I. ECONOMIC BACKDROP AND BANKING ENVIRONMENT Director Report.pdf · I. ECONOMIC BACKDROP AND...

48

32 Directors’ Report GLOBAL ECONOMIC SCENARIO Global economic activity gathered momentum in the second half of last year and it continues to grow in 2018. World GDP growth recovered to an estimated 3.8% in 2017 compared to 3.2% in the previous year. Both the developed and the developing countries performed well, growing at 2.3% and 4.8% respectively. The US economy grew more than expected against the backdrop of abatement of past exchange rate appreciation impact and oil price movement coupled with support from good consumption growth and rebound in investment. Euro area also surprised positively witnessing its fastest pace of growth in a decade and surpassing the US growth in 2017. The uncertainty surrounding Brexit weighed on the UK economy, however it recovered in the final months of the year. In Japan, improved global demand for technological products stimulated investment in high- end sectors including auto, machinery including robots and semi-conductors. Among the emerging and developing world, economic contraction ended in Russia and Brazil, thereby adding to growth. However, despite improvement in oil dynamics Saudi Arabia witnessed negative growth owing to low oil output and sluggish performance of non-oil sector. Even Mexico suffered against the backdrop of uncertainty surrounding NAFTA and presidential elections. Meanwhile, China witnessed its first annual acceleration since 2010 with export growing at their quickest pace in four years. India’s GDP growth is expected to have moderated to 6.6% in FY2018. However, this is likely to be transitory. Meanwhile, Government reforms continue to provide support to aggregate demand. Looking ahead, as per IMF projections the world economy is poised to grow at 3.9% in 2018 as well as 2019. However, looming threat of trade wars against the background of increase in tariffs by the US and retaliation by China is one of the risks to global growth. World trade is recovering smartly in 2017, registering a growth of around 10% and 11% for exports and imports respectively, but rising protectionism and trade war can threaten trade and economic growth. In addition, uncertainty surrounding elections in many European countries including Russia, Italy, Hungary among others and escalation of sanction issue in Iran are other key risks that could dampen the growth prospects. Another major development having an impact on global economy is the oil price which has recovered to over US$ 80 per barrel recently. Looking ahead, geo-political tensions in middle-east with probable sanctions on Russia may affect oil price dynamics. INDIA’S ECONOMIC SCENARIO India’s economic growth is expected to gather momentum in FY2019, benefitting from a conducive domestic and global environment. The factors that will help in achieving 7.4% GDP growth in FY2019 compared to 6.7% in FY2018 are: (i) the troubles relating to implementation of the GST have been sorted out, (ii) credit off-take has improved and is becoming increasingly broad-based, (iii) large resource mobilisation from the primary market strengthening investment activity, (iv) the process of recapitalisation of PSBs and resolution of distressed assets under the Insolvency and Bankruptcy Code may improve the business and investment environment, (v) global trade growth has accelerated, which should encourage exports and reduce the drag from net exports, and (vi) the thrust on rural and infrastructure sectors in the Union Budget 2018-19 could rejuvenate rural demand and also encourage private investment. Inflation, both CPI and WPI remain under control for entire FY2018. Average CPI was 3.6% in FY2018 compared to 4.5% in FY2017, while the corresponding figures for WPI are 2.9% and 1.8%, respectively. Assuming a normal monsoon and no major exogenous/policy shocks, CPI is expected to remain in the range of 4.0- 4.5% for FY2019 and even go below 3.5% for some months in Q3 FY2019. Major risks to the inflation outlook are crude oil and other commodity prices and fiscal slippage at both the central and state levels. For the third consecutive year, Indian Meteorological Department (IMD) has forecasted that monsoon would be “Normal” or around 97% of Long Period Average (LPA) with an error of ± 5% and I. ECONOMIC BACKDROP AND BANKING ENVIRONMENT with a fair distribution of rainfall across major parts of country in 2018. As a result of normal rainfall during monsoon 2017 and various policy initiatives taken by the Government, the country has witnessed record foodgrain production at 279.50 million tonnes for FY2018, 1.6% higher than the previous record achieved in FY2017 (275.1 million tonnes). The production of rice, pulses and coarse cereals touched new highs during the year, but wheat production declined. Gross value added in the industrial sector at basic prices decelerated to 6.8% in FY2018 from 9.8% in FY2017. The slowdown in FY2018 was due to a sharp deceleration in mining and quarrying. In the mining sector, contraction was on account of slowdown in its key constituents such as coal and natural gas production, and decline in crude oil output. The growth of manufacturing, on the other hand, improved with the waning of the transient effects of GST. On the external front, the current account deficit (CAD) increased to 2% of GDP (US$ 13.5 billion) in Q3 FY2018 from 1.4% of GDP (US$ 8.0 billion) a year ago. For FY2018, we believe CAD would be around 1.8% of GDP compared to 0.7% of GDP in FY2017. This slight increase in CAD during FY2018 is due to US$ 156.8 billion trade balance, which is at a 5-year high. BANKING ENVIRONMENT FY2018 remained an eventful year for the banking fraternity. Asset quality, resolution of stressed assets and muted credit growth in H1 continued as major challenges for most banks during the current year. Higher NPAs impacted interest income adversely and led to elevated provisions, thus putting pressure on the profitability of banks. Further, some Public Sector Banks (PSBs) have been put under the Prompt Corrective Action (PCA) framework of RBI, which puts restrictions on key areas viz. dividend payment, branch expansion, etc. After remaining depressed for nearly two years, the bank credit built upon the uptick that started around June, 2017 and expanded in double digits from December, 2017. The resurgence in credit growth was observed across bank groups, though the pace of growth continues to vary among bank groups. The YoY growth rate of bank Directors’ Report

Transcript of I. ECONOMIC BACKDROP AND BANKING ENVIRONMENT Director Report.pdf · I. ECONOMIC BACKDROP AND...

32 Directors’ Report

GLOBAL ECONOMIC SCENARIOGlobal economic activity gathered momentum in the second half of last year and it continues to grow in 2018. World GDP growth recovered to an estimated 3.8% in 2017 compared to 3.2% in the previous year. Both the developed and the developing countries performed well, growing at 2.3% and 4.8% respectively. The US economy grew more than expected against the backdrop of abatement of past exchange rate appreciation impact and oil price movement coupled with support from good consumption growth and rebound in investment. Euro area also surprised positively witnessing its fastest pace of growth in a decade and surpassing the US growth in 2017. The uncertainty surrounding Brexit weighed on the UK economy, however it recovered in the final months of the year. In Japan, improved global demand for technological products stimulated investment in high-end sectors including auto, machinery including robots and semi-conductors.

Among the emerging and developing world, economic contraction ended in Russia and Brazil, thereby adding to growth. However, despite improvement in oil dynamics Saudi Arabia witnessed negative growth owing to low oil output and sluggish performance of non-oil sector. Even Mexico suffered against the backdrop of uncertainty surrounding NAFTA and presidential elections. Meanwhile, China witnessed its first annual acceleration since 2010 with export growing at their quickest pace in four years.

India’s GDP growth is expected to have moderated to 6.6% in FY2018. However, this is likely to be transitory. Meanwhile, Government reforms continue to provide support to aggregate demand.

Looking ahead, as per IMF projections the world economy is poised to grow at 3.9% in 2018 as well as 2019. However, looming threat of trade wars against the background of increase in tariffs by the US and retaliation by China is one of the risks to global growth. World trade is recovering smartly in 2017, registering a growth of around 10% and 11% for exports and imports respectively, but rising protectionism and trade war can threaten trade and economic growth. In addition, uncertainty surrounding elections in many

European countries including Russia, Italy, Hungary among others and escalation of sanction issue in Iran are other key risks that could dampen the growth prospects.

Another major development having an impact on global economy is the oil price which has recovered to over US$ 80 per barrel recently. Looking ahead, geo-political tensions in middle-east with probable sanctions on Russia may affect oil price dynamics.

INDIA’S ECONOMIC SCENARIOIndia’s economic growth is expected to gather momentum in FY2019, benefitting from a conducive domestic and global environment. The factors that will help in achieving 7.4% GDP growth in FY2019 compared to 6.7% in FY2018 are: (i) the troubles relating to implementation of the GST have been sorted out, (ii) credit off-take has improved and is becoming increasingly broad-based, (iii) large resource mobilisation from the primary market strengthening investment activity, (iv) the process of recapitalisation of PSBs and resolution of distressed assets under the Insolvency and Bankruptcy Code may improve the business and investment environment, (v) global trade growth has accelerated, which should encourage exports and reduce the drag from net exports, and (vi) the thrust on rural and infrastructure sectors in the Union Budget 2018-19 could rejuvenate rural demand and also encourage private investment.

Inflation, both CPI and WPI remain under control for entire FY2018. Average CPI was 3.6% in FY2018 compared to 4.5% in FY2017, while the corresponding figures for WPI are 2.9% and 1.8%, respectively. Assuming a normal monsoon and no major exogenous/policy shocks, CPI is expected to remain in the range of 4.0-4.5% for FY2019 and even go below 3.5% for some months in Q3 FY2019. Major risks to the inflation outlook are crude oil and other commodity prices and fiscal slippage at both the central and state levels.

For the third consecutive year, Indian Meteorological Department (IMD) has forecasted that monsoon would be “Normal” or around 97% of Long Period Average (LPA) with an error of ± 5% and

I. ECONOMIC BACKDROP AND BANKING ENVIRONMENT

with a fair distribution of rainfall across major parts of country in 2018.

As a result of normal rainfall during monsoon 2017 and various policy initiatives taken by the Government, the country has witnessed record foodgrain production at 279.50 million tonnes for FY2018, 1.6% higher than the previous record achieved in FY2017 (275.1 million tonnes). The production of rice, pulses and coarse cereals touched new highs during the year, but wheat production declined.

Gross value added in the industrial sector at basic prices decelerated to 6.8% in FY2018 from 9.8% in FY2017. The slowdown in FY2018 was due to a sharp deceleration in mining and quarrying. In the mining sector, contraction was on account of slowdown in its key constituents such as coal and natural gas production, and decline in crude oil output. The growth of manufacturing, on the other hand, improved with the waning of the transient effects of GST.

On the external front, the current account deficit (CAD) increased to 2% of GDP (US$ 13.5 billion) in Q3 FY2018 from 1.4% of GDP (US$ 8.0 billion) a year ago. For FY2018, we believe CAD would be around 1.8% of GDP compared to 0.7% of GDP in FY2017. This slight increase in CAD during FY2018 is due to US$ 156.8 billion trade balance, which is at a 5-year high.

BANKING ENVIRONMENTFY2018 remained an eventful year for the banking fraternity. Asset quality, resolution of stressed assets and muted credit growth in H1 continued as major challenges for most banks during the current year. Higher NPAs impacted interest income adversely and led to elevated provisions, thus putting pressure on the profitability of banks. Further, some Public Sector Banks (PSBs) have been put under the Prompt Corrective Action (PCA) framework of RBI, which puts restrictions on key areas viz. dividend payment, branch expansion, etc.

After remaining depressed for nearly two years, the bank credit built upon the uptick that started around June, 2017 and expanded in double digits from December, 2017. The resurgence in credit growth was observed across bank groups, though the pace of growth continues to vary among bank groups. The YoY growth rate of bank

Directors’ Report

33

credit for ASCBs was 10% as on 30th March, 2018. Credit extended by private sector banks is higher than PSBs, while credit extended by foreign banks has returned to positive territory after a long contraction. Credit to sectors is becoming broad-based, with off-take by industry turning positive after a protracted period of contraction. Due to the continued stress in other sectors, most of the banks made efforts to lend to retail sector, which registered reasonably good growth, with most banks expanding their retail loan book. However, with resolutions through National Companies Law Tribunal (NCLT) expected to gather momentum and global growth and private investment in India beginning to pick up, green shoots of credit demand have started appearing. On the other hand, the aggregate deposits growth (YoY) continued to decline and is at 54-year low of 6.2%, due to the base effect and currency withdrawal by public.

During the last quarter of FY2018, the bond yields continued to firm up which hit severely the banks’ balance sheet, due to the mark-to-market losses incurred by the banks in their investments. In the post-demonetisation period, banks have invested a huge amount of money in Government bonds due to tepid credit growth. In Q3 FY2018 quarterly results, most of the banks have reported a loss due to their higher provisioning against the mark-to-market losses in investments in Government bonds. To ease the pressure, RBI recently has advised the banks to do the mark-to-market loss provisioning in the next four quarters.

On a positive note, in the year, the Government took a significant step to capitalise PSBs in a front-loaded manner, with a view to support credit growth and job creation. This entails the mobilisation of capital to the tune of about ` 2.11 lakh crore over two years, through budgetary provisions of ` 18,139 crore, recapitalisation bonds to the tune of ` 1.35 lakh crore, and the balance through raising of capital by banks from the market while diluting non-Government equity (estimated potential ` 58,000 crore). The other possibility is to raise funds through rights issue to maintain parity of holdings. Going by the MoF (Ministry of Finance) estimates, the ` 1.35 lakh crore package seems largely adequate. In FY2018, Government has notified ` 80,000 crore recapitalisation bonds to capitalise 20

PSBs for meeting their regulatory capital requirement and growth needs.

State Bank of India has merged its five associate banks and Bharatiya Mahila Bank Ltd. with itself from 1st April, 2017. This is the first such large scale consolidation in the Indian Banking industry. With this merger, your Bank is ranked at the 54 position among the top 1,000 global banks, as per the global ranking by “The Banker” in July 2017. This merger helped your Bank to reduce 1,805 branches and rationalised 244 administrative offices, which saves around ` 1,099 crore per annum. We believe that the long-term benefits of the merger will significantly outweigh the near term challenges and the efficiencies generated through the merger will help the Bank to sustain the mission of being an enduring value creator.

Meanwhile, under the Pradhan Mantri Jan Dhan Yojna (PMJDY), banks have opened 31.4 crore accounts with ` 79,012 crore deposits (around 6% of the total demand deposits of the ASCBs) till 4th April, 2018 deposited in their accounts. Out of the 31.4 crore accounts, PSBs have opened 25.4 crore accounts, RRBs have opened 5.1 crore accounts, whereas private sector banks (PrSBs) have opened only 0.9 crore accounts. This indicates that PSBs have accepted the responsibility and have fulfilled their promises in a record time. On a positive note, zero balance accounts under PMJDY have been continuously declining from 76.8% in September, 2014 to around 20% now. PMJDY has also helped the implementation of the Mudra Yojana with `5.28 lakh crore distributed to 11.96 crore beneficiaries in the last 3-years. In an in-house study within your Bank, we have found that there is a traction across Jan Dhan and Mudra accounts.

In regards to competition, while the new breed of Payment and Small Finance Banks, which have started functioning, are still in the process of fine tuning their business models, the Fintech companies with disruptive technologies and having capabilities to address specific pain-points of financial customers, such as remittance, credit and savings, have emerged as a challenge to the banking system.

OUTLOOKThe coming years will be very challenging for the banking system as a whole. The operating environment has become increasingly complex. Although, resolution of stressed assets has progressed satisfactorily, the final outcome will take some more time to reflect in the P&L. This delay is mainly because new laws take some time to mature in practice. However, the structural transformation of banks must move beyond the NPA resolution and address other pressing issues, such as frauds, customer retention and servicing, human resource, cyber security and governance.

The policy initiatives over the last four years have gathered momentum with far reaching structural transformation in all sectors. GST is moving to the next phase with the introduction of e-ways module. Infrastructure growth has notably picked in roads, civil aviation and railways. Digitalisation will gather pace as evident from the Report of the Taskforce on Artificial Intelligence. It is unlikely that banks will escape these transformations. Digitalisation of banking process will continue during the next year creating new improved service experience. With capital infusion, it is now up to the banks to grab the opportunity and deploy technology in addressing some of the pressing issues mentioned above.

The external environment nevertheless has become uncertain, despite a positive outlook on growth. Trade wars, which are a sign of renegotiation of the old order, have become more acute. The situation will continue in the same direction in 2018. Thus, across the world, banks have revisited their foreign business strategy in line with growing risks. Such cautions prevails among Indian banks as well. The Government of India has advised banks to rationalise their foreign branches. However, this does not constitute a blanket withdrawal but a more realistic strategy in line with changing trade patterns of the country. This rationalisation in foreign business will therefore continue.

The coming year will be the last year after which general elections are due. However, we do not expect that policy direction will markedly turn populist. The fiscal and monetary conditions will continue to remain stable even if there are momentary aberrations. But the challenge will lie in taking a decision amid growing uncertainty. Overall the NPA resolution is in sight and the time is opportune for tough and strategic decision making.

34 Directors’ Report

II. FINANCIAL PERFORMANCE

ASSETS AND LIABILITIESThe total assets of your Bank have increased by 27.67% from ` 27,05,966.30 crore at the end of March 2017 to ̀ 34,54,752.00 crore as at the end of March 2018. During the period, the loan portfolio increased by 23.16% from ` 15,71,078.38 crore to ̀ 19,34,880.19 crore. Investments increased by 38.51% from ` 7,65,989.63 crore to ` 10,60,986.71 crore as at the end of March 2018. A major portion of the investment was in the domestic market in government securities.

Your Bank’s aggregate liabilities (excluding capital and reserves) rose by 28.52% from ` 25,17,680.24 crore as on 31st March, 2017 to ` 32,35,623.44 crore as on 31st March 2018. The deposits rose by 32.36% and stood at ` 27,06,343.28 crore as on 31st March 2018 against ` 20,44,751.39 crore as on 31st March 2017. The borrowings also increased by 13.99% from ` 3,17,693.66 crore, at the end of March 2017 to ` 3,62,142.07 crore as at the end of March 2018.

NET INTEREST INCOMENet interest income increased by 21.01% from ` 61,859.74 crore in FY2017 to ` 74,853.71 crore in FY2018. Total interest income has increased from ` 1,75,518.24 crore in FY2017 to ` 2,20,499.31 crore in FY2018 registering a growth of 25.63%.

PROVISIONS & CONTINGENCIESMajor provisions made in FY2018 were as under:` 70,680.24 crore for non-performing assets (as against ̀ 32,246.69 crore in FY2017), write back of ` 3,603.66 crore towards Standard Assets (as against provision of ` 2,499.64 crore in FY2017), ` 8,087.57 crore towards Investments Depreciation (as against ` 298.39 crore in FY2017).

RESERVE & SURPLUSSince the Bank has incurred loss in FY2018, no amount (as against ` 3,145.23 crore in FY2017) has been transferred to Statutory Reserves. An amount of ` 3,288.88 crore (as against ` 1,493.39 crore in FY2017) has been transferred to Capital Reserves. An amount of ` 1,165.14 crore (as against ` 143.69 crore in FY2017) has been transferred from Investment reserve to Revenue and other Reserves and ` 192.32 crore from Revaluation Reserve to General Reserve.

REVALUATION OF FIXED ASSETSYour bank has reversed the effect of revaluation amounting to ` 11,210.94 crore made in earlier periods in the value of certain leasehold properties, which has resulted in write back of depreciation charged in previous year amounting to ` 193.24 crore. Consequential effect on capital adequacy ratio arising from the above has been made in the results for the year ended March, 2018.

PROGRESS ON IMPLEMENTATION OF IND ASRBI, in its press release dated 5th April, 2018, has deferred implementation of Ind AS by one year till 1st April, 2019. Earlier, RBI had issued a road map for implementation of Ind AS for Banks in India for accounting periods beginning from 1st April, 2018.

A Steering Committee headed by Managing Director (Risk, IT & Subsi-diaries) is monitoring the progress in implementation of Ind AS in the Bank to ensure a smooth transition to Ind AS as per the time schedule.

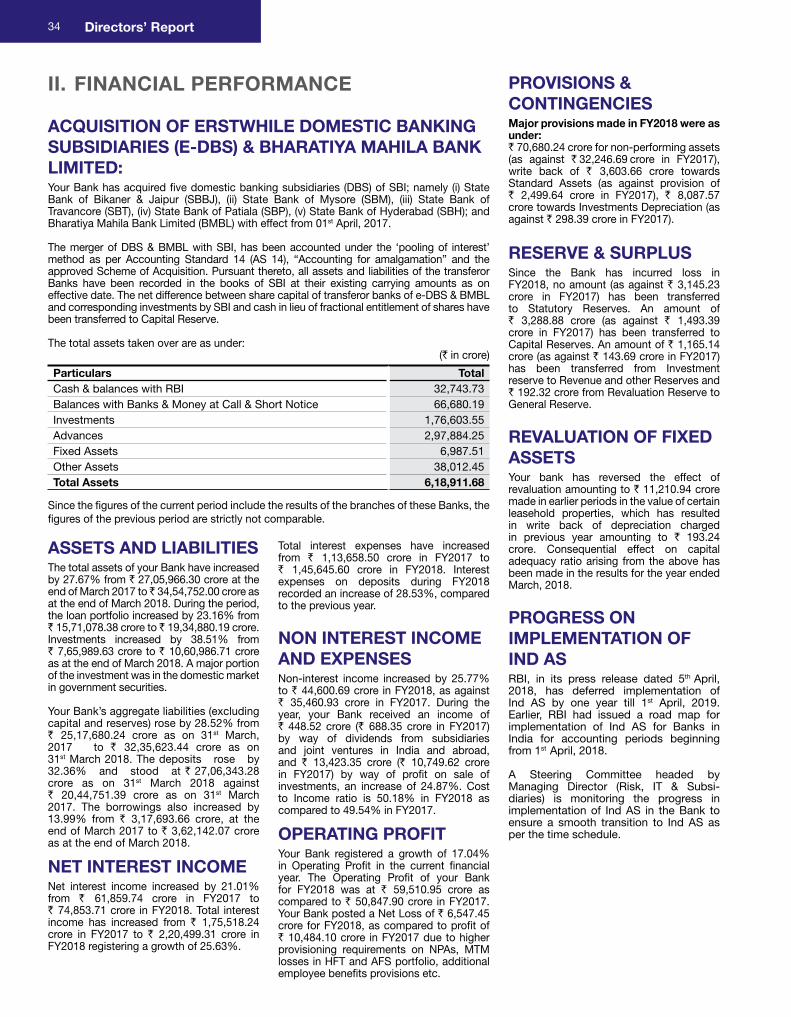

ACQUISITION OF ERSTWHILE DOMESTIC BANKING SUBSIDIARIES (E-DBS) & BHARATIYA MAHILA BANK LIMITED:Your Bank has acquired five domestic banking subsidiaries (DBS) of SBI; namely (i) State Bank of Bikaner & Jaipur (SBBJ), (ii) State Bank of Mysore (SBM), (iii) State Bank of Travancore (SBT), (iv) State Bank of Patiala (SBP), (v) State Bank of Hyderabad (SBH); and Bharatiya Mahila Bank Limited (BMBL) with effect from 01st April, 2017.

The merger of DBS & BMBL with SBI, has been accounted under the ‘pooling of interest’ method as per Accounting Standard 14 (AS 14), “Accounting for amalgamation” and the approved Scheme of Acquisition. Pursuant thereto, all assets and liabilities of the transferor Banks have been recorded in the books of SBI at their existing carrying amounts as on effective date. The net difference between share capital of transferor banks of e-DBS & BMBL and corresponding investments by SBI and cash in lieu of fractional entitlement of shares have been transferred to Capital Reserve.

The total assets taken over are as under:(` in crore)

Particulars Total Cash & balances with RBI 32,743.73 Balances with Banks & Money at Call & Short Notice 66,680.19 Investments 1,76,603.55 Advances 2,97,884.25 Fixed Assets 6,987.51 Other Assets 38,012.45 Total Assets 6,18,911.68

Since the figures of the current period include the results of the branches of these Banks, the figures of the previous period are strictly not comparable.

Total interest expenses have increased from ` 1,13,658.50 crore in FY2017 to ` 1,45,645.60 crore in FY2018. Interest expenses on deposits during FY2018 recorded an increase of 28.53%, compared to the previous year.

NON INTEREST INCOME AND EXPENSESNon-interest income increased by 25.77% to ` 44,600.69 crore in FY2018, as against ` 35,460.93 crore in FY2017. During the year, your Bank received an income of ` 448.52 crore (` 688.35 crore in FY2017) by way of dividends from subsidiaries and joint ventures in India and abroad, and ` 13,423.35 crore (` 10,749.62 crore in FY2017) by way of profit on sale of investments, an increase of 24.87%. Cost to Income ratio is 50.18% in FY2018 as compared to 49.54% in FY2017.

OPERATING PROFITYour Bank registered a growth of 17.04% in Operating Profit in the current financial year. The Operating Profit of your Bank for FY2018 was at ` 59,510.95 crore as compared to ` 50,847.90 crore in FY2017. Your Bank posted a Net Loss of ` 6,547.45 crore for FY2018, as compared to profit of ` 10,484.10 crore in FY2017 due to higher provisioning requirements on NPAs, MTM losses in HFT and AFS portfolio, additional employee benefits provisions etc.

35

III. CORE OPERATIONS

1. RETAIL & DIGITAL BANKING GROUP

The Retail & Digital Banking Group is the largest business vertical of your Bank, anchoring 96% of total Domestic Deposits, and 57.53% of total Domestic Advances, as of 31st March, 2018. The Group comprises seven strategic business units and is the largest in terms of its branch network and human resources.

Retail Banking is playing an increasing role in customer acquisition and CASA growth. Your Bank continues to see a strong momentum in the addition of retail deposit customers and consequently, a steady growth in the retail deposits base. Simultaneously, to meet the aspirations of this growing customer base, retail assets are being strategically positioned with a view to occupying a much larger proportion of total advances. Within the retail portfolio, Home and Auto loans are the major contributors. Your Bank is also the largest dispenser of education loans, which demonstrates its unflinching commitment to serve the society at large.

A steady stream of technology driven innovations necessitated by changing customer preferences are transforming the retail banking landscape. Your Bank has a multi-channel delivery model, which allows it to offer its customers a choice to carry out transactions through any channel, at any time and at any place. In FY2018, your Bank increased its offerings across various channels – digital, mobile, internet, social media, in addition to branches, ATMs and Customer Service Points.

With collective efforts across functions, especially operational level, your Bank has streamlined a number of key issues surrounding the Bank. Amidst heightened concern on future regulatory requirements, cost of funds, fast changing consumer preferences, intensifying competition and profitability pressure, your Bank has made a road map towards profitability-oriented performance management. As a way forward to achieve this, your Bank has introduced Return on Risk Weighted Assets (RoRWA) budgeting including bench marking efficiency parameters.

With a view to increase the profitability and Return on Assets (ROA), curtailment of overheads has always been the prime focus of your Bank. With this objective

of containing costs, especially in the post-merger scenario, your Bank has conducted various audits like Space Audit, Energy Audit, Telephone Audit and Internet Audit, to name a few, in erstwhile Associate Bank (e-ABs’) branches.

Your Bank accords highest priority towards creating an environment of increased risk awareness at all levels. It also aims at constantly safeguarding the appropriate security measures, including cyber security measures, to ensure avoidance or mitigation of various risks. Your Bank is equipped with a Disaster Recovery/Business Continuity Plan (BCP) across all branches and offices to render uninterrupted services in the event of any possible business disruption.

A. PERSONAL BANKING The significant transformation of the banking industry in India is clearly evident from the changes that have occurred in the financial market. Disruptive innovations in the technological and digital banking products has opened up new vistas for banks to augment revenues and enhance customer delight. This has entailed greater competition and consequently greater risks. Cross-border flows and entry of new products have significantly impacted the domestic banking sector. This is paving the way for innovative product mix, and also necessitates rapid changes in the process and operations to remain competitive. These developments have facilitated greater choice for consumers, and subsequently requires adoption of a strong and transparent, prudential, regulatory, supervisory, technological and institutional framework in the financial sector at par with international best practices.

Your Bank offers a wide range of services in the Personal Banking Segment as mentioned below:

1. Home LoansYour Bank has the largest Home Loan portfolio in the country, with a market share of 32.13% as on 31st March 2018, amongst All Scheduled Commercial Banks (ASCBs). Home Loan portfolio constituted 18% of the Whole Bank Advances as on 31st March 2018.

Total Home Loan and Home Loan Related portfolio as on 31st March 2018 stood at ` 3,41,081 crore.

During the current financial year, there were internal challenges with the merger of five Associate Banks and Bharatiya Mahila Bank Ltd. with your Bank. Further, slowdown in project launches, due to the teething problems in implementation of RERA, impacted business during the first half of the year. Your Bank undertook initiatives to streamline the operations post merger, and the growth revived back in second half of the year despite slow down in the Home Loan market. Various initiatives were taken up during the year to provide superior experience to a home buyer and maintain its position of the most preferred Home Loan provider. Some of the key initiatives undertaken during the year are as under:

To meet the customer expectations of better and faster delivery, your Bank undertook:

z Home Loan Customer Connect Programme, through which the Bank reached out to over 1 lakh Home Loan Customers across the country, to thank them for their continued patronage and to offer after-sales services.

z Assured Turn-Around-Time Drive, resulted in reduction of average turn around time (TAT) of Home Loan Sanction to 9 days for the month of March 2018. This TAT is comparable to the best in the industry.

z Increased number of feet-on-street to provide door step service at more than 25 centres.

The rise in internet penetration and faster adoption of internet has necessitated easy access to information at the touch of customers’ fingertips. To fulfil these needs, your Bank launched two websites this financial year:

z SBI Home Loans website (https://homeloans.sbi): It is an exclusive website for Home Loans which apprise customers with instant information regarding Bank’s home loan products. It also provides customers with pre and post sales services, including Application for Disbursement, Statement of Accounts, Next Instalment Due Date and Interest Rate History, among others.

36 Directors’ Report

z SBI Realty Website (www.sbirealty.in): This website showcases your Bank’s approved projects across India to prospective home buyers. It helps to bring together developers and buyers on a single platform, giving buyers the access to the deals on SBI approved projects.

Affordable Housing is a thrust area of the Government to bridge the huge demand-supply gap of houses in India. Your Bank has been working in tandem to fulfil the mission of “Housing for All” by 2022, by facilitating affordable housing to home buyers. Few initiatives in this regard are as follows:

z The launch of “SBI Grih Nirman Affordable Housing Project Finance Scheme” with attractive features to tap the emerging potential for financing affordable Housing Projects and is especially geared towards first-time home buyers.

z Partnered with CREDAI in an event where 375 affordable housing projects were launched by builders across India.

z Sanctioned 37,007 home loans under PMAY scheme, aggregating to ` 7,997 crore during the financial year.

2. Auto Loans

Auto Advances Level (` in crore)

FY 2016-17 FY 2017-18

57,609

66,362

Your Bank is helping upgrade the living standards of its customers by providing auto loans and making owning a car affordable. These auto loan products of your Bank are available in many variants to suit the requirements of various customer segments - salaried, businessmen, self-employed, professionals, senior citizens, NRIs, agriculturists and existing borrowers, among others. Multi-channel sourcing of proposals and faster TAT has made the auto loan products highly popular. This has helped your Bank to increase its penetration in financing cars sold by various manufacturers such as Maruti, Hyundai, TATA Motors, to name a few. The market share of your Bank in Car Loans has also gone up from 33.77% as on 31st March, 2017 to 34.97% as on 31st March, 2018.

3. Education LoansEducation is the key growth driver for any economy as it helps create skilled and productive human resources who contribute to the development of the nation. Your Bank takes pride in being the largest Education Loan provider in the country. It has helped 56,042 meritorious students during the financial year to realise their dreams by providing financial assistance to the tune of ` 4,949 crore (out of which 35% of the loans have been extended to girl students). In order to broaden the scope of Education Loans to book quality business and enhance customer satisfaction as under, your Bank has taken various steps:

z Provided Education Loans to students of 147 top-rated, premier and reputed institutions identified by the Bank at relaxed norms and concessional interest rates.

37

z Door-step services are extended for sourcing high-value education loan applications at select centres.

z All courses and institutes approved by the Director General of Civil Aviation (DGCA)/ Director General of Shipping (DGS) in the list of eligible courses covered under Education Loans, have been included for financing by the Bank.

z Bank’s Loan Origination System has been integrated with Vidya Lakshmi Portal (VLP) of Government of India to ensure better tracking of the loan applications and faster sanctioning of loans.

4. Personal LoansPersonal Loan is one of the most popular products of your Bank and is amongst the leaders in this segment. Your Bank has been aggressively catering to the needs of salaried class (both government and private), pensioners and other customers. During FY2018, your Bank has provided Personal Loans to 14 lakh customers amounting to ` 50,971 crore. The Bank’s delinquency under this segment is one of the lowest in the industry. This has been possible because of your Bank’s utmost caution in selection of borrowers and careful due diligence.

Your Bank has adopted various technological innovations mentioned as under, to serve the digital-savvy customers:

z Top-up Insta Credit loan to existing Xpress credit Personal Loan borrowers through internet banking in an end to end digitised mode.

z Pre-approved instant Personal Loans to the existing SB account holders of the Bank through its YONO app.

z Overdraft (OD) facility for select customers for purchases done through online shopping websites like Flipkart.

z Tatkal e-Personal Loans to cater to the needs of unserved and under-served non-salaried customers, based on selected parameters.

z Personal loan against security of Sovereign Gold Bonds of Government of India on a pilot basis.

z Personal loans to non-customers by evaluating credit history of the applicants and Credit Information Reports (CIR) of various CICs.

Shri Rajnish Kumar, Chairman, Inaugurating Global NRI Centre At Ernakulam.

5. NRI BusinessAs on 31st March, 2018 your Bank has a 33.34 lakh strong NRI customer base, who are being catered to by 150 NRI intensive branches and 95 dedicated branches across India. With an aim of providing all the NRI related service at a single point, your Bank has set up a centralised back office. This major process innovation undertaken in NRI services will handle the entire gamut of non-financial services including customer support and query management. Your Bank has introduced a mobile app-based remittance facility to the Indian diaspora residing in USA to remit the funds to India, with a cap of US$ 10,000. SBI Intelligent Assistant (SIA) also known as Smart Chat Assistant evolved from the cutting-edge technology, which efficiently answers queries, is also extended to NRIs.

6. Corporate and Institutional Tie-ups for Salary Package

A dedicated Sales Architecture has been created in your Bank to facilitate opening of salary accounts of Corporate Employee, Armed forces and other Central/ State Government Employees. A dedicated marketing force named Key Accounts Manager (KAM) provides personalised service along with a bouquet of products under Corporate Salary Package (CSP) at the door step of the salaried customers. The total Salary account customer base has reached 124.07 lakh accounts registering a growth of 38% over FY2017. Under CSP, your Bank offers Complimentary Accident (Death) Insurance cover up

to ` 20 lakh. During the year, Bank has settled 763 insurance claims amounting to ` 37.77 crore.

7. Wealth Management Business - SBI EXCLUSiF

Your Bank’s Wealth Management Services are now made available at 13 centres with 76 dedicated Wealth Hubs and 3 e-Wealth centres. An addition of 5 new centres and 55 new wealth hubs were made during the financial year. The Wealth Hubs are managed by a dedicated group of Relationship Managers and Investment Counsellors having in-depth knowledge on markets and products along with senior internal staff in operational roles.

An open platform for investment with a state-of-the-art technology and right selling approach based on Risk Profiling provides the best possible experience to your Bank customers through the EXCLUSiF journey.

The e-Wealth Centres are equipped with on-Video and on-Phone transaction execution facilities with extended Banking Hours. Your Bank’s endeavour is to provide a best in class holistic experience to Customers.

Your Bank also launched Wealth Management Services for Non-Resident Indians. Clients residing in U.A.E., Bahrain, Qatar, Kuwait and Sultanate of Oman are eligible to onboard as wealth customers. They can access services through e-Wealth Centres or through Wealth Hub during their visit to India.

38 Directors’ Report

Your Bank also conducted Signature ‘Annual Investment Conclaves’ addressed by the experts from Financial Industry and Markets on the prevalent market conditions and investment opportunities. These Conclaves were well attended by a large number of existing and prospective EXCLUSiF customers.

Your Bank’s Wealth Management Business has shown an exponential growth in terms of client acquisition and Net New Money

generation during FY2018. The number of wealth clients grew 528% during the year to reach 24,168 clients as on 31st March, 2018. The Net New Money grew by 566% to `1,998 crore and AUM increased by 390% to `14,284 crore.

Your Bank aspires to play a leading role in building the momentum for investments by embracing the changes happening in the economy and enhancing wealth creation for esteemed customers.

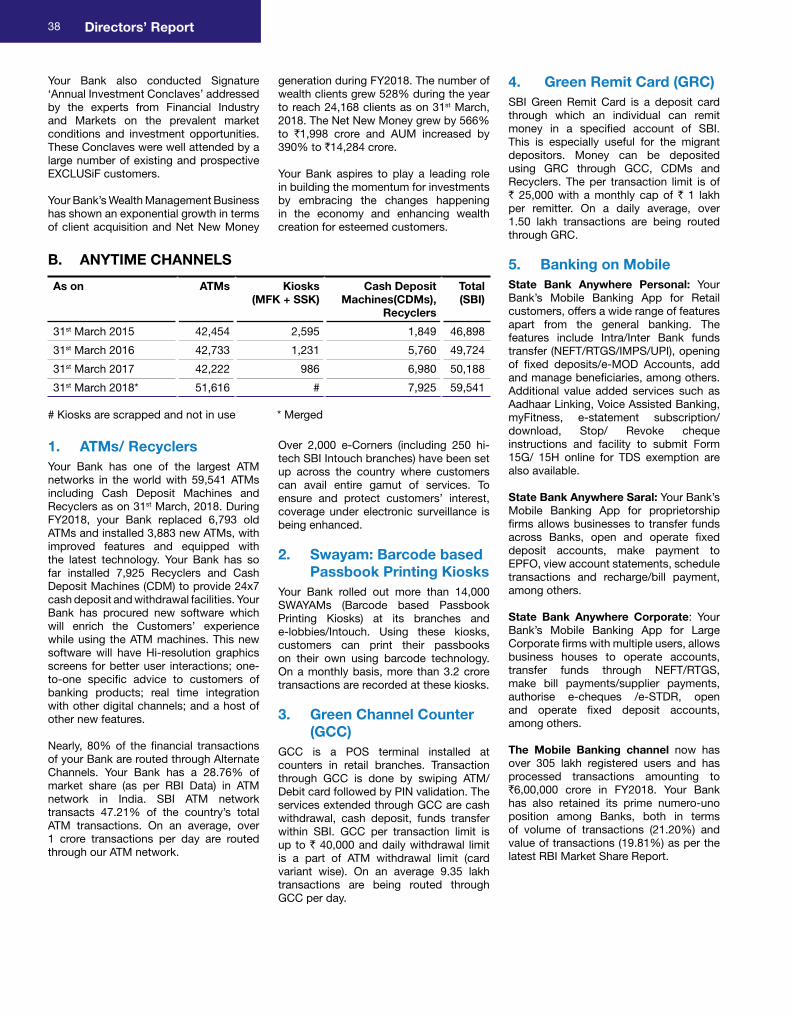

B. ANYTIME CHANNELS

As on ATMs Kiosks (MFK + SSK)

Cash Deposit Machines(CDMs),

Recyclers

Total (SBI)

31st March 2015 42,454 2,595 1,849 46,898

31st March 2016 42,733 1,231 5,760 49,724

31st March 2017 42,222 986 6,980 50,188

31st March 2018* 51,616 # 7,925 59,541

# Kiosks are scrapped and not in use * Merged

1. ATMs/ RecyclersYour Bank has one of the largest ATM networks in the world with 59,541 ATMs including Cash Deposit Machines and Recyclers as on 31st March, 2018. During FY2018, your Bank replaced 6,793 old ATMs and installed 3,883 new ATMs, with improved features and equipped with the latest technology. Your Bank has so far installed 7,925 Recyclers and Cash Deposit Machines (CDM) to provide 24x7 cash deposit and withdrawal facilities. Your Bank has procured new software which will enrich the Customers’ experience while using the ATM machines. This new software will have Hi-resolution graphics screens for better user interactions; one-to-one specific advice to customers of banking products; real time integration with other digital channels; and a host of other new features.

Nearly, 80% of the financial transactions of your Bank are routed through Alternate Channels. Your Bank has a 28.76% of market share (as per RBI Data) in ATM network in India. SBI ATM network transacts 47.21% of the country’s total ATM transactions. On an average, over 1 crore transactions per day are routed through our ATM network.

Over 2,000 e-Corners (including 250 hi-tech SBI Intouch branches) have been set up across the country where customers can avail entire gamut of services. To ensure and protect customers’ interest, coverage under electronic surveillance is being enhanced.

2. Swayam: Barcode based Passbook Printing Kiosks

Your Bank rolled out more than 14,000 SWAYAMs (Barcode based Passbook Printing Kiosks) at its branches and e-lobbies/Intouch. Using these kiosks, customers can print their passbooks on their own using barcode technology. On a monthly basis, more than 3.2 crore transactions are recorded at these kiosks.

3. Green Channel Counter (GCC)

GCC is a POS terminal installed at counters in retail branches. Transaction through GCC is done by swiping ATM/Debit card followed by PIN validation. The services extended through GCC are cash withdrawal, cash deposit, funds transfer within SBI. GCC per transaction limit is up to ` 40,000 and daily withdrawal limit is a part of ATM withdrawal limit (card variant wise). On an average 9.35 lakh transactions are being routed through GCC per day.

4. Green Remit Card (GRC)SBI Green Remit Card is a deposit card through which an individual can remit money in a specified account of SBI. This is especially useful for the migrant depositors. Money can be deposited using GRC through GCC, CDMs and Recyclers. The per transaction limit is of ` 25,000 with a monthly cap of ` 1 lakh per remitter. On a daily average, over 1.50 lakh transactions are being routed through GRC.

5. Banking on Mobile State Bank Anywhere Personal: Your Bank’s Mobile Banking App for Retail customers, offers a wide range of features apart from the general banking. The features include Intra/Inter Bank funds transfer (NEFT/RTGS/IMPS/UPI), opening of fixed deposits/e-MOD Accounts, add and manage beneficiaries, among others. Additional value added services such as Aadhaar Linking, Voice Assisted Banking, myFitness, e-statement subscription/download, Stop/ Revoke cheque instructions and facility to submit Form 15G/ 15H online for TDS exemption are also available.

State Bank Anywhere Saral: Your Bank’s Mobile Banking App for proprietorship firms allows businesses to transfer funds across Banks, open and operate fixed deposit accounts, make payment to EPFO, view account statements, schedule transactions and recharge/bill payment, among others.

State Bank Anywhere Corporate: Your Bank’s Mobile Banking App for Large Corporate firms with multiple users, allows business houses to operate accounts, transfer funds through NEFT/RTGS, make bill payments/supplier payments, authorise e-cheques /e-STDR, open and operate fixed deposit accounts, among others.

The Mobile Banking channel now has over 305 lakh registered users and has processed transactions amounting to `6,00,000 crore in FY2018. Your Bank has also retained its prime numero-uno position among Banks, both in terms of volume of transactions (21.20%) and value of transactions (19.81%) as per the latest RBI Market Share Report.

39

2,413

FY2016 FY2017 FY2018

2,706

Mobile Banking - No. of Transactions

(In Lakh)

1,456

Mobile Banking - Value of Transactions

(` in crore)

FY2016 FY2017

6,12,790

FY2018

6,00,502

1,04,390

SBI ICICI PayTM AXIS

Mobile Banking - Market Share (In %)

12.76

21.87

9.73

19.50

16.84

17.10

0.25

17.20

No. of Transaction Value of Transactions

6. SBI Pay (BHIM) Your Bank’s Unified Payments Interface based-app provides any registered/on-boarded user/merchant the convenience of transferring funds across different Bank accounts through multiple modes (Virtual Payment Address, Bank Account Number, IFSC and scanning QR Code), making it a truly inter-operable offering. 184 lakh users have registered on the SBI UPI system and transactions amounting to `68,000 crore have been successfully processed through the SBI UPI channel.

Large multinational corporations have leaped on to the digital payments bandwagon to help India become a less cash economy. Your Bank has leveraged on this opportunity to provide the latest digital payment offerings through various collaboration. Your Bank has also partnered with Google India to offer PSP services to their UPI App – Google Tez under the UPI Multi-Bank Integration Model. Over 13 lakh Tez users have linked their Bank accounts with their @OKSBI handle offered by SBI to transact on the App. In addition, debit card based payment services, P2P lending services

are also being planned among others. Users now have the convenience of making bill payments, booking flight tickets, recharging and ordering food through BHIM SBI Pay. Your Bank has also brought digital payments to the masses to enable UPI payments for over 37 lakh members of Self Help Groups under the Shri Kshetra Dharmasthala Rural Development Programme (SKDRDP) in the state of Karnataka. This was launched in the presence of Hon’ble Prime Minister of India on 29th October, 2017.

Exchange of MOU between SBI and SKDRDP in the presence of Hon’ble Prime Minister of India

7. SBI Buddy Your Bank’s Mobile Wallet allows users to send and receive money. In addition, users can also shop; book rail, movie or flight tickets; use virtual debit card – Buddy Card to make payments; withdraw cash at SBI ATMs using the wallet and a lot more. Users can now complete the full KYC check to enjoy enhanced limits on the wallet as well. Buddy has seen remarkable growth and has reached a user base of 129 lakh as on 31st March, 2018. The wallet has facilitated over 496 lakh transactions to the tune of ` 1,505.79 crore as on 31st March, 2018.

Emergence of Fintech companies has made data the prime point for selectively and effectively targeting customers. Increasingly, digital products from banks are being promoted through social networking sites and online advertising. Your Bank has established digital solutions that offer one of the best all-round omni-channel experience for its customers.

8. YONOOn 24th November, 2017, State Bank of India launched India’s first comprehensive

digital service platform “YONO”, an acronym for ‘You Only Need One’. An integrated omni-channel digital platform, YONO offers banking and other financial products along with access to India’s largest B2C marketplace for its customers to meet their lifestyle needs across 16 categories including Fashion & Lifestyle, Electronics, Education, Home & Furnishing, Travel & Hospitality, Cab Booking & Car Rentals, Entertainment, Food & Dining, Health & Personal Care and others. Your Bank has partnered with 70+ top e-commerce players to provide customised offers and discounts to its customers. With YONO, customers can:

z Open an SBI bank account digitally in 4 minutes

z Avail Pre-approved personal loan sans any paperwork in 4 clicks

z Get overdraft facility against fixed deposit instantly online

z Get one view of the banking and financial portfolio of SBI Group companies

z Benefit from intelligent spend analyser

40 Directors’ Report

z Utilise Chatbot ‘SIA’

z Create dreams to target and fund the dreams

z Access B2C Marketplace

z Open a new demat/trading account

z Link trading/demat account

z Apply for credit cards online

z Link credit cards and pay credit card bills seamlessly

z Avail insurance products online.

Performance highlights of YONO as on 31st March 2018

z 4.37 Million Application Downloads

z 1.36 Lakh Digital and Insta Savings Accounts opened

z 6.52 Lakh Funds Transfers executed

z 17,000+ Fixed Deposits opened

z 71,000+ Bill payments done

z 77,000+ SBI Credit Cards linked; 41,000 Card payments of ` 43 crore done; 33,000 new Card leads generated

z 41,000+ SBI Cap Sec portfolios linked; 9,000 new demat account leads generated

z 11,000+ SBI Life policies linked

z 2,400+ Pre-approved Personal Loans of ` 12 crore disbursed

9. Customer Experience Excellence Project (CEEP)

The Customer Experience Excellence Project CEEP has been rolled out at 5,364 branches across the country which are equipped with Self Service machines as ATM, CDM/ Recycler, SWAYAM for Passbook Printing, Electronic Cheque Drop Box and Internet enabled PCs. An integrated Queue Management system (QMS) is in place at these branches to ensure that the customers are serviced promptly without having to wait in queues at the counters. There is a provision of separate token for Senior Citizens/Disabled persons in QMS to give them preferential service. A Customer Feedback Tab is provided at these branches to enable the customers to give their feedback on the services of the branch. Real time monitoring and Branch choreography are undertaken at these branches to give the customers an excellent service experience.

Your Bank’s Mobile App “State Bank No Queue” enables customers to self-generate e-tokens for availing Banking services at CEEP Branches. This App is available on both Android and iOS phones and it helps in reducing waiting time for customers at the branch. It also reduces crowding at a branch as the token is generated before the customer reaches the branch. This helps customers to skip the queue and avail banking services faster. As on 31st March, 2018, the App has registered more than 23,66,000 (2.37 million) downloads. The usage of the App is increasing on daily basis. The HNI customers are tagged as Priority Customers at these branches.

Your Bank has also undertaken Customer Service Feedback Survey at select CEEP branches to assess the impact of the CEEP initiative on the quality of customer service. The feedback thus received is being used to improve the customer service and facilities available for the customers.

10. Digital BankingYour Bank has always been a pioneer in innovating new concepts in Banking Sector. One such step was setting up the high-tech, one of its kind, sbiINTOUCH branches, which has brought in a new paradigm in banking. At present, your Bank has 262 sbiINTOUCH branches equipped with state-of-the-art digital technology. These sbiINTOUCH branches cover more than 148 districts across the country.

At the sbiINTOUCH branches, your Bank provides banking services such as the opening of accounts and the printing of personalised Debit Cards in 15 minutes. This has been made possible

by revolutionary Touch Technology. Your Bank’s strategy is to create a ‘Phygital’ marketplace within these futuristic branches, to offer customers 1) Banking through self- service kiosks and 2) Services of other SBI subsidiaries such as Life Insurance, General Insurance, Mutual Funds, Credit Cards and online trading through SBI Cap Securities. Financial counselling through hi-definition Audio Video conferencing service is provided at select sbiINTOUCH branches, where customers can interact with financial experts.

In August, 2017, your Bank has also launched, the facility of instant issuance of personalised Photo Debit Card – ‘Quick Photo Debit Card’ within five minutes to Saving Bank (SB) account holder of any branch of SBI. Under the facility, an individual SB account holder who has an account with SBI and has lost or damaged his debit card, can visit any sbiINTOUCH Branch with his Aadhar Card and obtain Instant Photo Debit Card, bearing his photograph, through Debit Card Printing Kiosk.

11. Cross SellingYour Bank is the Corporate Agent of SBI Life Insurance Co. Ltd & SBI General Insurance Co. Ltd. and has Distribution Agreement with SBI Mutual Fund, SBI Cards & Payment Services Pvt. Ltd & SBI Cap Securities Limited for distributing their products. Your Bank also distributes mutual fund products of UTI Mutual Fund, Tata Mutual Fund, Franklin Templeton Mutual Fund, L&T Mutual Fund, ICICI Mutual Fund, and HDFC Mutual Fund. In addition, all branches are authorised for opening pension accounts under National Pension System.

Performance Highlights (Income)

(` in crore)

ACTUALS

JVs YTD March, 2017

YTD March, 2018

% YoY change

SBI LIFE 575.97 714.75 24.10

MF 185.24 560.51 202.59

SBI GENERAL 125.97 212.57 68.74

SBI CARDS 25.13 135.83 440.51

SSL 2.43 5.14 111.52

NPS - 2.44 -

TOTAL 914.74* 1631.24 78.33

*YTD Mar’17 figure inclusive of e ABs data - 776.61 (SBI) + 138.13 (eABs)

41

The key highlights for FY2018 are mentioned below:

z SBI Mutual Fund became 2nd largest amongst Bank distributors in the Industry with an AUM of more than ` 54,000 crore. Your Bank has become India’s number one Bank distributor in SIP with 14.6 lakh live SIPs. Net sales increased from ` 11,464 crore in March, 2017 to `24,374 crore YTD March, 2018 reporting an increase of 113%.

z Cards issued through Banca Channel crossed 10 lakh and sourcing has increased from an average of 35% upto September, 2017 to 53% in March, 2018.

z Your Bank received SKOCH Award – Platinum for its National Pension System Application and was ranked No. 1 in Point of Presence (POP) under various log in day campaigns observed by PFRDA.

z Under SBI Life, CIF grew to 46,180 in YTD March, 2018 as against 24,470 in YTD March 2017, reporting an increase of 89%. The Home Loan Insurance penetration increased from 45% to 58%.

z Under SBI General, SP number has increased to 20,646 in YTD March, 2018 as against 14,348 in YTD March, 2017, reported a growth of 44%. The number of Health Insurance policies issued increased by 11% to 7.82 lakh and premium increased by 16% to `179.45 crore over March, 2017. In FY2018, net profit earned by SBI General Insurance Co. stood at ` 380 crore out of which ̀ 170 crore seeding commission was earned from Long Term Home (LTH) reinsurance.

12. Internet Banking and e-Commerce

Your Bank’s Internet Banking Service brings on board a seamless online experience hosting diverse Banking offerings. Opening and operation of Fixed Deposits/PPF accounts, Intra/Inter Bank transfer of funds through NEFT/RTGS, submission of Form 15G/15H, Nomination updation facility, foreign international remittances are among the many functionalities, being offered. Some of the services/features launched during the year, that have made Bank’s digital platform more robust and customer-friendly, are access to CIBIL score, Aadhaar linking with CIF, purchase of Sovereign Gold Bonds, SMS alerts in Hindi, GSTN integration, submission of 15G/H Form through RINB portal, submission of Financial Follow up Report

(FFR-I & FFR- II) by Vyapaar/Vistaar corporate users and creation of e-TDR & e-STDR for amount of ` 1 crore and above through CINB. This highly secure and cost-effective channel has processed 159 crore transactions during FY2018, and the addition of new INB users has registered a growth of 35% over the previous year.

To rejuvenate the e-Commerce ecosystem proactive initiatives have been taken for technology partnerships with various Government Departments enabling them to leverage their e-Governance channels like e-Auction, e-Tendering, e-Freight and online collection of tax dues. Over 17,515 merchants have been on-boarded under ASVA model during FY2018. BHIM SBI Pay has been added as one of the options in SBMOPS.

FY2017 FY2018

74.00

97.12

New INB Users Added (in lakh)

FY2017 FY2018

148.63

158.92

No. of INB Transactions (in crore)

FY2017 FY2018

79,67,967

98,82,905

Value of INB Transactions

(` in crore)

C. SMALL AND MEDIUM ENTERPRISES

Your Bank is pioneer and market leader in SME financing. With over one million customers, the SME portfolio of ` 2,69,875 crore, as on 31st March, 2018 accounts for nearly 13.17% of the Bank’s total advances.

Considering the important role being played by SMEs in the Indian economy in terms of their contribution to manufacturing output, exports and employment generation, your Bank has always held SME as an important segment.

Your Bank is committed to providing Simple and Innovative Financial Solutions. Your Bank’s approach in driving SME growth rests on the following three pillars:

a) Customer Convenience,

b) Risk Mitigation,

c) Technology based digital offerings.

1) Customer Convenience With a view to building and sustaining the momentum for Transforming India, your Bank has created largest number of touch points in terms of number of branches and other modes, reaching out to public at large, which includes RMSEs (866), RMMEs (775), CSOs (900), SMECs (89), RASMECs (81) and SME Intensive Branches (1,248).

With a view to enhancing Ease of Doing Business to the Small and Micro Enterprises, your Bank modified its existing delivery model for Small & Medium Enterprises Center (SMEC) and created Asset Management Teams (AMT) for providing end to end relationship with the customers for small value loans up to ` 50 lakh. The SMECs have also been strengthened in terms of manpower which has resulted in improvement in service.

Web based loan application and tracking system: Your Bank is hosting an online loan application and tracking facility for MSME borrowers on the Corporate Website www.sbi.co.in. It is an Intranet-based Credit Proposal Tracking System called Lead Management system (LMS), which allows customers to apply online loan request and receive an acknowledgement in the form of application reference number. The data of customers is then automatically forwarded (through concerned network in Circles) to relationship points for converting these leads into business.

42 Directors’ Report

Participation in Business Conclaves/Summits: Your Bank has been actively participating in Business Conclaves and Summits to reach out to entrepreneurs and understand and meet their requirements.

2) Risk MitigationYour Bank has been increasingly shifting focus towards Risk Mitigated Products, which includes Supply Chain finance, Asset Backed Loans, Overdraft against Bank Deposits/Govt. Securities, Bills Discounting facility and CGTMSE covered loans, among others.

Supply Chain Finance: Leveraging the state-of-the-art technology and branch network, your Bank is further strengthening its relationship with the Corporate World and has emerged as a major player in Supply Chain Finance.

During the fiscal, your Bank entered into 49 new e-DFS (Electronic Dealer Finance Scheme) and 8 new e-VFS (Electronic Vendor Finance Scheme) tie-ups covering 292 Industrial Majors and 22,406 of their dealers and 12,512 vendors. The number of oil dealers (Petrol Pumps) on e-DFS crossed 13,000 during the last fiscal. There has been 19% YoY growth in e-DFS portfolio.

March2015

10,024

March2016

14,048

March2017

March2018

18,078

21,532

e-DFS (` in crore)

The market segment wise and sector wise diversification of eDFS portfolio is represented in the pie-chart below:

11%

8%

10%

13%

4%

22%

32%

Oil & Petrochem

Auto PV

Others

FMCG

Steel

Auto 2W

Auto CV

Shri P. K. Gupta, MD (R&DB), felicitating officials of M/s TATA Motors Ltd. for SBI-TATA Motors Ltd., Tie-up under SBI - Supply Chain Finance (e-DFS & e-VFS)

Pradhan Mantri Mudra Yojana: In line with the initiatives of the Government of India, your Bank has laid considerable emphasis on extending credit facilities to eligible units under different variants of Pradhan Mantri Mudra Yojana and has disbursed ` 28,556 crore for FY2018 under PMMY against a target of ` 28,300 crore.

Credit Flow to Micro and Small Enterprises under CGTMSE: Your Bank has been a pioneer in supporting MSMEs and for Micro and Small business. Your Bank is extending collateral free lending up to ` 2 crore under guarantee of CGTMSE. SBI has a portfolio of ` 12,549 crore under CGTMSE as on 31st March, 2018.

SME ASSIST: Introduction of GST is a transformational move by the Government of India. Your Bank conducted GST workshops in 91 modules/centers as a part of knowledge dissemination initiative on GST, covering 4,087 SME borrowers. Town Hall Meetings were also conducted at all the District Headquarters to bring awareness about GST among MSMEs.

Your Bank rolled out a new Product - SME ASSIST during the fiscal to finance pending input credit claims under GST. As on 31st March, 2018, your Bank has funded 431 units with a total portfolio of ` 228 crore.

3) Digital offeringsYour Bank is leveraging technology in every aspect of the value proposition from sourcing business, designing products, streamlining process, improving delivery to monitoring.

Your Bank has taken several initiatives to build SME portfolio in a risk mitigated manner and has brought about significant changes in (i) Product suite, (ii) Process (iii) Delivery.

Ecosystem Financing (Project Shikhar) has been introduced by your Bank to take advantage of growing e-commerce footprint in the economy.

Cluster Based Funding: Cluster based approach enables your Bank to deal with well-defined and recognised groups and

43

to tap the growth potential. Since the units belong to a cluster with same kind of activity, it helps in assessing their needs and monitor the overall portfolio. As on 31st March, 2018, your Bank has helped 441 units under Cluster Finance with total portfolio of ` 450 crore.

Warehouse Receipt Finance: Your Bank has introduced Warehouse Receipt Financing scheme (WHR) to extend finance to traders/owners of goods/manufacturers for own processing against Warehouse Receipts. Warehouse receipt is issued by Collateral Managers with whom your Bank has a tie-up (presently NBHC, NCML, Star Agri, Origo). Further, WHR issued by Central Warehousing Corporation (CWC)/State Warehousing Corporation (SWC) is also eligible for WHR finance. The WHR portfolio as on 31st March, 2018 stands at ` 5,795 crore.

Project VivekProject Vivek, heralded paradigm shift in your Bank’s appraisal system from traditional Balance Sheet based funding to a more objective appraisal system of leveraging cash flow and other information sources. It is a promising initiative taken and launched by your Bank for new Credit Underwriting Engine (CUE) for the SME segment, which brings in objectivity for better risk assessment. It also reduces Turn Around Time (TAT) resulting in better customer experience. As on 31st March, 2018 , a total 13,713 proposals have been processed under Project Vivek.

Trade Receivables Discounting System (TReDS): TReDS have been set up for flow of finance to MSMEs. Your Bank was first among all PSBs to register on the TReDS platform RXIL and M1xchange. Your Bank has been actively participating in the online biddings on the platform and has been offering very competitive rates to the benefit of MSMEs.

Loan Origination Software (LOS-SME) and Loan Life-Cycle Management System (LLMS): With a view to adopt the uniform standards of credit dispensation and for ensuring quality and preserving corporate memory, LOS & LLMS have been introduced for small and high value loans, respectively.

Digital Inspection Application (DIA-SME): This is a Tab and Mobile based application for recording inspection of SME units as a process of digitalisation of pre-sanction/ post sanction processes of SME units. Your Bank also records collateral security, location of the properties and place of business with photograph and geo-coordinates through this Digital application.

D. RURAL BANKING

1. Agri BusinessAgainst the background of the Union Government’s goal of doubling farmers’ income by 2022, Agriculture and allied activities have got greater focus during the year in your Bank’s lending activity. Your Bank serves about 1.35 crore farmer families all over India. It surpassed the Agri credit flow target set by the Government of India during FY2018, as it has done in the past. This is depicted in the table below:

Flow of Credit to Agriculture Trend

(` in crore)

Year Target Disbursement % Achievement

FY2015 84,500 86,193 102%

FY2016 89,781 1,02,423 114%

FY2017 95,168 1,25,270 132%

FY2018 1,05,741 1,66,819 158%

In order to ease the flow of credit for Agriculture, your Bank has now raised the limit for renewal of mortgage-free crop loans from ` 1 lakh to ` 1.5 lakh. It has also introduced a scheme for financing of dairy units under the Mudra scheme with liberalised terms for loans up to ` 10 lakh, as allied agricultural activity is a mean of increasing farmers’ income.

A new product which is designed to meet the general-purpose needs of farmers against the collateral of property called the Asset Backed Agri Loan (ABAL), picked up momentum during the year and the growth under this product was about 200%, albeit on a lower base. This product has been accepted by customers because of the flexibility it offers.

Your Bank is de-risking its Agri portfolio and supporting farmers at the same time

by entering into local level and national level tie-ups with Agri Corporates, wherein the supply chain will ensure cash flows for timely renewal of loan and better incomes for the farmers. Your Bank is also lending under a Cluster-based approach to tap opportunities that revolve around areas and centres which have traditionally been known for activities like shrimp farming, dairy, poultry and higher value horticulture crops like pineapple and mango.

Recognising the contribution of rural India to the nation’s economic growth, your Bank has been striving to meet the financial needs of the rural segment through various new channels and services. A pilot project on a hub-and-spoke model for improving turn-around time and the quality of credit appraisals in the Rural and Semi-urban branches was rolled out in over 80 Regions across the country.

Improving Productivity through Soil Testing Programme Branch : Dalgaon, North-East Circle

44 Directors’ Report

more than 10 crore accounts up to 31st March, 2018 and issued 6.62 crore RuPay debit cards to eligible customers. These initiatives taken under financial inclusion are a part of key economic policy agenda of the Government. Over the last decade, your Bank has a major share in providing access to banking services to the excluded in the ecosystem.

59%

41%

No. of PMJDY A/CsSBI

Others PSBs

73%

27%

Deposits in A/Cs (PMJDY)SBI

Others PSBs

63%

37%

No. of Rupay Cards Issued (PMJDY) SBI

Others PSBs

To fulfill the needs of Social Security measures, low cost Micro insurance products (PMJJBY, PMSBY) and pension schemes(APY) to the unorganised sector are also provided in a big way, covering over 2 crore of customers. These initiatives are empowering the population to have the benefit of the financial system and move towards a cashless economy.

As widely reported, the Agriculture sector saw a number of developments with a few States announcing waiver of farm loans in response to demands by the farmers. Your Bank on its own announced two Rinn Samadhan schemes, covering farm sector loans and the internal targets set under both the schemes were achieved.

Keeping in view the large number of customers served by your Bank, it took the lead and organised mass contact programmes on six occasions during the year. Under this initiative, on a pre-fixed day, all Rural and Semi-urban branches of your Bank held informal meetings with farmers to improve customer connect and spread awareness about the Bank’s and Government’s schemes. It is estimated that at least 1.5 million farmers attended these meets.

Other important initiatives taken during the year included issuance of 71.66 lakh KCC-ATM-RuPay Cards to Kisan Credit Card (KCC) borrowers for ease and operational convenience. KCC RuPay Cards work seamlessly with ATMs and PoS machines, enabling farmers to purchase their day-to-day farm requirements on 24x7 basis.

2. Financial Inclusion (FI)Your Bank realises the role it must play as the largest bank in the country in practicing and promoting financial inclusion activities. The spread of digital banking channels and expansion of Business Correspondents (BC) networks are giving your Bank the impetus to further grow its financial inclusion activities. Thus, to achieve inclusive development and growth, your Bank has worked out several strategies and leveraged technology to expand financial services to the door steps of people with the purpose of bringing the excluded under the ambit of formal banking system.

Your Bank has 58,274 operating Business Correspondents and over 22,400 branches across the country to offer banking services. The Business Correspondent channel has recorded 31.21 crore transactions amounting to ` 1,24,930 crore in FY2018, translating to around 1-1.5 million transactions per day. The Business Correspondent channel provides customers with access to various banking products and services, reducing the foot-falls in the branches.

Under the Pradhan Mantri Jan Dhan Yojana (PMJDY), your Bank has paved the way for universal financial access by being a pioneer in implementing the programme. Your Bank has opened

a. Imparting Financial LiteracyWith the objective of imparting financial literacy and facilitating effective use of financial services, your Bank has set up 336 Financial Literacy Centres (FLCs) across the country. During FY2018, a total of 23,962 financial literacy camps were conducted by these FLCs across the country. As part of the pilot project being implemented by RBI, your Bank has also set up 15 centres for Financial Literacy at Block level, 5 each in the state of Maharashtra, Chhattisgarh and Telangana in association with NGOs identified by RBI.

b. Rural Self Employment Training Institutes (RSETIs)

Rural Self Employment Training Institutes (RSETIs) play an important role in skill development by imparting comprehensive quality training programme to rural youth. It also facilitates them in setting up of micro enterprises. Your Bank has set up 151 RSETIs spread across 27 States and one Union Territory.

Your Bank RSETIs have trained more than 1 lakh rural youth during FY2018. Over 63% of the candidates trained are women and 83% of the candidates trained belong to non-general categories (SC/ST/OBC/Minorities). More than 6 lakh candidates have been trained by SBI-RSETIs over a period of seven years of which 67% have been settled, thus building momentum for transforming rural India.

E. OTHER NEW BUSINESS INITIATIVES

1. Payment Solution VerticalBanking system is witnessing new challenges in its traditional business domain from new digitally enabled entrants. Payment systems, of late, have become the most sought after aspect of banking business on account of the growing penetration of smart phones, e-commerce and launch of a number of innovative products/mobile apps.

Debit Cards: With approximately 26 crore actively used Debit Cards as on 31st March, 2018, your Bank continues to lead in Debit Card issuance in the country. SBI has a market share of 32.35% in terms of Debit Card penetration as on 31st March, 2018. In line with the approach of moving towards a digital economy, your Bank has adopted a focused strategy on shifting the usage of Debit Cards by customers from ATM (for cash withdrawals) to PoS/eCom websites by executing regular promotional/activation campaigns in collaboration with leading

45

e-comm and retailers. Your Bank has successfully launched various innovations and functionalities around Debit Cards like Contactless Debit Cards, Bharat QR, Samsung Pay and Visa Checkout.

In order to increase digital participation with customers, your Bank has also tied up with various institutions like Mumbai Metro, Chennai Metro, IIM Ahmedabad, College of Engineering - Pune and others for launching co-branded Debit Cards/combo Cards.

Such consistent initiatives towards digitising payment transactions, not only reduce cost of transactions but also help in reducing carbon footprint through lesser use of paper. As a result of these initiatives, your Bank has improved its market share in Debit Card spends from 29.33% as on 31st March, 2017 to 30.40% as on 31st March, 2018.

State Bank Foreign Travel Cards: State Bank Foreign Travel Cards (SBFTC) are available on the VISA platform, in eight Foreign currencies namely Japanese Yen, Canadian Dollar, Australian Dollar, Saudi Riyal, Singapore Dollar, US Dollar, Euro and British Pound, providing safety, security and convenience to overseas travellers. SBFTC is also issued as Multicurrency card on MasterCard platform. Initially, it was launched in four currencies viz. US$, GBP, Euro and SGD. During the year, three new currencies viz. AUD, CAD and AED have been added. Your Bank is also aggressively promoting tie-ups with FFMCs (Full Fledged Money Changers).

Rupee Prepaid Cards: Prepaid card usage has been growing for purchase of goods and services as well as for funds transfer in India. Your Bank has issued PPIs for ` 950.31 crore during FY2018 registering a growth of 122.90% over the previous year.

Enterprise Wide Loyalty Program - State Bank Rewardz: To encourage and maximise digital adoption amongst SBI customers and also to attract more customers on SBI platform, your Bank launched Loyalty Rewardz program across seven channels during 2015, which is being extended to 4 more channels including YONO. This will encourage repetitive usage of digital transactions thereby creating digital habit amongst customers. State Bank Rewardz has also been implemented through mobile app, which can be downloaded from the Google Play Store and from App Store in iOS

Foray into digitalisation of Mass Transit: The advent in digital technology along with rapid urbanisation and infrastructure development, has given a significant boost to the urban public transportation in India. With a vision to ‘Be the Bank of Choice for a Transforming India’, your Bank has taken the following steps on its journey of transforming the transit space in India:

(a) Your Bank has successfully imp-lemented the ambitious project of NHAI - National Electronic Toll Collection (NETC). Your Bank is issuing SBI FASTag; working on Radio Frequency Identification technology (RFID) and enables the Customers to pay the toll electronically across all the National Highway Toll plazas.

Through SBI FASTag, customers can pay their toll electronically and can top up/recharge their SBI FASTag wallet online through a dedicated portal by using various modes like Debit Cards, Credit Cards, Internet Banking of any Bank. The customer can also view the history of transactions of their vehicle.

Your Bank has issued more than 2.7 lakh tags to customers. Toll transactions through the SBI FASTag has crossed a mark of 68 lakh and total transaction amount has crossed ` 140 crore level in FY2018.

(b) With the aim of digitising micro-payments rapidly, your Bank has participated in various metro and transit projects. Your Bank has been awarded the Nagpur and Noida metro project for implementation of open loop Automatic Fare Collection System based on the qSPARC technology on the RuPay platform.

Your Bank has designed SARVATRA Card in line with the National Common Mobility Card (NCMC) guidelines as envisioned by Ministry of Urban Development (MoUD). This card offers features of a metro travel card on RuPay Prepaid Card, wherein transactions can be conducted offline. Apart from payment of fares in the multi modal transit, this card offers extended usage for retail payments as well as e-commerce.

2. Acceptance Infrastructure (Merchant Acquiring Businesses vertical)

Your Bank is playing effective role in building momentum for transforming India through digitalisation of the economy. In sync with the focus of the Government of India to create a less-cash economy, your Bank has expanded digital payment acceptance infrastructure and rolled out new payment acceptance solutions. Your Bank continues to be the top acquirer in the country in terms of number of terminals with a market share of 20.20% (as per the latest available RBI data as on 28th February, 2018). During the year, your Bank introduced two new digital payment acceptance products - Bharat QR and BHIM-Aadhhar-SBI; and on-boarded 2.02 lakh and 4.97 lakh merchants respectively on these platforms. PoS deployed by your Bank has grown from 5.09 lakh as on 31st March, 2017 to 6.10 lakh as on 31st March, 2018. In total, the number of merchant payment acceptance touch points crossed 1.96 million as on 31st March, 2018.

The value of acquiring transactions has reached almost ` 1 trillion with 68% increase on Y-o-Y basis. Your Bank has been successful in digitising sale transactions of retail outlets of oil marketing companies by installing 34,000+ PoS terminals at more than 20,000 retail outlets.

In order to increase penetration of digital merchant payment acceptance infrastructure in semi-urban and rural areas, your Bank has focused on tier V and tier VI centers. As on 31st March, 2018, about 31% of total PoS terminals deployed are in rural and semi urban areas.

In addition to offering basic acquiring services, your Bank is also providing Value Added Services such as:

z DCC-Dynamic Currency Conversion

z EMI facility

z Cash@POS facility for cash dispensation to debit card holders