Hunting Elephants in East Africa’s Rift Basins · Hunting Elephants in East Africa’s Rift...

31

1 A Lundin Group Company Hunting Elephants in East Africa’s Rift Basins May 2012

Transcript of Hunting Elephants in East Africa’s Rift Basins · Hunting Elephants in East Africa’s Rift...

1A Lundin Group Company

Hunting Elephants in East Africa’s Rift Basins May 2012

2

Exploring in Four Major Rift Systems

Africa Oil Assets

• Tertiary rifts (Kenya & Ethiopia)

• Cretaceous rifts (Kenya, Mali)

• Jurassic rifts (Puntland‐Somalia)

• Permo‐Triassic rifts (Ethiopia)

All of AOC plays are extensions of proven multi‐billion barrel rifts

*

East African extensions of these proven rift trends highly under‐explored

EUR

Regional oil resource volumes are sourced from government, industry and company websites. Readers are cautioned that the y p yfigures are not reported in accordance with NI51-101 policy.

*Lake Albert Oil Fields: 1.0 BBO Discovered + 1.4 BBO Potential

3

Play Summary• Have assembled massive acreage position of 300,000 sq km (74 MM acres) in 4 distinct rift related petroleum systems with billion barrel potential

• Completing seismic and FTG programs on all blocks in preparation for aggressive drilling program

• Currently have two rigs under contract and investigating bringing in two additional rigs

• First two wells in program have made two apparently significant oil discoveries in Kenya and Somalia

• Strong balance sheet with $109 MM cash (Dec. 2011) that will fund activities through 2012

4

Tullow Partnership in Tertiary and Cretaceous Rift Trend

• Tullow farmed into AOC blocks in 2010 and now operates blocks outlined in red.

& O• Tullow & partners have discovered 1.1 BBO (discovered) + 1.4 BBO (potential) in the Lake Albert region, and did so with greater than 90% success rate90% success rate.

• Tullow brings :– Experience of Lake Albert exploration

T l t d l ti l– Talented exploration personnel– In-house seismic processing expertise– Drilling expertise and staff

A t th U d t i li– Access to the Uganda export pipeline

5

Tertiary Rift Exploration Block 10BB, 10BA, 12A, 13T in KenyaSouth Omo and Rift Valley Study Blocks in Ethiopia

• New Ngamia Discovery extends• New Ngamia Discovery extends the Lake Albert Play into the Lake Turkana area *

• Similar size to entire North Sea Graben system

• Over 80 prospects & leads mapped from seismic and FTG

*Lake Albert Oil Fields: 1.1 BBO Discovered + 1.4 BBO Potential

6

Kenya Block 10BB/13T – Lockichar Sub BasinNgamia‐1Ngamia 1

Lead ‘E’

• AOC: 50% working interest

Twiga N.

K i• Ngamia Discovery confirms petroleum system previously tested by Shell Loperot‐1 (1992)

N i il i il U d il

Kongoni

• Ngamia oils similar to Ugandan oils

• Numerous identical prospects along trend now de‐risked20 km

• Lockichar Sub‐Basin similar in scale to Albert Graben of Uganda with estimated resources of 1.1 BBO (discovered) + 1.4 BBO (potential)

Prospects Seismic LeadsFTG Leads

7

Block 10BB Ngamia Prospect: “Play opener”Line LOK-10-24

Ngamia DiscoveryDip Line

Strike Line KongoniKongoni--AA

Analogous to Tullow Lake Albert Discoveries; Kingfisher, Mputa, Waraga

8

Waraga, Lake Albert Uganda Analogue: “Tullow Play Opener”

Waraga‐1

DST 33,650 bopd (1” choke)

Flowed 12,050 BOPDWaraga-1• Downthrown trap like Ngamia

• Flowed more than 12,050 BOPD Waraga 1

15.4m net pay

DST 2

(1 choke)33.80 API

0.5 Sec

6.7m net pay

DST 24,200 bopd (1” choke)33.80 API

1 Sec

DST 14,200 bopd (1” choke)33.80 API

3 R i Z4.6m net pay

3 Reservoir Zones27m net pay12,050 BOPD

2.5 kmBasement

Figure from TullowFigure from Tullow

9

Ngamia-1 Well ResultsGeneralized Stratigraphy

0Meters

Generalized Stratigraphy

• Oil in Miocene Sandstones

• Porosities from logs: 23-29% SWC’s500

Volcanics

Meters

Porosities from logs: 23-29%, SWC s indicate good porosity

• Gross Reservoir Section: 650 m (~2,132 ft)1000

Upper Miocene

Sandstones 855m

• Net Pay greater than 100 m

• Oil recovered to surface from four sampled intervals1500

Upper Lokhone

Sandstones

Current1500m

sampled intervals

• Oil quality greater than 30o API

• Pressure data confirms multiple oil pools2000L

Lokhone Shale

Current TD

1510m

Pressure data confirms multiple oil pools

• Drilling ahead to lower objectives

2500

Lower Lokhone

SandstoneLower

Objective

2500

2700ProjectedTotal Depth

10

Lockichar String of Pearls

• Prospects extending more than 100 km along trend

• Currently acquiring 700 km 2D

Lokichar Basin

• Currently acquiring 700 km 2D infill seismic

• Twiga-1 to spud 2H 2012Twiga-1

20 km

Prospects Seismic LeadsFTG Leads

50 km

11

Another Key Prospect on Block 10BB –Kamba ProspectKamba Prospect

SW NEKamba Prospect

P50

P10KAMBA PROSPECT

Depth Structure, CI: 20m

P10

• Along trend of shallow drilling program Internal Estimated Resource (gross 100%):

5 KM5 KM

• Large structure: 60 km2 (15,000 ac) & 700 m vertical relief

• Stacked Tertiary Sandstone Reservoirs, 10-18% Porosity• P50: 200 MMBO

• P10: 750 MMBO

12

Block 10BA - Northern String of Pearls• AOC: 50%WIAOC: 50% WI

• Block centered on Lake Turkana

• Loose grid of legacy seismicSouth Omo Block, ET

• Oil slicks observed in satellite imagery

• FTG complete, 1,350 km 2D seismic underwayTurkana

Western Shore Play

• First well spuds 2H‐2013

• Would prove up another ‘Ngamia‐type’ sub‐basin

FaruChui TwigaNdovuN SNgamia Play

25km

13

South Omo Block - Northern String of Pearls cont.South Omo Block Northern String of Pearls cont.• AOC 30% WI, Tullow Operates with 50%

South Omo • Extension of Tertiary rift trend north of Lake TurkanaPlanning

Seismic

2012 W ll• Unexplored, no previous seismic or wells

FTG l t d

2012 Well

• FTG completed

• Acquiring 1000 km 2D seismic, additional 20 km700km planned for 2012

• First well to spud in Q4, 2012

ProspectsSeismic LeadsFTG Leads

Lake Turkana

p ,

14

Cretaceous Rift Exploration Block 10A and 9 in KenyaBlocks 7 and 11 in Mali

• Over 6 billon barrels of oil discovered l d i S d i i il l ialong trend in Sudan in a similar geologic

setting

E l ll i Bl k 9 &10A t d• Early wells in Blocks 9 &10A encountered thick sequences of sandstones with oil and/or gas shows

• Trap-definition required newer seismic, 1500 km 2D acquired in 2011

• One well planned in each block within the next 18 months

15

Block 10A

•AOC 30% WI, Tullow 50% WI (Operator)

ProspectsSeismic Leads

•3 wells drilled in the 80’s by Amoco

W ll t d id l il t i i•Wells encountered residual oil staining over thousands of feet, free oil recovered to surface in Sirius‐1Paipai‐

Spud 2H, 2012

•Trap failure, trap definition?

•Acquired 750 km 2D seismic and FTG

Lake Turkana

Acquired 750 km 2D seismic and FTG survey to improve trap definition

•Pai Pai prospect to spud 2H 2012Pai Pai prospect to spud 2H 2012

25km

16

Regional Seismic line- Pai Pai Prospect

Maikona formation MiocenePliocene Volcanics

Recent Play LakePaipai Prospect Bellatrix-1Sirius-1

Maikona formation Miocene

Upper CretaceousLower Tertiary

Volcanics

Jurassic?

Lower Cretaceous

Basement

Internal Estimated Gross Resources:P10: 287 MMBOP50: 116 MMBOPaipai-1

• Located in the basin with less exposure to Tertiary faulting.Located in the basin with less exposure to Tertiary faulting.• Will test Cretaceous sandstones in a large anticlinal trap.Prospects

Leads 25km

17

Block 9

Tertiary Play

3D Residual Gravity

• AOC 100%Ndovu

Kaisut Sub Basin

Play

• AOC 100%

• Cretaceous Oil‐prone play extending from Sudan

• Acquired 750 km 2D in oil‐prone Kaisut Sub‐basin

Pundamilla

‐Oil prone‐

• Kinyonga prospect to spud in 2013

• Extension of Tertiary Play along graben edgeBogal

Gas Discovery

Kinyonga‐Spud 2013

25km• Studying commercialization of 2010 Bogal Gas Discovery,

~2‐3 TCF of prospective gas resources

25km

18

Kiyonga Prospect-Block 9

60 SQ KM 4‐WAYCLOSURE

Kinyonga Prospect

MetresSW NE

Kinyonga Prospect

5km

Time Structure

Metres

Tertiary Play

Internal Estimated Gross Resources:

Tertiary-Cret. Unconformity

Tertiary Mrkr2

Tertiary Mrkr1

Internal Estimated Gross Resources:250‐1,200 MMBO RecoverableMean: 750 MMBO

Tertiary-Cretaceous U f itUnconformity

Basement

Play/Trap Types

19

Bogal Gas Discovery• Bogal-1 Gas Discovery drilled in 2010Depth Structure Near Top Cretaceous Gas Sands Bogal 1 Gas Discovery drilled in 2010

• Gas bearing Cretaceous Sandstones: 3150-3285 m

p p

• 28m net gas pay with >8% porosity

• DST’s in Jurassic were tight, Cretaceous untested

10 k10 km

Cretaceous Gas Reservoirs

Jurassic

• Large Structure (>260 sqkm; 65,000 acres)

• Bogal-1 at edge of closureJurassic

Volcanics• Est. Recoverable Gas Resources:

1 to 4.5 TCF

Mean: 2.5 TCF

20

Kenyan Energy Market

16000

18000

20000

Kenya Total Primary Energy Supply

Geothermal/Wind 6%,

8000

10000

12000

14000

ktoe

Biomass 77%

0

2000

4000

6000 Hydro 1%

Oil 16%

Source: IEA, 2010

• Energy demand growth is ~5% per yearThe majority is met by traditional sources (burning wood) which is deforesting Kenya– The majority is met by traditional sources (burning wood), which is deforesting Kenya.

– Imported oil is second, but negatively impacts foreign exchange balances

• Bogal Gas could compete w/ all other imported energy (ET hydro, TZN gas, etc.)Bogal Gas could compete w/ all other imported energy (ET hydro, TZN gas, etc.)• A 2-3 TCF gas field could supply Kenya with ~2000 MW (gas to power) for 15 years• Kenya’s installed capacity is ~1400 MW, so impact would be material!

21

Jurassic Rift Exploration Dharoor and Nugaal Blocks in Puntland, SomaliaAdigala Block in Ethiopia

• Prolific, proven play in Yemen expected to extend into Puntland, which shares a common geologic history

*

• Yemen fields produce from high-quality Cretaceous and Jurassic

i d kreservoirs and source rocks

• First well in Dharoor Block (drilling) encountered shows and(drilling) encountered shows and possible net pay in Cretaceous sandstones

• Second well to spud mid 2012*Lake Albert Oil Fields: 1.1 BBO Discovered + 1.4 BBO Potential

New Puntland Focused VehicleDEAL

• Share exchange agreement between AOC and Denovo (HornPetroleum Corporation)

• AOC transfer of its 60% interest in both Dharoor and Nugaal

FINANCING

• AOC put in $10 MM cash and additional $31 MM raised• Proceeds to fund the drilling of two wells in PuntlandProceeds to fund the drilling of two wells in Puntland

OWNERSHIP

• AOC holds approximately 50% of Horn Petroleum

PROFILE

• 74.8 million shares outstanding/122.3 million fully diluted• Horn Petroleum listed on TSXV

60% ki i t t i N l d Dh il l ti• 60% working interest in Nugaal and Dharoor oil explorationprojects in Puntland, Somalia

• Service contract with AOC to provide technical, operational andfinancial supportfinancial support

• President: David Grellman; Directors: Keith Hill, Ian Gibbs

Dharoor Block, Puntland DARIN‐1

SHABEEL NORTH

• Shabeel-1 spud in January 2011, and is testing a large anticlinal structure.

SHABEEL

• Shabeel North Prospect will spud mid-2012 and will test a large fault-bounded closure.

Turonian

SW NEMeters

SHABEEL‐1 SHABEEL NORTH Line AOC-08-052 DHAROOR BLOCKTURONIAN DEPTH M

CI= 50 METRES0 10 KM

Cret Mrkr

L Cret Carb

MJ Uncf

Resource Estimates Pre‐Drill (internal estimates)

~300 MMBO range Rig on Shabeel-1 location

24

Shabeel-1 Well ResultsCretaceous Jesomma Sandstones

MetersQr

Rate of H i G C1 C

Generalized Stratigraphy

500

Taleh

A d

Terti

ary

Rate of Penetration

Hotwire Gas C1-C5

1000 Auradu

1500

Cretaceous

Tisje

Jesomma

2000

Gumburo Lst

• Oil shows in Cretaceous Sandstones 2500

etac

eous

• Gross Section: 150 m (~490ft)•• 12-20 m Possible Net Pay (Mud & Elogs)

Qishn Age?

3000

Cre

• Shows in deeper sandstones (drilling)3500

TDBas

emen

t

Triassic

Current TD

3300M

25

Community Development and National Initiatives

FOOD SECURITY •Five‐year partnership with FARM AFRICA on long‐term livestock and agriculture; access to improved inputs, micro‐irrigation, VSL, livestock and veterinary services•Investments in improved seed production/distribution, micro‐loan fund for smallholder farmers

WATER •Partnership with AMREF to provide potable water to vulnerable pastoralist populations

HEALTH •Funding Intensive Care Unit and MCM Hospital in Addis•Establishment of Advanced Rural Nursing program (Aga Khan University)University)•Investment in rural health franchise enterprise

EDUCATION •Funding primary schools and income‐generating activities•Establishment of Africa’s first Management Case Study Development Centre (Aga Khan University)

CD projects include:• School rehabilitationB F dCD projects must have:

• Religious neutrality• Sustainability• Local content

• Bursary Fund• Farm tools• Birkahs (water storage)• Human health postsM di i f li t k• Potential for capacity building

• High Impact relative to cost• Political neutrality

• Medicines for livestock• Support for hospitals• Solar lights/cookers

26

World Class Potential in Multiple Petroleum Systems

Africa Oil CorpSummary of Unrisked and Undiscovered Oil Prospective Resources1

Current Working InterestsGeographic Region

PSC/PSA Operator Gross Best Estimate(MMBbl)

AOC Working Interest

Net Best Estimate(MMBbl)(MMBbl) Interest (MMBbl)

Kenya2 10BB Tullow 2,066 50.0% 1,033

Kenya2 9 AOI 1,399 100.0% 1,399

Kenya2 10A Tullow 423 30.0% 127

• Resource estimates for 13T, 12A & South Omo not included in Dec 2010

• Resource estimates for 13T, 12A & South Omo not included in Dec 2010

Ethiopia2 7&8 AOI 155 55.0% 85

Kenya3 10BA Tullow 2,188 50.0% 1,094

Puntland (Somalia)4 Nugaal AOI 4,083 30% 5 1,225

Puntland (Somalia)4 Dharoor AOI 1,210 30% 5 363

report• Currently revising with

expected completion in Q3 2012

report• Currently revising with

expected completion in Q3 2012

( ) , 5

11,524 5,326

1 This summary table was prepared by Company management for the convenience of readers.2 Please refer to the Company’s press release dated March 29, 2011 for details of the prospective resources by prospect and lead, including the geologic chance of success.3 Please refer to independent resource evaluation report, dated January 1, 2010 posted on February 11, 2010 at www.sedar.com under Centric Energy Corp.4 Please refer to independent resource evaluation report effective June 30 2011 posted on Sept 2 2011 at www sedar com under Denovo Capital Corp4 Please refer to independent resource evaluation report, effective June 30, 2011, posted on Sept. 2, 2011 at www.sedar.com under Denovo Capital Corp.5 Transaction with Denovo Capital Corp. provides AOC with ~50% ownership of Denovo, who holds 60% working interest in Puntland Blocks.

There is no certainty that any portion of the resources will be discovered. If discovered, there is no certainty that the discovery will be commercially viable to produce any portion of the resources.Net Prospective Resources are stated herein in terms of the Company’s net working interest in the properties. Due to the very immature nature of these Prospective Resources, have not been computed as net entitlement volumes under the PSAs/PSCs. In this regard the volumes stated herein will exceed the volumes which will arise to AOC under the terms of the PSAs/PSCs.

27

Size of the Prize

Prospective Resources Net Best Estimate

(MMbbl)

Indicative Risk Factor

Risked Potential Prospective Resources

(MMbbl)

Potential Value($MM)( ) ( ) ($ )

5,326 20% 1,065 4,506

10% 533 2,253

• Recently completed East African sale transaction:H it l f i t t i U d L k Alb t (Bl k 1 & 3A) t T ll

1% 53 225

– Heritage sale of interest in Uganda Lake Albert (Blocks 1 & 3A) to Tullow– 355 Mmboe mean working interest contingent resource sold– $1.5 billion transaction value– $4 23/boe$4.23/boe

The above summary table was prepared by the Company for the convenience of readers.

There is no certainty that any portion of the resources will be discovered. If discovered, there is no certainty that the discovery will y y p y ybe commercially viable to produce any portion of the resources.

Net Prospective Resources are stated herein in terms of the Company’s Working Interest (WI) in the properties and, due to thevery immature nature of these resources, have not been computed as net entitlement volumes under the PSAs. In this regard, the volumes stated herein will exceed the volumes which will arise to AOC under the PSA terms.

28

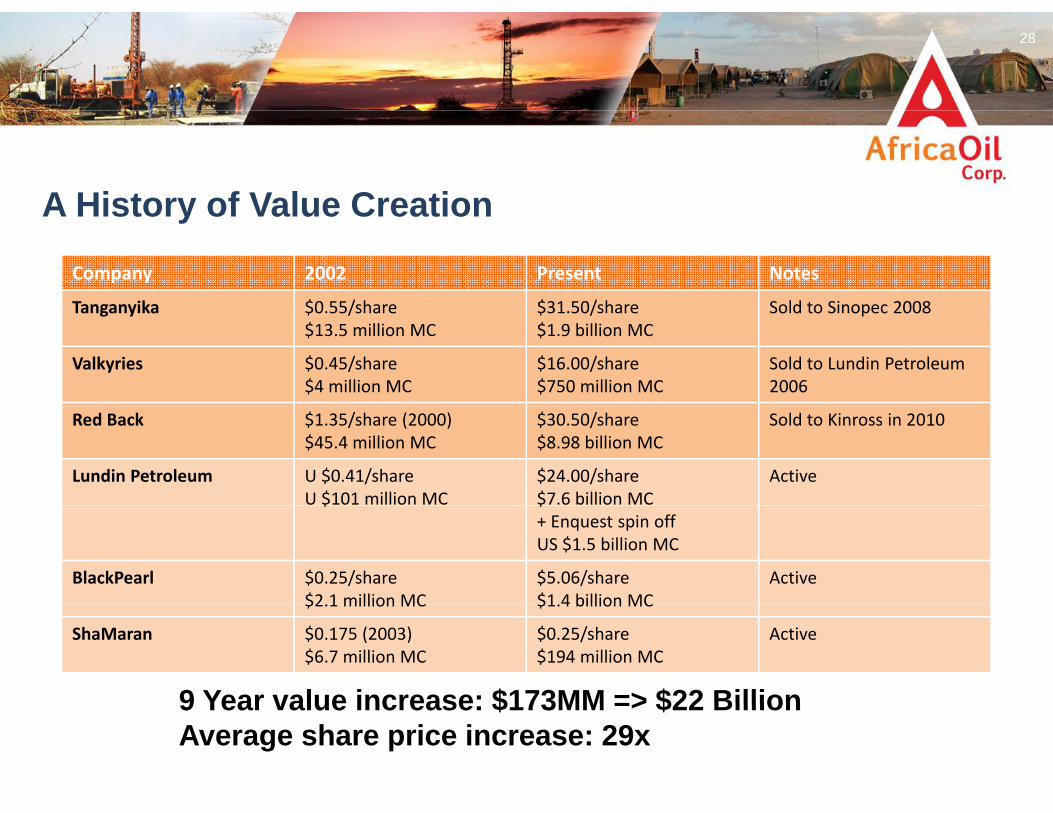

A History of Value CreationA History of Value Creation

Company 2002 Present Notes

Tanganyika $0 55/share $31 50/share Sold to Sinopec 2008Tanganyika $0.55/share$13.5 million MC

$31.50/share$1.9 billion MC

Sold to Sinopec 2008

Valkyries $0.45/share$4 million MC

$16.00/share$750 million MC

Sold to Lundin Petroleum 2006

Red Back $1.35/share (2000)$45.4 million MC

$30.50/share$8.98 billion MC

Sold to Kinross in 2010

Lundin Petroleum U $0.41/shareU $101 million MC

$24.00/share$7.6 billion MC

Active$ $

+ Enquest spin off US $1.5 billion MC

BlackPearl $0.25/share$2 1 million MC

$5.06/share$1 4 billion MC

Active$2.1 million MC $1.4 billion MC

ShaMaran $0.175 (2003)$6.7 million MC

$0.25/share$194 million MC

Active

9 Year value increase: $173MM => $22 Billion9 Year value increase: $173MM => $22 BillionAverage share price increase: 29x

29

Summary • AOC has assembled a highly prospective East African portfolio that spans• AOC has assembled a highly prospective East African portfolio that spans

4 different proven petroleum provinces with multi-billion barrel potential

E i d t d t ff ith ffi i V C l• Experienced management and staff with offices in Vancouver, Calgary, Addis Ababa, Nairobi, and Bosasso

• Excellent partners, such as Tullow, to help fund exploration programs and guide/accelerate operational activities

• Continuous multi-rig program to drill 10-12 wells in the next 18 months

C lid t d b l h t i t $109MM h (D 2011)• Consolidated balance sheet is strong; $109MM cash (Dec, 2011)

Shares Outstanding: 218.6MM, Fully Diluted 228.7MM Market cap: ~ $1 7 BMarket cap: ~ $1.7 B Symbol: AOI – TSXV AOI – OMX Stockholmwww.africaoilcorp.com

30

AOI has a Strong Management TeamKeith Hill, President and CEOM Hill h 25 i i h il i d i l di i i l d i l i i i O id l P l d Sh ll Oil CMr. Hill has over 25 years experience in the oil industry including international new venture management and senior exploration positions at Occidental Petroleum and Shell Oil Company. His education includes a Master of Science degree in Geology and Bachelor of Science degree in Geophysics from Michigan State University as well as an MBA from the University of St. Thomas in Houston. Prior to his involvement with Africa Oil, Mr. Hill was President and CEO of Valkyries where he led the company through rapid growth and ultimately a highly successful $700 million takeover by Lundin Petroleum. In addition, Mr. Hill was one of the founding directors of Tanganyika Oil which was recently the subject of a $2 billion takeover by Sinopec International Petroleum.

J Philli COOJames Phillips, COOBefore joining Africa Oil, Mr. Phillips was Vice President Exploration‐Africa and Middle East for Lundin Petroleum AB where he played a pivotal role in securing the majority of Africa Oil’s current portfolio. Mr. Phillips is a graduate of the University of California, Berkeley and San Diego State University where he obtained BS and MS degrees, both in Geology. He has over 25 years of experience in the oil industry including senior positions with Shell Oil company and Occidental including heading up Oxy’s African exploration ventures.

Paul Martinez, VP ExplorationDr. Martinez, most recently Director of International Business Development with Occidental Petroleum Corporation, has over 20 years of domestic US and international senior management experience in oil and gas exploration and development, including projects in the Texas Gulf Coast, Permian Basin, Rockies, Latin America, Africa, Middle East, and Russia. He has held overseas management positions for Oxy in Libya, Oman and Peru. Dr. Martinez holds a doctorate in petroleum geology from Stanford University and a Bachelor of Science degree in geology from the University of Texas at Austin. Dr. Martinez is based in the Africa Oil Calgary technical office and is responsible for all geological and geophysical activities of the Company.

Gibb C OIan Gibbs, CFOIan Gibbs is a Canadian Chartered Accountant and a graduate of the University of Calgary where he obtained a bachelor of commerce degree. Ian Gibbs has held a variety of prominent positions within the Lundin Group of Companies; most recently as CFO of Tanganyika Oil Company Ltd. where he played a pivotal role in the recent $2 billion acquisition by Sinopec International Petroleum . Prior to Tanganyika, Mr. Gibbs was CFO of Valkyries Petroleum Corp which was the subject of a $700 million takeover.

David Grellman, VP OperationsDavid Grellman, VP OperationsMr. Grellman is General Management/Operations professional with a unique blend of technical and management skills combined with extensive operations experience in the upstream global oil and gas industry. Mr. Grellman spent the majority of his career at Occidental Oil and Gas Corporation as Exploration Manager or General Manager in numerous countries including the Philippines, Sri Lanka, China, Syria Albania and Pakistan.

Gary Guidry, DirectorMr Guidry brings to the Board of Africa Oil Corp an extensive background and proven track record in international petroleum development and project execution A Petroleum EngineerMr. Guidry brings to the Board of Africa Oil Corp. an extensive background and proven track record in international petroleum development and project execution. A Petroleum Engineer by training, he is an Alberta‐registered Professional Engineer with expertise in diverse environments ranging from deep‐water West Africa and the Gulf of Mexico, South American rainforests to the deserts of the Middle East. Most recently, Mr. Guidry was President of Tanganyika Oil Company Ltd. where he led the company from an early stage oil development project in Syria to a $2 billion takeover by Sinopec International Petroleum in late 2008.

31

Cautionary Statements

• This document contains statements about expected or anticipated future events and financial results that are forward-looking in nature and, as a result, are subject to certain risks and uncertainties, such as legal and political risk, civil unrest, general economic, market and business conditions, the regulatory process and actions, technical issues, new legislation, competitive and general economic factors and conditions the uncertainties resulting from potential delays or changesfactors and conditions, the uncertainties resulting from potential delays or changes in plans, the occurrence of unexpected events and management’s capacity to execute and implement its future plans. Actual results may differ materially from those projected by management.

• Regional resource and reserve references as resource information on other companies have been sourced from websites and other public information and may

t b t d t t t d i d ith NI 51 101not be accurate and are not stated in accordance with NI 51-101.