Housing Finance Report

67

HOUSING FINANCE History of housing Finance The housing finance system in india has had three distinct phases the first phse was before 1970s, when only provider of support to house building activity was government, through its various social schemes for public housing government implemented its schemes through State Housing Board The 1970s saw two major developments in housing finance. A public sector housing company HUDCO (Housing and Urban Development Corporation) was established in 1970 and a private sector company HDFC(Housing Development Finance Corporation) was formed in 1977. The mandate for HUDCO was to assist and promote housing and urban developments with government agencies. HDFC pioneered individual lending based on market principles for homeownership in india. The success of HDFC over years indicated that Financing House can be profitable business. The 1980s also saw enhanced government involvement in directing various agencies like insurance companies ,provident funds , mutual funds etc to invest part of their annualincremntal resources in Housing. And an important event of Formation of National Housing Bank (NHB) in 1987. The objective was to source housing finance through promotion sound, healthy and cost effective housing finance system. In the post liberal era , three distinct groups emerged ; specialized housing finace companies , housing finance companies created as subsidiary of some commercial banks and housing finance companies setup by insurance companies. Drastic changes came in after 1991 in Housing finance The total housing shortage in the country in 1997 was estimated to be 13.66 million units, of which 7.57 million units were in

-

Upload

hirenchavla93 -

Category

Documents

-

view

33 -

download

1

description

Contains detailed working about the Housing finance cos in India

Transcript of Housing Finance Report

HOUSING FINANCE

History of housing Finance

The housing finance system in india has had three distinct phases the first phse was before 1970s, when only provider of support to house building activity was government, through its various social schemes for public housing government implemented its schemes through State Housing Board

The 1970s saw two major developments in housing finance. A public sector housing company HUDCO (Housing and Urban Development Corporation) was established in 1970 and a private sector company HDFC(Housing Development Finance Corporation) was formed in 1977. The mandate for HUDCO was to assist and promote housing and urban developments with government agencies. HDFC pioneered individual lending based on market principles for homeownership in india. The success of HDFC over years indicated that Financing House can be profitable business.

The 1980s also saw enhanced government involvement in directing various agencies like insurance companies ,provident funds , mutual funds etc to invest part of their annualincremntal resources in Housing. And an important event of Formation of National Housing Bank (NHB) in 1987. The objective was to source housing finance through promotion sound, healthy and cost effective housing finance system.

In the post liberal era , three distinct groups emerged ; specialized housing finace companies , housing finance companies created as subsidiary of some commercial banks and housing finance companies setup by insurance companies. Drastic changes came in after 1991 in Housing finance

The total housing shortage in the country in 1997 was estimated to be 13.66 million units, of which 7.57 million units were in urban areas. More than 90 per cent of this shortage was for the poor and low income category. Against this background, the National Housing and Habitat Policy (NHHP) was formulated in 1998 and stressed on:

removing legal, financial and administrative barriers for facilitating access to loans, finance and technology;

ensuring that housing, along with supporting services, was treated as a priority and at par with the infrastructure sector;

the creation of surpluses in housing stock; and providing quality and cost-effective shelters especially to the vulnerable groups and the

poor.The NHB has issued guidelines to the HFCs on prudential norms for income recognition, asset classification, provisioning for bad and doubtful debts, capital adequacy and concentration of credit investment. The NHB also conducts inspection of the HFCs to ensure proper compliance with the prudential norms and prevent the affairs of any of them being conducted in a manner

detrimental to the interests of the depositors or their own. Guidelines for asset liability management system for the HFCs have also been issued by the NHB.

Housing finance

Housing finance is a business of financial intermediation wherein money raised through various sources such as public deposits, institutional borrowings, refinance from national housing bank and their own capital, is lent to borrowers for purchasing a house. These intermediates lend money by accepting mortgage by deposit of title deeds of residential properties.

Types of housing finance

1. Home Purchase Loans: Home Purchase Loans are the basic home loan you can opt for purchasing new home. This type of Home Loan is offered by all kinds of Banks and HFCs.

2. Home Construction Loans: Home Construction Loans are especially meant for the construction of a new home. Formality of availing this loan has a little different from the normal Housing Loan. The plot on which the construction is being erected is purchased within a period of one year, the cost of the plot is then also included as the component for thevaluation of total cost of the property.

3. Home Extension Loans: Home Extension Loans is offered for meeting the operating cost of alteration to an existing building. Extension here means addition of an extra room etc.

4. Home Conversion Loans: Home Conversion Loans are offered to those who want finance for the purchase of another home by converting the already existing home and on which loan is already sanctioned. Through this loan, the existing loan is transferred to the new home including the extra amount required and there is no need for pre-payment of the previous loan

5. Land Purchase Loans: Land Purchase Loans can be availed for purchasing land for both home construction as well as investment purposes.

6. Stamp Duty Loans: Stamp Duty Loans is offered for the payment of stamp duty in the transaction of the property.

7. Bridge Loans: Bridge Loans are offered for selling the existing home and purchasing of another. The bridge loan assists in the finance of new home, until a buyer is found for the old home.

8. Balance-Transfer Loans: Balance Transfer of the loan is the transfer of the balance of an existing home loan at a higher rate of interest (ROI) to either the same company or another.

9. Re-finance Loans: Refinance loans are availed when a loan from an organization at a particular ROI is dropping leading to a loss. Then the option of swap of the loan can be availed. One can avail this from either the same HFI or other at the current rates of interest.

10. NRI Home Loans: NRI Home Loans are meant for Non-Resident Indians who wish to build or buy a home.

INSTITUTIONS PROVIDING HOUSING FINANCE

In India, the following types of institutions provide long term finance for housing:

Commercial banks Cooperative banks Regional rural banks, Agriculture and rural development banks Housing finance companies and Cooperative housing finance societies.

Advantages

Your costs are predictable and more stable than renting because they’re ideally based on a fixed-rate mortgage.

The interest and property tax portion of your mortgage payment is a tax deduction.

Disadvanatges

Homeownership is a long-term financial commitment. Although mortgage payments are usually fixed, they’re generally higher than rent

payments. Buying a home requires a down payment, closing costs and moving expenses. The value of your house may not increase – especially during the first few years. Higher interest component offset the property appreciation to large extent

I personally feel that any financial decision should not be biased and prejudice. We should look at both the aspects before arriving at final decision. Based on rough estimates, 80% residential real estate transactions in India are executed by availing Home Loan. For majority of Indians real estate affordability is major concern. At the same time there is no love lost for Real Estate & Gold. Home Loan is blessing in disguise for this section. Buying a property on Home Loan is a major financial decision and each financial decision comes with own set of advantages and disadvantages.

Home Loan is Long Term CommitmentThough average duration of home loan is 8 years but it is just an average. Median is normally 10-12 years. If you have any major financial goal lined up in next 10 years like kids education or marriage than Home loan is a major hurdle to fulfill the same. Home

Loan put major burden on finances atleast for initial 4-5 years and then it takes another 3-5 years to recover from same. You must be wondering, salary will also increase but we need to account inflation also which is devaluing the salary hike. Last year suppose i got hike of 7% in salary but with average inflation of 10%, in real terms my salary reduced by 3%. This point remain remain one of key disadvantages of home loan until unless there is sharp jump in income levels.

Volatile Interest Rate MovementDaily i get 4-5 cases where people are serving EMI from last 2 years but principal outstanding is still same as it was at the time of availing loan. Reason, when interest rate increases banks increase the loan tenure rather increasing EMI thus your interest component increases in EMI. In few cases, principal outstanding is more than original amount even after 2 years. Uncertainty in Interest rate movement is one of key disadvantages of Home Loan. You may opt for Fixed Rate Home Loan but it also not fixed in true sense.

Opportunity LostThe biggest flaw in our calculations & one of critical disadvantages of home loan is that we don’t consider opportunity lost. If i am paying 2 Lac as principal component during a year then my opportunity lost is returns which i would have received, if i would have invested same money in some other financial instrument say Bank FD. Assuming 9% interest rate, my opportunity lost for the year is Rs 18000 & it should be reduced from home loan benefits.

Actual Cost of PropertyMy friend purchased a 3 BHK apartment in year 2007 for 50 Lac. In 2012, he sold the same flat for 70 lac. Sounds good & prime facie he made profit of 20 lac on his investment. This is not the case as he paid approx 24 Lac interest on Home Loan of 40 Lacs in 5 years. Now, next question coming to your mind will be that he saved income tax also. We will address this in next point but in real sense the actual cost of property is 74 Lacs i.e. 50 lac (Cost) + 24 Lac interest. Notwithstanding this, his principal liability at the time of sale was approx 20 Lacs. Reason for very high interest rate payout initially is that principal

Objectives of the study The current work revolves around the following major objectives.

1. To study the present condition of housing sector in India such as current position of housing stock, household and its comparison with population growth etc.

2. To evaluate and contrast the evolution and recent trends in housing finance system in India.

3. To assess housing shortage and affordable housing policies in Indian housing market.

4. To give some significant recommendations to improve the affordability in housing development in India.

Performance output of key organizations in India India is the second largest populous country in the world, next only to china. Home to roughly 1.1 billion people, India is the second most populous country after China and is expected to overtake it by 2030. About one in every sixth person on earth lives in India, and the growth rate of the population is still rapid. Housing finance is a relatively new concept in India comparing to other financial services that are widely available in the country since a long year back (Annual report ICRA,2011)33. However, the speedy development in housing and various housing activities have understandably led to the growth of Indian housing finance market. As a result, a number of players have barged into the market.

RBI The Reserve Bank of India (RBI) is India's central banking institution, which controls the monetary policy and plays an important role in the development of the nation. In pursuance of National Housing Policy of Central Government, Reserve Bank of India has been facilitating the flow of credit to housing sector. Since housing has emerged as one of the sectors attracting a large quantum of bank finance, the current focus of RBI's regulation is to ensure orderly growth of housing loan portfolios of banks.

National Housing PolicyAs a part of the strategy to overcome the colossal housing shortage, the Central Government adopted a comprehensive National Housing Policy which, among other things, envisaged:

i. Development of a viable and accessible institutional system for the provision of housing finance;

ii. Establishing a system where housing boards and development authorities would concentrate on acquisition and development of land and infrastructure; and Creation of conditions in which access to institutional finance is made easier and affordable for individuals for construction/buying of houses/flats.

iii. This may include outright purchase of houses/flats constructed by or under the aegis of public agencies.

HUDCO It was in the year 1970 when Housing and Urban Development Corporation (HUDCO) was established to finance various housing and urban infrastructure activities. However, the Housing Development Finance Corporation (HDFC) was the India's first private sector housing finance company came into existence in 1977. Since then, the housing finance in India has been flying high. It's expected to grow at a growth rate of 36% in the coming years. Through its

‗Niwas‘scheme, HUDCO offers housing loans for the buying/constructing house/flat. Loans are also offered for Enovation/extension/alteration of existing house/flat.

In the financial year 2009-10 (ended on March 31, 2010), HUDCO registered a net profit of ` 495.31crore, comparing to ` 400.99crore of the previous year.

Commercial banks As the commercial banks started expanding housing-related disbursements, the market share also started growing up. In 2000, the Indian housing finance companies accounted for 70 per cent of the disbursements, while their collective share decreased to 36 per cent within 5 years. In 2005, banks accounted for 64 per cent of the disbursements.

Housing Development Finance Corporation Limited (HDFC)

Housing Development Finance Corporation Ltd (HDFC) is one of the leaders in the Indian housing finance market with almost 17% market share as on March 2010. Serving more than 38lakh Indian customers as on March 2011, HDFC also offers customized solutions that fit to the need of the customer. In the FY 2010-11, it registered a net profit of `4528.41crore. It also registered a net profit of ` 971crore in the quarter ended September 30, 2011.

State Bank of India Home Finance (SBI):

State Bank of India is another major player in the Indian housing finance market with 17% of the market share, same as HDFC's share as on March 2010. The SBI Housing Loan schemes are specifically designed to meet the varied requirements of the customers. It offers home loan for various purposes including new house/flat, purchase of land, renovation/ alteration/ extension of existing house/flat etc. SBI Home Finance registered a net profit of ` 24.63 crore in the year ended March 31, 2009.

LIC Housing Finance Limited:

LIC Housing Finance is another major player in housing finance sector in India with about 8% of market share. Promoted by Life Insurance Corporation of India, LICHFL has an extensive distribution network with a strong brand presence. Recently, the company has been awarded ―Consumer Super brand 2009/10 Status‖ by Super brands Council. In the last financial year (ended on March 31, 2011), LICHFL earned a net profit of ` 974.49 crore, comparing to ` 662.18 in the previous FY. It also registered a net profit of ` 256.50 crore in April- June quarter of 2011.

ICICI Home Finance Company Limited:

ICICI is the third largest housing finance company in India with almost 13% market share. It offers various types of home loans for its customers which may have tenure up to 20 years. The home loan interest rate is connected to the ICICI Bank Floating Reference Rate (FRR/PLR). Here it can be added here that, the PLR has been increased to 17.5% from its previous rate of

17% since February 23, 2011. As on March 31, 2010, ICICI HFC has 2009 branches with an asset of ` 363400crore. The net profit of the company rose 45.19% to Rs 233.29crore in the year ended March 2011 compared to Rs160.68crore profit it earned during the previous year.

IDBI Home finance Limited (IHFL):

Founded in January 10, 2000, IDBI Home finance Limited has become one of the major players in the Indian housing finance market with about 4% market share as on March 2010. It offers a range of housing financial solutions to its customers including Individual Home Loans, Home Improvement Loan, Home Extension Loan, and Home Loans for NRIs, Plot Loans, and Loan against Home etc. The home loan advances of IHFL as of March 2010 were Rs 3,537crore compared to Rs 3,089crore in the previous year. In the financial year 2010-11, IDBI Bank registered a profit of ` 1650crore, comparing to a net profit of ` 1031crore in the previous financial year.

PNB Housing Finance LimitedPNB Housing Finance Limited offers a wide range of loans for purchase/construction of property to resident Indians as well as NRIs. It also offers housing finance for renovations, repairs and enhancement of immovable properties. In the last financial year ended on March 31, 2011, PNB Housing Finance Limited registered a net profit of 69.37crore, which is 3.93% more than the net profit of its previous financial year of 66.75crore.

Dewan Housing Finance Corporation Limited (DHFL)Dewan Housing Finance Corporation Limited is one of the largest housing finance solution providers in India with an extensive network of 74 branches, 78 service centers and 35 camps spread across the nation. For the year ended March 31, 2011, DHFL registered a net profit of Rs. 265.13crore which is a growth of 75.9% over net profit of Rs. 150.69crore in the previous fiscal. In the quarter ended on September 30, 2011, DHFL earned a profit (after tax) of Rs. 71.89crore.

GIC Housing Finance LimitedGIC Housing Finance Limited, one of the leading housing finance companies in India, was initially established as ‗GIC Grih Vitta Limited‘on December 12, 1989. Promoted by General Insurance Corporation of India, GIC Housing Finance Limited offers extensive range of housing finance solutions to its customers through its wide network of 24 Business Centers and 3 Collection Centers across the nation. In the financial year 2010-11, GIC Housing Finance Limited registered a profit (after tax) of Rs.113.76crore. Furthermore, in the quarter ended June 30, 2011, it registered a profit of Rs.1756lakhs.

Can Fin Homes Limited (CFHL)Can Fin Homes Limited is another big player in the Indian housing finance market with an extensive network of 40 branches. It is also the first and one of the biggest bank-sponsored (sponsored by Canara Bank) housing finance companies in India. In the financial year 2010-11, Can Fin Homes Limited registered a net profit of Rs. 4201.6lakhs. It also registered a net profit

of Rs.814lakh in the quarter ended on September 30, 2011. The increase in population (more than 1027 million in 2001 with CAGR of 2.13% during the decade 1991-2001) has led to increase in total number of household from 83.50 million in 1951 to 191.96 million in 2001 (with CAGR of 2.7% during 1991-2001). However, there has also been correspondingly consistent increase in construction of additional houses. As a result, the number of occupied houses in Indian GDP has grown at 6% for the past 10 years and 8% for the last 3 years and interestingly service sector accounts for 60% of GDP (Parekh, D, 2006)

Bibliography: http://www.moneycontrol.com/stocks/marketinfo/netsales/bse/finance-housing.html

Housing Finance in India

Let me now turn to housing in India. As per the Census, during the decade of 2001 to 2011, while housing stock increased by 51 per cent, number of households has increased by 47 per cent. Notwithstanding recent improvements, urban India in 2012 had an estimated shortfall of about 19 million houses. Most of the housing shortage is obviously for economically weaker section (56 per cent) and low income group (39 per cent) people5.

Institutional financing for housing in India is dominated by commercial banks. As on March 2012, outstanding housing loans by banks and housing finance companies was `6.2 trillion, of which about two-thirds were accounted for by banks.

Overall trend in annual growth of credit of scheduled commercial banks in India indicates that the share of credit for housing in aggregate credit rose from under 5 per cent in March 2001 to 12 per cent by March 2006. This was facilitated by a number of favorable factors: First, sustained reduction in inflation resulted in lowering of lending rates. Second, removal of the restriction of prime lending rate (PLR) as the floor rate for pricing housing loan coupled with reduction in risk weight from 100 per cent to 50-75 per cent for housing loan to individuals aided competitive pricing of such loans. Third, the acceleration in GDP growth raised the demand for housing. Thereafter, the rate of growth in housing credit has moderated. Consequently, its share in total bank credit has declined gradually to about 8 per cent by March 2012.

As a percentage of GDP, outstanding housing credit from banks rose from 1.2 per cent in 2001 to a peak of 5.3 per cent in 2006 before moderating to 4.2 per cent by March 2012. The weighted average lending rate (WALR) on housing loan first declined from 12.8 per cent in March 2001 to a low of 8.6 per cent in 2006 before rising to 11.1 per cent by March 2012. Though the interest rate on housing finance has gone up since 2006, it has remained below the overall weighted average lending rate of banks (

Eligible Category of Borrowers

UCBs may grant loans to the following categories of borrowers:

i. Individuals and co-operative / group housing societies.ii. Housing boards undertaking housing projects or schemes for economically weaker sections

(EWS), low income groups (LIG) and middle income groups (MIG).iii. Owners of houses / flats for extension and up-gradation, including major repairs.

Eligible Housing Schemes

The borrowers in the above categories will be eligible for finance for the following types of housing schemes:

a. Construction / purchase of houses / flats by individualsb. Repairs, alterations and additions to houses / flats by individuals

Schemes for housing and hostels for scheduled castes and scheduled tribes

c. Under slum clearance schemes - directly to the slum dwellers on the guarantee of the Government, or indirectly through Statutory Boards established for this purpose

d. Education, health, social, cultural or other institutions / centres which are part of a housing project and considered necessary for the development of settlements or townships

e. Shopping centres, markets and such other centres catering to the day to day needs of the residents of the housing colonies and forming part of a housing project

Terms and Conditions for Housing Loans

Finance provided by the UCBs to the eligible categories of borrowers for eligible housing schemes will be subject to the following terms and conditions:

1 Maximum Loan Amount & Margins

i. UCBs, based on their commercial judgment and other prudential business considerations, with the approval of their Board of Directors, are free to identify the eligible borrowers, decide margins and grant housing loans depending upon the repaying capacity of borrowers.

ii. Tier-I UCBs are permitted to extend individual housing loans upto a maximum of `30 lakh per beneficiary of a dwelling unit and Tier II UCBs (UCBs other than Tier I) to extend individual housing loans up to a maximum of `70.00 lakh per beneficiary of a dwelling unit subject to extant prudential exposure limits.

iii. The maximum loan should not exceed 15 percent of capital funds of the bank in case of individual borrowers and 40 per cent of the capital funds in case of group of borrowers. The capital funds for the purpose shall include both Tier I Capital and Tier II capital.

* Tier I UCBs are categorised as under:

- Banks having deposits below `100 crore operating in a single district

- Banks with deposits below `100 crore operating in more than one district will be treated as Tier I provided the branches are in contiguous districts and deposits and advances of branches in one district separately constitute at least 95% of the total deposits and advances respectively of the bank and

- Banks with deposits below `100 crore, whose branches were originally in a single district but subsequently, became multi-district due to reorganization of the district

Deposits and advances as referred to in the above definition may be reckoned as on 31st March of the immediate preceding financial year.

2 A. Interest

Banks may, with the approval of their Boards, determine the rate of interest, keeping in view the size of accommodation, degree of risk and other relevant considerations.

B. Foreclosure Charges / Prepayment Penalty

With effect from June 26, 2012 it has been decided that UCBs will not be permitted to charge foreclosure charges / prepayment penalties in home loans on floating interest rate basis.

3 Charging of Penal Interest

Banks may formulate, with the approval of their Boards, transparent policy for charging penal interest rates to be levied for reasons such as default in repayment, non-submission of financial statements, etc. The policy should be governed by well accepted principles of transparency, fairness, incentive to service the debt and due regard to genuine difficulties of customers.

4 Security

(i) UCBs may secure housing loans either

a. by mortgage of property, orb. by government guarantee where forthcoming, orc. by both.

(ii) Where this is not feasible, banks may accept security of adequate value in the form of LIC policies, Government Promissory Notes, shares / debentures, gold ornaments or such other security as they deem appropriate.

5 Period of Loan

(i) Housing loans may be repayable within a maximum period of 20 years, including moratorium or repayment holiday.

(ii) The moratorium or repayment holiday may be granted

a. at the option of the beneficiary, orb. till completion of constructions, or 18 months from the date of disbursement of first instalment of

the loan, whichever is earlier.

https://www.rbi.org.in/scripts/BS_ViewMasCirculardetails.aspx?id=8106#

http://www.censusindia.gov.in/2011census/hlo/HLO_Tables.html

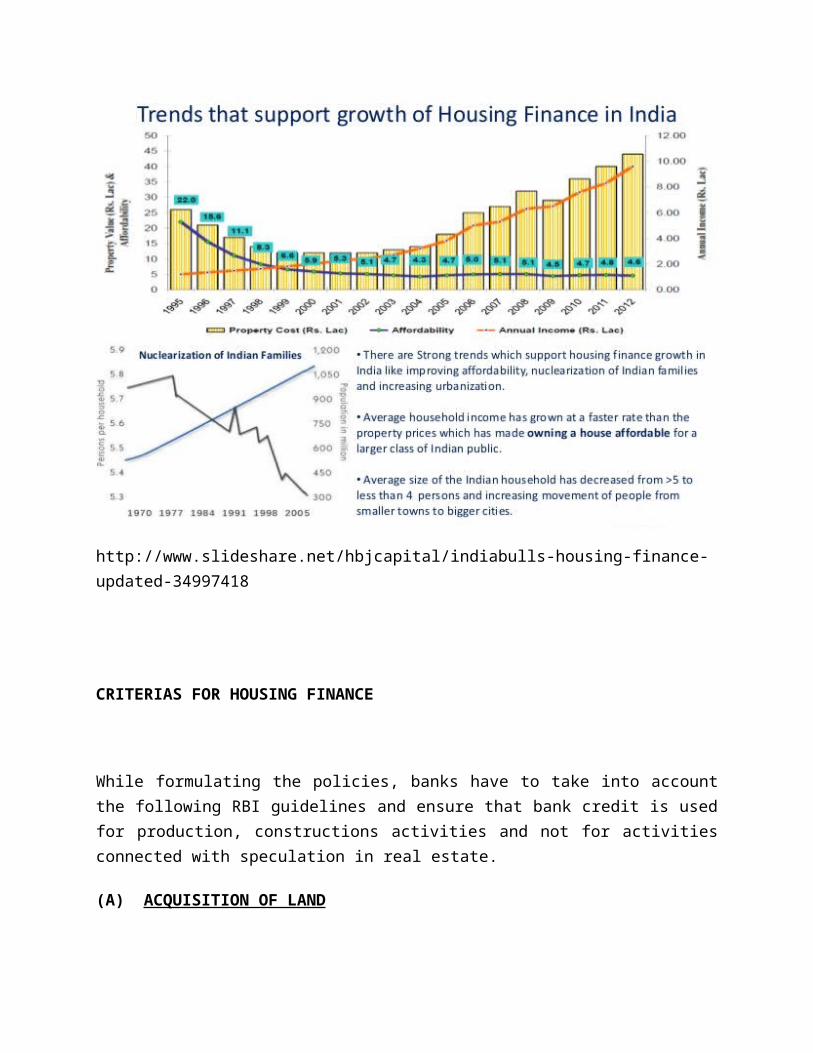

http://www.slideshare.net/hbjcapital/indiabulls-housing-finance-updated-34997418

CRITERIAS FOR HOUSING FINANCE

While formulating the policies, banks have to take into account the following RBI guidelines and ensure that bank credit is used for production, constructions activities and not for activities connected with speculation in real estate.

(A) ACQUISITION OF LAND

Bank finance granted only for purchase of a plot, provided a declaration is obtained from the borrower that he intends to construct a house on the said plot, with the help of bank finance or otherwise, within such period as may be laid down by the banks themselves.

(B) CONSTRUCTION OF BUILDING / READY-BUILT HOUSE

1) Banks may grant loans to individuals for purchase/construction of dwelling unit per family and loans given for repairs to the damaged dwelling units of families.

2) Bank may extend finance to a person who already owns a house in town/village where he resides, for buying/ constructing a second house in the same or other town/ village for the purpose of self-occupation.

3) Bank may extend finance for purchase of a house by a borrower who proposes to let it out on rental basis on account of his posting outside the headquarters or because he has been provided accommodation by his employer.

4) Bank may extend finance to a person who proposes to buy an old house where he is presently residing as a tenant.

5) Banks may finance for construction meant for improving the conditions in slum areas for which credit may be extended directly to the slum-dwellers on the guarantee of the Government, or indirectly to them through the State Governments.

6) Bank may provide credit for slum improvement schemes to be implemented by Slum Clearance Boards and other public agencies.

7) Banks are advised to also adhere to the following conditions, in the light of the observations of Delhi High Court on unauthorized construction:

In cases where the applicant owns a plot/land and approaches the banks/FIs for a credit facility to construct a house, a copy of the sanctioned plan by competent authority in the name of a person applying for such credit facility must be obtained by the Banks/FIs before sanctioning the home loan.

An affidavit-cum-undertaking must be obtained from the person applying for such credit facility that he shall not violate the sanctioned plan, construction shall be strictly as per the sanctioned plan and it shall be the sole responsibility of the executants to obtain completion certificate within 3 months of completion of construction, failing which the bank shall have the power and the authority to recall the entire loan with interest, costs and other usual bank charges.

An Architect appointed by the bank must also certify at various stages of construction of building that the construction of the building is strictly as per sanctioned plan and shall also certify at a particular point of time that the completion certificate of the building issued by the competent authority has been obtained.

In cases where the applicant approaches the bank/FIs for a credit facility to purchase the built up house/flat, it should be mandatory for him to declare by way of an affidavit-cum-undertaking that the built up property has been constructed as per the sanctioned plan and/or building bye-laws and as far as possible has a completion certificate also.

An Architect appointed by the bank must also certify before disbursement of the loan that the built up property is strictly as per sanctioned plan and/or building bye-laws.

No loan should be given in respect of those properties which fall in the category of unauthorized colonies unless and until they have been regularized and development and other charges paid.

No loan should also be given in respect of properties meant for residential use but which the applicant intends to use for commercial purposes and declares so while applying for loan.

8) Supplementary Finance

Banks may consider requests for additional finance within the overall ceiling for carrying out alterations/ additions/repairs to the house/flat already financed by them.

In the case of individuals who might have raised funds for construction/ acquisition of accommodation from other sources and need supplementary finance, banks may extend such finance after obtaining paripassu or second mortgage charge over the property mortgaged in favour of other lenders and/or against such other security, as they may deem appropriate.

Banks may consider for grant of finance to –

A. The bodies constituted for undertaking repairs to houses. B. The owners of building/house/flat, whether occupied by themselves or by tenants,

to meet the need-based requirements for their repairs/additions, after satisfying themselves regarding the estimated cost (for which requisite certificate should be obtained from an Engineer / Architect, wherever necessary) and obtaining such security as deemed appropriate.

9) Bank finance should, however, not be granted for the following:

Banks should not grant finance for construction of buildings meant purely for Government/Semi-Government offices, including Municipal and Panchayat offices. However, banks may grant loans for activities, which will be refinanced by institutions like NABARD.

Projects undertaken by public sector entities which are not corporate bodies (i.e. public sector undertakings which are not registered under Companies Act or which are not Corporations established under the relevant statute) may not be financed by banks. Even in respect of projects undertaken by corporate bodies banks should satisfy themselves that

the project is run on commercial lines and that bank finance is not in lieu of or to substitute budgetary resources envisaged for the project. The loan could, however, supplement budgetary resources if such supplementing was contemplated in the project design. Thus, in the case of a housing project, where the project is run on commercial lines, and the Government is interested in promoting the project either for the benefit of the weaker sections of the society or otherwise, and a part of the project cost is met by the Government through subsidies made available and/or contributions to the capital of the institutions taking up the project.

Banks had, in the past, sanctioned term loans to Corporations set up by Government like State Police Housing Corporation, for construction of residential quarters for allotment to employees where the loans were envisaged to be repaid out of budgetary allocations. As these projects cannot be considered to be run on commercial lines, it would not be in order for banks to grant loans to such projects.

(C) LENDING TO HOUSING INTERMEDIARY AGENCIES

Financing of Land Acquisitiona) In view of the need to increase the availability of land and house sites for increasing

the housing stock in the country, banks may extend finance to public agencies and not private builders for acquisition and development of land, provided it is a part of the complete project, including development of infrastructure such as water systems, drainage, roads, provision of electricity, etc. Such credit may be extended by way of term loans. The project should be completed as early as possible and, in any case, within three years, so as to ensure quick re-cycling of bank funds for optimum results. If the project covers construction of houses, credit extended therefore in respect of individual beneficiaries should be on the same terms and conditions as stipulated for financing the beneficiary directly.

b) Banks should have a Board approved policy in place for valuation of properties including collaterals accepted for their exposures and that valuation should be done by professionally qualified independent valuers.

c) As regards the valuation of land for the purpose of financing of land acquisition as also land secured as collateral, banks may be guided as under: Banks may extend finance to public agencies and not to private builders for

acquisition and development of land, provided it is a part of the complete project, including development of infrastructure such as water systems, drainage, roads, provision of electricity, etc. In such limited cases where land acquisition can be financed, the finance is to be limited to the acquisition price (current price) plus development cost. The valuation of such land as prime security should be limited to the current market price.

Wherever land is accepted as collateral, valuation of such land should be at the current market price only.

Lending to Housing Finance Institutions

Banks may grant term loans to housing finance institutions taking into account (long-term) debt-equity ratio, track record, recovery performance and other relevant factors including the other applicable regulatory guidelines.

Lending to Housing Boards and Other Agencies

Banks may extend term loans to state level housing boards and other public agencies. However, in order to develop a healthy housing finance system, while doing so, the banks must not only keep in view the past performance of these agencies in the matter of recovery from the beneficiaries but they should also stipulate that the Boards will ensure prompt and regular recovery of loan instalments from the beneficiaries.

Term Loans to Private Builders

a. In view of the important role played by professional builders as providers of construction services in the housing field, especially where land is acquired and developed by State Housing Boards and other public agencies, commercial banks may extend credit to private builders on commercial terms by way of loans linked to each specific project.

b. Banks however, are not permitted to extend fund based or non-fund based facilities to private builders for acquisition of land even as part of a housing project.

c. The period of credit for loans extended by banks to private builders may be decided by banks themselves based on their commercial judgment subject to usual safeguards and after obtaining such security, as banks may deem appropriate.

d. Such credit may be extended to builders of repute, employing professionally qualified personnel. It should be ensured, through close monitoring, that no part of such funds is used for any speculation in land.

e. Care should also be taken to see that prices charged from the ultimate beneficiaries do not include any speculative element that is, prices should be based only on the documented price of land, the actual cost of construction and a reasonable profit margin.

Terms and Conditions for Lending to Housing Intermediary Agencies

a. In order to enhance the flow of resources to housing sector, term loans may be granted by banks to housing intermediary agencies against the direct loans

sanctioned/ proposed to be sanctioned by the latter, irrespective of the per borrower size of the loan extended by these agencies.

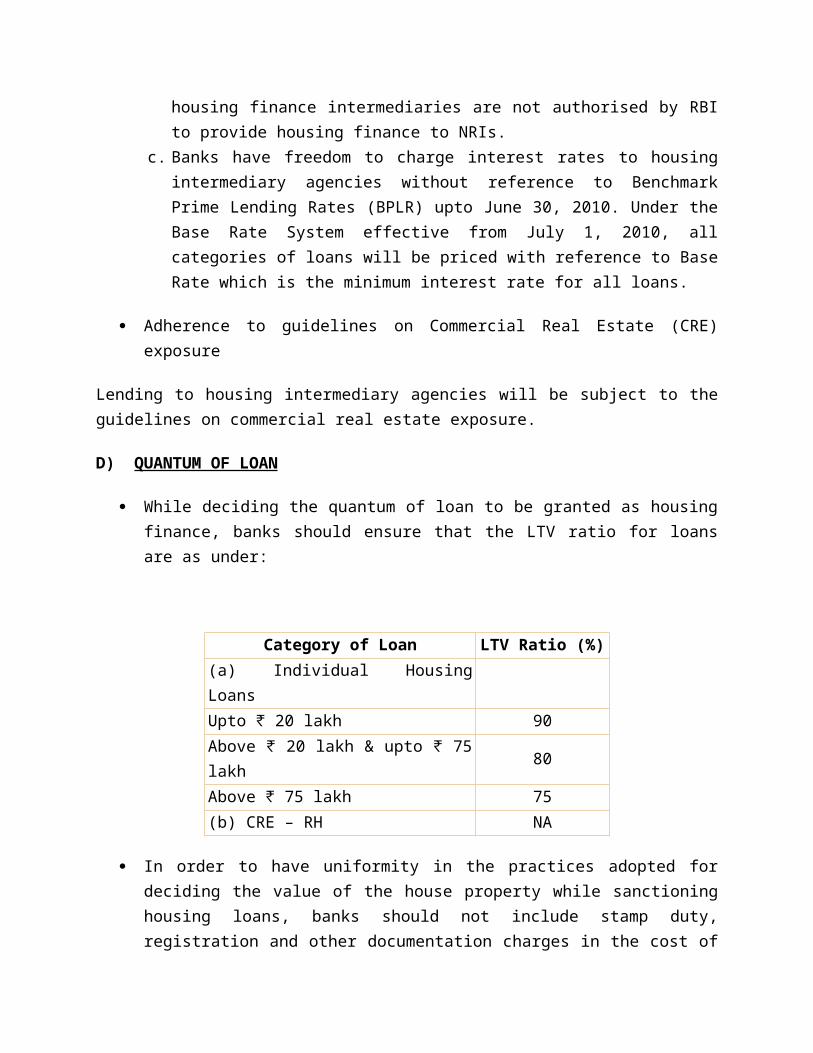

b. Banks can grant term loans to housing intermediary agencies against the direct loans sanctioned/proposed to be sanctioned by them to Non-Resident Indians also. However, banks should ensure that housing finance intermediary agencies being financed by them are authorised by RBI to grant housing loans to NRIs as all housing finance intermediaries are not authorised by RBI to provide housing finance to NRIs.

c. Banks have freedom to charge interest rates to housing intermediary agencies without reference to Benchmark Prime Lending Rates (BPLR) upto June 30, 2010. Under the Base Rate System effective from July 1, 2010, all categories of loans will be priced with reference to Base Rate which is the minimum interest rate for all loans.

Adherence to guidelines on Commercial Real Estate (CRE) exposure

Lending to housing intermediary agencies will be subject to the guidelines on commercial real estate exposure.

D) QUANTUM OF LOAN

While deciding the quantum of loan to be granted as housing finance, banks should ensure that the LTV ratio for loans are as under:

Category of Loan LTV Ratio (%)(a) Individual Housing LoansUpto 20 lakh₹ 90Above 20 lakh & upto 75 lakh₹ ₹ 80Above 75 lakh₹ 75(b) CRE – RH NA

In order to have uniformity in the practices adopted for deciding the value of the house property while sanctioning housing loans, banks should not include stamp duty, registration and other documentation charges in the cost of the housing property they finance so that the effectiveness of LTV norms is not diluted.

In cases where the cost of the house/dwelling units does not exceed Rs.10 lakh, bank may add stamp duty, registration and other documentation charges to the cost of the house/dwelling unit for the purpose of calculating LTV ratio.

Banks are advised that disbursal of housing loans sanctioned to individuals should be closely linked to the stages of construction of the housing project / houses and upfront

disbursal should not be made in cases of incomplete / under-construction / green field housing projects.

However, in cases of projects sponsored by Government/Statutory Authorities, banks may disburse the loans as per the payment stages prescribed by such authorities, even where payments sought from house buyers are not linked to the stages of constructions, provided such authorities have no past history of non-completion of projects.

It is emphasized that banks while introducing any kind of product should take into account the customer suitability and appropriateness issues and also ensure that the borrowers/ customers are made fully aware of the risks and liabilities under such products.

(E) RATE OF INTEREST

Banks should charge interest on housing finance granted by them in accordance with the directives on “Interest Rates on Advances” issued by Reserve Bank of India from time to time.

(F) APPROVALS FROM STATUTORY/ REGULATORY AUTHORITIES

While appraising loan proposals involving real estate, banks should ensure that the borrowers should have obtained prior permission from government / local governments / other statutory authorities for the project, wherever required. In order that the loan approval process is not hampered on account of this, while the proposals could be sanctioned in normal course, the disbursements should be made only after the borrower has obtained requisite clearances from the government authorities.

(G) DISCLOSURE REQUIREMENTS

In view of the observations of High Court of Judicature at Bombay, while granting finance to specific housing / development projects, banks are advised to stipulate as a part of the terms and conditions that:

Disclose in the Pamphlets / Brochures etc., the name(s) of the bank(s) to which the property is mortgaged.

Append the information relating to mortgage while publishing advertisement of a particular scheme in newspapers / magazines etc.

Indicate in their pamphlets / brochures, that they would provide No Objection Certificate (NOC) / permission of the mortgagee bank for sale of flats / property, if required.

Banks are advised to ensure compliance of the above terms and conditions and funds should not be released unless the builder/developer/company fulfils the above requirements.

The above mentioned provisions will be mutatis-mutandis, applicable to Commercial Real Estate also.

(H) EXPOSURE TO REAL ESTATE

Banks are well advised to frame comprehensive prudential norms relating to the ceiling on the total amount of real estate loans, single/group exposure limit for such loans, margins, security, repayment schedule and availability of supplementary finance and the policy should be approved by the bank’s board. While framing the bank’s policy the guidelines issued by the Reserve Bank should be taken into account.

(I) ADDITIONAL GUIDELINES

It is advised that banks should adhere to the National Building Code (NBC) formulated by the Bureau of Indian Standards (BIS) in view of the importance of safety of buildings especially against natural disasters. Banks may consider this aspect for incorporation in their loan policies. Banks should also adopt the National Disaster Management Authority (NDMA) guidelines and suitably incorporate them as part of their loan policies, procedures and documentation.

NHB (National Housing Bank)

NHB is wholly owned by RESERVE BANK OF INDIA. Its an apex financial institution for housing which commenced its operations on 9 July 1988. It operates as a principal agency to promote housing finance institutions both at local and regional levels and to provide financial and other support to such institutions.

VISION: To promote inclusive expansion with stability in housing finance market

MISSION: To harness and promote the market potentials to serve the housing needs of all segments

of the population with the focus on low and moderate income housing

OBJECTIVES:

a. Promote a sound, healthy, viable and cost effective housing finance system to cater to all segments of the population and to integrate the housing finance system with the overall financial system.

b. Promote a network of dedicated housing finance institutions to adequately serve various regions and different income groups.

c. Augment resources for the sector and channelize them for housing.d. Make housing credit more affordable.

e. Regulate the activities of housing finance companies based on regulatory and supervisory authority derived under the Act.

f. Encourage increased supply of buildable land and also building materials for housing and to upgrade the housing stock in the country.

g. Motivate public agencies to emerge as facilitators and suppliers of serviced land, for housing.

Entire paid-up capital contributed by RBI. NHB grants direct loans to Public Agencies directly or in partnership with private developers

under PPP model to development of housing projects as per the Schemes/Guidelines of NHB. NHB does not grant any loan (housing loan/mortgage loan/reverse mortgage loan) directly to

individual. For commencing the housing finance business, an HFC is required to have the following in addition to the requirements under the Companies Act, 1956: Certificate of registration from NHB, Minimum net owned fund of Rs. 10 crores ( w.e.f. 01.04.2014)

HFC (HOUSING FINANCE COMPANY) falls under the NHB (National Housing Bank). The names of various HFCs are- DHFL Housing Finance Limited, GIC, GRUH, HDFC (Housing Development Finance Corporation Limited), ICICI Home Finance Company Limited, India Bulls Housing Finance Limited, etc. The following will give clear understanding of HFC and how it is a part that falls below NHB.

Housing Finance Company (HFC)

A company registered under the Companies Act, 1956 which primarily transacts or has as one of its principal objects, the transacting of the business of providing finance for housing, whether directly or indirectly.

HFCs are categorized in terms of the type of liabilities, by NHB, into Deposit and Non-Deposit accepting HFCs and are issued Certificate of Registration accordingly

Apart from Registrar of Companies, registration from NHB is needed by HFC It’s needed from NHB to commence or carry out the business of housing finance. Moreover, w.e.f. April 1, 2014, NHB has specified the net owned fund requirements of Rs. 10 crores to be by abided by HFC.

Requirements for commencing housing finance business by an HFC with NHB

Requirements under the Companies Act, 1956:

A company must be registered (Certificate Of Registration) under the Companies Act, 1956 and desirous of commencing business of a housing finance institution.

Either it should primarily transacts or has as one of its principal objects of transacting the business of providing finance for housing, whether directly or indirectly

Should have a minimum NOF-Net Owned Fund(*) of Rs. 10 crore. ( w.e.f. 01.04.2014) HFC is/shall be in a position to pay its present/future depositors in full as and when their

claims accrue Proposed management of the HFC shall not be prejudicial to the public interest or to the

interests of its depositors Public interest shall be served and grant of certificate of registration shall not be

prejudicial to the operation and growth of the housing finance sector of the country

* Net Owned Fund (NOF) - Paid up capital + reserves & surplus(excluding revaluation reserve)+Long term liabilities(to be paid after one year)-Trading investment-Fictitious assets(like preliminary expenditure)

Can HFC appeal against the order of rejection of certificate of registration and if so with whom.Yes. An appeal to the Central Government within a period of 30 days from the date on which such order of rejection is communicated to it.

Whether NHB can cancel the Certificate of Registration granted to a HFC, and if so under what circumstances.In terms of sub-section (5) of Section 29 A of the National Housing Bank Act, 1987, NHB may cancel a certificate of registration granted to a housing finance company, subject to certain provisions, if such company:

Ceases to carry on the business of a housing finance institution in India Has failed to comply with any condition subject to which the certificate of registration

had been issued to it Failed to comply with any direction issued by the National Housing Bank under the

provisions of Chapter V of the National Housing Bank Act, 1987 Has not maintained accounts in accordance with the requirement of any law

/direction/order issued by the National Housing Bank under the provisions of Chapter V of the National Housing Bank Act, 1987.

Failed to submit/offer for inspection its books of account and other relevant documents when demanded by an inspecting authority of the National Housing Bank.

Has been prohibited from accepting deposit by an order made by the National Housing Bank under the provisions of the National Housing Bank Act, 1987 and such order has been in force for a period of more than three months.

How are HFC different from banks.HFCs lend and make investments and have their activities akin to that of banks. However, there are few differences stated as follows:I. HFCs cannot accept demand deposits.

II. HFCs do not form part of the payment and settlement system and cannot issue cheques drawn on it.

III. Deposit insurance facility of Deposit Insurance and Credit Guarantee Corporation is not available to depositors of HFCs, unlike in case of banks.

Grievance Redressal Mechanism in place for customers of HFCs

Complainant can lodge the complaint with the respective housing finance company (HFC) and an online (24x7) Grievance Registration and Information Database System (GRIDS) has been implemented for lodging the complaint by the complainant against HFCs and its status tracking for efficient and effective disposal. Further, if the complainant is still not satisfied with the outcome or his complaint is not resolved within a given period, he/she can approach other forms of legal remedies available.

Can all HFCs accept public deposits.For acceptance of public deposits HFCs can be divided into two categories, i.e. HFCs carrying on the business of housing finance before June 12, 2000 and HFCs commencing housing finance business after that date.

(a) Companies carrying on business of housing finance before June 12, 2000 can accept deposits provided they have NOF of over Rs. 25 lakhs and have applied for certificate of registration with NHB before December 12, 2000 and either have been granted the certificate of registration valid for acceptance of deposits by NHB or their application is still pending for issue of certificate of registration with NHB.

(b) Companies commencing the business of housing finance after June 12, 2000 can accept public deposits only after:

(i) obtaining certificate of registration from NHB valid for acceptance of deposits; and

(ii) having minimum net owned funds (NOF) of [Rs. 2 crores or more]*.

*this amount was Rs 25 lakhs or more for HFCs which commenced business before February 16, 2002.

Ceiling on the maximum amount of public deposit which can be accepted by an HFC

Yes. HFCs having credit rating from approved credit rating agencies not below ‘A’ and complying with all prudential norms requirements can accept deposit not exceeding five times of its net owned fund. The HFCs having no credit rating can accept deposit only upto two times of its net owned fund or Rs. 10 crores whichever is lower provided such HFC complies with all prudential norms and also has capital adequacy ratio of not less than fifteen percent as per the last audited balance sheet.

Is credit rating compulsory for acceptance of public deposits by an HFC?No. The HFC having credit rating can accept more deposits as per the conditions laid down for acceptance of deposits in such a case as compared to an HFC without such rating.

The following credit rating agencies have been approved for the purpose

The Credit Rating Information Services of India Ltd. (CRISIL)

ICRA Ltd.

Credit Analysis and Research Limited (CARE)

FITCH Ratings India Pvt. Ltd.

Action that can be taken by NHB against HFCs if not complying with the provisions of the Act or the Housing Finance Companies (NHB) Directions, 2001.

Issuing specific directions prohibiting acceptance of deposits and alienation of assets Cancellation of certificate of registration. Filing of applications for winding up petition Imposition of financial penalties on the HFC and its principal officers Filing of complaints before the Magistrate for imposition of penalties

Ceiling on the rate of interest offered by an HFC on public deposits

The Housing Finance Companies (NHB) Directions, 2001 provide for ceiling on the maximum rate of interest which can be offered by an HFC on public deposits. The present ceiling is twelve and half per cent per annum compounded at intervals not shorter than monthly rests. However, there is no stipulation with regard to the minimum rate of interest required to be offered on public deposits by an HFC.

Limitation/ restriction on the period for which public deposit can be accepted by a HFC.HFCs can accept public deposits for periods of 1 year - 7 years only.

Can an HFC on its own repay the deposit prematurely?No, acceptance of public deposit is a contract between the HFC and the depositor for a definite period of time. However, any novation of the contract has to be mutually agreed between the parties and should be in conformity with the provisions of Housing Finance Companies (NHB) Directions, 2001.

Are public deposits of HFCs guaranteed by NHB No. The depositor is advised to satisfy himself about the financial position and all relevant aspects before placing his deposit with the HFC. A person making public deposits with HFCs should satisfy himself that it holds a valid certificate of registration for accepting public deposits from NHB. NHB while issuing certificate of registration to an HFC specifically mentions whether or not it can accept public deposits.

Remedies available to a depositor when the HFC does not re-pay the deposits on maturity.The depositor can file a civil suit for recovery of the amount of deposit. He can also make a complaint to the Consumer Forums set up under the Consumer Protection Act, 1986. The depositor should also bring such cases to the notice of NHB for taking action against the defaulting companies under the provisions of the NHB Act. On being satisfied that the company has defaulted in repayment of deposits NHB may issue directions prohibiting it from acceptance of further deposits and alienation of its assets. NHB may also impose financial penalties and take action for imposition of other penalties. NHB may also file winding up petition against such companies.

Provisions for regulation of HFCs under the National Housing Bank Act, 1987.The provisions for regulation of the HFCs as provided under the NHB Act, 1987 are:

Requirement of Registration and Net Owned Fund Maintenance of percentage of assets in specified securities Creation of Reserve Fund by the HFCs Regulation or prohibition of issue of prospectus or advertisement soliciting deposits Determination of Prudential Norms for HFCs Collection of information as to deposits and to give directions Issue of directions to the auditors of the HFCs relating to financial statements and

disclosure requirements Prohibition of acceptance of deposits and alienation of assets Penalty for violation of the provisions of the Act or the directions issued thereunder.

Filing of winding up petition against erring HFCs.

Methodology adopted by NHB to regulate the HFCs under the NHB Act, 1987 and Housing Finance Companies (NHB) Directions, 2001.The methodology adopted by NHB broadly comprises the following:

Entry level regulation, i.e., scrutiny of the HFC at the time of Registration Off-site surveillance, i.e., through analysis of the information, return, periodicals etc.

filed by the HFCs from time to time. On-site inspections, i.e., visit by the officers of the NHB to the offices of HFCs and

verification/ scrutiny of the books of accounts, returns, etc. Constant interaction with other regulatory authorities

The returns/ statements required to be submitted by the HFCs to NHB are:

Annual Return Half-yearly Return on Prudential Norms Quarterly Return on maintenance of Liquid Assets Auditor’s Certificate on annual basis certifying the capability of the HFC to repay

deposits Copy of financial statements / Annual Report Returns on changes pertaining to address of the registered office of the HFC, its

Directors etc. Filing a copy of the advertisement soliciting Public Deposits or statement in lieu

thereof. Provisions under the NHB Act, 1987 and Housing Finance Companies (NHB) Directions,

2001 for safeguarding the interest of the depositors.

Some of the safeguards under the NHB Act, 1987 and Housing Finance Companies (NHB) Directions, 2001 are enumerated below:

Imposition of ceiling on the amount that can be accepted by an HFC Imposition of ceiling on the rate of interest on deposits Provision for nomination facility Requirement of disclosures to the depositors Imposition of ceiling on brokerage to be paid by HFC for raising deposits Prohibition on alienation of assets in case of default in repayment of deposits Requirement of maintenance of Liquid Assets by HFC Creation of Reserve Fund

HFCs are doing functions similar to banks as bank also provides housing loans. What is difference between banks & HFCs.

HFCs lend and make investments and hence their activities are akin to that of banks. However, there are a few differences as given below:

HFCs cannot accept demand deposits HFCs do not form part of the payment and settlement system and cannot issue

cheques drawn on it. Deposit insurance facility of Deposit Insurance and Credit Guarantee Corporation is not

available to depositors of HFCs, unlike in case of banks.

MORTGAGE BACKED SECURITIZATION

Mortgage-backed securities (MBS) are debt obligations that represent claims to the cash flows from pools of mortgage loans, most commonly on residential property. Mortgage loans are purchased from banks, mortgage companies, and other originators and then assembled into pools by a governmental, quasi-governmental, or private entity. The entity then issues securities that represent claims on the principal and interest payments made by borrowers on the loans in the pool, a process known as securitization.

The transactions between parties in the housing finance sector can be broadly classified as those relating to ‘primary residential mortgage market’ and ‘secondary residential mortgage market’. The primary mortgage market activity mainly comprises creation of mortgages as a result of transactions between the borrowers and primary lenders. The primary lenders create mortgages against loans provided by them to the purchasers of houses. The mortgages held as assets, generate cash flows represented by repayments of both principal and interest, on the loans.

The secondary mortgage market mainly involves the conversion of mortgages into tradable financial instruments and the sale of these instruments to prospective investors. The cash flows which come as repayments from the borrowers to the originators, can be transferred to a third party with simultaneous transfer of assets to an intermediary agency (SPV) designated for the purpose of managing the bought over pool of mortgages. These cash flows are passed on to the investors by the SPV. In the process, the mortgages are converted into securities which are tradable financial instruments and sold to investors. The secondary mortgage market is thus made up of securities which are backed by mortgages (MBS) and refers to the transactions between the issuers and investors.

Once the securitized mortgages are sold by the originators viz., the primary lending institutions, they are either de-recognized in the originator’s books of account or presented in a specific manner. All future transactions in the mortgage backed financial instruments then take place in the secondary mortgage market, depending up the depth of the market. The overall liquidity in the capital market and housing finance system would increase with the number of transactions among investors in the secondary mortgage market.

Securitization : Benefits

Supportive fiscal measures and the policies of Reserve Bank of India (RBI) have established a systemic framework for specialized mortgage finance in the country and the sector has been witnessing steady growth of over 28% in the past few years. In the recent past, with the emergence of the capital market as the central pool of resources for sectorial development, Securitization not only offers a viable and sustainable market oriented sourcing mechanism with the potential of integrating housing market with the domestic as well as the international capital markets, but also brings in a range of specializations, resulting in efficient and cost effective structures and practices.

Improves Capital Adequacy Ratio (CAR) through transfer of risk weighted assets; Aids Asset Liabilities Management and helps long term source for deployment in housing

sector; Enables better spread management, and facilitates improvement of return on assets and

return on equity; Enables new source of fee based income

The transaction involves :

a) Assignment and Transfer of a pool of housing loans along with the underlying mortgages, from the primary lending institution to NHB.

b) Securitization of Mortgage Debt: On acquiring the pool along with the underlying mortgages, an express declaration of trust will be made by NHB in respect of the mortgage debt, appointing itself as the trustee for the benefit of the investors. Once the assets have been declared property in trust (“the Trust”), the Trust will issue PTCs to investors.

STEP NO. 1

Authorization for securitization by originator: Originator to obtain authorization from its relevant internal highest authority for securitization its pool of home loans.

Intimation to NHB : The originator (HFC / Bank) to write a formal letter to NHB indicating its intention to securitize its home loans with copies of relevant authorization of its relevant authorities (for instance Board Resolution) and proposal to go ahead with securitization of its home loan portfolio with NHB’s SPV arrangement.

STEP NO. 2

selection of pool of loans

time frame: as per originator’s convenience

NHB’s Pool Selection Criteria (given separately) - the home loans should satisfy the standards for being considered for selection in the Mortgage Pool offered for securitization.

Identification of Geographic Locations for Selection of Loans –To begin with, loans originated in Tamil Nadu, Gujarat (compulsory), Karnataka, Maharashtra, and West Bengal may be considered.

Initial Pool Size Decision (by Originator in consultation with NHB) Supply of Initial Pool Information to NHB

STEP NO. 3

Due diligence & rating of the mortgage pool (may be done simultaneously)

(a)

Appointment of Rating Agency by Originator (for AAA(So) Rating) (in consultation with NHB)

Supply Pool Information to Rating Agency Commencement of Rating Process Award of Rating by Rating Agency

(b)

Appointment of Auditors for Due Diligence Audit of Mortgage Pool (with consultations between NHB and Originator)

Verification of Mortgage Pool by Auditors for certifying Due-diligence (Auditors may be Statutory Auditors of Bank/HFC or a Chartered Accountancy Firm)

Completion of Due Diligence Audit and Certification by Auditors

STEP NO. 4

(may be done simultaneously with step 5, as offer document is a part of memorandum of agreement to be executed between NHB & bank)

Appointment of Issue Arranger(s) by NHB – (On consultations between NHB and Originator)

Preparation of Offer Document by Issue Arrangers

STEP No. 5

EXECUTION OF MEMORANDUM OF AGREEMENT WITH NHB

Draft Agreement to be sent from NHB to Bank/HFC Finalization of Agreement by Bank/HFC Signing the Agreement by NHB and Originator

STEP NO. 6

Issue opens Receipt of application money by NHB Issue closes Finalization of allotment by NHB and issue arrangers Issue of allotment letter to investors by NHB (immediately after finalization of allotment) Payment of consideration by NHB to originators (simultaneously with issue of allotment

letter to investors)

STEP No. 7

PAY-OUTS TO INVESTORS ON STIPULATED PAY-OUT DATE(S)

STEP No. 8

DOCUMENTATION

Execution of:

- Deed of Assignment - Deed of Declaration of Trust - Servicing and Paying Agency Agreement - Any other Document(s)

Registration of Documents (Deed of Assignment and Declaration of Trust) at the Office of Sub-Registrar of Assurances

(NHB shall provide all legal and advisory support pertaining to execution of documents at Gujarat. For the purpose of local coordination at Gujarat, the Originating HFC /Bank may engage an advocate in consultation with NHB)

Selection of Pool of Housing Loans The pool of housing loans would be selected by the Primary Lending Institution from its existing

housing loans based upon a ‘pool selection criteria’.

ELIGIBILITY CRITERIA FOR HOME LOANS TO QUALIFY FOR SECURITISATION

The home loans should satisfy the following standards for being considered for selection in the Mortgage Pool offered for securitization:

The borrower should be individual(s). The home loans should be current at the time of selection/securitization. The home loans should have a minimum seasoning of 12 months (excluding moratorium

period). The Maximum Loan to Value (LTV) Ratio permissible is 85%. Housing loans originally

sanctioned with an LTV of more than 85% but where the present outstanding is within 85% of the value of the security, will be eligible.

The Maximum Installment to (EMI) to Gross Income ratio permissible is 45%. The loan should not have over dues outstanding for more than three months, at any time

throughout the period of the loan. The Quantum of Principal Outstanding Loan size should be in the range of Rs.0.50 lakh

to Rs.100 lakhs. The pool of housing loans may comprise of fixed and/or variable interest rates. The Borrowers have only one loan contract with the Primary Lending Institution (PLI). The loans should be free from any encumbrances/charge on the date of

selection/securitization. The sole exception to this norm being loans refinanced by NHB (In such cases, the loans may be securitized subject to the originator substituting the same with other eligible housing loans conforming with the provisions of the refinance schemes of NHB).

The Loan Agreement in each of the individual housing loans, should have been duly executed and the security in respect thereof duly created by the borrower in favour of the PLI and all the documents should be legally valid and enforceable in accordance with the terms thereof.

The Bank/HFC has with respect to each of the housing loans valid and enforceable mortgage in the land/building/dwelling unit securing such housing loan and have full and absolute right to transfer and assign the same to NHB.

The Pool selection criteria may be modified by NHB from time to time at its sole discretion.

Valuation of the pool and Consideration of Assignment NHB will consider making payment of purchase consideration to the Primary Lending Agency under the following methodology, with a view to obtain a sound and efficient pricing structure to the benefit of originators:

(i) Par Pricing Methodology: The consideration payable to the Primary Lender for transferring the pool would be equal to the total future outstanding principal balances of the individual loans on a Cut-Off Date.

(ii) Premium Pricing Methodology: The consideration paid to the Primary Lender for transferring the pool would be decided and paid on the basis of discounting of future stream of net cashflows relating to the pool. It shall normally be higher than the total outstanding principal balances of the individual loans on a Cut-Off Date as the discounting rate used shall be lower than the weighted average coupon of the pool.

(iii) Discount Pricing Methodology: The consideration paid to the Primary Lender for transferring the pool would be lower than the total outstanding principal balances of the individual loans on a Cut-Off Date as the discounting rate used shall be higher than the weighted average coupon of the pool due to higher risk perception.

Working out cutoff date balancesThe outstanding principal as on the cut-off date, may be worked out by adjusting the original loan amount to the extent of the principal component of the EMIs payable up to the cut-off date together with the adjustment for any prepayments received during this period.Liquidity Adjustment FacilityIn view of delayed receipt of installments from some borrowers at times and grace periods allowed by the primary lending agencies to its borrowers, collection efficiencies may vary from month to month leading to inadequacy of cash flow required for servicing. In order to protect the purchaser of housing loans/investors in MBS from such uncertainties, there may be a need to set up a ‘Liquidity Adjustment Facility’ as a temporary stopgap arrangement.

VISITS

Housing Development Finance Corporation (HDFC)The Housing Development Finance Corporation, popularly known as HDFC Bank, was

established in the year 1994 and is one of the first Indian banks to receive an in-principle approval from the RBI. At present, HDFC is one the largest lenders in India and the fifth largest bank in the country by assets. HDFC is also ranked one among the top 50 banks in the world in terms of market capitalization. The bank has also received an array of awards like J.P Morgan Quality Recognition Award and Fab 50 by Forbes Asia that stands as a testimony to its impeccable quality and customer services.

HDFC home loan products are popular in the Indian market because of the customer-centric advantages and the features that it offers.

HDFC is the pioneer in home loan section With features like attractive rate of interest, flexible tenure, tailored schemes for different individuals and customized repayment solutions, HDFC Home Loans will delight the borrowers.

A pioneer in home loan section who has served over 4.4 million happy home owners, HDFC Home Loans will take away the monetary-constraint factor so you have a happy property financing experience.

The USP of HDFC is their developed system and their understanding of this sector.

Features and Benefits of HDFC Housing Loans:

Read on to find more about the features that make HDFC Home Loans one of the most-sought after product in the Indian financial market.

Attractive and affordable rate of interest Customers can enjoy flexible repayment tenure of up to 30 years. An extensive range of specially crafted home loan products & solutions like home extension

loans, automated repayment of EMI and home improvement loan Different tailored solutions like pre-approved home loans, home loan transfer and Home loans

for Non-resident Indians Special offers for horticulturalists, planters, agriculturalists and farmers. Quick and efficient loan processing with door-step service Absolutely no hidden charges and completely transparent process Legal and technical counseling by experts to help the customer make the right decision Extensive branch network for loan servicing and availing, anywhere across the country HDFC Bank offers you the flexibility to schedule your home loan as part floating or fixed as

per your requirements.

Products Offers

HDFC NRI Home LoanThis loan is offered for Non-Resident Indians who are of Indian origin or is a citizen of India.

HDFC Rural Home LoanThis loan is specially offered for planters, agriculturalists, horticulturalists and dairy farmers.

Co-applicant for the home loanWhen you are applying jointly for HDFC bank housing loan, all proposed owners of the house must be co-applicants. But, all co-applicants need not necessarily be co-owners. Co-applicants are generally immediate family members.

The income requirements vary depending on the loan amount, tenure, type of housing loan scheme and other conditions.

Documents required for HDFC Home Loans:

Having all necessary documents in place will ensure a quick and easy loan processing, here is a list of documents that you must have when applying for HDFC Housing Loan.

Mandatory Documents:For Agriculturalists, Salaried Customers, Businessmen and Professionals:

Application form with recent photographs Bank statements for the last 6 months Identity and Address Proof

Income Documents:

For Agriculturalists

Copies of title documents for agricultural land showing the land holdingCopies of title documents for agricultural land showing crops being cultivatedStatement of loans availed in the last 2 years

Salaried Applicants

Latest salary slipsForm 16

Businessmen and professionals

Business profile documentsIT Returns for the last 3 years for business & selfLast three years profit and loss statement (P&L) and balance sheetCertificate of educational qualificationsProof of business

Other Documents: Proof of identity and residence can be any of a valid passport, voter ID card, valid driving

license and Aadhar card. Applicants might be asked to submit the following documents as income proof - PAN

card, last 3 months salary slips, last 6 months bank statements showing salary credit and the latest ITR & Form-16.

As property documents, the applicant must submit a copy of the allotment letter, buyer agreement and receipt of payment made of the developer.

If the applicant’s employment is less than 1 year, the employment contract or appointment letter will be asked for.

Different Types of Home Loan Available at HDFC Bank Ltd:

The following types of home loan schemes are offered by HDFC Bank.

Home Loan for Salaried and Self-Employed HDFC Pre-Approved Loan Scheme HDFC NRI Home Loan HDFC Home Loan Transfer Home Improvement Loan (HIL) Home Extension Loan HDFC Special Home Loan for Agriculturists HDFC Rural Housing Finance

HDFC Home Loans Interest Rates:

HDFC Bank, as one of the flag-bearers of banking in India, offers home loans at an interest rate that is considered very appealing and competitive. Currently, this interest rate starting from 9.85% to 10.35%, and is applicable to different home loan products and eligible customer groups banking with HDFC.

Home Loan Interest Rates for Salaried and Self-Employed Professionals:

Home Loan/Home Improvement Loan/Refinancing/Home Extension Loan

Revised Rate 9.90 %

Basis RPLR – 6.65 %

HDFC Housing Loan Interest Rate for Self-Employed Non-Professionals:

Home Loan/Home Improvement Loan/Refinancing/Home Extension Loan

Revised Rate9.90 %

Basis RPLR – 6.65 %

For Self-Employed Value plus Home Loans:

Home Loan/Home Improvement Loan/Refinancing/Home Extension Loan

Revised Rate 10.90 %

Basis RPLR – 5.65 %

Interest Rates for Top-Up Home Loans in HDFC:

Interest rate for home loan plus the top-up loan 9.90%

Interest Rates for TruFixed plus Home Loans - 2 and 3 year variants:

Loan Slabs

For employed and self-employed professionals

Self Employed Non-Professionals

Interest Rate

ARHL interest rate post fixed rate period

Interest Rate

ARHL interest rate post fixed rate period

Up to and including Rs.75 lakhs

9.95% RPLR - 6.60 9.95% RPLR - 6.60

Above Rs.75 lakhs to Rs.5crore

10.05% RPLR - 6.50 10.15% RPLR - 6.40

Above Rs.5crore 10.15% RPLR - 6.40 10.25% RPLR - 6.30

Interest Rates for TruFixed Plus Home Loans - 10 Year variant:

Loan Slabs

For employed and self-employed professionals

Self Employed Non-Professionals

Interest Rate

ARHL interest rate post fixed rate period

Interest Rate

ARHL interest rate post fixed rate period

Up to and including Rs.75 lakhs

10.05% RPLR - 6.50 10.05% RPLR - 6.50

Above Rs.75 lakhs to Rs.5 crore

10.20% RPLR - 6.35 10.30% RPLR - 6.25

Above Rs.5 crore 10.30% RPLR - 6.25 10.40% RPLR - 6.15

HDFC Adjustable rate home Loan for Women:

Loan Quantum- Any Interest Rate per annum 9.85% to 10.35% RPLR Minus Spread RPLR 6.70 to 6.20

HDFC Home Loan Repayment:

Step Up Repayment Facility (SURF)This repayment scheme is based on the expected income growth of the borrower. In the initial years, you can pay substantially lower installments and still avail a high quantum of loan. Subsequently, the repayment increases proportionally with the assumed growth in the borrower’s income.

Tranche Based EMIIn case you purchase a property that is under construction, you are required to pay the interest amount for the loan till the final disbursement of loan amount and then pay the EMIs thereafter. With tranche based EMI, customers can immediately start on the principal repayment and start paying EMIs on cumulative disbursed amount.

Flexible Loan Installments Plan (FLIP)FLIP is essentially a customized solution which is linked to the repayment capacity of the borrower which may change during the loan tenure. The repayment schedule is in such a way that the installment is higher during initial years of the term and then decreases proportionally to the income.

Accelerated Repayment SchemeThis is a flexible scheme where you can increase the EMIs every year, proportional to your income growth which will enable you to repay the loan much faster.

Telescopic Repayment Option

Telescopic repayment plan will get the borrower a longer repayment tenure of up to 30 years which means the EMIs will be more affordable and the loan eligibility will also be enhanced.

Prepayment of loan