Housing Inequality An Intergenerational Perspective · Housing Inequality An Intergenerational...

43

Housing Inequality An Intergenerational Perspective February 1, 2018 Kyung-Hwan Kim Visiting Fellow, Perry World House University of Pennsylvania Professor of Economics, Sogang University

Transcript of Housing Inequality An Intergenerational Perspective · Housing Inequality An Intergenerational...

Housing InequalityAn Intergenerational Perspective

February 1, 2018

Kyung-Hwan KimVisiting Fellow, Perry World House

University of PennsylvaniaProfessor of Economics, Sogang University

Outline

What is the issue?

How relevant is it?

What are the problems?

What are the root causes?

What can be done?

Contexts and prospects

Generation on generation living standards improvement may no longer

be possible, most markedly so in housing.

2007 Global Financial Crisis, housing market volatility

Many young people are priced out from the housing market.

1% vs 99% (top 1% has 36% of wealth in U.S. and 14% in UK)

Stagnant real wages at the lower end

Diminishing social mobility

Industry 4.0 and new technologies

Population ageing, decline in household formation and fertility

Slowing down of economic growth

Fiscal constraints

3

Some rhetoric of intergenerational conflict

The frustrated younger generation

UK: IPOD (insecure, pressured, over-taxed and debt-ridden) generation,

generation rent (the Telegraph, Sep 18, 2006)

Japan: Satori generation

Korea: ‘Sampo’ generation (Give up courtship, marriage, and childbirth)

U.S.: Boomerang generation

Resentment against the older generation

UK: Pinch: How the Baby Boomers Took Their Children's Future - And Why

They Should Give It Back (2011, Willetts)

Korea: The Intergenerational War

Australia: SKI (spending kid’s inheritance)

4

Housing inequality

Income inequality vs wealth inequality

Income inequality relates to labor market, human capital, technology (cost of living adjustment needed)

Wealth inequality relates to cumulated income, capital gains from assets

Housing has two dimensions, and so does housing inequality.

Shelter: Quantity, quality and affordable housing service

Asset: Wealth accumulation to homeowners due to appreciation

Why should we mind the housing gap?

Availability of affordable housing is a prerequisite for inclusive and diverse cities.

Housing comprises the largest share in the asset portfolio of a typical household in many countries.

Homeownership rate among the younger generation is falling.

Housing wealth can be passed onto the next generation.

Intergenerational transfers affect homeownership.

Homeownership affects education and therefore future income and living standards. (Boehm and Schlottmann 1999)

5

How relevant is it as a global issue?

North-South divide?

Housing wealth inequality is more relevant in major developed economies (in UK, Australia, Korea), and some rapidly urbanizingemerging economies (China)

Shelter inequality may be more relevant in many developing countries (affordability, access to credit and cost of finance)

The New Urban Agenda (NUA)

99. We will support the implementation of urban planning strategies, as appropriate, that facilitate a social mix through the provision of affordable housing options with access to quality basic services and public spaces for all, enhancing safety and security and favouring social and intergenerational interaction and the appreciation of diversity.

Perry World House, U Penn

Global shifts: Urbanization, migration and demography

6

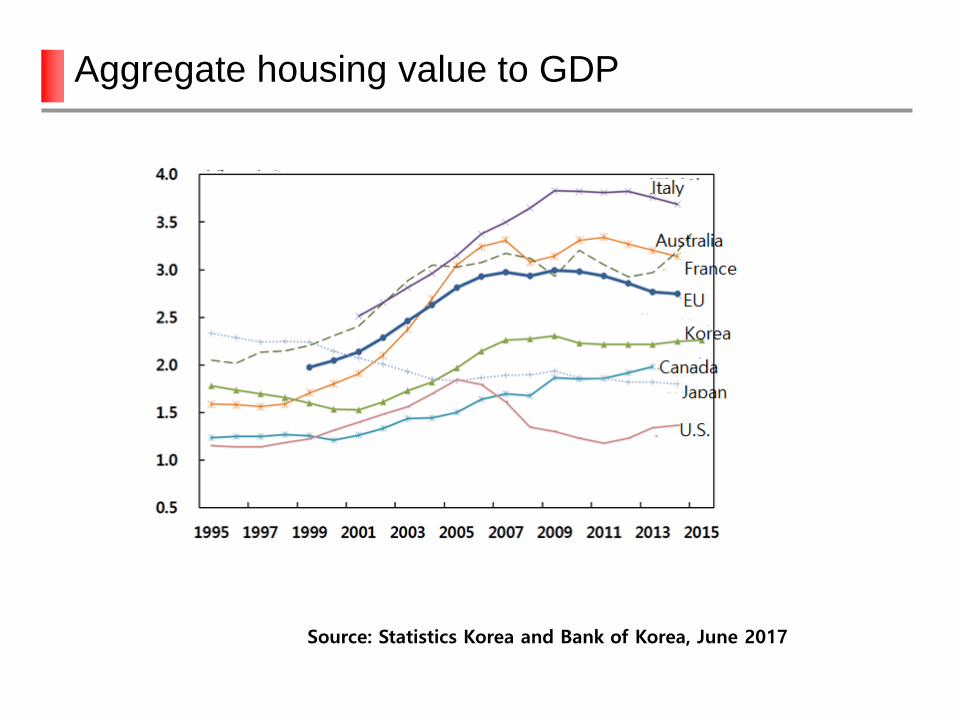

Aggregate housing value to GDP

Source: Statistics Korea and Bank of Korea, June 2017

The nature of housing inequality

Increases in real housing prices in major economies

Housing boom since late 1990s till mid 2000s

Driving forces: record low interest rate, liquidity, supply constraints

National average vs differences across cities

Windfall gains accruing to home owners

Passive gain due to housing price appreciation to the benefit of baby boomers

Members of younger generation could not participate in sharing the gain since their home ownership rate fell

Concentration of housing wealth and widening gap

Spatial

Across income groups

Across generations

8

Real house price appreciation 1996-2016

9

Source: The Economist

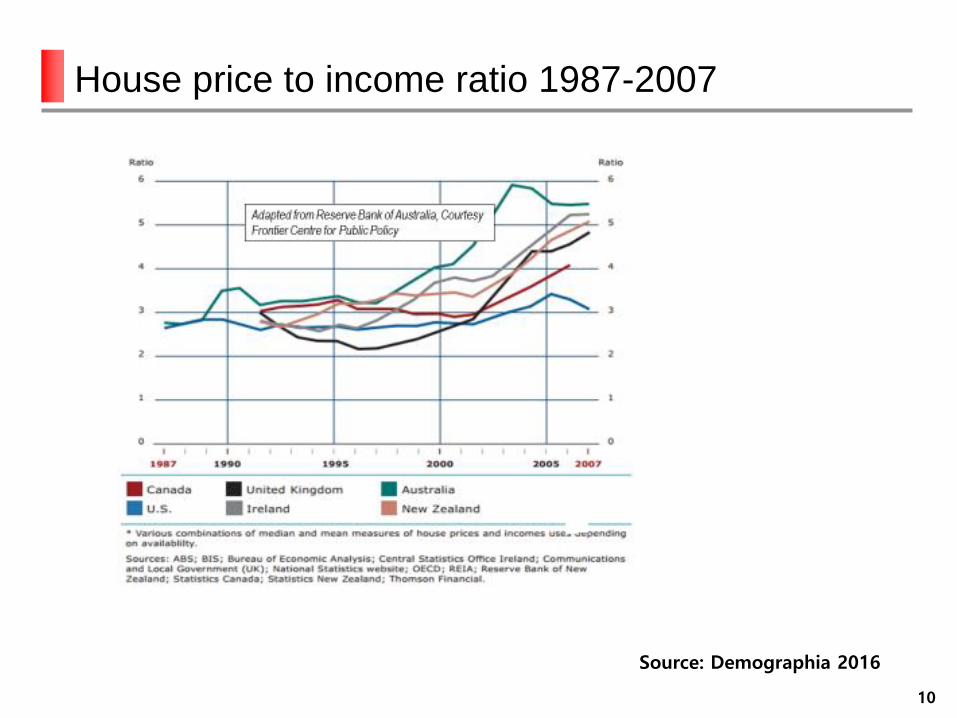

House price to income ratio 1987-2007

10

Source: Demographia 2016

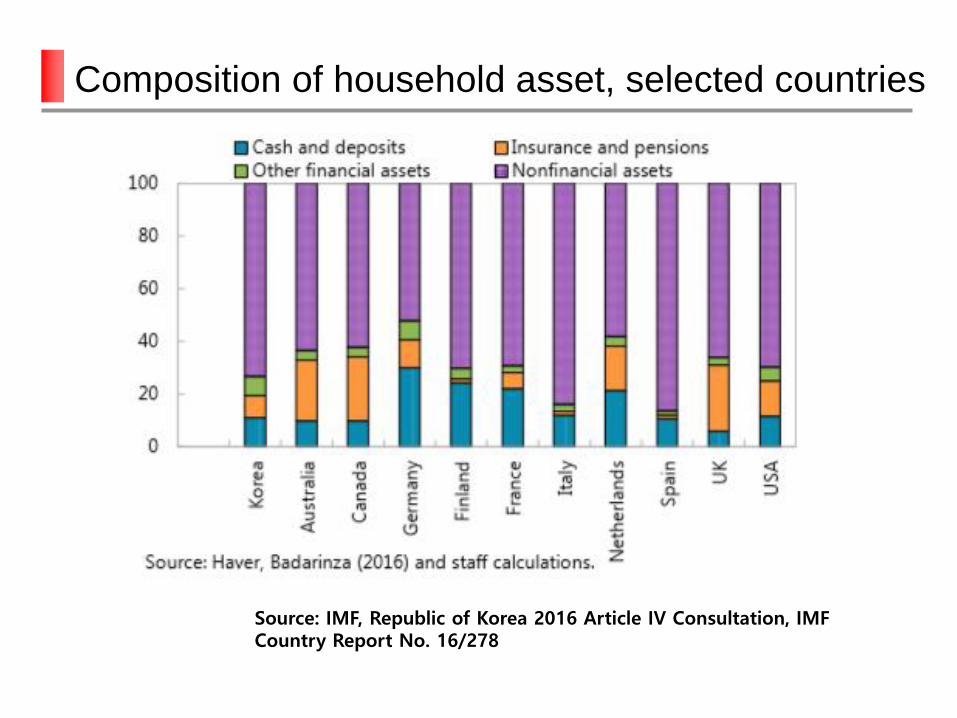

Source: IMF, Republic of Korea 2016 Article IV Consultation, IMF Country Report No. 16/278

Composition of household asset, selected countries

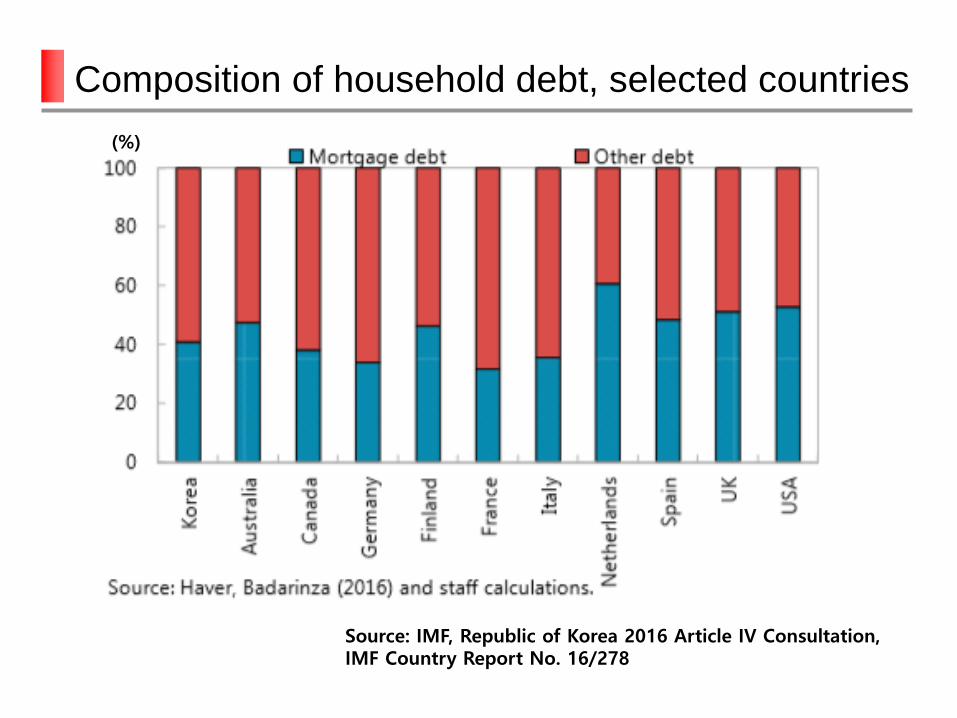

Composition of household debt, selected countries

Source: IMF, Republic of Korea 2016 Article IV Consultation, IMF Country Report No. 16/278

(%)

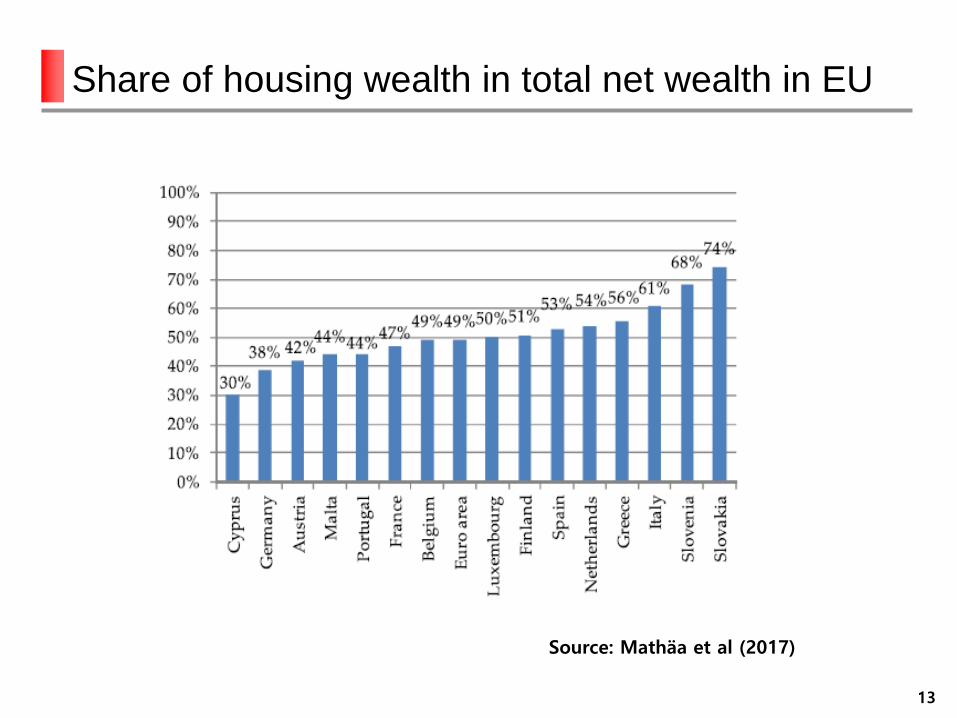

Share of housing wealth in total net wealth in EU

13

Source: Mathäa et al (2017)

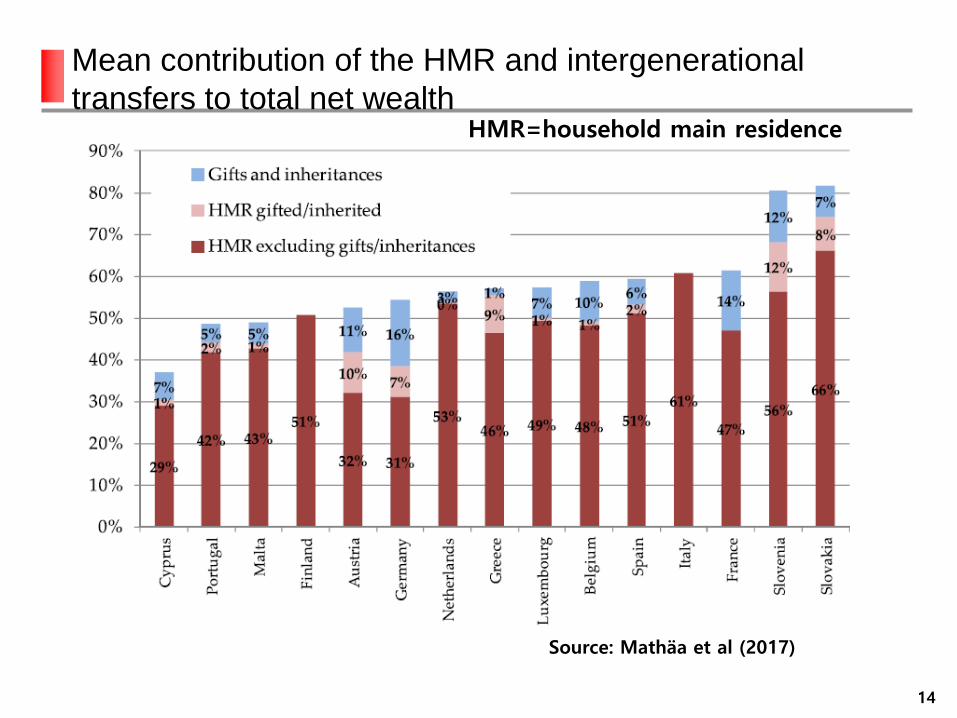

Mean contribution of the HMR and intergenerational

transfers to total net wealth

14

Source: Mathäa et al (2017)

HMR=household main residence

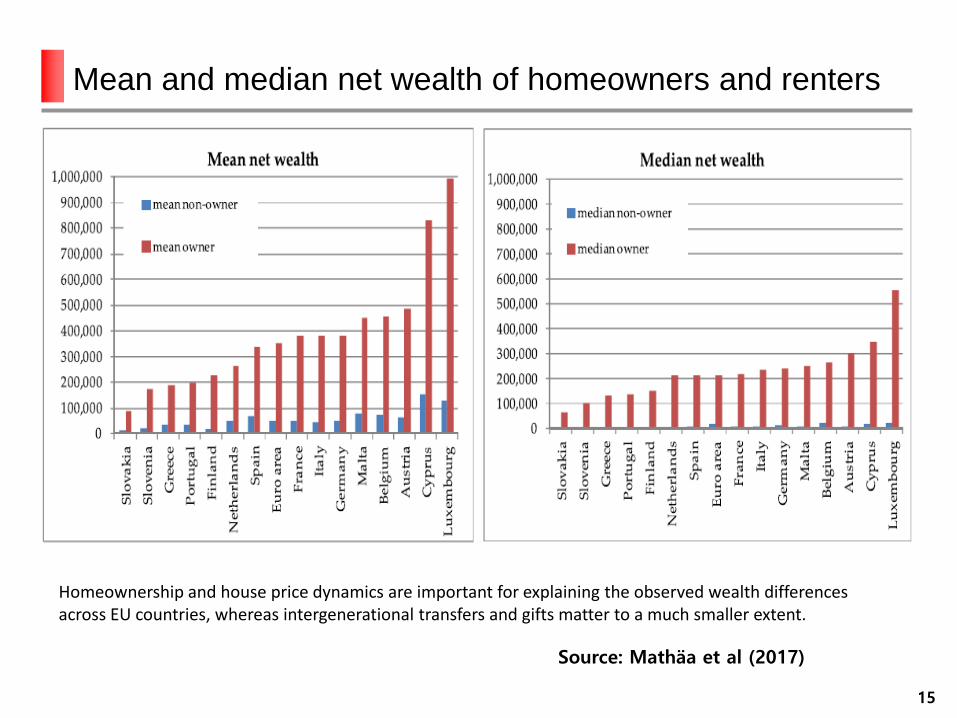

Mean and median net wealth of homeowners and renters

15

Source: Mathäa et al (2017)

Homeownership and house price dynamics are important for explaining the observed wealth differences across EU countries, whereas intergenerational transfers and gifts matter to a much smaller extent.

Housing and inequality: The Piketty thesis

Piketty (2014)

Capital income/GDP has been rising and worsening income distribution.

Rognlie (2015)

The net rate of return on capital other than housing has been stable since 1970s in seven major economies

Rate of return on housing has been rising due to the appreciation of housing price

Capital gains from housing accrue mainly to home owners

Piketty’s book should be entitled the theory of housing capital of the 21st

century.

La Cava (2016)

Capital gains from housing accrue to homeowners.

Supply elasticity matters.

Real interest rate matters.

16

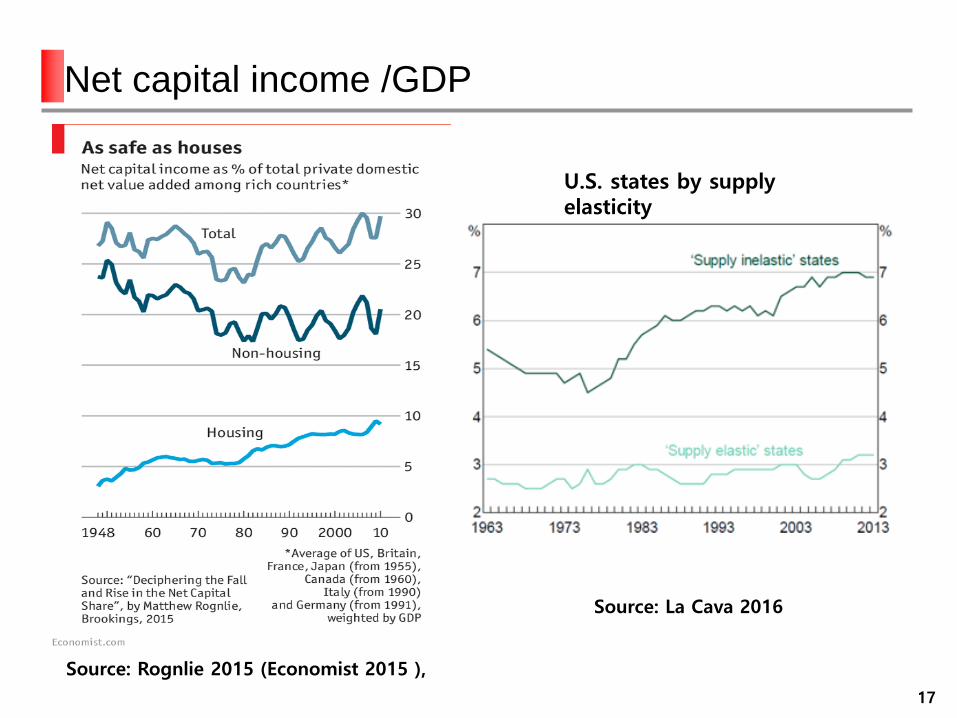

Net capital income /GDP

17

Source: Rognlie 2015 (Economist 2015 ),

U.S. states by supplyelasticity

Source: La Cava 2016

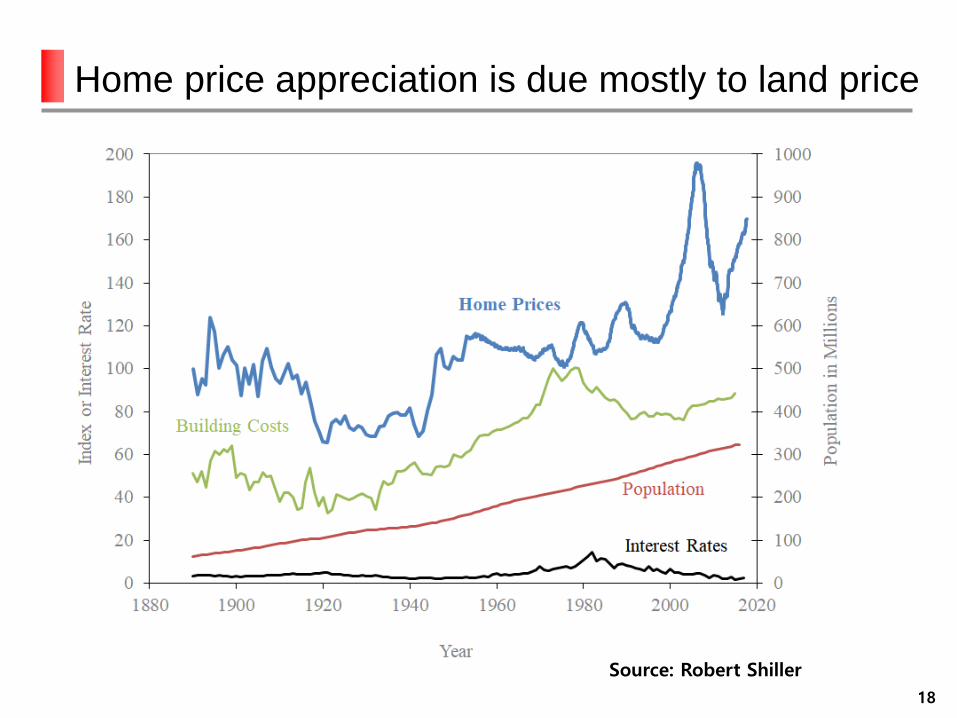

Home price appreciation is due mostly to land price

18

Source: Robert Shiller

Homeownership rates and housing wealth across

generation

Homeownership rate

Homeownership rate is higher among older cohorts

Homeownership rate of younger generation is falling over time

Housing wealth

Concentrated among the older households

Increases in housing wealth are due to capital gains from house

price appreciation

19

20

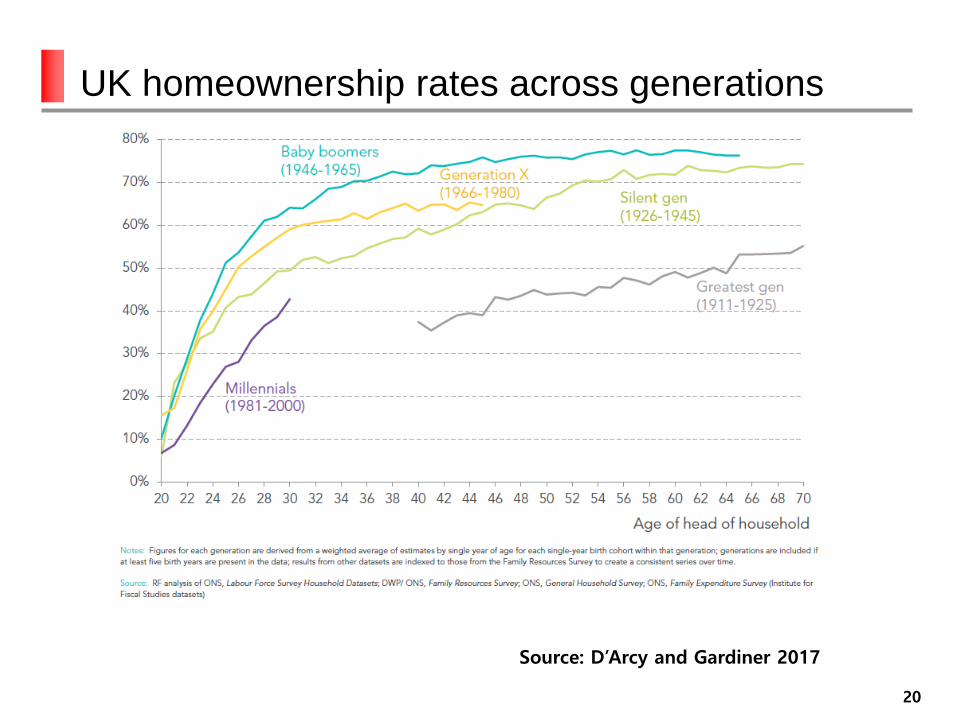

Source: D’Arcy and Gardiner 2017

UK homeownership rates across generations

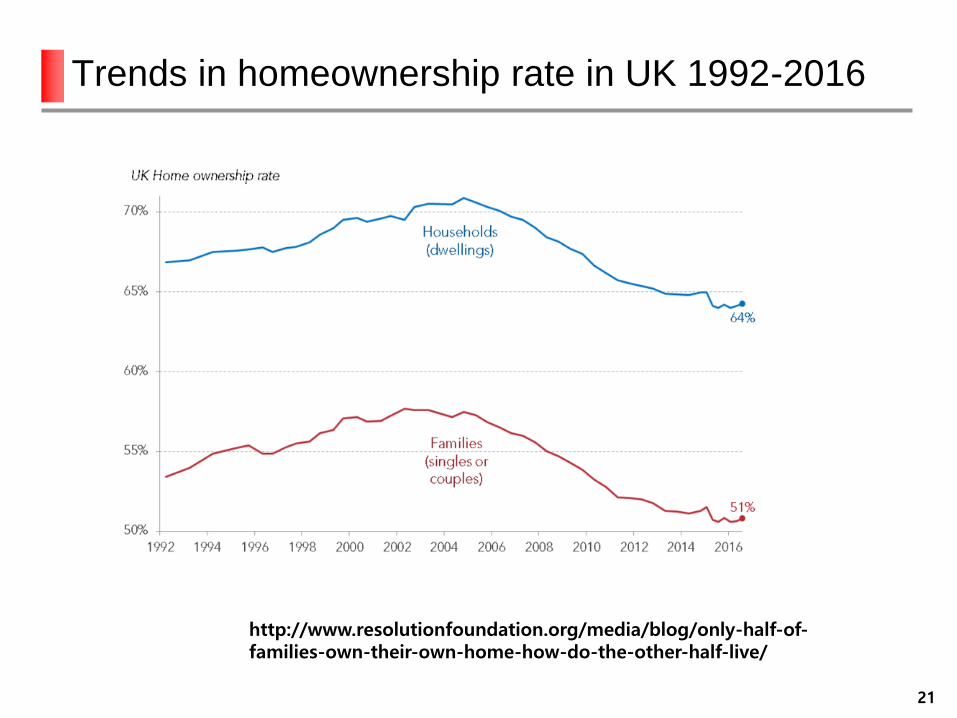

Trends in homeownership rate in UK 1992-2016

21

http://www.resolutionfoundation.org/media/blog/only-half-of-families-own-their-own-home-how-do-the-other-half-live/

22

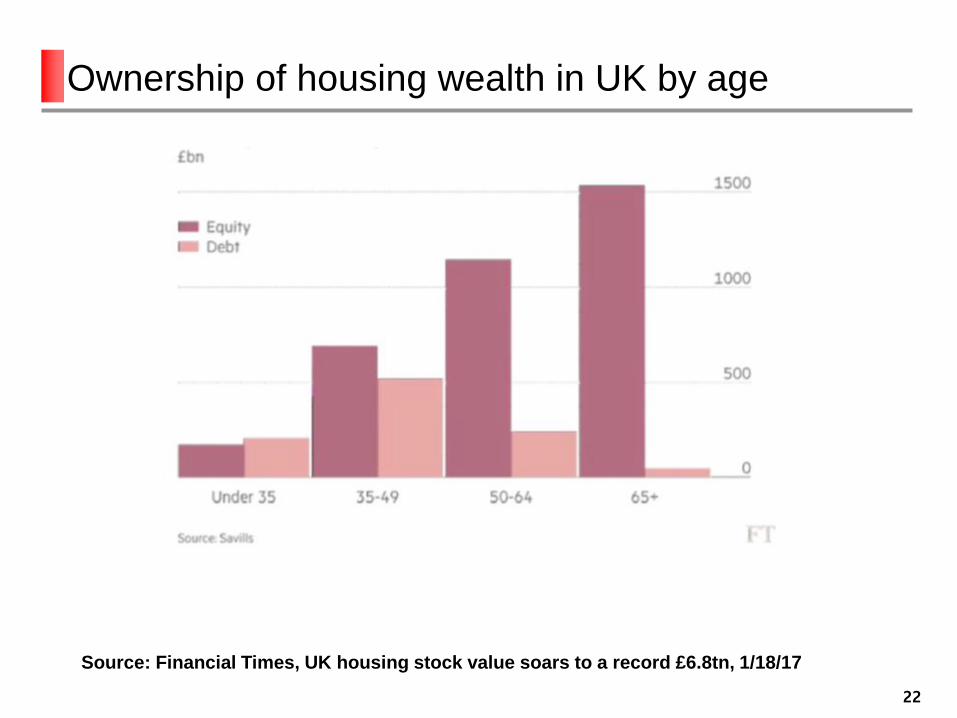

Source: Financial Times, UK housing stock value soars to a record £6.8tn, 1/18/17

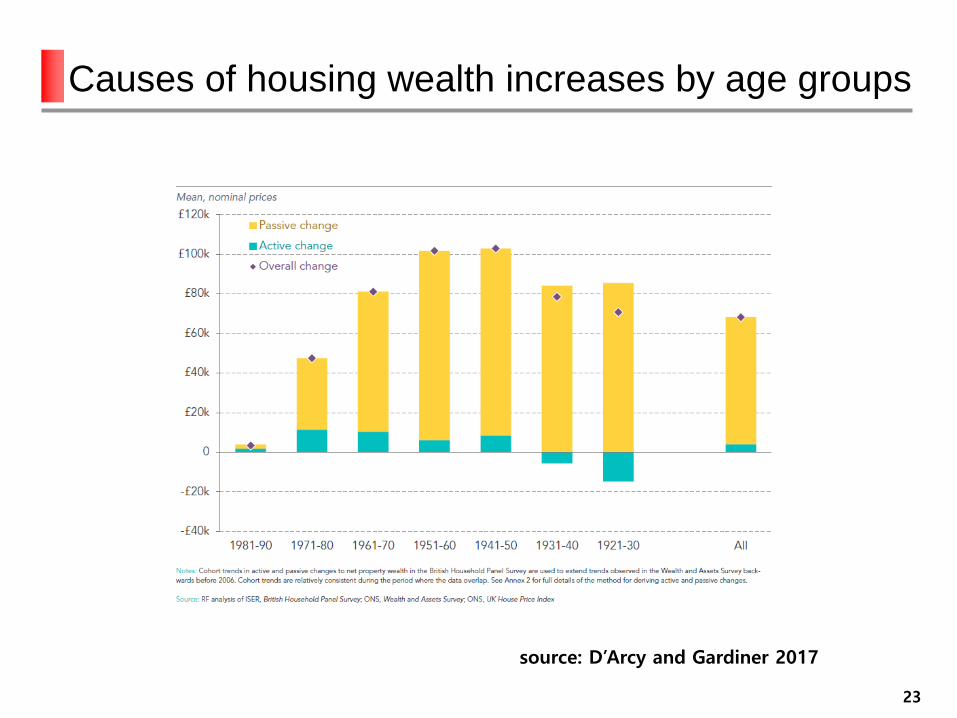

Ownership of housing wealth in UK by age

23

source: D’Arcy and Gardiner 2017

Causes of housing wealth increases by age groups

24

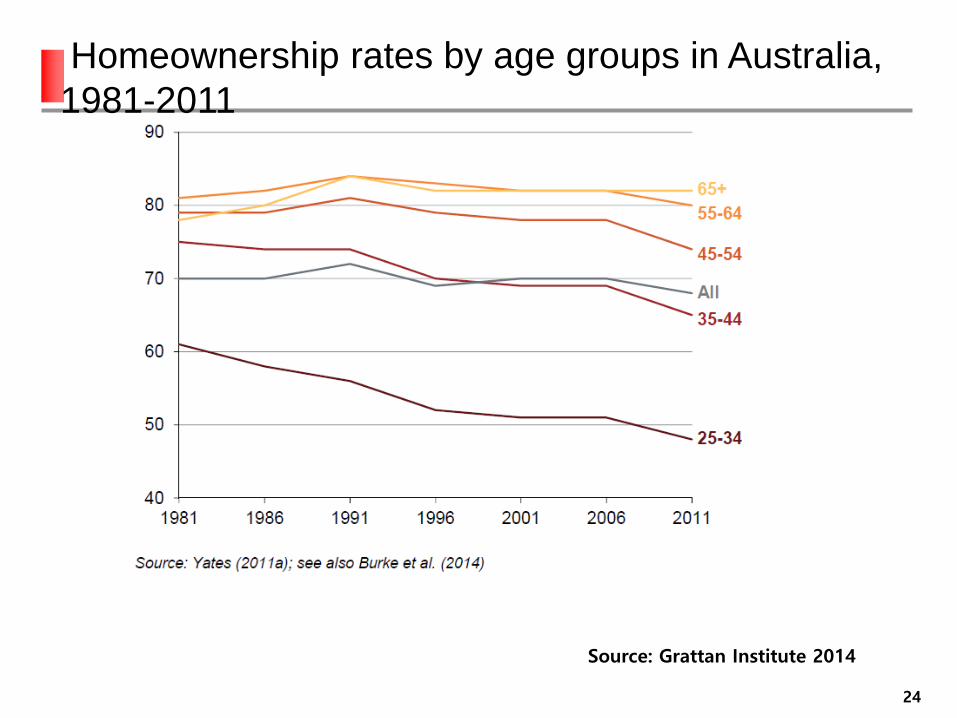

Homeownership rates by age groups in Australia,

1981-2011

Source: Grattan Institute 2014

25

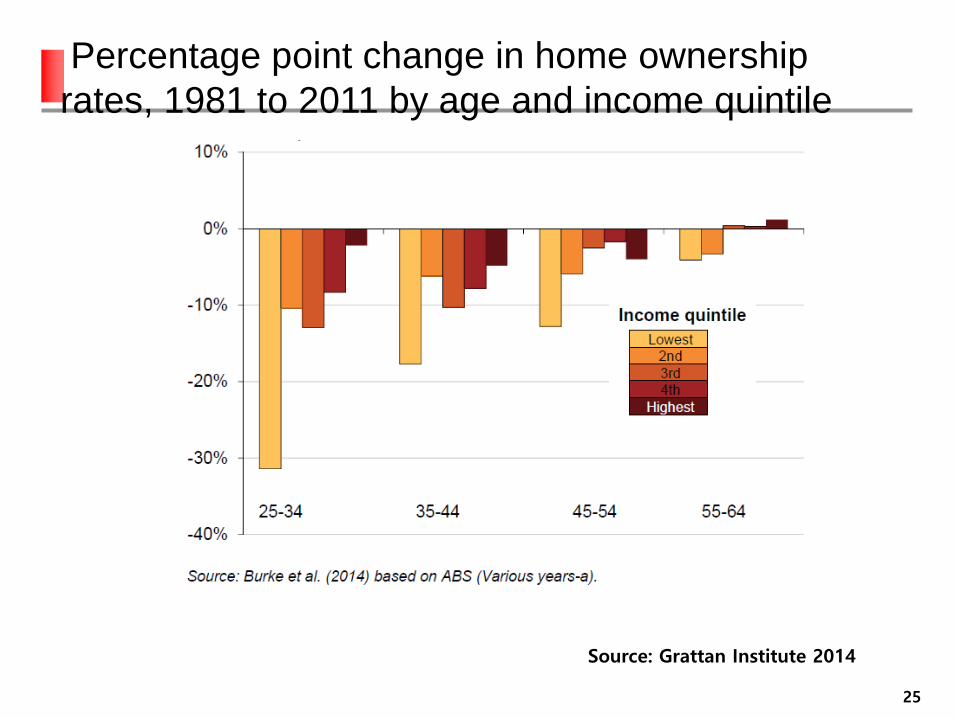

Percentage point change in home ownership

rates, 1981 to 2011 by age and income quintile

Source: Grattan Institute 2014

26

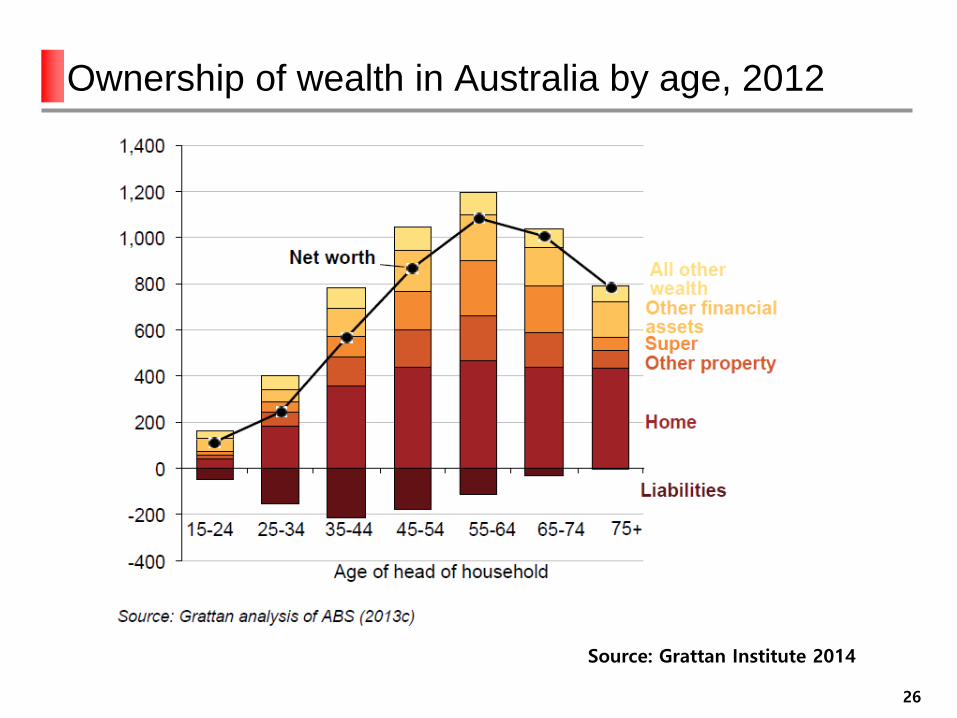

Ownership of wealth in Australia by age, 2012

Source: Grattan Institute 2014

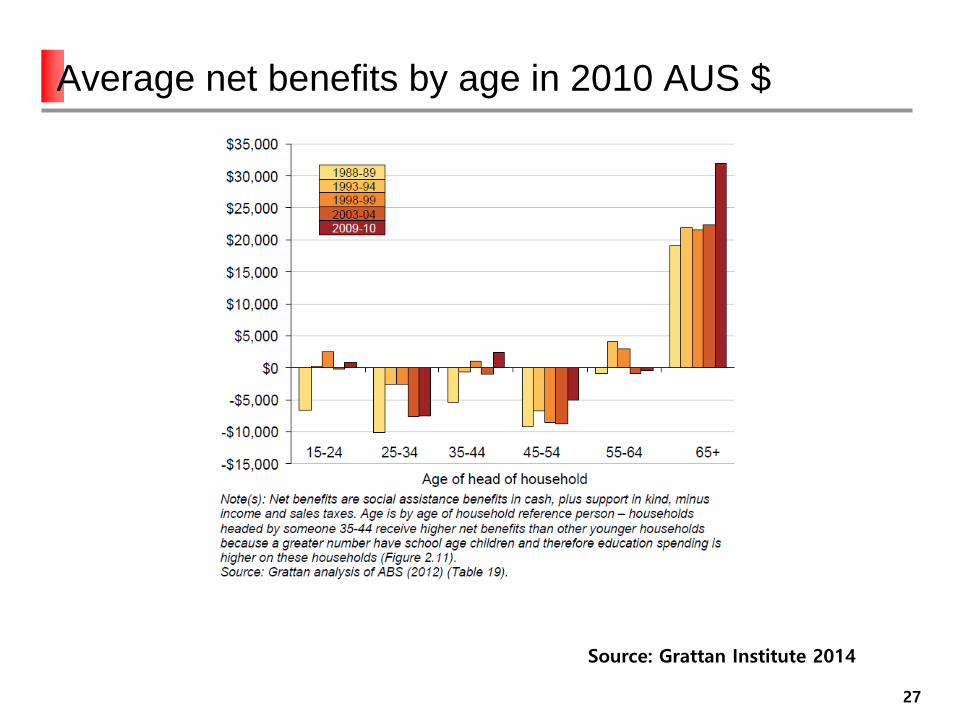

27

Source: Grattan Institute 2014

Average net benefits by age in 2010 AUS $

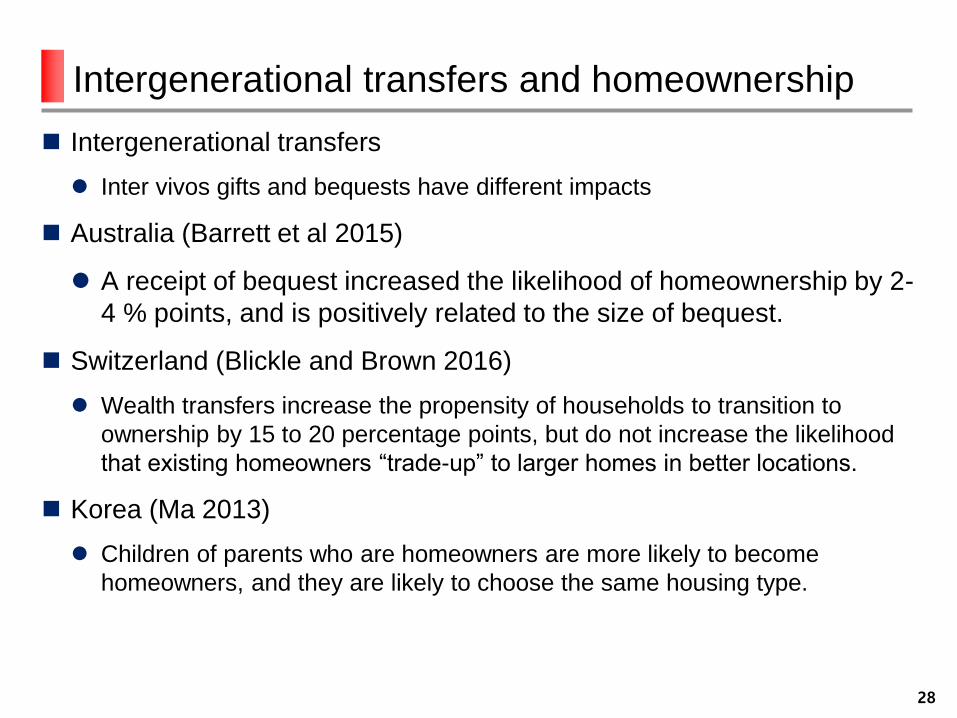

Intergenerational transfers and homeownership

Intergenerational transfers

Inter vivos gifts and bequests have different impacts

Australia (Barrett et al 2015)

A receipt of bequest increased the likelihood of homeownership by 2-

4 % points, and is positively related to the size of bequest.

Switzerland (Blickle and Brown 2016)

Wealth transfers increase the propensity of households to transition to

ownership by 15 to 20 percentage points, but do not increase the likelihood

that existing homeowners “trade-up” to larger homes in better locations.

Korea (Ma 2013)

Children of parents who are homeowners are more likely to become

homeowners, and they are likely to choose the same housing type.

28

29

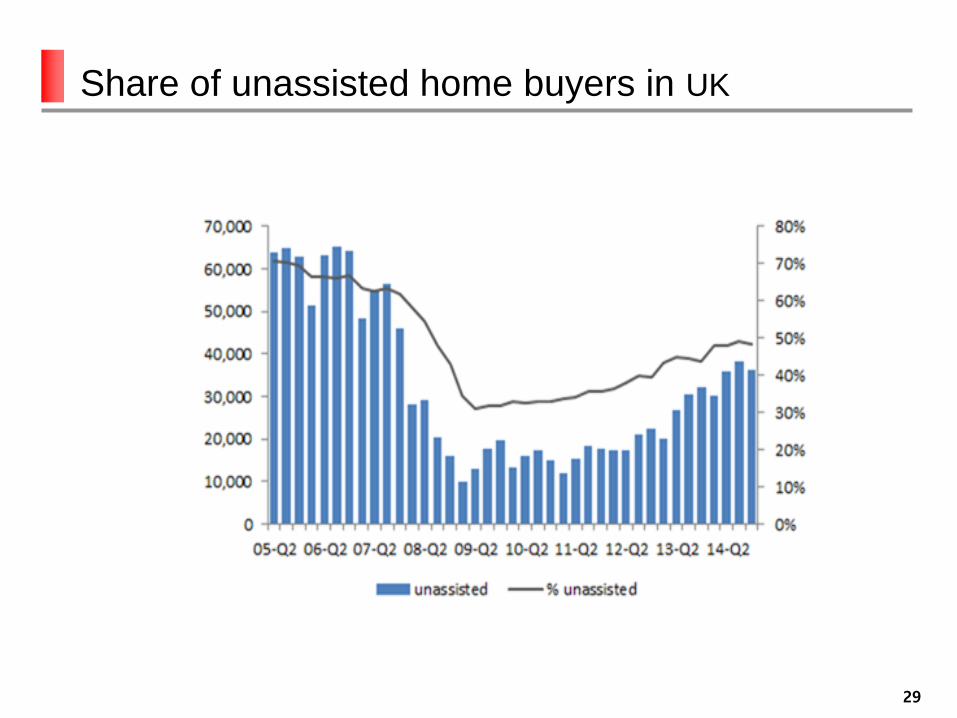

Share of unassisted home buyers in UK

30

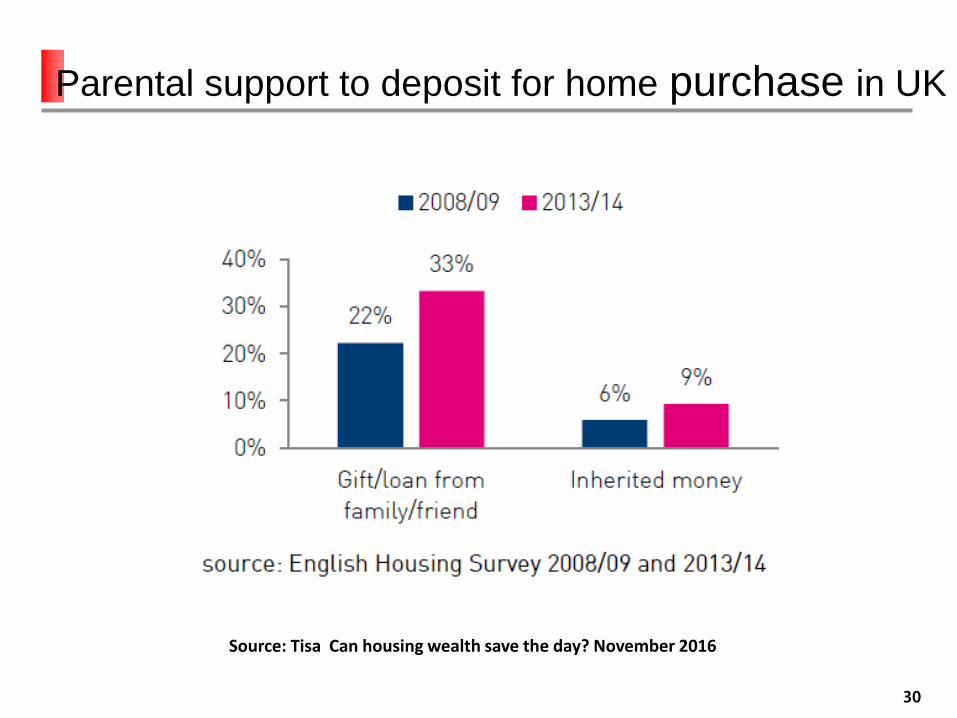

Source: Tisa Can housing wealth save the day? November 2016

Parental support to deposit for home purchase in UK

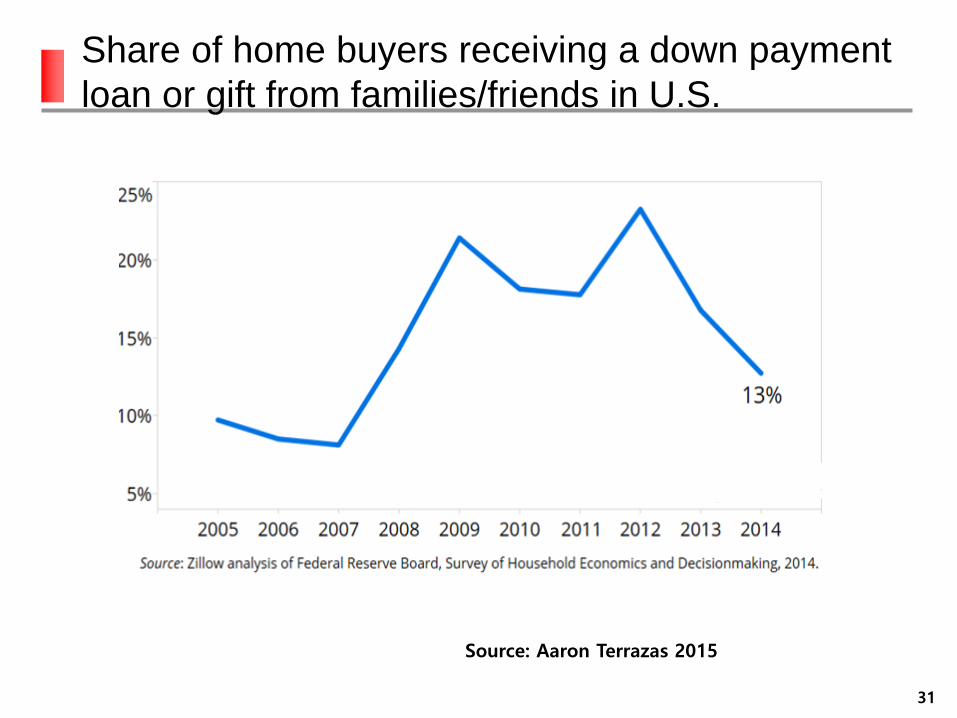

Share of home buyers receiving a down payment

loan or gift from families/friends in U.S.

31

The

Source: Aaron Terrazas 2015

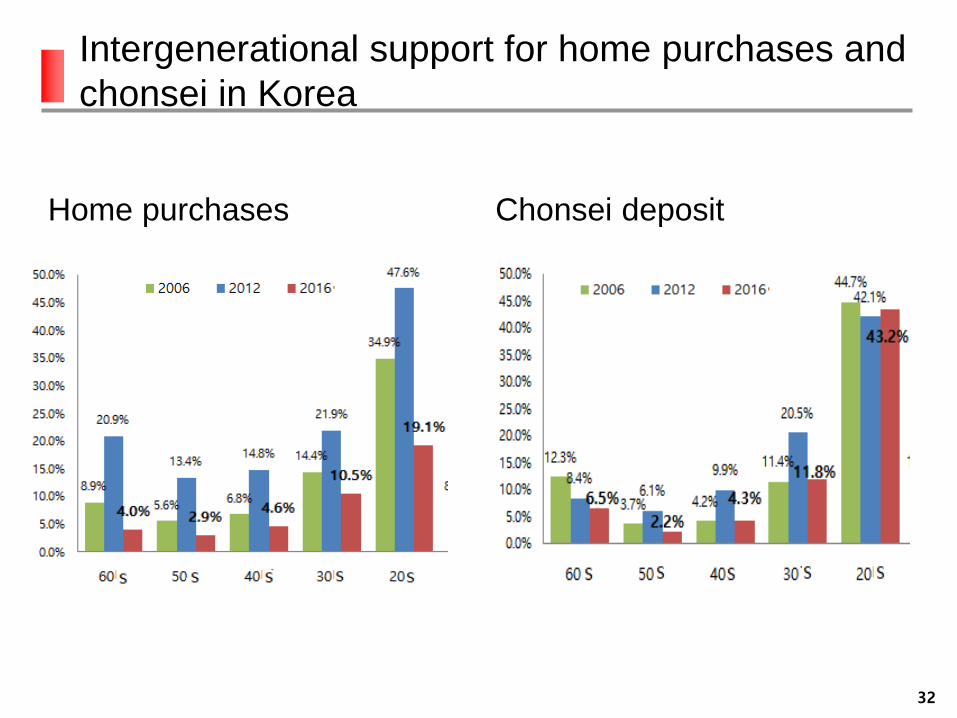

Intergenerational support for home purchases and

chonsei in Korea

Home purchases Chonsei deposit

32

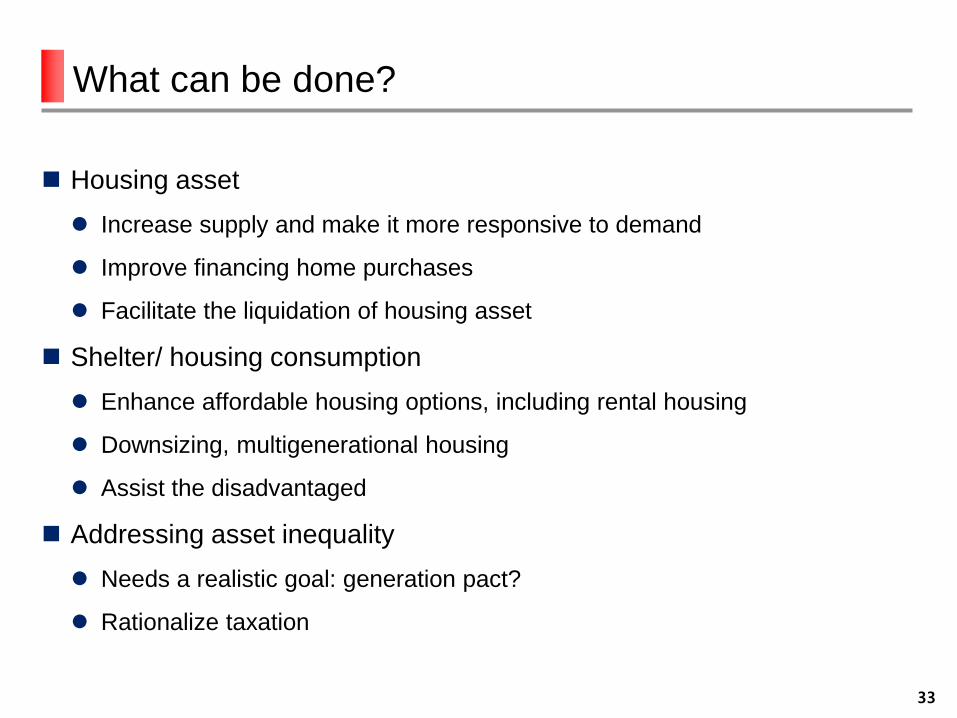

What can be done?

Housing asset

Increase supply and make it more responsive to demand

Improve financing home purchases

Facilitate the liquidation of housing asset

Shelter/ housing consumption

Enhance affordable housing options, including rental housing

Downsizing, multigenerational housing

Assist the disadvantaged

Addressing asset inequality

Needs a realistic goal: generation pact?

Rationalize taxation

33

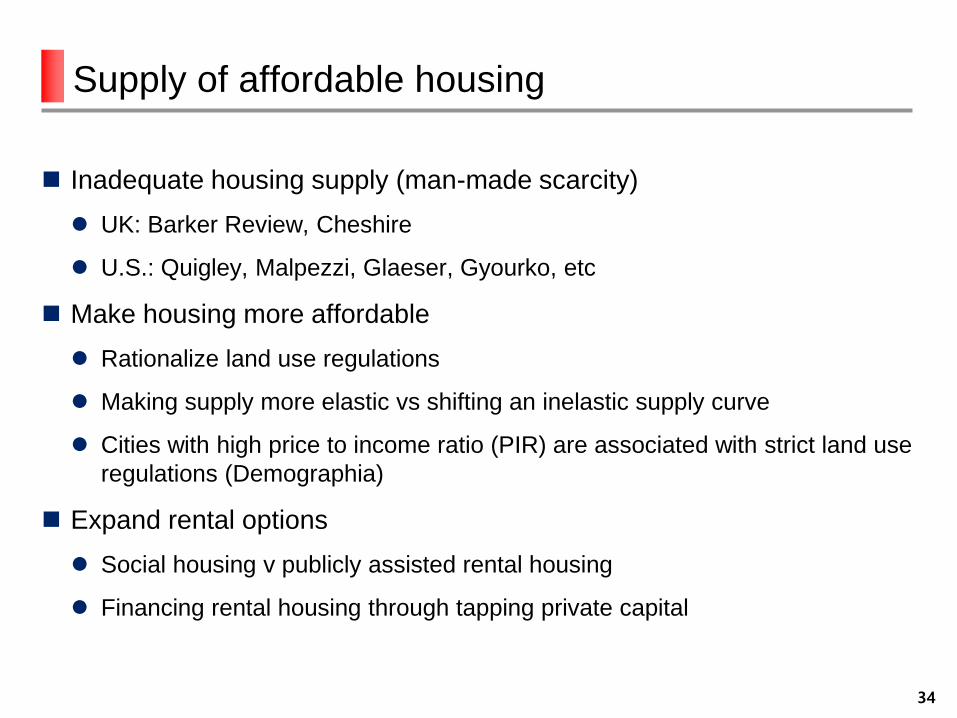

Supply of affordable housing

Inadequate housing supply (man-made scarcity)

UK: Barker Review, Cheshire

U.S.: Quigley, Malpezzi, Glaeser, Gyourko, etc

Make housing more affordable

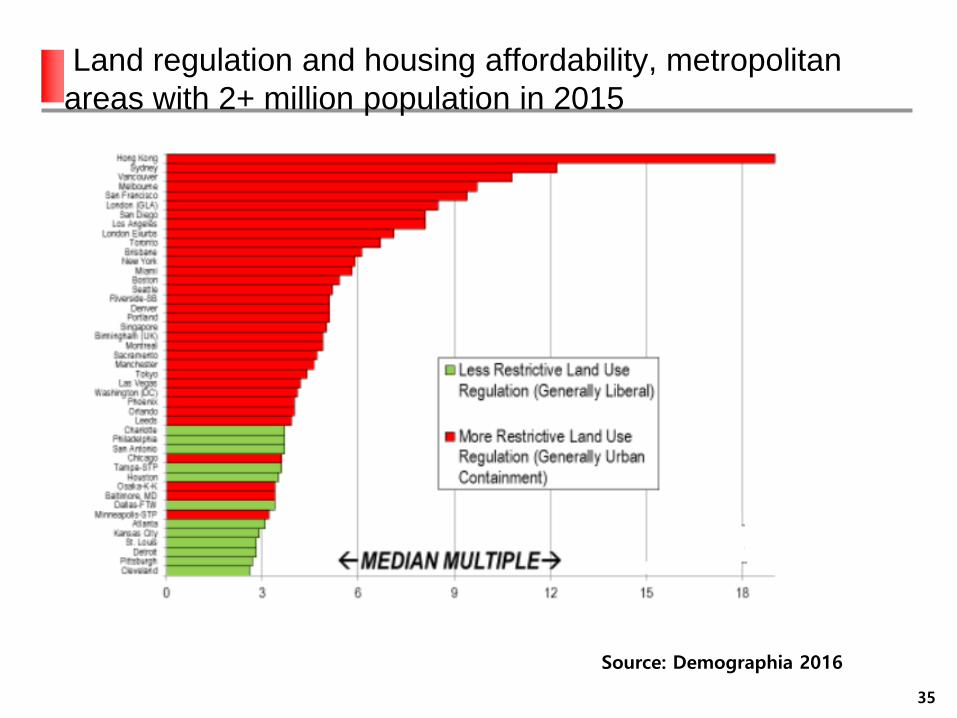

Rationalize land use regulations

Making supply more elastic vs shifting an inelastic supply curve

Cities with high price to income ratio (PIR) are associated with strict land use

regulations (Demographia)

Expand rental options

Social housing v publicly assisted rental housing

Financing rental housing through tapping private capital

34

Land regulation and housing affordability, metropolitan

areas with 2+ million population in 2015

35

Source: Demographia 2016

Inclusive and affordable mortgages

Whither home ownership?

Ensuring sustainable home ownership

Do younger people have diminished aspirations for owning homes?

Innovative financing?

Contractual savings for home purchase linked with (subsidized) loans

Support asset accumulation by the younger generation

Graduated payment mortgages

Reverse mortgages (‘housing pension’ in Korea)

Limitations and conflicts

Housing finance cannot solve the problem of high price to income ratio

altogether

Increasing household debt and macroprudential measures to contain it

36

Taxation and housing inequality

Dilemma of inheritance on housing inequality

Inheritance enhances the chances that members of the younger generation

can purchase homes, mitigating the reversal of generational progress (albeit

in late stage of life, 60+ years old)

But inheritance is not evenly distributed among different income groups,

thereby worsening housing wealth inequality, and exacerbating

intragenerational inequity.

Estate tax (death tax) not popular in U.S. but some countries see its value.

Wealth tax, property tax, and land value tax

Calling for replacing domestic rates with a land value tax in U.K.

Considering an increase in property holding tax in Korea

(Net) wealth tax is levied in some European countries.

Issues: implementation, Incidence, long-run impact on housing market

37

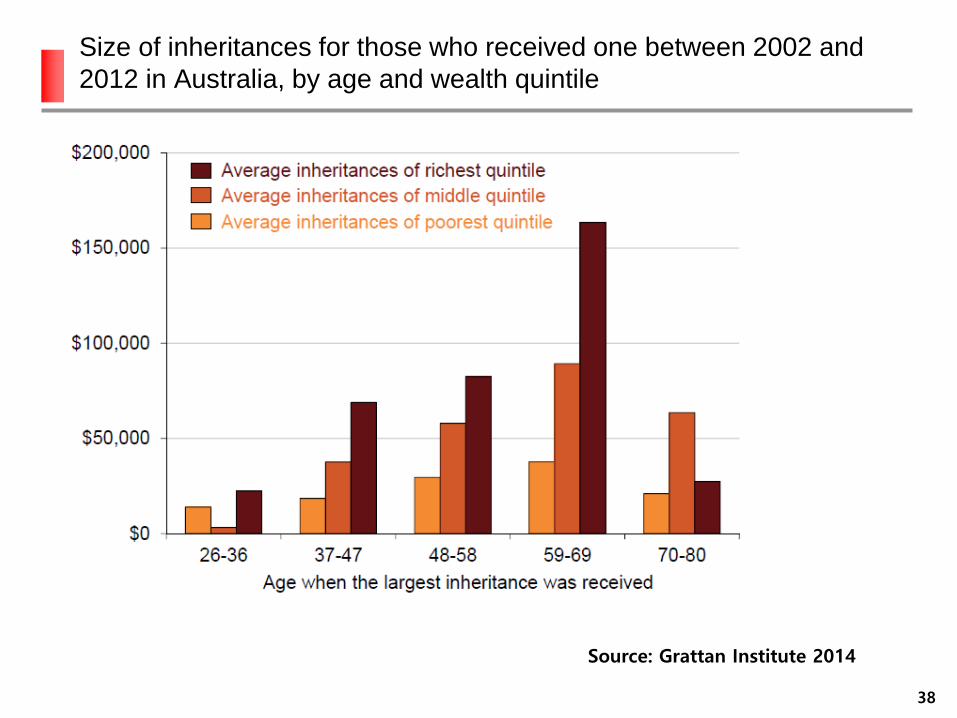

Size of inheritances for those who received one between 2002 and

2012 in Australia, by age and wealth quintile

38

Source: Grattan Institute 2014

Assistance for the disadvantaged

Demand subsidies over interest subsidies

Transparency and efficiency

Clarify the target groups

Incidence of poverty among different age groups (Housing rich, income poor)

In the US, poverty rate is the lowest among the elderly; in Korea, the

incidence of poverty is the highest among the elderly

Tightening budget constraints and tough choices

Ageing, low fertility and slow growth will lead to rapid increase in expenditure

needs and sluggish growth in revenue base

Need to choose between helping the very poor (including the elderly poor)

and helping the young (especially given the need to boos the fertility rate)

with limited financial resources of the government

39

Multigenerational living

Concept

A household that includes two or more adult generations, or one that includes grandparents and grandchildren Sharing space among different age groups

Provides the elderly an alternative to living alone (or in facilities)

Contributes to alleviating the problems of high housing costs and low-fertility (?)

Some data (definitions might differ)

U.S. 19% (2014) (9% in three or more generations)

China 33% (2014) (all in three or more generations)

Policies and research

Japan gives subsidy to building houses that can be inhabited by 3 generations.

Korea tries to encourage splitting up large apartments into two through remodeling.

Research on design

40

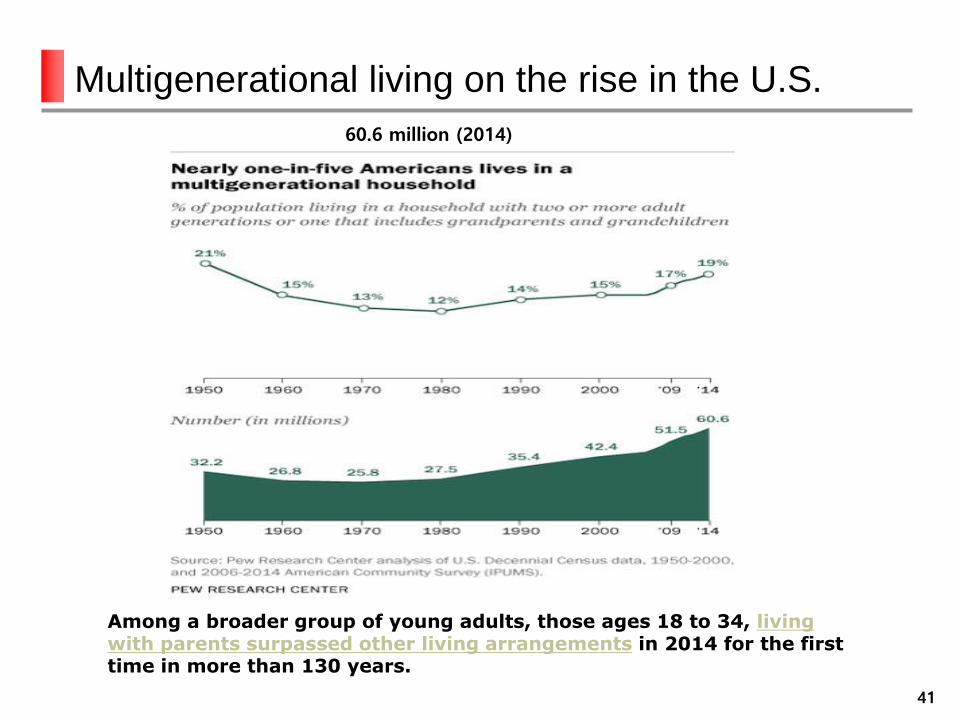

Multigenerational living on the rise in the U.S.

41

60.6 million (2014)

Among a broader group of young adults, those ages 18 to 34, living with parents surpassed other living arrangements in 2014 for the first time in more than 130 years.

Ageing in place and downsizing

Downsizing is not taking place on a large scale.

UK

Hoarding of bedrooms by the elderly. (Griffiths 2011)

Lack of adequate houses to move to discourages downsizing.

Australia

“Older people moved to larger houses between 1996 and 2006” (Judd et

al 2012)

Only 9% of old people downsized between 2006 and 2011 (Judd 2015?)

U.S.

Korea

Many people in their 60s do not sell their houses and downsize.

42

Housing inequality and the New Urban Agenda

Housing in the NUA

Integrated into urban planning

Finance and subsidies

Land and housing supply

Measuring progress

43

![Achievement and Inequality a Seasonal Perspective[1]](https://static.fdocuments.net/doc/165x107/577cd72b1a28ab9e789e3d6e/achievement-and-inequality-a-seasonal-perspective1.jpg)