Symantec Envisions Future Clouds As Safe Clouds November 2012

How Various Clouds Are Affecting Services Delivery in SEE, Your Opportunity! Vladimir Kroa

IDC CEMA, Prague

AGENDA

NEW AGE OF IT • EVOLUTION OF REQUIREMENTS • DIGITAL TRANSFORMATION

CONVERGENCE AT HYBRID SOLUTION? • WHAT OPTIONS USERS HAVE? • HOW WE INTEGRATE

WHAT DO THE USERS SAY? • FOLLOW THE MONEY • SEIZE THE OPPORTUNITY!

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 2

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 3

1980

2007

2012+

IT PLATFORMS IN PERSPECTIVE

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 4

CURRENT IT IS DRIVEN BY DIGITAL TRANSFORMATION

3rd Platform dominates IT industry growth: § Up by 15% § 29% of IT spending § 89% of growth

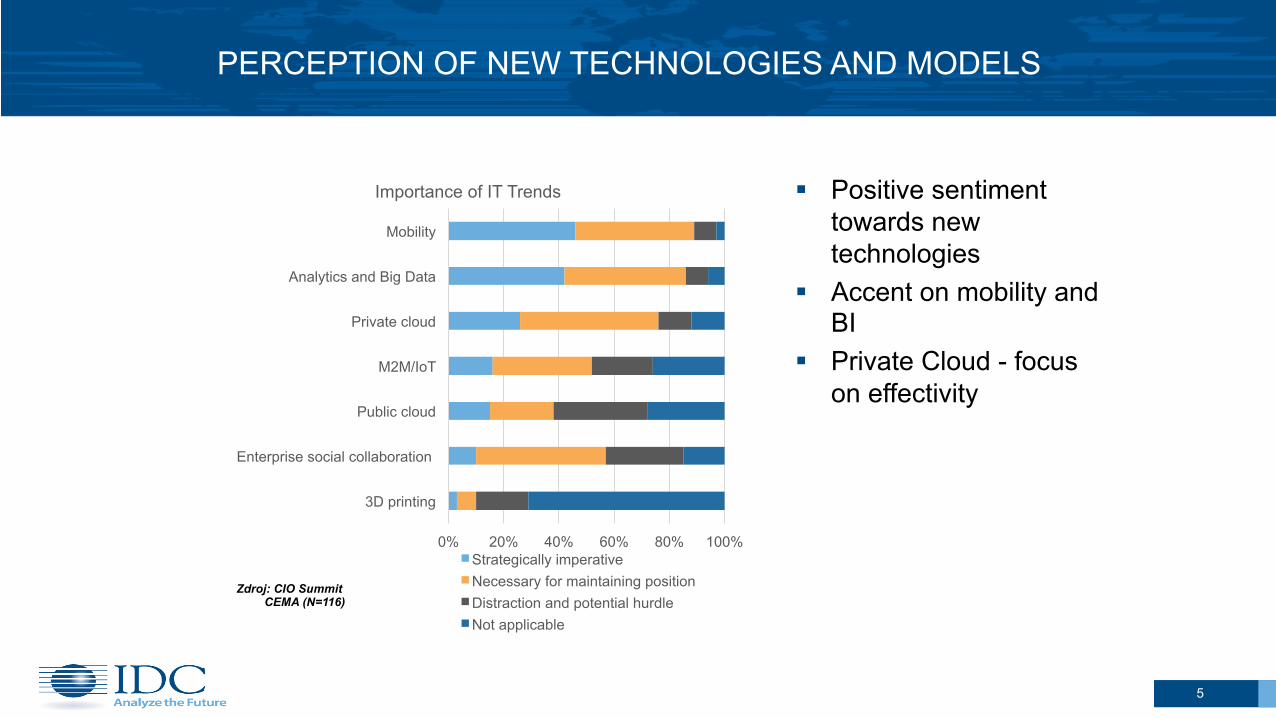

PERCEPTION OF NEW TECHNOLOGIES AND MODELS

0% 20% 40% 60% 80% 100%

3D printing

Enterprise social collaboration

Public cloud

M2M/IoT

Private cloud

Analytics and Big Data

Mobility

Importance of IT Trends

Strategically imperative Necessary for maintaining position Distraction and potential hurdle Not applicable

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 5

§ Positive sentiment towards new technologies

§ Accent on mobility and BI

§ Private Cloud - focus on effectivity

Zdroj: CIO Summit CEMA (N=116)

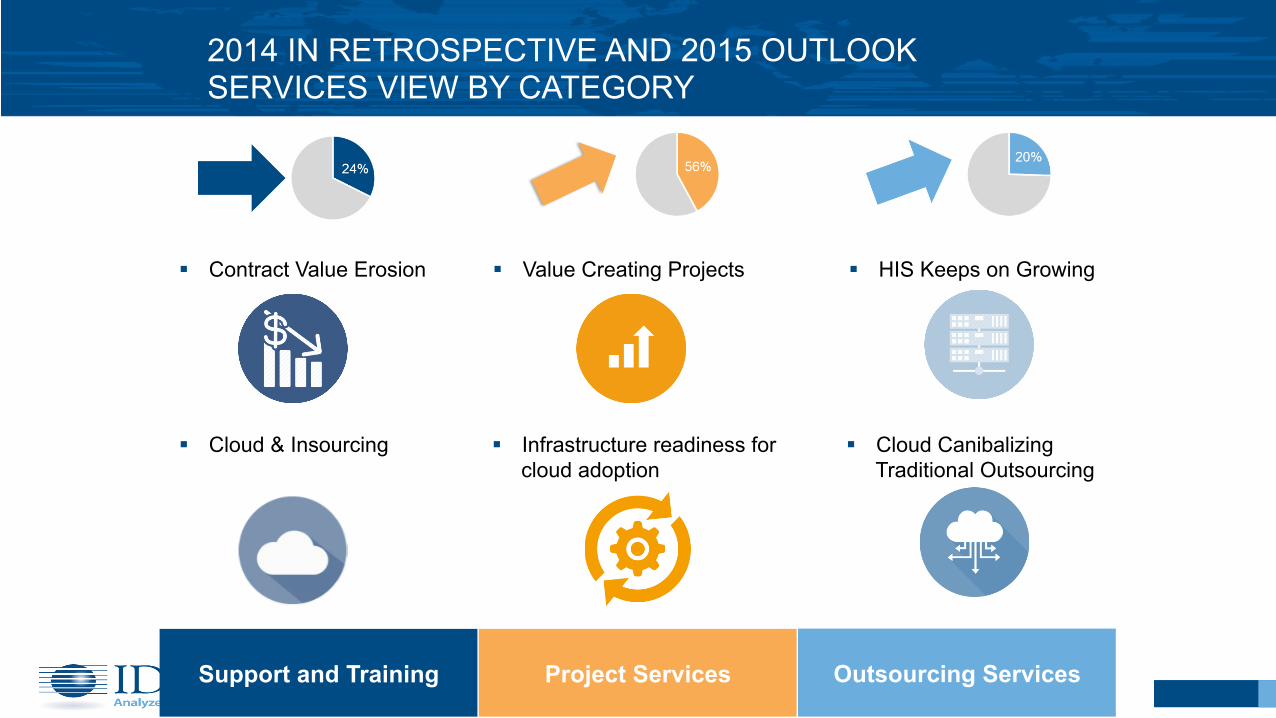

2014 IN RETROSPECTIVE AND 2015 OUTLOOK SERVICES VIEW BY CATEGORY

6 Support and Training Project Services Outsourcing Services

§ Contract Value Erosion

§ Cloud & Insourcing § Infrastructure readiness for cloud adoption

§ Cloud Canibalizing Traditional Outsourcing

§ HIS Keeps on Growing § Value Creating Projects

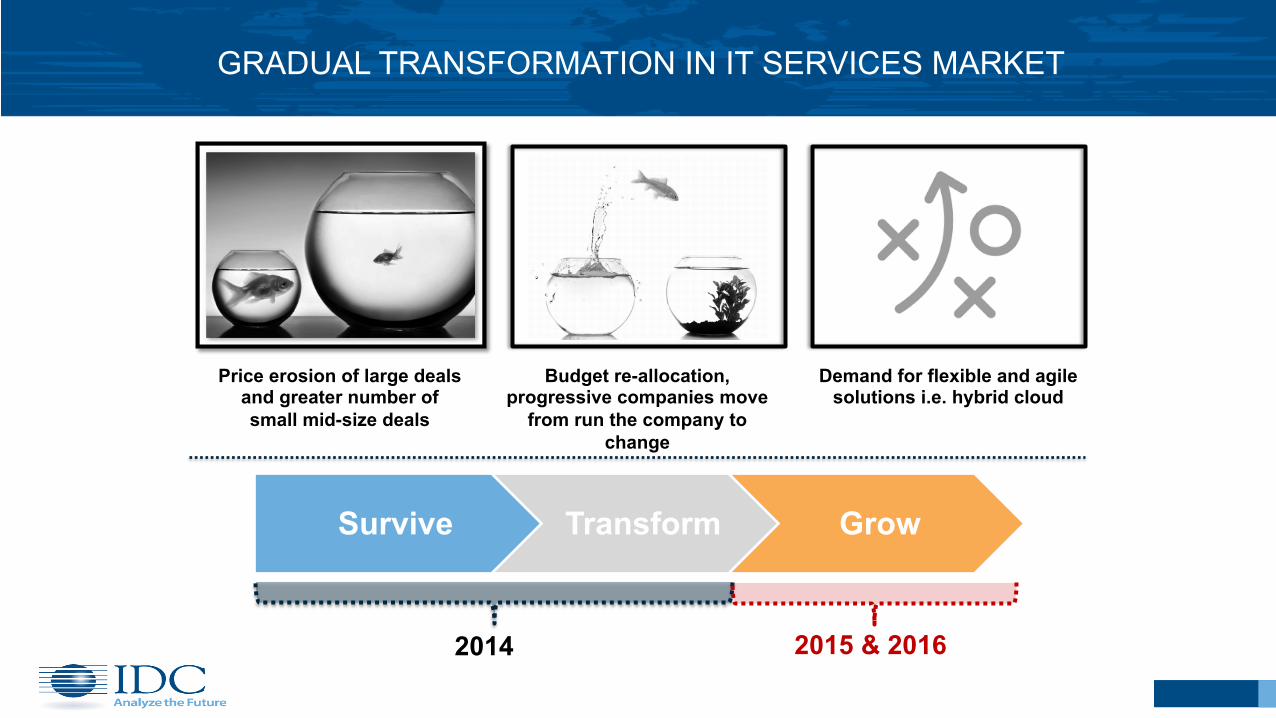

GRADUAL TRANSFORMATION IN IT SERVICES MARKET

Price erosion of large deals and greater number of small mid-size deals

7

Budget re-allocation, progressive companies move

from run the company to change

Demand for flexible and agile solutions i.e. hybrid cloud

Survive Transform Grow

2014 2015 & 2016

Private Infrastructure & Operations

Shared Infrastructure &

Operations

Private Infrastructure & Operations

Private Infrastructure &

Shared Operations

IT

Hybrid Cloud

Public Cloud

Outsourcing Legacy IT

Private Cloud

MANAGING THE IT MAZE

8

On-demand, Virtual, Automated

Scheduled, Physical, Manual

Supplier Control, Ownership, Responsibility

Customer Control, Ownership, Responsibility

© IDC Visit us at IDC.com and follow us on Twitter: @IDC

AGENDA

NEW AGE OF IT • EVOLUTION OF REQUIREMENTS • DIGITAL TRANSFORMATION

CONVERGENCE AT HYBRID SOLUTION? • WHAT OPTIONS USERS HAVE? • HOW WE INTEGRATE

WHAT DO THE DATA IMPLY? • FOLLOW THE MONEY • SEIZE THE OPPORTUNITY!

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 9

CLOUD SERVICE DEPLOYMENT MODELS

Self-run private cloud

Dedicated/single-tenant delivery platform Shared/multitenant delivery platform

Managed private cloud

Dedicated private cloud

Virtual private cloud

Public cloud

Hosted private cloud

Customer site Service provider site

10

§ Shared, standard service § Solution-packaged § Self-service § Elastic scaling

§ Use-based pricing § Accessible via the Internet § Standard UI technologies § Published service interface/API

Characteristics and definitions of cloud services

Source: IDC European Cloud Strategies CIS, 2014

© IDC Visit us at IDC.com and follow us on Twitter: @IDC

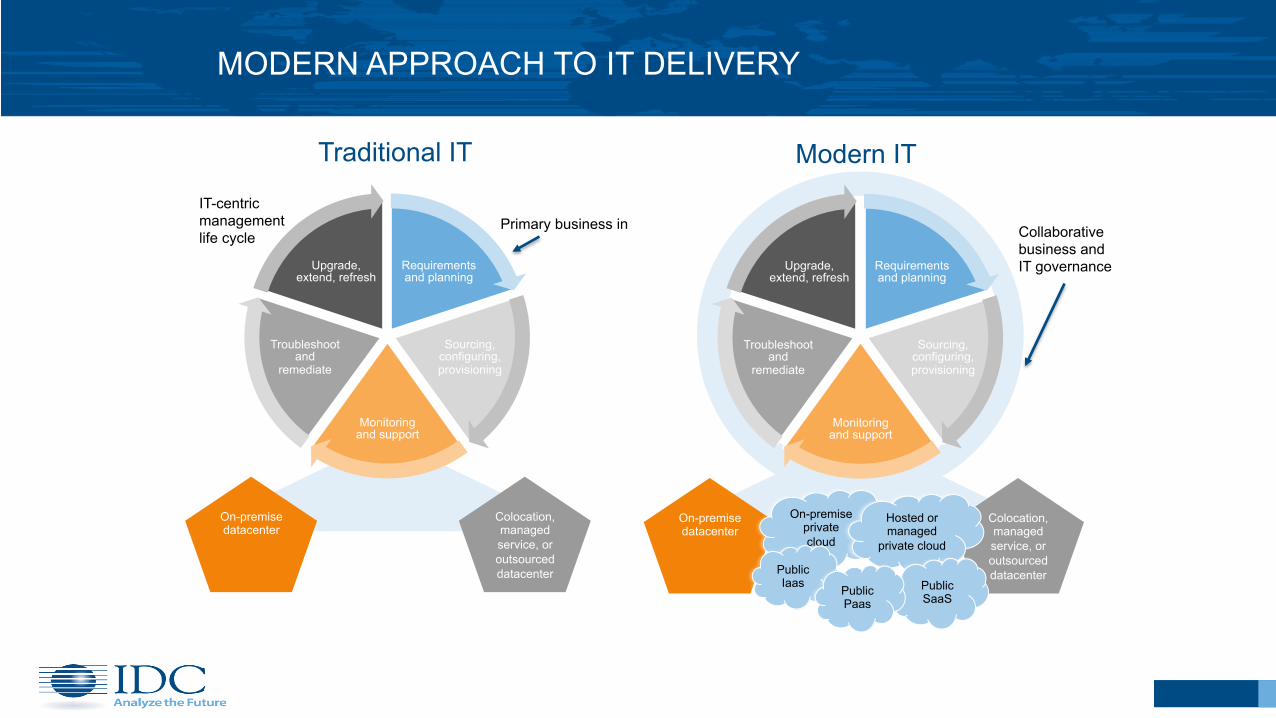

MODERN APPROACH TO IT DELIVERY

Requirements and planning

Sourcing, configuring, provisioning

Monitoring and support

Troubleshoot and

remediate

Upgrade, extend, refresh

Requirements and planning

Sourcing, configuring, provisioning

Monitoring and support

Troubleshoot and

remediate

Upgrade, extend, refresh

Colocation, managed service, or outsourced datacenter

On-premise datacenter

Colocation, managed service, or outsourced datacenter

On-premise datacenter

On-premise private cloud

Hosted or managed

private cloud

Public SaaS

Public Iaas Public

Paas

Traditional IT Modern IT

Primary business in Collaborative business and IT governance

IT-centric management life cycle

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 11

OPPORTUNITIES FOR 3RD. PARTY SERVICES

§ Core business focus § IoT, mobile and big data are the triggers

ü Cloud will be the key platform to support ü IT is becoming inherent in various industries

§ Economical reasons - Cloud with more standardized approach will be more economical than outsourcing

§ Hybrid cloud – integrating on – premise with datacenters with variety of public clouds

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 12

CHALLENGES AND THINGS TO CONSIDER – MIGRATION 2 CLOUD

1. Processes – audit, categorization 2. Business SLA 3. Portability & Workload Mobility 4. Legal aspects:

a) Compliance b) Legal, Safe Harbor

5. Branches connectivity 6. Complex TCO

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 13

DATACENTER DISRUPTION DUE TO THE CLOUD ADOPTION

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 14

Flash • 40% of external

storage revenue is flash-optimized

Cloud • 46% use Cloud

for Backup Software Defined

• 24% have already invested

Convergence • 15% of storage

spending is driven by converged systems

Readiness for Inter-Operability with on Premise Systems OpenSource / OpenStack

AGENDA

NEW AGE OF IT • EVOLUTION OF REQUIREMENTS • DIGITAL TRANSFORMATION

CONVERGENCE AT HYBRID SOLUTION? • WHAT OPTIONS USERS HAVE? • HOW WE INTEGRATE

WHAT DO THE USERS SAY? • FOLLOW THE MONEY • SEIZE THE OPPORTUNITY!

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 15

IT AND CLOUD BUDGET DISTRIBUTION OVER TIME

16

[Q3] Please estimate what percentage of your organization’s total annual IT budget is allocated to each of the following procurement/management models.

External Cloud: 40.8%

Today In 24 Months Non-cloud: 43.6% Cloud: 56.4% (34% growth)

Non-cloud: 57.9% Cloud: 42.1%

External Cloud: 31.4%

Provider Site:

52.9%

Customer Site:

47.1%

Provider Site: 56.8%

Customer Site: 43.2

Source: IDC CloudView Survey 2014, n=2378 worldwide IT respondents

Traditional Outsourced

(eg., Application Management)

21.5%

Dedicated Private Cloud 6.5%

Virtual Private Cloud 5.5%

Public Cloud 19.5%

Traditional In-house 35.4%

In-house Private Cloud 10.7%

Virtual Private Cloud 10.8%

Dedicated Private Cloud 12.0%

Public Cloud 17.9%

Traditional Outsourced

(eg., Application Manageme

nt) 21.5%

Traditional In-house 27.5%

In-house Private Cloud 15.7%

+ 12 pts.

17

HYBRID CLOUD DEFINITIONS AND ADOPTION

[Q2b] Has your organiza-on adopted a Hybrid Cloud strategy?

Source: IDC CloudView Survey 2014, n=3463 worldwide respondents

Currently Implemented Hybrid Cloud

Have firm plans for Hybrid Cloud within 12 months

Aspirations for Hybrid Cloud, but no firm plans

Hybrid Cloud not an area of focus 7.70%

17.50%

31.10%

40.90%

18

Per

cent

age

of R

espo

nden

ts

50%

40%

30%

20%

10%

0%

Acc

entu

re

Am

azon

AT

&T

Ato

s B

ell C

anad

a B

MC

C

itrix

C

isco

C

SC

C

A Te

chno

logi

es

Del

l E

MC

Fu

jitsu

G

oogl

e H

P/E

DS

IB

M

Info

rmat

ica

Mic

roso

ft N

EC

N

etsu

ite

Ora

cle

Rac

kspa

ce

Red

Hat

S

ales

forc

e.co

m

SA

P C

entu

ryLi

nk

Telu

s Ve

rizon

V

Mw

are

Wor

kday

O

ther

2nd place votes

1st place votes

4th place votes

3rd place votes

5th place votes

MOST QUALIFIED PRIVATE CLOUD VENDORS – ALL NORTH AMERICAN RESPONDENTS

[Q14b] Which of the following companies do you perceive as being the most qualified to support your organiza-on’s building and opera-ng of Private clouds (running at your company site)?

Source: IDC CloudView Survey, 2014, n=682 North American IT respondents

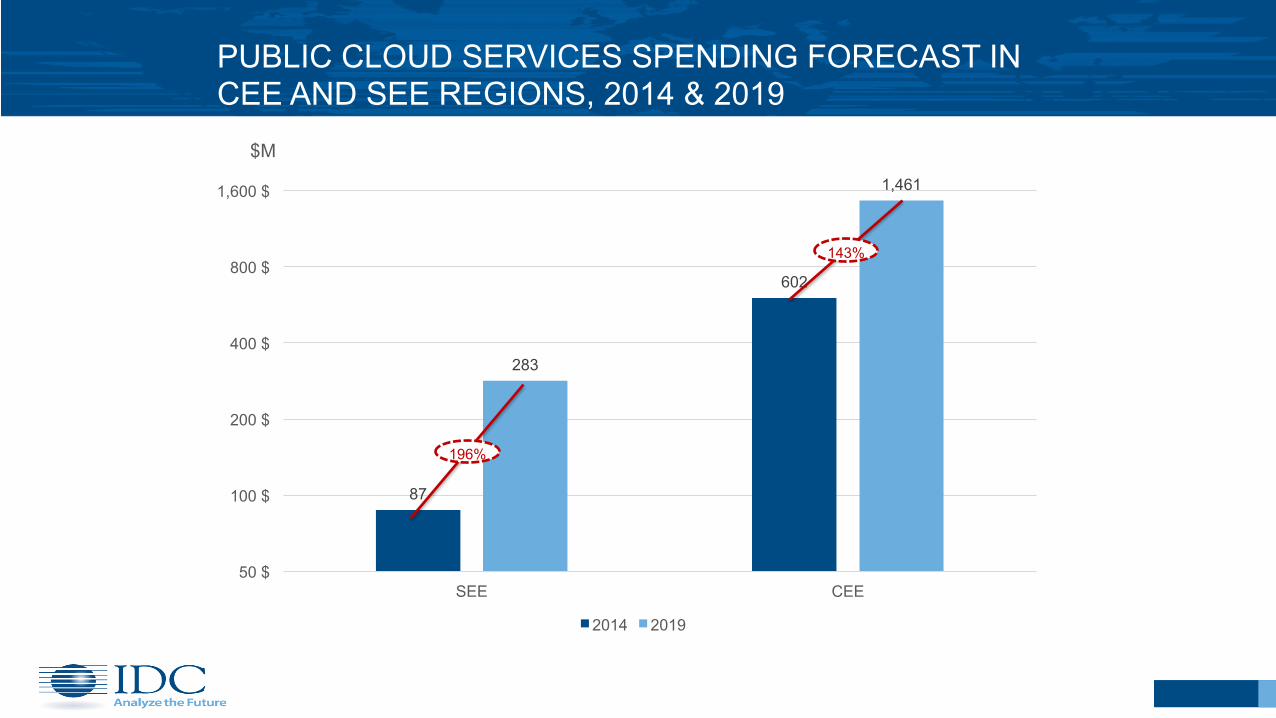

PUBLIC CLOUD SERVICES SPENDING FORECAST IN CEE AND SEE REGIONS, 2014 & 2019

19

87

602

283

1,461

50 $

100 $

200 $

400 $

800 $

1,600 $

SEE CEE

2014 2019

$M

196%

143%

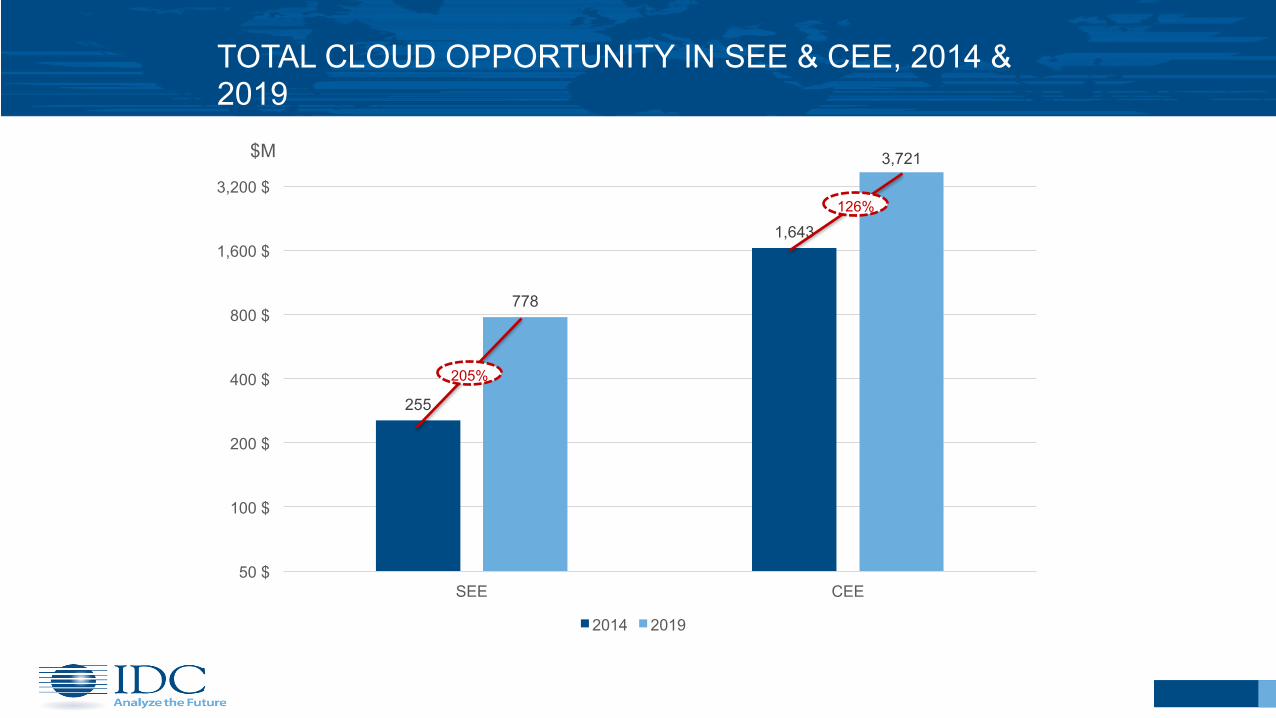

TOTAL CLOUD OPPORTUNITY IN SEE & CEE, 2014 & 2019

20

255

1,643

778

3,721

50 $

100 $

200 $

400 $

800 $

1,600 $

3,200 $

SEE CEE

2014 2019

$M

205%

126%

CONCLUSION

ü Business Requirements Call for Efficiency, Innovation & Flexibility

ü Hybrid Converged Solutions Answers Demand for Security, Privacy and Integration

ü SIs and VARs Can Tap into This 200% Growth Bonanza in SEE

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 21