20Delegation%20Report%20Card

4

2010 Alabama & Florida Congressional Report Card Voter’s Guide on Key Credit Union Issues Know Before You Vote!

-

Upload

thinkcreative -

Category

Documents

-

view

212 -

download

0

description

http://www.lscu.coop/content/download/22873/267238/Congressional%20Delegation%20Report%20Card.pdf

Transcript of 20Delegation%20Report%20Card

2010 Alabama & Florida Congressional Report CardVoter’s Guide on Key Credit Union Issues

Know Before You Vote!

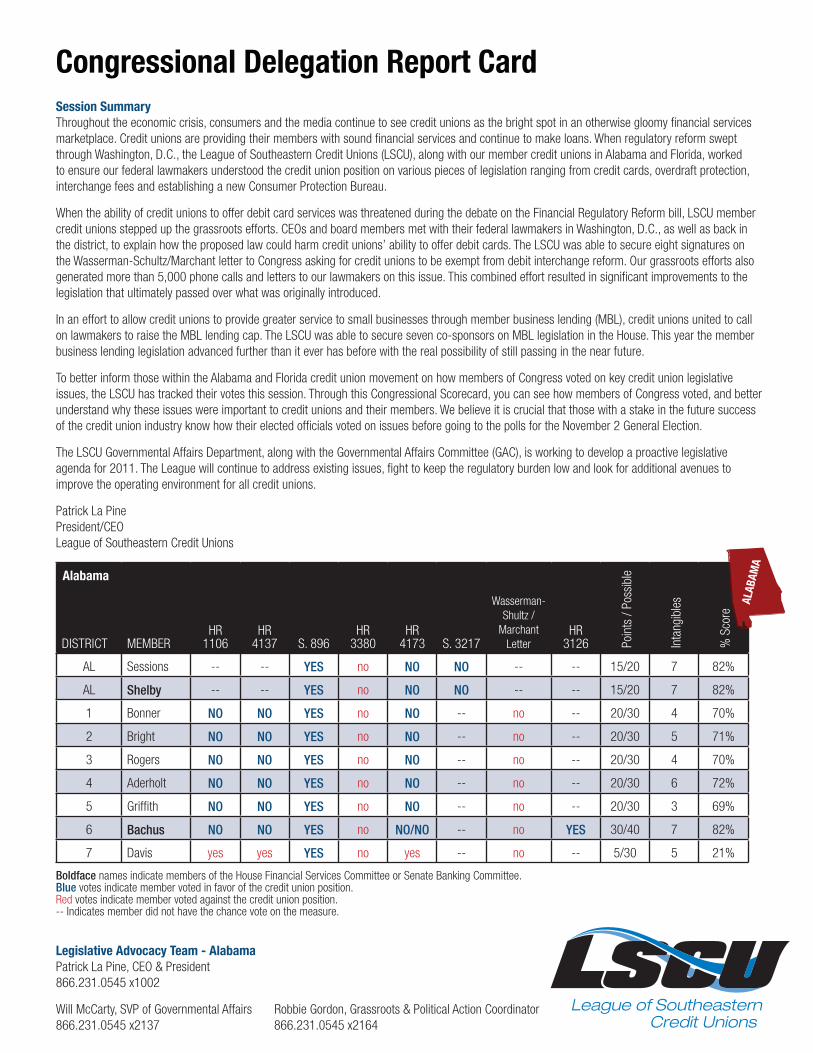

Congressional Delegation Report Card

Session Summary

Throughout the economic crisis, consumers and the media continue to see credit unions as the bright spot in an otherwise gloomy financial services marketplace. Credit unions are providing their members with sound financial services and continue to make loans. When regulatory reform swept through Washington, D.C., the League of Southeastern Credit Unions (LSCU), along with our member credit unions in Alabama and Florida, worked to ensure our federal lawmakers understood the credit union position on various pieces of legislation ranging from credit cards, overdraft protection, interchange fees and establishing a new Consumer Protection Bureau.

When the ability of credit unions to offer debit card services was threatened during the debate on the Financial Regulatory Reform bill, LSCU member credit unions stepped up the grassroots efforts. CEOs and board members met with their federal lawmakers in Washington, D.C., as well as back in the district, to explain how the proposed law could harm credit unions’ ability to offer debit cards. The LSCU was able to secure eight signatures on the Wasserman-Schultz/Marchant letter to Congress asking for credit unions to be exempt from debit interchange reform. Our grassroots efforts also generated more than 5,000 phone calls and letters to our lawmakers on this issue. This combined effort resulted in significant improvements to the legislation that ultimately passed over what was originally introduced.

In an effort to allow credit unions to provide greater service to small businesses through member business lending (MBL), credit unions united to call on lawmakers to raise the MBL lending cap. The LSCU was able to secure seven co-sponsors on MBL legislation in the House. This year the member business lending legislation advanced further than it ever has before with the real possibility of still passing in the near future. To better inform those within the Alabama and Florida credit union movement on how members of Congress voted on key credit union legislative issues, the LSCU has tracked their votes this session. Through this Congressional Scorecard, you can see how members of Congress voted, and better understand why these issues were important to credit unions and their members. We believe it is crucial that those with a stake in the future success of the credit union industry know how their elected officials voted on issues before going to the polls for the November 2 General Election.

The LSCU Governmental Affairs Department, along with the Governmental Affairs Committee (GAC), is working to develop a proactive legislative agenda for 2011. The League will continue to address existing issues, fight to keep the regulatory burden low and look for additional avenues to improve the operating environment for all credit unions.

Patrick La PinePresident/CEOLeague of Southeastern Credit Unions

DISTRICT MEMBERHR

1106HR

4137 S. 896HR

3380HR

4173 S. 3217

Wasserman-Shultz /

Marchant Letter

HR 3126 Po

ints

/ Po

ssib

le

Inta

ngib

les

% S

core

AL Sessions -- -- YES no NO NO -- -- 15/20 7 82%

AL Shelby -- -- YES no NO NO -- -- 15/20 7 82%

1 Bonner NO NO YES no NO -- no -- 20/30 4 70%

2 Bright NO NO YES no NO -- no -- 20/30 5 71%

3 Rogers NO NO YES no NO -- no -- 20/30 4 70%

4 Aderholt NO NO YES no NO -- no -- 20/30 6 72%

5 Griffith NO NO YES no NO -- no -- 20/30 3 69%

6 Bachus NO NO YES no NO/NO -- no YES 30/40 7 82%

7 Davis yes yes YES no yes -- no -- 5/30 5 21%

Boldface names indicate members of the House Financial Services Committee or Senate Banking Committee.Blue votes indicate member voted in favor of the credit union position.Red votes indicate member voted against the credit union position.-- Indicates member did not have the chance vote on the measure.

Legislative Advocacy Team - Alabama

Patrick La Pine, CEO & President866.231.0545 x1002

Will McCarty, SVP of Governmental Affairs Robbie Gordon, Grassroots & Political Action Coordinator866.231.0545 x2137 866.231.0545 x2164

Alabama

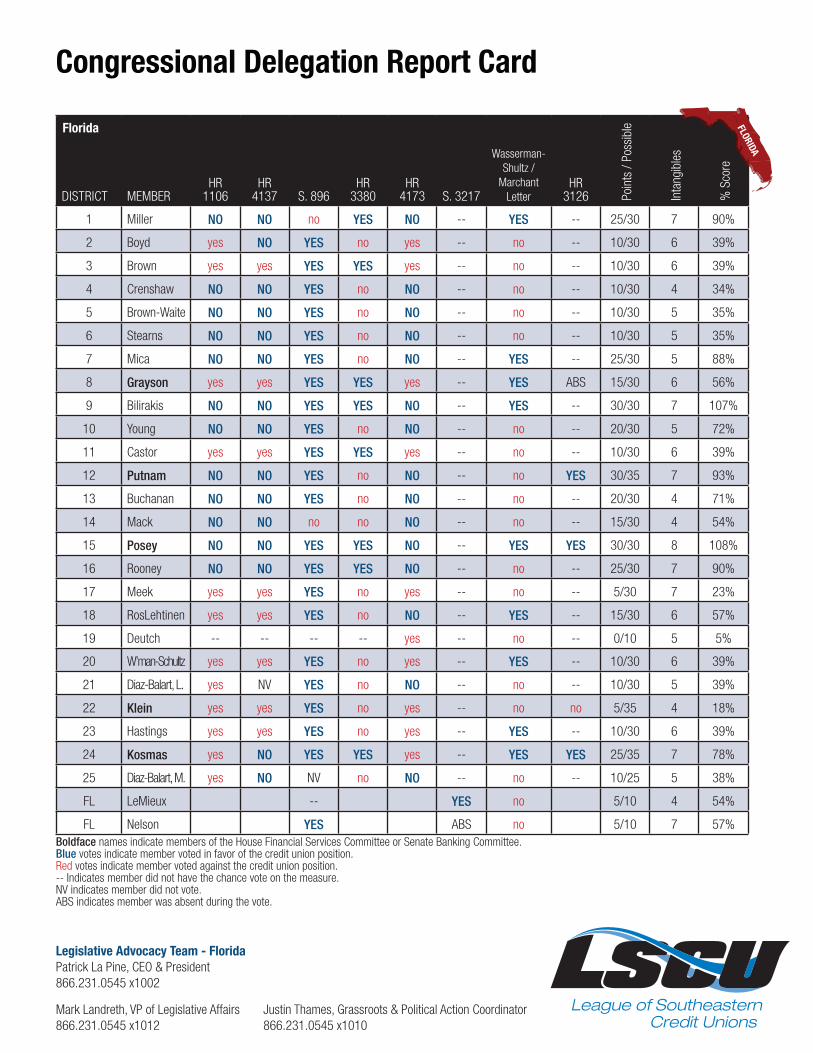

DISTRICT MEMBERHR

1106HR

4137 S. 896HR

3380HR

4173 S. 3217

Wasserman-Shultz /

Marchant Letter

HR 3126 Po

ints

/ Po

ssib

le

Inta

ngib

les

% S

core

1 Miller NO NO no YES NO -- YES -- 25/30 7 90%

2 Boyd yes NO YES no yes -- no -- 10/30 6 39%

3 Brown yes yes YES YES yes -- no -- 10/30 6 39%

4 Crenshaw NO NO YES no NO -- no -- 10/30 4 34%

5 Brown-Waite NO NO YES no NO -- no -- 10/30 5 35%

6 Stearns NO NO YES no NO -- no -- 10/30 5 35%

7 Mica NO NO YES no NO -- YES -- 25/30 5 88%

8 Grayson yes yes YES YES yes -- YES ABS 15/30 6 56%

9 Bilirakis NO NO YES YES NO -- YES -- 30/30 7 107%

10 Young NO NO YES no NO -- no -- 20/30 5 72%

11 Castor yes yes YES YES yes -- no -- 10/30 6 39%

12 Putnam NO NO YES no NO -- no YES 30/35 7 93%

13 Buchanan NO NO YES no NO -- no -- 20/30 4 71%

14 Mack NO NO no no NO -- no -- 15/30 4 54%

15 Posey NO NO YES YES NO -- YES YES 30/30 8 108%

16 Rooney NO NO YES YES NO -- no -- 25/30 7 90%

17 Meek yes yes YES no yes -- no -- 5/30 7 23%

18 RosLehtinen yes yes YES no NO -- YES -- 15/30 6 57%

19 Deutch -- -- -- -- yes -- no -- 0/10 5 5%

20 W’man-Schultz yes yes YES no yes -- YES -- 10/30 6 39%

21 Diaz-Balart, L. yes NV YES no NO -- no -- 10/30 5 39%

22 Klein yes yes YES no yes -- no no 5/35 4 18%

23 Hastings yes yes YES no yes -- YES -- 10/30 6 39%

24 Kosmas yes NO YES YES yes -- YES YES 25/35 7 78%

25 Diaz-Balart, M. yes NO NV no NO -- no -- 10/25 5 38%

FL LeMieux -- YES no 5/10 4 54%

FL Nelson YES ABS no 5/10 7 57%Boldface names indicate members of the House Financial Services Committee or Senate Banking Committee.Blue votes indicate member voted in favor of the credit union position.Red votes indicate member voted against the credit union position.-- Indicates member did not have the chance vote on the measure.NV indicates member did not vote.ABS indicates member was absent during the vote.

Legislative Advocacy Team - Florida

Patrick La Pine, CEO & President866.231.0545 x1002

Mark Landreth, VP of Legislative Affairs Justin Thames, Grassroots & Political Action Coordinator866.231.0545 x1012 866.231.0545 x1010

Congressional Delegation Report Card

Florida

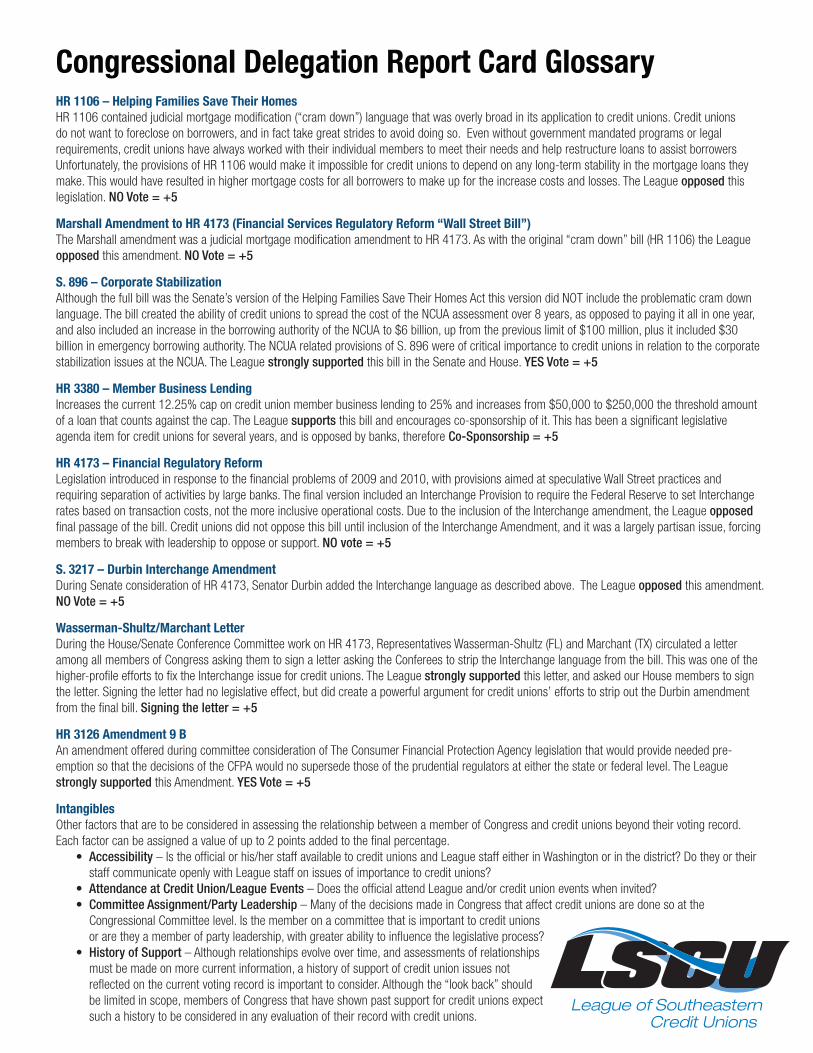

HR 1106 – Helping Families Save Their Homes

HR 1106 contained judicial mortgage modification (“cram down”) language that was overly broad in its application to credit unions. Credit unions do not want to foreclose on borrowers, and in fact take great strides to avoid doing so. Even without government mandated programs or legal requirements, credit unions have always worked with their individual members to meet their needs and help restructure loans to assist borrowers Unfortunately, the provisions of HR 1106 would make it impossible for credit unions to depend on any long-term stability in the mortgage loans they make. This would have resulted in higher mortgage costs for all borrowers to make up for the increase costs and losses. The League opposed this legislation. NO Vote = +5

Marshall Amendment to HR 4173 (Financial Services Regulatory Reform “Wall Street Bill”)

The Marshall amendment was a judicial mortgage modification amendment to HR 4173. As with the original “cram down” bill (HR 1106) the League opposed this amendment. NO Vote = +5

S. 896 – Corporate Stabilization

Although the full bill was the Senate’s version of the Helping Families Save Their Homes Act this version did NOT include the problematic cram down language. The bill created the ability of credit unions to spread the cost of the NCUA assessment over 8 years, as opposed to paying it all in one year, and also included an increase in the borrowing authority of the NCUA to $6 billion, up from the previous limit of $100 million, plus it included $30 billion in emergency borrowing authority. The NCUA related provisions of S. 896 were of critical importance to credit unions in relation to the corporate stabilization issues at the NCUA. The League strongly supported this bill in the Senate and House. YES Vote = +5

HR 3380 – Member Business Lending

Increases the current 12.25% cap on credit union member business lending to 25% and increases from $50,000 to $250,000 the threshold amount of a loan that counts against the cap. The League supports this bill and encourages co-sponsorship of it. This has been a significant legislative agenda item for credit unions for several years, and is opposed by banks, therefore Co-Sponsorship = +5

HR 4173 – Financial Regulatory Reform

Legislation introduced in response to the financial problems of 2009 and 2010, with provisions aimed at speculative Wall Street practices and requiring separation of activities by large banks. The final version included an Interchange Provision to require the Federal Reserve to set Interchange rates based on transaction costs, not the more inclusive operational costs. Due to the inclusion of the Interchange amendment, the League opposed final passage of the bill. Credit unions did not oppose this bill until inclusion of the Interchange Amendment, and it was a largely partisan issue, forcing members to break with leadership to oppose or support. NO vote = +5

S. 3217 – Durbin Interchange Amendment

During Senate consideration of HR 4173, Senator Durbin added the Interchange language as described above. The League opposed this amendment. NO Vote = +5

Wasserman-Shultz/Marchant Letter

During the House/Senate Conference Committee work on HR 4173, Representatives Wasserman-Shultz (FL) and Marchant (TX) circulated a letter among all members of Congress asking them to sign a letter asking the Conferees to strip the Interchange language from the bill. This was one of the higher-profile efforts to fix the Interchange issue for credit unions. The League strongly supported this letter, and asked our House members to sign the letter. Signing the letter had no legislative effect, but did create a powerful argument for credit unions’ efforts to strip out the Durbin amendment from the final bill. Signing the letter = +5

HR 3126 Amendment 9 B

An amendment offered during committee consideration of The Consumer Financial Protection Agency legislation that would provide needed pre-emption so that the decisions of the CFPA would no supersede those of the prudential regulators at either the state or federal level. The League strongly supported this Amendment. YES Vote = +5

Intangibles

Other factors that are to be considered in assessing the relationship between a member of Congress and credit unions beyond their voting record. Each factor can be assigned a value of up to 2 points added to the final percentage.

• Accessibility – Is the official or his/her staff available to credit unions and League staff either in Washington or in the district? Do they or their staff communicate openly with League staff on issues of importance to credit unions?

• Attendance at Credit Union/League Events – Does the official attend League and/or credit union events when invited?• Committee Assignment/Party Leadership – Many of the decisions made in Congress that affect credit unions are done so at the

Congressional Committee level. Is the member on a committee that is important to credit unions or are they a member of party leadership, with greater ability to influence the legislative process?

• History of Support – Although relationships evolve over time, and assessments of relationships must be made on more current information, a history of support of credit union issues not reflected on the current voting record is important to consider. Although the “look back” should be limited in scope, members of Congress that have shown past support for credit unions expect such a history to be considered in any evaluation of their record with credit unions.

Congressional Delegation Report Card Glossary