000

6500

7000

7500

price

fo

reca

st [E

UR

MW

h]

Power Price Forecast ndash Base Cases

AT BE ES FR DE IT NL PL UK

What is behind the latest carbon price move Have times really changed

Stefan FeuchtingerSenior Analyst ndash Carbon amp Power Analytics

Current Market Situation

copyright copy 2018 ICIS wwwiciscom 19

Last 5 years EUA price developmentsEverything before 2018 was boring

000

500

1000

1500

2000

2500

3000

ca

rbo

n p

rice [euro

to

nn

e]

EUA price

+258 in the

last 12 months+334 peak

copyright copy 2018 ICIS wwwiciscom 20

Last 5 years EUA price developmentsEverything before 2018 was boring

000

500

1000

1500

2000

2500

3000

ca

rbo

n p

rice [euro

to

nn

e]

EUA price 200 per Mov Avg (EUA price)

+258 in the

last 12 months+334 peak

EUA price developmentsVolumes are picking up EU carbon in second boom period

000

500

1000

1500

2000

2500

3000

000

500

1000

1500

2000

2500

3000

vo

lum

e [

m to

nn

es]

ca

rbo

n p

rice [euro

to

nn

e]

EUA trading volume EUA price EUA trading volume (yearly average) EUA trading volume (quarterly average)

copyright copy 2018 ICIS wwwiciscom 22

EUA price developments30-day-volatility was decreasing September massive increase towards historic heights then recently slight decrease

0

01

02

03

04

05

06

07

08

09

1

000

500

1000

1500

2000

2500

3000

30 d

ay v

ola

tilit

y

ca

rbo

n p

rice [euro

to

nn

e]

EUA price 30-day volatility

copyright copy 2018 ICIS wwwiciscom 23

EUA price and Article 29aBoogeyman or serious threat

000

500

1000

1500

2000

2500

3000

3500

ca

rbo

n p

rice [euro

to

nn

e]

Historical_Price Six months trigger_Overlapping Two-year average_Overlapping

Six months trigger_Successive Two-year average_Successive

copyright copy 2018 ICIS wwwiciscom 24

EUA auctions biddingBidding range increasing since early 2018 - successful bidders too

-6000

-4000

-2000

000

2000

4000

6000

000

500

1000

1500

2000

2500

No

O

f b

idde

rs

ca

rbo

n p

rice [euro

to

nn

e]

SuccessfulBidders BidRange auctionPrice

copyright copy 2018 ICIS wwwiciscom 25

The link to power pricesPower market spreads are key indicator for carbon price changes especially in key markets like Germany spreads are closely linked to carbon

Clean Brown Spread

000

500

1000

1500

2000

2500

3000

000

500

1000

1500

2000

2500

3000

ca

rbo

n p

rice [euro

to

nn

e]

CB

S [

euroM

Wh

]

CBS (front month) CBS (front year) EUA price

The link to power pricesPower market spreads are key indicator for carbon price changes especially in key markets like Germany spreads are closely linked to carbon

Clean Dark Spread

000

500

1000

1500

2000

2500

3000

-1000

-500

000

500

1000

1500

ca

rbo

n p

rice [euro

to

nn

e]

CD

S [

euroM

Wh

]

Axis Title

CDS (front month) CDS (front year) EUA price

copyright copy 2018 ICIS wwwiciscom 27

The link to power pricesPower market spreads are key indicator for carbon price changes especially in key markets like Germany spreads are closely linked to carbon

Clean Spark Spread

000

500

1000

1500

2000

2500

3000

-2000

-1500

-1000

-500

000

500

1000

ca

rbo

n p

rice [euro

to

nn

e]

CS

S [

euroM

Wh

]

CSS (front month) CSS (front year) EUA price

copyright copy 2018 ICIS wwwiciscom 28

The link to power pricesPower market spreads are key indicator for carbon price changes especially in key markets like Germany spreads are closely linked to carbon

Fuel Switching costs

000

500

1000

1500

2000

2500

3000

-1000

000

1000

2000

3000

4000

5000

ca

rbo

n p

rice [euro

to

nn

e]

To

tal sw

itch

ing

co

sts

[euro

MW

h]

FS (frontmonth) FS (frontyear) EUA price

copyright copy 2018 ICIS wwwiciscom 29

EUA price developmentsWhy did we see a bull run What did change that EUAs are suddenly hip again

Legal certainty about Phase 4

reform

000

500

1000

1500

2000

2500

3000

000

500

1000

1500

2000

2500

3000

vo

lum

e [

m to

nn

es]

ca

rbo

n p

rice [euro

to

nn

e]

EUA price

first vote in

Parliament

first vote in

Council

discussion Trilogue

negotiations

compromise

reached

rubberstamping

copyright copy 2018 ICIS wwwiciscom 30

EUA price developmentsWhy did we see a bull run What did change that EUAs are suddenly hip again

Legal certainty about Phase 4

reform

Market stability reserve a game

changer (already now)

0

200

400

600

800

1000

1200

[m E

UA

s]

MSR intake

final auction MSR intake

Increase intake rate from 12 to

24 for 5 years ndash 26bn from 21-30

copyright copy 2018 ICIS wwwiciscom 31

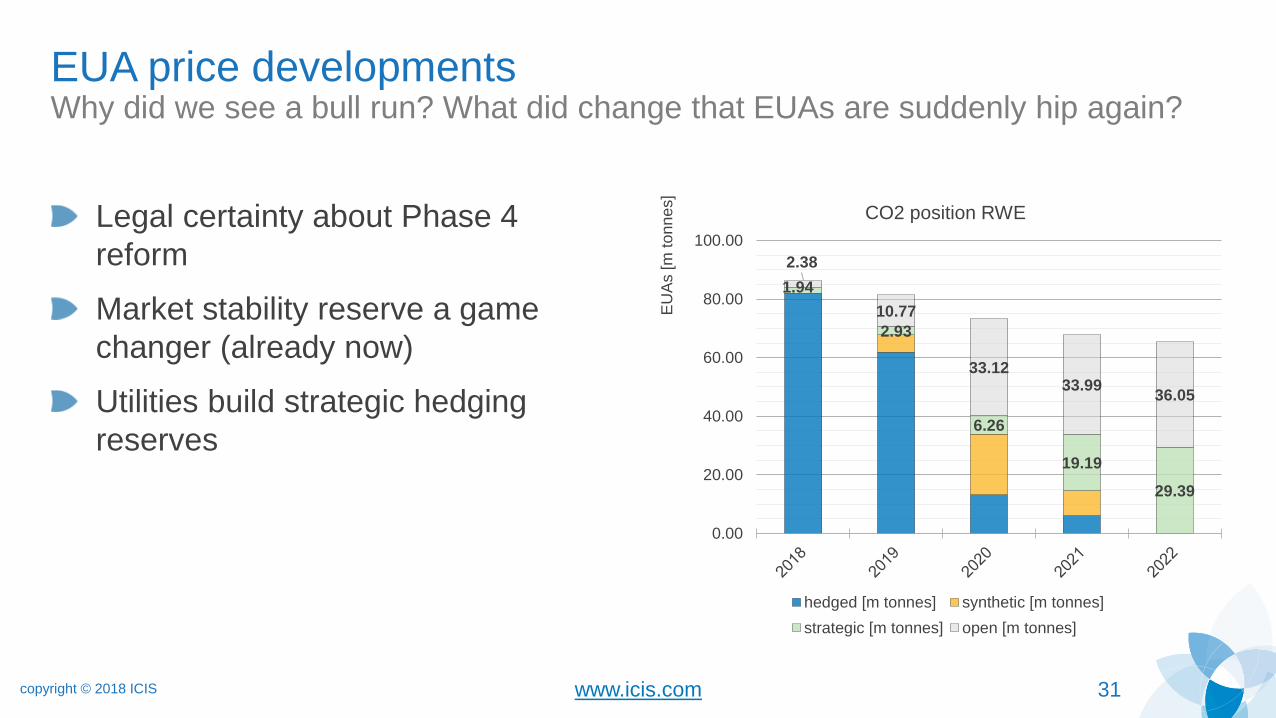

EUA price developmentsWhy did we see a bull run What did change that EUAs are suddenly hip again

Legal certainty about Phase 4

reform

Market stability reserve a game

changer (already now)

Utilities build strategic hedging

reserves

194

293

626

1919

2939

238

1077

33123399

3605

000

2000

4000

6000

8000

10000

EU

As [m

to

nn

es]

CO2 position RWE

hedged [m tonnes] synthetic [m tonnes]

strategic [m tonnes] open [m tonnes]

copyright copy 2018 ICIS wwwiciscom 32

EUA price developmentsWhy did we see a bull run What did change that EUAs are suddenly hip again

Legal certainty about Phase 4

reform

Market stability reserve a game

changer (already now)

Utilities build strategic hedging

reserves

New players getting active

(financials funds)

Sentiment amp price elasticity

000

500

1000

1500

2000

2500

3000

-1800

-1300

-800

-300

200

700

ca

rbo

n p

rice [euro

to

nn

e]

qu

art

erly m

ark

et b

ala

nce

[m

to

nn

es]

traded positions traded positions (revised) price

Mid-Term View

copyright copy 2018 ICIS wwwiciscom 34

The fundamentalsThe MSR is increasing the pressure on compliance companies in the next years

Yearly supply is not enough

anymore to cover yearly demand

Compliance companies will be

forced to invest in reduction

measures or historic surplus needs

to come to market

First available are fuel switch from

coal to gas

Later on industrial abatement

projects

00

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

em

issio

nsE

UA

s [m

to

nn

es]

allocation auction other MSR BAU emissions

copyright copy 2018 ICIS wwwiciscom 35

The fundamentalsWhere would CO2 reductions come from

Biggest abatement pressure is on

power sector in the beginning

Fuel switch on short notice available

No additional investments necessary

Immediate economic impact

Once fuel switch capacity is utilized

industrial and power sector need to

invest to abate emissions

Especially in second half of phase 4

industrials will start abating emissions

quicker

0

20

40

60

80

100

120

140

160

180

ab

ate

me

nt tr

igge

red

[m

to

nn

es]

abatement per sector

Power Industry

copyright copy 2018 ICIS wwwiciscom 36

Price ForecastThe Base Case ndash a conservative view

1000 euro

1500 euro

2000 euro

2500 euro

3000 euro

ca

rbo

n p

rice [euro

to

nn

e]

base

copyright copy 2018 ICIS wwwiciscom 37

Price ForecastScenarios around the risk of a hard Brexit

1000 euro

1500 euro

2000 euro

2500 euro

3000 euro

ca

rbo

n p

rice [euro

to

nn

e]

hardBrexit60m hardBrexit30m base

copyright copy 2018 ICIS wwwiciscom 38

The fundamentalsWhere does the historic surplus sit

0

400

800

1200

1600

2000

0

200

400

600

800

1000

cu

mu

lative

ho

ldin

g [m

EU

As]

ab

so

lute

ho

ldin

g [m

EU

As]

2017 holdings

utilities industry financial cumulative end of 2017

copyright copy 2018 ICIS wwwiciscom 39

Price ForecastScenario around changed speculative buying

1000 euro

1500 euro

2000 euro

2500 euro

3000 euro

ca

rbo

n p

rice [euro

to

nn

e]

base Spec-ContinuedSpecDemand Spec-Q2sellOff

copyright copy 2018 ICIS wwwiciscom 40

Price ForecastScenario around changed speculative buying

1000 euro

1500 euro

2000 euro

2500 euro

3000 euro

ca

rbo

n p

rice [euro

to

nn

e]

-18000

-14000

-10000

-6000

-2000

2000

6000

10000

sp

ecu

lative

vo

lum

e [

m E

UA

s]

Base case Continued spec demand Spec sell-off

copyright copy 2018 ICIS wwwiciscom 41

Conclusions

Only as of 2019 MSR intake leads to a significant scarcity on the market

In 2018 the increases are based on speculative buying and compliance

preparation for the MSR

Mid-term risks and opportunities

Hard Brexit

Clean spread development brown dark and spark spreads

Anticipation buying of compliance companies

Sell off triggered by one or few long players

Further behaviour of speculators

copyright copy 2018 ICIS wwwiciscom 42

Price ForecastScenario comparison

1000 euro

1500 euro

2000 euro

2500 euro

3000 euro

ca

rbo

n p

rice [euro

to

nn

e]

hardBrexit60m hardBrexit30m base Spec-ContinuedSpecDemand Spec-Q2sellOff price price

Peter ZapfelHead of Unit B1 ndash ETS policy Development and Auctioning European Commission

QampA

Marcus FerdinandHead of European Carbon amp Power Analytics

What to look out for ndash a mid to long-term forecast for Europersquos carbon market

copyright copy 2018 ICIS

Agenda

1) The market turns short

2) Market Stability Reserve ndash room for review

3) Coal phase-out ndash implications for the carbon price

copyright copy 2018 ICIS wwwiciscom 46

The market balance during phase 4 ndash fundamental

-500

0

500

1000

1500

2000

2500

-400

-200

0

200

400

600

800

1000

1200 cu

mu

lativ

e b

ala

nce

ba

nked

MS

R [m

ton

ne

s]

ye

arly b

ala

nce

in [m

to

nn

es]

FundamentalBalance CumulativeFundamentalBalance

copyright copy 2018 ICIS wwwiciscom 47

The market balance during phase 4 ndash traded

-1000

-500

0

500

1000

1500

2000

2500

-400

-200

0

200

400

600

800

1000

1200 cu

mu

lativ

e b

ala

nce

ba

nked

MS

R [m

ton

ne

s]

ye

arly b

ala

nce

in [m

to

nn

es]

TradedBalance FundamentalBalance CumulativeTradedBalance CumulativeFundamentalBalance

copyright copy 2018 ICIS wwwiciscom 48

The market balance during phase 4 ndash MSRbanked

-1000

-500

0

500

1000

1500

2000

2500

3000

-400

-200

0

200

400

600

800

1000

1200 cu

mu

lativ

e b

ala

nce

ba

nked

MS

R [m

ton

ne

s]

ye

arly b

ala

nce

in [m

to

nn

es]

CumulativeBanked CumulativeMSR TradedBalance FundamentalBalance CumulativeTradedBalance CumulativeFundamentalBalance

The market stability

reserve ndash room for review

copyright copy 2018 ICIS wwwiciscom 50

One key bit needs to be taken into account the TNAC is not the available surplus

Due to the exclusion of EUA compliance by the aviation sector the TNAC is higher than the available surplus

Leads to overestimation of market surplus

Higher MSR outtake

In case aviation shortfall gt400 Mt lower threshold obsolete

Higher threshold nearly impossible to undercut

But CORSIA effect

We expect this to be changed and incorporate a TNAC equal to the surplus in our analysis from 2022 onwards

0

500

1000

1500

2000

2500

EU

As [

m to

nn

es]

cumulative aviation short thresholds surplus TNAC

Source ICIS

copyright copy 2018 ICIS wwwiciscom 51

Our base case analysis

Market to be squeezed in early TP4

This will trigger significant emission

reductions in power and industry

Decreasing base emissions reduce

hedge demand significantly

MSR goes back to 12 and demand

decreases (lower base emissions)

Triggered abatement increases TNAC

MSR is not capable to reduce over-

supply at the same speed

000

1000

2000

3000

4000

0

200

400

600

800

1000

1200

1400

1600

1800

ca

rbo

n p

rice [euro

to

nn

e]

EU

As [

m to

nn

es]

MSR thresholds TNAC hedge demand base price

Source ICIS

copyright copy 2018 ICIS wwwiciscom 52

The MSR in the context of coal phase-outs all over Europe20 less coal in Europe than BAU

Basics

20GW less than BAU coal capacity

150TWh less generation than BAU

50 back-filled by gas rest by RES

Roughly 90m tonnes emission cuts

Hedge demand reduces by 10m EUAs in 2030

Surplus increases by 15m EUAs

Prices will be more pressured and tend lower

0

200

400

600

800

1000

1200

1400

1600

1800

EU

As [

m to

nn

es]

MSR thresholds TNAC hedge demand

Source ICIS

copyright copy 2018 ICIS wwwiciscom 53

The MSR in the context of coal phase-outs all over Europe50 less coal in Europe than BAU

Basics

50GW less than BAU coal capacity

375TWh less generation than BAU

50 back-filled by gas rest by RES (investment needed)

Roughly 225m tonnes emission cuts

Hedge demand reduces by 90m EUAs in 2030

Surplus increases by 70m EUAs

Prices will be more pressured and tend lower

0

200

400

600

800

1000

1200

1400

1600

1800

EU

As [

m to

nn

es]

MSR thresholds TNAC hedge demand

Source ICIS

copyright copy 2018 ICIS wwwiciscom 54

The MSR in the context of coal phase-outs all over Europe70 less coal in Europe than BAU

Basics

70GW less than BAU coal capacity

525TWh less generation than BAU

50 back-filled by gas rest by RES (investment needed)

Roughly 315m tonnes emission cuts

Hedge demand reduces by 150m EUAs in 2030

Surplus increases by 153m EUAs

Prices will be more pressured and tend lower

0

200

400

600

800

1000

1200

1400

1600

1800

EU

As [

m to

nn

es]

MSR thresholds TNAC hedge demand

Source ICIS

copyright copy 2018 ICIS wwwiciscom 55

Consequences for the MSR parameter discussion (50 coal)

MSR parameters can be amended

with review

Two potential scenarios

Reduce thresholds (600 280 Mt)MSR continues to trigger

allowances during all years

MSR withdraws 235m allowances

more compared to 833400

thresholds

TNAC remains on lower pathway

0

200

400

600

800

1000

1200

1400

1600

1800

EU

As [

m to

nn

es]

MSR_600280 thresholds

TNAC_600280 hedge demand_600280

Source ICIS

copyright copy 2018 ICIS wwwiciscom 56

Consequences for the MSR parameter discussion (50 coal)

MSR parameters can be amended

with review

Two potential scenarios

Reduce thresholds (600 280 Mt)

Remain on 24 withdrawal rateMSR continues to trigger

allowances during all years

MSR withdraws 790m allowances

more compared to old thresholds

and 12 rate

TNAC remains on lower pathway

0

200

400

600

800

1000

1200

1400

1600

1800

EU

As [

m to

nn

es]

MSR_600280 MSR_600280_24

thresholds TNAC_600280

hedge demand_600280 TNAC_600280_24

hedge demand_600280_24

Source ICIS

copyright copy 2018 ICIS wwwiciscom 57

Price trajectories ndash highly assumptions-driven

000 euro

1000 euro

2000 euro

3000 euro

4000 euro

5000 euro

ICIS base case base emissions - MSR withdrawal rate base emissions - MSR threshold and withdrawal rate

20 coal reduction 50 coal reduction 70 coal reduction

20 coal - MSR thresholds 50 coal - MSR thresholds 70 coal - MSR thresholds

20 coal - MSR thresholds and withdrawal 50 coal - MSR thresholds and withdrawal 70 coal - MSR thresholds and withdrawal

Source ICIS

copyright copy 2018 ICIS wwwiciscom 58

Conclusion

Changing power sector dynamics could lead to significantly lower emissions

If we factor in the current trend towards coal phase-outs all over EuropeThe surplus increases more

The hedge demand reduces more

With lower power sector demand TNAC increases with current MSR parameters

According to our analysis the MSR will not be strong enough to mitigate the surplus built-up due to lower emissions

Less demand results in laxer market balance lower prices

Adjustment of MSR parameters an option to keep market tightness

Southern Europe ndash a renewable revolution in Italy and Spain

Matteo MazzoniSenior Analyst ndash EU Carbon amp Power Analytics

Matt JonesSenior Analyst ndash EU Carbon amp Power Analytics

copyright copy 2018 ICIS

Agenda

1) Historical renewable developments in Spain and Italy

2) Recent and upcoming auctions

3) Renewable growth trajectories

4) Potential for lsquosubsidy-freersquo renewables

Drivers of subsidy-free RES

Merchant-risk

PPAs

Government de-risking

5) Signposts

6) Conclusions

Historical renewable

developments in Spain

and Italy

copyright copy 2018 ICIS wwwiciscom 62

Renewable generation within the energy mix

Gas41

Coal16

Nuclear19

Other fossil4

Hydro7

Solar1

Wind11

Biomass1

RES20

Gas25

Coal17

Nuclear21

Other fossil4

Hydro8

Solar5

Wind18

Biomass1

Others0

RES32

Gas58

Coal14

Other fossil8

Hydro14

Solar0

Wind2

Biomass3

Others2

RES20

Gas46

Coal11

Other fossil8

Hydro12

Solar8

Wind6

Biomass6

Others2

RES34

Italian Generation Mix Spanish Generation Mix

2008

2017

Source Terna Source REE

copyright copy 2018 ICIS wwwiciscom 63

Where are they now RES capacity grew quickly

0

20

40

60

80

100

120

GW

Installed RES capacity by country

Spain Germany Italy France UKSource IRENA

copyright copy 2018 ICIS wwwiciscom 64

Renewable targets for 2020

10

12

14

16

18

20

22

Spain Italy

sh

are

Renewable shares vs 2020 target ()

2016 2020 target

Italy is already exceeding

its 2020 target due to

rapid growth 2010-2012 in

particular

Spain remains behind on

its own target due to

stagnant growth in recent

years

Uncertainty over whether

the 201617 auctions will

be enough for Spain to

reach its target

copyright copy 2018 ICIS wwwiciscom 65

Feed-in-tariffs give way to auctions

Spain Italy

Market Premium scheme reformed 2012

-RES capacity almost flat since

-Numerous lawsuits under the ECT

-No longer open to installations

gt5MW

-De facto moratorium on new RES

FiT and FiP reformed in 2015

-RES capacity almost flat since

-No longer open to installations

gt5MW

-De facto moratorium on new RES

No Green Certificates scheme No Green Certificates scheme

Tendering scheme introduced in 2016

- Three rounds held

- Floor price mechanism

- More auctions planned but not

announced

RES auctions planned for 2019 and 2020

- First round suggested Jan-2019

- Contracts-for-differences style

scheme proposed

- Likely to be delayed again

Recent and upcoming

auctions

copyright copy 2018 ICIS wwwiciscom 67

The introduction of renewable auctions in Spain

Source ICIS OMIE

Auction Date TechnologyCapacity target

(MW)

Capacity awarded

(MW)Weighted average floor price (euroMWh)

Jan 2016Onshore wind

700 in total569 0

Biomass 200 0

May 2017

Onshore wind

3000 in total

2780 399

Other RES 19 416

Solar 1 422

Jul 2017Onshore wind

3000 in total1128 282

Solar 3909 327

Total 6700 8606

copyright copy 2018 ICIS wwwiciscom 68

Key features of the Spanish auctions

Prices cleared below market prices

Bidders can expect to get the market price except when prices fall below the auction floor price

Payments for unlimited duration

The floor price level calculation methodology can be revised every six years

0

10

20

30

40

50

60

70

Onshore windSpain

Solar Spain Onshore windItaly

Solar France Onshore windGermany

Solar Germany

euroM

Wh

(no

min

al)

Lowest subsidy price vs 2020 market price

Lowest subsidy 2020 power price (ICIS assessment 30 Oct)

copyright copy 2018 ICIS wwwiciscom 69

Auctions in Spain and Italy

0

20

40

60

80

100

120

140

160

euroM

Wh

(no

min

al)

Prices at auctions - Spain vs other EU countries

Onshore wind Spain Solar Spain Onshore wind Italy Onshore wind Germany Solar Germany Solar France

copyright copy 2018 ICIS wwwiciscom 70

Upcoming auctions in Italy

Italy is planning to auction 79 GW of capacity between January 2019 and May 2021

Of the total 56GW will be for solar and wind competing against one another

Winning bidders will be offered a CfD contract (like the UK model for RES support)

The latest draft of the decree sets a 70 euroMWh for wind and solar

Session Date Auction Registry Auction Registry Auction Registry Auction Registry

1 31012019 500 45 - 100 10 10 60 10

2 31052019 500 45 - 100 10 10 60 10

3 30092019 700 100 - 100 10 10 60 10

4 31012020 700 100 - 100 10 10 60 10

5 31052020 800 120 - 100 10 10 60 10

6 30092020 800 120 - 100 20 10 60 10

7 31012021 800 120 - 100 20 10 70 10

8 31052021 800 120 - 100 20 10 70 10

5600 770 0 800 110 80 500 80

Solar-Wind Solar asbestos sub Hydro-Biogas Repowering

Total

CAPACITY AVAILABLE (MW)

Source MiSE

Renewable growth

trajectories

copyright copy 2018 ICIS wwwiciscom 72

SpainItaly 2030 RES targets in the EU context

RES Targets 2020 2030

Europe20

(binding)

32

(binding)

Italy17

(binding)

28

(non-binding)

Spain20

(binding)

35

(non-binding)

The EU has recently agreed on a

32 RES target by 2030

Italy set a 28 RES target for

2030 which is below the EU target

Notwithstanding numerous

announcements Spain has yet to

publish the Energy Transition

Strategy which is expected to

come by the end of the year

copyright copy 2018 ICIS wwwiciscom 73

Italy the National Energy Strategy (SEN)

1740

22

28

2016 2030 BAU 2030 SEN

RES ON ENERGY CONSUMPTION

335038

55

2016 2030 BAU 2030 SEN

RES ON ELECTRICITY CONSUMPTION

The SEN was presented in November 2017 after a long consultation with more than 250 stakeholders

The SEN went beyond the RES EU target proposed by the EC but it now falls short of the new target

Great part of the rise is on the power sector with solar accounting for 24 of the electricity consumption and wind for 13

The SEN foresees EUR 35bn to be invested in RES and EUR 30bn to be invested in grids

Source MiSE

copyright copy 2018 ICIS wwwiciscom 74

Expectations for Spanish and Italian RES capacity

0

10

20

30

40

50

60

GW

Solar capacity forecast 2018-2030 (GW)

Spain Italy

0

5

10

15

20

25

30

35

GW

Wind capacity forecast 2018-2030 (GW)

Spain Italy

Source Icis Horizon Power model

Subsidy-free solar and

wind growth

copyright copy 2018 ICIS wwwiciscom 76

Why is subsidy-free renewables increasingly discussed

We have started to see the

first zero-subsidy solar and

onshore wind project come

online while offshore wind

projects are due in the

early 2020s

The development is driven

primarily by rapidly falling

technology costs 0

50

100

150

200

250

30

40

50

60

70

80

90

100

Ca

pa

city a

uctio

ne

d (

MW

)

Str

ike

price (

euroM

Wh

)

Solar auction results in Germany since 2015

capacity (MW) mean average successful bid (euroMWh)

copyright copy 2018 ICIS wwwiciscom 77

Why are Spain and Italy likely to be at the forefront

Both Spain and Italy have good resources for solar and wind

Both countries have high power prices by European standards

0

10

20

30

40

50

60

70

2016 2017 2018 YTD

euroM

Wh

Average power prices in Spain and Italy are ~euro16MWh higher vs Germany

Germany Italy Spain

copyright copy 2018 ICIS wwwiciscom 78

Why are Spain and Italy likely to be at the forefront

Both Spain and Italy have good resources for solar and wind

Both countries have high power prices by European standards

47

49

51

53

55

57

59

61

63

euroM

Wh

ICIS Horizon power price forecasts euroMWh

Italy Spain Germany

copyright copy 2018 ICIS wwwiciscom 79

Full merchant risk ndash price volatility

Merchant projects are risky given

uncertainty over future prices and

volatility

Without a guaranteed strike price

generators would be faced with

varying income on the wholesale

market

Volatility to increase over time

while seasonal variation will

increaseSource OMIE

0

10

20

30

40

50

60

70

80

90

100

euroM

Wh

Spanish hourly prices July 2017-July 2018

Hourly prices Average price

copyright copy 2018 ICIS wwwiciscom 80

Full merchant risk ndash price direction uncertainty

We expect power prices to be driven significantly by carbon prices through to 2030

As a result wholesale power prices will be at their highest in 202324 before declining

as EUA prices fall and as more RES capacity is added

47

49

51

53

55

57

59

61

63

euroM

Wh

ICIS Horizon power price forecasts euroMWh

Italy Spain Germany

copyright copy 2018 ICIS wwwiciscom 81

Full merchant risk ndash price cannibalisation

In the absence of subsidy the key metric is the capture price rather than the wholesale

price as this reflects what the generator will actually receive

Capture prices are pushed lower as addition RES units of the same type are added

(price cannibalisation)

40

45

50

55

60

65

euroM

Wh

Italy average price vs RES capture prices

Onshore wind capture price Solar capture price Annual average wholesale price

copyright copy 2018 ICIS wwwiciscom 82

Full merchant risk ndash price cannibalisation

In the absence of subsidy the key metric is the capture price rather than the wholesale

price as this reflects what the generator will actually receive

Capture prices are pushed lower as addition RES units of the same type are added

(price cannibalisation)

30

35

40

45

50

55

60

65

euroM

Wh

Spain average price vs RES capture price

Onshore wind capture price Solar capture price Annual average wholesale price

copyright copy 2018 ICIS wwwiciscom 83

Power Purchase Agreements (PPAs)

PPAs de-risk projects by locking

in long-term prices

We are starting to see the first

PPAs signed for RES projects in

Spain and Italy

Most in Spain have been supplier

PPAs rather than the more

publicised corporate PPAs

PPA

Corporate Supplier

copyright copy 2018 ICIS wwwiciscom 84

Power Purchase Agreements (PPAs)

PPAs de-risk projects by locking

in long-term prices

We are starting to see the first

PPAs signed for RES projects in

Spain and Italy

The question is whether there will

be enough demand for PPAs to

enable large-scale subsidy-free

rollout

Source ICISWindEurope

0

1

2

3

4

5

6

2010 2011 2012 2013 2014 2015 2016 2017

GW

European corporate PPA demand vs Spanish and Italian RES capacity anticipation

European RES capacity sourced through PPAs

Spain anticipated RES per year (2019-2030)

Italy anticipated RES per year (2019-2030)

copyright copy 2018 ICIS wwwiciscom 85

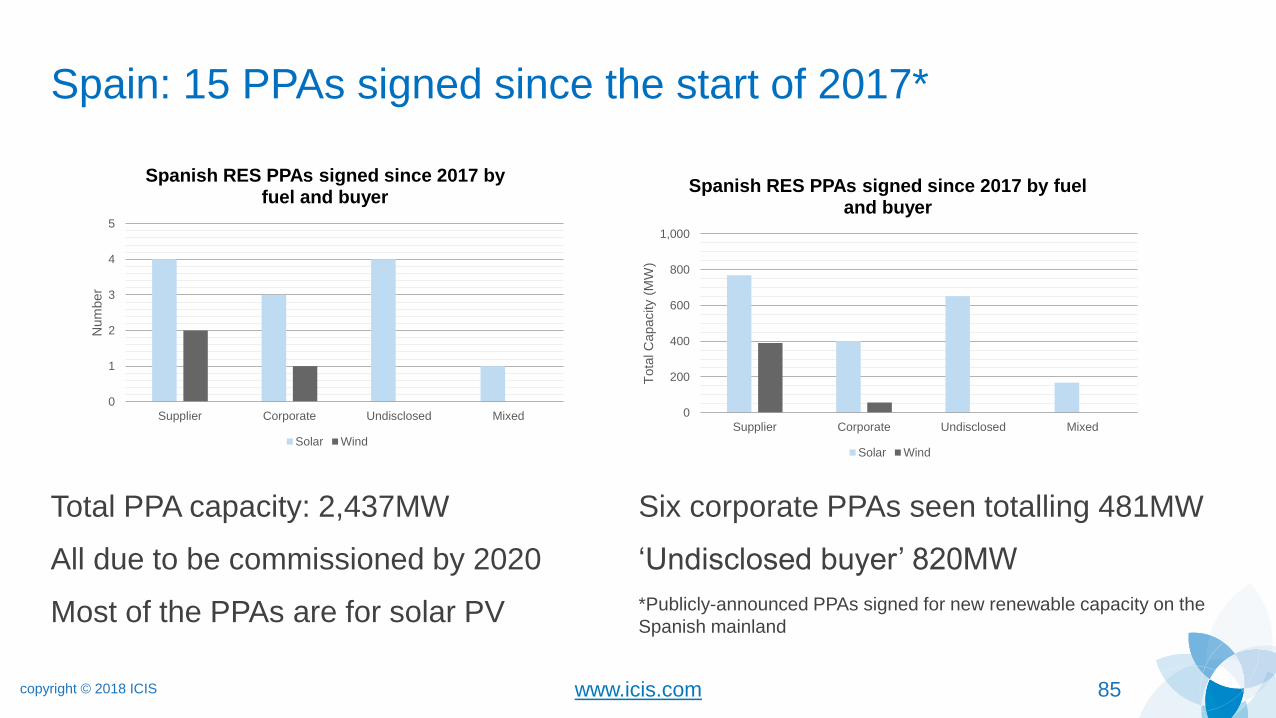

Spain 15 PPAs signed since the start of 2017

Total PPA capacity 2437MW

All due to be commissioned by 2020

Most of the PPAs are for solar PV

Six corporate PPAs seen totalling 481MW

lsquoUndisclosed buyerrsquo 820MW

Publicly-announced PPAs signed for new renewable capacity on the

Spanish mainland

0

1

2

3

4

5

Supplier Corporate Undisclosed Mixed

Num

ber

Spanish RES PPAs signed since 2017 by fuel and buyer

Solar Wind

0

200

400

600

800

1000

Supplier Corporate Undisclosed Mixed

Tota

l C

apacity (

MW

)

Spanish RES PPAs signed since 2017 by fuel and buyer

Solar Wind

copyright copy 2018 ICIS wwwiciscom 86

The most popular duration for PPAs in Spain is ten years

Five of the fifteen PPAs are for

ten years

Five PPAs are for longer than ten

years

Four PPAs are for an unreported

duration0

1

2

3

4

5

6

0

200

400

600

800

1000

1200

Nu

mb

er o

f P

PA

s

Tota

l cap

acit

y (M

W)

Duration (years)

Spanish RES PPAs signed since 2017 by duration

Capacity Count

copyright copy 2018 ICIS wwwiciscom 87

Government support Minimum price floors

Minimum price floors provide

some protection against worst

case scenario prices

However the price floor needs to

be high enough to improve

bankability but low enough to

protect the government from

paying large subsidies

The recent price floors seen in

Spain were set at very low levels

20

25

30

35

40

45

50

55

60

euroM

Wh

Spanish RES capture prices vs minimum price floors

Onshore wind capture price Solar capture price

Wind price floor Solar price floor

copyright copy 2018 ICIS wwwiciscom 88

Government support ldquoSubsidy-freerdquo CfDs

There is increasing talk in the UK

over ldquosubsidy-freerdquo CfDs for onshore

wind and solar

A similar idea could be seen in Italy

in the future

Generators would only be able to bid

in at the forecast power price level

Potential upside for the government

if prices rise above expectations but

downside if prices fall as subsidies

would be paid

40

45

50

55

60

65

70

euroM

Wh

Subsidy-free CfD price risk

ICIS price forecast Low price scenario High price scenario

copyright copy 2018 ICIS wwwiciscom 89

Signposts

The Spanish energy strategy due before end of 2018

The new Italian government announced it will revise its 2017 National Energy

Strategy

Strike prices in the upcoming Italian auctions

RES projects in Spanish recent auctions ndash how many projects will be

commissioned and on time

copyright copy 2018 ICIS wwwiciscom 90

Conclusions

Subsidy-free projects are beginning to emerge in a number of EU member

states

However Spain and Italy could be the first EU countries to attempt to roll out

subsidy-free capacity at scale driven by comparatively higher power prices

Investor appetite for risk given market price uncertainty will remain the greatest

challenge going forward How many projects can get off the ground

The PPA market can help de-risk projects but it remains in a nascent stage

Continued reductions in LCOE will help improve the prospects for projects

Our forecasts suggest that profit margins will be best for early movers

Coal phase-outs ndash key for the low carbon transition

Vija PakalkaiteAnalyst ndash EU Carbon amp Power Analytics

Matt JonesSenior Analyst ndash EU Carbon amp Power Analytics

Marcus FerdinandHead of EU Carbon amp Power Analytics

copyright copy 2018 ICIS

Agenda

1) Overview of coal phase-out in Europe Policy discussions and capacity

expectations

2) Netherlands Total phase-out and carbon price floor

3) Germany Gradual phase-out

4) Poland Clinging on to coal

5) Conclusions Comparing the three national approaches

Overview of coal-phase

out in Europe

copyright copy 2018 ICIS wwwiciscom 94

Europersquos current power mix

Nuclear 27

Coal and lignite 23Gas 17

Oil 2

Biomass 6

Hydro 12

Wind 10Solar 3

EU generation share

Coal and lignite account for 23 of the

European electricity mix at present

Coal and lignite have the second

largest installed capacity in the EU

(139GW) behind gas and ahead of

nuclear

Germany is the dominant country for

coal and lignite accounting for 31 of

EU capacity followed by Poland (21)

0

50

100

150

200

250

Gas Coal amp lignite Nuclear

GW

Installed capacity in the EU

copyright copy 2018 ICIS wwwiciscom 95

Coal phase-out plans

CountryCapacity

(MW)Phase-out date

UK 11160 2025

Italy 7806 2025

Netherlands 4692 2030

Denmark 2776 2030

France 2335 2021

Finland 1693 2029

Portugal 1677 2030

Ireland 855 2025

Austria 644 2025

Sweden 130 2022

copyright copy 2018 ICIS wwwiciscom 96

BREF limits

Put restrictions on the NOx and SO2

emissions from plants

Plants will have to abide by

regulations from 2021 or close

Estimates that up to a third of

Europersquos coal-fired capacity affected

Will countries be able to obtain

derogations

copyright copy 2018 ICIS wwwiciscom 97

Capacity market legislation

Council Parliament

Rule

New plants will only be eligible to receive payments in a capacity

market if their emissions are below 550 gr CO2KWh or if their

emissions are less than 700 Kg CO2

New plants will only be eligible to receive payments in a capacity market if their emissions are below 550 gr CO2KWh However specific lower limit of 200 Kg

CO2 on average per year per installed KW is applied to plants in a strategic reserve

Date applicable

2025 (new) 2030 (existing) 2019 (new) 2024 (existing)

Coal-fired plants wanting to enter a capacity market will be affected by

EU legislation in the Electricity Market Design Regulation

Hard coal 08tMWh

Lignite 11tMWh

700 (Council) 10 7

200 (Parliament) 3 2

copyright copy 2018 ICIS wwwiciscom 98

EU Coallignite capacity forecast 2018-2030

Coallignite capacity expected to decline from 139GW in 2018 to

88GW in 2025 and 58GW in 2030

0

20000

40000

60000

80000

100000

120000

140000

160000

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

MW

EU coal amp lignite capacity by country 2018-2030 (MW)

Germany Poland UK Czech Republic Spain Italy NetherlandsGreece Bulgaria Romania Denmark France Finland PortugalHungary Slovenia Ireland Austria Slovakia Croatia Sweden

Source ICIS Source ICIS

copyright copy 2018 ICIS wwwiciscom 99

EU Coallignite capacity forecast 2018-2030

Coallignite capacity expected to decline from 139GW in 2018 to

88GW in 2025 and 58GW in 2030

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

MW

EU coal amp lignite capacity 2018 and 2030 (MW)

2018 2030Source ICIS

copyright copy 2018 ICIS wwwiciscom 100

Differing trends for coal and lignite

We expect coal capacity to fall considerably while lignite will prove more resilient

Coal capacity to fall from 87GW in 2018 to 26GW in 2030

Lignite to decline from 52GW in 2018 to 32GW in 2030

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

MW

EU coal and lignite capacity 2018-2030 (MW)

Coal LigniteSource ICIS

Source ICIS

Netherlands Coal phase-

out and carbon price floor

copyright copy 2018 ICIS wwwiciscom 102

Complete coal phase-out by 2030

Currently the Netherlands has 47GW coal-fired capacity available (5 plants)

three of which came online as recently as 2015

Remaining units

Source ICIS

copyright copy 2018 ICIS wwwiciscom 103

Complete coal phase-out by 2030

The two oldest plants will be forced to close at the end of 2024 the three

newest plants by the end of 2029

Currently the Netherlands has 47GW coal-fired capacity available (5 plants)

three of which came online as recently as 2015

Remaining units

Source ICIS

copyright copy 2018 ICIS wwwiciscom 104

Dutch CO2 emissions and targets

Urgenda ruling called for 25 cut in CO2 (compared to 1990) by 2020 ndash

government in danger of missing this target

Government has set its own ambitions for a 49 cut by 2030 ndash this is driving

the plans for coal phase-out and the carbon price floor

0

50

100

150

200

250

mtC

O2

Dutch greenhouse gas emissions

Actual Urgenda target Coalition target

Source ICIS

copyright copy 2018 ICIS wwwiciscom 105

Coal amp gas in the Dutch power mix

Several older coal-fired plants have closed over the past three years which has

led to lower coal-fired generation output

Gas output has begun to exceed coal output and the trend will continue due to

carbon prices and coal closures

0

5

10

15

20

2015 2016 2017

Cap

acity [

GW

]

Dutch coal amp gas capacity (GW)

Coal Gas

0

10

20

30

40

50

2015 2016 2017

Ge

ne

ratio

n [T

Wh]

Dutch coal amp gas output (TWh)

Coal Gas

Source TenneT

copyright copy 2018 ICIS wwwiciscom 106

Modelling Impact on coal output

Coal capacity will close in line with the announced dates (20252030)

Output will be driven partially by these closures but also by our carbon price

expectations

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Cap

acity [

MW

]

Dutch coal capacity forecast (MW)

0

5

10

15

20

25

30

Ge

ne

ratio

n [T

Wh]

Dutch coal generation forecast (TWh)

Source ICIS

copyright copy 2018 ICIS wwwiciscom 107

Modelling Impact on gas output

Gas-fired output will increase through to 2023 as EUA prices drive fuel switching

Output will decline in the later 2020s due to softening EUAs and increased RES

Full coal phase-out in 2030 will lead to an increase in gas output

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

Cap

acity [

MW

]

Dutch gas capacity forecast (MW)

0

10

20

30

40

50

60

70

80

Ge

ne

ratio

n [T

Wh]

Dutch gas generation forecast (TWh)

Source ICIS

copyright copy 2018 ICIS wwwiciscom 108

Modelling Price impact

46

48

50

52

54

56

58

Duts

ch

po

we

r p

rice

fo

reca

st [euro

MW

h] Dutch power price forecast (euroMWh)

Final three coal

plants close

Prices driven higher by

EUA price increase

Fuel switching seen

EUA prices fall increasing

offshore wind and solar

output pressures prices

lower

Gas and coal

prices soften

new

interconnectors

Source ICIS

copyright copy 2018 ICIS wwwiciscom 109

Carbon price floor plan

In addition to the coal phase-out the government plans to introduce a carbon price floor for the

power sector

The floor would start at euro18tonne in 2020 increasing to euro43tonne in 2030

We anticipate the floor to be below EUA prices until 2026

0

10

20

30

40

50

Car

bo

n p

rice

flo

or

[eurot

on

ne

]

ICIS EUA forecast vs proposed Dutch carbon price floor

Proposed price floor ICIS carbon priceSource ICIS

copyright copy 2018 ICIS wwwiciscom 110

Carbon price floor ndash coal amp gas output

We anticipate that the carbon price floor would have no impact for the first five years after

implementation

From 2026-2030 the price floor would lead to a reduction in both coal and gas output

compared to the base case

0

5

10

15

20

25

30

Ge

ne

ratio

n [T

Wh]

Dutch coal output forecast (TWh)

Base case Carbon price floor

0

10

20

30

40

50

60

70

80

Ge

ne

ratio

n [T

Wh]

Dutch gas output forecast (TWh)

Base case Carbon price floor

Source ICIS

copyright copy 2018 ICIS wwwiciscom 111

Carbon price floor ndash net imports

Under the base case assumptions the Netherlands becomes a net exporter in 2023 and

maintains this position through to 2030

If the carbon price floor is introduced the Netherlands will revert back to a net importer status as

imports replace domestic coal amp gas generation

-15

-10

-5

0

5

10

15

20

25

Net im

po

rts [T

Wh

]

Base case net imports (TWh)

-10

-5

0

5

10

15

20

25

Net im

po

rts [T

Wh

]

Carbon price floor net imports (TWh)

Source ICIS

copyright copy 2018 ICIS wwwiciscom 112

Carbon price floor ndash prices

From 2026 the carbon price floor would start to increase prices

Modelling suggests that annual prices would be on average euro148MWh higher

than the base case 2026-2030

42

44

46

48

50

52

54

56

58

60

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Dutc

h p

ow

er

price

[euro

MW

h]

Dutch power price forecast (euroMWh)

Base case Carbon price floorSource ICIS

copyright copy 2018 ICIS wwwiciscom 113

Carbon price floor ndash Emissions

Under the base case assumptions power sector emissions would decline only

marginally through to 2029 before a big drop associated with coal phase-out in 2030

The carbon price floor would lead to a much more significant drop 2026-2030

However the emissions decline would be cancelled out by an increase elsewhere

0

5

10

15

20

25

30

35

40

45

50

Po

we

r se

cto

r e

mis

sio

ns [M

tCO

2]

Base case power sector emissions

0

5

10

15

20

25

30

35

40

45

50

Po

we

r se

cto

r e

mis

sio

ns [M

tCO

2]

Carbon price floor power sector emissions

Source ICIS

Germanylsquos coal phase-

out scenario analysis

copyright copy 2018 ICIS

Agenda

1) The bdquocoal commissionldquo at work

2) Market fundamentals

3) Our phase-out scenarios

4) Impact on German power prices

5) Hambacher Forest and its implications

copyright copy 2018 ICIS wwwiciscom 116

The bdquocoal commissionldquo

Two working groups

economic development and jobs in

the region

Energy industry and climate goals

Plenary and WGs meet once a

month

Equal voting rights

Two-thirds majority

Four commission leaders

Eight representatives of federal ministries (economy environment internal affairs labour transport finance agriculture and education)

Six representatives of federal states (North Rhine-Westphalia Brandenburg Saxony Saxony-Anhalt Lower Saxony and Saarland)

Three members of parliament without voting rights (CDU CSU and SPD)

24 experts (political groups research institutes associations NGOs and the private sector)

The secretariat with seven people is hosted within the economy ministry

copyright copy 2018 ICIS wwwiciscom 117

Aims and timeplan for decision making

Guidelines

Options for closing gap to 2020 target

Measures to ensure 2030 target

achievement

Step-wise reduction and phase-out of

coal generation incl phase-out date

Ensuring financial security for structural

changes

Potentially delaying final report

depending on ability to find consensus

Current status

1516 November next meeting discussiondetails expected regarding phase-out

So far intermediate report on structuralchanges adopted on 1 Nov details on financig instruments levels missing

Aim to have final report before end of year interim report expected by mid-December

German coalition struggle could impact theCommissions work (depending on nextCDU leader) pressure to meet timeplan

copyright copy 2018 ICIS wwwiciscom 118

Power generation in Germany

2017 generation

Lignite 134 TWh (242)

Hard coal 817 TWh (148)

Total production was 5571 TWh

Combined lignite and hard coal

~80 of emissions

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015 2016 2017

An

nu

al D

E p

ow

er

ge

ne

ratio

n [T

Wh

]

Lignite Hard coal Nuclear Gas Oil

Hydro Biomass Wind Solar Other

Source ICIS

copyright copy 2018 ICIS wwwiciscom 119

Capacity development ndash bdquomoderate scenarioldquo

Installed capacity 2018

Hard coal 227 GW

Lignite 20 GW

Lignite reserve 18 GW increasing

to 27 GW in 2019

Additional 23 GW hard coal and 30

GW lignite in grid reserve (not

available to market)

0

50

100

150

200

250

300

Insta

lled

ca

pa

city [G

W]

Lignite Hard coalNuclear Natural gasOil Hydro pump storage totalHydro reservoir Hydro run-of-riverBiomass Wind (onshore)Wind (offshore) Solar PVGeothermal

Source ICIS

copyright copy 2018 ICIS wwwiciscom 120

Scenario set-up

Four phase-out scenarios

Moderate 45 GW reduction by 2020 halved by 2030

Slow Reduction by approx frac14 towards2030

Speedy 105 GW drop towards 2020 70 drop by 2030

Lignite-only Lignite phase-out until 2030 hard coal stable

Lifetime approach for hard coal and lignite

Initial capacity reduction towards 2020 target

All other parameters unchanged

Nuclear phase-out by 2022

Nat gas capacity adjusted by additions and closures fluctuating around 24 GW

Hydro fluctuating around 96 GW

Wind onshore auction results+adjustedEEG2017 corridor

Wind offshore Adjusted EEG2017 corridor

Solar PV Auction+adjusted EEG2017 corridor

copyright copy 2018 ICIS wwwiciscom 121

Phase-out scenarios ndash capacity development

00

50

100

150

200

250

Insta

lled

lig

nite

ca

pa

city (

GW

)

Moderate lignite Slow lignite

Speedy lignite Lignite-only lignite

00

50

100

150

200

250

Insta

lled

ha

rd c

oa

l ca

pa

city (

GW

)

Moderate hard coal Slow hard coal

Speedy hard coal Lignite-only hard coal

Source ICIS

copyright copy 2018 ICIS wwwiciscom 122

Impact on German power prices

2019-2023 Prices predominantlydriven by higher carbon pricesirrespective of phase-out speed

Germany net-importer in 2023 under all scenarios 2022 to 2025 for lignite-only and speedy

After 2023 coallignite generationincentivised to ramp up

Declining carbon higherrenewables net exporter towardssecond half of 2020s

Source ICIS

30

35

40

45

50

55

60

65

Ge

rma

n p

ow

er

price

(euro

MW

h)

Moderate phase-out Slow phase-out

Speedy phase-out Lignite-only phase-out

copyright copy 2018 ICIS wwwiciscom 123

Hourly price comparison

Increasing number of

hours with high prices

in winter

Lack of gas in times

of low RES

generation

Speedy and lignite-

only scenarios more

visible spikes 30

80

130

180

230

280

330

380

430

480

530

1 6

11

16

21

26

31

36

41

46

51

56

61

66

71

76

81

86

91

96

101

106

111

116

121

126

131

136

141

146

151

156

161

166

Ge

rma

n h

ou

rly p

ow

er

price

w

ee

k 3

20

24

(euro

MW

h)

Hour of the week

Moderate phase-out Slow phase-out Speedy phase-out Lignite-only phase-out

Source ICIS

copyright copy 2018 ICIS wwwiciscom 124

Hambacher Forest ndash RWE impact

Muumlnster Higher Administrative Court ruled to halt forest clearance 5 Oct

Final decision to be reached in main proceedings likely end of 2020

Lignite mining possible until approx end 2019

But annual reduction expected from 40 Mt tobetween 25 and 30 Mt (2019-21)

RWE expects substantial short-term operational effects as of 2019

Power generation to decrease by between 9 and13 TWh

Affected plants are Neurath and Niederauszligem

Clearance work only permitted Oct to Feb Delay of at least a year

Neurath Capacity

[MW]

Commissioning

[year]

Expected

closure

A 294 1972 2021

B 294 1972 Oct-19

C 292 1973 2021

D 607 1975

E 604 1976

F 1060 2012

G 1060 2012

Niederauszligem Capacity

[MW]

Commissioning

[year]

Expected

closure

C 295 1965 2020

D 297 1968 2020

E 295 1970 Oct-18

F 299 1971 Oct-18

G 628 1974 2022

H 638 1974 2023

K 944 2003

copyright copy 2018 ICIS wwwiciscom 125

Impact on Hambach generation

With potential closures we see a

reduction of 182 TWh in 2023

This would translate to a reduction

of 138 Mt emissions in 2023

Below our assumptions for the

bdquomoderate scenarioldquo which assumes

68 GW lignite and 36 GW hard

coal to drop-out

Hambach can be seen as preview

towards coal commission result

00

50

100

150

200

250

300

350

2018 2019 2020 2021 2022 2023

Ha

mb

ach

po

we

r g

en

era

tio

n [T

Wh

]

Neurath - full generation Niederauszligem - full generation

Neurath - reduced generation Niederauszligem - reduced generation

Source ICIS

copyright copy 2018 ICIS wwwiciscom 126

Impact of Hambach Forest decision on carbon price

On average 2020 to

2030 Hambacher Forest

scenario euro05t lower

compared to base case

Reducing emissions by

a total of 35 Mt over

2020-23

00

50

100

150

200

250

300

350

400

450

EU

A p

rice

[euro

t]

Hambach impact base case

Source ICIS

The Polish energy market

and the coal dependency

copyright copy 2018 ICIS wwwiciscom 128

Production of solid fuels in the EU

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

2010 2011 2012 2013 2014 2015 2016

Eu

rosta

t so

lid f

ue

l p

rod

uctio

n [1

00

00

to

e]

Polish coal production EUs coal production without PolandSource Eurostat

copyright copy 2018 ICIS wwwiciscom 129

Future of coal in Poland ndash no clear strategy

Last adopted energy strategy ndash almost a decade old

New draft presented in 2015 under previous government

Draft update promised by December 2018 ndash COP24 in Katowice in parallel to

ldquoNational Energy and Climate Plan for 2021-2030rdquo

Bits and pieces in media

2018 July Energy Minister Krzysztof Tchoacuterzewski ldquothe share of coal in electricity

generation will systematically fall It is predicted that in 2050 it will be 50rdquo

2018 October ldquoPower from coal seen down at 50 by 2040-govt officialrdquo

copyright copy 2018 ICIS wwwiciscom 130

Industrial Emissions Directive

District heating plants (CHP) list ndash phase-out from 2023

Limited Lifetime Derogation (LLD) list ndash phase out from 2024

Unclear future of the plants in the Transitional National Plan

(TNP)

copyright copy 2018 ICIS wwwiciscom 131

Planned coal capacity additions

Max 4GW new coal capacity mid-term

Opole 900MW in late 2018 and 900MW in 2019

Byczyna (Jaworzno) unit 910MW in 2019

[2023]1000MW Ostroleka C in northeast Poland

Energy Minister Krzysztof Tchoacuterzewski about Ostroleka C lsquothe last coal-burning plant to be built in Polandrsquo

Ostrołęka C Power plant

copyright copy 2018 ICIS wwwiciscom 132

Capacity market auction to commence this week

Basic fuel Net reachable power [GW]

Existing physical generating units

Physical generating units planned

Gas 228 437

Coal and lignite 2632 402

Sum 3633 890

Sum existing and planned

4523

copyright copy 2018 ICIS wwwiciscom 133

Horizon base case Capacity and generation assumptions

0

20

40

60

80

100

120

140

160

180

200

Fo

reca

ste

d g

en

era

tio

n [

TW

h]

Hard Coal Gas Lignite

Oil Solar Wind

Hydropower Bio Demand

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

Fo

reca

ste

d c

ap

acity [

MW

]

Lignite Coal Gas Fuel oil Bio Hydro Solar Wind

copyright copy 2018 ICIS wwwiciscom 134

Zooming in ndash EUAs price forecast and fossil generation

00

50

100

150

200

250

300

350

400

450

0

20

40

60

80

100

120

140

160

180

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

EU

As p

rice

fo

reca

st [euro

to

nn

e]

Ge

ne

ratio

n fo

reca

st [T

Wh

]

Hard Coal Gas Lignite EUAs price forecast

copyright copy 2018 ICIS wwwiciscom 135

2019-2030 Polish power price outlook

25

35

45

55

65

75

85

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Po

lish

po

we

r p

rice

[euro

MW

h]

TGE day-ahead prices Horizon forecast

copyright copy 2018 ICIS wwwiciscom 136

2019-2030 Polish power price outlook

500

520

540

560

580

600

620

640

660

680

700

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Po

lish

po

we

r p

rice

[euro

MW

h]

Horizon price outlook

EUA increase

outweighed by coal

and gas prices

softening

Prices driven higher by

EUA price increase

Fuel switching seenSome coal capacity

phased-out

EUA prices fall more

RES capacity comes

onlineRegional coal

closures (especially

NL phase-out) push

regional prices higher

Conclusions

copyright copy 2018 ICIS wwwiciscom 138

Coal phase-out across the EU

Coal and lignite have the second largest installed capacity in the EU

10 EU countries decided to phase out coal several more in

discussion

Phase-out will come in waves 2021-2022 2025 and 2030

Regardless of coal phase-out plans BREF will affect one third of

Europersquos coal-fired capacity

copyright copy 2018 ICIS wwwiciscom 139

Capacity implications

Three very different policy approaches to coal

Netherlands Complete phase out by 2030 and (potentially) a carbon price floor

Germany Gradual reduction over the next ten years driven by government intervention

Poland Attempting to keep capacity online using the capacity mechanism to provide support

None of the three countries will phase out coal rapidly

In absence of policy decision Industrial Emissions DirectiveBREF will define the pathway

0

5

10

15

20

25

30

35

40

45

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Cap

acity [

GW

]

Coal-fired capacity expectations 2019-2030

Germany Poland Netherlands

Source ICIS

copyright copy 2018 ICIS wwwiciscom 140

Generation implications ndash carbon price importance

Coal generation will fall in all three

countries regardless of the coal

capacity developments because of

the bullish EUA prices

As EUA prices soften from 2024

coal-fired output will rebound

The most significant increase will be

seen in Poland as the majority of

capacity remains online 0

5

10

15

20

25

30

35

40

45

0

50

100

150

200

250

300

350

EU

As p

rice

fo

reca

st [euro

to

nn

e]

Po

we

r H

orizo

n f

ore

ca

ste

d g

en

era

tio

n [

TW

h]

Coal-fired generation 2019-2030

Germany Poland

Netherlands ICIS EUAs price forecast

Source ICIS ICIS Power Horizon

copyright copy 2018 ICIS wwwiciscom 141

Price implications

Power prices in all three markets will follow a similar pattern

2019-2023 EUA increase pushes prices higher

2024-2030 Softening of EUA prices and increased RES output leads to lower prices

Dutch carbon price floor and complete phase-out to boost prices comparatively 2026-2030

A speedier German phase-out would push prices higher compared to the base case

45

47

49

51

53

55

57

59

61

63

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Po

we

r p

rice

[euro

MW

h]

Wholesale price forecasts 2019-2030

Germany Poland Netherlands

Source ICIS

Stay focused on the power market developments that are important to your business with the new online tool from ICIS

Understand the impact of energy policy changes

Anticipate market developments across Europe

Foresee risks and spot profitable opportunities Fast

ICIS Power Perspective amp Horizon

Speak to us to find out more

Tel +44 20 7911 1919 | Email powerperspectiveiciscom | wwwiciscompowerperspective

Reliable provider of global carbon market analytics and forecasts

Learn more

Stay ahead of the carbon market trends and developments

Get the latest analysis and forecasts for global carbon trading

Make profitable investments within seconds

Strengthen you trading position

wwwiciscom

ICIS Power amp Carbon Seminar

Second Day

14-15 November 2018Berlin Germany

1230-1300 Power Purchase AgreementsVivianna Ciancibello EEX

0930-0945 WelcomePhilipp Ruf ICIS

0945-1115

Brexit and its impact on the UK electricity

market and the EU ETSHenry Evans amp Matt Jones amp Marcus Ferdinand ICIS

Mark Copley BEIS

Coffee Break

1145-1230 Renewable energy trends across EuropeMatteo Mazzoni amp Vija Pakalkaite ICIS

Goodbye and wrap-up

Brexit and its impact on the UK electricity market and the EU ETS

Henry EvansSenior Market Reporter

Matt JonesSenior Analyst ndash EU Carbon amp Power Analytics

Marcus FerdinandHead of EU Carbon amp Power Analytics

Mark CopleyDeputy Director ndash EU Exit Energy amp Climate Programme at BEIS

The future of the UK

electricity market post-

Brexit

copyright copy 2018 ICIS wwwiciscom 148

Deal or no-deal What is the timeline

November

bull Negotiators for UK and EU reach agreement in principle on Withdrawal Agreement

bull 25 November EU emergency Council meeting on Agreement

December

bull UK Parliament likely to vote on Agreement in early December

bull 13-14 Dec ndash last EU Council of 2018

2019

bull UK and EU parliamentary approval required for any deal

bull New UK legislation will need to be passed before 29 March

bull Potential for extension of date if no deal agreed

copyright copy 2018 ICIS wwwiciscom 149

EU vs UK ndash where do they both stand on energy

EU Commission publishes notice on

27 April detailing the UKrsquos position

in the EUrsquos internal energy market in

the event of ldquono dealrdquo

UK government published its Brexit

white paper on 12 July following the

fabled Chequers meeting ndash pages

44-45 are the important part

copyright copy 2018 ICIS wwwiciscom 150

Will the interconnectors stop flowing power

UK currently has three underwater cables connected to the EU ndash 2GW IFA with

France 1GW BritNed with Netherlands and 500MW East-West Interconnector

with Ireland

UK and EU papers make no mention of flows between the UK and EU halting

on 29 March 2019

National Grid 28 June 2018 ndash ldquoOur internal analysis backed up by two

separate external legal views has stated that there is no legal right for the

interconnectors to be simply ldquoswitched offrdquo post Brexitrdquo

copyright copy 2018 ICIS wwwiciscom 151

What will the commercial arrangements be

UK will lose access to the single allocation platform for forward interconnection capacity European balancing platforms and the single day-ahead and intraday coupling

UKrsquos NEMOs ndash ie EPEX Spot and Nord Pool ndash will become third country operators and will no longer be able to carry out market coupling services between UK and EU

Option 1 - open to remaining in the EUrsquos internal energy market (IEM) This includes remaining part of the EUrsquos Emissions Trading System One caveat ldquoThe UK does not believe that participation in the IEM should require a common rulebook on wider environmental and climate change rulesrdquo

Option 2 ndash Leave the IEM and explore how interconnector trade continues without automatic capacity allocation National Grid has contingencies in place

What has the EU said What has the UK said

copyright copy 2018 ICIS wwwiciscom 152

Regulations and REMIT

UK market participants will have to

register with the regulatory authority

of the Member State in which they

are active

The registration form has to be

submitted prior to entering into a

transaction which is required to be

reported

ldquoThe UK is putting in place

arrangements so that when trading

after exit businesses will have

certainty that they will not face

substantially different requirements

compared to their current

obligations under the Regulation on

Wholesale Energy Market Integrity

and Transparency (REMIT)rdquo

What has the EU said What has the UK said

copyright copy 2018 ICIS wwwiciscom 153

If the UK leaves the IEM what happens

Positive for existing interconnectors Increased price divergence between UK

and continental markets possible without market coupling

Negative for interconnectors in development Investor confidence weakens

New projects already delayed

Will liquidity in wholesale market be affected

Mark CopleyDeputy Director ndash EU Exit Energy amp Climate Programme at BEIS