Hutchison Telecommunications Hong Kong Holdings Limited ... · Hutchison Telecommunications Hong...

31

31 July 2013 Hutchison Telecommunications Hong Kong Holdings Limited (Stock Code: 215) 2013 Interim Results Presentation

Transcript of Hutchison Telecommunications Hong Kong Holdings Limited ... · Hutchison Telecommunications Hong...

31 July 2013

Hutchison Telecommunications Hong Kong Holdings Limited (Stock Code: 215) 2013 Interim Results Presentation

Disclaimer

1

These materials have been prepared by Hutchison Telecommunications Hong Kong Holdings Limited (HTHKH) solely for use at this presentation and have not been independently verified. No representations or warranties, express or implied, are made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions presented or contained in these materials.

It is not the intention to provide, and you may not rely on these materials as providing, a complete or comprehensive analysis of the financial or trading positions or prospects of HTHKH. None of HTHKH or any of their respective directors, officers, employees, agents, affiliates, advisers or representatives accepts any liability whatsoever in negligence or otherwise for any loss howsoever arising from any information or opinions presented or contained in these materials or otherwise arising in connection with these materials. The information presented or contained in these materials is subject to change without notice and its accuracy is not guaranteed.

These materials are for information purposes only and do not constitute or form part of any invitation or offer to acquire, purchase or subscribe for securities and none of them shall form the basis of or be relied upon in connection with any contract, commitment or investment decision in relation thereto.

These materials contain forward-looking statements. Statements that are not historical facts, including statements about the beliefs and expectations of HTHKH, are forward-looking statements. These statements are based on current plans, estimates and projections, and undue reliance should not be placed on them. Forward-looking statements speak only as of the date they are made, and HTHKH has no obligation to update any of them publicly in light of new information or future events. Forward-looking statements involve inherent risks, uncertainties and assumptions. HTHKH caution that if these risks or uncertainties ever materialize or the assumptions prove incorrect, or if a number of important factors occur or do not occur, actual results of HTHKH may differ materially from those expressed or implied in any forward-looking statement.

While non-generally accepted accounting principles (GAAP) measures such as EBITDA (earnings before interest, taxation, depreciation and amortisation and share of results of joint ventures) are often used by companies as an indicator of operating performance, they are not expressly permitted measures under the GAAP or the International Financial Reporting Standards (IFRS) and may not be comparable to similarly titled measures for other companies. Accordingly, such non-GAAP measures should not be considered as an alternative to operating income as an indicator of the operating performance of HTHKH and its subsidiaries or as an alternative to cash flows from operating activities as a measure of liquidity. The use of non-GAAP measures is provided solely to enhance the overall understanding of the current financial performance of HTHKH and its subsidiaries. Additionally, because HTHKH has historically reported certain non-GAAP results to investors, HTHKH considers the inclusion of non-GAAP measures provides consistency in its financial reporting.

Business Performance

3

2013 1H

HK$ millions

2012 1H (Restated)

HK$ millions

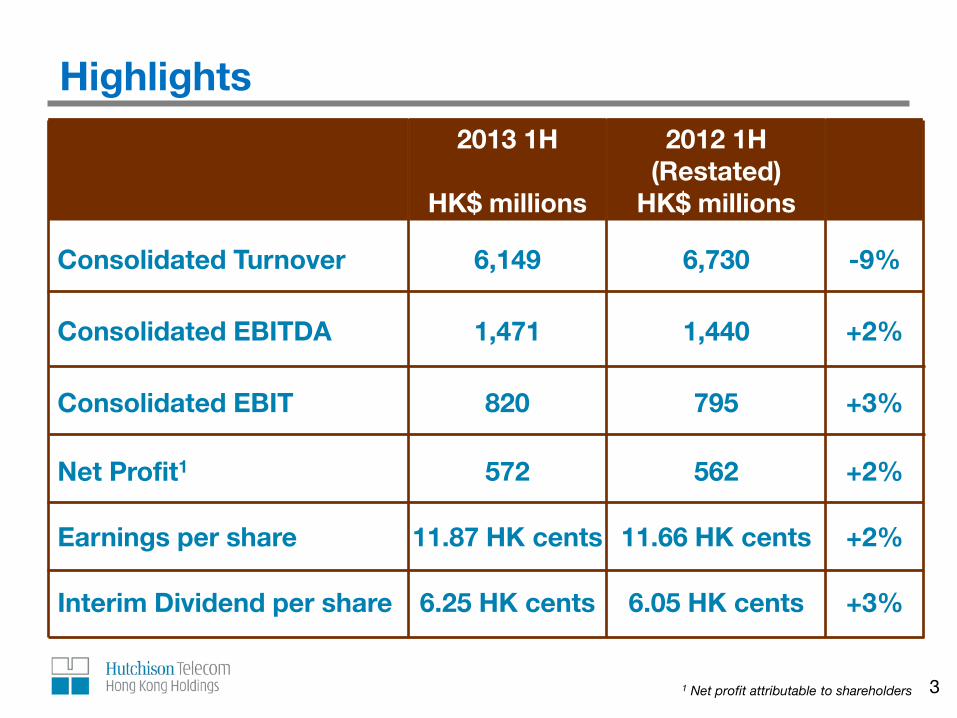

Consolidated Turnover 6,149 6,730 -9%

Consolidated EBITDA 1,471 1,440 +2%

Consolidated EBIT 820 795 +3%

Net Profit1 572 562 +2%

Earnings per share 11.87 HK cents 11.66 HK cents +2%

Interim Dividend per share 6.25 HK cents 6.05 HK cents +3%

1 Net profit attributable to shareholders

Highlights

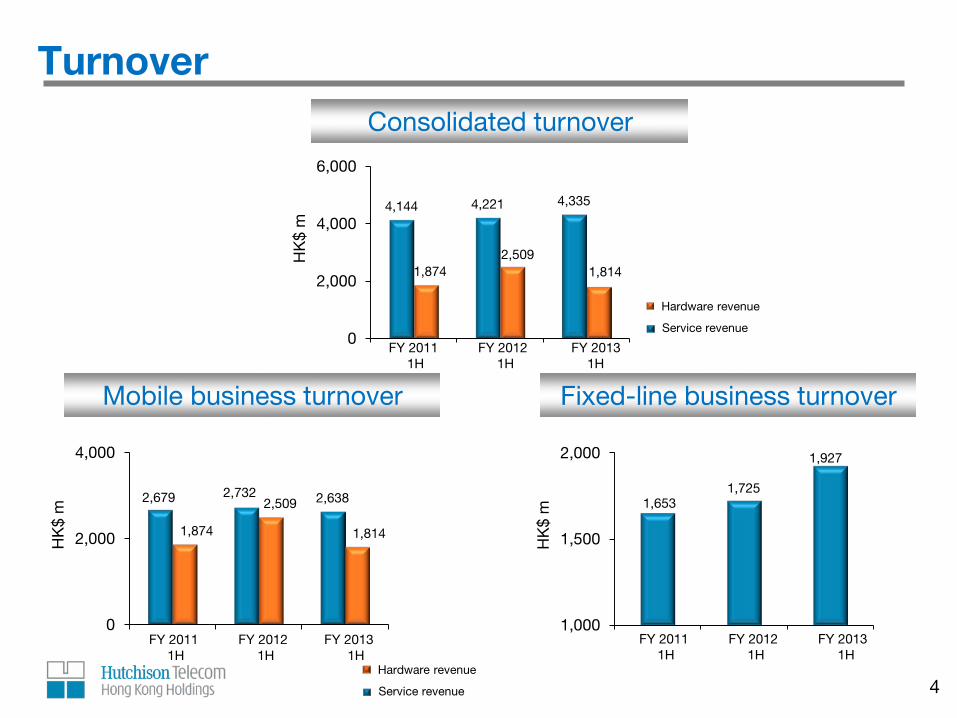

Turnover

1,630 1,653

Consolidated turnover

Mobile business turnover Fixed-line business turnover

4,144 4,221 4,335

1,874 2,509

1,814

0

2,000

4,000

6,000

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ m

2,679 2,732 2,638

1,874

2,509

1,814

0

2,000

4,000

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ m

Hardware revenue

Service revenue

1,000

1,500

2,000

FY 2011 1H FY 2012 1H FY2013 1H

HK

$ m

1,653 1,725

1,927

Hardware revenue

Service revenue

FY 2011 FY 2012 FY 2013 1H 1H 1H

FY 2011 FY 2012 FY 2013 1H 1H 1H

FY 2011 FY 2012 FY 2013 1H 1H 1H

4

Mobile

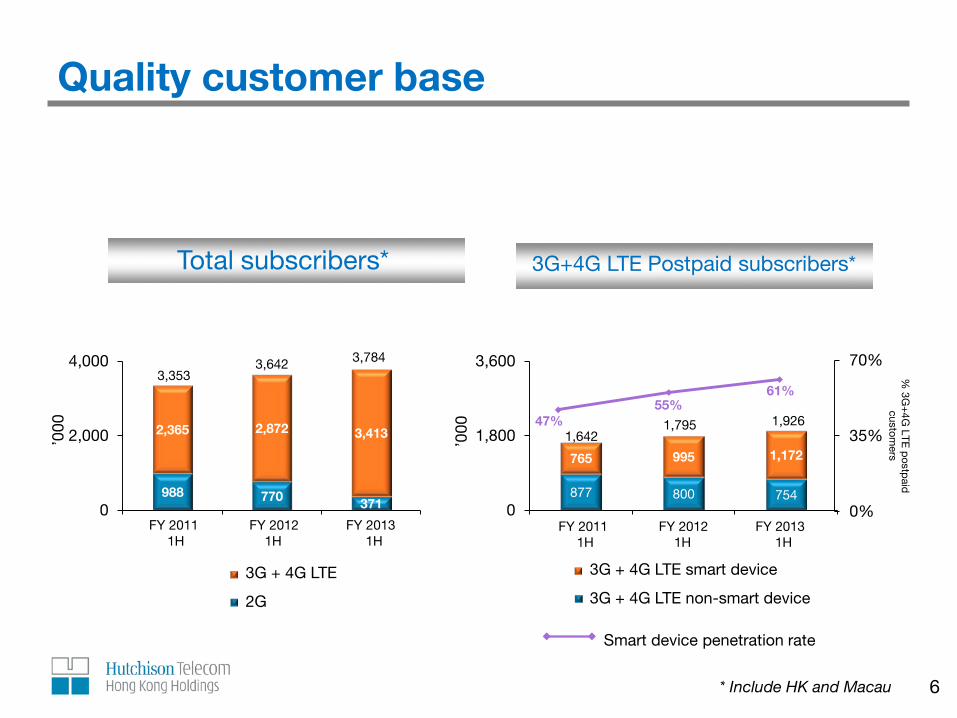

Quality customer base

2,014

* Include HK and Macau

3G + 4G LTE

2G

Total subscribers*

988 770 371

2,365 2,872 3,413

0

2,000

4,000

FY 2011 1H FY 2012 1H FY 2013 1H

’000

3,353 3,642 3,784

FY 2011 FY 2012 FY 2013 1H 1H 1H

6

47% 55%

61%

0%

35%

70%

% 3G

+4G

LTE p

ostpaid

custom

ers

877 800 754

765 995 1,172

0

1,800

3,600

FY 2011 1H FY 2012 1H FY 2013 1H

’000

1,642 1,795 1,926

3G+4G LTE Postpaid subscribers*

FY 2011 FY 2012 FY 2013 1H 1H 1H

Smart device penetration rate

3G + 4G LTE smart device

3G + 4G LTE non-smart device

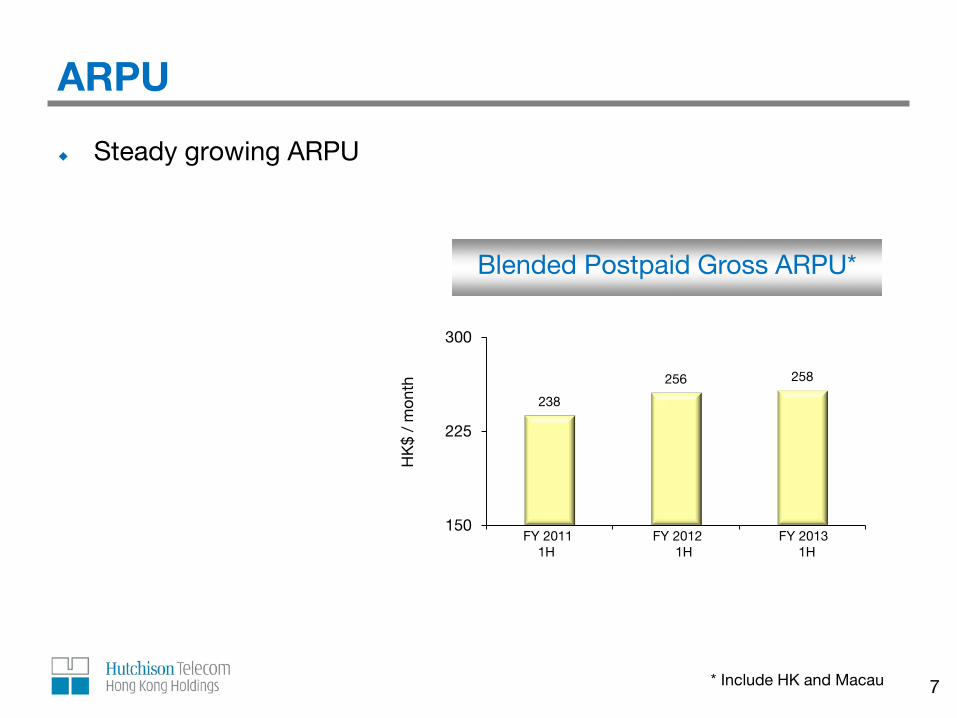

ARPU

* Include HK and Macau 7

Blended Postpaid Gross ARPU*

238

256 258

150

225

300

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ /

mon

th

FY 2011 FY 2012 FY 2013 1H 1H 1H

Steady growing ARPU

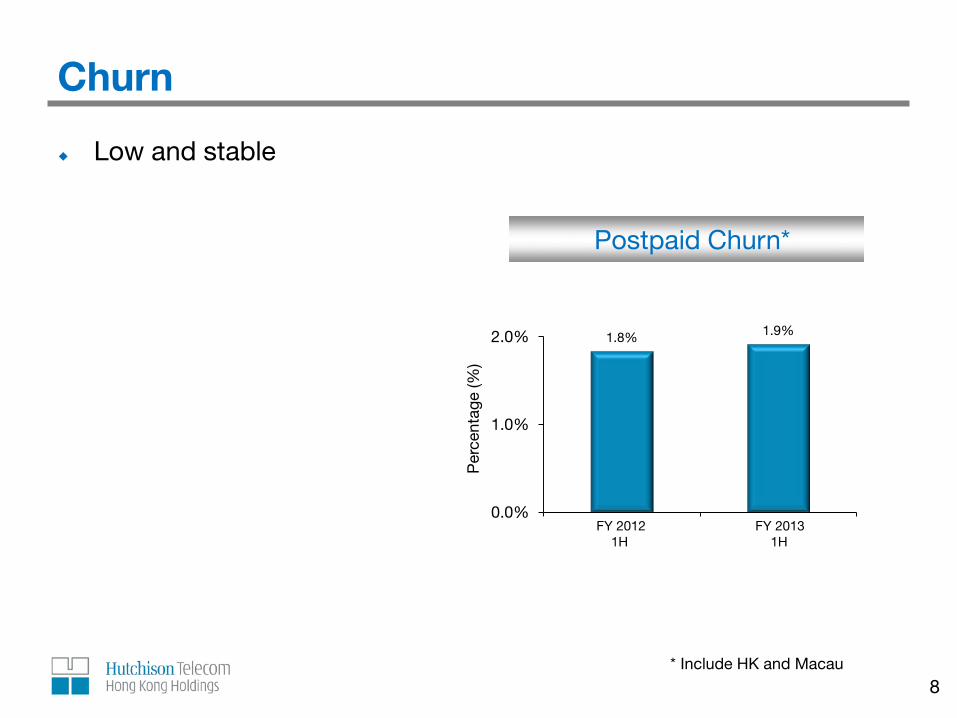

Churn

Low and stable

8 * Include HK and Macau

Postpaid Churn*

1.8% 1.9%

0.0%

1.0%

2.0%

FY 2012 1H FY 2013 1H

Per

cent

age

(%)

FY 2012 FY 2013 1H 1H

Fixed-line

10

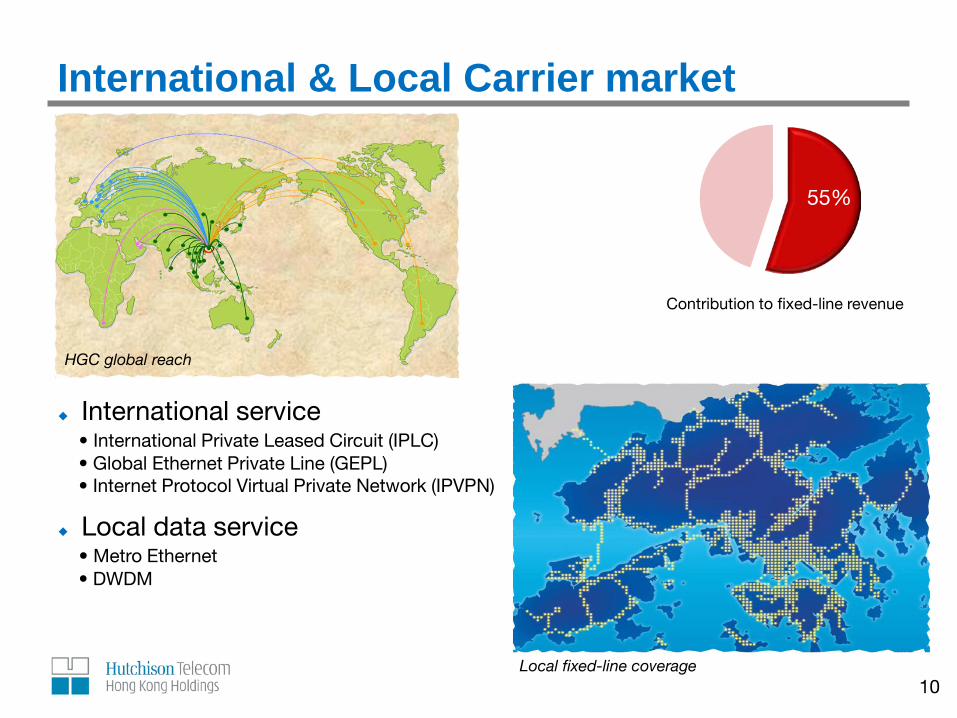

International & Local Carrier market

International service • International Private Leased Circuit (IPLC) • Global Ethernet Private Line (GEPL) • Internet Protocol Virtual Private Network (IPVPN)

Local data service • Metro Ethernet • DWDM

HGC global reach

Local fixed-line coverage

55%

Contribution to fixed-line revenue

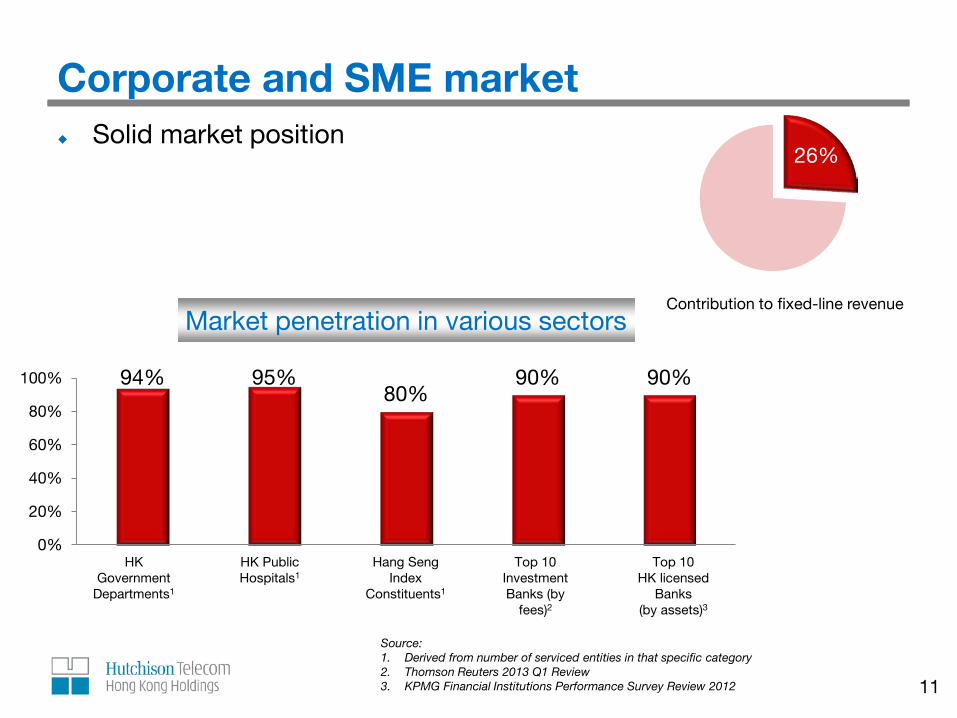

Corporate and SME market Solid market position

11

Market penetration in various sectors

94% 95% 80%

90% 90%

0%

20%

40%

60%

80%

100%

HK Government

Departments1

HK Public Hospitals1

Hang Seng Index

Constituents1

Top 10 Investment Banks (by

fees)2

Top 10 HK licensed

Banks (by assets)3

26%

Contribution to fixed-line revenue

Source: 1. Derived from number of serviced entities in that specific category 2. Thomson Reuters 2013 Q1 Review 3. KPMG Financial Institutions Performance Survey Review 2012

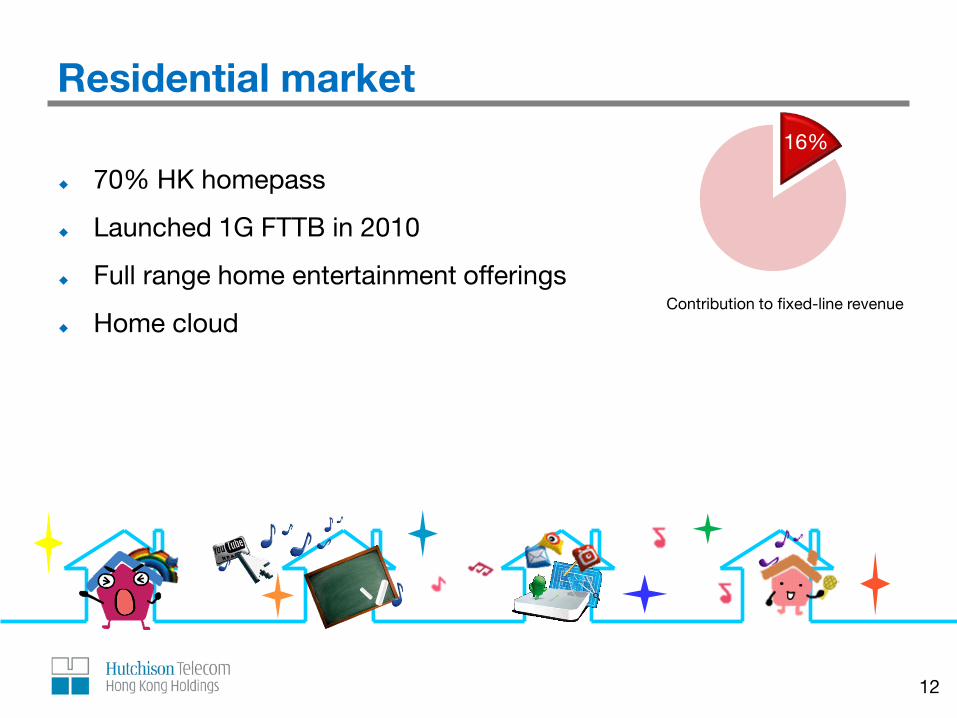

70% HK homepass

Launched 1G FTTB in 2010

Full range home entertainment offerings

Home cloud

12

Residential market 16%

Contribution to fixed-line revenue

Expertise in cloud computing

One-stop IT solution provider

Full range of cloud computing services

Collaboration with industry giants

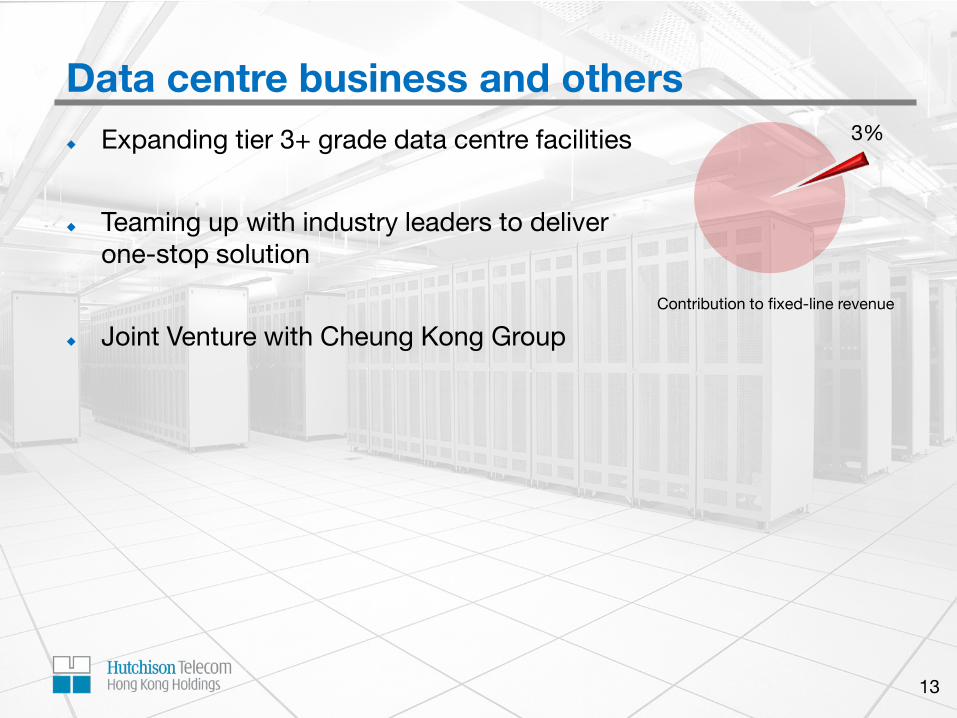

Expanding tier 3+ grade data centre facilities

Teaming up with industry leaders to deliver one-stop solution

Joint Venture with Cheung Kong Group

Data centre business and others

13

3%

Contribution to fixed-line revenue

Financial Overview

15

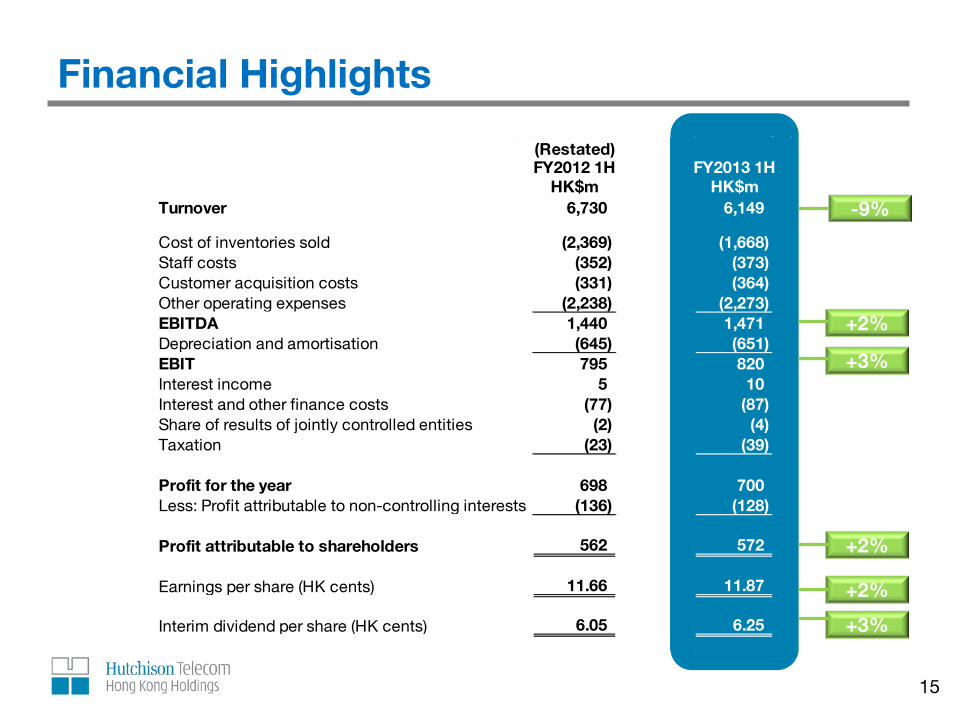

Financial Highlights

(Restated)FY2012 1H FY2013 1H

HK$m HK$mTurnover 6,730 6,149

Cost of inventories sold (2,369) (1,668) Staff costs (352) (373) Customer acquisition costs (331) (364) Other operating expenses (2,238) (2,273) EBITDA 1,440 1,471 Depreciation and amortisation (645) (651) EBIT 795 820 Interest income 5 10 Interest and other finance costs (77) (87) Share of results of jointly controlled entities (2) (4) Taxation (23) (39)

Profit for the year 698 700 Less: Profit attributable to non-controlling interests (136) (128)

Profit attributable to shareholders 562 572

Earnings per share (HK cents) 11.66 11.87

Interim dividend per share (HK cents) 6.05 6.25

-9%

+2%

+3%

+2%

+2%

+3%

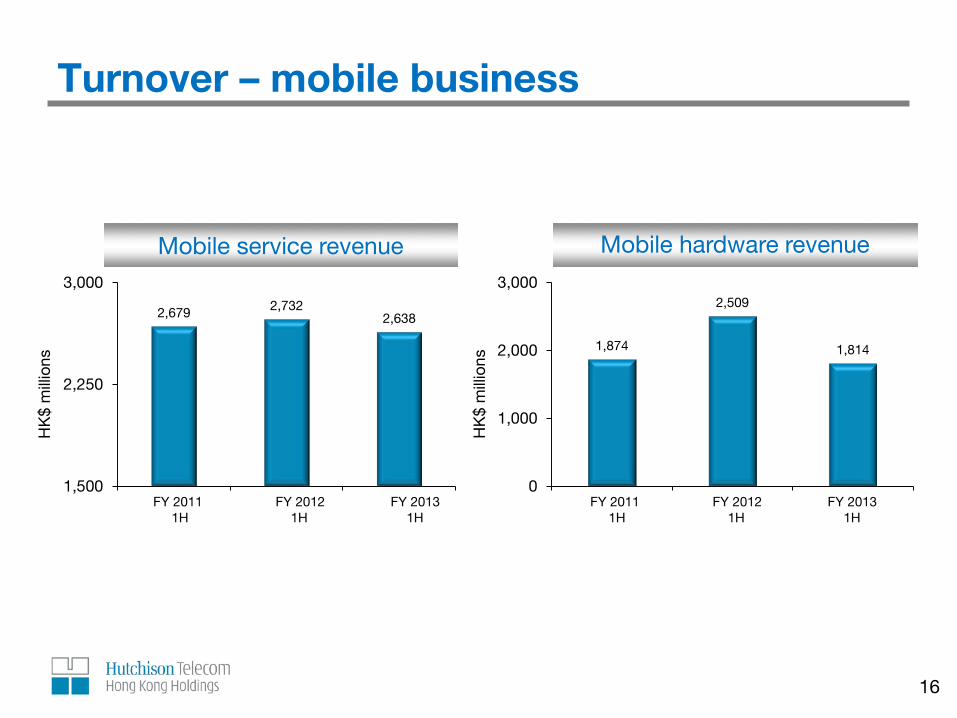

Turnover – mobile business

16

Mobile service revenue

2,679 2,732 2,638

1,500

2,250

3,000

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ m

illio

ns

FY 2011 FY 2012 FY 2013 1H 1H 1H

Mobile hardware revenue

1,874

2,509

1,814

0

1,000

2,000

3,000

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ m

illio

ns

FY 2011 FY 2012 FY 2013 1H 1H 1H

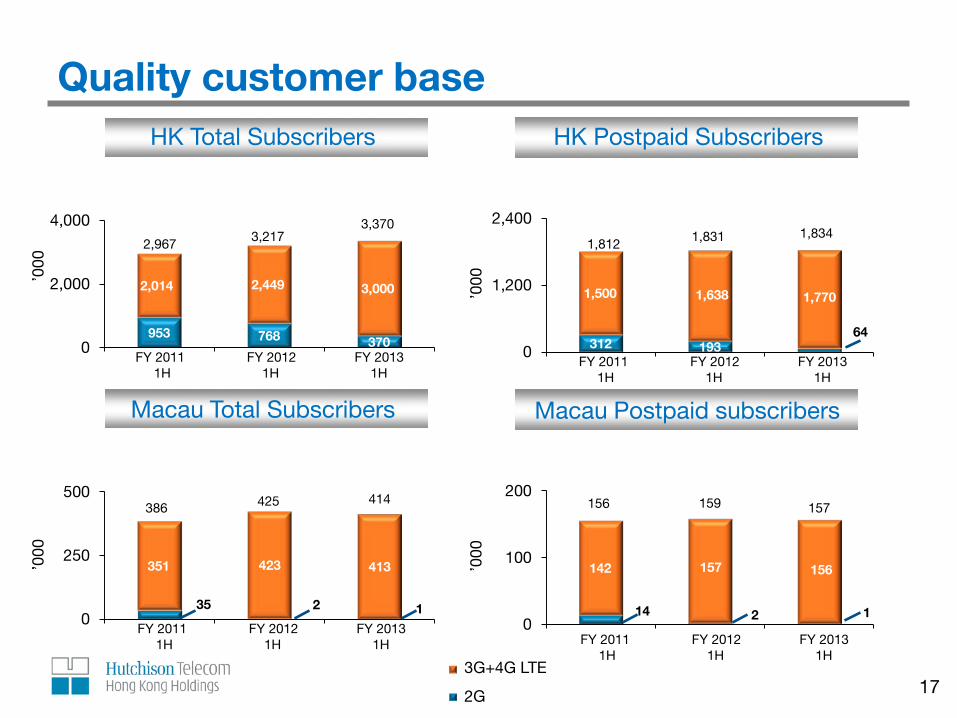

Quality customer base

17

1,519 1,761

2,014

All percentages represent compound annual growth rate

3G+4G LTE

2G

953 768 370

2,014 2,449 3,000

0

2,000

4,000

FY 2011 1H FY 2012 1H FY 2013 1H

’000

2,967 3,217 3,370

HK Total Subscribers

FY 2011 FY 2012 FY 2013 1H 1H 1H

312 193 64

1,500 1,638 1,770

0

1,200

2,400

FY 2011 1H FY 2012 1H FY 2013 1H

’000

1,812 1,831 1,834

HK Postpaid Subscribers

FY 2011 FY 2012 FY 2013 1H 1H 1H

35 2 1

351 423 413

0

250

500

FY 2011 1H FY 2012 1H FY 2013 1H

’000

386 425 414

Macau Total Subscribers

FY 2011 FY 2012 FY 2013 1H 1H 1H

14 2 1

142 157 156

0

100

200

FY 2011 1H FY 2012 1H FY 2013 1H

’000

156 159 157

Macau Postpaid subscribers

FY 2011 FY 2012 FY 2013 1H 1H 1H

Turnover – mobile service revenue

1H FY 2012

Residential 20%

Total service revenue: HK$2,732m

Total service revenue: HK$2,638m

Local non-data

31%

Roaming non-data

17%

Roaming data

10%

Local data 42%

Total Data Revenue: 52%

Local non-data

40%

Local data

37%

Roaming Voice 15%

Total Data Revenue: 45%

Roaming data 8%

1H FY 2013

18 * Data service revenue is defined as customer payment for internet and data access services, excluding messaging, content and related services.

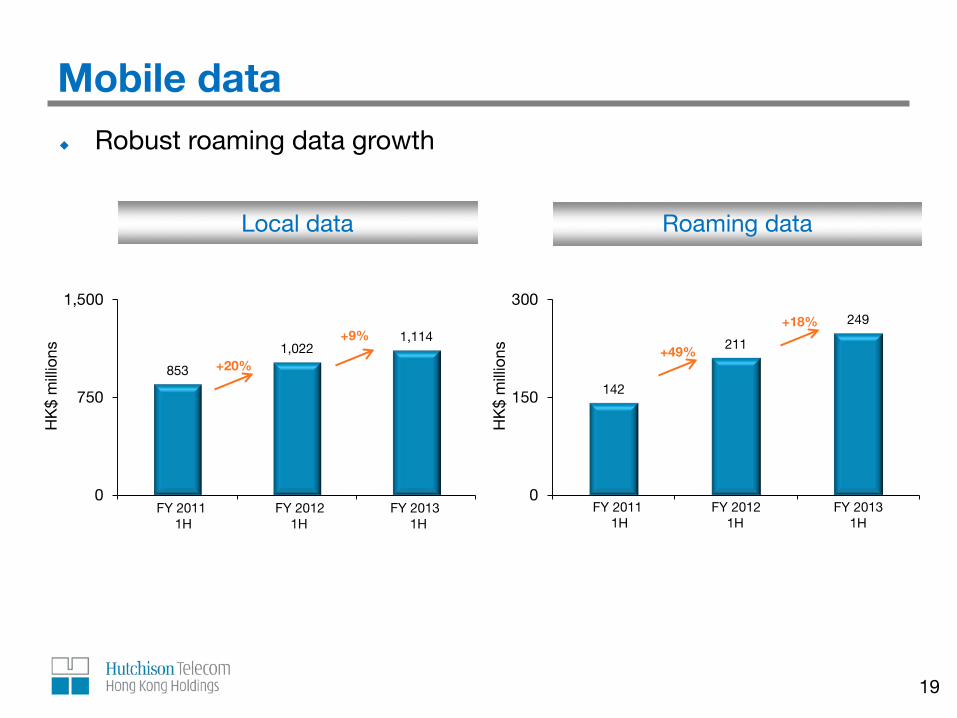

Mobile data

19

Robust roaming data growth

Roaming data

142

211

249

0

150

300

FY 2011 1H FY 2012 1H FY2013 1HH

K$

mill

ions

Local data

853

1,022 1,114

0

750

1,500

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ m

illio

ns

FY 2011 FY 2012 FY 2013 1H 1H 1H

FY 2011 FY 2012 FY 2013 1H 1H 1H

+20%

+9% +49%

+18%

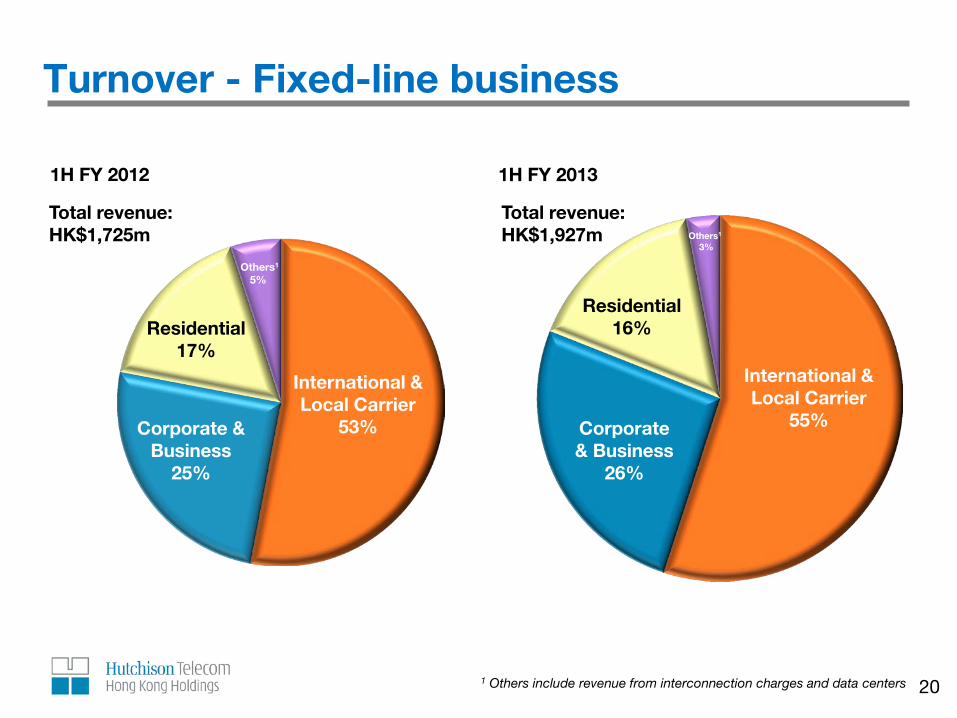

International & Local Carrier

55%

Others1 3%

Residential 16%

Corporate & Business

26%

International & Local Carrier

53%

Others1 5%

Residential 17%

Corporate & Business

25%

Turnover - Fixed-line business

20 1 Others include revenue from interconnection charges and data centers

1H FY 2012

Total revenue: HK$1,725m

Total revenue: HK$1,927m

1H FY 2013

21

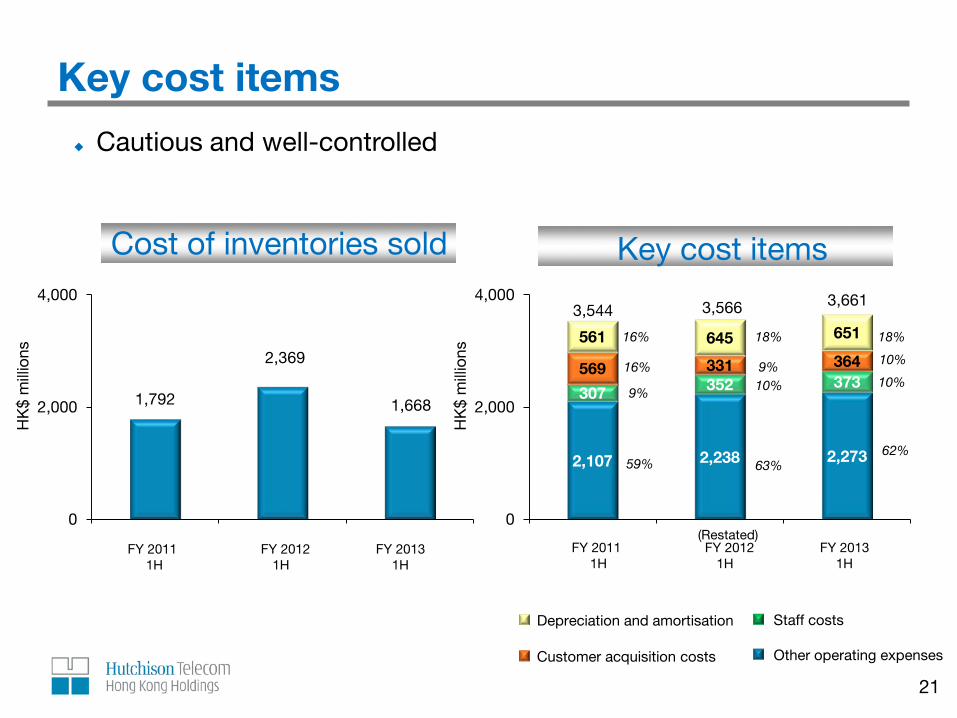

Key cost items

Cautious and well-controlled

65.0%

65.3% 64.9%

2,107 2,238 2,273

307 352 373 569 331 364

561 645 651

0

2,000

4,000

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ m

illio

ns

3,544 3,566 3,661

Key cost items

Customer acquisition costs

Staff costs

Other operating expenses

Depreciation and amortisation

1,792

2,369

1,668

0

2,000

4,000

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ m

illio

ns

Cost of inventories sold

16%

16%

9%

59%

18%

9% 10%

63%

FY 2011 FY 2012 FY 2013 1H 1H 1H

FY 2011 FY 2012 FY 2013 1H 1H 1H

18%

10%

10%

62%

(Restated)

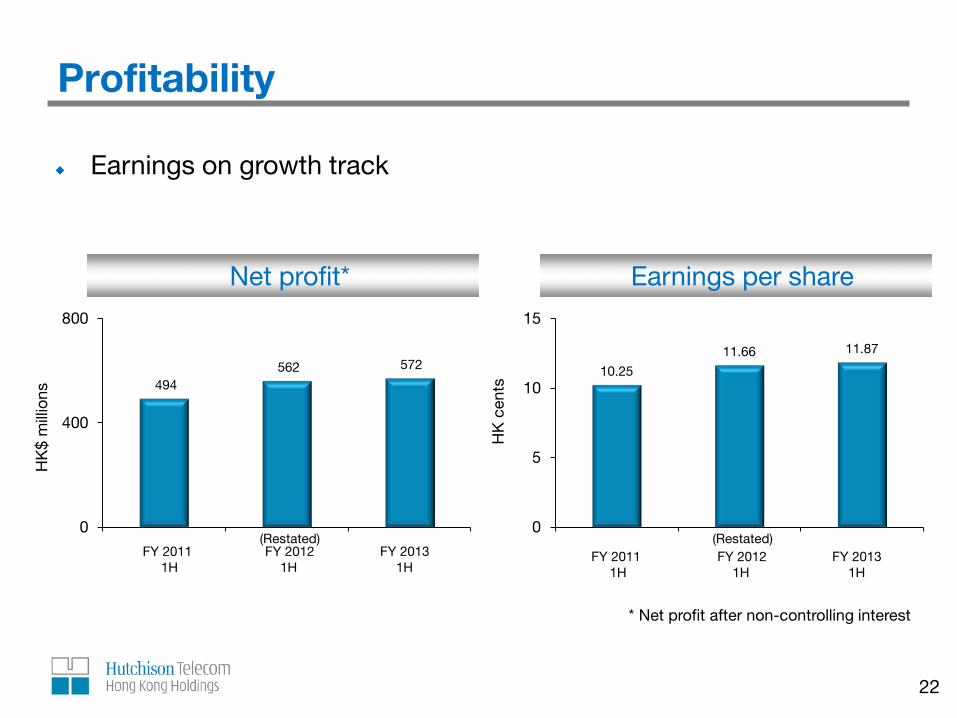

Profitability

22

Earnings on growth track

494 562 572

0

400

800

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ m

illio

ns

Net profit*

10.25

11.66 11.87

0

5

10

15

FY 2011 1H FY 2012 1H FY 2013 1H

HK

cen

ts

Earnings per share

* Net profit after non-controlling interest

FY 2011 FY 2012 FY 2013 1H 1H 1H

FY 2011 FY 2012 FY 2013 1H 1H 1H

(Restated) (Restated)

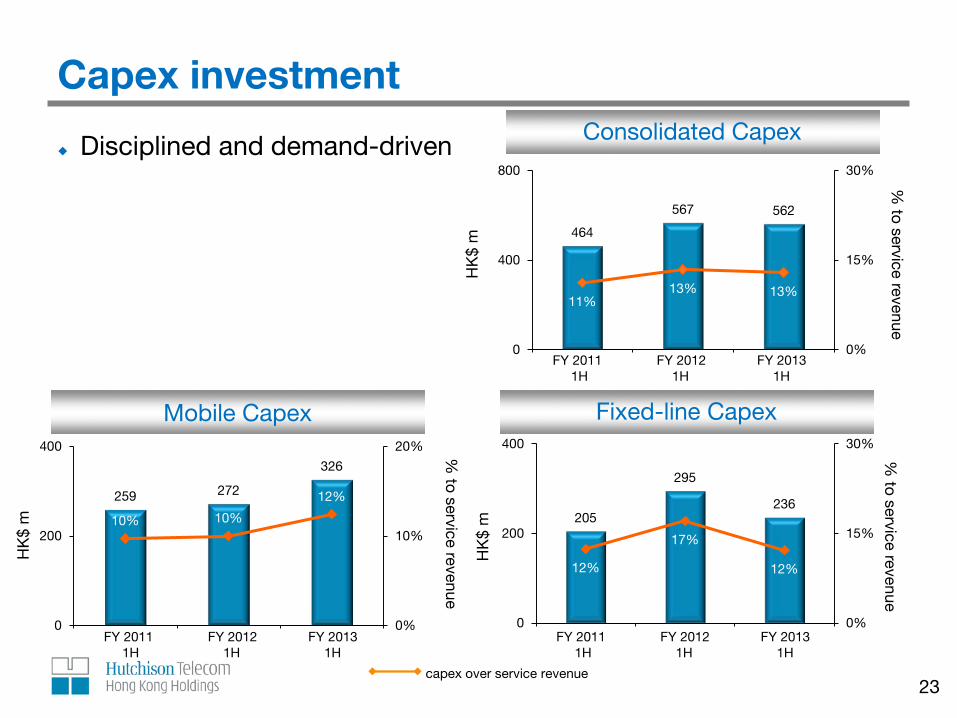

Capex investment

1 Excluding revenue from sale of telecommunications hardware

Mobile Capex

259 272

326

10% 10%

12%

0%

10%

20%

0

200

400

FY 2011 1H FY 2012 1H FY 2013 1H

% to service revenue

HK

$ m

15.5%

Disciplined and demand-driven

13.6%

Consolidated Capex

464

567 562

11% 13% 13%

0%

15%

30%

0

400

800

FY 2011 1H FY 2012 1H FY 2013 1H

% to service revenue

HK

$ m

Fixed-line Capex

205

295

236

12%

17%

12%

0%

15%

30%

0

200

400

FY 2011 1H FY 2012 1H FY 2013 1H

% to service revenue

HK

$ m

23

FY 2011 FY 2012 FY 2013 1H 1H 1H

FY 2011 FY 2012 FY 2013 1H 1H 1H

FY 2011 FY 2012 FY 2013 1H 1H 1H

capex over service revenue

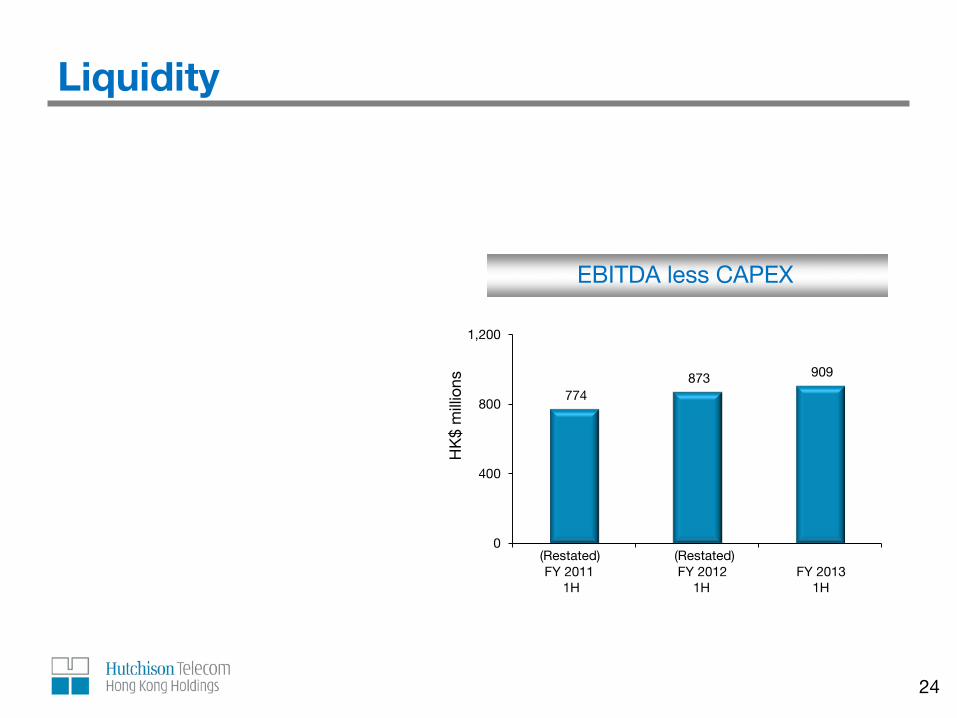

Liquidity

24

EBITDA less CAPEX

774 873 909

0

400

800

1,200

FY 2011 1H FY 2012 1H FY 2013 1H

HK

$ m

illio

ns

FY 2011 FY 2012 FY 2013 1H 1H 1H

(Restated) (Restated)

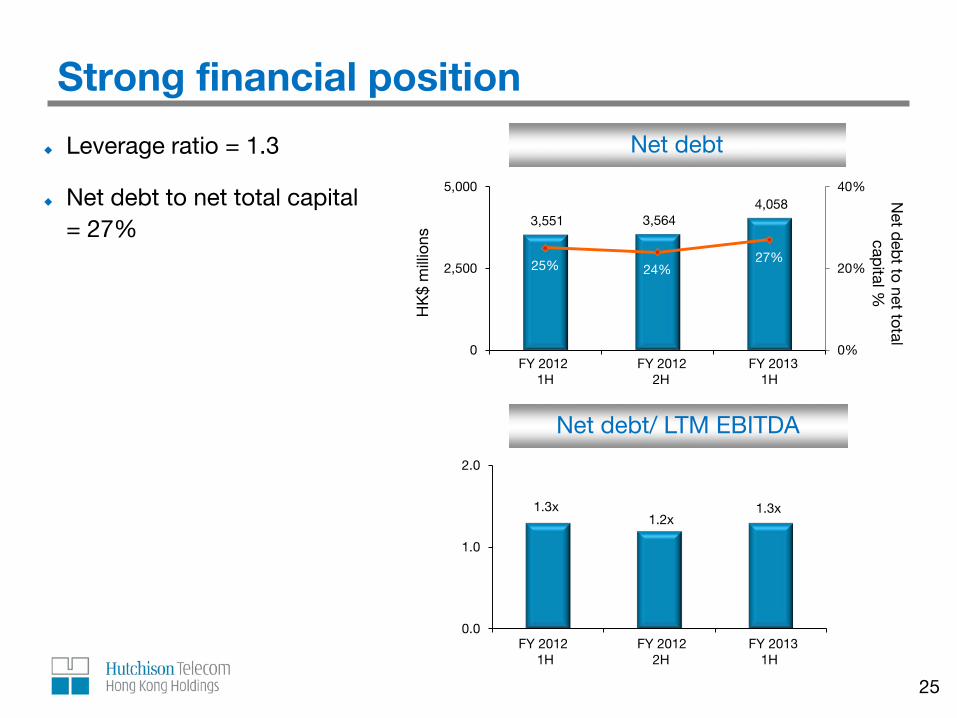

Strong financial position

25

Leverage ratio = 1.3

Net debt to net total capital = 27%

Net debt

3,551 3,564 4,058

25% 24% 27%

0%

20%

40%

0

2,500

5,000

FY 2012 1H FY 2012 2H FY 2013 1H

Net d

ebt to net total

capital %

HK

$ m

illio

ns

Net debt/ LTM EBITDA

0.0

1.0

2.0

FY 2012 1H FY 2012 2H FY 2013 1H

1.3x 1.2x

1.3x

FY 2012 FY 2012 FY 2013 1H 2H 1H

FY 2012 FY 2012 FY 2013 1H 2H 1H

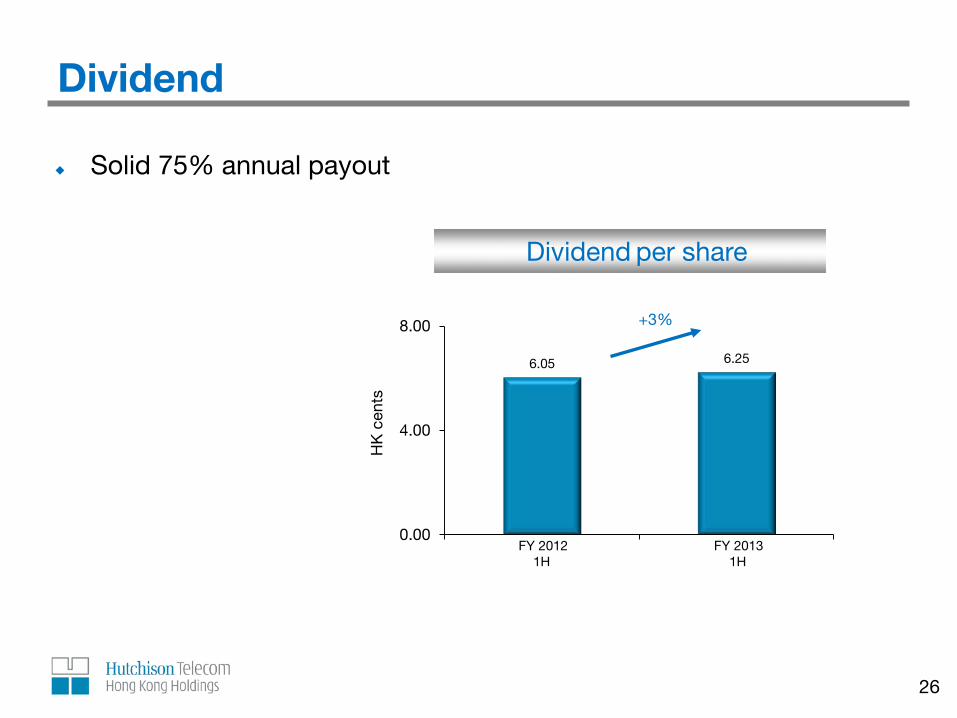

6.05 6.25

0.00

4.00

8.00

FY 2012 1H FY 2013 1H

HK

cen

ts

Dividend

26

Solid 75% annual payout Dividend per share

+3%

FY 2012 FY 2013 1H 1H

Forward

Outlook Group

Best positioned as an integrated operator in HK

Solid foundation to foster growth

Disciplined network investment

Increase returns for shareholders

Mobile

Embracing technology

Customer focus

Valued-added product development

Fixed-line

Further collaboration with overseas carriers and leading ICT players

Solution-based IT service provider

Full range residential multimedia offerings

28

Q & A

Thank You