HUD Update: For-Profit Entities Subject to the HUD ... Governmental AuditQuality Center ASU 2015-03...

33

12/14/2016 1 HUD Update: For-Profit Entities Subject to the HUD Consolidated Audit Guide A Governmental Audit Quality Center Web Event December 15, 2016 Governmental Audit Quality Center Administrative Notes Please ensure your pop-up blocker is disabled. Note the interactive toolbar at the bottom of your screen. Download slides and materials by clicking this icon. Ask questions by entering your question in the “Q&A” box. Please click the “Help” and/or “Contact Us” at the bottom of your screen. Call AICPA Member Service at 888.777.7077. 2

Transcript of HUD Update: For-Profit Entities Subject to the HUD ... Governmental AuditQuality Center ASU 2015-03...

12/14/2016

1

HUD Update: For-Profit Entities Subject to the HUD Consolidated Audit Guide

A Governmental Audit Quality Center Web Event

December 15, 2016

Governmental Audit Quality Center

Administrative NotesPlease ensure your pop-up blocker is disabled.

Note the interactive toolbar at the bottom of your screen.

Download slides and materials by clicking this icon.

Ask questions by entering your question in the “Q&A” box.

Please click the “Help” and/or “Contact Us” at the bottom of your screen.

Call AICPA Member Service at 888.777.7077.

2

12/14/2016

2

Governmental Audit Quality Center

Trouble Shooting

Troubleshooting Tips

No Audio?• Ensure that your computer speakers are turned on that the

volume is appropriately set

• Check to ensure that audio streaming is enabled on your computer

If the presentation slides stop advancing during the presentation• Close out of the presentation and re-launch the webcast

If you are still having audio or other technical difficulty

• Check with your IT personnel at your firm or state audit organization (SAO) to ensure that this event is not being blocked by a firewall

• Call the AICPA Service Center at 888.777.7077

3

Governmental Audit Quality Center

Continuing Professional Education

You must answer at least 75% of the random, attendance checks to earn CPE credit.

Please respond to the attendance checks during the live presentation.

You are not eligible to earn CPE by watching the archive of this event.

At the end of today’s presentation we will provide steps for obtaining your CPE certificate

4

12/14/2016

3

Governmental Audit Quality Center

Presenters

Chris Stanz, CPACliftonLarsonAllen LLP

Denise Toomey, CPAWolf & Company, P.C.

5

Governmental Audit Quality Center

What We Will Cover

Multifamily • Program Updates

• HUD Requirements to be Familiar With

Lender Program Update

An Update on the U.S. Department of Housing and Urban Development (HUD) Consolidated Audit Guide for Audits of HUD Programs (HUD Guide)

Planning Considerations for December 31, 2016, Year-End Audits

6

12/14/2016

4

Governmental Audit Quality Center

Multifamily Program Updates

7

Governmental Audit Quality Center

Multifamily Programmatic Changes and Other Updates

Updated User Guide, Industry User Guide for the Financial Assessment Subsystem – Multifamily Housing (FASSUB)

Financial Accounting Standards Board (FASB) Update No. 2015-03, Simplifying the Presentation of Debt Issuance Costs (ASU 2015-03): Accounting and HUD/FASSUB system requirements

Real Estate Assessment Center (REAC) Quality Assurance Subsystem

HUD to reinstate Management and Occupancy Reviews (MORs)

Other Multifamily Updates

8

12/14/2016

5

Governmental Audit Quality Center

Updates to FASSUB Systems and Industry User Guides

Updated Industry User Guide issued in July 2016

New version (7.3.3.0) of Financial Assessment of Federal Housing Administration (FHA) Housing (FASS-FHA) submission templates changed to require additional details for accounts 1330, Other Reserves, and S1200-255, Net Deposits to Other Reserves, if account values are $1,000 or more

9

Governmental Audit Quality Center

ASU 2015-03 Accounting Requirements

10

Assets ‐amortized over life of the loan Liability – discount

to debt

12/14/2016

6

Governmental Audit Quality Center

ASU 2015-03 Accounting Requirements

Effective for financial statement periods beginning after December 15, 2015

Applied retrospectively to all prior periods presented

Amortization of debt discount • Effective interest method vs. straight line

• Reported as a component of interest expense

• Present amount of unamortized costs (face of balance sheet or in notes)

Effect of adoption• Considered a change in accounting principle –

- disclosure,

- emphasis of matter paragraph in report,

- governance communication.

• Change in debt presentation footnote11

Governmental Audit Quality Center

ASU 2015-03 HUD Reporting Requirements

FASSUB System Release – October 6, 2016• Modified FASSUB system to align with ASU 2015-03

- Several changes will be made to the current chart of accounts as a result

• Two options allowed: Discounts on each debt obligation reported either individually or in the aggregate

• Added –

- Account 2340, Debt Issuance Costs

- Account 1200-486, Amortization of Debt Issuance Costs (indirect method section of cash flow statement)

• Updated definitions for certain accounts

12

12/14/2016

7

Governmental Audit Quality Center

REAC Quality Assurance Subsystem (QASS)

Ensures financial data received are free of material misstatements

Identifies high risk audit firms

Performs Quality Control Reviews (QCRs)

Makes referrals to oversight bodies

13

Governmental Audit Quality Center

Management and Occupancy Reviews

Letter issued to contract administrators regarding initiating MORs on higher-risk projects

MORs covered by HUD Handbook 4350.1, Multifamily Asset Management and Project Servicing

14

12/14/2016

8

Governmental Audit Quality Center

Other Multifamily Housing Program Updates – What’s New!

Updated Chapter 9 of Section 8 Renewal Guide

Implementation of Housing Protections Authorized in Violence Against Women Reauthorization Act of 2013

Rental Assistance Demonstration (RAD) Fair Housing, Civil Rights and Relocation Notice

Special and Add-on Management Fees Now Available for Properties that Implement a Homeless Preference

Amended and Restated Low-Income Housing Preservation and Resident Homeownership Act Use Agreement Notice

Draft Chapters of HUD Handbook 4350.1, Multifamily Asset Management and Project Servicing, Released

FY 17 Project Assistance Contracts (PAC) Renewals Oct. 5-Dec. 5, 2016

Previous Participation Final Rule

FY 2017 Utility Adjustment Factors Effective February 11, 2017

15

Governmental Audit Quality Center

Other Multifamily Housing Program Updates – What’s New!

Operating Cost Adjustment Factors Effective February 11, 2017

HUD Launches Utility Benchmarking in an Effort to Increase Energy and Water Efficiency and Save Costs

Reminder of Requirements for Lead-Based Paint Inspection

Eligibility of Independent Students for Assisted Housing Under Section 8

HUD Publishes Evaluation of Rental Assistance Demonstration

Family Self-Sufficiency Program Expanded to Privately Owned Multifamily Properties

16

12/14/2016

9

Governmental Audit Quality Center

Multifamily HUD Requirements to be Familiar With

17

Governmental Audit Quality Center

Section 202/811 Project Rental Assistance Contracts (PRAC) Recapture

Consolidated Appropriations Act, 2016 – December 2015• Gives authority to continue to recapture in fiscal year 2016

• Specific language for “housing for the elderly” and “housing for persons with disabilities”

• Applies to properties with PRAC contracts expiring between July 19, 2015 – September 30, 2019

• Excess residual receipts - $250 per unit

• Required to be paid upon termination of the contract

• Accounting considerations on recording loss/liability

• REAC – record losses to account 7190, Other Entity Expenses, and provide adequate explanation in the details

18

12/14/2016

10

Governmental Audit Quality Center

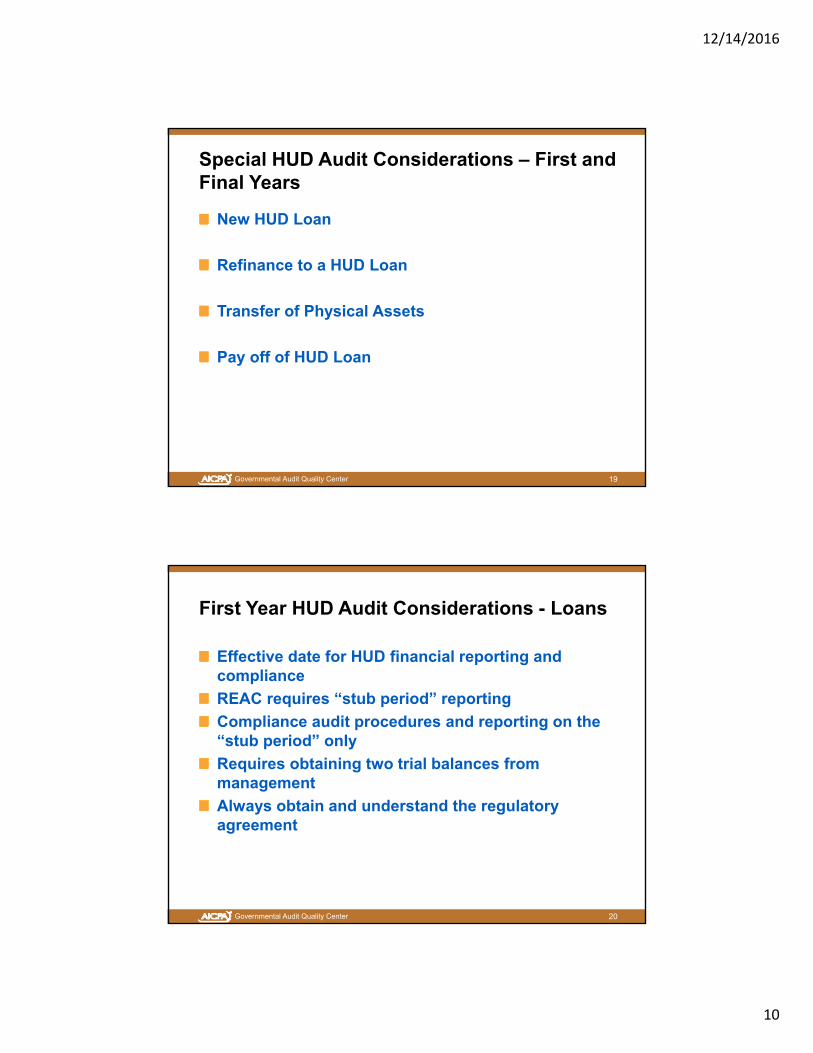

Special HUD Audit Considerations – First and Final Years

New HUD Loan

Refinance to a HUD Loan

Transfer of Physical Assets

Pay off of HUD Loan

19

Governmental Audit Quality Center

First Year HUD Audit Considerations - Loans

Effective date for HUD financial reporting and compliance

REAC requires “stub period” reporting

Compliance audit procedures and reporting on the “stub period” only

Requires obtaining two trial balances from management

Always obtain and understand the regulatory agreement

20

12/14/2016

11

Governmental Audit Quality Center

Other HUD Considerations

Transfer of Physical AssetsThe transfer of ownership of a HUD insured project when the existing mortgage remains in force requires a “transfer of physical assets” (TPA)

Reporting requirements for both the seller and the buyer

Pay off of HUD LoanContact HUD to determine if a final HUD audit, review or compilation is required

21

Governmental Audit Quality Center

HUD Regulatory Agreements and Surplus Cash

Understand the definitions in the HUD regulatory agreement

Currently multiple versions are being used• Original version

• 2011 version

• 2014 version

• Healthcare specific agreements

Calculations will differ based on date of agreement

22

12/14/2016

12

Governmental Audit Quality Center

Surplus Cash

Limitations on the ability to take surplus cash• Non-compliance from physical inspection

• Non-compliance with HUD notices

• Distribution made with borrowed funds

• Limited distribution owners

Common deviations• Including amounts that do not meet HUD requirements

• Liability for future repairs

• Replacement reserve requests

• Refer to HUD chart of accounts.

23

Governmental Audit Quality Center

Fair Housing and Nondiscrimination

HUD Guide, Chapter 2. Reporting Requirements and Sample Reports, revised in January 2013• Eliminated separate auditor reporting on Fair Housing

HUD compliance requirement

Affirmative Fair Housing Marketing Plan

Direct and material?

24

12/14/2016

13

Governmental Audit Quality Center

Equity Skimming

Regulatory agreement• Expenditures must be reasonable and necessary

Mortgage note in default / Non-surplus cash position• Cash distributions

• Repayment of owner advances

• Lending funds to owners or management agent

• Repayment of secondary financing without HUD approval

Appendix B, HUD Guide, Chapter 3, HUD Multifamily Housing Programs

HUD Office of Inspector General, National Single Audit Coordinator

25

Governmental Audit Quality Center

Lender Program Update

26

12/14/2016

14

Governmental Audit Quality Center

Recent HUD Program Activity – LendersVisit HUD’s Federal Housing Administration (FHA) Lenders page to keep current

http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/sfh/lender

• Includes:- Link to Lender Electronic Assessment Portal (LEAP) Information

page in the Approvals & Renewals section (including LEAP User Manual 2-5-16; Independent Public Accountant (IPA) Registration and Assignment Instructions 9-13-16)

- Link to subscribe to receive FHA INFO announcements and SF news

- Links to other useful information/resources

FHA Single Family Housing Policy Handbook (“HUD Handbook 4000.1” or “SF Handbook”) issued in 2015 with first sections becoming applicable starting in September 2015

27

Governmental Audit Quality Center

Recent HUD Program Activity – LendersChange to Annual Recertification on LEAP - Revised Certification Statements • Changes applied starting with lenders with fiscal year end July

2016

• Make sure your clients understand what they are certifying to and that they answer the questions correctly

• Any “NO” response to a certification statement will cause delays to the annual recertification process.

• FHA has posted documents that describe changes and a comparison of the previous versions to the current versions by mortgagee type. See HUD’s Annual Recertification page under FHA Lenders page

• These certifications are not subject to audit or agreed-upon procedures

28

12/14/2016

15

Governmental Audit Quality Center

Single Family Housing Policy Handbook

FHA’s SF Handbook is a consolidated, consistent and comprehensive single source for FHA Single Family Housing Policy:• SF Handbook only applies to single family (SF) lenders with the

exception of Section I.A.1 – I.A.9 (Doing Business with FHA), which also applies to multifamily lenders.

• Consistent format and terms throughout SF Handbook support easier use

• Eventually, all SF Mortgagee Letters, Housing Notices, Handbooks and other policy documents with be consolidated into SF Handbook

• SF Handbook will cover all SF Housing policy

29

Governmental Audit Quality Center

Single Family Housing Policy Handbook

FHA’s online and PDF SF Handbook accessible at HUD.gov (HUDClips)

Additional information on the SF Handbook Information Page on HUD.gov

SF Handbook was issued and effective in stages and original effective dates were 9/14/15 and 3/14/16

Certain sections still not complete

On-line SF Handbook is continually updated (last revision 9/30/16)

Effective dates are clearly indicated in each section

30

12/14/2016

16

Governmental Audit Quality Center

Single Family Housing Policy Handbook

Mortgagee Letters (ML) since date of last update need to be reviewed for any applicable changes• ML 2016-22 issued on 12/1/16 – extends implementation dates

of various parts of Section III, Servicing and Loss Mitigation that were set to become effective 12/1/16 to 3/1/17.

http://portal.hud.gov/hudportal/HUD?src=/program_offices/administration/hudclips/letters/

Section V, Quality Control, Oversight and Compliance, contains the most significant changes impacting lender compliance requirements • Auditors are required to test this area as detailed in HUD Guide,

Chapter 7, FHA-Approved Lenders Audit Guidance

31

Governmental Audit Quality Center

SF Handbook – Quality Control (QC) Changes

Applicable to Title I and Title II lenders

Provides specific definitions, standards, documentation for:• QC Program

• QC Plan

• Loan Administration

• Material Finding

• Mitigated Finding;

• Loan Sample Risk Assessment

Establishes institutional and loan level QC Program requirements

Eliminated on-site review of lender branch offices

32

12/14/2016

17

Governmental Audit Quality Center

SF Handbook – QC Changes

Updated requirements for participation for certain employees (Excluded Parties List, Limited Denial of Participation List, National Mortgage Licensing System and Registry (NMLS) registration)

Specific timeframes for completion of QC and reporting

Initial QC findings report drives reporting timeframes:• Initial QC findings report - within 30 days to senior management

• Final QC findings report - within 60 days to senior management

• Unmitigated/unresolved material findings - no later than 90 days to FHA

• Fraud/material misrepresentation determination – report immediately to HUD

33

Governmental Audit Quality Center

SF Handbook – QC Changes

Minimum requirements for QC review detailed in a bulleted list

Timeframe for selection and review of loan files:• Pre-closing - reviewed after approval by Direct Endorsement

(DE) underwriter and prior to closing

• Post-closing – select monthly and review within 60 days from the end of the prior one-month period

• Early payment defaults - select monthly and review within 60 days from the end of the month in which loan was selected

• Servicing – select monthly and review within 60 days from the end of the month in which loan was selected

34

12/14/2016

18

Governmental Audit Quality Center

SF Handbook – QC Changes

Updated Sample Size Standards:• < 3,500 FHA mortgages/year:

- 10% of FHA loans originated or serviced

• > 3,500 FHA mortgages/year:

- either 10% of FHA loans originated or serviced, or

- a stratified random sample of a size that ensures a 95% confidence level with a confidence interval not to exceed 2% on an annual basis, based on the defect rates for FHA-insured Mortgages recently reviewed

• Pre-closing reviews should be < 10% of sample size; Post-closing should be > 90% of sample size

• Exception for 9 or fewer loans in prior month – select a minimum of 1 loan each month for pre-closing review

35

Governmental Audit Quality Center

Recent HUD Program Activity - Government National Mortgage Association (Ginnie Mae)

Pooling Eligibility for Streamlined Refinance Loans(10/19/2016 - All Participant Memorandums (APM) 16-05)

Issued generally to announce policy and Mortgage Backed Security (MSB) Guide changes accessed by Issuers, Document Custodians and other participants in Ginnie Mae programs.

Home Equity Conversion Mortgage (HECM) Mortgage Backed Securities (HMBS) Monthly Reporting Cycle(11/17/2016 - APM 16-06)

Recent APMs -http://www.ginniemae.gov/issuers/program_guidelines/Pages/mostrecentapms.aspx

36

12/14/2016

19

Governmental Audit Quality Center

Recent HUD Program Activity - Government National Mortgage Association (Ginnie Mae)

Annual Audited Financial Statements Reminder• Published in Ginnie Mae’s Notes and News newsletter on

March 4, 2016

• http://www.ginniemae.gov/issuers/program_guidelines/NotesNews/NotesandNews_03_04_2016.pdf

• Issuers must submit annual audited financial statements and duplicate originals of Certificates of Insurance for Fidelity Bond and Errors and Omissions insurance annually

• Includes issuers that did not have outstanding Ginnie Mae securities or commitment authority to issue new securities at any time during the fiscal year.

37

Governmental Audit Quality Center

Recent HUD Program Activity - Government National Mortgage Association (Ginnie Mae)

Documents must be submitted via the IPA module in Ginnie Mae’s Enterprise Portal (GMEP) within 90 days of the Issuer’s fiscal year-end

Issuers with a fiscal year-end of December 31 must submit their annual financial statements with the transmittal checklist and supplementary documents to Ginnie Mae by March 30, 2016

To arrange access to GMEP refer to Appendix III-29 of the Ginnie Mae Mortgage-Backed Securities (MBS) Guide 5500.3, Rev. 1 for instructions for completing GMEP registration

38

12/14/2016

20

Governmental Audit Quality Center

Ginnie Mae Guidance

39

Reference Guidance Website

Consolidated Audit Guide for Audits of HUD Programs (Audit Guide) HUD Handbook 2000.04 REV-2 CHG-20, Chapter 6

Chapter 6: Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance - outlines the required documents that must be submitted.

https://www.hudoig.gov/sites/default/files/Audit%20guide_updated/Audit%20Guide%20Chapter%206%20%20Final%202%202016.pdf

Ginnie Mae Mortgage-Backed Securities Guide, Appendix VI-20

Appendix VI-20, Electronic Submission of Issuers’ Insurance and Annual Audited Financial Documents - instructions for submitting the financial documents electronically.

http://www.ginniemae.gov/issuers/program_guidelines/MBSGuideAppendicesLib/Appendix_VI-20.pdf

Ginnie Mae Mortgage-Backed Securities Guide, Sections 3-6 and 3-7

Section 3-6: Fidelity Bond and Errors and Omissions Insurance and Section 3-7: Required Financial Statements and Documents - outlines insurance eligibility requirements for maintaining Ginnie Mae Issuer status.

http://ginniemae.gov/doing_business_with_ginniemae/issuer_resources/MBSGuideLib/Chapter_03.pdf

Governmental Audit Quality Center 40

Update on the HUD Guide

12/14/2016

21

Governmental Audit Quality Center

HUD Guide Chapters

Chapter 1, General Audit Guidance

Chapter 2, Reporting Requirements and Sample Reports

Chapter 3, HUD Multifamily Housing Programs

Chapter 4, Mortgage Insurance for Hospitals Program

Chapter 5, Insured Development Cost Certification Audit Guidance

Chapter 6, Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance

Chapter 7, FHA-Approved Lenders Audit Guidance

41

Governmental Audit Quality Center

Chapter 1, General Audit GuidanceLast update in May 2013

Items of note:• HUD Guide mandatory for audits of all for-profit participants

• Auditors of entities subject to single audit should normally refer to the Office of Management and Budget (OMB) Compliance Supplement for compliance requirements and auditor information

• Audit sampling requirements

• Major program thresholds and related guidance (see next two slides)

• Retain audit documentation for a minimum of 6 years

• Withdrawal or termination after audit is initiated requires auditor to advise the Office of Inspector General National Single Audit Coordinator

42

12/14/2016

22

Governmental Audit Quality Center

Entities subject to Chapters 3 and 4 – individual assistance program for which expenditures equaled or exceeded $500,000 during the applicable year (including HUD-insured or HUD-guaranteed loan balance equal to or exceeding $500,000 as of the end of the audit period)

Entities subject to Chapter 5 – No major program designation is needed.

43

Chapter 1, Major Program Thresholds

Governmental Audit Quality Center

Chapter 1, Major ProgramsEntities subject to Chapter 6 – Ginnie Mae program is major if the issuer had a servicing portfolio or had any remaining principal balance at the end of the audit period.

Audits of entities subject to Chapter 7

• FHA-approved lender’s program is major regardless of the amount of loans originated or serviced during the period under audit.

• Note: If combined originations and a servicing portfolio is less than $2 million, the opinion on compliance need only cover requirements in 7-5(A), Quality Control Plan, and 7-5(G), Lender Annual Recertification, Adjusted Net Worth, Liquidity, and Licensing.

44

12/14/2016

23

Governmental Audit Quality Center

Chapter 2 - Reporting

Last update March 2013

Items of note:• Discusses the reporting requirements that result from the

performance of the required financial statement and compliance audit conducted in accordance with HUD Guide

• Describes required elements of reporting package

• Describes report distribution requirements

• Includes auditor report examples

• Includes requirements for Schedule of Findings and Questioned Costs and an example of the schedule

45

Governmental Audit Quality Center

Chapter 3, HUD Multifamily Housing Programs

Last updated July 2008

Items of note• Includes requirements for conducting the compliance portion of

the annual financial audits of profit-motivated and limited-distribution entities participating in HUD’s FHA multifamily housing programs

• Keep in mind that chapters 1 and 2 (which were revised in 2013) are used in conjunction with chapter 3

• Includes “group project-based sampling” of certain areas when conditions are met

46

12/14/2016

24

Governmental Audit Quality Center

Chapter 3, Compliance RequirementsFederal Financial Reports

Fair Housing and Nondiscrimination

Mortgage Status

Replacement Reserve

Residual Receipts

Distributions to Owners

Equity Skimming

Cash Receipts

Cash Disbursements

Tenant Applications, Eligibility, and Recertification

Units Leased to Extremely Low-Income Families

Tenant Security Deposits

Management Functions

Unauthorized Change of Ownership/Acquisition of Liabilities

Unauthorized Loans of Project Funds

Excess Income

Leased Nursing Homes

Mark to Market Program (M2M)

47

Governmental Audit Quality Center

Chapter 3 - Group Project-Based Sampling Refresher

Exceptions for testing when project is owned and/or managed by an entity that owns and/or manages multiple HUD/FHA assisted projects

Compliance sections - Tenant Application, Eligibility, and Recertification; Tenant Security Deposits and Management Functions

All other compliance sections except for the three cited above must be performed on each project

48

12/14/2016

25

Governmental Audit Quality Center

Chapter 3 - Group Project-Based Sampling Conditions Refresher

Same system is used by management for the compliance section for all projects

Projects have the same supervisor, procedures followed are identical and the test of internal controls did not disclose any weaknesses

Owner agrees to the project-based sample method (signed agreement – i.e., engagement letter)

Auditor fully documents all the above

49

Governmental Audit Quality Center

Chapter 3 - Group Project-Based Sampling Refresher

What is meant by “same supervisor?”• The person that

- Directly responsible to get the related work accomplished or in charge of the function

- Gets work accomplished through staff who reports the results to the individual that is ultimately responsible for accomplishing the function

- Can be at the project, regional or corporate office

50

12/14/2016

26

Governmental Audit Quality Center

Chapter 3 - Group Project-Based Sampling Refresher

Minimum Sampling Requirements• At least 20% of the projects

• No less than a minimum of four projects each year

• Each project reviewed at least every five years or less

If the auditor elects to do the five-year sampling plan, the sampling schedule and system for selecting must be included in the work papers

51

Governmental Audit Quality Center

Chapter 3 - Group Project-Based Sampling Refresher

If a condition is noted that is to be reported in a finding or management letter, it must be reported in all reports

Opinion on compliance provided for each individual project; testing must support the opinion for each individual project and not the group as a whole

52

12/14/2016

27

Governmental Audit Quality Center

Chapter 4, Mortgage Insurance for Hospitals Program

Last updated September 2014

Items of note:• Includes requirements for conducting the annual financial audits

of profit-motivated and limited-distribution entities participating as mortgagors in HUD’s FHA’s Mortgage Insurance for Hospitals Program, under Section 242 of the National Housing Act.

• Keep in mind that chapters 1 and 2 (which were revised in 2013) are used in conjunction with chapter 4.

53

Governmental Audit Quality Center

Chapter 4, Compliance Requirements

Federal Financial Reports

Mortgage Status

Mortgage Reserve Fund, Equipment Replacement Reserve Fund, and Special Escrows

Distributions to Owners or Affiliates

Equity Skimming

Cash Receipts

Cash Disbursements

Unauthorized Change of Ownership/Mergers/Acquisitions, and Liabilities

Unauthorized Loans or Loan Guarantees of Project Funds

Acquisition of Real Property and Personalty

Budget

Financial Monitoring by the Board

Additional Indebtedness

Minimum Account Presentation

Ratios

Cost Certification and Final Endorsement

Other Conditions

54

12/14/2016

28

Governmental Audit Quality Center

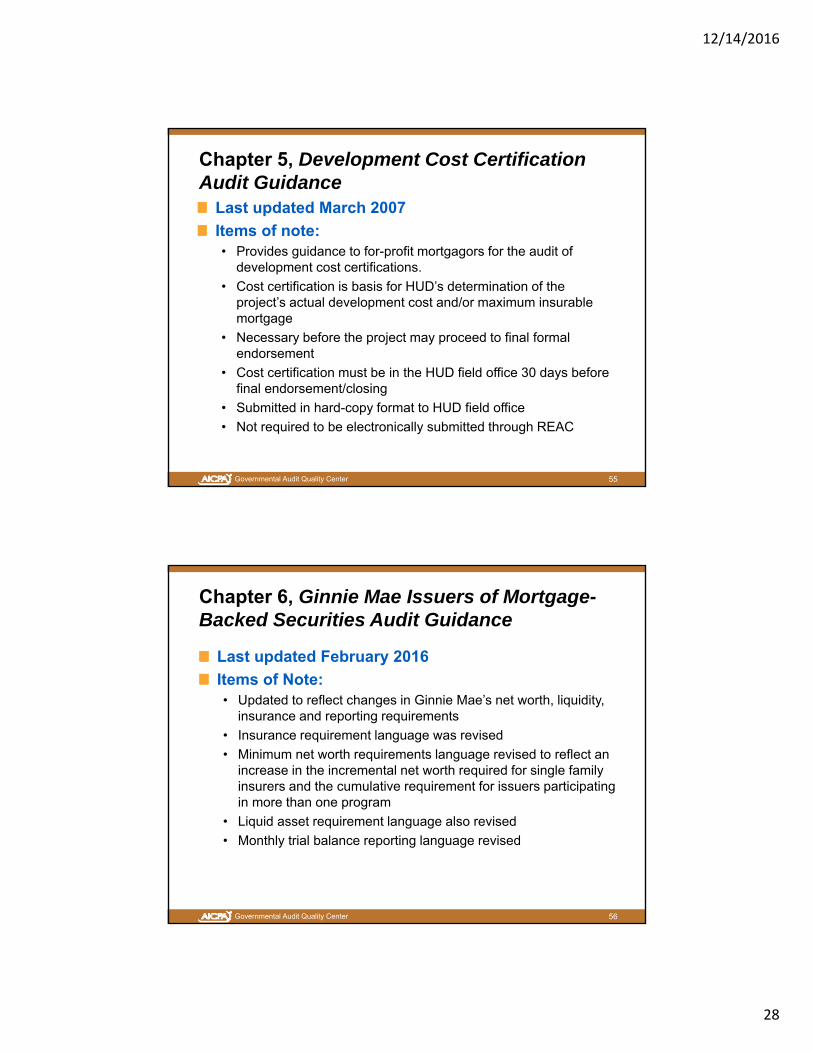

Chapter 5, Development Cost Certification Audit Guidance

Last updated March 2007

Items of note:• Provides guidance to for-profit mortgagors for the audit of

development cost certifications.

• Cost certification is basis for HUD’s determination of the project’s actual development cost and/or maximum insurable mortgage

• Necessary before the project may proceed to final formal endorsement

• Cost certification must be in the HUD field office 30 days before final endorsement/closing

• Submitted in hard-copy format to HUD field office

• Not required to be electronically submitted through REAC

55

Governmental Audit Quality Center

Chapter 6, Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance

Last updated February 2016

Items of Note:• Updated to reflect changes in Ginnie Mae’s net worth, liquidity,

insurance and reporting requirements

• Insurance requirement language was revised

• Minimum net worth requirements language revised to reflect an increase in the incremental net worth required for single family insurers and the cumulative requirement for issuers participating in more than one program

• Liquid asset requirement language also revised

• Monthly trial balance reporting language revised

56

12/14/2016

29

Governmental Audit Quality Center

Chapter 7, FHA-Approved Lenders Audit Guidance

Last updated October 2016

Items of note:• Revised chapter and transmittal letter posted to HUD's Office of

Inspector General Web site

• Applies to supervised and nonsupervised lenders

• Revised chapter became effective upon issuance

• Main reason for revision is to reflect changes needed as a result of the issuance of SF Handbook (discussed earlier)

- Entire HUD Guide also included with SF Handbook

57

Governmental Audit Quality Center

Chapter 7, FHA-Approved Lenders Audit Guidance - Changes

The "Quality Control Plan" section was most affected by the issuance of the SF Handbook both from the perspective of describing the entity's compliance requirements and the related suggested audit procedures. • See section 7-5 (A), "Compliance Requirements and Suggested

Audits Procedures Applicable to Lenders With both Title I and Title II Authorities.”

58

12/14/2016

30

Governmental Audit Quality Center

Chapter 7, FHA-Approved Lenders Audit Guidance - Changes

Quality Control Plan Suggested Audit Procedures with Changes• Item m – Revised procedure related to selection of early

payment defaults

• Item q – Revised procedure related to determine whether the lender reported any findings of fraud or material misrepresentation to FHA upon the lender’s confirmation of the deficiency, using the lender reporting feature in Neighborhood Watch

• Various other suggested audit procedures revised to refer to appropriate sections of the SF Handbook

59

Governmental Audit Quality Center

Chapter 7, FHA-Approved Lenders Audit Guidance - Changes

In various places in the chapter, the term "should" has been replaced with "must."

When "Operating Loss Reporting" is required to be made, it must be submitted as a "notice of material event" in LEAP (Section 7-4, "Electronic Submission of Audited Financial Statements and Compliance Data," section C, "Operating Loss Reporting”)

Extension requests (section 7-4 B.) Lender may request extension of recertification package due date through LEAP at least 45 days before due date

A number of editorial revisions made

60

12/14/2016

31

Governmental Audit Quality Center

Planning Considerations for December 31, 2016 Year-end Audits

61

Governmental Audit Quality Center

Planning Considerations

Ensure familiarity with program requirement changes discussed earlier in presentation

Review HUD audit requirements including major program determination in chapter 1 of HUD Guide

Review Government Auditing Standards (GAS) CPE and independence requirements (along with AICPA independence requirements) to ensure compliance

Ensure that engagement letters meet the requirements in chapter 1 of HUD Guide

62

12/14/2016

32

Governmental Audit Quality Center

Planning Considerations (continued)

Review reporting requirements in chapter 2 of HUD Guide applicable to entity

Make sure you review the most recent Regulatory Agreement for your client

For lender clients, make sure you are familiar with the changes to the SF Handbook and chapter 7 of the HUD Guide

Review communications from HUD to your client

63

Governmental Audit Quality Center

Questions ?????

64

12/14/2016

33

Governmental Audit Quality Center

How do I get my CPE certificate?Access your CPE certificate by

clicking this orange icon.

If at the end of this presentation you are eligible for but unable to print your CPE certificate, please log back in to this webcast in 24 hours and click the orange “Get CPE” button. Your certificate will still be available.

If you need assistance with locating your certificate, please contact the AICPA Service Center at 888.777.7077 or [email protected].

65

Governmental Audit Quality Center

Thank You for Attending!

66