Hotels & Hospitality - JLL · Hotels & Hospitality Hotel Intelligence Amsterdam ... timeshare and...

11

Hotels & Hospitality Hotel Intelligence Amsterdam 2013 Amsterdam's hotel industry posted flat year-on-year growth in RevPAR in 2012 and we do not anticipate a significant uplift in 2013 in light of persisting economic difficulties resulting in subdued domestic corporate demand as well as growth in supply, notably on the city fringes. The medium term is viewed more optimistically as a number of well-known international brands firmly put Amsterdam on the map globally aided by new economic developments and initiatives capturing substantial growth in foreign demand and international travel.

Transcript of Hotels & Hospitality - JLL · Hotels & Hospitality Hotel Intelligence Amsterdam ... timeshare and...

Hotels & Hospitality

Hotel Intelligence Amsterdam 2013

Amsterdam's hotel industry posted flat year-on-year growth in RevPAR in

2012 and we do not anticipate a significant uplift in 2013 in light of persisting

economic difficulties resulting in subdued domestic corporate demand as well

as growth in supply, notably on the city fringes. The medium term is viewed

more optimistically as a number of well-known international brands firmly put

Amsterdam on the map globally aided by new economic developments and

initiatives capturing substantial growth in foreign demand and international

travel.

2 Hotel Intelligence: Amsterdam

Authors

Market Snapshot Minor growth in tourism demand in 2012 Passenger arrivals at new record high of 51 million in 2012 Amsterdam remains one of Europe’s major conference and event destinations A growing number of overseas visitors Hotels in 3- and 4-star category take up major share 1st Hyatt Place to enter the market in 2013 No RevPAR growth in 2012 Upscale hotels outperforming the overall market

Josef Filser Associate, EMEA [email protected]

Table of Contents

3

4

5

5

6

6

7

8

9

Jones Lang LaSalle’s Hotels & Hospitality Group serves as the hospitality industry’s global leader in real estate services for luxury, upscale, select service and budget hotels; timeshare and fractional ownership properties; convention centers; mixed-use developments and other hospitality properties. The firm’s more than 265 dedicated hotel and hospitality experts partner with investors and owner/operators around the globe to support and shape investment strategies that deliver maximum value throughout the entire lifecycle of an asset. In the last five years, the team completed more transactions than any other hotels and hospitality real estate advisor in the world totaling nearly US$25 billion, while also completing approximately 4,000 advisory and valuation assignments. The group’s hotels and hospitality specialists pro-vide independent and expert advice to clients, backed by industry-leading research. For more news, videos and research from Jones Lang LaSalle’s Hotels & Hospitality Group, please visit: www.jll.com/hospitality

Marcus Linden Research Assistant, EMEA [email protected]

Hotel Intelligence: Amsterdam 3

Market Snapshot

Tourism: Tourism in Amsterdam is highly dependent on international demand, which accounted for 82% of total visitor arrivals in 2012. A majority of Amsterdam’s tourists are overseas leisure tourists, primarily from the UK, the US and Germany. Hotels also benefit from a robust business environment with various large conventions and exhibitions regularly hosted in the city. Tourism demand in Amsterdam has seen steady growth in recent years with visitation and overnight stays showing a cumulated annual average growth (CAAG) rate of 3.3% and 2.9% respectively between 2003 and 2012. Supply: As at January 2013 the hotel market in Amsterdam comprised of 398 hotels with roughly 24,000 hotel rooms. The market is dominated by 4- and 3-star hotels, which represent 66% of the entire hotel bedroom stock. Graded hotel room supply in the Dutch capital has grown at a compound annual average growth (CAAG) rate of 3.5% over the last 10 years. Growth in hotel supply has picked up within the last 5 years, growing by a CAAG rate of 4.5% . If all proposed developments are realised, total supply will increase by 4.4% in 2013 and by 4.3% in 2014. Trading: The Amsterdam upscale hotel market experienced solid growth in trading performance from 2004 until 2007, when weakening economic conditions started to impact occupancy and room rates. During 2008 and 2009 hoteliers suffered from double-digit declines in Revenue Per Available Room (RevPAR). Performance improved in 2010 and 2011, hotels posting year on year RevPAR growth of 19.8% and 7.7% respectively. Due to the effects of the Euro Crisis and a significant increase in hotel supply, performance weakened in 2012 with RevPAR declining by 0.5% year on year. Hotel trading in the upscale segment, however, has seen a considerable improvement during the first 4 months of 2013 with occupancy and RevPAR levels growing by 5.2% and 5.4% respectively.

4 Hotel Intelligence: Amsterdam

Minor growth in tourism demand in 2012

Amsterdam: Tourism Trends

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 CAAG

2003-12

Visitor Arrivals (‘000s) Domestic 501 533 623 743 954 863 938 1,099 991 980 7.7%

International 3,484 3,659 3,894 3,955 3,910 3,664 3,689 4,184 4,330 4,360 2.5%

Total 3,985 4,192 4,517 4,698 4,864 4,527 4,627 5,283 5,321 5,340 3.3%

Growth p.a. -2.4% 5.2% 7.8% 4.0% 3.5% -6.9% 2.2% 14.2% 0.7% 0.3% Bed Nights (‘000s) Domestic 866 888 995 1,185 1,510 1,388 1,577 1,858 1,684 1,673 7.6%

International 6,745 7,037 7,204 7,472 7,334 6,922 6,984 7,867 8,064 8,128 2.1%

Total 7,611 7,925 8,199 8,657 8,844 8,310 8,561 9,725 9,748 9,802 2.9%

Growth p.a. -5.1% 4.1% 3.5% 5.6% 2.2% -6.0% 3.0% 13.6% 0.2% 0.6%

Source: Dienst onderzoek en statistiek * Preliminary figures

Amsterdam: Tourism Demand

Source: Dienst onderzoek en statistiek

7,000

7,500

8,000

8,500

9,000

9,500

10,000

4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

5,600

2005 2006 2007 2008 2009 2010 2011 2012

Bed

Nig

hts

(000

s)

Arr

ival

s (0

00s)

Visitor Arrivals Bed Nights

Source: Dienst onderzoek en statistiek

Amsterdam: Top Feeder Markets 2012 vs. 2011

0 200 400 600 800 1,000 1,200 1,400 1,600

UK

USA

Germany

Asia

Italy

France

Spain

Bed Nights (Thousands)

Visitor Origin 2012 Visitor Origin 2011

Amsterdam lies on the banks of two bodies of water, the IJ-bay and the Amstel river. Founded in the late twelfth century as a small fishing village, it is now a financial and cultural centre. Although the seat of the Dutch government is in The Hague, Amsterdam is the country’s nominal capital. It is also the country’s largest city, with a population of 790,000. Tourism in Amsterdam is highly dependent on international demand, which in 2012 accounted for 82% of total visitor arrivals. A majority of tourists are leisure visitors (64% of overnight stays in 2012) attracted by the city’s wealth of cultural attractions including its renowned museums such as the Van Gogh Museum, the Rijksmuseum and Anne Frank House. A large proportion of tourism in Amsterdam is also accounted for by business/corporate visitors (30%) which is further supported by the large number of foreign companies in the city.

Tourism demand has seen steady growth in the last 10 years with visitation and overnight stays showing a cumulated annual average growth (CAAG) rate of 3.3% and 2.9% respectively. This was fuelled by a strong growth in foreign demand. In 2012, tourism demand reached a new record at 5.3 million arrivals and 9.8 million overnight stays. Amsterdam’s major foreign feeder markets are the UK (14% of foreign overnight stays in 2012) followed by the US ( 10%) and Germany (7%). Most visitors come from major European cities, most notably London, Paris, Barcelona, Madrid and Milan. According to the Amsterdam Tourism & Convention Board, US and UK leisure tourists have the highest spending power at €181 and €155 per day respectively. Similar to other destinations emerging markets have gained importance with a growing amount of overseas visitors coming from BRIC countries: Brazil (+23%), Russia (+25%), India (+10%) and China (30%).Strong growth in foreign demand has also been witnessed from other emerging economies in Asia and South America.

Hotel Intelligence: Amsterdam 5

Passenger arrivals at new record high of 51 million in 2012

The municipal council of Amsterdam has recently started the implementation of project 1012 which is aimed at improving the quality of the city centre within the ‘1012’ postcode. These improvements will be achieved through discouraging crime and corruption, substantial investments in public areas, regulating and closing several coffee shops & adult shops and alleviating some restrictions on planning consent for the development of new hotels, restaurants and businesses. The complete realisation of Project 1012 will take approximately 10 years to complete, however initiatives and implementations have already begun.

Schiphol Airport: Passenger Arrivals

-

10

20

30

40

50

60

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Pass

enge

rs (m

illio

ns)

Source: Schiphol Airport Group

In 2012, Schiphol was Europe’s fourth largest airport with 317 direct connections to European and intercontinental airports in 99 countries. A number of additional intercontinental destinations were added, such as Guangzhou, Rio de Janeiro, Buenos Aires and Orlando. Since the dip in passenger traffic in 2009, the airport has seen consistent growth in passenger arrivals and in 2012 witnessed a new record high at 51 million, reflecting a 2.6% growth year on year. This was fuelled by an increase in passenger arrivals from Europe (+2.4%) and overseas (+3.0%). In recent years, the airport has continuously modernised and expanded its infrastructure and opened a new general aviation terminal in 2011. For 2013, the airport expects a small increase in the number of passengers and a slight shrinkage in freight traffic.

Amsterdam remains one of Europe’s major conference and event destinations

Amsterdam: International Conference & Exhibition Demand

Source: RAI

0

20

40

60

80

100

120

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Num

ber o

f Eve

nts

Amsterdam’s main conference centre is the RAI complex, which is located in the Zuidas (South Axis) business district. It is now one of the Europe’s busiest exhibition and conference centres, and has welcomed over 90 million visitors since it was opened in 1961. Each year the venue hosts some 600 events and attracts about 1.5 million visitors. The venue is therefore a major demand generator for the local hotel industry. Amsterdam is also an important city for trade shows, the largest being the Auto Rai, a biannual motor show, hosted in the Amsterdam RAI. The fair attracted about 270,000 visitors in 2011. In November 2012 it was announced that the AutoRAI 2013 would be cancelled due to the economic crisis and lack of applications from car importers. Another major trade show is the Huishoudbeurs, one of the largest consumer goods fairs, hosted annually and attracted around 250,000 visitors in 2012. In the global ranking by the International Congress and Convention Association (ICCA), Amsterdam achieved 10th place with 122 meetings in 2012. This reflected a significant improvement from 114 events held in 2011. The ICCA ranking relates to events attended by at least 50 participants, organised on a regular basis and moving between at least three different countries. In 2013, we expect the MICE segment to struggle in light of the absence of the AutoRAI and a weak economy. This will likely impact the 4 and 5-star hotels where about 86% of the corporate meetings are generally held according to the Amsterdam Tourism & Convention Board (ATCB). Some of this loss in demand is expected to be offset by various cultural events such as the 400th anniversary of the canals and the 125th anniversary of the city’s concert hall and the reopening of some of the most renowned museums.

6 Hotel Intelligence: Amsterdam

A growing number of overseas visitors

Hotels in 3- and 4-star category take up major share

Amsterdam: Graded Hotel Supply (2012)

Grade Hotels Rooms % Of Total 5 star 12 2,982 12% 4 star 55 8,819 36% 3 star 105 7,372 30% Other 226 5,043 21% Total 398 24,216 100%

Source: Amsterdamse bureau voor onderzoek en statistiek, Jones Lang LaSalle

Amsterdam tourism sector benefits from a balanced mix of both leisure and business demand. Especially the leisure segment has grown in importance with foreign visitation accounting for a majority of total overnight stays and arrivals in the capital. Recent research also revealed that a growing amount of visitors to Amsterdam are attaching an increasing importance to the city’s range of cultural offerings. Emerging markets have also boosted arrivals with the city witnessing a growing amount of visitors coming from the so called BRIC (Brazil, Russia, India and China) countries. In 2013, we expect tourism demand to remain stable despite difficult economic condition. Business demand will likely come under pressure especially in light of the absence of the Auto Rai, being one of the leading trade fairs in Amsterdam. Some of these losses are, however, expected to be compensated by an increase in leisure visitors. In the long term, Amsterdam’s visitor profile is expected to change significantly due a growing amount of visitors from emerging economies, in particular Asia and South America. These often young and affluent visitors will very likely put Amsterdam on top of their agenda when travelling to Europe. Tourism demand is therefore anticipated to further grow over the coming years.

There are currently 398 graded hotels in Amsterdam, comprising about 24,000 rooms. The market is dominated by 4-star and 3-star hotels, which represent 66% of total hotel bed supply. Various large international operators have entered the Amsterdam hotel market and about 70% of total hotel room stock is branded. This is relatively high in comparison to other major European cities. Graded hotel room supply in the Dutch capital has grown at a CAAG of 3.5% over the last 10 years. Growth has picked up in recent years, increasing by a CAAG rate of 4.5% between 2007 and 2012. A number of these projects were redevelopments of existing buildings and office to hotel conversions. In 2012, a large number of hotels opened in the 3 and 4 star segment. Major operators such as the Carlson Rezidor Hotel Group and the InterContinental Hotel Group (IHG) expanded their presence in the capital thereby enhancing the number of internationally branded hotels in the city.

F = forecast Source: Jones Lang LaSalle

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

Tota

l Roo

ms

Developments Existing

Amsterdam: Graded Hotel Supply

InterContinental Amstel Amsterdam

Hotel Intelligence: Amsterdam 7

1st Hyatt Place to enter the market in 2013

Amsterdam: Hotel developments (as at February 2013)

Hotel Location Rooms Grade Date Operator

Recently Opened

Holiday Inn Express Sloterdijk railway station 254 3 Q1 2012 IHG

Fletcher Hotel "Foodstrip" - Southeast 120 4 Q3 2012 Fletcher Hotel Group

Park Inn Schiphol 150 4 Q3 2012 Carlson Rezidor

Ramada Apollo Amsterdam Centre Staalmeesterslaan 410 446 4 Q3 2012 Apollo Hotels & Resorts

Andaz Amsterdam Prinsengracht 122 4 Q3 2012 Aedes Real Estate

Meininger Hotel Amsterdam City West Orlyplein 1-67 219 3 Q3 2012 Meininger Hotels

Golden Tulip Amsterdam West Molenwerf 1 206 4 Q3 2012 Louvre Hotels

Holiday Inn Express Amsterdam South Zwaansvliet 20 80 3 Q3 2012 IHG

Hotel Sir Albert Albert Cuyp 2-6 90 4 Q3 2012 Independent

Total Rooms Under Construction 2012 1057

New Developments 2013 art'otel Central Station 107 4 Q2 2013 Carlson Rezidor

Hyatt Place Amsterdam Airport Schiphol Airport 330 3 Q4 2013 Hyatt

Hampton by Hilton Schiphol Airport 172 3 Q3 2013 Hilton

Courtyard by Marriott Atlas Park Arena Football Stadium 169 4 Q3 2013 Marriott

Room Mate Westerdokseiland Ijdock 293 3 Q3 2013 Room Mate

Total Rooms Under Construction 2013 1071

New Developments 2014 Waldorf Astoria Herengracht 94 5 Q1 2014 Waldorf

Park Inn by Radisson La Guardiaweg, 3-5 478 4 Q3 2014 Carlson Rezidor

Holiday Inn South East 95 4 Q3 2014 IHG

Holiday Inn Express South East 345 2 Q3 2014 IHG Staybridge Suites Valkenburgerstraat 14 - 16 80 3 Q3 2014 IHG

Total Rooms Under Construction 2014 1092

New Developments 2015

Motel One Zuidas district 280 3 Q3 2015 Motel One

Hilton Amsterdam Airport Schiphol Schiphol Airport 433 5 Q3 2015 Hilton

Total Rooms Under Construction 2015 924 Source: Jones Lang LaSalle

Hyatt Regency City Centre 211 2015 Hyatt

Being a major gateway destination in Europe Amsterdam remains a top priority for many international hotel operators. Room supply is expected to continue to grow with the majority of new supply being internationally branded and positioned in the upscale segment. Park Plaza for example will enter the market with its lifestyle brand art’otel in Summer 2013 and Motel One with its first Dutch hotel at the beginning of 2015. Hyatt is also increasing its presence with the opening of a 330 room Hyatt Place (the first in Europe) by the end of 2013 and announced plans to open a 211 room Hyatt Regency in 2015. The hotel chain recently opened the 5-star 122 bedroom Andaz, on the Prinsengracht in central Amsterdam. If all hotel projects are realised Amsterdam is expected to see 10 hotel openings between 2013 and 2014, reflecting a room stock increase of 8%.

Hyatt Place - opening end of 2013

8 Hotel Intelligence: Amsterdam

No RevPAR growth in 2012

Amsterdam Upscale Segment: Hotel Trading Performance

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Occupancy 76.1% 71.5% 74.9% 78.5% 81.1% 78.5% 70.2% 66.5% 75.4% 75.4% 76.8%

ARR (€) 172.34 158.68 153.88 158.83 168.09 174.43 175.51 148.42 156.89 169.06 165.14

RevPAR (€) 131.08 113.68 115.28 124.72 136.32 136.86 123.24 98.68 118.24 127.40 126.77

RevPAR Growth (%) -3.1% -13.3% 1.4% 8.2% 9.3% 0.4% -10.0% -19.9% 19.8% 7.7% -0.5%

Inflation 3.9% 2.2% 1.4% 1.5% 1.7% 1.6% 2.5% 1.2% 1.3% 2.3% 2.5%

ARR 2012 values (€) 206.38 185.93 177.82 180.83 188.17 192.19 188.66 157.65 164.51 173.29 165.14

RevPAR 2012 values (€) 156.97 133.20 133.21 141.99 152.60 150.80 132.48 104.82 123.98 130.59 126.77 Source: STR Global

Amsterdam: Quality Hotel Trading

0%

20%

40%

60%

80%

100%

50

70

90

110

130

150

170

190

210

230

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Occ

upan

cy

€(2

012

valu

es)

ARR 2012 values (€) Yield 2012 values (€) Occupancy

Source: STR Global

Hotel performance in the upscale segment suffered significantly in 2008 and 2009 due to the global and domestic economic crisis that also had a negative impact on tourism demand. Occupancy levels fell to 66.5% by year-end 2009, the lowest experienced in the millennium. Room yield fell by 19.9% at year-end 2009. In 2010, upscale hotel performance showed a strong recovery from the economic downturn, with hotels posting a 19.8% increase in room yield compared to 2009. The improvement was backed by a 13.3% growth in occupancy and a 5.7% rise in average room rates. Amsterdam’s well-diversified demand mix is a key factor in the city’s resilience during the crisis, allowing demand to quickly bounce back. Growth in hotel performance continued into 2011, with average room yield increasing by 7.7% compared to 2010. This was due to a 7.7% increase in average room rates, while occupancy remained stable at 75.4%. In 2012, hotel demand continued growing despite a strong supply growth and occupancy increased from 75.4% in 2011 to 76.8%. However, RevPAR remained flat (-0.5%) due to a 2.3% decline in ADR. Historically demand has been price sensitive, however, the future arrival of true luxury hotels is likely to fuel ADR growth.

Upscale Hotels: Amsterdam Year to date Trading 2013

April 2012 2013 % Change

Average Occupancy 67% 71% 5.2%

ADR (€) 155.89 156.16 0.2%

RevPAR 104.60 110.25 5.4%

Source: STR Global

Despite experiencing flat performance results in 2012, Amsterdam’s upscale hotel market has fared considerably well during the first four months of 2013. During this period, major events fuelled hotel demand such as the inauguration of Dutch King Willem Alexander on 30 April 2013. As a result upscale hotels in the capital posted a 5.2% increase in occupancy, boosting RevPAR by 5.4% year on year. It must be noted, however, that the wider Amsterdam’s hotel market has been much more vulnerable to the difficult economic circumstances and growth in hotel supply. Performance results in the overall market have been negative at YTD April 2013 with RevPAR down by 1.4%, when compared to the same time period last year.

General Market: Year to date Trading 2013

April 2012 2013 % Change

Average Occupancy 68% 68% 0.3%

ADR (€) 123.64 121.58 -1.7%

RevPAR 84.20 83.04 -1.4%

Source: STR Global

The table below shows the evolution of trading in Amsterdam in real terms. Average occupancy in the last five years was 1.1% lower than in the last 10 years. This, however, was primarily due to very weak results during the crisis years of 2008 and 2009. Despite several years of positive results, the real change in room yield was negative over both periods.

Amsterdam Trading Growth Rates

2002-2012 2007-2012

Average Occupancy 75.0% 73.8%

ARR CAAG (2012 values) -2.2% -3.0%

RevPAR CAAG (2012 values) -2.1% -3.4%

Source: STR Global

Hotel Intelligence: Amsterdam 9

Source: STR Global

Amsterdam: RevPAR Seasonality

0

40

80

120

160

200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

€

2010 2011 2012

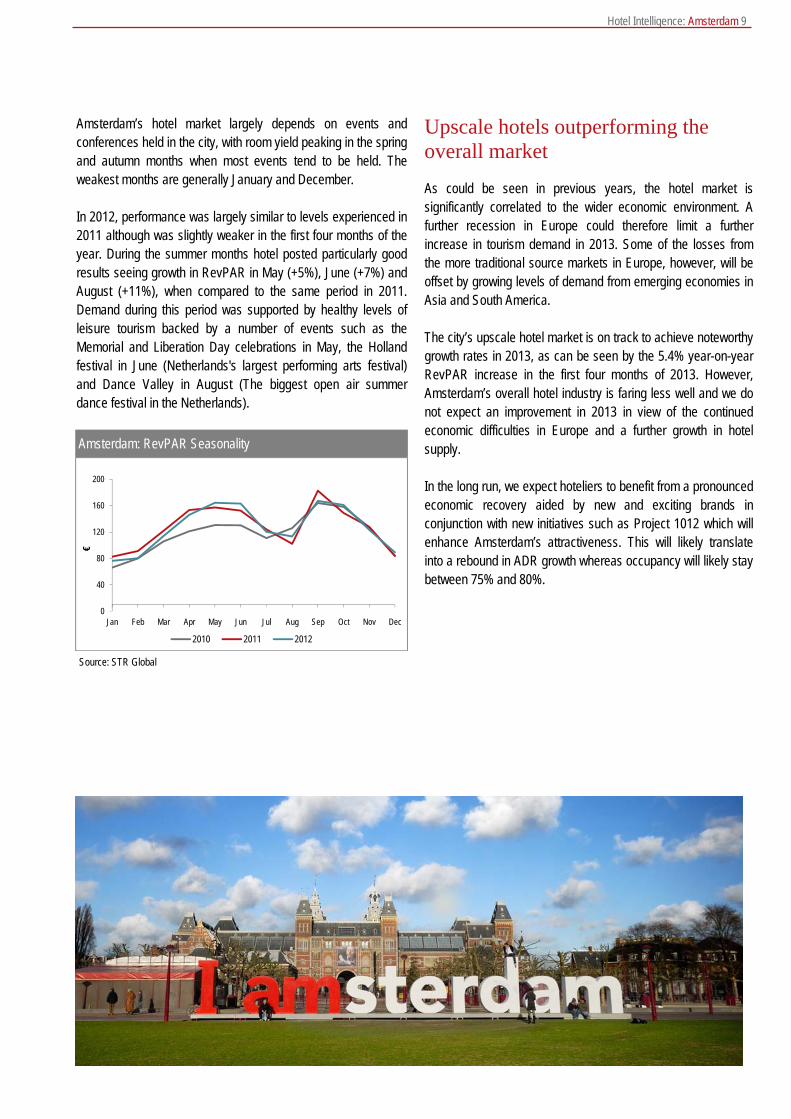

Amsterdam’s hotel market largely depends on events and conferences held in the city, with room yield peaking in the spring and autumn months when most events tend to be held. The weakest months are generally January and December. In 2012, performance was largely similar to levels experienced in 2011 although was slightly weaker in the first four months of the year. During the summer months hotel posted particularly good results seeing growth in RevPAR in May (+5%), June (+7%) and August (+11%), when compared to the same period in 2011. Demand during this period was supported by healthy levels of leisure tourism backed by a number of events such as the Memorial and Liberation Day celebrations in May, the Holland festival in June (Netherlands's largest performing arts festival) and Dance Valley in August (The biggest open air summer dance festival in the Netherlands).

Upscale hotels outperforming the overall market

As could be seen in previous years, the hotel market is significantly correlated to the wider economic environment. A further recession in Europe could therefore limit a further increase in tourism demand in 2013. Some of the losses from the more traditional source markets in Europe, however, will be offset by growing levels of demand from emerging economies in Asia and South America. The city’s upscale hotel market is on track to achieve noteworthy growth rates in 2013, as can be seen by the 5.4% year-on-year RevPAR increase in the first four months of 2013. However, Amsterdam’s overall hotel industry is faring less well and we do not expect an improvement in 2013 in view of the continued economic difficulties in Europe and a further growth in hotel supply. In the long run, we expect hoteliers to benefit from a pronounced economic recovery aided by new and exciting brands in conjunction with new initiatives such as Project 1012 which will enhance Amsterdam’s attractiveness. This will likely translate into a rebound in ADR growth whereas occupancy will likely stay between 75% and 80%.

Hotel Intelligence: Amsterdam

This report is confidential to the recipient of the report. No reference to the report or any part of it may be published in any document, state-ment or circular or in any communication with third parties without the prior written consent of Jones Lang LaSalle, including specifically in relation to the form and context in which it will appear. We stress that forecasting is a problematical exercise which at best should be regarded as an indicative assessment of possibilities rather than absolute certainties. The process of making forward projections involves assumptions in respect of a considerable number of varia-bles which are acutely sensitive to changing conditions, variations in any one of which may significantly affect the outcome and we draw your attention to this factor. Jones Lang LaSalle makes no representation, warranty, assurance or guarantee with respect to any material with which this report may be issued and this report should not be taken as an endorsement of or recommendation on any participation by any intending investor or any other party in any transaction whatsoever. This report has been produced solely as a general guide and does not constitute advice. Users should not rely on this report and must make their own enquiries to verify and satisfy themselves of all aspects of information set out in the report. We have used and relied upon information from sources generally regarded as authoritative and reputable, but the information obtained from these sources may not have been independently verified by Jones Lang LaSalle. Whilst the material contained in the report has been prepared in good faith and with due care, no representation or warranty is made in relation to the accuracy, currency, completeness, suitability or otherwise of the whole or any part of the report. Jones Lang LaSalle Hotels, its officers, employees, subcontractors and agents shall not be liable (to the extent permitted by law) to any person for any loss, liability, damage or expense (‘liability’) arising directly or indirectly from or connected in any way with any use of or reliance on this report. If any liability is established, notwithstanding this exclusion, it shall not exceed $1,000.

12 Hotel Intelligence: Amsterdam

AMERICAS

Atlanta

Buenos Aires Chicago

Dallas Denver

Los Angeles Mexico City

Miami New York

San Francisco Sao Paulo

Washington DC

EMEA

Barcelona

Dubai Dusseldorf

Exeter Frankfurt

Glasgow Istanbul

Leeds London

Lyon Madrid

Manchester

ASIA

Bangkok

Chengdu Jakarta

New Delhi Peking

Shanghai Singapore

Tokyo

ANZ

Auckland

Brisbane Melbourne

Perth Sydney

Marseille

Milan Moscow

Munich Paris

Rome

Our domestic & global reach Hotels & Hospitality

George Nicholas Executive Vice President Hotel Investment Sales +44 20 7399 5829 [email protected]

Daniel O’Connor Vice President Hotel Investment Sales +44 20 7399 5803 [email protected]

Larissa Esser Associate Hotel Investment Sales +44 20 7399 5067 [email protected]

Jake Egberts Senior Vice President Hotel Valuations +44 20 7399 5673 [email protected]

Our dedicated team & expertise:

www.jll.com/hospitality | www.jllhotels.nl

COPYRIGHT © JONES LANG LASALLE IP, INC. 2013

LONDON 30 Warwick Street W1B 5NH United Kingdom

Katleen Van den Brande Vice President Hotel Valuations +44 20 7399 5941 [email protected]