Hotel Report - Fairmas · rates bands from last year’s Hotel Report (June 2014) in order to...

23

Hotel Report In Focus Rate bands – Berlin, Dusseldorf, Munich Edition October 2015 © INFINITY - fotolia.com

Transcript of Hotel Report - Fairmas · rates bands from last year’s Hotel Report (June 2014) in order to...

Hotel Report

In Focus Rate bands – Berlin, Dusseldorf, Munich

Edition October 2015

© INFINITY - fotolia.com

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 2

FairmasHotel Reportin cooperation with SolutionsDotWG

Index

Dear readers, 3

August 2015 in comparison to the previous year 4

Fairmas Trendbarometer 8

In Focus 16

Disclaimer 22

Fairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.com© 2014 Fairmas GmbH/Solutions Dot WG GmbH

Seite | 3

FairmasHotel Reportin cooperation with SolutionsDotWG

Dear readers,

It was a good September in most destinations. Berlin was even able to prove that the absence of a major

trade fair no longer needs to represent a disaster for the hotel industry when all the opportunities for price

increases are exploited. Given this insight, we ask whether this applies across all categories and how the

price range has actually developed since last year. For this purpose we have, together with the Allgemeine

Hotel & Gastronomie-Zeitung (AHGZ), a newspaper for the German hospitality industry, dug out the room

rates bands from last year’s Hotel Report (June 2014) in order to expand the information and update the

figures. Have there actually been any changes, perhaps even improvements? We investigate this question

in depth in our concise analysis.

Besides this, there is our usual focus on the performance of the month just ended, while we also look

forward into the future. The last quarter of 2015 has arrived – what are hoteliers in the major destinations

expecting for the rest of the year?

Enjoy our Hotel Report and have an interesting read.

The team of Fairmas Hotel Report

(Gabriele Kiessling & Nadine Kilian)

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 4

FairmasHotel Reportin cooperation with SolutionsDotWG

September 2015 in comparison to the previous year1

A brief overview of hotel performances at selected German destinations:

1 All the figures (daily collected) quoted are comparisons with those for the previous year, rounded to full amounts Source: Fairmas GmbH/STR Global, Data as of 01.10.2015

Berlin

Occ: 90%, ADR: €116, RevPar: €104

September is generally the best month in Berlin.

This year, however, the “InnoTrans” trade show was

missing. It takes place every two years, regularly

generating very high room rates in the city. A fall in

ADR was thus unavoidable. But the much higher

fall that had originally been expected did not occur.

The IFA, HAI and CMS trade fairs, as well as the

Marathon weekend all developed very well. There

was also business group and conference sector

trade. The large number of smaller events in the

city should not be underestimated, either. These

included the Pyronale, the EUROBASKET (at the

beginning of September), the “Lollapalooza Festi-

val Tempelhof” (12 to 13 September 2015), as well

as two “U2” concerts (on 24 and 25 September),

and a variety of smaller congresses. So there was

a lot going on in Berlin in September. Thus, it was

no surprise that occupancy could be increased by

almost 4%, despite the absence of the InnoTrans

event. Room rates declined by 3%, though RevPar

still increased by 1%.

Cologne/Bonn

Occ: 77%, ADR: €107, RevPar: €82

The prospects in Cologne/Bonn were not good in

September and the actual figures confirmed the

negative expectations. The Photokina trade fair

is only held every two years and the event was

missing in 2015. That could be felt well before from

the preliminary booking situation and room rates.

In addition, the “spoga + gafa” events shifted

a little further into August. This also pushed the

September ADR downwards. The school sum-

mer holidays were still taking place in September

in some German federal states. The “Kind & Ju-

gend” trade fair and the “dmexco” event, which

were very successful this year, generated short-

term pickup and clearly exceeded expectations

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 5

FairmasHotel Reportin cooperation with SolutionsDotWG

following their surprising success last year. Overall,

however, there was very little corporate business.

In all, there was a 4% decline in occupancy in Co-

logne and Bonn. Room rates fell by as much as

7%. That led to a 11% fall in RevPar.

Dresden

Occ: 79%, ADR: €77, RevPar: €61

September seemed very unpredictable in Dresden

and the forecasts were correspondingly gloomy.

On top of this, there have been major declines

in group trade and many cancellations. But quite

a lot was going on in the city in September. The

Dresden hotels had not been expecting as much

from some of the conventions and conferences.

For example, the specialist medical congress, the

autumn meeting of the “Gesellschaft für Arbe-

itswissenschaft” and the “Interspeech” event were

all successful and generated significant increases

in both occupancy and room rates. The impact of

the Dresdner Oktoberfest was also nothing to be

sneezed at, even if visitors to the city were other-

wise rather cautious, especially at weekends. The

Dresden hotel industry was able to enjoy increases

in all key indicators (Occ: + 2%, ADR: + 2%, Rev-

Par: + 4%)

Dusseldorf

Occ: 75%, ADR: €103, RevPar: €77

The September forecasts for Dusseldorf provided

few grounds for optimism. However, in fact, things

turned out far better than expected. Overall, Rev-

Par increased by 0.7%, the result of the negative

occupancy figures (Occ: -3%) and a 3% increase

in room rates. In the end, the “Expopharm” trade

show and the FIP Congress in the last week of

September (a convention that rotates between

different venues, and which was absent in 2014)

enjoyed far more success than expected. The “Eu-

romold” trade fair, now in Dusseldorf for the first

time after previously being held in Frankfurt, was

also a success.

Frankfurt

Occ: 82%, ADR: €135, RevPar: €110

September generated growth in Frankfurt through

a 15% increase in RevPar, due to the positive room

rate trend (+11%). This year, the “IAA Pkw” trade

show took place (last year had been the turn of

the “Automechanika” event), and it lasted for two

weeks. Although the Automechanika did lead to

higher room rates, the IAA also had a strong influ-

ence due to the days needed to set up and dis-

mantle the show, as well as its longer duration. The

fair was also accompanied by events such as car

presentations. During the same month last year,

the last week of September was not a complete

business week due to the public holiday on 3 Oc-

tober being on a Friday. This year it the public holi-

day falls on a Saturday, so there will be corporate

and conference business during the week. In addi-

tion, the later scheduling of the school holidays this

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 6

FairmasHotel Reportin cooperation with SolutionsDotWG

year has had particularly positive effects (they take

up one week less of September in Bavaria and in

Baden-Württemberg).

Hamburg

Occ: 85%, ADR: €120, RevPar: €103

September in Hamburg was marked by a generally

very poor development (RevPar: -10%), primarily

due to the fall in room rates (ADR: -9%). This year,

the high-priced “SMM” trade show was absent (it

is only held every two years). This was the main

reason for the very high fall in room rates. Besides,

last year also saw the “Wind Energy” trade show,

which is also held every two years. Highlights in

September 2015 included the “Seatrade” fair, as

well as the “Hamburg Cruise Days”, an event

which also took place last year. The later start of

the “Alstervergnügen” event (this time it began in

September) was not enough to compensate for

the lack of the two trade fairs. The two congresses

(the “DGU Kongress” and the „European PC Solar

Energy Conference and Exhibition”, the latter event

held at rotating venues) as well as the reschedul-

ing of the “Alstervergnügen” in September was not

enough to make up for the two absent trade fairs.

Munich

Occ: 86%, ADR: €188, RevPar: €162

September in Munich was much less rosy than last

year. This year, two major congresses were miss-

ing. The early end of Ramadan meant that guests

from the Arab region arrived earlier in July. For the

same reason, they also left earlier. The IBA trade

fair, which takes place only every three years, also

remained well below both expectations and last

year’s congresses. Room rates were thus very low

in both cases. The interim balance for the Oktober-

fest was very disappointing for the organizers, not

only because of the overcast weather. The hotel

industry also felt it. Contrary to expectations, oc-

cupancy fell by 2%. Room rates were down by just

1%. This meant a 3% decline in RevPar in Sep-

tember.

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 7

FairmasHotel Reportin cooperation with SolutionsDotWG

Overview of all destinations

2015 2014 Var. Var.% 2015 2014 Var. Var.% 2015 2014 Var. Var.%

Berlin 89,6% 85,8% 3,8 4,4% 115,5 119,1 -3,6 -3,0% 103,6 102,2 1,4 1,4%Cologne / Bonn 77,1% 80,0% -2,9 -3,6% 106,6 114,6 -8,0 -7,0% 82,2 91,8 -9,6 -10,5%Dresden 79,0% 77,4% 1,6 2,1% 76,5 75,2 1,3 1,7% 60,5 58,2 2,3 4,0%Dusseldorf 74,5% 76,5% -2,0 -2,6% 102,9 99,7 3,2 3,2% 76,7 76,2 0,5 0,7%Frankfurt 81,8% 78,8% 3,0 3,8% 134,7 121,5 13,2 10,9% 110,2 95,7 14,5 15,2%Hamburg 85,4% 86,3% -0,9 -1,0% 120,1 132,3 -12,2 -9,2% 102,5 114,2 -11,7 -10,2%Munich 85,8% 87,7% -1,9 -2,2% 188,2 189,0 -0,8 -0,4% 161,5 165,8 -4,3 -2,6%

*Source: Fairmas GmbH / STR Global, based on data from participants with daily data entry, Data as of 01.10.2015

LegendOCC OccupancyADR Average Daily Rate (net rooms revenue)RevPar Revenue per available Room (net logistics revenue per available room)

Hotel Performance September 2015/2014*

Occupancy in % Average Daily Rate in Euro RevPar in Euro

4,4%

-3,6%

2,1%

-2,6%

3,8%

-1,0%-2,2%

-3,0%

-7,0%

1,7%3,2%

10,9%

-9,2%

-0,4%

1,4%

-10,5%

4,0%

0,7%

15,2%

-10,2%

-2,6%

Berlin Cologne / Bonn Dresden Dusseldorf Frankfurt Hamburg Munich

Occ ADR RevPar

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 8

FairmasHotel Reportin cooperation with SolutionsDotWG

Fig.1: Trendbarometer Berlin 2015 – Trend versus last year

-2,0%

-3,8%

-6,5%

6,3%

0,6%

3,3%

4,1%

-3,2%

-3,4%

October

November

December

Last Year

Occ Adr RevPar

Source: Fairmas GmbH / Data as of 01.10.2015

Fairmas Trendbarometer

A peek into the future – in detail:

Berlin

Berlin seems to be taking the good impetus from

September into October. The third of October

(Germany’s national holi-

day) falls on a Saturday this

year, so there will be no long

weekend this time, but the

weekend itself is still looking

very good. However, the ES-

ICM Congress is also making

it difficult for tourists to book

for the first weekend in Oc-

tober 2015, since prices are

tailored to congress visitors

and not tourists. The weekend

will also be marked by many

events celebrating “25 years of German unity” in

the city, though. This year, the “Festival of Lights”

will not be taking place during the autumn school

holidays, meaning that much higher demand can

be expected. The ECNP Congress is also being

held this year, and this generates good demand.

The absence of the “belektro” event (which takes

place only every two years) is hurting occupancy

(Occ: -2%; ADR: +6%; RevPar: +4%).

Last year, ceremonies took place to mark the 25

years of the fall of the Berlin Wall. The city was able

to enjoy strong demand, matched by higher room

rates. The conference situation is similar to last

year. The DGPPN is especially interesting for the

inner city hotels, but it also has a potential for over-

flow into surrounding districts. Hoteliers are thus

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 9

FairmasHotel Reportin cooperation with SolutionsDotWG

hopeful that the month can still recover the nearer

it gets. Many industries only decide on last-quarter

meetings and conventions at very short notice. A

4% decline in occupancy is expected and ADR is

set to rise by 0.6% (RevPar: -3%).

Expectations for December are marked by a lack

of confidence. Preliminary bookings are currently

well below those of last year. New Year’s Eve and

the Advent weekends are again looking very well

favourable and room rates are already very prom-

ising. Due to the convenient timing the end of the

year, a lot of good business can be expected,

thanks to the long weekends in January. Some

MICE inquiries are still expected. December has a

lot of potential, even if prospects currently still ap-

pear difficult. At present, occupancy is expected to

fall by 7%, while room rates are expected to rise by

3%. This means that RevPar will be 3% lower than

last year. But there is still plenty of time until then

and a lot can still happen. Berlin has every reason

to look forward to the New Year. Demand is strong,

prices are rising and this success is proving the

Berlin hotel industry right.

Cologne/Bonn

October will be a superb month for the hospital-

ity industry in Cologne/Bonn. The “Anuga” event,

which takes place only every two years, will be a

great driver of room rates in 2015. It was already ful-

ly booked out for months before the start, and the

local hotel industry has been experiencing this very

positively. Room rates are extremely high. In addi-

tion, this year the “Aquanale/FSB” double trade fair

takes place in Cologne again. The strong demand

these generate means that even better room rates

can be achieved at the end of

the month. The Cologne Mara-

thon and the two U2 concerts

will do the rest to ensure an

outstanding performance for

the Cologne hotel market. The

city’s hoteliers expect a 0.5%

occupancy increase. However,

ADR is forecast to soar by an

extremely healthy 45%. This

would mean a very impressive

46% rise in RevPar.

Fig.2: Trendbarometer Cologne/Bonn 2015 – Trend versus last year

0,5%

-3,0%

-9,6%

45,4%

1,2%

-0,4%

46,1%

-1,8%

-9,9%

October

November

December

Last Year

Occ Adr RevPar

Source: Fairmas GmbH / Data as of 01.10.2015

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 10

FairmasHotel Reportin cooperation with SolutionsDotWG

For a long time the forecast

for November was positive.

The COMPAMED/MEDICA is

again very much in demand

(according to the trade fair

ranking of the AHGZ, this was

the German trade event that

provided the greatest yield).

Although it takes place in Dus-

seldorf, it always provides

plenty of overflow business in

Cologne, even well in advance.

However, the overall demand in the business and

leisure segments is otherwise very subdued at

this time. As a result, expectations have been cor-

rected downwards slightly. Nevertheless, the first

Christmas market weekend will also be a Novem-

ber highlight ensuring healthy occupancy figures,

and above all good room rates. Currently, a 3%

fall in occupancy is expected in November. Room

rates, however, are expected to rise by more than

1%, so that RevPar is expected to decline by 2%.

December will also be difficult to predict. The Ad-

vent business with the Christmas Market week-

ends greatly depends on the weather every year

and is correspondingly short. Business at New

Year’s Eve is traditionally strong though, and ex-

tremely convenient for employees this time around,

giving the timing of the public holidays at the end

of the year (and at the beginning of the next). Local

hoteliers are very cautiously forecasting a decline

in occupancy of around 10% and a slight (0.4%)

decrease in room rates. RevPar would thus remain

nearly 10% below last year’s figure. However, the

last word has certainly not been spoken.

Dresden

The advance-booking situation in Dresden for Oc-

tober is still far from ideal. There will be no long

weekend this year to attract more tourists to the

city, because 3 October (Day of German National

Unity) and Reformation Day both fall on Saturdays.

However, the “Semicon” congress will be held

again this year. This event did not take place in

2014, as it is only held every other year. This time,

the congress may again generate high room rates.

The DTG Congress and the Dresden Marathon

both have the potential to boost performance. Be-

sides this, the Dresden Oktoberfest is still running

Fig.3: Trendbarometer Dresden 2015 – Trend versus last year

-3,9%

2,6%

-1,8%

8,0%

-0,9%

3,4%

3,8%

1,6%

1,5%

October

November

December

Last Year

Occ Adr RevParSource: Fairmas GmbH / Data as of 01.10.2015

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 11

FairmasHotel Reportin cooperation with SolutionsDotWG

at the beginning of the month. Hoteliers in Dresden

are expecting a 4% fall in occupancy in October,

though ADR is expected to increase by 8%. This

means that RevPar would grow by nearly 4% on a

year-on-year basis.

November is traditionally a weak month in Dres-

den. The city’s hoteliers are similarly guarded in

their predictions. However, there will be a number

of conventions in the city that could generate better

room rates. For example, the FAD Conference will

be taking place on 4 and 5 November 2015. Be-

sides this, the ITI Symposium (9 to 11 November

2015) and the Dresden “Energy in Future” confer-

ence (10 and 11 November 2015) are also taking

place. The ever-popular “Striezelmarkt” also takes

up one day more of November this year. Short-

term tourist trade will depend enormously on the

weather. In the local programme offered by three

to five-star hotels together with the Dresden tour-

ism authority, overnight stays are being promoted

in November at highly competitive prices. Cau-

tiously, a 3% increase in occupancy and a 1% de-

cline in room rates are being predicted for the city’s

hotels. RevPar would thus be around 2% higher

than last year.

The expectations for December are also positive.

The Advent weekends are traditionally good, not

only because of the “Striezelmarkt”. The local

hotels also expect much pickup at good rates at

New Year. This year, New Year’s Eve is very con-

venient for employees and much end-of-the-year

business will carry on into January. The Dresdner

hoteliers are cautiously forecasting a decline in oc-

cupancy of less than 2%. However, room rates are

expected to rise by more than

3%, which would result in a

RevPar increase of almost 2%.

Dusseldorf

Strong growth is again promised

in Dusseldorf in October with

overall performance set to grow

by 12%. This year, the calendar

includes the “A + A” Trade Fair

(held every two years, running

over four days) and the five-day

“Anuga” event in Cologne. The

Fig.4: Trendbarometer Dusseldorf 2015 – Trend versus last year

-1,1%

-1,0%

-9,2%

11,9%

3,1%

-4,1%

10,7%

2,1%

-12,8%

October

November

December

Last Year

Occ Adr RevParSource: Fairmas GmbH / Data as of 01.10.2015

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 12

FairmasHotel Reportin cooperation with SolutionsDotWG

“Expopharm” takes up two days

of October. Moreover, the “Re-

haCare” trade fair (three days)

is taking place in October again

after three years and not (as in

previous years) in September.

Hoteliers expect high room rate

levels from all these trade fairs,

especially from the A + A.

November looks set to be a

month of growth, albeit with a

decline in occupancy. The main reason for this is

the high increase in room rates (ADR: +3%). Ac-

cording to statements from many hoteliers, Novem-

ber 2015 will be similar to last year. The four-day

“Medica” trade fair is being held again. Due to the

high demand and the good advance bookings, a

higher ADR is expected, though this will be at the

expense of occupancy. Otherwise, November will

be a strong business month with much corporate

and MICE business.

The forecast for this December is very poor in terms

of all three parameters (Occ: -9%, ADR: -4%, and

RevPar: -13%). Even so, some hoteliers do expect

a more positive development in the months to

come, due to the healthy advanced booking situa-

tion in the MICE sector. The weekends are already

well booked, thanks to the Christmas markets in

Dusseldorf. It is expected that the overall result will

Frankfurt

October in Frankfurt was marked by growth in all

three indicators (Occ: +3.2%, ADR: 1.7%, and

RevPar: +5.0%). This year, is according to ho-

telier statements, there will be a particularly high

demand in the group and banquet sectors. The

third of October public holiday falls on a weekend

this year (in 2014 on a Friday), so permitting a full

business week with higher room rates. Besides

this, the “Buchmesse“ (book fair) took place ex-

actly one week earlier this year (one week before

the autumn school holidays), presenting Frankfurt

with exactly two full business weeks. It is assumed

that higher-priced business can be sold, which ex-

plains the increase in room rates. There was only

one business week in the same month last year to

counter the “Buchmesse“ and the two-week au-

tumn holidays.

Fig.5: Trendbarometer Frankfurt 2015 – Trend versus last year

3,2%

0,9%

3,1%

1,7%

-0,2%

-1,1%

5,0%

0,8%

2,0%

October

November

December

Last Year

Occ Adr RevPar

Source: Fairmas GmbH / Data as of 01.10.2015

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 13

FairmasHotel Reportin cooperation with SolutionsDotWG

The forecasts still suggest that November is still

on course for growth, with a 1% increase in Rev-

Par. However, it remains to be seen just how the

month will finally develop, although increased de-

mand is already expected in the banquet sector.

This year will be opened by the first annual “form-

next”, a trade fair for tool and mould-making (17

to 20 November 2015). The “Allerheiligen” public

holiday (Halloween) in Baden-Württemberg und

North Rhine-Westphalia is also on a Sunday this

year (1 November), so that the business week in

these two federal states will not be ruined as it

was last year, as was clearly noticed by a number

of hoteliers. As a rule, the month of November is

marked by healthy inquiries from the conference

and corporate sectors.

The outlook in December is also overall posi-

tive with RevPar set to increase by 2%. This year,

Christmas Eve falls on a Thursday. Hoteliers are

expecting a very popular fourth Advent weekend

(Christmas market trade), influenced by higher de-

mand in the group business segment, which ex-

plains the growth in occupancy of more than 3%.

Apart from that, December is already marked by

good demand in the conference and banqueting

segment. Certainly, it is still to be seen whether this

demand will also be upheld and bookings will not

be cancelled, but the trend so far is a positive one.

Hamburg

Up to now, October in Hamburg has been marked

by a 1% decline in RevPar. October is largely

marked by tourist sector business. The expected

decline in room rates is due to the holiday situation

in October. There was still a full business week in

the last week of October in 2014. This year, the

entire month is dominated by school holidays (in

North Rhine-Westphalia during

the first two weeks of October

and in the third and fourth Oc-

tober weeks in Hamburg. It re-

mains to be seen whether the

overall result will be adjusted

upwards, for example, due to

the EANM Congress of Nuclear

Medicine (an event held at dif-

ferent venues) that takes place

from 10 to 14 October this year,

as well as the World Publishing

Fig.6: Trendbarometer Hamburg 2015 – Trend versus last year

-0,8%

-1,4%

0,2%

-0,3%

1,5%

0,8%

-1,0%

0,1%

1,0%

October

November

December

Last Year

Occ Adr RevPar

Source: Fairmas GmbH / Data as of 01.10.2015

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 14

FairmasHotel Reportin cooperation with SolutionsDotWG

Expo Congress (also held at different locations)

from 5 to 7 October 2015.

On the other hand, the forecast for November

does promise more hope. There should be a slight

(0.1%) increase in RevPar due to higher room rates.

This year, the annual “Hanseboot” boat show is

taking place again. It will take up six more days of

November than was the case in 2014.

December looks promising in all three key indi-

cators (Occ: +0.2%, ADR: +0.8%, and RevPar:

+1.0%). Here too, as in many other cities, improved

MICE and leisure business is to be reckoned with.

This year, Christmas Eve falls on a Thursday (in

2014 it was on a Wednesday), meaning that there

will be an extra business day, which will have a

positive effect on room rates.

Munich

The prospects for October are

good. Last year, the autumn

school holidays were entirely in

October but this year they fall in

November. As a result, there will

be one additional and full busi-

ness week to be sold in October.

The event situation is otherwise

very similar to last year. The Ok-

toberfest and EXPO are expect-

ed to create a similar level of

demand as last year. The “ceramitec” trade fair will

provide figures around as good as for last year’s

DGGG Congress. Good weather at the weekends

and economically priced Bayern Munich Champi-

ons League games could also boost occupancy.

Currently, however, the Munich hotel industry is

anticipating a 0.3% drop in occupancy. However,

ADR is expected to increase by 2%, with RevPar

up by the same amount.

However, November is again expected to be

marked by serious declines. The school autumn

holidays will still be taking place in the first week of

November. October business should benefit from

this, but high room rate business and MICE sec-

tor trade will suffer in November. Besides this, the

very highly priced “electronica” event took place

in 2014. Nonetheless, the “productronica” trade

show was marked by significantly lower room

Fig.7: Trendbarometer Munich 2015 – Trend versus last year

-0,3%

0,8%

-3,7%

1,8%

-4,5%

-0,7%

1,5%

-3,7%

-4,4%

October

November

December

Last Year

Occ Adr RevPar

Source: Fairmas GmbH / Data as of 01.10.2015

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 15

FairmasHotel Reportin cooperation with SolutionsDotWG

rates this year and demand is lower. Hoteliers are

currently expecting a very small increase in occu-

pancy of 0.8%. ADR, though, is projected to drop

by almost 5%. RevPar would hence decline by a

year-on-year 4%.

December is also expected to be worse in Munich.

Because of the holiday situation, only two and a

half business weeks are available. The group res-

ervation situation is so far well behind last year’s.

During Advent, the weekends provide traditionally

good business and individual reservations are be-

ing made a much shorter notice. Hoteliers are

therefore predicting improvements over the com-

ing weeks. After all, New Year’s Eve is extremely

convenient for employees this year. Currently, the

city’s hotels are still expecting occupancy to fall by

almost 4%. Room rates are expected to decline

by 0.7%. RevPar would thus be at least 4% below

last year’s figure. It remains to be seen over the

next few weeks just how the month will develop.

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 16

FairmasHotel Reportin cooperation with SolutionsDotWG

In Focus

Rate bands – Berlin, Dusseldorf, Munich

In last June’s issue, we looked at the issue of room rate bands. In the meantime, three quarters of the “new”

year is already behind us. Reason enough to cast a critical eye over the developments once again. Together

with the “AHGZ” newspaper for the German hospitality industry, we have looked at the room rate bands for

Berlin, Dusseldorf and Munich again.

Typically, a hotel’s positioning in a specific category is also associated with different cost levels. This means

that higher numbers of stars (in the classification used by the DEHOGA Hotel and Restaurant Association)

are often reflected in a higher level of staff per guest. In the five-star luxury hotel business, where guest’s

service expectations are often very high, personnel costs are also according large.

Is it possible for hoteliers in the higher categories to

distinguish themselves from lower classified com-

petitors sufficiently and force through higher room

prices for their product than the competition? We

have examined this issue in detail exclusively for

the “AHGZ”, the newspaper for the German hos-

pitality industry. Mid-range hotels (and higher cat-

egories) were subjected to a great deal of scrutiny.

In each of the three cities concerned, the room

rate bands of the three-star hotels were compared

with those of the four-star hotels; the results are

displayed in a diagram.

Likewise, the room rates bands were recorded for

the five-star hotel industry in the respective cities

and compared with the four-star price ranges in

graphs. A comparison between the room rates of

the four-star and five-star hotel industry in Berlin,

Dusseldorf and Munich is shown in the graphs.

Our investigation into all three cities covers the pe-

riod from January 2009 to August 2015.

The diagrams show the overlaps and distinct fea-

tures of the various categories, as well as the sig-

nificance of events. Thus, the price peaks in the

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 17

FairmasHotel Reportin cooperation with SolutionsDotWG

hospitality industry at the time of trade fairs in Dus-

seldorf, the Munich Oktoberfest or for the Champi-

ons League final in Berlin can clearly be seen.

In Berlin, there has apparently never been a clear

demarcation between the three-star and four-star

categories. On the contrary, the room rates in the

three-star sector are nowadays almost entirely at

the lower level of four-star hotel prices. In recent

years, the three-star hotels in particular have been

raising their rates. Room rates in the city have risen

significantly, especially in recent months. However,

Fig.8: Rate band 3* and 4* hotels

0

100

200

300

400

500

600

0

100

200

300

400

500

600

Jan‐09

Feb‐09

Mar‐09

Apr‐09

May‐09

Jun‐09

Jul‐09

Aug‐09

Sep‐09

Oct‐09

Nov‐09

Dec‐09

Jan‐10

Feb‐10

Mar‐10

Apr‐10

May‐10

Jun‐10

Jul‐10

Aug‐10

Sep‐10

Oct‐10

Nov‐10

Dec‐10

Jan‐11

Feb‐11

Mar‐11

Apr‐11

May‐11

Jun‐11

Jul‐11

Aug‐11

Sep‐11

Oct‐11

Nov‐11

Dec‐11

Jan‐12

Feb‐12

Mar‐12

Apr‐12

May‐12

Jun‐12

Jul‐12

Aug‐12

Sep‐12

Oct‐12

Nov‐12

Dec‐12

Jan‐13

Feb‐13

Mar‐13

Apr‐13

May‐13

Jun‐13

Jul‐13

Aug‐13

Sep‐13

Oct‐13

Nov‐13

Dec‐13

Jan‐14

Feb‐14

Mar‐14

Apr‐14

May‐14

Jun‐14

Jul‐14

Aug‐14

Sep‐14

Oct‐14

Nov‐14

Dec‐14

Jan‐15

Feb‐15

Mar‐15

Apr‐15

May‐15

Jun‐15

Jul‐15

Aug‐15

BerlinRate band3*‐ und 4*‐Hotels

3 Sterne 4 Sterne

Source: Fairmas GmbH / Data as of 01.10.2015

Fig.9: Rate band 4* and 5* hotels

0

100

200

300

400

500

600

0

100

200

300

400

500

600

Jan‐09Feb‐09Mar‐09

Apr‐09May‐09

Jun‐09Jul‐09Aug‐09Sep‐09Oct‐09

Nov‐09

Dec‐09Jan‐10Feb‐10Mar‐10

Apr‐10May‐10

Jun‐10Jul‐10Aug‐10Sep‐10Oct‐10

Nov‐10

Dec‐10Jan‐11Feb‐11Mar‐11

Apr‐11May‐11

Jun‐11Jul‐11Aug‐11Sep‐11Oct‐11

Nov‐11

Dec‐11Jan‐12Feb‐12Mar‐12

Apr‐12May‐12

Jun‐12Jul‐12Aug‐12Sep‐12Oct‐12

Nov‐12

Dec‐12Jan‐13Feb‐13Mar‐13

Apr‐13May‐13

Jun‐13Jul‐13Aug‐13Sep‐13Oct‐13

Nov‐13

Dec‐13Jan‐14Feb‐14Mar‐14

Apr‐14May‐14

Jun‐14Jul‐14Aug‐14Sep‐14Oct‐14

Nov‐14

Dec‐14Jan‐15Feb‐15Mar‐15

Apr‐15May‐15

Jun‐15Jul‐15Aug‐15

BerlinRate band 4*‐ und 5*‐Hotels 5 Sterne 4 Sterne

Source: Fairmas GmbH / Data as of 01.10.2015

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 18

FairmasHotel Reportin cooperation with SolutionsDotWG

middle class hotels have been unable to set them-

selves apart. Competition in the capital’s four-star

hotel sector is apparently so great and the price

competition so intense that entry prices for these

hotels do not start at around the top of the three-

star room rates band, but instead attack the three-

star hotels near to their starting prices. This trend

has continued and there seems to be no improve-

ment in sight, even though the four-star hotels

have also expanded their rates band upwards.

In terms of room rates, the three-star hoteliers in

Berlin find themselves in direct comparison with

four-star hotels, and have to provide good rea-

sons why their guests should stay in three-star ac-

commodation, even though visitors to the city can

book higher category rooms for the same price.

They have to try to score points with features other

than the simple classification standards. However,

Berlin’s four-star hotels can hardly be happy with

the price situation, either. They want to use their

comparatively low entry prices to increase occu-

pancy and poach guests away from the three-star

segment. However, such business practices rather

prevent hoteliers clearly positioning their own ho-

tels and thus achieving higher rates in the long

term.

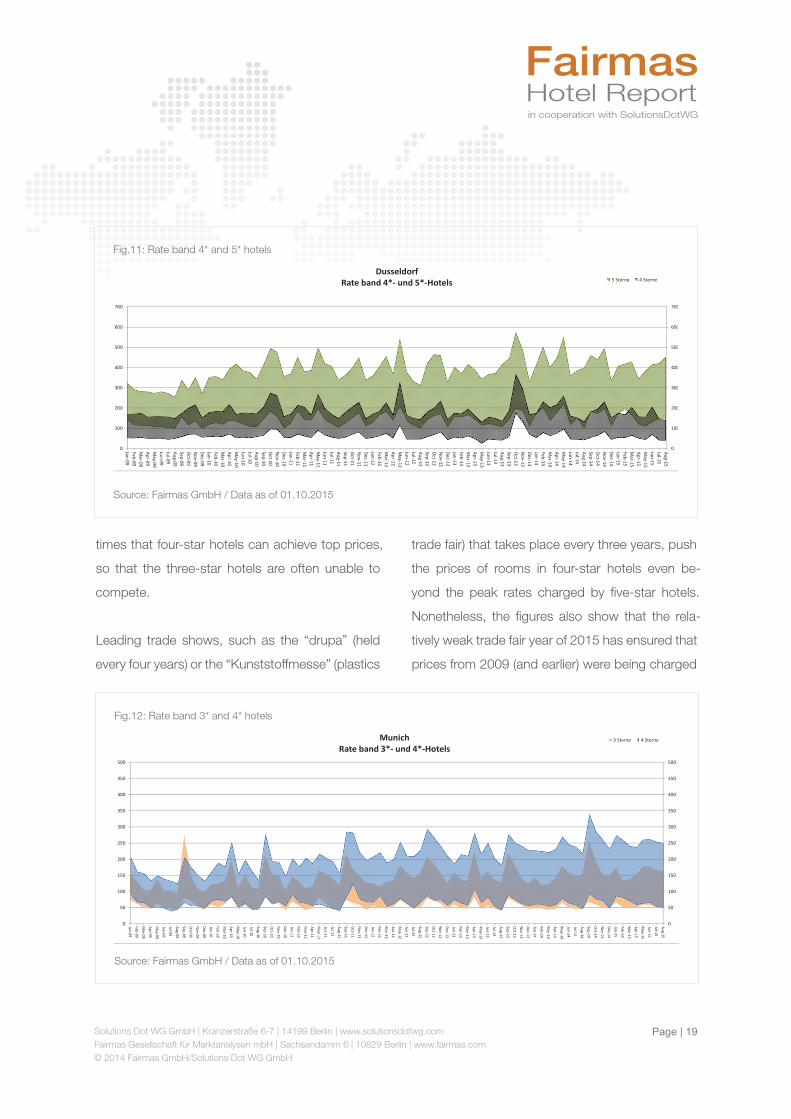

In Dusseldorf, the overlap in room rates between

three-star and four-star hotels is far smaller. Here,

numerous peaks illustrate just how heavily Dussel-

dorf depends on trade fairs. It is precisely at such

Fig.10: Rate band 3* and 4* hotels

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

Jan‐09Feb‐09Mar‐09

Apr‐09May‐09

Jun‐09Jul‐09Aug‐09Sep‐09Oct‐09

Nov‐09

Dec‐09Jan‐10Feb‐10Mar‐10

Apr‐10May‐10

Jun‐10Jul‐10Aug‐10Sep‐10Oct‐10

Nov‐10

Dec‐10Jan‐11Feb‐11Mar‐11

Apr‐11May‐11

Jun‐11Jul‐11Aug‐11Sep‐11Oct‐11

Nov‐11

Dec‐11Jan‐12Feb‐12Mar‐12

Apr‐12May‐12

Jun‐12Jul‐12Aug‐12Sep‐12Oct‐12

Nov‐12

Dec‐12Jan‐13Feb‐13Mar‐13

Apr‐13May‐13

Jun‐13Jul‐13Aug‐13Sep‐13Oct‐13

Nov‐13

Dec‐13Jan‐14Feb‐14Mar‐14

Apr‐14May‐14

Jun‐14Jul‐14Aug‐14Sep‐14Oct‐14

Nov‐14

Dec‐14Jan‐15Feb‐15Mar‐15

Apr‐15May‐15

Jun‐15Jul‐15Aug‐15

DusseldorfRate band 3*‐ und 4*‐Hotels

3 Sterne 4 Sterne

Source: Fairmas GmbH / Data as of 01.10.2015

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 19

FairmasHotel Reportin cooperation with SolutionsDotWG

times that four-star hotels can achieve top prices,

so that the three-star hotels are often unable to

compete.

Leading trade shows, such as the “drupa” (held

every four years) or the “Kunststoffmesse” (plastics

trade fair) that takes place every three years, push

the prices of rooms in four-star hotels even be-

yond the peak rates charged by five-star hotels.

Nonetheless, the figures also show that the rela-

tively weak trade fair year of 2015 has ensured that

prices from 2009 (and earlier) were being charged

Fig.11: Rate band 4* and 5* hotels

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

Jan‐09Feb‐09Mar‐09

Apr‐09May‐09

Jun‐09Jul‐09Aug‐09Sep‐09Oct‐09

Nov‐09

Dec‐09Jan‐10Feb‐10Mar‐10

Apr‐10May‐10

Jun‐10Jul‐10Aug‐10Sep‐10Oct‐10

Nov‐10

Dec‐10Jan‐11Feb‐11Mar‐11

Apr‐11May‐11

Jun‐11Jul‐11Aug‐11Sep‐11Oct‐11

Nov‐11

Dec‐11Jan‐12Feb‐12Mar‐12

Apr‐12May‐12

Jun‐12Jul‐12Aug‐12Sep‐12Oct‐12

Nov‐12

Dec‐12Jan‐13Feb‐13Mar‐13

Apr‐13May‐13

Jun‐13Jul‐13Aug‐13Sep‐13Oct‐13

Nov‐13

Dec‐13Jan‐14Feb‐14Mar‐14

Apr‐14May‐14

Jun‐14Jul‐14Aug‐14Sep‐14Oct‐14

Nov‐14

Dec‐14Jan‐15Feb‐15Mar‐15

Apr‐15May‐15

Jun‐15Jul‐15Aug‐15

Dusseldorf Rate band 4*‐ und 5*‐Hotels 5 Sterne 4 Sterne

Source: Fairmas GmbH / Data as of 01.10.2015

Fig.12: Rate band 3* and 4* hotels

0

50

100

150

200

250

300

350

400

450

500

0

50

100

150

200

250

300

350

400

450

500

Jan‐09

Feb‐09

Mar‐09

Apr‐09

May‐09

Jun‐09

Jul‐09

Aug‐09

Sep‐09

Oct‐09

Nov‐09

Dec‐09

Jan‐10

Feb‐10

Mar‐10

Apr‐10

May‐10

Jun‐10

Jul‐10

Aug‐10

Sep‐10

Oct‐10

Nov‐10

Dec‐10

Jan‐11

Feb‐11

Mar‐11

Apr‐11

May‐11

Jun‐11

Jul‐11

Aug‐11

Sep‐11

Oct‐11

Nov‐11

Dec‐11

Jan‐12

Feb‐12

Mar‐12

Apr‐12

May‐12

Jun‐12

Jul‐12

Aug‐12

Sep‐12

Oct‐12

Nov‐12

Dec‐12

Jan‐13

Feb‐13

Mar‐13

Apr‐13

May‐13

Jun‐13

Jul‐13

Aug‐13

Sep‐13

Oct‐13

Nov‐13

Dec‐13

Jan‐14

Feb‐14

Mar‐14

Apr‐14

May‐14

Jun‐14

Jul‐14

Aug‐14

Sep‐14

Oct‐14

Nov‐14

Dec‐14

Jan‐15

Feb‐15

Mar‐15

Apr‐15

May‐15

Jun‐15

Jul‐15

Aug‐15

MunichRate band 3*‐ und 4*‐Hotels

3 Sterne 4 Sterne

Source: Fairmas GmbH / Data as of 01.10.2015

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 20

FairmasHotel Reportin cooperation with SolutionsDotWG

in the three and four-star sector. In Dusseldorf too,

the costs of rooms in four-star and five-star hotels

clearly overlap. Here again, as in Berlin, it can be

seen that rooms in four-star hotels can sometimes

be had for less than €50. And, even more than a

year ago, the question arises of whether such low

rates are really needed only in order to increase

occupancy.

By way of contrast, and similar to the situation in

Berlin, the rates band of the three-star hotels in

Munich almost completely matches that of the

four-star hotel segment. In the process, it emerges

that three-star hotels in Munich are equally capa-

ble of hiking up prices when the four-star hotels

are charging top rates. Here too, in the lower room

Fig.13: Rate band 4* and 5* hotels

0

100

200

300

400

500

600

700

800

900

1000

0

100

200

300

400

500

600

700

800

900

1000

Jan‐09Feb‐09Mar‐09

Apr‐09May‐09

Jun‐09Jul‐09Aug‐09Sep‐09Oct‐09

Nov‐09

Dec‐09Jan‐10Feb‐10Mar‐10

Apr‐10May‐10

Jun‐10Jul‐10Aug‐10Sep‐10Oct‐10

Nov‐10

Dec‐10Jan‐11Feb‐11Mar‐11

Apr‐11May‐11

Jun‐11Jul‐11Aug‐11Sep‐11Oct‐11

Nov‐11

Dec‐11Jan‐12Feb‐12Mar‐12

Apr‐12May‐12

Jun‐12Jul‐12Aug‐12Sep‐12Oct‐12

Nov‐12

Dec‐12Jan‐13Feb‐13Mar‐13

Apr‐13May‐13

Jun‐13Jul‐13Aug‐13Sep‐13Oct‐13

Nov‐13

Dec‐13Jan‐14Feb‐14Mar‐14

Apr‐14May‐14

Jun‐14Jul‐14Aug‐14Sep‐14Oct‐14

Nov‐14

Dec‐14Jan‐15Feb‐15Mar‐15

Apr‐15May‐15

Jun‐15Jul‐15Aug‐15

MunichRate band 4*‐ und 5*‐Hotels 5 Sterne 4 Sterne

Source: Fairmas GmbH / Data as of 01.10.2015

rate range there is no clear demarcation between

three and four-star hotels. However, the luxury

segment in Munich is not letting itself be overtaken

by the lower category and is pulling the market

continuously upwards with its very high room rates.

In Munich, the impact of events and trade shows

on room pricing can easily be observed. Distinct

peaks emerge regularly during the Oktoberfest,

particularly in the five-star sector. Major trade fairs,

such as “Bauma”, which takes place in April every

three years, regularly drive room prices up to peak

levels.

While the Bavarian capital remains the most ex-

pensive city in Germany, able to record good

growth rates in the upmarket segment in 2015,

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 21

FairmasHotel Reportin cooperation with SolutionsDotWG

the different price category bands have been even

more blurred than in Berlin for years.

Berlin’s five-star hotels are marked by a huge price

range. Although there is a large overlap with the

four-star hotels, the luxury class establishments

charge room rates that are far higher than the

peak rate for four-star hotels. The competition in

the five-star range is great; in recent years, many

new openings by international chains and private

investors have revived the capital, which is now

extremely attractive to tourists. Yet, just as before,

room rates of well below €100 can still be found,

even in the five-star sector.

So the price problem persists. Finally, extremely

low prices have a negative effect on quality and

– in the last analysis – on credibility and economic

efficiency. That is why price dumping is not the

solution at all. On the contrary, a way must be

found to escape this dilemma. Above all, luxury

segment hoteliers have to be asked to refrain from

participating in price dumping, and – in particular

– need to stand up for their product and its quality.

They need to differentiate themselves from the low-

er categories once again in order to ensure long-

term room rate growth. By upwardly correcting the

rate structure, the entire market could follow suit

and provide a basis for an overall improvement in

ADR. Here, Munich is leading by example.

Steadily increasing numbers of beds are leading to

cut-throat competition in many places. Budget ho-

tels are springing up like mushrooms while for sev-

eral years now, providers of apartments have also

more been taking more guests away from higher-

category hotels. Online platforms have also been

adding to the difficulties the hotels face. Yet price

dumping offers no guarantee for survival in the

face of this competition. Large hotel chains, cross-

financed by business at other locations, might be

able to resist, but smaller companies will be quick-

ly forced into bankruptcy. Berlin’s three-star estab-

lishments have already made a good start.

Marina Behre and Nadine Kilian

In cooperation with the AHGZ

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 22

FairmasHotel Reportin cooperation with SolutionsDotWG

The Fairmas Hotel Report is published by:

Fairmas Gesellschaft für Marktanalysen mbH, Sachsendamm 6, 10829 Berlin, Deutschland

Solutions Dot WG GmbH, Kranzer Strasse 6-7, 14199 Berlin, Deutschland

Fairmas Gesellschaft für Marktanalysen mbH specializes in market

analyses and the development of planning and controlling software

for the hotel industry. The company offers its international clientele a

hotel benchmarking platform, as well as various software applications

for the fields of budgeting, forecasting, controlling, management re-

porting and work process optimization.

As a strategic management consultancy, Solutions Dot WG develops

individual and customized strategies and solutions for companies in

the hotel, catering and tourism, and provides support in implementing

plans. Solutions dot also manages independent project implementa-

tion, is active in support management and interim management, as

well as in the total quality management (TQM) sector.

The Fairmas Hotel Report is edited by:

Nadine Kilian, Marketing & Communications Manager,

Fairmas Gesellschaft für Marktanalysen mbH, e-mail: [email protected]

Gabriele Kiessling, Consultant und Project Management,

Solutions Dot WG GmbH, e-mail: [email protected]

Solutions Dot WG GmbH | Kranzerstraße 6-7 | 14199 Berlin | www.solutionsdotwg.comFairmas Gesellschaft für Marktanalysen mbH | Sachsendamm 6 | 10829 Berlin | www.fairmas.com © 2014 Fairmas GmbH/Solutions Dot WG GmbH

Page | 23

FairmasHotel Reportin cooperation with SolutionsDotWG

Disclaimer

No representation or warranty (express or implied) is given as to the accuracy or complete-ness of the

information contained in this publication, and, to the extent permitted by law, Fairmas GmbH / Solutions

Dot WG do not accept or assume any liability, responsibility or duty of care for any consequences of you

or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for

any decision based on it.