Hotelia - Market Overview 2015

27

Norwegian Hotel Industry Hotelia’s mid-year report 2015

-

Upload

geir-lundkvist -

Category

Documents

-

view

64 -

download

6

Transcript of Hotelia - Market Overview 2015

Norwegian Hote l Indus t ryHote l i a ’s mid-yea r repor t 2015

Norwegian Hotel Industry Overview | Pg. 2

TABLE OF CONTENTS

1. Introduction……………………………………………………

2. Hotel Industry Performance in the Major Cities……………..

Norway

Oslo

Bergen

Trondheim

Gardermoen (Ullensaker)

Stavanger

Tromsø

Kristiansand

3. Norwegian Hotel Industry in General………………………...

4. Colliers International Mid-year Real Estate Report…………..

5. Highlights from 2015 & 2016………………………………...

…4

…5

21

22

23

Advisory services and business development for hotels, hotel

property owners and the travel industry

Behind Hotelia stands a team of experienced consultants with a long track record from hotel real estate and operations

Services provided by Hotelia include feasibility studies, hotel market research reports, transactions, valuations, operator searches and general advisory services to hotel and travel industry clients

We are specialized in the Nordic region, and base our advices on a wide experience and extensive network from this region

WH

O A

RE

WE

?

Norwegian Hotel Industry Overview | Pg. 4

INTRODUCTION

Hotelia releases a brief market report about the Norwegian hotel industry twice a year, and is draftedduring the two months prior to publication. The majority of data are collected from Statistics Norway(SSB) and Statistikknett. Hotelia have supplied additional data as well.

The main focus of this report is:

Development in the Norwegian hotel industry up to, and including, mid-year 2015 for Norway

and the seven largest cities (based on sold room nights)

Updated overview of the largest hotel chains in Norway, based on number of rooms and hotels

Important events and highlights in the Norwegian hotel industry and real estate market, as wellas highlights from the Swedish market that is of interest for Norwegian investors

A quote from Colliers International’s mid-year report for the Norwegian real estate market, with

link to the entire report

Some reflections of the industry’s outlook in the coming year

The next report is scheduled in February 2016. Please do not hesitate to contact us for furtherinformation, comments or suggestions.

Hotelia AS has conscientiously prepared this report based on our own analyses and the information made available to us or collected during the process of executing the assignment. Hotelia AS can therefore not guarantee for the accurateness or trueness of all the information and estimates carried out in this report.

HOTEL PERFORMANCE

IN THE MAJOR CITIES

Statistikk for Oslo

Norwegian Hotel Industry Overview | Pg. 6

NORWAY

A slightly higher increase in demand than in room capacity, and a moderate growth in ADR contributes toa 1.8% growth in RevPAR this mid-year compared to first half-year 2014.

There are primarily a strong growth in the leisure segment. The growth’s main drivers are a combinationof the currently depreciated NOK, improvements in selected countries’ economy that are important forthe Norwegian tourist industry, and the popularity of northern lights (new winter market).

USD: -21.9% | EUR: -5.4% | GBP: -15.6%

The business segment in total, including conference, decreased by 0.7% compared to first half-year 2014.

Thus, the fall is so far relatively smaller compared to the fall in oil prices and the overall development inthe Norwegian economy.

In total, Norway has experienced an increase in both domestic and foreign travellers by 4.2% and 9.8%respectively compared to first half-year 2014.

13.4 %

-3.1 %

6.6 %

Guest segments development mid-year 2014 vs. 2015

Leisure

Business

Conference

-4%

-2%

0%

2%

4%

300

350

400

450

500

550

600

650

Rolling 12 month RevPAR with %-change

NOK 2014 2015 Nominel chg. Change %

Leisure 4 220 706 4 786 564 565 858 13.4 %

Business 3 934 608 3 811 540 -123 068 -3.1 %

Conference 1 322 293 1 409 186 86 893 6.6 %

Room cap. 13 107 685 13 589 534 481 849 3.7 %

Room nights 6 743 591 7 009 299 265 708 3.9 %

ADR 896 910 13 1.5 %

Occ% 51.4 % 51.6 % 0.1 % 0.3 %

RevPAR 461 469 8 1.8 %

2008 2009 2010 2011 2012 2013 2014 2015

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1 000

1 200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Development in key figures - Norway

ADR RevPAR Occ% Average Occ%

*First half-year 2014 vs. half-year 2015

NORWEGIAN HOTEL INDUSTRY OVERVIEW

Hotelia | Pg. 7

Oslo

Astrup Fearnley+9.1%

Growth in RevPAR

Statistikk for Oslo

Norwegian Hotel Industry Overview | Pg. 8

OSLO

-4%

-2%

0%

2%

4%

300

400

500

600

700

800

Rolling 12 month RevPAR with %-change

500

550

600

650

700

750

-

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15

Yearly rolling 12 month RevPAR & room cap.

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1 000

1 200

1 400

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Development in key figures - Oslo

ADR RevPAR Occ% Average Occ%

Overall we see a weak trend change in RevPAR development. The demand side is at the moment slightlygreater than the supply side.

The strong development in June Is mainly dominated by the “Nor-Shipping trade” fair. This also affectsthe total figures for Oslo in the first half

Oslo continues to grow business from the leisure market by 12.8 %. During the last ten years thenumber of guests from this segment has increased by 70 %

Regardless of «Nor-Shipping», price development (ADR ) is positive so far

There are no major projects coming into the market this year, and the pipeline of additional roomcapacity is low

NOK 2014 2015 Nominel chg. Change %

Leisure 793 923 895 602 101 679 12.8 %

Business 865 556 901 410 35 854 4.1 %

Conference 200 622 224 856 24 234 12.1 %

Room cap. 2 047 520 2 183 196 135 676 6.6 %

Room nights 1 354 730 1 460 416 105 686 7.8 %

ADR 901 972 71 7.9 %

Occ% 66.2 % 66.9 % 0.7 % 1.1 %

RevPAR 596 650 54 9.1 %

2008 2009 2010 2011 2012 2013 2014 2015

RevPARRoom cap.

*First half-year 2014 vs. half-year 2015

NORWEGIAN HOTEL INDUSTRY OVERVIEW

Hotelia | Pg. 9

Bergen

-12.9%Growth in RevPAR Bryggen

Statistikk for Oslo

Norwegian Hotel Industry Overview | Pg. 10

BERGEN

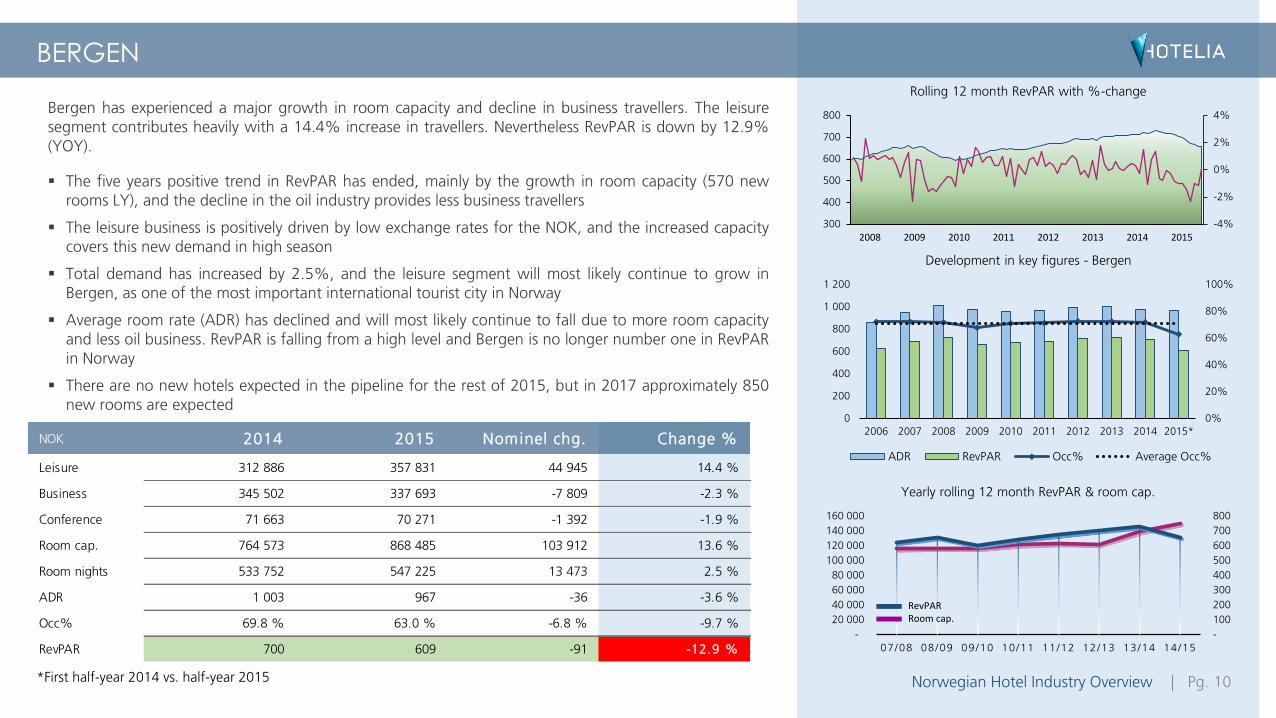

Bergen has experienced a major growth in room capacity and decline in business travellers. The leisuresegment contributes heavily with a 14.4% increase in travellers. Nevertheless RevPAR is down by 12.9%(YOY).

The five years positive trend in RevPAR has ended, mainly by the growth in room capacity (570 new

rooms LY), and the decline in the oil industry provides less business travellers

The leisure business is positively driven by low exchange rates for the NOK, and the increased capacitycovers this new demand in high season

Total demand has increased by 2.5%, and the leisure segment will most likely continue to grow inBergen, as one of the most important international tourist city in Norway

Average room rate (ADR) has declined and will most likely continue to fall due to more room capacityand less oil business. RevPAR is falling from a high level and Bergen is no longer number one in RevPARin Norway

There are no new hotels expected in the pipeline for the rest of 2015, but in 2017 approximately 850new rooms are expected

-4%

-2%

0%

2%

4%

300

400

500

600

700

800

Rolling 12 month RevPAR with %-change

-

100

200

300

400

500

600

700

800

-

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15

Yearly rolling 12 month RevPAR & room cap.

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1 000

1 200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Development in key figures - Bergen

ADR RevPAR Occ% Average Occ%

NOK 2014 2015 Nominel chg. Change %

Leisure 312 886 357 831 44 945 14.4 %

Business 345 502 337 693 -7 809 -2.3 %

Conference 71 663 70 271 -1 392 -1.9 %

Room cap. 764 573 868 485 103 912 13.6 %

Room nights 533 752 547 225 13 473 2.5 %

ADR 1 003 967 -36 -3.6 %

Occ% 69.8 % 63.0 % -6.8 % -9.7 %

RevPAR 700 609 -91 -12.9 %

2008 2009 2010 2011 2012 2013 2014 2015

RevPARRoom cap.

*First half-year 2014 vs. half-year 2015

Trondheim

-10.2%Growth in RevPAR

Statistikk for Oslo

Norwegian Hotel Industry Overview | Pg. 12

TRONDHEIM

Trondheim continues to experience more demand from conference as well as the leisure segment.Additional room capacity continues to grow in Trondheim, including the shortfall in business travellers

causes RevPAR to fall by 10.2%.

The increase in room capacity started in 2010 and continues to grow by 11.5% in 2015.

Increase in demand is not making up for the additional rooms. RevPAR trend since 2011 is fallingheavily – from 553,- in 2011 to 475,- in 2015 (-14.1%)

There is no new projects expected into the market in 2015/2016

-4%

-2%

0%

2%

4%

300

350

400

450

500

550

600

650

Rolling 12 month RevPAR with %-change

420

440

460

480

500

520

540

560

-

20 000

40 000

60 000

80 000

100 000

120 000

08/09 09/10 10/11 11/12 12/13 13/14 14/15

Yearly rolling 12 month RevPAR & room cap.

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1 000

1 200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Development in key figures - Trondheim

ADR RevPAR Occ% Average Occ%

NOK 2014 2015 Nominel chg. Change %

Leisure 174 388 201 888 27 500 15.8 %

Business 232 386 216 254 -16 132 -6.9 %

Conference 71 823 81 573 9 750 13.6 %

Room cap. 579 125 645 567 66 442 11.5 %

Room nights 350 755 359 936 9 181 2.6 %

ADR 818 797 -20 -2.5 %

Occ% 60.6 % 55.8 % -4.8 % -7.9 %

RevPAR 495 445 -51 -10.2 %

2008 2009 2010 2011 2012 2013 2014 2015

RevPARRoom cap.

*First half-year 2014 vs. half-year 2015

Gardermoen

+12.2%Growth in RevPAR New Terminal

Statistikk for Oslo

Norwegian Hotel Industry Overview | Pg. 14

GARDERMOEN (MUNICIPALITY: ULLENSAKER)

The majority of the huge expansion of new capacity, launched in 2008-2011, is now absorbed by theincreased demand. This is driven by both ADR and occupancy rate.

Gardermoen continues to grow their business and achieved the highest increase in RevPAR comparedto the 7 largest hotel destinations in Norway

We assume that the increase in the conference segment comes from the newly opened «The Cube» atClarion Hotel in august 2014. Thon Hotels has also newly opened a new congress hall close to their

operations at Gardermoen

There are no additional room capacity expected in the coming 2-3 years at Gardermoen

-4%

-2%

0%

2%

4%

300

350

400

450

500

550

600

650

Rolling 12 month RevPAR with %-change

-

100

200

300

400

500

600

700

-

20 000

40 000

60 000

80 000

100 000

120 000

07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15

Yearly rolling 12 month RevPAR & room cap.

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1 000

1 200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Development in key figures - Gardermoen

ADR RevPAR Occ% Average Occ%

NOK 2014 2015 Nominel chg. Change %

Leisure 164 503 186 778 22 275 13.5 %

Business 197 051 169 426 -27 625 -14.0 %

Conference 85 230 110 348 25 118 29.5 %

Room cap. 582 351 570 771 -11 580 -2.0 %

Room nights 331 750 341 981 10 231 3.1 %

ADR 816 871 54 6.7 %

Occ% 57.0 % 59.9 % 2.9 % 5.2 %

RevPAR 465 522 57 12.2 %

2008 2009 2010 2011 2012 2013 2014 2015

RevPARRoom cap.

*First half-year 2014 vs. half-year 2015

Stavanger

-28.1%Growth in RevPAR

Vågen

Statistikk for Oslo

Norwegian Hotel Industry Overview | Pg. 16

STAVANGER

Stavanger, “The Oil Capital”, is facing the most dramatic downturn of all the Norwegian cities. RevPARdown by 28.1%. The business segment is heavily hit by the oil price and the restricted travel policy in the

oil industry.

The city of Stavanger sold only 1.8% fewer room nights than LY, but the 25% additional new room

capacity made the shift and lowered the occupancy rate by 14% points

Average rate down by 8.7%, mainly due to lack of business travellers and lower paying business fromthe leisure and conference segments

Downturn in the oil sector and the effect of more room capacity in the Stavanger region was partlycovered in Stavanger city by visitors who previously stayed in hotels in the neighbouring cities of

Sandnes, Forus and Sola

Conference segment picking up slowly, but far behind the volume that Oslo, Bergen and Trondheimmanaged to sell

There are still several hotels planned in the pipeline for 2016, approximately 485 new rooms, yet

several projects are put on hold

-5%

-3%

-1%

1%

3%

5%

300

400

500

600

700

800

Rolling 12 month RevPAR with %-change

-

100

200

300

400

500

600

700

800

-

20 000

40 000

60 000

80 000

100 000

120 000

07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15

Yearly rolling 12 month RevPAR & room cap.

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1 000

1 200

1 400

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Development in key figures - Stavanger

ADR RevPAR Occ% Average Occ%

NOK 2014 2015 Nominel chg. Change %

Leisure 124 394 147 209 22 815 18.3 %

Business 242 344 209 282 -33 062 -13.6 %

Conference 21 434 37 787 16 353 76.3 %

Room cap. 473 263 590 228 116 965 24.7 %

Room nights 312 283 306 798 -5 485 -1.8 %

ADR 1 091 996 -95 -8.7 %

Occ% 66.0 % 52.0 % -14.0 % -21.2 %

RevPAR 720 518 -202 -28.1 %

2008 2009 2010 2011 2012 2013 2014 2015

RevPARRoom cap.

*First half-year 2014 vs. half-year 2015

Tromsø

-10.5%Growth in RevPAR

Tromsø Bridge

Statistikk for Oslo

Norwegian Hotel Industry Overview | Pg. 18

TROMSØ

Tromsø has for years had a strong market growth, but in recent years the substantial increase in capacityhas provided a drop in RevPAR. The city is now back at a level close to the level in 2010 when the positive

development started.

Still a solid increase of the leisure segment. Tromsø has experienced a growth of 250 % in leisure segment since 2007 – mainly caused by the popularity of northern lights

Since 2007 the room capacity has doubled

Compared to the massive increase in capacity over the years , the prices (ADR) are only showing a

minor drop in the same period

New hotels in the pipeline, approximately 250 rooms in 2015/2016, plus some projects that are not yet confirmed

-4%

-3%

-2%

-1%

0%

1%

2%

3%

300

350

400

450

500

550

600

650

Rolling 12 month RevPAR with %-change

460

480

500

520

540

560

580

600

620

-

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15

Yearly rolling 12 month RevPAR & room cap.

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1 000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Development in key figures - Tromsø

ADR RevPAR Occ% Average Occ%

NOK 2014 2015 Nominel chg. Change %

Leisure 152 924 191 683 38 759 25.3 %

Business 132 000 123 994 -8 006 -6.1 %

Conference 48 967 48 432 -535 -1.1 %

Room cap. 340 312 407 483 67 171 19.7 %

Room nights 233 418 257 626 24 208 10.4 %

ADR 887 862 -25 -2.9 %

Occ% 68.6 % 63.2 % -5.4 % -7.8 %

RevPAR 609 545 -64 -10.5 %

2008 2009 2010 2011 2012 2013 2014 2015

RevPARRoom cap.

*First half-year 2014 vs. half-year 2015

Kristiansand

-5.6%Growth in RevPAR Bølgen Hall of Culture

Statistikk for Oslo

Norwegian Hotel Industry Overview | Pg. 20

KRISTIANSAND

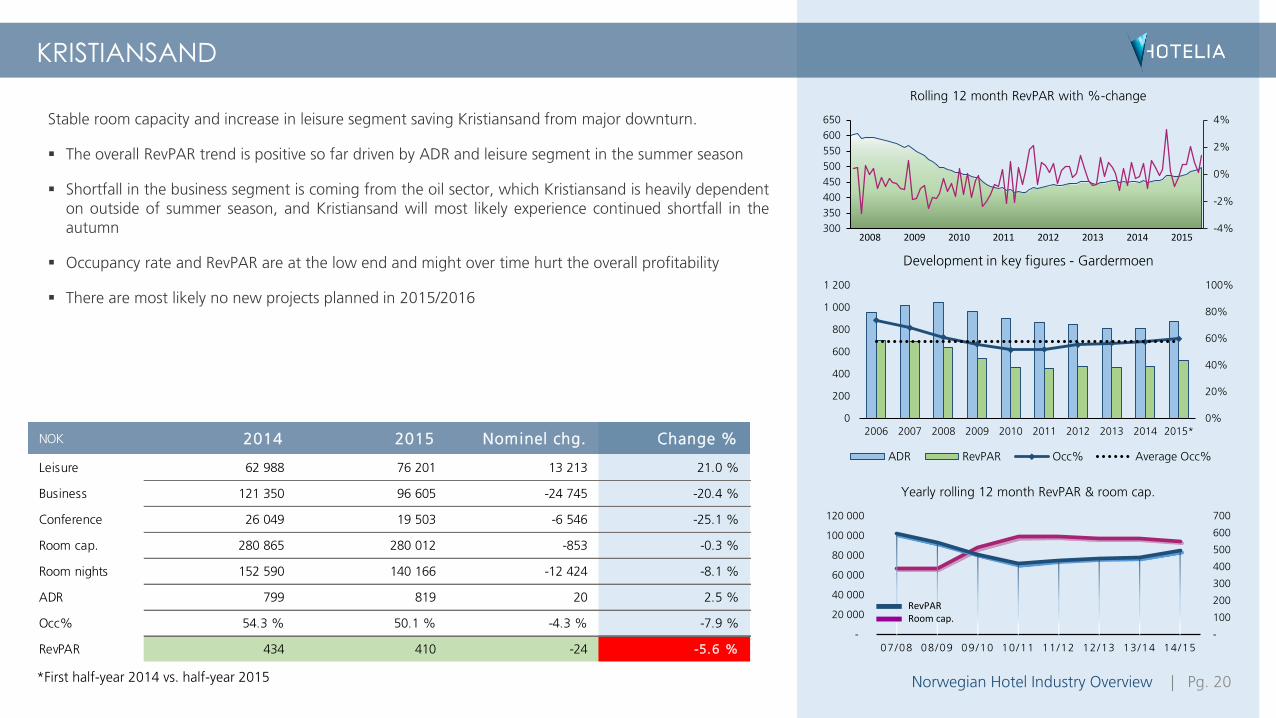

Stable room capacity and increase in leisure segment saving Kristiansand from major downturn.

The overall RevPAR trend is positive so far driven by ADR and leisure segment in the summer season

Shortfall in the business segment is coming from the oil sector, which Kristiansand is heavily dependenton outside of summer season, and Kristiansand will most likely experience continued shortfall in theautumn

Occupancy rate and RevPAR are at the low end and might over time hurt the overall profitability

There are most likely no new projects planned in 2015/2016

NOK 2014 2015 Nominel chg. Change %

Leisure 62 988 76 201 13 213 21.0 %

Business 121 350 96 605 -24 745 -20.4 %

Conference 26 049 19 503 -6 546 -25.1 %

Room cap. 280 865 280 012 -853 -0.3 %

Room nights 152 590 140 166 -12 424 -8.1 %

ADR 799 819 20 2.5 %

Occ% 54.3 % 50.1 % -4.3 % -7.9 %

RevPAR 434 410 -24 -5.6 %

-4%

-2%

0%

2%

4%

300

350

400

450

500

550

600

650

Rolling 12 month RevPAR with %-change

-

100

200

300

400

500

600

700

-

20 000

40 000

60 000

80 000

100 000

120 000

07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15

Yearly rolling 12 month RevPAR & room cap.

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1 000

1 200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Development in key figures - Gardermoen

ADR RevPAR Occ% Average Occ%

2008 2009 2010 2011 2012 2013 2014 2015

RevPARRoom cap.

*First half-year 2014 vs. half-year 2015

21 Hotels

5,600 Rooms

10 Hotels

2,940 Rooms

19 Hotels

2,650 Rooms

26 Hotels

1,500 Rooms

8 Hotels

780 Rooms

6 Hotels

1,350 Rooms

15,000 9,000 3,000 Number of rooms

Num

ber

of

room

s3,0

00

9,0

00

15,0

00

25 Hotels

2,500 Rooms

35 Hotels

6,430 Rooms

Norwegian Hotel Industry Overview | Pg. 21

NORWEGIAN HOTEL INDUSTRY IN GENERAL

In contrast to the popularity of management agreements in international hotel firms, Scandinavian hotel property owners favours rental agreements – often with one of the major brands

Scandic, Thon and Choice (consisting of Quality, Clarion, Clarion Collection and Comfort) dominates the industry

The hotels are mostly based in the mid-market, however the major brands diversify across all three markets

Figure updated September 2015

Norwegian Hotel Industry Overview | Pg. 22

COLLIERS – PROPERTY BROKERAGE

The Norwegian Commercial Real Estate market will see an all time high year in terms of transaction revenue. As of mid August, the total volume is

already close to NOK 65 bn with the office and retail sector being

responsible for over 2 / 3rds of the total. The interest in the Norwegian Commercial Real Estate market is very strong as Norwegian investors are

as present as ever and international investors are looking for low risk assets for their investments.

We firmly expect this development to continue throughout 2015 and we expect the transaction volume at years end to be approximately NOK 90

bn at a minimum. We would not be surprised if we see transactions for more than NOK 100 bn in 2015. However, for this to happen, certain key transactions have to go well.

The international macro economic climate remains very unstable. The oil price has as of August 24th seen levels as low as $ 43 per barrel and stock exchanges around the world in general, and China especially, is seeing

significant declines. China has been extremely volatile for a prolonged period of time, however, we might begin to see that larger parts of the

rest of the world is now increasingly following suit.

Looking at the domestic picture in Norway, the oil price is indeed of a high concern. The unemployment rate has increased in recent months and

salary growth is expected to be the lowest in 20 years. Norway is one of

the few western countries with quite strong inflation numbers at present with a yearly rate close to 2.5 %.

It is expected that the international and domestic appetite for Norwegian Commercial Real Estate will continue going forward. This is however, uncertain times with drastic changes in international financial markets currently happening each week. With record low interest levels and a very

strong financial backbone, we are hopeful going forward, especially for the transaction market.

Entire report available here.Source: Colliers International Norway

Balder

Acquired a Pandox Hotel portfolio in Sweden, with2,430 rooms in total for 2,200 MSEK

Geir Hove with partners

Acquired Scandic Stavanger City Hotel (226 rooms) from Øgreid Eiendom for 350 MNOK

DNB Scandinavian Property Fund

Acquired Quality Expo (301 rooms) for 530 MNOK, whichgave a yield on 5.2%

Balder

Acquired Courtyard by Mariot (280 rooms) in Stockholm from

Invesco European Hotel Real Estate for 670 MSEK

KLP Eiendom

Acquired a Scandic hotel currently under construction in Copenhagen with 370 rooms

Oslo Pensjonsforsikring

Acquired 58,000 m2 at Ullevål Stadion, including Thon Hotel

Ullevaal Stadion (144 rooms) from DNB Næringseiendom

Merkantilbygg

Acquired Park Inn by Radisson (208 rooms) Stavanger from KLP Eiendom

Other highlights Scandic have acquired the operations of three hotels located in Bergen from Bergen Hotel

Group (630 rooms)

Choice have launched a partner concept for its unbranded concept

Pandox are undergoing large changes – gone public on Stockholm Stock Exchange

Two hotels in Oslo rebranded to HTL (owned by Scandic)

Ligula Hospitality Group acquired Norse Hospitality from Svea Fastigheter / Midstar

Accor Hotel Group canceled 13 contracts with Norse Hospitality – the affected hotels

have been rebranded to Good Morning Hotels

SOME HIGHLIGHTS FROM LAST 12 MONTHS

Norwegian Hotel Industry Overview | Pg. 23

Norwegian Hotel Industry Overview | Pg. 24

OUTLOOK FOR THE REST OF 2015 AND 2016

The hotel industry is a cyclical business. Falling oil prices, rising unemployment and a general uncertainty

contributes to a reduction in travel activity in the private sector. The decline is already apparent in the

major cities of Bergen, Stavanger and Trondheim, as we can see in this report. We expect that these cities

will probably be hit even harder in the autumn and winter. Oslo will probably be affected less by the

decline, while hotels in the outskirt of the largest cities will be hit even harder.

Foreign investors still considers real estate investments in Norway as attractive, low exchange

rate and stability in the country is valuable

The summer season 2015 will be historical good

Further capacity growth in Stavanger and Bergen might cause a continued fall

Low exchange rate will create further growth in the foreign leisure business

The big chains will probably start and continue to “clean up“ in their portfolios of hotels in their own

operations. For landlords outside the main cities and region centers can cause that they have to find new

tenants. This will probably strengthen the position of the multi brand companies.

Anders VatnePartner

+47 926 97 [email protected]

Geir LundkvistPartner

+47 928 87 [email protected]

Hotelia monitors the hotel industry in Norway and the Nordics carefully in order to ensure that our clients are updated with relevant market information. In spite of the fact that there have been a record summer in Norwegian tourism industry, we see many challenges for the industry going forward.

During this summer we in Hotelia have develop new and improved existing products and are ready for a new and exciting fall. Our team Anders Vatne, Geir Lundkvist, Commercial Estate Lawyer Chistoffer Aasebø and market analyst Christian Hagen are ready to assist you.

Please do not hesitate to contact us by phone + 47 41 38 44 33

For more information, please visit our websitewww.hotelia.no

Scandic Flesland Airport - BergenContracted by Hotelia

Hotelia AS | Inkognitogata 33 A | 0256 Oslo | Norway | Tlf. +47 41 38 44 33 | [email protected] | hotelia.no | Org.nr. 998 811 910 MVA