How Strategic Shifts within the Pharmaceutical Sector · PDF fileHow Strategic Shifts within...

35

How Strategic Shifts within the Pharmaceutical Sector will Transform Supply Chain and Distribution Models LogiPharma Oct 23 rd , 2013 Eelco Dijkstra Senior Strategy Consultant +31 6 246 61 688 [email protected] Singapore

Transcript of How Strategic Shifts within the Pharmaceutical Sector · PDF fileHow Strategic Shifts within...

How Strategic Shifts within thePharmaceutical Sector will TransformSupply Chain and Distribution Models

LogiPharma Oct 23rd, 2013

Eelco DijkstraSenior Strategy Consultant

+31 6 246 61 [email protected]

Singapore

1

BCI IntroductionBoutique consulting and implementation firm with areas of activity for:

Corporate clients

Supply chain strategy development Supply chain network optimization/modeling Inventory analysis and optimization Transport & carrier optimization Logistic outsourcing Location and Site selection Real estate investment strategies

Profile

Headquartered in the Netherlands Founded in 1985 Employs 70 full-time professionals Global network partnership with St.Onge (US based)

and OLE (China based) Partnership with 175 professionals Global presence based upon local know how and

expertise Focus industries: Pharma, Medtech, FMCG, Industrial,

Lifestyle/Fashion, FoodUnderstanding…

ChangePeopleNetworkPartnersStrategy Organization

Aligning supplychain strategywith businessobjectives &goals

Aligning supplychain strategywith tradingpartnerstrategies

Translatingsupply chainstrategy inoptimizednetworks

Designorganizationand processeslinked with thestrategy

Using the humanintellect todetail the futurestate and act asagents forchange

Impactassessment anddeveloping thetransitioningstrategy

Managing thetransition andsustaining thesuccess

Implementation

Buck Consultants International

Linking strategy to execution

ConsultingStrategy, Network

Inventory Optimization& TransportationS&OP planning

EngineeringHigh Performance

Manufacturing,Packaging, Distribution

FacilitiesOperations

Planning,Management

& Training

Supply Chain Information Systems

Project Management

Implementation Planning Execution Change mngt

2 Buck Consultants International

A unique base of experience of healthcarelogistics projects around the globe

3

EMEA North-America

Latin-America China/Asia-Pacific

Buck Consultants International

Agenda

1. Changing Operating Landscape2. Results APAC Survey3. Distribution Optimisation – Business Case4. Step changes ahead

Buck Consultants International, 2013 4

Business StrategyThe commercial model is changing and willcontinue to change, having an impact onthe supply chain set-up of the future

Source: arvato services, adjusted by BCI

Wholesaler

Pharmacy,Hospital,Care Institution

Patient

PhysicianDirect to ...

Direct to patient

Sales Management

e-fulfilment

Order-to-cash

Phar

mac

eutic

al co

mpa

ny

Direct to

Patient

Changing business elements within the current businessmodel of Pharmaceutical companies.

Buck Consultants International, 2013 5

A. Changing Landscape

Buck Consultants International, 2013 6

Trends in the healthcare market and impact on supplychainsMarket/businessenvironment

Business strategy Supply chain

• Ending patents

• Generic entries

• Cost-cutting in healthcaresystems

• QA / RA (e.g. new GDP)

• More direct sales

• eCommerce?

• Mergers/acquisitions

• New product launches

• Customer segmentation

• Centralization management

• Emerging markets

• Overall focus on costreduction

• Central management

• Consolidated distribution

• Supply chain integration &differentiation

• Visibility

• Collaboration

• Direct models

Main Pharma SC Trends and DevelopmentsThe Brand Owner’s Perspective

Buck Consultants International, 2013 7

Centralization ofSupply Chain Control

Network Redesign

Outsourcing & PartnerPortfolio Reduction

Strengthening of Corporate SC Organizations Investments in SC Talent Corporate SC taking ownership of the downstream

supply chain

Consolidation of Distribution Networks Mix of full centralization, regionalization and hub-

spoke models Scope: downstream, still lack of full chain scope

3PL landscape in pharma has improved highly Towards LLP/4PL models Strong reduction of number of partners used Towards harmonized (global) contracts

Visibility Control Tower / Transport Management concepts Linking inbound, intercompany and secondary

distribution Information is Key

Main Pharma SC Trends and DevelopmentsThe Brand Owner’s Perspective

Buck Consultants International, 2013 8

Customer Service /Order to Cashprocessharmonization

Supply ChainDifferentiation

Supply ChainCollaboration

CS and O2C activities closely linked to physicalsupply chains

Harmonization & centralization of CS and O2Corganizations

From one size fits all to differentiated supply chainsper product/market combination

SC becoming a stronger counterpart for thecommercial team, challenging service requirements

Logistics not a key differentiator, therefore theindustry is recognizing the opportunities ofcollaboration

How to break through from pilots to full realization?

B. Results APAC Survey

Buck Consultants International, 2013 9

We asked Pharma Executives how they view their keychallenges in APAC

Company Characteristics

Buck Consultants International, 2013 10

64%

20%

16%

Corporation Type

Pharmaceutical/bio-pharma company

Medical Devicecompany

Other

24%

7%

7%62%

0%

Sales Model Type

Distributor model percountry all channels

Distributor model percountry, hospitals direct

Direct sales all channels

Hybrid, mix of all beforementioned models

Other

Key Business Challenges in APAC

Buck Consultants International, 2013 11

1

1

2

2

6

10

18

18

21

24

40

SEA as a set of markets

Japan as a market

Bribery and corruption

Patent expiries

India as a market

Integration as result of a company Merger/acquisition

China as a market

Maintaining current levels of sales

Regulatory, Import licenses, customs

Increasing Operating Costs and reduced margins

Revenue growth across the region

Types of Business ChallengesType of Challenges weighted by importance

Key Supply Chain Challenges in APAC

Buck Consultants International, 2013 12

5

6

6

10

10

12

15

15

16

21

22

No APAC Supply chain strategy in place

Complexity in # languages, # regulations and # packaging

Not scalable for future growth

Integrating supply chain's due to merger/acquisition

Managing LSP contracts and performancer metrics across region

Fragmented local for local country set up in place

Increasing warehousing and transportation costs

Regulatory environment (import licences and duties)

Shift from distributor to go direct business model in certaingeographies

Supporting sales growth new markets

Mitigating supply chain risks across region

Supply Chain ChallengesTypes of Challenges weighted by importance

Supply Chain Configuration

Buck Consultants International, 2013 13

52%

12%

15%

9%

9%

3%

Supply Chain Network Design

Country for Countrydistribution centresreplenished from globalplants

Regional distributioncentre - combined withdirect distribution to APACcustomers

Regional distributioncentre - replenishingcountry distributioncentres

Global distribution centre

Central distribution withpostponement / re-labelling capabilities

Other

1 2 to 5 5- to 10 >10# of DC's 0 4 3 16

02468

1012141618

Number of Finished Goods DCs operatingacross APAC

Outsourcing Mixed Model Own AccountDistribution Type 13 11 0

0

2

4

6

8

10

12

14

Distribution Network Approach

Supply Chain Configuration (2)

Buck Consultants International, 2013 14

1 2 to 5 5 to 10 >10# Logistics Providers 0 8 8 16

02468

1012141618

# Logistics Providers

13%

17%

70%

Approach towards order to cash

Outsourcing

Own Account

Mixed Model

Regionalization (1)

Buck Consultants International, 2013 15

32%

17%

51%

# of companies having explored theoption to regionalize their distribution

network in APAC

Yes

No

N/A 20%

23%

9%

19%

27%

2%

Benefits of regionalization

Reduced time to market

Increased availability ofmaterials

Lower corporate tax rate

Reduced supply chaincosts

Scalable platform forgrowth

Other

Network (Re)Design

Buck Consultants International, 2013 16

80%

15%

5%

Last review of SC network configuration

Currently being reviewed

approx 1 year ago

more than 2 years ago

80%of pharma companies are currently reviewing their supply chain in the APAC region

Supply ChainStrategy is more thanmeets the eye

It’s about securing optimalvalue from your supplychain network and from yourservice providers

… at lowest possible totalcost

Transport and Warehouse costs

Network optimisationInventory managementIT & TechnologiesVisibility and Control TowersCollaborationRelationship ManagementEnd-to-end lead time optimisationCost to Serve diversification

C. Network Redesign

Buck Consultants International, 2013 18

The majority of a supply chain’slifecycle costs are locked-in at thestart Manufacturing/supplier network Distribution network Inventory Locations Inventory Levels Service policies

Also the supply chain putsboundaries on/createsopportunities for flexibility anddifferentiation in terms of servicelevels, speed to market, etc.Decisions Solutions Value

APS

ERP / MRP

Execution

Strategic andTactical

Supply ChainOptimization

80%

20%Ope

ratio

nal

Tac

tical

S

trate

gic

Why (re)design your network?

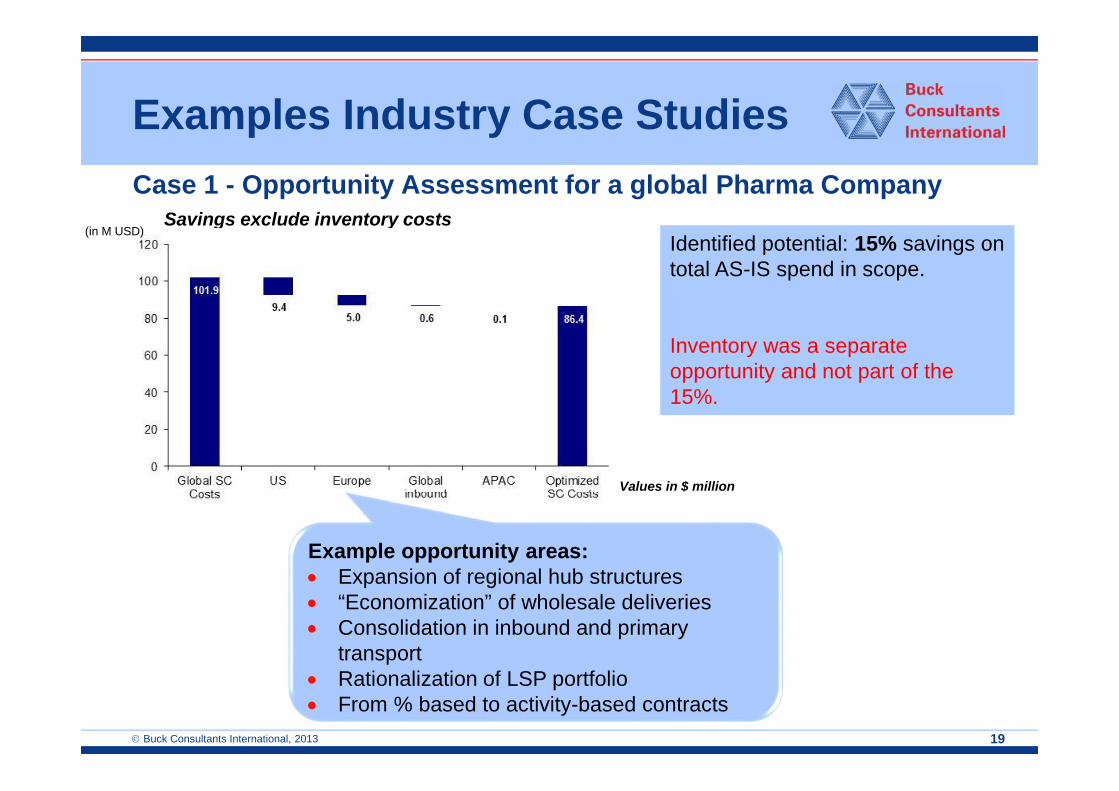

Case 1 - Opportunity Assessment for a global Pharma Company

19

Savings exclude inventory costsIdentified potential: 15% savings ontotal AS-IS spend in scope.

Inventory was a separateopportunity and not part of the15%.

Values in $ million

(in M USD)

Example opportunity areas: Expansion of regional hub structures “Economization” of wholesale deliveries Consolidation in inbound and primary

transport Rationalization of LSP portfolio From % based to activity-based contracts

Examples Industry Case Studies

Buck Consultants International, 2013

Case 2 – Cost To Serve Analyses GlobalPharma Company

Company profile Global Pharma company Top management driving towards step-

changes BCI challenged to go beyond the basic

network optimization

Solutions identified and proposed to management

“economic wholesale model” changing order behavior of wholesalersthroughout Europe, moving to a general policy of: max 1 order/delivery frequency perweek, shipped with a lead-time of 48-72 hours savings: 25+%

“Differentiated supply chain” creating basically three supply chains,managed centrally: Centralized: high value bio products Regionalized: 6 hubs throughout Europe shipping to wholesalers and

hospitals/pharmacies Localized: narcotics products and products that are time critical

savings: ~12.5%20 Buck Consultants International, 2013

Case 3 – Network Optimization ofDiversified Pharma Company

Company profile Global Pharma company Need to rationalize the supply chain from a cost, compliance and “fit for future”

perspective

2012-2015 2015-2018

To 1, 2, 3 RDCs?From Local for Local network To regional DC networks

No harmonization Relatively high costs Limited visibility Compliance?

Harmonization / Differentiation Lower costs 15% Improved visibility Compliance!

Harmonization! Lower costs! 25+% Full Visibility! Compliance!

21 Buck Consultants International, 2013

Case Study APACNetwork Optimization Study

(1) Country Level Distribution Networkreplenished from global production sources.

(2) RDC in APAC in combination with directship program to country level market channels.

(3) RDC in APAC with Country Level Satellitesfor Distribution.

Buck Consultants International, 2013 23

Supply Chain Configurations -Scenarios

(4) Combination of scenarios 2 and 3. Scenario 3 replenishment is applied to NEA, Scenario 2 direct ship from RDC is applied to

SEA.

(5) Combination of scenarios 1 and 2. Scenario 1 country for country distribution is

applied to NEA, Scenario 2 direct ship from RDC is applied to

SEA

Buck Consultants International, 2013 24

Supply Chain Configurations -Scenarios (cont.)

NEA

SEA

SEA

NEA

1. Country level 2. RDC 3. RDC withsatellites

4. Combi of 2(SEA) and 3 (NEA)

5. Combi of 1(NEA) and 2 (SEA)

total costs 39,7 43,1 47,5 46,4 41,2cost index incl inventory 100 109 120 117 104inventory 20,0 20,0 20,0 20,0 20,0outbound transportation 6,0 9,9 6,0 7,2 7,2replenishment 6,3 4,4labour 1,4 1,2 1,7 1,5 1,7space 6,0 6,5 8,1 7,8 6,3inbound transportation 6,3 5,6 5,6 5,6 6,1

-

10,0

20,0

30,0

40,0

50,0

Buck Consultants International, 2013 25

Results with InventoryScenarios (in Million USD)

Introducing the Postponement Concept

By applying postponement, the moment of product labelling can be delayed,which effectively enables companies to reduce their inventory levels, due to theadvantages of inventory pooling.

Buck Consultants International, 2013 26

Postponement Centre

Applying the Postponement Strategy

Let’s apply the postponement strategy to scenarios 2,3 and 4 which have a RDC to enablepostponement.

Buck Consultants International, 2013 27

RegionalPostponement

Centre SIN

AFTER

ID

TH

MY

BEFORE

Instead of shipping products directly to consumer markets, one can delay the labelling phase untilproducts reach the postponement centre. By doing so, one can benefit from inventory pooling.

In the example above, we have assumed that the inventory costs for the NEA markets were diminishedby 40%. However, we have also experienced higher possible inventory savings. Therefore, in the

“before” scenario 15 products we needed, whereas in the “after” scenario 9 products were required tofulfil consumer markets in NEA.

Buck Consultants International, 2013 28

Results with Inventory and withPostponement (in Million USD)

1. Country level (nopostponement) 2. RDC + postponement 3. RDC with satellites +

postponement4. Combi of 2 (SEA) and3 (NEA) + postponement

total costs 39,7 35,1 39,6 38,4cost index incl inventory 113 100 113 109inventory index 100 60 60 60inventory 20,0 12,0 12,0 12,0outbound transportation 6,0 9,9 6,0 7,2replenishment 6,3 4,4labour 1,4 1,2 1,7 1,5space 6,0 6,5 8,1 7,8inbound transportation 6,3 5,6 5,6 5,6

-

10,0

20,0

30,0

40,0

50,0

Buck Consultants International, 2013 29

Total costIncl. inventory

Cost with inventorywith postponement

Inventory Index

Lead Times

1. Country Level

$ 39.7M

$ 39.7M

100

1-2 Days

2. RDC

$ 43.1M

$ 35.1M

60

2-4 Days

3. RDC & Satellites

$ 47.5M

$ 39.6M

60

1-2 Days

4. Combi of scenario’s2 (SEA) and 3 (NEA)

$ 46.4M

$ 38.4M

60

1-4 Days

Overview Customer Flows & SummaryScenarios: Costs (in millions)

5. Combi of scenario’s 1(NEA) and 2 (SEA)

$ 41.2M

-

-

1-4 Days

More Responsive Supply Chain Model

One size for sure doesn’tfit all!

Many variables: Marketvolumes, product value,product sources,regulatory environment

Cost to serve modelprovides ability todifferentiate per product,market and customer type

Supplychain

complexity

Productsand

services

Processesand

systems

Configurationand

structure

Buck Consultants International, 2013 30

Buck Consultants International, 2013 31

Opportunity Potential Depends Heavily onSupply Chain Scope Under Review

Widening the scope of a supply chain review increases the number ofalternative solutions and therefore the potential savings. But there is more.Complexity and risks are factors that increase as well when wideningthe scope

• # Alternativesolutions

• Complexity

• Risks

• Savingspotential

Project scopeLimited scope Broader scope

No structuralchange =>

2-3% savings

Structural change=> 10-20% savings

+Repositioning thevalue proposition

Value focus

Strategic

Cost focus

Tactical

Analytics andReporting

Carrier and partnerselection

Rate discussions

Supply chainCosts

On timeperformancePlanning

Business model

Delivery and Networkmodel

Customerexperience

Transactionalrelationships

Transport costs

Value addedLogistics services

Inventory Management

Concluding:The Industry is going through a Period of Change… AnExcellent Opportunity for Supply Chain to Move up theValue Chain

Buck Consultants International, 2013 32

How Does this Translate to you?

Drive real change within your company Take the current momentum to position supply chain as a

strategic asset towards Executive Management Everything starts with data & information

Although cost is not always the driver: on average ourclients saved 10 – 18% through “basic” network re-design projects

Clear upside potential when broadening the scope toinventory management and business model changessupported by supply chain

Buck Consultants International, 2013 33