HSBC SIP Plus HSBC Mutual Fund A little every month can help fulfil your dreams & cover your health...

29

HSBC SIP Plus HSBC Mutual Fund A little every month can help fulfil your dreams & cover your health Issued by HSBC Asset Management (India) Private Limited

-

Upload

julia-patterson -

Category

Documents

-

view

216 -

download

0

Transcript of HSBC SIP Plus HSBC Mutual Fund A little every month can help fulfil your dreams & cover your health...

HSBC SIP Plus

HSBC Mutual Fund

A little every month can help fulfil your dreams & cover your health

Issued by HSBC Asset Management (India) Private Limited

2

Flow of Presentation

Understanding Inflation

Rupee Cost Averaging

What is Systematic Investment Plan (SIP)?

HSBC SIP PLUS

3

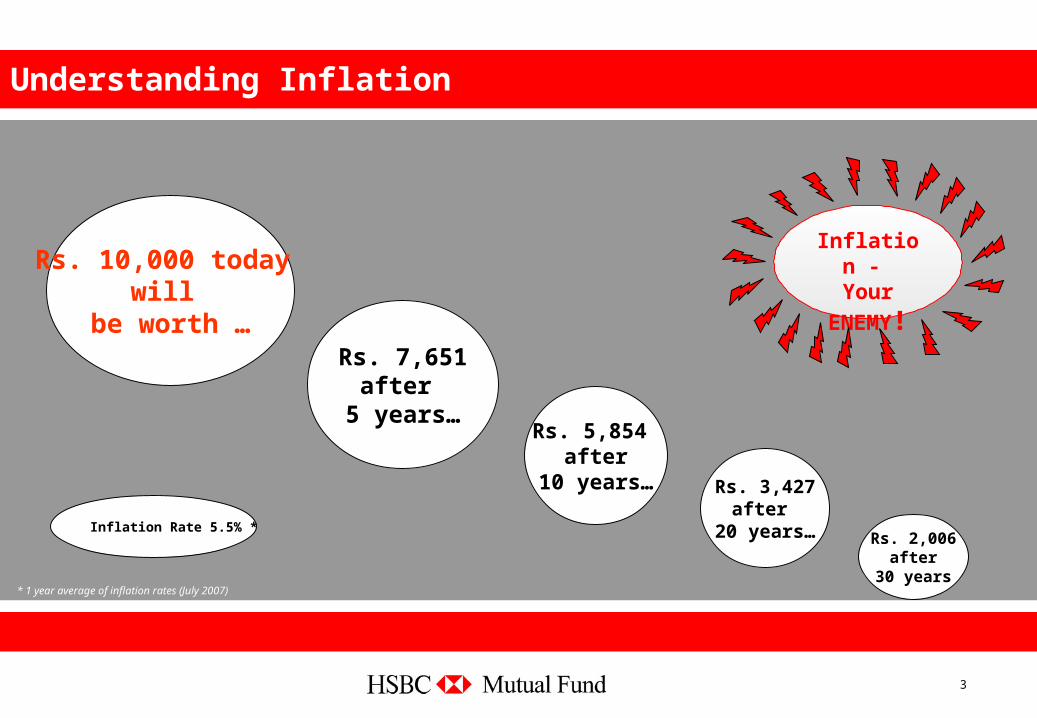

Understanding Inflation

Inflation Rate 5.5% *

Rs. 10,000 today will

be worth …Rs. 7,651

after 5 years…

Rs. 5,854 after

10 years… Rs. 3,427after

20 years… Rs. 2,006after

30 years

Inflation - Your

ENEMY!

* 1 year average of inflation rates (July 2007)

4

Inflation and Fixed Income Investments

Consider the 8% taxable RBI Savings Bonds

Interest rate = 8%

YOU ARE LOSING YOUR

CAPITAL!

Less: [email protected]%*

Less: [email protected]%**i.e. 2.72%

Post-tax & inflationInterest =- 0.22%!

Inflation - Your

ENEMY!

* 1 year average of inflation rates (July 2007)

** Assuming highest tax rate

5

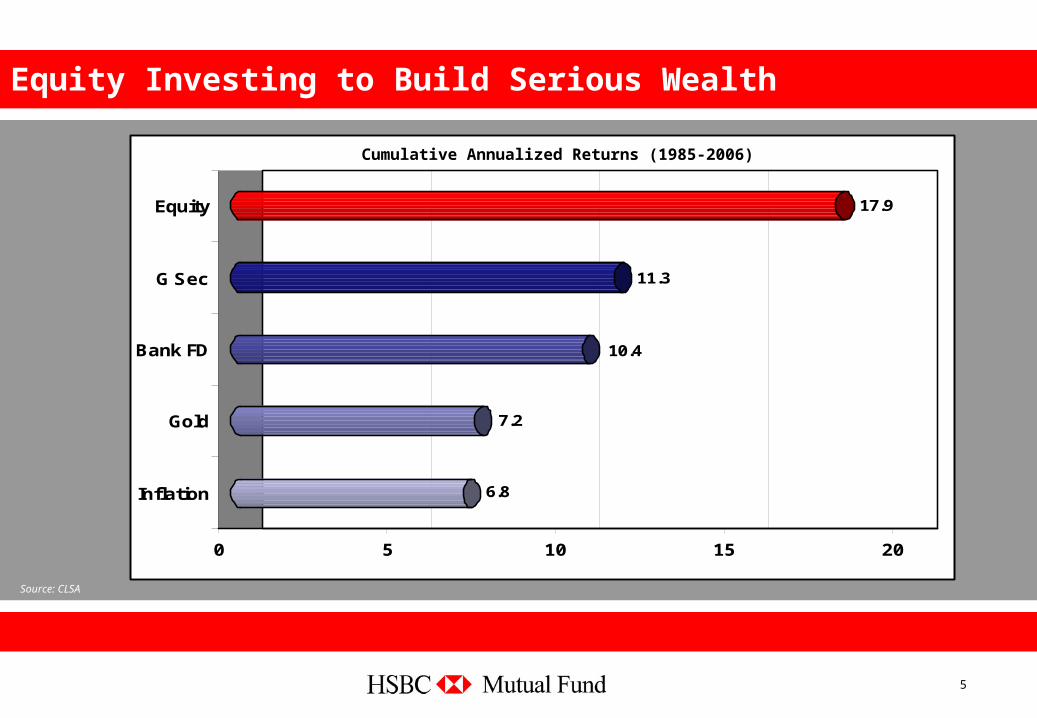

Equity Investing to Build Serious Wealth

6.8

7.2

10.4

11.3

17.9

0 5 10 15 20

Inflation

Gold

Bank FD

G Sec

Equity

Source: CLSA

Cumulative Annualized Returns (1985-2006)

Equities could be the best long term bet

6

Regular Investing

Consider the BSE Sensex

as an investmentoption…

Investment overa 3-year period*

One-time investment 44%

42%

Investment overa 5-year period**

39%

Regularinvesting

41%

Source: MFIE. Past performance may or may not be sustained in the future

* Investing Rs 10,000 each month from Jul 2004 to Jun 2007 and computing market value of investments as on 31 Jul 2007

** Investing Rs 10,000 each month from Jul 2002 to Jun 2007 and computing market value of investments as on 31 Jul 2007

7

Regular Investing

Consider the BSE-200

as an investmentoption…

Investment overa 3-year period*

One-time investment 41%

38%

Investment overa 5-year period**

39%

Regularinvesting

40%

Source: MFIE. Past performance may or may not be sustained in the future

* Investing Rs 10,000 each month from Jul 2004 to Jun 2007 and computing market value of investments as on 31 Jul 2007

** Investing Rs 10,000 each month from Jul 2002 to Jun 2007 and computing market value of investments as on 31 Jul 2007

8

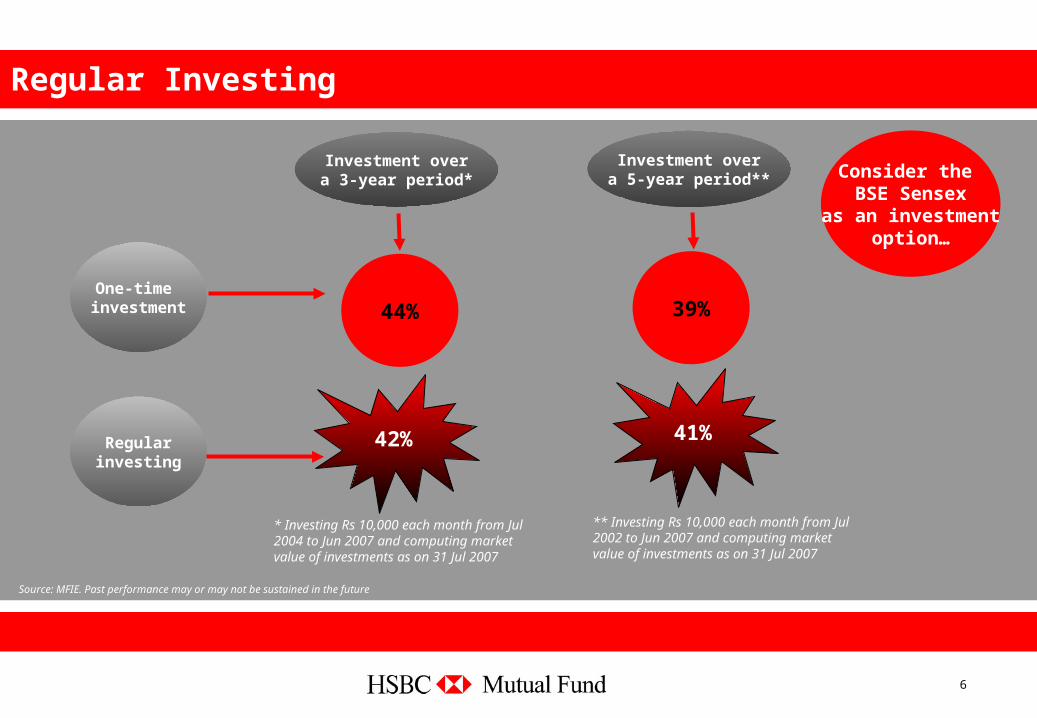

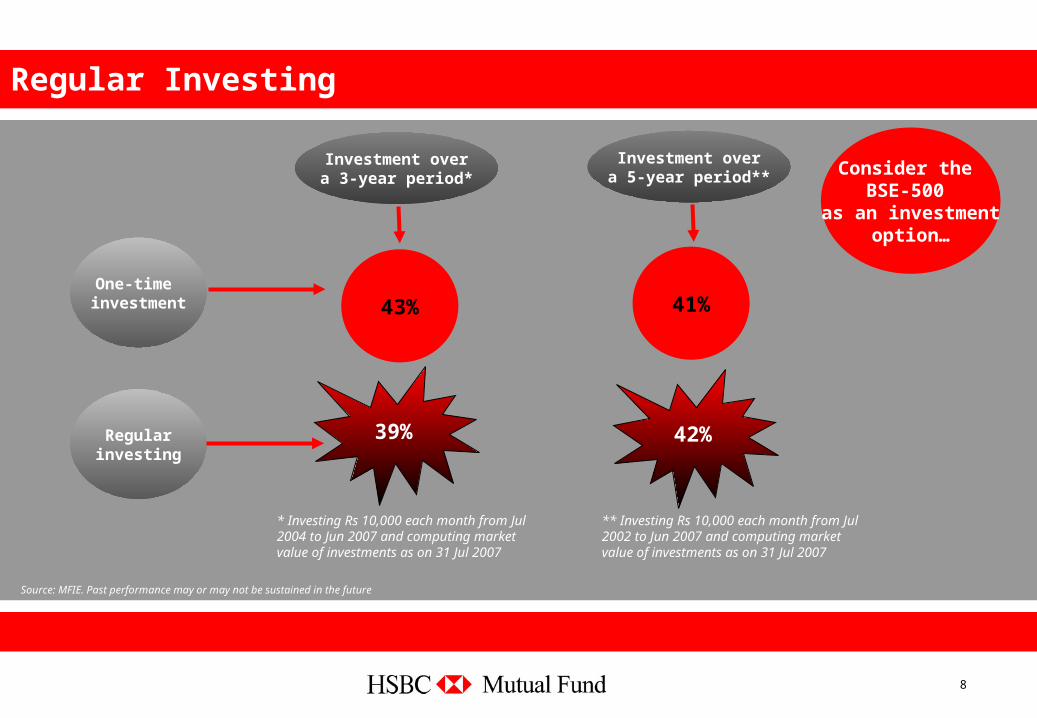

Regular Investing

Consider the BSE-500

as an investmentoption…

Investment overa 3-year period*

One-time investment 43%

39%

Investment overa 5-year period**

41%

Regularinvesting

42%

Source: MFIE. Past performance may or may not be sustained in the future

* Investing Rs 10,000 each month from Jul 2004 to Jun 2007 and computing market value of investments as on 31 Jul 2007

** Investing Rs 10,000 each month from Jul 2002 to Jun 2007 and computing market value of investments as on 31 Jul 2007

9

Regular Investing – A MUST

Using the concept of Rupee Cost Averaging…

It may help regular additions to your investment kitty

It helps you average out your investment cost…

10

Rupee Cost Averaging

Regular investing works on the principle of rupee-cost averaging

It means buying more units when the prices are low and fewer units when the prices are high

This helps to average out your purchase price

For example:

Month Amount Invested (Rs.) Purchase Price (Rs.) No. of Units Purchased1 2,000 10 2002 2,000 9 222.223 2,000 10 2004 2,000 11 181.82

Total Investment = Rs. 8,000

No. of units purchased = 804.04

Average cost per unit = Rs. 9.95 < 10

Equity investing is not about timing

the market but time in the market…

11

Staying in the Market…

Staying invested for 1-year

periods

InvestingIn

Sensex

62%

InvestingIn

BSE-200

Equity investing is not about timing

the market but time in the market…

InvestingIn

BSE-500

64%

64% The best way to use the advantage of disciplined saving and rupee cost

averaging is through a

Systematic Investment Plan

Percentage of positive rolling periods

Consider 1-year, 3-year and 5-year rolling returns for the Sensex, BSE-200 & BSE-500

Staying invested for 3-year

periods

Staying invested for 5-year

periods

59%

61%

61%

As on 31 July 2007

Source: MFIE. Past performance may or may not be sustained in the future

58%

60%

60%

12

What is a Systematic Investment Plan (SIP)?

An Example

Investing Rs 2,000 each month in a mutual fund

The investment is done at the applicable NAV of the mutual fund on the date of investment

fixed amounts

at the prevailing NAV+ +

at regular intervals

A ‘Systematic Investment Plan’ is an investment strategy used in mutual fund investing that allows investments of

13

Advantages of SIP

Instills discipline – forced saving

Helps avoid investing large sums in volatile and overheated markets

Forces the investor to commit investments in any market scenario

Allows investments of small amounts

Easy to understand and operate

14

Performance of SIP

SIP investing in the BSE SENSEX Assume you had Rs 360,000 to invest & you go for an SIP in the Sensex putting in Rs 10,000 every month from Oct 04 to 25 Sep 07 You would have 38.99 units of the Sensex at the end of 25 Sep 07 Taking the Sensex closing of 16899.54 as on 25 Sep 07, the value of your investment would stand at

Rs. 658960 - Return on investment – approx 43.82%

Source: MFIE. Past performance may or may not be sustained in the future. Note: This is a working example only. Load, if any, has not been considered for calculation. The NAVs of the last working day of each month have been used. If the last working day is a non-business day, the NAV of the next business day is taken.

SIP investing in the BSE 200 Index (Benchmark) Assume you had Rs 360,000 to invest & you go for a SIP in the BSE 200 putting in Rs 10,000 every month from Oct 04 to 25 Sep 07 You would have 307.58 units of the BSE 200 at the end of 25 Sep 07 Taking the BSE 200 closing of 2072.91 as on 25 Sep 07, the value of your investment would stand at

Rs. 637576 - Return on investment – approx 41.19%

SIP investing in the HSBC Equity Fund Assume you had Rs 360,000 to invest & you go for a SIP with HSBC Equity Fund (Growth Plan) putting in Rs 10,000 every month from Oct 04 to

25 Sep 07 You would have 7277.21 units of HSBC Equity Fund at the end of 25 Sep 07 Taking the NAV of Rs 87.23 as on 25 Sep 07, the value of your investment would stand at

Rs. 634791 - Return on investment – approx 40.84%

15

Who Wants to be a Millionaire?

No. of Years

Amount (In Rs. Lacs)

No. of Years

Amount (In Rs. Lacs)

No. of Years

Amount (In Rs. Lacs)

1 0.32 11 7.34 21 32.91

2 0.69 12 8.68 22 37.78

3 1.11 13 10.19 23 43.31

4 1.58 14 11.92 24 49.62

5 2.12 15 13.89 25 56.79

6 2.73 16 16.13 26 64.95

7 3.43 17 18.68 27 74.23

8 4.23 18 21.58 28 84.80

9 5.14 19 24.88 29 96.83

10 6.17 20 28.64 30

Let’s say you invest Rs. 2500 per month… how will your money grow?

Assuming 13% CAGR and that investments are made at the beginning of each month. All figures cited in the illustration are notional

110.52

1

CRORE!!!

16

Presenting HSBC SIP Plus

A little every month can help fulfil your dreams &

cover your health

Presenting HSBC SIP Plus with

FREE Critical Illness Cover

17

Investor Benefits

Free critical illness cover

Accidental death cover

Accidental permanent total disability cover

No medical tests required

Cover available on diagnosis on the specified critical illness*

No additional application i.e., initial documentation required

*Requires survival period of 1 month post first diagnosis

18

Why is this important?

The chances of contracting any of the critical illnesses with our current lifestyle is High

The cost of treatment and medical facility is very expensive

Critical Illness will impact our Earning capacity and eat our savings and investments

planned in advance for the future

Critical Illness Cover, protects you with a safety net against financial loss

Source: ICICI Lombard General Insurance

19

Scope of Cover*

Critical Illness Cover

– Cancer

– End Stage Renal Failure

– Major Organ Transplant

– Stroke

– Heart Valve Replacement

– Bypass surgery

Additional Cover

– Accidental death

– Accidental permanent total disability

*As designed by ICICI Lombard (IL). For complete details refer addendum to the respective Offer Document

20

Product features/coverage

Who is covered?

– Age completed as on last birthday is 20yrs to 50 yrs

Sum insured– SIP amount x Total tenure in months

– Example: if an investors takes a monthly SIP of Rs. 15,000 for 60 months, the sum insured is Rs.9,00,000

– Minimum HSBC SIP Plus amount of Rs.2000* monthly for minimum period of 36 months

– Maximum cover of Rs.10 lakhs irrespective of multiple SIPs. Not available to NRI’s

Period of the critical illness cover– Insurance tenure = SIP tenure

– Available in multiples of 1 yr

– Subject to a maximum tenure of 5 yrs

*Investments of lower amounts can be made through our regular HSBC SIP

21

SIP Plus available on the following Schemes

HSBC Equity Fund

HSBC India Opportunities Fund

HSBC Midcap Equity Fund*

HSBC Advantage India Fund

HSBC Dynamic Fund

HSBC Tax Saver Equity Fund

*The Trustees/AMC reserve the right to temporarily suspend subscriptions, switches into the Scheme, if the assets under management of the Scheme exceeds Rs 700 Crores. Please read Offer Document for more details.

All STP’s into the above mentioned Schemes that meet the minimum criteria are also eligible for the

cover

22

Customer’s nominee to intimate ICICI Lombard Call center in case of any claim. For policy details or for lodging a claim, please

visit the website www.icicilombard.com

ICICI Lombard (IL) intimates the claimant about the documents requirement

IL collects the documents as mentioned from the customer

In case of incomplete forms, ICICI Lombard writes back to Customer asking for the pending documents

ICICI Lombard’s Customer service department to decide the admissibility of any claim after receiving the documents and

investigation report, if applicable

On admissibility, the payment will be made. The payment will be made within 7 days of receipt of all complete documents

In case, the documents are not received form the customer within 3 months of intimation the claim would be closed. However

before closing the claim ICICI Lombard would send a letter to customer that the claim is closed because of non-receipt of

documents

The loss should be reported in writing to the insurance company/call center within 90 days of happening of the event

Any claim due to violation of law or misrepresentation, concealing of facts would not be eligible for any payment

The communication contains only some illustrative elements of the policy. In case of any queries on terms and conditions,

kindly get in touch with ICICI Lombard Call centre

Claims process

23

Documents Required for Claims

Accidental death cover– Claim Form – Death Certificate, FIR and Police Report– Doctor’s report and/ or Post-mortem report– No objection and indemnity letter

Accidental permanent total disability cover– Claim Form – FIR and Police Report – Doctor’s disability Report– Investigation reports such as laboratory tests, X-rays & reports essential for confirmation of

injury

Critical illness cover – Claim Form– Doctor’s certificate confirming the nature and medical details of the illness– Other relevant medical reports– Any other document as may be required

24

Product Exclusions

Critical illness cover

– Any of the critical illnesses diagnosed within the first 3 months of the inception of the policy

– Pre-existing illness

– Requires survival period of 1 month post first diagnosis

Accidental death cover

– Caused by mental disorder or psychosomatic dysfunction

Accidental permanent total disability cover

– Will not cover any injury, sickness or disease for which medical care, treatment, or advice was

recommended by or received from a Doctor or from which the Insured Person suffered or

which was present before the commencement of the Period of Insurance

25

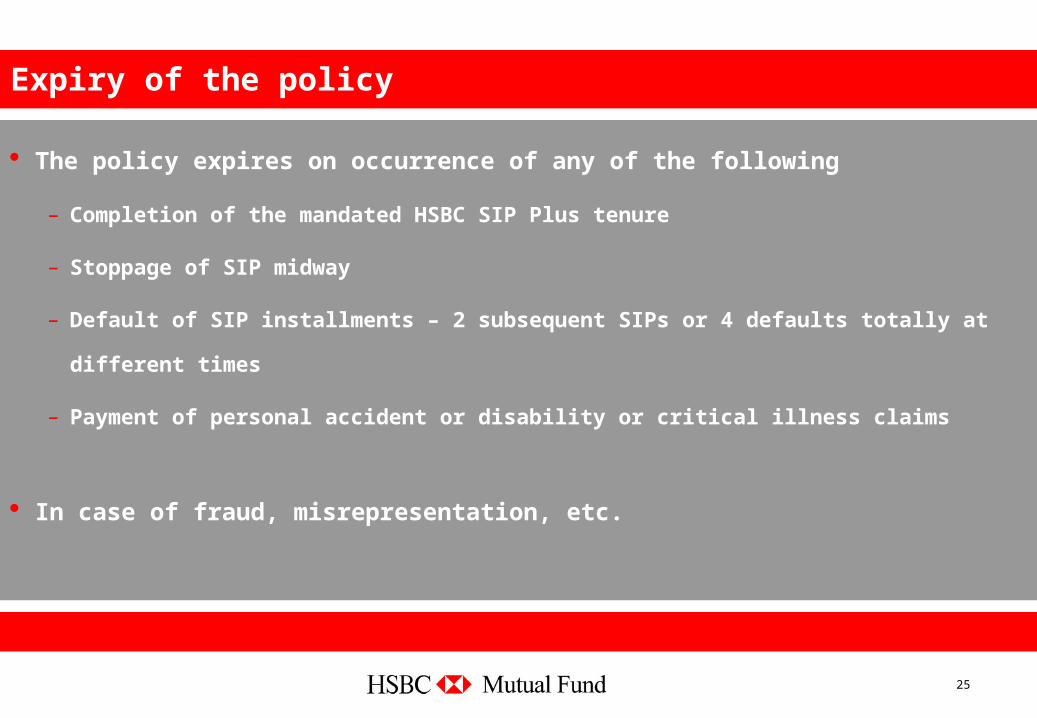

Expiry of the policy

The policy expires on occurrence of any of the following

– Completion of the mandated HSBC SIP Plus tenure

– Stoppage of SIP midway

– Default of SIP installments – 2 subsequent SIPs or 4 defaults totally at different times

– Payment of personal accident or disability or critical illness claims

In case of fraud, misrepresentation, etc.

26

HSBC SIP Plus A little every month can help fulfil your dreams

and cover your health

27

Disclaimer

All returns have been sourced from MutualFundsIndia Explorer software unless otherwise stated. With regard to equity schemes (including the equity component of MIPs), Fund performance is calculated on a total return basis (i.e. it includes dividends re-invested) while the benchmark is calculated on a price return basis (i.e. it does not consider dividends re-invested).

This document has been prepared by HSBC Asset Management (India) Private Limited (HSBC) for information purposes only and should not be construed as an offer or solicitation of an offer for purchase of any of the funds of HSBC Mutual Fund. All information contained in this document (including that sourced from third parties), is obtained from sources HSBC, the third party believes to be reliable but which it has not independently verified and HSBC, the third party makes no guarantee, representation or warranty and accepts no responsibility or liability as to the accuracy or completeness of such information. The information and opinions contained within the document are based upon publicly available information and rates of taxation applicable at the time of publication, which are subject to change from time to time. Expressions of opinion are those of HSBC only and are subject to change without notice. It does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies that may have been discussed or recommended in this report and should understand that the views regarding future prospects may or may not be realized. Neither this document nor the units of HSBC Mutual Fund have been registered in any jurisdiction. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. Mutual fund investments are subject to market risks. Please read the offer documents carefully before investing.

© Copyright. HSBC Asset Management (India) Private Limited 2007, ALL RIGHTS RESERVED.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management (India) Private Limited.

HSBC Asset Management (India) Private Limited; 314, D. N. Road, Fort, Mumbai 400 001. Tel: 6614 8819.

28

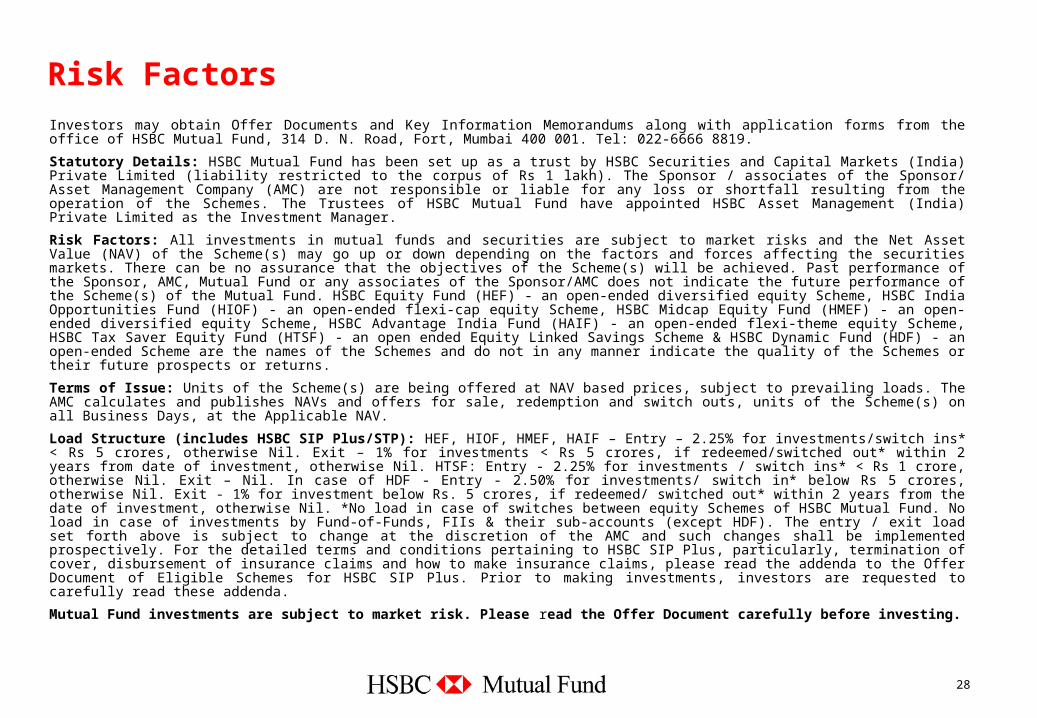

Risk Factors

Investors may obtain Offer Documents and Key Information Memorandums along with application forms from the office of HSBC Mutual Fund, 314 D. N. Road, Fort, Mumbai 400 001. Tel: 022-6666 8819.

Statutory Details: HSBC Mutual Fund has been set up as a trust by HSBC Securities and Capital Markets (India) Private Limited (liability restricted to the corpus of Rs 1 lakh). The Sponsor / associates of the Sponsor/ Asset Management Company (AMC) are not responsible or liable for any loss or shortfall resulting from the operation of the Schemes. The Trustees of HSBC Mutual Fund have appointed HSBC Asset Management (India) Private Limited as the Investment Manager.

Risk Factors: All investments in mutual funds and securities are subject to market risks and the Net Asset Value (NAV) of the Scheme(s) may go up or down depending on the factors and forces affecting the securities markets. There can be no assurance that the objectives of the Scheme(s) will be achieved. Past performance of the Sponsor, AMC, Mutual Fund or any associates of the Sponsor/AMC does not indicate the future performance of the Scheme(s) of the Mutual Fund. HSBC Equity Fund (HEF) - an open-ended diversified equity Scheme, HSBC India Opportunities Fund (HIOF) - an open-ended flexi-cap equity Scheme, HSBC Midcap Equity Fund (HMEF) - an open-ended diversified equity Scheme, HSBC Advantage India Fund (HAIF) - an open-ended flexi-theme equity Scheme, HSBC Tax Saver Equity Fund (HTSF) - an open ended Equity Linked Savings Scheme & HSBC Dynamic Fund (HDF) - an open-ended Scheme are the names of the Schemes and do not in any manner indicate the quality of the Schemes or their future prospects or returns.

Terms of Issue: Units of the Scheme(s) are being offered at NAV based prices, subject to prevailing loads. The AMC calculates and publishes NAVs and offers for sale, redemption and switch outs, units of the Scheme(s) on all Business Days, at the Applicable NAV.

Load Structure (includes HSBC SIP Plus/STP): HEF, HIOF, HMEF, HAIF – Entry – 2.25% for investments/switch ins* < Rs 5 crores, otherwise Nil. Exit – 1% for investments < Rs 5 crores, if redeemed/switched out* within 2 years from date of investment, otherwise Nil. HTSF: Entry - 2.25% for investments / switch ins* < Rs 1 crore, otherwise Nil. Exit – Nil. In case of HDF - Entry - 2.50% for investments/ switch in* below Rs 5 crores, otherwise Nil. Exit - 1% for investment below Rs. 5 crores, if redeemed/ switched out* within 2 years from the date of investment, otherwise Nil. *No load in case of switches between equity Schemes of HSBC Mutual Fund. No load in case of investments by Fund-of-Funds, FIIs & their sub-accounts (except HDF). The entry / exit load set forth above is subject to change at the discretion of the AMC and such changes shall be implemented prospectively. For the detailed terms and conditions pertaining to HSBC SIP Plus, particularly, termination of cover, disbursement of insurance claims and how to make insurance claims, please read the addenda to the Offer Document of Eligible Schemes for HSBC SIP Plus. Prior to making investments, investors are requested to carefully read these addenda.

Mutual Fund investments are subject to market risk. Please read the Offer Document carefully before investing.

Thank You

HSBC Mutual Fund July 2007

![Welcome [] · HSBC Reward+ is a mobile app dedicated to HSBC Credit Card customers in Hong Kong. With HSBC Reward+, you can use With HSBC Reward+, you can use your RewardCash, browse](https://static.fdocuments.net/doc/165x107/5e158a930ded3378e33b0c9f/welcome-hsbc-reward-is-a-mobile-app-dedicated-to-hsbc-credit-card-customers.jpg)