How the new client money rules affect your firm - Grant … · How the new client money rules...

104

How the new client money rules affect your firm High quality professional advice and expert insight in client money February 2015

Transcript of How the new client money rules affect your firm - Grant … · How the new client money rules...

How the new client money rules affect your firmHigh quality professional advice and expert insight in client moneyFebruary 2015

In June 2014 the Financial Conduct Authority (FCA) issued Policy Statement 14/09 which announced a wide range of changes including but not limited to:• custody assets reconciliations• delivery versus payment

exclusion • recordkeeping and

reconciliations• acknowledgement of trust

letters.

We summarise each key topic within the document on pages 5 and 6 and then discuss each in further detail describing the impact to firms from page 6 onwards. This material is extracted and summarised from the policy statement and set out in logical groupings for ease of reference.

When the new rules will applyThe changes set out in the Policy Statement apply in stages. Some rule changes are already in effect as of July and December 2014 (the latter mainly for new business which firms conduct). The remaining changes come into effect from 1 June 2015 for existing business relationships.

Firms should be aware that in certain sections of the handbook, the rules were renumbered in December 2014 and there will be further renumbering in June 2015. This may entail the firm undertaking new mappings of the rules to ensure that they keep track of the relevant rules in a given timeframe.

What action you need to takeThe changes set out in the Policy Statement affect a wide variety of firms across the financial services industry, excluding insurers. The rules concerning acknowledgement of trust letters, due diligence, unclaimed assets and transfers of business could affect most firms regardless of industry sector. Other rules regarding the alternative approach, use of buffers, delivery versus payment exclusion, and custody reconciliations will apply to some firms but not others.

In an important change the CASS 7 Annex 1 has been replaced with a new chapter 7.16. Firms should carefully study the clarifications which the FCA have issued in respect of how firms should calculate the client money requirement, for example

the amount of money the firm should appropriate and segregate as client money to cover an unresolved shortfall.

Firms should assess for themselves which rule changes will impact their business. We would expect that firms will now have in place programmes to assess, design and then implement the changes which they consider are necessary to comply with the revised rulebook.

We consider that the impacts require firms, amongst other things, to revisit their terms of business, client disclosures, client money and assets policies and even the functioning of technology tools which calculate segregation amounts and provide MI. Client asset governing bodies need to ensure that arrangements have been put in place to provide assurance that their firm is on track to implement required changes in the prescribed timeframe.

Finally firms should take note of the fact that the FCA require auditor assurances in respect of a number of internal systems and controls as a result of these new regulations.

Overview of the proposed changes to the CASS rules in Policy Statement 14/09.

Introduction

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 3

Our servicesGrant Thornton’s CASS specialist team has extensive experience working with clients across the investment management, investment banking, wealth management, brokerage, custody, and platform sectors.

Our detailed knowledge of the operational complexities at firms and their administrators, combined with our close working relationship with the FCA means that we bring practical as well as technically robust assessments to each of the firms with whom we perform CASS work.

We have set out below some of the ways in which Grant Thornton can support your firm as you implement the changes required by PS 14/9:• we can help your firm undertake structured

reviews to determine whether the firm is compliant with the new rules set out in this publication

• we can bring to you practical and insightful advice relating to the required changes to operational systems and controls

• we can design and deliver remediation plans• we understand the FCA’s expectations around

good governance and can provide you and your CF10a with support to build, enhance or redesign current governance structures and supporting MI in light of the changes necessary from the PS

• we regularly provide training and awareness workshops to firms ranging from one-to-one in depth discussions to group workshops to high level executive sessions covering key CASS principles.

If you would like to discuss how we can help you in more detail please get in touch.

How we can help you prepare for the new rules

Paul GarbuttPartnerT +44 (0)20 7728 2884 E [email protected]

Paul StaplesSenior ManagerT +44 (0)117 305 7799E [email protected]

Chris GollandSenior ManagerT +44 (0)20 7383 5100 E [email protected]

Owen LeathemManagerT +44 (0)20 7865 2297 E [email protected]

Rukaiya RashidManagerT +44 (0)20 7383 5100E [email protected]

4 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

EXECUTIVE SUMMARY

Executive summary

Policy topic Summary of changes Effective date

CASS 6 – Custody Assets Reconciliations

• Internal custody reconciliation – choice of methods introduced – at least monthly

• Physical asset reconciliation

• External custody reconciliation

• Determining frequencies for custody record checks and reconciliations

• Handling discrepancies and shortfalls in custody assets

• Recordkeeping, record checks and reconciliations

1 June 2015

May comply before this date

CASS 6 – Other • Registration of custody assets

• Written custody agreements

1 June 2015

(1 Dec 2014 new business)

CASS 6 and 7 – Delivery Versus Payment Exclusion

• Transactions through a commercial settlement system. Exemption from client money rules until third business day. Introduce written agreement with clients

• Regulated collective investment schemes (‘CIS’). Window reduced to one day for authorised fund managers. Introduce written agreement with clients

1 June 2015 (1 Dec 2014 new business)

1 June 2015

CASS 6 and 7 – Unclaimed Money and Assets

• There is now more clarity and prescription associated with ‘gone aways’

• Prescribed steps taken to contact client

• De minimis amounts

• Onus on firm to check legal position – requires unconditional undertaking

• Paid to charity – not to the firm

• Six years since last movement

• All associated costs to be borne by firm

1 Dec 2014

CASS 7 – Banking Exemption

• Operation of the Banking Exemption – notifications to clients 1 Dec 2014

CASS 7 – Trustee firms • Application 1 July 2014

CASS 7 – Transfers of Business

• Transfer clauses

• Post transfer notifications

1 Dec 2014

1 Dec 2014

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 5

Policy topic Summary of changes Effective date

CASS 7 – Immediate Segregation

• Interaction with the EMIR for firms that are members of ‘CCPs’ – clearing arrangement mandatory prudent segregation amount

• Interaction with the DvP window for transactions in settlement systems

• Prudent Segregation

1 June 2015

CASS 7 – Physical Receipts and Allocation of Client Money

• Paying physical receipts into a client bank account

• Cleared funds

• Allocation of client money receipts

1 June 2015

CASS 7 – Alternative Approach

• Firms’ use of the alternative approach

• Auditor assurances

• Obtaining revised auditor reports

• Intra-day adjustments

1 June 2015

(1 Dec 2014 new business)

CASS 7 – Recordkeeping and Reconciliations

• External client money reconciliations

• Internal client money reconciliations

• Non-standard methods of internal client money reconciliation

• Standard methods of internal client money reconciliation

1 June 2015

CASS 7 – Acknowledgement Letters

• Acknowledgment letters and template letters

• Overseas counterparties

• Removal of 20-business day ‘grace period’

• Authorised central counterparties (CCP)

• Recordkeeping and periodic reviews

• Establishing signatory authority/electronic signatures

• Overnight money market deposits

1 June 2015 for repapering existing letters

Templates must be in place for accounts opened after 30 November 2014

CASS 7 – Client Bank Accounts

• Diversification

• Due diligence

1 June 2015

CASS 7 – Money Held by Third Parties

• Client money held by third parties

• Client money relating to custody assets of custodians

1 Dec 2014

1 June 2015

CASS 7 – Other Issues • Interest

• Money ceasing to be client money

• Unbreakable client money term deposits

• Commodity Futures Trading Commission Part 30 Exemption Order

1 July 2014

CASS 8 • Non-written mandates 1 June 2015

CASS 9 • Regular reporting to clients (on client assets)

• Information to clients on client assets protection arrangements

1 Dec 2014

1 June 2015

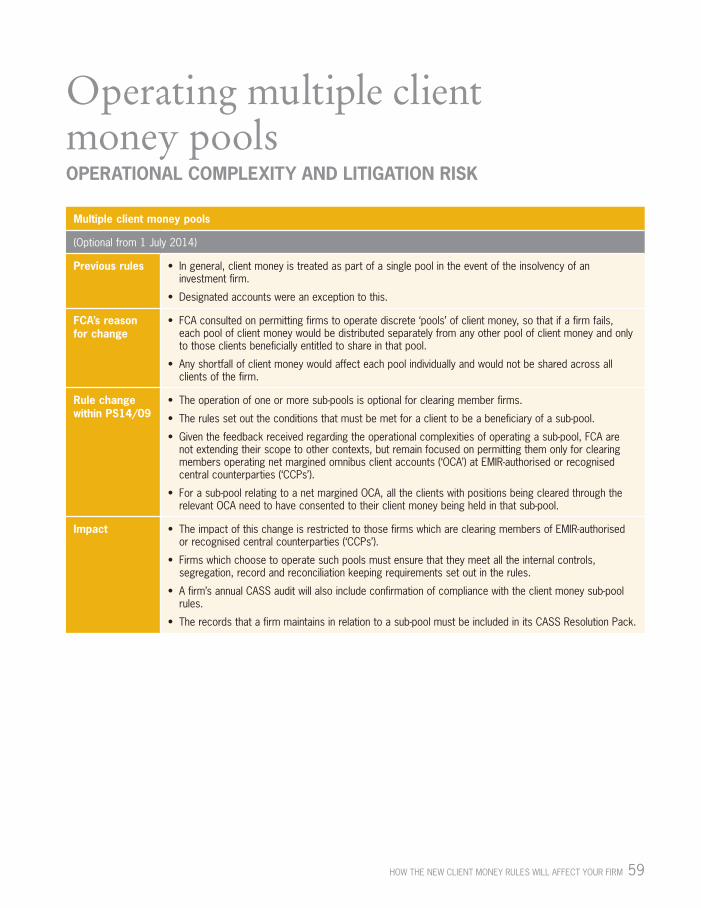

CASS 7, 7A Multiple Client Money Pools

• Operational complexity and litigation risk

• Operating multiple client money pools – Diversification

• Operating multiple client money pools – Sub-pool disclosure document

• Operation of ‘immediate segregation’ in the context of sub-pools

1 July 2014

6 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

CHANGES RELEVANT TO CASS 6Custody assets reconciliations

Internal custody reconciliation 7

Physical asset reconciliation 8

External custody reconciliation 9

Determining frequencies for custody record checks and reconciliations 10

Handling discrepancies and shortfalls in custody assets 11

Custody asset recordkeeping, record checks and reconciliations 12

Custody rules (CASS 6)

(Deadline 1 June 2015)

Current rules • Investment firms are required to maintain records of custody assets in a manner which ensures their accuracy, and that they correspond with the custody assets they hold.

• Internal and external reconciliations should be carried out as often as necessary and as soon as practicable after the date of the reconciliation.

• Any discrepancies identified through the reconciliation process must be corrected promptly.

• Firms must also correct and make good any shortfall in custody assets where there are reasonable grounds for concluding that the firm is responsible for the shortfall.

FCA’s reason for change

• FCA has observed frequent occurrences of firms having poor record-keeping practices, and inadequate systems and controls to ensure the accuracy of records.

• FCA also consider that many firms do not understand their requirements in respect of custody asset recordkeeping, record checks and reconciliations.

• FCA are aware that firms using integrated systems to keep their custody records may not be able to carry out internal custody reconciliations, as it is not possible to extract two independent records from such a system. Consequently these firms will be required to carry out an internal custody record check.

Rule change within PS14/09

• All firms must perform internal custody record checks as regularly as necessary, but at least monthly, to ensure that their records of safe custody assets correspond with their obligations to clients for holding safe custody assets.

• Internal custody record checks must be carried out by one of two methods:

1) Internal custody reconciliation method: a comparison on a particular date between two separately maintained records (which need not be independent of one another) to ensure that the firm’s records of its safe custody assets correspond with its obligations to clients to hold safe custody assets:

a) a ‘client-specific safe custody asset record’; and

b) an ‘aggregate safe custody asset record’; OR

2) Internal system evaluation method: a process to evaluate:

(a) the completeness and accuracy of the firm’s internal records and accounts of custody assets held for clients – including whether sufficient information is being recorded by the firm to enable it to identify a client-specific safe custody asset record, and readily determine the total of all custody assets held for clients; and

(b) whether the firm’s systems and controls correctly identify and resolve all discrepancies in its internal records and accounts of custody assets it holds for its clients (including identification of any negative balances, ‘test’ data or ‘balancing’ entries, IT processing or journal entry errors).

Impact • All firms, regardless of type and business model, will be permitted to undertake their internal custody record checks by way of the internal system evaluation method.

• Firms will be permitted to undertake these processes without first seeking a confirmation or any other report from an independent auditor. The processes will be reviewed by the auditor in the annual client assets report.

• Firms will need to review their processes and procedures to ensure that they will be able to comply with the new regulations.

Custody assets reconciliationsINTERNAL CUSTODY RECONCILIATION

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 7

Custody rules (CASS 6)

(Deadline 1 June 2015)

Current rules • Investment firms are required to maintain records of custody assets in a manner which ensures their accuracy, and that they correspond with the custody assets they hold.

• Internal and external reconciliations should be carried out as often as necessary and as soon as practicable after the date of the reconciliation.

• Any discrepancies identified through the reconciliation process must be corrected promptly.

• Firms must also correct and make good any shortfall in custody assets where there are reasonable grounds for concluding that the firm is responsible for the shortfall.

FCA’s reason for change

• FCA has observed frequent occurrences of firms having poor record-keeping practices, and inadequate systems and controls to ensure the accuracy of records.

• FCA also consider that many firms do not understand their requirements in respect of custody asset recordkeeping, record checks and reconciliations.

• FCA are aware that firms using integrated systems to keep their custody records may not be able to carry out internal custody reconciliations, as it is not possible to extract two independent records from such a system. Consequently these firms will be required to carry out an internal custody record check.

Rule change within PS14/09

All firms that physically hold custody assets must undertake a physical asset reconciliation as often as necessary, but at least every six months. This comprises a comparison between a firm’s internal records and a count of the actual physical safe custody assets it holds for its clients, performed by one of two methods:

• ‘total count method’ – the count being of all physical custody assets held by the firm on a particular date; and

• ‘rolling stock method’ – the count of all physical custody assets held by the firm being undertaken in more than one stage, with each stage referring to a count of a line of stock or group of stock lines (eg all the securities held in connection with a particular business line being counted at the same time).

• Before using the rolling stock method, firms must document their reasons for concluding that they have systems and controls in place that will effectively mitigate the risk of its records being manipulated (eg ‘teeming and lading’).

• Firms will be permitted to use either of the physical count methods without first obtaining a written report on the adequacy of the proposed method from an independent auditor. However, review of the method used will be a requirement of the annual auditor’s client assets report.

Impact • Firms will need to ensure that they have systems and procedures which enable them to fulfil the physical count requirements.

• Firms carrying out the ‘rolling stock method’ will need to ensure that they have appropriate documentation in place setting out why they consider their systems and controls are adequate. Fees for the annual auditor’s client assets report can also be expected to increase due to the extra time requirement.

Custody assets reconciliationsPHYSICAL ASSET RECONCILIATION

8 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Custody rules (CASS 6)

(Deadline 1 June 2015)

Current rules • Investment firms are required to maintain records of custody assets in a manner which ensures their accuracy, and that they correspond with the custody assets they hold.

• Internal and external reconciliations should be carried out as often as necessary and as soon as practicable after the date of the reconciliation.

• Any discrepancies identified through the reconciliation process must be corrected promptly.

• Firms must also correct and make good any shortfall in custody assets where there are reasonable grounds for concluding that the firm is responsible for the shortfall.

FCA’s reason for change

• FCA has observed frequent occurrences of firms having poor record-keeping practices, and inadequate systems and controls to ensure the accuracy of records.

• FCA also consider that many firms do not understand their requirements in respect of custody asset recordkeeping, record checks and reconciliations.

• FCA are aware that firms using integrated systems to keep their custody records may not be able to carry out internal custody reconciliations, as it is not possible to extract two independent records from such a system. Consequently these firms will be required to carry out an internal custody record check.

Rule change within PS14/09

• The changes comprise a number of clarifications as to how external custody reconciliations should be carried out.

• The reconciliations must be performed as regularly as necessary, but at least monthly.

• They must be carried out between the firm’s internal records and those provided by the relevant third party – being the entity with whom the firm deposits custody assets; or with whom it registers custody assets (as the case may be – for instance operators of collective investment schemes).

• The third party’s records for the purpose of carrying out the external custody reconciliation may comprise any appropriate information (including statements or other confirmations).

• Where firms hold physical custody records such as paper share certificates, they are not required to undertake external custody reconciliations in respect of the relevant assets. However, firms would be expected to carry out periodic ‘spot checks’ on whether title to an appropriate sample of custody assets they hold is registered in accordance with the CASS rules.

Impact • Firms should ensure that they are carrying out external reconciliations as required, and at least monthly.

• Firms which physically hold custody assets should establish procedures for carrying out periodic ‘spot checks’ on whether title to an appropriate sample of physical custody assets has been registered correctly.

Custody assets reconciliationsEXTERNAL CUSTODY RECONCILIATION

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 9

Custody rules (CASS 6)

(Deadline 1 June 2015)

Current rules • Investment firms are required to maintain records of custody assets in a manner which ensures their accuracy, and that they correspond with the custody assets they hold.

• Internal and external reconciliations should be carried out as often as necessary and as soon as practicable after the date of the reconciliation.

• Any discrepancies identified through the reconciliation process must be corrected promptly.

• Firms must also correct and make good any shortfall in custody assets where there are reasonable grounds for concluding that the firm is responsible for the shortfall.

FCA’s reason for change

• FCA has observed frequent occurrences of firms having poor record-keeping practices, and inadequate systems and controls to ensure the accuracy of records.

• FCA also consider that many firms do not understand their requirements in respect of custody asset recordkeeping, record checks and reconciliations.

• FCA are aware that firms using integrated systems to keep their custody records may not be able to carry out internal custody reconciliations, as it is not possible to extract two independent records from such a system. Consequently these firms will be required to carry out an internal custody record check.

Rule change within PS14/09

• At least annually, firms must review the frequency of their custody record checks, physical asset reconciliations and external custody reconciliations (unless they are undertaken on a daily basis).

• FCA has indicated that, as best practice, it would expect firms to carry out daily external reconciliations if they hold assets electronically with a central securities depository and the third party is able to provide information on the firm’s holdings on a daily basis.

• Currently CASS 6.5.9 states that ‘whenever possible’ reconciliations should be carried out by a person who is independent of the production or maintenance of the records being reconciled. The Policy Statement extends this to those responsible for checking the reconciliations as well.

Impact • Firms carrying out custody records, physical asset reconciliations and external custody reconciliations less frequently than daily must introduce procedures to review and document why the frequency they choose is appropriate.

• Firms holding assets electronically with a central securities depository should consider whether they should carry out daily reconciliations (if the relevant information about holdings can be provided by the third party).

• Firms will need to consider the practical impact of the extension of the independence criteria to those who check reconciliations and how this will be implemented.

Custody assets reconciliationsDETERMINING APPROPRIATE FREQUENCIES FOR CUSTODY RECORD CHECKS AND RECONCILIATIONS

10 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Custody rules (CASS 6)

(Deadline 1 June 2015)

Current rules • Investment firms are required to maintain records of custody assets in a manner which ensures their accuracy, and that they correspond with the custody assets they hold.

• Internal and external reconciliations should be carried out as often as necessary and as soon as practicable after the date of the reconciliation.

• Any discrepancies identified through the reconciliation process must be corrected promptly.

• Firms must also correct and make good any shortfall in custody assets where there are reasonable grounds for concluding that the firm is responsible for the shortfall.

FCA’s reason for change

• FCA has observed frequent occurrences of firms having poor record-keeping practices, and inadequate systems and controls to ensure the accuracy of records.

• FCA also consider that many firms do not understand their requirements in respect of custody asset recordkeeping, record checks and reconciliations.

• FCA are aware that firms using integrated systems to keep their custody records may not be able to carry out internal custody reconciliations, as it is not possible to extract two independent records from such a system. Consequently these firms will be required to carry out an internal custody record check.

Rule change within PS14/09

• Where a reconciliation has highlighted a shortfall in the safe custody assets held by the firm caused by a discrepancy, the firm must resolve the discrepancy immediately.

• If it is unable to do so, it must ensure client protection by segregating an equivalent amount of the firm’s own assets/client money, so that this is held in such a way that it will be realised for clients’ benefit if the firm fails.

• If another person is responsible for the shortfall (or it is caused by timing differences between the firm’s and a third party’s accounting systems), the firm does not have to make good the deficit but may do so. Firms should take steps to resolve any such shortfalls as soon as possible.

• In certain circumstances firms may also need to consider whether to inform affected clients of the shortfall (for instance if the firm is informed by a third party of the loss of a custody asset).

Impact • Firms will need to ensure that their policies and procedures meet the requirements to make good shortfalls.

• They should also check their own client money permissions and then ensure that any amounts they transfer for this purpose would only be available for clients’ benefit in the event of the firm’s failure, and are clearly recorded.

• Firms which normally operate under the ‘banking exemption’ or use title transfer collateral arrangements for monies received or held on behalf of clients will need to ensure that they have appropriate systems and controls in in place to hold client money in compliance with the client money rules.

• If a firm in these circumstances wishes to use its own money to cover shortfalls in custody assets, then it may need to repaper its agreements or other documentation with the client concerned to ensure that money may be held for the client’s benefit as client money.

• Where a firm segregates its own money as client money to cover a custody shortfall, it will need to revisit the valuation each day to ensure it is still segregating the correct amount to cover the shortfall – such assets will then form part of the custody assets included in the firm’s next internal custody record check.

Custody assets reconciliationsHANDLING DISCREPANCIES AND SHORTFALLS IN CUSTODY ASSETS

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 11

Custody rules (CASS 6)

(Deadline 1 June 2015)

Current rules • Existing systems and controls requirements require firms to document their policies and procedures for their custody reconciliations.

FCA’s reason for change

• FCA has observed frequent occurrences of firms having poor record-keeping practices, and inadequate systems and controls to ensure the accuracy of records.

• FCA also consider that many firms do not understand their requirements in respect of custody asset recordkeeping, record checks and reconciliations.

• FCA are aware that firms using integrated systems to keep their custody records may not be able to carry out internal custody reconciliations, as it is not possible to extract two independent records from such a system. Consequently these firms will be required to carry out an internal custody record check.

Rule change within PS14/09

• Policy documents should set out the frequencies the firm will follow for its custody reconciliations and the rationale for these frequencies. They should also set out the procedures for the resolution of reconciliation discrepancies and the firm’s procedures for escalating breaches and related issues to the firm’s board and to the FCA where appropriate (this would include any materiality policies a firm adopts).

• Firms will be required to make and retain copies of each custody record check and/or reconciliation undertaken, each review conducted of these arrangements and their policy and procedures for complying with these requirements, including those around recordkeeping and reconciliations.

• Where a firm will be unable to comply with a specified requirement or where the firm materially fails to comply with a rule (ie there is a breach of the rule), a notification must be made to FCA.

• A materiality threshold applies to actual breaches, meaning not all breaches need to be notified to the FCA. What is material will depend on the circumstances and firms will need to consider this on a case-by-case basis.

Impact • The requirement to establish and maintain written policies and procedures for some firms may need a significant resource commitment.

• The FCA did not provide additional guidance on whether or not a breach is material. Firms will need to consider the factors they will take into account when assessing whether a breach is considered ‘material’ enough to warrant disclosure to FCA.

Custody asset recordkeeping, record checks and reconciliations

12 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

CHANGES RELEVANT TO CASS 6

Physical share certificates 13

Registration of custody assets 13

Written custody agreements 14

Custody rules (CASS 6)

(Effective from 1 July 2014)

Current rules • Firms which safeguard and administer assets must comply with the relevant safeguarding and administering rules.

• They require appropriate permissions, and must comply with the custody rules as required.

FCA’s reason for change

• No change – merely a clarification, because some firms had questioned whether paper share certificates fall within the definition of designated investments or MiFID financial instruments (as legal title is recorded on the company register or in CREST).

Rule change within PS14/09

• As the loss or destruction of share certificates could harm the client in certain circumstances, even though it might not automatically create a loss of title to shares, FCA reiterate that firms which are safekeeping physical share certificates do fall within the scope of the ‘safeguarding’.

Impact • As a result, where a firm is also administering an asset for which it is holding a physical share certificate (eg processing corporate actions), it requires the appropriate permissions and must comply with the custody rules in respect of those assets.

Custody rules (CASS 6)

(Deadline 1 June 2015)

Current rules • In certain circumstances, a firm may currently register or record legal title to its own applicable assets in the same name as that in which legal title to a client’s safe custody asset is registered.

FCA’s reason for change

• This poses the risk that when a firm fails, the client’s safe custody assets may not be easily identifiable as separate from a firm’s assets.

Rule change within PS14/09

• Firms may record their own assets in the same name as any custody asset for no longer than is reasonably necessary:

A) where doing so arises incidentally to the investment business the firm carries on for the account of a client, or to other steps taken by the firm to comply with the custody rules. For example:

• correcting dealing or transaction errors that relate to client positions;

• processing or allocating assets for bulk deals;

• maintaining a small balance of the firm’s own assets (eg as a float to cover custody breaks);

• allowing clients to trade in fractional shares or units and when processing corporate actions;

• making good a shortfall in custody assets with a firm’s own assets.

B) where doing so arises only as a result of the law or market practice of a jurisdiction outside the UK.

Impact • Firms should maintain documentation to demonstrate that they have considered each of the options available to them for the registration of their own applicable assets.

• Firms may not use the exceptions for any longer than is reasonably necessary and must also consider whether there are any means of avoiding using the exceptions.

• When placing assets in overseas jurisdictions, firms will continue to be obliged to disclose these circumstances in specific situations to certain clients.

Physical share certificates

Registration of custody assets

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 13

Custody rules (CASS 6)

(Deadline 1 June 2015 for existing business)(Deadline 1 Dec 2014 for new business)

Current rules • There is no explicit requirement for investment firms to have written documentation in place to show the terms on which they place client assets with third parties (whether they are ‘depositing’ them in the course of acting as their clients’ custodian, or by arranging custody of them on their clients’ behalf).

FCA’s reason for change

• The failure to adequately document the terms upon which assets are held creates uncertainty as to how assets should be treated in the event of a firm’s insolvency and may lead to disputes over the responsibilities and obligations of the different parties involved.

Rule change within PS14/09

• FCA are introducing an explicit requirement for firms to have written agreements in place whenever they place custody assets with a third party – irrespective of whether that third party is an affiliate of the firm.

• Written agreements must:

1) set out the binding terms of the arrangement between the firm and the relevant third party;

2) be in force for the duration of that arrangement; and

3) clearly set out the custody service(s) that the third party is contracted to provide.

• Alternatively, the investment firm and the custodian could exchange their standard terms of business, or other documentation, as evidence of the terms on which the custodian services are provided.

Impact • Firms will have to undertake a review of their terms of business agreements and establish whether these meet the revised requirements.

• If changes are required, a repapering exercise will be required with the custody service providers.

• If firms rely on standard terms of business or other documentation for this purpose, they must ensure that these meet all the requirements of PS14/09. Care must also be taken to ensure clarity as to which document takes precedence if there is a conflict.

• Any changes to documentation will need to be reflected by firms in their CASS resolution packs.

Written custody agreements

14 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Title transfer collateral arrangements 15

CHANGES RELEVANT TO CASS 6 & 7

Changes relevant to both CASS 6 and 7

(Deadline 1 June 2015 for repapering existing business and adjusting processes)(Deadline 1 Dec 2014 for new business)

Current rules • Under the rules, a firm may stop treating money as client money if the money was transferred to the firm to secure or otherwise cover present or future, actual or contingent or prospective obligations.

• The FCA restricted the use of TTCA for retail clients of Contract For Difference (CFD) and spread betting products following supervisory work which showed that for certain businesses the use of TTCA was not appropriate for retail clients and was not generally in the clients’ best interests.

FCA’s reason for change

• FCA wishes to reduce the potential for disputes over the status of assets or monies held under TTCA when a firm enters insolvency proceedings.

• FCA is also aware of disputes arising over the status of assets when a firm is approaching insolvency and clients wish to move assets from TTCA so that they are protected.

• In this context, FCA has particular concerns regarding protections for retail customers.

Rule change within PS14/09

• Written agreements must be in place for each TTCA and must include the following:

– client’s agreement to the terms of the TTCA;

– any terms under which ownership of the client’s assets may transfer back from the firm to the client; and

– any terms and process to be followed for the termination of the TTCA or the overall agreement through which it was arranged.

• The requirement to have written agreements for TTCA can be fulfilled though the use of market standard documentation (for instance in connection with securities lending activities).

• A set process must be followed by firms if a client ask for assets held under TTCA to be given CASS protections. This must include documenting the client’s request and the firm’s response, including when the protection becomes effective.

• If the effective date of protection is not specified, it is assumed to be within one business day of the firm’s agreement to the request.

• Firms are not obliged to agree to the client’s request to give protection to assets held under TTCA.

• FCA recognises that the termination of TTCA could give rise to a (potentially lengthy) renegotiation of a client’s overall contractual relationship with the firm.

Impact • If firms do not already have written arrangements in place in respect of TTCA, then these will need to be drafted, with legal input.

• Firms must also establish processes and procedures for responding to any requests from clients to move their assets out of TTCA so that they are protected.

• Firms are reminded that communications in this regard must be clear, fair and not misleading.

Title transfer collateral arrangements (‘TTCA’)WRITTEN AGREEMENTS AND PROCEDURE FOR SWITCHING

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 15

16 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

CHANGES RELEVANT TO CASS 6 & 7Delivery versus payment exclusion

Transactions through a commercial settlement system 17

Regulated collective investment schemes (‘CIS’) 18

Changes relevant to both CASS 6 and 7

(Deadline 1 June 2015 for existing business)(Effective 1 December 2014 for new business)

Current rules • DvP window: Both the custody rules (CASS 6) and client money rules (CASS 7) currently allow firms to disapply the rules during the course of a ‘delivery versus payment’ transaction through a commercial settlement system if certain conditions are met.

FCA’s reason for change

• FCA has observed some firms stretching the use of the DvP window – leading to money and assets being held for significant periods of time during which client money and custody assets protections are not available.

Rule change within PS14/09

• Client’s purchase – the DvP window will start from the date of the client’s payment and then close at the earlier of: – the date the relevant delivery versus payment transaction settles, or– the close of business on the third business day following the date the client fulfils its payment

obligation to the firm. • Where delivery of the asset to the client has not occurred by the close of business on the third business

day, the firm will need to treat the money as client money until such time as the delivery by the firm to the client does occur.

• Client’s sale – the DvP window will start from the date the client fulfils its delivery obligation to the firm and then close at the earlier of:– the date the relevant delivery versus payment transaction settles, or – the third business day following the date the client fulfils its delivery obligation to the firm.

• Where payment to the client has not occurred by the close of business on the third business day because the transaction has not yet settled, the firm will need to treat the asset as a custody asset until such time as payment by the firm to the client occurs.

• Client agreement – each client’s agreement must be obtained to holding its assets or monies within the DvP window.

• Until a DvP transaction in respect of a client’s sale settles, a firm may, if its regulatory permissions allow, segregate its own money as client money, at an amount equivalent to the value at which that client’s custody asset is reasonably expected to settle.

• The firm must first confirm that the relevant client for whom the firm would otherwise be holding the custody asset is entitled to protection under the client money rules.

• The firm will need to ensure it incorporates this money into its internal and external client money reconciliations, and keeps appropriate records of such transactions.

Impact • Firms using commercial settlement systems will need to check that settlement timescales fall within the prescribed timescales.

• Firms will need to review the likely funding requirement if timescales fall outside the revised rules. Funding lines will need to be put in place or settlement arrangements modified.

• Firms will need to ensure they have procedures for:– identifying transactions which fall outside the window and protecting these amounts, and– promptly segregating amounts which settle before the window closes.

• Firms will need to ensure that agreements with clients include the client’s agreement to the use of the DvP window – this may require amendment to their existing terms of business agreements and a repapering exercise with their customer base.

• Some firms may incur additional costs associated with the extra staff time required to prepare and update records of cash amounts which have been segregated to protect the value of unsettled custody assets.

Delivery vs payment (DvP) exclusionTRANSACTIONS THROUGH A COMMERCIAL SETTLEMENT SYSTEM

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 17

20 Allocated but unclaimed client money

21 Unclaimed custody assets

Changes relevant to both CASS 6 and 7

(Deadline 1 June 2015)

Current rules • The current rules permit managers of regulated collective investment schemes (CIS) to make use of the DvP window for the purpose of settling a transaction in relation to units in a regulated collective investment scheme – meaning that settlement amounts are not protected by CASS rules during this window.

FCA’s reason for change

• If a firm fails some clients could become unsecured creditors.

• There have been differing interpretations of the DvP window including the length of time that redemption proceeds are subject to the window.

• The rules currently exclude any cheques issued to clients for redemption proceeds from the normal requirement to protect the money until the cheque has cleared.

Rule change within PS14/09

Authorised Fund Managers (‘AFM’) will be allowed a ‘one day window’ during which the DvP exclusion may apply. This will operate as follows:

1) When a firm receives money that would otherwise be client money from a client in relation to the issue of units in a regulated collective investment scheme, if this has not been passed on to the trustee/depository by the close of business on the business day following receipt, the AFM must segregate it and treat it in accordance with the client money rules; and

2) When a firm receives money that would otherwise be client money in the course of redeeming units in a regulated collective investment scheme, if this has not been passed on to the unit holder/client by the close of business on the business day following receipt, the AFM must segregate it and treat it in accordance with the client money rules.

• Where a firm makes a payment of redemption proceeds to a client by cheque, the cheque should be issued from a client bank account.

• The rules require firms to evidence each client’s agreement in writing to the firm’s use of the DvP CIS window. This could appear in the standard terms of business, and must be retained for the duration of the time that the firm makes use of the exemption for that client.

• AFMs will not be required to protect the value of redemption proceeds as client money, before they have received that money.

Impact • Firms will have a one day window following receipt of money from clients (although the window will ‘close’ on T+1 irrespective of unit price determination). This is a significant change given the current T+3 window.

• Some firms will have less liquidity following these changes, and will need to assess how this will be financed.

• Firms should consider carrying out analysis on when and where client money is held; mapping payment flows; and reviewing fund and investor documentation to ensure that they have clients’ agreement to such use of the DvP CIS window.

• AFMs will not have to apply the immediate segregation requirements so will not have to receive all client money directly into client bank accounts.

Delivery vs payment (DvP) exclusionREGULATED COLLECTIVE INVESTMENT SCHEMES (CIS)

18 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Allocated but unclaimed client money 19

Unclaimed custody assets 20

CHANGES RELEVANT TO CASS 6 & 7Unclaimed money and assets

Changes relevant to both CASS 6 and 7

(Rule changes effective from 1 December 2014)

Previous rules • CASS 7.2.19 R allowed a firm to cease to treat as client money any unclaimed client money balances allocated to an individual client when those balances were unclaimed and the firm was not able to return the money to the client.

• The firm could do this if it could prove that it had taken reasonable steps which included:

– entering into a written agreement, in which the client consented to the firm releasing balances from client bank accounts

– making attempts to trace the client concerned and to return the relevant balance

– ensuring that there had been no transactions on the account (other than charges or interest) for at least six years.

FCA’s reason for change

• It was unclear what should happen to money once it ceased to be client money. This resulted in some firms writing such amounts back to their balance sheet.

• This was in conflict with general principles of trust law, which state that a trustee should not benefit financially from his position as trustee.

Rule change within PS14/09

• Firms may pay away unclaimed client assets (to charity only), having checked that this would be consistent with the arrangements they have put in place with their clients, and that this would be permitted by law.

• A number of changes are being made to the actions which a firm may take as ‘reasonable steps’ to contact a client before paying away unclaimed client assets:

– firms will be expected to attempt to communicate with the client three times in writing (by email or letter) or by telephone using the most recent contact details, allowing at least 28 days between each communication

– firms may use media advertisements to seek the current contact details for, or attempt to communicate with, a ‘gone-away’ client

– any other available means may also be used to seek contact details (including internal records, public records, mortality records and tracing agents).

• Firms will not be expected to continue to attempt to contact clients having received confirmation that contact details are inaccurate.

• When unclaimed client assets are paid away to charity, a firm (or its affiliate) is required to unconditionally undertake to make good any subsequent valid claim from a client and to retain the requisite records indefinitely.

• Any costs incurred by the firm in attempting to contact clients, or insuring against future valid claims in respect of amounts paid away, must be paid from the firm’s own funds.

• For de-minimis amounts up to £25 for retail clients and £100 for professional clients, an abbreviated procedure can be followed whereby the balance may be paid away 28 days after the firm has attempted to contact the client at least once using the most up-to-date contact details.

Impact • Firms should review and amend their procedures and policies for paying away unclaimed client money to ensure that these are consistent with the new rules.

• Firms which do decide to pay away unclaimed client money should consider whether to insure against future valid claims being made from their own funds.

• However, firms are not obliged to pay away unclaimed client money balances and can choose to maintain them indefinitely.

• Firms may need to re-visit customer documentation and agreements in light of the outcome of their impact assessments.

Allocated but unclaimed client money

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 19

Changes relevant to both CASS 6 and 7

(Effective 1 December 2014)

Previous rules • There were no provisions in the custody rules (CASS 6) to deal with unclaimed custody assets.

FCA’s reason for change

• Without a mechanism in the rules to allow firms to deal with unclaimed custody assets, firms had limited choice in resolving the holdings of unclaimed custody assets.

Rule change within PS14/09

• Firms may pay unclaimed custody assets to charity in specie or liquidate those assets and pay the proceeds to charity.

• This procedure will not be available for an unclaimed custody asset until at least 12 years since the firm last received instructions concerning any custody assets from or on behalf of the client.

• Firms should follow the same ‘reasonable steps’ set out above in respect of unclaimed client money balances, but should not wait to the end of this 12 year period to ensure they are holding up-to-date contact details for their clients.

• Firms must also ensure that paying away custody assets in this way would be consistent with the arrangements under which it holds such assets, and would be permitted by law.

Impact • Firms should review and amend their procedures and policies for paying away unclaimed custody assets to ensure that these are consistent with the new rules.

• There are no abbreviated procedures for smaller de-minimis custody balances.

Unclaimed custody assets

20 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Banking exemption 21

Allocation of monies received while operating 22 under the banking exemption

CHANGES RELEVANT TO CASS 7Banking exemption

Client money rules (CASS 7)

(Effective 1 December 2014)

Current rules • This exemption allows firms with permission to accept deposits (banks) to hold money as a deposit.

FCA’s reason for change

• Firms are uncertain as to how they should be holding money under the banking exemption and in what circumstances the money would cease to be held in this way.

• Firms were incorrectly depositing this money in the firm’s own name with third party banks. Firms have used the banking exemption to transfer money to third parties in situations which amounted to them ceasing to use the exemption.

Rule change within PS14/09

• The provision to clients of updated terms of business to reflect the circumstances (if any) in which money would cease to be treated within the banking exemption and be treated as client money is sufficient for the purposes of meeting FCA’s requirement for notifications to clients when operating under the banking exemption.

• If, having assessed their situation, firms do not believe there are any circumstances in which they will cease to treat money within the banking exemption, they do not need to specifically address this point in their terms of business.

• When using the banking exemption firms will be obliged to make the requisite notifications to clients. However, although failure to do so will mean that the firm is in breach of the rules, it should not of itself affect the status of the money.

• If a firm chooses to use the banking exemption for some of its business and it also holds client money as trustee in accordance with the client money rules in relation to other business for that client, the firm will be required to make both notifications to the relevant clients.

Impact • Firms should ensure that they have assessed their own activities to determine whether they do fall outside the banking exemption.

• Firms with complex product and business-lines should conduct assessments to determine that they are operating the exemption correctly.

• It may be necessary to clarify and re-issue terms of business to clients.

• This proposal does not impose a requirement on firms to renegotiate their terms of business with clients.

• The final rules require firms to be more transparent in their terms of business about how they treat the money they receive from clients, but FCA are not expecting these firms to change their business models.

Banking exemption

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 21

Client money rules (CASS 7)

(Effective 1 December 2014)

Current rules • Previously the rules did not discuss this scenario.

FCA’s reason for change

• Seeking to clarify the situation and standardise practices within the industry, the FCA proposed guidance specifying the timeframe within which firms must allocate receipts of client money to the relevant clients.

Rule change within PS14/09

• Where a firm using the banking exemption receives money which, but for the exemption, would otherwise be held as client money, FCA have amended the guidance to say that they would expect firms to allocate these receipts of money promptly and no later than ten business days following receipt.

• The final rules do not specify the way a firm should treat sums of money that it fails to allocate within the time set out in the guidance.

Impact • FCA expects firms to operate systems which enable them to meet this timeframe.

• Where a firm acts as banker to its clients under the banking exemption, failure to allocate the money to clients promptly should not of itself affect the status of how the money is held.

Allocation of monies received while operating under the banking exemption

22 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Trustee firms 23

Trustee firms – acknowledgement letters 24

CHANGES RELEVANT TO CASS 7Trustee firms

Client money rules (CASS 7)

(Effective from 1 July 2014)

Current rules • A firm that acted as a trustee firm when it conducted designated investment business, which was not MiFID business, was required to apply only some of the client money rules.

FCA’s reason for change

• FCA had encountered confusion as to whether the client money distribution rules applied to client money held by a trustee firm.

• The client money rules apply to all client money held by a firm, whereas the trustee may think it prudent to hold all money relating to a specific trust separately from all other trust or firm money. The client money rules currently do not facilitate this.

Rule change within PS14/09

• Client money distribution rules do not apply to trustee firm client money, but still apply to any non-trustee firm client money held by a firm other than in its capacity as a trustee.

• The final rules still allow trustee firms the ability to opt in to complying with all the requirements relating to the following:

a) segregation of client money

b) client money records

c) accounts and reconciliations

d) the acknowledgment letter requirements

e) client money held by a third party.

• When firms hold both trustee firm client money and non-trustee firm client money, these ‘pots’ of client money must be segregated from each other and the relevant rules must be applied to each ‘pot’ separately.

• The rules allow trustee firms to elect to apply the relevant CASS provisions separately to each trust of which they are the trustee firm.

Impact • These changes should provide trustee firms with improved clarity to enable them to treat client money appropriately under the client money rules, or under trust legislation.

• When designing systems and controls, firms must take into account that client money distribution rules only apply in relation to non-trustee client money held by the firm and any other applicable legislation.

Trustee firms

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 23

Client money rules (CASS 7)

(Effective from 1 July 2014)

Current rules • Trustee firms were not required to obtain trust acknowledge-ment letters from institutions with whom they held client money.

FCA’s reason for change

• In response to CP 13/05, FCA received queries from a few trustee firms which had already obtained acknowledgement letters, asking whether they would consequently be required to put new acknowledgement letters in place.

Rule change within PS14/09

• Trustee firms are able to choose to comply with the requirements for acknowledgment letters, but if they do so they must comply with the new rules in full.

Impact • If trustee firms that already have acknowledgement letters in place do not elect to comply with the new rules, they should consider whether they need to take steps to ensure it is clear to the FCA what rules they have chosen to comply with going forward (ie they have not opted in).

Trustee firmsACKNOWLEDGEMENT LETTERS

24 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Transfer clauses 25

Post transfer notifications 26

CHANGES RELEVANT TO CASS 7Transfer of business

Client money rules (CASS 7)

(Effective from 1 December 2014)

Previous rules • When a firm transferred client money to a third party in the course of a transfer of business, the firm had to first obtain each client’s consent to the transfer at at the time of the transfer.

FCA’s reason for change

• Timing issues arose with obtaining consent to the transfer of client money and the process rarely resulted in all clients responding to a request for consent.

Rule change within PS14/09

• The final rules do not restrict the type of transferee that client money can be transferred to.

• There are three ‘ways’ in which a firm may transfer client money to a third party in the context of a transfer of business and in doing so that money will cease to be client money for the firm making the transfer:

1) it may obtain client consent at the time of the transfer;

2) it may include in its client agreement a clause which allows the firm to transfer the client’s money to a third party in the future should the situation arise (where the conditions in the rules are met, including notification requirements); or

3) if the client holds less than or equal to a de minimis amount of client money per client (£25 for retail clients and £100 for other clients), neither form of consent is required (but such clients must be notified within seven days of the transfer taking place).

• Firms may choose whether they include a transfer clause within their written client agreements.

• If firms wish to ensure that the option to transfer client money under such a transfer clause is available to them in the future, they can repaper their client agreements with the appropriate wording.

• If at the time of transfer firms do not have such clauses in their client agreements, they are required to obtain the consent of their clients at the time of the transfer and/or apply the ‘de minimis’ provisions to the extent possible.

• Firms should have regard to legal obligations to clients including requirements under the Unfair Terms Regulations.

• In choosing to insert a transfer clause into client agreements, firms are required to commit:

A) to transferring the sums to another firm that will hold those sums under the client money rules

or

B) to exercising all due skill, care and diligence in assessing whether the person to whom the client money is being transferred will apply adequate measures to protect the sums being transferred.

Impact • Firms involved in business transfers should take into account the revised transfer of business clauses in their project plans.

• Consideration should be given to inserting a clause in standard terms and conditions if firms are re-papering these.

Transfer of businessTRANSFER CLAUSES

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 25

Client money rules (CASS 7)

(Effective from 1 December 2014)

Previous rules • When a firm transferred client money to a third party in the course of a transfer of business, the firm had to first obtain each client’s consent to the transfer at at the time of the transfer.

FCA’s reason for change

• To provide clarity regarding the timing of notifications to clients after a business transfer has taken place.

Rule change within PS14/09

• The transferring firm must ensure that the following notifications are made to clients no later than seven days after the transfer has taken place:

– how the money will be held by the transferee firm;

– the relevant applicable compensation scheme;

– and the option for a client to have transferred sums returned as soon as possible.

• Clients may be notified prior to the transfer taking place.

• The transferring firm has the obligation to ensure that the notifications are made.

Impact • Firms involved in business transfers should take into account the revised transfer of business clauses in their project plans.

• Consideration should be given to inserting a clause in standard terms and conditions if firms are re-papering these.

Transfer of businessPOST TRANSFER NOTIFICATIONS

26 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Immediate segregation 27

Immediate segregation – Interaction with the European Market 28 Infrastructure Regulations (EMIR) for firms that are members of ‘CCPs’

Immediate segregation – Interaction with the DvP window 29 for transactions in commercial settlement systems

Prudent segregation of client money 30

CHANGES RELEVANT TO CASS 7Immediate segregation

Client money rules (CASS 7)

(Deadline 1 June 2015)

Current rules • Unless they use the alternative approach, firms receiving any client money must segregate it promptly into client money bank accounts.

FCA’s reason for change

• A delay in prompt segregation could result in client money being treated by an Insolvency Practitioner as the firm’s own money, and hence a shortfall in the client money available to be distributed.

Rule change within PS14/09

• The Policy Statement clarifies that, unless the firm uses the alternative approach, all client money must be received directly into a client bank account, and may not be received via the firm’s own accounts.

• Firms should ensure that clients and any third parties make transfers of any money which will be client money directly into the firm’s client bank accounts.

• Where firms cannot obtain acknowledgement letters from banks (which may include overseas banks), any receipt of client money into such a bank account would be in breach of the rules.

Impact • Firms adopting the normal approach which currently receive client money into their own bank accounts, must request payment into client bank accounts only.

• Firms must set up procedures whereby client monies received into firm accounts are returned, with a request for payment to the appropriate client bank account.

• This may involve the communication of amended settlement instructions.

• Firms may continue to make payments from their own accounts to client bank accounts in respect of any sum which is due and payable to the client from the firm.

Immediate segregation

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 27

Client money rules (CASS 7)

(Deadline 1 June 2015)

Current rules • Unless they use the alternative approach, firms receiving any client money must segregate it promptly into client money bank accounts.

FCA’s reason for change

• A delay in prompt segregation could result in client money being treated by an Insolvency Practitioner as the firm’s own money, and hence a shortfall in the client money available to be distributed.

• Some respondents to the Consultation Paper commented that firms that are also clearing members of CCPs may be required by CCPs to make and receive single payments due to both the firm and client segregated accounts at the CCP into a single bank account. This will be used to make payments from the firm to the CCP in respect of margin covering all the firm’s accounts (including client segregated accounts), as well as to receive payments from the CCP to the firm.

Rule change within PS14/09

• Firms must use ‘reasonable endeavours’ to ensure that their arrangements with CCPs enable them to make and receive payments relating to the firm’s business into and out of the firm’s bank accounts; and those relating to client payments into or out of client bank accounts.

• If this segregation cannot be achieved, ‘mixed’ amounts must be paid into or out of the firm’s bank accounts. This is to minimise the risk of client money being used to cover margin calls on proprietary accounts at the CCP.

• The client money element of the mixed payments received into the house account must be paid into a client bank account promptly and in any event by the close of business of the next business day following receipt.

• Firms will be required to maintain a prudent segregation of client money (which FCA are calling a ‘clearing arrangement mandatory prudent segregation amount’ (‘CAMPSA’) in their client bank accounts. This is to address the risk that on any given day insufficient client money is held in client bank accounts as a result of the client money element of the mixed payment being received into, and held for a period in, the firm account.

• Firms will be required to create and maintain a ‘clearing arrangement mandatory prudent segregation record’.

• Firms will be required to review the CAMPSA amount that they hold at least quarterly, and will have a period of ten business days to carry out each review and complete any adjustments to the CAMPSA in the client bank account.

Impact • Clearing member firms will need to review and amend their procedures accordingly.

• This should include arrangements in respect of the requirement to maintain and review the CAMPSA which will require appropriate documentation and need to be reflected in CASS resolution packs.

Immediate segregationINTERACTION WITH THE EUROPEAN MARKET INFRASTRUCTURE REGULATION FOR FIRMS THAT ARE MEMBERS OF RECOGNISED CENTRAL COUNTERPARTIES (‘CCPs’)

28 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Client money rules (CASS 7)

(Deadline 1 June 2015)

Current rules • Unless they use the alternative approach, firms receiving any client money must segregate it promptly into client money bank accounts.

FCA’s reason for change

• A delay in prompt segregation could result in client money being treated by an Insolvency Practitioner as the firm’s own money, and hence a shortfall in the client money available to be distributed.

• Some respondents to the Consultation Paper commented that firms that are also clearing members of CCPs may be required by CCPs to make and receive single payments due to both the firm and client segregated accounts at the CCP into a single bank account. This will be used to make payments from the firm to the CCP in respect of margin covering all the firm’s accounts (including client segregated accounts), as well as to receive payments from the CCP to the firm.

• It was noted by respondents to the Consultation Paper that, given the way that some commercial settlement systems operate, firms may need to receive settlement proceeds into their own account prior to making payments to clients or making payments into client bank accounts.

Rule change within PS14/09

• FCA acknowledge that this is how some commercial settlement systems operate. As a result, the final rules clarify that client money received in settlement of a client’s sale that a firm carries out through a commercial settlement system using the DvP window must be segregated into a client bank account promptly, and in any event by the close of business on the business day following its receipt.

Impact • Firms using commercial settlement systems and using the DVP window will need to ensure that their systems and procedures enable the segregation requirements to be carried out within these timeframes.

Immediate segregationINTERACTION WITH THE DVP WINDOW FOR TRANSACTIONS IN COMMERCIAL SETTLEMENT SYSTEMS

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 29

Client money rules (CASS 7)

(Deadline 1 June 2015)

Current rules • Firms are required to transfer out promptly any money paid into a client money account which was not client money, unless it was a minimum sum required to keep the account open.

• Firms are allowed to pay their own money into the account if it is prudent to do so, such monies becoming client money thereafter (often referred to as ‘buffers’).

FCA’s reason for change

• Differing practices within industry indicate that firms currently are uncertain as to when prudent over-segregation is permitted.

• There is a risk that a liquidator could seek to reclaim ‘buffer’ amounts from client money bank accounts and that corporate and client monies are considered to be ‘mixed’.

Rule change within PS14/09

• The rules confirm that firms may transfer their own funds into a client money bank account and keep it there in order to prevent a shortfall occurring – such amounts becoming client money and being referred to as ‘prudent over-segregation’.

• Firms must have a written policy to set out why they consider the use of prudent over-segregation is a reasonable means of addressing each risk and the method that the firm used to calculate the amount segregated to address each risk.

• Firms must maintain a ‘prudent segregation record’ relating to segregation payments made into a client bank account and amounts withdrawn when no longer necessary under the relevant rules. The document should record:

– amounts of payments and withdrawals,

– why such payments or withdrawals were made,

– that each payment or withdrawal was made in accordance with the policy and the relevant client money rules, and

– the total amount of client money segregated pursuant to the rules.

• This record must be retained for a period of five years after the firm ceases to prudently segregate

• Due to the variety of risks that firms may wish to address using this rule, it is for firms to determine the best way of calculating the prudent segregation amount in relation to each risk.

• Firms may prudently segregate for an ad hoc risk not covered by the policy at that time, but must create or amend the policy as soon as practicable to reflect this.

• Prudent over-segregation balances are to be included in firms’ client money reconciliations.

• Prudent over-segregation should not be used by firms as a substitute for accurate and timely record keeping in accordance with other requirements in the client money rules.

Impact • Firms will need to undertake analysis and make a written record of the risks which are to be mitigated through ‘prudent over-segregation.’

• Firms which use, or wish to use ‘prudent over- segregation’ in client money bank accounts must establish a formal policy, and a process for maintaining a ‘prudent segregation record’,

• The ‘prudent segregation record’ must be kept for five years from the date the firm ceases to prudently over segregate.

Prudent segregation of client money

30 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Paying physical receipts into a client bank account 31

Cleared funds 32

Allocation of client money receipts 33

CHANGES RELEVANT TO CASS 7Physical receipts and allocation

of client money

Client money rules (CASS 7)

(Deadline 1 June 2015)

Current rules • CASS 7.4.1 – 7.4.2 requires a firm which receives any client money to pay it promptly into a client money bank account.

FCA’s reason for change

• Differing practices within the industry may leave clients with different levels of protection over their money when received by firms.

• There is a risk that cheques (which are themselves client money), may not be held securely by a firm before being banked.

• Various risks around client money not being allocated to clients in a timely manner and the firm’s records not showing clients’ true entitlement have been identified.

Rule change within PS14/09

• Firms receiving client money in the form of cash, cheque, or other physical means must bank it into a client money bank account (or the firm’s own account if operating under the alternative rules) promptly, and no later than one business day after receipt.

• If a firm is unable to meet the requirement to pay client money received in this format into a client bank account no later than the business day after receipt because of regulatory or other restrictions (such as the Money Laundering Regulations), it must record the receipt in its books, hold it in a secure location and deposit it as soon as possible.

• If a firm receives a post-dated cheque, it must keep it in a secure location, record its receipt in its books and records, and the cheque must be deposited in a client bank account by no later than the date on the cheque (if that is a business day or, if not, the next business day after the date on the cheque).

Impact • Firms need to ensure that they have a secure location such as a safe for holding client money awaiting banking.

• Firms must introduce a control and reconciliation procedure in respect of receipts held prior to banking.

• Any such control will need to be documented in the procedure manual.

Physical receipts and allocation of client moneyPAYING PHYSICAL RECEIPTS INTO A CLIENT BANK ACCOUNT

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 31

Client money rules (CASS 7)

(Deadline 1 June 2015)

Current rules • Although the FCA have indicated disapproval of this practice, the rules do not specifically prohibit trading on uncleared cheques.

FCA’s reason for change

• FCA has seen evidence of some firms trading on receipt of cheques (before they have cleared), and have concerns that this practice can lead to one client’s money inappropriately cross-funding other clients’ trades; and the risk of a potential shortfall in client money if a cheque is dishonoured after a deal has been placed.

Rule change within PS14/09

• The final rules set out explicit guidance that states that a firm should ensure its organisational arrangements are ‘adequate to minimise the risk’ that client money may be used on behalf of a client whose money has yet to be received by the firm.

• The final rules also reiterate that the statutory trust does not permit a firm to use client money to advance credit to the firm’s clients, to itself, or to any other person

• The rules do not prohibit firms using their own money to fund clients’ trades (for example, before receiving funds from clients).

• Firms which receive post-dated cheques may return them to clients, or keep them in a secure location. If kept, the cheques must be recorded in the firm’s records, and deposited in a client bank account on the date of the cheque (or the next business day, if the cheque date isn’t a business day).

Impact • Firms should ensure that their systems and procedures ensure that:

– client money received from a client has cleared, before trades are carried out in respect of the sums received

– client money received from a sale has cleared before any payment is made to the client.

• They must also ensure that they have appropriate procedures and controls in place if they choose to transfer the firm’s own money into the client bank account in order to fund deals relating to clients whose funds have not yet cleared.

• Although firms may be able to make use of the prudent segregation rules in this context, this would require considerable care to ensure that these rules were not breached.

• Firms will need to review their procedures for post-dated cheques in light of the explicit rules relating to them.

Physical receipts and allocation of client moneyCLEARED FUNDS

32 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Client money rules (CASS 7)

(Deadline 1 June 2015)

Current rules • Firms are required to allocate client money to individual clients promptly, and no later than 10 business days after notification of receipt.

• If mixed remittances of client and firm money are received, these should be paid into the client bank account; with the non-client element transferred out within one business day.

FCA’s reason for change

• Firms may receive money which they know is client money, but are unable to identify which client(s) it relates to. (For instance an HMRC refund covering a large number of clients invested in the same product).

• Lack of clarification within the industry has led to differing practices, resulting in different levels of protection being offered to clients.

• FCA also has concerns about risks arising when client money is not allocated to clients promptly, meaning their true entitlements may not be reflected in the firm’s records.

Rule change within PS14/09

• Firms will be required to allocate client money receipts promptly, and within ten business days of receipt.

• They must record this money as ‘unallocated client money’ while working to allocate the payment.

• Where a firm is unable to identify money it receives as client money or its own money, it must treat this as ‘unidentified client money’ while taking all necessary steps to determine its status.

• Firms should segregate the amount reasonably believed to represent client money as client money, while working to allocate the payment.

• If firms cannot identify whether money received is client money or the firms’, they should consider whether it should be returned to the payer.

Impact • Firms will need to review and adjust their allocation and reconciliation procedures if necessary.

• Firms will need to consider the circumstances under which unidentified money is returned to the sender, and update their procedures accordingly.

Physical receipts and allocation of client moneyALLOCATION OF CLIENT MONEY RECEIPTS

HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM 33

34 HOW THE NEW CLIENT MONEY RULES WILL AFFECT YOUR FIRM

Firms’ use of the alternative approach 35

Auditor assurances 36