How America Eats

58

How America Eats: What Impact the Choices? Sally Lyons Wyatt Executive Vice President & Practice Leader April 21, 2016

Transcript of How America Eats

How America Eats: What Impact the Choices?

Sally Lyons Wyatt

Executive Vice President & Practice Leader

April 21, 2016

THE GAME PLAN

The Field (Industry Trends)

Past and Present Teams (Consumer Eating Trends) Plays of the Day (Millennials, Hispanics, H&W, & Claims)

How to Win Going Forward (The Strategy)

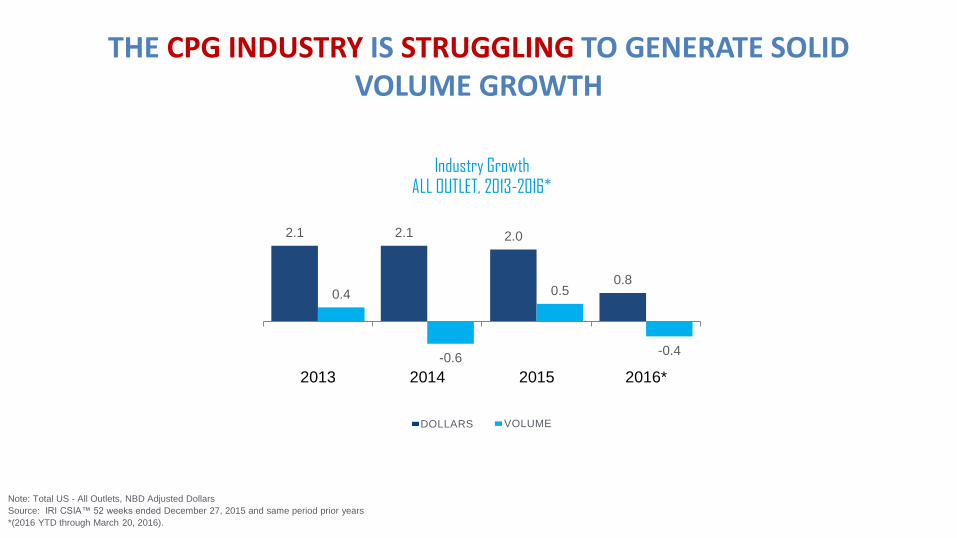

THE CPG INDUSTRY IS STRUGGLING TO GENERATE SOLID VOLUME GROWTH

ALL OUTLET, 2013-2016*

DOLLARS VOLUME

Note: Total US - All Outlets, NBD Adjusted Dollars

Source: IRI CSIA™ 52 weeks ended December 27, 2015 and same period prior years

*(2016 YTD through March 20, 2016).

Industry Growth

2.1 2.1 2.0

0.8 0.4

-0.6

0.5

-0.4

2013 2014 2015 2016*

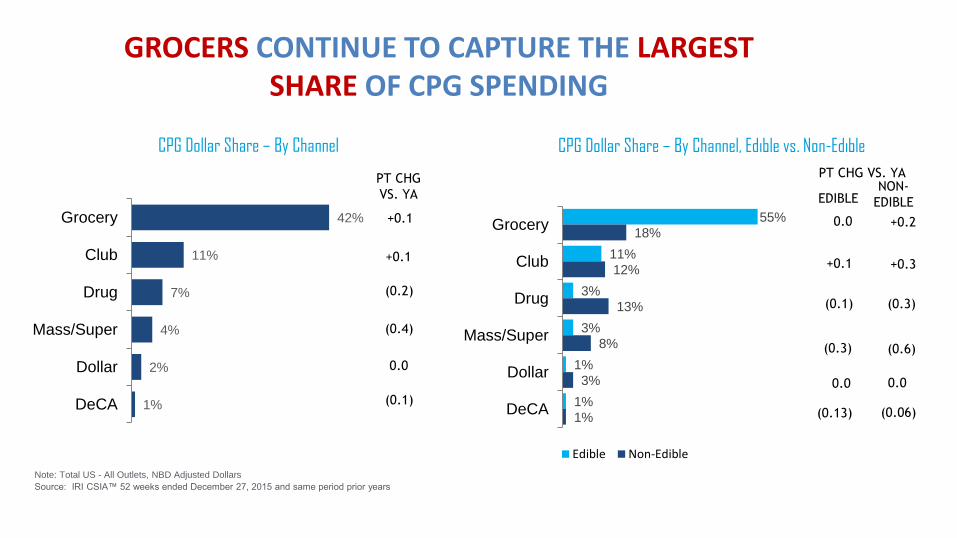

GROCERS CONTINUE TO CAPTURE THE LARGEST SHARE OF CPG SPENDING

Note: Total US - All Outlets, NBD Adjusted Dollars

Source: IRI CSIA™ 52 weeks ended December 27, 2015 and same period prior years

CPG Dollar Share – By Channel CPG Dollar Share – By Channel, Edible vs. Non-Edible

PT CHG

VS. YA

0.0

0.0

(0.3)

(0.1)

+0.1

EDIBLE

+0.2

0.0

(0.6)

(0.3)

+0.3

NON-

EDIBLE

PT CHG VS. YA

42%

11%

7%

4%

2%

1%

Grocery

Club

Drug

Mass/Super

Dollar

DeCA

+0.1

0.0

(0.4)

(0.2)

+0.1

(0.1)

55%

11%

3%

3%

1%

1%

18%

12%

13%

8%

3%

1%

Grocery

Club

Drug

Mass/Super

Dollar

DeCA

Edible Non-Edible

(0.13) (0.06)

VARIETY OF TRENDS IMPACTING CATEGORIES ACROSS THE STORE

CPG Sales % Chg. vs. YA, by Department, MULOC

3.2%

5.4% 5.3% 5.1% 4.7%

2.9% 2.5%

2.0% 2.0% 2.0% 1.3%

0.90%

3.2% 3.1% 3.6%

1.6% 1.0%

1.3%

0.1% 0.2%

-0.4%

-1.2% TOTAL

STORE

BEVERAGES LIQUOR TOBACCO HEALTH GENERAL

MERCH

REFRIG. BEAUTY HOME

CARE

GENERAL

FOOD

FROZEN

Source: IRI Market Advantage™ 52 weeks ended December 27, 2015, and same period prior year

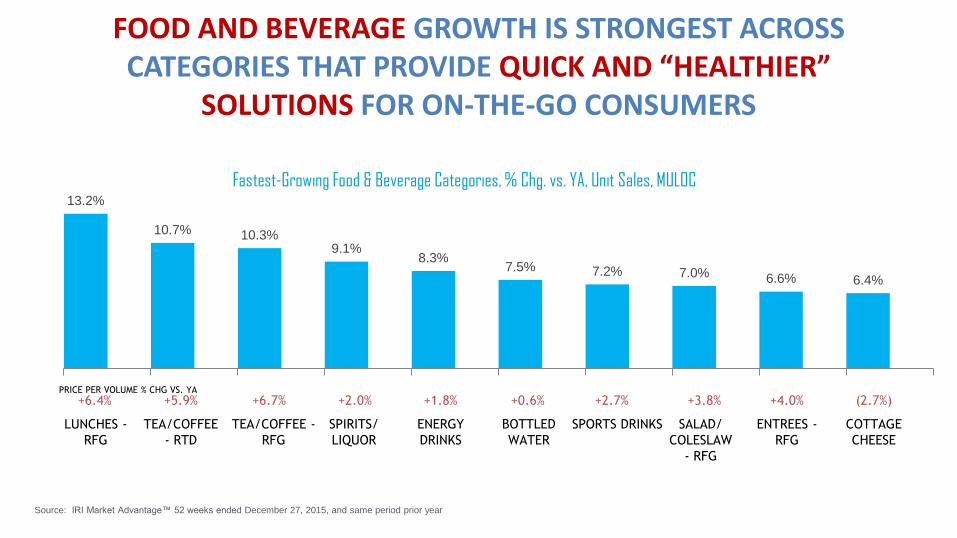

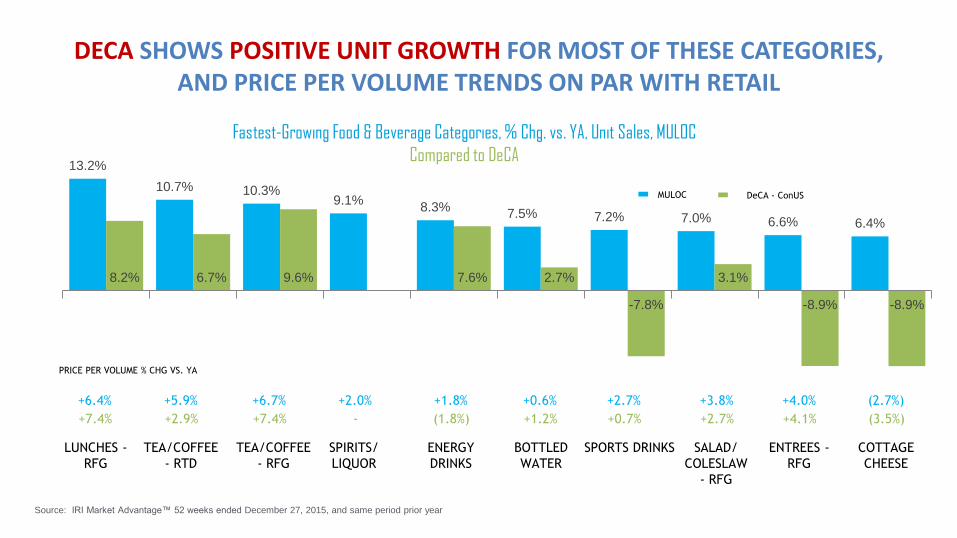

13.2%

10.7% 10.3% 9.1%

8.3% 7.5% 7.2% 7.0% 6.6% 6.4%

FOOD AND BEVERAGE GROWTH IS STRONGEST ACROSS CATEGORIES THAT PROVIDE QUICK AND “HEALTHIER”

SOLUTIONS FOR ON-THE-GO CONSUMERS

Fastest-Growing Food & Beverage Categories, % Chg. vs. YA, Unit Sales, MULOC

Source: IRI Market Advantage™ 52 weeks ended December 27, 2015, and same period prior year

+6.4% +5.9% +6.7% +2.0% +1.8% +0.6% +2.7% +3.8% +4.0% (2.7%)

LUNCHES -

RFG

TEA/COFFEE

- RTD

TEA/COFFEE -

RFG

SPIRITS/

LIQUOR

ENERGY

DRINKS

BOTTLED

WATER

SPORTS DRINKS SALAD/

COLESLAW

- RFG

ENTREES -

RFG

COTTAGE

CHEESE

PRICE PER VOLUME % CHG VS. YA

13.2%

10.7% 10.3% 9.1%

8.3% 7.5% 7.2% 7.0% 6.6% 6.4%

8.2% 6.7% 9.6% 7.6% 2.7%

-7.8%

3.1%

-8.9% -8.9%

DECA SHOWS POSITIVE UNIT GROWTH FOR MOST OF THESE CATEGORIES, AND PRICE PER VOLUME TRENDS ON PAR WITH RETAIL

Fastest-Growing Food & Beverage Categories, % Chg. vs. YA, Unit Sales, MULOC

Compared to DeCA

Source: IRI Market Advantage™ 52 weeks ended December 27, 2015, and same period prior year

+6.4% +5.9% +6.7% +2.0% +1.8% +0.6% +2.7% +3.8% +4.0% (2.7%)

LUNCHES -

RFG

TEA/COFFEE

- RTD

TEA/COFFEE

- RFG

SPIRITS/

LIQUOR

ENERGY

DRINKS

BOTTLED

WATER

SPORTS DRINKS SALAD/

COLESLAW

- RFG

ENTREES -

RFG

COTTAGE

CHEESE

MULOC DeCA - ConUS

PRICE PER VOLUME % CHG VS. YA

+7.4% +2.9% +7.4% - (1.8%) +1.2% +0.7% +2.7% +4.1% (3.5%)

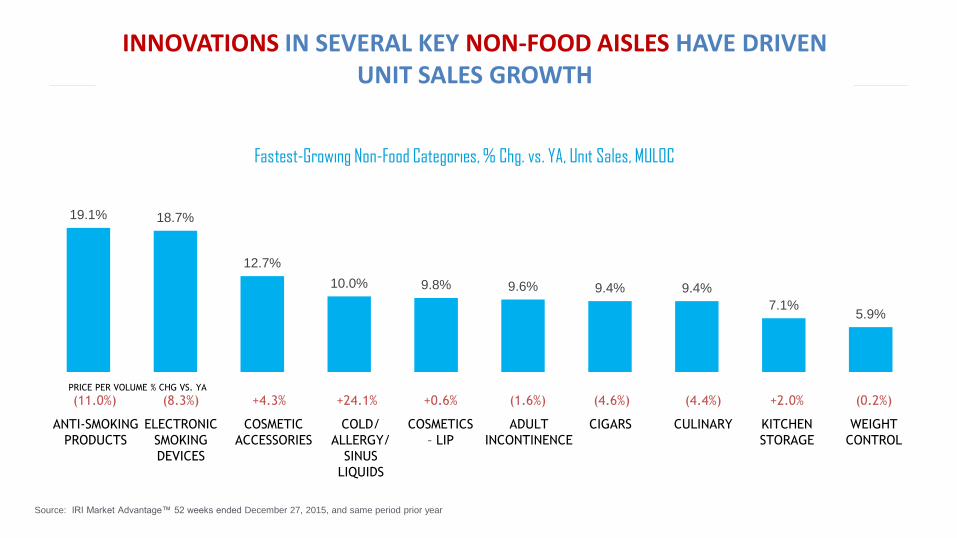

19.1% 18.7%

12.7%

10.0% 9.8% 9.6% 9.4% 9.4%

7.1% 5.9%

INNOVATIONS IN SEVERAL KEY NON-FOOD AISLES HAVE DRIVEN UNIT SALES GROWTH

Fastest-Growing Non-Food Categories, % Chg. vs. YA, Unit Sales, MULOC

Source: IRI Market Advantage™ 52 weeks ended December 27, 2015, and same period prior year

(11.0%) (8.3%) +4.3% +24.1% +0.6% (1.6%) (4.6%) (4.4%) +2.0% (0.2%)

ANTI-SMOKING

PRODUCTS

ELECTRONIC

SMOKING

DEVICES

COSMETIC

ACCESSORIES

COLD/

ALLERGY/

SINUS

LIQUIDS

COSMETICS

– LIP

ADULT

INCONTINENCE

CIGARS CULINARY KITCHEN

STORAGE

WEIGHT

CONTROL

PRICE PER VOLUME % CHG VS. YA

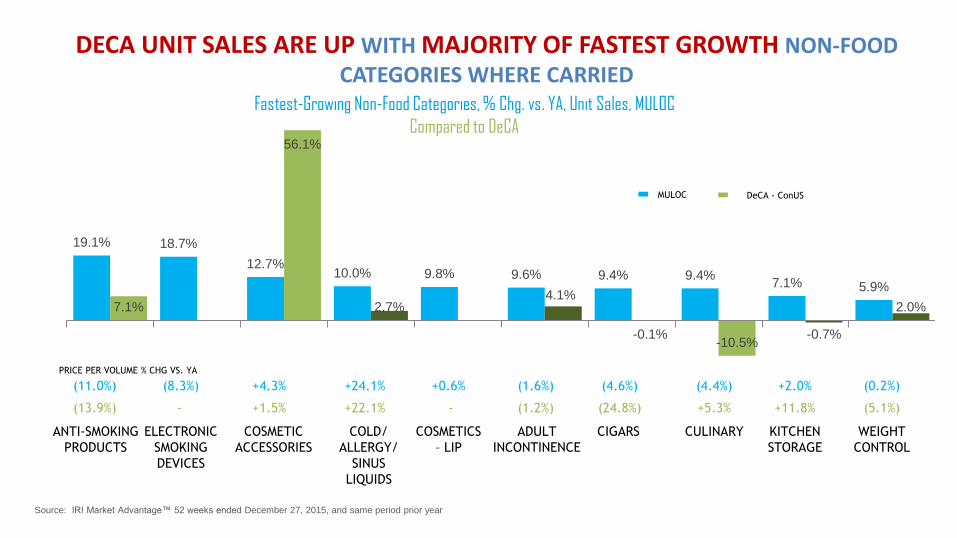

19.1% 18.7%

12.7% 10.0% 9.8% 9.6% 9.4% 9.4%

7.1% 5.9%

7.1%

56.1%

2.7% 4.1%

-0.1% -10.5%

-0.7%

2.0%

DECA UNIT SALES ARE UP WITH MAJORITY OF FASTEST GROWTH NON-FOOD CATEGORIES WHERE CARRIED

Fastest-Growing Non-Food Categories, % Chg. vs. YA, Unit Sales, MULOC

Compared to DeCA

Source: IRI Market Advantage™ 52 weeks ended December 27, 2015, and same period prior year

(11.0%) (8.3%) +4.3% +24.1% +0.6% (1.6%) (4.6%) (4.4%) +2.0% (0.2%)

ANTI-SMOKING

PRODUCTS

ELECTRONIC

SMOKING

DEVICES

COSMETIC

ACCESSORIES

COLD/

ALLERGY/

SINUS

LIQUIDS

COSMETICS

– LIP

ADULT

INCONTINENCE

CIGARS CULINARY KITCHEN

STORAGE

WEIGHT

CONTROL

MULOC DeCA - ConUS

PRICE PER VOLUME % CHG VS. YA

(13.9%) +1.5% +22.1% (1.2%) (24.8%) +5.3% +11.8% (5.1%) - -

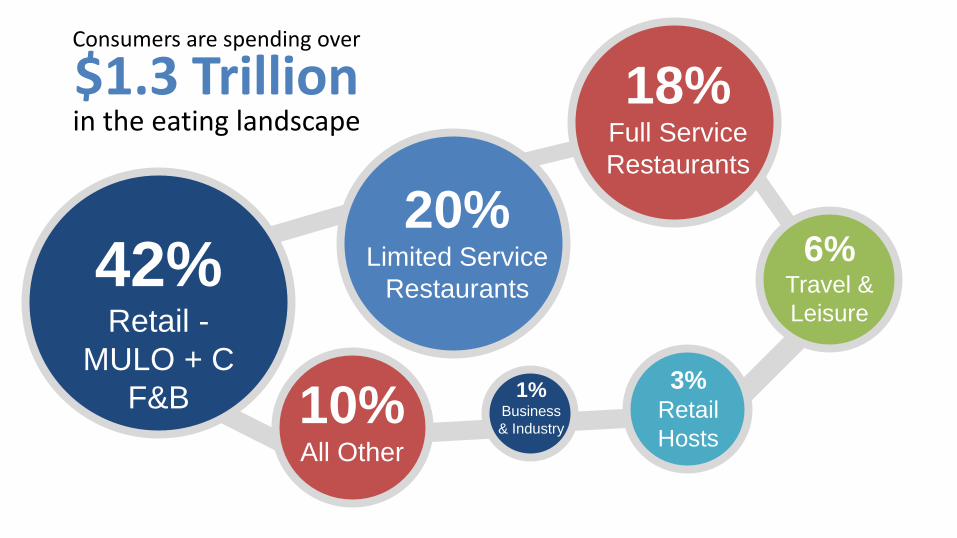

Consumers are spending over

$1.3 Trillion in the eating landscape

42% Retail -

MULO + C

F&B

20% Limited Service

Restaurants

6% Travel &

Leisure

3% Retail

Hosts

1% Business

& Industry

18% Full Service

Restaurants

10% All Other

THE EATING LANDSCAPE IS DIVERSE

VENDING MACHINES HAVE EVOLVED TO ADDRESS CONSUMER NEEDS AND DEMAND MOMENTS

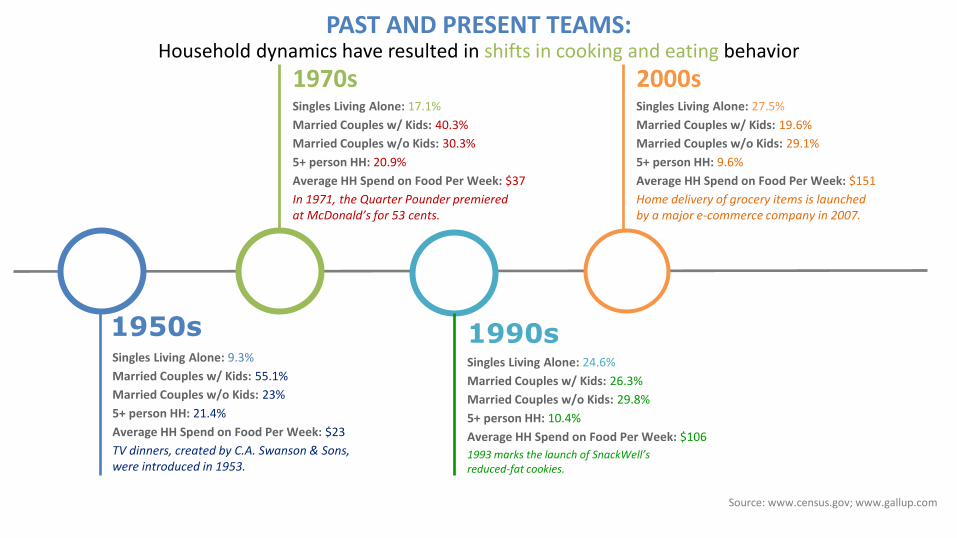

PAST AND PRESENT TEAMS: Household dynamics have resulted in shifts in cooking and eating behavior

1950s Singles Living Alone: 9.3%

Married Couples w/ Kids: 55.1%

Married Couples w/o Kids: 23%

5+ person HH: 21.4%

Average HH Spend on Food Per Week: $23

TV dinners, created by C.A. Swanson & Sons, were introduced in 1953.

1970s Singles Living Alone: 17.1%

Married Couples w/ Kids: 40.3%

Married Couples w/o Kids: 30.3%

5+ person HH: 20.9%

Average HH Spend on Food Per Week: $37

In 1971, the Quarter Pounder premiered at McDonald’s for 53 cents.

1990s Singles Living Alone: 24.6%

Married Couples w/ Kids: 26.3%

Married Couples w/o Kids: 29.8%

5+ person HH: 10.4%

Average HH Spend on Food Per Week: $106

1993 marks the launch of SnackWell’s reduced-fat cookies.

2000s Singles Living Alone: 27.5%

Married Couples w/ Kids: 19.6%

Married Couples w/o Kids: 29.1%

5+ person HH: 9.6%

Average HH Spend on Food Per Week: $151

Home delivery of grocery items is launched by a major e-commerce company in 2007.

Source: www.census.gov; www.gallup.com

EVOLUTION OF COOKING AND EATING

The “Then” Team

Tried and true family recipes

Three meals a day

Cooking as a chore

Source: WBTB Shopping Study, November 2014

THE U.S. SHOPPER IS BECOMING MORE DIVERSE

309M USA Population 2010

3M White

10% growth

13M Hispanic

53% growth

4M Black

16% growth

4M Asian

15% growth

1M Other

5% growth

Hispanics will account for 53% of population growth

334M USA Population 2020

PLAYERS HAVE CHANGED - More people working and not retiring at 65

CONSUMERS WANT TO CONSUME FRESHER FOODS AS PART OF THEIR WELLNESS GOALS

Source: National Consumer Panel Survey: Total US: CY 2013

Health and Wellness Trends

Being physically fit & active

Consuming fresher foods

Consuming more Gluten-free foods

Feeling good about yourself

Portion control

Buying organic / natural products

Not being overweight

Cooking at home / eating with family

EATING OCCASIONS HAVE CHANGED

“I eat 3 square meals a day and no snacks”

“I eat 3 square meals and several snacks”

“I eat 4-5 mini meals”

“I eat on the run and grab food when I have a chance”

LEADING TO “TODAY’S” TEAM COOKING AND EATING STYLE

“Social” recipes

Hybrid homemade & meal preparation

Cooking is fun

Source: WBTB Shopping Study, November 2014

We are obsessed with food

10.9% 9.6%

5.0% 3.6% 3.3% 2.7%

1.5% 1.3% 0.7%

-7.1%

3.2% 0.1%

-7.7% -3.7% -3.6% -4.8% -4.5% -7.0% -4.8% -12.8%

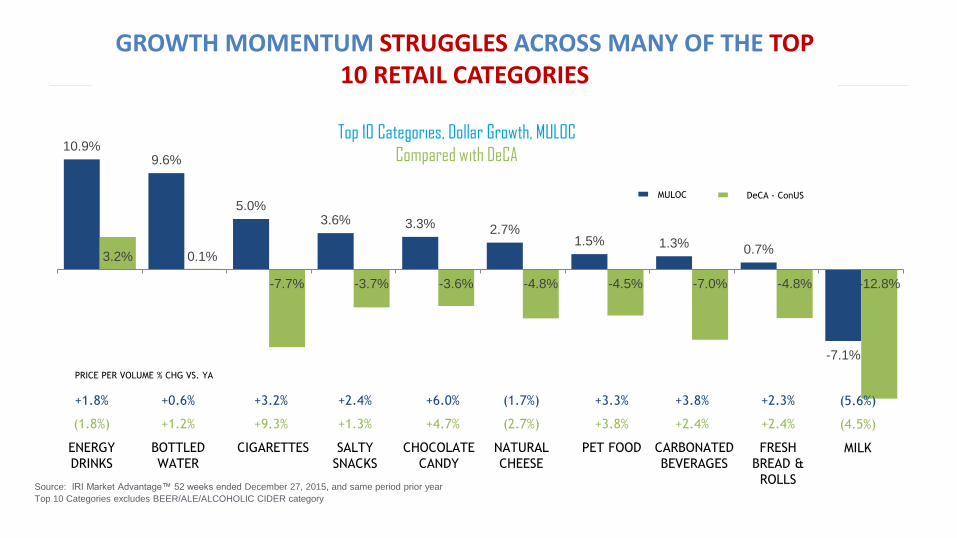

GROWTH MOMENTUM STRUGGLES ACROSS MANY OF THE TOP 10 RETAIL CATEGORIES

Top 10 Categories, Dollar Growth, MULOC

Compared with DeCA

Source: IRI Market Advantage™ 52 weeks ended December 27, 2015, and same period prior year

Top 10 Categories excludes BEER/ALE/ALCOHOLIC CIDER category

+1.8% +0.6% +3.2% +2.4% +6.0% (1.7%) +3.3% +3.8% +2.3% (5.6%)

ENERGY

DRINKS

BOTTLED

WATER

CIGARETTES SALTY

SNACKS

CHOCOLATE

CANDY

NATURAL

CHEESE

PET FOOD CARBONATED

BEVERAGES

FRESH

BREAD &

ROLLS

MILK

(1.8%) +1.2% +9.3% +1.3% +4.7% (2.7%) +3.8% +2.4% +2.4% (4.5%)

MULOC DeCA - ConUS

PRICE PER VOLUME % CHG VS. YA

1.9%

-3.7% -4.5% -4.8% -4.8%

-6.0% -6.2% -7.0%

-8.4%

-12.8%

7.2%

3.6%

1.5% 0.7%

2.7%

0.1%

-0.2%

1.3%

-1.1%

-7.1%

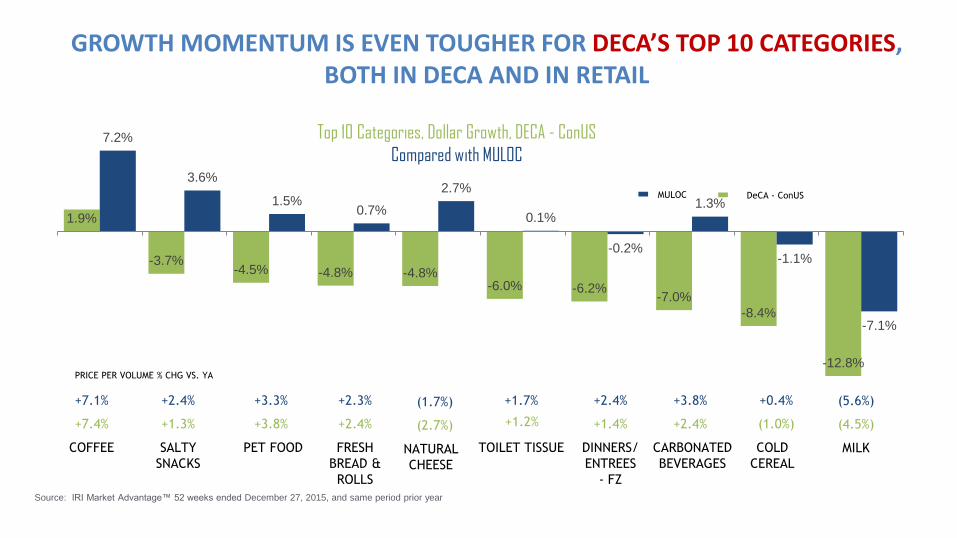

GROWTH MOMENTUM IS EVEN TOUGHER FOR DECA’S TOP 10 CATEGORIES, BOTH IN DECA AND IN RETAIL

Top 10 Categories, Dollar Growth, DECA - ConUS

Compared with MULOC

Source: IRI Market Advantage™ 52 weeks ended December 27, 2015, and same period prior year

+7.1% +2.4% +3.3% +2.3% (1.7%) +1.7% +2.4% +3.8% +0.4% (5.6%)

COFFEE SALTY

SNACKS

PET FOOD FRESH

BREAD &

ROLLS

NATURAL

CHEESE

TOILET TISSUE DINNERS/

ENTREES

- FZ

CARBONATED

BEVERAGES

COLD

CEREAL

MILK

+7.4% +1.3% +3.8% +2.4% (2.7%) +1.2% +1.4% +2.4% (1.0%) (4.5%)

MULOC DeCA - ConUS

PRICE PER VOLUME % CHG VS. YA

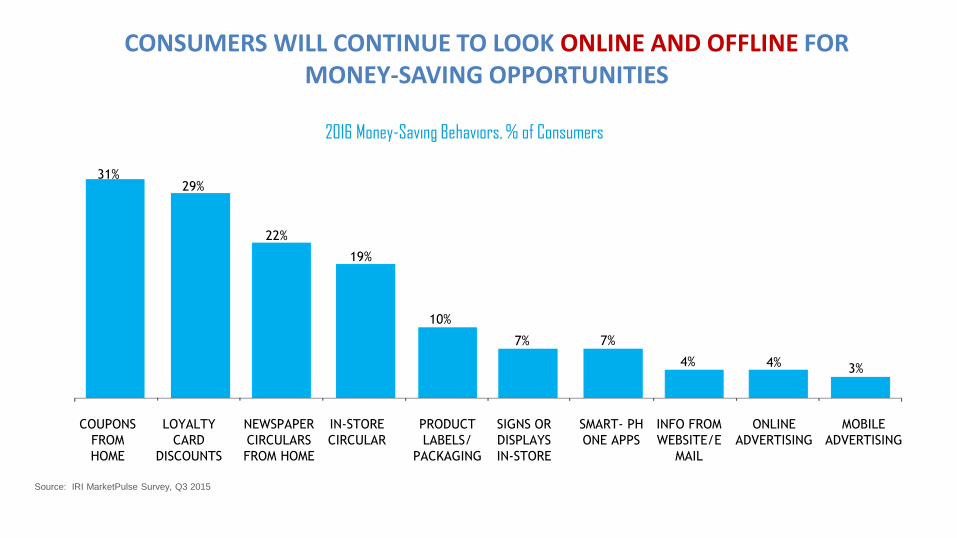

CONSUMERS WILL CONTINUE TO LOOK ONLINE AND OFFLINE FOR MONEY-SAVING OPPORTUNITIES

2016 Money-Saving Behaviors, % of Consumers

Source: IRI MarketPulse Survey, Q3 2015

31% 29%

22%

19%

10%

7% 7%

4% 4% 3%

COUPONS

FROM

HOME

LOYALTY

CARD

DISCOUNTS

NEWSPAPER

CIRCULARS

FROM HOME

IN-STORE

CIRCULAR

PRODUCT

LABELS/

PACKAGING

SIGNS OR

DISPLAYS

IN-STORE

SMART- PH

ONE APPS

INFO FROM

WEBSITE/E

ONLINE

ADVERTISING

MOBILE

ADVERTISING

COMPLICATING THE PATH-TO-PURCHASE

0% 10% 20% 30% 40% 50% 60%

Personal Care

Frozen Food

OTC Medications

Non-Alcoholic Beverages

Meat or Poultry

Snacks

Dairy

Beer, Wine, Spirits

% Past Week Category Buyers Who Did ANY Pre-Store Activity Online

Q18. Before buying category from S.2, which, if any, of the following things did you do? Where/how did you do them?

81% Used a laptop or desktop computer

40% Used a smart phone

24% Used a digital tablet

TO ADDRESS CONSUMER NEEDS, THE PERIMETER IS BECOMING:

The fulcrum point for maximum retail differentiation Base for deeper and more engaging customer experiences Focus for space expansion

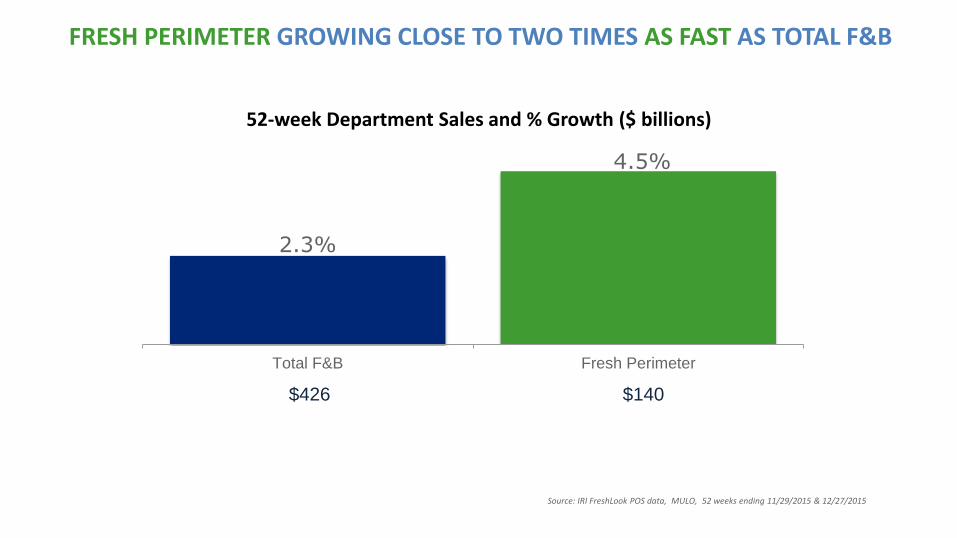

FRESH PERIMETER GROWING CLOSE TO TWO TIMES AS FAST AS TOTAL F&B

2.3%

4.5%

Total F&B Fresh Perimeter

$426 $140

52-week Department Sales and % Growth ($ billions)

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015 & 12/27/2015

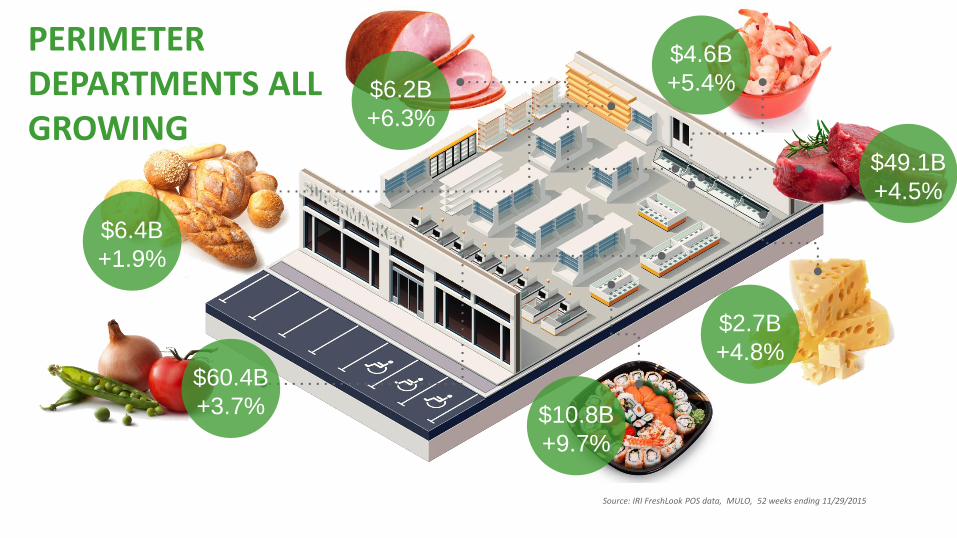

PERIMETER DEPARTMENTS ALL GROWING

$6.4B

+1.9%

$2.7B

+4.8%

$6.2B

+6.3%

$10.8B

+9.7%

$49.1B

+4.5%

$60.4B

+3.7%

$4.6B

+5.4%

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

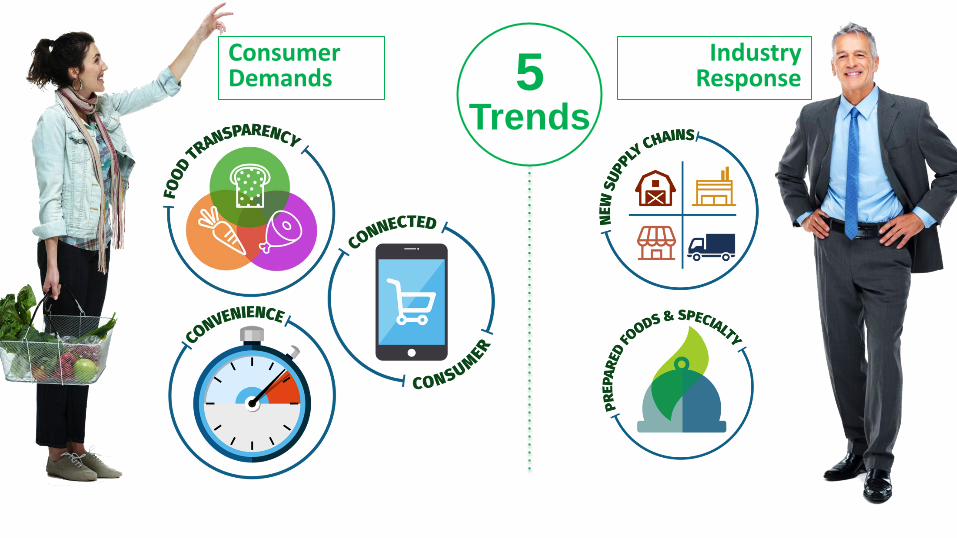

Consumer Demands

Industry Response 5

Trends

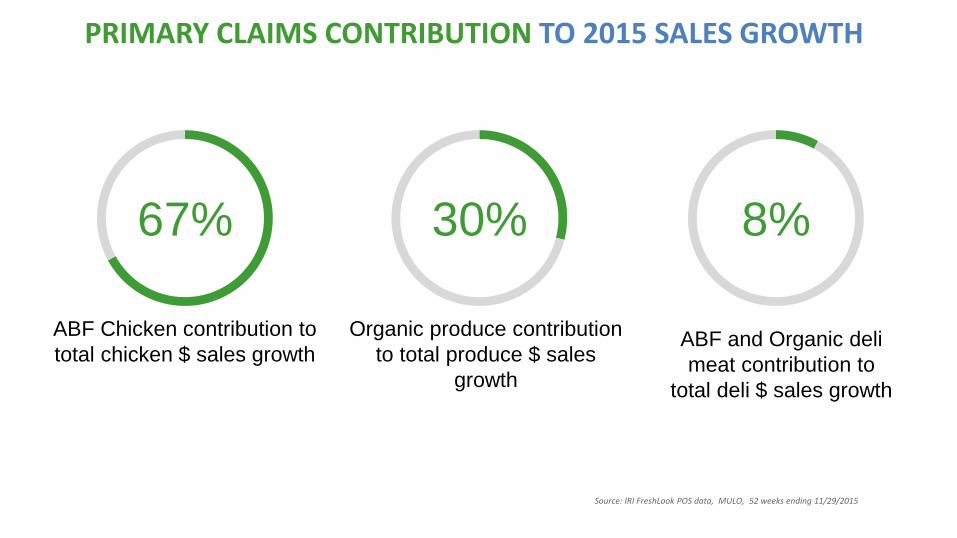

PRIMARY CLAIMS CONTRIBUTION TO 2015 SALES GROWTH

67% 30% 8%

ABF Chicken contribution to

total chicken $ sales growth

Organic produce contribution

to total produce $ sales

growth

ABF and Organic deli

meat contribution to

total deli $ sales growth

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

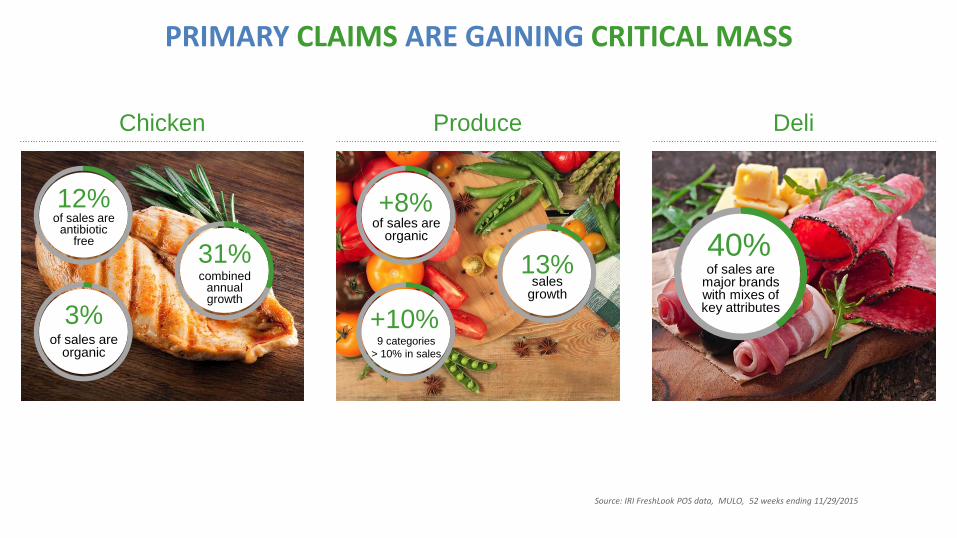

PRIMARY CLAIMS ARE GAINING CRITICAL MASS

Chicken Produce Deli

12% of sales are

antibiotic free

3% of sales are

organic

31% combined

annual growth

+8% of sales are

organic

+10% 9 categories

> 10% in sales

13% sales

growth

40% of sales are

major brands with mixes of key attributes

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

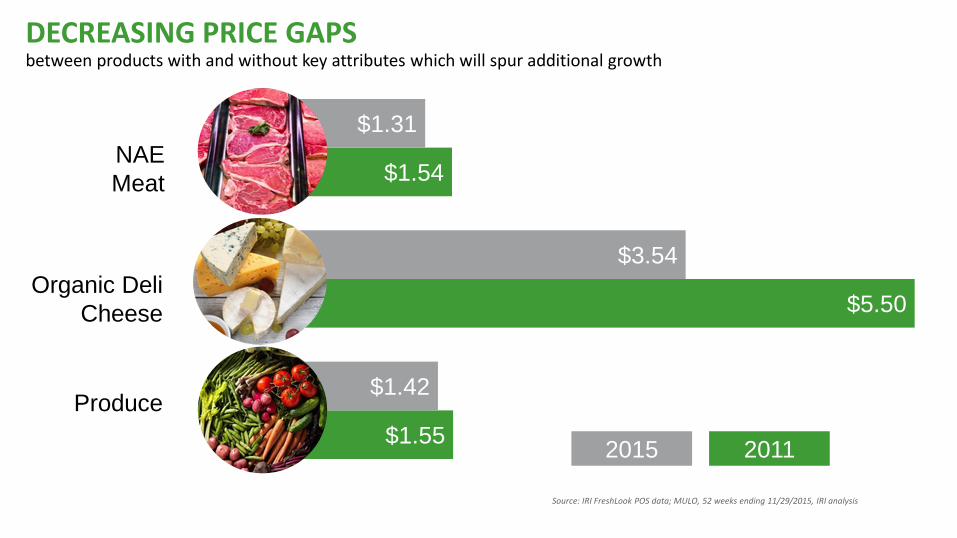

$1.55

$5.50

$1.54

$1.42

$3.54

$1.31

DECREASING PRICE GAPS between products with and without key attributes which will spur additional growth

2015 2011

NAE

Meat

Organic Deli

Cheese

Produce

Source: IRI FreshLook POS data; MULO, 52 weeks ending 11/29/2015, IRI analysis

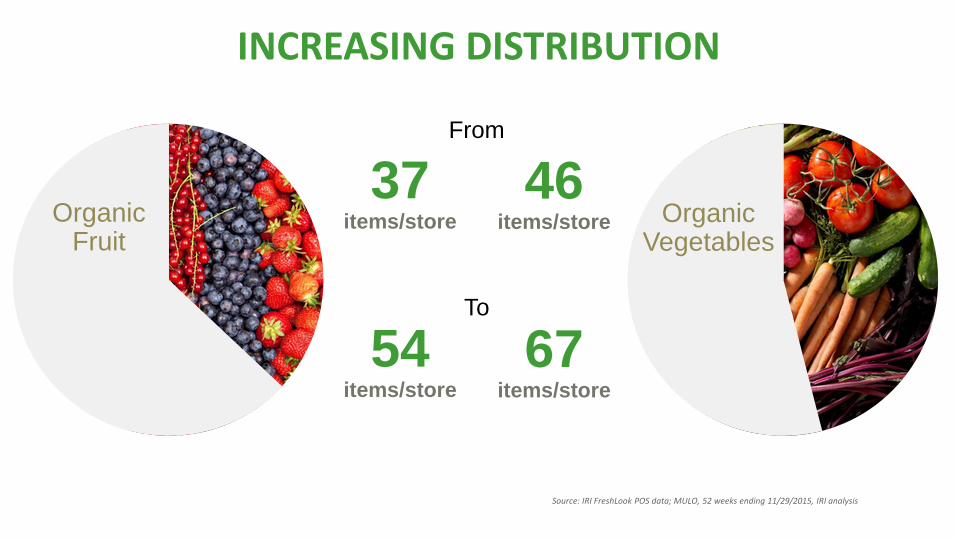

INCREASING DISTRIBUTION

37 items/store Organic

Fruit

54 items/store

46 items/store Organic

Vegetables

67 items/store

From

To

Source: IRI FreshLook POS data; MULO, 52 weeks ending 11/29/2015, IRI analysis

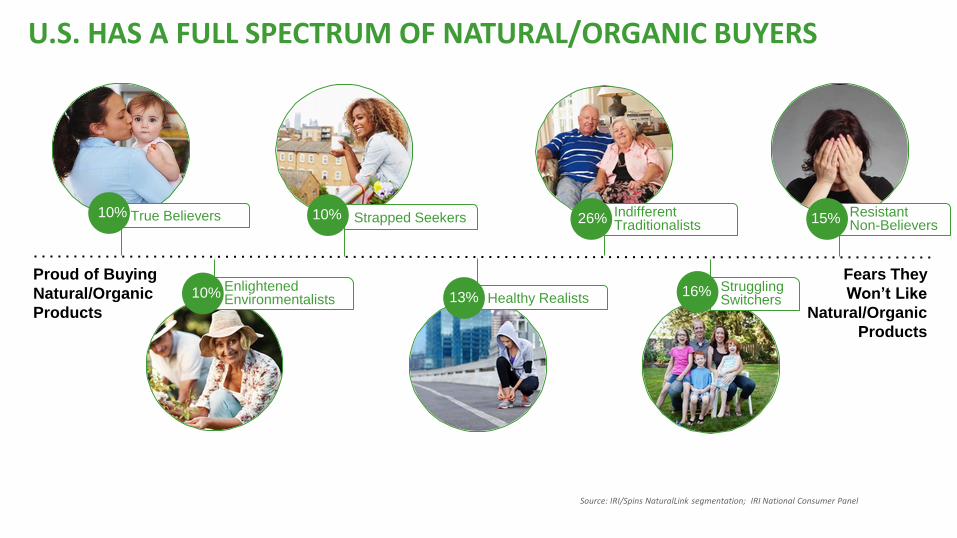

U.S. HAS A FULL SPECTRUM OF NATURAL/ORGANIC BUYERS

Fears They

Won’t Like

Natural/Organic

Products

Proud of Buying

Natural/Organic

Products

True Believers

Enlightened Environmentalists

Strapped Seekers Indifferent Traditionalists

Healthy Realists

Resistant Non-Believers

Struggling Switchers

10% 10% 26% 15%

16% 13% 10%

Source: IRI/Spins NaturalLink segmentation; IRI National Consumer Panel

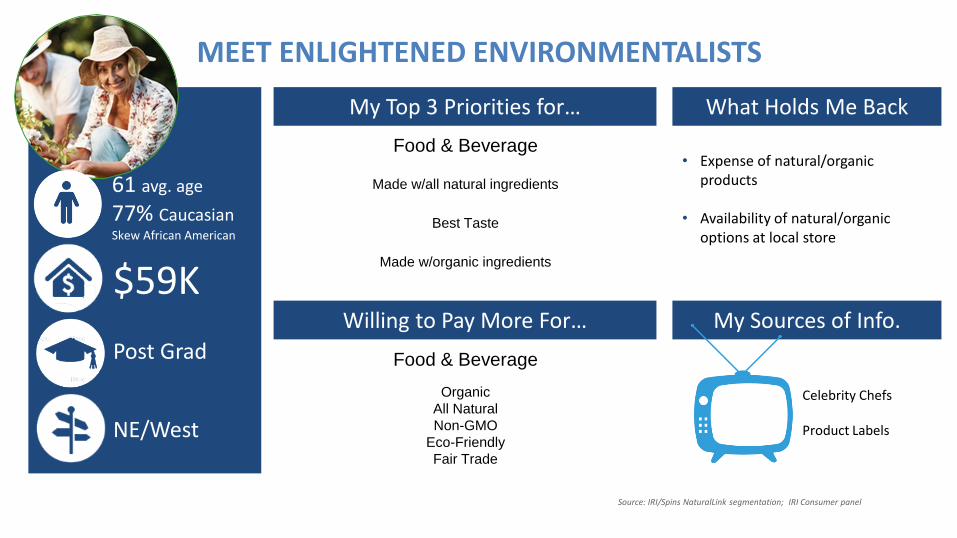

MEET ENLIGHTENED ENVIRONMENTALISTS

$59K

Post Grad

NE/West

61 avg. age

77% Caucasian Skew African American

My Top 3 Priorities for…

Willing to Pay More For…

What Holds Me Back

My Sources of Info.

Food & Beverage

Made w/all natural ingredients

Best Taste

Made w/organic ingredients

Food & Beverage

Organic

All Natural

Non-GMO

Eco-Friendly

Fair Trade

• Expense of natural/organic products

• Availability of natural/organic options at local store

Celebrity Chefs Product Labels

Source: IRI/Spins NaturalLink segmentation; IRI Consumer panel

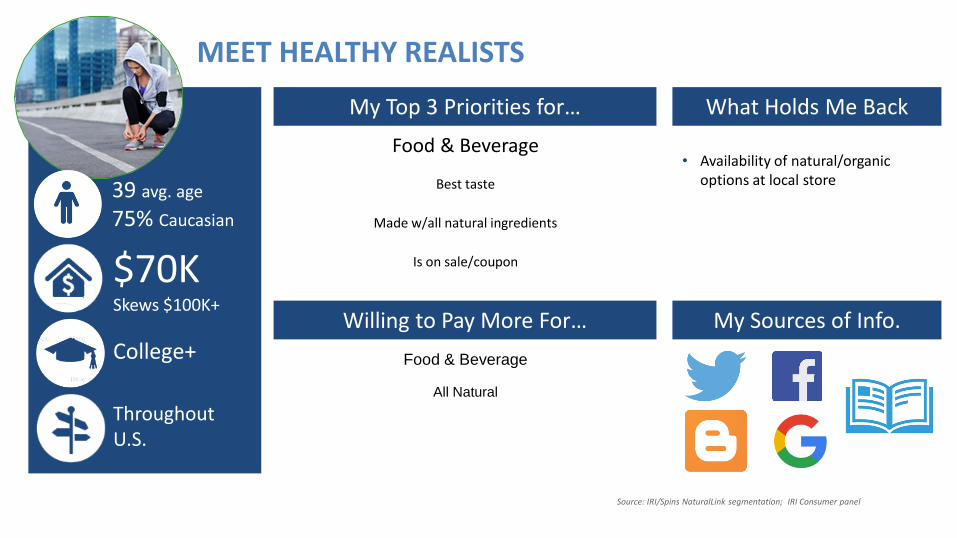

MEET HEALTHY REALISTS

$70K Skews $100K+

College+

Throughout U.S.

39 avg. age

75% Caucasian

My Top 3 Priorities for…

Willing to Pay More For…

What Holds Me Back

My Sources of Info.

Food & Beverage

Best taste

Made w/all natural ingredients

Is on sale/coupon

Food & Beverage

All Natural

• Availability of natural/organic options at local store

Source: IRI/Spins NaturalLink segmentation; IRI Consumer panel

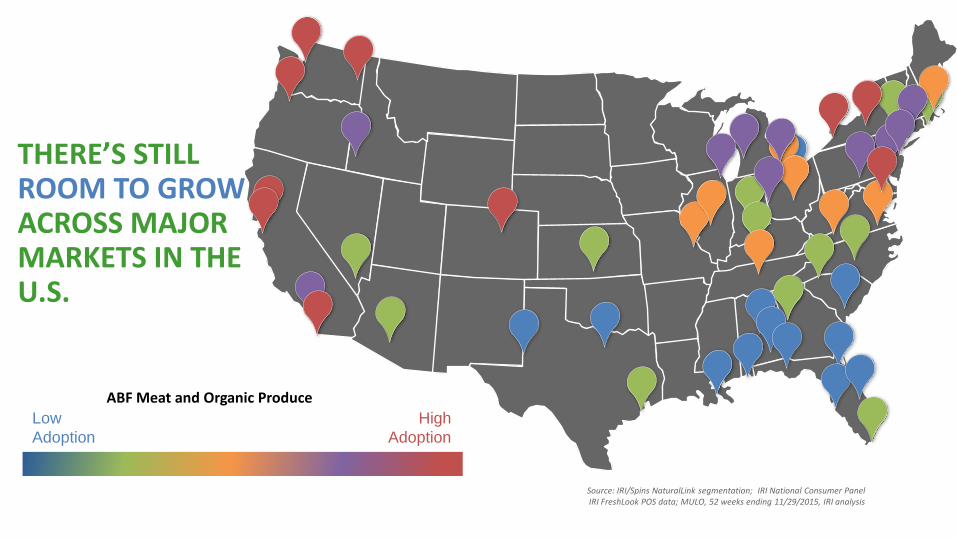

THERE’S STILL ROOM TO GROW ACROSS MAJOR MARKETS IN THE U.S.

Low

Adoption

High

Adoption

Source: IRI/Spins NaturalLink segmentation; IRI National Consumer Panel IRI FreshLook POS data; MULO, 52 weeks ending 11/29/2015, IRI analysis

ABF Meat and Organic Produce

FOOD TRANSPARENCY 3-5 YEAR OUTLOOK:

• Continued fast growth in Organic

Produce (at least 50% growth over the

next 5 years)

• Accelerating growth in Meat claims (NAE

chicken, gestation crate-free pork)

• Continued focus on health and wellness

from consumers

• Increased consumer engagement and

demand for traceability

• Evolving sophistication and growth in

local-based supply programs

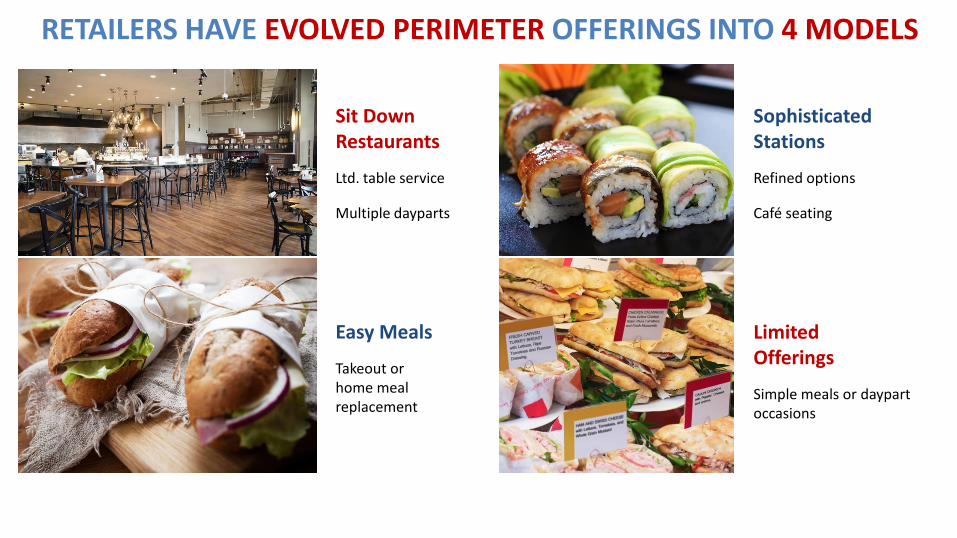

RETAILERS HAVE EVOLVED PERIMETER OFFERINGS INTO 4 MODELS

Sit Down Restaurants

Ltd. table service

Multiple dayparts

Sophisticated Stations

Refined options

Café seating

Easy Meals

Takeout or home meal replacement

Limited Offerings

Simple meals or daypart occasions

LEADERS ARE USING FRESH PREPARED TO:

Compete with restaurants and

specialty channels

Create stronger emotional linkages

with customers

Create dominant franchises and

separate from competitors

Gain bargaining power with

suppliers

Photo Courtesy: Ravings by Rae

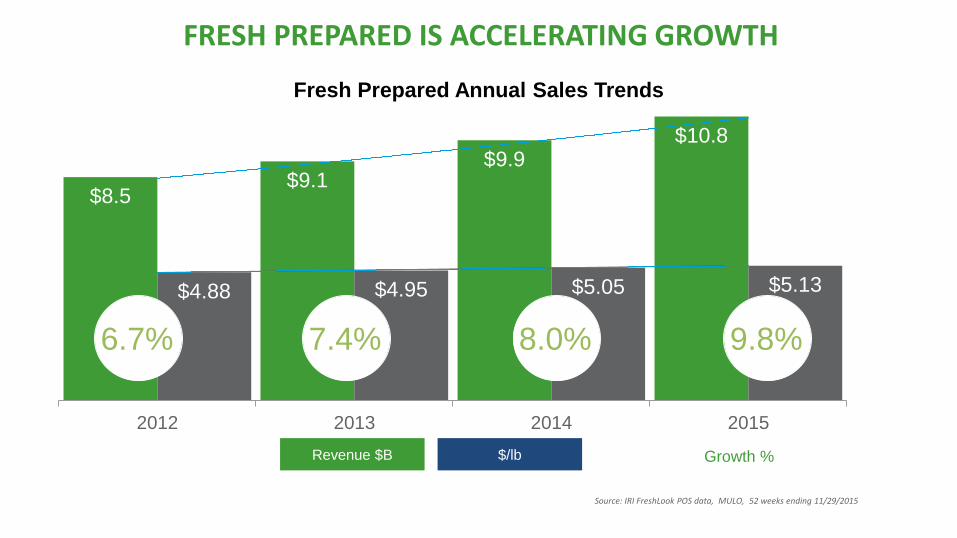

FRESH PREPARED IS ACCELERATING GROWTH

$8.5 $9.1

$9.9 $10.8

$4.88 $4.95 $5.05 $5.13

2012 2013 2014 2015

Revenue $B $/lb Growth %

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

6.7% 7.4% 8.0% 9.8%

Fresh Prepared Annual Sales Trends

THE GREATEST UNTOLD STORY IN FOOD RETAIL

Larger Than

Growing Faster Than

US Supermarkets

Foodservice sales are:

vs.

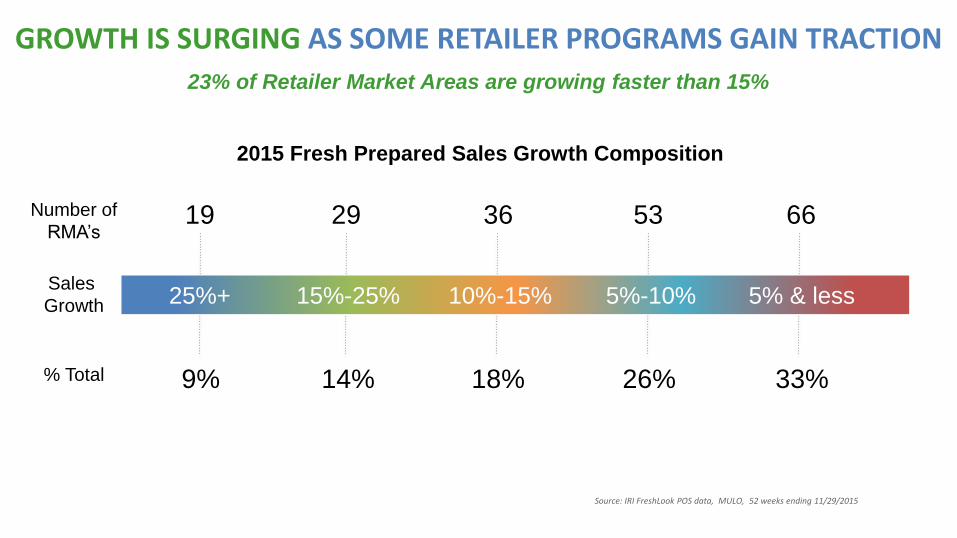

19 29 36 53 66

9% 14% 18% 26% 33%

23% of Retailer Market Areas are growing faster than 15%

2015 Fresh Prepared Sales Growth Composition

25%+ 15%-25% 10%-15% 5%-10% 5% & less

GROWTH IS SURGING AS SOME RETAILER PROGRAMS GAIN TRACTION

Sales

Growth

Number of

RMA’s

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

% Total

A GOOD FRESH PREPARED DEPARTMENT CAN BRING IN

NEW, LOYAL SHOPPERS

31% Of Fresh Prepared buyers

have a different primary chain

for Fresh Prepared than Total

Grocery

76% Shoppers spend 76% of their

Fresh Prepared dollars at

their primary Fresh Prepared

chain

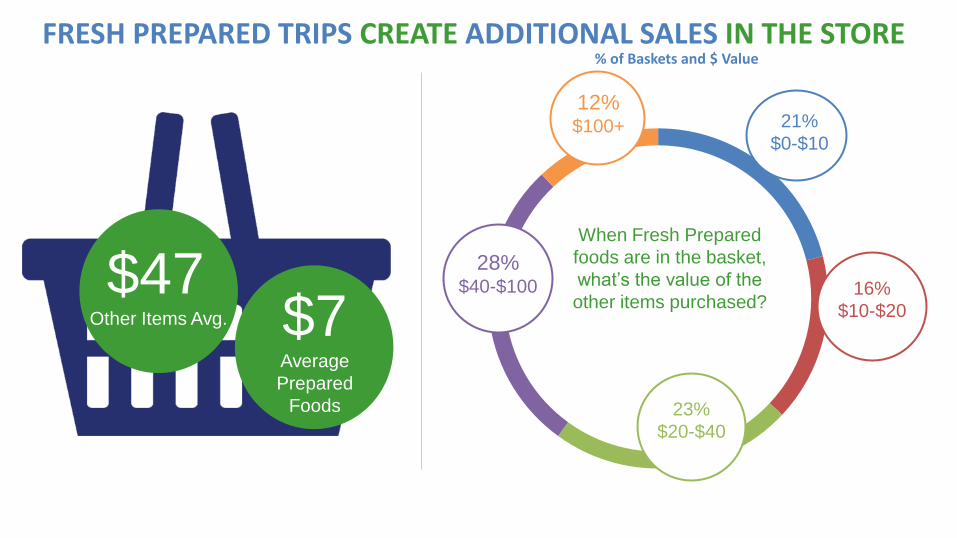

FRESH PREPARED TRIPS CREATE ADDITIONAL SALES IN THE STORE

$47 Other Items Avg. $7

Average

Prepared

Foods

When Fresh Prepared

foods are in the basket,

what’s the value of the

other items purchased?

21%

$0-$10

16%

$10-$20

23%

$20-$40

28% $40-$100

12% $100+

% of Baskets and $ Value

FRESH PREPARED 3-5 YEAR OUTLOOK:

Continued 2x perimeter growth

Accelerated separation of high

performers

Continued refinement in concept

sophistication

Expansion of Fresh Prepared in

small format stores

ON-THE-GO AND BUSIER LIFESTYLES ARE LEAVING LESS TIME FOR THE YOUNGER GENERATION TO STICK TO OLD SCHOOL FORMAL MEALS

Millennials look for

GREATER BREAKFAST OPTIONS such as later hours, breakfasts all day, ethnic ingredients, gourmet

options and and healthier ingredients

Millennials eat out most at lunch

Four smaller meals a day at non-

traditional times

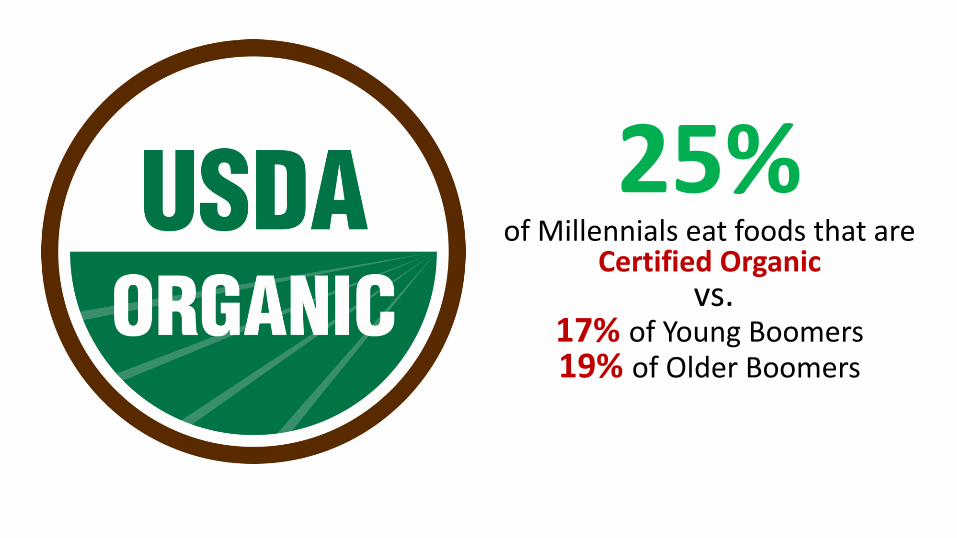

25% of Millennials eat foods that are

Certified Organic vs.

17% of Young Boomers 19% of Older Boomers

Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

more dollars per trip vs. Younger & Older Boomers $10.67 vs. $9.94 vs. $8.91

Millennials

less deal reliant vs. Younger & Older Boomers 34.0% vs. 35.9% vs. 35.3%

NOT ONLY ARE THEIR EATING HABITS DIFFERENT, THE WAY THEY SHOP AT THE SUPERMARKETS IS ALSO NOTE WORTHY

Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

NOT ONLY ARE THEIR EATING HABITS DIFFERENT, THE WAY

THEY SHOP AT THE SUPERMARKETS IS ALSO NOTE

WORTHY

larger basket size $65.27 vs. $62.26

more dollars per trip $10.03 vs. $9.54

less deal reliant 33.7% vs. 35.5%

Hispanics

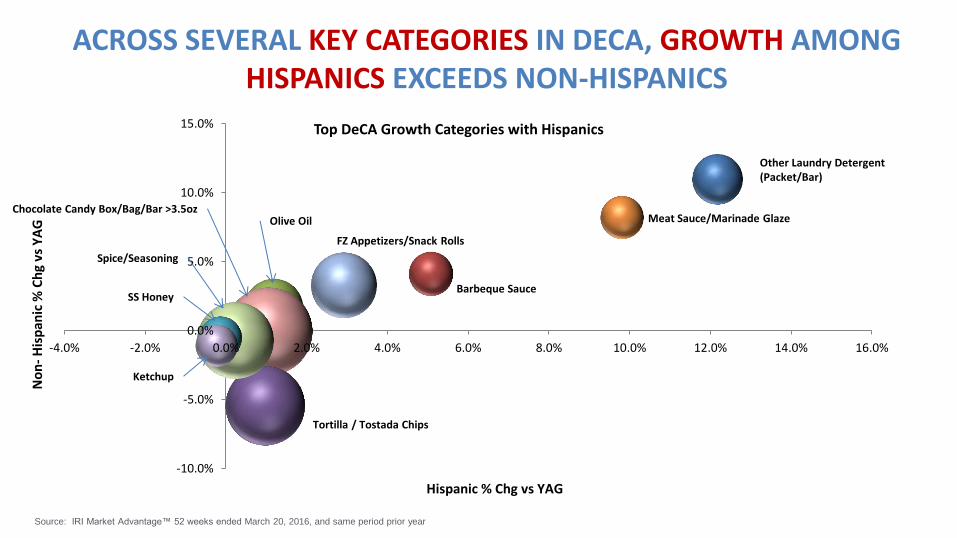

ACROSS SEVERAL KEY CATEGORIES IN DECA, GROWTH AMONG HISPANICS EXCEEDS NON-HISPANICS

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

-4.0% -2.0% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0%

Top DeCA Growth Categories with Hispanics

Hispanic % Chg vs YAG

No

n-

His

pan

ic %

Ch

g vs

YA

G

Source: IRI Market Advantage™ 52 weeks ended March 20, 2016, and same period prior year

FZ Appetizers/Snack Rolls

Meat Sauce/Marinade Glaze

Barbeque Sauce

Other Laundry Detergent (Packet/Bar)

Tortilla / Tostada Chips

Ketchup

SS Honey

Spice/Seasoning

Chocolate Candy Box/Bag/Bar >3.5oz Olive Oil

Trending

QUEST FOR WELLNESS IS BOOSTING CLAIMS THAT ALIGN TO HIS OR HER NEEDS

Calorie Per

Serving

No Trans

Fat

Gluten Free

Kosher

USDA Organic

All Natural

No Hormones

No Preservatives

Non-GMO

Verified

Calcium

No Cholesterol

Individual Desserts

+18% over previous year

EMERGING TRENDS

Personalization

Entertainment

Customization

(breads/cakes, etc)

1 Nutrition and Wellness

Consumers want cleaner eating and smarter food & beverage choices and are drawn to the perimeter

• Highlight how your products fit into a healthy lifestyle • Use store-level insight into current and potential

shoppers to identify customize by store • Drive major programs using strategically selected

claims and attributes

HOW TO WIN GOING FORWARD

2 Convenient and Simple

• Consumers are food-savvy but time-starved

• Strive for the ‘easy button’ of meal solutions – convenient and simple

• Let shoppers quickly assemble meals and clearly demonstrate the time savings

• Understand which stores may have more opportunities for convenience trips vs. stock-up

HOW TO WIN GOING FORWARD

3 Tailor Made Innovation & Messaging

• Leverage personalization, entertainment and customization to target different consumer segments

• Foster and broaden the relationship with Millennial consumers and their very diverse flavor profiles

• Engage shoppers by keeping things interesting and new

• Understand price gaps to ROM, especially with Private Label

HOW TO WIN GOING FORWARD

4 Identify Ways To Reach Each Generation

• Inform Millennials about the exciting flavors and different food combination ideas with baking items

• Significant cross-selling benefits by utilizing in-store demonstrations and cooking classes in-store

• Merchandise to the type of households to which each store caters

• Know where DeCA’s shoppers buy products when not shopping at DeCA, and understand competitive assortment

HOW TO WIN GOING FORWARD