HOW TO ADMINISTER AN ESTATE IN NEW · PDF fileHOW TO ADMINISTER AN ESTATE IN NEW JERSEY...

30

HOW TO ADMINISTER AN ESTATE IN NEW JERSEY Douglas A. Fendrick, Esquire FENDRICK & MORGAN, LLC 1307 White Horse Road Voorhees, NJ 08043 Phone: 856/489-8388 www.FENDRICKMORGANLAW.COM [email protected]

-

Upload

hoangthien -

Category

Documents

-

view

217 -

download

2

Transcript of HOW TO ADMINISTER AN ESTATE IN NEW · PDF fileHOW TO ADMINISTER AN ESTATE IN NEW JERSEY...

HOW TO ADMINISTER AN ESTATE IN NEW JERSEY

Douglas A. Fendrick, Esquire FENDRICK & MORGAN, LLC

1307 White Horse Road Voorhees, NJ 08043

Phone: 856/489-8388 www.FENDRICKMORGANLAW.COM

INTRODUCTION

If the decedent had a Will then the executor should read the Will

thoroughly so that he or she completely understands all of its provisions. In order for a

document to be considered a will, the statutory requirements of the state in which the

testator resides must be met. These requirements will vary from state to state. In general,

they will set forth a minimum age requirement for a testator (typically eighteen years of

age) as well as the number of witnesses required to ensure the validity of a typewritten

will or to make the Will self-proving. The statutory requirements for the execution of a

Will in New Jersey are contained in N.J.S.A. 3B:-1 and 3B:-2.

In significant part, this statute states, “Any person eighteen (18) or more years of

age who is of sound mind may make a Will and appoint a Testamentary Guardian.” The

Will shall be signed by the Testator, and shall also be signed by at least two (2) persons,

each of whom witnessed the signing of the Testator’s signature of the Will. To avoid the

necessity of the executor producing the witnesses at probate, N.J.S.A. 3B:3-4 provides

that a Will, executed in compliance with N.J.S.A. 3B:3-2 “may be simultaneously

executed, attested, and made self-proved by the acknowledgment thereof by the Testator

and Affidavits of the witnesses, each made before an officer authorized” (i.e. an attorney

or notary public) to take acknowledgments and proofs of instruments in the State of New

Jersey.

I PROBATE IF DECEDENT HAD A WILL

If a decedent had executed a Last Will and Testament, then the Will should be

probated at the Surrogate’s Court in the county where the decedent was domiciled at the

time of death. Although there is a statutory ten-day waiting period after death before a

Will can be admitted to probate, the process may nevertheless begin before such waiting

period has expired and the Surrogate’s Court will hold the papers until that time.

Each Surrogate’s Court has procedures which must be followed to probate a Will.

In New Jersey Rule 4:80 and Rule 4:81 deal with the routine matters typically handled by

the Surrogate's Court. These matters are initiated in the Surrogate's Court by an

application. It is only in the Superior Court that actions are instituted by a Complaint.

Rule 4:80-1(a) sets forth the following items which must be included in a probate action

which is filed with the Surrogates Court:

A. Applicant's residence.

B. Name and date of death of decedent, domicile at the time of

death, and date of Will if any.

C. Names and addresses of the decedent's spouse, if any,

decedent's heirs, next-of-kin and other persons entitled to letters and their relationships to

the decedents.

D. Ages of any minor heirs or minor next-of-kin and in an

application for probate of a Will, whether the Testator had issue living when the Will was

made, whether he left any child born thereafter, or any issue of such after-born child,

whether he left any child adopted thereafter, or any issue of such adopted child, and the

names of after-born children and children adopted since the date of the Will or their issue,

if any.

I I INTESTATE ADMINISTRATION

If the decedent died without leaving a Will, then an application must be made to

the Surrogate’s Court to have an administrator (not an executor) appointed. If there is a

surviving spouse, he or she has priority to be appointed as administrator. If there is no

surviving spouse or the spouse renounces the right to serve as administrator, then the

next-of-kin (those persons who inherit under the New Jersey intestacy law, as discussed

below) may apply to become the administrator, in the order in which they would so

inherit. A person applying to become administrator must obtain renunciations from all

persons whose priority is equal to or greater than that of the applicant. In lieu of such

renunciations, the applicant may send notices to the other heirs who have equal or greater

priority.

Unlike the probate procedures where the decedent left a Will, in an

intestate estate the administrator must post a bond with the Surrogate’s Court, unless the

administrator is the surviving spouse and the sole beneficiary of the estate. The bond

premium is an expense to be paid out of the estate funds and is charged on an annual

basis. The administration bond can be obtained from a surety company which is

approved by the Surrogate’s Court.

Where an individual dies without a will, or where an individual dies with a

will but the will fails to dispose of all of the decedent’s property, the portion of the

decedent’s estate not effectively disposed of by will passes by intestate succession in

accordance with the provisions of N.J.S.A. 3B:5-3 – N.J.S.A. 3B:5-14. N.J.S.A. 3B:5-

2(a).

A. Distributing Assets

In determining how assets are to be distributed in the case of an intestate

estate in the State of New Jersey, you first must determine what the surviving spouse

or civil union partner, (hereinafter referred to as “domestic partner”) if any, is

entitled to receive. N.J.S.A. 3B:5-3. The surviving spouse or civil union partner is

entitled to:

(i). The entire intestate estate IF:

a. No descendant or parent of the decedent survives the decedent;

or

b. All of the decedent's surviving descendants are also

descendants of the surviving spouse or domestic partner and there is no other

descendant of the surviving spouse or domestic partner who survives the decedent;

(ii) The first 25% of the intestate estate, but not less than $50,000 nor

more than $200,000, plus three-fourths (3/4) of any balance of the intestate estate, if

no descendant of the decedent survives the decedent, but a parent of the decedent

survives the decedent;

(iii). The first 25% of the intestate estate, but not less than $50,000 nor

more than $200,000, plus one-half of the balance of the intestate estate if:

a. All of the decedent's surviving descendants are also

descendants of the surviving spouse or domestic partner and the surviving spouse or

domestic partner has one or more surviving descendants who are not descendants of

the decedent; or

b. One or more of the decedent's surviving descendants is not

a descendant of the surviving spouse or domestic partner.

(iv). The balance of the decedent’s estate not passing to the surviving

spouse or domestic partner, or the entire estate if there is no surviving spouse or

domestic partner, is to be distributed in accordance with N.J.S.A. 3B:5-4 as follows:

a. To the decedent's descendants by representation;

b. If there are no surviving descendants, to the decedent's

parents equally if both survive, or to the surviving parent;

c. If there are no surviving descendants or parent, to the

descendants of the decedent's parents or either of them by representation;

d. If there is no descendant, parent or descendant of a parent,

but the decedent is survived by one or more grandparents, half of the estate passes to the

decedent's paternal grandparents equally if both survive, or to the surviving paternal

grandparent, or to the descendants of the decedent's paternal grandparents or either of

them if both are deceased, the descendants taking by representation; and the other half

passes to the decedent's maternal relatives in the same manner; but if there is no surviving

grandparent, or descendant of a grandparent on either the paternal or the maternal side,

the entire estate passes to the decedent's relatives on the other side in the same manner as

the half.

e. If there is no surviving descendant, parent, descendant of a

parent, or grandparent, but the decedent is survived by one or more descendants of

grandparents, the descendants take equally if they are all of the same degree of kinship to

the decedent, but if of unequal degree those of more remote degree take by

representation.

f. If there are no surviving descendants of grandparents, then

the decedent's step-children or their descendants by representation.

Additionally, and notwithstanding the foregoing, where the total value of the

decedent’s real and personal property does not exceed $20,000, the surviving spouse or

domestic partner, as the case may be, shall be entitled absolutely “to all the real and

personal assets without administration, and the assets of the estate up to $5,000.00 shall

be free from all debts of the intestate.” The surviving spouse or domestic partner must

execute an affidavit before the Surrogate of the county where the intestate decedent

resided at his death, or, if then nonresident in this State, where any of the assets are

located, or before the Superior Court. The affidavit must state that the affiant is the

surviving spouse or domestic partner of the intestate and that the value of the intestate's

real and personal assets will not exceed $20,000, and shall set forth the residence of the

intestate at his death, and specifically the nature, location and value of the intestate's real

and personal assets. The affidavit shall be filed and recorded in the office of such

Surrogate or, if the proceeding is before the Superior Court, then in the office of the clerk

of that court. Where the affiant is domiciled outside this State, the Surrogate may

authorize in writing that the affidavit be executed in the affiant's domicile before any of

the officers authorized by R.S.46:14-7 and R.S.46:14-8 to take acknowledgments or

proofs. Upon the execution and filing of such affidavit, the surviving spouse or domestic

partner will have all of the rights, powers and duties of an administrator duly appointed

for the estate. The surviving spouse or domestic partner may be sued and required to

account as if he had been appointed administrator by the Surrogate or the Superior Court.

N.J.S.A. 3B:10-3.

Where the total value of an intestate estate will not exceed $10,000 and the

intestate decedent died leaving no spouse or domestic partner, if any one heir can obtain

the consent of the remaining heirs (if any), in writing, and such heir has executed before

the Surrogate of the county where the intestate resided at his death (or, if then nonresident

in this State, where any of the intestate's assets are located, or before the Superior Court),

an affidavit (as described below), such heir shall be entitled to receive the assets of the

intestate estate for the benefit of all the heirs and creditors without administration or

entering into a bond. Upon executing the affidavit, and upon filing it and the consent, the

appointed heir shall have all the rights, powers and duties of an administrator duly

appointed for the estate and may be sued and required to account as if he had been

appointed administrator by the Surrogate or the Superior Court. The affidavit shall set

forth the residence of the intestate at his death, the names, residences and relationships of

all of the heirs and specifically the nature, location and value of the real and personal

assets and also a statement that the value of the intestate's real and personal assets will

not exceed $10,000. The consent and the affidavit shall be filed and recorded, in the

office of the Surrogate or, if the proceeding is before the Superior Court, in the office of

the clerk of that court. Where the affiant is domiciled outside this State, the Surrogate

may authorize in writing that the affidavit be executed in the affiant's domicile before any

of the officers authorized by R.S.46:14-7 and R.S.46:14-8 to take acknowledgments or

proofs. N.J.S.A. 3B:10-4.

Additionally, an individual may, in his or her will, expressly include or exclude

the right of an individual or class to succeed to his or her property which passes by

intestate succession. Where a decedent expressly excludes, for example, a member of a

class in the decedent’s Will and that excluded individual survives the decedent, the share

of the decedent’s estate which might have otherwise passed to such excluded individual

is to pass as if that excluded individual disclaimed his or her intestate share (and,

therefore, as if he or she predeceased the decedent). N.J.S.A. 3B:5-2.

For purposes of the intestacy statutes, if it cannot be determined by clear and

convincing evidence that an individual survived the decedent by 120 hours, that

individual is deemed to have predeceased the decedent. N.J.S.A. 3B:5-1.

B. Priority of Administrators

When an individual dies without a will, not only have they failed to direct how

their assets will be distributed, but they have also failed to designate an executor to

administer the estate. In the absence of an executor’s appointment, N.J.S.A. 3B:10-2

provides that a personal representative (“administrator”) shall be appointed in the

following order of priority: (1) the surviving spouse or domestic partner, (2) the

remaining heirs of the intestate estate, or, if none, (3) any other person who will accept

the appointment. If the intestate estate leaves no heirs entitled to administer the estate, of

if the heirs do not claim the administration within forty (40) days of the decedent’s death,

the Superior Court ort the surrogate’s court may grant letters of administration to any

person who applies for letters. A person applying to become administrator must obtain

renunciations from all persons whose priority is equal to or greater than that of the

applicant. In lieu of such renunciations, the applicant may send notices to the other heirs

who have equal or greater priority.

Unlike the probate procedures where the decedent left a Will, in an intestate

estate, the administrator must post a bond with the Surrogate’s Court, unless the

administrator is the surviving spouse and the sole beneficiary of the estate. The bond

premium is an expense to be paid out of the estate funds and is charged on an annual

basis. The administration bond can be obtained from a surety company which is

approved by the Surrogate’s Court.

III. LOST/WITHHELD WILLS

A. Lost Wills

Recent studies have estimated that only 41% of the adults in our country have

Wills. If you die without having a will then your estate will be governed by the intestacy

laws of the state in which you reside at the time of your death. Furthermore, if you are

one of the 41% who have prepared a last will and testament then it is extremely important

that somebody knows where you keep your original will. Common law in New Jersey

provides that if a will is last known to have been in the decedent’s possession and the will

cannot be found after the decedent’s death, there is a rebuttable presumption that the will

was destroyed and, therefore, the intestacy rules would govern the estate administration.

To overcome that presumption, the moving party has the burden of convincing the court

that, more likely than not, the will was not destroyed.

A photocopy of a will can be admitted to probate by the Superior Court, Chancery

Division, but not by the surrogate court. Accordingly, where the original will cannot be

located, a verified complaint and an order to show cause to have the photocopy admitted

to probate must be filed with the Superior Court, Chancery Division, in the county in

which the decedent resided. In the complaint, the proponent of a will can present the

evidence necessary to have the will admitted. For example, an affidavit stating that the

affiant witnessed a child destroy the original will or that the affiant lost the original will

should be filed, together with the complaint. Additionally, an affidavit of someone who

can attest to the testator’s signature, or an affidavit by one of the witnesses, should also

be attached. Often, if all of the parties in interest consent to the probate of the

photocopied will, it can be admitted to probate without a hearing or court appearance.

Common law in New Jersey provides that if a will is last known to have been in

the decedent’s possession and the will cannot be found after the decedent’s death, there is

a rebuttable presumption that the will was destroyed and, therefore, the intestacy rules

would govern the estate administration. To overcome that presumption, the moving party

has the burden of convincing the court that, more likely than not, the will was not

destroyed.

In our office we give clients the option to keep the original will in our fireproof

safe or to take it with them. No matter what decision the client makes we ask them to

sign something stating what happened to their original Will. Either they will sign

something stating that they left the original Will in our office and if they do so we will

give them a copy of the will with a stamp stating that our firm has their original will. If

the client takes their original Will then we make them sign a receipt. Furthermore, in

their estate planning binder we insert a page in front of their Will which reads as follows:

PLACEMENT OF ORIGINAL LAST WILL AND TESTAMENT

You have executed your Last Will and Testament prepared by the offices of

Fendrick & Morgan, LLC.

The law presently presumes that a lost original Will is presumed to be revoked by

you and a photocopy may not necessarily be admitted to probate because of this

presumption.

You have taken possession and will personally safeguard your original

Last Will and Testament. Please understand that in your binder is only a copy of your

Last Will and Testament.

B. Withheld Wills

Where an interested party believes that a decedent died testate and that a will is

being knowingly withheld by an individual, the interested party may file a verified

complaint and order to show cause to compel the production of the original will with the

Superior Court, Chancery Division, in the county in which the decedent resided.

IV. EXCEPTIONS TO PROBATE

Certain estates do not require probate. For example, the decedent and another

person may own real estate as joint tenants. In addition, the decedent may have an

insurance policy payable to a spouse and no assets in his name alone. In that type of

situation, there are no assets requiring administration. The estate may be subject to

inheritance and estate taxes and still be a non-probate estate. Generally, though, there

will be some assets that require appointment of the appropriate fiduciary. There may be,

for example, a car in the name of the decedent or an uncashed social security check or a

checking account in the sole name of the decedent. In such event, probate proceedings

will be required. The procedures for handling the estate depend on how the property was

titled and whether beneficiary designations are listed.

Generally speaking there are different ways property can pass at a person’s

death. Let’s briefly discuss some of the different ways.

A. Property Passing By Operation of Law

(i). Deed with Joint Tenants with Right of Survivorship (JTWROS)

Any property titled JTWROS will automatically pass to the surviving joint tenant upon

the death of a co-owner. A new deed may have to be prepared reflecting the change in

ownership. If the surviving joint tenant is the decedent’s spouse, it is not necessary to

prepare a deed. Rather, when the surviving spouse sells or retitles the property, a recital

should be added to the deed referencing how the property vested in the surviving spouse.

Even though it is not needed, the surviving spouse may want a deed prepared anyway. If

the co-owner was a person other then the surviving spouse a new deed should be

prepared.

(ii) POD Account -

Bank accounts titled “POD” or “for the benefit of” will be payable to

that person after the death of the owner. After the tax waivers are received from the

State, the account will be closed and paid to the beneficiary.

(iii) Joint Tenant Bank Account

A bank account titled “Joint Tenants” will pass to the surviving co-

owner after the death of a co-owner. Accordingly, different rules apply for the handling

of these assets. A brief overview of these rules are as follows:

a. Bank Accounts - Banking institutions generally have two

(2) designations for joint accounts. The "or" accounts are titled as though the account

was jointly held with rights of survivorship. "And" accounts establish a tenancy which

assumes that each co-owner holds a pro rata share of the account. This designation is

important in determining the rightful recipient or beneficiary of the account.

b. "OR" accounts - Because this title infers joint tenancy with

right of survivorship, a surviving owner of the account is entitled to the entire balance. In

order to transfer the account to the survivor's name alone, either the personal

representative or the personal representative and the co-owner must submit

documentation to the bank.

c. “AND” accounts - Because this title infers a tenant in

common relationship the surviving owner of the account is entitled to a pro rata of the

balance. In order to transfer the account to the survivor and the estate, the personal

representative must submit the same documentation as for “OR” accounts, plus an

Executor’s Short Certificate and W-9 for the estate.

1. Stocks and Bonds - Following the same “OR/AND”

designations as bank accounts. These holdings can be transferred by sending a stock or

bond power with signature guaranteed to the transfer agent along with a certified copy of

the decedent’s death certificate. If the asset is an “AND” an executor’s short certificate

no longer than sixty (60) days and a affidavit of domicile must be submitted. Again, the

“OR/AND” determines whether the surviving tenant or the estate’s beneficiary are

entitled to the stock or bond. As a note, New Jersey corporations require tax waivers in

addition to the other documentation.

B. Property passing by Contract

Property passing by contract includes any property or account that has a

named beneficiary. If no beneficiary is named, the institution where the account is held

may have its own specific order in which the property passes. However, if no beneficiary

is named, the property usually passes to the estate.

(i) Life Insurance - Send original policy, proof of claim, and

certified death certificate to insurance company. Life insurance proceeds that pass

directly to a beneficiary are not probate assets and are not under the control of the

executor.

(ii) Retirement Plans - Most retirement plans are funded with

pre-taxed income. This means that when distributions are made, the beneficiary will be

taxed on all of the proceeds. As a result, care should be taken in making withdrawals

from a retirement plan. Generally the goal is to defer the income tax on the distribution

for as long as possible.

Each institution has its own forms for beneficiaries to make a

notification of the decedent’s death. These forms usually ask for a method of making a

withdrawal. If all of the proceeds are withdrawn immediately, all of the proceeds will be

subject to income tax. This can be a painful trap for the unwary.

C. Probate Property Passing Under Will

Any property that does not pass by contract or by operation of law is

probate property. This property will pass by the terms of the Will and will be included in

the accounting. Before property can be distributed, waivers must be received from the

State indicating that all Inheritance taxes have been satisfied. After waivers are received,

proceed with the accounting process below.

(i) Real Estate - The personal representative must look to the

deed

itself for direction on how to transfer this property. There are three (3) basic types of

ownership:

a. Tenants by the Entirety - It is established when a

husband and

wife own a piece of property jointly. Although the real estate passes by operation of law,

a tax waiver should be obtained by using the form L-9 and recorded with the County

Clerk=s Office.

b. Joint with Right of Survivorship - Establishes that the

surviving joint tenant is entitled to the deceased tenant=s share. In this case, a waiver

should be obtained and filed with the county recording officer with the Executor=s deed

naming the surviving joint tenant as owner. The Executor=s deed should recite the death

of the deceased joint tenant.

c. Tenants in Common - Indicates that the property was

held

pro rata. It is not necessary that tenancy in common be equal. The deed may indicate

otherwise. In the absence of a contrary indication it is presumed that the tenancies are

equal. The Executor must prepare new deeds transferring the property to the surviving

tenant and is called for by the dispositive provisions in the Will and intestacy statute.

Again, the tax waiver should be filed with the County Recording Officer.

(ii) Stocks and Bonds - Following the same AOR/AND@

designations

as bank accounts. These holdings can be transferred by sending a stock or bond power

with signature guaranteed to the transfer agent along with a certified copy of the

decedent=s death certificate. If the asset is an AAND@ an executor=s short certificate no

longer than sixty (60) days and a affidavit of domicile must be submitted. Again, the

AOR/AND@ determines whether the surviving tenant or the estate=s beneficiary are

entitled to the stock or bond. As a note, New Jersey corporations require tax waivers in

addition to the other documentation.

(iii) Transferring Other Probate and Non Probate Assets to the

Distributee

a. Tangible Personal Property - Such as household

contents, collections, and jewelry are distributed in any of the following manners:

i. Memorandum referenced or attached to the

Will, which is signed by the Testator and designates the beneficiaries.

ii. Will provision setting forth the specific

devises.

iii. Beneficiaries determine and agree upon

distribution.

iv. Decisions are made by the Executor as to

distribution in the absence of any of the above.

b. Motor Vehicles - Are transferred by presenting the

Certificate of ownership to the motor vehicle agency. The title is endorsed over to the

recipient, by the personal representative. The only requirement to effectuate the transfer

is a short certificate evidencing the personal representative=s appointment.

c. Insurance - The named beneficiary must submit

company specified claimant=s forms and a certified copy of the decedent=s death

certificate. When the beneficiary is the estate, the personal representative must file the

claimant=s forms along with the certified death certificate and a short certificate. Some

companies also require a copy of the obituary and the original insurance policy.

d. Employee Benefits - Pension, profit sharing, 401(k)

and IRA benefits are distributed to the named beneficiary. For these assets, claim forms

and certified death certificates must be submitted by the named beneficiary. In the case

of the estate being named, a short certificate must be submitted.

e. Partnership Interests - Are distributed most

frequently by agreements between the partners in a formal writing. In the absence of a

written partnership agreement, New Jersey law provides that a partnership between two

(2) partners is dissolved when one (1) partner dies. If there are more than two (2)

partners, the partnership may continue and the value of the deceased partner=s share is to

be determined by the remaining partners and personal representative.

f. Buy- Sell - Where the decedent had an interest in a

closely- held corporation or partnership, the terms of the Buy-Sell Agreement between

the partners or shareholders control.

V. FILING REQUIREMENTS FOR NEW JERSEY ESTATE TAX RETURNS

A. NEW JERSEY TAXES.

The State of New Jersey imposes two death taxes: (1) the New Jersey Transfer

Inheritance Tax (hereinafter “inheritance tax”) and (2) the New Jersey Estate Tax

(hereinafter “NJ estate tax”). The former tax is assessed to the beneficiaries of an estate

while the latter is assessed to the estate itself.

(i) Inheritance Tax.

The inheritance tax is a transfer tax imposed on the transferee’s right to receive a

gift. devise, or bequest from a decedent. Unlike the estate tax, it is imposed directly upon

the beneficiary, not the estate. However, for planning purposes, it should be noted that the

personal representative of an estate, through a will, can be directed to pay this tax.

The tax is calculated after determining the value of property that may be received

by a particular beneficiary against the relationship of the beneficiary to the decedent. As

to this latter factor, the state establishes a different tax rate and amount of exemption,

depending on the relationship of the beneficiary to the decedent. The New Jersey

inheritance tax is due eight (8) months after the decedent’s date of death, and is required

for all residence unless the estate is wholly distributable to class A beneficiaries.

N.J.A.C. 18:26-9.1.

a. Classifications of Transferees.

The State of New Jersey created the following five categories of beneficiaries

subject to the inheritance tax:

1. Class A. Includes surviving spouses, partners who

have entered into a civil union, parents, grandparents, children, grandchildren. and any

other lineal ancestor or descendant;

2. Class B. Repealed;

3. Class C. Siblings, as well as daughters-in-law and

sons-in-law:

4. Class D. More distant relatives and other

individuals: and

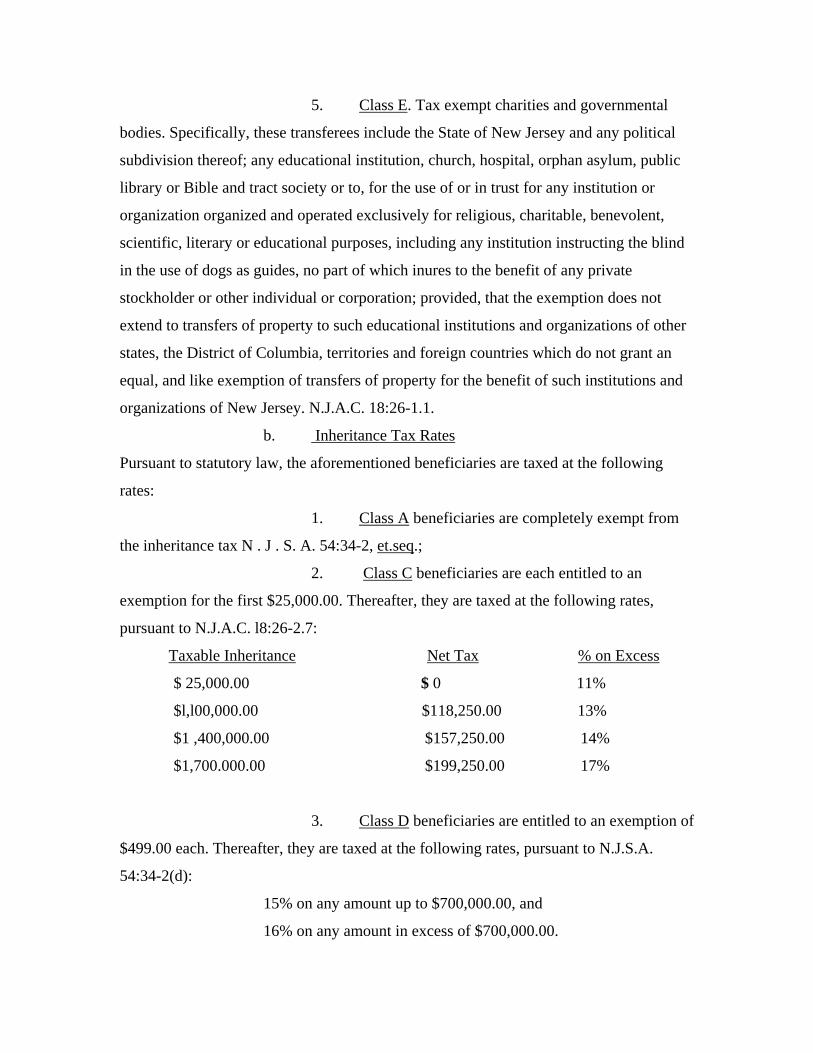

5. Class E. Tax exempt charities and governmental

bodies. Specifically, these transferees include the State of New Jersey and any political

subdivision thereof; any educational institution, church, hospital, orphan asylum, public

library or Bible and tract society or to, for the use of or in trust for any institution or

organization organized and operated exclusively for religious, charitable, benevolent,

scientific, literary or educational purposes, including any institution instructing the blind

in the use of dogs as guides, no part of which inures to the benefit of any private

stockholder or other individual or corporation; provided, that the exemption does not

extend to transfers of property to such educational institutions and organizations of other

states, the District of Columbia, territories and foreign countries which do not grant an

equal, and like exemption of transfers of property for the benefit of such institutions and

organizations of New Jersey. N.J.A.C. 18:26-1.1.

b. Inheritance Tax Rates

Pursuant to statutory law, the aforementioned beneficiaries are taxed at the following

rates:

1. Class A beneficiaries are completely exempt from

the inheritance tax N . J . S. A. 54:34-2, et.seq.;

2. Class C beneficiaries are each entitled to an

exemption for the first $25,000.00. Thereafter, they are taxed at the following rates,

pursuant to N.J.A.C. l8:26-2.7:

Taxable Inheritance Net Tax % on Excess

$ 25,000.00 $ 0 11%

$l,l00,000.00 $118,250.00 13%

$1 ,400,000.00 $157,250.00 14%

$1,700.000.00 $199,250.00 17%

3. Class D beneficiaries are entitled to an exemption of

$499.00 each. Thereafter, they are taxed at the following rates, pursuant to N.J.S.A.

54:34-2(d):

15% on any amount up to $700,000.00, and

16% on any amount in excess of $700,000.00.

Interestingly, the tax on Class D transferees has a cruel twist in that a bequest in

the amount of $500.00 or greater is taxed retroactive to the first dollar. Thus, an

individual who receives $499.00 from an estate pays no tax, yet an individual who is to

receive $500 must first pay a tax of $75.00 before receiving his or her net inheritance of

$425.00.

4. Class E beneficiaries are totally exempt from the

inheritance tax. N.J.S.A. 54:34-4.

(ii) New Jersey Estate Tax - In addition to the New Jersey

inheritance tax, the state has a State estate tax. This estate tax applies to all individuals

dying as New Jersey citizens. The State of New Jersey also has a Credit Shelter Amount

that can pass tax free to an individual. The Credit Shelter Amount for New Jersey is

$675,000. The State of New Jersey also exempts all transfers between husband and wife

provided that they were both United States citizens. The New Jersey estate tax rates

range from 4.8 to 16 percent. The New Jersey estate tax return is due nine (9) months

after the decedent’s death and is required to be filed for estate’s with values exceeding

$675,000. An estate is required to pay the higher of the New Jersey Estate Tax or the

New Jersey Inheritance Tax.

B. Federal Estate Tax - The federal government has an estate tax.

The estate tax rate is 40% and applies to all assets owned by a decedent at the time of his

or her death. Presently, the federal government allows the first $5,430,000 of assets to

pass to an individual estate tax free. Furthermore, the federal government exempts any

assets passing from one spouse to another provided that both spouses were United States

citizens. The $5,340,000 exemption is referred to as a Credit Shelter Amount. The

federal estate tax return is due nine (9) months after the decedent’s death and is required

to be filed for estate’s with values exceeding $5,430,000.

VI. ADDITIONAL DUTIES OF EXECUTOR

In New Jersey additional duties of the executor are as follows:

A. Notices of Probate - Within 60 days after the Will has been admitted to

probate by the Surrogate’s Court, R. 4:80-6 of the New Jersey Court Rules require that a

notice of probate be sent to all of the beneficiaries under the decedent’s Will as well as to

his or her spouse, heirs and next-of-kin, i.e., to those persons who would be entitled to

inherit had the decedent died intestate. The notice must inform the recipient of the date

the Will was admitted to probate, the name and address of the executor, and must state

that a copy of the Will is available upon request. Proof of mailing of the notices of

probate must be filed in the Surrogate’s Court by a certification within 10 days thereafter.

If the Will contains a charitable bequest, whether specific or residuary, a notice of

probate must also be sent to the New Jersey Attorney General’s office.

B. File IRS Forms SS-4, 2848 and 56 - The executor will need to obtain a

Federal identification number for the estate. This number must appear on all income tax

returns filed for the estate (Forms 1041) and is needed when opening any bank or

brokerage accounts in the name of the estate. A Federal identification number is obtained

by filing I.R.S. Form SS-4 with the Internal Revenue Service.

If a trust is created under the Will, it is also necessary to file Form SS-4 with the

I.R.S. to obtain a Federal identification number for the testamentary trust. Again, the

trust’s identification number must appear on all income tax returns (Forms 1041) filed for

the trust, and it must be provided to institutions where a trust account will be opened.

I.R.S. Form 2848 is a power of attorney form to be filed with the I.R.S. if the attorney

anticipates filing a Federal estate tax return (Form 706). This power of attorney will

allow the I.R.S. to communicate with the attorney regarding the estate, and will authorize

the I.R.S. to provide the attorney with a copy of the closing letter or an audit notice.

Lastly, I.R.S. Form 56 notifies the estate that a fiduciary relationship has been created so

that any tax notices will be sent to the executor or administrator. It is necessary to attach

to Form 56 an executor’s or administrator’s certificate issued by the Surrogate’s Court.

C. Notify Social Security Administration - It is necessary to notify the Social

Security Administration of the decedent’s death. This will often be taken care of by the

funeral home, but if not, it can be done by the executor or administrator or by the attorney

for the estate. A photocopy of the decedent’s death certificate should be submitted to

Social Security. If the decedent was receiving Social Security benefits at the time of his

or her death, it should be noted that benefits for the month of death must be returned if in

the form of a check. If the benefits were directly deposited at the decedent’s bank, the

Social Security Administration will remove the last month’s benefits from the bank

account automatically. A very small Social Security death benefit may be payable.

D. Open an Estate Account - It is usually necessary for the executor or

administrator to open a checking account at a bank or brokerage firm. The reason for

opening an estate account is to provide an account where checks for interest, dividends,

refunds, etc. that are received either in the decedent’s name or in the name of her estate

can be deposited, and an account on which the executor or administrator can write checks

to pay estate expenses. If the spouse is the sole beneficiary of the estate, it is possible to

deposit checks and pay expenses through an account in the spouse’s name, although it is

preferable that a separate estate account be used for record-keeping purposes.

E. Notify Post Office - Especially in the case where the decedent is not

survived by a spouse or children who live locally, it may be beneficial to have the

decedent’s mail forwarded to the home of the executor or administrator, or to the

fiduciary in care of the attorney’s office. This can be accomplished by providing the

decedent’s local post office with a certified copy of the death certificate and a Surrogate’s

Court certificate evidencing the appointment of the executor or administrator. It may also

be necessary to have a letter of authorization signed by the executor or administrator if

the attorney’s office address will be used. In this way, the attorney can be sure that any

checks, bills or notices received in the decedent’s mail will be processed. The decedent’s

mail may also provide the attorney with clues as to assets and expenses that need to be

reported on the estate and inheritance tax returns.

F. Settle Debts and Distribute Assets – The duties of an executor or

administrator are to settle debts and distribute the assets. However, a fiduciary should

refrain from making distributions during the first six (6) months of administration

because of potential claims by creditors. The timing of distributions thereafter depends

upon the nature of the assets, whether there are any claims by creditors, and whether tax

waivers are necessary. If it appears that an estate cannot be closed within a reasonable

period of time, the personal representative should consider making a partial distribution

on account. Sufficient reserve should be made for all liabilities, anticipated and

unanticipated.

G. Notify the Attorney General for All Charitable Bequests - Where a

decedent’s will provides for a charitable bequest, the personal representative is required by

Rule 4:80-6 to notify the Attorney General of the probate of the will. Such notice shall state

that the will has been probated, the place and the date of probate, the name and address of the

personal representative and a statement that a copy of the will shall be furnished upon

request. Such notice is to be given within 60 days after the probate of the will and proof of

the mailing of such notice shall be filed with the Surrogate within 10 days thereof. It is not

sufficient to only notice the charitable beneficiary, the Attorney General must also be

notified.

H. Locate any Missing Heirs - The personal representative should use best effort

to locate an absent person. When all efforts have failed, a notice to the beneficiary must

be published in a news paper having general circulation in the county in which the

decedent died. Court Rule 4:86. If a response is not received, the personal representative

should seek the appointment of a trustee for an absent person pursuant to N.J.S.A. 3B:26-

1 et. seq. The trustee has a responsibility to hold the property for the absent person, and

to make distribution in a manner as the court may deem proper.

I. Prepare an Accounting of the Estate - Regardless of the type of accounting

method chosen, some simple guidelines must be met:

(i) Cover Page - Should disclose the nature and function of the

account, identify the personal representative, note the importance of examining the

account, and give an address where more information can be obtained.

(ii) Summary of Account - Serves as a “table of contents” which

indicates the order of details presented and reflects the separate totals for the aggregate of

the assets on hand at the beginning of the accounting period, transactions during the

period, and assets on hand at the end of the period.

(iii) Schedule of Receipts - Must start with the assets originally

inventoried in the estate and any additional receipts during the accounting period. For

consistency an appropriate carrying value should be established and used throughout

administration. This value should be the value as of the date of death or the subsequent

purchase date.

(iv) Net Gains (Loses) On Sales or Other Dispositions - Should be

reported on the same schedule for the most meaningful measure of performance.

(v) Principal Disbursements - Must be detailed in terms of the

transactions grouped into categories such as administrative expenses, debts of the

decedent, taxes, and fiduciary commissions.

(vi) Principal Distributions To Beneficiaries - When it becomes

desirable or necessary to distribute assets on account, the transaction should be reflected

on this schedule.

(vii) Principal Balance on Hand - Lists all the assets in the hands of the

fiduciary at the end of the accounting period.

(viii) Income Receipts and Disbursements - These schedules reflect all

income received and disbursed by the personal representative. Categorical listings are

easier to check for discrepancies and therefore are preferable.

(ix) Income Distributions to Beneficiaries - Distributions of income to

beneficiaries should be recorded on this schedule.

(x) Proposed Plan of Distribution to Beneficiaries - This schedule

captures the name and age of each beneficiary and the assets to which they are entitled.

If death taxes are attributable to each transferee, the transferee’s relationship to the

decedent and the amount of tax attributable to each should be specified.

J. Timing of Distributions.

Distributions should not be made by the executor until the appropriate:

(i) State Taxes - The New Jersey inheritance tax is due eight (8)

months after the decedent’s date of death, and is required for all residents unless the

estate is wholly distributable to class A beneficiaries. N.J.A.C. 18:26-9.1.

(ii) Federal Taxes - The federal estate tax return is due nine (9) months

after the decedent’s death and is required to be filed for estate’s with values exceeding

$5,430,000. The typical time frame for a closing letter, if all documentation is submitted

can run from six (6) months to one (1) year. However, returns may be sent to the IRS

office in Trenton. Those closing letters are submitted much more quickly.

(iii) New Jersey Estate Taxes - The New Jersey estate tax return

is due nine (9) months after the decedent’s death and is required to be filed for estates

with values exceeding $675,000.

VII. ACCURATE AND INCLUSIVE VALUATION OF ASSETS

Typically, the fair market value of the asset is used to determine value. The fair

market value of property is the price at which it will change hands between a willing

buyer and a willing seller, neither being under any compulsion to buy or sell and both

having reasonable knowledge of the facts. Willow Trace Development Co., Inc. v.

Commissioner, 345F.2D 933 (CA5 1965)

Fair market value is not established by bargain sales, forced sales,

unusual market conditions, or a manipulated market. For estate and gift tax purposes, the

fair market value of a particular asset is determined by the sale price of the asset in the

Amarket@ in which the asset is most commonly sold.

The fair market value of property is determined based upon the actual

condition of the property. If the property has a condition or restriction which limits its

marketability, its fair market value must be determined after taking into account the

condition or restriction involved. However, the condition or restriction involved must be

real and actual.

In administrating an estate, the first step to take, in the valuation of assets,

is to determine the date of valuation. The executor of the estate may choose to value the

assets in the gross estate either on the date of the decedent’s death or six (6) months

thereafter. This latter date is referred to as the Alternate Valuation Date. Specifically,

I.R.C. ' 2032 permits the re-valuation of assets for a period not to exceed six months

after the date of death. Alternate valuation can only be elected if the election decreases

the gross estate and the estate tax.

The alternate valuation election applies to all property included in the gross

estatei. For any given asset, it is the earliest of six months after death or the prior date on

which the asset was Adistributed, sold, exchanged, or otherwise disposed of (or separated

or passed from the gross estate by any method) by the estate or any trust or person

holding it.

Any property, interest or estate which is Aaffected by mere lapse of time@ is

valued as of the date of decedent=s death. However, the date of death value may be

changed to account for any change in value that is not due to a Amere lapse of time@ on

the date of its distribution, sale, exchange, or other disposition.

VIII. COMMON PROBATE MISTAKES TO AVOID

A. Multiple Domiciles

(i). How To Avoid The Issue of Multiple Domiciles In the Planning

Process

When a client owns real property in a state other than the state in which he or she

resides, upon the client’s death, an ancillary estate administration will need to be

undertaken in that foreign jurisdiction in order to deal with that property. The probate

procedures, and fees, of that foreign jurisdiction will govern that ancillary administration.

Additionally, the now deceased client’s estate may need the services of an attorney who

practices in that foreign jurisdiction to assist with the estate administration in that state;

this, is not only cumbersome but is also costly (and may detract from your value as estate

counsel in the client’s eyes). Lastly, depending on the estate and/or inheritance tax laws

in that foreign jurisdiction, the estate may owe additional death taxes as a result of the

decedent’s ownership interest in the foreign real estate. Accordingly, when counseling a

client who owns real estate outside of the state in which the client resides, it is important

to discuss how the client’s estate can avoid probate in the foreign jurisdiction(s) in which

the client owns real estate. Perhaps the simplest way to avoid probate in a foreign

jurisdiction in which a client has an interest in real property is to transfer ownership of

the real property to a revocable trust.

Revocable trusts are commonly used to avoid probate. These types of revocable

trusts are called “Living Trusts”. A Living Trust can be thought of as a will substitute.

The concept is that assets are retitled in the name of the Trustee of the Living Trust.

During the lifetime of the grantor, the Trust is for his/her benefit and he/she can be the

Trustees. Upon the death of the grantor/beneficiary, the assets pass in accordance with

the terms of the Trust and no probate is necessary. In order for the trust to be effective,

the grantor’s assets must be retitled in the name of the Trust. The attorney drafting the

trust should assume responsibility for this task. Advising clients that retitling is

necessary and leaving them with the responsibility to retitle the assets seldom results in

the trust working effectively. The beauty of this type of Trust is that it is revocable

during the lifetime of the grantor, and it can be amended as needed. On the death of the

grantor, the trust can continue, if so desired. An applicable exemption equivalent trust,

QTIP Trust, special needs trust or other type of trust can be built into the initial revocable

trust document, which does become irrevocable upon the death of the grantor. As stated

above, the virtue of the living trust is that it avoids probate. These trusts do not save

death taxes – that is not their purpose.

Where a revocable living trust is used, there should always be a pour over will.

The pour over will transfers to the trust any assets which the grantor either intentionally

or unintentionally did not transfer to the trust during his or her lifetime. If, in fact, all

assets had been transferred to the living trust, probate of the pour over will would not be

necessary.

Because a living trust avoids probate, they are particularly useful to avoid multi-

state administration. If a client is a resident of New Jersey but owns real estate in a

foreign jurisdiction, ancillary administration in the foreign jurisdiction can usually be

avoided by having a living trust own the foreign jurisdiction real estate. Upon the death

of the grantor, the Trustee administers the Trust in accordance with its terms and the real

estate is distributed as set forth in the trust document; no probate is necessary.

(ii) Decedent Dies With Real Property In Multiple States

Where an individual dies owning real property in a state, or in multiple states,

other than the state of his residence, an ancillary estate will need to be raised in each

foreign state in which the decedent owned property. The estate administration in such

foreign jurisdiction(s) is considered to be ancillary because such administration is

secondary, or subordinate, to the estate administration in the decedent’s state of

residence.

Practicing in New Jersey, many of our clients are “snowbirds” and own homes in

states which enjoy milder winters than we do here in the north. Where, for example, a

New Jersey decedent owns real estate in Florida, upon the decedent’s death, probate

proceedings must be initiated in Florida in order to convey title to such Florida real

estate. In Florida, probate is a court supervised process for identifying and gathering the

decedent’s assets, paying taxes, claims and expenses of the administration, and,

ultimately, distributing the assets to the beneficiaries. (The Florida Probate Code is

found in Chapters 731 through 735 of the Florida Statutes.) Florida, like every state, has

its unique rules and procedures for the administration of an estate. However, what is

difficult about Florida probate (and very different from New Jersey probate) is that, as

stated above, it is a “court supervised” process. Accordingly, it may sometimes be most

efficient for the estate to have you, the New Jersey estate attorney, refer the executor to a

Florida attorney to navigate through the Florida probate proceedings. As estate

practitioners, we simply cannot know the probate procedures in all jurisdictions. Of

course, if you happen to be familiar with the probate procedures of the foreign

jurisdiction, you are free to assist your client in the foreign jurisdiction. However, if the

real estate is in a state such as Florida, where probate is court supervised, you will need to

have a Florida attorney submit your filings to the court. (Again, this is certain to result in

additional fees for the estate.)

Whether you are familiar with the foreign probate procedures or not, you should

advise your client at an early stage of the administration that the issue of real estate in

multiple jurisdictions is an added complexity to the estate. The client’s expectations

should be appropriately managed. The unfortunate consequence of this multi-state

administration is that the time and fees relative to the administration will most certainly

be greater than they would have been if all of the decedent’s property was located in one

state.

In order to raise an ancillary estate in the foreign jurisdiction, you should obtain

an exemplified copy of the New Jersey probate record. This will contain copies of all

documents executed by the personal representative at the time of the initial probate, along

with a certified statement by the Surrogate as to the accurateness of the underlying

probate record. The Surrogate’s certification (and seal), together with the exemplified

probate record should be submitted to the office empowered to qualify personal

representatives in the foreign jurisdiction. (In Pennsylvania, for example, that would be

the Register of Wills in the county in which the real estate is situated). Again, if you

require assistance, it may be helpful to seek the counsel of an estate attorney who

practices in that jurisdiction.

You also will need to consider what, if any, additional death taxes will be due by

the estate as a result of the foreign real estate. For example, if the decedent’s real estate

was situated in Florida, there would be no additional tax liability (although the probate

process would be necessary in order to convey good title to the property), but if, instead,

the property was located in Pennsylvania, a Nonresident Pennsylvania Inheritance Tax

Return would need to be filed and a Pennsylvania Inheritance tax might be due. In any

case, it will be important to understand the estate and/or inheritance tax laws of the

foreign jurisdiction. Additionally, care must be paid to the filing and payment deadlines

for the estate and/or inheritance taxes due to the foreign jurisdiction. In Pennsylvania, a

five percent (5%) discount on the total tax due is offered when the inheritance tax is paid

early (within three (3) months of the decedent’s death), rather than with the inheritance

tax return (nine (9) months from the decedent’s death). Accordingly, as the resident

estate attorney, one of the first questions you must answer for the client, and for yourself,

is what the death tax laws in the foreign jurisdiction(s) say: when are taxes due; how does

the tax scheme apply; and are there any discounts available for early payment of the tax.

B. Insolvent Estates

Where the assets of an estate are insufficient to satisfy all claims in full, the

personal representative shall make payment in the following specified by N.J.S.A. 3B:22-

2, as follows: (1) reasonable funeral expenses; (2) Costs and expenses of estate

administration; (3) debts for the reasonable value of services rendered to the decedent by

the Office of the Public Guardian for Elderly Adults; (4) Debts and taxes with preference

under federal law or the laws of New Jersey; (5) reasonable medical and hospital

expenses of the last illness of the decedent, including compensation of persons attending

to him; (6) judgments entered against the decedent according to their priorities of their

entries respectively; and (7) all other claims. The statute provides that no priority shall be

given to the payment of any claim over any other claim in the same class. Additionally, a

claim due and payable has no priority over a claim of the same class not yet due. The

fact that a debtor commences an action against the personal representative of the estate

for recovery of a debt or claim, or the entry of a judgment thereon against the personal

representative shall not entitle such debt or claim to preference over any other debt or

claim of the same class. N.J.S.A. 3B:22-2.

Care must be taken in the administration process to not satisfy the claim of any

one creditor, or any beneficiary, before it can be determined that the assets of the estate

are sufficient to satisfy all creditors, in the order of priority assigned by N.J.S.A. 3B:22-2.

C. Abatement

Where an estate is not insolvent, but still does not have sufficient assets to satisfy

all of the legatees, care must be paid to the order in which bequests are satisfied.

Specifically, distributions should not be made to any beneficiary until the abatement

statutes and any testamentary instructions are considered.

A decedent may, by his will or testamentary plan, express an order of abatement.

Additionally, in determining the order in which the property of a decedent’s estate shall

abate, consideration may be given to the express or implied purpose of a particular devise

in the decedent’s testamentary documents and, if the testamentary plan would be defeated

by the order of abatement set forth in N.J.S.A. 3B:23-12, shares of the distributees abate

as may be found necessary to give effect to the intention of the testator. N.J.S.A. 3B:23-

14.

If the decedent’s will does not express an order of abatement, and if the

decedent’s dispositive intent would not be frustrated by the order set forth therein, the

property of a decedent’s estate will abate for the purposes of paying debts and claims in

the order prescribed in N.J.S.A. 3B:23-12. N.J.S.A. 3B:22-3. N.J.S.A. 3B:23-12

provides that the shares of distributes abate, without any preference or priority as between

real and personal property, in the following order:

(a) Property passing by intestacy;

(b) Residuary devises;

(c) General devises; and

(d) Specific devises.

Abatement within each class is in proportion to the amount of property each of the

beneficiaries would have received if full distribution of the property had been made in

accordance with the terms of the will. A caveat to the above is the surviving spouse’s

right to make an election against the will, which is given preference over all other estate

beneficiaries. N.J.S.A. 3B:23-12.

Questions often arise regarding whether a particular bequest is general or specific

and, therefore, whether such bequest is entitled to some priority over all other

testamentary bequests under N.J.S.A. 3B:23-12. For example, if a decedent’s will

bequeaths to one child a specific amount of cash and to the other child “all real estate

which I may own at the time of my death,” is one bequest general and the other specific,

or are both general bequests? That was the issue in the unpublished decision of the New

Jersey Appellate Division in In the Matter of the Estate of Jennie Tateo, A-3249-99T2

(App. Div. March 21, 2001). The Court, in rendering its decision in that case, sets forth a

detailed discussion of the relevant inquiry here: the probate intent of the testator.

Where a question exists as to whether or not a bequest is general or specific for

abatement purposes, New Jersey courts will look to the probable intent of the testator.

The seminal decision defining the doctrine of probable intent in New Jersey is Fidelity

Union Trust Co. v. Robert, 36 N.J. 561 (1962). In that case, the Court expanded on the

then rule that required determination of the testator's intent from the four corners of the

will itself, and made clear that the judicial inquiry must focus on the subjective intent of

the testator as evidenced not merely by the text of the will but, primarily, by the testator's

"dominant plan and purpose as they appear from the entirety of his will when read and

considered in the light of the surrounding circumstances," ascribing to the testator, "[s]o

far as the situation fairly permits 'those impulses which are common to human nature....'"

Id. at 565 (quoting Greene v. Schmurak, 39 N.J.Super. 392, 400 (App. Div.), certif.

denied, 21 N.J. 469 (1956)). The Supreme Court went on to say that courts should

"strain towards effectuating the probable intent of the testator ...” and, since it is a

particular testator's intent that is at issue in a particular will construction case, generally

applicable canons of construction as well as precedents involving the construction of

other wills have no controlling force. Id. at 566, 568.

D. Qualified Disclaimers

As a general proposition, a beneficiary cannot be forced to accept a bequest. If,

for any reason, a beneficiary does not wish to receive an asset passing to him/her, the

beneficiary may "disclaim" (or, refuse to accept) his or her interest in the asset. In order

for the refusal to be respected for federal and state death tax purposes, the disclaimer

must be "qualified". A "qualified disclaimer" is defined in§ 2518 of the Internal Revenue

Code of 1986, as amended (the "Code"), an irrevocable and unqualified refusal by a

person to accept an interest in property but only if – (1) such refusal is in writing, (2)

such writing is made within nine (9) months, (3) such person has not accepted any of

the benefits, and (4) as a result of the refusal, the interest passes without the direction of

the person making the disclaimer to either the decedent’s spouse or someone other than

the person making the disclaimer.

E. Premature Distribution

In distributing assets of an estate, a personal representative should never distribute

estate assets, even personalty, before he or she is released for his or her administration,

whether such release is obtained formally or informally.